A Maximum Principle approach to deterministic Mean Field Games of Control with Absorption

††thanks: This work was supported through the profile partnership program between Humboldt-Universität zu Berlin and Princeton University.

Paulwin Graewe111Deloitte Consulting GmbH, Kurfürstendamm 23, 10719 Berlin, Germany; email: pgraewe@deloitte.deUlrich Horst222Department of Mathematics, and School of Business and Economics, Humboldt-Universität zu Berlin,

Unter den Linden 6, 10099 Berlin, Germany; email: horst@math.hu-berlin.deRonnie Sircar333Department of Operations Research and Financial Engineering, Princeton University, Sherrerd Hall, Princeton, NJ 08544; email: sircar@princeton.edu

Abstract

We study a class of deterministic mean field games on finite and infinite

time horizons arising in models of optimal exploitation of exhaustible resources. The main characteristic of our game is an absorption constraint on the players’ state process. As a result of the state constraint the optimal time of absorption becomes part of the equilibrium. This requires a

novel approach when applying Pontyagin’s maximum principle. We prove the existence and uniqueness of equilibria and solve the infinite horizon models in closed form. As players may drop out of the game over time, equilibrium production rates need not be monotone nor smooth.

AMS Subject Classification: 93E20, 91B70, 60H30.

Keywords: stochastic control, mean field game, optimal exploitation, maximum principle

1 Introduction

This paper establishes existence and uniqueness of equilibrium results for a class deterministic mean field games (MFGs) arising in models of optimal exploitation of exhaustible resources. MFGs provide a convenient tool

for analyzing complex strategic interactions among many players when each

individual player has only a small impact on the behavior of other players. In a standard mean field game each player solves a control problem in which an individual player’s payoff functional and the dynamics of the controlled state process depend on the empirical distribution of the other players’ actions or states. The existence of Nash equilibria in MFGs can be established by solving either a coupled system of two partial differential equations (PDEs), a backward Hamilton-Jacobi-Bellman equation determining the players’ utility, and a forward Kolmogorov equation determining the evolution of the distribution of states or actions, or by solving a system of McKean-Vlasov forward-backward SDEs where the

forward component describes the state dynamics and the backward component

describes the dynamics of the adjoint variable. We refer to the monograph

[1] for further background.

In the economics literature MFGs are often called anonymous games. First introduced by Rosenthal [25] and Jovanovic and Rosenthal [22], anonymous games have received renewed attention among economists

in the last two decades; see [2, 9, 19] and references therein. Huang, Malhamé and Caines [20] and Lasry and Lions [23] independently introduced MFGs into the engineering and mathematical literature. Ever since, MFGs have become an important driver of mathematical innovation, especially in the areas of PDEs and backward stochastic equations. Complementing the theoretical work

on MFGs, there is a by now substantial literature where anonymous and mean field games have been successfully applied to an array economic and engineering problems, ranging from network security and traffic networks [14, 26] and systemic risk management [5], to portfolio liquidation [10, 11, 13, 21] and oil and energy production in competitive markets [6, 7, 15, 16, 17].

Oligopoly models of markets with a small number of competitive players that compete on the amount of output they produce go back to the classical work of Cournot [8] in 1838. These have typically been static (or one-period) models, where the existence and construction of a Nash equilibrium have been extensively studied. Dynamic Cournot models for energy production in a competitive market have been proposed and analyzed by many authors in recent years; we refer to [24] for a survey on

energy production models. In these models market participants are often endowed with limited amounts of exhaustible resources such as oil, coal or

natural gas that they choose to extract for sale. The models may lead to continuous time single player control problems [3], finite player nonzero-sum differential games [18], or continuum mean field games [6, 7]. In the context of nonzero-sum dynamic games between finitely many players the computation of a solution is a

challenging problem, typically involving coupled systems of nonlinear PDEs, with one value function per player, and existence theory is sparse. MFGs allow one to handle certain types of competition in the continuum limit of an infinity of small players by solving either systems of PDEs or forward-backward SDEs.

One of the key characteristics of games with exhaustible resources is that resources may run out and change the structure of the game. In a stochastic setting, the strict absorption constraint is often ignored, assuming

that resource levels fluctuate randomly and recover as soon as they reach

positive levels again. The situation is very similar in models of optimal

portfolio liquidation. When asset portfolios are liquidated on behalf of third parties, short positions are not allowed legally. Nonetheless, these constraints are usually ignored for reasons of mathematical tractability. The non-negativity constraint may be binding even in deterministic games as shown in [11].

Incorporating non-negativity constraints on the state processes leads to MFGs with absorbing boundaries. The literature on MFGs with absorbing state dynamics is sparse. Models of mean field type without strategic interactions have been applied to model interactive default times by various authors. Graber and Bensoussan [15] consider a modification of the

model of Chan and Sircar [6] on a bounded domain. While the restriction to bounded domains simplifies the mathematical analysis it seems undesirable from an economic perspective. We impose only non-negativity constraints but restrict ourselves to deterministic settings. MFGs with absorbing state constraints in stochastic settings have recently

been considered by Campi and Fischer in [4]. Their model heavily relies on diffusive state dynamics, though.

We consider a deterministic MFG model of optimal exploitation of exhaustible resources in which players with zero resources drop out of the game before the terminal time in equilibrium. Both finite and the infinite horizon models are studied. As we will see there can be very different equilibrium strategies depending on whether a terminal time is imposed or not. The fact players may exit the game before the terminal time requires a novel approach to the maximum principle associated with an individual player’s optimization problem. Due to the non-negativity constraint on the state process, the Hamiltonian depends on the initial condition, while the terminal value of the adjoint process is unknown. The latter is very similar to portfolio liquidation models where the terminal condition of the adjoint process is unknown, due to the liquidation constraint; see [11, 12] for details. In order to overcome this problem we consider the Hamiltonian only up a candidate optimal exploitation time. Obtaining such candidate requires a candidate terminal condition for the adjoint

process. In our deterministic setting the candidate terminal condition and hence the candidate optimal exploitation time can be given in closed form; the stochastic case is much more involved and left for future work.

The key observation in solving the MFG is that a certain best response function is independent of the mean field equilibrium. More precisely, we prove that the dynamics of the amount of resource extracted by an individual player up to any given time by using a strategy that would be optimal if the optimal exhaustion time was equal to that given time is independent of the equilibrium mean production rate. Moreover, we show that the dynamics follows an ODE that depends only the initial distribution of the resource levels and the risk free interest rate. The ODE can be

solved in closed form. The solution is strictly monotone and the optimal exhaustion time is given by the inverse function. In the infinite horizon case where the equilibrium mean production rate converges to zero as time increases to infinity, this allows us to fully describe the unique

MFG equilibrium in terms of the said ODE. In the finite horizon case the equilibrium mean production rate at the terminal time is unknown. This results in an additional fixed point problem that can easily be solved. Thus we provide among the very few explicit solutions to MFGs outside the linear-quadratic framework.

To illustrate our main ideas we first consider in Section 2 the benchmark case of a single monopolist oil producer. We fully characterize optimal exploitation strategies. In particular, we prove that full exploitation may not be optimal in finite horizon problems. The MFG of optimal extraction is analyzed in Section 3. We first determine the equilibrium time of exploitation as a function of the competitors’ strategies and own initial resources. Subsequently, we determine the equilibrium exploitation times and strategies. We illustrate by two simple examples that equilibrium exploitation rates do need not be monotone, nor smooth.

2 The Monopoly Case

As a motivation for our general analysis we illustrate in this section our main ideas in the framework of monopolist oil producer. We fix a time

horizon and denote the monopolist’s resource at time by . The monopolist extracts the resource according to a measurable rate function (control) . A control is called admissible if the corresponding state process

is non-negative on . Following [6, 7], we assume that the price function when the production rate is employed is given by . For a given constant discount rate , the monopolist’s value function is then defined by

(2.1)

where

is the monopolist’s discounted revenue, and

denotes the time of depletion of the resource under the control . We put

Due to the dependence of on the control, the Hamiltonian depends

on the initial state. This calls for a non-standard approach when applying the maximum principle. We can rewrite the value function as

(2.2)

and so the Hamiltonian is given by

The maximum principle formally states that if is an optimal control

and the induced state process, then there exists an adjoint process , to be interpreted as , that follows the dynamics

and that satisfies the maximum condition

(2.3)

However, for , while does not exist. Moreover, the terminal condition of is not well defined; it will turn out that the derivative does not exist. The way to overcome this problem is to apply the maximum principle only up to the time where is the candidate optimal strategy. In order to obtain the candidate optimal strategy we will determine the value of the adjoint process at the time of depletion and then define the adjoint process on the entire time interval as

(2.4)

We need to distinguish three different cases, depending on whether full exploitation occurs strictly before time , exactly at the terminal time

or whether full exploitation is not optimal. In what follows, we derive a

characterization of the candidates for the optimal exploitation time and terminal condition of the adjoint process in terms of the initial resource level.

•

. In this case the maximum condition (2.3) suggests that to ensure that in

and hence that and

Then is determined by the identity

This gives

(2.5)

where denotes the principal branch of the Lambert-W function, defined as the inverse function of , restricted to the range and the domain . This recovers the formula found by dynamic programming methods for the case in [6, Proposition

3].

•

. In this case we expect the terminal value to be obtained by the identity

which yields

(2.6)

Note that in general, and that only if . This suggests that full exploitation is not optimal if .

•

. In this case, we expect the problem to be locally independent of , and hence that . This yields and therefore necessarily and .

Using the above obtained terminal values we now define the adjoint process by (2.4) for every . By construction for all and for . Moreover, if or . In particular, for any admissible control , the Hamiltonian satisfies

(2.7)

We can now prove that the above constructed candidate optimal strategy is

indeed optimal.

Theorem 2.1(Verification Theorem).

The optimal control at time to the control problem (2.2) with initial state is given by

where and are given by (2.5) and (2.6), respectively.

Proof.

For notational convenience we drop the dependence of and on . A direct computation verifies that is admissible. Let

be another admissible control and be the corresponding exhaustion time. We put

By definition of the adjoint process on where and if . Moreover, for any admissible control

(2.8)

We now distinguish two cases.

•

The case . In this case it follows from (2.8) that

where the last equality follows from the fact that if and that the term in parenthesis vanishes if .

•

The case . In this case, it follows again from (2.8) that

In view of Equation (2.7), the Hamiltonian is non-positive on and hence

If , then . Else, , and . As a result,

∎

Having determined the optimal control allows us to compute the value function.

Corollary 2.2.

The value function to the control problem (2.1)

is given by the smooth function

This corresponds with the solution to the dynamic programming equation in

the case found in [18, Section 5].

3 The Mean Field Game

To motivate the form of demand functions that we are going to use in the continuum MFG, we first introduce a finite market with oil producers that compete for market share in a one-period game. Associated to each firm are variables and representing the price and quantity, respectively. In the Cournot model, players choose quantities as a strategic variable in non-cooperative competition with the other firms, and the market determines the price of each

good. The market model is specified by linear inverse demand functions, which give prices as a function of quantity produced.

The firms are suppliers, and so quantities are nonnegative.

For , the price received by player is where

(3.1)

The inverse demand functions are decreasing in all of the quantities, and

measures the strength of interaction between players.

In the linear model (3.1), some of the prices may

be negative, meaning player produces so much that he has to pay to have his goods taken away, but negative prices do not arise in competitive equilibrium. Moreover, the goods are similar but differentiated, meaning each player potentially receives a different price as there will be some residual loyalty to obtaining the product from individual suppliers. Most

crucially, the interaction is of mean field type: is affected by the mean production of the other players, and players and () are exchangeable as far as player is concerned.

In the MFG version, there is a continuum of players, say oil producers, who are labeled by their reserves at time. Initial reserves are distributed according to the probability measure on .

Each producer extracts oil in continuous time at a rate , and the price received by this producer is , where is the mean production rate of all the players, and quantifies the degree of interaction between the players. In

the following, the time horizon .

3.1 The best response function

In a first step, we consider the representative player’s best response given the aggregate production of all the other players.

Aggregate production is described by a nonnegative and absolutely continuous function . The derivative of exists a.e. and is denoted by .

Remark 3.1.

It is in fact sufficient here to simply assume which is immediately evident to guarantee nonnegative prices. The a priori bounds are motivated by the following observation: for any candidate optimal control we have

where the right-hand side is the optimal control given infinite reserves.

Any aggregate production function leading to a solution to the MFG therefore necessarily satisfies

We assume throughout that the aggregate production function satisfies the

following compatibility condition. We will see that this condition guarantees that each player fully exploits her initial resources if is large enough. The assumption will be satisfied in equilibrium.

Assumption 1.

There exists such that the aggregate exploitation rate satisfies the compatibility condition

(3.2)

Remark 3.2.

Our compatibility condition is equivalent to . Since we expect to be decreasing in equilibrium (production slows as resources run out), the condition (3.2) puts a lower bound on how quickly that may occur over time.

Let us now consider a representative producer with any initial state at time . We call a control admissible if the state process

is always non-negative.

For or , depending on whether the finite or infinite horizon case is considered,

the value function for the representative producer with respect to a given function is defined by

(3.3)

and the exhaustion time is

By analogy to the single player case, the corresponding Hamiltonian is given by

3.1.1 Heuristics by the maximum principle

As in the single player case Pontryagin’s maximum principle formally states that if is an optimal control, with associated optimal state process and vanishing time , then there exists an adjoint process given by

(3.4)

and satisfies the maximum condition

(3.5)

The challenge is again that the terminal condition of the adjoint process

is unknown. As in the single player case we distinguish again three different cases depending on whether full exploitation is optimal or not.

•

The case . In this case we expect , and so, from (3.5),

the terminal condition of the adjoint process is .

Hence, from (3.4), we have

and the optimal strategy is

(3.6)

•

The case .

In this case the terminal value of the adjoint process is obtained by the identity

which yields

(3.7)

In particular, the terminal condition depends on the initial resource level and if and only if

(3.8)

In this case, the candidate optimal strategy is

•

The case and .

In this case we expect the optimization problem to be independent of and hence that . From (3.5),

this leads to the candidate optimal strategy

Thus, this case occurs when .

3.1.2 Verification Result

In order to carry out the verification argument it will be convenient to define the function

(3.9)

which is the amount of resource extracted up to time by using the strategy (3.6) that would be optimal if the exhaustion time was equal to . The function allows us to determine the optimal exploitation time as a function of the initial resource level. In fact the

derivative of is given by

(3.10)

The compatibility condition (3.2) guarantees that . As a result, the inverse is well-defined on . By Assumption 1,

. Moreover, we see that

(3.11)

and hence that is determined implicitly by the identity

The preceding heuristics suggest that an optimal exploitation strategy for a given initial resource level and a given aggregate production function that satisfies our compatibility condition can be obtained by

first computing the optimal exploitation time by inverting the function introduced in (3.9) on its range , and then applying the maximum principle on . The following result shows that the above heuristics do indeed give us an optimal control.

Theorem 3.3(Verification Theorem).

Let be an absolutely continuous function that satisfies the compatibility condition (3.2). Define the function by (3.9), and

let .

•

. For initial state , , and the optimal control is given by

(3.12)

•

. The optimal control for the initial state is given by

(3.13)

where and are defined in (3.7) and (3.8), respectively.

Proof.

For notational convenience we drop the dependence of

and on the initial state . The proof is similar to the monopoly case; we give it for completeness. First, we recall from the argument following (3.10), that is well-defined. Moreover, it is straightforward to check that i) the candidate in (3.12) and (3.13) are of the form

(3.14)

where the adjoint process is defined in (3.4) , and ii) are admissible. In particular , and the corresponding state process are non-negative. Denoting , we see from the formulas (3.12) and (3.13) that . In order to verify the optimality of the strategy for the first

case in (3.13), we fix an admissible control

, whose exhaustion time is , with the convention if the strategy does not exhaust all of the resource. We denote by . Admissibility requires that . Moreover, since satisfies the maximum condition (3.5),

(3.15)

•

The case . In this case it follows from (3.15) and that

As in the monopoly case, if . If , then the term in parenthesis vanishes. In both cases

•

The case . In this case it follows again from (3.15) that

Using that on , and hence that for all

, we arrive at

If , then . Else, , while because . As a result,

∎

It follows from the verification theorem that all the optimal production rates satisfy the same ODE, albeit on possibly different time horizons and with possibly different terminal conditions. Moreover, from (3.10), the mapping is strictly increasing and so

In particular, if we denote by the survival function associated with the initial distribution ,

then the proportion of players with remaining resources at time is given by . With this, we have the following corollary.

Corollary 3.4.

For all and all functions that satisfy the compatibility condition (3.2), the optimal rate and the aggregate production rate

(3.16)

satisfy the ODEs

(3.17)

(3.18)

on the time interval .

In the case , the terminal condition for (3.17) is , while for (3.18), .

If , then the optimal production rate has terminal condition

(3.19)

where was given in (3.7).

In this case, the terminal condition for the aggregate production rate is

(3.20)

Proof.

The ODE (3.17) follows from differentiating the expression (3.14) for (the positive part being unnecessary on ), using the ODE for , and substituting back for in terms of and . The ODE (3.18) for follows from integrating (3.17) with respect to over . The terminal conditions for follow from (3.12) and (3.13). The terminal condition for comes from integrating (3.19) with respect to over .

∎

Remark 3.5.

Under the compatibility condition, we have as . As a result, . This

shows that the infinite horizon case can indeed be viewed as a limiting case when .

3.2 Solution to the MFG

In this section we prove the existence of a solution to the mean field game. In terms of the optimal controls we are looking for a fixed point of the mapping (3.16). We consider the infinite and the finite horizon case separately. The main difference is that full exploitation occurs in equilibrium if , but may not occur if . It turns out that the infinite horizon case can be solved in closed form. In view of Corollary 3.4 , we have the following characterization.

Setting and in (3.18) to and re-arranging leads to

(3.6),

which is equivalent to

(3.21)

from which compatibility of easily follows.

∎

For any fixed point the equations (3.10) and (3.21) yield the following ODE for :

(3.22)

The key observation is that (3.22) does not depend on . We prove below that the (unique) solution to the MFG can be defined in terms

of the unique solution to the above ODE.

Proposition 3.7.

If the initial distribution has a bounded density or is concentrated on finitely many points, then the preceding ODE has a unique global solution.

The solution can be expressed in terms of the functions defined by

respectively as

(3.23)

Proof.

If has a bounded density, then the mapping is Lipschitz continuous. If is concentrated on finitely many points, then this mapping is locally independent of and hence can be solved iteratively. The functions and are well-defined, strictly increasing, surjective, and satisfy

Now, a direct computation verifies that satisfies the desired ODE.

∎

Note that the inverse of is, in terms of the principle branch of the Lambert- function,

3.2.1 Infinite horizon

We are now ready to solve the MFG in the infinite horizon case. In terms of the functions and , and their inverses we obtain

•

•

In view of (3.21) we can express the unique solution to the ODE (3.17) with terminal condition (3.18) fully in

terms of these functions as

The following theorem verifies that this production rate does indeed solve the MFG in the infinite horizon case.

Theorem 3.8.

The aggregate production rate

is absolutely continuous, takes values in and satisfies the compatibility condition (3.2) as well as the

fixed point property .

Hence, is the unique solution to the MFG (that is absolutely continuous and satisfies the compatibility condition).

Proof.

To verify we use the following representation by Fubini:

(3.24)

Next, by construction satisfies the ODE

(3.25)

and is absolutely continuous in the time variable with

(3.26)

The latter yields that is absolutely continuous with

(3.27)

which is equivalent to

As a result, satisfies the compatibility condition. Moreover, in view of (3.10) and (3.25),

>From this we conclude that and hence the fixed point property . Applying the verification result Theorem3.3 finally verifies that is the unique solution the MFG.

∎

While the individual production rate may not be monotone in general

as illustrated below, it is a direct consequence of (3.24) and (3.27) that the aggregate production rate is nonincreasing.

Corollary 3.9.

The aggregate production rate is nonincreasing.

3.2.2 Finite horizon

In the finite horizon case an additional challenge emerges. While we can still solve the ODE (3.17) using (3.21), due to the dependence of the second and third terminal conditions in (3.19) on we obtain the equilibrium production rate only up to its

terminal value.444In the infinite horizon game both the dynamics and the terminal conditions were defined in terms of and its inverse . This is no longer the case in the finite horizon game. An additional fixed point argument on the terminal value is required

to solve the game. In terms of the yet to be determined terminal condition we do know that

In terms of

(3.28)

we obtain for any admissible process ,

Putting

we obtain for any aggregate equilibrium production rate function that

This means that is a fixed point of the map definied by

where we added the nonnegative cut-off (being redundant for any fixed point) to obtain a map on . Moreover, is nonincreasing and continuous. Hence, it admits a unique fixed point . Since

it follows that

This is important to verify that the induced takes indeed values in

. For ,

The fact that satisfies the compatibility condition has already been established in Corollary 3.6. Let us summarize.

Theorem 3.10.

In terms of the above definitions, the function is absolutely continuous, takes values in , and satisfies the compatibility

condition (3.2) and the fixed point property

Hence, is the unique solution to the finite-time MFG (that is absolutely continuous and satisfies the compatibility condition).

3.3 Examples

We close this section with two examples with infinite time horizon that illustrate that equilibrium production rates need not be monotone, nor smooth.

3.3.1 Discrete initial distribution

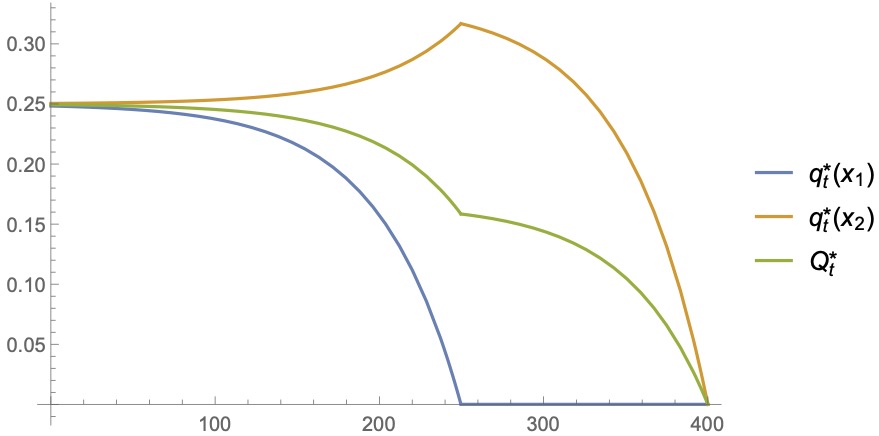

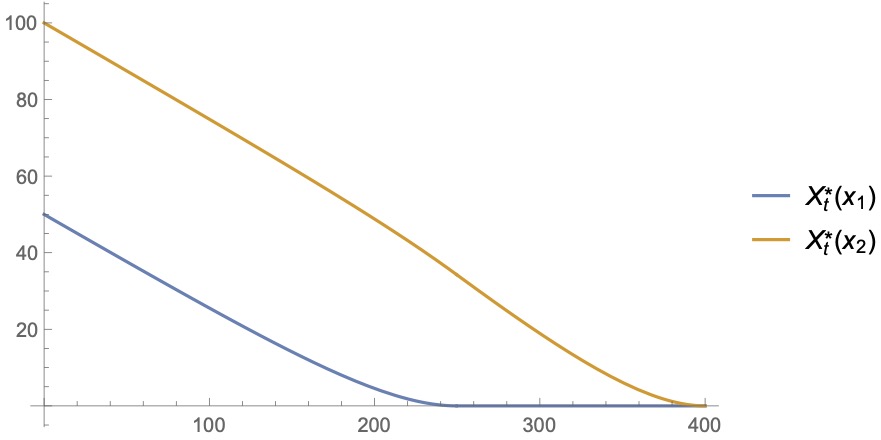

Let us assume that the population of producers splits into two groups within which producers are identical. Producers in Group 1 have an initial resource ; producers in Group 2 have an initial resource . That is, the initial distribution is given by

for and where

denotes the proportion of producers that belong to Group 2. We refer to a representative producer in Group as Player where . The equilibrium production rates can be computed in closed form. The equilibrium production rate of Player 1 is given by

(3.29)

where , while the equilibrium production rate of Player 2 is given by

where . We notice that the equilibrium rate of Player 2 is continuous, but not

differentiable at time . Figure 1 illustrates the

equilibrium production rates and resources of both players. While both Players initially produce at the same rate, Player 1 produces at a decreasing rate while Player 2 initially produces at an

increasing rate, and then at a decreasing rate once Player 1 has run out of resources. Player 2 anticipates the fact Player 1 will eventually drop

out of the market; her production rate reaches it peak at the time Player

1’s resources have been depleted.

Figure 1: , , , ,

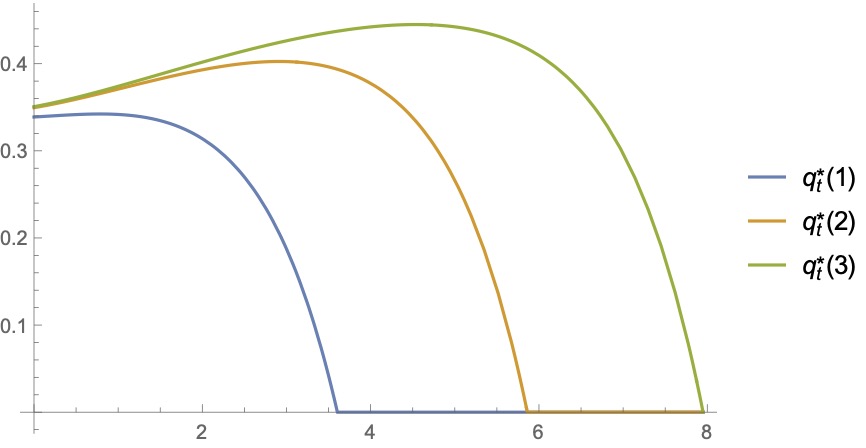

3.3.2 Exponential initial distribution

Figure 2 illustrates the equilibrium production rates for players with initial resources for the

benchmark case of an exponential initial distribution. For absolutely continuous initial distributions players “gradually” drop out of the market so equilibrium production rates do not display kinks. However, we still

observe non-monotonicity of production rates. Players with larger resources do again anticipate that players with lower reserves will eventually drop out of the game. For them it is optimal to produce at higher rates once the number of and the price pressure from their competitors decreases.

Figure 2: ,

References

[1]

A. Bensoussan, J. Frehse, and P. Yam.

Mean Field Games and Mean Field Type Control Theory.

Springer, 2013.

[2]

M. Blonski.

Anonymous games with binary actions.

Games and Economic Behavior, 28(2):171–180, 1999.

[3]

I. Brown, J. Funk, and R. Sircar.

Oil prices & dynamic games under stochastic demand.

Preprint, 2017.

[4]

L. Campi and M. Fischer.

-player games and mean-field games with absorption.

Annals of Applied Probability, 28(4):2188–2242, 2018.

[5]

R. Carmona, J-P. Fouque, and L. Sun.

Mean field games and systemic risk.

Communications in Mathematical Sciences, 13:911–933, 2015.

[6]

P. Chan and R. Sircar.

Bertrand & Cournot mean field games.

Applied Mathematics & Optimization, 71(3):533–569, 2014.

[7]

P. Chan and R. Sircar.

Fracking, renewables & mean field games.

SIAM Review, 59(3):588–615, 2017.

[8]

A. Cournot.

Recherches sur les Principes Mathématiques de la Théorie des

Richesses.

Hachette, Paris, 1838.

English translation by N. T. Bacon published in Economic Classics,

Macmillan, 1897, and reprinted in 1960 by Augustus M. Kelly.

[9]

C. Daskalakis and C. Papadimitriou.

Approximate Nash equilibria in anonymous games.

Journal of Economic Theory, 156:207–245, 2015.

[10]

D. Evangelista and Y. Thamsten.

On finite population games of optimal trading.

ArXiv e-prints, 2020.

[11]

G. Fu, P. Graewe, U. Horst, and A. Popier.

A mean field game of optimal portfolio liquidation.

Mathematics of Operations Research, to appear.

[12]

G. Fu and U. Horst.

Mean-field leader-follower games with terminal state constraint.

SIAM Journal on Control and Optimization, 58(4):2078–2113,

2020.

[13]

G. Fu, U. Horst, and X. Xia.

Portfolio liquidation games with self-exciting order flow.

ArXiv e-prints, 2020.

[14]

J. Gao and H. Tembine.

Distributed mean-field-type filter for vehicle tracking.

In 2017 American Control Conference (ACC), pages 4454–4459,

2017.

[15]

P. J. Graber and A. Bensoussan.

Existence and uniqueness of solutions for Bertrand and Cournot

mean field games.

Applied Mathematics & Optimization, 77:47–71, 2016.

[16]

P. J. Graber and C. Mouzouni.

On mean field games models for exhaustible commodities trade.

ESAIM: Control, Optimisation and Calculus of Variations, 26:11,

2020.

[17]

O. Guéant, J.-M. Lasry, and P.-L. Lions.

Mean field games and oil production.

Technical report, College de France, 2010.

[18]

C. Harris, S. Howison, and R. Sircar.

Games with exhaustible resources.

SIAM J. Applied Mathematics, 70:2556–2581, 2010.

[19]

U. Horst.

Stationary equilibria in discounted stochastic games with weakly

interacting players.

Games and Economic Behavior, 51(1):83–108, 2005.

[20]

M. Huang, R. P. Malhamé, and P. E. Caines.

Large population stochastic dynamic games: closed-loop

McKean-Vlasov systems and the Nash certainty equivalence principle.

Communications in Information & Systems, 6(3):221–252, 2006.

[21]

X. Huang, S. Jaimungal, and M. Nourian.

Mean-field game strategies for optimal execution.

Applied Mathematical Finance, 26:153–185, 2019.

[22]

B. Jovanovic and R. Rosenthal.

Anonymous sequential games.

Journal of Mathematical Economics, 17(1):77–87, 1988.

[23]

J.-M. Lasry and P.-L. Lions.

Mean field games.

Japanese Journal of Mathematics, 2(1):229–260, 2007.

[24]

M. Ludkovski and R. Sircar.

Game theoretic models for energy production.

In Commodities, Energy and Environmental Finance, pages

317–333. Springer, 2015.

[25]

R. W. Rosenthal.

A class of games possessing pure-strategy nash equilibria.

International Journal of Game Theory, 2:65–67, 1973.

[26]

Y. Wang, F. R. Yu, H. Tang, and M. Huang.

A mean field game theoretic approach for security enhancements in

mobile ad hoc networks.

IEEE Transactions on Wireless Communications, 13(3):1616–1627,

2014.