Logarithmic law of large random correlation matrix

Nestor Parolyaa111Corresponding author n.parolya@tudelft.nl, Johannes Heinyb and Dorota Kurowickaa

a

Delft Institute of Applied Mathematics, Delft University of Technology,

Delft, The Netherlands

b Ruhr-University Bochum, Department of Mathematics, Bochum, Germany

Abstract

Consider a random vector , where the elements of the vector are i.i.d. real-valued random variables with zero mean and finite fourth moment, and is a deterministic matrix such that the spectral norm of the population correlation matrix of is uniformly bounded. In this paper, we find that the log determinant of the sample correlation matrix based on a sample of size from the distribution of satisfies a CLT (central limit theorem) for and . Explicit formulas for the asymptotic mean and variance are provided. In case the mean of is unknown, we show that after recentering by the empirical mean the obtained CLT holds with a shift in the asymptotic mean. This result is of independent interest in both large dimensional random matrix theory and high-dimensional statistical literature of large sample correlation matrices for non-normal data. At last, the obtained findings are applied for testing of uncorrelatedness of random variables. Surprisingly, in the null case , the test statistic becomes completely pivotal and the extensive simulations show that the obtained CLT also holds if the moments of order four do not exist at all, which conjectures a promising and robust test statistic for heavy-tailed high-dimensional data.

AMS 2010 subject classifications: 60B20, 60F05, 60F15, 60F17, 62H10

Keywords: Sample correlation matrix, CLT, log determinant, large-dimensional asymptotics, random matrix theory, dependent data.

1 Introduction

Sample correlation matrices have always been of vital importance from both theoretical and practical points of view. Principal component analyis, for example, extracts valuable information about large data sets from the eigenvalues of the sample correlation matrix. In particular, the determinant of the sample correlation matrix is one of the most fundamental matrix functions and has been extensively studied in the theory of random matrices as well as in multivariate statistics (see, for instance, the classical monographs Muirhead, (1982) and Anderson, (2003)). The determinant of a random correlation matrix has numerous applications in stochastic geometry (volume of parallelotope, see Nielsen, (1999)) and hypothesis testing (likelihood ratio test) in multivariate statistics (see, Anderson, (2003)). Its properties have been studied by many authors under various settings (see, e.g., Nguyen and Vu, (2014) and references therein). For instance, Goodman, (1963) proved the central limit theorem (CLT) of the logarithmic determinant for random Gaussian matrices, Tao and Vu, (2012) for Wigner matrices, Nguyen and Vu, (2014) for real i.i.d. random matrices under subexponential tail conditions, and Bao et al., (2015); Wang et al., (2018) for general i.i.d. matrices under existence of the 4th moments of matrix entries, to mention a few. In some special cases where a suitable stochastic representation is available, Grote et al., (2019) also proved large deviation results and Heiny et al., 2021a fast Berry–Esseen bounds.

Our particular interest covers the sample correlation matrix denoted by which is computed from a random sample . The determinant is the likelihood ratio test statistic for testing the independence of the entries of a large dimensional random vector coming from a multivariate normal population. If the population correlation matrix is equal to identity, i.e., , several results are available about its sample counterpart . In particular, under multivariate normality the density of is proportional to , see, (Muirhead,, 1982, Theorem 5.1.3). However, the density of the eigenvalues of cannot be obtained in the closed form, which makes the analysis of this random matrix challenging. Nevertheless, some asymptotic properties of the large sample correlation matrix have been obtained in case of and normally distributed data. For example, the empirical distribution of eigenvalues of follows the well-known Marchenko-Pastur law as first shown in Jiang, 2004b (see also Bai and Zhou, (2008); Heiny and Mikosch, (2018) for more general conditions) , while its largest eigenvalue obeys the Tracy-Widom law Bao et al., (2012). The properly normalized largest off-diagonal entry of congerges to a Gumbel distribution as shown in Jiang, 2004a and later generalized in various directions in Zhou, (2007); Li et al., (2012); Liu et al., (2008); Cai and Jiang, (2011) and most recenty to a point process setting in Heiny et al., 2021b .

Moreover, under multivariate normality with , the CLT for holds (see, Jiang and Yang, (2013); Jiang and Qi, (2015)). These results were further generalized to non-normal populations by Gao et al., (2017). On the other hand, not much is known in case . Recently the paper by Jiang, (2019) sheds some light on this challenging case when the data comes from multivariate normal distribution. Particularly, Jiang, (2019) showed that the properly normalized logarithmic determinant of satisfies the CLT under some conditions on the eigenvalues of the population correlation matrix (minimum eigenvalue greater than ).

In this paper we will prove the CLT for under very generic conditions on the data generating process, i.e., non-normality and general population correlation matrix . We provide a closed form expression of the asymptotic mean and variance and discuss how these correspond to Jiang, (2019) in case of normality. The work is under setting of increasing dimension and sample size diverging to infinity simultaneously, while their ratio tends to a constant . Our results are further applied to testing the uncorrelatedness of the elements of a high-dimensional random vector from arbitrary population with finite 4th moments. Moreover, we investigate in detail the behavior of the log-determinant near singularity, i.e., as , constructing of test on uniformity of entries of the sample correlation matrix. Interestingly, the distribution of the test statistic is independent of the population’s fourth moments under in case of non-normal data. This property indicates a very well-behaved statistic for heavy-tailed distributions of the entries of large data matrix and opens a new direction for research in this topic.

Our paper is structured as follows: in Section 2 we formulate the main result, namely the CLT for the logarithmic determinant of the sample correlation matrix for observations with mean zero. We also prove a similar CLT for observations with non-zero mean, for which an additional centering by the sample mean is needed. Section 3 is devoted to applications of the obtained results. Here we study the behavior of the test statistic for testing the uncorrelatedness of the entries of large random vector and testing the uniformity of the entries of a large random correlation matrix. In Section 4 the proofs are given and Section 5 with auxiliary lemmas finishes the paper.

2 Logarithmic law of sample correlation matrix

We consider a -dimensional population , where the elements of the vector are i.i.d. real-valued random variables and is a deterministic matrix. The corresponding population correlation matrix of is then given by , where denotes the diagonal matrix with the same diagonal elements as . We write for the spectral norm of , that is the square root of the largest eigenvalue of .

For a sample from the population with , the (non-centered) sample correlation matrix is given by

where is the (non-centered) sample covariance matrix. We are interested in the asymptotic fluctuations of the logarithmic determinant of as and tend to infinity simultaneously.

Throughout the paper, we will assume that the dimension is a function of the sample size , i.e., , and that . All limits are for , unless explicitly stated otherwise. Strictly speaking, the sample correlation and covariance matrices as well as their population counterparts depend on , that is . For simplicity, we suppress the dependence on in our notation. We write for the identity matrix if the dimension is clear from the context, and denotes convergence in distribution.

The following CLT is our first main result.

Theorem 2.1 (Logarithmic law in the non-centered case).

Assume that are i.i.d. random variables with mean zero, variance one and finite fourth moment . If the spectral norm of is uniformly bounded and with , and let

then

| (2.1) |

where , denotes the Hadamard product and is the symmetric square root of the matrix .

The proof of Theorem 2.1 is given in Section 4. Note that the terms and are uniformly bounded in due to our assumption of boundedness of the largest eigenvalue (spectral norm) of . The term is kept instead of in order to incorporate the case . In particular, if , we deduce from Theorem 2.1 that (2.1) holds with

Noteworthy, if the true mean of the data generating process is known one can already use the above CLT for the purpose of testing but in general one needs to estimate the population mean vector. Thus, one has to consider rather a centered sample correlation matrix

| (2.2) |

where is the centered (by the sample mean) sample covariance matrix given by

| (2.3) |

and denotes the -dimensional vector of ones. In our second main result, we provide a CLT for the logarithmnic determinant of the centered sample correlation matrix.

Theorem 2.2 (Logarithmic law in the centered case).

The proof of Theorem 2.2 is given in Section 4.3. This result is inline with the substitution principle derived by Zheng et al., (2015) for linear spectral statistics of sample covariance matrices in the sense that a substitution of with in the expression for yields up to lower order terms.

Remark 1.

We compare our result with previous ones given in the literature.

(1) It must be noted that the case in Theorem 2.2 was proven for general linear spectral statistics by Gao et al., (2017), one has to, however, compute complex contour integrals first to see the structure of the CLT. The CLT in Theorem 2.2 is proven under milder conditions including arbitrary with bounded norm, the case ; and it obeys a closed form. We also point out that no information is required about the limiting spectral distribution of the population correlation matrices , which appears in the characterization of the Stieltjes transform of the limiting spectral distribution of ; see for example (El Karoui,, 2009, Theorem 1).

(2) Theorem 2.2 generalizes the recent result of Jiang, (2019) to an arbitrary distribution of the entries and removes the restriction on the smallest eigenvalue of . Indeed, assuming that one can rewrite the limiting mean and variance in the following way

which coincide with the centering and normalization sequences in Theorem 1 of Jiang, (2019) up to the term , which is obviously equal to zero in case or, more general, . Nevertheless, it is not the single case when this term disappears, it happens also if . Indeed, by Jensen’s inequality with equality if and only if . Interestingly, in this case the statistic on the left-hand sides in (2.1) and (2.4) become independent of the moment of order four and one could expect that the restriction could be weakened222The investigation of this observation is continued in a subsequent paper..

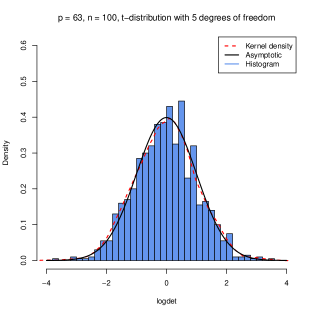

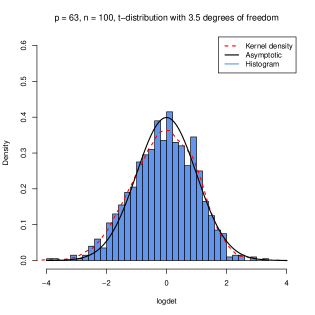

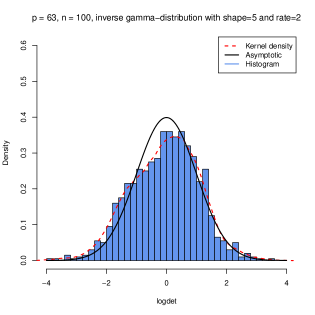

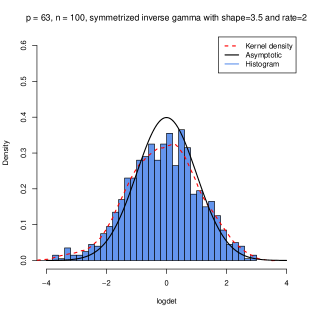

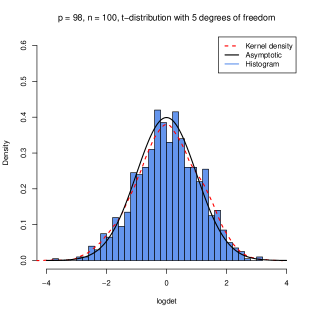

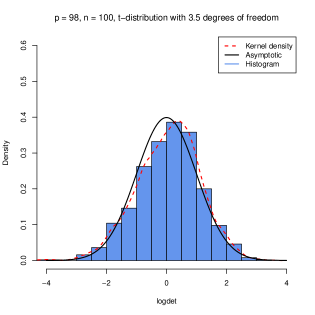

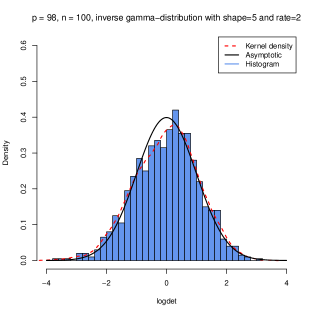

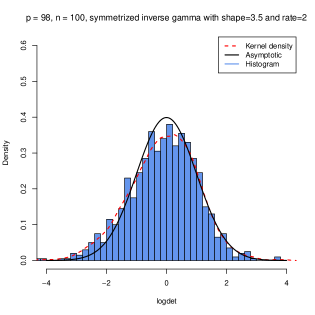

In Figure 1, we have simulated the entries of from a -distribution with different degrees of freedom and from inverse gamma distribution (symmetrized for the case with infinite 4th moment). In case the 4th moment is finite we took the population correlation matrix , while when the 4th moment is infinite . We compute 1000 times and produce the histogram for . Then we compare the obtained histogram and kernel density with the standard normal bell curve in order to judge the goodness of fit.

We proceed by discussing Theorem 2.1 which provides elegant and unified formulas for the asymptotic mean and variance that, in contrast to previous results, avoid heavy computations involving factorials. The CLT in Theorem 2.1 is also valid in the case for both and , which recently has received particular attention for sample covariance matrices in Wang et al., (2018); Nguyen and Vu, (2014); Bao et al., (2015). The following remark sheds additional light on this case.

Remark 2.

(1) We point out that in case the leading term in variance of the provided CLT tends to infinity. For example, if is constant, is of order . Therefore, provided that the largest eigenvalue of is uniformly bounded in , the terms in the asymptotic mean and variance, which are proportional to , and will vanish asymptotically. Although one can expect that the convergence to the normal distribution is much slower in this case, this observation has an interesting implication on the test of uncorrelatedness, i.e., . More precisely, it reveals the fact that this test will loose its power asymptotically in case on any alternative hypothesis as long as has no large eigenvalues (spikes). A very similar result was recently found by Bodnar et al., (2019) by constructing the test on block diagonality of large covariance matrices.

(2) Interestingly, in case Theorem 2.1 also generalizes several results in the literature. First, it is the first result related to the works of Wang et al., (2018) and Bao et al., (2015), where the sample covariance matrix was considered. Secondly, one can recover up to the vanishing constants the result of (Hanea and Nane,, 2018, Theorem 3) taking the result of the CLT for the non-centered sample correlation matrix , setting and . The latter we will further use for testing on uniformity on the entries of the large random correlation matrix because the obtained CLT applies also for non-normal data. For illustration we again simulate the entries of the data matrix from and inverse gamma-distribution 1000 times, similarly as in Figure 1. In Figure 2 we plot the kernel densities together with histograms of properly standardized (as to Theorem 2.2) logarithmic determinant of centered sample correlation matrix in case and . The asymptotic formula provides still a very convenient fit to the sampled logarithmic determinant. Moreover, the extra assumption seems to be purely technical.

At last, the proof of the main results reveals a very interesting fact about the logarithmic determinant of sample correlation matrix. Indeed, one can show, for example in non-centered case, under generic conditions that the following expansion holds

| (2.5) |

where and is a random variable that converges to zero in probability as . One may call this asymptotic expansion of the logarithmic determinant of sample correlation matrix. It shows how the logarithmic determinant of the sample covariance matrix is connected with the latter one for correlation matrix asymptotically. Precisely, going through the proof of Theorem 2.1 one can show that under the asymptotic regime , as , the first and the second summands in (2.5) are asymptotically jointly normal, whereas the third one is converging to a constant in probability. This result is the key ingredient for further investigations of the centered sample correlation matrix and gives very convenient interpretation of the obtained results.

3 Applications

In the subsequent sections the derived CLT will be applied for testing the uncorrelatedness of the elements of and uniformity of the entries of random correlation matrix.

3.1 Testing the uncorrelatedness

Assume that we are interested in testing the hypothesis

| (3.1) |

In order to provide a proper statistical test we need to construct a test statistic and specify its asymptotic pivotal distribution under . In view of Theorem 2.2, a natural test statistic is given by which is asymptotically standard normal under . We will reject the null hypothesis in case is ”too large”, i.e., larger than the quantile of standard normal distribution.

For that reason we generate the data with , where the components of the noise vector are i.i.d. -distributed random variables with degrees of freedom, mean zero and variance equal to one. The experiment was repeated times. Without loss of generality we assume that the population covariance matrix is equal to the correlation matrix (standardized data), which is generated in the following manner:

-

1.

Uncorrelated case: ;

-

2.

Autoregressive case: for ;

-

3.

Equicorrelated case: for .

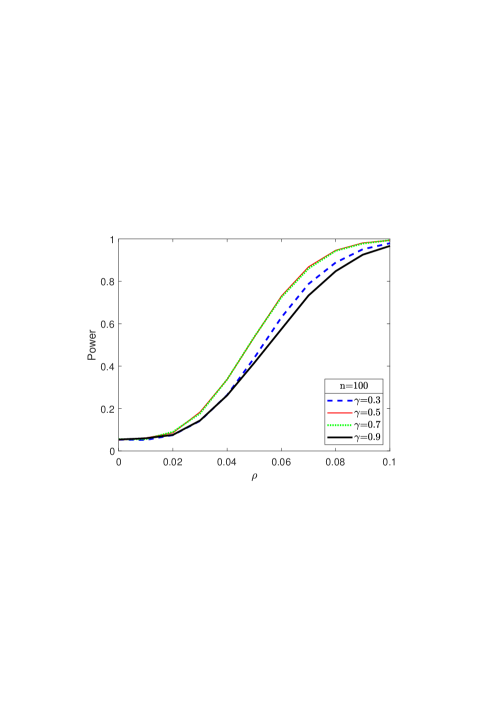

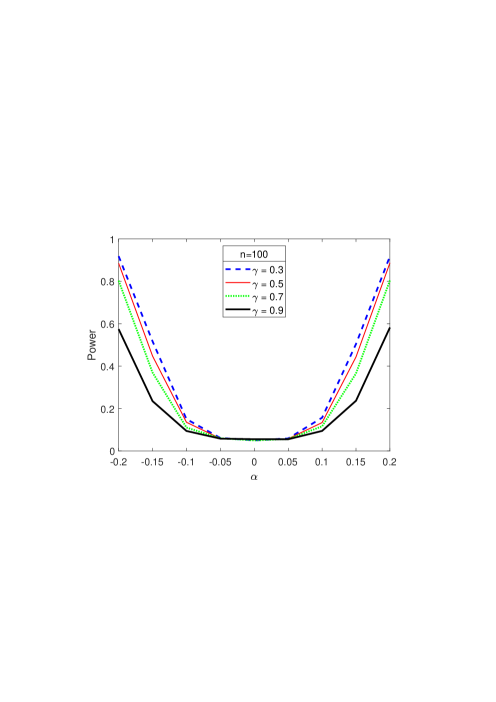

First, we present the empirical sizes of the uncorrelated case in Table 1. The results are plausible even for small values of although the size of is a bit overestimated for . In general, the larger the more pronounced is this effect but it vanishes if we increase and as expected. Even for the test is holding its confidence level quite well, which emphasizes its applicability for moderate finite samples. Next, in Figure 3 we present the empirical powers of the test against the equicorrelated case for , where the test shows non-trivial power. On the top part of the Figure 3 we consider the equicorrelation case. Left we take and is varying to get different gamma’s from to with a step of , while on the right figure we fix and proceed in the same way but with changing . For fixed we observe a tendency towards more power in case of smaller values of except of the case , which can be easily explained by too small value of , where our asymptotic result seems not to work well. This indicates that and should be at least in this situation to guarantee a reasonable approximation. Indeed, when is fixed to we see a natural ranking of the power curves because both and are large enough. Interestingly, we have still nontrivial power for as small as even in case when is near to singularity, i.e., . A very similar picture is observed on the bottom part of Figure 3, where the power of test against autocorrelation structure was examined. Again, even in the worst case the test still provides a reasonable power for . In general, the powers in the autocorrelated case are a bit smaller as in case of equicorrelation, which is not surprising because the correlations are decaying to zero exponentially for the former one.

| 0.3 | 0.5 | 0.7 | 0.9 | |

|---|---|---|---|---|

| 40 | 0.0492 | 0.0528 | 0.0545 | 0.0586 |

| 60 | 0.05 | 0.0493 | 0.0539 | 0.0578 |

| 80 | 0.0522 | 0.0548 | 0.0515 | 0.056 |

| 100 | 0.0504 | 0.053 | 0.053 | 0.052 |

| 500 | 0.0501 | 0.05 | 0.0492 | 0.0527 |

| 1000 | 0.0496 | 0.0523 | 0.0492 | 0.0508 |

|

|

|

|

3.2 Testing the uniformity

In case of independent normal distributed data, the joint density of the elements of the sample correlation matrix is proportional to its determinant. More direct (independent of the data generating process) approach of generating a random correlation matrix, such that the density of its entries is proportional to power of the determinant has been proposed by Joe, (2006). In this paper it was shown that any positive definite correlation matrix can be parametrized in terms of appropriately chosen correlations and partial correlations taking independently values from the interval . If these partial correlations are beta distributed (beta distribution transformed to the interval ) with parameters dependent on the size of the conditioning sets of the partial correlations, then the joint density of entries of the correlation matrix is proportional to , where . Each correlation coefficient in such correlation matrix has a distribution on . The uniform joint density is obtained in case .

Using this fact and the proven CLT we construct a test on the uniformity of the entries of random correlation matrix.

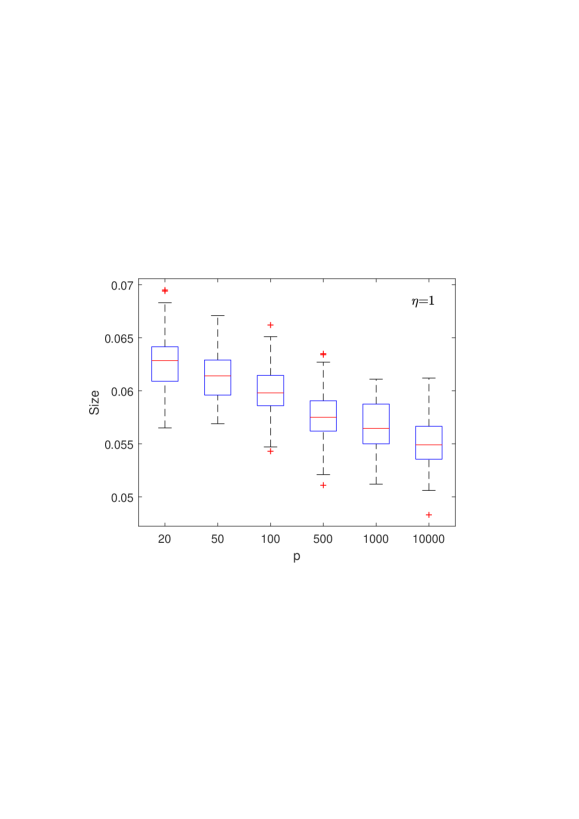

To test this hypothesis to the level of we generate random correlation matrices of dimension using the expansion of the determinant based on partial correlations (due to Joe, (2006)) for different values of and apply our CLT in Theorem 2.1 for . Note that in this situation we do not need to generate data samples, compute correlation matrix and its determinant. We observe only the determinant of -dimensional correlation matrix. Moreover, the formula for the determinant of Joe, (2006) gives us the possibility to generate really large matrices without loss of efficiency. First, in Figure 4 we plot the box-plots of empirical sizes where we observe a slight overestimation of the nominal level of for small dimensions. The convergence to the right size of seems to be quit slow. This is in line with our theoretical finding, where the variance was of order of . So, in order to apply our test dimension must be reasonably large.

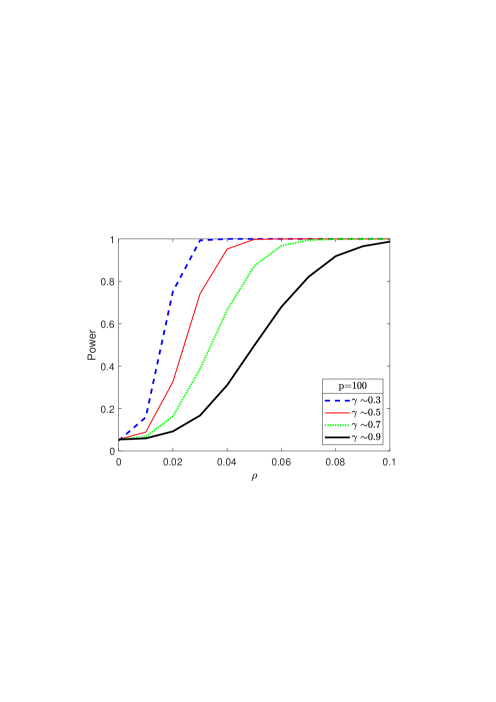

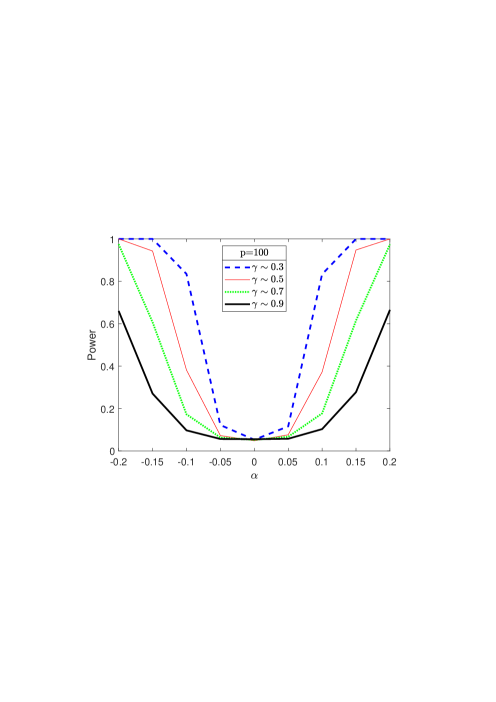

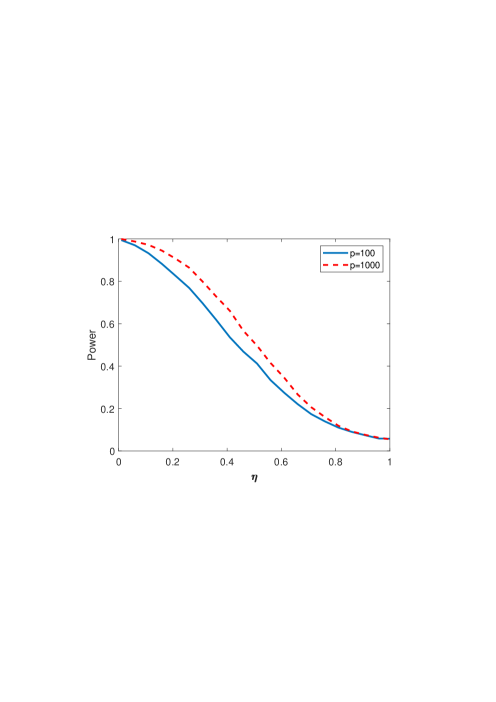

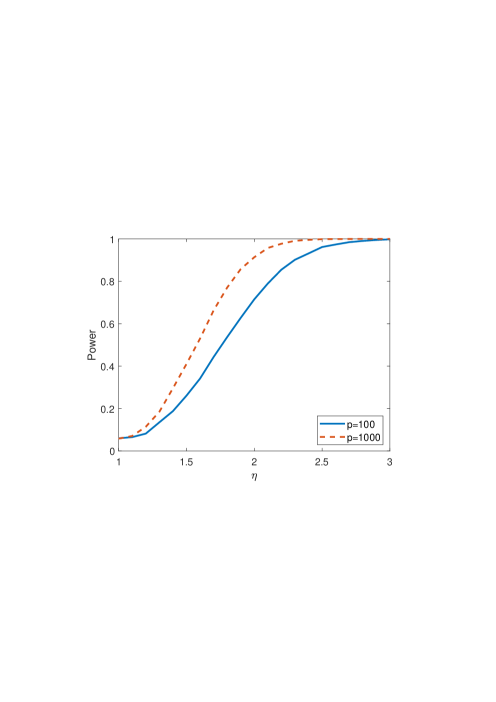

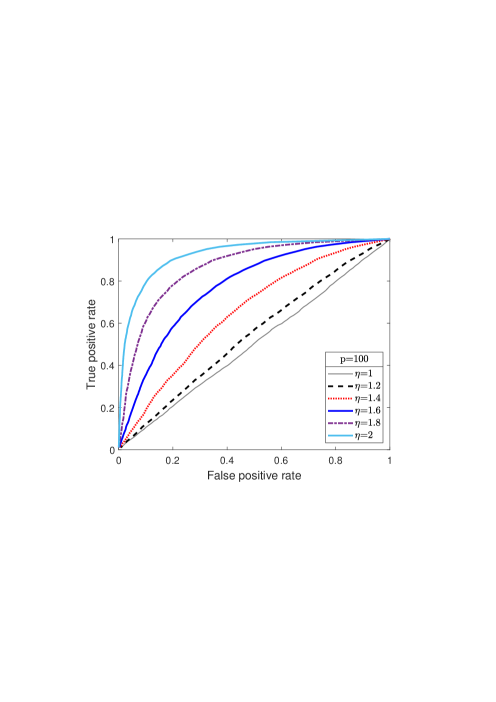

Next we look on the power of the test against alternative . The empirical power functions for and in case of and are presented in Figure 5. One clearly observes an increasing power when dimension gets larger, e.g., for ( similarly for ) both power curves are close to one. In order to investigate their behavior closer we plot the corresponding ROC (Receiver Operating Characteristic) curves for some fixed values of . The results are given in Figure 6. The effect of increasing dimension is more pronounced here but the obtained results show an acceptable behavior even for small changes like . This indicates the usefulness of the obtained CLT for the sample correlation matrix in the extreme case for a large class of distributions.

|

|

|

|

.

Conclusions

In this work we prove the CLT for logarithmic determinant of the large dimensional sample correlation matrix under weak assumptions on data generating process, i.e., we need the existence of the moments of order four. It is also assumed that the dimension of the matrix is proportional to the sample size; the case when they are equal is treated as well. In our work we distinguish between two cases a centered and a non-centered one with slightly different limiting means. Moreover, at the end we apply our obtained results to the testing on uncorrelatedness of high-dimensional random vectors and uniformity of the entries of large random correlation matrix. Simulations suggest that the fourth moment assumption can be further weakened, which opens a new research direction for heavy-tailed sample correlation matrices.

4 Proofs of the main results

We recall that the dimension is a function of the sample size , i.e., , and that . All limits and asymptotic equivalences are for , unless explicitly stated otherwise.

4.1 Proof of Theorem 2.1

From Section 2 we recall the definition of the population correlation matrix and write . Denote and rewrite in the following way

| (4.1) | |||||

where the last equality follows from the fact that

Now we proceed to the second term in (4.1). With the vector denoting the th row of the matrix , it holds

Note that although the elements of one vector are independent zero mean, unit variance variables, the vectors depend through the nonzero covariances in the matrix , i.e., for .

Due to Heiny, (2021) we have almost surely. Recall that all limits are for , unless explicitly stated otherwise. Therefore, using Taylor expansion of around the point zero we get

where is defined by the last equality. Together with (4.1) this gives

Next we show that as . Because we assumed that we can use the same truncation method as Bai and Silverstein, (2004) page 559, namely we can choose a positive (arbitralily) slowly decreasing to zero sequence such that, e.g.,

| (4.2) |

Thus, we may truncate the variables by without altering the asymptotic results. Note that on the contrary to the original variables all the moments of the truncated variables exist. Indeed, it holds for fixed

| (4.3) |

Denote and obtain for the following bound

| (4.4) | |||||

where one has to fix such that for large enough. Now using (4.4) we immediately get that for and, thus, this result is also valid for and .

As a result, we have got the following asymptotic expansion of the logarithmic determinant

| (4.5) |

The asymptotic equality (4.5) is the key ingredient. It obviously holds

In the sequel, we will show that the first two summands of the expansion (4.5) are asymptotically jointly normal, whereas the last one converges to some constant in probability. More precisely, in Section 4.2 we will prove for that

| (4.6) |

with and

In Section 4.2.2 we will prove that

| (4.7) |

Finally, a Taylor expansion yields for , as ,

| (4.8) |

In view of (4.5), equations (4.6), (4.7) and (4.8) imply Theorem 2.1 for . The case will be discussed in Section 4.2.3.

4.2 Proof of (4.6)

Our goal is to find the asymptotic distribution of in the case .

First, consider the term . Now we can apply the CLT proved in Bai and Silverstein, (2004) for the sample covariance matrix of noise, namely , with the function ; see also (Yao et al.,, 2015, p. 37); and get for ,

| (4.9) |

with as in (4.6) and . Here, we prefer to write instead of the asymptotically equivalent in order to obtain a unified formula that incorporates the case .

For the second term it is easy to check that

| (4.10) | |||||

| (4.11) | |||||

where for the calculation of the variance we have used Lemma 5.2.

Next, we calculate the covariance. Since it holds

| (4.12) |

Due to Wang and Yao, (2013) we know that as and we have

| (4.13) |

Concerning the second term in (4.2), it is shown in Section 4.2.1 that

| (4.14) |

Altogether, we obtain from (4.2), (4.13) and (4.14) that

| (4.15) |

independently of the structure of population correlation matrix .

Now using the result of Najim and Yao, (2016) we get for ,

| (4.16) |

where denotes the Levy-Prokhorov distance [we refer to Najim and Yao, (2016) for its definition] and denotes the law of random vector . The vector follows a two-dimensional normal distribution with mean vector zero and covariance matrix . It is important to note that convergence in Levy-Prokhorov distance implies convergence in distribution.

Next, we determine the entries of . From (4.9) we get . Along the lines of the proof of (4.11) one can show that is uniformly bounded in for some . Thus, DasGupta, (2008, Theorem 6.2) ensures that also the moments of linear combinations of the components of converge to the corresponding moments of . From (4.11) and (4.15), we deduce that the remaining entries of can be chosen as and so that

4.2.1 Proof of (4.14)

Using we get

By the matrix determinant lemma we may write

which, because of the independence of and and , implies

| (4.17) |

Next we consider the term . It holds

This implies that

Now, using Lemma 5.1 we can see that

because . By the union bound and Markov’s inequality, we have for any small ,

which implies that as . The latter justifies the Taylor expansion of the logarithm, namely it holds that

Thus, we get

where . Regarding the first term we have using Lemma 5.2

The symbol ”” in the last line means asymptotic equivalence in terms of the convergence of absolute difference to zero. This result follows from Bodnar et al., (2018, Lemma A1)333It has to be noted that Bodnar et al., (2018) need here moments to exist, while we assume . This is due to the fact that they consider the almost sure convergence, while in our situation the convergence in probability is enough. Indeed, it can be easily shown that this extra follows from the Borel-Cantelli lemma. and convergence is uniform over because can be safely replaced by without altering the limit. Similarly, for the second term we have again due to Lemma 5.2 and Bodnar et al., (2018, Lemma A1 and (A.18))

4.2.2 Proof of (4.7)

Set

Denote the elements of the matrix and let be the th row of , while the vector is the th row of the matrix . In order to proceed we need to rewrite the vector in the following way

| (4.18) |

and, thus,

| (4.19) |

Here we denoted for simplicity . Note that from the construction the following elementary identities hold

| (4.20) | |||

| (4.21) |

Let us proceed to , using (4.19), (4.21) and Lemma 5.2 it holds

Denoting and using the properties of the Hadamard product one can simplify the sum as follows

which (recalling the definition of ) implies

| (4.22) |

To prove (4.7), we will show that the variance of converges to zero as . We have

| (4.23) |

and is given in (4.22). For and set and observe that . Since are independent, it follows that whenever . By definition of and (4.19), we have

Therefore we get

| (4.24) |

In view of and , an application of Lemma 5.2 yields

| (4.25) |

This implies that for a constant not depending on (which may change from one appearance to the next), we have

| (4.26) |

Here we used and .

Next, set . By (4.25) and the definition of , we have . It easily follows that

Hence, we deduce that

| (4.27) |

A combination of (4.23), (4.24), (4.26) and (4.27) shows that

| (4.28) |

It remains to prove that

| (4.29) |

To this end we bound . Write . Using the inequality we get

and therefore

| (4.30) |

We proceed by bounding the terms in (4.30). Regarding the first term, a direct calculation yields

| (4.31) |

For the second term, an application of Lemma 5.3 and yield

By Cauchy-Schwarz, we have

| (4.32) |

Now we turn to the third and fourth terms. We have

from which it easily follows that

| (4.33) |

Finally, we prove (4.29). Combining (4.30) and the inequalities for the individual terms (namely (4.31), (4.32) and (4.33)), we obtain

Since and , we have . This completes the proof of (4.29).

4.2.3 The case .

One important difference in the case is that the variance tends to infinity. More precisely, it holds that

| (4.34) |

In Section 4.2, we have shown that the last summand in (4.1) is , which gives us . Using that and Slutsky’s lemma, we deduce that the CLT in (2.1) follows from

| (4.35) |

where

It remains to prove (4.35). To this end, we refine the result of Wang et al., (2018) using the unified expression. So, due to Wang et al., (2018) we get that as and

| (4.36) |

and otherwise if we have

| (4.37) |

We start with the case , where . Using the Stirling formula , it is straightforward to show that

Next, we turn to the case and . Taking the logarithm on both sides of the identity

we get

| (4.38) |

Using (4.38) one can rewrite the CLT in (4.37) for in the case as

Now we apply the Stirling formula to approximate the centering terms for and as follows

Since we conclude that for

| (4.39) |

A similar argument shows that (4.39) also holds if . In view of (4.36), this establishes (4.35) in the case and .

4.3 Proof of Theorem 2.2

The proof is very similar to the proof of the main theorem, thus, we will skip some parts for the sake of simplicity and brevity.

The centered sample correlation matrix can be rewritten in terms of the non-centered sample covariance matrix in the following way

| (4.40) |

where . Now using some matrix calculus we get

Again, denote the vector as the th row of the matrix , it holds

One can check by Lemma 5.1 that

in probability. Therefore, using Taylor expansion of around we get

where and are the expressions from the second and the third lines, respectively. Altogether this gives

Now we use the matrix determinant lemma to get

and after some simplifications can be rewritten as

| (4.41) | |||||

First, we show that . Here we proceed similarly as in the proof of Theorem 2.1 by replacing the term by . It can be seen that all of the arguments apply in the same way and the norm of the matrix is obviously uniformly bounded. The next term we consider is

| (4.42) | |||||

where we have used together with

with . Moreover, it is easy to check that

Now, from the proof of Theorem 2.1 we know that is asymptotically equivalent to . Regarding the other terms in we will show that they converge to zero in probability. It has to be noted that this will follow from the fact that for

where the latter is the consequence of the union bound, Markov inequality and Lemma 5.1 for some large enough. Thus, we get for the second term in (4.42)

because using Theorem 2.1 we know that is a linear spectral statistics which is asymptotically normal with zero mean and, thus, it is bounded. Regarding the third term in (4.42) we receive

where the last line follows from the fact that and is vanishing.

Therefore, we get that and are asymptotically equivalent. Moreover, the term

from (4.41) is exactly the same as in Theorem 2.1. Furthermore, it is easy to see using triangle inequality that for in probability

where the latter follows from (Rubio and Mestre,, 2011, Lemma 4) and (Bai and Silverstein,, 2010, Theorem A.44).

Note also that for

| (4.43) | |||

| (4.44) |

where we have used the Taylor expansion of the logarithm. Thus, taking into account (4.43), (4.44) and (4.8) it is enough to show under different regimes, namely and that the is asymptotically equivalent to .

4.3.1 The case .

Next we show that for as holds

| (4.45) |

Writing and using (4.43), (4.44) and (4.8) one can immediately see that this result corresponds to the substitution of by in the main formula of Theorem 2.1. Let’s consider now . Using Woodbury matrix identity we get

The application of Bai et al., (2007)[see, Theorem 1] yields, as ,

where is the limiting Stieltjes transform of , namely the limit of . Now letting and taking into account that we get

| (4.46) |

The result (4.45) for follows now from (4.46) and the continuous mapping theorem.

4.3.2 The case .

In this case we require to approach zero with a specific speed. We will need the following lemma, which follows from a combination of the proof of Theorem 1 by Bai et al., (2007) and Lemma A.1 in Bao et al., (2015). This result is rather straightforward, thus, we omit here the details.

Lemma 4.1.

Let be a random matrix with and are i.i.d. with mean zero, variance one and . Denote and let . Then we have

and

First, denote and let be a symmetric square root of , then we have

which reveals, e.g., that for with it holds for sufficiently large that

| (4.47) |

because the smallest eigenvalue of is asymptotically equivalent to as . Thus, we may replace by without altering the limit. Reusing the calculations for the case we get

Thus, we have

| (4.48) |

Using Lemma 4.1 we get taking

and

Now using the Markov inequality we may conclude that (4.48) is bounded in probability as and because (4.48) is additionally divided by we get by (4.47) and the triangle inequality that

| (4.49) |

which finishes the proof of Theorem 2.2 in case .

5 Auxiliary results

Lemma 5.1 (Bai and Silverstein, (2010), Lemma 9.1).

Let be an nonrandom matrix and be a random vector of independent entries. Assume that , , , and . Then for any given and , we have

We need the following lemma; see for example parts and of Theorem in Wiens, (1992).

Lemma 5.2 (Moments of quadratic forms).

Let be a random vector with i.i.d. entries, with , and let be real and symmetric nonrandom matrices. Then

where denotes the Hadamard product. As a special case we get the variance

If aditionally , one has

Particularly,

The next result is Lemma 7.10 in Erdös and Yau, (2017).

Lemma 5.3.

Let be independent centered random variables and assume that

for some fixed constants . Then we have for any deterministic complex numbers that

where the constant does not depend on .

Acknowledgments

J.Heiny’s research was supported by the Deutsche Forschungsgemeinschaft (DFG) via RTG 2131 High-dimensional Phenomena in Probability – Fluctuations and Discontinuity. The authors thank Gabriella F. Nane for fruitful discussions.

References

- Anderson, (2003) Anderson, T. (2003). An introduction to multivariate statistical analysis. John Wiley & Sons, New Jersey.

- Bai and Zhou, (2008) Bai, Z. and Zhou, W. (2008). Large sample covariance matrices without independence structures in columns. Statist. Sinica, 18(2):425–442.

- Bai et al., (2007) Bai, Z. D., Miao, B. Q., and Pan, G. M. (2007). On asymptotics of eigenvectors of large sample covariance matrix. The Annals of Probability, 35:1532–1572.

- Bai and Silverstein, (2004) Bai, Z. D. and Silverstein, J. W. (2004). CLT for linear spectral statistics of large dimensional sample covariance matrices. Annals of Probability, 32:553–605.

- Bai and Silverstein, (2010) Bai, Z. D. and Silverstein, J. W. (2010). Spectral Analysis of Large Dimensional Random Matrices. Springer, New York.

- Bao et al., (2012) Bao, Z., Pan, G., and Zhou, W. (2012). Tracy-widom law for the extreme eigenvalues of sample correlation matrices. Electron. J. Probab., 17:32 pp.

- Bao et al., (2015) Bao, Z., Pan, G., and Zhou, W. (2015). The logarithmic law of random determinant. Bernoulli, 21(3):1600–1628.

- Bodnar et al., (2019) Bodnar, T., Dette, H., and Parolya, N. (2019). Testing for independence of large dimensional vectors. Ann. Statist., 47(5):2977–3008.

- Bodnar et al., (2018) Bodnar, T., Parolya, N., and Schmid, W. (2018). Estimation of the global minimum variance portfolio in high dimensions. European Journal of Operational Research, 266(1):371–390.

- Cai and Jiang, (2011) Cai, T. T. and Jiang, T. (2011). Limiting laws of coherence of random matrices with applications to testing covariance structure and construction of compressed sensing matrices. Ann. Statist., 39(3):1496–1525.

- DasGupta, (2008) DasGupta, A. (2008). Moment Convergence and Uniform Integrability, pages 83–89. Springer New York, New York, NY.

- El Karoui, (2009) El Karoui, N. (2009). Concentration of measure and spectra of random matrices: applications to correlation matrices, elliptical distributions and beyond. Ann. Appl. Probab., 19(6):2362–2405.

- Erdös and Yau, (2017) Erdös, L. and Yau, H.-T. (2017). A dynamical approach to random matrix theory, volume 28 of Courant Lecture Notes in Mathematics. Courant Institute of Mathematical Sciences, New York; American Mathematical Society, Providence, RI; Available at http://www.math.harvard.edu/htyau/RM-Aug-2016.pdf.

- Gao et al., (2017) Gao, J., Han, X., Pan, G., and Yang, Y. (2017). High dimensional correlation matrices: the central limit theorem and its applications. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 79(3):677–693.

- Goodman, (1963) Goodman, N. R. (1963). The distribution of the determinant of a complex wishart distributed matrix. Ann. Math. Statist., 34(1):178–180.

- Grote et al., (2019) Grote, J., Kabluchko, Z., and Thäle, C. (2019). Limit theorems for random simplices in high dimensions. ALEA Lat. Am. J. Probab. Math. Stat., 16(1):141–177.

- Hanea and Nane, (2018) Hanea, A. M. and Nane, G. F. (2018). The asymptotic distribution of the determinant of a random correlation matrix. Statistica Neerlandica, 72(1):14–33.

- Heiny, (2021) Heiny, J. (2021). Large correlation matrices: A comparison theorem and its applications. In review.

- (19) Heiny, J., Johnston, S., and Prochno, J. (2021a). Thin-shell theory for rotationally invariant random simplices. arXiv preprint arXiv:2103.11872.

- Heiny and Mikosch, (2018) Heiny, J. and Mikosch, T. (2018). Almost sure convergence of the largest and smallest eigenvalues of high-dimensional sample correlation matrices. Stochastic Processes and their Applications, 128(8):2779–2815.

- (21) Heiny, J., Mikosch, T., and Yslas, J. (2021b). Point process convergence for the off-diagonal entries of sample covariance matrices. Ann. Appl. Probab., 31(2):538–560.

- (22) Jiang, T. (2004a). The asymptotic distributions of the largest entries of sample correlation matrices. Ann. Appl. Probab., 14(2):865–880.

- (23) Jiang, T. (2004b). The limiting distributions of eigenvalues of sample correlation matrices. Sankhy: The Indian Journal of Statistics (2003-2007), 66(1):35–48.

- Jiang, (2019) Jiang, T. (2019). Determinant of sample correlation matrix with application. Ann. Appl. Probab., 29(3):1356–1397.

- Jiang and Qi, (2015) Jiang, T. and Qi, Y. (2015). Likelihood ratio tests for high-dimensional normal distributions. Scandinavian Journal of Statistics, 42(4):988–1009.

- Jiang and Yang, (2013) Jiang, T. and Yang, F. (2013). Central limit theorems for classical likelihood ratio tests for high-dimensional normal distributions. Ann. Statist., 41(4):2029–2074.

- Joe, (2006) Joe, H. (2006). Generating random correlation matrices based on partial correlations. Journal of Multivariate Analysis, 97(10):2177–2189.

- Li et al., (2012) Li, D., Qi, Y., and Rosalsky, A. (2012). On Jiang’s asymptotic distribution of the largest entry of a sample correlation matrix. J. Multivariate Anal., 111:256–270.

- Liu et al., (2008) Liu, W.-D., Lin, Z., and Shao, Q.-M. (2008). The asymptotic distribution and Berry-Esseen bound of a new test for independence in high dimension with an application to stochastic optimization. Ann. Appl. Probab., 18(6):2337–2366.

- Muirhead, (1982) Muirhead, R. (1982). Aspects of Multivariate Statistical Theory. Wiley, New York.

- Najim and Yao, (2016) Najim, J. and Yao, J. (2016). Gaussian fluctuations for linear spectral statistics of large random covariance matrices. Ann. Appl. Probab., 26(3):1837–1887.

- Nguyen and Vu, (2014) Nguyen, H. H. and Vu, V. (2014). Random matrices: Law of the determinant. Ann. Probab., 42(1):146–167.

- Nielsen, (1999) Nielsen, J. (1999). The distribution of volume reductions induced by isotropic random projections. Advances in Applied Probability, 31(4):985–994.

- Rubio and Mestre, (2011) Rubio, F. and Mestre, X. (2011). Spectral convergence for a general class of random matrices. Statistics & Probability Letters, 81(5):592–602.

- Tao and Vu, (2012) Tao, T. and Vu, V. (2012). A central limit theorem for the determinant of a wigner matrix. Advances in Mathematics, 231(1):74–101.

- Wang and Yao, (2013) Wang, Q. and Yao, J. (2013). On the sphericity test with large-dimensional observations. Electron. J. Statist., 7:2164–2192.

- Wang et al., (2018) Wang, X., Han, X., and Pan, G. (2018). The logarithmic law of sample covariance matrices near singularity. Bernoulli, 24(1):80–114.

- Wiens, (1992) Wiens, D. P. (1992). On moments of quadratic forms in non-spherically distributed variables. Statistics, 23(3):265–270.

- Yao et al., (2015) Yao, J., Zheng, S., and Bai, Z. (2015). Large sample covariance matrices and high-dimensional data analysis. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, New York.

- Zheng et al., (2015) Zheng, Z., Bai, Z. D., and Yao, J. (2015). Substitution principle for clt of linear spectral statistics of high-dimensional sample covariance matrices with applications to hypothesis testing. The Annals of Statistics, 43:546–591.

- Zhou, (2007) Zhou, W. (2007). Asymptotic distribution of the largest off-diagonal entry of correlation matrices. Trans. Amer. Math. Soc., 359(11):5345–5363.