Value Function Estimators for Feynman-Kac Forward-Backward SDEs in Stochastic Optimal Control

Abstract

Two novel numerical estimators are proposed for solving forward-backward stochastic differential equations (FBSDEs) appearing in the Feynman-Kac representation of the value function in stochastic optimal control problems. In contrast to the current numerical approaches which are based on the discretization of the continuous-time FBSDE, we propose a converse approach, namely, we obtain a discrete-time approximation of the on-policy value function, and then we derive a discrete-time estimator that resembles the continuous-time counterpart. The proposed approach allows for the construction of higher accuracy estimators along with error analysis. The approach is applied to the policy improvement step in reinforcement learning. Numerical results and error analysis are demonstrated using (i) a scalar nonlinear stochastic optimal control problem and (ii) a four-dimensional linear quadratic regulator (LQR) problem. The proposed estimators show significant improvement in terms of accuracy in both cases over Euler-Maruyama-based estimators used in competing approaches. In the case of LQR problems, we demonstrate that our estimators result in near machine-precision level accuracy, in contrast to previously proposed methods that can potentially diverge on the same problems.

1 Introduction

Feynman-Kac representation theory and its associated forward-backward stochastic differential equations (FBSDEs) has been gaining traction as a framework to solve nonlinear stochastic optimal control problems, including problems with quadratic cost [6], minimum-fuel (-running cost) problems [9], differential games [7, 8], and reachability problems [6, 23]. Although FBSDE-based methods have seen growing attention in both the controls and robotics communities recently, much of the research originated in the mathematical finance community [1, 16, 18]. While initial results demonstrate promise in terms of flexibility and theoretical validity, numerical algorithms which leverage this theory have not yet matured. For even modest problems, state-of-the-art algorithms can be unstable, producing value function approximations which quickly diverge. Thus, producing more robust numerical methods is critical for the broader adoption of FBSDE methods for real-world tasks.

Numerical solution methods for Feynman-Kac-type FBSDEs broadly consist of two steps, a forward pass, which generates Monte Carlo samples of the forward stochastic process, and a backward pass, which iteratively approximates the value function backwards in time. Typically, FBSDE methods perform this approximation using a least-squares Monte Carlo (LSMC) scheme, which implicitly solves the backward SDE using parametric function approximation [16]. The approximate value function fit in the backward pass is then used to improve sampling in an updated forward pass, leading to an iterative algorithm which, ideally, improves the approximation till convergence. Although FBSDE methods seem similar to differential dynamic programming (DDP) techniques [13, 26, 25], the approach is significantly different. DDP methods require first and second order derivatives of the dynamics, and directly compute a quadratic approximation of the value function using constraints on the derivatives of the value function. Comparatively, FBSDE LSMC only uses estimates of the value function at a distribution of states, using the derivative of the value function to improve the accuracy of the estimator. FBSDE methods are more flexible in that they do not require derivatives of the dynamics and can be used with models of the value function which are not necessarily quadratic. Furthermore, for most DDP applications, a quadratic running cost with respect to the control is required for appropriate regularization [24, Section 2.2.3], whereas the FBSDE method more easily accommodates non-quadratic running costs (e.g., of the class or zero-valued), lending to a variety of control applications [9].

The underlying foundation of Feynman-Kac-based FBSDE algorithms is the intrinsic relationship between the solution of a broad class of second-order parabolic or elliptic PDEs to the solution of FBSDEs (see, e.g., [28, Chapter 7]), brought to prominence in [19, 21, 5]. Both Hamilton-Jacobi-Bellman (HJB) and Hamilton-Jacobi-Isaacs (HJI) second order PDEs, utilized for solving, respectively, stochastic optimal control and stochastic differential game problems, can thus be solved via FBSDE methods, even when the dynamics and costs are nonlinear and non-quadratic, respectively. This provides an alternative to the grid-based direct solution of PDEs, typically solved using finite-difference, finite-element, or level-set schemes, known for poor scaling in high dimensional state spaces ().

In this work, we investigate the discrete-time approximation of the backward SDE in the context of solving for the value function in the backward pass in FBSDE methods. Although for some special cases analytic solutions of the backward SDEs over short intervals can be accommodated into the associated algorithms [16], for many nonlinear problems analytic solutions are not available and numerical integration based on time-discretization is a necessity. In the currently available algorithms in the literature Euler-Maruyama approximations are employed for discretizing the continuous-time FBSDEs [6], to solve for an approximation of the continuous-time value function. In this paper, instead of the direct application of the Euler-Maruyama approximation on the Feynman-Kac FBSDEs, we formulate a discrete time problem with the Euler-Maruyama approximation of the dynamics, costs, and value function, and then we derive discrete-time relationships using Taylor expansions which resemble their continuous-time counterparts. By doing so, we arrive at a set of alternative estimators for the value function.

The primary contributions of this paper are as follows:

-

•

Proposing a pair of alternative estimators for the value function used in the backward pass of a Girsanov-drifted Feynman-Kac FBSDE numerical method.

-

•

Characterizing the theoretical bias and variance of these estimators and show their theoretic superiority to previously proposed estimators.

-

•

Numerically confirming the theoretical results on representative stochastic optimal control problems.

This paper expands upon the authors’ prior work in [11], first by providing more details into how the proposed estimators are constructed. Second, we provide detailed proofs for the stated theorems, especially the discrete-time version of Girsanov’s theorem, which allows for the interpretation of the error. In addition, we discuss how the methodology can be adapted to produce an approximate policy improvement. Finally, in addition to a more detailed presentation of the scalar nonlinear example in [11], we present results of experiments on a four-dimensional LQR problem, verifying our theoretical claims about the accuracy of the proposed estimators.

The structure of the paper is as follows. In Section 2 we introduce the stochastic optimal control problem we are interested in, as well as the continuous-time approach to solving for an on-policy value function using drifted FBSDEs. At the end of this section we describe a discrete-time method of approximating the backward SDE which we will improve upon. In Section 3 we introduce our proposed approach, beginning by replacing the continuous-time problem with a discrete-time approximation. We then use discrete-time relationships to arrive at estimators which resemble the estimators derived from continuous-time theory. We also provide an error analysis for the proposed estimators. Next, in Section 4, we briefly show how a similar approach to derive the estimators can be used to approximate the Q-value function for policy improvement methods in reinforcement learning problems. Finally, in Section 5 we present results from two numerical experiments which confirm the error analysis and illustrate the benefits of our approach over previously proposed estimators.

2 Continuous-Time Feynman-Kac FBSDEs

In this section we introduce the stochastic optimal control problem we are interested in, and show how its solution can be obtained as a pair of forward-backward stochastic differential equations (FBSDEs). Further, we discuss how these continous-time FBSDEs can be approximated using the Euler-Maruyama method.

2.1 Stochastic Optimal and On-Policy Value Functions

We start with a complete, filtered probability space , on which is an -dimensional standard Brownian (Wiener) process with respect to the probability measure and adapted to the filtration . Consider a stochastic nonlinear system governed by the Itô differential equation

| (1) |

where is a state process taking values in , is a measurable and adapted input process taking values in the compact set , and , are the Markovian drift and diffusion functions, respectively. The cost associated with a given control signal is

| (2) |

where is the running cost, and is the terminal cost. We assume that are uniformly continuous and Lipschitz in for all , and that exists and is uniformly bounded on its domain.

The stochastic optimal control (SOC) problem is to determine the optimal value function

| (SOC) |

(see [28, Section 4.3]). Given the previous assumptions on the dynamics and costs, is a unique viscosity solution, continuous on , of the associated Hamilton-Jacobi-Bellman PDE [28, Chapter 4 Theorem 5.2; Theorem 6.1].

The iterative approach to solving the optimal control problem is to successively improve approximations of the optimal policy and optimal value function , refining an arbitrary policy and its associated on-policy value function , which characterizes the cost-to-go under this policy. Consider the space of admissible feedback policies, that is, measurable functions for which there exists a weak SDE solution for

| (3) |

where , , and henceforth abbreviate , and similarly. The on-policy value function is defined as

| (4) |

with the process satisfying the forward SDE (FSDE) (3), and its associated Hamilton-Jacobi PDE is

| (5) |

for , where and are the partial derivative operators with respect to and , and is the Hessian with respect to . Under the typical assumptions of [28, Chapter 5, Theorem 6.6], a feedback policy satisfying the inclusion

| (6) |

when is differentiable,111When is not differentiable a similar result can be obtained using the superdifferentials of the viscosity solution. is optimal, that is, . More generally, when are uniformly continuous and Lipschitz in for all (which we henceforth assume), the on-policy PDE (5) admits a unique viscosity solution [28, Chapter 7, Theorem 4.1]. 222We assume without proof that the space of policies for which this condition is satisfied either contains or a close approximation of it.

2.2 On-Policy FBSDE

The positivity of yields that (5) is a parabolic PDE and, hence, by the Feynman-Kac Theorem (see, e.g. [20]) its solution is linked to the solution of the pair of FBSDEs composed of the FSDE (3) and the backward SDE (BSDE)

| (7) |

where and are, respectively, one and -dimensional adapted processes.

Theorem 2.1 (Feynman-Kac Representation).

Proof.

See [28, Chapter 7, Theorem 4.5, (4.29)].

In numerical methods this theorem is often applied over short time intervals, leading to the following result.

Corollary 2.1.

Proof.

The fact that , -a.s., follows directly from the definition of an SDE solution. Since (and consequently ) is -measurable due to (8), it follows that . The equality follows immediately from the standard property of Itô integrals (and the tower property of conditional expectation) that yields [28, Chapter 7, Theorem 3.2].

2.3 Least Squares Monte Carlo

Least squares Monte Carlo (LSMC) is a scheme for obtaining the parameters of a parametric model of the value function , originally credited to [16].

Corollary 2.2.

The minimizer of

| (13) |

over -measurable square integrable variables coincides with the value function, that is, .

Proof.

In LSMC numerical methods, we approximate the minimization in (13) over the subspace of -measurable variables , where is a function representation with parameters (we assume henceforth that for all ). Let be a set of samples approximating the joint distribution , denoted as . The optimal parameters for this representation are found by minimizing

| (14) |

When the function representation is linear in the parameters this optimization is a linear least squares regression problem in . The optimal parameters define the new approximate representation of the value function, by

| (15) |

2.4 Off-Policy Drifted FBSDE

We now present a result based on Girsanov’s theorem, namely, that an alternative pair of drifted FBSDEs with a different trajectory distribution can be used to estimate the same value function . This result will be used to disentangle the drift of the forward distribution from the policy associated with the value function.

Theorem 2.2.

Let be a new filtered probability space on which is Brownian and let be any -progressively measurable process on the interval such that

| (16) |

is bounded and

| (17) |

admits a unique square-integrable solution (see e.g. [28, Chapter 1, Theorem 6.16]). Then, the Hamilton-Jacobi PDE (5) has a representation as the unique square-integrable solution to the FBSDEs (17) and

| (18) |

in the sense that

| (19) |

-a.s..

Proof.

The existence of a square-integrable solution to (17) allows the conditions of [28, Chapter 7, Theorem 3.2] to be satisfied for (18), guaranteeing a unique square-integrable solution . Now define the processes

| (20) | ||||

| (21) |

for . Since is bounded, Girsanov’s theorem [10, Chapter 5, Theorem 10.1] implies that the process defined by (20) is Brownian in some measure derived from in the form of

| (22) |

where be the Radon-Nikodym derivative. With a simple algebraic reduction, Girsanov’s theorem also guarantees separately that solves the on-policy FSDE (3), and that solves the on-policy BSDE (7). Here, the idea is that the sample functions for the processes are the same, but the probability measure (acting on sets of trajectory samples ) which characterizes their distributions changes.

Since is bounded, it satisfies Novikov’s criterion [3, Theorem 15.4.2] and thus, it follows that is -a.s. strictly positive, and further that the measures and are equivalent, that is, they are absolutely continuous with respect to the other [17]. Since (8) holds -a.s., there exists an such that , where , and . It subsequently follows from the definition of absolute continuity that . Thus, (8) holds -a.s. as well.

As before, the corresponding relationship over short intervals follows.

Corollary 2.3.

Proof.

The proof follows similarly to the proof of Corollary 2.1.

Further, the discussion in Section 2.3 holds true when the measure is replaced with . We can interpret this result in the following sense. As long as the diffusion function is the same as in the on-policy formulation, we can pick an arbitrary process to be the drift term, which generates a distribution for the forward process in the corresponding measure . The BSDE yields an expression for using the same process as used in the FSDE. The term acts as a correction in the BSDE to compensate for changing the drift of the FSDE. We can again use the minimization (14) to approximate the value function , the only difference being that are now samples approximating the distribution .

It should be highlighted that need not be a deterministic function of the random variable , as is the case with . For instance, it can be selected as the function for some appropriate function , producing a non-trivial joint distribution for the random variables .

2.5 Euler-Maruyama FBSDE Approximation

Many approaches to solving the FBSDEs propose approximating both the forward and backward steps with Euler-Maruyama-like SDE approximations, see, for instance, [2], [6], and the survey in [12]. For the drifted FSDE the approximation is

| (27) |

where and . For the drifted BSDE step we have

| (28) |

where is either

| (29) | ||||

| or | ||||

| (30) | ||||

The variable is evaluated at the end of the interval so that it can utilize the latest approximation of the value function gradient. Note also that the on-policy Euler-Maruyama estimators arise when and thus . The primary contribution of this paper, discussed in the next section, is to propose new estimators for to be used in the LSMC function regression step.

3 Forward-Backward Difference Equations

In the previous section we presented results from continuous-time FBSDE theory, then used standard methods in SDE approximation to form a discrete-time approximation of the forward and backward SDEs. In this section we propose the converse approach: we begin by forming a discrete-time approximation of the dynamics and the value function, then we derive relationships which resemble those arrived at previously. In doing so, we make two contributions: first, we arrive at better estimators compared to the direct discretization of the continuous time relations because we are able to exploit characteristics of the discrete-time formulation obscured by the continuous-time problem, and, secondly, we provide a discrete-time intuition for the continuous-time theory.

3.1 Discrete Time SOC Approximation

The interval is partitioned into subintervals of length with the partition . We abbreviate variables for brevity. Let be the discrete-time filtered probability space and let be a discrete time Brownian process in , that is, is normally distributed, -measurable, and are mutually independent. The on-policy forward stochastic difference equation is

| (31) |

where, using the Euler-Maruyama approximation method,333Or some other approximation scheme that results in the form (31), (33).

| (32) |

and the on-policy value function is

| (33) |

where

| (34) |

According to [14, Chapter 10, Theorem 10.2.2], when a linear growth condition in is imposed on , , and along with a few other conditions, then it can be shown that the absolute error between the Euler-Maruyama approximation and the continuous forward process is of order . When is constant with respect to , the error bound improves to [14, Chapter 10, Theorem 10.3.5].

3.2 Discrete-Time BSDE Approximation

For the discrete-time value function and forward process we define the process . Further, we define the term as one that satisfies the backward difference,

| (35) |

where we use separate estimators and to obtain a combined estimator

| (36) |

with the interpretation . Both and can be chosen according to different approximation schemes; these choices are investigated below. These approximation schemes assume the availability of some approximate representation of the value function at the next step , as well as its derivatives, and they produce a representation using LSMC.

3.3 On-Policy Taylor-Expanded Backward Difference

We now propose an estimator for , the discrete analogue to the on-policy terms defined in (10) and (11). We begin by noting that the on-policy value function satisfies the on-policy Bellman equation

| (37) |

Consider the second-order Taylor expansion of the approximation of the term inside the conditional expectation,

| (38) | ||||

| (39) |

centered at the conditional mean,

| (40) |

where

| (41) | ||||

| (42) | ||||

| (43) |

and includes the third and higher order terms in the Taylor series expansion. Substituting in for in (37) and rearranging terms, and in light of (36), we arrive at an estimator for the backward step

| (44) |

For the purposes of comparison we restate the on-policy Euler-Maruyama estimators derived in the previous section,

| (45) | ||||

| (46) |

where

| (47) |

There are two differences in the proposed Taylor series expansion approach compared to the Euler-Maruyama approach. First, the gradient of the value function is evaluated at instead of . This effect can be exploited because in the discrete-time approach the difference equation separates the drift step and the diffusion step, whereas in the continuous-time approach the drift and diffusion are considered inseparable. However, if the continuous-time SDEs are eventually discretized using Euler-Maruyama, this assumption is broken over short intervals. Secondly, the trace term now appears in the Taylor-expansion estimator. While in the continuous-time counterpart second-order effects are infinitesimally small, they can no longer be ignored in the discrete-time approximation. Note, however, that since and is -measurable.

The following theorem suggests that this choice of approximation of has relatively small residual error.

Theorem 3.1.

The choice in (44) is an unbiased estimator of the actual value function difference , i.e.,

| (48) |

Further, the residual error is

| (49) | ||||

| (50) |

where is the error in the step value function representation.

Proof.

In general, the Taylor expansion residual has a small mean due to the following result.

Proposition 3.1.

Of the higher order terms in the Taylor expansion residual , the terms with odd order, starting with the third order term, have zero conditional expectations given .

Proof.

See Appendix A.

Further, under a very basic function approximation scheme, we can entirely dismiss the term .

Proposition 3.2.

If the value function approximation is quadratic then . Thus, the residual error is determined entirely by the residual error of the function approximation of ,

| (53) |

Proof.

This is a direct consequence of the fact that if is quadratic then its second order Taylor expansion is exact.

Note that this does not require the true value function to be quadratic, only its approximation. Although using a less expressive representation improves the error coming from the term , there may be a trade-off in terms of increasing the magnitude of the error in , since the function might be less appropriately modeled.

The most remarkable aspect of Proposition 3.2 is that it suggests that for linear-quadratic-regulator (LQR) problems these estimators are exact up to function approximation error, due to the fact that for LQR problems itself is in the class of quadratic functions. This provides a fundamental guarantee for these estimators. On the contrary, the Euler-Maruyama estimators are not exact when applied to LQR problems.

Remark 3.1.

If the value function approximation is quadratic, the residual error of the Euler-Maruyama estimators is

| (54) |

Though all three estimators are unbiased, the Taylor-expansion estimator is theoretically far superior on the baseline LQR problem. In numerical experiments illustrated later we confirm this near-machine precision performance of the Taylor estimator and the divergence of the EM estimators on the same LQR problem.

3.4 Estimators of

We propose two potential estimators for . First, we propose using the value function approximation associated with the previous backward step to re-estimate the values,

| (55) |

Alternatively, we can also use the estimator

| (56) |

which ends up cancelling out the terms with in them, so that (36) reduces to

| (57) |

The following theorem establishes the error analysis of the two Taylor-expansion-based estimators.

Theorem 3.2.

Proof.

See Appendix C.

This theorem shows that the re-estimate condition has less bias than the noiseless condition, but it is a higher variance estimator. We also observe that when the bias and variance of these two estimators are identical. However, since it is not immediately clear which condition is superior when this is not true, we examine both methods and compare the results in Section 5.

3.5 Drifted Taylor-Expanded Backward Difference

We now offer a discrete-time approximation of the drifted off-policy FBSDEs. Let be an alternative discrete-time filtered probability space where is the associated Brownian process. Define on this space the difference equation

| (62) |

where the process is chosen at will, -measurable, and independent of . For example, can be constructed using the function , where is some random process where is -measurable and independent of (but not necessarily of ). Each must also be selected such that

| (63) |

is bounded.

Similar to the construction in Section 2.4, a discrete time version of Girsanov’s theorem can be used to produce the measure which satisfies the assumptions of Section 3.1 and show how the drifted forward difference (62) can be transformed to the on-policy forward difference (31). To this end, define the sequence of measures

| (64) |

for , where is the discrete time version of (21) defined as

| (65) |

where . Further, as in (20), define the process

| (66) |

for .

Lemma 3.1 (Discrete-Time Girsanov).

Let be a sequence of bounded and -measurable random variables where each is independent of . Then, the process defined by (66) is Brownian with respect to , that is, is normally distributed, -measurable, and the set of variables are mutually independent.

Proof.

See Appendix B.

Henceforth, we let for notational simplicity. It is easy to see that the drifted forward difference (62) and the on-policy forward difference (31) are identical under the substitution (66). Thus, we conclude that the drifted process still satisfies the on-policy Bellman equation (37) for the same on-policy value function .

To derive the backward step, we perform a Taylor expansion centered at

| (67) |

instead of . The expressions defining , , , and (38),(39),(41),(42),(43) are all identical except for replacing with . Again, substituting in for in (37) and rearranging terms in light of (36), we arrive at an estimator for the backward step

| (68) |

Recognize that this is a generalization of (44), by noting that when then and the drifted forward difference (62) and the backward step reduce to their on-policy form (31), (44).

Lemma 3.2.

Proof.

Substituting (66) into

| (70) |

yields

Note that , , , and , are -measurable. Taking the conditional expectation in the on-policy measure yields

| (71) |

Comparing (68), (70), and (71), it can be easily shown that

| (72) |

The Taylor expansion (38) immediately yields . Combining these two expressions yields

| (73) |

Substituting in the Bellman equation (37) and rearranging, we have

| (74) |

Under the measure , is independent of given , so we have

and by subsituting into the previous equation we arrive at (69).

The distribution of the residual error depends on the measure we use to interpret it. For numerical applications we sample from the measure instead of , and thus this estimator is no longer unbiased with respect to the sampled distribution. The conditional expectation with respect to of the right hand side of (69) is

| (75) |

The two estimators for , (55) (56), presented in Section 3.4, can be used without modification, given that in the noiseless condition, is taken to be (70). The drifted noiseless estimator now resolves to

| (76) |

Theorem 3.3.

Proof.

See Appendix C.

Since is not available during computation, we characterize exclusively in the measure using the next result.

Proposition 3.3.

Proof.

See Appendix D.

Although the error bound in Proposition 3.3 suggests that the bias grows rapidly with the magnitude , when this magnitude is small () the first term in the product on the right hand side of (81) is bounded by . To illustrate the effect of on the error bound, consider a one-dimensional problem where we select for some random variable with bounded magnitude a.s.. It subsequently follows that a.s.. This suggests that, in general, the magnitude of the difference should be proportional to the diffusion . Further, it is still the case that if the value function approximation is quadratic then the higher order terms drop out.

These analytical results justify the assumption that for appropriately chosen , the choice of (68) represents a low bias, low variance approximator for the backward difference step. It also provides guidance for how to select .

4 Policy Improvement

In this section we discuss how policies can be improved based on the value function parameters obtained from the backward passes. First, we discuss a naïve continuous-time approximation approach arising from the Hamiltonian used in HJB equations. Continuous-time analysis of the Hamiltonian suggests that the optimal control policy satisfies the inclusion (6), so a naïve approach to improving the policy would be to use the Euler-Maruyama approximation of the dynamics and costs along with the gradient of the recent approximation of the value function to evaluate this policy optimization. This Hamiltonian-based approach

| (82) |

According to the discussion in the previous section, we propose an alternative Taylor-based approach to (82) as follows. We begin with a discrete approximation of the continuous problem and form the Q-value function at time , given the value function ,

| (83) |

where is the measure corresponding to the forward difference step

| (84) |

The optimal Bellman equation indicates that the optimal policy satisfies and the optimal value function satisfies . Notice that when and then , so will be an improved policy over . Letting

| (85) |

and performing the same Taylor expansion approach as in (38), (39), we arrive at the approximation defined as

| (86) |

where

Proposition 4.1.

Proof.

In general, we seek a policy that minimizes this Q-value function,

| (88) |

When the function is quadratic in terms of and/or contains an regularization term like , is an interval set, is affine in the control, and is quadratic, then the optimization (88) has an analytic solution. Also, similarly to the previous section, when is quadratic, as is the case in LQR problems, the Taylor expansion of the Q-value function is exact. Thus, this optimization will yield the exact optimal control solution for the LQR problem.

5 Numerical Results

Next, we numerically evaluate and compare the proposed Taylor estimators to the naïve Euler-Maruyama estimators on two problems, a nonlinear 1-dimensional problem and an LQR 4-dimensional problem. The estimators discussed in this work are summarized in Table 1.

| Estimator | |

|---|---|

| Taylor | |

| Noiseless | |

| Taylor | |

| Re-estimate | |

| Euler-Maru. | |

| Noiseless [6] | |

| Euler-Maru. | |

| Noisy |

5.1 Nonlinear 1D Problem

Consider the scalar optimal control problem with the dynamics and cost

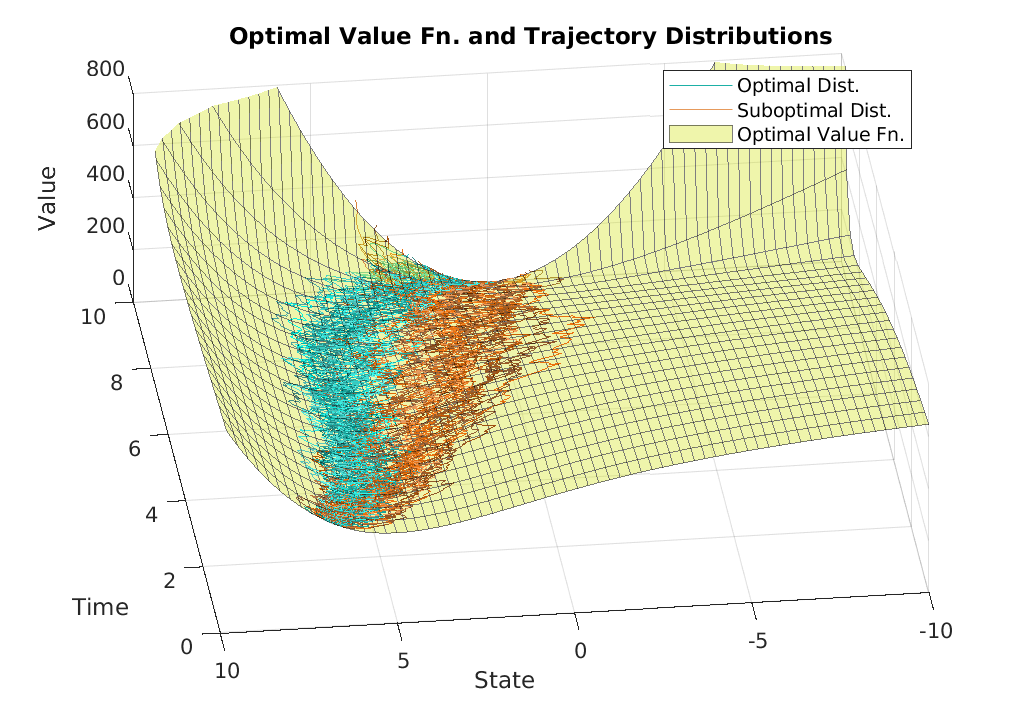

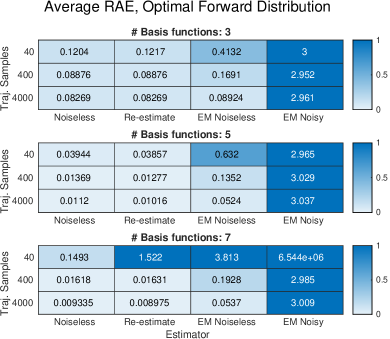

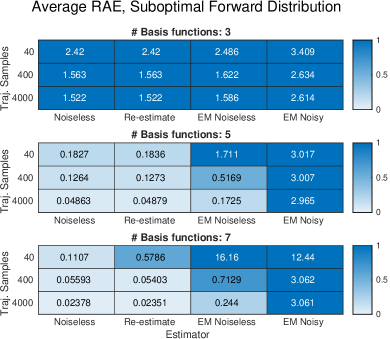

over a time interval of length , with discrete timesteps. We compute a ground-truth optimal value function by directly evaluating the optimal Bellman equation using a finely-gridded state space, control space, and noise space, and set the optimal policy as the target . The optimal value function is visualized in Fig. 1 (the yellow surface), along with two forward-backward trajectory distributions considered for evaluation: (a) the optimal (the cyan trajectories in Fig. 1), and (b) the suboptimal (the orange trajectories). We ran a series of simulations to investigate how each estimator performs under different algorithmic conditions, visualized in Fig. 2. Each trial performs one forward pass, and then uses Chebyshev polynomials to locally approximate the optimal value function in a single backward pass. For the purposes of evaluation we use the relative absolute error (RAE) metric [27, Chapter 5]

| (89) |

where

| (90) |

for , where are the mean and standard deviation of for the optimal forward trajectory distribution (the cyan trajectories in Fig. 1). For each element in Fig. 2 we average the RAE approximations (89) over both trials and timesteps.

The results show that in all cases the proposed Taylor-based estimators perform as well as the Euler-Maruyama estimators and for the vast majority perform significantly better. Although the Taylor-based estimators generally perform equally well, there are slight differences in how they perform in different conditions. The Taylor-noiseless estimator seems to outperform the re-estimate estimator when the number of trajectory samples is low, and vice versa when the number is high. Recall that the error analysis suggests that the re-estimate estimator has lower bias but higher variance than the Taylor-noiseless estimator. The simulated results confirm the theoretical results, that is, when the number of trajectory samples is low, high variance makes the re-estimate estimator perform poorly, but when there are enough samples to overcome the variance in the estimator, the low bias properties can result in better accuracy. In practice, however, it is likely that the low variance of the Taylor-noiseless estimator is preferable to the slightly more bias it introduces.

5.2 LQR 4D Problem

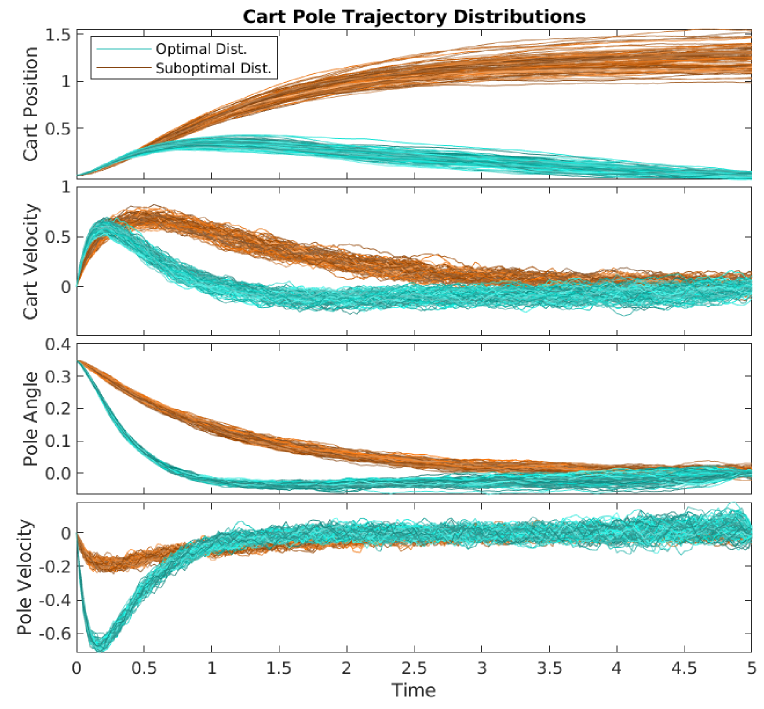

We also tested the proposed estimators on a linearized version of the 4-dimensional finite time cart-pole problem,

where are constant parameters and . For the suboptimal sampling distribution we selected a discrete time approximation of the time-invariant feedback policy

where are constant parameters. The optimal policy is found through the solution of the associated Riccati equations (distributions visualized in Fig. 3(a)).

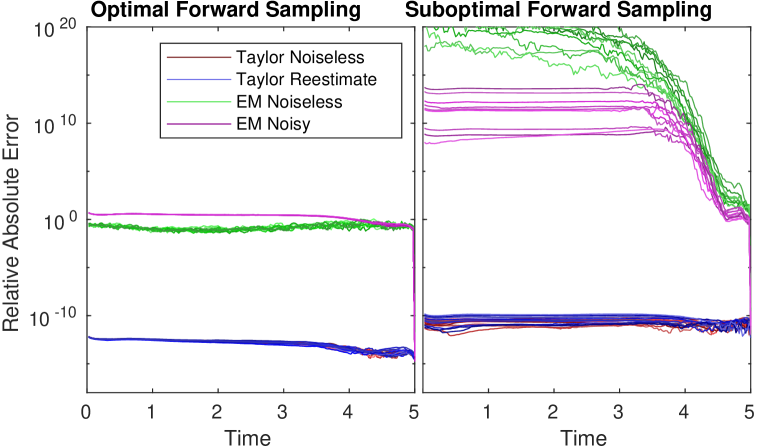

The value function model for used Chebyshev functions of degree 2 and lower (15 basis functions). The RAE approximations (89) are visualized in Fig. 3(b) where and each is defined similarly to (90) based on the mean and standard deviation of the optimal trajectories in each of the 4 dimensions.

As predicted by the error analysis, since this is an LQR problem and the value function is in the class of quadratic functions, the Taylor expansion-based estimators are able to produce approximations of the value function with accuracy near machine precision for both conditions. For the suboptimal forward sampling condition the EM estimators diverge quickly during the backward pass. For the optimal forward sampling condition, corresponding to the on-policy estimation, the EM estimators perform mediocre compared to the value function’s variance and their error is still several orders of magnitudes higher than the Taylor estimators.

These results confirm that the proposed estimators are able to achieve near perfect performance on the most common problem in stochastic optimal control. Further, they confirm that utilizing the second-order derivatives of the value function is crucial for Girsanov-inspired off-policy estimator schemes, contrary to what naïve application of the theory would suggest.

6 Conclusion

Taylor-based estimators for numerically solving Feynman-Kac FBSDEs have been demonstrated to be significantly more accurate than naïve Euler-Maruyama-based estimators through both error analysis and numerical simulation. These estimators are derived by using higher-order Taylor expansions and following the spirit of the continuous-time Feynman-Kac-Girsanov formulation. Both error analysis and numerical simulation confirm that these estimators have very high accuracy when applied to LQR problems. Further, in simulation, the proposed estimators are orders of magnitude more accurate than the EM estimators in both LQR and nonlinear problems. Using these results, this paper also proposes a method to use the estimated value function parameters for generating an improved policy.

Moving forward, the primary challenge with Feynman-Kac FBSDE methods as presented here is how to produce robust iterative methods. Although value function approximation can be extremely accurate in the proximity of the initial forward pass, even for off-policy methods, Runge’s phenomenon begins dominating outside the sampling distribution. As a consequence, when in some extrapolative region, the approximation significantly underestimates the true value function, policy improvement begins to fail and future iterations are constructed based on divergent policies with little room for improvement aside from starting over.

To overcome such difficulties, a potential solution is to use a two-phase algorithm where in the first phase, following the steps presented in this article, the initial policy is sampled and a single on-policy backward pass is performed to find the value function associated with the initial policy. This work establishes that we can obtain a high-accuracy estimate of the value function in this way. In the second phase, a gradual optimization technique such as stochastic gradient descent can be used to refine the value function and policy approximation. The arguments in the minimizations (14) and (88) need not be fully minimized, but can be differentiated with respect to the value function and policy parameters to produce a step of stochastic gradient descent. Such techniques are similar to those used in deep reinforcement techniques such as deep deterministic policy gradient (DDPG) [15], but when combined with the proposed estimators might accelerate convergence considerably.

7 Acknowledgements

This work has been supported by NSF awards CMMI-1662523 and IIS-2008686 and ONR award N00014-18-1-2828. The authors would like to thank Evangelos Theodorou for many helpful discussions and comments.

References

- [1] Christian Bender and Robert Denk. A forward scheme for backward SDEs. Stochastic Processes and their Applications, 2007.

- [2] Christian Bender and Thilo Moseler. Importance sampling for backward SDEs. Stochastic Analysis and Applications, 28(2):226–253, 2010.

- [3] Samuel N Cohen and Robert James Elliott. Stochastic calculus and applications, volume 2. Springer, 2015.

- [4] Edwin L Crow and Kunio Shimizu. Lognormal Distributions. Marcel Dekker New York, 1987.

- [5] Nicole El Karoui, Shige Peng, and Marie Claire Quenez. Backward stochastic differential equations in finance. Mathematical Finance, 7(1):1–71, 1997.

- [6] Ioannis Exarchos and Evangelos A. Theodorou. Stochastic optimal control via forward and backward stochastic differential equations and importance sampling. Automatica, 87:159–165, 2018.

- [7] Ioannis Exarchos, Evangelos A. Theodorou, and Panagiotis Tsiotras. Game-theoretic and risk-sensitive stochastic optimal control via forward and backward stochastic differential equations. In Conference on Decision and Control, pages 6154–6160, Las Vegas, NV, 2016.

- [8] Ioannis Exarchos, Evangelos A. Theodorou, and Panagiotis Tsiotras. Stochastic Differential Games: A Sampling Approach via FBSDEs. Dynamic Games and Applications, 2018.

- [9] Ioannis Exarchos, Evangelos A. Theodorou, and Panagiotis Tsiotras. Stochastic -optimal control via forward and backward sampling. Systems and Control Letters, 118:101–108, 2018.

- [10] Wendell H. Fleming and Raymond W. Rishel. Deterministic and stochastic optimal control. Bulletin of the American Mathematical Society, 82:869–870, 1976.

- [11] Kelsey P Hawkins, Ali Pakniyat, and Panagiotis Tsiotras. On the Time Discretization of the Feynman-Kac Forward-Backward Stochastic Differential Equations for Value Function Approximation. In 60th IEEE Conference on Decision and Control, Austin, TX, 2021. (submitted).

- [12] Desmond J. Higham. An introduction to multilevel Monte Carlo for option valuation. International Journal of Computer Mathematics, 92(12):2347–2360, 2015.

- [13] David H. Jacobson and David Q. Mayne. Differential dynamic programming. North-Holland, New York, NY, 1970.

- [14] Peter E Kloeden and Eckhard Platen. Numerical Solution of Stochastic Differential Equations, volume 23. Springer Science and Business Media, 2013.

- [15] Timothy P. Lillicrap, Jonathan J. Hunt, Alexander Pritzel, Nicolas Heess, Tom Erez, Yuval Tassa, David Silver, and Daan Wierstra. Continuous control with deep reinforcement learning. 4th International Conference on Learning Representations (ICLR), 2016.

- [16] Francis A. Longstaff and Eduardo S. Schwartz. Valuing American options by simulation: A simple least-squares approach. Review of Financial Studies, 14:113–147, 2001.

- [17] George Lowther. Girsanov transformations, May 2010.

- [18] Jin Ma and Jiongmin Yong. Forward-Backward Stochastic Differential Equations and their Applications. Springer, 2007.

- [19] E. Pardoux and S. G. Peng. Adapted solution of a backward stochastic differential equation. Systems and Control Letters, 14(1):55–61, 1990.

- [20] Shige Peng. Probabilistic interpretation for systems of quasilinear parabolic partial differential equations. Stochastics Stochastics Rep, 37(1-2):61–74, 1991.

- [21] Shige Peng. Backward stochastic differential equations and applications to optimal control. Applied Mathematics and Optimization, 27(2):125–144, 1993.

- [22] Sidney Resnick. A Probability Path. Birkhäuser Verlag AG, 2003.

- [23] Halil M. Soner and Nizar Touzi. A stochastic representation for the level set equations. Communications in Partial Differential Equations, 27(9-10):2031–2053, 2002.

- [24] Yuval Tassa. Theory and Implementation of Biomimetic Motor Controllers (Ph.D. Thesis). Hebrew University of Jerusalem, 2011.

- [25] Yuval Tassa, Tom Erez, and William D. Smart. Receding Horizon Differential Dynamic Programming. In Advances in Neural Information Processing Systems 20, pages 1465–1472, 2008.

- [26] Evangelos A. Theodorou, Yuval Tassa, and Emo Todorov. Stochastic differential dynamic programming. In American Control Conference, pages 1125–1132, Baltimore, MD, 2010.

- [27] Ian H Witten, Eibe Frank, and Mark A Hall. Data Mining: Practical Machine Learning Tools and Techniques. Elsevier Inc., 3rd edition, 2011.

- [28] Jiongmin Yong and Xun Yu Zhou. Stochastic Controls: Hamiltonian Systems and HJB Equations, volume 43. Springer, 1999.

Appendix A Proof of Proposition 3.1

Proof.

In the following, the variable

is used as multi-index notation,

Let be an odd number and suppose for some . The -th order term of the Taylor expansion residual is given by Taylor’s theorem as

| (91) |

It can be shown with algebra and the multinomial theorem that there exists functions such that the terms can be linearly separated from the others,

| (92) |

Since both and are -measurable, when taking the conditional expectation the operator passes inside

| (93) |

Due to the independence of the different dimensions of , the conditional expectation inside (93) can be expanded into the product

| (94) |

Since is odd, there exists an such that is odd. The properties of the standard normal distribution guarantee

| (95) |

and thus, (93) is zero as well, so we arrive at the result

| (96) |

Appendix B Proof of Lemma 3.1

Proof.

We have that is -measurable because and are measurable by definition. For the joint distribution to be mutually independent normal random variables, its density function must be where

| (97) |

is the multivariate normal density where and is a normalizing constant. We now verify this is indeed the density of by showing

| (98) |

where , the product of sets in the sigma algebras and . 444We prove this only for the rectangle semi-algebra over sets constructed as [22, p. 144], and assume that the filtration is constructed such that for all . The probability measure (98) over is clearly -additive [22, p. 43] so we can use an extension theorem [22, p. 48] to show that there exists a probability measure that extends to all .

Notice that

and let , where , be the restriction of to the set . By (64) we have

and by the properties of conditional expectation [28, p. 10] we have

where

is the derivative with respect to the distribution over the variables , the conditional expectation is with respect to these variables’ values given, and is the image . The value can be taken outside the conditional expectation because it is deterministic with respect to the conditioned variables . From [28, Chapter 1, Proposition 1.10], it follows that

where is a regular conditional probability. By a change-of-variable and using the independence assumption on , we can write this integral as

where is the distribution in over alone. Converting the distribution to a density gives

which can be algebraically reduced to

Define the change-of-variable mapping , noting that the Lebesgue measures will be equivalent due to translation invariance , and apply it to the integral, giving

The value of this integral does not change for any in the range of . Plugging this back into the original integral and pulling it out due to its invariance, we have

Conditioning the right integral on the variables we can continue this process until the right integral disappears and we are left with the right hand side of (98).

Appendix C Proof of Theorem 3.2 & Theorem 3.3

Proof.

Using the result (69) of Lemma 3.2 we have

and so the expression for the bias is

The variance of the estimator is

noting that we can drop the terms and because they are -measurable.

For the re-estimate estimator we have

| (99) |

and for the noiseless estimator we have

| (100) |

due to (38). Plugging these two equalities into the general expressions for the bias and variance and doing simple reductions yields the theorem results. Note that Theorem 3.2 is proved by setting , which entails , and by excluding from the conditional expectations.

Appendix D Proof of Theorem 3.3

Proof.

First note that the process is a martingale in , that is, for . This can be shown by defining the measures

and noting that, for all ,

where the inner equality is due to and agreeing on .

From [17, Lemma 1] we have

where the final equality is due to the tower property of conditional expectation and the measurability of the remaining terms. Again by the tower property of conditional expectation we have

By the Cauchy-Schwartz inequality, we have that

Using properties of log-normal distributions [4] we have

which, upon substitution, yields the desired result.