Gumbel convergence of the maximum of convoluted half-normally distributed random variables

Abstract

In this note, we establish the convergence in distribution of the maxima of i.i.d. random variables to the Gumbel distribution with the associated normalizing sequences for several examples that are related to the normal distribution. Motivated by tests for jumps in high-frequency data, our main interest is in the half-normal distribution and the sum or difference of two independent half-normally distributed random variables. Since the half-normal distribution is neither stable nor symmetric, these examples are non-obvious generalizations. It is shown that the sum and difference of two independent half-normally distributed random variables and other examples yield distributions with tail behaviours that relate to the normal case. It turns out that the Gumbel convergence for all such distributions can be proved following similar steps. We illustrate the results in Monte Carlo simulations.

keywords:

Convolution tails , extreme value theory, Gumbel convergence , half-normal distributionMSC:

[2010] 60G701 Introduction

From extreme value theory it is known that non-degenerate limit distributions of normalized maxima of i.i.d. real-valued, absolutely continuously distributed random variables are always extreme value distributions of Weibull, Fréchet or Gumbel type, see Gnedenko (1943). If denotes the cumulative distribution function (cdf) of such i.i.d. random variables, we write , that is, is in the maximum domain of attraction of the generalized extreme value distribution which is specified by the extreme value index . If the right-end point of is , the limit is a Fréchet distribution, , if has Pareto tails and Gumbel, , if has exponential tails. This note considers cdfs with exponential tails, such that , where we use the standard notation for the Gumbel distribution . We write , if the random variable has cdf , and , if is normally distributed with mean , and variance . , and , means that all random variables of a sequence are independent and identically distributed. We write

| (1) |

for the convergence in distribution to the Gumbel limit distribution, i.e. when it holds for all that

| (2) |

For , has a half-normal distribution. The density of the half-normal distribution

| (3) |

is easily obtained from the density of the normal distribution exploiting its symmetry. The distribution of is the convolution of the distributions of and . The convolution of two normally distributed random variables and is again normally distributed. Since the half-normal distribution does not satisfy such a stability, the extreme value convergences for and are not obvious and established in this note together with some related examples. For all examples, we establish a sufficient condition that the distributions are in the maximum domain of attraction of the Gumbel distribution although this is clear by the exponential tail behaviour. The main open problem solved here is rather to determine the normalizing sequences and in (1) for the different examples. The analysis provided in this note leads me to the conjecture, that for all distributions with a certain tail behaviour of Gaussian type, that is, the right tails are asymptotically proportional to , with some rational function , the Gumbel convergence can be proved by a modification of the proof given here following the same steps. Moreover, the distributions of sums and differences remain within this class.

The question about the precise result of the Gumbel convergence (1), when are (absolute) differences of two independent half-normally distributed random variables, arose when working on a test for jumps in high-frequency financial order-book data which are modelled by a sum of a semi-martingale efficient price process and one-sided microstructure noise. This model has been proposed by Bibinger et al. (2016). There, the half-normal distribution occurs as the distribution of the maximum of Brownian motion over some fix interval which by the reflection principle for Brownian motion equals the distribution of the absolute value of the end-point. Comparing values on neighboured intervals to test for jumps leads to the (absolute) difference of two independent half-normally distributed random variables. A global test for jumps is then based on the maximal (absolute) difference for which we need the result provided in Proposition 2.1 of this note.

There are more standard methods in econometrics based on the considered examples of Gumbel convergence. The Gumbel test for price jumps in high-frequency financial data by Lee and Mykland (2008) is very popular. The asymptotic distribution under the null hypothesis of no price jump, when the price is modelled by discrete recordings of a continuous semi-martingale, is by Lemma 1 of Lee and Mykland (2008) the Gumbel distribution. However, there is a small but relevant typo in the result, since the test statistic uses absolute returns combined with the normalizing sequences for the normal instead of the half-normal distribution. We shall see in the Monte Carlo simulations in Section 4 that, although the results in (4a)-(4f) look very similar at a quick glance, the differences of the normalizing sequences are important.

2 Results and discussion

Proposition 2.1.

Let be a -dimensional vector of i.i.d. standard normally distributed random variables.

-

-

1.

If , (1) holds with the sequences

(4a) -

2.

If , (1) holds with the sequences

(4b) -

3.

If , and as well for , (1) holds with the sequences

(4c) -

4.

If , (1) holds with the sequences

(4d) -

5.

If , (1) holds with the sequences

(4e) -

6.

If , (1) holds with the sequences

(4f) Remark 2.2.

While the normal distribution in (4a) is a well-known example for a distribution in the maximum domain of attraction of the Gumbel distribution, the half-normal case (4b) and the (absolute) difference and the sum of independent half-normally distributed random variables, (4d)-(4f), have so far not been focussed on in the literature. The half-normal case (4b) might appear intuitive by the symmetry of the normal distribution. The convergence of the maximum of i.i.d. random variables which are defined as sums is usually not readily obtained from known extreme value convergences of the summands. For the normal distribution, however, (4c) is obvious by (4a) with the convolution property that . Let me point out that and instead are not half-normally distributed, that is, the half-normal distribution is not a stable distribution. Nevertheless, the convergences (4d)-(4f) can be proved using similar ingredients as for (4a) and an asymptotic expansion of the convolution integrals. Naturally, in contrast to (4c), which applies to the sum and difference, (4d) and (4e) are different, since the half-normal distribution is not symmetric.

3 Proof of the results

We begin with a lemma which is used to exploit the symmetry of a distribution in a simple way.

Lemma 1.

Suppose that , with

| (5) |

with the (cdf of the) generalized extreme value distribution , and let be symmetric such that and are identically distributed, . For , it follows that , with

| (6) |

Proof.

For asymptotic equivalence of two positive functions and , we write , which means that

The second lemma provides a neat asymptotic relation between tail functions and densities of normal and half-normal distributions.

Lemma 2.

For some constant , it holds true that

Proof.

The chain or product rule of differentiation yield that

L’Hospital’s rule hence yields that

what proves the claim. ∎

We first prove (4a). There are different proofs for this result available in the literature, see, for instance, Example 1.1.7 in de Haan and Ferreira (2006). We follow the proof from Section 5.4 of Kabluchko (2015), which can be generalized with Lemmas 1 and 2 below to prove (4b)-(4f). Denote by

the density and the cdf of the standard normal distribution, respectively. Lemma 2 yields that . By Theorem 1.2.1, Equation (1.2.4), in de Haan and Ferreira (2006), (1) is satisfied if and only if there exists a function , such that for all , the cdf of the random variables satisfies

| (7) |

is the right end-point of the distribution which is in our cases. We verify this condition for with :

We conclude that . We determine the sequences and in (4a). We can start with

| (8) |

or directly use , with the general notation for the left-continuous generalized inverse of , which is known from extreme value theory, see Remark 1.1.9 in de Haan and Ferreira (2006). This yields that

| (9) |

We set , with a null sequence . Inserting this gives

and we find that the identity holds true for

The sequence can be obtained in general by , see Remark 1.1.9 in de Haan and Ferreira (2006). Here, we derive that

what can be deduced directly from (8).

Next, (4b) is readily implied by (4a) and Lemma 1.

Since

is for any constant equivalent to

with , the convolution property of the normal distribution, that , gives (4c). By symmetry , such that the sum and the difference have the same distribution.

If denotes the density of the half-normal distribution from (3), we write

for the convolution square determined by the equation

The integral has an explicit solution which we express using the erf and erfc functions associated with by the identities

We obtain that

This expansion is included in the more general illustration of the tails of the convolution of two densities with Gaussian tail behaviour given in Balkema et al. (1993) with a different proof. For the tail function , Lemma 2 yields that

Hence, (7) is satisfied with , since

We conclude that the convoluted half-normal distribution is in the maximum domain of attraction of the Gumbel distribution. We determine the normalizing sequences, and , similarly as in the normal case, but establish some crucial differences. We know that

and set , with a null sequence . Inserting this yields that

and we obtain that

Computing , starting with , gives for the sequence that

We have proved (4d).

Denote with the density of on the positive real axis. With similar steps as for the convolution, we compute

We then use that

obtained from Lemma 2, to deduce that

Different to all previous densities, we have the additional factor in the tail behaviour and not only an exponential decay. Using that

l’Hospital’s rule yields that

We conclude that the associated tail function satisfies

Again, (7) is satisfied with , since

Setting , with a null sequence , we determine the normalizing sequences and , based on

We conclude that

4 Monte Carlo simulations

We perform Monte Carlo simulations where for each example we generate realizations of standard normally distributed random variables . We then take in Monte Carlo repetitions the maxima of

| (10a) | ||||

| (10b) | ||||

| (10c) | ||||

| (10d) | ||||

| (10e) | ||||

| (10f) | ||||

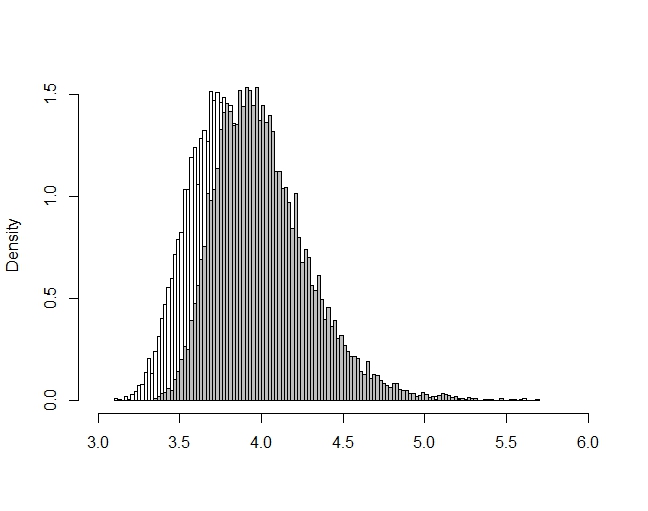

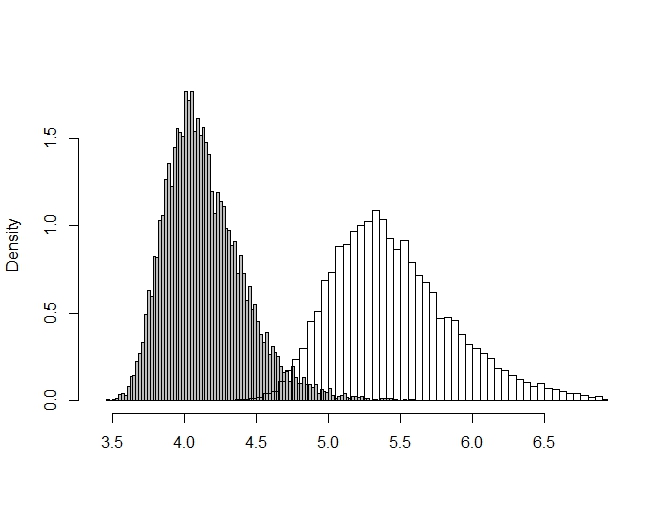

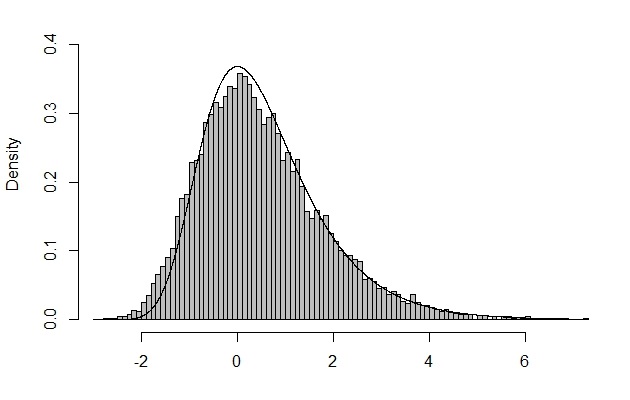

In Figure 1 the left plot compares histograms for the values of and . The two empirical distributions are not that far from each other. This might be one reason why the normalizing sequences in (4a) and (4b) are sometimes confused without notice. However, for the precision of an asymptotic test, the different normalizing sequences are nevertheless crucial. In fact, is distributed as , when we have instead of i.i.d. observations, and not as . The right plot of Figure 2 compares the empirical distributions of the values of and . These two empirical distributions are quite different in their location and scale.

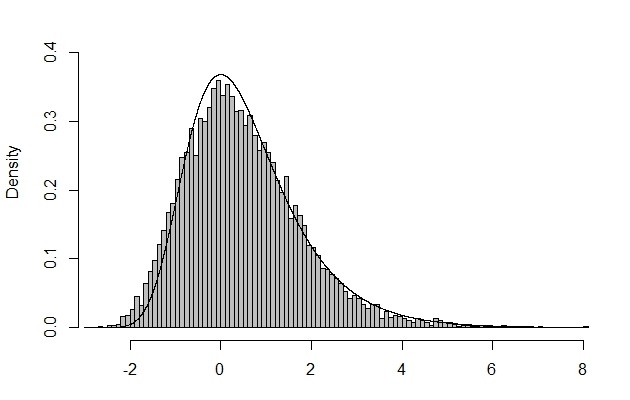

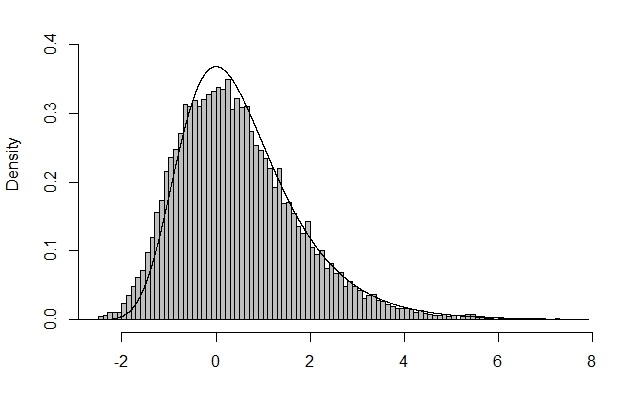

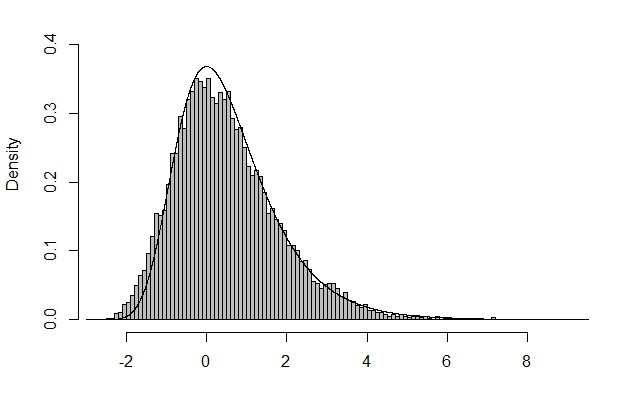

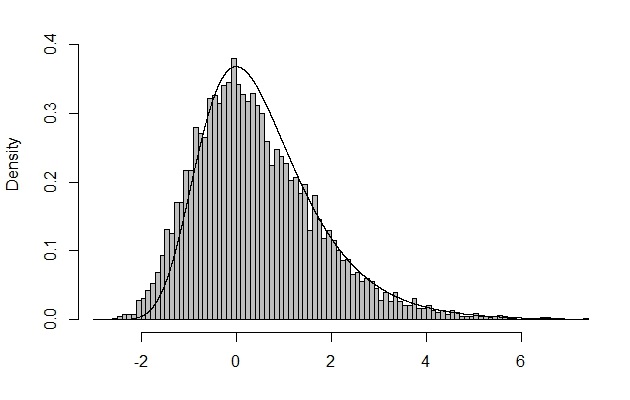

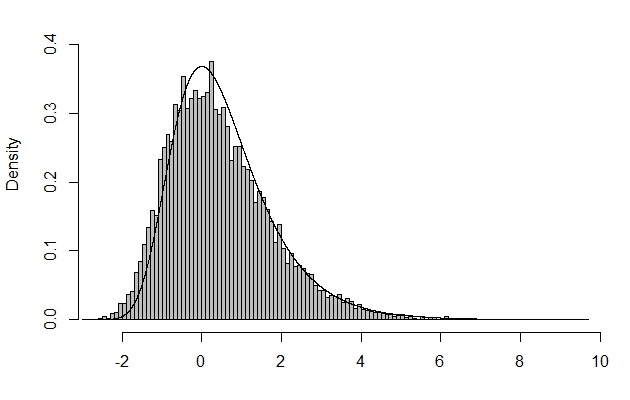

Figure 2 illustrates the finite-sample precision of the asymptotic standard Gumbel limit distribution for the empirical distribution of properly normalized maxima in our six examples. The histograms are for the statistics left-hand side in Eq. (4a)-(4f) and the black line shows the density of the standard Gumbel limit distribution to draw a comparison. For all examples, the Gumbel limit distribution closely tracks the empirical distributions. In particular, the fit for convoluted half-normally distributed random variables appears to be as good as in the standard normal case. With their different normalizing sequences, the normalized maxima have the same standard Gumbel limit distribution, including normalized versions of and , whose empirical distributions are quite different as shown in the right plot of Figure 1.

References

- Balkema et al. (1993) Balkema, A. A., C. Klüppelberg, and S. I. Resnick (1993). Densities with Gaussian tails. Proceedings of the London Mathematical Society s3-66(3), 568–588.

- Bibinger et al. (2016) Bibinger, M., M. Jirak, and M. Reiß (2016, 10). Volatility estimation under one-sided errors with applications to limit order books. Ann. Appl. Probab. 26(5), 2754–2790.

- de Haan and Ferreira (2006) de Haan, L. and A. Ferreira (2006). Extreme value theory. An introduction. New York, NY: Springer.

- Gnedenko (1943) Gnedenko, B. W. (1943). Sur la distribution limite du terme maximum d’une serie aleatoire. Annals of Mathematics 44(3), 423–453.

- Kabluchko (2015) Kabluchko, Z. (2015). Extremwerttheorie. Vorlesungsskript, Universität Münster.

- Lee and Mykland (2008) Lee, S. and P. A. Mykland (2008). Jumps in financial markets: A new nonparametric test and jump dynamics. Review of Financial Studies 21, 2535–2563.