A Powerful Subvector Anderson-Rubin Test in Linear Instrumental Variables Regression with Conditional Heteroskedasticity††thanks: We would like to thank the Editor, Peter Phillips, the Co-Editor, Michael Jansson, and two referees for very helpful comments. Guggenberger thanks the European University Institute for its hospitality while parts of this paper were drafted. Mavroeidis gratefully acknowledges the research support of the European Research Council via Consolidator grant number 647152. We would like to thank Donald Andrews for detailed comments and for providing his Gauss code of, and explanations about, Andrews (2017) and Lixiong Li for outstanding research assistance for the Monte Carlo study. We thank seminar participants in Amsterdam, Bologna, Bristol, Florence (EUI), Indiana, Konstanz, Manchester, Mannheim, Paris (PSE), Pompeu Fabra, Regensburg, Rotterdam, Singapore (NUS and SMU), Tilburg, Toulouse, Tübingen, and Zurich, and conference participants at the Institute for Fiscal Studies (London) for helpful comments.

Abstract

We introduce a new test for a two-sided hypothesis involving a subset of the structural parameter vector in the linear instrumental variables (IVs) model. Guggenberger et al. (2019), GKM19 from now on, introduce a subvector Anderson-Rubin (AR) test with data-dependent critical values that has asymptotic size equal to nominal size for a parameter space that allows for arbitrary strength or weakness of the IVs and has uniformly nonsmaller power than the projected AR test studied in Guggenberger et al. (2012). However, GKM19 imposes the restrictive assumption of conditional homoskedasticity. The main contribution here is to robustify the procedure in GKM19 to arbitrary forms of conditional heteroskedasticity. We first adapt the method in GKM19 to a setup where a certain covariance matrix has an approximate Kronecker product (AKP) structure which nests conditional homoskedasticity. The new test equals this adaption when the data is consistent with AKP structure as decided by a model selection procedure. Otherwise the test equals the AR/AR test in Andrews (2017) that is fully robust to conditional heteroskedasticity but less powerful than the adapted method. We show theoretically that the new test has asymptotic size bounded by the nominal size and document improved power relative to the AR/AR test in a wide array of Monte Carlo simulations when the covariance matrix is not too far from AKP.

Keywords: Asymptotic size, conditional heteroskedasticity, Kronecker product, linear IV regression, subvector inference, weak instruments

JEL codes: C12, C26

1 Introduction

Robust and powerful subvector inference constitutes an important problem in Econometrics. For instance, it is standard practice to report confidence intervals on each of the coefficients in a linear regression model. By robust we mean a testing procedure for a hypothesis of (or a confidence region for) a subset of the structural parameter vector such that the asymptotic size is bounded by the nominal size for a parameter space that allows for weak or partial identification. Recent contributions to robust subvector inference have been made in the context of the linear instrumental variables (IVs from now on) model (see, for example, Dufour and Taamouti (2005), Guggenberger et al. (2012) (GKMC from now on), Guggenberger et al. (2019) (GKM19 from now on), and Kleibergen (2021)), GMM models (see, for example, Chaudhuri and Zivot (2011), Andrews and Cheng (2014), Andrews and Mikusheva (2016), Andrews (2017), and Han and McCloskey (2019)), and also models defined by moment (in)equalities (see, for example, Bugni et al. (2017), Gafarov (2017), and Kaido et al. (2019)). GKM19 introduce a new subvector test that compares the AR subvector statistic to conditional critical values that adapt to the strength or weakness of identification and verify that the resulting test has correct asymptotic size for a parameter space that imposes conditional homoskedasticity (CHOM from now on) and uniformly improves on the power of the projected AR test studied in Dufour and Taamouti (2005).

The contribution of the current paper is to provide a robust subvector test that improves the power of another robust subvector test by combining it with a more powerful test that is robust for only a smaller parameter space. More specifically, in the context of the linear IV model, we first provide a modification of the subvector AR test of GKM19, called the ARAKP,α test, where denotes the nominal size. We verify that it has correct asymptotic size for a parameter space that nests the setup with CHOM and also allows for particular cases of conditional heteroskedasticity (CHET from now on), namely setups where a particular covariance matrix has a Kronecker product (KP from now on) structure. For example, the data generating process (DGP from now on) has a KP structure if the vector of structural and reduced-form errors equals a random vector independent of the IVs times a scalar function of the IVs. In particular then, the variances of all the errors depend on the IVs by the same multiplicative constant given as a scalar function of the IVs. In the companion paper Guggenberger et al. (2022) (GKM22 from now on) we find that KP structure is not rejected at the 5% nominal size in more than 63% of empirical data sets we studied of several recently published empirical papers (namely, 38 of 60 specifications are not rejected; and, including cases with clustering, 56 out of 118 are not rejected). For comparison, CHOM is rejected for 57 of the 60 specifications considered at the 5% nominal size, using the test in Kelejian (1982). Of course, these findings do not prove that empirical data sets do have KP structure as the low number of rejections of KP structure may be due to type II errors of the test. However, coupled with the quite favorable finite sample power results of the test of KP structure reported in GKM22 (for sample sizes of ) we believe that KP structure might be compatible with a sizable subset of empirical data sets.

Second, depending on a model selection mechanism that determines whether the data are compatible with KP, the recommended test then equals the ARAKP,α test or the AR/AR test in Andrews (2017) that is robust to arbitrary forms of CHET. We show that the recommended test has correct asymptotic size. An important ingredient in establishing that is showing that the ARAKP,α test does not reject less often under the null hypothesis than the AR/AR test when the data are close to KP structure.

We propose two different model selection methods. One is based on the KPST test statistic introduced in GKM22 for testing the null hypothesis that a covariance matrix has KP structure. The other one is based on the standardized norm of the distance between the covariance matrix estimator and its closest KP approximation. As in the model selection method proposed in Andrews and Soares (2010), we compare the test statistic to a user chosen threshold that, in the asymptotics, is let go to infinity. The thresholds can be chosen differently depending on the number of IVs and parameters not under test. Based on comprehensive finite sample simulations we provide choices for the thresholds for several values of that lead to good control of the finite sample size.

As the main contribution of the paper, we verify that the resulting test, called test, has asymptotic size bounded by the nominal size under certain conditions on the selection mechanism and implementation of the AR/AR test at nominal size for some arbitrarily small .

In a Monte Carlo study, we compare the suggested new test with several alternatives given in Andrews (2017), in particular, the AR/AR and the AR/QLR1 tests. Andrews (2017) fills a very important gap in the literature on subvector inference by providing two-step Bonferroni-like methods111See McCloskey (2017) for a general reference on Bonferroni methods in nonstandard testing setups. for a rich class of models that nests GMM, that i) control the asymptotic size under relatively mild high-level conditions that allow for CHET, ii) are asymptotically non-conservative (in contrast to standard Bonferroni methods) and iii) for the case of AR/QLR1 is asymptotically efficient under strong identification (while the AR/AR test is not asymptotically efficient under strong identification in overidentified situations). In contrast, the test considered here, , can only be used in the linear IV model and is not asymptotically efficient under strong identification. The Monte Carlo study finds that has uniformly higher rejection probabilities than the AR/AR test for all the DGPs considered. That includes the null rejection probabilities (NRPs from now on) with the test having finite sample size of 6% versus the 5.4% of the AR/AR test at nominal size 5%. Based on the Monte Carlo study we conclude that relative to the AR/QLR1 test, can be a useful alternative in terms of power in situations of weak or mixed identification strengths when the degree of overidentification is small and the covariance matrix of the data is not too far from KP structure. Whenever the data are compatible with KP structure, it also offers an important computational advantage because the ARAKP,α test is given in closed form. In contrast, implementation of the two-step Bonferroni-like methods require minimization of a statistic over a set that has dimension equal to the number of parameters not under test. The computation time should grow exponentially in the dimension of that set which constitutes a computational challenge especially when an applied researcher uses the proposed methods for the construction of a confidence region by test inversion. This being said, an applied researcher who uses the test has to be ready to implement the AR/AR test in case it is determined that KP structure is not compatible with the data. Given the construction of the ARAKP,α test it is not surprising to find the relative best performance of the test to occur under weak identification. Namely, the critical values of the former test adapt to the strength of identification and can be substantially lower than the corresponding chi-square critical values when identification is deemed to be weak.

The rest of the paper is organized as follows. In Section 2 we introduce a version of a subvector Anderson and Rubin (1949) test that has correct asymptotic size for a parameter space that imposes an approximate Kronecker product (AKP) structure for the covariance matrix. In Section 3 we introduce the new test that has correct asymptotic size for a parameter space that does not impose any structure on the covariance matrix and therefore, in particular, allows for arbitrary forms of conditional heteroskedasticity. Finally, in Section 4 we study the finite sample properties of the test. Proofs are given in the Appendix at the end.

Notation: Throughout the paper, we denote by “” the KP of two matrices, by the column vectorization of a matrix, and by the Frobenius norm.222Recall the Frobenius norm for a matrix is defined as . When is a vector the Frobenius and the Euclidean norm are numerically equivalent. We use the notation and for any full rank matrix

2 Subvector AR Test under Approximate Kronecker Product Structure

Assume the linear IV model is given by the equations

| (2.1) |

where and Here, contains endogenous regressors, while the regressors may be endogenous or exogenous. We assume that and The reduced form can be written as

| (2.2) |

where (which depends on the true and By for we denote the -th row of written as a column vector and similarly for other matrices.

The objective is to test the subvector hypothesis

| (2.3) |

using tests whose size, i.e. the highest NRP over a large class of distributions for and the unrestricted nuisance parameters and , equals the nominal size , at least asymptotically. In particular, weak identification and non-identification of and are allowed for. The setup allows testing the coefficients of exogenous or endogenous regressors in the presence of endogenous regressors . We impose the following assumption as in GKM19 (from where the name of the assumption is inherited).

Assumption B: The random vectors for in (2.1) are i.i.d. with distribution

For a given sequence in we define a sequence of parameter spaces for under the null hypothesis that is larger than the corresponding ones in GKMC and GKM19 in that general forms of AKP structures for the variance matrix

| (2.4) |

are allowed for.333Regarding the notation and elsewhere, note that we allow as components of a vector column vectors, matrices (of different dimensions), and distributions. Namely, for (which equals ), and let

| (2.5) |

for symmetric matrices such that

| (2.6) |

positive definite (pd from now on) symmetric matrices (whose upper left element is normalized to 1) and . Note that the factors in the KP are not uniquely defined due to the summand . Note that no restriction is imposed on the variance matrix of and, in particular, does not need to factor into a KP.

The factorization of the covariance matrix into an AKP in line three of (2.5) is a weaker assumption than CHOM. Under CHOM, we have and (prior to the normalization of the upper left element of ) and The AKP structure allowed for here (but not in GKMC and GKM19) also covers some important cases of CHET involving .

Examples. i) Consider the case in (2.1) where are i.i.d. zero mean with a pd variance matrix, independent of and for some scalar valued function of 444For example, Andrews (2017) considers In that case, the covariance matrix can be written

| (2.7) |

and thus has KP structure even though, obviously, CHOM is not satisfied because

| (2.8) |

depends on

We can construct illustrative examples where the proportionality (that would imply KP structure) holds. Consider e.g. the model

where the covariates and are exogenous, the variables are endogenous, and has heterogeneous causal effects on denoted by respectively. Let define and and assume that are orthogonal to Then, this fits exactly into the setup above with In other words, KP structure can result as a special case of heterogeneous causal effects.

ii) In a wage regression to assess the effect of ”years of education”, the assumption of CHOM would require that e.g. the variance of ”wage” does not depend on the included regressor ”race”. This assumption is incompatible with recent US data where the wage dispersion is largest for Asians. Instead, the construction in i) allows for dependence of the variances of the regressand and all endogenous regressors on a scalar function of The maintained restriction is that all these variances are affected approximately by the same scalar function of In the related paper, GKM22, we test the null hypothesis of KP structure for 118 specifications in about a dozen highly cited papers and find that at the 5% nominal size in 47.5% of the cases the null is not rejected.

In this section we will introduce a new conditional subvector ARAKP test and show it has asymptotic size with respect to the parameter space equal to the nominal size. We next define the new test statistic and the critical value for the case considered here of AKP structure.

Estimation of the two factors in the AKP structure: Define

| (2.9) |

and with rows given by for 555For simplicity, we do not use the more precise notation for It is explained in detail in Comment 3 below Theorem 1 why we introduce namely to obtain invariance of the testing procedure with respect to nonsingular transformations of the IVs. Define an estimator of the matrix

| (2.10) |

by

| (2.11) |

Note that is automatically a centered estimator because, as straightforward calculations show, From it follows that for

| (2.12) |

Let

| (2.13) |

where the minimum is taken over for being pd, symmetric matrices, and normalized such that the upper left element of equals 1.

It can be shown that are given in closed form by the following construction.666This follows from a combination of Lemma 2 below and Theorem 5.8 in van Loan and Pitsianis (1993, Corollary 2.2). First, for a pd matrix define the rearrangement of as

| (2.17) | ||||

| (2.21) |

where denotes the submatrix of dimensions where Second, denote by

| (2.22) |

a singular value decomposition of ,777In van Loan and Pitsianis (1993, Corollary 2), the orthogonal matrices and are called and respectively, notation that we have already used for other objects. where the singular values for are ordered non-increasingly. Finally, denote by and singular vectors corresponding to the largest singular value and let denote the first component of Then, letting the role of be played by in (2.22), minimizers to (2.13) are defined by

| (2.23) |

where whenever is pd. By Lemma 4 below, the definition given in (2.23) is unique for all large enough wp1888Note that it would not be unique if the eigenspace associated with the largest singular value had dimension larger than 1. and

| (2.24) |

under certain sequences as defined in for which (where is defined in (2.10) with replaced by ), (as defined in (2.12)), and the upper left element of is normalized to 1.

Definition of the conditional subvector test: We denote the subvector AR statistic when the variance matrix has AKP structure by and define it as the smallest root of the roots (ordered nonincreasingly) of the characteristic polynomial

| (2.25) |

The conditional subvector test ARAKP,α rejects at nominal size if

| (2.26) |

where is defined as follows. Muirhead (1978), in the case where and assuming normality, provides an approximate, nuisance parameter free, conditional density of the smaller eigenvalue given the larger one for any degree of overidentification see (2.12) in GKM19 for the conditional pdf. For given and arbitrary denotes the -quantile of that approximation. GKM19 (Table 1 and Supplement C) provide for and a fine grid of values for say for some large We reproduce Table 1 (that covers the case and from GKM19 below. Conditional critical values for values of not reported in the tables are obtained by linear interpolation. Specifically, let denote the quantile of the distribution whose density is given by (2.12) in GKM19 with replaced by . The end point of the grid should be chosen high enough so that . For any realization of , find such that with and , and let

| (2.27) |

Table 1: for for various values of

| cv | cv | cv | cv | cv | cv | cv | cv | cv | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1.2 | 1.1 | 2.1 | 1.9 | 3.2 | 2.9 | 4.5 | 3.9 | 5.9 | 4.9 | 7.4 | 5.9 | 9.4 | 6.9 | 12.5 | 7.9 | 20.9 | 8.9 |

| 1.3 | 1.2 | 2.3 | 2.1 | 3.5 | 3.1 | 4.7 | 4.1 | 6.2 | 5.1 | 7.8 | 6.1 | 9.9 | 7.1 | 13.4 | 8.1 | 26.5 | 9.1 |

| 1.4 | 1.3 | 2.5 | 2.3 | 3.7 | 3.3 | 5.0 | 4.3 | 6.5 | 5.3 | 8.2 | 6.3 | 10.5 | 7.3 | 14.5 | 8.3 | 39.9 | 9.3 |

| 1.6 | 1.5 | 2.7 | 2.5 | 4.0 | 3.5 | 5.3 | 4.5 | 6.8 | 5.5 | 8.6 | 6.5 | 11.1 | 7.5 | 15.9 | 8.5 | 57.4 | 9.4 |

| 1.8 | 1.7 | 3.0 | 2.7 | 4.2 | 3.7 | 5.6 | 4.7 | 7.1 | 5.7 | 9.0 | 6.7 | 11.7 | 7.7 | 17.9 | 8.7 | 1000 | 9.48 |

Denote by the probability of an event under the null hypothesis when the true values of the structural and reduced form parameters and the distribution of the random variables are given by Recall the definition of the parameter space in (2.5). We can now formulate the main result of this section.

Theorem 1

Under Assumption B, the conditional subvector test ARAKP,α defined in 2.26 implemented at nominal size has asymptotic size, i.e.

equal to for and

Comment. 1. The conditional subvector test ARAKP,α adapts the test in GKM19 from a setup under CHOM to AKP structure. The modification involves replacing the matrices and in GKM19 by the matrices and respectively, in (2.25) to account for the more general structure of the covariance matrix. Some portions of the proof follow similar steps as the proof of Theorem 5 in GKM19. In particular, one portion of the proof relies on a one-dimensional simulation exercise to prove that the NRPs are bounded by the nominal size. This exercise could be extended to choices of and beyond those in the theorem and likely the theorem would extend to many more choices.

2. Trivially, under the same assumptions as in Theorem 1, we obtain that

That is, the generalization of the subvector test in GKMC to AKP structure has correct asymptotic size. This result is obtained fully analytically; its proof does not require any simulations.

3. Invariance with respect to nonsingular transformations of the IV matrix. The identifying power of the model comes from the moment condition This moment condition obviously still holds when the instrument vector is premultiplied by a nonrandom nonsingular matrix i.e. It then seems reasonable to look for testing procedures whose outcome is invariant to such nonsingular transformations. In the weak IV literature, e.g. Andrews et al. (2006) and Andrews et al. (2019) and references therein, the class of (similar) invariant tests to orthogonal transformations , that is, changes of the coordinate system, has been studied. The transformation of the IVs in (2.9) is performed in order for the test to be invariant to nonsingular transformations of the IVs.

If the conditional subvector ARAKP test defined in (2.26) (and in (2.11)) was defined with in place of it would be invariant to orthogonal transformations but not necessarily to nonsingular ones. To see the former, denote by the matrix when the instrument vector has been transformed to (and consequently is changed to Then the claim follows from (which holds for any nonsingular matrix by straightforward calculations using for any conformable matrices and and which implies and when is orthogonal, where again and denote the matrices and when the instrument vector has been transformed to . It then follows that the matrix in (2.25) (and thus its eigenvalues) remain invariant under orthogonal transformations of the instrument matrix. This test however is not invariant in general to arbitrary nonsingular transformations.

But with the replacement of by as done in (2.11) and, correspondingly, by in (2.25), the test is invariant against nonsingular transformations . The invariance of this test to arbitrary nonsingular transformations of the instrument matrix (which leads to a transformation of to ) follows from straightforward calculations and the fact that the matrix

| (2.28) |

is orthogonal. In particular, one can easily show that the matrices and that appear as ingredients in the conditional subvector test ARAKP,α with are related to the corresponding matrices and , when is an arbitrary nonsingular matrix, via

| (2.29) |

which immediately implies the desired invariance result.

4. The conditional subvector test can be generalized to a stationary time series setting, see the Appendix, Section A.5, for details. In the context of a time series setting we offer another example of AKP structure. Namely, consider a structural vector autoregression where and suppose that . If for some scalar function of time i.e., the volatilities of all the shocks change over time in a proportional manner, then the variance of has KP structure. In this model, identification can be achieved by exclusion restrictions (Sims, 1980) that render some of valid instruments. It can also be achieved with external instruments if available (Stock and Watson, 2018). Time-variation in volatilities has been reported in many contexts. For instance, the ‘great moderation’ is a well-documented phenomenon of a fall in macroeconomic volatility in the US in the early 1980s (cf. Bernanke (2004), ch. 4). AKP would result if the fall in the volatilities were similar across variables.

5. Note that under the null hypothesis the test does not depend on the value of the reduced form matrix because the test statistic and the critical value are affected by only through

6. GKM19 establish that the conditional subvector AR test introduced there enjoys near optimality properties in the linear IV model with conditional homoskedasticity in a certain class of tests that depend on the data only through the roots when On the other hand, when gets bigger the test may be quite conservative. The power gains over the projected AR subvector test discussed in Dufour and Taamouti (2005) arise in weakly identified scenarios while under strong identification these two tests become identical. Similarly, we expect the power properties of the new conditional subvector test ARAKP,α to be most competitive for small in particular, when in weakly identified situations.

Intuition behind the result derived in GKM19 that conditioning on the largest eigenvalue when leads to a test with correct size is based on i) the corresponding result for and ii) the so-called ”inclusion principle” that provides a ranking of the corresponding eigenvalues of a Hermitian matrix and its principal submatrices (see GKM19 bottom p.499-500, in particular eq (2.23)).

3 Subvector Testing under Arbitrary Forms of Conditional Heteroskedasticity

We now allow for arbitrary forms of CHET, that is, the parameter space does not impose an AKP structure for . We describe a testing procedure under high level assumptions that we then verify in the next subsections for particular implementations of the test. In particular, Lemma 1 below verifies Assumptions RT and RP below for a particular implementation of the AR/AR test.

In what follows, is a generic parameter space for that does not impose an AKP structure, but if the restriction as in in (2.5) was added to the conditions in then For example, the null parameter space may impose stronger moment conditions than so that certain Lyapunov CLTs apply. See the definitions of in the next subsections. We summarize the restrictions on the parameter space (PS) in the following assumption.

Assumption PS: where is equal to without the condition (AKP structure) and without the assumptions for

We assume there exists a robust test (RT) that has asymptotic size for the parameter space bounded by the nominal size . For example, in the next subsection we consider a particular implementation of the AR/AR test in Andrews (2017). In general, we think of as a test whose power can be substantially improved on by the test when has AKP structure.

Assumption RT: The test of (2.3) has asymptotic size bounded by the nominal size for the parameter space .

We now define a new test that, roughly speaking, coincides with or depending on whether the data seems consistent or not with AKP structures. We now provide the details.

Consider a given sequence of constants such that

| (3.1) |

e.g. or for some constant and define

| (3.2) |

where the minimum (here and in analogous expressions below) is taken over for being pd, symmetric matrices, normalized such that the upper left element of equals 1.999The expression is pre- and postmultiplied by for invariance reasons. The quantity measures how far from KP structure the covariance matrix in (2.10) when is. To show that the new test defined below has asymptotic significance level , it is sufficient (as proven in the Appendix) to consider two types of drifting sequences of DGPs in and to establish that the test has limiting NRP bounded by the nominal size in each case. The first type of sequences are those for which

| (3.3) |

that is sequences where the covariance matrix is ”far away” from KP structure. We assume that there is a model selection (MS) method such that when is ”far from” KP structure it will choose the robust test wpa1. The next assumption makes that statement more precise. To properly formulate the assumption we require terminology that is provided in the Appendix because it requires a lot of space. In particular, we need to consider particular sequences of drifting parameters (defined in (A.21) in the Appendix) where denotes a subsequence of .

Assumption MS: The model selection method satisfies wpa1 under parameter sequences (with underlying parameter space with .

By definition, along and thus when the sequence is not local to KP structure.

Definition of the fully robust test: Let The new suggested test of nominal size of the null hypothesis (2.3) is defined as

| (3.4) |

We typically write rather than to simplify notation. Ideally, can be chosen in this construction. To verify Assumption RP below using the AR/AR test as we need to have (Potentially, Assumption RP may hold with but our current proof technique does not allow verifying it).

By Assumption MS, wpa1 in case (3.3). Thus, by Assumption RT, the new test has limiting NRP bounded by of the test in that case.

For the model selection methods introduced below, the sequence of constants reflects a trade-off between size and power. Large values of will imply frequent use of which should translate into good power properties. On the other hand, use of could distort the NRPs in finite samples if the test is used in a scenario where the covariance matrix does not have AKP structure. Below we make a recommendation regarding the choice of based on comprehensive Monte Carlo studies. Note that can also depend on observed nonrandom quantities such as e.g. and but for the sake of notational simplicity we do not make that explicit.

To guarantee correct asymptotic significance level of the test and to rule out any potential pretesting issue, we have to implement the test at a nominal size infinitesimally smaller than For example, we can pick which should not make any practical difference in terms of power relative to using the test with

In addition, we have to impose one additional assumption regarding the relative NRPs (Assumption RP below) of the robust test and under sequences with AKP structure in order to make sure that has limiting NRP bounded by More precisely, consider a sequence of DGPs in such that

| (3.5) |

Using one can then show that and the sequences are of AKP structure. Therefore, under such sequences the test has limiting NRP bounded by . The notation denotes probability of an event when the true DGP is characterized by . By definition, along and thus when the sequence is local to KP structure.

Assumption RP: Under sequences of DGPs in for subsequences for which satisfies

Assumption RP says that under null sequences local to KP structure the robust test has critical region that is contained in the critical region of with probability going to one. Even when this does not need to imply that the two tests are asymptotically identical because the robust test may have limiting NRP strictly smaller than and may be more conservative than Under Assumption RP one can show that in case (3.5) (i.e. under drifting sequences of DGPs with finite has limiting NRP bounded by the nominal size of the test (because from the proof of Theorem 1 the test has limiting NRP bounded by ; and the limiting NRP of the new test is then bounded by by the assumption that has asymptotic size bounded by .)

From the above, it then follows quite straightforwardly, that the asymptotic size of is bounded by the nominal size for the parameter space . Also, the new test is at most as nonsimilar asymptotically as which translates into favorable power properties of the new test.

Theorem 2

Comments. 1. If is continuous in at then as the new test is asymptotically not more nonsimilar (i.e. less conservative) than , i.e.

| (3.6) |

See the proof of Theorem 2 for a proof. Property (3.6) should translate into improved power of relative to

2. The restriction to and in the formulation of Theorem 2 is an artifact of Theorem 1 where the conditional subvector test was shown to have correct asymptotic size for these cases only. The same is true for other theorems formulated below.

In the next subsection we specifically use the AR/AR subvector procedure due to Andrews (2017) as

3.1 Model selection methods

In this subsection we discuss two methods that can be used for as model selection procedures. The first one is akin to the moment selection method in Andrews and Soares (2010) to check which moment inequalities are binding in a model defined by moment inequalities. The second one is based on the test for KP structure introduced in GKM22.

Method 1: Define

| (3.7) |

with and defined in (2.13), to evaluate how far the true model is away from KP structure. Define the first choice for model selection as

| (3.8) |

Recall the definition of given in Assumption PS. Here we take

| (3.9) |

It is easy to show using the formulae in (2.29) and the analogous one for , orthogonality of , and using the fact that the Frobenius norm is invariant to orthogonal transformations, that is invariant to nonsingular transformations of the instrument vector. Crucial for this result is again that in (2.11) in the definition of (and as a result in the definition of and in (2.13)) is implemented with the transformed instrument vector (rather than with ).

Method 2: Define

| (3.10) |

where is the test statistic introduced in GKM22 to test the null of a KP structure of 101010The test statistic is defined in (19) and (22) in GKM20 and not reproduced here for brevity. In their notation our is compare the formula below (7) in GKM20 to our (2.11). To employ this method, we need to strengthen the moment restrictions in to for see Theorem 3 in GKM22.

3.2 Choice for The AR/AR test in Andrews (2017)

In this subsection we define one particular version of the various weak IVs and heteroskedasticity robust subvector tests suggested in Andrews (2017), namely the so-called AR/AR test and verify that it satisfies Assumptions RT and RP from the previous subsection. We define it for nominal size

To do so, we use the following quantities. For let111111To simplify notation we write here and in other situations, rather than the more correct

| (3.11) |

Define

| (3.12) |

The heteroskedasticity-robust AR statistic for testing hypotheses involving the full parameter vector , evaluated at is defined as

| (3.13) |

For denote by the -th column of Next, as in Andrews (2017, (7.9)-(7.10)) let

| (3.14) |

where is a -AR statistic, obtained as a quadratic form in the moment conditions projected onto the space orthogonal to the orthogonalized Jacobian with respect to . The random perturbation (with a random matrix of independent standard normal random variables that are independent of all other statistics considered) in the last line of (3.14) is introduced in Andrews (2017, p.23), to guarantee that the space projected on has rank a.s. Here is a tiny positive constant.

Let . The AR/AR test at nominal size is defined as follows.

-

1.

Fix an As in Andrews (2017, (7.1)) define

(3.15) where for

(3.16) is the so-called “estimator set”, see Andrews (2017, p.1 and (7.3)). If is invertible (which would happen wpa1 under the assumption (not imposed here) that is full column rank) then the first condition in has the unique solution and therefore (Note that along certain sequences for which it follows that and therefore if the function only has one local extremum it must be a global minimum.)

-

2.

For defined below (and depending on and , in (2.3) is rejected if

The second step size is chosen as

| (3.18) |

for some positive number , e.g., and see Andrews (2017, (7.8) and p.34)121212Andrews (2017, (7.8)) allows for more involved definitions of We choose the version that takes in the notation of Andrews (2017) that is also used in the Monte Carlos in Andrews (2017). Regarding the definition of note that it constitutes a slight modification compared with the definitions in Andrews (2017, (7.5)). In particular, the modification in the definition of is necessary to make the procedure invariant to nonsingular transformations of the instrument vector. We thank Donald Andrews for suggesting this updated version of his test statistic., where

| (3.19) |

see Andrews (2017, (7.4)-(7.5)), where denotes the -th component of .

Coming back to the statistic given in (2.25) note that

| (3.20) |

using the fact that the minimal eigenvalue of any symmetric square matrix is obtained as Furthermore,

| (3.21) |

and defined in (2.23).

Let be an element in We impose a mild technical condition below, namely that

| (3.22) |

and under sequences in (defined in (3.24) below) that are of AKP structure, i.e. under sequences for which .

Condition (3.22) has been established for several closely related estimators. E.g. holds under weak IV sequences (for some fixed matrix and homoskedasticity when is the LIML estimator, see Staiger and Stock (1997, Theorem 1). Results in Hahn and Kuersteiner (2002, Theorem 1) imply (3.22) for the 2SLS estimator under a setup where for Stock and Wright (2000, Theorem 1(ii)) and Guggenberger and Smith (2005, Theorem 2) implies (3.22) for the CU estimator under mixed weak/strong IV asymptotics for a fixed full rank matrix with (using high level assumptions, such as Assumptions B and D in Stock and Wright (2000)) and possible CHET.

Stock and Wright (2000, Theorem 1(ii)) can also be applied in the current situation to show (3.22) under sequences for which Given we need to show that for some compact set with probability at least for all large enough sample sizes. Assuming then for all is contained in a compact set with probability at least for all large enough sample sizes. Consider the estimator that is defined as a minimizer of in over Thus and are numerically identical for all sample sizes large enough with probability at least Note that has the same structure as the criterion function in (2.2) in Stock and Wright (2000) with playing the role of the weighting matrix and playing the role of . Therefore, under drifting sequences of mixed weak/strong IVs, namely the limiting distribution of is given in Stock and Wright (2000, Theorem 1(ii)) if Assumptions B and D in Stock and Wright (2000) hold for parameter space for and has a unique minimum. Stock and Wright (2000, Theorem 1(ii)) states that those components of that correspond to the columns of in are and those that correspond to the columns of in are which establishes .

Assumption B in Stock and Wright (2000) holds for (in fact, Assumption B’ in Stock and Wright (2000), which is sufficient for Assumption B, holds by linearity of the moment conditions in and compactness of To establish Assumption D note that under sequences and (note that the right hand side limits exist by definition of Therefore, under sequences

| (3.23) |

uniformly over (noting that , and with the limit matrix being nonrandom, continuous, symmetric, and pd for all Thus, by Stock and Wright (2000, Theorem 1(ii)), if has a unique minimum in and it follows that Thus there exists a compact set such that at least with probability for all large enough. Because and coincide at least with probability for all large enough sample sizes, it then follows that at least with probability for all large enough.

Deriving (3.22) under all possible drifting sequences is technically tedious and involves e.g. also consideration of so-called sequences of non-standard weak identification, see Andrews and Guggenberger (2019, AG from now on) for more discussion. If (3.22) is not already implied by the restrictions in the parameter space below then the asymptotic size results should simply be interpreted for sequences of parameter spaces that impose additional restrictions on such that (3.22) holds.

The null parameter space is restricted by the conditions in of Andrews (2017, (8.8)) and some weak additional ones, namely,

| (3.24) |

for constants and and a bounded set such that for some we have where denotes the null nuisance parameter space for and denotes the union of closed balls in with radius centered at points in

3.3 Main result

We obtain the following corollary of Lemma 1, Theorem 2, and the verification of Assumption MS in subsection 3.1 for the two model selection methods suggested there.

Define the parameter space as the intersection of the parameter spaces defined in 3.9 and 3.24 when the method in (3.8) is used as (and a slightly more restricted parameter space when (3.10) is used, as explained below (3.10).)

Corollary 3

Assume the same condition as in Lemma 1. Then the test defined in 3.4 with and satisfying the conditions in 3.1 implemented with the AR/AR test of Andrews (2017) playing the role of and either of the two model selection methods described above used for has asymptotic size bounded by the nominal size for the parameter space defined in the paragraph above for and

Comment. Note that under the null hypothesis the test does not depend on the value of the reduced form matrix

4 Monte Carlo study

In this section we investigate the finite sample performance in model (2.1) of the suggested new test defined in (3.4) and juxtapose it to the performance of alternative methods suggested in the extant literature, namely the two-step tests AR/AR, AR/LM, and AR/QLR1 in Andrews (2017). For the implementation of we use both methods considered in Section 3.1 and call the resulting tests MS-AKP1 and MS-AKP2 for the remainder of this section. We also simulate the performance of the test ARAKP,α (which is of course size distorted in the setups with CHET that are outside of KP structure).

All results below are for nominal size Unless otherwise stated, we take We consider the case and and pick and test the null hypothesis in (2.3) with

Choice of tuning parameters

The implementation of the various tests depends on a large number of user chosen constants. In particular, to implement the AR/AR, AR/LM, and the AR/QLR1 tests we pick as already mentioned above after (3.18). To calculate the estimator set we employ the closed form solution provided below (3.16). We choose and pick the elements of the random matrix as i.i.d. independent of all other variables considered, see the last line of (3.14).131313Note that by choosing the tests are no longer invariant to nonsingular transformations of the IV vector. However, for small the differences after a transformation are usually very small. The confidence interval (or region) for that appears in (3.15) is obtained by grid search over an interval (or rectangle) of length 20 centered at the true value of with 100 equally spaced gridpoints.141414When the dimension of grows then the implementation of that step by grid search will cause an exponential increase in computation time for each of the two-step methods. To implement the AR/QLR1 test, as in Andrews (2017) we pick and . We refer to Table II in Andrews (2017) that provides the results of a comprehensive sensitivity analysis on most of the user chosen constants above. To calculate the data-dependent critical values for the AR/QLR1 test we use 10,000 i.i.d chi-square random variables. There was no noticeable difference between and for given in (3.4); therefore, for the sake of computational simplicity, we pick the former in the simulations. Finally, has to be chosen, which we do in the next subsection.

Recommended choices for

First, we perform a large number of simulations in order to determine recommendations for the sequence of constants satisfying (3.1). We make recommendations for as a function of the number of IVs and the subvector dimension and consider choices from and .

For each , sample size and with

| (4.1) |

with corresponding to “very weak”, “weak”, and “strong” identification of and, relevant for the power results below, with and equal to when is even and equal to when we randomly generate different DGPs (that is a choice for the covariance matrix) as described below and simulate the NRPs (using i.i.d samples of each given DGPs) of MS-AKP1 and MS-AKP2 for choices of given as

| (4.2) |

with taken from the set

In finite sample simulations for the DGPs considered here, the AR/AR test sometimes slightly overrejects. For example, under CHOM, strong IVs, and covariance matrix being chosen as below (4.8), where i.i.d. the AR/AR test has NRP equal to 5.4%. From our theory we also know that the test ARAKP,α (at least under AKP structures) has nonsmaller NRP than the AR/AR test. Define as the ”simulated size of a test when there are IVs” the highest empirical NRP of the test over all choices of , , and () random DGPs considered. For each of the two methods MS-AKP1 and MS-AKP2 and for each our recommendation for then is to take the largest in such that the simulated size does not exceed 6% (that is, we allow for a distortion of 1% in the ”simulated size”). It turns out that in our simulations this criterion for always leads to well defined choice of (when a priori it could be that even for the smallest/largest choice of in the simulated size exceeds/is still below 6%).

To generate random DGPs we consider the following mechanism. Given all tests considered above, including AR have correct asymptotic size under AKP structure we focus attention on designs with conditional heteroskedasticity that are not of AKP structure. In particular, we choose

| (4.3) |

with i.i.d. and independent of i.i.d. for . Each of the 1,000 random DGPs is determined by choosing and where has diagonal elements equal to 1. The scalars and the components of are obtained by i.i.d. draws from a and the off-diagonal ones of are obtained by i.i.d. draws from a (subject to the restriction that the resulting matrix is pd). Note that the setup in (4.3) nests KP structure when e.g. and CHOM when e.g.

For each the binding constraint on always came from the combination and “strong” identification, while for the “very weakly” identified scenario even the largest choice of typically did not yield overrejection for any of the sample sizes considered. Based on the above setup we recommend the following choices for For Method 1 in Section 3.1, MS-AKP1, that is for based on the distance in Frobenius norm statistic, we suggest

| (4.4) |

while for Method 2, MS-AKP2, that is for based on the KPST statistic in GKM22, we suggest

| (4.5) |

Recall that with these choices of and chosen as in (4.2) the tests and MS-AKP1 and MS-AKP2 have correct asymptotic size for a parameter space with arbitrary forms of conditional heteroskedasticity.

Next we consider We take . As pointed out above already, the computational effort in the above exercise increases exponentially in the dimension of if we use the same number of gridpoints in each dimension in the calculation of the confidence interval for that appears in (3.15). Therefore, we use a grid of a product of two intervals of length 20 centered at the true value of with only 50 equally spaced gridpoints in each dimension (rather than 100 in the case .) Everything else is the same, mutatis mutandis (e.g. is now a 4x4 matrix), as described in the case except that is taken as with and that the search set for is increased to .

For Method 1 in Section 3.1, MS-AKP1 we suggest

| (4.6) |

while for Method 2, MS-AKP2 we suggest

| (4.7) |

Just like in the case the highest null rejection probabilities occur in the strongly identified case.

Size results

All results below are for the case where Under a setup with CHET outside of KP, the tests MS-AKP1 and MS-AKP2 equal the AR/AR test wpa1. We therefore first consider the KP setup in Andrews (2017) in Section 9.1 which is obtained from (4.3) with and . We also consider the setup with CHOM obtained from (4.3) with and Then, finally, below we also examine how power is affected as the DGP transitions from CHOM to CHET outside of KP.

In both cases of CHET and CHOM, we take the matrix

| (4.8) |

to have diagonal elements equal to one, and the (1,2) and (1,3) elements equal to .8 and the (2,3) element equal to .3, as in Andrews (2017). We consider in (4.1), again, representing ”very weak”, ”weak”, and ”strong” IVs, also see Andrews (2017). Finally, we take and sample sizes Altogether, that makes for 36 different specifications. In addition, we also obtain results for certain cases of mixed identification strength, e.g. when and also some results for larger sample sizes.

As reported in Andrews (2017), we also find that in an overall sense the AR/AR and AR/LM tests are dominated by the AR/QLR1 test. For instance, regarding the AR/LM test, its power function (even in the strong IV context under CHOM) is not always U-shaped and suffers from power dips against certain alternatives. For example, for the KP setup for with weak IVs, the power of the AR/LM and AR/QLR1 tests when are 8.6% and 75.6%, respectively, while in the setup with CHOM when the power of the AR/LM test is 34.9% while all the other tests have power equal to 100%. On the other hand, the AR/AR test fares worse than the AR/QLR1 test in strongly identified overidentified situations. In what follows, we do not therefore discuss the AR/LM test in much detail.

We consider rejection probabilities under the null and (for power) under a grid of seven values on each side of 0 with distances from the hypothesized value 0 chosen depending on the strength of identification. For example, in the very weakly, weakly, and strongly identified cases we take in the interval , and , respectively, around the true value of 0. Results are obtained from i.i.d samples from each DGP.

First, we discuss the NRPs. Over the 18 DGPs of the KP setups, the NRPs of MS-AKP1, MS-AKP2, AR/AR, AR/LM, and AR/QLR1 lie in the intervals (all numbers in %): [3.5,5.9], [3.3,6.0], [1.9,5.1], [.6,5.2], and [1.5,4.9]. As set up above, the tests MS-AKP1 and MS-AKP2 slightly overreject the null for small sample sizes (especially in the strongly identified case), but the size distortion disappears as grows. For example, the NRPs of MS-AKP2 in the KP setup with and strong identification is 6.0, 5.5, 5.2, and 5.1%, respectively, when and On the other hand, the tests AR/AR, AR/LM, and AR/QLR1, while controlling the NRP very well, underreject the null in weakly identified scenarios. This leads to relatively poor power properties relative to the tests MS-AKP1 and MS-AKP2 in weakly identified situations.

Regarding the 18 DGPs with CHOM, the one important difference relative to the KP setup is that the three tests AR/AR, AR/LM, and AR/QLR1 are less conservative with NRPs over the 18 DGPs in the intervals [4.1,5.4], [3.5,5.4], and [3.7,5.1], respectively. As a consequence, these tests have relatively better power properties than in the KP setup.

Power results

Next we discuss the power results. We focus again on the case where Power for MS-AKP1, MS-AKP2, AR/AR, and AR/QLR1 increases as the IVs become stronger. On the other hand, by the local-to-zero design considered here (see (4.1) and below), as increases, power for these three tests changes only slightly. We therefore only provide details for the case where . Power of all the tests is much higher in the setting with CHOM compared to the KP setting and especially so for the AR/QLR1 test (because it underrejects the null hypothesis less under CHOM than under KP). As one example, consider the case with weak identification. In that case, when the tests MS-AKP2, AR/AR, and AR/QLR1 have power 48.7, 46.3, and 45.4% under KP, but power equal to 95.9, 95.6, and 95.4% under CHOM!

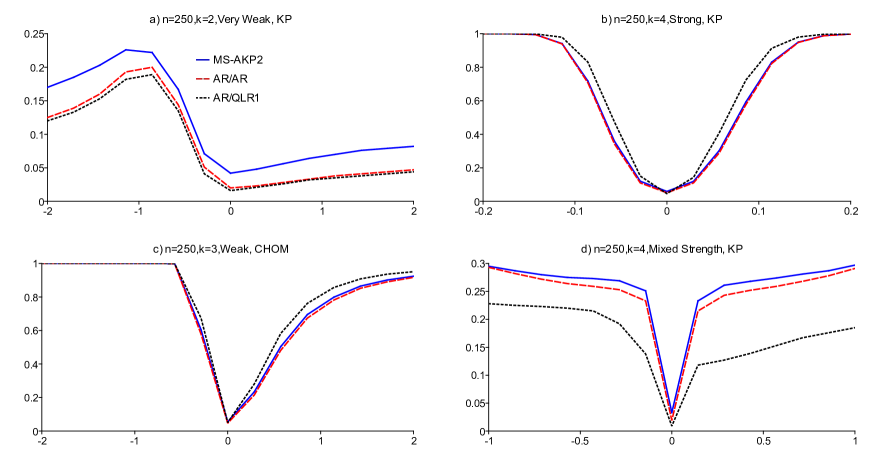

A representative selection of power curves in four different cases is plotted in Figure 1. Note that in the figures corresponding to the different cases, both the scale of the horizontal and the vertical axes vary by a lot depending on the strength of identification.

The key takeaways from the power study are as follows:

i) Based on the DGPs considered here we cannot make a clear recommendation as to which one of the two tests MS-AKP1 and MS-AKP2 is preferable. In most cases, they have virtually identical power. In few cases, one dominates the other, but only by a small difference. In the Figures below we only report results for MS-AKP2.

ii) Regarding the comparison between the tests MS-AKP1, MS-AKP2 and AR/AR we find that the former two virtually uniformly dominate the latter in all the designs considered. This is not surprising given the construction of the new tests and given they satisfy Assumption RP above. The relative power advantage of the tests MS-AKP1, MS-AKP2 over AR/AR partly stems from the underrejection of the latter test under the null. See e.g. Figure 1a that contains power curves for very weak identification, and KP structure for MS-AKP2, AR/AR, and AR/QLR1. (The NRPs of the three tests reported here are 4.2, 2.0, and 1.6%, respectively. Note that the x-axis in Figures I-IV plots the true value )

iii) Regarding the comparison between the tests MS-AKP1, MS-AKP2 and AR/QLR1 in the case of equal identification strength we find that the former two are generally more powerful under weak identification and small while the reverse is true under strong identification and larger see Figures 1a and b for the cases “ and very weak identification” and “ and strong identification,” respectively, both for and KP. (In Figure 1b, the NRPs of the tests MS-AKP2, AR/AR, and AR/QLR1 are 5.9, 5.1, and 4.6%, respectively.) These two figures show the best relative performances for the MS-AKP1, MS-AKP2 and AR/QLR1 tests in the “equal identification” settings where . In Figure 1a the power advantage of MS-AKP2 over AR/QLR1 is as high as 5.2%, while in Figure 1b the power of AR/QLR1 can be up to 13.1% more powerful than MS-AKP2.

In the “intermediate” case between these extremes, namely “ and weak identification” (again with and KP; not reported in Figure 1), the MS-AKP1 and MS-AKP2 tests have slightly higher power than AR/QLR1 when is positive while the reverse is true for negative values of . In all cases, the relative performance of the AR/QLR1 test improves under CHOM; under CHOM, for the “intermediate” case “ and weak identification” (again with ) the AR/QLR1 test has uniformly higher power than the MS-AKP1 and MS-AKP2 tests, see Figure 1c. (In Figure 1c, the NRPs of the tests MS-AKP2, AR/AR, and AR/QLR1 are 5.5, 4.7, and 5.1%, respectively.)

In cases of mixed identification strength, we find that when and the tests MS-AKP1 and MS-AKP2 have uniformly higher power than AR/QLR1 for all considered whereas in the case and all tests have comparable power. See Figure 1d that contains the case and with KP structure where the power gap between the new tests and AR/QLR1 is as high as 13.4%. (In Figure 1d, the NRPs of the tests MS-AKP2, AR/AR, and AR/QLR1 are 3.3, 1.9, and 0.9%, respectively.) It seems that in these cases of mixed identification strength the new tests enjoy their most competitive relative performance.

Results for non-KP DGPs

Finally, we examine how rejection probabilities are affected as the DGP transitions from KP to CHET outside of KP. To do so, we report rejection probabilities under the null and certain alternatives and probabilities with which MS-AKP1 and MS-AKP2 equals the AR/AR test in the second stage for a class of DGPs that under KP coincide with the ones considered in Figure 1b ( and Figure 1d (. In particular, we choose and the matrix equals the one in (4.8). In (4.3) we take

| (4.9) |

for and Note that for the design leads to KP while for it leads to CHET outside of KP. In particular, (with defined in (2.4) with equals , and when respectively. The latter numbers are found by simulations based on simulation repetitions using Theorem 1 in GKM22.

As before, we report results for simulation repetitions at nominal size .

Null rejection probabilities. Here we report results when that is, we report NRPs.

First, in the setup of Figure 1b the probability with which MS-AKP1 and MS-AKP2 coincide with AR/AR is strictly increasing in and e.g. equals 66.2% and 64.9%, 82.9% and 85.1%, and 98.8% and 99.5%, respectively for and , respectively. (We also simulated these probabilities when for and they equal 20.8% and 20.2%, respectively). The highest NRP of both the MS-AKP1 and MS-AKP2 tests is 5.9% which occurs when and is caused by a 7.4% NRP of the conditional subvector test ARAKP,α (even though by Theorem 1 this test has correct asymptotic NRP for this DGP; interestingly, this test has NRP equal to 5.8% when a case that is not covered by Theorem 1). Given the MS-AKP1 and MS-AKP2 tests equal the AR/AR test with increasing probability as increases, their NRPs get closer (but not monotonically so) to 5% as increases. As both tests have NRP equal to 5.2%.

Second, in the setup of Figure 1d the probability with which MS-AKP1 and MS-AKP2 coincide with AR/AR are identical as just reported for the setup in Figure 1b. The highest NRPs of the MS-AKP1 and MS-AKP2 tests are 3.5% and 3.2% respectively, which occur when . The AR/AR and AR/QLR1 tests have NRPs in the intervals [1.2%,1.9%] and [.3%,.8%], respectively, and therefore, quite substantially underreject the null hypothesis. As the MS-AKP1 and MS-AKP2 tests equal the AR/AR test with increasing probability as increases, their NRPs approach 1.2% as gets closer to

Power results. Here we examine how power is affected as the DGP transitions from KP to CHET outside of KP.

First, in the setup of Figure 1b) we consider the alternative The probabilities with which MS-AKP1 and MS-AKP2 coincide with AR/AR are increasing in and are very similar to the corresponding values when e.g. the probabilities equal 68.6% and 68.9% when , respectively, and equal 98.2% and 99.1% when Power for all tests monotonically decreases as increases, e.g. for AR/QLR1, AR/AR, and MS-AKP1 from 83.5% to 44.4%, from 71.5% to 32.4% and from 72.5% to 32.4%, respectively, when goes from 0 to .1.

Second, in the setup of Figure 1d) we consider the alternative When MS-AKP1 and MS-AKP2 coincide with AR/AR with probability 78.3% and 75.5%, respectively and for both MS-AKP1 and MS-AKP2 coincide with AR/AR at least 99.6% of the cases. The power of the AR/AR and the AR/QLR1 for all values of are in the intervals [27.9%,29.4%] and [21.2%,23.5%], respectively, with neither test’s power being monotonic in While the power of MS-AKP1 and MS-AKP2 slightly exceeds the power of the AR/AR test for their power is identical to the one of the AR/AR test for larger values of

In sum, as one would expect given the construction of MS-AKP1 and MS-AKP2 tests, when moving from KP to CHET outside of KP, their rejection probabilities get closer and closer to those of the AR/AR test.

5 Conclusion

We propose the construction of a robust test that improves the power of another robust test by combining it with a powerful test that is only robust for a subset of the parameter space. We implement this construction in the context of the linear IV model applied to the ARAKP,α test that has correct asymptotic size for a parameter space that imposes AKP structure and the AR/AR test that is robust even when allowing for arbitrary forms of CHET. We believe that the particular construction and implementation suggested here, namely combining a powerful but non fully robust test with a less powerful fully robust test in order to obtain a fully robust more powerful test, might be successfully applied in other scenarios and also in the current scenario based on different choices of testing procedures. For instance, it might be feasible to combine the LR type subvector test of Kleibergen (2021) with the AR/QLR1 of Andrews (2017) but it would be technically substantially more challenging to verify the assumptions given above that are sufficient for control of the asymptotic size of the resulting test. Other extensions include improving the power of the ARAKP,α test by making the conditional critical value depend on more than just the largest eigenvalue.

Appendix A Appendix

The Appendix is structured as follows. In Section A.1 the proof of Theorem 1 is given, prepared for first with several technical lemmas in Subsection A.1.1. Next in Section A.2 the proof of Theorem 2 is given. We provide verifications of the high level assumptions for particular implementations of the test including for both and AR/AR in Sections A.3 and A.4, respectively. Finally, in Section A.5, we generalize the conditional subvector test to a time series framework.

A.1 Proof of Theorem 1

A.1.1 Technical lemmas

In what follows below we will require results about solutions to certain minimization problems involving the Frobenius norm. The next lemma provides a special case of Corollary 2.2 in van Loan and Pitsianis (1993). Note that van Loan and Pitsianis (1993) point to Golub and van Loan (1989, p.73) for a proof of Corollary 2.2. However, the result in Golub and van Loan (1989, p.73) is for a minimization problem using the -norm for and not the Frobenius norm which is used here.

Lemma 2

Consider the minimization problem

for a given nonzero matrix with singular value decomposition for singular values with and rectangular , orthogonal matrices and Then a minimizing argument is given by and the minimum equals If then is the unique minimizer.

Proof of Lemma 2. Note that

| (A.1) |

by viewing and because for any matrix and conformable orthogonal matrices and We can write any matrix with as

| (A.2) |

for and for Because where denotes the Frobenius inner product, and for we have

| (A.3) |

Viewing (A.3) as a function in and taking first order conditions (FOCs) with respect to we obtain or

| (A.4) |

Taking FOCs with respect to we obtain and thus

| (A.5) |

and for we have and therefore

| (A.6) |

The objective is to find such that the two summands in (A.3) that depend on are being minimized. Using (A.4) we thus need to find such that

| (A.7) |

is minimized. Let be the largest index for which Given that for it follows that a vector is a minimizing argument if and only if and and the minimum in (A.3) equals

| (A.8) |

For example, one solution is for which the minimizing matrix in (A.1) becomes Correspondingly, a minimizing matrix becomes

If then Therefore, any minimizing equals for some and therefore, by (A.2) and (A.4), the only minimizing matrix equals And consequently, there can only be a unique minimizer

Let and be a singular value decomposition of where has singular values of on the diagonal and zeros elsewhere, is an orthogonal matrix of eigenvectors of and is an orthogonal matrix of eigenvectors of In general, and are not uniquely defined. The matrix is uniquely determined by the restriction that the singular values are ordered nonincreasingly. We assume that this is the case from now on. Let be the geometric multiplicity of the largest eigenvalue of Write for Thus denotes an orthogonal basis for the eigenspace associated with the largest eigenvalue of .

Lemma 3

Let and for be matrices such that as . Let and be any singular value decompositions of and respectively, where the singular values are ordered nonincreasingly. For , denote by and the -th column of and respectively. Decompose where is an orthogonal basis for the eigenspace associated with the largest eigenvalue of Conformingly, let 151515But note that does not necessarily correspond to a basis for the eigenspace of the largest eigenvalue of but may represent eigenvectors corresponding to several different eigenvalues because the multiplicities of eigenvalues of and may not be the same. As a trivial example, consider and equal to a diagonal matrix with first and second diagonal elements equal to and , respectively. Assume does not equal the zero matrix. Then for and .

Proof of Lemma 3. Wlog we can assume (If add rows of zeros to the bottom of and Then the result for

for any orthogonal matrix implies the desired result for ) Denote by the -th singular value of (i.e. equals the -th element of ) for and likewise denotes the -th singular value of By definition (and given that the algebraic and geometric multiplicities coincide for any diagonalizable matrix), is the largest index for which . Define

| (A.9) |

Then by Wedin’s (1972) theorem (see, e.g. Li (1998) equations (4.4) and (4.8)161616A comprehensive reference for background reading on Wedin’s (1972) theorem is Stewart and Sun (1990, p.260, Theorem 4.1).), it follows that

| (A.10) |

where denotes the angle matrix between and (see Li (1998), equation (2.3) for a definition). Furthermore, by Lemma 2.1 and equation (2.4) in Li (1998), we have

| (A.11) |

Note that is bounded away from zero for all large because (1) by the assumption that (2) if by construction and therefore is uniformly bounded away from zero (because singular values are continuous as functions of the matrix elements and , and (3) if then because we take a minimum of the empty set. Therefore, by (A.10) and (A.11) we have

| (A.12) |

which implies that for and

A.1.2 Uniformity Reparametrization

To prove that the new conditional subvector ARAKP test has asymptotic size bounded by the nominal size we use a general result in Andrews, Cheng, and Guggenberger (2020, ACG from now on). To describe it, consider a sequence of arbitrary tests of a certain null hypothesis and denote by the NRP of when the DGP is pinned down by the parameter vector where denotes the parameter space of By definition, the asymptotic size of is defined as

| (A.13) |

Let be a sequence of functions on where with Define

| (A.14) |

Assumption B in ACG: For any subsequence of and any sequence for which for some 171717By definition, the notation means that

The assumption states, in particular, that along certain drifting sequences of parameters indexed by a localization parameter the NRP of the test cannot asymptotically exceed a certain threshold indexed by

Proposition 4

ACG, Theorem 2.1a and Theorem 2.2 Suppose Assumption B in ACG holds. Then,

We next verify Assumption B in ACG for the conditional subvector ARAKP test and establish that when the test is implemented at nominal size . In the setup considered here, the parameter space actually depends on which does not affect the conclusion of Theorem 2.1(a) and Theorem 2.2 in ACG.

We use Proposition 16.5 in AG, to derive the joint limiting distribution of the eigenvalues in (2.25). We reparameterize the null distribution to a vector The vector is chosen such that for a subvector of convergence of a drifting subsequence of the subvector (after suitable renormalization) yields convergence of the NRP of the test. For given and any and such that as in (2.5) define

| (A.15) |

where again from (2.12). Denote by

| (A.16) |

ordered so that the corresponding eigenvalues are nonincreasing. Denote by

| (A.17) |

The corresponding eigenvalues are Denote by

| (A.18) |

which are nonnegative, ordered so that is nonincreasing. (Some of these singular values may be zero.) As is well-known, the squares of the singular values of a matrix equal the largest eigenvalues of and In consequence, for In addition, for

Define the elements of to be191919For simplicity, as above, when writing (and likewise in similar expressions) we allow the elements to be scalars, vectors, matrices, and distributions. Note that is included so that Proposition 16.5 in AG can be applied.

| (A.19) |

Note that by (A.15) we have and In Section 3 the additional element defined in (3.2) is appended to with corresponding changes to several objects below, e.g. and in (A.20) and in (A.19) and (A.21); e.g. becomes

The parameter space for and the function (that appears in Assumption B in ACG) are defined by

| (A.20) |

We define and as in (A.19) and (A.20) because, as shown below, the asymptotic distributions of the test statistic and conditional critical values under a sequence for which depend on and for Note that we can view (for an appropriately chosen finite ).

For notational convenience, for any subsequence

| (A.21) |

It follows that the set defined in (A.14) is given as the set of all such that there exists for some subsequence

We decompose analogously to the decomposition of the first seven components of : where and have the same dimensions for We further decompose the vector as where the elements of could equal Again, by definition, under a sequence we have

| (A.22) |

Note that because where denotes the rank of a matrix

By Lyapunov-type WLLNs and CLTs, using the moment restrictions imposed in (2.5), we have under

| (A.27) | |||

| (A.28) |

where the random vector is defined here, denotes the distribution of under and, by definition above, and denote the limits of and under

Let be such that

| (A.29) |

where for by (A.22) and the distributions correspond to defined in (A.21). This value exists because are nonincreasing in (since are nonincreasing in as defined in (A.18)). Note that is the number of singular values of that diverge to infinity when multiplied by Note again that because

A.1.3 Asymptotic Distributions

One might wonder whether the definition of in 2.23 as where are minimizers in (2.13) is unique. If for instance the eigenspace corresponding to the largest eigenvalue was of dimension bigger than one, then clearly would not be uniquely defined. The following lemma shows that the definition of is unique and derives its limit.

To simplify notation a bit, we write shorthand for and likewise for other expressions.

Lemma 4

Comment. Note that under sequences and do exist. On the other hand, the matrices and may not be uniquely pinned down by the restrictions in (2.5) in . The results and a.s. hold for any possible choice of and

Proof of Lemma 4. Recall the definition

| (A.30) |

in (2.10). By Theorem 1 in van Loan and Pitsianis (1993),

| (A.31) |

for any conformable matrices and Thus, for

| (A.32) |

it follows that and because and in it follows that has rank 1. It follows also that (which exists under sequences ) has rank 1 (even though the rank of could be larger than 1 for every ). By continuity of the singular values and because the geometric and algebraic multiplicity coincide for diagonalizable matrices, the dimension of the eigenspace of corresponding to the largest singular value of is one for all large enough.

By the uniform moment restrictions in (2.5) in namely for and a strong law of large numbers implies that

| (A.33) |

Therefore, the dimension of the eigenspace of corresponding to the largest singular value of is one for all large enough wp1.

By the uniqueness statement of Lemma 2 for the rank 1 case, it follows that the formula for minimizers of the KP approximation problem in (2.13) given in van Loan and Pitsianis (1993, Corollary 2 and Theorem 11), namely

| (A.34) |

yields symmetric pd matrices and When applying Theorem 11, note that for all large enough wp1, which holds by (A.33), and because and in . Given that Sylvester’s criterion for positive definiteness implies that for all large enough wp1, and we can therefore define and as in 2.23 with normalization to 1 of the upper left element of for all large enough wp1.

Next we apply Lemma 3 with and the roles of and in Lemma 3 played by and , respectively. By (A.33), the lemma implies

| (A.35) |

wp1. for , where denotes the -th column of in the singular value decomposition of and denotes the first column of in the singular value decomposition of For any orthogonal basis of and we have In particular, we have wp1., where the second equality holds by (A.35). Together with the normalization of the upper left elements of and to 1, this implies a.s. and a.s. follows analogously.

An analogue to Lemma 16.4 in AG and Lemma 1 in GKM19 is given by the following statement. Define

| (A.36) |

Denote by the inverse operation that transforms a vector into a matrix.

Lemma 5

Proof of Lemma 5. We have

| (A.37) |

where the first equality uses the definition of in (A.36), the second equality uses the formulas in (2.1), and the convergence results holds by the (triangular array) CLT and WLLN in (A.28). The remaining statement holds by the WLLN in (A.28) and the consistency of for proven above.

For notational convenience, write

| (A.38) |

Note that the matrix equals which appears in (2.25). Thus, for equals the th eigenvalue of ordered nonincreasingly, and is the subvector ARAKP test statistic. To describe the limiting distribution of we need additional notation, namely:

| (A.42) | ||||

| (A.43) |

where and .212121There is some abuse of notation here. For example, and denote different matrices even if equals Let and The same proof as the one of Lemma 16.4 in AG shows that under all sequences with . The following proposition is an analogue to Proposition 16.5 in AG and to Proposition 2 in GKM19.

Proposition 5

Under all sequences with

a for all

b the ordered vector of the smallest eigenvalues of i.e., converges in distribution to the ordered vector of the eigenvalues of

c the convergence in parts (a) and (b) holds jointly with the convergence in Lemma 5, and

d under all subsequences and all sequences with the results in parts a-c hold with replaced with

Comments. 1. The proof of the proposition follows from the proof of Proposition 16.5 in AG. Note that Assumption WU in AG (assumed in their Proposition 16.5) is fulfilled with the roles of and in AG played here by and respectively, while the roles of and in AG are played by the identity function. The roles of and in AG are both played by and those of both and by . Lemma 5 then shows consistency and under sequences with and trivially the functions and are continuous in our case. Note that by the restrictions in in (2.5) the requirements in the parameter space in AG, namely “ and are uniformly bounded away from zero and and are uniformly bounded away from infinity”, are fulfilled. For example, the former follows because and is uniformly bounded.

2. Proposition 5 yields the desired joint limiting distribution of the eigenvalues in (2.25). Using repeatedly the general formula for three conformable matrices we have for the expression that appears in

| (A.46) | |||

| (A.47) |

where, by definition, are i.i.d. normal -vectors with zero mean and covariance matrix and the distributional statement follows by straightforward calculations using (A.28). Therefore, by Lemma 5, the definition of in (A.43), and by noting that

| (A.48) |

we obtain

| (A.51) | ||||

| (A.54) |

where, by definition, are i.i.d. normal -vectors with zero mean and covariance matrix The distributional equivalence in the second line holds because where are i.i.d. as has orthogonal columns of length 1. Analogously, because has orthogonal columns of length 1.

For example, when (which could be called the ”strong IV” case), we obtain from (A.54) Therefore and thus by part (b) of Proposition 5 the limiting distribution of the subvector ARAKP test statistic is in that case, while all the larger roots in (2.25) converge in probability to infinity by part (a).

A.2 Proof of Theorem 2

Proof of Theorem 2. It is enough to verify Proposition 4 above for the parameter space and the test To verify Assumption B in ACG consider a sequence defined as in (A.19) and (A.21) above except that the component

| (A.55) |

is added to , where the minimum (here and in similar expressions below) is taken over for being pd, symmetric matrices, normalized such that the upper left element of equals 1. In (A.20), we replace by and define To simplify notation, we write instead of from now on.

Consider first a sequence with By Assumption MS, wpa1 and therefore, wpa1. Thus, the new test has limiting NRP bounded by in that case because has asymptotic size bounded by its nominal size by Assumption RT .

Second, consider a sequence with In that case, implies that By submultiplicativity of the Frobenius norm and being uniformly bounded in it then follows that That is, the covariance matrix has AKP structure. Therefore, also the covariance matrix has AKP structure. By the proof of Theorem 1 the test then has limiting NRP bounded by under sequences with . It therefore follows that

| (A.56) |

where the equality uses Assumption RP, which implies that and the last inequality follows from the fact that the limiting NRP of the test is bounded by

To prove Comment 1 below Theorem 2, note that by the assumed continuity,

| (A.57) |

But note that

| (A.58) |

where in the first equality is chosen such that in the second equality a subsequence of can be found, and in the third equality may denote a further subsequence along which is of type for some (We are allowing here for the possibility that may depend on the particular sequence rather than just ) If then wpa1 by Assumption MS and

| (A.59) |

On the other hand, if then by Assumption RP, wpa1 and

| (A.60) |

and the desired conclusion then follows as in (A.59).

A.3 Assumption MS for the model selection method

Here we verify Assumption MS for the two suggested methods for

Method 1, defined as To simplify notation we write again instead of and subscripts as Consider a sequence with Rewrite

| (A.61) |

In the proof of Lemma 4 we use the uniform moment restrictions in (2.5) in to obtain ; here the stronger uniform moment condition allows the application of a Lyapunov CLT and to establish that Because by assumption in we thus have . Furthermore,

| (A.62) |

where the inequality holds by the definition of in (3.2). Because and norms are continuous, it thus follows that wpa1.

Method 2: The desired result is obtained using Theorem 3 in GKM22.

A.4 Proofs of Results Involving the AR/AR test

Proof of Lemma 1. Assumption RT is satisfied by the AR/AR test by Theorem 8.1 in Andrews (2017) noting that the parameter space in Andrews (2017, (8.8)) contains the parameter space defined in (3.24). In particular, note that defined in (8.2) in Andrews (2017), equals in the linear IV model considered here and therefore the condition in (8.8) being bounded holds trivially. Also, Assumption W in Andrews (2017) holds with the choice considered here.

Assumption RP is verified by the following argument that uses Lemma 6 below. To simplify notation we write instead of Let be an element in

Consider first the case where defined in (3.15). Then, in particular, it must be that We obtain

| (A.63) |

where the equality follows from Lemma 6. But no matter what value takes on. Given and we have that wp1 for some Because it follows from that wpa1. In other words, the conditional subvector ARAKP test rejects wpa1.