sok short = SoK, long = systematization of knowledge \DeclareAcronymdefi short = DeFi, long = decentralized finance \DeclareAcronymamm short = AMM, long = automated market maker \DeclareAcronymcfmm short = CFMM, long = constant function market maker \DeclareAcronymdex short = DEX, long = decentralized exchange, short-plural-form = DEXs, long-plural-form = decentralized exchanges \DeclareAcronymlp short = LP, long = liquidity provider, short-plural-form = LPs, long-plural-form = liquidity providers \DeclareAcronympmm short = PMM, long = proactive market maker \DeclareAcronymdao short = DAO, long = Decentralized Autonomous Organization \DeclareAcronymnft short = NFT, long = non-fungible token \DeclareAcronymlmsr short = LMSR, long = logarithmic market scoring rule \DeclareAcronymido short = IDO, long = initial DEX offering \DeclareAcronymieo short = IEO, long = initial exchange offering \DeclareAcronymddos short = DDoS, long = distributed denial-of-service \DeclareAcronymdns short = DNS, long = domain name server \DeclareAcronymbgp short = BGP, long = border gateway protocol \DeclareAcronymmev short = MEV, long = miner extractable value \DeclareAcronymbdos short = BDoS, long = blockchain denial-of-service \DeclareAcronymzkp short = ZKP, long = zero-knowledge proof \DeclareAcronymmpc short = MPC, long = multiparty computation \DeclareAcronyml7ddos short = L7 DDoS, long = application-layer distributed denial-of-service \DeclareAcronymdlt short = DLT, long = distributed ledger technology \DeclareAcronymbsc short = BSC, long = Binance Smart Chain \DeclareAcronymdapp short = dApp, long = decentralized application \DeclareAcronympbs short = PBS, long = proposer/builder separation \DeclareAcronymnizk short = NIZK, long = non-interactive zero-knowledge \DeclareAcronymlbp short = LBP, long = Liquidity Bootstrapping Pool \DeclareAcronymcmm short = CMM, long = Custom Market Maker \DeclareAcronymevm short = EVM, long = Ethereum Virtual Machine

\acssok: Decentralized Exchanges (DEX) with Automated Market Maker (\acsamm) Protocols

Abstract.

As an integral part of the \acdefi ecosystem, \acfpdex with \acfamm protocols have gained massive traction with the recently revived interest in blockchain and \acdlt in general. Instead of matching the buy and sell sides, \acpamm employ a peer-to-pool method and determine asset price algorithmically through a so-called conservation function. To facilitate the improvement and development of \acamm-based \acpdex, we create the first systematization of knowledge in this area. We first establish a general \acamm framework describing the economics and formalizing the system’s state-space representation. We then employ our framework to systematically compare the top \acamm protocols’ mechanics, illustrating their conservation functions, as well as slippage and divergence loss functions. We further discuss security and privacy concerns, how they are enabled by \acamm-based \acpdex’ inherent properties, and explore mitigating solutions. Finally, we conduct a comprehensive literature review on related work covering both \acdefi and conventional market microstructure.

1. Introduction

With the revived interest in blockchain and cryptocurrency among both the general populace and institutional actors, the past year has witnessed a surge in crypto trading activity and accelerated development in the \acfdefi space. Among all the prominent \acdefi applications, \acfpdex with \acfamm protocols are in the ascendancy, with an aggregate value locked exceeding $100 billion at the time of writing (202, 2021a).

An \acamm-based \acdex bears attractive features such as decentralization, automation and continuous liquidity. With traditional order-book-based exchanges, the market price of an asset is determined by the last matched buy and sell orders, ultimately driven by the supply and demand of the asset. In contrast, on an \acamm-based \acdex, a liquidity pool acts as a single counterparty for each transaction, with a so-called conservation function that prices assets algorithmically by only allowing the price to move along predefined trajectories. \acpamm implement a peer-to-pool method, where \acplp contribute assets to liquidity pools while individual users exchange assets with a pool or pools containing the input and the output assets. Users obtain immediate liquidity without having to find an exchange counterparty, whereas \acplp profit from asset supply with exchange fees from users. Furthermore, by using a conservation function for price setting, \acpamm render moot the necessity of maintaining the state of an order book, which would be costly on a distributed ledger.

amm benefit both \acplp and exchange users with accessible liquidity provision and exchange, especially for illiquid assets. Despite the apparent advantages, \acpamm are often characterized by high slippage and divergence loss, two implicit economic risks imposed on the funds of exchange users and \acplp respectively. Moreover, \acamm-based \acdex are associated with myriads of security and privacy issues. Throughout the last three years, new protocols have been introduced to the market one after another with incremental improvements, attempting to tackle different issues which had been identified as weak spots in a previous version. On top of that, new use cases are being addressed, and new applications of \acamm iterations are proposed to the market. While innovative in certain aspects, the various \acamm protocols generally consist of the same set of composed mechanisms to allow for multiple functionalities of the system. As such, these systems are structurally similar, and their main differences lie in parameter choices and/or mechanism adaptations.

As one of the earliest \acdefi application categories, \acamm-based \acpdex also constitute the most fundamental and crucial building blocks of the \acdefi ecosystem. Their importance prompts the emergence of studies covering various aspects of \acamm-based \acpdex: economics (Bartoletti et al., 2021b), security (Zhou et al., 2021a; Yüksel et al., 2021; Zhou et al., 2021c), privacy (Baum et al., 2021b; Bowe et al., 2020), etc. While there has arisen a large number of surveys on general \acdefi (Sam M. Werner et al., 2022; Schär, 2021) as well as various \acdefi applications (Cousaert et al., 2022b; Bartoletti et al., 2021a), there is a dearth of literature that systematically studies and critically examines \acpdex with \acamm protocols in a comprehensive manner. To the best of our knowledge, this paper fills this gap as the first \acsok on \acamm-based \acdex with examples of deployed protocols. We contribute to the body of literature mainly by:

-

(1)

generalizing mechanisms and economics of \acamm-based \acpdex with a formalized state space modeling framework and a summary of key common properties;

-

(2)

illustrating instantiations of our framework by comparing major \acamm-based \acpdex with mathematical derivation and parameterized visualization on their conservation function, slippage and divergence loss functions;

-

(3)

positioning \acamm-based \acpdex within the broader taxonomy of \acdefi, and examining their relationships and interactions with other \acdefi protocols;

-

(4)

establishing a taxonomy of security and privacy issues concerning \acamm-based \acpdex, and exploring mitigation solutions;

-

(5)

conducting a state-of-the-art literature review summarizing current research priorities as well as existing output in \acamm-based \acpdex and related fields, and identifying potential directions for future research.

The rest of the paper is structured as follows: in §2 we lay out fundamental concepts and components of \acpamm; in §3 we formalize \acamm mechanisms with a state-space representation; in §4 we compare main protocols in terms of conservation function, exchange rates, slippage and impermanent loss; in §5 we address issues related to security and privacy of \acamm-based \acdex; in §6 we indicate several avenues of future \acamm research; in §7 we present related work; in §8 we conclude.

2. AMM Preliminaries

This section presents \acpamm-based \acpdex’ main components, including different actors and assets, as well as their generalized mechanism and economics.

2.1. Actors

2.1.1. \Acflp

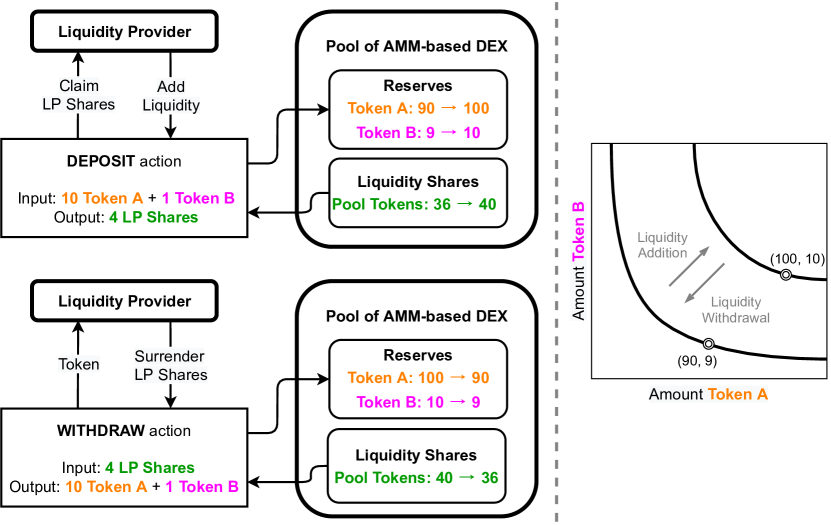

A liquidity pool can be deployed through a smart contract with some initial supply of crypto assets by the first \aclp. Other \acplp can subsequently increase the pool’s reserve by adding more of the type of assets that are contained in the pool. In turn, they receive pool shares proportionate to their liquidity contribution as a fraction of the entire pool (Evans, 2020). \acplp earn transaction fees paid by exchange users. While sometimes subject to a withdrawal penalty, \acplp can freely remove funds from the pool (Martinelli and Mushegian, 2019) by surrendering a corresponding amount of pool shares (Evans, 2020).

2.1.2. Exchange user (Trader)

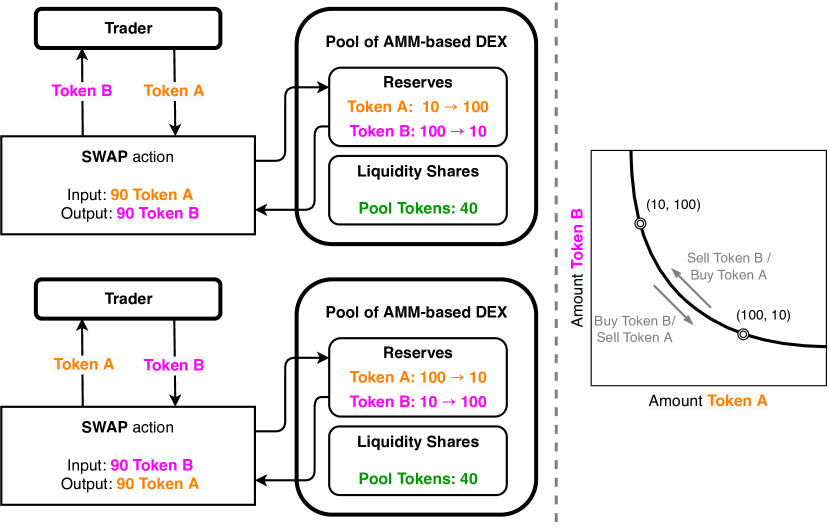

A trader submits an exchange order to a liquidity pool by specifying the input and output asset and either an input asset or output asset quantity; the smart contract automatically calculates the exchange rate based on the conservation function as well as the transaction fee and executes the exchange order accordingly.

2.1.3. Protocol foundation

A protocol foundation consists of protocol founders, designers, and developers responsible for architecting and improving the protocol. The development activities are often funded directly or indirectly through accrued earnings such that the foundation members are financially incentivized to build a user-friendly protocol that can attract high trading volume.

2.2. Assets

Several distinct types of assets are used in \acamm protocols for operations and governance; one asset may assume multiple roles.

2.2.1. Risk assets

Characterized by illiquidity, risk assets are the primary type of assets \acamm-based \acpdex are designed for. Like centralized exchanges, an \acamm-based \acdex can facilitate an \acieo to launch a new token through liquidity pool creation, a capital raising activity termed “\acido” that is particularly suitable for illiquid assets. To be eligible for an \acido, a risk asset sometimes needs to be whitelisted, and must be compatible with the protocol’s technical requirements (e.g. ERC20 (202, 2021b) for most \acpamm on Ethereum).

2.2.2. Base assets

Some protocols require a trading pair always to consist of a risk asset and a designated base asset. In the case of Bancor, every risk asset is paired with BNT, the protocol’s native token (Bancor, 2020b). Uniswap V1 requires every pool to be initiated with a risk asset paired with ETH. Many protocols, such as Balancer and Curve, can connect two or more risk assets directly in liquidity pools without a designated base asset.

2.2.3. Pool shares

Also known as “liquidity shares” and “\aclp shares”, pool shares represent ownership in the portfolio of assets within a pool, and are distributed to \acplp. Shares accrue trading fees proportionally and can be redeemed at any time to withdraw funds from the pool.

2.2.4. Protocol tokens

Protocol tokens are used to represent voting rights on protocol governance matters and are thus also termed “governance tokens” (see §2.4.1). Protocol tokens are typically valuable assets (Xu et al., 2022) that are tradeable outside of the \acamm and can incentivize participation when e.g. rewarded to \acplp proportionate to their liquidity supply. \acpamm compete with each other to attract funds and trading volume. To bootstrap an \acamm in the early phase with incentivized early pool establishment and trading, a feature called liquidity mining can be installed where the native protocol’s tokens are minted and issued to \acplp and/or exchange users.

2.3. Fundamental \acamm dynamics

2.3.1. Invariant properties

The functionality of an \acamm depends upon a conservation function which encodes a desired invariant property of the system. As an intuitive example, Uniswap’s constant product function determines trading dynamics between assets in the pool as it always conserves the product of value-weighted quantities of both assets in the protocol—each trade has to be made in a way such that the value removed in one asset equals the value added in the other asset. This weight-preserving characteristic is one desired invariant property supported by the design of Uniswap.

2.3.2. Mechanisms

An \acamm typically involves two types of interaction mechanism: asset swapping of assets and liquidity provision/withdrawal. Interaction mechanisms have to be specified in a way such that desired invariant properties are upheld; therefore the class of admissible mechanisms is restricted to the ones which respect the defined conservation function, if one is specified, or conserve the defined properties otherwise.

2.4. Fundamental \acamm economics

2.4.1. Rewards

amm protocols often run several reward schemes, including liquidity reward, staking reward, governance rights and security reward distributed to different actors to encourage participation and contribution.

Liquidity reward

lp are rewarded for supplying assets to a liquidity pool, as they have to bear the opportunity costs associated with funds being locked in the pool. \Acplp receive their share of trading fees paid by exchange users.

Staking reward

On top of the liquidity reward in the form of transaction income, \acplp are offered the possibility to stake pool shares or other tokens as part of an initial incentive program from a certain token protocol. The ultimate goal of the individual token protocols (see e.g. GIV (CryptoLocally, 2020) and TRIPS (De Giglio, 2021)) is to further encourage token holding, while simultaneously facilitating token liquidity on exchanges and product usage. These staking rewards are given by protocols other than the \acamm.

Governance right

An \acamm may encourage liquidity provision and/or swapping by rewarding participants governance rights in the form of protocol tokens (see §2.2.4). Currently, governance issues such as protocol treasury management (demosthenes.eth, 2021) are proposed and discussed mostly on off-chain governance portals such as snapshot (snapshot.org), Tally (tally.xyz) and Boardroom (boardroom.io), where protocol tokens are used as ballots (see §2.2.4) to vote on proposals.

Security reward

Just as every protocol built on top of an open, distributed network, \acamm-based \acpdex on Ethereum suffer from security vulnerabilities. Besides code auditing, a common practice that a protocol foundation adopts is to have the code vetted by a broader developer community and reward those who discover and/or fix bugs of the protocol with monetary prizes, commonly in fiat currencies, through a bounty program (Breidenbach et al., 2018).

2.4.2. Explicit costs

Interacting with \acamm protocols incurs various costs, including charges for some form of “value” created or “service” performed and fees for interacting with the blockchain network. \acamm participants need to anticipate three types of fees: liquidity withdrawal penalty, swap fee and gas fee.

Liquidity withdrawal penalty

Swap fee

Users interacting with the liquidity pool for token exchanges have to reimburse \acplp for the supply of assets and for the divergence loss (see §2.4.3). This compensation comes in the form of swap fees that are charged in every exchange trade and then distributed to liquidity pool shareholders. A small percentage of the swap fees may also go to the foundation of the \acamm to further develop the protocol (Xu and Xu, 2022).

Gas fee

Every interaction with the protocol is executed in the form of an on-chain transaction, and is thus subject to a gas fee applicable to all transactions on the underlying blockchain. In a decentralized network, validating nodes need to be compensated for their efforts, and transaction initiators must cover these operating costs. Interacting with more complex protocols will result in a higher gas fee due to the higher computational power needed for transaction verification.

2.4.3. Implicit costs

Two essential implicit costs native to \acamm-based \acpdex are slippage for exchange users and divergence loss for \acplp.

Slippage

Slippage is defined as the difference between the spot price and the realized price of a trade. Instead of matching buy and sell orders, \acpamm determine exchange rates on a continuous curve, and every trade will encounter slippage conditioned upon the trade size relative to the pool size and the exact design of the conservation function. The spot price approaches the realized price for infinitesimally small trades, but they deviate more for bigger trade sizes. This effect is amplified for smaller liquidity pools as every trade will significantly impact the relative quantities of assets in the pool, leading to higher slippage. Due to continuous slippage, trades on \acpamm must be set with some slippage tolerance to be executed, a feature that can be exploited to perform e.g. sandwich attacks (see §5.1.3).

Divergence loss

For \acplp, assets supplied to a protocol are still exposed to volatility risk, which comes into play in addition to the loss of time value of locked funds. A swap alters the asset composition of a pool, which automatically updates the asset prices implied by the conservation function of the pool (Eq. 3). This consequently changes the value of the entire pool. Compared to holding the assets outside of an \acamm pool, contributing the same amount of assets to the pool in return for pool shares can result in less value with price movement, an effect termed “divergence loss” or “impermanent loss” (see §4). This loss can be deemed “impermanent” because as asset price moves back and forth, the depreciation of the pool value continuously disappears and reappears and is only realized when assets are actually taken out of the pool. Well-devised \acpamm charge appropriate swap fees to ensure that \acplp are sufficiently compensated for the divergence loss (see §4.2.2). Despite the fact that “impermanent loss” is a more widely used term on the Internet, we adhere to the more accurate term “divergence loss” in a scientific context. In fact, for the majority of \acamm protocols, this “loss” only disappears when the current proportions of the pool assets equal exactly those at liquidity provision, which is rarely the case.

Since assets are bonded together in a pool, changes in prices of one asset affect all others in this pool. For an \acamm protocol that supports single-asset supply, this forces \acplp to be exposed to risk assets they have not been holding in the first place (see §3.3.1).

2.5. \acamm-based \acpdex within \acdefi

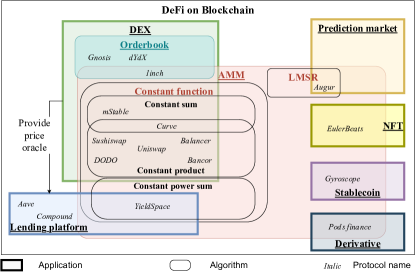

For brevity, we use “\acamm” or “\acdex” to refer to \acamm-based \acdex throughout the paper, unless indicated otherwise. Nevertheless, it is to be noted that the term “\acamm” emphasizes the algorithm of a protocol, whereas “\acdex” emphasizes the use case, or application, of a protocol. Within the context of blockchain-based \acdefi, there also exist orderbook-based \acpdex such as Gnosis and dYdX that do not rely on \acamm algorithms. Recently, \acdex aggregators (§4.3.8) such as 1inch have emerged which incorporate both limited order books and \acamm pools. On the other hand, \acamm algorithms are also not exclusively employed by \acpdex. \Acdefi applications such as lending platforms, \acpnft, stablecoins and derivatives all have protocols that make use of different \acamm algorithms.

amm can also assume various forms (see §7.2.2). Prediction markets for example commonly employs \aclmsr, whereas \accfmm is the primary underpinning for \acpdex. In particular, constant sum and constant product are the most representative forms of \accfmm, widely adopted by \acamm-based \acdex protocols. Fig. 1 illustrates \acamm-based \acdex within the broader taxonomy of \acdefi on blockchain.

The ensuing sections, §3 and §4, focus on \accfmm mechanisms which have been adopted by major \acpdex, with their exact formulas derived in Appendix A. §4.3 briefly presents other \acdefi applications with \acamm implementations.

3. Formalization of Mechanisms

Overall, the functionality of an \acamm can be generalized formally by a set of few mechanisms. These mechanisms define how users can interact with the protocol and what the response of the protocol will be given particular user actions.

3.1. State space representation

The functioning of any blockchain-based system can be modeled using state-space terminology. States and agents constitute the main system components; protocol activities are described as actions (Fig. 2); the evolution of the system over time is modeled with state transition functions. This can be generalized into a state transition function encoded in the protocol such that , where represents an action imposed on the system while and represent the current and future states of the system respectively.

The object of interest is the state of the liquidity pool which can be described with

| (1) |

where denotes the quantity of tokenk in the pool, the current spot price of tokenk, the conservation function invariant(s), and the collection of protocol hyperparameters. This formalization can encompass various \acamm designs.

The most critical design component of an \acamm is its conservation function which defines the relationship between different state variables and the invariant(s) . The conservation function is protocol-specific as each protocol seeks to prioritize a distinct feature and target particular functionalities (see §4).

The core of an \acamm system state is the quantity of each asset held in a liquidity pool. Their sums or products are typical candidates for invariants. Examples of a constant-sum market maker include mStable (Andersson, 2020). Uniswap (Uniswap, 2020) represents constant-product market makers, while Balancer (Martinelli and Mushegian, 2019) generalizes this idea to a geometric mean. The Curve (Egorov, 2019) conservation function is notably a combination of constant-sum and constant-product (see §4).

3.2. Generalized formulas

In this section, we generalize \acamm formulas necessary for demonstrating the interdependence between various \acamm invariants and state variables, as well as for computing slippage and divergence loss. Mathematical notations and their definitions can be found in Table 1.

Hyperparameter set is determined at pool creation and shall remain the same afterwards. While the value of hyperparameters might be changed through protocol governance activities, this does not and should not occur on a frequent basis.

Invariant , despite its name, refers to the pool variable that stays constant only with swap actions (see §3.3.2) but changes at liquidity provision and withdrawal. In contrast, trading moves the price of traded assets; specifically, it increases the price of the output asset relative to the input asset, reflecting a value appreciation of the output asset driven by demand (see §3.3.5). Liquidity provision and withdrawal, on the other hand, should not move the asset price (see §3.3.1). In particular, a pure liquidity provision and withdrawal activity requires a proportional change in reserves (Eq. 2).

| Notation | Definition | Applicable protocols |

| Preset hyperparameters, | ||

| Weight of asset reserve | Balancer | |

| Slippage controller | Uniswap V3, Curve, DODO | |

| Number of assets in a pool () | Curve | |

| Conservation function invariants, | ||

| Conservation function constant | Uniswap V2, Balancer, Curve | |

| Initial reserve of tokenk | Uniswap V3, DODO | |

| State variables | ||

| Quantity of tokenk in the pool | all | |

| Current spot price of tokenk | all | |

| Process variables | ||

| Input quantity added to tokeni reserve (removed if ) | all | |

| Output quantity removed from tokeno reserve (added if ) | all | |

| Token value change | all | |

| Functions | ||

| Conservation function | all | |

| Implied conservation function | all | |

| tokeno price in terms of tokeni | all | |

| Slippage | all | |

| Reserve value | all | |

| Divergence loss | Uniswap, Balancer, Curve | |

Formally, the state transition induced by pure liquidity change and asset swap can be expressed as follows.

| (2) |

| (3) |

3.2.1. Conservation function

An \acamm conservation function, also termed “bonding curve”, can be expressed explicitly as a relational function between \acamm invariant and reserve quantities :

| (4) |

A conservation function for each token pair, say —, must be concave, nonnegative and nondecreasing (Angeris et al., 2021a) (see also Fig. 3). For complex \acpamm such as Curve, it might be convenient to express the conservation function (Eq. 4) implicitly in order to derive exchange rates between two assets in a pool:

| (5) |

Equation 5 contains invariants , whose value is determined by the initial liquidity provision (liquidity pool creation); afterwards, given the change in reserve quantity of one asset, the reserve quantity of the other asset can be solved.

3.2.2. Spot exchange rate

The spot exchange rate between tokeni and tokeno can be calculated as the slope of the — curve (see examples in Fig. 3) using partial derivatives of the conservation function .

| (6) |

Note that when .

3.2.3. Swap amount

The amount of tokeno received (spent when ) given amount of tokeni spent (received when ) can be calculated following the steps below.

Note that and . Their lower bound corresponds to the case when the received asset is depleted from the pool, i.e. its new reserve becomes 0 (see also Eq. 7 below). With common \acamm protocols, theoretically often do not have a upper bound: if the reserve quantity is 1 unit, a trader can still sell 2 or more units into the pool, but mostly accompanied with a high slippage (see Fig. 4 in the next section).

Update reserve quantities

Input quantity is simply added to the existing reserve of tokeni; the reserve quantity of any token other than tokeni or tokeno stays the same:

| (7) | ||||

| (8) |

Compute new reserve quantity of tokeno

The new reserve quantity of all tokens except for tokeno is known from the previous step. One can thus solve , the unknown quantity of tokeno, by plugging it in the conservation function:

| (9) |

Apparently, can be expressed as a function of the original reserve composition , input quantity , namely,

| (10) |

Compute swapped quantity

The quantity of tokeno swapped is simply the difference between the old and new reserve quantities:

| (11) |

3.2.4. Slippage

Slippage measures the deviation between effective exchange rate and the pre-swap spot exchange rate , expressed as:

| (12) |

3.2.5. Divergence loss

Divergence loss describes the loss in value of all reserves in the pool compared to holding the reserves outside of the pool, after a price change of an asset (see §2.4.3). Based on the formulas for spot price and swap quantity established above, the divergence loss can generally be computed following the steps described below. In the valuation, we assign tokeni as the denominating currency for all valuations. While the method to be presented can be used for multiple token price changes through iterations, we only demonstrate the case where only the value of tokeno increases by , while all other tokens’ value stay the same. Tokeni is the numéraire. Designating one of the tokens in the pool as a numéraire can also be found in DeFi simulation papers such as (Angeris et al., 2021a).

Calculate the original pool value

The value of the pool denominated in tokeni can be calculated as the sum of the value of all token reserves in the pool, each equal to the reserve quantity multiplied by the exchange rate with tokeni:

| (13) |

Calculate the reserve value if held outside of the pool

If all the asset reserves are held outside of the pool, then a change of in tokeno’s value would result in a change of in tokeno reserve’s value:

Obtain re-balanced reserve quantities

Exchange users and arbitrageurs constantly re-balance the pool through trading in relatively “cheap”, depreciating tokens for relatively “expensive”, appreciating ones. As such, asset value movements are reflected in exchange rate changes implied by the dynamic pool composition. Therefore, the exchange rate between tokeno and each other tokenj () implied by new reserve quantities , compared to that by the original quantities , can be expressed with Equation set 14. At the same time, the equation for the conservation function must stand (Eq. 15).

| (14) | ||||

| (15) |

A total number of -equations ( with Equation set 14, plus 1 with Eq. 15) would suffice to solve unknown variables , each of which can be expressed as a function of and :

| (16) |

Calculate the new pool value

The new value of the pool can be calculated by summing the products of the new reserve quantity multiplied by the new price (denominated by tokeni) of each token in the pool:

| (17) |

Calculate the divergence loss

Divergence loss can be expressed as a function of , the change in value of an asset in the pool:

| (18) |

| Protocol | Value locked ($bn) | Trade volume ($bn) | Market (%) | Governance token | Governance token holders | Fully diluted value ($bn) |

| Uniswap | 6.15 | 11.4 | 66.7 | UNI | 269,923 | 21.1 |

| Sushiswap | 3.92 | 2.9 | 14.2 | SUSHI | 71,007 | 2.4 |

| Curve | 11.64 | 1.8 | 6.4 | CRV | 44,654 | 4.0 |

| Bancor | 1.37 | 0.4 | 2.5 | BNT | 38,124 | 0.8 |

| Balancer | 1.74 | 0.5 | 2.2 | BAL | 37,613 | 1.0 |

| DODO | 0.07 | 0.4 | 2.1 | DODO | 11,330 | 1.2 |

3.3. Key common properties of \acamm-based \acpdex

In this section, we summarize key common properties featured in \acamm-based \acpdex. We also clarify that protocol-specific intricacies and real-life implementations may result in “violations” of certain properties listed below.

3.3.1. Zero-impact liquidity change

The price of assets in an \acamm pool stays constant for pure, balanced liquidity provision and withdrawal activities. This feature describes when an \aclp provides or withdraw liquidity, usually by linearly scaling up or down the existing reserves in the pool, no price impact shall occur (see Eq. 2).

The asset spot price can remain the same only when assets are added to or removed from a pool proportionate to the current reserve ratio (). In any other case, a change of quantities in any pool would result in changes in relative prices of assets. To manage to uphold the invariances a disproportionate addition or removal can be treated as a combination of two actions: proportionate reserve change plus asset swap (see e.g. §4.1.3).

3.3.2. Path-deterministic swap

By its algorithm-based pricing nature, how a given swap transitions an \acamm pool’s reserve balance can be deterministically computed.

In an idealized, frictionless market, an \acamm pool’s conservation function (see §3.2.1) stipulates that the pool’s invariant stays constant for pure swapping activities (see Eq. 3). Figuratively speaking, absent additional liquidity provision/withdrawal, the coordinates of the reserve quantities in a liquidity pool would always slide up and down along the bonding curve (see 2(b)) through swaps. In reality, swap fees (see §2.4.2), when kept within a pool, cause invariant to become variant through trading. Also, as float numbers are not yet fully supported by Solidity (Ethereum, 2020)—the language for Ethereum smart contracts, \acamm protocols typically recalculate invariant after each trade to avoid the accumulation of rounding errors.

3.3.3. Output-boundedness

With an output-bounded \acamm, there is always a sufficient quantity of output tokens for a swap, i.e. a user can never deplete one side of the pool reserve. An \acamm with this feature usually constructs its bonding curve such that, when one reserve token is close to depletion (approaching 0), its price—denominated in the other reserve token of the pool—becomes astronomically high (approaching infinity) (Bartoletti et al., 2021b).

Output-boundedness usually applies to continuous \acpamm. Hybrid \acpamm such as Uniswap V3 which incorporates bounded bonding curves, assimilating an order-book-like mechanism (Chitra et al., 2021), naturally do not carry this property.

3.3.4. Liquidity sensitivity

3.3.5. Demand sensitivity

An \acamm is demand-sensitive when the average swap price (i.e. the effective exchange rate ) increases as the swap size (input quantity ) increases. Intuitively, this suggests that as with the increment of the demand in output token, its price denominated input token will be driven up.

A constant product \acamm is both liquidity-sensitive and demand-sensitive, whereas, strickly speaking, a constant sum one is neither.

4. Comparison of AMM protocols

amm-based \acpdex are home to billions of dollars’ worth of on-chain liquidity. Table 2 lists major \acamm protocols, their respective value locked, as well as some other general metrics. Uniswap is undeniably the biggest \acamm measured by trade volume and the number of governance token holders, although it is remarkable that Curve has more value locked within the protocol. The number of governance token holders of smaller protocols as Bancor and Balancer is relatively high compared to CRV token holders, as they do approximately a third of the volume but have only slightly fewer governance token holders.

4.1. Major \acamm protocols

This section focuses on the four most representative \acpamm: Uniswap (including V2 and V3), Balancer, Curve, and DODO. These protocols were selected based on their market share (hagaetc, 2021) on the Ethereum blockchain and the representativeness in their overall mechanism.

We describe the liquidity pool structures of those protocols in the main text. We also derive the conservation function, slippage, as well as divergence loss of those protocols. A summary of formulas can be found in Table 4. We refer our readers to Appendix A for a detailed explanation and derivation of those formulas. The protocols’ conservation function, slippage, as well as divergence loss under different hyperparameter values are plotted in Fig. 3, 4 and 5, respectively. We always use token1 as price or value unit; namely, token1 is the assumed numéraire.

4.1.1. Uniswap V2

The Uniswap protocol prescribes that a liquidity pool always consists of one pair of assets. Uniswap V2 implements a conservation function with a constant-product invariant (see §A.1.1), implying that the reserves of the two assets in the same pool always have equal value.

Liquidity provision or withdrawal at Uniswap V2 must be balanced and makes no price impact (§3.3.1). Swaps with Uniswap V2 are path-deterministic (§3.3.2); however, due to the positive swap fee charged and then immediately deposited back into the pool (Uniswap, 2022), a trading action can be decomposed into asset swap and liquidity provision. This action is, therefore, no longer a pure asset swap and would thus move the value of (Senchenko, 2020). Uniswap V2 carries the properties of output-boundedness (§3.3.3), liquidity sensitivity (§3.3.4) and demand sensitivity (§3.3.5).

4.1.2. Uniswap V3

Uniswap V3 enhances Uniswap V2 by allowing liquidity provision to be concentrated on a fraction of the bonding curve (Adams et al., 2021) (see §A.2.1), thus virtually amplifying the conservation function invariant and reducing the slippage.

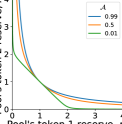

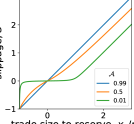

The protocol’s slippage controller determines the degree of liquidity concentration. Specifically, signifies how concentrated the liquidity should be provided around the initial spot price: when , the covered price range approaches , and the LP’s individual conservation function approximates a Uniswap V2 one (approximated with in 3(a)); on the other extreme, when , the liquidity only supports swaps close to the initial exchange rate, and the conservation function approximates a constant-sum one (3(a)).

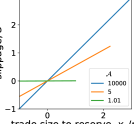

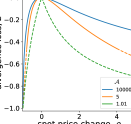

Like V2, liquidity provision or withdrawal at Uniswap V3 must respect the existing ratio between two reserve assets, which results in zero price impact (§3.3.1). Different from V2 where fees are retained in the pool, Uniswap V3 deducts swap fees as a fraction of the input asset and credit that amount to \aclp’s fee revenue balance; hence, swaps with V3 are path deterministic with no impact on the bonding curve invariants (§3.3.2). By design, Uniswap V3 is not output-bounded (§3.3.3)—a sufficiently large swap can deplete one reserve asset and leave the liquidity pool only with the other one in (see 3(a)). Uniswap V3 also features liquidity sensitivity (§3.3.4). Thanks to its liquidity concentrating feature, Uniswap V3 is less demand sensitive (§3.3.5) than V2—a swap with a fixed input quantity would experience a lower slippage at Uniswap V3 than at V2 with the same level of pre-swap reserves (see 4(a)).

4.1.3. Balancer

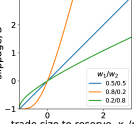

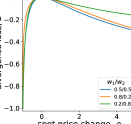

The Balancer protocol allows each liquidity pool to have more than two assets (Martinelli and Mushegian, 2019). Each asset reserve is assigned a weight at pool creation, where . Weights are pool hyperparameters and do not change with either liquidity provision/withdrawal or asset swap. The weight of an asset reserve represents the value of the reserve as a fraction of the pool value. Balancer can also be deemed a generalization of Uniswap; the latter is a special case of the former with for asset-pair pools (3(b)).

Balancer allows both balanced liquidity provision/withdrawal as well as single-asset liquidity change (Martinelli and Mushegian, 2019); the former does not cause price impact, whereas the latter does (§3.3.1). When only one asset is provided instead of e.g. eight, the protocol would first execute seven trades to swap this one asset to arrive at a vector of quantities in current proportions and next add this vector to the liquidity pool. Consequently, this sequence of actions is no longer a pure liquidity provision/withdrawal and would thus move the asset spot price. As Uniswap V2, swap fees with Balancer are also retained in the pool (Balancer, 2022), leading to an update of the bonding curve after each swap (§3.3.2). Balancer also features output-boundededness (§3.3.3), liquidity sensitivity (§3.3.4) and demand sensitivity (§3.3.5).

4.1.4. Curve

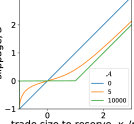

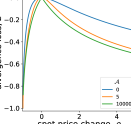

With the Curve protocol, formerly StableSwap (Egorov, 2019), a liquidity pool typically consists of two or more assets with the same peg, for example, USDC and DAI, or wBTC and renBTC. Curve approximates Uniswap V2 when its constant-sum component (§A.4.1) has a near-0 weight, i.e. (3(c)).

Like Balancer, Curve allows both proportionate and disproportionate liquidity change to the pool, depending on which the \aclp’s action can induce either zero or some price impact (§3.3.1). As Uniswap V2 and Balancer, Curve updates its invariant after each trade to account for swap fees retained in the pool (§3.3.2). Curve is also output boundeded (§3.3.3), liquidity sensitive (§3.3.4) and demand sensitive (§3.3.5).

4.1.5. DODO

DODO supports customized pools (DODO, 2021b) where a pool creator provides reserves on both sides of the trading pair with arbitrary quantities, which determines the pool’s initial equilibrium state. Unlike conventional \acpamm such as Uniswap, Balancer and Curve where the exchange rate between two assets in a pool is derived purely from the conservation function, DODO does it the other way around. Resorting to external market data as a major determinant of the exchange rate, DODO has its conservation function (see §A.5.2) derived from its exchange rate formula (see §A.5.1).

Specifically, the pool exhibits an arbitrage opportunity—namely a gap between the price offered by the pool and that from the external market—as soon as the reserve ratio between the two assets in the pool deviates from its equilibrium state. Price alignment by arbitrageurs always pulls the reserve ratio back to its equilibrium state set by the \aclp, thus eliminating any divergence loss. Due to this feature, DODO differentiates itself from other \acpamm and terms their pricing algorithm as “\aclpmm”, or \acspmm.

In DODO, a higher slippage controller results in a greater slippage around the market price—i.e. the equilibrium price. Specifically, when , the DODO bonding curve resembles Uniswap V2 (approximated with in 3(d)); and with a high slippage around the market price (4(d)), the pool exhibits a strong tendency to fall back to the equilibrium state. When , the DODO bonding curve resembles a constant sum one (approximated with in 3(d)); and with a near-flat slippage (4(d)), the algorithm’s force to pull the reserve ratio back to equilibrium is at its weakest due to little arbitrage profitability exhibited.

As with Balancer and Curve, \acplp can provide/withdraw both balanced and unbalanced reserves to a DODO pool (§3.3.1). Similar to Uniswap V3, swap fees with DODO are recorded outside of the liquidity pool. DODO’s bonding curve is thus redrawn not after each swap, but after each price change reported by the oracle (§3.3.2). DODO is also output boundeded (§3.3.3). Although relying on external price feeds for the construction of its conservation function, DODO is still liquidity sensitive (§3.3.4) and demand sensitivite (§3.3.5) since the size of a trade relative to the pool depth determines the magnitude of slippage and the price movement local to the pool.

4.1.6. Other \acamm-based \acdexs

Sushiswap

Sushiswap is a fork of Uniswap V2 (see §5.1.3). Though the two mainly differ in governance token structure and user experience, Sushiswap share the same conservation function, slippage and divergence loss functions as Uniswap.

Kyber Network

Currently in its 3.0 version, the \acdex uses a Dynamic Market Maker (DMM) mechanism, which allows for dynamic conservation functions based on amplified balances, called “virtual balances” (Krishnamachari et al., 2021). This is supposed to result in higher capital efficiency for \acplp and better slippage for traders. Also, the trading fees are adjusted automatically to market conditions. A volatile market causes increased fees, to offset impermanent loss for \acplp.

Bancor

While Bancor’s white paper (Hertzog et al., 2018) gives the impression that a different conservation function is applied, a closer inspection of their transaction history and smart contract leads to the conclusion that Bancor is using the same formula as Balancer (confirmed by a developer in the Bancor Discord community). As the majority of Bancor pools consist of two assets, one of which is usually BNT, with the reserve weights of 50%–50%, Bancor’s swap mechanism is equivalent to Uniswap. Bancor V2.1 now allows single-sided asset exposure, and provides divergence loss insurance (Bancor, 2020a) (see §4.2.3).

Summary

Each \acamm has its quirks. Uniswap V2 implements an rudimentary bonding curve that achieves a low gas fee; Uniswap V3 allows for concentrated liquidity provision which improves capital efficiency; Balancer supports more than 2 assets in a pool; Curve is suitable for swapping assets with the same peg; DODO proactively reduces divergence loss by leveraging external price feeds. As discussed in §4.1, common \acpamm can be predominantly seen as a generalization, or an extension, of the most fundamental constant-product protocol that is applied by Uniswap V2.

When hyperparameters such as reserve weights and slippage controller are assigned with certain values, various \acpamm can be reduced to the basic form equivalent to Uniswap V2 (illustrated with blue curves in Fig. 3, 4 and 5). In fact, the majority of top \acpamm—including Sushiswap, PancakeSwap, VVS Finance, Quickswap and BiSwap—are a simple clone of the Uniswap protocol (DefiLlama, 2022) with some adjustment in the fee and reward structure.

When deciding on a new conservation function, \acamm developers and designers must consider the trade-off between different features and properties (§3.3). For example, seeking liquidity insensitivity (§3.3.4) and demand insensitivity (§3.3.4) for low slippage leads to higher divergence loss (see §2.4.3): given a range of price movement, traders would be able to swap out an asset with a larger quantity, whereas \acplp would suffer a bigger divergence loss. In the extreme case like Uniswap V3, the trader-favoring feature sacrifices the output-bounded property (§3.3.3), which is to the detriment of \acplp, leaving them completely “rekt”111\Acdefi jargon for “wrecked”, in this context, meaning exposed to a single, undiversified asset has has depreciated in value. in the case of significant price swings. Seemingly capable of achieving both low slippage and zero divergence loss at equilibrium by setting its low, DODO appears to be an exception. Nevertheless, it is to be noted that with a small , DODO’s \acpmm algorithm is less effective in restoring the pool to its equilibrium state (see §4.1.5), thus still exposing \acplp to divergence loss risks in non-equilibrated states.

In a similar vein, users interacting with an \acamm-based \acdex, including both traders and \acplp, form a zero-sum game. They should understand the protocol design, and beware of embedded hidden costs such as slippage and divergence loss, which impose economic risks on their funds.

4.2. Additional features of \acamm-based \acpdex

4.2.1. Time component

A time component refers to the ability to change traditionally fixed hyperparameters over time. Balancer V1 and V2 implement this (Table 3), by allowing liquidity pool creators to set a scheme that changes the weights of two pool assets over time. This implementation is called a Liquidity Bootstrapping Pool (see §4.3.4).

4.2.2. Dynamic swap fee

Dynamic fees are introduced by Kyber 3.0 to reduce the impact of divergence loss for \acplp. The idea is to increase swap fees in high-volume markets and reduce them in low-volume markets. This should result in more protection against divergence loss, as during periods of sharp token price movements during a high-volume market, \acplp absorb more fees. In low-volume and -volatility markets, trading is encouraged by lowering the fees.

4.2.3. Divergence loss insurance

Popularized by Bancor V2.1, \acplp are insured against divergence loss after 100 days in the pool, with a 30-day cliff at the beginning. Bancor achieves this by using an elastic BNT supply that allows the protocol to co-invest in pools and pay for the cost of impermanent loss with swap fees from its co-investments (Bancor Network, 2021). This insurance policy is earned over time, 1% each day that liquidity is staked in the pool.

| \acamm | \acamm add-ons | ||||||||||

| \ac dex | Pool structure | CP | CS | OP | CC | T | Divergence loss compensation | Chain | Mainnet launch | ||

| Uniswap V1 | (Adams, 2018) | asset-pair | ● | ○ | ○ | ○ | ○ | — | Ethereum | 11/2018 | |

| Uniswap V2 | (Adams et al., 2020) | asset-pair | ● | ○ | ○ | ○ | ○ | — | Ethereum | 05/2020 | |

| Uniswap V3 | (Adams et al., 2021) | asset-pair | ● | ○ | ○ | ● | ○ | — | Ethereum | 05/2021 | |

| Balancer V1 | (Martinelli and Mushegian, 2019) | multi-asset | ● | ○ | ○ | ○ | ● | — | Ethereum | 03/2020 | |

| Balancer V2 | (Martinelli, 2021) | multi-asset | ● | ○ | ○ | ○ | ● | — | Ethereum | — | |

| Curve | (Egorov, 2019) | multi-asset | ● | ● | ○ | ○ | ○ | — | Ethereum | 01/2020 | |

| DODO | (DODO Team, 2020) | various | ● | ○ | ● | ○ | ○ | — | Ethereum, BNB Chain | 09/2020 | |

| Bancor V1 | (Hertzog et al., 2018) | asset-pair | ● | ○ | ○ | ○ | ○ | — | Ethereum, EOS | 06/2017 | |

| Bancor V2 | (Bancor, 2020a) | asset-pair | ● | ○ | ● | ○ | ○ | — | Ethereum, EOS | 04/2020 | |

| Bancor V2.1 | (Bancor, 2020b) | asset-pair | ● | ○ | ○ | ○ | ○ | Divergence loss insurance | Ethereum, EOS | 10/2020 | |

| SushiSwap | (Sushiswap, 2020) | asset-pair | ● | ○ | ○ | ○ | ○ | — | Ethereum | 08/2020 | |

| Mooniswap | (Bukov and Melnik, 2020) | asset-pair | ● | ○ | ○ | ○ | ● | — | Ethereum | 08/2020 | |

| mStable | (Andersson, 2020) | asset-pair | ○ | ● | ○ | ○ | ○ | — | Ethereum | 07/2020 | |

| Kyber 3.0 | (Kyber Network, 2021) | multi-asset | ● | ○ | ○ | ● | ○ | Dynamic swap fee | Ethereum, Tezos | 03/2021 | |

| Saber | (Saber, 2021) | multi-asset | ● | ● | ○ | ○ | ○ | — | Solana | 06/2021 | |

| HydraDX | (HydraDX, 2021) | multi-asset | ● | ○ | ● | ● | ○ | — | Polkadot | — | |

| Uranium Finance | (Uranium.finance, 2021) | asset-pair | ● | ○ | ○ | ○ | ○ | — | BNB Chain | 05/2021 | |

| QuickSwap | (QuickSwap Official, 2020) | asset-pair | ● | ○ | ○ | ○ | ○ | — | Polygon | 10/2020 | |

| Burgerswap | (Burgerswap, 2020) | asset-pair | ● | ○ | ○ | ○ | ○ | — | BNB Chain | 10/2020 | |

4.3. Other \acdefi protocols with \acamm implementations

amm form the basis of other \acdefi applications (see Fig. 1) that implement existing or invent newly designed bonding curves, facilitating the functionalities of these implementing protocols. In this section, we present a few examples of projects that use \acamm designs under the hood.

4.3.1. Gyroscope

Gyroscope (Gyroscope Finance, 2021b) is a stablecoin backed by a reserve portfolio that tries to diversify \acdefi tail risks. Gyro Dollars can be minted for a price near $1 and can be redeemed for around $1 in reserve assets, as determined through a new \acamm design that balances risk in the system. Gyroscope includes a Primary-market \acamm (P-\acamm), through which Gyro Dollars are minted and redeemed, and a Secondary-market \acamm (S-\acamm) for Gyro Dollar trading. Similar to Uniswap V3 where a price range constraint is imposed, the P-\acamm yields a mint quote and a redeem quote that serves as a price range constraint for the S-\acamm to decide upon concentrated liquidity ranges (Gyroscope Finance, 2021a).

4.3.2. EulerBeats

EulerBeats (EulerBeats, 2021) is a protocol that issues limited edition sets of algorithmically generated art and music, based on the Euler number and Euler totient function. The project uses self-designed bonding curves to calculate burn prices of music/art prints, depending on the existing supply. The project thus implements a form of \acamm to mint and burn NFTs price-efficiently.

4.3.3. Pods Finance

Pods (Pods Finance, 2021) is a decentralized non-custodial options protocol that allows users to create calls and or puts and trade them in the Options \acamm. Users can participate as sellers and buy puts and calls in a liquidity pool or act as \acplp in such a pool. The specific \acamm is one-sided and built to facilitate an initially illiquid options market and price option algorithmically using the Black-Scholes pricing model. Users can effectively earn fees by providing liquidity, even if the options are out-of-the-money, reducing the cost of hedging with options.

4.3.4. Balancer \acflbp

lbp are pools where controllers can change the parameters of the pool in controlled ways, unlike immutable pools described in §4. The idea of an \aclbp is to launch a token fairly, by setting up a two-token pool with a project token and a collateral token. The weights are initially set heavily in favor of the project token, then gradually “flip” to favor the collateral coin by the end of the sale. The sale can be calibrated to keep the price more or less steady (maximizing revenue) or declining to the desired minimum (e.g., the initial offering price) (Balancer, 2021).

4.3.5. YieldSpace

The YieldSpace paper (Niemerg et al., 2020) introduces an automated liquidity provision for fixed yield tokens. A formula called the “constant power sum invariant” incorporates time to maturity as input and ensures that the liquidity provision offers a constant interest rate—rather than price—for a given ratio of its reserves. fyTokens are synthetic tokens that are redeemable for a target asset after a fixed maturity date (Robinson and Niemerg, 2020). The price of a fyToken floats freely before maturity, and that price implies a particular interest rate for borrowing or lending that asset until the fyToken’s maturity. Standard \acamm protocols as discussed in §4 are capital-inefficient. By introducing the concept of a constant power sum formula, the writers want to build a liquidity provision formula that works in “yield space” instead of “price space”.

4.3.6. Notional Finance

Notional Finance (Notional Finance, 2021) is a protocol that facilitates fixed-rate, fixed-term crypto-asset lending and borrowing. Fixed interest rates provide certainty and minimize risk for market participants, making this an attractive protocol among volatile asset prices and yields in DeFi. Each liquidity pool in Notional refers to a maturity, holding fCash tokens attached to that date. For example, fDai tokens represent a fixed amount of DAI at a specific future date. The shape of the Notional \acamm follows a logit curve, to prevent high slippage in normal trading conditions. Three variables parameterize the AMM: the scalar, the anchor, and the liquidity fee (Notional Finance, 2020). The first and second mentioned allowing for variation in the steepness of the curve and its position in a xy-plane, respectively. By converting the scalar and liquidity fee to a function of time to maturity, fees are not increasingly punitive when approaching maturity.

4.3.7. Gnosis \accmm

The Gnosis \accmm (Gnosis, 2020) allows users to set multiple limit orders at custom price brackets and passively provide liquidity on the Gnosis Protocol. The mechanism used is similar to the Uniswap V3 structure, although it allows for even more possibilities to market makers by allowing them to choose price upper and lower limits and a number of brackets within that price range. Uniswap V3 allows \acplp to solely choose the upper and lower limits. Because users deposit funds to the assets at different price levels specifically, the protocol behaves more like a central limit order book than an \acamm pool.

4.3.8. \acdex aggregators

dex aggregators are a type of emerging \acdefi protocols that connect to various other \acpdex and can also have their own liquidity pools (Ushida and Angel, 2021). They offer traders superior swap rates through routing across liquidity pools from different \acpdex with one single user interface (Raikwar and Gligoroski, 2021). 1inch and Paraswap are two major \acpdex aggregators for \acevm-compatible chains that incorporate \acpamm such as Uniswap and Curve. Rango (Rango, 2022) is an example of cross-chain \acpdex aggregators incorporate \acpamm, \acdex aggregators and bridges to facilitate token swaps across both \acevm and non-\acevm blockchains.

4.4. \acpamm on Layer 2 solutions

The growth and success of \acdefi on Ethereum have put a strain on the Ethereum network’s ability to process transactions, leading to increasing gas (YCharts, 2021). As the Ethereum Network becomes busier, user experience decreases because of increasing gas prices and decreasing transaction speed. Users aim to outbid each other by increasing the gas prices. Also, transaction speed decreases, which results in poor user experience for certain types of \acpdapp. And as the network gets busier, gas prices increase as transaction senders aim to outbid each other. In an attempt to prevent these consequences, “layer 2 solutions” (L2) are being developed. These solutions handle transactions outside of the Ethereum network, but still rely on the decentralized security model of the mainnet (ethereum.org, 2021a). Examples of layer 2 technologies include Plasma, Sidechains, Optimistic Rollups and ZK-Rollups. For a more comprehensive reading on this topic, we direct the reader to (ethereum.org, 2021b). Examples of Ethereum layer 2 solutions are Polygon (Polygon, 2021), Arbitrum (Arbitrum, 2021), Optimism (Optimism, 2021) and Starknet (StarkWare Industries Ltd., 2021).

Characteristics of layer 2 solutions, such scaling and security, have been well-documented across different sources (Gudgeon et al., 2020a) (Hafid et al., 2020) (Jourenko et al., 2019) and are out of scope for this \acsok. The advantages and disadvantages of transacting on layer 2 solutions are not specifically related to \acpamm, but to all protocols on these technologies. Therefore, we focus on the security issues and user experience of interacting with \acpamm on layer 2.

Daian et al. (Daian et al., 2020) note that abstraction achieved by layer 2 exchange systems is not sufficient to prevent sandwich attacks and a report of Delphi Digital (Delphi Digital, 2020) concludes that there is still front-running risk when a protocol wants to aggregate liquidity across layer 1 and layer 2 pools. The front-running and sandwich attacks does not seem to be solved by layer 2 solutions. (Konstantopoulos, 2021) proposes a simple solution for front-running attacks on Optimistic Rollups technology.

One of the most important advantages of deploying a protocol on layer 2 is the reduction in gas fees. This dramatically enhances the user experience, and opens up ways to introduce new forms of decentralized exchanges. One example is ZKSwap (ZKSwap, 2021), allowing users to trade with zero gas fees. Sushiswap and Curve have deployed their contracts on Polygon and QuickSwap is a fork of Uniswap on that same layer 2 solution (Nasdaq, 2021). As a result, users are now able to use the same products on layer 2 solutions, with drastically reduces costs and allows faster transactions. In 2021, dYdX launched its order book-based \acpdex on StarkEx (dYdX, 2021).

In sum, \acpamm on layer 2 solutions result in faster transactions and a reduction of costs due to zero or decreased gas costs, ultimately enhancing the user experience.

5. Security and privacy concerns

The previous sections focus on implicit economic costs—including slippage and divergence loss—imposed on the funds of users interacting with \acamm-based \acpdex. Besides those risks, security and privacy matters are also to be taken into account when using \acamm-based \acpdex.

In particular, as a complex, distributed system with a variety of software and hardware components interacting with each other, \acamm-based \acpdex are prone to exhibit attack interfaces (Li et al., 2020; Lin and Liao, 2017; Zhang et al., 2019; Massacci and Ngo, 2021). With conventional exchanges, the success of market manipulation is uncertain as each trade must be agreed upon between the sell and buy sides. In contrast, \acamm-based \acpdex are subject to atomic, risk-free exploits on the protocol’s technical structure such as its algorithmic pricing scheme (Sam M. Werner et al., 2022). Built on top of public blockchain infrastructures featuring transparency and traceability, \acamm-based \acpdex also expose their users to privacy risks.

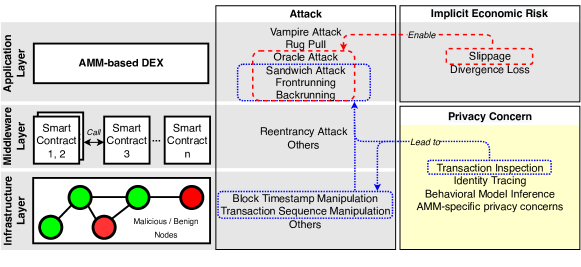

In this section, we define a taxonomy (illustrated in Fig. 6) to enumerate potential security and privacy concerns of \acamm-based \acpdex, expounding their root causes and possible mitigation solutions.

5.1. Associated attacks

We identify three classes of attacks according to the architectural layer on which they occur: infrastructure-layer attacks, middleware-layer attacks, and application-layer attacks. Sometimes, a certain attack (e.g. frontrunning) can target multiple layers simultaneously. We present known historical attacks affecting \acpamm in Table 5.

5.1.1. Infrastructure-layer attacks

The proper operation of \acpdex are based upon healthy and stable blockchain infrastructures (i.e., validators, network, full nodes, etc.). However, since the birth of the blockchain systems, various attacks have threatened their normal operations, potentially affecting the robustness and user experience of \acpdex.

Block timestamp manipulation

A timestamp field is set by miners during the validation process. However, malicious miners can manipulate the block timestamps within constraints to win rewards from certain smart contracts (Crypto Market Pool, 2020), or to tamper with the execution order of \acdex transactions packed in different blocks (Huang, 2019).

To mitigate the negative impact of such manipulation, \acdex contracts should be timestamp independent (Antonopoulos and Wood, 2018). For example, smart contract engineers should avoid using block timestamps as program inputs or make sure a contract function can tolerate variations by a certain time period (e.g. 15 seconds (Narayanan et al., 2016)) and still maintain integrity (Mense and Flatscher, 2018). Besides, \acpdex should choose to be built on a blockchain that applies rigorous constraints to the timestamps of committed blocks or uses external timestamp authorities to assert a block creation time (Szalachowski, 2018).

Transaction sequence manipulation

While transactions within a block share the same timestamp, miners can order transactions, and choose to include or exclude certain transactions at their discretion. Malicious miners can abuse their “power” to prioritize transactions in their favor, profiting from the \acmev, which is the value that is extractable by miners directly from smart contracts during the validation or mining process (Zhou et al., 2021b; Qin et al., 2022) This can be further facilitated by open-source software such as Flashbots (Daian et al., 2020).

To prevent transaction sequence manipulation, \acpdex should first be built upon reputable, frequently-used blockchain systems, as they feature high miner/validator participation, making transaction sequence manipulation difficult. Besides, this attack can be mitigated through an enforced transaction sequencing rule that relies on a trusted third party to assign sequential numbers to transactions (Eskandari et al., 2020). We also discuss how \acpdex and their transactions can practice transaction sequencing from application-layer in §5.1.3, and how privacy-preserving blockchain and \acpdex are resistant to this attack in §5.2.

Other infrastructure-layer attacks

Aiming to perturb operations of blockchain systems (Saad et al., 2019), many other attacks do not target \acamm-based \acdex specifically, but can indirectly affect the service of \acdex. For example, attackers can launch spam or \acddos attacks towards the blockchain system (Greene and Johnstone, 2018; Perez et al., 2020), thereby increasing the latency or even hindering the accessibility of \acdex services; \acbdos attacks exploit the reward mechanism to discourage miner participation, thereby causing a blockchain to a halt with significantly fewer resources (Mirkin et al., 2020); the 51% attack (Saad et al., 2019), the most classic blockchain attack, is able to tamper with the blockchain in any way by controlling more than 50% of the network’s mining hash rate; network attacks can destroy the network connections between the users and the blockchain system through \acdns hijacking (Ramdas and Muthukrishnan, 2019) or \acbgp hijacking (Apostolaki et al., 2017).

In short, \acamm-based \acpdex should be built upon distributed ledgers with active service, community maintenance, and upgrades, as well as modular security designs. Only by ensuring each module of the blockchain system and the interactions between them are secure, can the relative security of the entire blockchain system be ensured.

5.1.2. Middleware-layer attacks

An \acamm-based \acdex usually consists of various smart contracts, in which each serves as a middleware that bridges some application-layer functions with blockchain infrastructures, and collectively support operations of \acpdex. However, the smart contracts and complex collaborations between them can also lead to potential system vulnerabilities (Tsankov et al., 2018). Attackers can exploit such attack interfaces to steal tokens from a \acdex or even paralyze it.

Reentrancy attack

Reentrancy attack can happen when two or more entities (e.g. smart contract, side-chain) call or execute certain functions in specific sequences or frequencies. Ever since July 2016, reentrancy attacks have captured the attention of the crypto industry, when the \acdao, an Ethereum smart contract, was executed maliciously with such an attack, causing a $50 million economic loss in tokens (Popper and Nathaniel Popper, 2016). Afterwards, despite the emergence of various proposals addressing the reentrancy problems (Luu et al., 2016; Tsankov et al., 2018; Albert et al., 2020), reentrancy attacks persist, and became particularly threatening to \acamm-based \acpdex. In January 2019, an audit identified a reentrancy vulnerability in Uniswap (Consensys Diligence, 2019), which was then exploited by hackers to steal $25 million worth of tokens in April 2020 (PeckShield, 2020a) Hackers performed this attack by leveraging a subtle interaction between two contracts that were secure in isolation, and a third malicious contract (Cecchetti et al., 2021). In March 2021, $3.8 million worth of tokens were stolen from DODO through a series of attacks, which began with reentrancies via the init() function in a liquidity pool smart contract, followed by frontrunning and honeypot attacks (DODO, 2021a).

The security community has proposed a variety of approaches to tackle reentrancy attacks (Huang et al., 2019). For example, Rodler et al. (Rodler et al., 2019) protect existing smart contracts on Ethereum in a backwards compatible way based on run-time monitoring and validation; Das et al. (Das et al., 2021) propose Nomos, a reentrancy-aware language that enforces security using resource-aware session types; Cecchetti et al. (Cecchetti et al., 2021) formalize a general definition of reentrancy and leverage information flow control to solve this problem in general. However, with the increasing complexity of \acamm, it can become more difficult for developers to reason about the reentrant interface, thus making reentrancy attacks a more intractable problem for \acamm-based \acpdex.

Other middleware-layer attacks

On the middleware layer, there are many other attacks and threats that can affect normal operations of smart contracts (Sayeed et al., 2020), such as replay attack (Ramanan et al., 2021), exception mishandling (Praitheeshan et al., 2019), integer underflow/overflow attacks (Sun et al., 2021), etc. These threats are not specifically targeted at \acpdex, but can potentially be harmful to \acdex operation. The security community has proposed a variety of approaches to secure smart contract from these threats, such as Smartshield (Zhang et al., 2020a), Zether (Bünz et al., 2020), and NeuCheck (Lu et al., 2019). Users may also purchase insurance cover to hedge smart contract risks (Cousaert et al., 2022a). To fundamentally counter those attacks, smart contract coders must strictly abide by software development specifications and conduct thorough security tests.

5.1.3. Application-layer attacks

Oracle attack

A flash loan is a feature provided by lending platforms where an uncollateralized borrow position can be created as long as the borrowed funds can be repaid within one transaction (Xu and Vadgama, 2022). Flash loans can be used to repay at discount debts that are liquidable without having to acquire borrowed assets in the first place. In this kind of attack, adversaries manipulate lending platforms that use a \acdex as their sole price oracle (see Fig. 1).

Following Attack Algorithm 1, an attacker profits with tokenA less any transaction fees incurred. Utilizing continuous slippage native to an \acamm-based \acdex (see §3.2.4), the attack temporarily distorts the price of tokenA relative to tokenB. After the prices are arbitraged back, the attack would leave the loan taken from step 3 undercollateralized, jeopardizing the safety of lenders’ funds on the lending platform. Examples of such attacks are exploits on Harvest finance (Harvest Finance, 2020), Value DeFi (PeckShield, 2020b) and Cheese bank (Pirus, 2020).

This broken design can generally be fixed by either providing time-weighted price feeds, or using external decentralized oracles. The first solution ensures that a price feed cannot be manipulated within the same block, while the second solution aggregates price data from multiple independent data providers that add a layer of security behind the aggregation algorithm, making sure that prices are not easily manipulated (SmartContent, 2021).

Rug pull

A rug pull involves the abandonment of a project by the project foundation after collecting investor’s funds (Xia et al., 2021). One way of doing this, is to lure people into buying the coin with no value through a \acdex, subsequently swapping this coin for ETH or another cryptocurrency with value, as shown in Attack Algorithm 2. \acpdex allow users to deploy markets without audit and for free (barring the gas costs), which makes them an excellent target to scam investors. One method is to create a coin with the same name as an existing one. This attracts a lot of attention since everyone wants to pick up the coin at the lowest price possible. The coin is being bought up, and the original \aclp swaps his fake coin for ETH. In other cases, the creators of the scam token reach out to several prominent people, creating false hype. Once potential buyers see that major players have purchased the token, they start buying themselves, before realizing that the token cannot be swapped back for ETH. Sometimes, the attackers let people trade the coin back for ETH, but only for a short period since they are running the risk of losing money. (Xia et al., 2021) research data on scam tokens on Uniswap and confirm that rug pulls commonly find their victims through \acpdex.

In August 2020, an rug puller extracted 3 ETH by imitating the well-known AMPL token (Ampleforth, 2021) with a scam token TMPL. The token’s transaction history shows the provision of 150 ETH and TMPL tokens to a Uniswap V2 pool by the attacker, who removed 153.81 ETH only 35 minutes later (Etherscan, 2021).

To protect themselves from being rugged, investors should exercise caution and always confirm a project’s credibility before investing in its \acido (Bybit Learn, 2021; The European Business Review, 2021). Usually, reputable \acpido feature high liquidity and a pool lock (rug, 2021) that disables withdrawal for a fixed period, so that \acplp are unable to quickly empty the pool once it has absorbed a sufficient amount of valuable assets from investors (Mudra Manager, 2021).

Frontrunning

Frontrunning is often enabled through access to privileged market information about upcoming transactions and trades (Eskandari et al., 2020). Since all transactions are visible for a very short period of time before being committed to a block, it is possible for a user to observe and react to a transaction while it is still in the mempool. Those who place their trade immediately before someone else’s are called frontrunners (Daian et al., 2020; Eskandari et al., 2020). Frontrunners attempt to get the best price of a new coin before selling them onto the market. They can buy up a great portion of the supply of a new token to create exorbitant prices. Due to the hype, this does not stop retail traders from further buying. The frontrunner, who is the seller with the most significant supply, can swap the purchased token for popular coins (e.g. ETH) paid by retail traders. For example, a considerable amount of \acpido on Polkastarter are frontran on Uniswap (Taylor, 2021).

Frontrunning can also be achieved through transaction sequence manipulation (see §5.1.1) and by exploiting the general mining mechanism. Most mining software, including the vanilla Go-Ethereum (geth), the most popular command-line interface for running Ethereum node, sorts transactions based on their gas price and nonce (Zhou et al., 2021c; Eskandari et al., 2020; Daian et al., 2020). This feature can be exploited by malicious users of \acdex who broadcast a transaction with a higher gas price than the target one to distort transaction ordering and thus achieve frontrunning.

Frontrunning can be avoided with various approaches (Baum et al., 2021a). Normal exchange users can set a low slippage tolerance to avoid suffering from a price elevated by front-runners. However, an overly low slippage tolerance may lead a transaction to fail, especially when the trade size is large, resulting in a waste of gas fee (Degate, 2021). \acpdex can enforce transaction sequencing to fundamentally solve frontrunning. Some exchanges, such as EtherDelta (Narayanan et al., 2016) and 0xProject (Warren and Bandeali, 2017), utilize centralized time-sensitive functionalities in off-chain order books (Eskandari et al., 2020). In addition, transactions can specify the sequence by including the current state of the contract as the only state to execute on (Eskandari et al., 2020), thereby preventing some types of frontrunning attacks. Frontrunning can further be tackled by addressing privacy issues (see §5.2) and transaction sequence manipulation on the infrastructure layer (see §5.1.1).

Backrunning

Backrunners place their trade immediately after someone else’s trade. The attacker needs to fill up the block with a large number of cheap gas transactions to definitively follow the target’s transaction. Compared to frontrunning which only requires a single high valued transaction and is detrimental to the user being frontrun, backrunning is disastrous to the whole network by hindering the throughput with useless transactions (livnev, 2020).

Backrunning attacks can be mitigated through anti-\acbdos solutions such as A2MM (Zhou et al., 2021a). Theoretically, defense solutions of \acl7ddos attacks (Feng et al., 2020; Xie and Yu, 2008; Wang et al., 2017) can also be adopted to tackle backrunning problems, as they all aim to secure usability of web services to legitimate users. In addition, backrunning can be addressed by confidentiality-enhancing solutions that hide the content of a transaction before it is committed to a block (see §5.2).

Sandwich attacks

Combining front- and back-running, an adversary of a sandwich attack places his orders immediately before and after the victim’s trade transaction. The attacker uses front-running to cause victim losses, and then uses back-running to pocket benefits. While there are endless examples of sandwich attacks, Zhou et al. (Zhou et al., 2021c) detail two types that can occur on an \acamm: an \aclp attacking an exchange user (see Attack Algorithm 3) by exploiting \acamm’s liquidity sensitive property (§3.3.4), and one exchange user attacking another (see Attack Algorithm 4) by taking advantage of \acamm’s demand sensitive property (§3.3.5). The latter is particularly common. Fig. 7 shows two examples of such attacks on Uniswap V2 within a time frame of 3 minutes.

Considering swap fee (see §2.4.2), gas fee (see §2.4.2) and slippage (see §2.4.3), sandwich attacks are only profitable if the size of the target trade exceeds a certain threshold, a value that depends on the \acdex’s design and the pool size. \acpdex can thus prevent sandwich attacks by disallowing transactions above the threshold (Zhou et al., 2021a). Naturally, sandwich attacks can also be curbed by deterring either frontrunning (see §5.1.3) or backrunning (see §5.1.3).

Vampire attack

A vampire attack targets an \acamm by creating a more attractive incentive scheme for \acplp, thereby siphoning out liquidity from the target \acamm (Jakub, 2020) to the detriment of the protocol foundation (see §2.1.3). In September 2020, Sushiswap gained $830 million of liquidity through a vampire attack (Dale, 2020), where Sushiswap users were incentivized to provide Uniswap \aclp tokens into the Sushiswap protocol for rewards in SUSHI tokens (Sushiswap, 2020). A migration of liquidity from Uniswap to protocol Sushiswap was executed by a smart contract that took the Uniswap \aclp tokens deposited in Sushiswap, redeeming them for liquidity on Uniswap which was then transferred to Sushiswap and converted to Sushiswap \aclp tokens.

Legal approaches such as applying a restrictive license to the protocol code base—as done later by Uniswap with its V3 new release (Foxley, 2021a)—can be employed to hinder vampire attacks.

5.2. Privacy concerns

Most blockchain systems are open, traceable, and transparent, which can raise severe privacy concerns to \acpdex that built upon them. Besides, \acamm protocols will reveal real-time \acpdex information to the public, bringing additional privacy concerns to \acamm-based \acpdex. In this section, we introduce the privacy issues that users may face in using \acamm-based \acdex and discuss their possible solutions.

5.2.1. Transaction inspection

The transparency and openness of public blockchains, where most \acamm-based \acpdex are built, allow transactions to be observable to everyone. However, this characteristic enables malicious parties to inspect transactions, thereby seeking profits or even disrupting the market (Eskandari et al., 2020). The inspection activities can occur before or at the moment that the transaction is committed to the blockchain by miners, validators, or even any third parties. For example, the aforementioned frontrunning, backrunning, sandwich attacks, transaction sequence manipulation, and block timestamp manipulation in Section 5.1 are all based on transaction inspections (Goldreich and Oren, 1994). In fact, major \acamm-based \acpdex are fraught with bots, constantly monitoring transactions for possible profit opportunities (Narayanan et al., 2016).

5.2.2. Identity tracing

Although most blockchains and \acamm-based \acpdex usually feature a certain degree of anonymity, the linkabilities of transactions and accounts over time still enable attackers to dig identities information of users (Zhang et al., 2019). Actually, with some off-chain information (e.g. social network posts, public speak, location (DuPont and Squicciarini, 2015)), eavesdroppers can launch de-anonymization inference attacks to bridge virtual accounts with real-world individuals or uncover the true identities of traders by linking the transactions of an account together and matching relevant information (Narayanan et al., 2016).

5.2.3. Behavioral model inference