Risk aggregation and capital allocation using a new generalized Archimedean copula

Abstract

In this paper, we address risk aggregation and capital allocation problems in the presence of dependence between risks. The dependence structure is defined by a mixed Bernstein copula which represents a generalization of the well-known Archimedean copulas. Using this new copula, the probability density function and the cumulative distribution function of the aggregate risk are obtained. Then, closed-form expressions for basic risk measures, such as tail value-at-risk (TVaR) and TVaR-based allocations, are derived.

Keywords : Bernstein copulas; Capital allocation; Copulas; Dependence; Tail value at risk; Value-at-Risk

1 Introduction

Risk aggregation and risk-based capital allocation have attracted considerable attention in actuarial sciences and quantitative risk management over the past years. One of the crucial applications of risk aggregation is to determine the required regulatory capitals and to price insurance and reinsurance products. For this purpose, an adequate risk measure should be used to evaluate the whole level of risk for a given portfolio. An important risk measure is the Value at Risk (VaR), which is defined as a threshold value such that the probability the loss on a portfolio exceeds this value is a given probability . Another interesting risk measure is the Tail Value at Risk (TVaR), also known as the conditional tail expectation (CTE), which represents the average amount of a loss given that the loss exceeds a specified quantile. The TVaR is known to be a coherent risk measure over the space of continuous random variables (see Dhaene et al. (2008); Furman and Zitikis (2008a); Furman and Landsman (2006)).

In this paper, we address risk aggregation and capital allocation using the TVaR risk measure. Consider a vector of continuous and non-negative random variables (rv’s) , the component denotes the marginal risk (claim or loss). We define the aggregate loss as . For a given confidence level , the value at risk of , , is defined by

where and is the cumulative distribution function (cdf) of . We also define the tail value at risk of , , as follows

| (1.1) |

The contribution of the -th risk to the aggregate risk is given by

| (1.2) |

for The additivity of the expectation allows the decomposition of the TVaR into the sum of TVaR contributions as follows

Adequate economic capital and capital allocation relay on accurate dependences modeling between different components of the portfolio. For this reason, multivariate risk models incorporating dependence are very important in risk modeling in finance and insurance. In the literature, several classes of multivariate distributions have been proposed. Landsman and Valdez (2003) obtained the explicit formulas of and for the multivariate elliptical distributions, which include the distributions such as multivariate normal, stable, student, etc. Other closed-form expressions for the economic capital and risk contribution under multivariate phase-type distributed risks have been given in Cai and Li (2005). The case of multivariate gamma distribution for risks has been studied in Furman and Landsman (2005) as well as a multivariate Tweedie distribution in Furman and Landsman (2010). Chiragiev and Landsman (2007) consider the case of multivariate Pareto risks. In these papers, explicit expressions for the and the TVaR-based allocation are derived. For further details on the TVaR-based allocation of risk capital, Kim (2007) and references within can be consulted. Other researchers addressed the risk aggregation problem using copulas. For example, Cossette et al. (2013) consider a portfolio of dependent risks whose multivariate distribution is the Farlie-Gumbel-Morgenstern copula with mixed Erlang marginal distributions. Sarabia et al. (2016) give explicit formulas for the probability density function of for some multivariate mixed exponential distributions for which the dependence structure is an Archimedean copula. Recently, Marri et al. (2018) derive explicit expressions for the higher moments of the discounted aggregate renewal claims with dependence.

The focus of this paper is to derive explicit formulas of and for , with a more general dependence structure that allows us to capture different types of dependence between structure. The multivariate model that we suggest is a mixed Bernstein copula. The mixed Bernstein copulas have many attractive properties and, in particular, they are non-exchangeable. This is useful for risk aggregation in many insurance and financial applications. Our model provides a new generalization of the well-known Archimedean copulas. The remainder of this paper is structured as follows. In Section (2), we introduce the mixed Bernstein copulas. The distribution of the aggregated risk is investigated in Section (3). In Section (4), we derive closed-formulas of the and for dependent rv’s joined by the mixed Bernstein copulas. We obtain specific expressions for the aggregated distribution in Section (5). The results are illustrated with numerical applications in Section (6).

2 Mixed Bernstein copulas

In this section, we will construct a new family of copulas that will be used in the different models.

Let be a vector of continuous and positive random variables (rv’s) with joint survival distribution function (sf) denoted by and univariate survival marginal distributions . Let be a positive random variable (rv) with probability density function (pdf) , cumulative distribution function (cdf) , and Laplace transform . In this paper, we assume that are dependent, positive and continuous rv’s such that

| (2.1) |

where is a vector of continuous rv’s with joint survival distribution function denoted by and with standard exponential marginal distributions (with mean ).

In Sarabia et al. (2018) and Albrecher et al. (2011), the rv’s are supposed to be independent. While such an assumption significantly simplifies the model setup, it is also to possible that it leads to a misidentification of the dependence structure. Indeed, the variable only capture the common factor of dependence between all the n variables (e.g., climate conditions, age,,etc.). In this paper, we add another level of dependence by assuming the vector has dependent components. According to Sklar’s theorem for survival functions (see e.g. Sklar (1959)), the multivariate survival function of can be written as a function of the marginal survival functions and a copula describing the dependence structure as follows: for and

In this paper, we assume that is defined with the Bernstein copulas introduced in Sancetta and Satchell (2004) and defined under some specifics conditions on the function , by

| (2.2) |

for every in such that , where

| (2.3) |

is the th Bernstein polynomial of order . Sancetta and Satchell (2004) showed that the coefficients of the Bernstein copulas have a direct interpretation as the points of some arbitrary approximated copula , i.e., This justifies our choice of Bernstein copulas since our mixed Bernstein model could approximate many different dependence structures. In Cottin and Pfeifer (2014), it has been proved that any copula function can be approximated uniformly using Bernstein polynomials. In the following theorem, we give sufficient conditions for to be a copula.

Theorem 2.1.

Proof.

A proof of this theorem was given by Yang et al. (2020).∎

The application of Bernstein copulas in actuarial science is recent. Salmon et al. (2006) and Hurd et al. (2007) apply Bernstein copulas to the pricing of two-asset derivatives written on foreign exchange rates. Diers et al. (2012) use Bernstein copulas to model the dependence between non-life insurance risks. Tavin (2013) analyze properties of Bernstein copulas in a context of multi-asset derivatives pricing. In contrast to Archimedean copulas, Bernstein copulas can model non-exchangeable dependence structures.

From Sancetta and Satchell (2004) and Cottin and Pfeifer (2014), the corresponding pdf of the copula is given by

| (2.7) |

where

Cottin and Pfeifer (2014) show that the Bernstein copulas density function can also be expressed as

| (2.8) |

where is a random vector whose marginal component follows a discrete uniform distribution over and For more details about Bernstein copulas, we refer readers to Kulpa (1999) and Sancetta and Satchell (2004).

From (2.1), the joint survival function of can be written as

| (2.9) |

for . It implies that the marginal survival function of is given by

| (2.10) |

for where is the Laplace transforms of . Note that the marginal random variables are necessarily completely monotone (see, e.g.,Oakes (1989)).

A closed-form expression for the survival function of is given in the next theorem.

Theorem 2.2.

Let be a vector of continuous and non-negative rv’s defined by the stochastic representation (2.1). Then the survival function of is given by

| (2.11) |

for , where

Proof.

On the other hand, according to Sklar’s theorem for survival functions, see e.g. Sklar (1959), the joint survival function of can be written as a function of the marginal survival functions and a copula describing the dependence structure as follows:

| (2.13) |

for and Then, the following proposition holds.

Proposition 2.1.

The copula function that corresponds to the general dependence structure defined in Theorem (2.2) is given, for by

| (2.14) |

where

This new family of copulas extends the well-known Archimedean copulas and could be seen as a mixture of distorted Archimedean copulas with generator . The study of the properties of this copula are beyond the scoop of this paper and we leave it for a future research.

Remark 2.1.

From (2.5), one gets for

Remark 2.2.

If , then the copula in (2.14) reduces to a n-dimensional Archimedean copula with generator and given by .

Remark 2.3.

For the sake of simplicity, it is assumed that for .

An appropriate choice of the joint cumulative distribution in the calculation of the coefficient could lead to a different dependence structure. This point is illustrated in the following example. In fact, the copulas defined in Proposition (2.1) could significantly change the obtained dependence by an Archimedean copula.

Example 2.1.

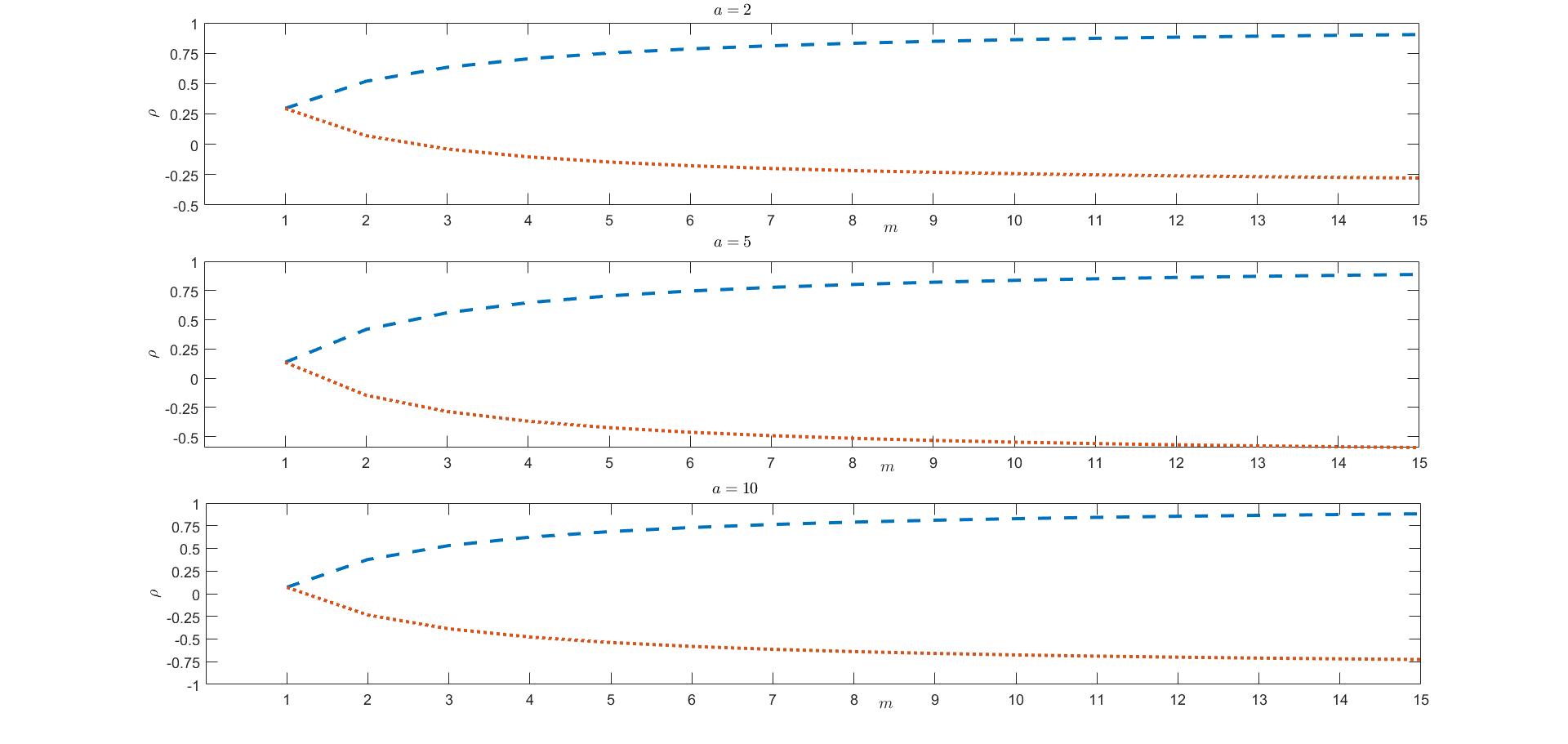

Assume that the mixing rv is following a Gamma distribution such that

Thus, when the copula in (2.14) is reduced to a Clayton copula. For different values of and for different choices of , the dependence structure is assessed via the Spearman’s that is given by

| (2.16) |

This allows us to measure the impact of introducing the Bernstein copula on the dependence structure of the mixed exponential model. In this illustrations, we consider two cases for

- (i)

-

Counter-comonotonic: , and

- (ii)

-

Comonotonic: .

Given this choices for , the obtained values of will consist of an upper bound if is comonotonic and a lower limit if is counter-comonotonic. In Figure 1, the values of are displayer for and for , and 10.

It is obvious that the decreases (increases) as increases when the Bernstein copula has a negative (positive) dependence. Moreover, the dependence is significantly changing, which means that the introduction of the mixed-Bernstein copula improves the obtained range of dependence and allows to reach values beyond the value in the case of Archimedean copula (when ). Similar results with the same pattern are obtained under different choices of the copula .

3 The distribution of the aggregated risk

In this section, we obtain the probability density function and the survival function of the aggregated risk .

The joint probability density function (pdf) of is given by

| (3.1) |

Combining (2.7) and (3.1), the pdf of becomes

| (3.2) | |||||

where are independent rv’s with pdf Note that is the density function of the th of the smallest order statistic from i.i.d. rv’s exponentially distributed with mean 1 . For more details about order statistics, we refer readers to David and Nagaraja (2004). Furthermore, it is known that (see, e.g., Basu and Singh (1998))

| (3.3) |

where are independent exponential distributions with mean 1. (Here, stands for the ’equality in distribution).

To derive the pdf of the aggregated random variable with the mixed Bernstein copulas presented in Section (2), the following result is needed.

Theorem 3.1.

Assume that the rv’s are dependent and defined with the Bernstein copulas and distributed as exponential , such as assumed in Section (2). Then, the pdf of the aggregated random variable is given by

| (3.4) |

where and form a sequence of independent rv’s, independent of for and such that follow a shifted geometric distribution with probability mass function for for and

Proof.

From (3.2) and (3.3), the Laplace transform of is

In fact, we can rewrite the above result as

where denoting the indicator function on , we readily obtain that

On the other hand, we have

can then be rewritten as

| (3.5) | |||||

where form a sequence of independent rv’s, independent of for and such that follow a shifted geometric distribution for and . The inversion of (3.5) with respect to yields (3.4) with

| (3.6) |

Since the support of the rv is then for The expression in (3.4) follows immediately. ∎

Now, we are in position to derive a closed-form expression of the pdf of

In the following corollary, we use Theorem (3.1) to derive the pdf of the aggregated random variable

Corollary 3.1.

Let be a vector of continuous and non-negative rv’s defined by the stochastic representation (2.1). Then, the pdf of the aggregated random variable is given by

| (3.7) |

for

Proof.

Remark 3.1.

We further derive the survival function of the distribution of

Corollary 3.2.

The survival function of the distribution of is given by

for where

Proof.

Remark 3.2.

If , then one gets the survival function of the aggregated risk discussed in Sarabia et al. (2018) and given by

4 TVaR with the mixed Bernstein copulas

In this section we derive an expression of the TVaR for dependent rv’s joined by the mixed Bernstein copulas with generator

Theorem 4.1.

Let dependent rv’s joined by the mixed Bernstein copulas with generator , then the TVaR of the aggregate risk is

| (4.1) | |||||

where and form a sequence of independent rv’s, independent of for and such that follow a shifted geometric distribution .

Proof.

Corollary 4.1.

If we take , then the in Theorem (4.1) reduces to

Proof.

Substituting into (4.1), we get the desired result. ∎

To derive the TVaR-based contribution of risk , to the sum with the mixed Bernstein copulas presented in Section (2), the following result is needed.

Lemma 4.2.

Assume that the rv’s are dependent and defined with the Bernstein copulas and distributed as exponential , such as assumed in Section (2). Then, the pdf of the random vector is given by

| (4.3) |

for and where

and form a sequence of independent rv’s, independent of for and such that follow a shifted geometric distribution .

Proof.

Let be the joint Laplace transform of the random vector defined by It follows from (3.2) and (3.3)

| (4.4) | |||||

After some rearrangements, (4.4) becomes

| (4.5) |

On the other hand, we have and Substituting the latter expressions in (4.5), it follows that the joint Laplace transform can be rewritten as

| (4.6) |

where form a sequence of independent rv’s, independent of for and such that follow a shifted geometric distribution .

Since the support of the rv is the inversion of (4.6) with respect to and yields the required result. ∎

Now, we are in a position to derive a closed-formula for the TVaR-based contribution of risk , to the sum with the mixed Bernstein copulas presented in Section (2).

Theorem 4.3.

Let dependent rv’s joined by the mixed Bernstein copulas with generator . Then the TVaR-based contribution of risk , to the sum at level , , is

| (4.7) | |||||

where and form a sequence of independent rv’s, independent of for and such that follow a shifted geometric distribution .

Proof.

Corollary 4.2.

If we take , then (4.7) reduces to

Proof.

If we take , it follows from (4.7) that if and if Therefore, the proof is complete. ∎

Corollary 4.3.

Let dependent rv’s joined by the mixed Bernstein copulas with generator . Then

Corollary 4.4.

Let dependent rv’s joined by the mixed Bernstein copulas with generator . If the joint probability mass function of the random vector is exchangeable, then

Proof.

The proof follows from Theorem (4.3) by using elementary calculus. ∎

5 Models

In this section, we present some results as consequences of our main results stated previously. We will consider dependent models with different claim distributions of the type Pareto and Gamma distributions, see Albrecher et al. (2011) and Sarabia et al. (2018) for more details.

5.1 Pareto claims with Clayton copula dependence

We assume that has a gamma distribution, with pdf , and a Laplace transform defined by

| (5.1) |

It follow that with survival function given by for Using (5.1), the expression for in (2.14) turns into

| (5.2) |

where

Using (2.13), the expression for the survival function of turns into

| (5.3) |

which is the joint survival function of a Pareto distribution.

Remark 5.1.

In the following theorem, we give a close expression for the pdf of the aggregated risk for the special case of the Pareto claim with Clayton copula dependence.

Theorem 5.1.

Let be the sum of dependent rv’s with joint cdf defined by the multivariate mixed Bernstein copulas. Then the pdf of the aggregated random variable is given by

| (5.4) |

for where denotes the Beta function.

Proof.

5.2 Gamma claims with dependence claims

Our next model is based on a Gamma claim distribution, , for it follows that the survival function of the claim is

| (5.7) |

Using (2.11), the multivariate survival function of can be written as

We are now ready to apply the preceding result to derive a closed expression for the pdf of the aggregated risk with dependent Gamma claim.

Theorem 5.2.

Let be the sum of dependent rv’s with gamma marginal distributions and with joint cdf defined by the multivariate mixed Bernstein copulas. Then the pdf of the aggregated random variable can be written as a finite mixture of Gamma distributions

| (5.8) |

where

Proof.

6 Numerical illustrations

In this section, numerical examples are given to illustrate our findings. We assume that the rv has a Gamma distribution, . In the first example, the Bernstein copula is based on an exchangeable copula, while in the second one, we use a non exchangeable copula.

Example 6.1.

In this example, the values for the risk measures and are computed for different values of in the following two cases

- (i)

-

The copula is comonotonic, i.e.,

- (ii)

-

The copula is counter-comonotonic, i.e.,

The obtained results are displayed in Table 6.1.

| Case (i) | |||||||

| 139.12 | 155.60 | 159.76 | 162.15 | 162.95 | 163.34 | 163.55 | |

| 205.30 | 233.06 | 241.33 | 247.00 | 249.30 | 250.57 | 251.37 | |

| Case (ii) | |||||||

| 139.12 | 123.41 | 119.98 | 118.06 | 117.39 | 117.05 | 116.84 | |

| 205.30 | 178.71 | 173.63 | 170.91 | 169.98 | 169.51 | 169.22 | |

As expected, introducing a positive dependence (negative dependence) between the risks leads to a heavier (a lighter) tail for the aggregate risk .

Example 6.2.

In this example, two non-exchangeable copulas are considered

(i)

A piece-wise copula based on two different Gaussian copulas

where is the Gaussian copula with parameter . In our numerical computation, it is assumed that , , and .

(ii)

Following Liebscher (2008), we consider a non-exchangeable copula based on transformations of two Clayton copulas (Cf. Equation (4) in (Liebscher (2008))

with , , , and .

For these two copulas, we compute the , , , and . The obtained values are given in Table 6.2.

Table 2: Impact of on the VaR, TvaR in the case of non-exchangeable copulasReferences