Deep Hedging: Learning Risk-Neutral Implied Volatility Dynamics

Abstract

We present a numerically efficient approach for learning a risk-neutral measure for paths of simulated spot and option prices up to a finite horizon under convex transaction costs and convex trading constraints.

This approach can then be used to implement a stochastic implied volatility model in the following two steps:

-

1.

Train a market simulator for option prices, as discussed for example in our recent work Bai et al. (2019);

-

2.

Find a risk-neutral density, specifically the minimal entropy martingale measure.

The resulting model can be used for risk-neutral pricing, or for Deep Hedging (Buehler et al., 2019) in the case of transaction costs or trading constraints.

To motivate the proposed approach, we also show that market dynamics are free from “statistical arbitrage” in the absence of transaction costs if and only if they follow a risk-neutral measure. We additionally provide a more general characterization in the presence of convex transaction costs and trading constraints.

These results can be seen as an analogue of the fundamental theorem of asset pricing for statistical arbitrage under trading frictions and are of independent interest.

March 2021. This version: July 2021

1 Introduction

One of the long-standing challenges of quantitiative finance is the development of a tractable stochastic implied volatility model.

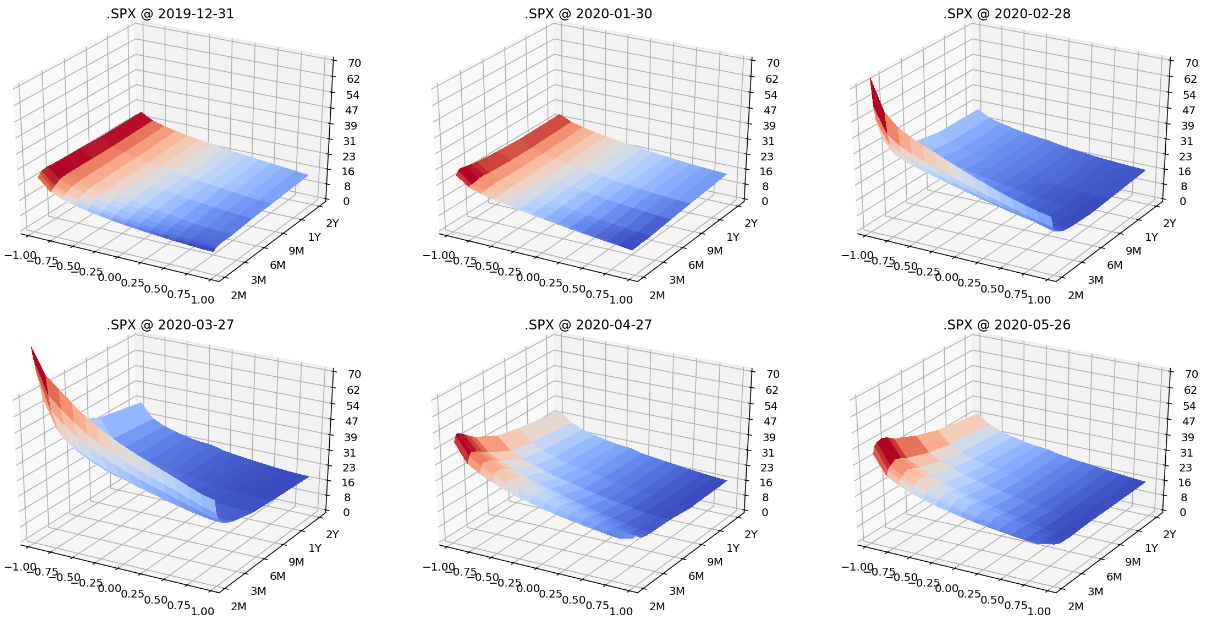

The aim of such a model is the simulation of spot and a number of options across strikes and maturities under risk neutral dynamics. Naturally, we will want to express option prices in a reasonably intuitive parametrization such as Black & Scholes implied volatilities. Moreover, we typically look at floating option surfaces, where implied volatilities are parameterized in time-to-maturity and moneyness, not in fixed maturity dates or cash strikes. Figure 1 shows examples of such historical surfaces.

The primary use case in practice for such models is in risk-neutral pricing where the value of any portfolio of financial instruments is given as an expectation. Since this is a linear operation it lends itself to mass-parallel evaluation of large portfolios of instruments. Computing a consistent hedge requires merely the computation of first order derivatives with respect to each of the hedging instruments.111It is worth noting that the vast majority of financial derivatives in equities and FX depends on spot, and not usually on option prices. Key exceptions are futures and options on volatilty indices such as VIX and VSTOXX. This approach, however, does not incorporate transaction costs or trading restrictions such as liquidity constraints or risk limits. For such a setup we have introduced our Deep Hedging Buehler et al. (2019) approach. As we will explain below even this non-linear approach to derivative pricing and hedging is easier to deploy in production when run under a risk-neutral measure.

Stochastic Implied Volatility

The classic quantitative finance approach to stochastic implied volatility models is specifying the model dynamics in a suitable parameter space under the risk-neutral measure with model dynamics designed to be somewhat analytically tractable. The working paper Brace et al. (2001) summarizes various Heath-Jarrow-Morton (HJM) type drift conditions for diffusion dynamics option surfaces. It is clear that if the model generates paths with static arbitrage such as negative prices for butterflies or calendar spreads, no equivalent risk-neutral measure can exist. It is therefore imperative to use a parameterization of the option price surface which allows efficient control for absence of arbitrage. This is in particular not the case for Black & Scholes implied volatilities.

First applicable results for a term structure of implied volatilities were presented in Schönbucher (1999), and extended to the entire option price surface in the seminal work of Wissel (2007). There, option prices are parameterized in what are called “implied local volatilities” and which we will refer to as discrete local volatilities because, they are a discrete form of Dupire’s local volatilities. Non-negativity alone ensures absence of static arbitrage; translation from discrete local volatilities to option prices is numerically efficient with modern machine learning tools.222The complexity of translating a discrete local volatility surface to option prices is equivalent to solving the respective very sparse implicit finite different scheme, inverting a tridiagonal matrix in every step. This operation is natively supported by TensorFlow. Wissel then proceeds to describe the required continuous time drift adjustment for a diffusion driving a grid of such discrete local volatilities as a function of the free parameters. Unnaturally, in his approach the resulting spot diffusion takes only discrete values at the strikes of the options at each maturity date and the approach is limited to a set grid of options defined in cash strikes and fixed maturities.

More recently, a number of works have shown that when representing an option surface with a Lévy kernel we can derive suitable HJM conditions on the parameters of the diffusion of the Lévy kernel such that the resulting stock price is arbitrage-free, c.f. Kallsen & Krühner (2015) and the references therein. Simulation of the respective model requires solving the respective Fourier equations for the spot price and options at each step in the path.

While impressive from an analytical perspective, each of these approaches faces challenges in practical implementation as the model dynamics are made to fit a particular analytical outcome, and are inherently continuous-time models. They are therefore not in a natural form conducive to statistical training.

Here, we present an alternative approach which is primarily driven by the desire to have realistic implied volatilty dynamics for a finite grid of options with efficient numerics, rather than tractable explicit analytics: we wish to first build a market simulator of the market under the statistical measure, and then learn an associated risk-neutral measure using non-parametric machine learning methods. While we prefer to represent option prices with discrete local volatility for numerical efficiency, our approach will work with any other parametrization which is free of static arbitrage.

Moreover, we postulate that trading incurs transaction costs and is subject to trading restrictions such as liquidity constraints and risk limits. We therefore aim to extend our results to find measures under which a trader cannot make money within her trading constraints and after paying trading costs. While such a measure is not necessarily a martingale measure, it ensures that the expected returns from trading any instruments are within the bid/ask spread. Such a measure is a natural candidate for running our previously discussed Deep Hedging (Buehler et al., 2019) approach below.

Machine Learning Risk-Neutral Volatility Dynamics

When training a machine learning model on historical market data, it will pick up the historical drift present in actual financial instruments. For example, when looking at the S&P500 index and its options from 2015 to 2021, the model may infer that being long SPY calls is a winning strategy. More subtly, it makes economic sense that puts, in particular, trade at a risk premium, i.e. that selling puts will on average generate profits. These effects are not statistically incorrect, but place too much trust in the implicitly estimated magnitude and persistence of the returns of those instruments. For the purpose of risk managing a portfolio of financial instruments we therefore deem it preferable to “remove the drift” of any tradable instrument. This is a complex operation for a surface of options, and requires the construction of an equivalent martingale measure.333Since we are in discrete time with continuous variables, there is no sensible notion of a “unique” martingale measure.

We propose the following approach: given a market simulator we first train a “Deep Hedging” model under the statistical measure to find an optimal statistical arbitrage strategy , i.e. a strategy which starting from an empty portfolio makes the most out of the perceived drift opportunities in the market by trading across all instruments considering prevailing transaction costs and trading constraints. If the strategy exists and is finite, we use it to construct a change of measure through

| (1) |

Under this measure, no strategy starting from an empty portfolio can have a positive risk-adjusted return after adjusting for cost. Furthermore, if there are no transaction costs or trading constraints, then is the minimal entropy martingale measure. We will elucidate this novel insight in Theorems 2.1 and 2.2, which are of independent interest.

As in our previous work Buehler et al. (2019), the approach is entirely “model free” in the sense that the numerical implementation of finding the risk-neutral measure change does not depend on the simulator. This allows efficient division of work between experts in machine learning to train a simulator with realistic volatility dynamics, and experts in classic quantitative finance who focus on efficient implementation of the risk-neutral expectation machinery.

In particular, while not discussed here, our approach also lends itself to non-equity markets and multiple assets across several currencies.

Arbitrage Free Parametrization of Option Surfaces

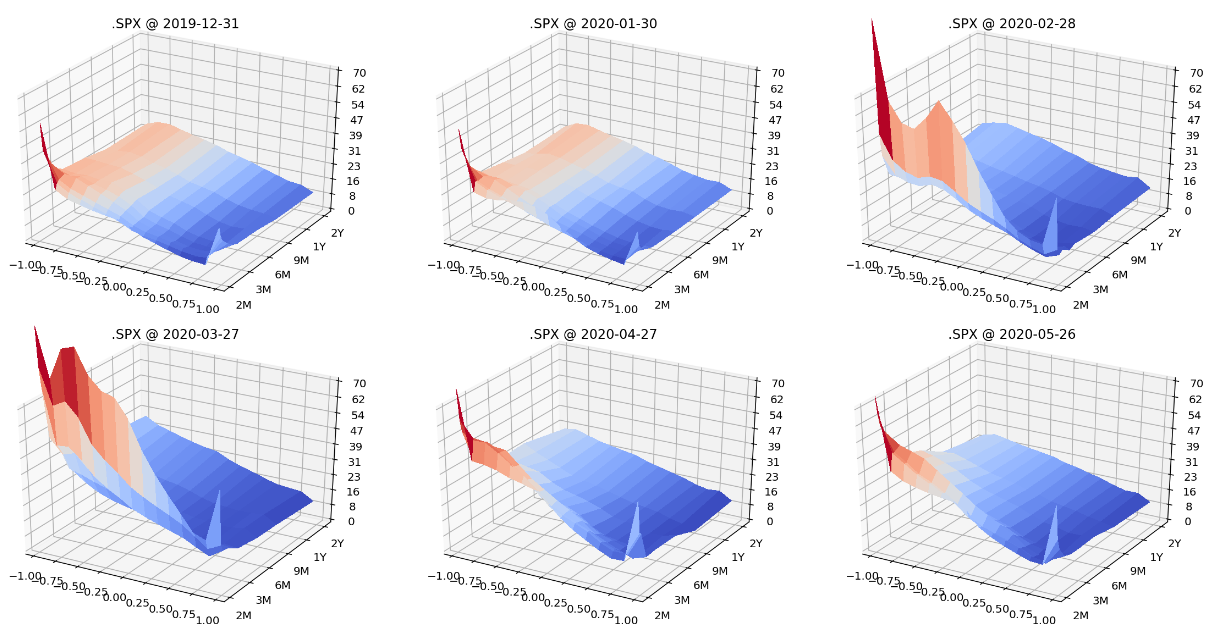

It is clear that if the market simulator generates paths with static arbitrage such as negative prices for butterflies or calendar spreads, no such measure can exist. To avoid static arbitrage, we propose to use discrete local volatilities in our market simulators as a numerically efficient sparse parametrization of our option surfaces. Figure 4 shows such historic discrete local volatility surfaces as illustration.

We have shown in our previous work Bai et al. (2019) how to use modern machine methods such as generative adversarial networks to train realistic simulators of the discrete local volatility surface. Here, we will refer to a simpler vector-autoregression model which performs less well when generating paths over several times steps, but is easily interpretable.

We want to point out that our approach to computing the risk-neutral measure for a market simulator does not depend on the choice of using discrete local volatilities.

Deep Hedging with Risk-Neutral Dynamics

The original motivation for the work in this article is to provide a means to “remove the drift” when applying the non-linear Deep Hedging approach in the presence of transaction costs and trading constraints. There, we value portfolios of financial instruments via indifference pricing by minimizing a convex risk measure. As we have noted in our original work Buehler et al. (2019), presence of statistical arbitrage means that the returned strategy is a mixture of the sought, “true” hedging strategy and proprietary trading strategy which seeks to make profits.

Running Deep Hedging under a risk-neutral measure removes this concern. In spirit this is the same approach as risk-managing a portfolio of stocks and futures using an industry “covariance” risk model that also does not provide a view on the drifts of the underlying names. We comment on the theoretical interpretation of this approach below.

Related Work

There have been a number of previous works on the statistics and simulation of implied volatility surfaces. A PCA approach to the dynamics of the surface was presented in Cont & da Fonseca (2002). Simulators that are constrained to prevent static arbitrage have been less well researched. Besides our own work Bai et al. (2019), we also want to point at Bergeron et al. (2021), where the authors build a variational auto encoder to simulate the full implied volatility surface, including the ability to penalize for absence of arbitrage somewhat. While they report no issues in application for scenario analysis, their approach does not strictly prevent arbitrage as the no-arbitrage condition is only introduced through soft penalities, but is not an inherent property of the resulting volatility surfaces. Our approach applies to this method, too, provided the resulting surfaces are indeed arbitrage free.

We not aware of any application of machine learning methods for estimating the measure change towards the minimal entropy martingale measure for paths of simulated derivatives; the closest related field of work is that of estimating a stochastic “pricing kernel”; see Cochrane (2005) and the numerous references therein. In this approach, observed option data is fit statistically to historical samples of observed spot data. This amounts in spirit to learning directly the density of the risk-neutral measure under the statistical measure for the spot price process itself. As the number of possible densities is large, an additional penalty function is required. If this penalty is the relative entropy, then in the absence of transaction costs the results here are analytically equivalent when applied to just the asset spot price. We are not aware of any work applying this approach to markets of derivatives as primary tradable assets as opposed to just spot prices.

2 Theoretical Background

In this section we will focus on the theoretical underpinning of our approach. We will use a notation which we aim to be accessible to both readers with stochastic calculus and reinforcement learning background. Throughout, we assume discounting rates, funding, dividends, and repo rates are zero. Extension to the case where they are non-zero and deterministic is straightforward.444For the stochastic rates case care need to be taken on the choice of discounting and investment of future proceeds.

We will trade over time steps where is the maximum maturity. For each , we denote by the state of the market at time , including relevant information from the past. The state represents all information available to us, and therefore specifically also the information required to compute the mid-prices of the hedging instruments available to trade at . In other words we may assume that is a function of . Mathematically speaking, the sequence of states generates a sequence of -algebras forming a filtration. Being generative means that any -measurable function can be written as a function of as . We will generally say “measurable” when a variable with index is a function of the state .

We further assume that for each instrument we observe at time a final mark-to-market mid-value which will usually be the sum of any cashflows along the path, and which is also assumed to be a function of . That means must contain sufficient information from the past along the path: for example, if an instrument tradable at is a call with relative strike and time-to-maturity on a spot price process , then .

We also assume that , where is the set of essentially bounded measurable random variables;555See also Remark 2.4. furthermore we simplify notation by stipulating that the total number of instruments at each timestep is always .

At each time step we may chose an action to trade in the hedging instruments based on the information available in the state , i.e. . Given , each is constrained to a convex set . We assume . It defines the set of admissible actions and represents risk and liquidity constraints. For an action also define elementwise.

For the current discussion we will assume that has a specific structure which will allow us to make structural statements such as Theorem 2.1 on page 2.1. Assume we observe a state . We postulate then that if there is any admissible strategy with (), then there is a () such that the strategy of doing nothing except buying (selling ) units of is also admissible.

We model trading costs and trading restrictions via a non-negative measurable generalized cost function with values in , which is convex in and normalized to . We further make the structural assumption that for a non-negative measurable ask spread and bid spread with values in .666We note that the use of this property below is invariant with respect to a linear transformation, i.e. the statements can be generalized to linear combinations of tradable instruments.

The convex set defines the set of admissible actions available at time , conditional on . We call our problem unconstrained if is finite for all for real-valued actions in which case for all and . We also set which denotes the set of admissible policies.

Remark 2.1

We note that the following construction leads to an acceptable generalized cost function: assume that is a convex set given , and that is convex in and normalized, but finite and defined only on . Then, is a valid cost function.

A common use case are sets of the form where are convex functions and where . For example, for classic “Vega” constraints or for quadratic risk constraints.

Convexity implies for any admissible policy . We note that the th asset can be bought (for a finite price) only on and sold (for a finite price) only on . In the following, we will refer to the joint vector with to ease notation.

We say that transaction costs are proportional if simply over and infinite elsewhere.

The terminal gain of implementing the trading policy is then given by

| (2) |

Note that if and transaction costs are proportional then with for .

We make the further assumption that for any admissible policy , which implies in particular that . 777This assumption is to some degree necessary. Our results may not hold if the gains of admissible policies have no finite moments. See Remark 2.4 for a concrete example.

Remark 2.2

Our slightly unusual notation of taking the performance of each instrument to maturity reflects our ambition to look at option simulators for “floating” implied volatility surfaces where the observed financial instruments change from step to step. If the simulator were to simulate the same options with fixed cash strikes and maturities across time steps, with prices of the same options available at every time step, then the usual notation applies:

| (3) |

This was the notation used in the original Deep Hedging paper of Buehler et al. (2019).

Remark 2.3

We note that (2) implies that spot and options which mature after are valued at mid-prices. The above can easily be extended to take into account liquidation cost at maturity.

In order to assess the performance of a trading strategy, we need a risk-adjusted measure of performance. Reversing sign relative to Buehler et al. (2019) we use a family of normalized monetary utility functions parameterized by , where maps from all random variables integrable under to .

In this article we focus on the (certainty equivalent of the) entropy,

| (4) |

If is normally distributed then the entropy reduces to the well-known mean-variance metric pioneered by Markowitz (1952). It is well known that is monotone888Lemma 2.1 establishes ths condition for the entropy., concave and cash-invariant.

Remark 2.4

2.1 Removing Statistical Arbitrage

A natural question is whether there is a strategy which has positive risk-adjusted expected return .

We call such a strategy a statistical arbitrage strategy. As we have discussed in the introduction, this is not an unusual

situation: practical strategies such as selling puts systematically are on average profitable if we have sufficient risk capacity

and can withstand the occasional large loss.

Define

| (5) |

This optimisation program can be implemented efficiently with modern “reinforcement learning” policy search using AAD packages such as TensorFlow, c.f. Buehler et al. (2019). We note that means that even a risk neutral trader cannot find profitable opportunities in the market. We then say that the market is free from statistical arbitrage. This definition is justified as absence of statistical arbitrage then implies also for all , as a result of the following lemma.

Lemma 2.1

The map for is non-increasing and non-negative.

In the specific case of the entropy, we have the following stronger result, proved in the Appendix on page A.2:

Proposition 2.1

Assume is the entropy, and that transaction costs are proportional. Then, for some implies for all .

It is self-evident that if , then we have and therefore absence of statistical arbitrage. In fact, we prove in the Appendix on page A.3 the even stronger statement:

Theorem 2.1

The market is free from statistical arbitrage if and only if the following two conditons hold:

-

1.

The marginal purchase price of any instrument exceeds its expected gains:

(6) -

2.

The marginal sale proceeds of any instruments do not exceed the expected liability arising from the sale:

(7)

In particular, in the absence of transaction costs or trading constraints for the th asset we recover the classic martingale condition

| (8) |

Remark 2.5

Under the conditions of the above theorem the conditional expectation defines a martingale “micro-price” (Stoikov, 2018) within the bid–ask spread in the sense that

Theorem 2.1 motivates the desire to “remove the drift” in order to simulate market dynamics free from statistical arbitrage. To do so, we draw on the theory of minimax measures (see for example Goll & Rüschendorf (2001)) to construct a suitable measure with the following result. We provide a brief proof in the Appendix on page A.4 in a less restrictive setting.

Theorem 2.2 (Robustly removing the Drift under Transaction Costs and Trading Constraints )

Assume that the market is constrained and that transaction costs are super-additive. Suppose that is a (not neccessarily unique) policy that minimizes

| (9) |

satisfying

Then, the market under the measure given by

| (10) |

is free from statistical arbitrage for any transaction cost and any tighter constraints .

Evidently, the market under is free of statistical arbitrage for all families of monetary utility functions with .101010More generally, if a convex risk-measure is law-invariant under , then , c.f. Föllmer & Knispel (2013, Corollary 5.1).

Note that for generalized transaction costs, the measure constructed here need not be a martingale measure, but one under which the drift of all tradable instruments is dominated by transaction costs, in the sense of Theorem 2.1. Therefore there are no statistical arbitrage strategies in the market at this level of transaction cost, or higher levels, since for any given policy, increasing transaction costs leads to lower gain. Indeed, for any higher transaction cost , the unique optimal policy at all risk aversion levels (including the risk neutral trader) under is . To see this, note that clearly for all , and for any we can write and so have which in turn implies that for all .

The practical application of the above theorem is that we may apply a measure change through a search for a statistical arbitrage strategy with smaller but not zero transaction cost. The reason for doing so is that the inclusion of some (proportional) trading cost will act as an -regularizer for the search of . Using smaller transaction costs than present in the market ensures that the resulting measure is risk-neutral even in the presence of numerical inaccuracies.

In the case of zero transaction costs, the resulting measure is in fact an equivalent martingale measure, and furthermore, under our assumptions that and , the result coincides with the following classic result, see Frittelli (2000).

Proposition 2.2

Assume that generalized transaction costs are zero . Let be a minimizer of (9). This is equivalent to saying maximizes for any . Further assume that under these assumptions the minimizer satisfies

Then the measure given by the density (10) is a martingale measure.

More specifically, the measure is the minimal entropy martingale measure (MEMM) in the sense that it minimizes the relative entropy

| (11) |

over all equivalent martingale measures . Trivially, this implies that the market with trading constraints and transaction costs is free of statistical arbitrage under this measure.

To illustrate our results, it is helpful to work out the following toy example:

Example 1 (One-period binomial model, with transaction costs)

Let and let be a one-dimensional random variable with

where and are parameters. Assume also that , . (We note that is then non-random.) Any admissible policy is then of the singleton form , a (non-random) parameter — let us assume here that it is unrestricted. With symmetric proportional transaction cost we have:

Firstly,

Thus, equals zero in the case and otherwise. Note that this includes the zero transaction cost case implying then that .

Secondly, for ,

whereby finding the maximizer of boils down to finding the minimizer of . If or (the case where there is classical arbitrage) then is strictly monotonic with , so that . Now, assume we are outside of those cases. For we have,

Now is ensured to exist provided that

and it is positive (as assumed) provided that

By symmetry, for we find that for

we have , which exists provided that and is negative as required provided that

Since , is convex and continuous, including at zero, where , it must hold that in both cases. That is, we have statistical arbitrage provided that . Otherwise, we have no turning points for and instead acheive a global minimum at . Note that the case immediately implies that and hence we have no statistical arbitrage.

Thirdly, for ,

In the so-called strong arbitrage cases and , choosing and , respectively, we get and letting shows that . In the cases and we have classical (non-strong) arbitrage and for any policy , whereby , attained at . Finally, in the arbitrage-free case we have similarly , so that .

3 Numerical Results

To illustrate the change of measure constructed in Theorem 2.2 and Proposition 2.2 and, we begin by implementing the approach in some model examples where the theoretical baselines are tractable, although we stress that the approach described above does not rely on any model specification and is fully versatile to be utilized with any market simulator, in particular “black box” neural network simulators.

In the numerical implementation, we consider a scenario where we want to remove statistical arbitrage from a specific set of paths generated from . We parametrize our policy by a neural network where is the entire parameter vector. We train the network using the usual stochastic gradient descent methods, to obtain a policy . We can then obtain probability weights for each path under via

| (12) |

and then expectations under are just weighted sums using these weights.

Although neural networks are well known to be universal approximators, due to the estimation and approximation error inherent in this method, given the non-smoothness of our cost function we still expect some numerical noise from the minimizer of the metric, the resulting measure may not be entirely free of statistical arbitrage in the sense of Therorem 2.2. However, provided our trained policy is close to optimal on the second set of sample paths, we can bound the maximum utility of a risk averse trader under in the following way.

Proposition 3.1

Suppose that is the truly optimal policy, and let be the approximated policy from a neural network with unknown approximation error such that . Denote by the entropy under under the measure given by .

For any risk aversion , and any policy we have then with equality attained in the absence of transaction cost.

3.1 Toy example: Black-Scholes model

As a simple example, consider first a market described by a discrete version of a one-dimensional Black Scholes model with spot dynamics where and a one-dimensional Brownian motion. No options are simulated. We ensure the integrability condition of the spot process by simulating only a finite set of paths. Clearly, if we have statistical arbitrage since the will no longer be a martingale, indeed for , a simple ‘buy and hold’ policy , for all will produce positive utility.

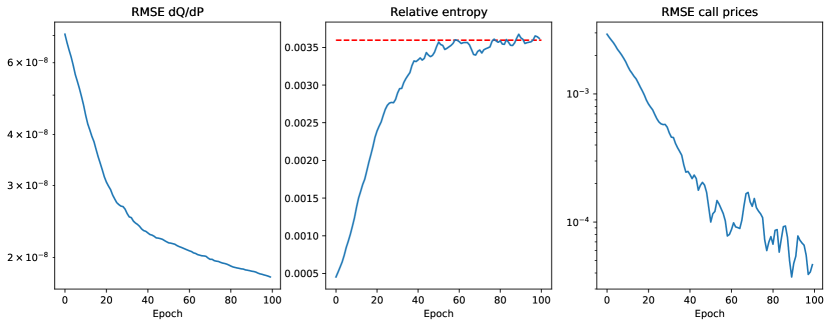

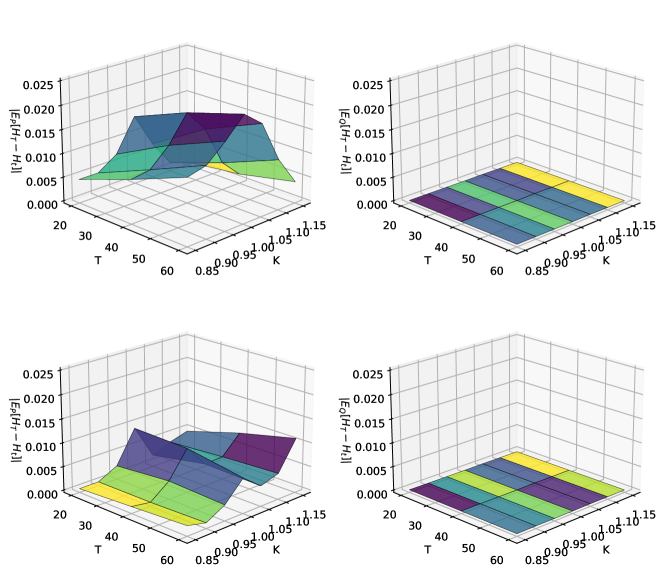

For a numerical implementation of this scenario, we set a trading horizon of 30 trading days (), allowing daily rebalancing of the spot. The spot drift is and the volatility is We simulate a set of paths as training data for our policy. We parametrize our policy with a neural network trained via the Adam optimizer. Specifically, we use a two layer recurrent neural network structure with 32 units in each layer and with global learning rate of , batch size of 256, and trained for 100 epochs. To assess the performance, we track three metrics:

-

1.

Mean square error for . In the Black Scholes model, under the assumption of continuous trading we have a unique equivalent martingale measure, given by the Radon-Nikodym density

(13) and that is a standard Brownian motion with respect to . Hence we can calculate this density for each simulated path in the validation set and then compare to the estimates generated by our neural network, tracking the mean square error in this estimate.

-

2.

Relative entropy. From the above, it is straightforward to obtain the entropy . Thus by tracking the finite sample relative entropy on our validation set we can assess convergence to this value.

-

3.

Mean square error for vanilla option prices. A further simple metric is to assess whether the expected payoff of vanilla options under match with the option prices derived from the Black Scholes formula. To do so we calculate call prices on a grid of relative strikes and calculate the mean square error between the theoretical prices and the Monte Carlo prices

To reduce the Monte Carlo variance in these metrics, we evaluate them every 100 gradient steps on a separate validation set of size . Results are plotted in Figure 2. We can clealy see good convergence in all three metrics, with the mean square errors of the density and option prices converging to zero, and the relative entropy converging to the correct value.

3.2 Toy example: Black-Scholes model realized volatility

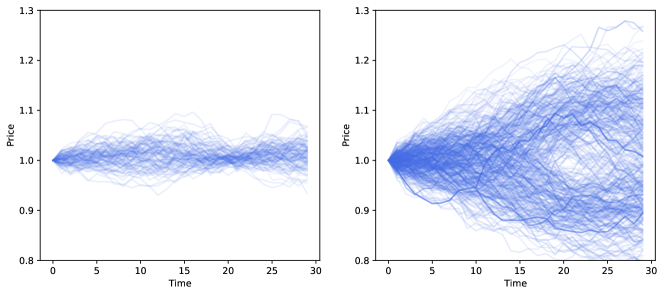

To illustrate the effect of the measure change, we apply it to a Black Scholes market where spot and at the money puts and calls can be traded at each timestep. We simulate market paths where the spot is free of drift, but the options are priced with . Specifically, we simulate market paths with In this case, an effective statistical arbitrage strategy would be to sell puts and calls, and delta hedge against that with spot.

In discrete time, equivalent measure changes can change realized volatility, contrary to the invariance of quadratic variation in continuous time. Hence, to remove statistical arbitrage we need to reweight the spot distribution so that the realised volatility is in line with the implied volatility. The outcome of this is demonstrated in Figure 3 where on the left, paths with low realised volatility are given low weight, and on the right paths with high realized volatility are given high weight.

3.3 Example: Vector Autoregressive model

A simple multivariate model for spot and option prices could be to simulate a market through a vector autoregressive model. To this end, we recap briefly the notion of discrete local volatilities Buehler & Ryskin (2015). Assume maturities and relative strikes .111111See Buehler & Ryskin (2015) for the use of inhomogeneous strike grids. We also define the additonal ghost strikes and for which we assume each option has intrinsic value. Set . We ignore discounting and forwards here, but adding them is a minor extension.

For and we denote by the option with payoff at maturity . Define

| (14) |

The discrete local volatility surface is given by

| (15) |

We recall that the options are free of static arbitrage 121212E.g. there is a martingale process which generates these option prices. if and only if , c.f. Buehler & Ryskin (2015). Moreover, given a surface of finite discrete local volatilities, we may reconstruct the original surface by solving for the call prices using the implicit finite difference scheme implied by (15). This involves inverting sequentially tridiagonal matrices. We note that this operation is available “on graph” in modern automatic adjoint differentiation (AAD) machine learning packages such as TensorFlow. Figure 4 shows such historic discrete local volatility surfaces as illustration.

Removing the Drift

Given vectors of (backward) log spot returns and logs of discrete local volatilities on maturities and relative strikes we can simulate a process:

| (16) |

where is a coefficient matrix. We fit the model to data from EURO STOXX 50, using standard regression techniques from the Statsmodels Python package (Seabold & Perktold, 2010). Once the model has been fit, we can simulate new sample paths of log spot returns and discrete local volatilities and convert them to option prices using the methods detailed above, so that we can simulate market states of spot and option prices. To this end, we generate paths, of length 30 days, where each path consists of spot and both put and call option prices on a grid of maturities of and relative strikes . For the measure change, we set transaction costs for all instruments to be proportional at level .

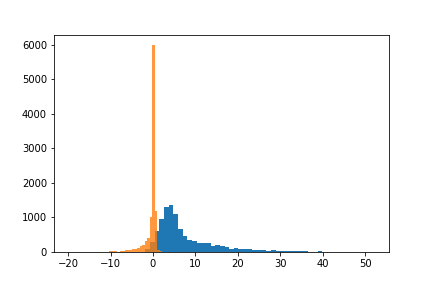

We then construct the measure which is free from statistical arbitrage. To parametrize the policy action, we use a two layer feedforward neural network, with 64 units in each layer and ReLU activation functions. We train for 2000 epochs on a training set of paths. Figure 5 compares the expected value of payoffs vs. their prices under both the statistical and the risk-free measure in relation to trading cost. The expected payoff under the changed measure has clearly been flattened towards zero, and now lies within the transaction cost level, so that the drift has been removed. To confirm that statistical arbitrage has indeed been eliminated from the market simulator under this measure, we train two new, identical, network to find an optimal policy under the exponential utility, on the same simulated paths, one with unweighted, and one weighted by the output of the measure change, this time with proportional transaction costs at level . Figure 6 shows the distributions of terminal gains of respective estimated optimal policies under and . Here the distribution of gains has been shifted so that it is centred at zero confirming that statistical arbitrage has been removed.

4 Deep Hedging under Risk-Neutral Dynamics

In this short section we briefly comment on the implications of using the MEMM when solving the Deep Hedging problem (Buehler et al., 2019).

Assume here that we have a portfolio of financial instruments with terminal payoff . The Deep Hedging problem is then

| (17) |

If we wanted to sell a new product with terminal payoff to a client, then our new terminal portfolio becomes . The minimal risk-adjusted price is then given by

| (18) |

We note that this implies our fair mark-to-market of closing our portfolio is , giving rise to the need assessing the presence of statistical arbitrage strategies. To this end, define the entropy under our MEMM as,

| (19) |

Define also the Deep Hedging problem under ,

| (20) |

Evidently, . The following result generalizes lemma 3.3 in Buehler et al. (2019) where a similar formula was shown for the case where has a replication strategy. The proof for the proposition and the following corollary are provided in the Appendix.

Proposition 4.1

Assume that transaction cost are super-additive i.e. . Then,

| (21) |

with equality if transaction costs are zero and the problem is unconstrained.

Corollary 4.1 (Optimal policy for Risk Neutral Deep Hedging)

Assume transaction costs are zero. Under the statistical measure suppose that is a solution to the Deep Hedging problem for , and that is an optimal statistical arbitrage policy, i.e. .

Then the policy is a solution to the Deep Hedging problem under the minimal entropy martingale measure .

The previous two results show that in the absence of transaction costs, solving the Deep Hedging problem under directly removes the statistical arbitrage element of the policy that was present under . Indeed, the risk-neutral Deep Hedging problem could be solved implicitly by solving the two optimisation problems under and taking their difference.

5 Conclusion

We have presented a numerically efficient method for computing a risk-neutral density for a set of paths over a number of time steps. Our method is applicable to paths of derivatives and option prices in particular, hence we effectively provide a framework for statistically learned stochastic implied volatility models using only basic linear algebra and comonly available machine learning tools. Our method is generic and does not depend on the market simulator itself, except that it requires that the simulator does not produce static arbitrage opportunities. It also caters naturally for transaction cost and trading constraints, and is easily extended to multiple assets.

Finally, with Theorem 2.1 we have also provided novel insights into the relationship between statistical arbitrage under trading frictions and to what degree the prices of instruments may deviate from their expected values.

Appendix A Proofs

A.1 Proof of Lemma 2.1

of Lemma 2.1.

Consider , and let be a random variable such that . Firstly, we have

where the map is convex since . Thus, by Jensen’s inequality,

(We may have or , but the inequality remains nevertheless valid.) Secondly, since is also convex, Jensen’s inequality further implies , whereby

Thirdly, since , we have

In summary,

| (22) |

Now, for ,

by (22), which proves that is non-increasing. To establish non-negativity, it remains to note that

A.2 Proof of Proposition 2.1

of Proposition 2.1.

we will prove that for all implies for the entropy, since then the result follows from monotonicity of . Suppose instead that , while for all . Then there is an admissible policy such that

Since , , for this policy is almost surely bounded, and so we have

by Föllmer & Knispel (2011), implying in turn that for some . But this contradicts the assumption for all , so it follows that .

A.3 Proof of Theorem 2.1

To prove Theorem 2.1, we need a few auxiliary results:

Lemma A.1

Let be a random variable such that and let be a -algebra. Suppose that is a non-negative, -measurable random variable such that

| (23) |

Then,

| (24) |

Proof.

We will aim to reduce the proof of Theorem 2.1 to the case of proportional costs. To this end, define by the respective proportional cost

| (25) |

and the associated gains process

| (26) |

Lemma A.2

We have if and only if .

Proof.

Since by construction we have to show that also implies . Assume the contrary, i.e. is a strategy such that but . Concavity of and imply that and therefore . Taking the monotone limit yields the contradiction .

of Theorem 2.1.

Thanks to Lemma A.2 we may focus on the case where transaction costs are proportional. We first prove that if the market is free from statistical arbitrage, then inequalities (6) and (7) in the theorem hold.

Define

| (27) |

Evidently, and, in particular, whereever and where .

Fix and where is not empty, let be arbitrary, and let be the policy which is zero except over where we buy units of . Note that .

which implies on with Lemma A.1

| (28) |

i.e. equation (6). Note that on we have so that (6) holds trivially there, too.

For selling, fix again and where is not empty, let agan be arbitrary, and let be the policy which is zero except over where we sell units of .

Reording on yields

| (29) |

and therefore equation (7).

Remark A.1

It may be of interest to note the following dichotomy for the entropy with proportional transaction costs, which follows since is linear and positive homogeneous. In the unconstrained case, for either or . To see this, note that on the one hand, if then by Lemma 2.1. On the other hand, if then there exists an admissible policy such that . But for any constant the policy is also admissible, while for we have

by positive homogeneity. Letting shows that then . Note that if the policy is constrained, then the case is replaced by an optimal strategy being a boundary point in .

A.4 Proof of Theorem 2.2

of Theorem 2.2.

superadditivity means and therefore . For as defined as in Theorem 2.2 we find

| (32) |

where becomes an equality in the absence of transaction cost, and where is due to optimality of . With the results of Proposition 2.1 and Theorem 2.1, this implies that the market under with cost and constraints is free from statistical arbitrage. The extension to higher cost or tighter restrictions is trivial.

A.5 Proof of Proposition 3.1

A.6 Proof of Proposition 4.1 and Corollary 4.1

for Proposition 4.1.

For this proof, we note that for all . We have equality if trading cost are proportional and finite (i.e., unconstrained). Since is superadditive we have .

We have equality in if transaction costs are proportional and in if transaction costs are zero.

for Corollary 4.1.

This follows directly from the previous result and the proof is virtually identical:

| (34) |

References

- Bai et al. (2019) Bai, L., Buehler, H., Wiese, M., and Wood, B. Deep hedging: Learning to simulate equity option markets. Working paper, 2019. URL https://ssrn.com/abstract=3470756.

- Bergeron et al. (2021) Bergeron, M., Fung, N., Hull, J., and Poulos, Z. Variational autoencoders: A hands-off approach to volatility. Working paper, 2021. URL https://arxiv.org/abs/2102.03945.

- Brace et al. (2001) Brace, A., Goldys, B., Klebaner, F., and Womersley, R. Market model of stochastic implied volatility with application to the BGM model. Working paper, 2001. URL http://www.maths.unsw.edu.au/statistics/files/preprint-2001-01.pdf.

- Buehler & Ryskin (2015) Buehler, H. and Ryskin, E. Discrete local volatility for large time steps (extended version). Working paper, 2015. URL https://ssrn.com/abstract=2642630.

- Buehler et al. (2019) Buehler, H., Gonon, L., Teichmann, J., and Wood, B. Deep hedging. Quantitative Finance, 0(0):1–21, 2019. URL https://ssrn.com/abstract=3120710.

- Cochrane (2005) Cochrane, J. Asset Pricing: Revised Edition. Princeton University Press, 2005.

- Cont & da Fonseca (2002) Cont, R. and da Fonseca, J. Dynamics of implied volatility surfaces. Quantitative Finance, 2(1):45–60, 2002. URL https://ssrn.com/abstract=295859.

- Föllmer & Knispel (2011) Föllmer, H. and Knispel, T. Entropic risk measures: Coherence vs. convexity, model ambiguity and robust large deviations. Stochastics and Dynamics, 11(02n03):333–351, 2011.

- Föllmer & Knispel (2013) Föllmer, H. and Knispel, T. Convex risk measures: Basic facts, law-invariance and beyond, asymptotics for large portfolios. Handbook of the Fundamentals of Financial Decision Making, pp. 507–554, 7 2013. URL https://www.insurance.uni-hannover.de/fileadmin/house-of-insurance/People/knispel_thomas/RiskMeasures_FoellmerKnispel.pdf.

- Frittelli (2000) Frittelli, M. The minimal entropy martingale measure and the valuation problem in incomplete markets. Mathematical finance, 10(1):39–52, 2000.

- Goll & Rüschendorf (2001) Goll, T. and Rüschendorf, L. Minimax and minimal distance martingale measures and their relationship to portfolio optimization. Finance and Stochastics, 5(4):557–581, 2001.

- Kallsen & Krühner (2015) Kallsen, J. and Krühner, P. On a Heath-Jarrow-Morten approach for stock options. Finance and Stochastics, 19:583–615, 2015. URL https://arxiv.org/pdf/1305.5621.pdf.

- Markowitz (1952) Markowitz, H. Portfolio selection. The Journal of Finance, 7(1):77–91, 1952. doi: 10.2307/2975974.

- Schönbucher (1999) Schönbucher, P. A market model for stochastic implied volatility. Phil. Trans. R. Soc. A., pp. 2071–2092, 1999. URL https://ssrn.com/abstract=182775.

- Seabold & Perktold (2010) Seabold, S. and Perktold, J. statsmodels: Econometric and statistical modeling with python. In 9th Python in Science Conference, 2010.

- Stoikov (2018) Stoikov, S. The micro-price: a high-frequency estimator of future prices. Quantitative Finance, 18(12):1959–1966, 2018.

- Wissel (2007) Wissel, J. Arbitrage-free market models for option prices. Working paper, 2007. URL http://www.nccr-finrisk.uzh.ch/media/pdf/wp/WP428_D1.pdf.

Disclaimer

Opinions and estimates constitute our judgement as of the date of this Material, are for informational purposes only and are subject to change without notice. It is not a research report and is not intended as such. Past performance is not indicative of future results. This Material is not the product of J.P. Morgan’s Research Department and therefore, has not been prepared in accordance with legal requirements to promote the independence of research, including but not limited to, the prohibition on the dealing ahead of the dissemination of investment research. This Material is not intended as research, a recommendation, advice, offer or solicitation for the purchase or sale of any financial product or service, or to be used in any way for evaluating the merits of participating in any transaction. Please consult your own advisors regarding legal, tax, accounting or any other aspects including suitability implications for your particular circumstances. J.P. Morgan disclaims any responsibility or liability whatsoever for the quality, accuracy or completeness of the information herein, and for any reliance on, or use of this material in any way.

Important disclosures at: www.jpmorgan.com/disclosures