About subordinated generalizations of 3 classical models of option pricing

Abstract

In this paper, we investigate the relation between Bachelier and Black-Scholes models driven by the infinitely divisible inverse subordinators. Such models, in contrast to their classical equivalents, can be used in markets where periods of stagnation are observed. We introduce the subordinated Cox-Ross-Rubinstein model and prove that the price of the underlying in that model converges in distribution and in Skorokhod space to the price of underlying in the subordinated Black-Scholes model defined in [31]. Motivated by this fact we price the selected option contracts using the binomial trees. The results are compared to other numerical methods.

keywords:

subdiffusion, subordinator, option contracts, Monte Carlo, Bachelier model, Black-Scholes model, Cox-Ross-Rubinstein modelIntroduction

The theories of finance and economy began nearly a century ago with the works of Walras and Pareto and their mathematical description of equilibrium theory (see [13] and references therein). Soon after L. Bachelier in his thesis [3] began the theory of option pricing. In the same work, he initiated the research of diffusion processes five years before recognized as the pioneering works of A. Einstein [12], M. Smoluchowski [42] and decades before famous works of P. Lévy [25], K. Itô [18] and N. Wiener [47]. Bachelier was the first who found the practical application of random walk in finance. Despite the groundbreaking character, the theory of Bachelier was forgotten for over fifty years. In Samuelson [39] used the Geometric Brownian Motion (GBM) to model prices of underlying instrument. The culminating event in the developmenet of the theory of option pricing was when Black, Scholes and Merton found consistent formulas for the fair prices of European options [4, 35]. The discovery was of such great importance that Merton and Scholes were awarded the Nobel Prize in Economics in .

The Bachelier model is intuitive and elegant, but it allows the underlying financial process to drop into the negative regime. The underlying asset in B-S model instead of the Arithmetic Brownian Motion (ABM) follows GBM. Hence, the obvious property of non-negativity of the underlying process is conserved. The classical Black-Scholes (B-S) model, despite its popularity, can not be used in many different cases. Note that one of the greatest weaknesses of B-S model is the presence of volatility smile - in other words the assumption of constant volatility results that B-S price often does not fit the market price [17]. Therefore, the B-S model was generalized to weaken its strict assumptions, allowing such features as the possibility of jumps [8, 49], stochastic volatility [1, 49], market regulations [2], transactions costs [27, 45], regime switching [26] and stagnation of underlying asset [22, 23, 29] to name only few.

Nowadays, we know that financial data are often far away from classical models. Neither the B-S nor the Bachelier model can capture the characteristic motionless periods observed among many markets (see, e.g., [5] and the references therein). Such dynamics can be observed in every nonliquid market, e.g., in emerging markets where the number of transactions and participants is low. Similar behaviour can be observed in experimental physics where the motion of small particles is interrupted by trapping events. During that random time, the particle is immobilized and stays motionless. For the discussed systems, the subdiffusive model was proposed and nowadays it is well-established approach with many practical applications [6, 14, 19, 38, 43].

In order to properly price the option contracts in markets where the subdiffusive character of the underlying asset was observed, the generalization of Bachelier [32] and B-S model [29] were proposed. For the subdiffusive B-S model, effective numerical methods for valuing vanilla and barrier options were proposed [22, 23]. The subdiffusive models of Bachelier and B-S are generalizations of the standard models to the case where the underlying assets display characteristic periods in which they stay motionless. The classical models do not take these phenomena into account. As a consequence of an option valuation for the market displaying the stagnation property, the fair price provided by the Bachelier/B-S model is misestimated. To describe these dynamics properly, the subordinated Bachelier/B-S model assumes that the underlying instrument is driven by an inverse subordinator.

Let us focus on the inverse tempered stable subordinator. In this case, time periods in which their value are observed to be constant depend on the subdiffusion parameter and tempering parameter . If , the subordinated Bachelier/B-S reduce to the classical models [29, 32].

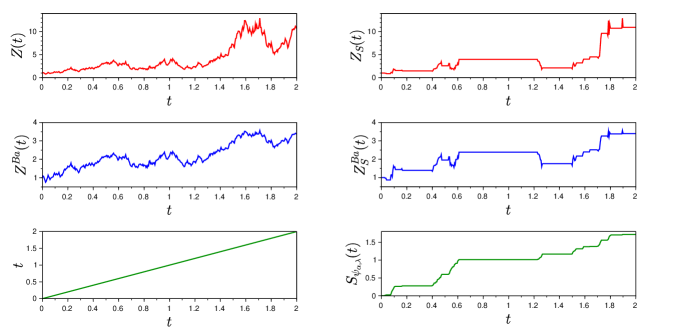

In Figure 1 we compare sample trajectories of the underlying assets in the classical Bachelier and B-S models compared to their equivalents characterized by -tempered -stable inverse subordinator. Even a small stagnation of an underlying can not be simulated by a classical model. As a generalization of the standard Bachelier and B-S models, their subordinated equivalents can be applied in a wide range of markets - including all cases where Bachelier and B-S can be used.

The Cox-Ross-Rubinstein (CRR) model is a discrete version of B-S model and provides a general and easy way to price a wide range of option contracts [10].

In this paper, we find the relation between the European options prices in the subordinated Bachelier and B-S model. By this way, we show that the earliest and the most popular models of option pricing are in some sense close even if they are run by inverse subordinators. We also define the subordinated CRR (called also subordinated binomial) model and prove that the price of the underlying/European option converges to the price of the underlying/European option in the subordinated B-S model. We use this fact to price the selected types of options. Finally, we compare the results with other numerical methods.

1 Inverse subordinators

We begin with defining the Laplace exponent

| (1) |

where is the Lévy measure such that . We assume that . Then the so-called inverse subordinator can be defined as [30, 31, 32]

| (2) |

where is the strictly increasing Lévy process (subordinator) [40] with the Laplace transform

and is given by (1). Since is a pure jump process with cádlág trajectories and not compound Poisson, has continuous and singular sample paths with respect to the Lebesgue measure. Moreover, every jump of correspond to the flat period of inverse. Note that inverse subordinators except of compound Poisson (which does not satisfy the assumption ) have density [34]. In the next sections we use the notation . In the whole paper, we call the model “subdiffusive” if it is driven by the -stable inverse subordinator, i.e. if , . We call the model “subordinated” if it is driven by any inverse subordinator . Note that in the literature subordinated models are the models run by the subordinators or, like in this paper, by the inverse subordinators.

2 Subordinated Bachelier model

Bachelier’s model is based on the observation that the stock price dynamics is analogous to the motion of small particles suspended in liquids [3]. Therefore, in modern terms, the stock price follows ABM

where is the price of the underlying instrument, , , , and is a standard Brownian motion on the probability space . Here, is the sample space, is a -algebra interpreted as the information about the history of underlying price and is the “objective” probability measure.

The price of an underlying asset in the subordinated Bachelier model is defined by the subordinated ABM:

| (3) |

where is defined in (2). We assume that is independent of for each . Let us introduce the probability measure

| (4) |

where , . As it is shown in [32], is a -martingale. The subordinated Bachelier model is arbitrage-free and incomplete [32]. Let us recall that the lack of arbitrage is one of the most expected properties of the market and claims that there is no possibility to gain money without taking the risk. The market model is complete if the set of possible gambles on the future states can be constructed with existing assets. More formally, the market model is complete if every - measurable random variable admits a replicating self-financing strategy [9]. The Second Fundamental theorem of asset pricing [9] states that a market model described by and underlying instrument with filtration is complete if and only if there is a unique martingale measure equivalent to . Despite that defined in (4) is not unique, it is the “best” martingale measure in the sense of the criterion of minimal relative entropy. The relative entropy (we use the Kullback-Leibler approach) is the distance between measures [24]. The criterion of its minimal value in this case means, that the measure minimizes the distance to the “real-life” measure [32].

3 Subordinated B-S model

The assumptions here are the same as in the classical B-S model [21] with the exception that we do not assume the market liquidity and that the underlying instrument, instead of GBM, follows subordinated GBM [31]:

| (5) |

where - the price of the underlying instrument. The constants , and the stochastic processes , are defined in the same way as in the previous section. Note that equivalently can be defined by the subordinated ABM, i.e.,

where is defined in (3). Let us introduce the probability measure

| (6) |

where , . As shown in [31], is a -martingale. The subordinated B-S model, similar to the subordinated Bachelier model, is arbitrage-free and incomplete [31]. Despite that defined in (6) is not unique, it is the “best” martingale measure in the sense of the criterion of minimal relative entropy [31]. Note that for the case of stable and tempered stable inverse subordinators (where , respectively, for , , , ), for and reduce to the measures of the classical Bachelier and B-S models which are arbitrage-free and complete [29, 32].

At the end of this section, we will find the relation between the European call and put options in the subordinated B-S model.

Proposition 3.1.

Between the prices of the European call and put options in the subordinated B-S model, the following relation holds:

| (7) |

where and denote the fair prices of the European put and call options in the subordinated B-S model, respectively.

Proof:

By [31], we have

| (8) |

and

4 Relation between the subordinated model of Bachelier and B-S

Although the Bachelier and B-S models have a lot in common, they follow different concepts: an equilibrium argument in the Bachelier case, as opposed to the no-arbitrage argument in the B-S approach [41]. The next theorem finds the direct relation between the European option prices in both models.

Theorem 4.1.

Let us denote - expiration time, - volatility of the B-S model, and - fair prices of a call option in the subordinated Bachelier and the subordinated B-S model with respect to the measures and , respectively. We assume that (at the money), and that where is the strike, is the value of the underlying instrument at time , is an interest rate, and is the volatility of the Bachelier model. Then the following relation holds:

| (11) |

for the inverse subordinator , .

Proof:

Note that (11) is the generalization of the analogous relation between option prices in the classical Bachelier and B-S model [41]:

| (12) |

for Let us consider

| (13) |

and

| (14) |

where - PDF of . Note that (13) and (14) hold by [32] and [31], respectively. Let us observe that

where the equality holds by (13) and (14), and inequality by (12).

Now let us use the same idea for the upper boundary of :

where the first equality holds by (13) and (14), and the inequality by (12). Both results can be finalized as two-sided inequalities:

Note that by the relations between European put and call options for the subordinated Bachelier [32] and the subordinated B-S model (7) (which for the case has the same form

), (11) also holds for put options.

Example 1.

Let be an stable inverse subordinator.

Here is the -stable subordinator [29, 33]. Note that . An important feature of the subordinator is that it is self-similar, and thus its density function satisfies [37]

where . With that, we can also obtain a similar formula for the density of the inverse stable subordinator [37]

where . Therefore, the formula [37]

| (15) |

Using the connection with the Laplace transform (15), we can obtain the formula for any given moment [37]

| (16) |

Thus, by Theorem 11, Equation (16) and by the self-similarity of the inverse subordinator, we have:

| (17) |

Let us observe that, for real-life parameters, the right-hand side of (17) is low; therefore, both models are close to each other. This result is also interesting because it indicates the relation between the solutions of two different fractional diffusion equations. Indeed, the fair price of the European call option in the subdiffusive B-S model [23, 22] is equal to , where is determined by:

| (18) |

for . Similarly, the fair price of the European call option in the subdiffusive Bachelier model is , where is given by

| (19) |

for . In (18) and (19) ”” denotes the limiting behavior of a function when the argument tends toward . Furthermore, in both (18) and (19) denotes a fractional Caputo derivative defined as [44]:

Note that the interpretation of and in both (18) and (19) is the value of the underlying asset and the time left to , respectively. The derivation of (19) can be done using the same approach as in the proof of Theorem 1.3. in [20]. In fact, it suffices to take and replace the standard B-S equation satisfied by with the classical Bachelier PDE.

5 Subordinated CRR model

In this section, we will consider a binomial tree approximation of the subordinated B-S model introduced in Section 3. Similarly to the classical B-S binomial tree approximation [10], we will prove that the subordinated CRR is close to the B-S model. More precisely, we will show that the underlying instrument in the subordinated CRR model converges in distribution to its equivalent in the subordinated B-S model and that in many cases the subordinated CRR option price converges to its (subordinated) B-S analogue - in both cases, the convergence is taken over the number of nodes in the binomial model. The idea presented in this paper follows the idea given by Gajda and Magdziarz article [31]. We have that:

| (20) |

where denotes the martingale measure of the classical B-S model. We will justify that the subordinated CRR and B-S are close to each other. to calculate the innermost expectation on the right-hand side of formula (20), but applied to the binomial tree approximation. Then, we will use Monte Carlo simulations to calculate the sample mean using the simulated trajectories of the inverse subordinator. An alternative view to this approach is that we are randomizing the time horizon on the classical binomial tree. Randomization is given by the inverse subordinator. Furthermore, to calculate the option price, we calculate the appropriate sample mean of prices from randomized binomial trees.

5.1 Convergence of binomial tree asset price model to subordinated GBM

We will consider the subordinated GBM defined in (5). In this section, we will prove that the stock price given by the modified binomial tree converges in distribution to the subordinated GBM (conditionally on ).

Consider the realization of for any . We will begin by introducing a discrete model for our approximation of the asset price. We consider the set of equidistant times . Let denote the initial price of the stock , its price in “subordinated” time . We consider a discrete conditional model of CRR type [10]:

where and is the conditional return of the stock. Random variables naturally depend on and on the number of steps (and other parameters of the model, such as and ). Thus, the price of the asset in time is given by

To provide a probability model, we assume that for fixed , , are mutually (conditionally on ) independent and identically distributed random variables in a common probability space .That is,

Theorem 5.1.

Let us assume that the conditional expectation and variance of (conditional) returns of the stock are proportional to time interval :

Under this assumption and the previously introduced construction of a conditional binomial tree, we have

| (21) |

Proof:

For the purpose of this proof, let us define

for . Let us denote: - PDF of , - PDF of , - PDF of . By the total probability formula, we get:

| (22) |

Let us consider the characteristic function of :

| (23) |

where the second equality holds by (22). Furthermore, we could change the integration order in the third equality of (23) by the Fubini Theorem, because the densities are non-negative a.s. and integrable, and the absolute value of the characteristic function is bounded by . By convergence of the underlying instrument in the standard CRR model [10] we get

where and . To finish the proof, it suffices to show the convergence of the characteristic functions of to the characteristic function of :

where the second equality holds by Lebesgue’s Dominated Convergence Theorem.

Theorem 5.1 can be strengthened for the case of functional convergence in the Skorokhod space. To formulate the corresponding theorem, let us first introduce the Definitions 5.1-5.3 [46].

Definition 5.1.

The Skorokhod space is a space of all functions of -type defined on some interval having values in . For , we use the notation .

Definition 5.2.

The metrics and we define by

where is a set of parametric representations of in and is a completed graph defined as:

for some and . Moreover, is a Hausdorff’s metrics defined as

for the distance of point from set defined by

where is a standard metrics in .

Definition 5.3.

Let be a subset of all , where for each , where is the -th coordinate of . Then denotes the set of functions belonging to , which do not decrease with respect to each coordinate.

Theorem 5.2.

Suppose that in . If

1. is continuous and strictly increasing at whenever and

2. is monotone on and , whenever ,

then in , where the topology throughout is or .

In Theorem 5.2, denotes a set of discontinuities of .

Proof:

Let us denote , , , , where is a Brownian motion. Observe that due to the convergence of the price of the underlying instrument in the classical CRR model to the price of this asset in the standard B-S model in [11], we have . All other assumptions of Theorem 5.2 are satisfied because and have continuous trajectories and is nondecreasing. So, based on Theorem 5.2, the proof is completed. Let us observe that the limit process has a continuous distribution, hence there holds also a convergence of finite-dimensional distributions.

5.2 Convergence of the subordinated binomial tree model to subordinated B-S model

We will use the following notations: - risk neutral probability of up-movement on a binomial tree, - a risk neutral measure corresponding to and , and - parameters of the binomial tree model (dependent on and ). By the basic properties of the classical binomial model, we get [10]:

| (24) |

| (25) |

| (26) |

where is a realization of . Since we consider a discrete model, we assume that

| (27) |

Let us focus on the European option with the payoff function (where is the price of the stock at time ) in the subordinated CRR and subordinated B-S model. Then, we have

Theorem 5.4.

Let us assume that there exists a constant such that for the payoff function follows:

| (28) |

Then, according to the assumptions of Theorem 5.1, the price of the European option in the subordinated binomial model, which is given by the following formula:

converges to the option price in the subordinated B-S model:

where denotes the martingale measure of the classical B-S model.

Sketch of proof for pointwise convergence:

By the convergence of the CRR model to the B-S [10], for expiration time we have:

| (29) |

Therefore, using the fact that for there holds (21), after conditioning (29) by we have

| (30) |

After taking the expected value on both sides of (30), we get

| (31) |

To finish the proof, we have to show that

| (32) |

By (28), we have

| (33) |

where the third equality is satisfied by (24)-(26),and the last equality is satisfied by (27).

Since we bounded

by the integrable function independent of , by the dominated convergence theorem, (32) holds. Therefore, the proof is completed.

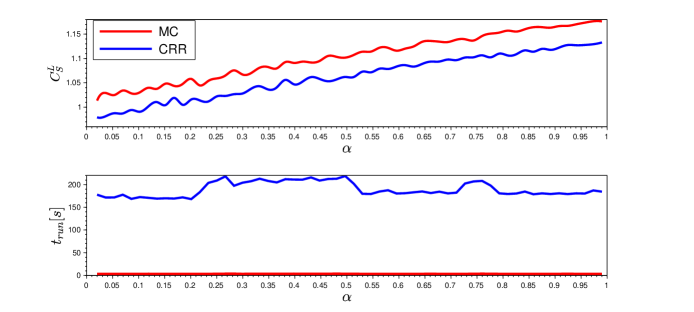

Analogously, the convergence of prices of a wide range of options can be shown. Indeed, it is enough to change in the proof the option pricing formula of the CRR model. Note that (28) is satisfied, for example, for payoffs of the vanilla call (or put) options. However, (28) does not hold, e.g., for the lookback option considered in Figure 4. Figure 4 indicates that the output of the CRR method is close to the real value. However, the use of the binomial method for such options should be avoided as long as the theoretical justification is missing.

Thus, we have the following algorithm for pricing any option in the subordinated B-S model:

We recall the observation of [15] that the convergence rate depends on the smoothness of the option payoff functions. Since most of the payoff functions are not continuously differentiable (e.g., in the case of European options the critical point is at the strike), the rate of convergence can be much lower than is assumed by many academics and practitioners. This problem can resolve the smoothing of the payoff function, for example, by transforming the original payoff function into [15] for space step . The same remark is true for both the CRR method and the finite difference (FD) method [22, 23] (the reference method for numerical examples). The impact of smoothing the payoff function on numerical methods will not be further investigated in this paper, and therefore the smoothing techniques will not be used in numerical examples.

6 Numerical examples

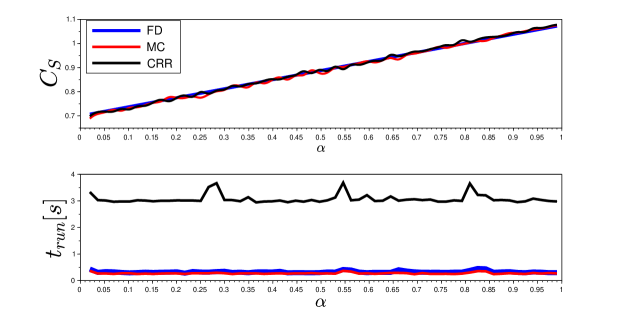

Let us focus on the -stable inverse subordinator. We compare the numerical methods for computing the prices of European call (), American put (), and European lookback call option () with floating strike (with the payoff function ) with regard to parameter for Figures 2 -4 respectively. We take , and for the FD method , , [22, 23]. For vanilla options, we choose as the reference FD method [22, 23], for the lookback option the Monte Carlo (MC) method explained in Appendix B. In Figure 2 a MC method introduced in [29] is also presented.

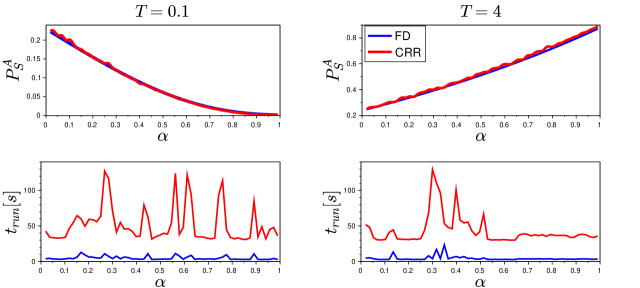

In Figure 2 all methods converge to the same result, but CRR is slower than the FD and MC methods. The parameters are , , . For FD, the number of time and space nodes are , , respectively. For CRR, the number of tree nodes . For MC and CRR, . In Figure 3 we compare CRR with the FD method introduced in [22]. Both methods match the real solution, but the CRR is significantly slower than the FD. It is worth mentioning that the CRR works clearly better than the Longstaff-Schwarz (L-S) method introduced in [28]. In contrast to L-S, the CRR method also works correctly for small values of and (see Figure in [22]). The parameters are , , , , , . To prepare the Figure 4, for each realization of we are looking for the minimum iteratively, as is proposed in [7]. The parameters are , , and for both methods . In Figures 2, 3 and 4 we see that CRR is the slowest/least precise presented numerical method (increasing and in each case follows getting closer to the real solution, but also increasing the time of computation). Note that the greatest advantage of the introduced binomial approach is that it can be applied to a wide range of options and inverse subordinators.

Conclusions

In this paper, we have introduced the subordinated CRR model. We have shown that in terms of convergence in the distribution and in Skorokhod space, of the underlying assets and convergence of many option prices (in both cases with respect to the number of nodes), this model is close to the subordinated B-S model. This is a generalization of the celebrated Cox-Ross-Rubinstein result [10] and gives motivation to approximate an option price in the subordinated B-S by the binomial MC method proposed in this paper. Furthermore, we have generalized the Schachermayer-Teichmann result [41] by providing the analytical relation between the prices of European options in the subordinated Bachelier and B-S models. As a supplement to the main course of the paper, we have also derived the PDE describing the price of the European call option in the subdiffusive Bachelier model, and we have presented the Monte Carlo method for valuing lookback options in the subordinated B-S model. Finally, we present some numerical examples.

Appendix A

Theorem 6.1.

Let be a fair price of the European lookback call option with floating strike in the B-S model, given by the semidirect formula [16]:

where , and is the CDF of the normal distribution. Then its subordinated equivalent is equal:

Moreover, if we consider the -stable inverse subordinator , then

where is given in terms of the Fox function (see [29] and the references therein).

Proof:

The proof is analogous to the proof of Theorem from [29].

Note that the analogical result can be obtained for other lookback options. The first statement provides an easy and fast numerical method, we only have to approximate the expected value by its finite equivalent. Therefore, we have

where () are independent realizations of and “” denotes an approximation (which reduces to the equality for ). Note that the Monte Carlo methods considered in this paper can be improved, e.g., using variance reduction techniques [48].

Acknowledgements

The research of G.K. and M.M. was partially supported by the NCN Sonata Bis 9 grant nr 2019/34/E/ST1/00360.

References

- [1] Moawia Alghalith. Pricing options under simultaneous stochastic volatility and jumps: A simple closed-form formula without numerical/computational methods. Physica A: Statistical Mechanics and its Applications, 540:123100, 2020.

- [2] Hazhir Aliahmadi, Mahsan Tavakoli-Kakhki, and Hamid Khaloozadeh. Option pricing under finite moment log stable process in a regulated market: A generalized fractional path integral formulation and monte carlo based simulation. Communications in Nonlinear Science and Numerical Simulation, 90:105345, 2020.

- [3] Louis Bachelier. Théorie de la spéculation. Annales scientifiques de l’Ecole normale supérieure, 17:21–86, 1900.

- [4] Fischer Black and Myron Scholes. The pricing of options and corporate liabilities. Journal of Political Economy, 81(3):637–654, may 1973.

- [5] Szymon Borak, Adam Misiorek, and Rafał Weron. Models for heavy-tailed asset returns. In Statistical tools for finance and insurance, pages 21–55. Springer, 2011.

- [6] Victor Chechkin, Aleksei Chechkin, et al. Edge fluctuation studies in heliotron j. Journal of Nuclear Materials, 337:332–336, 2005.

- [7] Terry Cheuk and Ton Vorst. Currency lookback options and observation frequency: a binomial approach. Journal of International Money and Finance, 16(2):173–187, 1997.

- [8] Julien Chevallier and Stéphane Goutte. On the estimation of regime-switching Lévy models. Studies in Nonlinear Dynamics & Econometrics, 21(1):3–29, 2017.

- [9] Rama Cont and Peter Tankov. Financial modelling with jump processes, Chapman & Hall/CRC Financ. Math. Ser, 2004.

- [10] John Cox, Stephen Ross, and Mark Rubinstein. Option pricing: A simplified approach. Journal of Financial Economics, 7(3):229–263, 1979.

- [11] Julia Di Nunno and Bernt Øksendal. Advanced mathematical methods for finance. Springer Science & Business Media, 2011.

- [12] Albert Einstein. Über die von der molekularkinetischen Theorie der Wärme geforderte bewegung von in ruhenden Flüssigkeiten suspendierten Teilchen. Annalen der Physik, 322(8):549–560, 1905.

- [13] Sergio Focardi and Frank Fabozzi. The mathematics of financial modeling and investment management, volume 138. John Wiley & Sons, 2004.

- [14] Vsevolod Gonchar, Aleksei Chechkin, Ed Sorokovoi, Victor Chechkin, Lyudmila Grigor’eva, and Evgeny Volkov. Stable Lévy distributions of the density and potential fluctuations in the edge plasma of the U-3M torsatron. Plasma Physics Reports, 29(5):380–390, 2003.

- [15] Steve Heston and Guofu Zhou. On the rate of convergence of discrete-time contingent claims. Mathematical Finance, 10(1):53–75, 2000.

- [16] Fabien Heuwelyckx. Convergence of European lookback options with floating strike in the binomial model. International Journal of Theoretical and Applied Finance, 17(04):1450025, 2014.

- [17] John Hull. Options futures and other derivatives. Pearson Education India, 2003.

- [18] Kiyosi Itô. On stochastic processes (i). Japanese Journal of Mathematics: Transactions and Abstracts, 18(0):261–301, 1941.

- [19] Aleksander Janicki and Aleksander Weron. Can one see -stable variables and processes? Statistical Science, pages 109–126, 1994.

- [20] G. Krzyżanowski and M. Magdziarz. A tempered subdiffusive Black-Scholes model. arXiv preprint 2103.13679, 2021.

- [21] Grzegorz Krzyżanowski. Selected applications of differential equations in Vanilla Options valuation. Mathematica Applicanda, 46(2), 2018.

- [22] Grzegorz Krzyżanowski and Marcin Magdziarz. A computational weighted finite difference method for American and barrier options in subdiffusive Black–Scholes model. Communications in Nonlinear Science and Numerical Simulation, 96:105676, 2021.

- [23] Grzegorz Krzyżanowski, Marcin Magdziarz, and Łukasz Płociniczak. A weighted finite difference method for subdiffusive Black–Scholes model. Computers & Mathematics with Applications, 80(5):653–670, 2020.

- [24] Solomon Kullback and Richard Leibler. On information and sufficiency. The annals of mathematical statistics, 22(1):79–86, 1951.

- [25] Paul Lévy. Processus Stochastiques et Mouvement Brownien. Suivi d’une note de M. Loève. Gauthier-Villars, Paris, 1948.

- [26] Sha Lin and Xin-Jiang He. A regime switching fractional Black–Scholes model and european option pricing. Communications in Nonlinear Science and Numerical Simulation, 85:105222, 2020.

- [27] Hsuan-Ku Liu and Jui-Jane Chang. A closed-form approximation for the fractional black–scholes model with transaction costs. Computers & Mathematics with Applications, 65(11):1719–1726, 2013.

- [28] Francis A Longstaff and Eduardo S Schwartz. Valuing american options by simulation: a simple least-squares approach. The review of financial studies, 14(1):113–147, 2001.

- [29] Marcin Magdziarz. Black-Scholes formula in subdiffusive regime. Journal of Statistical Physics, 136(3):553–564, 2009.

- [30] Marcin Magdziarz. Langevin picture of subdiffusion with infinitely divisible waiting times. Journal of Statistical Physics, 135(4):763–772, 2009.

- [31] Marcin Magdziarz and Janusz Gajda. Anomalous dynamics of Black-Scholes model time-changed by inverse subordinators. Acta Physica Polonica B, 43(5), 2012.

- [32] Marcin Magdziarz, Sebastian Orzeł, and Aleksander Weron. Option pricing in subdiffusive Bachelier model. Journal of Statistical Physics, 145(1):187, 2011.

- [33] Mark Meerschaert and Peter Straka. Inverse stable subordinators. Mathematical Modelling of Natural Phenomena, 8(2):1–16, 2013.

- [34] Mark M Meerschaert and Hans-Peter Scheffler. Triangular array limits for continuous time random walks. Stochastic processes and their applications, 118(9):1606–1633, 2008.

- [35] Robert Merton. Theory of rational option pricing. The Bell Journal of Economics and Management Science, 4:141–183, 1973.

- [36] Marek Musiela and Marek Rutkowski. Martingale methods in financial modeling, 1997. Stochastic Modelling and Applied Probability, 36, 1995.

- [37] Alexandra Piryatinska, Alexander Saichev, and Wojbor Woyczynski. Models of anomalous diffusion: the subdiffusive case. Physica A: Statistical Mechanics and its Applications, 349(3-4):375–420, 2005.

- [38] Svetlozar Rachev and Stefan Mittnik. Stable Paretian models in finance, volume 7. Wiley, 2000.

- [39] Paul Samuelson. Rational theory of warrant pricing. pages 195–232. Springer, 2015.

- [40] Ken-Iti Sato. Lévy processes and infinitely divisible distributions. Cambridge University Press, 1999.

- [41] Walter Schachermayer and Josef Teichmann. How close are the option pricing formulas of Bachelier and Black–Merton–Scholes? Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 18(1):155–170, 2008.

- [42] Marian Smoluchowski. Zur kinetischen Theorie der Brownschen Molekularbewegung und der Suspensionen. Annalen der Physik, 326(14):756–780, 1906.

- [43] Bart Stuck and Beat Kleiner. A statistical analysis of telephone noise. Bell System Technical Journal, 53(7):1263–1320, 1974.

- [44] Dina Tavares, Ricardo Almeida, and Delfim FM Torres. Caputo derivatives of fractional variable order: numerical approximations. Communications in Nonlinear Science and Numerical Simulation, 35:69–87, 2016.

- [45] Yingxu Tian and Haoyan Zhang. European option pricing under stochastic volatility jump-diffusion models with transaction cost. Computers & Mathematics with Applications, 79(9):2722–2741, 2020.

- [46] Ward Whitt. Stochastic-process limits: an introduction to stochastic-process limits and their application to queues. Space, 500:391–426, 2002.

- [47] Norbert Wiener. The average of an analytic functional and the Brownian movement. Proceedings of the National Academy of Sciences of the United States of America, 7(10):294–298, 1921.

- [48] Yunyu Zhang. The value of Monte Carlo model-based variance reduction technology in the pricing of financial derivatives. PloS one, 15(2):e0229737, 2020.

- [49] Fang Zhen and Jin E Zhang. Dissecting skewness under affine jump-diffusions. Studies in Nonlinear Dynamics & Econometrics, 24(4), 2020.