Distributed and Asynchronous Algorithms for N-block Convex Optimization with Coupling Constraints

1 Introduction

In this work, we focus on designing a distributed algorithm for solving block-separable convex optimization problems with both linear and nonlinear coupling constraints. More specifically, we consider the following problem:

| (1) | ||||

| subject to | ||||

where each block of decision variable is constrained by a closed and convex set for all , and . The objective function is block-separable, and each function is assumed to be continuous and convex for all . All blocks ’s are coupled in a linear equality constraint, where each is a given matrix for all , and is a given vector. All blocks ’s are also coupled in a system of nonlinear inequality constraints, where each constraint function is also block-separable and each function is assumed to be continuous and convex for all and . A wide range of application problems can be mathematically formulated as optimization problems of the form (1), arising from the areas including optimal control [14], network optimization [7], statistical learning [2] and etc.

The alternating direction method of multipliers (ADMM) [2], as well as its variants [6, 12, 13], is an efficient distributed algorithm for solving convex block-separable optimization problems with linear coupling constraints, but problems of (1) with nonlinear coupling constraints can not be directly handled by ADMM-typed algorithms.

To overcome the above-mentioned limitations of the ADMM-typed algorithms, we first extend the -block Predictor Corrector Proximal Multiplier Method (PCPM) algorithm to solve an -block convex optimization problem with both linear and nonlinear coupling constraints. We further extend the -block PCPM algorithm to an asynchronous iterative scheme, where a maximum tolerable delay is allowed for each distributed unit, and apply it to solve an -block convex optimization problem with general linear coupling constraints.

The remainder of the chapter is organized as follows. In Section 2, we present an extended -block PCPM algorithm for solving general constrained -block convex optimization problems. We first establish global convergence under mild assumptions, and then prove the linear convergence rate with slightly stronger assumptions. In Section 3, we further extend the N-block PCPM algorithm to an asynchronous scheme with the bounded delay assumption. We establish both convergence and global sub-linear convergence rate under the conditions of strong convexity. Section 4 presents the numerical results of applying the proposed algorithms to solve a graph optimization problem arising from an application of housing price prediction. Finally, Section 5 concludes this chapter with discussions of the limitations of the algorithms and possible future research directions.

2 Extending the PCPM Algorithm to Solving General Constrained N-block Convex Optimization Problems

2.1 PCPM Algorithm

To present our distributed algorithm, we first briefly describe the original PCPM algorithm [5] to make this paper self-contained. For this purpose, it suffices to consider a 2-block linearly constrained convex optimization problem:

| (2) | ||||

| subject to |

where and are closed proper convex functions, and are full row-rank matrices, is a given vector, and is the corresponding Lagrangian multiplier associated with the linear equality constraint. The classic Lagrangian function is defined as:

| (3) |

It is well-known that for a convex problem of the specific form in (2) (where the linear constraint qualification automatically holds), finding an optimal solution is equivalent to finding a saddle point such that . To find such a saddle point, a simple dual decomposition algorithm can be applied to . More specifically, at each iteration , given a fixed Lagrangian multiplier , the primal decision variables can be obtained, in parallel, by minimizing . Then a dual update is performed.

While the above algorithmic idea is simple, it is well-known that convergence cannot be established without more restrictive assumptions, such as strict convexity of and (e.g., Theorem 26.3 in [10]). One approach to overcome such difficulties is the proximal point algorithm, which obtains by minimizing the proximal augmented Lagrangian function defined as . The parameter is given, which determines the step-size for updating both primal and dual variables in each iteration, and plays a key role in the convergence of the overall algorithm. The primal minimization step now becomes:

| (4) |

With (4), however, and can no longer be obtained in parallel due to the augmented term . To overcome this difficulty, the PCPM algorithm introduces a predictor variable :

| (5) |

Using the predictor variable, the optimization in (4) can be approximated as:

| (6) |

which allows and to be obtained in parallel again. After solving (6), the PCPM algorithm updates the dual variable as follows:

| (7) |

which is referred to as a corrector update.

2.2 N-block PCPM Algorithm for General Constrained Convex Optimization Problems

In the -block PCPM algorithm presented in Section 2.1, we observe that the introduction of the predictor variable eliminates the quadratic term in the proximal augmented Lagrangian function and make the primal minimization step parallelizable again, which is a major difference from the ADMM algorithm. For an -block convex optimization problem with additional nonlinear coupling constraints:

| (8) | ||||

| subject to | ||||

the potential coupling caused by the quadratic term could be even worse. Using the same technique of introducing the predictor variable, we extend the -block PCPM algorithm for solving (8).

First, we make a blanket assumption on problem (8) throughout this chapter that the Slater’s constraint qualification (CQ) holds.

Assumption 2.1 (Slater’s CQ).

There exists a point such that

where denotes the relative interior of the convex set for all .

To apply the PCPM algorithm to (8), at each iteration , with a given primal dual pair, , we start with a predictor update:

| (9) | ||||

where denotes the projection of a vector onto a set , and refers to the set of all non-negative real numbers.

After the predictor update, we update the primal variables by minimizing the Lagrangian function evaluated at the predictor variable , plus the proximal terms. The primal minimization step can be decomposed as

| (10) | ||||

A corrector update is then performed for each Lagrangian multiplier :

| (11) | ||||

The overall structure of -block PCPM algorithm is presented in Algorithm 1 below.

2.3 Convergence Analysis

We make the following additional assumptions on the optimization problem (8).

Assumption 2.2 (Lipschitz Continuity).

For all and , each single-valued function is Lipschitz continuous with modulus of , i.e., for any .

Assumption 2.3 (Existence of a Saddle Point).

For the Lagrangian function of (8):

| (12) |

we assume that a saddle point exists; that is, for any , , and ,

| (13) |

Note that coupled with the blanket Assumption 2.1 that Slater’s CQ holds for the optimization problem (8), the above assumption is equivalent to say that an optimal solution of (8) is assumed to exist (see Corollary 28.3.1 in [10]).

Next, we derive some essential lemmas for constructing the main convergence proof. The following lemma is due to Proposition in [9], and for completeness, we provide the detailed statements below.

Lemma 2.1 (Inequality of Proximal Minimization Point).

Given a closed, convex set , and a continuous, convex function . With a given point and a positive number , if is a proximal minimization point; i.e. , then we have that

| (14) |

Proof.

Denote . By the definition of , we have . Since is strongly convex with modulus , it follows that for any . ∎

Lemma 2.2.

Similar to the convergence analysis of the PCPM algorithm in [5], we now establish some fundamental estimates of the distance at each iteration between the solution point and the saddle point .

Proposition 2.3.

Proof.

The details of the proof are provided in Section A.1. ∎

Theorem 2.4 (Global Convergence).

Proof.

Please see Section A.2 for details. ∎

To establish convergence rate, we need to make an additional assumption on Problem (8), as follows.

Assumption 2.4 (Lipschitz Inverse Mapping).

Assume that there exists a unique saddle point such that, given an inverse mapping :

| (19) | ||||

and a fixed positive real number , we have

for some , whenever the point and

The above assumption states that the inverse mapping is Lipschitz continuous at the origin with modulus . By Proposition 2 in [8], to obtain a plausible condition for the Lipschitz continuity of at the origin, we appeal to the strong second-order conditions for optimality which are comprised of the following properties:

-

(i)

There is a saddle point of the optimization problem (8) such that for all , where denotes the interior of the convex set . Moreover, for all and , function is twice continuously differentiable on a neighborhood of .

-

(ii)

Let denote the set of active constraint indices at the point of : . Then for all , and forms a linearly independent set.

-

(iii)

The Hessian matrix satisfies for any

We now establish the linear convergence rate of Algorithm 1.

Theorem 2.5 (Linear Convergence Rate).

Assume that Assumption 2.1 to Assumption 2.4 hold. Let satisfy (18) and let be a sequence generated by Algorithm 1, with an arbitrary starting point ; then the sequence converges linearly to the unique saddle point . More specifically, there exists an integer such that, for all , we have:

| (20) | ||||

where .

Proof.

Please see Section A.3 for details. ∎

2.4 Numerical Experiments

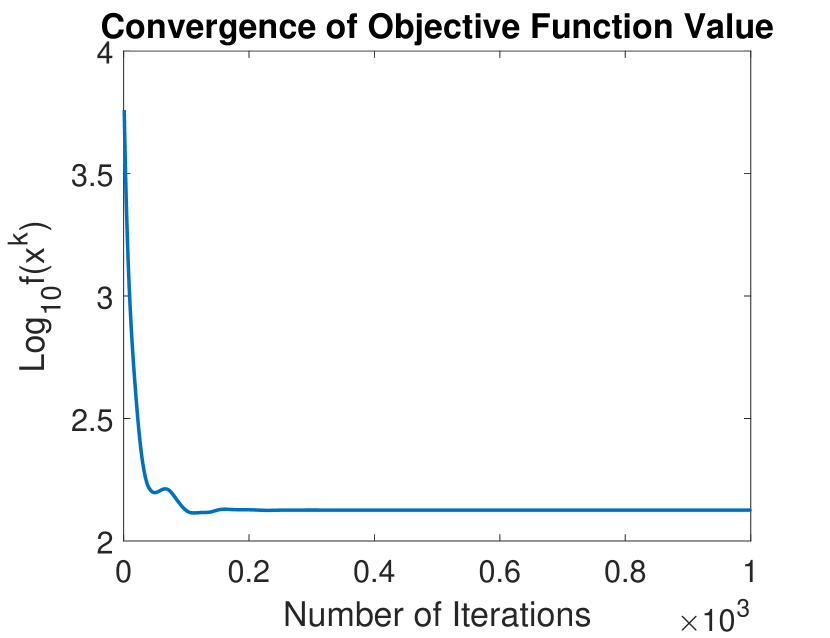

Consider the following -dimensioned, block-separable convex optimization problem with nonlinear coupling constraints, modeling a decentralized planning of an economic system and suggested by [1]:

| subject to | ||||

| (21) |

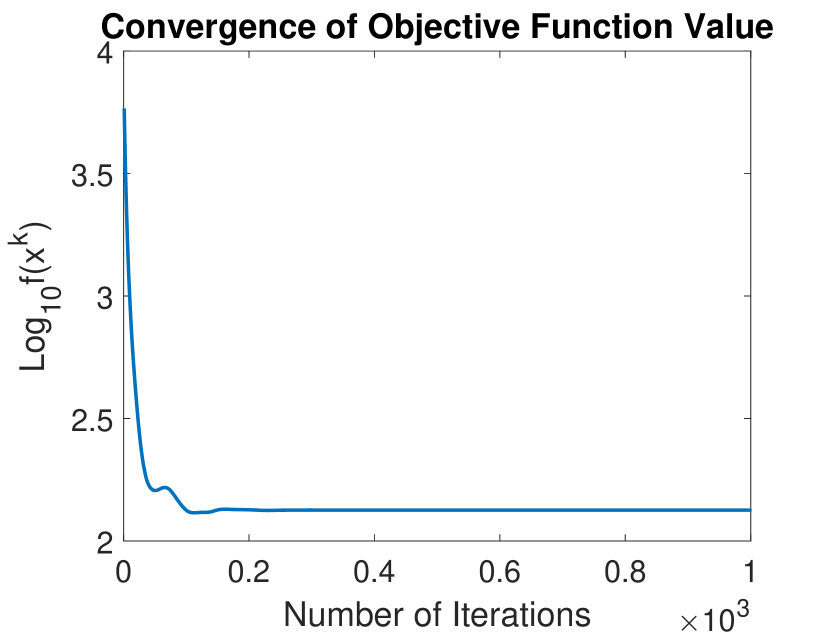

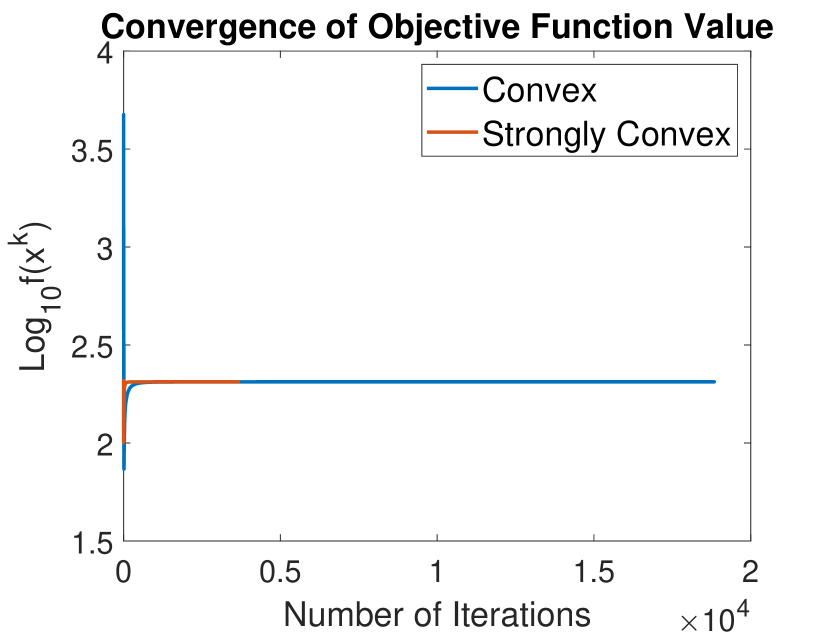

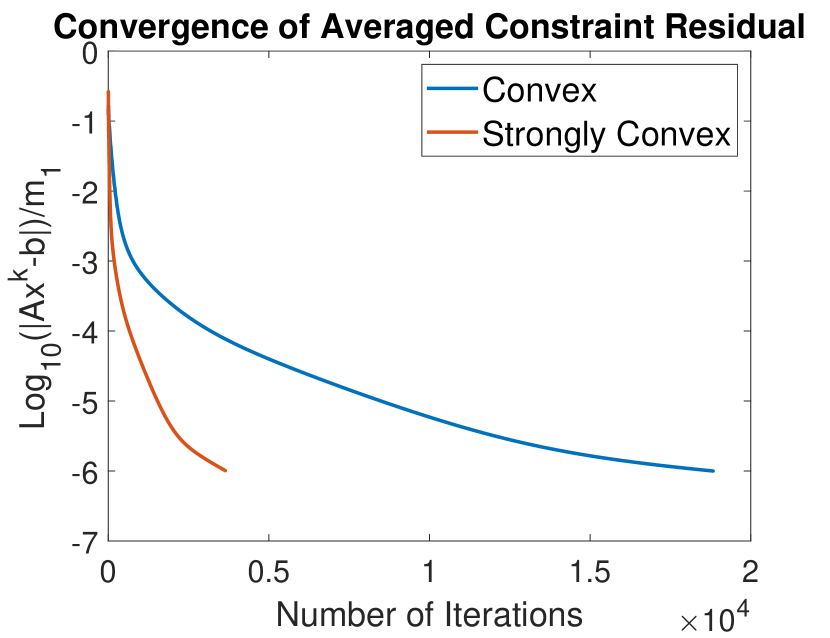

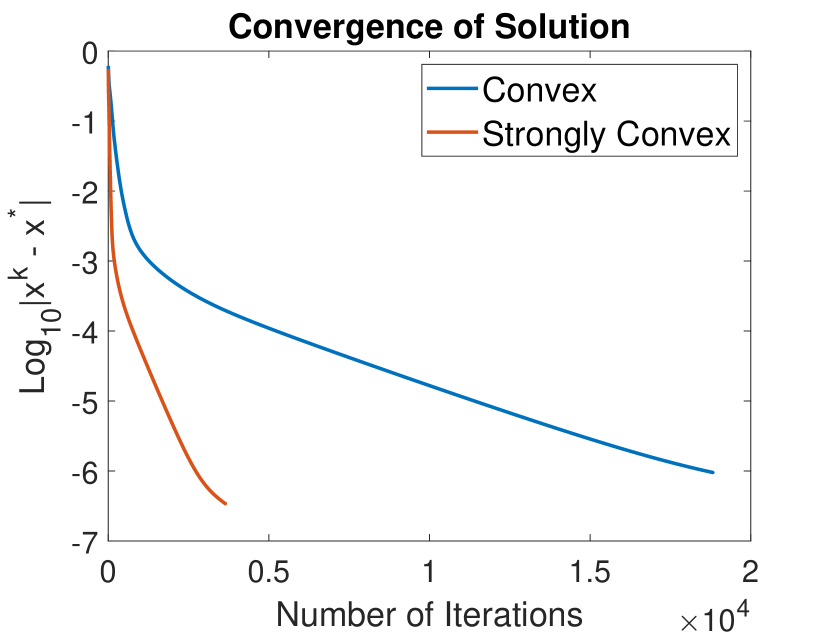

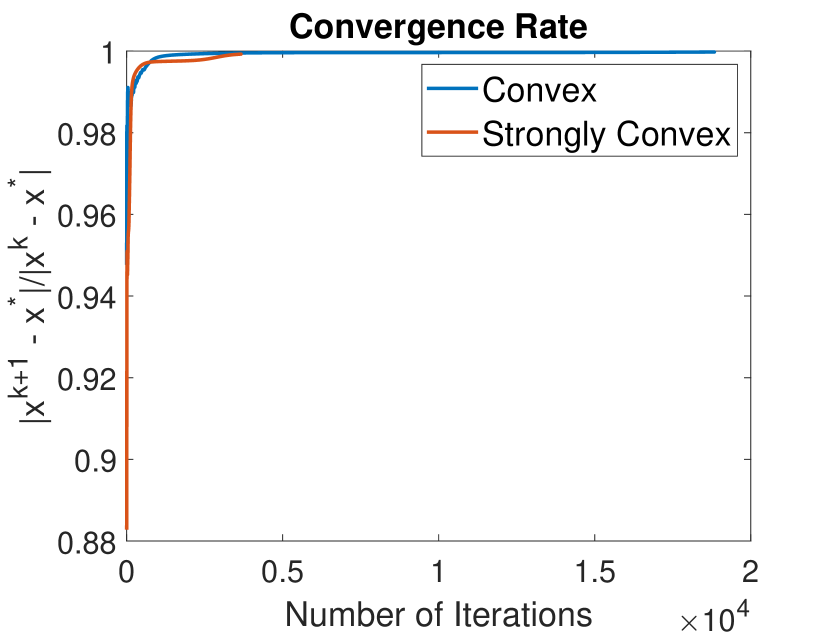

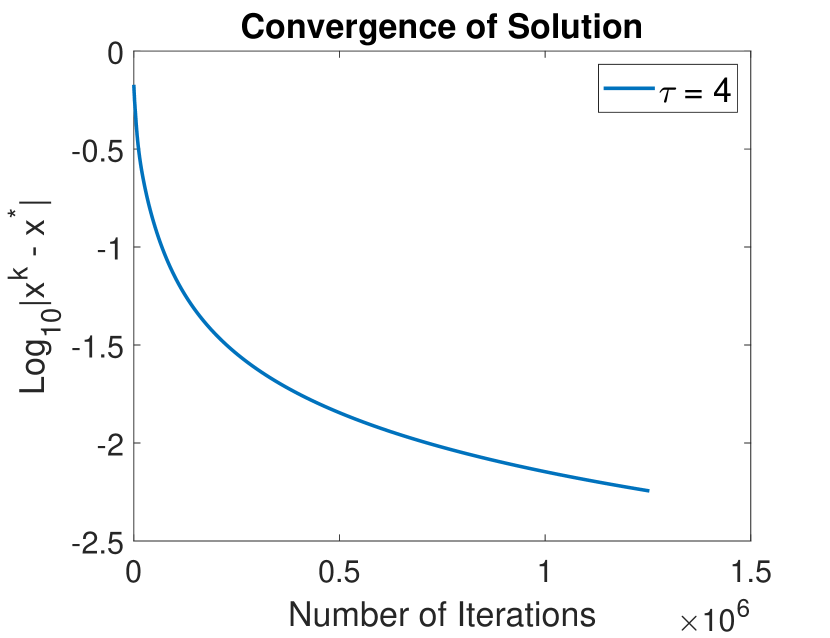

A minimum function value of can be obtained at the point of (, , , , , , , , , , , , , , , , , , , ).111The solution is obtained using the nonlinear constrained optimization solver filter of Neos Solver at https://neos-server.org/neos/solvers/. Applying Algorithm 1 and decomposing the original problem into small sub-problems, we achieve the following convergence results, presented in Figure 1.

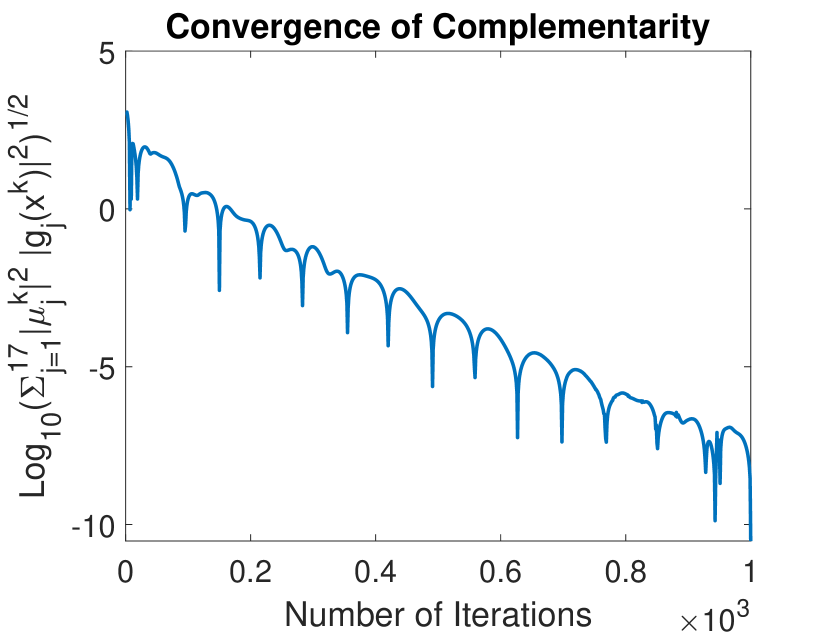

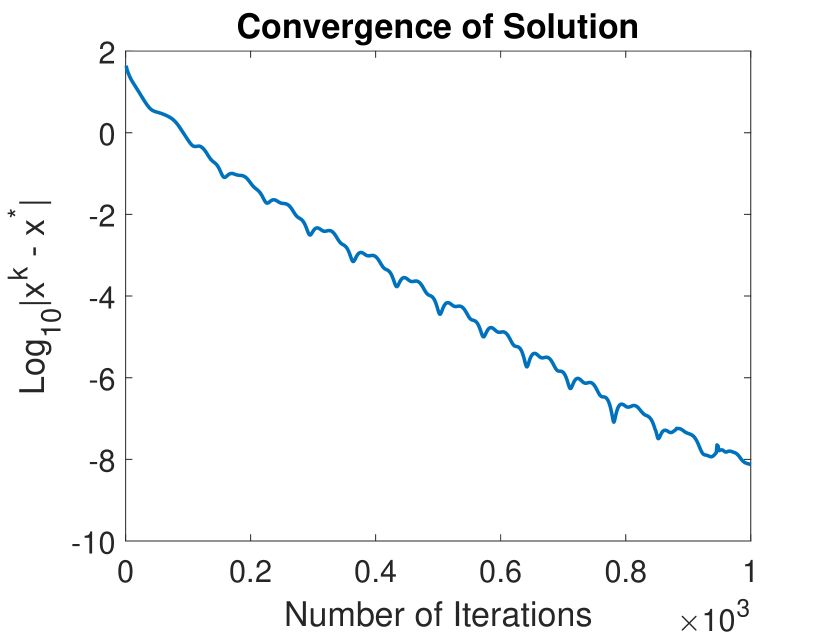

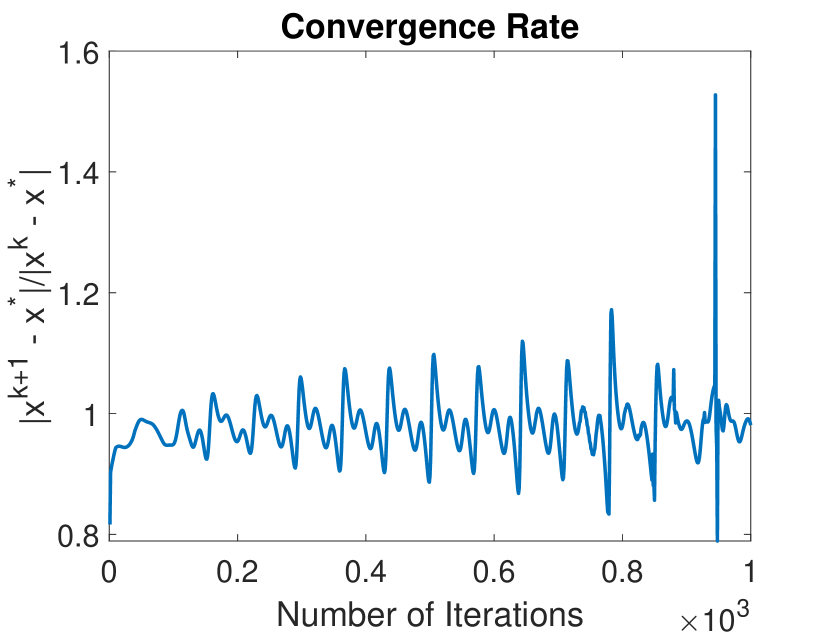

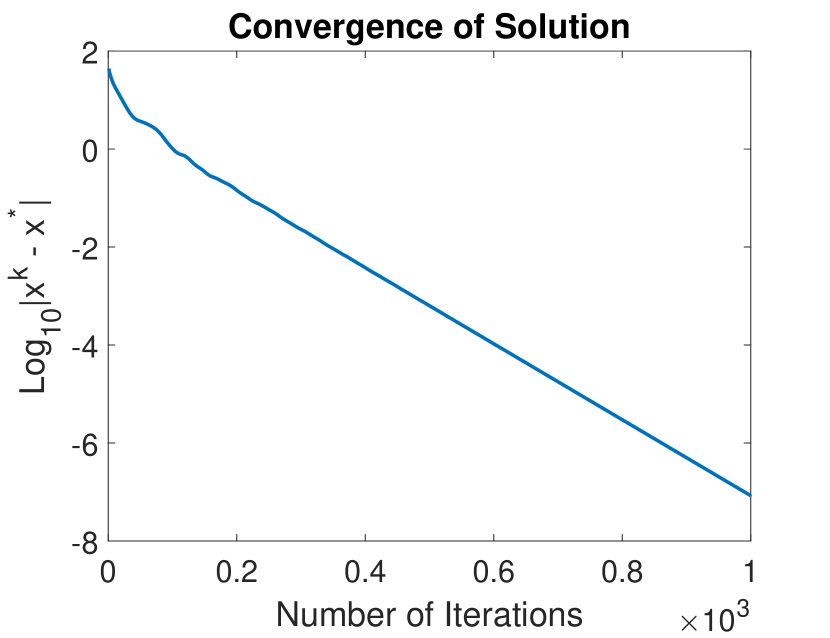

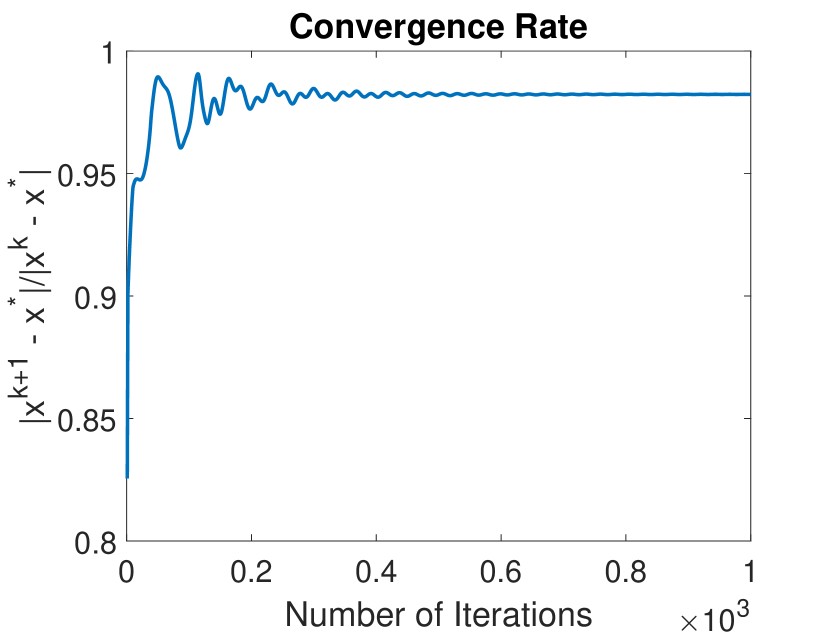

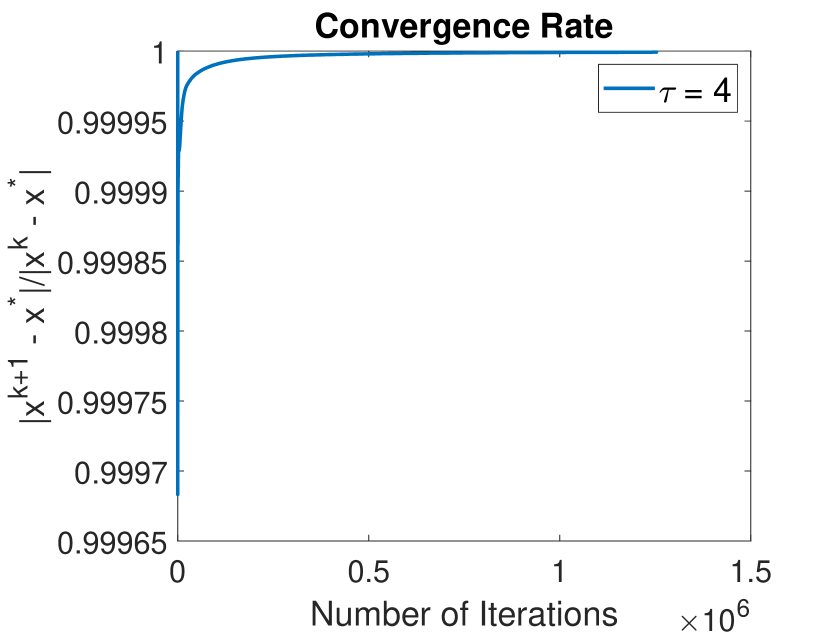

Next, by replacing the term of in the objective function of (21) with and the term of in the -th constraint with , we make the modified problem satisfy Assumption 2.4. A minimum function value of can be obtained at the point of (, , , , , , , , , , , , , , , , , , , ). An additional linear convergence rate of applying Algorithm 1 is observed in the following convergence results, presented in Figure 2.

3 Extending the N-block PCPM Algorithm to an Asynchronous Scheme

As a starting point, we first consider the following N-block convex optimization problem with only linear coupling constraints:

| (22) | ||||

| subject to | ||||

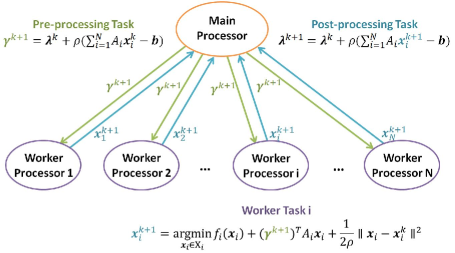

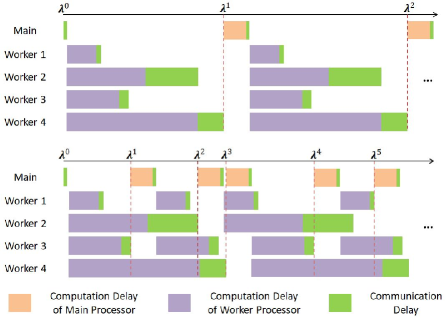

The decision variables, the objective function and the constraints are the same as in the optimization problem (1). When applying Algorithm 1 to solving the above problem, each iteration can be interpreted as main-worker paradigm [11], shown in Figure 3.

At each iteration , a predictor update of is first performed on a main processor and is broadcast to each worker processor, which is called a pre-processing task. Upon receiving the updated predictor variable from the main processor, each worker processor solves the decomposed sub-problem in parallel and send its updated primal decision variable back to the main processor, which is called a worker task. After gathering all updated decision variables, a corrector update is then performed on the main processor, which is called a post-processing task.

The speed of the algorithm is significantly limited by the slowest worker processor, since the post-processing task can not start until all worker tasks are finished and the results are sent back to the main processor. For large-scale problems, with the number of worker processors increasing, the issue of node synchronization can be a major concern for the performance of synchronous distributed algorithms. While in an asynchronous scheme, the main processor can proceed with only part of worker tasks finished. Figure 4

shows an example of main processor and worker processors with different lengths of computation and communication delays. In the asynchronous scheme, the main processor starts a new iteration whenever receives the results from at least worker processors, which leads to much faster iterations than the synchronous scheme.

In this section, we extend the -block PCPM algorithm to an asynchronous scheme to solve the linearly constrained -block convex optimization problem (22).

3.1 Asynchronous N-block PCPM Algorithm for Convex Optimization Problems with Linear Coupling Constraints

To achieve the convergence of the asynchronous -block PCPM algorithm, similar to [3, 4], we require that the asynchronous delay of each parallel worker processor is bounded. Let denote the iteration index on the main processor. At each iteration , let denote the subset of worker processors from whom the main processor receives the updated decision variable , and let denote the rest of the worker processors, whose information does not arrive.

Definition 3.1 (Bounded Delay).

Let an integer denote the maximum tolerable delay. At any iteration , with a bounded delay, it must holds that for all . When , it’s a synchronous scheme.

At each each iteration on the main processor, all worker processors are divided into two sets and , distinguished by whether their information arrives or not at the current moment. Let denote the number of iterations that each worker processor is delayed. If for each worker processor , the main processor uses the partially updated decision variables to perform both corrector and predictor updates for the Lagrangian multiplier; otherwise, the main processor must wait until the worker processors with finish their tasks with information received by the master processor. Consequently, new divide of worker processors into and is generated, and the bounded delay condition is then satisfied. The overall structure of the Asynchronous -Block PCPM algorithm for solving the linearly constrained convex optimization problem (22) is presented in Algorithm 2 and Algorithm 3.

| (23) |

| (24) | ||||

| (25) |

| (26) |

3.2 Convergence Analysis

Different from the synchronous -block PCPM algorithm, the convexity of is not enough to achieve the global convergence due to the asynchronous delay in the system. We make the following additional assumption on problem (22).

Assumption 3.1 (Strong Convexity).

For all , each is a continuous, strongly convex function with modulus .

Accordingly, we extend Lemma 2.1 to functions with strong convexity.

Lemma 3.1 (Inequality of Proximal Minimization Point with Strong Convexity).

Given a closed, convex set , and a continuous, strongly convex function with modulus . With a given point and a positive number , if is a proximal minimization point; i.e. , then we have that

| (27) |

Proof.

Denote . By the definition of , we have . Since is strongly convex with modulus , it follows that for any . ∎

Now, we present the main convergence result.

Theorem 3.2 (Sub-linear Convergence Rate).

Proof.

Please see Section B.1 for details. ∎

4 Numerical Experiments

4.1 An Optimization Problem on a Graph

In this subsection, we consider an optimization problem on a graph, arising from the training process of regressors with spatial clustering, proposed by [7]. Traditional regressors obtains a parameter vector via solving the following optimization problem on a training data set:

| (30) |

where is the number of data points, describes the constraints on the parameter vector, each function denotes the loss function on each training data point for all , and denotes some type of regularization function.

When the spatial information is accessible, such as the latitude and longitude data, a map of data points then becomes available. Instead of using a global regressor with a common parameter vector for the whole data set, a local regressor can be built at each data point with a local parameter vector . Let denote the distance between the data point and (). Different from distributed learning, where a consensus constraint should be satisfied for all local variables, we require that the difference between two local parameter vectors decreases as the distance decreases. Let denote a set of data points within a neighborhood of point , i.e., . If any data point is regarded as a vertex and any two data points within a neighborhood are connected through an edge, a graph is then constructed as , where denotes the set of vertices with and denotes the set of edges with . Consider the following optimization problem on the graph:

| (31) | ||||

| subject to |

Different from [7], we use instead of . The parameter along each edge , describing the weight of the penalty term of the difference between the two connected vertices, increases as decreases. The global parameter describes the trade-off between minimizing the individual loss function on each data point and agreeing with neighbors. When , is simply the solution to the optimization problem: , obtained locally at each vertex . When , the model reduces to a traditional regressor without spatial clustering.

Once the optimal solution is obtained, for any new node , the local regressor can be evaluated with the local parameter vector , estimated through the interpolation of the solution:

| (32) |

4.2 Two Problem Reformulations

To apply -block PCPM algorithm to solve the graph optimization problem (31), we first need to reformulate it into the block-separable form as in (22).

Similar to [7], for each pair of connected vertices along the edge , introducing a copy , we can rewrite the graph optimization problem (31) as

-

•

Problem Reformulation 1

(33) subject to

The reformulated problem can be decomposed into sub-problems on vertices and sub-problems along edges, using -block PCPM algorithm. One small issue is that the objective function of the edge sub-problem, , is not strongly convex.

To overcome this limitation, we propose an alternative way of rewriting (31). For each edge , introducing a slack variable , we can rewrite the graph optimization problem (31) as

-

•

Problem Reformulation 2

(34) subject to

The reformulated problem can also be decomposed into sub-problems on vertices and sub-problems along edges. However, in this way of rewriting (31), the objective function of each decomposed sub-problem enjoys the nice property of strong convexity. When applying -block PCPM algorithm, a linear convergence rate is expected for synchronous iteration scheme, and a sub-linear convergence rate is expected for an asynchronous scheme.

4.3 Housing Price Prediction

In this subsection, we present an application example of the graph optimization problem, where the housing price is predicted based on a set of features, including the number of bedrooms, the number of bathrooms, the number of square feet, and the latitude and longitude of each house. We use the same data set as [7], a list of 985 real estate transactions over a period of one week during May of 2008 in the Greater Sacramento area. All data is standardized with zero mean and unit variance, and all missing data is then set to zero. We randomly select a subset of 193 transactions as our test data set, and use the rest as our training data set.

The graph is constructed based on the latitude and longitude of each house. The rule of selecting neighbors is slightly different from [7]. For each house, we connect it with all the other houses within a distance of mile. If the number of connected houses is less then , we connect more nearest houses until the number of neighbors reaches . The resulting graph has vertices and edges. Thus, the graph optimization problem can be decomposed into sub-problems, using -block PCPM algorithm.

At each data point , the decision variable is . The predicted price for each house is:

where , and are the number of bedrooms, the number of bathrooms and the number of square feets for each house respectively. At each vertex , the objective function

is strongly convex, as well as the regularization function

where is the actual sales price for each house, and is a constant regularization parameter, fixed as .

4.4 Numerical Results of Synchronous N-block PCPM Algorithm

We first apply Algorithm 1 to solve the two reformulated problem (33) and (34), and compare the performance. The convergence results are shown in Figure 5.

Due to the strong convexity of the reformulated problem (34), the algorithm converges much faster than solving the reformulated problem (33).

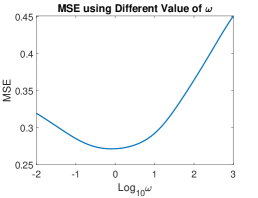

We also plot the mean square error (MSE) on the testing data set using various values of , shown in Figure 6.

When , a minimum MSE of can be obtained on the testing data set. We fixed for all the numerical experiments.

4.5 Numerical Results of Asynchronous N-block PCPM Algorithm

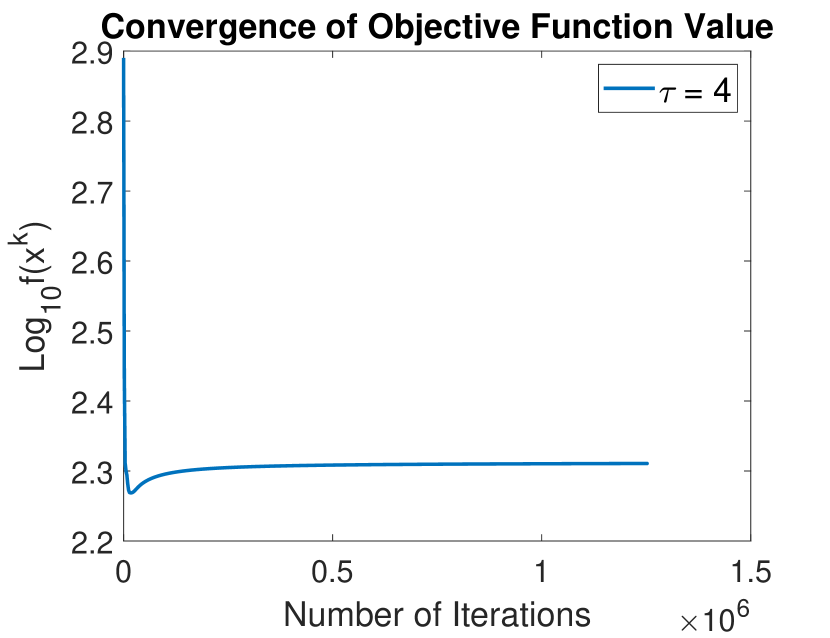

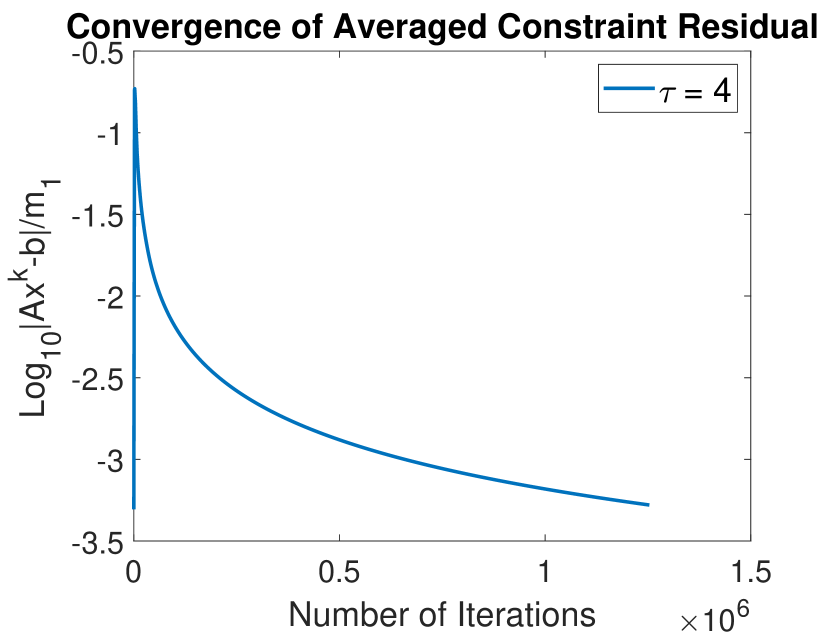

We apply Algorithm 2 and Algorithm 3 to solve the reformulated problem (34) with a maximum delay . The convergence results of are shown in Figure 7.

A sub-linear convergence rate is observed.

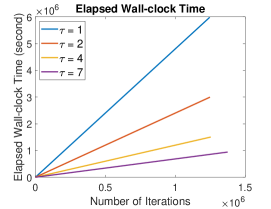

While implementing the algorithm as a sequential code, we simulate the elapsed wall-clock time on the main processor. As illustrated in Figure 4, the computation delay of the main processor is set as second, the computation delay of each worker processor for solving vertex sub-problem is set as second, the computation delay of each worker processor for solving edge sub-problem is set as second, and the communication delay of each worker processor is uniformly drawn from a range of to second. Under these settings, we simulate the elapsed wall-clock time on the main processor for the different values of maximum delay , shown in Figure 8.

We observe that, with a larger number of maximum delay, the number of iterations, used for the asynchronous algorithm to converge, increases but the simulated elapsed wall-clock time decreases, which implies a faster convergence with more short-time iterations.

5 Conclusion and Future Works

In this paper, we first proposed an -block PCPM algorithm to solve -block convex optimization problems with both linear and nonlinear constraints, with global convergence established. A linear convergence rate under the strong second-order conditions for optimality is observed in the numerical experiments. Next, for a starting point, we proposed an asynchronous -block PCPM algorithm to solve linearly constrained -block convex optimization problems. The numerical results demonstrate the sub-linear convergence rate under the bounded delay assumption, as well as the faster convergence with more short-time iterations than a synchronous iterative scheme.

However, the performance of real asynchronous implementation of -block PCPM algorithm is unknown, and thus in the future, more experiments (probably with much larger problem sizes) will be conducted on a multi-node computer cluster using MPI functions without blocking communication, such as MPI_Isend and MPI_Irecv. Also, the extension of the asynchronous -block PCPM algorithm to solve -block convex optimization problems with both linear and nonlinear constraints is worth to be explored.

References

- [1] J. Asaadi. A computational comparison of some non-linear programs. Mathematical Programming, 4(1):144–154, 1973.

- [2] Stephen Boyd, Neal Parikh, and Eric Chu. Distributed optimization and statistical learning via the alternating direction method of multipliers. Foundations and Trends® in Machine learning, 3(1):1–122, 2011.

- [3] Tsung-Hui Chang, Mingyi Hong, Wei-Cheng Liao, and Xiangfeng Wang. Asynchronous distributed ADMM for large-scale optimization—part i: Algorithm and convergence analysis. IEEE Transactions on Signal Processing, 64(12):3118–3130, 2016.

- [4] Tsung-Hui Chang, Wei-Cheng Liao, Mingyi Hong, and Xiangfeng Wang. Asynchronous distributed admm for large-scale optimization—part ii: Linear convergence analysis and numerical performance. IEEE Transactions on Signal Processing, 64(12):3131–3144, 2016.

- [5] Gong Chen and Marc Teboulle. A proximal-based decomposition method for convex minimization problems. Mathematical Programming, 64(1-3):81–101, 1994.

- [6] Wei Deng, Ming-Jun Lai, Zhimin Peng, and Wotao Yin. Parallel multi-block ADMM with o (1/k) convergence. Journal of Scientific Computing, 71(2):712–736, 2017.

- [7] David Hallac, Jure Leskovec, and Stephen Boyd. Network lasso: clustering and optimization in large graphs. In Proceedings of the 21th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 387–396. ACM, 2015.

- [8] R Tyrrell Rockafellar. Augmented Lagrangians and applications of the proximal point algorithm in convex programming. Mathematics of Operations Research, 1(2):97–116, 1976.

- [9] R Tyrrell Rockafellar. Monotone operators and the proximal point algorithm. SIAM Journal on Control and Optimization, 14(5):877–898, 1976.

- [10] R. Tyrrell Rockafellar. Convex Analysis. Princeton University Press, 2015.

- [11] Sartaj Sahni and George Vairaktarakis. The master-slave paradigm in parallel computer and industrial settings. Journal of Global Optimization, 9(3-4):357–377, 1996.

- [12] Huahua Wang, Arindam Banerjee, and Zhi-Quan Luo. Parallel direction method of multipliers. In Advances in Neural Information Processing Systems, pages 181–189, 2014.

- [13] Xiangfeng Wang, Mingyi Hong, Shiqian Ma, and Zhi-Quan Luo. Solving multiple-block separable convex minimization problems using two-block alternating direction method of multipliers. arXiv preprint arXiv:1308.5294, 2013.

- [14] Hao Yu and Michael J Neely. A simple parallel algorithm with an o(1/t) convergence rate for general convex programs. SIAM Journal on Optimization, 27(2):759–783, 2017.

Appendix A Proofs in Section 2.3

A.1 Proof of Proposition 2.3

We first prove the inequality (16). From the primal minimization step (10), we know that is the unique proximal minimization point of the Lagrangian function evaluated at the predictor variable: . Applying Lemma 2.1 with , and , we have:

| (35) | ||||

Since is a saddle point of the Lagrangian function , i.e., , we have:

| (36) |

Adding the above two inequalities yields the inequality (16) in Proposition 2.3.

To prove the second inequality, (17), in Proposition 2.3, we use a similar approach as above. By Lemma 2.2, we know that is the unique proximal minimization point of the function . Applying Lemma 2.1 with , and , we have:

| (37) |

By Lemma 2.2, we also know that is the unique proximal minimization point of the function . Applying Lemma 2.1 with , and , we have:

| (38) |

Adding the above two inequalities yields the inequality (17) in Proposition 2.3.

A.2 Proof of Theorem 2.4

By adding the two inequalities (16) and (17) in Proposition 2.3, we have:

| (39) |

Before we continue with the proof, we first show an extension of the Young’s inequality222Young’s inequality states that if and are two non-negative real numbers, and and are real numbers greater than 1 such that , then . on vector products that will play a key role in the following proof. Given any two vectors , we have that

where is a non-zero real number. Applying Young’s inequality on each summation term with , we obtain that

| (40) |

Applying (40) on each term yields

| (41) | ||||

and letting yields

| (42) | ||||

Applying (40) on each term yields

| (43) | ||||

and letting yields

| (44) | ||||

Substituting (42) and (44) into (39) yields

| (45) |

Since , we have:

| (46) |

It implies that for all :

| (47) |

It further implies that the sequence is monotonically decreasing and bounded below by ; hence the sequence must be convergent to a limit, denoted by :

| (48) |

Taking the limit on both sides of (46) yields:

| (49) | |||||

Additionally, (48) also implies that is a bounded sequence, and thus there exists a sub-sequence that converges to a limit point . We next show that the limit point is indeed a saddle point and is also the unique limit point of . Applying Lemma 2.1 with , and any , we have:

| (50) |

Taking the limits over an appropriate sub-sequence on both sides and using (49), we have:

| (51) |

Similarly, applying Lemma 2.1 with , and any , we have:

| (52) |

Taking the limits over an appropriate sub-sequence on both sides and using (49), we have:

| (53) |

Therefore, we show that is indeed a saddle point of the Lagrangian function . Then (48) implies that

| (54) |

Since we have already argued (after Eq. (49)) that there exists a bounded sequence of that converges to 0; that is, there exists such that

which then implies that . Therefore, we show that converges globally to a saddle point .

A.3 Proof of Theorem 2.5

Letting

| (55) | ||||

we first show that . By the primal minimization step (10), we have, for all :

| (56) |

where denotes the normal cone to the set at the point for all . Plugging

into the above expression, we have that, for all :

| (57) |

which implies

| (58) | ||||

Similarly, by the interpretation of in Lemma 2.2, we have:

| (59) | ||||

which imply

| (60) |

The first-order optimality conditions (58) and (60) together imply that

By (49), we have . Choose in integer such that, for all , , then by Assumption 2.4, we have:

| (61) |

The last inequality is due to (46), and . We further derive

| (62) | ||||

where and .

Appendix B Proofs in Section 3.2

B.1 Proof of Theorem 3.2

For all , we can equivalently write the update steps in Algorithm 2 and Algorithm 3 as

| (63) |

| (64) |

| (65) |

where is the last iteration when the main processor receives from the worker processor before iteration . For each worker processor , we denote as the last iteration when the main processor receives from the worker processor before iteration , and further denote as the last iteration when the main processor receives from the worker processor before iteration . We can rewrite the primal minimization step as

| (66) |

At each iteration , for any , applying Lemma 3.1 with , , and , we have:

| (67) |

At each iteration , for any , applying Lemma 3.1 with , , and , we have:

| (68) |

Summing (67) over all and (68) over all yields

| (69) |

The term (a) can be rewritten as:

| (70) |

The term (b) + (c) can be rewritten as:

| (71) |

The term (d) can be rewritten as:

| (72) |

We substitute (70), (71) and (72) into (69), and sum it over . Taking the average yields

| (73) |

The term (e) in (73) can be rewritten as:

| (74) | ||||

The term (f) in (73) can be bounded as:

| (75) |

where the first inequality is obtained by (40), and the second inequality is due to the fact that the term does not appear more than times for each iteration .

Similarly, the term (g) in (73) can be bounded as:

| (76) |

By substituting (74), (75) and (76) into (73) and denoting

for all , we have:

| (77) |

where the first inequality is due to the convexity of for all . By choosing and , which implies

we derive:

| (78) |

Let , and note that by the duality theory, we have:

| (79) |

Then, we further derive:

| (80) |

which implies

On the other hand, let , and note that:

| (81) | ||||

Then, we have:

| (82) |

where and .