Regenerativity of Viterbi process for pairwise Markov models111This is a post-peer-review, pre-copyedit version of an article published in Journal of Theoretical Probability. The final authenticated version is available online at: http://dx.doi.org/10.1007/s10959-020-01022-z 222The research is supported by Estonian institutional research funding IUT34-5 and PRG865.

Abstract

For hidden Markov models one of the most popular estimates of the hidden chain is the Viterbi path – the path maximising the posterior probability. We consider a more general setting, called the pairwise Markov model (PMM), where the joint process consisting of finite-state hidden process and observation process is assumed to be a Markov chain. It has been recently proven that under some conditions the Viterbi path of the PMM can almost surely be extended to infinity, thereby defining the infinite Viterbi decoding of the observation sequence, called the Viterbi process. This was done by constructing a block of observations, called a barrier, which ensures that the Viterbi path goes trough a given state whenever this block occurs in the observation sequence. In this paper we prove that the joint process consisting of Viterbi process and PMM is regenerative. The proof involves a delicate construction of regeneration times which coincide with the occurrences of barriers. As one possible application of our theory, some results on the asymptotics of the Viterbi training algorithm are derived.

Keywords: Viterbi path, MAP path, Viterbi training, Viterbi algorithm, Markov switching model, hidden Markov model

1 Introduction and preliminaries

1.1 Introduction

We consider a Markov chain with product state space , where is a finite set (state space) and is an arbitrary separable metric space (observation space). Thus, the process decomposes as , where and are random processes taking values in and , respectively. The process is identified as an observation process and the process , sometimes called the regime, models the observations-driving hidden state sequence. Therefore our general model contains many well-known stochastic models as a special case: hidden Markov models (HMM), Markov switching models, hidden Markov models with dependent noise and many more. The segmentation or path estimation problem consists of estimating the realization of given a realization of . A standard estimate is any path having maximum posterior probability:

Any such path is called Viterbi path and we are interested in the behaviour of as grows. The study of asymptotics of Viterbi path is complicated by the fact that adding one more observation, can change the whole path, and so it is not clear, whether there exists a limiting infinite Viterbi path.

It has been recently proven [28] that under some conditions the infinite Viterbi path exists for almost every realization of , allowing to define an infinite Viterbi decoding of , called the Viterbi process. This was done trough construction of barriers. A barrier is a fixed-sized block in the observations that fixes the Viterbi path up to itself: for every continuation of , the Viterbi path up to the barrier remains unchanged. Therefore, if almost every realization of -process contains infinitely many barriers, then the infinite Viterbi path exists a.s.

Having infinitely many barriers is not necessary for existence of infinite Viterbi path (see [28, Example 1.2]), but the barrier-construction has several advantages. One of them is that it allows to construct the infinite path piecewise, meaning that to determine the first elements of the infinite path it suffices to observe for big enough. In the present paper we show that the barrier construction has another great advantage: namely, the process , where denotes the Viterbi process, is under certain conditions regenerative. This is proven by, roughly speaking, applying the Markov splitting method to construct regeneration times for which coincide with the occurrences of barriers. Regenerativity of allows to easily prove limit theorems to understand the asymptotic behaviour of inferences based on Viterbi paths. In fact, in a special case of HMM this regenerative property has already been known to hold and has found several applications [29, 22, 25, 23, 12].

The paper is organized as follows. In Subsection 1.2, we introduce our model and some necessary notation. In Subsection 1.3, the segmentation problem, infinite Viterbi path, barriers and many other concepts are introduced and defined. In Subsection 1.4 we state the two barrier construction theorems from [28] (Theorem 1.1 concerning HMM and Theorem 1.2 concerning general PMM) as well as introduce some general Markov chain terminology. In Section 2 we prove our main regeneration-theorem. In Section 3 we apply this theorem to more specific cases, namely HMM (Subsection 3.1), discrete (Subsection 3.2) and linear Markov switching model (Subsection 3.3). In Section 4 we demonstrate an application of our theory by providing some regeneration-based analysis of the Viterbi training algorithm.

1.2 Pairwise Markov model

Let the observation-space be a separable metric space equipped with its Borel -field . Let the state-space be , where is some positive integer. We denote , and equip with product topology , where denotes the topology induced by the metrics of . Furthermore, is equipped with its Borel -field , which is the smallest -field containing sets of the form , where and . Let be a -finite measure on and let be the counting measure on . Finally, let

be a such a measurable non-negative function that for each the function is a density with respect to product measure .

We define random process as a homogeneous Markov chain on the two-dimensional space having the transition kernel defined by

In other words, is the transition kernel density of . The marginal processes and will be denoted with and , respectively. Following [33, 7, 8], we call the process a pairwise Markov model (PMM). It should be noted that even though is a Markov chain, this doesn’t necessarily imply that either of the marginal processes and are Markov chains.

The letter will be used to denote the various joint and conditional densities. By abuse of notation, the corresponding probability law is indicated by arguments of , with lower-case , and indicating random variables , and , respectively. For example

where and . Sometimes it is convenient to use other symbols beside as the arguments of some density; in that case we indicate the corresponding probability law using the equality sign, for example

Also denotes the initial distribution density of with respect to measure , where is some -finite measure on . Thus the joint density of is . For every and we also denote

| (1) |

Thus

If doesn’t depend on , and doesn’t depend on neither nor , then is called a hidden Markov model (HMM). In that case, denoting

the transition kernel density factorizes into

Density functions are also called the emission densities.

If doesn’t depend on , and doesn’t depend on , then following [4] we call a Markov switching model. Thus HMM’s constitute a sub-class of Markov switching models. In the case of Markov switching model, denoting

the transition kernel density becomes

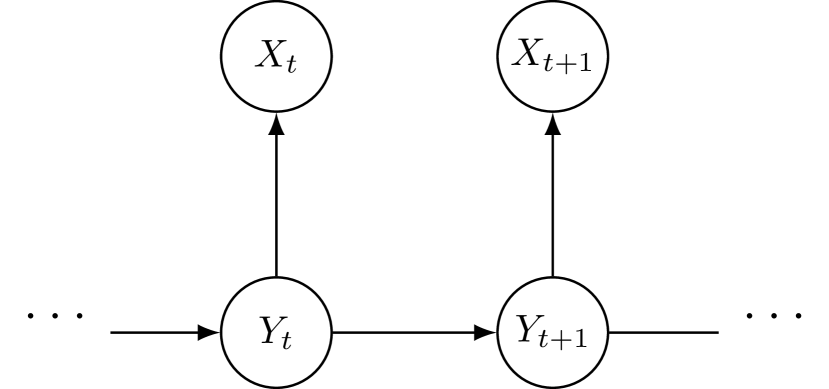

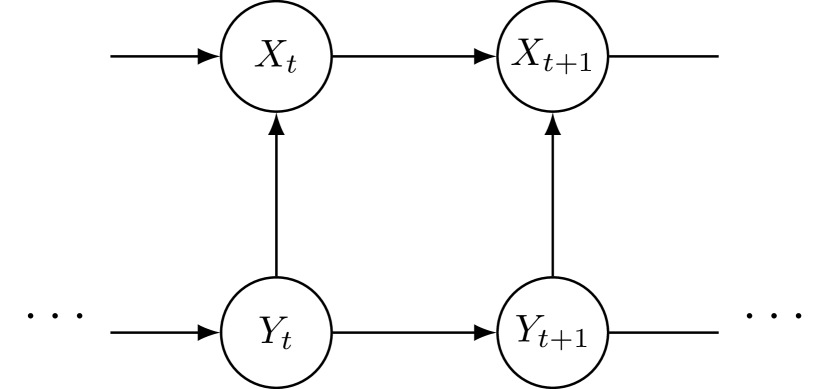

It is easy to confirm that in case of Markov switching model (and therefore also in case of HMM) is a homogeneous Markov chain with transition matrix [33]. Most PMM’s used in practice fall into the class of Markov switching models. Figure 1 depicts the directed dependence graph of HMM, Markov switching model and the general PMM.

Throughout this paper we write for any event and for any random variable .

1.3 Infinite Viterbi path

The segmentation problem in general consists of guessing or estimating the unobserved realization of process – the true path – given the realization of the observation process . Since the true path cannot be exactly known, the segmentation procedure merely consists of finding the path that in some sense is the best approximation. Probably the most popular estimate is the path with maximum posterior probability. This path will be denoted with and also with , when is assumed to be fixed:

Typically is called Viterbi or MAP path (also Viterbi or MAP alignment). It can be found by a dynamic programming algorithm called Viterbi algorithm [34]. Clearly might not be unique. For more detailed discussion about the segmentation problem and the properties of different estimates, we refer to [30, 21, 38, 23, 24]. Although these papers deal with HMM’s only, the general theory applies for any model including PMM’s.

To study the statistical properties of Viterbi path-based inferences, one has to know the long-run or typical behaviour of random vectors . As argued in [29], behaviour of is not trivial since the observation can in principle change the entire alignment based on the previous observations . It might happen with a positive probability that the first entries of are all different from corresponding entries of . If this happens again and again, then the first element of keeps changing as grows and there is not such thing as limiting Viterbi path. On the other hand, it could be intuitively claimed that sometimes there is a positive probability to observe such that regardless of the value of the observation (provided is sufficiently large), the paths and agree on first elements, where . If this is true, then no matter what happens in the future, the first elements of the paths remain constant. Provided there is an increasing unbounded sequence () such that the path up to remains constant, one can define limiting or infinite Viterbi path. Let us formalize the idea. In the following definition is a Viterbi path and are the first elements of the -elemental vector .

Definition 1.1.

Let be a realization of . The sequence is called infinite Viterbi path of if for any there exists such that

| (2) |

Hence is the infinite Viterbi path of if for any , the first elements of are the first elements of a Viterbi path for all big enough . In other words, for every big enough, there exists at least one Viterbi path so that . For the definition of infinite Viterbi path in the case is infinite, see [6, 28].

As we shall see, for many PMM’s the infinite Viterbi path exists for almost every realization of . However, it is possible to construct a model where almost no realization has an infinite Viterbi path (see [28, Example 1.1]).

Nodes

Suppose now is such that infinite Viterbi path exists. It means that for every time , there exists time such that the first elements of are fixed as soon as . Note that if is such a time, then is such a time too. Theoretically, the time might depend on the whole sequence . This means that after observing the sequence , it is not yet clear, whether the first elements of Viterbi path are now fixed (for any continuation of ) or not. In practice, one would not like to wait infinitely long, instead one prefers to realize that the time is arrived right after observing . In this case, the (random) time is the stopping time with respect to the observation process. In particular, it means the following: for every possible continuation of , the Viterbi path at time passes the state , let that state be . This requirement is fulfilled, when the following holds: for every two states

| (3) |

where

and is defined in (1). Indeed, there might be several states satisfying (3), but the ties can always be broken in favour of the state , so that whenever , there is at least one Viterbi path that passes the state at time . Therefore, if at time , there is a state satisfying (3), then is the time required in (2) and it depends on only.

Definition 1.2.

Let be a vector of observations. If inequalities (3) hold for any pair of states and , then the time is called an -node of order . Time is called a strong -node of order , if it is an -node of order , and the inequality (3) is strict for any and for which the left side of the inequality is positive. We call a node of order if for some , it is an -node of order .

In [36] the concept of node is used under the name “coalescence point” to describe a memory-efficient modification of the Viterbi algorithm. Our theory justifies the use of such algorithm and could be used to derive bounds on its memory complexity.

Barriers

Whether a time is a node of order or not depends, in general, on the sequence . Sometimes, however, there is some small block of observations that guarantees the existence of a node regardless of the other observations. Let us illustrate this by an example.

Example 1.

([28, Example 3]) Suppose that there exists a state such that for any triplet

| (4) |

Then

We thus have that is an -node of order 1, because for every pair

Whether (4) holds or not, depends on triplet . In case of Markov switching model, (4) is

And in a more special case of HMM, (4) is equivalent to

| (5) |

The inequalities (5) have very clear meaning – when the observation has relatively big probability of being emitted from state (in comparison of being emitted from any other state), then regardless of the observations before or after , time is a node. On the other hand, for many models, there are no such possible, so (5) is rather an exception than a rule.

Definition 1.3.

Given , is called an (strong) -barrier of order and length , if, for any with for some , is an (strong) -node of order .

Suppose now that an -barrier of order occurs in infinitely often. By definition of a barrier, there must exist infinitely many -nodes of order in , let these nodes be . Let . There must exist a Viterbi path passing state at time . There also exists a Viterbi path passing at time . If is unique, then the path passes at both times, but if Viterbi path is not unique and and are too close to each other, then there might not be possible to break ties in favour of at and simultaneously (see [28, Example 1.4]). This problem does not occur, if the nodes are strong or if . Indeed, since is an -node of order , then by definition of -order node, between times and , the ties can be broken so that whatever state the Viterbi path passes at time , it passes at time . Thus, if the locations of nodes are such that for all , it is possible to construct the infinite Viterbi path so that it passes the state at every time . In what follows, when the nodes and are such that , then the nodes are called separated. Of course, there is no loss of generality in assuming that the nodes are separated, because from any non-separated sequence of nodes it is possible to pick a separated subsequence. Another approach is to enlarge the barriers so that two barriers cannot overlap and, therefore, are separated. This is the way barriers are defined in [27].

Piecewise construction of infinite Viterbi path

Having infinitely many separated nodes or order , it is possible to construct the infinite Viterbi path piecewise. Indeed, we know that for every , there is a Viterbi path such that , . Because of that property and by optimality principle clearly the piece depends on the observations , only. Therefore can be constructed in the following way: first use the observations to find the first piece as follows:

Then use to find the second piece as follows:

and so on. Finally use to find the last piece as follows:

The last piece might change as grows, but the rest of the Viterbi path is now fixed. Thus, if contains infinitely many nodes, the whole infinite path can be constructed piecewise.

If the nodes are strong (not necessarily separated) then regardless of tie-breaking scheme for all and . Therefore the piecewise construction detailed above is in that case achieved when the Viterbi estimation is done by a lexicographic333Here the term “lexicographic” includes both left-to-right and right-to-left lexicographic ordering (the latter is sometimes called co-lexicographic ordering). tie-breaking scheme induced by some ordering on . Furthermore, under lexicographic ordering, each piece in the piecewise construction is also found by lexicographic ordering. The latter observation will be crucial to our proof of regenerativity.

If the nodes are not strong, then the lexicographic ordering may fail to produce the piecewise construction. However from practice point of view the lexicographic ordering is clearly advantageous, since it can easily be implemented via Viterbi algorithm. For that reason we will from now on almost exclusively focus on strong nodes and strong barriers. Fortunately, this does not seem to impose any significant restrictions.

1.4 Viterbi process

The notion of infinite Viterbi path of a fixed realization naturally carries over to an infinite Viterbi path of , called the Viterbi process. Formally, this process is defined as follows.

Definition 1.4.

A random process on space is called a Viterbi process, if the event is contained in a set of zero probability measure.

If there exists a barrier set consisting of -barriers of fixed order and satisfying , where

then the Viterbi process can be constructed by applying the piecewise construction detailed above to the process . Having infinitely many barriers not only ensures the existence of the Viterbi process, but – as we shall see briefly – will also provide a rather straightforward route to proving that the Viterbi process is regenerative. As follows we state two theorems which ensure the existence of Viterbi process. The first one only concerns HMM while the latter applies to any PMM.

Recall that in case of HMM are the emission densities with respect to measure . Denote

The conditions for the HMM-theorem are the following.

- (HMM1)

-

For each state

- (HMM2)

-

There exists a set such that

and the sub-stochastic matrix is primitive in the sense that consists of only positive elements for some positive integer .

Note that condition (HMM2) only depends on transition matrix and the probability laws induced by densities . Also, this condition is not very restrictive. It is fulfilled when consists of only positive elements. It is also fulfilled when is primitive and there exists some -positive set such that are positive on that set.

Theorem 1.1.

[28, Cor. 4.1] Let be HMM satisfying (HMM1) and (HMM2) and let Markov chain be irreducible. There exists a set consisting of strong -barriers of fixed order and satisfying .

Theorem (HMM1) is not the only result in literature guaranteeing the existence of Viterbi process for HMM, but it is the latest and has the most general conditions (cf. [3, 2, 27, 20]).

In order to state the PMM-theorem we need introduce some general state Markov chain terminology. Markov chain is called -irreducible for some -finite measure on , if implies for all . If is -irreducible, then there exists (see [32, Prop. 4.2.2.]) a maximal irreducibility measure in the sense that for any other irreducibility measure the measure dominates , . The symbol will be reserved to denote the maximal irreducibility measure of . A point is called reachable if for every open neighbourhood of ,

For -irreducible , the point is reachable if and only if it belongs to the support of [32, Lemma 6.1.4]. Since we have equipped space with product topology , where denotes the topology induced by the metrics of , the above-stated definition of reachable point is in fact equivalent to the following: point is called reachable, if for every open neighbourhood of ,

Chain is called Harris recurrent, if it is -irreducible and implies for all .

For any define

| (6) |

For any set consisting of vectors of length we adopt the following notation:

Hence

Observe that if and then not necessarily

The conditions for the PMM-theorem are the following.

- (PMM1)

-

For any there exist , an open set , and such that denoting we have for all and all

(7) (8) where either inequalities (7) or (8) could be non-strict. We assume that and are independent of , and that there exists a compact set , which is independent of , such that is contained in . Furthermore, we assume that there exists such that is reachable.

- (PMM2)

-

There exists an open set , , such that is the same for every and satisfies the following property: for every and . Furthermore, we assume that there exists a reachable point in .

Theorem 1.2.

[28, Th. 3.1] Let be strictly postive444A measure is called strictly positive if it assigns a positive measure to all non-empty open sets. and let for every pair of states function be lower semi-continuous and bounded. If satisfies (PMM1) and (PMM2), then there exists consisting of strong 1-barriers of fixed order. Moreover, if is Harris recurrent, then .

2 Regenerativity

For any sequence and a sequence of times , , a shift operator , , is defined by , where . A process is called regenerative [19, 37] (in the classic sense), if there exists a sequence of random times , , called regeneration times, such that for each

Random variables are called inter-regeneration times. Typically one is interested in the case where inter-regeneration times have finite mean, i.e. .

Let from now on denote the Viterbi process, whenever it exists, obtained by a lexicographic tie-breaking scheme. The main goal of the present paper is to prove that under some conditions the joint process is regenerative. Regenerativity of a general state space Markov chain is typically proved by applying the so-called splitting method [19, 37]. If the regeneration times of obtained by the splitting method are also strong nodes, then is regenerative as well. This is the idea behind our main regeneration theorem below. The theorem is proven under assumptions (R1)-(R3), where (R1) ensures the existence of an appropriate barrier set, (R2) ensures that the splitting method can be applied to obtain suitable regeneration times for and (R3) guarantees that the inter-regeneration times have finite expectation.

For any let denote the number of time-steps for to reach after time 1:

- (R1)

-

There exists a set satisfying the following conditions:

-

(i)

and consists of strong -barriers of order ;

-

(ii)

there exist state , such that for every

where ;

-

(iii)

it holds ;

-

(iv)

there exists such that for all

-

(i)

- (R2)

-

Denote and . There exists a probability measure on and such that and

- (R3)

-

It holds .

Theorem 2.1.

Proof.

Construction of regeneration times. Denote

By (R2) we have that are probability measures. Hence for all the measure is a mixture of measures and :

| (9) |

We now apply the standard splitting technique to construct regeneration times for Markov chain . We define a homogeneous Markov chain on space as follows. Whenever we take and generate according to , and whenever we flip a coin: with probability we take and generate according to and with probability we take and generate according to (independently of ). The initial distribution of is defined by

It follows from (9) that . Let

Since are stopping times for and , we have by strong Markov property that are regeneration times for and therefore also for . In fact, for every , is a Markov chain with initial distribution and transition kernel .

Let , where denotes maximum, and let

Times are regeneration times for (since are regeneration times), with being a Markov chain with initial distribution and transition kernel for each . But this time we always have some separation between regeneration times:

| (10) |

Define

where denotes the indicator function and is as defined in (R1)(ii). Since , then (10) implies that are i.i.d. sequences. We will show that there exists such that

| (11) |

Denote

By (R1)(ii) every is almost surely finite. Denote and note that is i.i.d. sequence with . Indeed, fix and consider the homogeneous Markov chain , where . Since is stopping time for that Markov chain, we have by strong Markov property for every

Since by definition of , then . Furthermore, by strong Markov property depends on only through . But, as we saw, is independent of and therefore also of . This implies that is i.i.d. as claimed. Thus

which implies that satisfying (11) indeed exists.

Take now

Note that by (11) are almost surely finite. Again, are stopping times for and , so it follows from strong Markov property and (10) that are regeneration times for , with being a Markov chain with initial distribution and transition kernel for each . Also, by construction satisfies for .

Finally, we take

Note that by (R1)(iv) and the assumption of (R2) are almost surely finite. We will now show are regeneration times for . Let

and let be such that . Hence if and only if and . Also note that by (10) . We can express the conditional distribution of , , given past history:

Here the first equality follows because ; the second equality can be easily confirmed using the fact that for every and ; the third equality follows from the fact that is independent of (recall that is a regeneration time); the fourth equality follows from the fact that . That are regeneration times for easily follows. Also, we have for all by construction and by the assumption ((R1)(iii)). Therefore . Also by (R1)(i) are strong 1-nodes, and so by piecewise construction with lexicographic tie-breaking inside each piece the process is regenerative as claimed.

Inter-regeneration times have finite mean. We will now show that . Denote , so that by (R3) . We write for any event and for any random variable . First we show that

| (12) |

where denotes minimum. Indeed, note that for any and

Therefore, for every ,

This implies (12).

Next, we will show that . Denote

Exactly like in the case of , it can be shown that is i.i.d. with . Set and . Note that for any

Here we used the fact that for second equality, that is a stopping time for and strong Markov property for third equality, and (12) for the inequality. Thus we have

Since has a geometric distribution, then , as claimed.

It follows that . Next, let be such that . Then has negative binomial distribution,

Therefore

where the equality follows by Wald’s equation.

Finally, let be such that . Then has negative binomial distribution,

and applying Wald’s equation again gives the desired result:

∎

Recall the sequence and set of (PMM1). A set is called regular when is -irreducible, if for all satisfying , . When conditions of Theorem 1.2 hold, then regularity of is sufficient for (R1)-(R3) to hold:

Lemma 2.1.

Proof.

We omit some of the technical details from the proof since they largely concern the specific construction of the barrier set given in [28]. By Theorem 1.2 there exists barrier set consisting of strong 1-barriers of order . Using the lower semi-continuity assumption, this barrier set can be constructed so that it satisfies (R1) with some and . Furthermore, denoting , we may with no loss of generality assume that for all . There exists such that set

| (13) |

is non-empty. Since is open, then by the lower semi-continuity assumption (13) is also open, so there exist open balls such that is contained in (13). Thus and for all . By construction of (see [28] for details) we may with no loss of generality assume that . For any write for . Take and

Then for all

and so (R2) holds. Since and since (R1)(ii) implies (see [32, Prop. 8.3.7]), then (R3) follows by regularity of . ∎

3 Examples

3.1 Hidden Markov model

We consider some simple examples of applications of Theorem 2.1 to specific models. For HMM no additional conditions than those of barrier construction theorem 1.1 are needed for (R1)-(R3) to hold.

Proof.

The assumptions of the statement guarantee the existence of the barrier set consisting of strong -barriers with fixed order for some labelling of . Furthermore, it follows from the construction of that (R1) holds with and – see [28] for details. Recall that denote the emission densities with respect to measure . For denote . The barrier set is constructed in such a way that – see [28]. For any and we write . Taking now

we have that (R2) is fulfilled with . Indeed, for all

Finally note that since is -irreducible, where

then (R1)(ii) implies (see [32, Prop. 8.3.7]). It is not difficult to show that in case of HMM with irreducible every set in is regular and so (R3) holds. ∎

3.2 Discrete

Consider the case where is discrete (finite or countable) and is an irreducible and positive recurrent Markov chain with (discrete) state space . Here the state-space refers to the set of possible values of . Note that can be a proper subset . Recall the definition of (6). We assume that the transition kernel is defined on and so for every .

3.3 Linear Markov switching model

Let for some and for each state let be an i.i.d. sequence of random variables on with having density with respect to Lebesgue measure on . We consider the “linear Markov switching model”, where is defined recursively by

| (16) |

Here are some matrices, is a Markov chain with transition matrix , is some random variable on , and random variables are assumed to be independent and independent of and . Recall that for Markov switching model, the transition density expresses as . For the current model measure is Lebesgue measure on and . When are zero-matrices, then the linear Markov switching model simply becomes HMM with being the emission densities. When , we obtain the “switching linear autoregression of order 1”. The switching linear autoregressions are popular in econometric modelling, see e.g. [14, 15, 16, 13].

To show that (R1)-(R3) hold for the linear Markov switching model it suffices to show that the conditions of Lemma 2.1 are fulfilled. That is strictly positive is trivially fulfilled in case of Lebesgue measure on . That are lower semi-continuous and bounded is fulfilled when are lower semi-continuous and bounded (composition of lower semi-continuous function with continuous function is lower semi-continuous). The conditions for (PMM1) are given by

Lemma 3.3.

[28, Lem. 4.2] Let be the linear Markov switching model. If the following condition is fulfilled, then satisfies (PMM1) with being an open ball: there exists such that

-

(i)

;

-

(ii)

is reachable;

-

(iii)

is continuous at for all , and

In what follows, for any and let denote an open ball in with respect to 2-norm with center point and radius . The conditions for (PMM2) are given by

Lemma 3.4.

[28, Lem. 4.1] Let be the linear Markov switching model. If the following conditions are fulfilled, then satisfies (PMM2).

-

(i)

There exists set and such that the following two conditions are satisfied:

-

1.

for , if and only if ;

-

2.

the sub-stochastic matrix is primitive, i.e. there exists such that matrix has only positive elements.

-

1.

-

(ii)

Denote . There exists such that is reachable.

Conditions (i) and (ii) are not very restrictive. For example, when all the elements of are positive, then (i) is fulfilled if densities are either positive around 0 or zero around 0 and there exists at least one such that is positive around 0. If densities are all positive around 0, then (i) is fulfilled when is primitive with . If are positive everywhere and is irreducible, then all points in are reachable and so (ii) trivially holds.

For we denote with the 1-norm of , and for a matrix we denote with the 1-norm of matrix , that is is the maximum absolute column sum of . The following lemma addresses Harris recurrence of and regularity of sets in . This can be proved analogously to Lemma 4.3 in [28] by using [32, Th. 11.3.11] instead of [32, Th. 9.1.8].

Lemma 3.5.

Let be the linear Markov switching model. If the following conditions are fulfilled, then is Harris recurrent and every compact set in is regular:

-

(i)

is -irreducible and support of has non-empty interior;

-

(ii)

for all ;

-

(iii)

.

To recapitulate: if are lower semi-continuous and bounded and the conditions of Lemmas 3.3, 3.4 and 3.5 are fulfilled, then the conditions of Lemma 2.1 are satisfied and therefore (R1)-(R3) hold. Applying this fact to the case where are Gaussian yields

Corollary 3.1.

Let be the linear Markov switching model, with densities being Gaussian with respective mean vectors and positive definite covariance matrices . If the following conditions are fulfilled, then (R1)-(R3) hold.

-

(i)

Matrix is primitive, i.e. there exists such that consists of only positive elements.

-

(ii)

It holds .

-

(iii)

Matrix , where denotes the identity matrix of dimension , is non-singular, and for all and

where we denote , if or , and

otherwise

-

(iv)

It holds .

4 Asymptotics of Viterbi training: regeneration-based analysis

Regenerative property of has numerous potential theoretical applications ranging from SLLN’s and CLT’s to proving the existence of asymptotic risks. In this section we look at one such application, namely regeneration-based analysis of the Viterbi training algorithm.

Convergence of empirical measures

Firstly, let us state a general SLLN that provides a theoretical basis for several regeneration-based inferences, including the ones in the present section. The proof of the theorem is a rather straightforward application of the regenerative property of and is given in Appendix A. An analogous result for HMM was proven in [29]. Let denote, the Viterbi path of , i.e. . Here the tie-breaking scheme is assumed lexicographic as above. Whenever (R1)-(R3) hold, let denote the regeneration times of , as constructed in the proof of Theorem 2.1.

In what follows, we study empirical measures

where denotes the indicator function on . Also define measure

From Theorem 4.1 it follows that a.s., where stands for the weak convergence of measures:

Corollary 4.1.

Proof.

Denote

It follows from Theorem 4.1 that

– just take . To prove (18), we need to show that . This follows by the standard machinery of measure theory: if is a simple function, then the equality follows by definition of . For non-negative measurable take a monotone convergent sequence of simple functions and use Monotone Convergence Theorem to see that the equality holds also in the limit. For arbitrary we have by (17) that and , and hence follows.

The weak convergence now follows from the standard theory of weak convergence of probability measures, see e.g. proof of [9, Th. 11.4.1]. ∎

Note that when (R1)-(R3) hold, then there exists such that

where denotes the indicator function. Indeed, this follows directly from Theorem 4.1, by taking

The limit is simply the asymptotic pairwise misclassification rate of the Viterbi estimation. For any pair of measures and on common -field, we denote with the total variation distance of measures and :

where supremum is taken over all measurable . Recall (Lemma 2.2) that when (R1)-(R3) hold, then the transition kernel of admits an invariant probability measure . Let denote the probability measure with respect to the stationary initial distribution . The following result is useful for our purposes.

Proposition 4.1.

Proof.

Note that by Theorem 4.1

| (19) |

Similarly, denoting

we have

| (20) |

where is a probability measure defined by

Now we have for every

and so by (19)

By Lemma 2.2 (R1)-(R3) imply that is Harris recurrent and positive. To prove the statement, it suffices to show that . From the ergodic theorem for aperiodic and positive Harris Markov chains [32, Th. 13.3.3.] it follows that for all it holds , which implies

Thus applying Dominated Convergence Theorem to (20) yields . ∎

Viterbi training

The empirical measures are central in many Viterbi-inferences based applications. In this section we look at one of such applications, namely Viterbi training.

For any application of PMM one needs to estimate the parameters of the model. The standard go-to method of parameter estimation in case of Markov switching models is the EM-algorithm, also known as Baum-Welch or forward-backward algorithm [4, 1, 34, 14]. In practice the EM-algorithm is often replaced with the Viterbi training algorithm (VT) [35, 17, 31] (also known as segmental K-means algorithm [10, 18] and classification EM in the mixture case [5, 11]) due to its ease of implementation and significantly smaller computational cost. However, compared to the EM-algorithm, VT can sometimes lead to sub-optimal results. It could be argued that the closer the Viterbi path is to the real path, the better VT performs. Thus VT is expected to work well when the dimension of observation space is relatively high compared to the number of hidden states, since the Viterbi path is in that case – in some sense – probably very similar to the real hidden path. By the same logic, replacing a HMM with a more general PMM (for instance the linear Markov switching model) can improve the accuracy of the Viterbi path estimation and therefore also that of VT. We will see that asymptotic analysis of VT is made possible by the convergence of empirical measures and, therefore, by regenerativity of .

We start by formulation of VT for PMM’s. We assume that transition densities are known up to a parametrization , where is the unknown “true” parameter vector belonging to parameter space , . For any parameter vector denote with the Viterbi path of obtained by using the parameters . Hence . Viterbi training is a method of estimating the unknown parameters using the following algorithm.

Viterbi training algorithm:

-

1.

Choose , the initial values for the parameter vector, and set .

-

2.

Using current parameters , obtain the corresponding Viterbi path .

-

3.

Define empirical measure

and update the parameters by taking

-

4.

Put and repeat from step 2.

As a special case, we can consider the Markov switching model defined by transition kernel density , where is the unknown parameter vector. Then (as one can see by applying Lagrange multipliers method) the estimates of of at the 3rd step of Viterbi training algorithm can simply be calculated by

Then also , the estimates of at the 3rd step of Viterbi training algorithm, can be calculated separately by

where is the parameter space corresponding to . Recall that Markov switching model also includes HMM in which case is independent of .

Assume for now that (R1)-(R3) hold and is aperiodic. In the light of Theorem 4.1 we may want to seek the answer to the following question: what is the output of the 3rd step of the Viterbi training algorithm if the input is the correct parameter ? Ideally, we would like to see that that the output is in that case close to the input: . This is called the fixed point property. Write for . Assuming that is positive everywhere on and satisfies (17) we have by Corollary 4.1 that

This gives hope that at least under some conditions

| (21) |

In [22] an analogous convergence is proved under certain conditions. Although [22] deals with HMM’s only, we believe that the same idea can be applied to PMM as well to obtain the convergence (21). Denote

Assuming that (21) holds and that the sample size is sufficiently large, the fixed point property holds when . It is not difficult to confirm that has a density with respect to measure , where denotes counting measure on . Let denote this density. Writing in place of we have

It is not difficult to confirm that the invariant measure has a density with respect to measure – denote this density with . Assuming that and are both -integrable, we have

| (22) |

Defining measure by

we can see that (22) minimizes the Kullback-Leibler divergence of from . If the Viterbi path is perfect estimate of the hidden path, i.e. , then by Proposition 4.1 . The Kullback-Leibler divergence of from is minimal when , implying that the fixed point property indeed holds when the Viterbi path is perfect, at least under appropriate identifiability conditions. In practice however the Viterbi path is almost never perfect and so whether holds or not depends on how closely resembles . If the pairwise misclassification rate is small, then by Proposition 4.1 , and so the fixed point property is in that case expected to hold.

If is not close to , we can correct the estimation error at the 3rd step of the VT by taking the estimate to be

In case of HMM this modified version of the VT has been called the adjusted Viterbi training (AV) [29, 26, 22]. AV ensures that the fixed point property holds simply by virtue of convergence (21). The simulations in [26, 22] show how the fixed point property significantly improves the accuracy of the estimator so that AV outperforms VT and is comparable to EM-algorithm. The key component of AV is the map . This map is generally not known analytically and should therefore be estimated by simulations. The estimation takes some time and effort but could be worthwhile if a single model is to be applied repeatedly.

Simulations

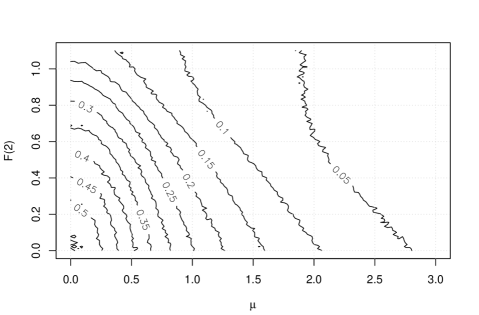

Based on the arguments above it should be believable that the pairwise misclassification rate provides a fairly adequate measure on how well VT performs in practice (smaller values of indicating a better performance). This rate also has the advantage of being easy to calculate in simulations. Recall now the linear Markov switching defined by (16). We consider the case where , , , , is standard normal and is normal with mean and standard deviation 1. It follows from Corollary 3.1 that (R1)-(R3) hold whenever and .

Figure 2 depicts the estimated value of depending on and . In case of Viterbi path is constantly 1 (due to lexicographic ordering) and all non- pairs, which constitute slightly more than half of all the pairs, are misclassified. As and increase, the misclassification rate decreases. The case corresponds to HMM. From Figure 2 we see that as increases, i.e. the model “moves away from HMM”, decreases.

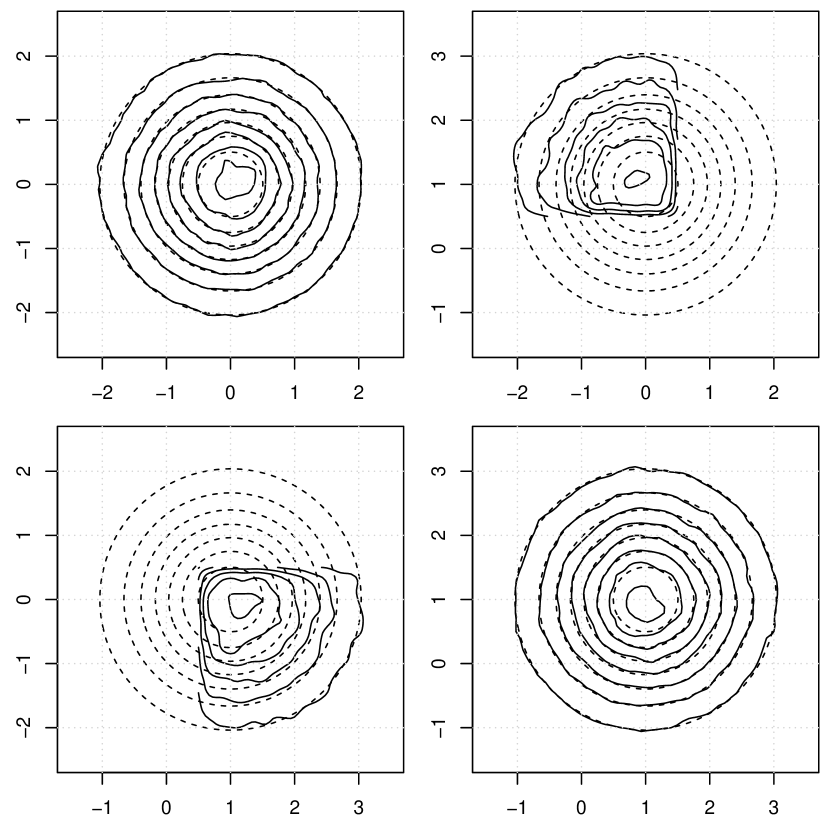

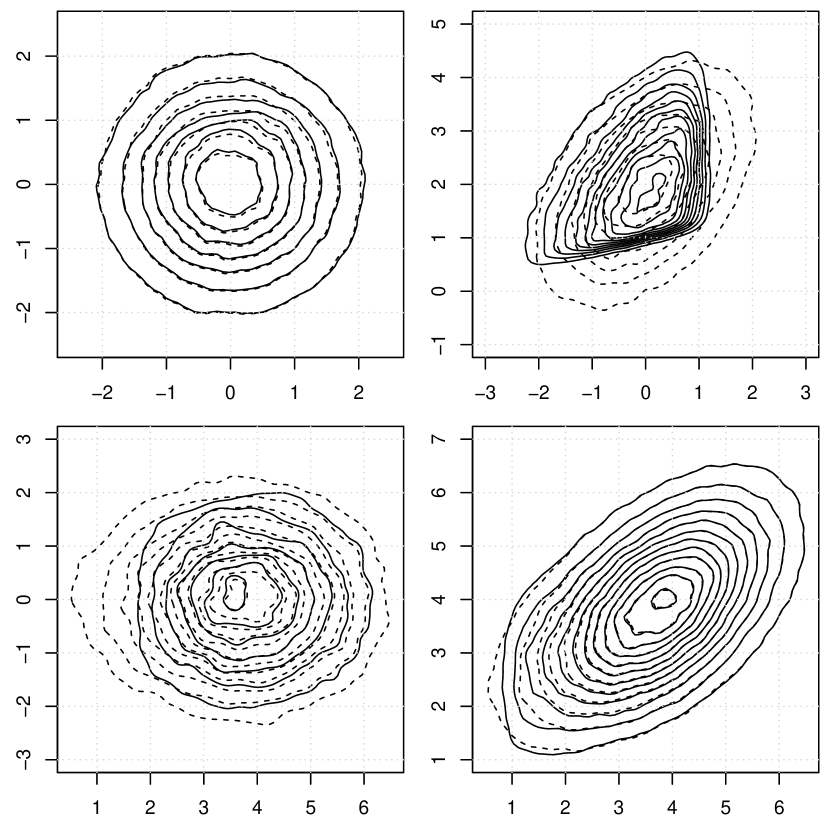

Let be a random vector having distribution . Figure 3 depicts the densities of , drawn with solid line, and , drawn with dotted line. The upper left, upper right, bottom left and bottom right plot represent pairs , respectively. In Figure 3(a) (i.e. the model is HMM) and . In Figure 3(b) and . In the HMM-case the density of is and can thus be directly calculated; all other densities are estimated by simulation. In the HMM-case (Figure 3(a)) the difference of densities and seem to be insignificant for and greater for . In the PMM-case (Figure 3(b)) the difference between two densities is still very small for while for pairs the densities appear to be closer than in the HMM-case. This accords with the fact that in the HMM-case – as can be seen from Figure 2 – the value of is about 0.25 while in the PMM-case is much smaller – roughly about 0.05.

Appendix A Proof of Theorem 4.1

Let be a measurable function satisfying (17). Denote

and

We need to show that

Denote . The regeneration times and Viterbi process are constructed in such a way that for each . Thus for we have

| (23) |

We will take a closer look at the three terms on the right side of (23). Since a.s., then the first term converges to zero (a.s.) as .

Next we show that the third term converges to zero as well. Denote

The regeneration times split into i.i.d. cycles, so and are both i.i.d. ( is not generally i.i.d. because and are not independent). By (17) , so by SLLN we have

This implies that converges to zero as increases. Since , a.s., we have

as claimed.

Denote

It remains to show that the second term on the right side of (23) converges to . We have by SLLN almost surely

and so inequalities imply convergence

Note that . By regenerativity and are both i.i.d., so by SLLN

References

- Baum and Petrie [1966] L. E. Baum and T. Petrie. Statistical inference for probabilistic functions of finite state markov chains. The annals of mathematical statistics, 37(6):1554–1563, 1966.

- Caliebe [2006] A. Caliebe. Properties of the maximum a posteriori path estimator in hidden Markov models. IEEE Transactions on Information Theory, 52(1):41–51, 2006.

- Caliebe and Rösler [2002] A. Caliebe and U. Rösler. Convergence of the maximum a posteriori path estimator in hidden Markov models. IEEE Transactions on Information Theory, 48(7):1750–1758, 2002.

- Cappé et al. [2005] O. Cappé, E. Moulines, and T. Rydén. Inference in hidden Markov models. Springer, 2005.

- Celeux and Govaert [1992] G. Celeux and G. Govaert. A classification em algorithm for clustering and two stochastic versions. Computational statistics & Data analysis, 14(3):315–332, 1992.

- Chigansky and Ritov [2011] P. Chigansky and Y. Ritov. On the Viterbi process with continuous state space. Bernoulli, 17(2):609–627, 2011.

- Derrode and Piecynski [2004] S. Derrode and W. Piecynski. Signal and image segmentation using pairwise Markov chains. IEEE Transactions on Signal Processing, 52(9):2477–2489, 2004.

- Derrode and Piecynski [2013] S. Derrode and W. Piecynski. Unsupervised data classification using pairwise Markov chains with automatic copula selection. Computational Statistics and Data Analysis, 63:81–98, 2013.

- Dudley [2002] R. M. Dudley. Real analysis and probability, volume 74. Cambridge University Press, 2002.

- Ephraim and Merhav [2002] Y. Ephraim and N. Merhav. Hidden markov processes. IEEE Transactions on information theory, 48(6):1518–1569, 2002.

- Fraley and Raftery [2002] C. Fraley and A. E. Raftery. Model-based clustering, discriminant analysis, and density estimation. Journal of the American statistical Association, 97(458):611–631, 2002.

- Ghosh et al. [2011] A. Ghosh, E. Kleiman, and A. Roitershtein. Large deviation bounds for functionals of Viterbi paths. IEEE Transactions on Information Theory, 57(6):3932–3937, 2011.

- Goodwin [1993] T. H. Goodwin. Business-cycle analysis with a markov-switching model. Journal of Business & Economic Statistics, 11(3):331–339, 1993.

- Hamilton [1989] J. D. Hamilton. A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica: Journal of the Econometric Society, pages 357–384, 1989.

- Hamilton [1990] J. D. Hamilton. Analysis of time series subject to changes in regime. Journal of econometrics, 45(1-2):39–70, 1990.

- Hamilton [2010] J. D. Hamilton. Regime switching models. In Macroeconometrics and time series analysis, pages 202–209. Springer, 2010.

- Huang et al. [1990] X. D. Huang, Y. Ariki, and M. A. Jack. Hidden Markov models for speech recognition, volume 2004. Edinburgh university press Edinburgh, 1990.

- Juang and Rabiner [1990] B.-H. Juang and L. R. Rabiner. The segmental k-means algorithm for estimating parameters of hidden markov models. IEEE Transactions on Acoustics, Speech, and Signal Processing, 38(9):1639–1641, 1990.

- Kalashnikov [1994] V. V. Kalashnikov. Topics on regenerative processes. CRC Press, 1994.

- Koloydenko and Lember [2008] A. Koloydenko and J. Lember. Infinite Viterbi alignments in the two state hidden Markov models. Acta et Commentationes Universitatis Tartuensis de Mathematica, 12:109–124, 2008.

- Koloydenko and Lember [2014] A. Koloydenko and J. Lember. Bridging Viterbi and posterior decoding: A generalized risk approach to hidden path inference based on hidden Markov models. Journal of Machine Learning Research, 15:1–58, 2014.

- Koloydenko et al. [2007] A. Koloydenko, M. Käärik, and J. Lember. On adjusted Viterbi training. Acta Applicandae Mathematicae, 96(1):309–326, 2007.

- Kuljus and Lember [2012] K. Kuljus and J. Lember. Asymptotic risks of Viterbi segmentation. Stochastic Processes and their Applications, 122(9):3312–3341, 2012.

- Kuljus and Lember [2016] K. Kuljus and J. Lember. On the accuracy of the MAP inference in HMMs. Methodology and Computing in Applied Probability, 18(3):597–627, 2016.

- Lember [2011] J. Lember. On approximation of smoothing probabilities for hidden Markov models. Statistics & probability letters, 81(2):310–316, 2011.

- Lember and Koloydenko [2007] J. Lember and A. Koloydenko. Adjusted Viterbi training. A proof of concept. Probability in the Engineering and Informational Sciences, 21(3):451–475, 2007.

- Lember and Koloydenko [2010] J. Lember and A. Koloydenko. A constructive proof of the existence of Viterbi processes. IEEE Transactions on Information Theory, 56(4):2017–2033, 2010.

- Lember and Sova [2017] J. Lember and J. Sova. Existence of infinite viterbi path for pairwise markov models. arXiv preprint arXiv:1708.03799, 2017.

- Lember et al. [2008] J. Lember, A. Koloydenko, et al. The adjusted Viterbi training for hidden Markov models. Bernoulli, 14(1):180–206, 2008.

- Lember et al. [2011] J. Lember, K. Kuljus, and A. Koloydenko. Theory of segmentation. In P. Dymarsky, editor, Hidden Markov Models, Theory and Applications, pages 51–84. InTech, 2011.

- McDermott and Hazen [2004] E. McDermott and T. J. Hazen. Minimum classification error training of landmark models for real-time continuous speech recognition. In Acoustics, Speech, and Signal Processing, 2004. Proceedings.(ICASSP’04). IEEE International Conference on, volume 1, pages I–937. IEEE, 2004.

- Meyn and Tweedie [2009] S. P. Meyn and R. Tweedie. Markov Chains and Stochastic Stability. Cambridge University Press, 2009.

- Pieczynski [2003] W. Pieczynski. Pairwise Markov chains. IEEE Transactions on Pattern Analysis and Machine Intelligence, 25(5):634–639, 2003.

- Rabiner [1989] L. R. Rabiner. A tutorial on hidden markov models and selected applications in speech recognition. Proceedings of the IEEE, 77(2):257–286, 1989.

- Rodríguez and Torres [2003] L. Rodríguez and I. Torres. Comparative study of the baum-welch and viterbi training algorithms applied to read and spontaneous speech recognition. Pattern Recognition and Image Analysis, pages 847–857, 2003.

- Šrámek et al. [2007] R. Šrámek, B. Brejová, and T. Vinar. On-line viterbi algorithm for analysis of long biological sequences. Algorithms in Bioinformatics, 4645:240–251, 2007.

- Thorisson [2000] H. Thorisson. Coupling, stationarity, and regeneration, volume 200. Springer New York, 2000.

- Yau and Holmes [2013] C. Yau and C. Holmes. A decision-theoretic approach for segmental classification. Annals of Applied Statistics, 7(3):1814–1835, 2013.