Replicating Market Makers

Abstract

We present a method for constructing Constant Function Market Makers (CFMMs) whose portfolio value functions match a desired payoff. More specifically, we show that the space of concave, nonnegative, nondecreasing, 1-homogeneous payoff functions and the space of convex CFMMs are equivalent; in other words, every CFMM has a concave, nonnegative, nondecreasing, 1-homogeneous payoff function, and every payoff function with these properties has a corresponding convex CFMM. We demonstrate a simple method for recovering a CFMM trading function that produces this desired payoff. This method uses only basic tools from convex analysis and is intimately related to Fenchel conjugacy. We demonstrate our result by constructing trading functions corresponding to basic payoffs, as well as standard financial derivatives such as options and swaps.

Introduction

Constant Function Market Makers (CFMMs) [AC20] are a family of automated market makers that enable censorship-resistant asset exchange on public blockchains. CFMMs are capitalized by liquidity providers (LPs) who supply reserves to an on-chain smart contract. The CFMM uses these reserves to execute swaps for traders, allowing a swap only if it preserves some function of reserves, known as the trading function or invariant. For example, Uniswap [ZCP18] only allows trades that keep the product of the reserves after the trade equal to the product of the reserves before the trade.

A key question first explored in [AKC+19] concerns the returns that LPs receive for their capital. As shown in [AC20], the value of the LP’s assets in a CFMM can be determined by solving a convex problem over the CFMM’s trading set. This method allows one to compute explicit expressions for the value LPs receive from most popular CFMMs, such as Uniswap and Balancer, as well practical lower bounds for a larger class for trading functions. Additional work such as [AEC20, EAC21] has explored the impact of parameters such as trading-function curvature and swap fees on LP returns.

Here, we consider what may be called the ‘inverse’ problem. Rather than deriving the LP’s payoff for a given trading function, we seek to find the trading function that guarantees that LPs receive a certain payoff. By contributing capital to the CFMM, LPs will statically replicate their desired payoff. This is a generalization of the problem considered in [Eva20, §5] that shows how to replicate continuously-differentiable payoffs using constant mean trading functions with dynamically-adjusted weights. These constructions require continual updates from on-chain oracles that may be expensive, complex to manage, and are often vulnerable to front-running attacks. In contrast, the trading functions we derive in this work are not time-varying and do not depend on external price oracles, so they are likely easier to implement in practice.

Hedging.

One obvious question is: why would one want to implement such desired payoffs? Trading on blockchains has a number of idiosyncrasies that make dynamic hedging strategies expensive to execute. In particular, unlike centralized venues, most blockchains prevent spam and denial of service attacks by charging users a fee per transaction. This fee, known as gas on networks like Ethereum, can be a dominant cost to on-chain traders during times of high market volatility [DGK+19, KCCM20]. Moreover, the volatility of gas costs on Ethereum makes on-chain dynamic hedging strategies more complex to manage successfully.

In contrast, CFMMs allow the LP to achieve a desired payoff by passively contributing capital. Rather than requiring LPs to continually rebalance their holdings through on-chain trades, CFMMs incentivize arbitrageurs to adjust reserves to the level required to achieve their desired hedge. In effect, this approach outsources the cost and complexity of on-chain trading to specialized parties. As discussed in §A, the added simplicity for the hedger is not without trade-offs as LPs are subject to arbitrage losses. However, small fees have been shown mitigate these costs in certain settings [EAC21].

Limitations.

The payoffs one can replicate using the methodology presented in this paper are limited to concave, nonnegative, nondecreasing functions of price. An instructive analogy is as follows. In limit order books, a resting limit order can roughly be thought of as an option which the market maker sells to participants—who are executing market (liquidity removing) orders—that allows them to purchase or sell a quantity of an asset at a given price [Gre16, Chapter 6]. (The precise replication of a market maker’s portfolio of limit orders as a covered options is complicated somewhat by the fact that trades depend on the positions in the queue [FMT07, MY14], but this point is not essential here.) Being short an option generates a concave, or ‘negative gamma,’ payoff. By virtue of allowing users to execute a set of trades at predetermined prices, CFMMs can also be seen as having negative gamma payoffs which lead to ‘impermanent loss’ [AC20, AEC20, Cla20] for LPs. On the other hand, replicating convex payoffs (such as long positions in options) requires the ability to short shares in a CFMM, or to use external price oracles, as described in [Eva20].

Summary.

The outline of this article is as follows. In the next section, we describe the problem of constructing a trading function that produces a CFMM with a desired payoff function. In §1, we present some basic definitions along with a solution method for recovering the desired trading set and corresponding (equivalent) trading functions. We derive trading functions for some basic examples such as linear and quadratic payoffs in §2. In §3, we proceed with practical applications, such as recovering the constant-mean function used in Balancer [MM19] as well as constructing trading functions for replicating the Black-Scholes prices of covered European calls and perpetual American puts. We give some possible future directions in §4.

1 General solution

In this section, we will present a general method for constructing a CFMM trading function whose value function matches a desired payoff function, within a reasonable domain. We start with some basic definitions and provide a relatively general solution method. We continue with some basic (and not so basic) applications of the method.

Trading function.

A (path independent) CFMM is defined by its trading function and its reserves . The reserve specifies the quantity of coin available to the CFMM contract, while the function specifies the behavior of the contract. More specifically, the contract will allow any agent to trade with the reserves, so long as the new reserves, , after the agent has added or withdrawn the required quantities, satisfy

Some definitions require that the inequality be an exact equality, but this point is not essential, since, in practice can always be made an increasing function in its arguments, so any rational agent will ensure that the inequality is saturated; see, e.g., [AC20, §2.1] for more.

Portfolio value function.

We will assume there exists some external market with a fixed reference price . Here is the price vector for the coins the CFMM trades, such that is the price of coin in this external market. We will call the total value of reserves, after arbitrage, the portfolio value or liquidity provider payoff of a CFMM, represented by some function . In the case where the CFMM is path-independent, with concave nonincreasing trading function and constant , [AC20, §2.5] shows that the function is equal to

The economic interpretation of this definition of is simple: an arbitrageur is engaged in a zero-sum game with liquidity providers. The arbitrageur’s payoff is maximized when the portfolio value, , of a liquidity provider is minimized over the valid reserves ; i.e., those that satisfy . (This is a simple restatement of the optimal arbitrage problem. For more see, e.g., [AC20, EAC21].)

Very generally, we will define the portfolio value over a feasible set of reserves as

| (1) |

This includes the previous definition by setting , and this ‘more general’ definition will slightly simplify the derivation presented below. (In fact, both definitions are equivalent in that, given a convex set , we can construct a concave function whose 0-superlevel set is equal to . We give an explicit construction later in this section.)

Desired payoff.

One very natural question is: given a desired payoff function (i.e., a desired ), is it possible to create a trading function which results in this payoff? Another slightly more casual way of phrasing this problem is: can we ‘invert’ formula (1), given ?

In general, the answer is no. It is nearly immediate, given any , the function is always a concave function because it is the infimum of a family of linear functions, indexed by . Second, because is some infimum over with both and nonnegative, it must be nonnegative. Third, given any , we have that

so is nondecreasing in its arguments. And, finally, note that the function is 1-homogeneous in terms of , by definition; i.e., for any , the payoff function satisfies

This limits the set of payoff functions we can find a CFMM trading function for, since must be concave, nonnegative, nondecreasing, and 1-homogeneous in order for there to exist a CFMM trading function with as its liquidity provider payoff. (We will see that 1-homogeneity is not as strong of a condition as it appears at first glance, and we show how to deal with this in §2.)

Consistent payoff functions.

We will then say is a consistent payoff function if it is concave, nonnegative, nondecreasing, and 1-homogeneous. Clearly, then, the value function of any CFMM will always be consistent, from the discussion above. In the next section, we will also see that the converse of the above statement is true: any consistent payoff function has a path independent CFMM that yields this payoff. We will also show how to construct a CFMM with a desired consistent payoff.

Discussion.

The conditions above all have nice economic interpretations. The concavity of the function implies that ‘impermanent loss’, also known as ‘negative gamma’ in finance, is an intrinsic property of liquidity provision in path-independent CFMMs, as it holds for any possible CFMM in practice. The nonnegativity simply implies that a liquidity provider position always has nonnegative value, while the fact that is nondecreasing implies that the position of liquidity providers does not get worse as coins increase in value. Finally, the 1-homogeneity is a notion of ‘scale-invariance,’ i.e., scaling the numéraire should simply scale the total portfolio value of a liquidity provider’s position. While we have shown that these conditions are necessary, we will also show that they are sufficient in the remainder of this section.

1.1 Solution method and equivalence

The method presented here can be seen as a special case of Fenchel conjugacy, with some slight modifications. Though not necessary, since we will introduce the tools required in this note and give self-contained proofs, the results here are essentially corollaries of well-known theorems in convex analysis, with the most notable being strong duality. We refer the reader to, e.g., [BV04, §5] for further reading.

Given a consistent payoff function , we will first find a set of reserves corresponding to the payoff function . We will then show that the set will also have as its payoff function, as defined in (1). We then find an explicit trading function, , whose 0-superlevel set is equal to and therefore has the desired payoff function, .

Feasible reserve set.

Given some concave payoff function , we will define its feasible reserve set as

| (2) |

In other words, is the set of reserves for which the portfolio value of the reserves, at any cost vector , is always no smaller than . Note that the set is convex as it is the intersection of a family of hyperplanes parametrized by .

1.1.1 Equivalence

We will show that, if is a nonnegative, concave, 1-homogeneous payoff function with feasible reserve set , then has payoff, as defined in (1), given by .

Using the definition of in (2), we can rewrite problem (1) in extended form

| minimize | (3) | |||||

| subject to |

with variable . We will write for the optimal value of (3), which depends on .

Lower bound.

Clearly, we know that

since, if is optimal for , then

where the inequality follows from the fact that is a feasible point for problem (3). (In the case that an optimal value doesn’t exist, though one can show it always does, we may replace with a sequence that is feasible and converges to the optimal value.)

Upper bound.

It will suffice to show that there exist some reserves such that ; i.e., is feasible for problem (3) with objective value equal to . Because is feasible for (3), then, by definition of optimality, we will have that , as required.

First, pick any ; i.e., is a supergradient of at , such that, for any we have

| (4) |

Such an exists because is a concave function and is nonnegative because is nondecreasing. (As a side note, is equal to when the function is differentiable at . See, e.g., [Roc70, Thm. 25.1].) Now, let in (4) to get

where by the homogeneity of . On the other hand, let in (4) to get

Since because is 1-homogeneous, we have

so . We can now rearrange (4) to get

for any , which means that by the definition of in (2). From before, this means that is feasible for (3) and, because its objective value is , we must have that .

Result.

Putting both statements together yields that for every , and therefore the set has the desired payoff. In fact, the proof given above has a few simple but important consequences. For example, dropping the monotonicity requirement on implies that there might exist reserves in which are negative. One way to deal with such a problem is to take the intersection of with the nonnegative reals, , but then need not equal as defined above, and the proof above also gives a simple way of quantifying the gap. Similar results and extensions also hold for the nonnegativity requirement for , the concavity of , and so on, which we leave as open questions for future research.

1.1.2 Constructing a trading function

From the previous discussion, given a desired payoff function we can easily find a trading set such that has payoff equal to . While this may suffice for some applications, it is often easier to work with the functional form of a CFMM. More specifically, we will look for a concave trading function such that some superlevel set of the function is equal to the set .

One example of such a functional form (there are many equivalent ones) is given by

| (5) |

where ranges over all real -vectors. This function has the desired property since

and therefore if, and only if, , so can be used as the CFMM trading function, as required. We also note that is the negative Fenchel conjugate of , with negated arguments, i.e.:

This equation, along with the portfolio value equation in [AC20, §2.5] implies, roughly speaking, that the portfolio value function and the trading function for a CFMM are essentially Fenchel conjugates of each other.

Discussion.

In general, unless certain conditions are satisfied, it is possible that applying equation (5) directly to any desired payoff function need not yield a CFMM whose payoff function is equal to at all prices. We only guarantee equality in the case that is consistent, but find that this procedure is also useful in cases where is not. (As discussed, the proof given in §1.1.1 gives a way of quantifying how much the payoff might differ in cases where is not consistent.) Additionally, we note that the function (5) will always be a set-indicator function; i.e., will always be either 0 or at every point, due to the 1-homogeneity of . In some cases, the set-indicator description can be simplified, but this need not always be true.

2 Basic examples and properties

We show two basic examples, where the desired payoff is linear and, later, quadratic, and introduce some basic tools which help simplify derivations.

2.1 Linear payoffs and offsets

In this case, we will find a CFMM that produces a linear payoff function; i.e., what is a CFMM that corresponds to the payoff function:

where , . It is not difficult to intuit what the behavior of the LP (and therefore, of the CFMM’s trading function) should be. In order to replicate this payoff, the LP should simply hold of asset , which would be equivalent to the CFMM disallowing any trades other than the null trade. We will apply the method to this example, where the solution is known, as a simple, but potentially useful exercise.

Linear payoff.

As before, we have that

which is exactly the CFMM we expect from the intuitive result: the CFMM can only allow trading if it a trade leaves the reserves at .

Linear offsets.

A useful and general tool used in the previous derivation is that a linear offset of the payoff function results in a linear offset of the arguments of the trading function. More specifically, given a payoff function , with trading function , the trading function corresponding to the ‘linearly offset’ payoff:

| (6) |

where , is

This follows immediately from (5) and has an obvious economic interpretation: any linear offset in the value function is simply equivalent to adding that quantity of coins to the reserves. This may help in simplifying derivations since a number of payoffs are simply linear offsets of other, potentially well-known payoff functions.

2.2 Perspective transform and quadratic payoffs

It is also sometimes easier in practice to specify the payoff with respect to a numéraire, rather than with respect to a general price vector. For example, if we assume that the th coin is the numéraire, and is the price vector for the first coins with respect to the th coin, then this is equivalent to specifying the ‘reduced payoff function’ for each , which depends only on the first coins.

Perspective transform.

A simple approach to constructing an coin, 1-homogeneous payoff function that is concave, nonnegative whenever is also concave, nonnegative is by the use of the perspective transform of , which we define here as the function such that

| (7) |

where is the price of the first coins while is the price of the numéraire. The concavity of , given the concavity of , follows from a basic argument (see, e.g., [BV04, §3.2.6]), while positivity is immediate from the definition. The fact that is 1-homogeneous is easy to see as well since, if and we have

while the case where is obvious. Additionally, it is worth noting that

so this recovers the original payoff when the numéraire’s value, , is set to 1, as expected.

Quadratic payoff.

Given the affine case, the next natural question is, can we find the CFMMs corresponding to more complicated payoff functions? For this case, we will consider a CFMM whose payoff is a concave quadratic. To our knowledge, a CFMM of this form is not known in the literature, but the procedure above gives a simple derivation. In particular, we want a CFMM that yields a payoff of

where is a strictly positive definite matrix (the case of positive semidefinite matrices is also easy to identify, but requires some additional conditions on and the nullspace of , which we leave as a simple extension). Note that this is not positive everywhere so the payoff of this CFMM cannot match that of everywhere. On the other hand, we will see that both are equal within some specific set of cost vectors .

To start, we will first consider the perspective transformation (7) of to get

Using (6), it suffices to consider the simpler function

as the rest is simply a linear offset of this function, which follows from the previous discussion. From (5) we have

where are the reserves of the first coins, while is the reserve of the numéraire. To find we will first partially minimize over , using the first order optimality conditions, to get

so

Finally, adding the linear offset , using (6) gives

as required. Note that, because is negative and decreasing for large enough , the payoff may not be correctly replicated at all possible price vectors . In fact it is not hard to show that once is outside of some compact set, the resulting payoff is always 0, and we leave this as a simple, but interesting, exercise for the reader.

3 Practical applications

In this section, we outline several practical applications of this general solution method in the more specific case where we have two coins, a traded coin and the numéraire. The first example gives a simple way of reconstructing the well-known constant mean market makers, such as those created and implemented by Balancer, by attempting to replicate an intuitive payoff function.

We then proceed with a realistic financial product, the covered call. We present both static replication of the asset payoff at expiry and of the option price using the Black-Scholes model. In [Eva20] it was shown that the covered call can be statically replicated by a constant mean market maker with dynamic weights. The replication methodology used here does not require one to update the trading function using an external price oracle. We expect that this will reduce the cost and complexity of implementing these CFMMs in practice. Finally, we present the example of a perpetual American put option. In this subsection, unlike in the previous subsections, we have that , , and are all scalar quantities, where is the price of the asset in question.

3.1 Balancer

We can recover some known payoff functions in a few important cases. For example, we can ask: what is a CFMM trading function whose payoff is a (concave) power of the price? In other words, can we find a CFMM whose payoff is:

for some ? As is known in the literature (see, e.g., [AC20, Eva20, MM19]) we will see that the trading function for Balancer, or that of a constant mean market, is one such trading function (and, in fact, will be the trading function we recover).

Taking the perspective of as in (7), we have, where is the new variable (the ‘price of the numéraire’), we have

(Note that is then the weighted geometric mean of and with weights .) So, we can recover the trading function by using (5),

This implies that

| (8) |

It is also easy to show that

is equivalent to . We can of course simplify this further by dropping the constant multiplier , which yields the usual form for constant mean markets; i.e.,

To show (8), we consider three separate cases. First, , otherwise is unbounded from below. On the other hand, if

then picking and for with means that

as . Finally, if

then, using the weighted AM-GM inequality we find, for any ,

which means that . Clearly, equality is achievable by choosing , yielding (8).

This proof easily generalizes to the case where and

where and for , with equivalent trading function, for ,

(This is just the coin constant mean market maker, e.g., Balancer, as is used in practice.)

3.2 Covered call at expiry

In the following examples, we assume that we have a ‘risky’ asset with reserve amount and a ‘risk-free’ asset with reserve amount . We seek to find the trading function that corresponds to certain derivative securities. We will restrict our attention to ‘covered’ instruments whose replication does not require short positions in either asset (negative reserve quantities). We note that lending markets and offsetting positions have been proposed as solutions for replicating these types of instruments [Eva20], but do not explore this further in this work.

In this first application, we consider the terminal payoff of a covered call. This strategy involves combining a long position in the risky asset with a short position in a call option on the risky asset. A covered call allows the writer to generate additional income from a long position in exchange for giving up upside for prices above the strike. At expiry, the payoff of a covered call with strike at expiry is

We take the perspective,

For , we have the trading function

where

and

We therefore have the trading function,

In other words, the CFMM only will either hold one unit of the underlying asset or units of the risk-free asset. When the option is out of the money, , the CFMM will hold only one unit of the risky asset . The CFMM will function equivalently to a limit order to sell one unit of the underlying at . When the option is in the money, the CFMM will therefore hold only units of the risk free asset, i.e. . In either case, the arbitrageur will ensure that the CFMM holdes the lower of of and . This implies that the constant sum curve,

will yield the same payoff by allowing the arbitrageur to trade between the underlying and the risk-free asset. This is analogous to the trading rule used in the stop-loss start-gain strategy for replicating an option position [CJ90], but requires full collateralization.

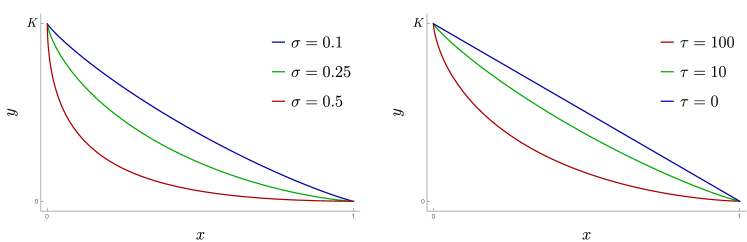

3.3 Black-Scholes covered call price

While the previous example gives the terminal payoff of a covered call, it requires full collateralization, which we expect will not be particularly useful in practice. In this example, we instead replicate the price of the covered call under the Black-Scholes. We chose this model as a standard example because it is well-studied, but note that our approach could accommodate different pricing models and assumptions. The replication in this section will require less initial capital and apply to the price of the instrument at any time prior to expiry. In this case, given a price , we can create a two-coin CFMM whose portfolio value function replicates the Black-Scholes price of a covered call, given by

where is the time to maturity, is the strike price, is the standard normal CDF, and

where is the implied volatility. Here, we assume zero risk-free rate, i.e., , but the extension to the case of a positive risk-free rate is immediate. Taking the perspective of

where we have modified the constants to satisfy

Using (5), we write, for , So, we can recover the trading function by using (5),

Partially minimizing over , we have the first-order conditions

where is defined as

for convenience. We can substitute this result back, and, after cancellations, find:

It is then immediate that:

We plot some examples in Figure 1. When the price of the risky asset and the time to matury are both strictly positive, the covered call payoff will require more capital to replicate a covered call closer to maturity. This can be seen in both the formula for and visually in Figure 1. If one were to update the trading function over time as the option neared maturity, each update would require additional capital. The difference over time is determined by ‘theta’ which captures the time-decay of the option’s price. The no-fee CFMM will not capture gains from theta decay and as such will fail to offer self-financing replication. We conjecture that fees may restore the ability of the LP to profit from theta decay when replicating such positions, as demonstrated in a simpler case in [EAC21]. We discuss theta decay further in §A, but do not resolve this question directly in this work.

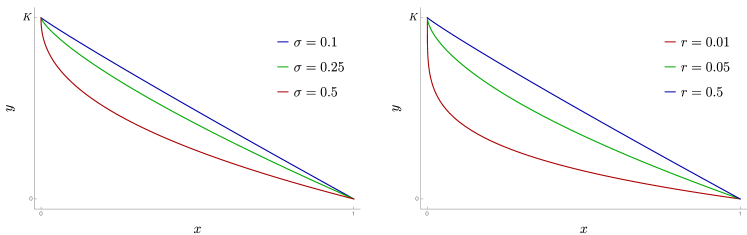

3.4 Perpetual American put option price

We consider a payoff of , where is the Black-Scholes price of a perpetual put option struck at . From [Shr04, Chapter 6], this payoff is

where , is the volatility of the risky-asset and is the risk-free rate. Taking the perspective,

We have the trading function

where

and

The first-order condition is

Substituting this back and after some cancellations we get

Noting that , we can simply use as our trading function. Unlike the previous example, the perpetual American put does not require one to update the curve or contribute additional capital to continue the replication.

4 Conclusion

We demonstrated an equivalence between CFMM trading functions and consistent (i.e., concave, nonnegative, nondecreasing, 1-homogeneous) payoff functions. Our methodology relies only on basic tools from convex analysis and can produce the appropriate trading function for replicating a number of theoretically and practically interesting payoffs. However, we also point to cases where replication requires additional initial capital due to arbitrage costs. Finally, the results presented in this article may have implications for the design of existing CFMMs and indeed qualitatively matches some results in previous work. In particular, the result of [AEC20] that lower-curvature CFMMs are more suitable to lower- volatility assets appears to be confirmed in the discussion of options in 3, wherein the trading functions have lower curvature for lower implied volatility (for a visual illustration, see figures 1 and 2).

Future work.

There are several interesting directions for future research. For example, determining whether fees can mitigate arbitrage losses, allowing replication without additional capital, would be a very useful result. We conjecture that such a result would generalize the framework of [EAC21] from constant-mean marker makers to arbitrary CFMMs. As previously discussed, another possibility is, when the replication of a given payoff is impossible, how closely one can approximate the payoff with a CFMM. Another area for research involves extending the results to include convex payoffs as well as positions that require leverage to replicate. Convex instruments may require the ability to establish short positions in CFMMs shares. Similarly, levered instruments require one to facilitate lending secured by the value of CFMM shares. A model for secure lending and borrowing of CFMM shares would therefore expand the range of payoffs one can replicate with a CFMM.

References

- [AC20] Guillermo Angeris and Tarun Chitra. Improved price oracles: Constant function market makers. In Proceedings of the 2nd ACM Conference on Advances in Financial Technologies, AFT ’20, page 80–91, New York, NY, USA, 2020. Association for Computing Machinery.

- [AEC20] Guillermo Angeris, Alex Evans, and Tarun Chitra. When does the tail wag the dog? curvature and market making. arXiv preprint arXiv:2012.08040, 2020.

- [AKC+19] Guillermo Angeris, Hsien-Tang Kao, Rei Chiang, Charlie Noyes, and Tarun Chitra. An analysis of Uniswap markets. Cryptoeconomic Systems, 2019.

- [BV04] Stephen P. Boyd and Lieven Vandenberghe. Convex Optimization. Cambridge University Press, Cambridge, UK ; New York, 2004.

- [CJ90] Peter P. Carr and Robert A. Jarrow. The stop-loss start-gain paradox and option valuation: A new decomposition into intrinsic and time value. The Review of Financial Studies, 3(3):469–492, 1990.

- [Cla20] Joseph Clark. The replicating portfolio of a constant product market. Available at SSRN 3550601, 2020.

- [DGK+19] Philip Daian, Steven Goldfeder, Tyler Kell, Yunqi Li, Xueyuan Zhao, Iddo Bentov, Lorenz Breidenbach, and Ari Juels. Flash Boys 2.0: Frontrunning, transaction reordering, and consensus instability in decentralized exchanges. arXiv:1904.05234 [cs], April 2019.

- [EAC21] Alex Evans, Guillermo Angeris, and Tarun Chitra. Optimal fees for geometric mean market makers. https://web.stanford.edu/ guillean/papers/g3m-optimal-fee.pdf, 2021.

- [Eva20] Alex Evans. Liquidity provider returns in geometric mean markets. arXiv preprint arXiv:2006.08806, 2020.

- [FMT07] Thierry Foucault, Sophie Moinas, and Erik Theissen. Does anonymity matter in electronic limit order markets? The Review of Financial Studies, 20(5):1707–1747, 2007.

- [Gre16] Greg N. Gregoriou. The Handbook of Trading: Strategies for Navigating and Profiting from Currency, Bond, and Stock Markets. The McGraw-Hill Companies, 2016.

- [KCCM20] Hsien-Tang Kao, Tarun Chitra, Rei Chiang, and John Morrow. An analysis of the market risk to participants in the compound protocol. In Third International Symposium on Foundations and Applications of Blockchains, 2020.

- [MM19] Fernando Martinelli and Nikolai Mushegian. Balancer: A non-custodial portfolio manager, liquidity provider, and price sensor. 2019.

- [MY14] Ciamac Moallemi and K Yuan. The value of queue position in a limit order book. Market Microstructure: Confronting Many Viewpoints, 2014.

- [Neu94] Anthony Neuberger. The log contract. The Journal of Portfolio Management, 20(2):74–80, 1994.

- [Roc70] R. Tyrrell Rockafellar. Convex Analysis, volume 28. Princeton university press, 1970.

- [Shr04] S. E. Shreve. Stochastic Calculus for Finance II: Continuous-Time Models. Springer, 2004.

- [ZCP18] Yi Zhang, Xiaohong Chen, and Daejun Park. Formal specification of constant product (xy=k) market maker model and implementation. 2018.

Appendix A Delta hedging

As in section 3, we have that , , and are all scalar quantities, where is the price of the asset in question. We seek to construct a trading function such that for all . We define,

which is the marginal price of the traded coin. Recalling that can be thought of as an implicit function of , we have

Therefore,

will give a family of trading functions with the desired property.

Hedging a covered call.

Extending the example in section 3, we now look at delta hedging a covered call. In this case, we hold units of the risky asset, i.e. . We therefore have,

where is defined as before where is defined as . In this case, we have the trading function

where k is an arbitrary constant. As before, will control where the hedge will fail as the CFMM runs out of reserves. An appropriate choice wil be to select such that the intial value of reserves match the initial price of the covered call. In this case, we have

Substituting the values for and and solving for , one obtains . Substituting this value recovers the trading function we derived in 3.

Hedging a log contract.

We consider the case of delta-hedging a short position in a log contract. As noted in [Neu94], delta-hedging a contract paying the natural logarithm of the futures price will replicate a variance swap. In this case, we seek a trading function for which . In other words, to achieve the desired hedge, we seek a CFMM that holds one unit of asset 2 worth of asset 1. Noting that,

we get

where is an arbitrary constant. Any trading function of the form

| (9) |

will achieve the desired hedge insofar as or , as the CFMM will otherwise run out of the reserves required to continue hedging.

Path dependence and arbitrage loss.

Suppose the price of the asset at time is and consider delta-hedging a short position in the log contract by holding units of the asset under zero transaction costs. The PNL of this strategy over a discrete period is . When continuously rebalancing over , we have PNL . For simplicity of illustration, suppose follows a geometric Brownian motion with stochastic differential

where is a standard Brownian motion. One can check that the expected PNL of the delta-hedging strategy is zero. Now, we contrast this with delta-hedging with the CFMM we recovered in (9). One can check that this CFMM has payoff

The expected PNL of this strategy is therefore,

In other words, implementing the delta-hedge through a no-fee CFMM instead of continual rebalancing under no transaction costs will result in a supermartingale. This observation is analogous to the result in [AC20, Eva20] that the portfolio value of a G3M or constant-mean market maker is a supermartingale under the risk-neutral measure due to arbitrage losses.

More generally, a no-fee CFMM has payoff , which is always path-independent. In contrast, the equivalent delta-hedging strategies continually-rebalanced at no cost are path-dependent. When delta-hedging a convex strategy, one’s portfolio will be short gamma and long theta [Shr04]. The equivalent CFMM does not benefit from positive theta due to arbitrage, resulting in the supermartingale behavior. In other words, delta hedging a convex claim with a CFMM with the appropriate concave payoff will underperform the equivalent delta hedge rebalanced under no transaction costs. We conjecture that a result similar to that of [EAC21] may allow one to arbitrarily approximate unconstrained delta-hedging strategies with CFMMs by taking the directional limit as the fee approaches zero, but do not pursue this direction further in this paper.