Confidence disc and square for Cauchy distributions

Abstract.

We will construct a confidence region of parameters for a sample of size from Cauchy distributed random variables. Although Cauchy distribution has two parameters, a location parameter and a scale parameter , we will infer them at once by regarding them as a single complex parameter . The region should be a domain in the complex plane, and we will give a simple and concrete formula to give the region as a disc and a square.

Key words and phrases:

confidence disc; Cauchy distribution; central limit theorem2000 Mathematics Subject Classification:

62F251. Introduction

The Cauchy distribution is one of typical bell-shaped and stable laws that has a longer and flatter tail, which makes mathematical handling difficult. But for that reason, typical samples from the Cauchy distribution concentrate on its centre except for a few “outliers” so that there might be cases that to model in Cauchy distribution rather than Gaussian is preferable. From this point of view, in preceding articles [2, 3], we have investigated estimators for the parameters of Cauchy distributions from observations. They are point estimations. We are, however, in the present paper, concerned with an interval estimation, that is, to construct confidence regions. Confidence regions are not only practically often used but also relate to statistical hypothesis testing (see e.g., [15, §7.1.2]), so it goes without saying its statistical importance.

On the other hand, to our knowledge, no concrete regions for Cauchy distributions have been known, while few studies examined them. One of them is a paper by Haas, Bain and Antle [6] which is based on [7]. They discussed mainly the maximal likelihood estimators for Cauchy distributions and proposed confidence intervals for the location parameter ; but unfortunately, the explicit formula for the maximal likelihood estimator is known only for the case of sample sizes of 3 and 4, and furthermore, there is no algebraic closed-form formula for the case of sample size of 5. See [5] and [13]. If the explicit formula is not known, then, the Newton–Raphson method has often been used. Hinkley [8, (2.12)] gives confidence regions for the pair of the location and scale by using the maximal likelihood estimator. It is related to the likelihood ratio test, however, it is complicated, and we are hard to imagine the concrete shape of the region. Vrbik also obtained confidence regions [17] based on the maximal likelihood estimator. See also [4, 9, 10] for related inference methods for Cauchy distributions.

We also would like to point out that, though it is certainly true those numerical simulations using a computer have been becoming an effective method for statistically testing or even constructing confidence intervals, it is not trivial to apply them for Cauchy distributions. To see it, we see, for example, a simple arithmetic mean of the Cauchy random variables still obeys the Cauchy distribution which is independent of the number of the sizes of samples: we emphasize here that to choose a simple and nice estimator for Cauchy distributions is non-trivial. Let us also mention that few unbiased estimators were known so far except, for instance, using MLEs [11] or trimmed average [14] which actually eliminates the outliers from the observations.

In this situation, we would like to propose in the present paper to take a geometric mean (see Remark 2.2 for the terminology). There are several reasons why it is nicer than other quantities, but since this problem belongs to the theory of point estimation, we would not like to go in this direction further here. We point out here only that the geometric mean has enough high integrability, and is unbiased. See [3] for some additional properties of the geometric mean. Also since the geometric mean is an exponential of the arithmetic mean of the logarithms, it is harmless to compute the quantity. We, however, note that the geometric mean is a product of -th power of (probably negative) observations. So we are naturally led to treating all the quantities as complex numbers. In particular, () and are all complex random variables. Therefore, we will gather some basic quantities—mainly expectations of such random variables—in Section 2.

It is well known that, if obeys a Cauchy distribution, exists so that also exists for . The explicit formula of is given by [18, (3.0.3)]. However, the derivation of [18, (3.0.3)] is very complicated, so we will give another way of calculations of them along with in Section 2. They are rather simple and direct. We also would like to expect that, through these manipulations, it becomes clear that considering in the complex plane is not a technical restriction but an essential tool for the Cauchy distributions. In particular, we hope it will be natural to regard the location parameter and the scale parameter of the Cauchy distribution as a single complex parameter but two distinct real parameters; note that this idea was executed by McCullagh [12]. Thus, our statistical inference for the parameters of Cauchy distributions will be actually a problem for a single complex parameter, that is, we guess naturally the location parameter and the scale parameter at once.

Then we will indeed show that a central limit theorem holds for the geometric mean (Lemma 3.3), and then modify it to fit it to derive our confidence region (Lemma 3.4) in the complex plane. It is a standard procedure. Finally, based on the central limit theorem we obtain the confidence region for the Cauchy parameters; as a disc in the complex plane (Theorem 3.5). We will conclude the paper by showing several numerical examples for our confidence disc in Section 4.

2. Auxiliary quantities for Cauchy distribution

In this section, we will gather some basic quantities which will be used in the following sections. In the sequel of the paper, we will denote by a Cauchy distribution whose location parameter is and scale parameter is . We also denote by a real valued random variable when the push forward measure on is , where is a probability space that is defined on. The expectation of with respect to will be denoted by .

For non-integer real number , we almost surely define by as usual when . Here the logarithmic function is defined on a Riemann surface , , that is, using the usual ; is a single-valued holomorphic function. We may simply write as a function on for if there is no confusion. In this case, we regard the logarithmic function has branches, that is, , , , is a multivalued function on .

Remark 2.1.

Since we have an option to take a branch of , the values of and may differ, for instance if ,

Note that, even if , may not be a real number but contains an imaginary part. It does not affect any result while we keep arbitrariness to choose a branch.

Let us emphasise that both and never hold together at the same time. If we prefer then is no more real and if we prefer then becomes complex. Otherwise, neither nor is real.

Hence, it is natural to handle complex valued random variables. For such a complex valued random variable , the expectation is defined as usual: . We can also define a variance as a nonnegative real number: . Moreover, we may define pseudo-variance . If a complex random variable satisfies (1) , (2) and (3) , it is called proper. A proper random variable has a vanishing pseudo-variance. We set , and we also write in place of .

Proposition 2.1.

Let be holomorphic and sublinear growth, that is, and . For , we see that . In particular, the following hold:

-

(1)

for ;

-

(2)

for all .

Proof.

Note that the probability density function for Cauchy distribution is

| (1) |

Since , is holomorphic on the upper half plane. Therefore, the assertion follows immediately from Cauchy’s integral formula. ∎

Corollary 2.2.

If , , are independent, then

-

(1)

their geometric mean is an unbiased estimator for , that is, ;

-

(2)

.

Remark 2.2.

In this paper, we call the geometric mean. Note that is not equal to which may be usually referred to as the geometric mean.

Corollary 2.3.

If , then

-

(1)

pseudo-variances and ;

-

(2)

and are proper complex random variables.

Proposition 2.4.

If and , then,

-

(1)

;

-

(2)

;

-

(3)

;

-

(4)

;

-

(5)

;

-

(6)

.

Proof.

We will use the probability density of the Cauchy distribution in a form given by (1).

First, we will compute an integration along a curve like Figure 1. Using Cauchy’s integral formula and letting and , we clearly get

we note that two poles and stay on the same leaf but each segment in the left-hand side integrals stays on different leaves. Thus, we get (1):

Then, to compute (2), we first note that

Similarly to (1), we get, by Cauchy’s integral formula again,

Noting that with setting ,

we finally have (2):

Now, we note that is the moment generating function of . We also note that , and are holomorphic. Therefore, expanding them as

allows us the following expansion:

so that and provides (3). To show (4) is routine; letting , and ; . Since , (5) also follows.

To show (6), we first note that from the definition. Now we may fix a primary branch, that is, . Hence, . Thus, . Since , we have the conclusion. ∎

For the geometric mean, we obtain explicit values of the covariances of the real and imaginary parts.

Proposition 2.5.

If , then,

and

Proof.

Let and . By the unbiasedness, we see that

and

Since ,

Since

we see that

Since

we see that

3. Central limit theorem and asymptotic confidence disc and square for geometric mean

To state a central limit theorem for the geometric mean of the Cauchy random variables, let us begin with recalling that a complex random variable is standard complex normal if and are independent, and both and obey . Now let us assume that are independent and identically distributed random variables with whose real and imaginary parts have variance and covariance . Then, it holds that as , converge in law to the standard complex normal random variable ([16, Example 2.18]).

We already know from Corollary 2.3 that, if , is proper, that is, the real part and the imaginary part are independent and have a same distribution with mean 0. And we also have computed in Proposition 2.4 (6) that the variance of is . Therefore, we get the following central limit theorem for the logarithms of the Cauchy random variables.

Lemma 3.1.

Let be independent. Then it holds that

as in law.

To get a central limit theorem for the geometric mean around , we need the following complex version of the delta-method [15, Theorem 1.12], for which the proof is omitted since it is straightforward.

Lemma 3.2.

Let and be complex random variables satisfying

as in law, where and is a sequence of positive numbers with . Let be a holomorphic function on a domain containing , then

as in law.

Applying the complex delta method for a complex function , we get the following version of the central limit theorem.

Lemma 3.3.

Let be independent. Then it holds that

| (2) |

as in law.

Unfortunately Lemma 3.3 above could not be applied to get a confidence disc for Cauchy distributed random variables. We will derive the following variant of the central limit theorem.

Lemma 3.4.

Let be independent. Setting

| and | ||||

| (3) | ||||

which is an unbiased and consistent estimator for , we have

as in law.

Proof.

Since converges to and converges to as in probability, Lemma 3.3 implies the conclusion. ∎

Now we can state a formula for our asymptotic confidence disc.

Theorem 3.5.

Let be independent Cauchy random variables with location and scale . Set and as in Lemma 3.4. Then, we have

| (4) |

for , where and denotes a disc in with centre and radius .

Proof.

We first note that . Combining it with Lemma 3.4 asserts that

which immediately leads to the conclusion. ∎

A similar argument enables us to derive an asymptotic confidence square that is slightly smaller than the disc.

Corollary 3.6.

We denote by a square in the complex plane whose centre is and the length of one side is , namely, . Let be the upper -quantile of standard real normal distribution, that is, . Under same settings of Theorem 3.5, and , we have

Proof.

Recall that is rotation invariant in law, that is, for any complex number with , and share a same distribution. This fact guarantees that we may take an absolute value in the coefficient of (2), that is, we have

as in law. Therefore, a same argument with Lemma 3.4 leads

Since and are independent, and obeys , the right-hand side equals to . ∎

We can apply the idea of Corollary 3.6 to get confidence intervals for and , respectively.

Corollary 3.7.

Under the same settings of Corollary 3.6, we have

Proof.

Since we have , the results follow from the same computation with Corollary 3.6. ∎

4. Numerical examples

In this section we will show several numerical examples of Theorem 3.5.

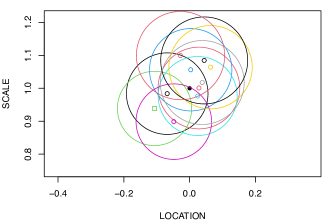

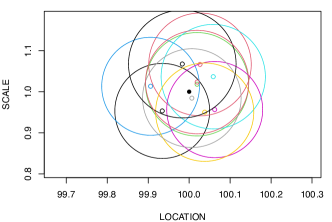

4.1. , 10 trials

centre

log-variance

radius

centre

log-variance

radius

Figure 2 shows 10 confidence discs; each of the samples has of size 1,000. Namely, we generated samples of . Then we computed the geometric mean by the formula , and sample variance by (3). We drew 10 discs using these quantities and (4). A symbol indicates the true value . Symbols point the centre of the disc containing the true value, while is the point that fails.

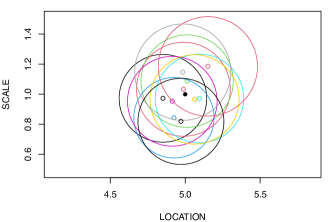

4.2. , 10 trials

Figure 3 also shows the same size of trials and samples, but and for larger true values; we fix to compare with Figure 2 easily. Note that, since , . Note that is small if is large but the radius of the confidence discs increases as increases.

centre

log-variance

radius

centre

log-variance

radius

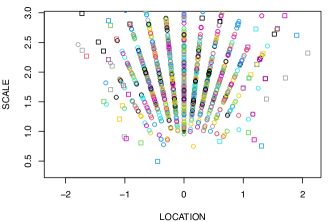

4.3. , 1000 trials

Since the formula (4) to compute our confidence disc is based on a central limit theorem (Theorem 3.4). Therefore, we may fail to guess the parameters if is small.

Figure 4 (omitting to draw circles) shows the case with . In this example, computed , only 925 trials of 1,000 contain the true value.

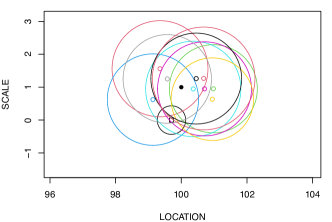

4.4. Large and small

When is much larger than , all data may have the same sign. In such a case, there is a possibility that the geometric mean has the vanishing imaginary part so that we shall guess as zero.

centre

median

log-variance

radius

centre

median

log-variance

radius

Figure 5 shows such a case. One practical way to avoid the situation is to subtract a constant from each datum. It is clear that, putting , an estimate using ’s plus is equal to that of ’s. We also emphasise that subtracting a constant may decrease the absolute value of the geometric mean so that our estimated discs may be smaller, i.e., we may improve the estimation. However, it is impossible to get a suitable constant to make the data consist of both positive and negative values. Therefore, practically speaking, it may be a candidate to subtract the median from all ’s. Then the data will consist of same numbers of positive and negative ones.

centre

log-variance

radius

centre

log-variance

radius

Figure 6 shows the effect of such manipulations. Let us, however, mention that are neither Cauchy nor independent though the central limit theorem may still hold. It seems difficult for us to get a suitable random variable to subtract from each datum. Figure 6 is shown just for convenience; we will not provide any detailed mathematically reasonable explanation for this sort of manipulations.

4.5. Outlier and Gaussian estimation

Here we deal with one-dimensional location-scale families and consider the estimation of the location when the scale is not known. It is common to assume the data are Gaussian distributed if the shape of the frequency forms a bell shape. But when the data have some outliers, using -distributions may give an inappropriate confidence interval. But it should be noted that the Cauchy distribution often gives such “outliers” due to its heavy tail of the density so that we may expect that an inference that is applicable to the Cauchy distribution is more robust.

Here we show a numerical example, which consists of 10 samples; each of them contains 100 values from a standard normal distribution. Then we replace each 100th datum with “5” to mimic an outlier. Tables 1 and 2 below exhibit these differences. The left parts of those tables are the original data, and the right parts are the modified data containing the outliers.

Table 1 shows how such contamination varies the confidence intervals when we use the -distribution with the degree of freedom 99, while Table 2 shows those by using Corollary 3.7. Here the AM and GM denote the arithmetic mean and the real part of the geometric mean, respectively.

It can be seen that the confidence intervals computed using Corollary 3.7 are not so affected by outliers.

4.6. Remark about subtraction

As we see in subsection 4.4 above, the manipulation of subtracting the median works well when the location is far from the origin. However, subtraction entails a delicate problem.

Let and be the real and imaginary parts of . Consider

There is a sequence of random variable such that a.s. and in the above does not converge to in probability as .

This occurs if we let , where and denotes the integer part of . In that case we see that and in particular . is the median of if is odd. In the above subsection, we deal with the case that is even.

Let be a closed interval containing the location in its interior. Then,

Since , we see that

We also have the following.

Proposition 4.1.

Let be a closed interval. Then,

is uniformly integrable.

Proof.

Let . Then, for every ,

Hence,

Since

we see that

∎

On the other hand, if we let , then, for even number , is the median of , and by numerical computations, approximates well, and we conjecture that , a.s. However, we do not have any proofs of it. We do not see why the case that is bad, but, on the other hand, the case that is good, although and are close to each other with high probability if is large.

One way to resolve this delicate issue is to consider the estimator

for some . This is also an unbiased estimator of . This is easier to handle due to the following.

Proposition 4.2.

Let be a closed interval. Then,

converges to a.s. and in as .

Proof.

The a.s. convergence follows from the uniform law of large numbers for .

In the same manner as in the proof of Proposition 4.1, we can show that

is uniformly integrable. Thus, we see the convergence. ∎

There is also a problem in this resolution because there are many possibilities of , and we do not see which should be taken.

We do not delve into this issue in this paper.

Acknowledgements The authors wish to give their gratitude to Dr Thomas Simon for references. The second and third authors were supported by JSPS KAKENHI 19K14549 and 16K05196 respectively.

References

- [1] Yuichi Akaoka, Parameter estimation using complex valued moments for Cauchy distributions, Master’s thesis, Department of mathematics, Shinshu University, January 2020.

- [2] Yuichi Akaoka, Kazuki Okamura, and Yoshiki Otobe, Bahadur efficiency of the maximum likelihood estimator and one-step estimator for quasi-arithmetic means of the Cauchy distribution, Annals of the Institute of Statistical Mathematics (2022).

- [3] by same author, Limit theorems for quasi-arithmetic means of random variables with applications to point estimations for the Cauchy distribution, Brazilian Journal of Probability and Statistics (2022), to appear.

- [4] Gabriela V. Cohen Freue, The Pitman estimator of the Cauchy location parameter, Journal of Statistical Planning and Inference 137 (2007), no. 6, 1900–1913.

- [5] Thomas S. Ferguson, Maximum likelihood estimates of the parameters of the Cauchy distribution for samples of size 3 and 4, Journal of the American Statistical Association 73 (1978), no. 361, 211–213.

- [6] Gerald Haas, Lee Bain, and Charles Antle, Inferences for the Cauchy distribution based on maximum likelihood estimators, Biometrika 57 (1970), no. 2, 403–408.

- [7] Gerald Nicholas Haas, Statistical inferences for the Cauchy distribution based on maximum likelihood estimators, Doctoral dissertations. 2274., University of Missouri–Rolla, 1969.

- [8] D. V. Hinkley, Likelihood inference about location and scale parameters, Biometrika 65 (1978), no. 2, 253–261.

- [9] O. Y. Kravchuk and P. K. Pollett, Hodges–Lehmann scale estimator for Cauchy distribution, Communications in Statistics - Theory and Methods 41 (2012), no. 20, 3621–3632.

- [10] J. F. Lawless, Conditional confidence interval procedures for the location and scale parameters of the Cauchy and logistic distributions, Biometrika 59 (1972), no. 2, 377–386.

- [11] Peter McCullagh, On the distribution of the Cauchy maximum-likelihood estimator, Proceedings of the Royal Society. London. Series A 440 (1993), 475–479.

- [12] by same author, Möbius transformation and Cauchy parameter estimation, The Annals of Statistics 24 (1996), no. 2, 787–808.

- [13] Kazuki Okamura and Yoshiki Otobe, Characterizations of the maximum likelihood estimator of the Cauchy distribution, Lobachevskii Journal of Mathematics (2021), to appear.

- [14] Thomas J. Rothenberg, Franklin M. Fisher, and C. B. Tilanus, A note on estimation from a Cauchy sample, Journal of the American Statistical Association 59 (1964), no. 306, 460–463.

- [15] Jun Shao, Mathematical statistics, 2nd ed., Springer New York, 2003.

- [16] A. W. van der Vaart, Asymptotic statistics, Cambridge Series in Statistical and Probabilistic Mathematics, Cambridge University Press, October 1998.

- [17] Jan Vrbik, Accurate confidence regions based on MLEs, Adv. Appl. Stat. 32 (2013), no. 1, 33–56.

- [18] V M Zolotarev, One-dimensional stable distributions, American Mathematical Society, 1986.