queue in two alternating environments and its heavy traffic approximation

Abstract

We investigate an queue operating in two switching environments, where the switch is governed by a two-state time-homogeneous Markov chain. This model allows to describe a system that is subject to regular operating phases alternating with anomalous working phases or random repairing periods. We first obtain the steady-state distribution of the process in terms of a generalized mixture of two geometric distributions. In the special case when only one kind of switch is allowed, we analyze the transient distribution, and investigate the busy period problem. The analysis is also performed by means of a suitable heavy-traffic approximation which leads to a continuous random process. Its distribution satisfies a partial differential equation with randomly alternating infinitesimal moments. For the approximating process we determine the steady-state distribution, the transient distribution and a first-passage-time density.

Keywords:

Steady-state distribution, First-passage time, Diffusion approximation, Alternating Wiener process

Mathematics Subject Classification:

60K25, 60K37, 60J60, 60J70

1 Introduction

The queue is the most well-known queueing system, whose customers arrive according to a Poisson process, and the service times are exponentially distributed. Its generalizations are often employed to describe more complex systems, such as queues in the presence of catastrophes (see, for instance, Di Crescenzo et al. [15], Kim and Lee [28], and Krishna Kumar and Pavai Madheswari [29]). In some cases, the sequence of repeated catastrophes and successive repairs yields alternating operative phases (see, for instance, Paz and Yechiali [37] and Jiang et al. [25] for the analysis of queues in a multi-phase random environment). Moreover, realistic situations related to queueing services are often governed by state-dependent rates (cf., for instance, Giorno et al. [21]), or by alternating behavior, such as cyclic polling systems (cf. Avissar and Yechiali [3]). Specifically, the analysis of queueing systems characterized by alternating mechanisms has been object of investigation largely in the past. The first systematic contribution in this area was provided in Yechiali and Naor [39], where the queue was analyzed in the steady-state regime when the rates of arrival and service are subject to Poisson alternations. A recent study due Huang and Lee [26] is concerning a similar queueing model with a finite size queue and a service mechanism characterized by randomly alternating behavior.

Other types of complex systems in alternating environment are provided by two single server queues, where customers arrive in a single stream, and each arrival creates simultaneously the work demands to be served by the two servers. Instances of such two-queue polling models have been studied in Boxma et al. [7] and Eliazar et al. [19]. In other cases, instead, the alternating behavior of queueing systems is described by time-dependent arrival and service rates, such as in the queue subject to under-, over-, and critical loading. Heavy-traffic diffusion approximations or asymptotic expansions for such types of systems have been investigated in Di Crescenzo and Nobile [16], Giorno et al. [22], Mandelbaum and Massey [32].

Attention has been devoted in the literature also to queues with more complex random switching mechanisms, that arise naturally in the study of packet arrivals to a local switch (see, for instance, Burman and Smith [8]). Similar mechanisms have been studied recently also by Arunachalam et al. [2], Pang and Zhou [36], Liu and Yu [30] and Perel and Yechiali [38].

Contributions in the area of queues with randomly varying arrival and service rates are due to Neuts [35], Kao and Lin [27], and Lu and Serfozo [31]. Moreover, Boxma and Kurkova [5] studied an queue for which the speed of the server alternates between two constant values, according to different time distributions. A similar problem for the queue was studied by the same authors in [6], whereas the case of the queue is treated by D’Auria [10].

1.1 Motivations

Along the lines of the above mentioned investigations, in this paper we study an queue subject to alternating behavior. The basic model retrace the alternating queue studied in [39]. Indeed, we assume that the characteristics of the queue are fluctuating randomly in time, under two operating environments which alternate randomly. Initially the system starts under the first environment with probability , or from the second one w.p. . Then, at time the customers arrival rates and the service rates are if the operational environment is , for . The operational environment switches from to with rate , whereas the reverse switch occurs with rate . This setting allows to model queues based on two modes of customers arrivals, with fluctuating high-low rates, where the service rate is instantaneously adapted to the new arrival conditions. Moreover, the considered model is also suitable to describe instances in which only one kind of rate is subject to random fluctuations. For instance, the case when only the service rate is alternating between two values and refers to a queue which is subject to randomly occurring catastrophes, whose effect is to transfer the service mechanism to a slower server for the duration of a random repair time.

The above stated assumptions are also paradigmatic of realistic situations in which the underlying mechanism of the queue is affected by external conditions that alternate randomly, such as systems subject to interruptions, or up-down periods. In this case, the adaptation of the rates occurs instantaneously, differently from other settings where customers observe the queue level before taking a decision (see, for instance, Economou and Manou [18]).

It is relevant to point out that the alternation between the rates may produce regulation effects for the queue mechanism. Indeed, if the current environment leads to a traffic congestion (i.e., for ), then the switch to the other environment may yield a favorable consequence for the queue length (if ). This can be achieved by increasing the service speed, or decreasing the customer arrival rates. Note that the above conditions on the arrival and service rates, with appropriate switching rates and , may lead to a stable queueing system, even if the queue is not stable under one of the two environments.

1.2 Plan of the paper

In Section 2 we investigate the distribution of the number of customers and the current environment of the considered alternating queue. We first obtain the steady-state distribution of the system, which is expressed as a generalized mixture of two geometric distributions. This result provides an alternative solution to that obtained in [39] with a different approach. It is worth noting that the system admits of a steady-state distribution even in a case when one of the alternating environments does not possess a steady state. Furthermore, we also obtain the conditional means and the entropies of the process.

The transient probability distribution of the queue is studied in Section 3. Since the general case is not tractable, we analyse such distribution under the assumption that only a switch from environment to environment is allowed. In this case, we express the transient probabilities in a series form which involves the same distribution in the absence of environment switch. A similar result is also obtained for the first-passage-time (FPT) density through the zero state, aiming to investigate the busy period. The Laplace transform of the FPT density is also determined in order to evaluate the probability of busy period termination, and the related expectation.

In order to investigate the queueing system also under more general conditions we are lead to construct a heavy-traffic diffusion approximation of the queue-length process. This is obtained in Section 4 by means of a customary scaling procedure similar to those adopted in Dharmaraja et al. [11] and Di Crescenzo et al. [15]. The distribution of the approximating continuous process satisfies a suitable partial differential equation with alternating terms. Examples of diffusive systems with alternating behavior can be found in the physics literature. For instance, Bezák [4] studied a modified Wiener process subject to Poisson-paced pulses. In this case the effect of pulses is the alternation of the infinitesimal variance. A similar (unrestricted) diffusion process characterized by alternating drift and constant infinitesimal variance has been studied in Di Crescenzo et al. [12] and [17]. This is different from the approximating diffusion process treated here, for which all infinitesimal moments are alternating. The approach adopted in [17] cannot be followed for the process under heavy traffic, since it is restricted by a reflecting boundary at 0.

Concerning the approximating process, which can be viewed as an alternating Wiener process, we determine the steady-state density, expressed as a generalized mixture of two exponential densities. Then, in Section 5 for the approximating diffusion process we obtain the transient distribution when only one kind of switch is allowed. The distribution is decomposed in an integral form that involves the expressions of the classical Wiener process in the presence of a reflecting boundary at zero. Also for the alternating diffusion process we investigate the FPT density through the zero state, in order to come to a suitable approximation of the busy period. In this case, we express the related distribution in an integral form, and develop a Laplace transform-based approach aimed to study the FPT mean.

In the paper, the quantities of interest are investigated through computationally effective procedures by using MATHEMATICA®.

2 The queueing model

Let be a two-dimensional continuous-time Markov chain, having state-space and transient probabilities

| (1) |

where

| (2) |

with . Here, describes the number of customers at time in a queueing system operating under two randomly switching environments, and denotes the operational environment at time . Specifically, if then the arrival rate of customers at time is whereas the service rate is , for , with constant parameters .

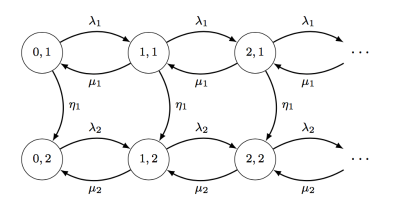

We assume that two operational regimes alternate according to fixed constant rates. In other terms, if the system is operating at time in the environment then it switches to the environment with rate , whereas if then the system switches in the environment with rate , with . Figure 1 shows the state diagram of . We recall that the considered setting is in agreement with the model introduced in [39].

For a fixed , we assume that the system is subject to random initial conditions given by a Bernoulli trial on the states and . Indeed, for a given , recalling (2), we have

| (3) |

where is the Kronecker’s delta.

From the specified assumptions we have the following forward Kolmogorov equations for the first operational regime:

| (4) |

and for the second operational regime:

| (5) |

Clearly, for all one has:

| (6) |

2.1 Steady-state distribution

Let us now investigate the steady-state distribution of the two-environment queue. We will show that it can be expressed as a generalized mixture of two geometric distributions. Our approach is different from the analysis performed in [39], where the steady-state distribution is achieved through recursive formulas.

Let be the two-dimensional random variable describing the number of customers and the environment of the system in the steady-state regime. We aim to determine the steady-state probabilities for the queue under the two environments, defined as

| (7) |

From (4) and (5) one has the following difference equations:

Hence, denoting by

the probability generating functions for the two environments in steady-state regime, one has:

| (8) | |||

where is the following third-degree polynomial in (see Eq. (22) of [39]):

| (9) |

By taking into account the normalization condition , from (8) we get:

| (10) |

It is worth noting that Eq. (10) is a suitable extension of the classical condition for the queue in the steady-state, i.e. . Moreover, recalling that , Eq. (10) shows that the existence of the equilibrium distribution is guaranteed if and only if one of the following cases holds:

-

(i) and ,

-

(ii) and ,

-

(iii) , and .

Hereafter, we consider separately the three cases.

Case (i)

If and one can easily prove that

| (11) |

Therefore, a steady-state regime does not hold for the queue under the environment , whereas a geometric-distributed steady-state regime exists for . In conclusion, if and then admits of a geometric steady-state distribution with parameter .

Case (ii)

If and , similarly to case (i), one has

Hence, in this case has a geometric steady-state distribution with parameter .

Case (iii)

Let , and . These assumptions are in agreement with the conditions given in [39]. Denoting by , , the roots of , given in (9), one has

| (12) | |||

so that , and . Moreover, we note that

| (13) |

and that, due to (9),

| (14) | |||

Hence, has three positive roots, two of them greater than 1 and one less than 1. Hereafter we show that the present method allows us to express the distribution of interest in closed form, as a generalized mixture of geometric distributions. Hence, we assume that , and , and thus .

Proposition 1

If , and , then the joint steady-state probabilities of can be expressed in terms of the roots , and of the polynomial (9) as follows:

| (15) |

where and

| (16) |

-

Proof.

Since , to ensure the convergence of the probability generating functions (8), we impose that their numerators tend to zero as . Hence, by virtue of (10), one has (see also Eqs. (26) and (27) of [39]):

(17) Note that, due to (12), (13) and (14), one has and . Making use of (17), from (8) one finally obtains:

(18) Expanding and , given in (18), in power series of , one finally is led to

(19)

We note that if , the steady-state probabilities do not depend on the initial conditions (3), i.e. on the probability .

By virtue of (13), from (18) one obtains (cf. also Eqs. (17) of [39]):

| (20) |

From Proposition 1, we have that and are both generalized mixtures of two geometric probability distributions of parameters and , respectively (see Navarro [34] for details on generalized mixtures).

Making use of Proposition 1 and of (20), we determine the conditional means in a straightforward manner:

| (21) |

Corollary 1

Eq. (22) shows that also is a generalized mixture of two geometric probability distributions of parameters and , respectively, so that

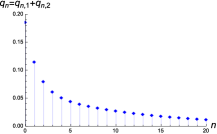

| (23) |

This result is in agreement with Eq. (33) of [39].

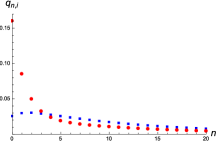

Figure 2 shows the steady-state probabilities (on the left) and (on the right), obtained via Proposition 1 and Corollary 1, for , , , , and . The roots of polynomial (9) can be evaluated by means of MATHEMATICA®, so that , , .

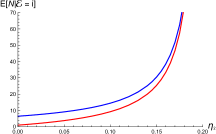

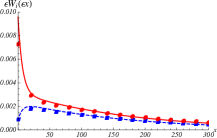

Figure 3 gives, on the left, a plot of the conditional means, obtained in (21), for a suitable choice of the parameters, showing that is increasing in , for . The mean , obtained via (23), is plotted as function of on the right of Figure 3.

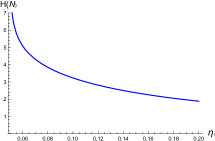

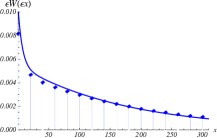

Similarly, on the left of Figure 4 are plotted the conditional means for a suitable choice of the parameters, showing that is decreasing in , for . The mean is plotted as function of on the right of Figure 4.

We remark that in the cases considered in Figures 3 and 4, the parameters satisfy the condition , and thus the joint steady-state probabilities of there exist due to Proposition 1. Moreover, in the cases considered in Figures 3 and 4, one has and , so that in absence of switching the queue should not admit a steady-state regime in the first environment, whereas a steady-state regime should hold in the second environment. This example shows that the switching mechanism is useful to obtain stationarity, in the sense that the alternating queue may admit a steady-state regime even if one of the alternating environments does not.

Making use of Proposition 1 and Eq. (20) it is easy to determine the (Shannon) entropies

| (24) | |||

| (25) |

where ‘’ means natural logarithm.

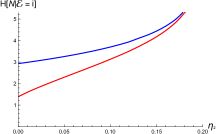

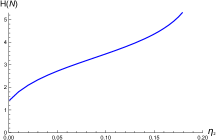

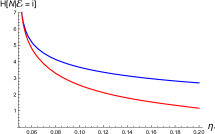

The conditional entropy (24) is a measure of interest in queueing, since it gives the average amount of information that is gained when the steady-state number of customers in the queue is observed given that the system is in environment . In Figure 5 we plot the conditional entropy (24) (on the left) and the entropy (25) (on the right) for the same case of Figure 3, showing that and are increasing in . Furthermore, for the same choices of Figure 4, in Figure 6 the entropies and are plotted, showing that are decreasing in .

Moreover, recalling (15), (20) and (22) one can also define the following entropies

| (26) | |||

| (27) |

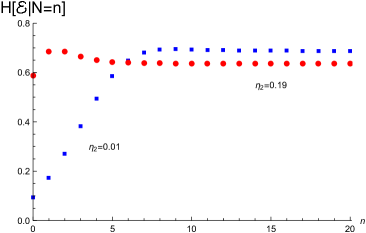

Note that and . The conditional entropy (26) gives the average amount of information on the environment when the number of customers in the queue is observed, whereas the entropy (27) gives the average amount of information on the environment. Note that, under the assumptions of Proposition 1, from (26) one has

| (28) |

with defined in (16). Therefore, the conditional average amount of information on the environment tends to the value given in (28) when the number of customers increases.

3 Analysis of case

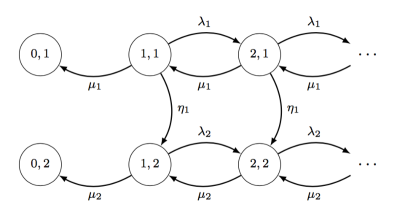

In the general case it is hard to determine the transient distribution of . Hence, we limit ourselves to the analysis of the system with and with the initial state given in (2). Figure 8 shows the state diagram of in this special case, where only transitions from the first to the second environment are allowed.

We remark that, the case can be studied similarly by symmetry.

3.1 Transient probabilities

Hereafter, we express the transient probabilities (1) in terms of the analogue probabilities of two queueing systems , , , characterized by arrival rate and service rate . Note that, for , and , we have (see, e.g., Zhang and Coyle [40], or Eq. (32) of Giorno et al. [23])

where denotes the modified Bessel function of the first kind. Moreover, making use of Eq. (49), pag. 237, of Erdélyi et al. [20], for , and , we have

| (30) |

Proposition 2

In the case , at most one switch can occur (from environment 1 to environment 2). Hence, Eq. (31) is also obtainable by noting that can be viewed as the probability that process is located at at time , starting from at time , with probability , and that no ‘switches’ occurred up to time . Similarly, resorting to the total probability law, Eq. (32) is recovered by taking into account that process is located at at time in two cases:

-

- when starting from at time , with probability , and performing a transition from to at time ,

-

- when starting from at time , with probability , then performing a transition from to at time (with and ), then switching from environment 1 to environment 2 at time , and finally performing a transition from state to in the time interval .

3.2 First-passage time problems

We now analyze the first-passage time through zero state of the system when . To this aim, first we define a new two-dimensional stochastic process whose state diagram is given in Figure 9. This process is obtained from by removing all the transitions from , . In this case only transitions from the first to the second environment are allowed. Moreover, and are absorbing states for the process .

We denote by

| (33) |

the state probabilities of the new process, where

| (34) |

Since the following equations hold:

| (35) | |||

and

| (36) | |||

with initial conditions

| (37) |

In order to obtain suitable relations for the state probabilities (33), we recall that the transition probabilities avoiding state 0 for the queue with arrival rate and service rate , for and is (cf. Abate et al. [1])

| (38) |

and, due to relation (cf. Eq. 8.486.1, p. 928 of [24]),

| (39) |

Proposition 3

The term in the right-hand-side of (40) can be interpreted as follows: starting from at time 0, with probability , the process reaches , with , at time without crossing in the interval , and no switches occurred up to time . Instead, the 2 terms in the right-hand-side of (41) have the following meaning:

-

- starting from at time 0, with probability , the process reaches at time , with , at time without crossing in the interval ;

-

- starting from at time 0, with probability , the process reaches , with , at time without crossing in the interval , then a switch occurs at time , and starting from the process reaches at time without crossing in the interval .

For , we consider the random variable

where is given in (2), with . Note that denotes the first-passage time (FPT) of the process through zero starting from with probability and from with probability , with . Hence, is the first emptying time of the queue, with the initial state specified in (2). For , the FPT of through or is identically distributed as the FPT of through the same states. Therefore, the first passage through or for can be studied via the probabilities obtained in Proposition 3. Specifically, recalling (33), for we have:

| (42) |

We focus our attention on the FPT probability density

| (43) |

Hereafter we show that such density can be expressed in terms of the first-passage-time density from state to state 0 of the queues with rates and , , given by (see, for instance, [1]):

| (44) |

Proposition 4

- Proof.

For , the 3 terms in the right-hand-side of the FPT density (45) can be interpreted as follows:

-

- starting from at time 0, with probability , the process reaches for the first time at time , and no switches occurred up to time ;

-

- starting from at time 0, with probability , the process reaches for the first time at time ;

-

- starting from at time 0, with probability , the process reaches , with , at time without crossing in the interval , then a switch occurs at time , and starting from the process reaches for the first time at time .

Let

be the Laplace transform of the FPT density .

Proposition 5

For and , one has

| (48) |

with

| (49) |

for , and

| (50) |

for .

The Laplace transform (48) is useful to calculate the probability that the process eventually reach the states or and the FPT moments.

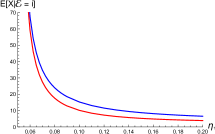

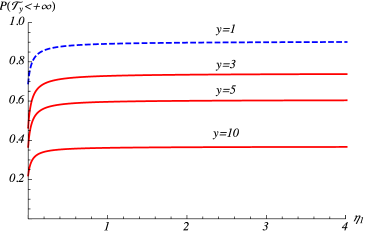

Let us now determine the probability of the eventual first queue emptying. Since , if then , so that , whereas if , then we have , so that for it results:

| (51) |

Note that if , represents the busy period density of the considered queueing model; hence, if the busy period termination is certain. On the contrary, if , (51) takes the simplest form:

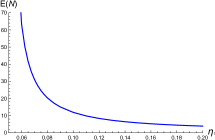

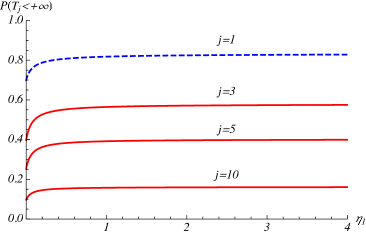

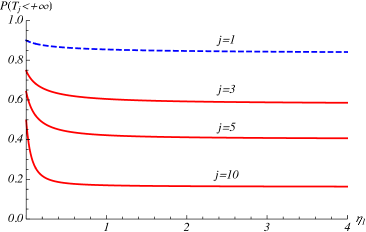

For , in Figure 10 we plot , given in (51), as function of for . The case corresponds to the probability that the busy period ends.

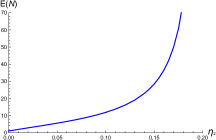

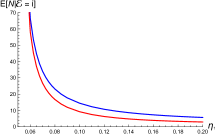

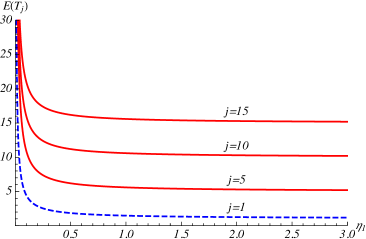

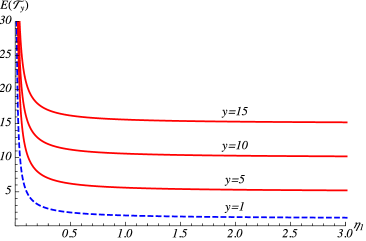

When , and , from (48) we obtain the FPT mean

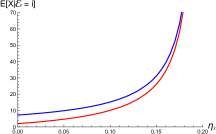

| (52) |

Clearly, for , the right-hand side of (52) corresponds to the FPT mean of the queue in the second environment.

Finally, in Figure 11 we plot the mean (52) as function of ; since , the first passage through zero state is a certain event.

4 Diffusion approximation

This section is devoted to the construction of a heavy-traffic diffusion approximation for the process . As customary, we adopt a scaling procedure that is usual in queueing theory and in other contexts (c.f. Di Crescenzo et al. [15] or Dharmaraja et al. [11], for instance). As a first step, we perform a different parameterization of the arrival and service rates of the stochastic model introduced in Section 2. Specifically, we set

| (53) |

where , , , for , and . We remark that is a positive parameter that has a relevant role in the scaling procedure indicated below.

Let us now consider the position , for any . Hence, the process is a two-dimensional continuous-time Markov chain, having state-space , where . We denote the transient probabilities of , , as

| (54) |

for and . In the limit as , it can be shown that the scaled process converges weakly to a two-dimensional stochastic process, say , having state-space . Note that may be viewed as a restricted Wiener process alternating between two environments, with switching rates and . For , and , let

| (55) |

denote the probability densities of the process , where the initial state is

| (56) |

with . Starting from the forward equations for , given in Eqs. (4) and (5), the scaling procedure mentioned above yields that the densities (55) satisfy the following partial differential equations of Kolmogorov type, for , and :

| (57) |

We note that the first 2 terms in the right-hand-side of (57) correspond to the classical diffusive operators of a Wiener process, whereas the last 2 terms express the joking between the two different environments, occurring with switching rates and . The first and second infinitesimal moments of the Wiener process in the -th environment are respectively and , . It is worth pointing out that, due to the scaling procedure, the first equations of systems (4) and (5) lead to the following reflecting condition at 0:

| (58) |

for and . Moreover, since for the process the initial condition is expressed by a Bernoulli trial, similarly as (3) we have the following dichotomous initial condition for densities (55):

| (59) |

where is the Dirac delta function. Furthermore, in analogy with (6), the normalization condition

| (60) |

holds for all . We remark that positions (53) express a heavy-traffic condition, since the rates and tend to infinity when in the approximation procedure.

4.1 Steady-state density

Let us now investigate the steady-state densities of . Let be the two-dimensional random variable of the system in the steady-state regime. We aim to determine the steady-state densities in the two environments, defined as

| (61) |

From (57) and (58) one has the following differential equations:

to be solved with the boundary conditions:

Hence, denoting by

the moment generating functions for the two environments in steady-state regime, one has:

| (62) | |||

where is the following third-degree polinomial in :

| (63) |

By taking into account the normalization condition , from (62) one obtains:

| (64) |

Recalling that , Eq. (64) shows that the steady-state regime exists if and only if one of the following cases holds:

-

(i) and ,

-

(ii) and ,

-

(iii) , and .

Hereafter, we consider separately the three cases.

Case (i)

If and , one can easily prove that

Hence, if and , the steady-state density is exponential, with parameter .

Case (ii)

If and , similarly to case (i), one has

so that the steady-state density is exponential with parameter .

Case (iii)

Let , and . Denoting by the roots of , given in (63), one has:

| (65) | |||

so that . Furthermore, from (63) it follows:

| (66) | |||

Making use of (65) and (66), it is not hard to prove that has one negative root and two positive roots. In the sequel, we assume that and , and .

Proposition 6

If , and , then the steady-state density of can be expressed in terms of the roots and of the polynomial (63) as follows:

| (67) |

where denotes an exponential density with mean and

| (68) |

for .

-

Proof.

Since , we require that also the numerators of and , given in (62), tend to zero as , so that by virtue of (64) one has:

(69) Note that from (65) and (66) we have and . Hence, substituting (69) in (62) one obtains:

(70) Since the functions (70) are finite for all in some interval containing the origin, the moment generating functions and determine the probability densities and . Indeed, by inverting the moment generating functions, for one obtains:

(71) from which (67) immediately follows.

In the continuous approximation, by virtue of (65), from (70) one has:

| (72) |

which provides the same result given in (20) for the discrete model.

Similarly to discrete case, we have that and are both generalized mixtures of two exponential distributions of means and , respectively.

Corollary 2

Eq. (74) shows that also is a generalized mixture of two exponential densities with means and , respectively, so that

| (75) |

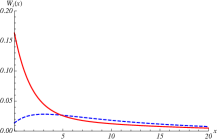

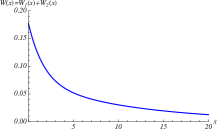

Figure 12 shows the steady-state densities (on the left) and (on the right), obtained via Proposition 6 and Corollary 2, for , , , , , , and . The roots of polynomial (63) can be evaluated by means of MATHEMATICA®, so that , , .

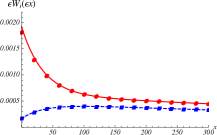

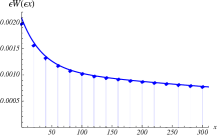

Figure 13 gives, on the left, a plot of the conditional means, obtained in (73), for a suitable choice of the parameters, showing that is increasing in , for . Furthermore, on the right of Figure 13 is plotted for the same choices of parameters. Similarly, in Figure 14 (on the left) and (on the left) are plotted for the same choices of parameters, showing that they are decreasing in .

To show the validity tof the approximating procedure given in Section 4, in Figures 15(a) and 16(a), we compare the functions , where is given in (67), with the probabilities , given in (15), for and , respectively. Furthermore, in Figures 15(b) and 16(b), we compare the functions , where is given in (74), with the probabilities , given in (22), for and , respectively. The probabilities (square), the probabilities (circle) and the probabilities (diamond) are represented for . According to (53), in Figures 15 we set , , , , whereas in Figures 16 one has , , , . From Figures 15 and 16, we note that the goodness of the diffusion approximation for the steady-state probabilities improves as decreases, due to an increase of traffic in the queueing system.

5 Analysis of the diffusion process for

Let us now analyze the transient behaviour of the process in the case , with the initial state specified in (56).

5.1 Probability densities

Similarly as in the discrete model, hereafter we express the probability densities (55) in terms of the transition densities of two Wiener processes , characterized by drift and infinitesimal variance , , restricted to , with reflecting boundary, given by (cf. [9])

| (76) |

where denotes the complementary error function.

Proposition 7

- Proof.

5.2 First-passage time problem

We consider the first-passage time through or states when . To this purpose, we define a two-dimensional stochastic process , obtained from by removing all the transitions from and . We assume that with probability and with probability , being . Similarly to the discrete queueing model, only transitions from the first to the second environment are allowed. Hence, for , denoting by

| (79) |

the transition density of the process , one has:

| (80) | |||

with the absorbing boundary conditions

| (81) |

and the initial conditions

| (82) |

Hereafter we express the transition densities (79) in terms of the probability densities of the Wiener processes in the presence of an absorbing boundary in the zero state for , which is given by (cf. [9])

| (83) |

Proposition 8

- Proof.

For , let

be the FPT through zero for starting from with probability and from with probability . We note that

| (86) |

Hereafter we focus on the FPT probability density

| (87) |

Specifically, we express such density in terms of the FPT densities from state to state for the Wiener processes , given by

| (88) |

Proposition 9

- Proof.

We note the high analogy in the FPT density , given in (89), with the FPT density , given in (45), of the discrete queueing model.

Let

be the Laplace transform of the FPT density .

Proposition 10

For and , one has

| (91) |

with

| (92) |

for , and

| (93) |

for .

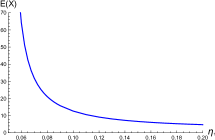

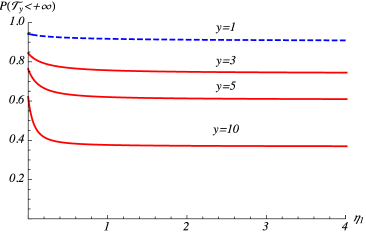

From (91) we determine the ultimate absorbing probability in or in . Since , if then , so that , whereas if , then we have , so that for it results:

| (94) |

with given in (92) for .

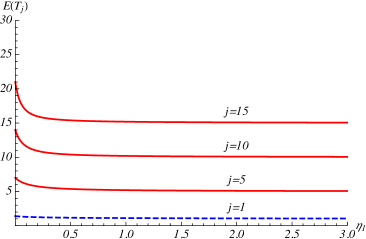

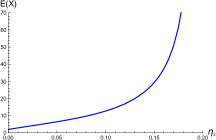

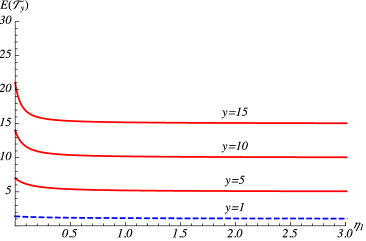

When , and , from (91) we obtain the FPT mean

| (95) |

Finally, in Figure 18 we plot the mean (95) as function of ; since , the first passage through zero state is a certain event.

Concluding remarks

In this paper we considered a an queue whose behavior fluctuates randomly between two different environments according to a two-state continuous-time Markov chain.

We first get the steady-state distribution of the system, which is expressed via a generalized mixture of two geometric distributions. A remarkable result is that the system admits of a steady-state distribution even if one of the alternating environments does not possess a steady state. Hence, the switching between the environments can be used to stabilize a non stationary queue by means of the random alternation with a similar queue characterized by steady state.

Moreover, attention has been given to the transient distribution of the alternating queue, which can be expressed in a series form involving the queue-length distribution in absence of switching. A similar result is obtained also for the first-passage-time density through the zero state, in order to investigate the busy period.

The second part of the paper has been centered on a heavy-traffic approximation of the queue-length process, that leads to an alternating Wiener process restricted by a reflecting boundary at zero. The analysis of the approximating process has been devoted to the steady-state density, which is expressed as a generalized mixture of two exponential densities. Moreover, we determined the transition density when only one type of switch is allowed. Such density can be decomposed in an integral form involving the expressions of the Wiener process in the presence of a reflecting boundary at zero. Finally, we analyzed the first-passage-time density through the zero state, which gives a suitable approximation of the busy period density.

Acknowledgements

This research is partially supported by the group GNCS of INdAM.

References

- [1] Abate, J., Kijima, M., Whitt, W. (1991) Decompositions of the transition function. Queueing Syst. 9, 323–336.

- [2] Arunachalam, V., Gupta, V., Dharmaraja, S. (2010) A fluid queue modulated by two independent birth-death processes. Comput. Math. Appl. 60, 2433–2444.

- [3] Avissar, O., Yechiali, U. (2012) Polling systems with two alternating weary servers. Semantic Scholar.

- [4] Bezák, V. (1992) A modification of the Wiener process due to a Poisson random train of diffusion-enhancing pulses. J. Phys. A 25, 6027–6041.

- [5] Boxma, O.J., Kurkova, I.A. (2000) The queue in a heavy-tailed random environment. Stat. Neerl. 54, 221–236.

- [6] Boxma, O.J., Kurkova, I.A. (2001) The queue with two service speeds. Adv. Appl. Prob. 33, 520–540.

- [7] Boxma, O.J., Schlegel, S., Yechiali, U. (2002) Two-queue polling models with a patient server. Ann. Oper. Res. 112, 101–121.

- [8] Burman, D.Y., Smith, D.R. (1986) An asymptotic analysis of a queueing system with Markov-modulated arrivals. Oper. Research 34, 105–119.

- [9] Cox, D.R., Miller, H.D. (1970) The Theory of Stochastic Processes. Methuen, London.

- [10] D’Auria, B. (2014) queue with on-off service speeds. J. Math. Sci. 196, 37–42.

- [11] Dharmaraja, S., Di Crescenzo, A., Giorno, V., Nobile, A.G. (2015) A continuous-time Ehrenfest model with catastrophes and its jump-diffusion approximation. J. Stat. Phys. 161, 326–345.

- [12] Di Crescenzo, A., Di Nardo, E., Ricciardi, L.M. (2005) Simulation of first-passage times for alternating Brownian motions. Methodol. Comput. Appl. Probab. 7, 161–181.

- [13] Di Crescenzo, A., Giorno, V., Krishna Kumar, B., Nobile, A.G. (2012) A double-ended queue with catastrophes and repairs, and a jump-diffusion approximation. Methodol. Comput. Appl. Probab. 14, 937–954.

- [14] Di Crescenzo, A., Giorno, V., Nobile, A.G. (2016) Constructing transient birth-death processes by means of suitable transformations. Appl. Math. Comput. 281, 152–171.

- [15] Di Crescenzo, A., Giorno, V., Nobile, A.G., Ricciardi, L.M. (2003) On the queue with catastrophes and its continuous approximation. Queueing Syst. 43, 329–347.

- [16] Di Crescenzo, A., Nobile, A.G. (1995) Diffusion approximation to a queueing system with time-dependent arrival and service rates. Queueing Syst. 19, 41–62.

- [17] Di Crescenzo, A., Zacks, S. (2015) Probability law and flow function of Brownian motion driven by a generalized telegraph process. Methodol. Comput. Appl. Probab. 17, 761–780.

- [18] Economou, A., Manou, A. (2016) Strategic behavior in an observable fluid queue with an alternating service process. European J. Oper. Res. 254, 148–160.

- [19] Eliazar, I., Fibich, G., Yechiali, U. (2002) A communication multiplexer problem: two alternating queues with dependent randomly-timed gated regime. Queueing Syst. 42, 325–353.

- [20] Erdélyi, A., Magnus, W., Oberhettinger, F., Tricomi, F.G. (1954) Tables of integral transforms. Vol. I. Based, in part, on notes left by Bateman, H. McGraw-Hill, New York.

- [21] Giorno, V., Nobile, A.G., Pirozzi, E. (2018) A state-dependent queueing system with asymptotic logarithmic distribution. J. Math. Anal. Appl. 458, 949–966.

- [22] Giorno, V., Nobile, A.G., Ricciardi, L.M. (1987) On some time-nonhomogeneous diffusion approximations to queueing systems. Adv. Appl. Prob. 19, 974–994.

- [23] Giorno, V., Nobile, A.G., Spina, S. (2014) On some time non-homogeneous queueing systems with catastrophes. Appl. Math. Comput. 245, 220–234.

- [24] Gradshteyn, I.S., Ryzhik, I.M. (2007) Tables of Integrals, Series and Products, 7th ed. Academic Press, Amsterdam.

- [25] Jiang, T., Liu, L., Li, J. (2015) Analysis of the queue in multi-phase random environment with disasters. J. Math. Anal. Appl. 430, 857–873.

- [26] Huang, L., Lee, T.T. (2013) Generalized Pollaczek-Khinchin formula for Markov channels. IEEE Trans. Commun. 61, 3530–3540.

- [27] Kao, E.P.C., Lin, C. (1989) The queue with randomly varying arrival and service rates: a phase substitution solution. Management Sci. 35, 561–570.

- [28] Kim, B.K., Lee, D.H. (2014) The M/G/1 queue with disasters and working breakdowns. Appl. Math. Model. 38, 1788–1798.

- [29] Krishna Kumar, B., Pavai Madheswari, S. (2005) Transient analysis of an queue subject to catastrophes and server failures. Stoch. Anal. Appl. 23, 329–340.

- [30] Liu, Z., Yu, S. (2016) The M/M/C queueing system in a random environment. J. Math. Anal. Appl. 436, 556–567.

- [31] Lu, F.V., Serfozo, R.F. (1984) queueing decision processes with monotone hysteretic optimal policies. Oper. Research 32, 1116–1132.

- [32] Mandelbaum, A., Massey, W.A. (1995) Strong approximations for time-dependent queues. Math. Oper. Res. 20, 33–64.

- [33] Medhi, J. (2003) Stochastic Models in Queueing Theory. Second edition. Academic Press, Amsterdam.

- [34] Navarro, J. (2016) Stochastic comparisons of generalized mixtures and coherent systems. TEST 25, 150–169.

- [35] Neuts, M.F. (1978) The queue with randomly varying arrival and service rates. Opsearch 15, 139–157.

- [36] Pang, G., Zhou, Y. (2016) queues with renewal alternating interruptions. Adv. Appl. Prob. 48, 812–831.

- [37] Paz, N., Yechiali, U. (2014) An queue in random environment with disasters. Asia-Pacific J. Oper. Res. 31, 1450016.

- [38] Perel, E., Yechiali, U. (2017) Two-queue polling systems with switching policy based on the queue that is not being served. Stoch. Models, 1–21.

- [39] Yechiali, U., Naor, P. (1971) Queuing problems with heterogeneous arrivals and service. Oper. Res., 19, 722–734.

- [40] Zhang, J., Coyle, E.J., Jr. (1991) The transient solution of time-dependent queues. IEEE Trans. Inform. Theory 37, 1690–1696.