Entropy dissipation and propagation of chaos for the uniform reshuffling model

Abstract

We investigate the uniform reshuffling model for money exchanges: two agents picked uniformly at random redistribute their dollars between them. This stochastic dynamics is of mean-field type and eventually leads to a exponential distribution of wealth. To better understand this dynamics, we investigate its limit as the number of agents goes to infinity. We prove rigorously the so-called propagation of chaos which links the stochastic dynamics to a (limiting) nonlinear partial differential equation (PDE). This deterministic description, which is well-known in the literature, has a flavor of the classical Boltzmann equation arising from statistical mechanics of dilute gases. We prove its convergence toward its exponential equilibrium distribution in the sense of relative entropy.

Key words: Agent-based model, uniform reshuffling, propagation of chaos, relative entropy

1 Introduction

Econophysics is an emerging branch of statistical physics that incorporate notions and techniques of traditional physics to economics and finance [33, 14, 18]. It has attracted considerable attention in recent years raising challenges on how various economical phenomena could be explained by universal laws in statistical physics, and we refer to [11, 12, 31, 25] for a general review.

The primary motivation for study models arising from econophysics is at least two-fold: From the perspective of a policy maker, it is important to deal with the raise of income inequality [16, 17] in order to establish a more egalitarian society. From a mathematical point of view, we have to understand the fundamental mechanisms, such as money exchange resulting from individuals, which are usually agent-based models. Given an agent-based model, one is expected to identify the limit dynamics as the number of individuals tends to infinity and then its corresponding equilibrium when run the model for a sufficiently long time (if there is one), and this guiding approach is carried out in numerous works across different fields among literature of applied mathematics, see for instance [30, 5, 8].

In this work, we consider the so-called uniform reshuffling model for money exchange in a closed economic system with agents. The dynamics consists in choosing at random time two individuals and to redistribute their money between them. To write this dynamics mathematically, we denote by the amount of dollar agent has at time for . At a random time generated by a Poisson clock with rate , two agents (say and ) update their purse according to the following rule:

| (1.1) |

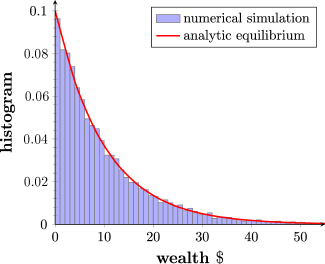

where is a uniform random variable over the interval (i.e. ). The uniform reshuffling model is first studied in [18] via simulation. The agent-based numerical simulation suggests that, as the number of agents and time go to infinity, the limiting distribution of money approaches the exponential distribution as shown in Figure 1.

It is well-known (see for instance [28, 6, 19, 3]) that under the large population limit, We can formally show that the law of the wealth of a typical agent (say ) satisfies the following limit PDE in a weak sense:

| (1.2) |

To our best knowledge, the rigorous derivation of the limit equation (1.2) from the particle system description is absent in most of the literature on econophysics (just like many other PDEs arising from models in econophysics [24, 21, 9]), because the propagation of chaos effect is implicitly assumed in the large limit in most derivations. The remarkable exception is the paper [15], where the author showed a uniform-in-time propagation of chaos by virtue of a delicate coupling argument. In section 5 of this manuscript, we will provide an alternative rigorous justification of the equation (2.8) under the limit .

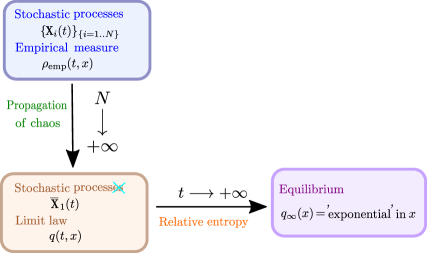

Once the limit PDE is identified from the interacting particle system, the natural next step is to study the problem of convergence to equilibrium of the PDE at hand, it has been shown in [19, 28] that the unique (smooth) solution of 1.2 converges to its exponential equilibrium distribution exponentially fast in Wasserstein and Fourier metrics. In the present work, we demonstrate a polynomial in time convergence in relative entropy, by establishing a entropy-entropy dissipation inequality (see Theorem 5 below) which is not available among the literature. An illustration of the general strategy used in this work (and implicitly in many of the works cited above) is shown in Figure 2.

Although only a very specific binary exchange model is explored in the present paper, other exchange rules can also be imposed and studied, leading to different models. To name a few, the so-called immediate exchange model introduced in [21] assumes that pairs of agents are randomly and uniformly picked at each random time, and each of the agents transfer a random fraction of its money to the other agents, where these fractions are independent and uniformly distributed in . The uniform reshuffling model with saving propensity investigated in [10, 27] suggests that the two interacting agents keep a fixed fraction of their fortune and only the combined remaining fortune is uniformly reshuffled between the two agents, which makes the uniform reshuffling model the particular case . For more variants of exchange models with (random) saving propensity and with debts, we refer the readers to [13] and [26].

This manuscript is organized as follows: in section 2, we briefly discuss the properties of the limit equation (1.2). We show in section 3 convergence results for the solution of (1.2) in Wasserstein distance and in the linearized region. We take on the most delicate analysis of the entropy-entropy dissipation relation in section 4. Finally, we present a rigorous treatment of the propagation of chaos phenomenon in section 5.

2 The limit PDE and its properties

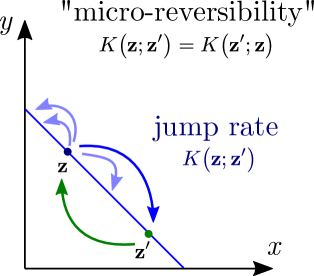

We present a heuristic argument behind the derivation of the limit PDE (2.8) arising from the uniform reshuffling dynamics in section 2.1. Several elementary properties of the solution of (2.8) are recorded in section 2.2. Section 2.3 is devoted to another formulation of the uniform reshuffling model, which can be viewed as a lifting of the reshuffling mechanics (1.1) and is implicitly exploited in [3]. In section 2.4, we highlight a key ingredient known as the micro-reversibility, of the collision operator determined by the right side of (2.8), which allows us to construct certain Lyapunov functions associated with (2.8) (such as entropy).

2.1 Formal derivation of the limit PDE

Introducing independent Poisson processes with intensity , the dynamics can be written as:

| (2.1) |

with independent of . As the number of players goes to infinity, one could expect that the processes become independent and of same law. Therefore, the limit dynamics would be of the form:

| (2.2) |

where is an independent copy of and a Poisson process with intensity . Taking a test function , the weak formulation of the dynamics is given by:

| (2.3) |

In short, the limit dynamics correspond to the jump process:

| (2.4) |

Let’s denote the law of the process . To derive the evolution equation for , we need to translate the effect of the jump of via (2.4) onto .

Lemma 2.1

(Hierarchy of probability distributions) Suppose and two independent random variables with probability density supported on . Let with independent of and . Then the law of is given by with:

| (2.5) | |||||

| (2.6) |

Proof Let’s introduce a test function .

using the change of variables and followed by . We conclude using Fubini that:

| (2.7) | |||||

with defined by (2.5).

We can now write the evolution equation for the law of (2.2), the density satisfies weakly:

| (2.8) |

with

| (2.9) |

2.2 Evolution of moments

Now we will establish several elementary properties of the solution of (2.8):

Proposition 2.2

Assume that is a classical (and global in time) solution of (2.8) and define by the -th moment of :

| (2.10) |

Then:

| (2.11) |

where represents the binomial coefficient.

Proof Notice that the moment can be written as: . Thus, we use the weak formulation of the evolution equation of (2.3) with and deduce that:

since is independent of and . Moreover, Using the independence of and and expanding lead to (2.11).

Corollary 2.3

Proof Writing (2.11) for leads to:

| (2.12) |

and thus . More generally, we proceed by induction to show that converges exponentially, more precisely is of the form:

| (2.13) |

with the limit value of . We first re-write the evolution equation of :

| (2.14) |

with . By induction, has to converge in time. Using variation of constant in (2.14) gives:

| (2.15) |

which leads to (2.13).

From the proposition, we observe that the second moment converges exponentially toward the constant . This behavior could be expected as the equilibrium of the dynamics (2.8) is given by:

| (2.16) |

for which the second moment is equal .

Remark. Moment calculations can be useful in the study of classical spatially homogeneous Boltzmann equation, and we refer the readers to [2] for more information on this regard.

2.3 Pairwise distribution

Before studying the evolution of the entropy of the solution , we make a detour with another formulation of the reshuffling model using a two-particles distribution. Indeed, the jump process (2.4) is a “truncated version” of the following dynamics:

| (2.17) |

where . Introducing a test function , this dynamics lead to:

| (2.18) |

We now translate this evolution equation into a PDE.

Proposition 2.4

Let the density distribution of the process . It satisfies (weakly) the linear evolution equation:

| (2.19) |

with

| (2.20) |

Proof The evolution equation (2.17) gives:

| (2.21) | |||||

To identify the operator associated with the equation, let’s rewrite the “gain term” (dropping the dependency in time for simplicity) using two changes of variables:

with leading to .

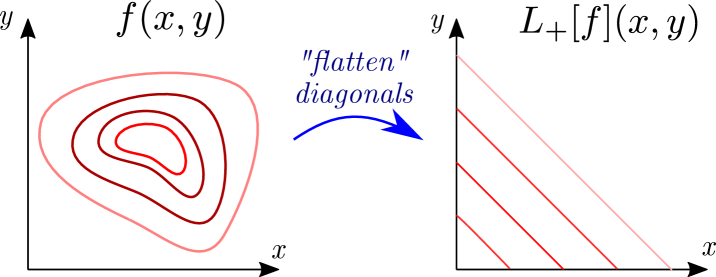

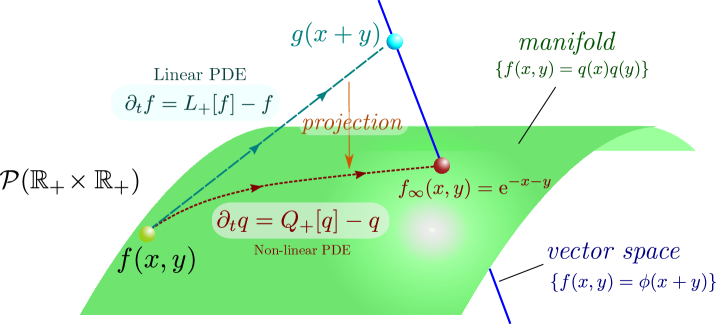

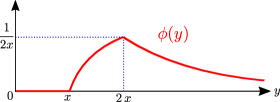

Remark. Notice that the operator (2.20) “flattens” the distribution over the diagonals and thus minimizing its entropy over each diagonal (see Figure 3). In particular, the equilibrium for the dynamics are the distribution of the form: .

The linear operator (2.20) is linked to the non-linear operator (2.5). Indeed, assuming and are independent, i.e. , integrating over the ’extra’ variable gives:

2.4 Micro-reversibility

The evolution equation for (2.19) corresponds to a collisional operator with the kernel:

| (2.22) |

where denote the Dirac distribution. Indeed, writing , the equation (2.19) could be written:

| (2.23) |

where denotes the post-collisional position and the pre-collision position.

Remark. A more rigorous way to define the kernel is through a weak formulation using a test function :

| (2.24) |

The collisional kernel satisfies a micro-reversibility condition, namely:

| (2.25) |

One has to integrate against a test function to make this statement rigorous. As a consequence, we deduce the lemma.

Lemma 2.5

Let a (smooth) test function and the solution of (2.25). Then:

| (2.26) |

Proof We drop the dependency in time to ease the reading:

We deduce that both the norm and the entropy of decay in time.

3 Convergence to equilibrium: Wasserstein and linearization

We carry out an linearization analysis around the exponential equilibrium distribution of the solution of (2.8) and demonstrate an explicit rate of convergence under the linearized (weighted ) setting in section 3.1. These arguments are reinforced in section 3.2 into a local convergence result for the full nonlinear equation. A coupling approach is encapsulated in section 3.3 in order to show that solution of (2.8) relaxes to its equilibrium exponentially fast in the Wasserstein distance.

3.1 Linearization around equilibrium

Now we perform a linearization analysis near the global exponential equilibrium , in a fashion that is similar to [4]. For this purpose, we define the linear operator to be

Setting for , we deduce from (4.3) that

| (3.1) |

where is orthogonal to in . For the linearized equation (3.1), the natural entropy is the norm of , and the entropy dissipation is given by

In particular, it implies that the spectrum of in is non-positive.

Remark. It is not hard to show that the linear operator enjoys a self-adjoint property on the space . Thus the existence of a spectral gap is equivalent to

Remark. Following [20], we give some comments on the space . If is the unique solution of (2.8) and we set as before for , then

where we used the fact that . Therefore, we can see that gives the first-order correction to the expansion of the entropy of around .

We will prove that the linearized entropy decays exponentially fast in time with an explicit sharp decay rate, the essence of which lies in the following lemma.

Lemma 3.1

Let and . Then

| (3.2) |

and the infimum in (3.2) is attained (up to a non-zero multiplication constant) at .

Proof The key ingredient in the proof is the fact that the so-called Laguerre polynomials, defined by

form an orthonormal basis for the weighted space [1]. Thus, for any which is not identically zero, we can write , in which for all . Next, notice that the condition implies that . Moreover, we have thanks to the orthonormality of the Laguerre polynomials . To proceed further, we recall that [32] and for all , whence

Finally, notice that the inequality above will become an equality if and only if for all , or in other words, if and only if up to a non-zero multiplication constant.

We are now in a position to prove the following result.

Theorem 1

Assume that solves the linearized equation (3.1), then we have

| (3.3) |

Proof We will only prove the result for , and the general case follows readily from a change of variable argument. From the discussion above, we already have that

| (3.4) | ||||

Thanks to , it is not hard to see through a change of variable that

Also, a simple calculation yields that

and

Consequently, (3.4) reads

in which the inequality follows directly from the previous lemma. Thus we can conclude by Gronwall’s inequality.

3.2 Local convergence in

We now extend the linearization argument from the previous subsection into a local convergence result for the full non-linear equation.

Theorem 2

There exists some such that if at some time ,

then converges to and for any , there exists such that

Proof For a solution , we denote and calculate

Denote

and calculate

So first of all,

On the other hand,

Hence,

Coming back to the equation, we have that

Using the previous calculations on the spectral gap of , we can conclude that

which finishes the proof with a Gronwall bound.

We can couple this with an interpolation argument to modify the smallness assumption in weighted by using the relative entropy, which leads us to Theorem 3 below, whose proof will be deferred to the appendix (as the proof of Theorem 3 relies on several a priori estimates established in section 4).

Theorem 3

Assume that for some , . Then there exists some such that if at some time ,

we have that converges to and for any , there exists such that

3.3 Coupling and convergence in Wasserstein distance

In this section we shall employ a coupling argument to demonstrate the convergence of the solution of (2.8) to the exponential probability density function given by (2.16). Before we state the main result of this section, we first collect several relevant definitions.

Definition 1

For random variables and taking values in , we write to mean that and are mutually independent. Also, the Wasserstein distance with exponent 2 between two probability density functions (say and ) is defined by

where the infinimum is taken over all pairs of random variables defined on some probability space and distributed according to and , respectively.

Next, we present a stochastic representation of the evolution equation (2.8), which is interesting in its own right.

Proposition 3.2

Assume that is a solution of (2.8) with initial condition being a probability density function supported on with mean . Defining to be a -valued continuous-time pure jump process with jumps of the form

| (3.5) |

where is a i.i.d. copy of , is independent of and , and the jump occurs according to a Poisson clock running at the unit rate. If , then for all .

Proof Taking to be an arbitrary but fixed test function, we have

| (3.6) |

Denoting as the probability density function of , (3.6) can be rewritten as

After a simple change of variables, one arrives at

| (3.7) |

Thus, must satisfy and the proof is completed.

Remark. Using a similar reasoning, we can show that if is a -valued continuous-time pure jump process with jumps of the form

| (3.8) |

where is a i.i.d. copy of , is independent of and , and the jump occurs according to a Poisson clock running at the unit rate. Then implies for all .

The main result of this section is recorded in the following theorem:

Theorem 4

Under the setting of Proposition 3.2, we have

| (3.9) |

Proof Fixing , we need to couple the two densities and . Suppose that and are -valued continuous-time pure jump processes with jumps of the form (3.5) and (3.8), respectively. We can take and as in the statement of Proposition 3.2 and Remark 3.3, respectively. Meanwhile, we require that , and , i.e., several independence assumptions can be imposed along the way when we introduce the coupling. We insist that the same uniform random variable is used in both (3.5) and (3.8). Moreover, we impose that and . As a consequence of the previous proposition and remark, and for all , whence and , . Also, we have that for all . Thanks to the aforementioned coupling, we then have

Now we pick with law so that , and a routine application of Gronwall’s inequality yields (3.9).

4 Entropy dissipation

We state our main result, Theorem 5, in section 4.1 so that readers know exactly what is at stake. We will present various expressions of the entropy and entropy dissipation associated to the solution of (2.8), along with a discussion of the strategy of the proof of Theorem 5 in section 4.2. A sequence of auxiliary lemmas and corollaries are recorded in section 4.3 and 4.4. Finally, a full proof of Theorem 5, built upon all of the preparatory work from 4.1 to 4.4, is shown in 4.5.

4.1 Main result

For the integro-differential equation (2.8), a common strategy [6, 19, 28] is to use the Laplace transform or Fourier transform of (2.8) to prove the exponential decay of solution of (2.8) to in some Fourier metric. However, little analysis of (2.8) has been carried out without resorting to Laplace or Fourier transform. In particular, we would like to show the dissipation of relative entropy, i.e., , along solution trajectories:

| (4.1) |

It is reasonable to expect the validity of (4.1) as the exponential probability density maximizes the negative entropy among all continuous probability density functions supported on with prescribed mean.

The following proposition together with its proof should be a reminiscent of the calculations carried out for a standard Boltzmann equation arising from the kinetic theory of (dilute) gases [35].

Proposition 4.1

Let be a (continuous) test function on and assume that is a smooth solution of (2.8), then we have

Moreover, inserting and employing the fact that total mass is conserved (i.e., for all ), we obtain the dissipation of relative entropy:

where

| (4.2) |

Proof We notice that the PDE (2.8) can be rewritten as

| (4.3) |

(thanks to Proposition 2.2). Omitting the time variable for simplicity, we deduce that

Remark. The dissipation of the relative entropy can also be seen via an alternative perspective. Indeed, we fix and assume that and are i.i.d -valued random variable with its probability density function given by , and we define with being independent of and . Then we deduce from the PDE (2.8) and Lemma 2.1 that

| (4.4) | ||||

where represents the cross entropy from to , if the laws of and are given by and . It can be shown [3] that the joint entropy of is always no more than the joint entropy of , whence the rightmost side of (4.4) is non-positive.

Corollary 4.2

Proof By Proposition 4.1, we see that

Since and , must be the exponential probability density provided by (2.16).

We will prove that polynomial in time. Without of loss generality, throughout the argument to be presented below we will set , i.e., for . Our main result is stated as follows:

Theorem 5

Under the assumptions of Lemma 4.7 below, we have for some constant and for any that

| (4.5) |

To our best knowledge, Theorem 5 is the first entropy-entropy dissipation inequality established for the uniform reshuffling dynamics.

4.2 Basic expressions of the entropy-entropy dissipation

Let us start by looking at the strong convergence of the pairwise distribution, which is essentially trivial. Indeed, we recall the linear PDE (2.19), which reads

where

Then denoting

| (4.6) |

we can rewrite (2.19) as , whence

Hence and trivially

| (4.7) |

Unfortunately this cannot be used to show the convergence on the actual equation for because the two models are not equivalent: If solves (2.8), which is nonlinear, then in general does not solve (2.19). The one exception is when is some exponential.

This can also be seen from the fact that in the argument above does not necessarily converge to an exponential but to whatever was. The rate of convergence is also too fast as the second moment of converges much slower for example.

We will still find some of the structure above in the entropy dissipation for but that is one reason why the entropy dissipation is not easy to handle. In particular, the entropy dissipation will vanish whenever which seems to create some degeneracy.

Next, we can rewrite the dissipation term in a manner that will make the connection with the exponential more apparent. We define for simplicity , and as before

Finally, we also define

We remark here that coincides with the collision gain operator defined via (2.5). With these definitions, we have

Lemma 4.3

One has that

or as well that

Formally this forces to be close to so this is a very similar term to the one that we had found when looking at equation (2.19). It is some sort of degeneracy because it does not directly force to be close to so we will have to resolve it. Of course since , forces to be some exponential and therefore this should be possible.

Proof We can first simply rewrite

Observe that by swapping and

Changing variable , we get that

Hence

In other words,

Now, we observe that

Indeed, a change of variable and yields

By the same change of variables, we also have

Hence

Finally as , we may also notice that

So we also have that

concluding the estimate.

Next, we intend to collect here some various bounds stemming from the dissipation term, the essence of those bounds lies in the following lemma.

Lemma 4.4

We have that

in which

for any such that .

Proof Indeed, as is concave,

and the proof is completed.

As a consequence of this lemma, inserting and then , we then deduce that

where

Remark. We also note that (since ) and so

by virtue of the fact that . Thus,

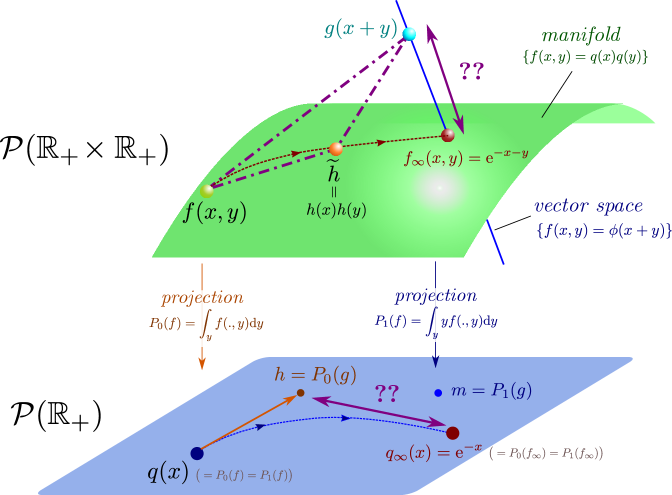

This leads to a possible strategy: Control in terms of , and . Then control by the previous quantities and . We can then estimate via and some control on the decay of at infinity. So in the end this would lead to some kind of bounds on in terms of the dissipation term. We illustrate the strategy in Figure 6.

However normally it is not possible to switch relative entropy estimates. Indeed, it is not so hard to find examples of non-negative functions with total mass such that

while

Therefore this strategy is not obvious to implement. It should work nicely if we had a control like but the general case is certainly trickier. What saves us is the key observation that here and are actually very nice functions in all cases. For example, and are monotone decreasing so bounded from above and bounded from below on any finite interval (from the propagation of moments on ). This gives us some hope when implementing the aforementioned machinery. We emphasize here that our entropy-entropy dissipation argument draws inspiration from earlier works on Becker-Döring equations and coagulation models [23, 7].

4.3 Switching relative entropies

We note that the relative entropy behaves in the following manner

Lemma 4.5

For any two and for any , then

| (4.8) | ||||

Proof We observe that

On the other hand, around , the function satisfies that for and for . On the other hand for and for . Furthermore lies between and when and larger than for .

Remark. One can also rewrite a little bit the statement of Lemma 4.5 so that we do not need to impose that and are probability measures.

This allows us to “switch” relative entropies between two measures that are comparable.

Corollary 4.6

There exists a constant such that if with and , then

Proof Apply Lemma 4.5 with first on and to find

Thanks to Lemma 4.5 again, we have

Now if then . Similarly if then and moreover

Conversely if then , and

Hence

Note that by Lemma 4.5 applied with , we have that

Also, Lemma 4.5 applied with gives rise to

Assembling these estimates, the proof is completed.

4.4 Additional a priori estimates

This leads us to try to compare and . We first observe that we can get easy upper bounds.

Lemma 4.7

Assume that for some , . Then we have that

Proof We use a Laplace transform by defining

and note that

It is useful to remark right away that the stationary solution to this equation satisfies that which has solutions of the form . Those do blow-up but only for large enough. As a matter of fact since , we can see that we should even have . For this reason, denote now with some such that on . We first show that for all . Indeed, let be such that , then

this is because if , while if then and , leading to the same inequality. Now since

| (4.9) |

together with , we deduce that

which yields via the maximum principle that . Now thanks to (4.9) again and the elementary observation that , we arrive at

which immediately proves the desired upper bound.

Remark. We believe it is possible to prove the exponential convergence of the Laplace transform to over . However, this is not strictly better though than having the exponential convergence in some weak Wasserstein norm plus the control of the exponential moments that is given above, so we did not try too much in this direction.

Out of Lemma 4.7, we may deduce pointwise bounds on and , for this purpose, we need the following preparatory result.

Lemma 4.8

We have that

i.e., is uniformly bounded in time.

Proof To show is uniformly bounded in time, we write

We know that there exists some uniformly in time such that

Moreover, for this we also have . Thus,

Now we recall the equation for to find that for any ,

so if is such that , then

By Gronwall’s inequality, we deduce that , which allows us to finish the proof.

Corollary 4.9

Assume that for some , , then we have that

Proof The first bound follows from the definition of . Indeed, as , we have

Next we observe that is decreasing in , so for any

Since is uniformly bounded in time, this shows the second point.

Finally we recall the equation for , which reads , so we may rewrite (2.8) as

| (4.10) |

Moreover, notice that

Combining these estimates with (4.10) ends the proof.

We now turn to lower bounds on and hence . We start with a lower bound on in terms of .

Lemma 4.10

There exists such that for any ,

| (4.11) |

Proof We note from the equation (2.8) that

Therefore

and we have that for any that

leading for example to the claimed result

with , thereby completing the proof.

Unfortunately, this is not enough to give us a bound between and which would solve everything. Instead, we can first deduce a bound near the origin.

Lemma 4.11

There exists a constant such that

| (4.12) |

Proof For any , we have that

By Cauchy-Schwartz, we have that

On the other hand the convergence of all moments of shows that there exists such that for all ,

Therefore there exists such that whenever and . Finally, we deduce the second result from Lemma 4.10.

We combine this with the following doubling type of argument.

Lemma 4.12

There exists a constant such that for any and , there holds

Proof This is a simple consequence of a lower bound on . Indeed, we have

Therefore,

We can again conclude by virtue of Lemma 4.10.

Lemma 4.13

There exists a constant such that for any and , we have

Proof This is again a consequence of a lower bound on . Indeed,

Thus, by the lower bound on on (thanks to Lemma 4.11), we arrive at

Using Lemma 4.10, we can again conclude.

Owing to Lemma 4.13, we immediately deduce that

Corollary 4.14

There exists some such that for any and any

Proof Define for and if (see Figure 7).

Note that is Lipschitz with

Hence

in which represents the Wasserstein distance (with exponent 1) between and . Thanks to the exponentially fast in time of the convergence , which is a simple consequence of Theorem 4, we deduce that

Note that

Therefore from Lemma 4.13, we can conclude provided that .

4.5 Proof of the main result

Armed with all the previous estimates, we can finally present the proof of Theorem 5.

Proof of theorem 5. We note from our earlier estimates that

For some , we can separate the integral into those , for which

On the other hand, denoting , which is a non-negative convex function on and satisfies for some constant if is bounded, we deduce for any that

where the inequality follows from the Fenchel’s inequality , in which denotes the Legendre convex conjugate of (and one can check that and also ).

We can immediately note that for large . Thus from Corollary 4.9, we have that

Combining both estimates gives rise to

and optimizing in leads to

| (4.13) |

The next step is to change this to . We decompose again

We note that since ,

Applying Corollary 4.9 again, this shows that for some constant , we have that

| (4.14) |

From Corollary 4.9 and Corollary 4.14, we note that on there holds , at least provided that . As we will see soon, we will choose logarithmic in which gives the assumption appearing in the statement of Theorem 5.

Now in the region , we can use Lemma 4.5 in exactly the same manner as what we did in Corollary 4.6, which yields that

Optimizing in , we find that for some (but unfortunately),

| (4.15) |

Now we recall that, as a simple consequence of Lemma 4.4, we have

| (4.16) |

Therefore we now want to change back from to . This is the same process and leads to

| (4.17) |

To finish the proof, we just need to combine (4.17) with (4.16) and (4.15).

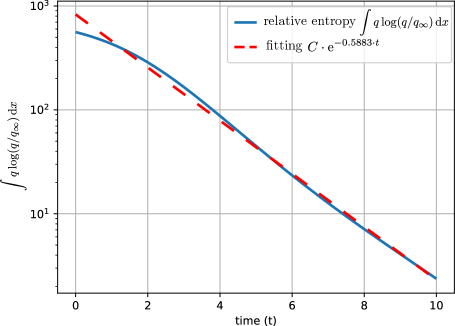

We end this section with a numerical experiment demonstrating the entropic convergence of to , see Figure 8.

5 Propagation of chaos

We give the statement of the propagation of chaos, Theorem 6 in 5.1. A technical lemma that will be employed in the proof of Theorem 6 is displayed in 5.2. We reveal the full proof of Theorem 6 in 5.3.

5.1 Statement of propagation of chaos

In this section, we try to adapt the martingale-based techniques developed in [29, 22] to justify the propagation of chaos [34]. For this purpose, we equip the space with the Wasserstein distance with exponent , which is defined via

for . We will also need the following version of Itô’s formula.

Lemma 5.1

Consider an inhomogeneous Poisson process with intensity , and a random variable left-continuous and adapted to the filtration generated by . We define the compound jump process and its associated compensated martingale by:

| (5.1) |

where is any other left-continuous and adapted process. Itô’s lemma then implies that for any function ,

| (5.2) |

Our main result in this section is stated as follows.

5.2 Switching supremum and expectation

We will also make use of the following result, which allows us to interchange the operation of supremum and of expectation.

Lemma 5.2

Consider a random Radon measure on with and with uniformly bounded second moment almost surely for some constant . Then there exists such that

Proof This is essentially an interpolation argument. First of all, we can always assume that by subtracting a constant. Introduce a classical convolution kernel . We have that which implies that

Then we reduce ourselves to a compact support: since then and

On , we have on the other hand that . Hence

Of course

and by using Fourier series

Hence by Cauchy-Schwartz,

Finally we have that

so that

This allows us to conclude that

or

which finishes the proof by optimizing in and .

5.3 Proof of propagation of chaos

The proof of Theorem 6 occupies the rest of the section.

Proof We recall that the map is defined via

and that a classical solution of

| (5.4) |

exists for , where and is an continuous probability density function with mean whose support is contained in . The map is Lipschitz continuous in the sense that

| (5.5) |

for any . Indeed, we have

where are i.i.d with law , are i.i.d with law , and is independent of and for . By Lipschitz continuity of the test function , we obtain

We now recall an alternative formulation of , given by

so in particular, we may take a coupling of and so that . Assembling these pieces together, we arrive at (5.5).

We are going to prove a more precise control than (5.5), by working directly on . Consider now two random probability measures and with bounded second moment and a deterministic test function . We have that

where we denote

Since , we can always assume without loss of generality that , whence . Now we observe that is deterministic with

| (5.6) |

By (5.6) and recalling that again is deterministic and obtained from , we obtain:

Therefore we conclude that

| (5.7) |

We now observe that the empirical measure is a compound jump process: Define a homogeneous Poisson process with constant intensity . Given the times when jumps, we take the independent: At each , with uniform probability we choose a pair and take

where the are i.i.d. in .

We immediately note that

| (5.8) |

where is uniformly distributed in and independent of all .

We also remark that by the standard control of moments, we immediately have that

| (5.9) |

We now show that the empirical measure of the stochastic system satisfies an approximate version of (5.4). Fix a deterministic test function with , and consider the time evolution of where for some probability measure , we denote by the duality bracket . We emphasize here that can also be random and will indeed be chosen according to to estimate Wasserstein distances involving . Then

Hence by (5.8),

where all are taken at time and where . Hence uniformly over and . On the other hand, we may calculate

by the change of variables . Therefore

| (5.10) |

By Dynkin’s formula, the compensated process

| (5.11) |

is a martingale. Furthermore, comparing with (5.4), we easily obtain that

Taking the supremum over , we therefore have that

By the definition of the distance, we deduce from (5.7) that

in which we have set

| (5.12) |

Thus, Gronwall’s inequality gives rise to

| (5.13) |

In order to establish propagation of chaos for , it therefore suffices to show that

| (5.14) |

To prove (5.14), we treat each term appearing in the definition of separately. The second term in (5.12) approaches to 0 as by our assumption.

To handle the first term, let us write and for notation simplicity. Of course is a compound jump process itself and by combining (5.10) and (5.11)

We may hence use Itô’s lemma as stated in Lemma 5.1, which yields

where and we define

Therefore, we have

By our previous calculations

as is random variable independent of and .

Therefore

and consequently

for a constant that depends only on . This lets us deduce that

Recalling the definition of , we have that

for some random Radon measure with uniformly bounded second moment. Furthermore since and .

Remark. One can readily check that

for all probability densities whose support are contained in , but as we are working on , we can not use any strong distances. Hence, equipping with an appropriate distance so that the operator has enjoys a Lipschitz continuity with respect to the chosen distance is an indispensable step to make the argument above work.

6 Appendix

6.1 Proof of Theorem 3

Proof The whole strategy is of course to find some such that if

| (6.15) |

then we have for the of Theorem 2

| (6.16) |

We start with using Lemma 4.5 for and note that

| (6.17) |

Observe that if then

so the first two terms already provides the straightforward bound

| (6.18) |

Now if then

Therefore for any ,

We now use Corollary 4.9 to find that

in which . Now we take close enough to such that which is always possible if . For this choice of , we hence obtain that

Going back to (6.17), we can conclude that

and combining this with (6.18), we deduce that for some and

It is enough to choose being small enough to conclude the proof.

References

- [1] Milton Abramowitz and Irene A. Stegun. Handbook of mathematical functions Dover Publications. New York, page 361, 1965.

- [2] Ricardo Alonso, Jose A. Canizo, Irene Gamba, and Clément Mouhot. A new approach to the creation and propagation of exponential moments in the Boltzmann equation. Communications in Partial Differential Equations, 38(1):155–169, 2013. Publisher: Taylor & Francis.

- [3] S. M. Apenko. Monotonic entropy growth for a nonlinear model of random exchanges. Physical Review E, 87(2):024101, 2013. Publisher: APS.

- [4] Céline Baranger and Clément Mouhot. Explicit spectral gap estimates for the linearized Boltzmann and Landau operators with hard potentials. Revista Matemática Iberoamericana, 21(3):819–841, 2005. Publisher: Departamento de Matemáticas, Universidad Autónoma de Madrid.

- [5] Alethea BT Barbaro and Pierre Degond. Phase transition and diffusion among socially interacting self-propelled agents. Discrete & Continuous Dynamical Systems-B, 19(5):1249, 2014. Publisher: American Institute of Mathematical Sciences.

- [6] Federico Bassetti and Giuseppe Toscani. Explicit equilibria in a kinetic model of gambling. Physical Review E, 81(6):066115, 2010. Publisher: APS.

- [7] José Cañizo, Amit Einav, and Bertrand Lods. Trend to equilibrium for the Becker–Döring equations: an analogue of Cercignani’s conjecture. Analysis & PDE, 10(7):1663–1708, 2017. Publisher: Mathematical Sciences Publishers.

- [8] Eric Carlen, Robin Chatelin, Pierre Degond, and Bernt Wennberg. Kinetic hierarchy and propagation of chaos in biological swarm models. Physica D: Nonlinear Phenomena, 260:90–111, 2013. Publisher: Elsevier.

- [9] Bikas K. Chakrabarti, Anirban Chakraborti, Satya R. Chakravarty, and Arnab Chatterjee. Econophysics of income and wealth distributions. Cambridge University Press, 2013.

- [10] Anirban Chakraborti and Bikas K. Chakrabarti. Statistical mechanics of money: how saving propensity affects its distribution. The European Physical Journal B-Condensed Matter and Complex Systems, 17(1):167–170, 2000.

- [11] Anirban Chakraborti, Ioane Muni Toke, Marco Patriarca, and Frédéric Abergel. Econophysics review: I. Empirical facts. Quantitative Finance, 11(7):991–1012, 2011.

- [12] Anirban Chakraborti, Ioane Muni Toke, Marco Patriarca, and Frédéric Abergel. Econophysics review: II. Agent-based models. Quantitative Finance, 11(7):1013–1041, 2011.

- [13] Arnab Chatterjee, Bikas K. Chakrabarti, and S. S. Manna. Pareto law in a kinetic model of market with random saving propensity. Physica A: Statistical Mechanics and its Applications, 335(1-2):155–163, 2004.

- [14] Arnab Chatterjee, Sudhakar Yarlagadda, and Bikas K. Chakrabarti. Econophysics of wealth distributions: Econophys-Kolkata I. Springer Science & Business Media, 2007.

- [15] Roberto Cortez. Particle system approach to wealth redistribution. arXiv preprint arXiv:1809.05372, 2018.

- [16] Ms Era Dabla-Norris, Ms Kalpana Kochhar, Mrs Nujin Suphaphiphat, Mr Frantisek Ricka, and Ms Evridiki Tsounta. Causes and consequences of income inequality: A global perspective. International Monetary Fund, 2015.

- [17] Jakob De Haan and Jan-Egbert Sturm. Finance and income inequality: A review and new evidence. European Journal of Political Economy, 50:171–195, 2017. Publisher: Elsevier.

- [18] Adrian Dragulescu and Victor M. Yakovenko. Statistical mechanics of money. The European Physical Journal B-Condensed Matter and Complex Systems, 17(4):723–729, 2000.

- [19] Bertram Düring, Daniel Matthes, and Giuseppe Toscani. Kinetic equations modelling wealth redistribution: a comparison of approaches. Physical Review E, 78(5):056103, 2008. Publisher: APS.

- [20] F. Alberto Grünbaum. Linearization for the Boltzmann equation. Transactions of the American Mathematical Society, 165:425–449, 1972.

- [21] Els Heinsalu and Marco Patriarca. Kinetic models of immediate exchange. The European Physical Journal B, 87(8):170, 2014.

- [22] Jonathan Hermon and Justin Salez. Cutoff for the mean-field zero-range process with bounded monotone rates. Annals of Probability, 48(2):742–759, 2020. Publisher: Institute of Mathematical Statistics.

- [23] Pierre-Emmanuel Jabin and Barbara Niethammer. On the rate of convergence to equilibrium in the Becker–Döring equations. Journal of Differential Equations, 191(2):518–543, 2003. Publisher: Elsevier.

- [24] Guy Katriel. The immediate exchange model: an analytical investigation. The European Physical Journal B, 88(1):19, 2015. Publisher: Springer.

- [25] Ryszard Kutner, Marcel Ausloos, Dariusz Grech, Tiziana Di Matteo, Christophe Schinckus, and H. Eugene Stanley. Econophysics and sociophysics: Their milestones & challenges. Physica A: Statistical Mechanics and its Applications, 516:240–253, 2019. Publisher: Elsevier.

- [26] Nicolas Lanchier and Stephanie Reed. Rigorous results for the distribution of money on connected graphs. Journal of Statistical Physics, 171(4):727–743, 2018. Publisher: Springer.

- [27] Nicolas Lanchier and Stephanie Reed. Rigorous results for the distribution of money on connected graphs (models with debts). Journal of Statistical Physics, pages 1–23, 2018.

- [28] Daniel Matthes and Giuseppe Toscani. On steady distributions of kinetic models of conservative economies. Journal of Statistical Physics, 130(6):1087–1117, 2008. Publisher: Springer.

- [29] Mathieu Merle and Justin Salez. Cutoff for the mean-field zero-range process. The Annals of Probability, 47(5):3170–3201, 2019. Publisher: Institute of Mathematical Statistics.

- [30] Giovanni Naldi, Lorenzo Pareschi, and Giuseppe Toscani. Mathematical modeling of collective behavior in socio-economic and life sciences. Springer Science & Business Media, 2010.

- [31] Eder Johnson de Area Leão Pereira, Marcus Fernandes da Silva, and HB de B. Pereira. Econophysics: Past and present. Physica A: Statistical Mechanics and its Applications, 473:251–261, 2017. Publisher: Elsevier.

- [32] Alexander D. Poularikas. Handbook of formulas and tables for signal processing. CRC press, 2018.

- [33] Gheorghe Savoiu. Econophysics: Background and Applications in Economics, Finance, and Sociophysics. Academic Press, 2013.

- [34] Alain-Sol Sznitman. Topics in propagation of chaos. In Ecole d’été de probabilités de Saint-Flour XIX—1989, pages 165–251. Springer, 1991.

- [35] Cédric Villani. A review of mathematical topics in collisional kinetic theory. Handbook of mathematical fluid dynamics, 1(71-305):3–8, 2002.