Modeling Random Directions in 2D Simplex Data

Abstract

We propose models and algorithms for learning about random directions in two-dimensional simplex data, and apply our methods to the study of income level proportions and their changes over time in a geostatistical area. There are several notable challenges in the analysis of simplex-valued data: the measurements must respect the simplex constraint and the changes exhibit spatiotemporal smoothness while allowing for possible heterogeneous behaviors. To that end, we propose Bayesian models that rely on and expand upon building blocks in circular and spatial statistics by exploiting a suitable transformation based on the polar coordinates for circular data. Our models also account for spatial correlation across locations in the simplex and the heterogeneous patterns via mixture modeling. We describe some properties of the models and model fitting via MCMC techniques. Our models and methods are illustrated via a thorough simulation study, and applied to an analysis of movements and trends of income categories using the Home Mortgage Disclosure Act data.

1 Introduction

In many real-world problems, some or all the primary quantities of interest are non-negative proportions that sum up to one and thus lie in a probability simplex. For instance, to study a collection of rocks and sediments, geologists might analyze the chemical, mineral, and/or fossil percentages of each sample to determine the effects of various natural processes or which samples are related (Aitchison, 1982). As another example, microbiolologists might examine microbiome data from a set of volunteers because of the microbiome’s effect on human health (Allaband et al., 2019). Here, the microbiome refers to the proportions of various microbes in the human gut (Allaband et al., 2019).

Modeling the variation and change of measurements that lie on the simplex can be challenging. To be concrete, we let denote the -dimensional probability simplex, i.e., the subset of elements in whose components are non-negative and sum to one. Given a data set represented by a collection of random samples , each data point is composed of the components for . The most immediate difficulty is the simplex constraint imposed by the proportions because they must sum up to one (Pawlowsky-Glahn et al., 2007). For this constraint to be maintained, a change in one proportion necessarily involves a change in the other proportions. If this is not handled correctly, the model might detect what Pearson called "spurious correlation" (Pearson, 1896). Another difficulty may arise if any of the proportions are zero. Customary composition data approaches rely on a standard transformation technique, e.g., taking the ratio of and the geometric mean of or the ratio of and for and for some reference and then applying the log transform to these ratios (Pawlowsky-Glahn et al., 2007). As a result, these "log-ratio" transformations convert the data from to . Note that if any of the proportions are zero, then some or all of these ratios are either or and the transformation becomes undefined.

To deal with this difficulty, we might model how the data shift as random movements of points within the simplex. Despite the potential challenge in modeling movements that respect the simplicial constraint, such an approach has several fundamental advantages. It would avoid picking up "spurious correlation" because all components of an observation would be dealt with simultaneously. Moreover, while the range of movements is restricted, boundary points could be treated in a similar framework as interior points.

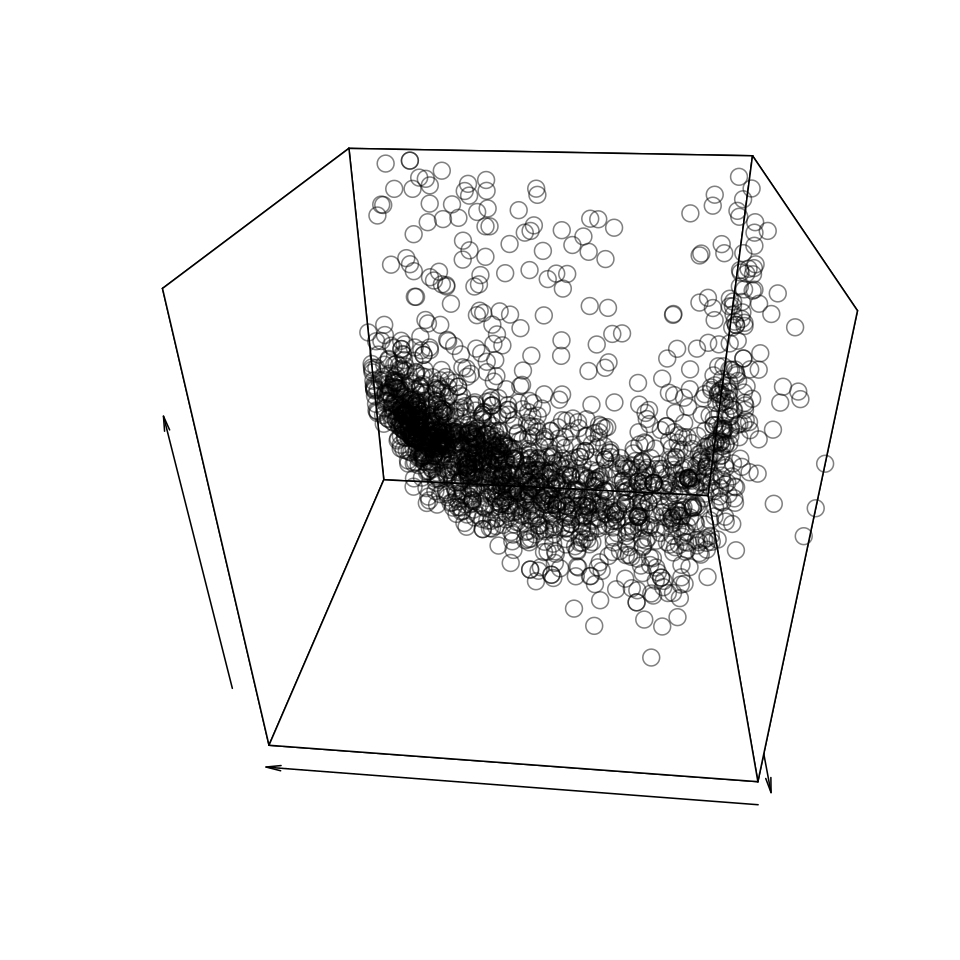

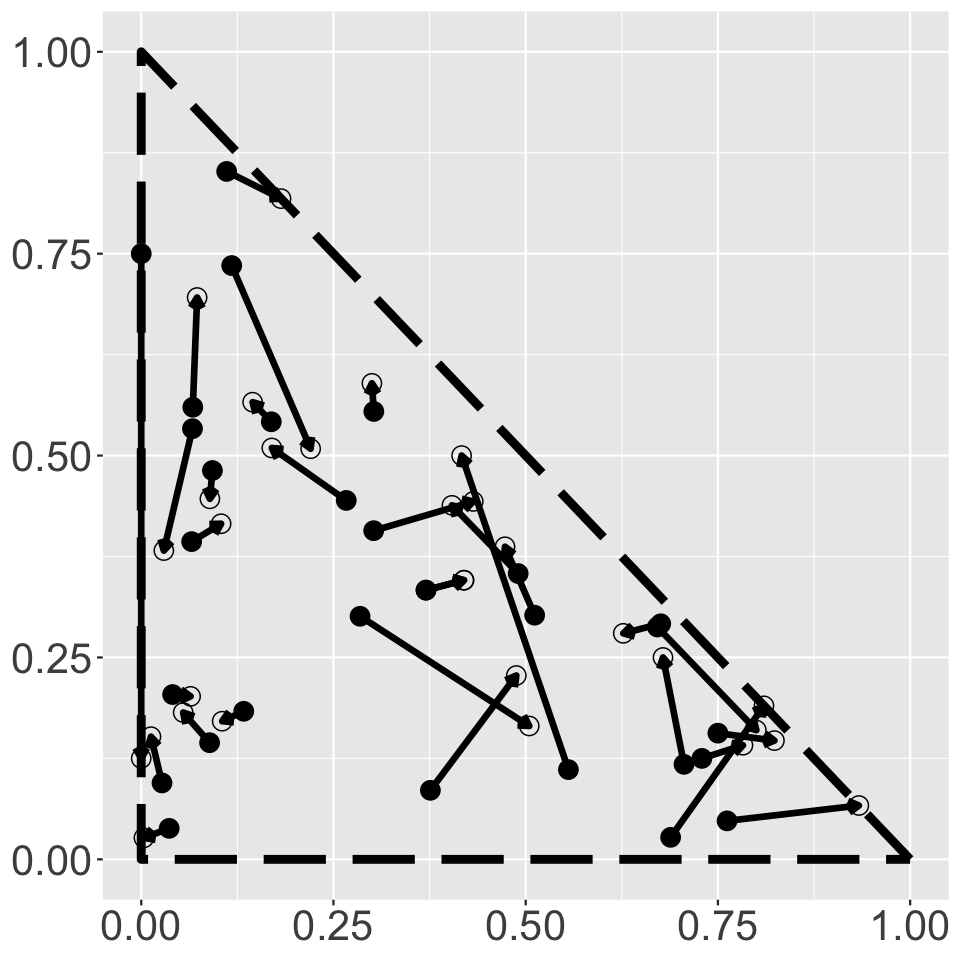

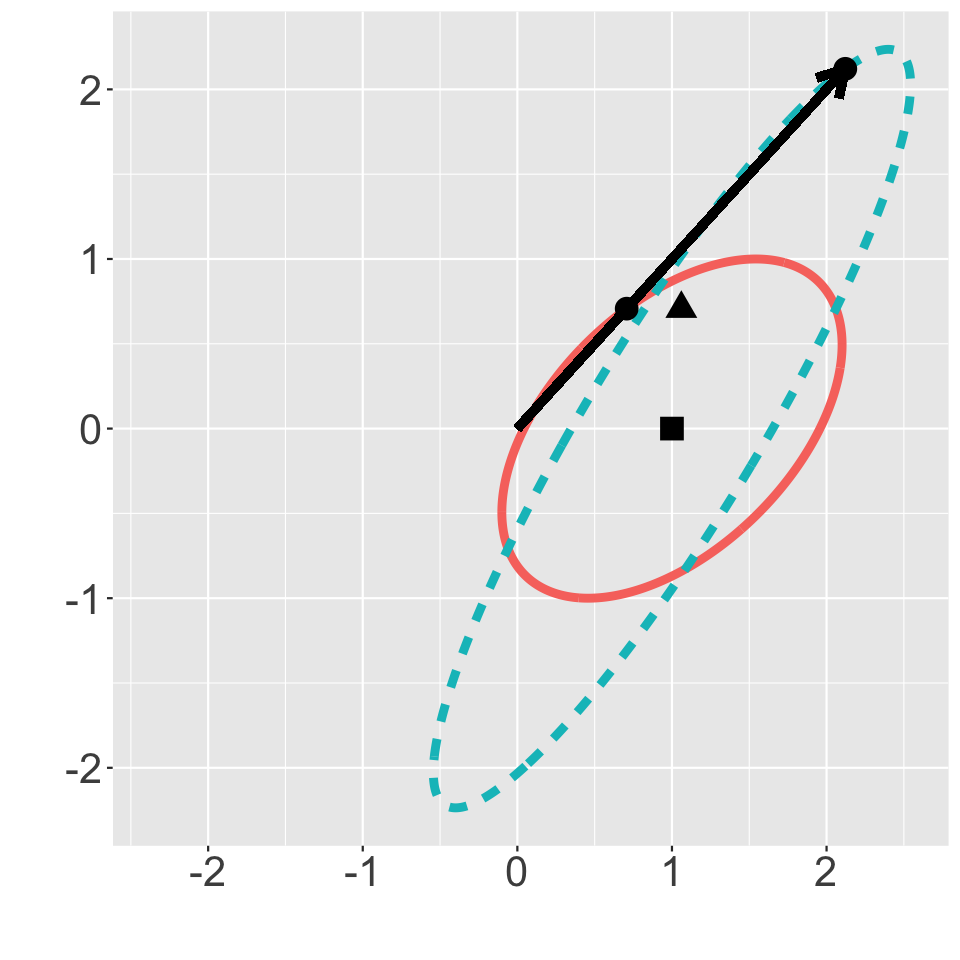

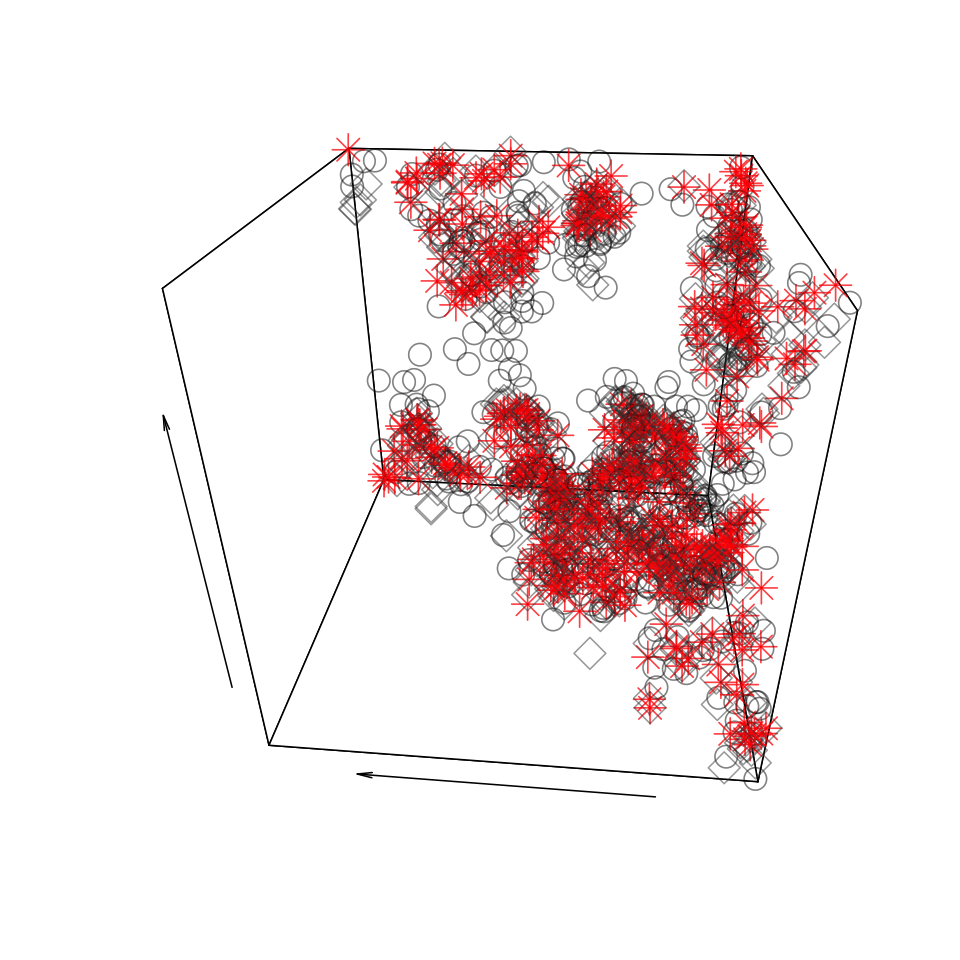

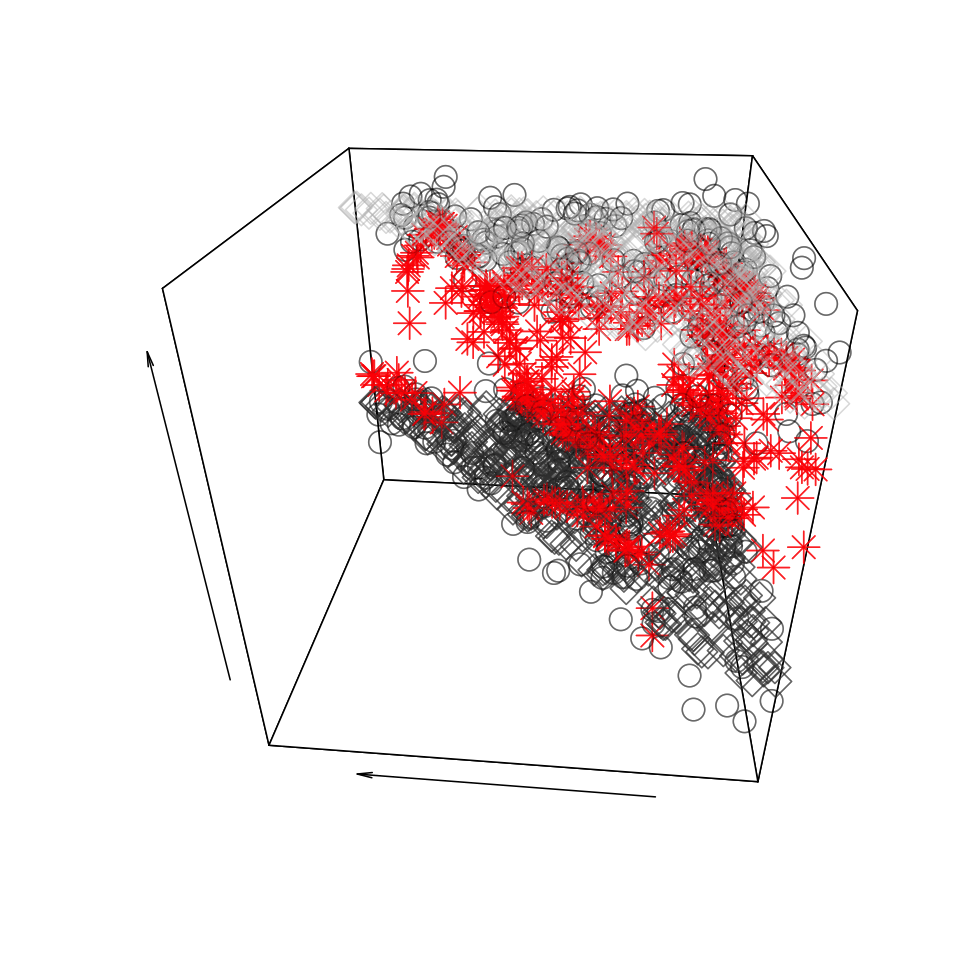

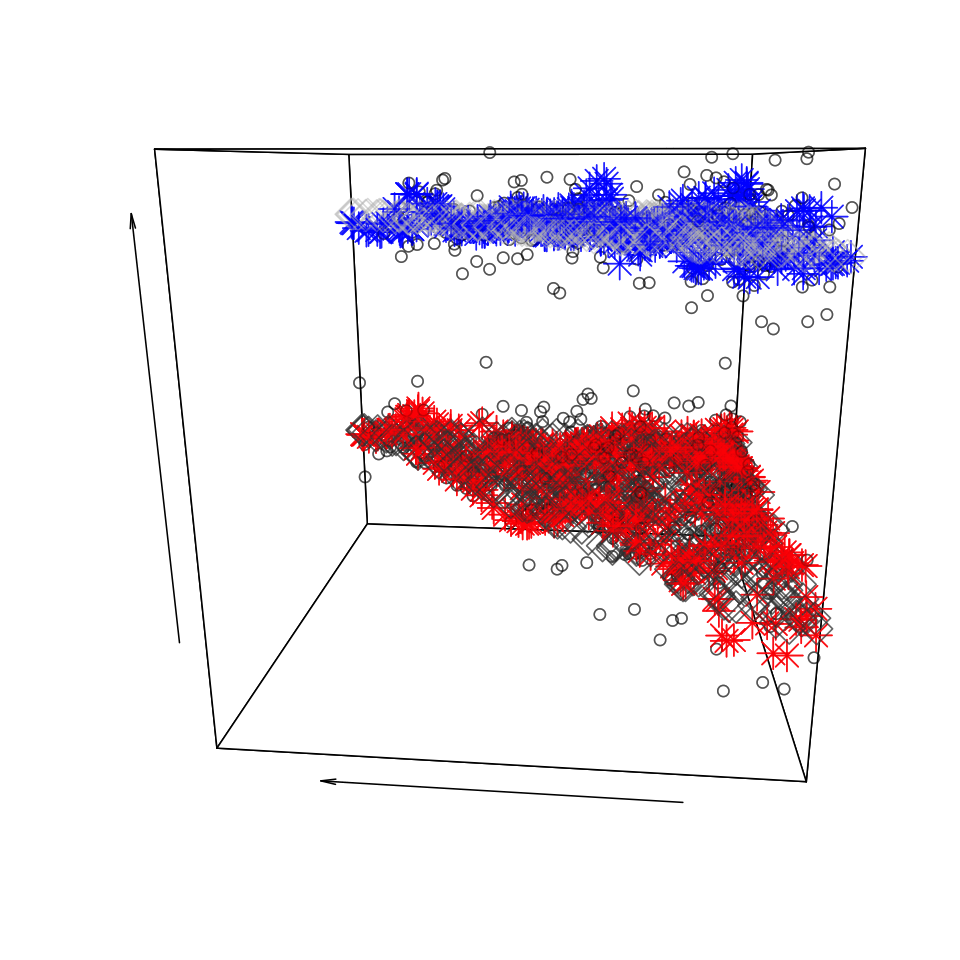

To help develop such a model for the random movement, this paper will examine an important aspect: modeling the random directions of such movements. This is a key step for two main reasons. First, at a high level, any movement in the simplex, including points on the boundary, can be decomposed into the direction and the magnitude. For a movement to respect the simplex constraint, the magnitude of a point’s movement is bounded by the maximum distance between the point and the boundary point in a given direction. Thus, not only is there greater flexibility in modeling the two aspects separately, but also doing so allows us to model the magnitude with greater care. The second reason is that even this modeling task presents potential non-trivial difficulties. An illustrative example is a data set of income proportions for all Census tracts or "neighborhoods" in Los Angeles County from 1990 to 2010. The proportions have been binned into three categories: $0 to $100,000, $100,000 to $200,000, and greater than $200,000. Using the Census tract IDs, we can track how the income proportions for a neighborhood changes from one year to the next. As we will demonstrate later, this shift appears dependent on the current income proportions and not on the neighborhood’s physical location. Then, Figure 1 shows that we cannot assume a uniform random direction in this change because there may be clearly preferred directions. We need a way to assign probability to these random directions. In order to start thinking about how to accomplish this, we first examine the 2D simplex case, which shall be the main focus of our paper. There, the simplex is essentially a two dimensional surface for our points to move in. It suffices to assume that these random directions are random angles and lie in the interval . One naive approach to assign probability to such an interval is by assigning probability to some random variable and using the inverse logit function to transform to that interval. Such an approach would be problematic because the endpoints of the interval and values near the end points are mapped near their respective and are far apart. Meanwhile, the end points for the random angle’s interval, and , denote the same direction and should not be so far apart. The issue here, mathematically, is that the inverse logit function that maps to the angles , while continuous and one-to-one, does not possess a continuous inverse.

Existing work Several useful techniques for modeling (random) angles and directions come from directional statistics (Mardia and Jupp, 2010). In particular, we can think of the random angle as circular data because these angles can be mapped to a point on the unit circle and circular data are observations that lie on a unit circle. There are several basic distributions on circular data that we can utilize for our purposes: the von Mises distribution and the projected normal distribution in two dimensions. The former can be loosely viewed as the circular version of the normal distribution (Lee, 2010). Meanwhile, the latter is a bivariate Gaussian distribution that is transformed to a distribution on the circle using the usual polar coordinate transform and integrating out the radius (Mardia and Jupp, 2010). There is another distribution that we might use. As seen in Figure 1, it is possible that nearby locations move in mostly similar directions. In other words, the random directions, depending on where the start points are, appear to be spatially correlated. Because the change in the pattern of random direction is also smooth as we pass across the simplex in this figure, an appropriate model might be the Gaussian process (Rasmussen and Williams, 2006). Even though we cannot use the inverse logit function to transform a Gaussian process because of what we discussed earlier about angles, we can use the circular version of the Gaussian process, i.e. the projected Gaussian process (Wang and Gelfand, 2013).

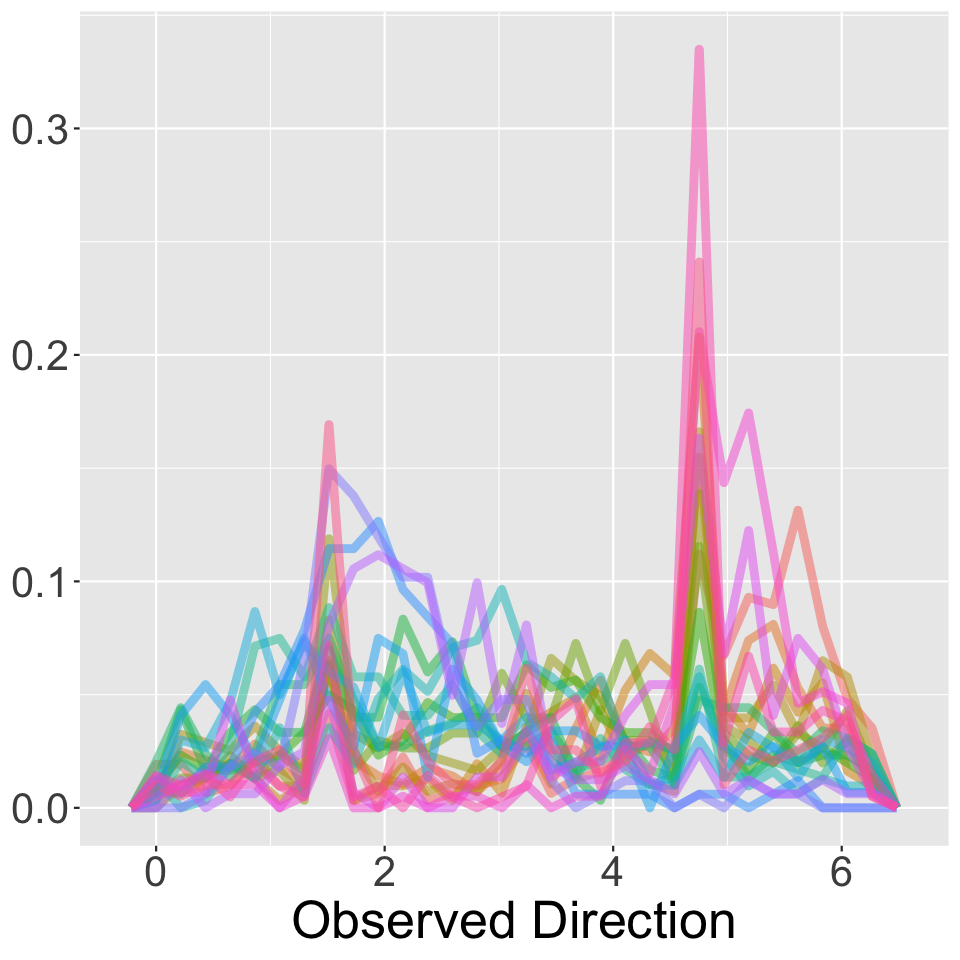

Our approach To model the random direction of movements for simplex-valued data, we will leverage and expand upon the building blocks advocated by Mardia and Jupp (2010); Rasmussen and Williams (2006) and the techniques of Wang and Gelfand (2013, 2014). As the first step of our approach, we assume that the observed random directions are distributed according to a von Mises distribution. We then correlate the von Mises distributions’ means with a projected Gaussian process. In other words, this is a circular version of the Gaussian process with Gaussian white noise. This modeling choice seems appropriate because there appears to be an unimodal empirical distribution for the random directions associated with the nearby locations for any location in the simplex. For example, Figure 1(d) shows such a distribution for the location in the simplex, . Such a choice also makes sense because the mean of the von Mises distribution can be thought of as a vector on the unit circle, which is what a projected Gaussian process outputs. In addition, it allows both the prior and likelihood to recognize the geometry of angles. Not only can this basic model harness the power of Gaussian processes to spatially correlate random directions of nearby locations and handle noisy directions, but also it does so in an interpretable way. After fitting our model, we can make a posterior prediction of the mean preferred direction for any location.

Extensions to the basic model described above are required to account for "heterogenous" patterns for random directions, which are evidently illustrated in Figure 1(e). Because the basic approach proves to be inadequate, the modeling extensions form a substantial portion of this paper. To capture such heterogeneity, we shall extend the basic model via several mixture modeling techniques. In particular, the observation is distributed according to one of von Mises distributions with some probability. Each of the distributions has a projected Gaussian process to correlate its mean. This simple extension still retains the advantages mentioned previously because each component now represents a mean preferred direction. We also discuss another modeling alternative. While there still are von Mises distributions, we extend the inverse logit to transform Gaussian processes to the mixing probability for each component.

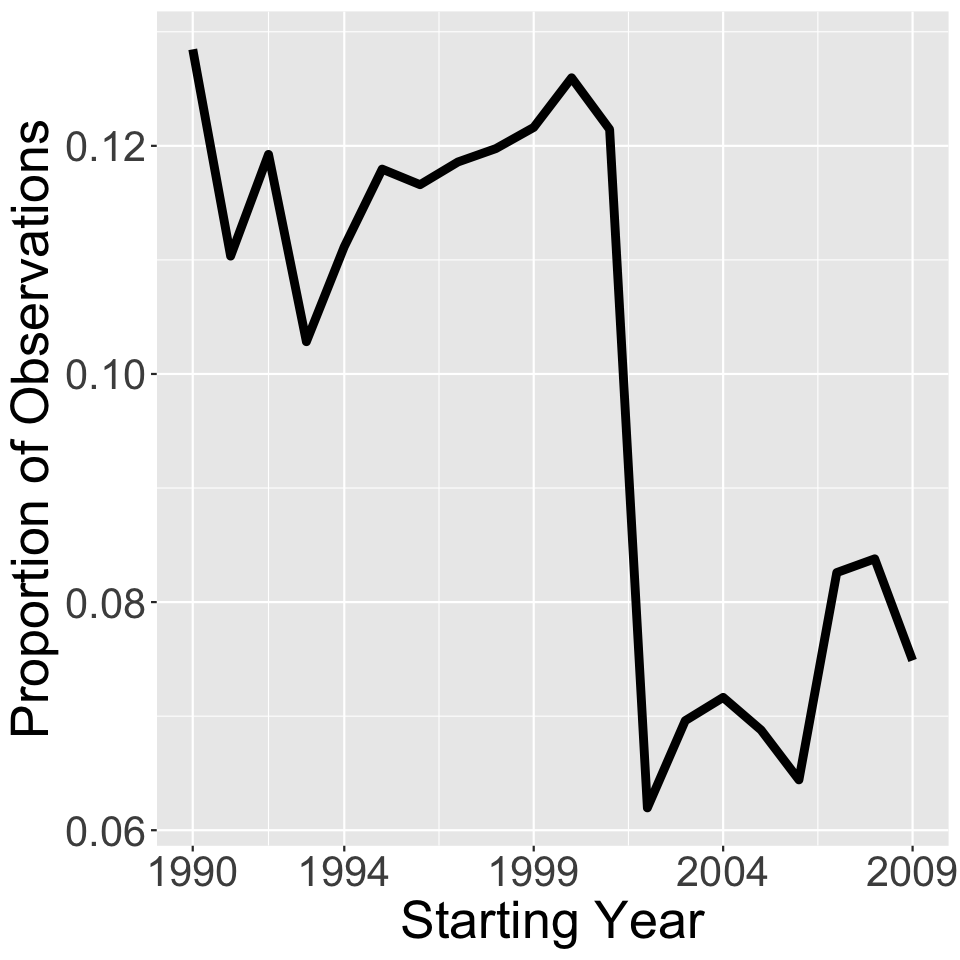

We have applied and evaluated these models to a simulated data set and the aforementioned data set of income proportions. For model selection, we compare the fitted models’ posterior predictive probabilities calculated on data withheld from each year. The chosen models enable us to discover several patterns of interest on the year-to-year income proportion movements. There appear to be four phases based on the patterns we discover, and interestingly enough, these phases correspond to the economic cycles observed during that time period. The first two phases charts the end of one cycle, the third phase follows the dot com bubble and the recession after the bubble, and the last phase represents the subsequent housing bubble and the housing market crash. Because we can also assign meaning to the random directions with respect to the income categories, interpreting the results from the models gives us further information about the year to year change during these phases.

These modeling techniques can also be extended to random directions in higher dimensions. In addition, it might be applied to data that lie on manifolds other than the simplex because any change in the data can be represented as a random movement, which can be decomposed accordingly. However, in this paper we shall restrict our attention to two dimensional simplex data in order to focus on the heterogeneous modeling and inference in the circular representation, which is already quite intricate. The rest of the paper is organized as follows. In Section 2, we describe how the polar coordinate transformation can be used to transform distributions in to distributions on the circle, such as the von Mises distribution or the projected normal distribution in two dimensions. We also discuss some properties of these transformed distributions and extend the projected bivariate normal distribution to the projected Gaussian process. While it is not a focus of this paper, we then introduce the higher dimension version of these distributions. Next, we more formally introduce our models in the Section 3 and describe a few properties of these models using ideas from directional statistics. We then briefly examine how to fit these models in Section 4. We fit them to simulated and real data in Section 5 and discuss these results. Section 6 discusses possible extensions.

2 Polar coordinate transformations for circular data

In this section, we examine how the polar coordinate transformation can be used to transform distributions in Euclidean domains, such as , to distributions on non-Euclidean domains, such as the unit circle. Because our paper is focused on random directions in , we begin by discussing tools from circular statistics and then introduce the higher dimension analogues. In circular statistics, the data are observations that lie on an unit circle (Mardia and Jupp, 2010), so they can be represented by their angles, which will be denoted by random variable .

Given any , there is a unique polar representation in terms of the corresponding radius and angles, namely , where and . In fact, this representation establishes a bijection between and . This suggests a natural recipe for assigning probability for (random) angles : this can be done by endowing a distribution for , which induces a distribution for the pair . We obtain a valid distribution on angles by either marginalizing out or conditioning on a particular value of .

The aforementioned bijection between and induces a function that maps to . This function is denoted by , where the notation is used to indicate a modified version of the standard arctan function. Recall that the standard arctan function maps the real line to the open interval . We may extend this continuous function to the closed domain and the closed range of angles . The function satisfies the following (which is commonly used as a definition): for ,

| (2.1) |

Using these representations, we can derive the von Mises and projected normal distributions, which will be useful building blocks in our subsequent modeling.

2.1 von Mises Distributions

A natural choice for constructing a probability distribution of is the bivariate Gaussian distribution with mean, , and variance, , for some and . The precise meaning of parameters and will be clear shortly. Applying change of variables, we obtain that for ,

By conditioning on , we arrive at the von Mises distribution on the interval (Mardia and Jupp, 2010):

In its original form, the von Mises distribution is defined by two parameters: a mean angle, , and a concentration parameter, . Given these parameters, the von Mises distribution has a density function of the following form:

| (2.2) |

Appearing in the normalizing constant, is the modified Bessel function of the first kind and of order 0. In general, the modified Bessel function of the first kind and of order on the interval of is defined to be

| (2.3) |

Since the domain of the angles, the unit circle, is non-Euclidean, one has to be careful when speaking of notions such as mean and variance. Here are several properties we wish to highlight. First, the distribution is unimodal and symmetric around its mean, , if . This makes sense because as discussed earlier, the density function is proportional and restricted to a bivariate Gaussian centered at a point on the unit circle. If , then the von Mises distribution becomes the uniform distribution on an interval of length . Next, the mean angle, , is different from the typical definition because for the von Mises distribution with , it is the such that the following quantity

| (2.4) |

where denotes the complex number, satisfies the following identity

| (2.5) |

Intuitively, the circular mean is a weighted average of points on the circle and the angles that correspond to them instead of the values of the angles. Indeed, if is some distribution on the circle, the circular mean in general is the such that

| (2.6) |

satisfies the following equation for some ,

| (2.7) |

For convenience, we may refer to the circular mean as the mean or average later on. It should be obvious from context if we refer to the typical or circular mean.

Finally, despite the circular variance still using the mean direction , the circular variance is different as well. It is defined on the interval to be

| (2.8) |

We may also write (Mardia and Jupp, 2010), where the left hand side refers to the circular variance, and the right hand side makes use of the usual expectation (of a scalar random variable). It should be obvious from context which type of variance we are discussing. Due to how circular variance is defined, it takes values between 0 and 1. At a high level, if is tightly concentrated around the mean direction , the variance will be close to zero. Conversely, if is dispersed around the circle, will be 0 so the variance will be 1. Because the variance indicates the spread of the data, can be seen as a measure of concentration for the distribution . For a von Mises distribution, the circular variance is

| (2.9) |

2.2 Projected Normal Distribution

The von Mises distribution is not the only distribution that we can derive from transforming a bivariate Gaussian distribution to a distribution on random angles. Let us consider a bivariate Gaussian with any mean, , covariance matrix, . Then, if we apply the polar coordinate transformation to this distribution, we have that

The projected normal distribution in two dimensions immediately follows from this because it is the marginal distribution of , i.e.

| (2.10) |

Even though this integral is tractable (Mardia and Jupp, 2010), we focus on the case because its properties are well-understood. Given , let and be the polar coordinate transform of . As shown by Wang and Gelfand (Wang and Gelfand, 2013), the distribution in this scenario has the following closed-form expression:

| (2.11) |

Here, and denote the standard normal PDF and CDF. If we also then set , the projected normal distribution becomes uniform. For , the projected normal distribution with the identity matrix is symmetric and unimodal around like the von Mises distribution. It is not surprising that based on this fact, the circular mean is (Wang and Gelfand, 2013). If is undefined due to , then the mean angle is because the projected normal distribution is a uniform distribution. Meanwhile, we can use Kendall’s technique to compute the circular variance (Kendall, 1974). Despite Kendall only considering the case in which and , it is straightforward to extend his result and show that the circular variance is , where and and are the modified Bessel functions defined in (2.3). Again, like the von Mises distribution, the circular variance is independent of the mean angle. Then, we can use the asymptotics of the Bessel function to show that the circular variance is 1 when and 0 when (Watson, 1995). As discussed before, the former occurs when and the distribution becomes uniform. The latter happens when and the probability (density) of other angles tend to 0.

We cannot use these results to derive closed-form expressions for the circular mean and variance in the general case because the projected normal distribution in that case has a more complicated closed-form expression. Fortunately, as we will demonstrate later in this paper, these results do allow us to compute the circular mean and variance of the models that we will introduce.

2.3 Projected Gaussian process

It is of interest to define a stochastic process of random directions indexed in a general domain . This is possible by exploiting the polar coordinate transformation as above, whereas the bivariate normal distribution for can be extended into a stochastic process defined on ; a common choice is to use the Gaussian process. This idea was studied by (Wang and Gelfand, 2014). We will present a simpler version of this idea.

Gaussian process is a powerful modeling tool for spatio-temporal data (Cressie and Wikle, 2011; Banerjee et al., 2015; Rasmussen and Williams, 2006). Given observations indexed by the corresponding locations , we assume that these observations are realizations of a stochastic process , i.e., for . To account for the spatial dependence of these observations, one may assume that is a Gaussian process, which is parameterized by a mean function and a covariance function on . Abusing notation, we let denote the mean function applied to every location such that . If is a matrix such that for , we will denote this as . We write it this way because .

We describe how to convert the Gaussian process to the projected Gaussian process. Suppose that and with . For identifiability of the angle-valued stochastic process, we might assume that is equal to for some fixed and covariance matrix, . While this may appear restrictive, it is similar in spirit to what Wang and Gelfand proposed to identify the projected normal distribution in two dimensions (Wang and Gelfand, 2013). Then, let denote the angle-valued stochastic process observed at the index points so that for and be a latent variable. We apply the polar coordinate transformation element-wise such that and for . As a shorthand, define and to be the vectors such that and for . Since the Jacobian of this transformation is , we have that

| (2.12) |

The projected Gaussian process is the marginal distribution of :

| (2.13) |

While this integral is intractable, we can still calculate its properties marginally for to understand this process. Because for , is marginally distributed according to . If , we can use the previous section’s discussion to do so. Otherwise, we will explain the computation later.

2.4 Higher Dimension Analogues

An alternative way to describe these distributions is to view them as distributions on vectors "projected" onto the unit sphere. In other words, given , the von Mises distribution and the projected normal distribution in two dimensions are distributions on . From this perspective, because in the polar coordinate transform, it further explains why the von Mises distribution is proportional to a particular bivariate Gaussian conditioned on . Meanwhile, the projected normal distribution arises by computing the probability of if is distributed according to a bivariate Gaussian with mean and . In other words, we have that

| (2.14) |

This calculation is easier to do with polar coordinates.

This perspective also suggests how to generalize the von Mises distribution and the projected normal distribution for higher dimensions. First, for the von Mises distribution, suppose that , . Let be distributed according to a Gaussian distribution of dimension with mean and covariance matrix, . Here, such that and . Then,

If we condition on , we get the von Mises-Fisher distribution:

The normalization constant for this distribution is where is the modified Bessel function defined in (2.3) (Mardia and Jupp, 2010). Note that this is identical to the von Mises distribution in two dimensions because if and for ,

The projected normal distribution in higher dimension can be derived in a similar manner from its lower dimensional analogue. The projected normal distribution is given by computing the probability of if is now distributed according to a Gaussian of dimension with mean, , and covariance matrix, . The calculation is the same as (2.14) except with and of the appropriate dimension. While this distribution might not be identifiable (Wang and Gelfand, 2013), can be set in certain ways to simplify fitting the distribution to data (Hernandez-Stumpfhauser et al., 2017).

This then provides a template for defining the projected Gaussian process in higher dimensions. Suppose that for all , . Again, and for any . Set , to be a stochastic process on the unit circle. We then element-wise project each to the unit circle such that . If we abuse notation and denote this element-wise projection as , then the probability is the following:

3 Modeling Random Directions

3.1 Model Description

The purpose of our models is to elucidate the patterns observed in random directions. We first introduce the notation that we intend to use.

We are given a location and an observation for that location for . We use as our index because of the spatial aspects of the data and model. To compare two observations, we will use to indicate a location and observation different from the location and observation corresponding to . If there are von Mises distributions indexed by , , each observation, , is assumed to be distributed according to one of the von Mises distributions with mean parameter, , and a concentration parameter, . We will use to indicate which von Mises observation is associated with. If there is one von Mises distribution, we will drop from the parameters’ index and will not use . We will remove from the index if the parameters are the same regardless of the location or if we wish to refer to the entire vector. While this overloading is unfortunate, any vector will be displayed in bold. Even though context should make it clear which definition we are referring to, we will specify the space the variable lies in.

We also need a set of notation for Gaussian processes because all the models that we will introduce use it. We let be a draw from a Gaussian process with mean and covariance matrix . For models that need two Gaussian processes for each component, we will further index these vectors as and and their parameters as , , , and . The specific value corresponding to observation will be denoted by or and . Again, we may drop if there is only one Gaussian process. In both cases, our choice of indices is to make the link between the specific Gaussian process and the particular von Mises distribution and observation more explicit.

| Observed Pattern | |||

| Homogeneous | Heterogeneous | ||

| Spatial | |||

| Ind. | iV (7.1) | iVM (7.2) | |

| Var. | SvM (7.3) | SvM-c (3.1) SvM-p (3.2), (3.3) | |

Heterogenous Spatial Random Direction Model There are two ways to incorporate spatial information for heterogeneous spatial random direction patterns. The first way is to integrate spatial information in the means of the von Mises distributions. We call this model the Spatially varying von Mises component mixture model or SvM-c. More specifically,

| (3.1) | |||||

According to this model specification, each observation may be distributed by one of von Mises distributions with probability regardless of its location. Each distribution’s mean parameters, , are transformed from two draws, , from one of Gaussian process with potentially its own mean and covariance matrix . This transformation is accomplished using the function element-wise. A distribution’s concentration parameters, , are again random variables, , that have been exponentiated. These random variables are distributed according to a hierarchical normal distribution. At a lower level, they are distributed according to a normal distribution with the same standard deviation, , but with different hierarchical means, . These hierarchical means, , are given the same hyperprior, .

In other words, for the concentration parameter in SvM-c, we use the following hierarchical prior:

We use the hierarchical prior for the concentration parameter because it is a compromise between assigning an individual and a global concentration parameter. Using a global parameter might affect the estimates of the mean if the variances differ significantly because the model cannot adjust the concentration parameter. Conversely, assigning an individual parameter makes the model too flexible. This might negatively affect the model’s ability to spatially correlate the observations. This concern also leads us to set the standard deviation for the lower term, , to a small value instead of sampling for it. Even with a tight prior on , the variance of the lower terms will be greater if we sample for the standard deviation. In addition, we do not use another Gaussian process to model the variance parameter for computation reasons and for fears of making the model too rich. Still, a normal distribution is useful because it will allow us to separately sample the hierarchical mean, , from the lower term, .

SvM-c included spatial information through the components. An alternative approach to meld spatial information into our models is through the mixing probability. In this approach, we assume that observations nearby are likely to belong to the same von Mises distribution instead of being distributed according to a von Mises distribution with similar means. This alternative model is still interpretable because the results describe the preferred von Mises distributions of certain regions.

More explicitly, we call this model the Spatially varying mixing probability for von Mises distributions model. Keeping with our previous convention, we will shorten it to SvM-p. For this model, is assumed to be distributed to according to one of von Mises distribution with mean parameter, , and concentration parameter, . Both parameters are assumed to be the same for a particular von Mises distribution regardless of the observations’ location. The mean parameters across all von Mises distributions are consequently given a prior of whereas the concentration parameters are given a prior of . If there is more prior knowledge about either parameter or if we want to force identifiability among the parameters, a von Mises distribution and a stronger Gamma distribution could instead be used for the mean parameter and concentration parameter respectively. Meanwhile, because the mixing probabilities sum up to 1, we only need to use the generalized inverse logit function, , to element-wise transform draws from Gaussian processes with mean and covariance matrix to the mixing probabilities. We define the generalized inverse logit function, , as a mapping from to in the following manner:

We will still use as our index for the Gaussian process draws to make clear which draw links to which von Mises distribution. In short, SvM-p can be described as following.

| (3.2) | |||||

If there are only two von Mises distributions, the general inverse logit function simplifies to the inverse logit and the model only needs one Gaussian process. The inverse logit function, , is defined to be . The function is a map from to . SvM-p reduces down to the following, which we will denote as SvM-p-2.

| (3.3) | |||||

We make a few more comments before we discuss the properties of the models. SvM-c and SvM-p can also be thought of in the framework of the Dependent Dirichlet Process or DDP (MacEachern, 2000). To understand the DDP, we need to briefly introduce the Dirichlet Process. Given a base distribution, , and for , a Dirichlet process assigns weights, , to atoms or draws, , from . If , then the weight for is given by in the stick breaking representation (Sethuraman, 1994). A Dependent Dirichlet Process extends the Dirichlet Process by attaching separate stochastic processes to and . If a stochastic process is based on location, nearby distributions that use DDP atoms can resemble each other (MacEachern, 2000). While we assume a finite number of components, we view as the means of a von Mises distributions for our models. Then, in this framework, SvM-c only attaches a stochastic process to whereas SvM-p only places a stochastic process on . Note that we do not endow stochastic processes to both and in this work because such a model might be too rich to depend only on the spatial information.

We also wish to discuss some notation. Because of our convention with SvM-p-2, we will denote the number of von Mises distributions after the model if we need to specify . For instance, SvM-c-3 indicates the model SvM-c with . The one exception to this guideline is SvM, which is SvM-c with and introduced in the supplementary material (cf, (7.3)).

Finally, despite the focus on the circular case, the framework we introduce can easily be extended into directions of higher dimensions. Based on the discussion in Section 2.4, we can plug in the von Mises-Fisher in place of the von Mises distribution. We can also use the higher dimension version of the projected Gaussian process as a prior for the von Mises-Fisher for SvM-c. The output from that process is marginally a unit vector, which can serve as the mean parameter for a von Mises-Fisher distribution.

3.2 Model Properties for Spatially Dependent von Mises Model

To better understand our models, we shall derive the prior circular mean, circular variance, and circular correlation for SvM and SvM-p-2. Due to space constraints we do not display the results for SvM-c because one can easily combine the iterated expectation formula with the results for the special case SvM to obtain such results. Due to lack of conjugacy, deriving properties for posterior distributions is difficult. Nonetheless, the following results are useful because practitioners can use them when setting informative priors. While the definition for the circular mean and variance are given in equations (2.7) and (2.8) respectively, we will calculate a notion of correlation proposed by (Jammalamadaka and Sarma, 1988). If and have means and respectively, then the correlation is defined to be

| (3.4) |

These expectations are taken over the interval with respect to some distribution on the circle, , or its marginal distributions. As noted by Jammalamadaka and Sarma, this is equivalent to

| (3.5) |

At a high level, the circular correlation is comparing how tightly concentrates around versus how tightly concentrates around . Then, the correlation defined in this manner has the usual desired properties (Jammalamadaka and Sarma, 1988). For instance, if and are independent, the correlation is 0.

SvM For SvM specified in (7.3), we will assume that there is a global . This is not unreasonable because when we use a hierarchical prior for , we set to a small value. Then, the circular mean, variance, and correlation are the following.

Lemma 3.1.

If and are generated according to SvM outlined in (7.3) with the random variables associated with them labeled accordingly and with and , , , then

| (3.6) | ||||

| (3.7) | ||||

| (3.8) |

The above lemma reveals the following characteristics of SvM. First, the prior circular mean for is . It is nice that this mean can be set so easily. Based on this, we say that if and , then SvM is centered at or has mean . Because this holds for any and , we might also say that of SvM-c is centered at . Second, the prior circular variance involves multiplying the concentrations of the von Mises’ distribution and mean parameter according to the projected normal distribution. This demonstrates a few ways the Gaussian process can change the prior circular variance without changing the prior circular mean. Recall that in (3.7). As , whereas the asymptotics of Bessel functions can be used to show that when and (Watson, 1995). The former occurs if or . As a result, the respective distribution for or and becomes uniform. On the other hand, when or while remains unchanged. In other words, becomes more concentrated at or . Note however that even if with probability 1, but is finite, the circular variance of is that of a von Mises distribution with concentration parameter, . If , the circular variance is 1 and will be uniformly distributed. This further supports our earlier observation that when SvM is considered in a generative sense, the von Mises distribution adds noise. Finally, it is difficult to compute the exact form of the circular correlation due to the interactions between the terms in the expectation and the projected normal distribution. Fortunately, it is straightforward to compute these values by simulation. Wang and Gelfand briefly explored this in their 2014 paper on projected Gaussian processes.

SvM-p We next compute the circular properties of SvM-p. Unlike before, there is no explicit distribution for the inverse logit or general inverse logit transformation of a normally distributed variable. Consequently, we will first derive a formula for any choice of hyperparameters to allow practitioners to understand how their choice will affect these quantities. We do so under the assumption that the von Mises parameters, , and , are fixed. This assumption is a simplification because we can set , , , and to their prior expected values. We then will calculate them for the choices we specified in this paper for the SvM-p-2 model. Under these assumptions, we have the following lemma.

Lemma 3.2.

We now discuss the properties in Lemma 3.2. In , SvM-p’s mean direction is an average of the components’ mean direction weighted by how concentrated each component is around its mean direction and the probability that an observation belongs to a component. If there are two components that are equally concentrated around their mean direction and equally likely of being selected, we can use trigonometric sum to product formulas to show that will be the average of the components’ mean angles. Otherwise, simulation must be used to understand how changing the hyperparameters of the Gaussian process affects and the mean angle . The circular variance in (3.10) is similar to the circular variance of SvM described in (3.7). From each component, we get the product of how tightly the observation concentrates around that component’s mean direction and how close that component’s mean direction is to the model’s mean direction. The circular variance in (3.10) is also like the circular mean of SvM-p in (3.9) because the probability parameters again serves as the weights for a convex combination of each component’s concentrations.

The numerator of the circular correlation in (3.11) is of interest. Each term in the numerator’s sum is comprised of three things. First, it has a comparison between the means concentrating around each other and the difference of one mean from the model mean concentrating around its negative counterpart. Next, it holds the product of the observations’ concentration around the mean directions with respect to the observations’ cluster. Finally, it contains the joint probability of the observations’ cluster memberships. It is this probability that will be affected by the spatial information and Gaussian process. At a high level, if observations are "nearby", they are likely to belong to the same cluster. More weight will be placed on the terms coming from the observations belonging to the same cluster. What observations are considered closed is determined by the hyperparameters of the Gaussian process.

SvM-p-2 We now calculate these properties for the SvM-p-2 model. Using the notation of the model (3.3), we will also assume that and . One technical issues arising in computing these quantities is that , which is intractable. Instead, we will bound any expectation involving the logistic function with the functions, and . We define , where is defined as following:

| (3.12) |

We will additionally assume that to ensure that for and for . Under such assumptions, . As a result, these functions, and , are not a bad choice.

We can also use these functions to prove that under our assumptions. This fact and Lemma 3.2 then gives us the following lemma.

Lemma 3.3.

We make the following comments based on the lemma above. First, because both component’s are equally favored, , , , and for the prior mean and variance become more important. The SvM-p-2 model’s prior mean direction is completely determined by these parameters. For the model’s prior circular variance, the concentration term is the average of the two components’ concentration terms, which underscores the importance of and . If we want the Gaussian process to have more of an effect on the prior mean or variance, it is necessary to change the mean for the Gaussian process. It can be shown that for distributed according to any normal distribution with mean 0. Next, in (3.15) can be expanded and written as a function of . Doing so shows that the numerator again represents the difference between the concentration of two observations belonging to the same component and the concentration of two observations belonging to different components. It is then possible to bound with . Due to the length and technical aspects, we leave the details of this derivation and the expansion to the supplementary material.

4 Posterior Inference

We now describe how to fit our models. Fitting SvM-c can be difficult because of the underlying non-Euclidean geometry of its parameter space. We will first describe the basic sampling schemes based on the Hamiltonian MCMC approach, and then discuss techniques for exploiting the geometric structures via a suitable application of elliptical slice sampling.

Sampling algorithms We use the following approaches to sample from our models. For SvM-p, we use Hamiltonian Monte Carlo (HMC) to sample from the following posterior:

Here, is the vector such that if , then . Further, note that the probability for a single observation is the following:

In other words, we marginalize out the label. As a result, we are using HMC to sample for ; ; and according to the non-centered parametrization.

Then, the gradients for the log likelihood and thus the update for the momentum vector are given below.

-

•

For and , the gradient for is the following:

(4.1) In the two parameter case, this reduces to the following:

(4.2) -

•

For , the gradient for is the following:

(4.3) -

•

For , the gradient for is the following:

(4.4)

On the other hand, for SvM-c, we use the following blocked Gibbs approach:

-

•

For , sample given ; ; ; and according to the following probability:

-

•

For , sample given , ; ; and using the elliptical slice sampling outlined in Algorithm 2 (Murray et al., 2010). If we use the terminology of the paper, the normal prior and the likelihood that we are sampling are and respectively.

-

•

Sample and given ; ; and using HMC and the following probability:

Unlike SvM-p, we sample for the labels, , because the mixing appeared to be better according to the trace plots.

To help the samplers, we used initial values obtained via a regularized version of Expectation Maximization algorithm derived from SvM-c and SvM-p. We leave the details for these algorithms to the supplementary material.

Exploiting geometric structure To sample SvM-c in an efficient manner, we need to sample for the mean angles while respecting the spatial information, which is embedded in the Gaussian process’ covariance matrix. HMC has trouble doing both even if we change the model parametrization. In one parametrization, the mean angles can be sampled using HMC, but at the cost of having to invert the covariance matrix. An alternative parametrization allows HMC to propose moves according to the covariance matrix without inverting it. However, these moves marginally lie in and may not result in new angles being sampled even if the proposal is accepted. For example, a marginal move along a ray from the origin might be accepted even though remains the same. Note that this is not the case for SvM-p because the Gaussian processes are mapped to probabilites via the general inverse logit function. Hence, each marginal move represents a different mixing probability for each observation. More discussion of why HMC struggles for SvM-c and not SvM-p and the exact parametrization discussed are given in the supplementary material.

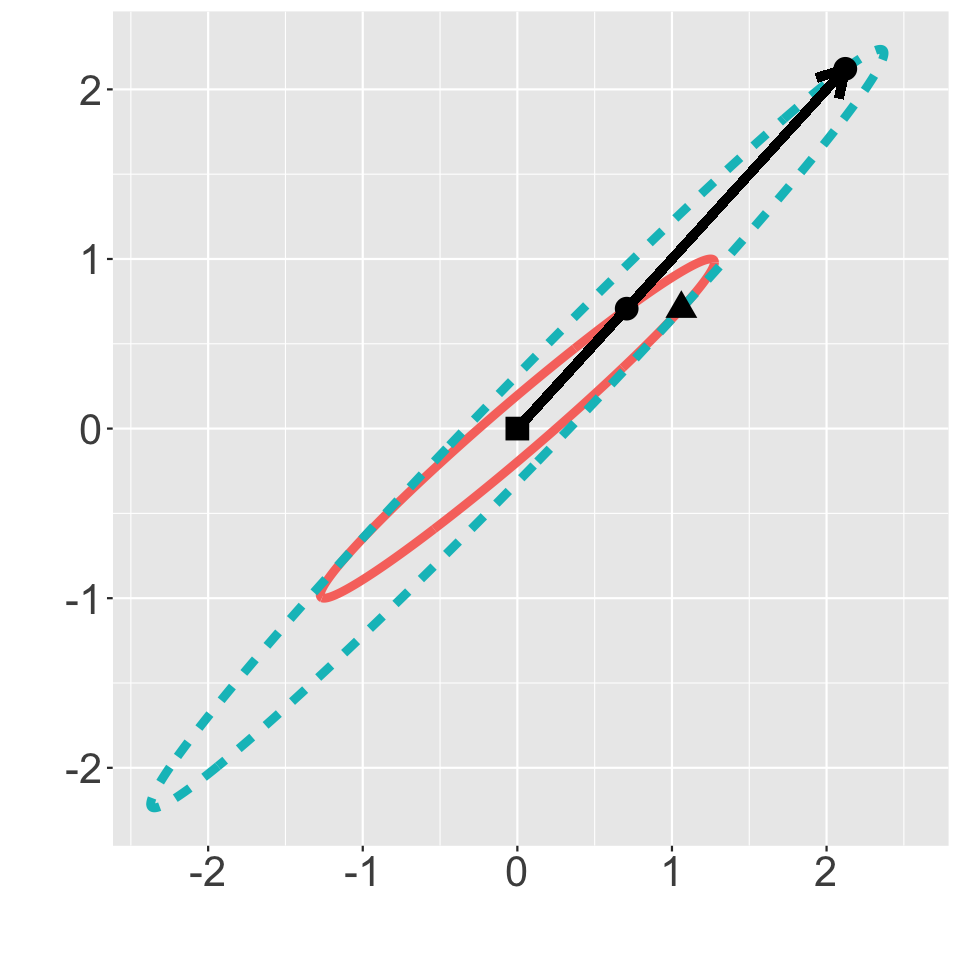

We turn to elliptical slice sampling instead (Murray et al., 2010). This technique allows us to draw samples for a random variable distributed according to a Gaussian prior with zero mean and any likelihood. For SvM-c, we use the elliptical slice sampler to sample for for . In this case, the Gaussian prior has covariance . Following the notation of the paper, we let represent the current location of . If we use the transformation specified in (2.1) on to get , then the likelihood is defined as follows: The likelihood becomes the following:

Note that even if is not included in the likelihood because , we still propose and . This will prove useful for predictive purposes.

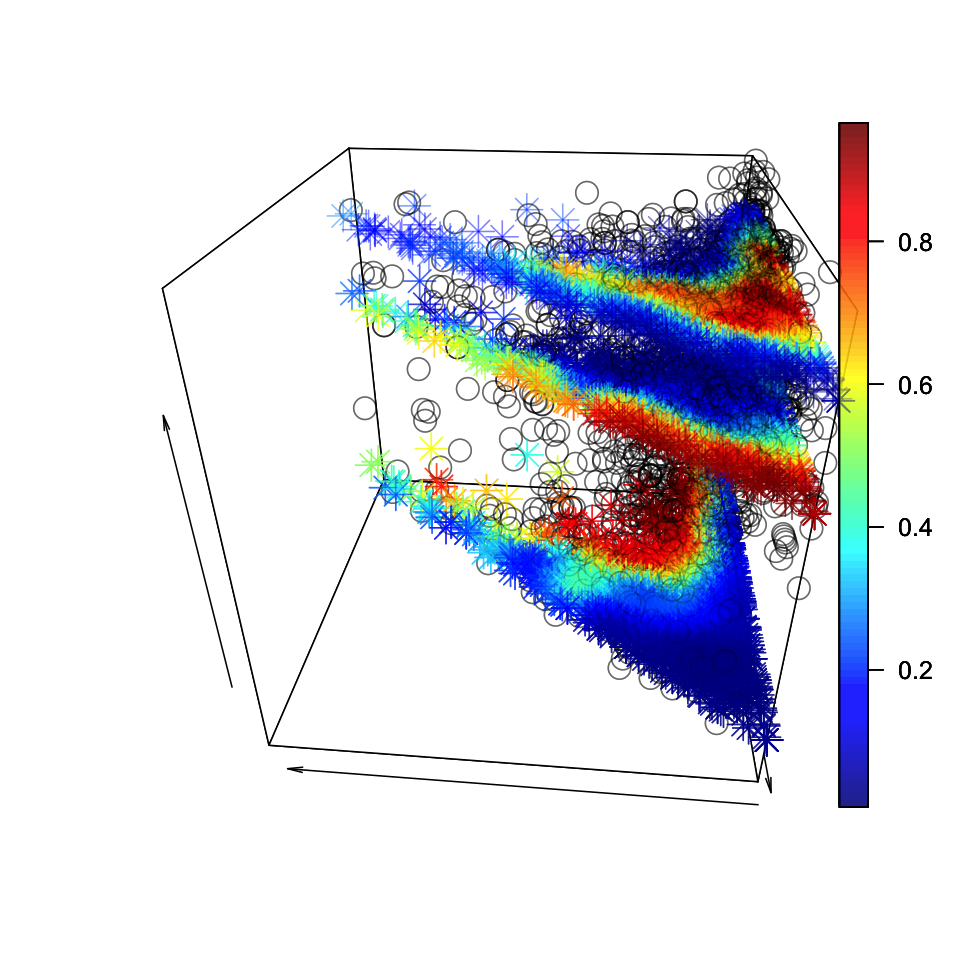

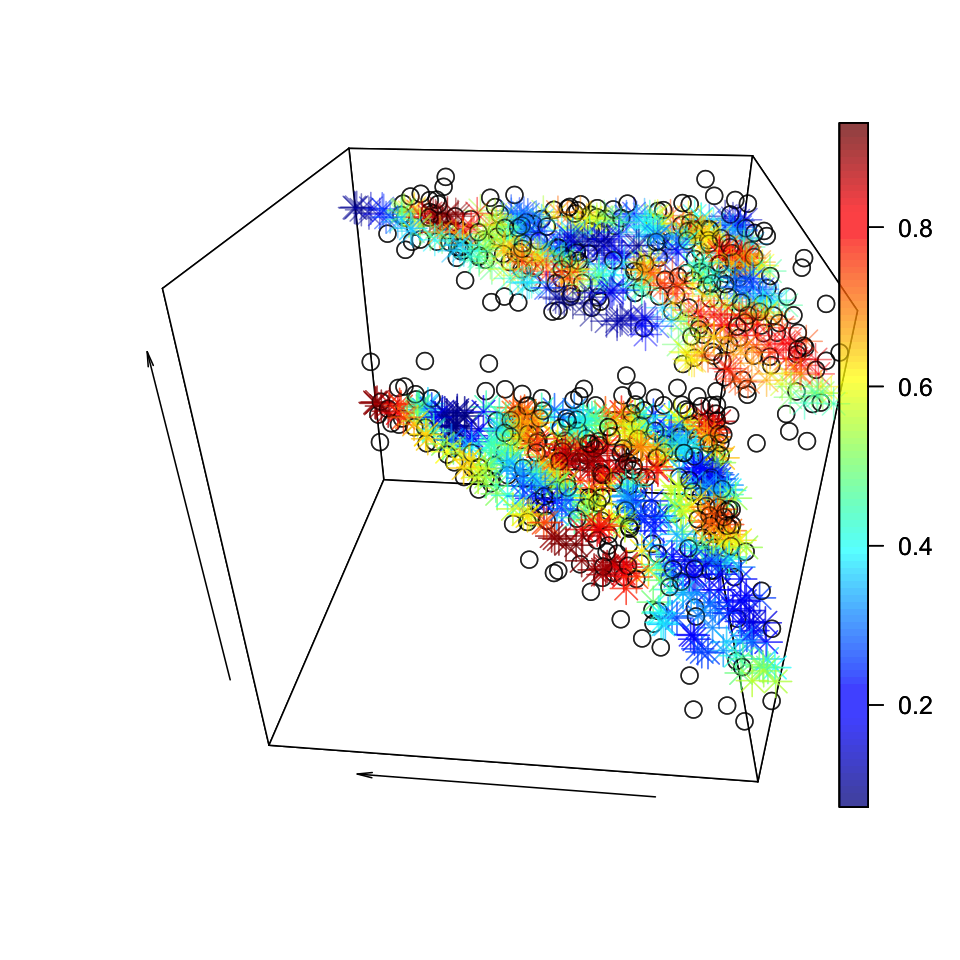

As seen in Figure 2, the elliptical slice sampler is marginally a sensible way to explore the space if and . We can then explore the entire space of with each run of the slice sampler. Unfortunately, if we set and to be , will be marginally distributed according to a uniform distribution. By not setting and to be , Figure 2 shows us that not only can the sampler potentially explore a subset of random angles, but also the subset might depend on its current location in and the point used to determine the ellipse. This might affect the next draw because for the same value of , the range of the next may be different. Still, even with this limitation, the elliptical slice sampler allows us to propose a valid move in the space of that respects the covariance information from the Gaussian process. Due to it being hard to characterize the dependence of the next draw on the location, we thin our MCMC chain to mitigate this issue. Luckily, the elliptical slice sampler runs reasonably quickly so this does not impose too much of an additional computational burden.

5 Simulations and Results

In this section we shall present a simulation study for the introduced models and then an application to the analysis of the income proportion data set.

5.1 Simulation study

Simulation overview The simulation study is conducted with following goals in mind. First, we wanted evidence that if we used our models for inference, our models could correctly recover the model parameters for data generated according to their respective models. Next, with this menagerie of simulated data, we could examine how these models behave in mis-specified settings and how to address model selection. Then, while fitting these models, we might notice inefficiencies in our sampling scheme and develop better approaches. Finally, inspecting the results might yield additional insights about the behaviors of these models.

To that end, we used a uniform distribution to generate 500 "locations" in . We created observations in six different ways. First, we generated observations using Von Mises(, 5). Next, we created them using a mixture of Von Mises(, 5) and Von Mises(, 10) with mixing probability of 0.3 and 0.7 respectively. As discussed in the supplementary material, these models are the iV and iVM models respectively. While these two methods did not use the spatial information, the remaining methods do. Third, we simulated observations according to SvM specified in Model (7.3) with a prior mean of for all locations. Fourth, we created them according to SvM-c specified in Model (3.1). One component’s mean was centered at and the other component’s mean at . There was equal probability of using either component. Next, we used the SvM-p model, (3.2), to simulate observations. We again used means of and . Finally, we simulated according to SvM specified in Model (7.3) with a prior mean of for all locations. This will test whether our model can handle data that appears to be separated due to where we set zero, but is actually connected.

Simulation model fitting We fit the SvM, SvM-c, and SvM-p models to these simulated observations using the approaches outlined in the previous section. Because there was at most two components, we only fit the two component versions of SvM-c and SvM-p to our simulated observations. Then, for the Gaussian processes, we used the squared exponential kernel with . For SvM-p, we set and = 0. Meanwhile, for SvM and SvM-c model, we set . We set for SvM and and for SvM-c. These values correspond to , , and respectively. We set and for SvM and SvM-c concentration parameter’s hierarchical prior. Our goal for these choices of parameters was to capture a larger range of probabilities for SvM-p whereas we wanted components to be more distinct for SvM and SvM-c models.

means in orange

fitted means in red

fitted means in red and blue

fitted means colored by

| Simulation | = 1.36 (0.41, 2.16) | ||

| = 4.85 (3.53, 5.64) | |||

| SvM cf. (7.3) | = 3.15 (1.93, 4.35) | = 0.01 (0.00, 0.04) | — |

| SvM-c cf. (3.1) | = 1.42 (0.90, 1.97) | = 2.79 (2.17, 3.52) | = 0.54 (0.49, 0.58) |

| = 4.79 (4.38, 5.20) | = 8.01 (6.11, 10.52) | = 0.46 (0.42, 0.51) | |

| SvM-p cf. (3.2) | = 1.38 (1.24, 1.51) | = 1.44 (1.07, 1.91) | = 0.58 (0.32, 0.82) |

| = 4.77 (4.68, 4.86) | = 4.08 (2.75, 5.55) | = 0.42 (0.18, 0.68) |

For posterior inference, any step involving HMC was implemented in Stan (Stan Development Team., 2018). Otherwise, we implemented our approach in R. Using this code111Our code can be found at https://github.com/rayleigh/housing_price., we ran four chains and 2000 iterations of the HMC sampler for SvM-p with 1000 iterations as burn-in. Meanwhile, for SvM and SvM-c sampler, we ran four chains and 10000 iterations, using every fifth iteration after the first 5000 iterations. On a cluster using 2x 3.0 GHz Intel Xeon Gold 6154 as its processor and with 192 GB as its RAM, SvM-c took between four and a half to eight and a half hours whereas SvM-p took between 8 and 20 minutes. We checked for convergence by primarily looking at trace plots of parameters and examining Rhat values for non-circular values as computed by Stan (Gelman and Rubin, 1992).

Simulation model findings These are a number of interesting results to report from these experiments. First, as exemplified by Figure 3 and other such figures in the appendix, the models appeared to correctly capture the mean surfaces for data simulated from their respective models. For example, the fitted mean surface for SvM matches the simulated mean surface, even when the simulated surface is centered at . While the numerical summaries of the random variables were slightly off, this could be due to the posterior credible intervals being averaged across all locations. Next, homogeneous models may have trouble capturing heterogeneous patterns. For instance, the fitted mean surface from SvM tries to match the observations as much as possible in the case of SvM-p or essentially gives up and becomes a uniform distribution in the case of SvM-c. It does not recognize the simulated mean pattern of either model. Finally, the results demonstrate that SvM and SvM-c are in a different class of models compared to the class of models SvM-p belongs to. As seen in Figure 3, SvM-p tries to put the von Mises distributions at the two components’ overall mean with small concentration parameters in the case of SvM-c. The fitted model is trying to make up for the variation in the observations by returning two diffuse von Mises distribution. A similar result happens in the SvM case, except that the two von Mises are placed at an "lower" and "upper" mean. In contrast, SvM-c correctly recovers the simulated mean surfaces in the SvM-p case, but it can only roughly capture the average probability of each surface. Interestingly enough, in the SvM case, SvM-c matches one fitted mean surface to the simulated mean surface and essentially "zeroes" out the other surface.

Simulation model selection We decided to compute the posterior predictive probability for another 50 random locations and their observations simulated according to the different scenarios in order to model select. Let represent the withheld locations, the withheld data, a posterior draw for the parameters based on and , and a draw for the parameters for and . The posterior predictive probability is given as follows.

| (5.1) |

We discuss how to compute this probability in the supplementary material because it is straightforward to compute according to our models defined in and . It is also simple to sample from due to the conditional formula for the Multivariate normal distribution to generate these draws from the Gaussian processes. We take advantage of this fact by sampling 100 times from to create our posterior predictive draws. To ensure that both the posterior draws and the posterior predictive draws speak equally, we first averaged across posterior draws. We then averaged these means across the posterior predictive draws. This gives us a sense how likely our posterior is on withheld data.

| iV | iVM | SvM Mean | SvM-c | SvM-p | SvM Mean | |

| iV | -39.85 | -78.20 | -68.08 | -91.99 | -92.05 | - |

| iVM | -39.92 | -47.60 | -68.24 | -86.47 | -61.80 | -85.69 |

| SvM | -42.42 | -84.28 | -59.34 | -92.43 | -97.86 | -63.49 |

| SvM-c | -45.78 | -56.79 | -62.19 | -73.40 | -70.90 | -60.67 |

| SvM-p | -39.98 | -49.60 | -66.61 | -90.03 | -62.78 | -73.54 |

Table 3 shows the results from doing so. There are a few interesting things to note. First, the posterior predictive probability confirms that the homogeneous models performs poorly in any heterogeneous scenarios. Next, the posterior predictive probability calculated after fitting SvM-p is higher when the means of the von Mises used to generate the data are constant. On the other hand, the posterior predictive probability calculated after fitting the SvM and SvM-c models is higher when the von Mises components’ means are spatially correlated. We might expect the former because spatially correlated observations might be overfitted to the data. For the latter, SvM-p might have difficulty in capturing the variability and thus cannot accurately predict the next value. Finally, while we do not report these cases, there are scenarios in which SvM-c can perform poorly according to the predictive posterior probability. When we plot them, we see that the worst performing observations lie between the fitted mean surface. Even though the fitted mean surface and concentration parameter may be mostly correct for the observed data, the model is being penalized for being "over-certain" about the withheld data. This means that if we desire well-separated components, the observations must also be well-separated. Even with this caveat, we use the posterior predictive probability to model select because it allows us to compare models that are different in their approaches and generally picks the model used to generate the data in simulation.

5.2 Data analysis

Data overview We now fit the proposed models to the random directions observed in the year to year income proportion changes in the Home Mortgage Disclosure Act (HMDA) data for each Census tract of Los Angeles County. While HMDA data is publicly available, the dataset we worked with is not because it is fused with data purchased from a private company. For this paper, there are three income categories: $0 to $100,000, $100,000 to $200,000, and greater than $200,000. We choose to examine these proportions because the number of mortgages recorded in a year differ per Census tracts. Analyzing proportions allows us to potentially ignore the biases that might arise from these differences. We also assume that these proportions observed are the true income proportions for a Census tract. This assumption may not be too unreasonable because people are likely to move into neighborhoods with demographic characteristics similar to their own.

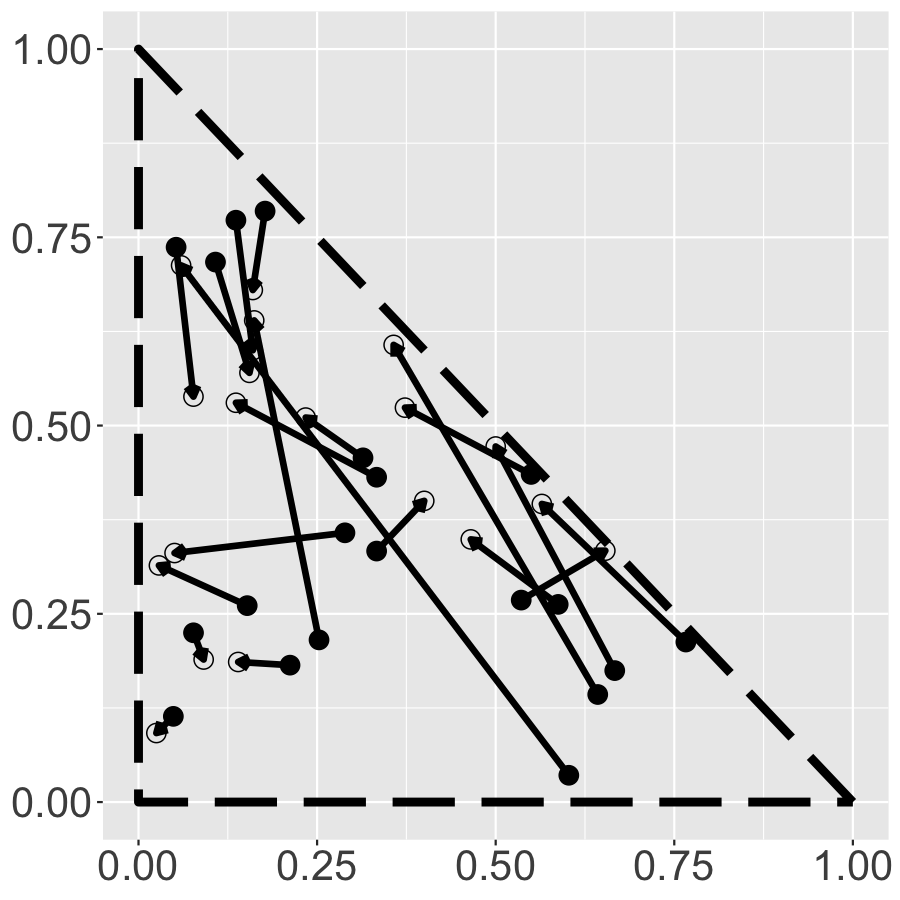

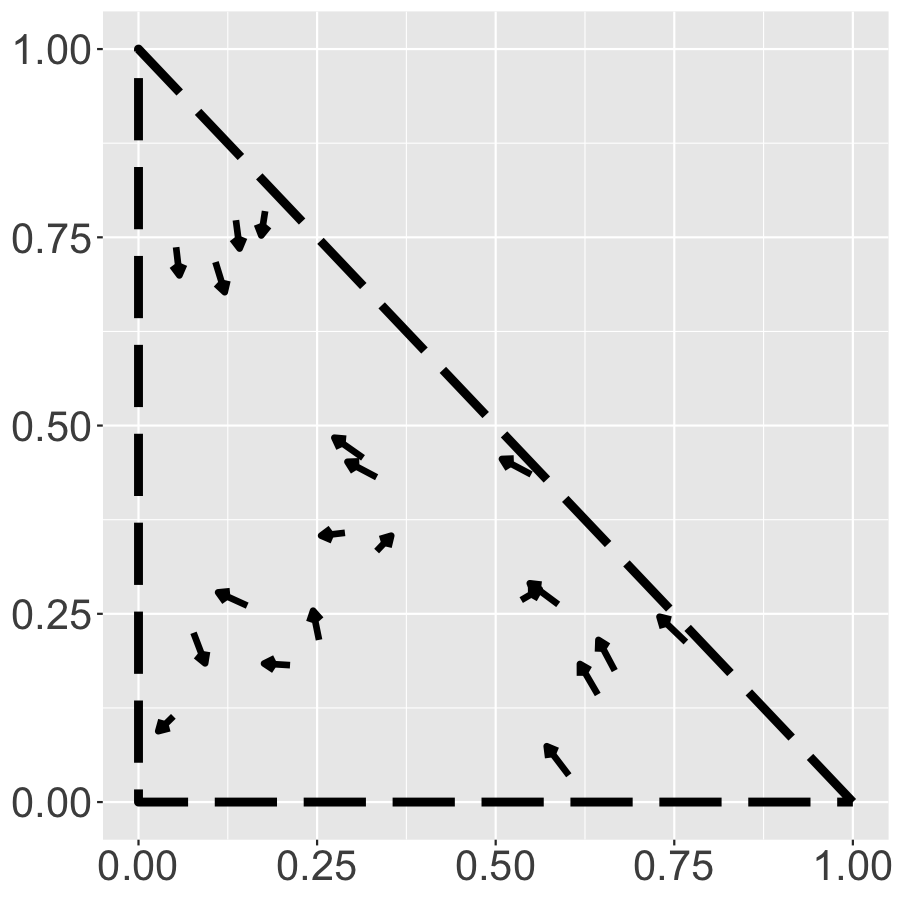

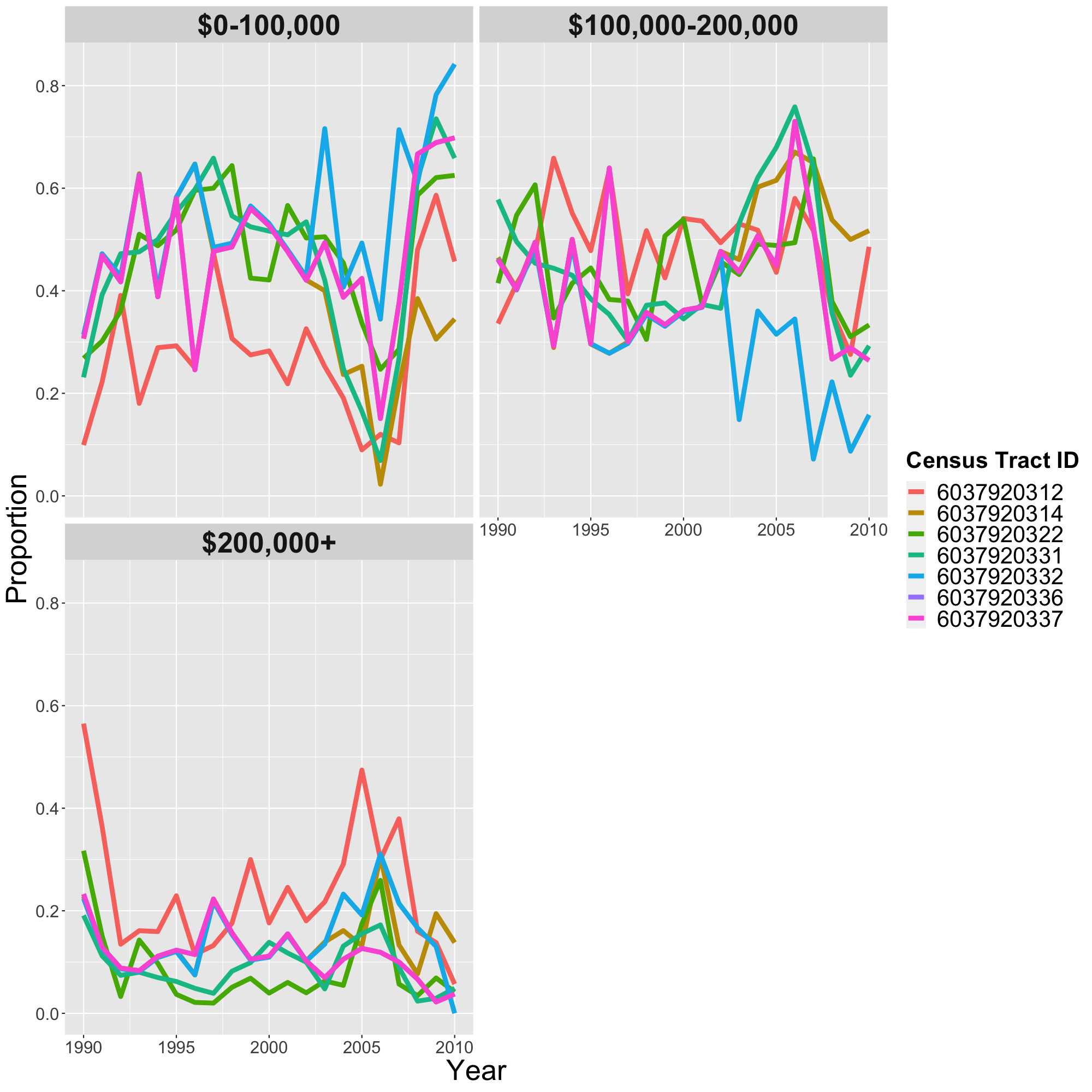

To model how these income proportions change, we also decided to use the proportions as locations because as seen in Figure 4, it can be challenging to do so otherwise. If we examine how the income proportions evolve for Census tract 6037920336 and its adjacent tracts, we see that the income proportion for the top category change in a similar manner. However, the proportions for the lower two income categories only mostly shift in a similar manner after 2005. Further, there is one adjacent Census tract that diverges from the other tracts for the second income category during this time period. As a result, it is hard to imagine a model that only uses Census tract information because it might need to borrow strength for one income category, but potentially ignore it for other categories. If we then extract the random direction using the procedure discussed in the next paragraph, Figure 4 also shows that it might not be helpful to model these directions using Census tracts. Even though the random direction is not uniformly distributed, the pattern appears to be the same across the different Census tracts.

Random direction Because we have the income proportion for a Census tract for a given year and the next year, we can extract the random direction using the following procedure. Let be the income proportion for one year and be the proportion for the next. Set and to be the spherical coordinates for . Then, define to be the following matrix:

This matrix transforms to . It is orthogonal because the first column is the spherical coordinates for and the second column is the spherical coordinates for and . Its inverse allows us to define a spherical coordinate system based on . If and and represent the spherical coordinates of , then is the random direction and represents how "far" goes in that random direction.

This random direction has some nice properties. Even if is zero for any proportions, the random direction can still be extracted and examined. It is also interpretable. In spherical coordinates, changing for a fixed only affects the first two coordinates. Due to the transformation defined in the previous paragraph, a change in the first two coordinates changes how the first two columns of the matrix that transforms to are weighted. To understand this random direction, we need to comprehend what the first two columns represent and how the random direction interacts with these columns. Because the first column represents the spherical coordinates for (, ), the simplest way to understand this column is to compare and . As corresponds to and for some , this first column represents a push away from the third income category. On the other hand, if we use a similar logic to compare and against and , then we see that the second column represents a pull toward the second income category. Because the first and second coordinate include and respectively, we will examine , , , and . Note that at and , the first coordinate will be and and the second will be zero by definition. A random direction of represent a push away from the third income category whereas represents a pull toward. The reverse is true for and . We can say that a random direction of and represent a pull toward and push away from the second income category. It is the opposite because the first column is a push away from a category whereas the second column is a pull toward a category.

We fitted our models to these random directions with one additional pre-processing step. We removed duplicated directions so that each location has at most one observation. This was done because duplicated directions at the same location should happen with probability zero according to our model and they can be easily identified. Indeed, their properties are further discussed in the supplementary material. As a result of this step, the number of observations are reduced from between 2302 to 2356 per year to between 1704 to 2164 per year. However, while we used the same priors that we utilized for simulation, it was still unclear what to set the hyperparameters for the squared exponential kernels. To pick, we used the same hyperparameters as simulation as a baseline. We then compared it against , and and , and for SvM-c and , and and , and for SvM-p.

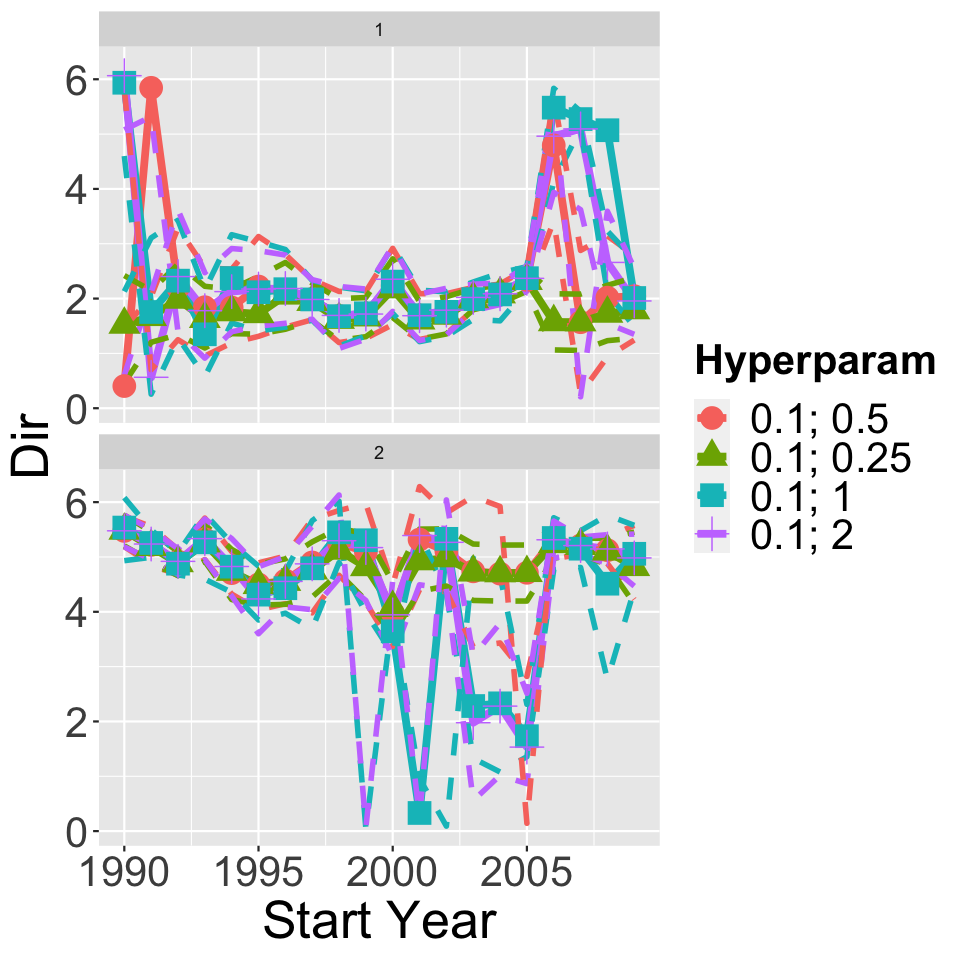

Hyperparameter and model selection Some of our findings from these experiments can be seen in Figure 5. If we examine SvM-p first, we see that while the overall mixing probability averaged across all locations remain mostly the same, the credible intervals averaged across all locations expands as increases or decreases. This is to be expected because increasing allows for a wider range of values for the Gaussian process whereas decreasing means the mixing probability is more sensitive to the observed direction at each location. Next, if we examine SvM-c, changing the hyperparameters does not appear to affect the first mean averaged by location between 1995 and 2005. However, there is greater stability in the second mean averaged by location when is changed, but not when is altered. Indeed, the latter only appears to have stability before 1998. Still, there are differences in the mean surfaces hidden by this statistic. If we focus on the results from 1996 to 1997, we see that while the second mean surface is mostly similar when we change , the first mean surface varies more when increases. For instance, the surface is mostly flat when , but the surface appears to be a series of thinly connected pillars that span zero to when . This makes sense that neighboring values on the mean surface can vary drastically when grows. On the other hand, the overall shape of the mean surface in 1996 mostly remains the same as we increase from 0.05 to 0.25. This is again particularly true for the second mean surface. However, the first mean surface becomes smoother as rises. This suggests that for this year, neighboring points are similar in value and the mean surface must reflect this fact.

After running these experiments, we selected the hyperparameters that had the average highest log posterior predictive probability across all years. Here, we take the average with respect to the number of observations. For SvM-c, this was and . The hyperparameters selected for SvM-p-2 was and . We then used these results to explore the choice of kernel. The other kernels were the Matern with three halves and five halves degrees of freedom. The Matern with one half degree of freedom was not compared because previous experiments demonstrated that kernels leading to results that are less smooth did not perform as well and the Matern kernel with one half is such a kernel (Rasmussen and Williams, 2006). For SvM-p, the results remained similar compared to the results from the optimal squared exponential kernel model. Indeed, the posterior predictive probability is similar between these models. Meanwhile, choosing the Matern kernels or the optimal squared exponential kernel for SvM-c result in similar mean directions averaged by location. However, if we again look at the mean surface from 1996 to 1997, we notice differences. While the lower mean surface is similar from the Matern kernel with five halves degrees of freedom and squared exponential kernel, the surface is more dispersed for the Matern kernel with three half degrees of freedom. However, for non-lower income neighborhoods. the top mean surface is more scattered for the Matern kernel than for the squared exponential kernel. Interestingly enough, the surface from the Matern kernel with five halves degrees of freedom is more diffuse even though it is smoother than the surface from the Matern kernel with three halves degrees of freedom. One other key difference is that the SvM-c models with the Matern kernels performed worse than the same model with the squared exponential kernel. This suggests that while the mean surface for the random direction might be sensitive to the choice of kernel, regions that are likely to move in the same direction are not sensitive.

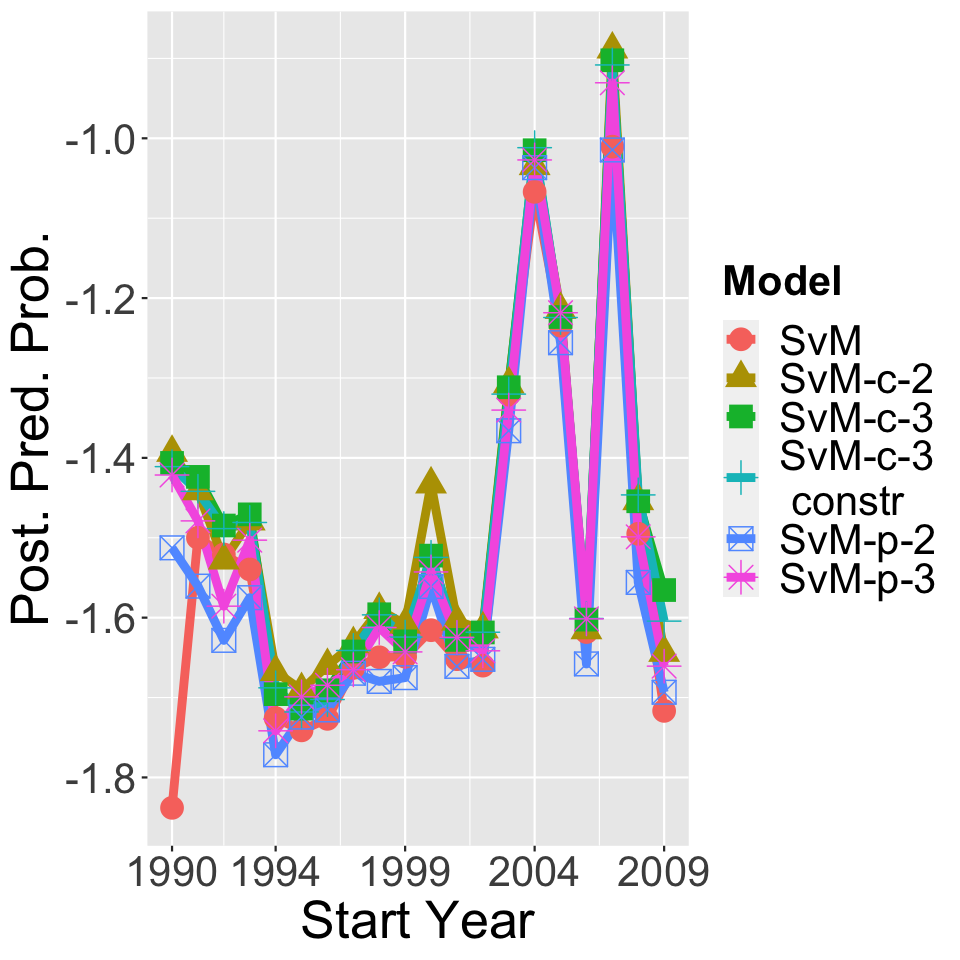

Finally, we also wanted to compare the results from the square exponential hyperparameter experiments against SvM and SvM-c-3 using the hyperparameters selected for SvM-c and SvM-p-3 with the hyperparameters selected according to SvM-p-2. Note that for years 1991-1993, 1996-1997, 1998-2000, 2005-2010, we used a strong von Mises prior on the mean component to force identifiability for SvM-p-3. Otherwise, we used an uniform prior on the mean component. Further, because of extreme estimates in the concentration parameters, we also ran a version of SvM-c-3 with the concentration parameter constrained to be between 1e-4 and 20. According to the log posterior predictive probability given in , SvM-c-2 perform the best for all years except 1991-1994, 2003-2005, 2006-2007, 2008-2010, and potentially 2008-2009. For those years, SvM-c-3 or the constrained version performs the best. However, the posterior predictive probability for SvM-c-3 is close to that of SvM-p-3 for 2006-2007 and of SvM-c-2 for 2008-2009. This suggests that the average observed change in income proportion is better explained by one of two random direction surfaces that varies depending on the income proportion proportions. Further, it tells us that having two components is sufficient in most cases.

(SvM-c-2)

(SvM-c-3)

(SvM-c-2)

(SvM-c-2)

(SvM-p-3)

(SvM-c-3)

Findings and interpretation Based on the Table 4 and Figure 9 in the supplementary material, the fitted mean surface can be grouped into four phases: 1990-1991, 1991-1993, 1993-2003, 2003-2010. These phases correspond to the early 1990 recession, the transition from President George HW Bush to President Bill Clinton, the economic boom in the 1990s, and the recovery from the dot com bubble with the subsequent housing market crash respectively. Representative examples of each phase can be found in Figure 6. As an example of the stories these surfaces can tell us, consider 2005 to 2006 and 2006 to 2007. Like the two years before 2005, there is one surface that is an curved, half spiral increasing from to around if we follow it from neighborhoods with income proportions largely below $100,000 to neighborhoods with income proportions largely between $100,000 and $200,000 and then to neighborhoods with income proportions largely greater than $200,000. This suggests that for these years, the income distributions for all neighborhoods are being pulled up a category. However, there is another surface that while similar for neighborhoods of lower income, is centered around zero for neighborhoods with income proportions in the second and third categories. This suggests that there already is a push away from the third income category for these neighborhoods, two years before the housing market crash. Because the posterior predictive probability is similar for SvM-c with three components and SvM-p with three components, it is interesting to see these two aforementioned mean surfaces re-partition into three. As hinted by the lower half of the non-spiral surface, there is one component at either or . This suggests a medium to semi-strong pull toward the second income category. Then, for the upper half of the non-spiral surface, SvM-p takes two components. Interestingly enough, as seen in Figure 6(e) and 6(f), the areas of high probability for SvM-p’s two components match the third component of SvM-c with two components. These two mean components are centered at roughly and , which represent semi-strong pushes away from the second and third income categories. In other words, the data already suggests the potential recession that might happen in the next year. Finally, the spiral mean surface changes as well and adopts characteristics of the other mean surface for the third mean surface for SvM-c-3 in 2007. As seen in 6(f), it matches the first surface for neighborhoods with the lowest income proportions before rising rapidly to meet the other mean surface for neighborhoods with the second highest income proportions. It then comes back down to , i.e. a pull toward the second income category, for neighborhoods with the highest income proportion.

6 Conclusion and Future Directions

In this paper, we have introduced two types of hierarchical models to draw inference about the random directions for simplex-valued measurements and discuss how these models might be utilized. These approaches creatively use the data’s location within the simplex to do so. Because the average random direction across all location or the "mean surface" and the mixing probability are important, the "spatial" information is naturally fed into them. Indeed, SvM-c is the model when this information is fed into the former whereas SvM-p is the model when this information is fed into the latter. Then, to better understand how to set the hyperparameters of these models, we derived the models’ prior circular means, variances, and correlations. We discussed how to fit these models using sampling schemes that respect the geometry of the parameters of interest. For instance, we used elliptical slice sampling to sample for the mean surface in SvM-c. Using these findings, we then applied the models to simulated data and then analyzed a data set of income proportions and random directions observed for a set of Census tracts in LA County from 1990 to 2010. There is evidence to suggest that the random direction is associated with the Census tract’s income proportions observed in a given year and not the tract’s physical location. This means that the data set is a highly relevant real world example to apply our models to. Consequently, it is noteworthy that the patterns our models discovered matches and potentially clarifies real world economic trends during the same time period.

There are several directions worth exploring moving forward. We might extend these models to random directions in dimensions greater than two. This would allow us to analyze the random directions for data that lie in for . The LA County data set has sixteen income categories before we reduced them down to three. Fortunately, as discussed in the paper, both the von Mises distribution and projected normal distribution can be extended to angles in higher dimensions. These higher dimensional distributions can be plugged into our models in place of their lower dimensional analogues. Next, to better sample SvM-c or the higher dimensional equivalents, we might combine Multiple Try MCMC with elliptical slice sampling. This could provide a principled approach to consider the entire range of angles during each proposal step for the next mean angles and thus result in better mixing. Finally, we might merge our random direction models with a model for the magnitude in order to model the random movement. As discussed earlier, the two components of the movement were separated to achieve greater modeling flexibility and to better deal with the challenges posed by them. For instance, modeling the magnitudes and directions on the simplex’s boundary require special care because the range of valid movements and directions are limited. In addition, the magnitudes in the interior have to be treated carefully. In order for the simplicial constraint to be respected, certain magnitudes in certain directions are not possible.

References

- Aitchison [1982] Aitchison, J. (1982). “The Statistical Analysis of Compositional Data.” Journal of the Royal Statistical Society: Series B (Methodological), 44(2): 139–160.

- Allaband et al. [2019] Allaband, C., McDonald, D., Vázquez-Baeza, Y., Minich, J. J., Tripathi, A., Brenner, D. A., Loomba, R., Smarr, L., Sandborn, W. J., Schnabl, B., Dorrestein, P., Zarrinpar, A., and Knight, R. (2019). “Microbiome 101: Studying, Analyzing, and Interpreting Gut Microbiome Data for Clinicians.” Clinical gastroenterology and hepatology : the official clinical practice journal of the American Gastroenterological Association, 17(2): 218–230.

- Banerjee et al. [2015] Banerjee, S., Carlin, B. P., and Gelfand, A. E. (2015). Hierarchical Modeling and Analysis for Spatial Data. Number 135 in Monographs on Statistics and Applied Probability. Boca Raton: CRC Press, Taylor & Francis Group, second edition edition.

- Cressie and Wikle [2011] Cressie, N. A. C. and Wikle, C. K. (2011). Statistics for Spatio-Temporal Data. Wiley Series in Probability and Statistics. Hoboken, N.J: Wiley.

- Gelman and Rubin [1992] Gelman, A. and Rubin, D. B. (1992). “Inference from Iterative Simulation Using Multiple Sequences.” Statistical Science, 7(4): 457–472.

- Hernandez-Stumpfhauser et al. [2017] Hernandez-Stumpfhauser, D., Breidt, F. J., and van der Woerd, M. J. (2017). “The General Projected Normal Distribution of Arbitrary Dimension: Modeling and Bayesian Inference.” Bayesian Analysis, 12(1): 113–133.

- Jammalamadaka and Sarma [1988] Jammalamadaka, S. and Sarma, Y. (1988). “A Correlation Coefficient for Angular Variables.” In Statistical Theory and Data Analysis II: Proceedings of the Second Pacific Area Statistical Conference, 349–364. Tokyo, Japan: Elsevier Science Ltd.

- Kendall [1974] Kendall, D. G. (1974). “Pole-Seeking Brownian Motion and Bird Navigation.” Journal of the Royal Statistical Society. Series B (Methodological), 36(3): 365–417.

- Lee [2010] Lee, A. (2010). “Circular Data.” WIREs Computational Statistics, 2(4): 477–486.

- MacEachern [2000] MacEachern, S. N. (2000). “Dependent Dirichlet Process.” Technical, Ohio State University.

- Mardia and Jupp [2010] Mardia, K. V. and Jupp, P. E. (2010). Directional Statistics. Chichester; New York: J. Wiley.

- Murray et al. [2010] Murray, I., Adams, R. P., and MacKay, D. J. C. (2010). “Elliptical Slice Sampling.” Proceedings of the 13th International Conference on Artificial Intelligence and Statistics (AISTATS) (JMLR: W&CP), 6: 8.

- Neal [2011] Neal, R. (2011). “MCMC Using Hamiltonian Dynamics.” In Brooks, S., Gelman, A., Jones, G., and Meng, X.-L. (eds.), Handbook of Markov Chain Monte Carlo, volume 20116022. Chapman and Hall/CRC.

- Pawlowsky-Glahn et al. [2007] Pawlowsky-Glahn, V., Egozcue, J. J., and Tolosana-Delgado, R. (2007). “Lecture Notes on Compositional Data Analysis.”

- Pearson [1896] Pearson, K. (1896). “Mathematical Contributions to the Theory of Evolution.–On a Form of Spurious Correlation Which May Arise When Indices Are Used in the Measurement of Organs.” Proceedings of the Royal Society of London, 60: 489–498.

- Rasmussen and Williams [2006] Rasmussen, C. E. and Williams, C. K. I. (2006). Gaussian Processes for Machine Learning. Adaptive Computation and Machine Learning. Cambridge, Mass: MIT Press, second edition.

- Sethuraman [1994] Sethuraman, J. (1994). “A Constructive Definition of Dirichlet Priors.” Statistica Sinica, 4(2): 639–650.

- Stan Development Team. [2018] Stan Development Team. (2018). “The Stan Core Library.”

- Wang and Gelfand [2013] Wang, F. and Gelfand, A. E. (2013). “Directional Data Analysis under the General Projected Normal Distribution.” Statistical methodology, 10(1): 113–127.

- Wang and Gelfand [2014] — (2014). “Modeling Space and Space-Time Directional Data Using Projected Gaussian Processes.” Journal of the American Statistical Association, 109(508): 1565–1580.

- Watson [1995] Watson, G. N. (1995). A Treatise on the Theory of Bessel Functions. Cambridge Mathematical Library. Cambridge [England] ; New York: Cambridge University Press, 2nd ed., cambridge mathematical library ed edition.

- Wolfram [1998] Wolfram (1998). “Modified Bessel Function of the First Kind: Differentiation.” http://functions.wolfram.com/Bessel-TypeFunctions/BesselI/20/ShowAll.html.

Acknowledgements

This research is supported by the NSF Graduate Research Fellowship Program (Grant No. DGE 1256260). Any opinions, findings, and conclusions or recommendations expressed in this material are those of the author and do not necessarily reflect the views of the National Science Foundation. We also want to thank Professor Elizabeth Bruch for introducing us to the data set and for her discussions and Lydia Wileden for preparing the data. XN gratefully acknowledges support from NSF grants DMS-1351362, CNS-1409303 and DMS-2015361.

7 Additional Models

7.1 Independent Random Direction Models

The most elementary model based on the von Mises distribution is the independent von Mises or iV model. For this model, the observations are assumed to be identically and independently distributed according to one von Mises distribution with mean and concentration parameter . A von Mises prior on the interval with mean and concentration parameter is placed on . As discussed earlier in Section 2.1, setting is equivalent to putting a uniform prior on . Meanwhile, the concentration parameter has a Gamma prior with parameters and . In summary, the iV model is the following.

| (7.1) | |||||

If there is heterogeneity in the observations, an extension of the model is the Independent von Mises Mixture or iVM model.

| (7.2) | |||||

An observation can now be distributed according to one of von Mises distribution in the interval of . Each distribution has its own mean and concentration parameter . Moreover, each distributions’ parameters are given different priors.

7.2 Homogeneous Spatial Random Direction Model

We proceed to modeling spatial patterns of random directions. For homogeneous spatial random direction patterns, we incorporate spatial information through the components, i.e., the parameters of the von Mises distribution. In particular, we link a Gaussian process to the mean parameters because it is a straightforward way to collate nearby observations and borrow strength. This also leads to fairly interpretable draws from the Gaussian process. Due to the von Mises distribution being concentrated at its mean, results from these models can describe the preferred random direction for a given location.

We introduce a model that applies this approach. This is the Spatially varying von Mises distribution model or SvM. Each observation has a mean parameter, , and a concentration parameter, . We use the modified arctan function defined in (2.1) to element-wise transform two draws from the Gaussian process, , into the mean parameters, . The positive-valued concentration parameter, , is transformed via exponentiation from a real-valued , which is then endowed with a normal prior. In summary, SvM is the following.

| (7.3) | |||||

8 Model Properties

8.1 SvM model

We begin by discussing how we derive Lemma 8.2. After using the law of total expectation and trigonometric identities, we see that calculating the properties of ’s are reduced to that of the corresponding . Because and , is distributed according to [11]. We can extend the techniques in [19] to demonstrate that is equivalently distributed according to . With this insight, we can use the discussion in Section 2.2 to compute the circular mean and variance. Then, we have the following lemmas.

Lemma 8.1.

Let . Let be random variables, , , such that and . In addition, set . Then,

Proof.

Following the derivation in Appendix A of [19], we have that

Applying the change of variables formula and still following the derivation in Appendix A, we have that

Set , then

∎

Lemma 8.2.

If and are generated according to SvM outlined in (7.3) with the random variables associated with them labeled accordingly and with and , , , then

| (8.1) | ||||

| (8.2) | ||||

| (8.3) |

Proof.

When deriving the circular mean and variance, we’ll drop the subscript out of convenience. For the circular mean, i.e. the quantity in 8.2, by the law of iterated expectations,

Because

by Lemma 8.1, . Thus, following the argument in Appendix A in [19],

As a result, the mean angle must be by definition.