Robust Remanufacturing Planning with Parameter Uncertainty

Abstract

We consider the problem of remanufacturing planning in the presence of statistical estimation errors. Determining the optimal remanufacturing timing, first and foremost, requires modeling of the state transitions of a system. The estimation of these probabilities, however, often suffers from data inadequacy and is far from accurate, resulting in serious degradation in performance. To mitigate the impacts of the uncertainty in transition probabilities, we develop a novel data-driven modeling framework for remanufacturing planning in which decision makers can remain robust with respect to statistical estimation errors. We model the remanufacturing planning problem as a robust Markov decision process, and construct ambiguity sets that contain the true transition probability distributions with high confidence. We further establish structural properties of optimal robust policies and insights for remanufacturing planning. A computational study on the NASA turbofan engine shows that our data-driven decision framework consistently yields better worst-case performances and higher reliability of the performance guarantee.

Keywords: remanufacturing planning, robust Markov decision process, control-limit policy, data-driven solutions

1 Introduction

The manufacturing industry is a major consumer of materials and energy and imposes a significant impact on environment. Manufacturing activities are responsible for approximately 31% of the United States’ total energy usage and 19% of the world’s greenhouse gas emissions within the industrial sector (Diaz et al., 2010; Faludi et al., 2015). Sustainable manufacturing with improved environmental performance has drawn a great attention from governments, companies and scientific communities. In the past decade, remanufacturing has emerged as one of the critical elements for developing a sustainable manufacturing industry (Ijomah et al., 2007). Comparing to manufacturing a new product, remanufacturing can reduce up to 80% of energy consumption and carbon dioxide emissions (Sutherland et al., 2008), and 40-65% of manufacturing costs (Shi and Min, 2014; Ford and Despeisse, 2016). The proceedings of the G7 Alliance on Resource Efficiency noted remanufacturing as one of the most important drivers for getting to a closed-loop economy and improving resource efficiency (EPA, 2016). The growing remanufacturing industry has become an important economic force in the United States with a well-developed market estimated at $53 billion per year (Lund and Hauser, 2012). Many products, especially the ones with long lifespans such as turbine blades and automobile parts (e.g., engines, water pumps), are now routinely remanufactured at the near-end of their life cycles and returned to service (Dulman and Gupta, 2018; Seitz, 2007).

Remanufacturing is an industrial process whereby used or broken-down products (or components), referred to as “cores”, are restored to a like-new condition with an extended lifetime (Östlin et al., 2009). During this process, the cores pass through a number of operations including inspection, dismantling, part reprocessing, repair, replacement and reassembly. The performance of the remanufactured cores is expected to meet the desired product standards similar to the original product. Remanufacturing is distinctly different from related activities, such as reuse, repair, and recycling (Skrainka, 2012; Lund and Hauser, 2012). A product is reused when it has not completed its life-cycle and the user decides to stop its use, and a consumer sector is willing to accept it in its current use state, perhaps to its original purpose. Repair fixes what is broken or worn with no attempt to fully restore the product to a like-new condition or to a new life. Recycling recovers materials at the end of the product life, returning them into the use stream. Recycling a complex product (e.g., car), however, can result in a loss of up to 95 percent of the value-added content (e.g., labor, energy) (Giuntini and Gaudette, 2001), in addition to the loss of all functionality of the original product. By reclaiming the material content and retaining the embodied energy and labors used for manufacturing the original product, remanufacturing is a more efficient means of resource recirculation than these related activities.

Current remanufacturing practices mainly consider end-of-life products. Such a reactive approach has a number of drawbacks (Sutherland et al., 2008; Song et al., 2015). First, for many products, remanufacturability is significantly reduced due to no adequate techniques to remanufacture retired products. Second, remanufacturing costs often increase significantly towards the end of a product’s life cycle. Third, substantial negative environmental effects are usually generated because much higher energy and material consumption is required for remanufacturing due to heavy damage at the end of a product’s life. Several studies have shown that in some cases, remanufacturing actually consumes more energy than manufacturing a new product (Chandler, 2011; Gutowski et al., 2011). It is paramount that decision makers make informed decisions on the timing of remanufacturing and ensure it is conducted when it is worth the effort.

The robustness of the remanufacturing planning decisions, however, can be threatened by data inadequacy. Since the optimal decision involves suggesting the optimal action, such as no intervention, remanufacturing, or scrapping, at different states (conditions), it is first and foremost to estimate the transition dynamics of a component. The estimation often faces a great challenge because of limited field data. The situation may be further exacerbated as the field data typically contain a large amount of noises and incorrect information. This data inadequacy poses a critical question to decision makers: How does uncertainty in model parameters translate into uncertainty in the performance of interest? The decision makers must assess whether any observed nominal improvement in the environmental and economic effects resulted from remanufacturing at certain states is likely to be a true improvement, suggesting remanufacturing in those states, or conversely, a consequence of the parameter uncertainties due to statistical estimation errors, favoring remanufacturing when it causes negative effects.

Several studies attempted to address the impacts of the uncertainty in model parameters. It has been shown that when the parameter uncertainty—the deviation of the model parameters from the true ones, is largely ignored, the optimal policy can lead to serious degradation in performance, because the optimal policy in sequential decision making is quite sensitive to parameter uncertainty, particularly perturbations in the transition probability (Mannor et al., 2007; Iyengar, 2005; Xu et al., 2012). Therefore, with a tacit understanding that the state transition dynamics of a component has to be estimated from historical data in practice, remanufacturing planning is confronted with the external uncertainty due to the deviation of the estimates from their true values in addition to the internal uncertainty due to the stochastic nature of a component’s condition evolution. To address both internal and external variations and prescribe robust remanufacturing policies, we formulate the remanufacturing planning problem as a robust Markov decision process (RMDP). We investigate the structural properties of the robust remanufacturing policies in the presence of statistical estimation errors. We further conduct a computational study based on the operational dataset of the turbofan engine operated by NASA (Frederick et al., 2007). The main contribution of this paper is threefold.

-

•

Provide a novel data-driven modeling framework for remanufacturing planning in which decision makers can remain robust with respect to statistical estimation errors in transition dynamics.

-

•

Establish structural properties of optimal robust policies and provide insights for decision making in remanufacturing planning in the presence of parameter uncertainties. Our findings also make contributions to the robust Markov decision process literature in which few papers have focused on characterizing the structure of the optimal robust policy.

-

•

Conduct computational studies to demonstrate the optimal robust policies, investigate the out-of-sample performance of the resulting optimal robust remanufacturing policies, and derive data-driven solutions to improve the out-of-sample performance.

The remainder of this paper is organized as follows. Section 2 reviews relevant literature on remanufacturing planning and sequential decision making with parameter uncertainty. In Section 3, we formulate the remanufacturing planning problem as a RMDP. Section 4 establishes conditions to ensure the optimal robust policies are of control-limit type. In Section 5, we present a computational study using simulated operational data of NASA’s turbofan engines. Section 6 concludes this study and suggests future research directions.

2 Literature Review

Our study is related to two streams of the literature: remanufacturing planning and sequential decision-making with parameter uncertainty.

2.1 Remanufacturing Planning

The management of remanufcturing production and control activities greatly differs from management activities in traditional manufacturing. Production planning and control activities are more complex for remanufacturing firms due to complicating characteristics such as the uncertain timing and quantity of returns (Guide Jr, 2000). The majority of literature in remanufacturing operational management focus on production planning and control activities, such as reverse logistic management, balancing returns and demands, and inventory control. Van Der Laan et al. (1999) consider production planning and inventory control in systems where manufacturing and remanufacturing operations occur simultaneously. Savaskan et al. (2004) identify and model three close-loop supply chains to address the problem of choosing the appropriate reverse channel structure for the collection of used products. Galbreth and Blackburn (2010) study the optimal core acquisition quantity problem subject to the uncertainty of core conditions. We refer the readers to a review (Govindan et al., 2015) and the papers therein for more research works relevant to reverse logistics and closed-loop suply chain.

Remanufacturing planning, while being recognized, has received little attentions. Existing works on remanufacturing timing decisions often either ignore both types of uncertainties in transition dynamics of a remanufacturing system or only focus on the internal variation. For example, Song et al. (2015) determine remanufacturing timing based on a deterministic degradation process charaterized by residual strength factors. Wang et al. (2016) recommend remanufacturing based on online monitoring: Products are remanufactured when it reaches the limit condition beyond which the product is no longer remanufacturable. External variation is largely ignored, and hence, remanufacturing could be blindly suggested even if it might lead to increased negative environmental or economic impacts, resulting in the robustness of remanufacturing planning decisions in question.

Remanufacturing planning bears a close resemblance to maintenance planning which aims to determine the optimal timing of preventive maintenance. In this paper, we use Markov models for remanufacturing planning; the most relevant works in maintenance optimization literature are the ones that model maintenance problems using a Markov decision process (e.g., Kurt and Kharoufeh (2010), Elwany et al. (2011), Kim and Makis (2013)). Most maintenance optimization models that are formulated as a Markov decision process (MDP), however, assume that the cost parameters and the transition kernel are known, and hence, cannot provide satisfactory out-of-sample performances when future realizations deviate from the predicted ones. One of the few papers that consider ambiguity in transition probabilities is by Kim (2016). In his paper, Kim (2016) considers a failing system whose underlying state is unobservable and accounts uncertainties in both posterior distributions and transition probabilities. The optimization of an ambiguous partially observable MDP (APOMDP) is generally challenging even for small state spaces. For remanufacturing planning, the state space would become large, rendering the optimization of the resulting APOMDP computationally prohibitive.

2.2 Sequential Decision-Making with Parameter Uncertainty

Conventional MDP assumes that the transition probabilities and rewards can be estimated confidently and focuses solely on the uncertainty stemming from the stochastic nature of MDPs. In practice, however, estimating the true transition probabilities is difficult, if not impossible, because of the limited data availability or inevitable statistical errors or both. When parameters deviate from the true ones and such uncertainty is ignored, the optimal policy can lead to serious inferior performance, because the optimal policy in sequential decision making is quite sensitive to parameter uncertainty, particularly deviations in the transition probability (Mannor et al., 2007; Iyengar, 2005; Xu et al., 2012).

Early works on the MDPs with parameter uncertainties, including Silver (1963); Satia and Lave Jr (1973); White III and El-Deib (1986) and White III and Eldeib (1994), formulate the uncertainty in either a game-theoretic or Bayesian approach. In the game-theoretic formulation, it is assumed that the uncertainty about the transition probabilities is encoded by describing the set of all transition probability rows. Hence, when the decision maker makes a decision for a given state, the nature selects a transition probability row from the set to minimize the reward. Satia and Lave Jr (1973) use the game-theoretic formulation to model the transition uncertainty in MDP and proposed a policy iteration procedure to solve the problem. White III and Eldeib (1994) further develop a modified policy iteration-based algorithm for the MDP with imprecise transition probabilities. The Bayesian approach, first introduced by Silver (1963), assumes a known priori probability distribution of each transition probability row. Hence, the transition probabilities can be updated along the Bellman’s equations. Dirichlet priors are a common choice of modeling the uncertainty in transition probabilities (Delage and Mannor, 2010).

Most of the early contributions, however, do not concern the construction of ambiguity sets. Inspired by the data-driven approaches, recent RMDP works (Iyengar, 2005; Nilim and El Ghaoui, 2005; Wiesemann et al., 2013) have developed various methods to construct the uncertainty set of transition probabilities that contain the true transition probabilities with high confidence. Many statistical methods, such as likelihood constraints, deviation-type constraints and distance metrics (e.g., Wasserstein ball, divergence balls), have been applied to construct an uncertainty set of transition probabilities with historical samples (Iyengar, 2005; Nilim and El Ghaoui, 2005; Wiesemann et al., 2013). Reformulation of RMDPs with different types of ambiguity sets and the corresponding tractability have also been studied in the literature. Compared to the theoretical orientation of these works, our present work focuses more narrowly on developing methods for a specific problem class, establishing structural properties of optimal robust policies, and providing executable insights.

3 Robust Remanufacturing Planning Problem

Consider remanufacturing planning of a single-unit system that degrades during its operation. Because we focus on single-unit systems, the words system and component are used interchangeably throughout the paper. The component is inspected at equally spaced discrete time epochs . Let be the state space, where represents the set of conditions and represents the set of cumulative numbers of completed remanufacturing activities. Note that a larger state denotes a worse condition and the worst state is an absorting state, meaning the systems stays there if there is no intervention. At each epoch, a decision maker oberves the state of the component and then chooses an action from the set , where 0 means continuing operation to the next observation time, 1 means remanufacturing, which takes one period, and 2 means scraping the component.

The most important objective of remanufacturing is to minimize the negative environmental impacts while sustaining profitable growth. The direct environmental impacts of a manufactured/remanufactured system are often measured by greenhouse gas emissions (e.g., CO2, CH4, N2O, etc.) using life cycle assessment (LCA). LCA is a technique that compiles an inventory of relevant energy consumption and material inputs and environmental releases, and then evaluates the potential environmental impacts associated with identified inputs and releases (Curran, 2011). Such an evaluation can be done using published databases (e.g., EcoScan) or commercial softwares (e.g., GaBi) if the system is complicated. There are several types of LCA. For instance, cradle-to-grave is the assessment of a full product life cycle from resource extraction (“cradle”) to use phase and disposal phase (“grave”), cradle-to-gate is an assessment of a partial product life cycle from resource extraction to the factory gate (i.e., before it transported to the consumer), and gate-to-gate, also a partial LCA, evaluates the eco-burden of a manufacturing facility. In this paper, rather than model different types of greenhouse gas emissions and formulate a multi-objective problem, we model the environmental impacts using carbon cost, which is determined by the amount of carbon emissions and the carbon price. As carbon trading increasingly recognized as one of the most effective approaches to incentivising companies to become environmental friendly (Abdallah et al., 2012) and more carbon trading systems established around the world, remanufacturing planning models that consider the carbon costs will become more relevant and applicable.

To model the profit of a remanufacturing system, we assume that during each decision period, the decision maker receives a gain (e.g., production revenue) if operation is not interrupted and incurs some environmental costs . The reward of keeping operation in one period is thus denoted by . If the decision is to remanufacture the component, a remanufacturing cost , which comprises the manufacturing and carbon costs, is incurred. If the system is scrapped, a salvage value is received. We assume that and are the same regardless of a component’s condition.

Although remanufactuirng is supposed to restore a component to like-new conditions, each remanufacturing process typically makes the component less resistant to deterioration. Hence, a component’s deterioration process depends on the cumulative number of completed remanufacturing activities, which is modeled as follows. For a system that has been remanufactured times, let denote the transition probability matrix when the decision is to wait. Note that remanufacturing brings the system status to an as-good-as-new condition, but increments the cumulative number of remanufacturings by one. We assume that the deterioration process is irreversible, and hence is an upper triangular matrix. Due to limited data availability and statistical estimation errors, the transition probability of a remanufacturing system is fundamentally unknown. To mitigate the effects of uncertain transition probabilities, we assume that the true transition kernel is contained in an ambiguity set.

Next, we present an important assumption regarding the ambiguity set, which ensures deterministic and Markovian policies (Iyengar, 2005).

Assumption 1 (Rectangularity).

An RMDP problem has a rectangular ambiguity set if the ambiguity set has the form where stands for the Cartesian product, and is the projection of onto the parameters of state .

The implications of the rectangularity assumption is often interpreted in an adversarial setting (Iyengar, 2005; Nilim and El Ghaoui, 2005): The decision maker first chooses a policy . Then an adversary observes , and chooses a distribution that minimizes the reward. In this context, rectangularity is a form of an independence assumption: The choice of a particular distribution for a given state does not limit the choices of the adversary of other states. There are two possible models for transition matrix uncertainty. In the first model, referred to as the stationary uncertianty model, the transition matrices chosen by the adversary depending on the policy once and for all, and remain fixed thereafter. In the second model, referred to as the time-varying uncertainty model, the transition matrices can vary arbitrarily with time, within their prescribed bounds. It has been shown in Nilim and El Ghaoui (2005) that for a finite horizon problem with a discounted cost function, the gap between the optimal value of the stationary uncertainty problem and that of its time-varying counterpart goes to zero as the horizon length goes to infinity. In this paper, we consider the stationary worst-case distribution, that is, the choices of are the same every time the state is encountered. Note that there is no ambiguity in transitions in the period during which remanufacturing is conducted, since remanufacturing takes one period and there is no transition in that period. Because the optimal robust policies of the remanufacturing planning are Markovian and deterministic under the rectangularity assumption, we have the robust remanufacturing planning optimization model in the following recursive form:

| (RRmPO) |

where

3.1 Construction of Ambiguity Sets

As mentioned in the introduction, the motivation for the robust methodology is the presence of the statistical errors associated with estimating the transition probabilities using historical data. A natural choice for the ambiguity set is the confidence regions associated with density estimation. We thus use the Kullback-Leibler (KL) distance to construct the ambiguity set around the empirical transition probabilities. Bootstrap resampling, a common non-parametric method to address the uncertainty, is also used to construct confidence intervals of estimators.

An important property of the ambiguity set constructed using these two methods is that it cannot pop a scenario while allows scenario suppression. A scenario that never occurs in the nominal problem cannot have a positive probability (or, “pop”) in the ambiguous problems. Such a property ensured that the assumption of no-self-improving in system’s deterioration is held in the ambiguous problem. More importantly, the ambiguity sets constructed using these two methods are convex, and hence leads to a computational tractable problem. In addition, the KL distance and bootstrapping are already being used in statistics, making them attractive to deal with data directly.

KL Distance. In a data-driven setting, the empirical distribution typically serves as the nominal distribution. For notational convenience, we drop the notations of and . Let be the maximum likelihood estimator of given a state :

| (1) |

where is the number of transitions from state to . The KL distance between and is defined as

| (2) |

It is obvious that with equality holds when . Given a state , the KL-distance-based ambiguity set is given by

| (3) |

Let . It has been shown that the normalized estimated KL-distance asymptotically follows a distribution (see more details in Ben-Tal et al. (2013)). We thus have the following (approximate) (1-)-confidence set around

| (4) |

where .

Bootstrap Resampling. Let be realizations of the Markov chain with transition matrix and be the maximum likelihood estimator of based on the observed data . For a large number of statistics of interest, the bootstrap distribution approximates the sampling distribution (i.e., asymptotic normality of where is the bootstrap estimator of ). From the bootstrap distribution, one can assess the uncertainty of each probability in the transition matrix and construct the confidence interval for each probability. The bootstrap distribution can be calculated by direct theoretical calculation, which draws samples with replacement, or Monte Carlo approximation. The reader is referred to Efron and Tibshirani (1994) for more detailed bootstrapping procedures. Note that the ambiguity set constructed by bootstrap resampling has the same form of the ambiguity set constructed using the interval matrix method in Nilim and El Ghaoui (2005). Therefore, we also refer to the method of constructing ambiguity sets using bootstrap sampling as the interval matrix method hereinafter since it better describes the form of the ambiguity sets.

4 Structure of the Optimal Robust Policy

In this section, we investigate the structural properties of the optimal robust remanufacturing policies. We will focus our attention on control-limit policies. We establish sufficient conditions that ensure the existence of monotonically control-limit policies. The optimality of such structured policies is important because they are appealing to decision makers and enables efficient computation and are easy to implement. Our analysis will make significant use of the notion of the stochastic dominance, which helps establish stochastic dominance relationships for transition behaviors. Below, we define some stochastic order concepts that are used in our analysis.

Definition 1.

-

(a)

A transition probability matrix is said to be IFR (increasing failure rate) if is non-decreasing in for all .

-

(b)

For two transition probability matrices and , we say dominates , , if for all .

Assumption 2.

Let denote the nominal transition probability matrix for a system that has been remanufactured times,

-

(a)

is IFR for all .

-

(b)

for all .

Assumption 2(a) implies that, given the cumulative number of completed remanufacturing activities , the system in a worse state at the current epoch is more likely than the other to be found in a worse condition at the next epoch. Assumption 2(b) imposes a first-order stochastic dominance relationship among the system’s deterioration matrices corresponding to different remanufacturing histories. More explicitly, given two systems with the same condition but different remanufacturing histories, the system with a larger is more likely to get worse than the other during operation. Additional assumption is made regarding the operational gains, environmental costs, and the salvage value.

Assumption 3.

-

(a)

The operational gain is non-increasing in and , and the carbon cost is non-decreasing in and ;

-

(b)

The reward at state , the salvage value and the discount factor satisfy the following condition: .

Assumption 3(a) implies that as the number of completed remanufacturing activities increases and its condition worsens, the gain decreases and the carbon cost increases. For example, an engine in a worse state usually incurs higher maintenance costs and consumes more gasoline or electricity. Assumption 3(b) ensures that the decision of no intervention (i.e., ) is excluded when a system is at the worst state for all because it is not practical that the system stays in the worst condition for an infinitely long time. This unrealistic scenario is eliminated by assuming that the total expected reward from doing nothing at state , computed as , is less than the salvage value. Since for all , the condition also eliminates the no-intervention option for state for all .

4.1 Remanufacturing Planning with KL-Distance-Based Ambiguity Sets

In this section, we consider Model (RRmPO) with KL-distance-based ambiguity sets. We provide reformulations and establish conditions that ensure control-limit type policies. We first reduce the bi-level problem (RRmPO) to a single-level problem by applying the Langurangian dual theory, and then investigate the structure of the robust value function, which is necessary for establishing control-limit robust remanufacturing planning policies.

Proposition 1.

Proof.

See Appendix A.1. ∎

Proposition 2.

For Model (RRmPO) with ambiguity sets constructed using the KL distance, the value function is non-increasing in and .

Proof.

See Appendix A.2. ∎

Next, we establish conditions that ensure control-limit robust policy structures, that is, the remanufacturing decisions are of control-limit type with respect to the condition of the system and the cumulative number of completed remanufacturing activities.

Theorem 1.

For Model (RRmPO) with KL-distance-based ambiguity sets, there exists a cumulative number of completed remanufacturing activities , and an operational state such that for

and for

Proof.

See Appendix A.3. ∎

Theorem 1 shows that for a system that has , the optimal decision is either wait until the next period or remanufacture, and the system is remanufactured when the condition is equal to or exceeds a limit. When the cumulative number of completed remanufacturing activities reaches the threshold , the optimal decision is either wait until the next period or scrap and there exists a scrapping threshold. This implies that despite the cost savings and environmental benefits that make remanufacturing appealing, remanufacturing activity is not recommended after being conducted certain number of times. Note that is a special case that remanufacturing is not optimal for all . Let denote the control limit for and denote the the control limit for . We further examine the structure of and in the next theorem.

Theorem 2.

Consider Model (RRmPO) with the KL-distance-based ambiguity sets. Then, the following holds:

-

(a)

If , is non-increasing in .

-

(b)

is non-increasing in .

Proof.

See Appendix A.4. ∎

The condition in Theorem 2(a) is restrictive. We will show that most violations do not change the monotone structure of and in Section 5.4.1 through some computational studies.

4.1.1 Solution Methodology for KL Distance Model

Model (RRmPO) can be efficiently solved using robust value iteration as described below:

To solve the inner problem in step 5, we can either employ a numerical search for the dual problem in Equation (5), or solve the primal problem as the following conic program:

| (7) |

where constraint (7) can be represented by the following exponential cone:

where is the exponential cone in .

4.2 Remanufacturing Planning with Interval-Matrix-Based Ambiguity Sets

In this section, we establish conditions that guarantee structural properties of the optimal robust policies of Model (RRmPO) with ambiguity sets constructed using the interval matrix model. The interval matrix model describes the uncertainty on the rows of the transition matrices in the form . Note that since components in each row vector of a transition matrix are constrained by , more effective lower and upper bounds of the transition probability of each state can be obtained. The effective upper bounds are

| (8) |

and the effective lower bounds are

| (9) |

The upper and lower bounds hereinafter are referred to the bounds defined in Equations (8) and (9). We first establish conditions that ensure the value function is monotone and the worst-case transition matrices are IFR, and then examine the structures of the robust optimal remanufacturing planning policies.

Proposition 3.

Consider Model (RRmPO) with the ambiguity set constructed using the interval matrix model.

-

(a)

If the lower and upper bounds of all states satisfy the following conditions,

(10) (11) then the value function is non-increasing in for all .

- (b)

Proof.

See Appendix A.5. ∎

Proposition 3 provides a set of conditions sufficient to guarantee the structure of the value function and the worst-case transition matrices, which are critical to the existence of control-limit robust optimal policies. These conditions are generally not restrictive, and are expected to be roughly satisfied. Conditions (10) and (11) ensure that the worst case transition matrices are IFR, and conditions (12) and (13) guarantee that the worst transition matrix dominates the worst transition matrix for all .

In the proof of Proposition 3, we also obtain the transition behaviors of worst-case transition probability matrices when the decision is to wait, which are summarized in the following corollaries.

Corollary 1.

Proof.

See Appendix A.6. ∎

Let denote the worst-case transition matrices in Corollary 1. Corollary 2 summarizes the structure of .

Corollary 2.

is IFR for all ; if (), .

Next we show that similar to optimal robust remanufacturing policies for model with KL-distance-based ambiguity sets, the optimal robust policies for model with interval-matrix-based ambiguity sets exhibit the same control-limit structure with respect to and under some conditions.

Theorem 3.

Proof.

See Appendix A.7. ∎

Theorem 4.

Proof.

See Appendix A.8. ∎

4.2.1 Solution Methodology for Interval Matrix Model

Model (RRmPO) with the ambiguity set constructed using the interval matrix model can be efficiently solved by the robust value iteration algorithm in Section 4.1.1, where the dual problem of the inner problem is give by:

where . Since this dual problem is piecewise linear on with break points , , the optimality is obtained at one of the break points. Suppose for . Then, the complementary slackness suggests if , if , and . Corollary 1 follows when is non-increasing in for any given .

4.3 Sensitivity Analysis

Consider two problem instances ( and ) with ambiguity sets constructed using the KL distance or the interval matrix model. Assume that these two problem instances satisfy the following: (1) reward functions are the same, (2) the ambiguity set of problem is contained in its counterpart of problem (i.e, ), and (3) all conditions that are needed to ensure the control-limit structure of the optimal robust policies are satisfied. Theorem 5 addresses the relationship between the optimal robust policies of these two systems. Let and denote the remanufacturing and scrap limits of problem given , respectively. Let be the same threshold defined in Theorems 1 and 3. We show that given , the remanufacturing thereshold in problem , is higher than or the same as its counter part in problem . In contrast, problem has a higher scrap control limit given . This shows that a decision maker needs to be more conservative about initiating a remanufacturing process in anticipation of more transition uncertainties and that decision makers should consider scrapping early to receive the terminal rewards, to hedge against uncertainties in future operational gains. We summarize our results in the following theorem.

Theorem 5.

Let and be two problem instances defined in this section. Then, the following holds.

-

(a)

for , if , where .

-

(b)

for ,

-

(c)

.

Suppose that a decision maker has problem implemented and is aware of its optimal robust policy. Theorem 5 offers valuable insights on the optimal policy if the decision maker decides to be more conservative by considering a larger ambiguity set. It is worth noting that if the system does not allow self-transition, i.e., for all , then Theorem 5 holds.

5 Computational Study

5.1 System Model Description

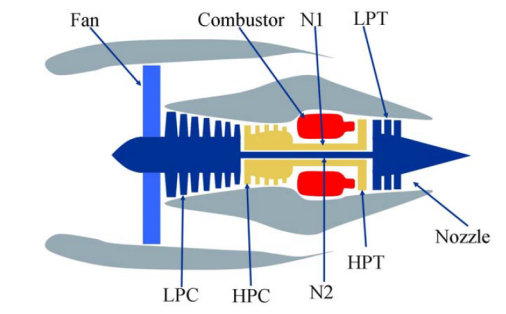

Real-world turbofan engine operating data acquired from sensors are used to demonstrate our robust remanufacturing planning model. Procuring actual turbofan engine system fault progression data is typically time consuming and expensive. Hence, we use the data simulated using the Commercial Modular Aero-Propulsion System Simulation (C-MAPSS) software (Frederick et al., 2007) developed at NASA to demonstrate our robust remanufacturing planning model and examine the performance of the optimal robust remanufacturing policies. The C-MAPSS engine is a 90,000 lb thrust class turbofan engine and has five rotating components: fan, low prpessure compressor(LPC), high pressure compressor(HPC), high pressure turbine(HPT), and low pressure turbine(LPT). The engine diagram in Figure 1 shows the main elements of the engine model (Saxena et al., 2008).

The overall simulation is implemented in the MATLAB and Simulink environment, providing flexible interaction with the software user. C-MAPSS offers 14 inputs and can produce several outputs for analysis. The system inputs include fuel flow, deviation from scheduled variable stator vanes angle, deviation from scheduled variable bleed valve position, and a set of 13 health parameters (e.g., Fan efficiency modifier, LPC flow modifier, HPC pressure-ratio modifier) that consist of flow, efficiency, and pressure-ratio modifiers for the fan, LPC, and HPC, and flow and efficiency modifiers for the HPT and LPT. Advanced users can readily modify and customize the model to their specific requirements to simulate the deterioration in any of the engine’s five rotating components. The outputs include various sensor response surfaces and operability margins. The total of 21 outputs are summarized in Table 1.

| Symbol | Description | Units |

|---|---|---|

| T2 | Total temperature at fan inlet | ∘R |

| T24 | Total temperature at LPC outlet | ∘R |

| T30 | Total temperature at HPC outlet | ∘R |

| T50 | Total temperature at LPT outlet | ∘R |

| P2 | Pressure at fan inlet | psia |

| P15 | Total pressure in bypass-duct | psia |

| P30 | Total pressure at HPC outlet | psia |

| Nf | Physical fan speed | rpm |

| Nc | Physical core speed | rpm |

| epr | Engine pressure ratio (P50/P2) | - |

| Ps30 | Static pressure at HPC outlet | psia |

| phi | Ratio of fuel flow to Ps30 | pps/psi |

| NRf | Corrected fan speed | rpm |

| NRc | Corrected core speed | rpm |

| BPR | Bypass Ratio | - |

| farB | Burner fuel-air ratio | - |

| htBleed | Bleed Enthalpy | - |

| Nf_dmd | Demanded fan speed | rpm |

| PCNfR_dm | Demanded corrected fan speed | rpm |

| W31 | HPT coolant bleed | lbm/s |

| W32 | LPT coolant bleed | lbm/s |

5.2 Dataset Description

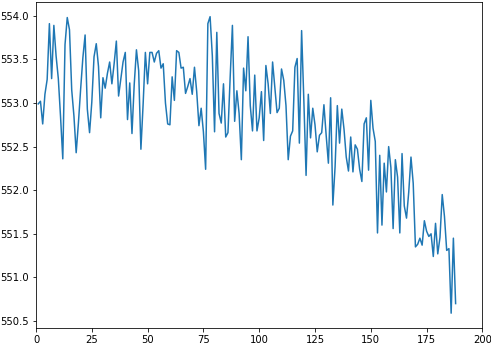

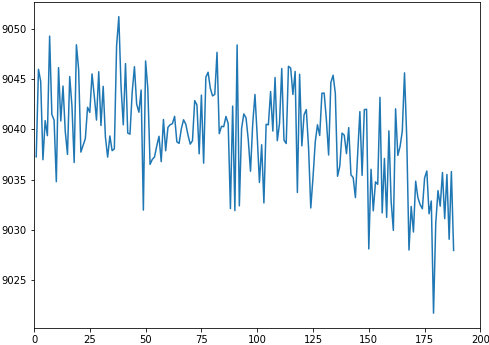

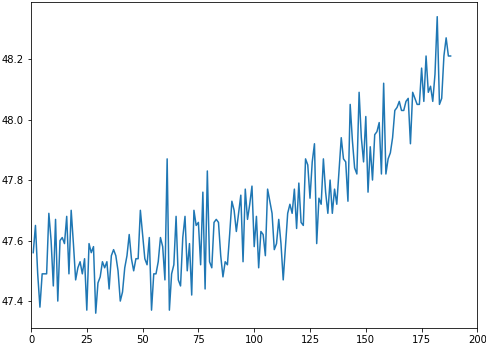

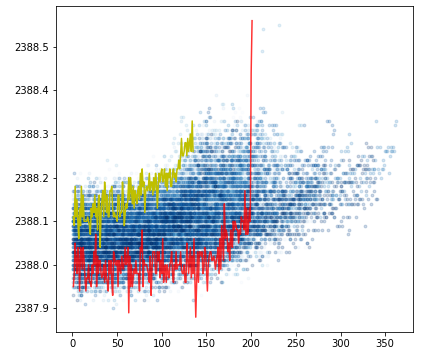

We consider the data pertaining to a single failure mode and a single operating condition. The dataset considered in this work consists of 100 units which are run to failure. Note that end-of-life can be subjectively determined as a function of operational thresholds that can be measured; these thresholds depend on user specifications to determine safe operational limits. For illustration purposes, we arbitrarily choose four features and plot the time series of these features for a randomly selected unit and all units (Figure 2).

From Figure 2, we can see that the data contains a lot of noises. Various sources can contribute to noises, and the main sources of noise are manufacturing and assembly variations, process noise, and measurement noise to name a few important ones (Saxena et al., 2008). Due to the large amount of noises and limited real-world operational data available, there often exists a high level of uncertainties in transition probabilities of the turbofan engines, and operators and manufacturers are in great need of robust remanufacturing planning.

5.3 Parameter Estimation

It is typically desirable to reduce the dimensionality of the data and reconstruct them from a lower dimensional samples. We therefore use the principal component analysis method to compress the high-dimensional sensor outputs and use the first principle component that accounts for the largest variability of data as the system health indicator. We further discretize the obtained health indicator into 7 intervals, representing 7 condition states, as recommended by Moghaddass and Zuo (2014). The -means method is used to partition health indicators. The nominal transition probability is estimated using the maximum likelihood method, i.e., , where is the number of transitions from state to for unit , and is the total number of units in a sample. We construct the ambiguity sets as described in Section 3.1. Note that when constructing interval-matrix-based ambiguity sets, 30 bootstrap samples are used. Based on discussions with researchers and field engineers, an engine typically lose about 7% useful life each time it is remanufactured. We modify the nominal transition probability matrix obtained for new turbonfan engines (i.e., ) to reflect such a loss for . For all the following experiments, the nominal transitional probability matrices satisfy Assumption 2, and the lower and upper bounds of transition probabilities satisfy conditions (10) to (13).

5.4 Experiments

Next, we demonstrate the structure of the optimal robust remanufacturing policy and examine the out-of-sample performance of the optimal robust policies. The following cost data is used for all experiments in this section: and . The discount factor is 0.9 for all following experiments.

5.4.1 Policy Structures

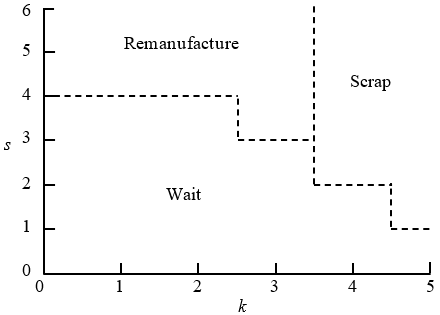

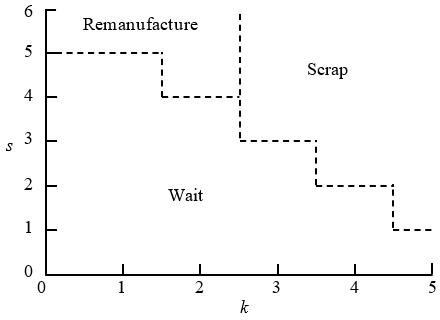

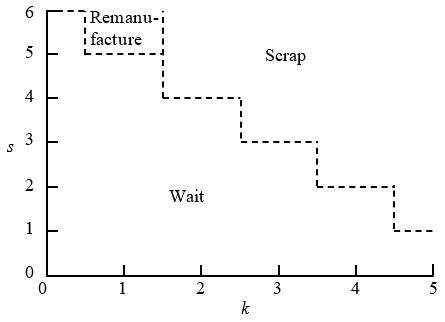

We have established conditions to ensure control-limit policies for Model (RRmPO) with ambiguity sets constructed using the KL distance or the interval matrix method. For illustration purposes, we show the structure of optimal robust policies for Model (RRmPO) with KL-distance-based ambiguity sets.

As Figure 3 shows, the remanufacturing policies exhibit control-limit structure. We can also see that as increases, the remanufacturing threshold increases and decreases (i.e., the scrap is performed earlier). This implies that when parameter uncertainty is large, a decision maker needs to be cautious about remanufacturing used products and to consider scrapping at an earlier stage. This is because (1) the remanufacturing cost may not be offset by the subsequent operational gains due to large parameter uncertainties and (2) securing the fixed salvage value better hedges against uncertainties in future gains.

As stated earlier, the condition of Theorem 2(a), which is the same as the condition of Theorem 4, is restrictive and difficult to satisfy. We further examine whether the optimal robust policies are still of control-limit type when this condition is violated. We test a total of 5000 instances and the generation of the test instances is described in Appendix B.1. Out of the 3060 test instances that violate the condition of Theorem 2(a), only 209 (i.e., approximately 6.8%) instances violate the monotone structure. Therefore, we believe that a control-limit policy with respect to can be obtained in most practical cases even when the condition that guarantees it is violated.

5.4.2 Impact of the Parameter Uncertianty

We first conduct experiments to investigate the impact of the parameter uncertainty on the out-of-sample performance. The radius determines the size of the KL-distance-based ambiguity set and the confidence level determines the size of the ambiguity set constructed using bootstrap resampling. For notational convenience, we use to denote the hyperparameter that controls the size of the ambiguity set.

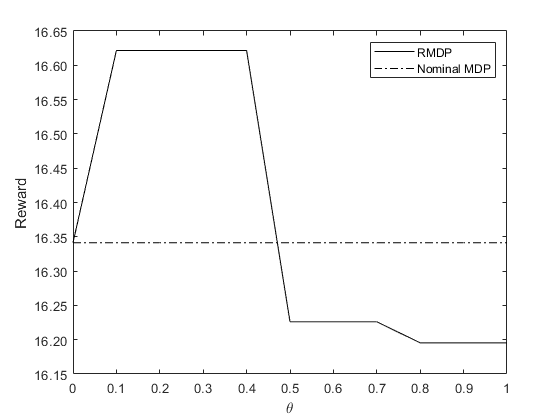

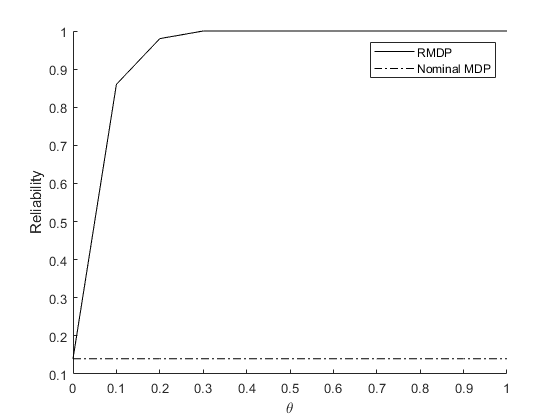

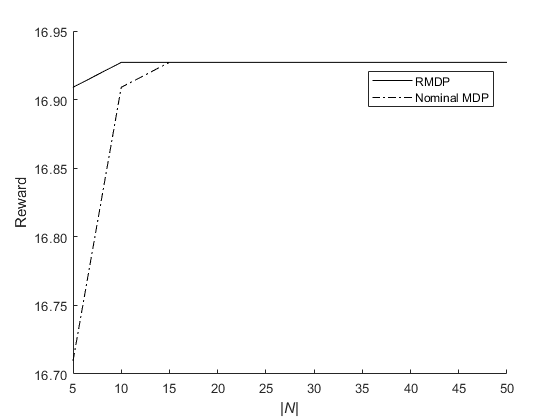

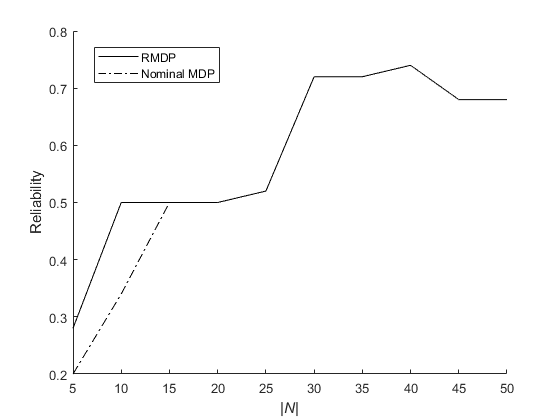

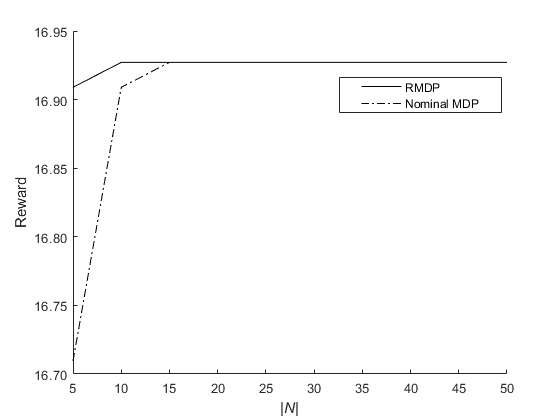

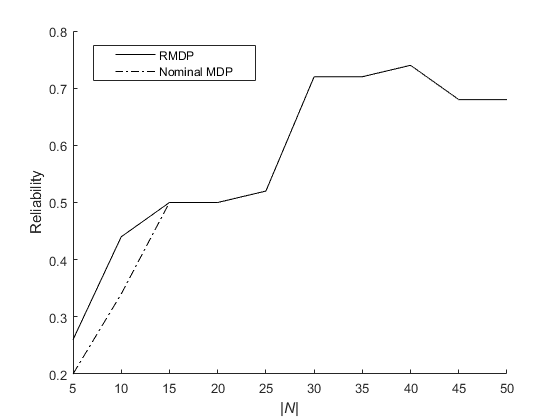

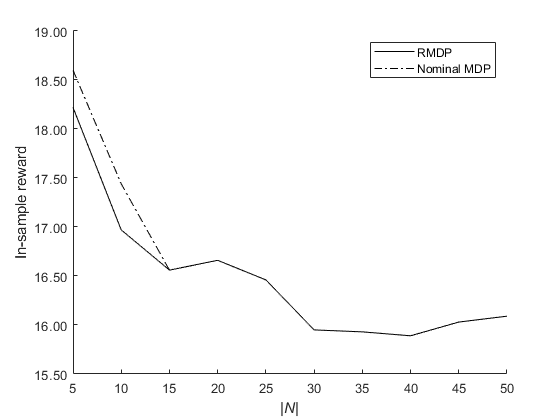

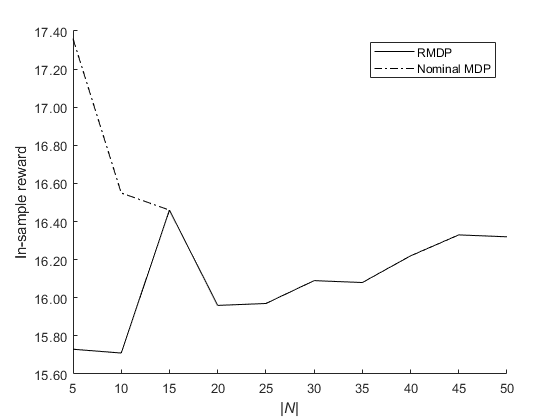

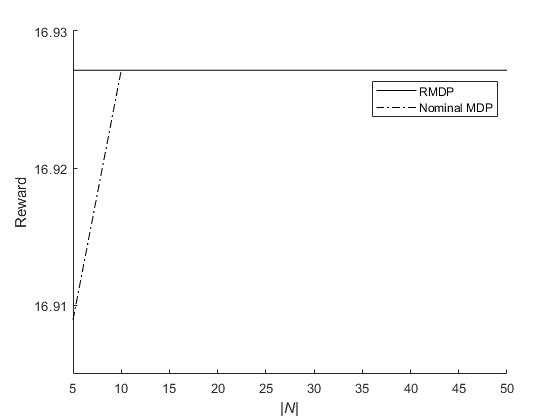

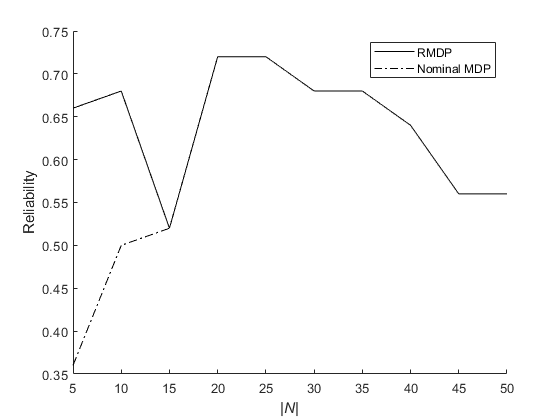

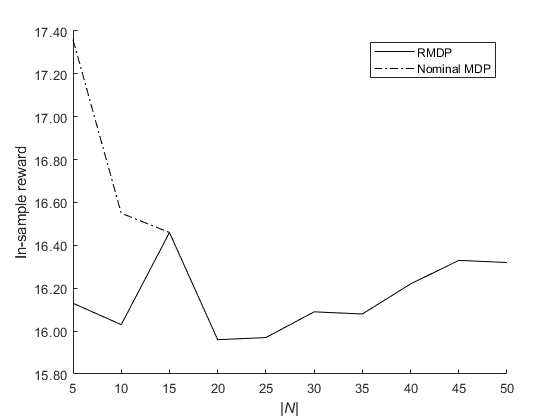

We use a training dataset . The optimal robust policies of Model (RRmPO) with ambiguity sets constructed under different hyperparameter values using the training dataset, , are then implemented in a test dataset to assess the out-of-sample performance. We examine two performance measurements: the average reward and the reliability of performance guarantees. The average reward is defined as , where is the expected reward of robust policy for test sample when the system is brand new (). The reliability is defined as the probability of the event , where is the in-sample value of under .

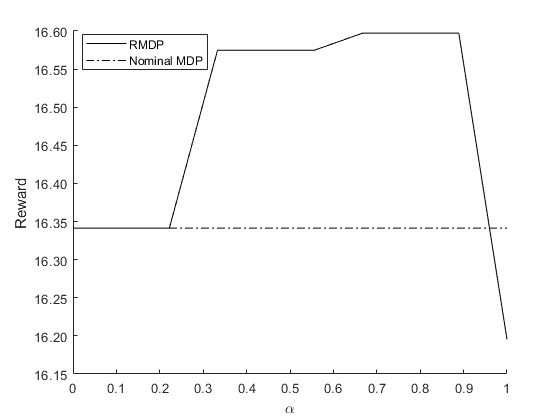

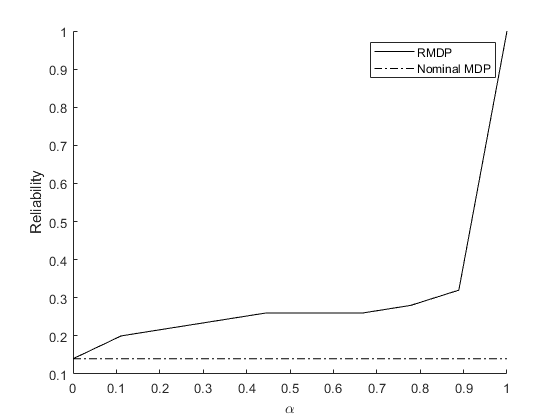

Figure 4 depicts the experiment results when the sizes of training dataset is 5 () and size of the test dataset is 50 (). From Figure 4(4(a)), we observe that the average reward of the robust policy is slightly higher than that of the nominal policy when is not too large. As keeps increasing, the average reward of the robust policy deteriorates because the robust policy is too conservative. The empirical reliability visualized in Figure 4(4(b)) is in general non-decreasing in , and the reliability of the performance guarantee under the robust approach is much higher than that under the nominal approach. We also find that the out-of-sample average reward using a robust approach is better as long as the reliability of the performance guarantee is noticeably smaller than 1 and deteriorates when it is close to 1. Figure 4(c) and (d) present the out-of-sample performance and the reliability of Model (RRmPO) with the interval-matrix-based ambiguity sets, respectively. Similar patterns are observed. Results of this experiment provide an empirical justification of adopting a robust remanufacturing approach, especially when the size of the dataset is small.

5.4.3 Remanufacturing Planning Driven by Out-of-Sample Performance

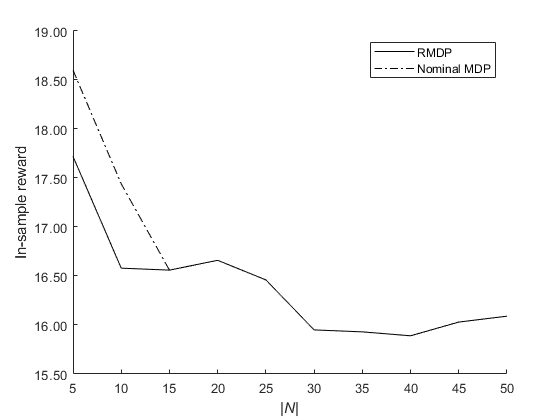

From the previous experiment on the impact of the parameter uncertainty, it is shown that different hyperparameter values may lead to robust remanufacturing policies with different out-of-sample performance . It is desired to select a that maximizes the average award . This, however, requires the true transition probability that is not precisely known. We select the optimal via validation using the training data. Specifically, we randomly select 60% of the training dataset for training and the remaining 40% of the training data is used for validation. Using newly formed training dataset to construct the ambiguity sets, solve Model (RRmPO) for a finite number of candidate hyperparameter . Use the validation dataset to evaluate the out-of-sample performance of , select the optimal as the one that maximizes of the validation set, and report as the data-driven solution.

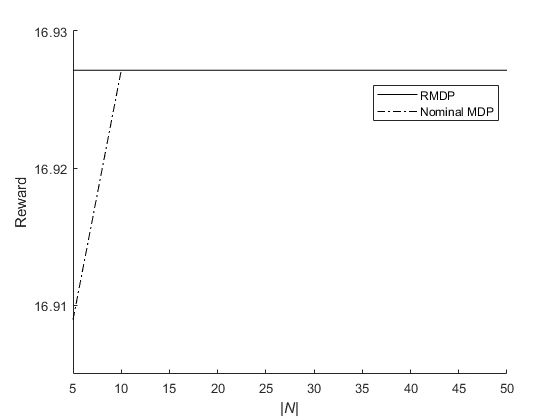

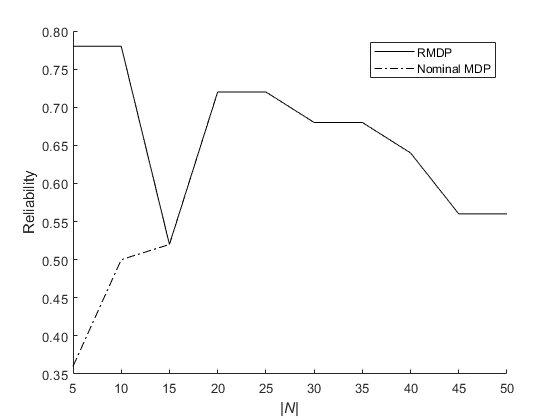

Figure 5(a) shows the mean value of the out-of-sample performance as a function of the sample size . We also observe that both out-of-sample and in-sample performances exhibit asymptotic consistency. Figure 5(b) shows the mean of the reliability of the guaranteed performance under different sample sizes. We can see that the robust policy significantly outperforms the nominal one, particularly when the training data is scarce. As more data become available, the optimal robust policy converges to the nominal policy, and so does the performance of the robust policy. Figure 5(c) reports in-sample estimate . We can see that the nominal approach is over-optimistic while the robust approaches act on the cautious side.

5.4.4 Remanufacturing Planning Driven by Reliability

From the previous experiment, we can see that there exists some trade-off between the out-of-sample performance and the reliability of the performance guarantee; reliability may be sacrificed if the optimal hyperparameter is selected by only maximizing the out-of-sample performance. In the next experiment, we consider an alternative objective that chooses a hyperparameter that results in satisfactory out-of-sample performance while ensuring a prescribed reliability level. We use the method described in Esfahani and Kuhn (2018) to find the smallest for which a desired reliability level () is guaranteed. An estimator of is constructed via bootstrapping the training data as follows. Construct bootstrap samples (with replacement) from the original training dataset. Solve Model (RRmPO) for a finite number of hyperparameters for each bootstrap sample () and obtain the optimal value , and then estimate the out-of-sample performance for the corresponding validation dataset. Set to the smallest that leads to a reliability level of , that is, the out-of-sample performance for the validation sets exceeds the in-sample performance in at least different bootstrap samples. Resolve Model (RRmPO) for and obtain the data-driven remanufacturing policies using the original training dataset . The ambiguity sets constructed in this method calibrates their size to guarantee the desired reliability level .

6 Conclusion and Future Work

In this paper, we consider the problem of remanufacturing planning in the presence of parameter uncertainty. We formulate the problem as a robust Markov decision process in which the true transition probability is unknown but lies in an ambiguity set with high confidence. Two statistical methods are used to construct the ambiguity set: the KL distance, and bootstrap resampling. We investigate the structure of the optimal robust policies and establish conditions to ensure the policies are of control-limit type. We also establish sufficient conditions for some of the intuitive results seen in our computational study. In particular, we derive the general decision insights for two systems—one system’s ambiguity set is contained in the other’s; we show that when large uncertainty in transition dynamics presents, the decision maker needs to be cautious about remanufacturing a product and should consider early scrapping to hedge against future uncertainties. We demonstrate the structure of the optimal robust policies via a computational study using the simulated operational data of the turbofan engine operated by NASA, investigate the out-of-sample performance, and derive the data-driven solutions to improve the out-of-sample performance.

Future extensions of this work will focus on investigating optimal production planning and inventory control policies for remanufacturing that build on this work. Moreover, at each decision epoch, decision makers make new observation about the system, and an important question that arises is that how the information that becomes available in the decision process can be leveraged to resolve some ambiguity, so that the optimal robust policies are not overly conservative. In addition, an implicit assumption made in this paper is that the states of a system are directly observable (i.e., the sensor data reveal the underlying state of the system with certainty). In practice, many systems are not directly observable and the states have to be inferred from signals collected. Future work will investigate the partially observable Markov decision process with parameter uncertainty.

References

- Abdallah et al. (2012) Abdallah, T., Farhat, A., Diabat, A., and Kennedy, S. (2012). Green supply chains with carbon trading and environmental sourcing: Formulation and life cycle assessment. Applied Mathematical Modelling, 36(9):4271–4285.

- Ben-Tal et al. (2013) Ben-Tal, A., Den Hertog, D., De Waegenaere, A., Melenberg, B., and Rennen, G. (2013). Robust solutions of optimization problems affected by uncertain probabilities. Management Science, 59(2):341–357.

- Chandler (2011) Chandler, D. L. (2011). When is it worth remanufacturing?

- Curran (2011) Curran, M. A. (2011). Scientific applications international corporation (saic). Life cycle assessment: principles and practice, dostupno na: http://www. epa. gov/nr mrl/lcaccess/pdfs/600r06060. pdf, 10.

- Delage and Mannor (2010) Delage, E. and Mannor, S. (2010). Percentile optimization for markov decision processes with parameter uncertainty. Operations research, 58(1):203–213.

- Diaz et al. (2010) Diaz, N., Choi, S., Helu, M., Chen, Y., Jayanathan, S., Yasui, Y., Kong, D., Pavanaskar, S., and Dornfeld, D. (2010). Machine tool design and operation strategies for green manufacturing.

- Dulman and Gupta (2018) Dulman, M. T. and Gupta, S. M. (2018). Maintenance and remanufacturing strategy: using sensors to predict the status of wind turbines. Journal of Remanufacturing, 8(3):131–152.

- Efron and Tibshirani (1994) Efron, B. and Tibshirani, R. J. (1994). An introduction to the bootstrap. CRC press.

- Elwany et al. (2011) Elwany, A. H., Gebraeel, N. Z., and Maillart, L. M. (2011). Structured replacement policies for components with complex degradation processes and dedicated sensors. Operations research, 59(3):684–695.

- EPA (2016) EPA, U. (2016). G7 alliance on resource efficiency: U.s.-hosted workshop on the use of life cycle concepts in supply chain management to achieve resource efficiency.

- Esfahani and Kuhn (2018) Esfahani, P. M. and Kuhn, D. (2018). Data-driven distributionally robust optimization using the wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming, 171(1-2):115–166.

- Faludi et al. (2015) Faludi, J., Bayley, C., Bhogal, S., and Iribarne, M. (2015). Comparing environmental impacts of additive manufacturing vs traditional machining via life-cycle assessment. Rapid Prototyping Journal.

- Ford and Despeisse (2016) Ford, S. and Despeisse, M. (2016). Additive manufacturing and sustainability: an exploratory study of the advantages and challenges. Journal of Cleaner Production, 137:1573–1587.

- Frederick et al. (2007) Frederick, D. K., DeCastro, J. A., and Litt, J. S. (2007). User’s guide for the commercial modular aero-propulsion system simulation (c-mapss).

- Galbreth and Blackburn (2010) Galbreth, M. R. and Blackburn, J. D. (2010). Optimal acquisition quantities in remanufacturing with condition uncertainty. Production and Operations Management, 19(1):61–69.

- Giuntini and Gaudette (2001) Giuntini, R. and Gaudette, K. (2001). Remanufacturing, the next great opportunity for improving us productivity. Business Horizons.

- Govindan et al. (2015) Govindan, K., Soleimani, H., and Kannan, D. (2015). Reverse logistics and closed-loop supply chain: A comprehensive review to explore the future. European journal of operational research, 240(3):603–626.

- Guide Jr (2000) Guide Jr, V. D. R. (2000). Production planning and control for remanufacturing: industry practice and research needs. Journal of operations Management, 18(4):467–483.

- Gutowski et al. (2011) Gutowski, T. G., Sahni, S., Boustani, A., and Graves, S. C. (2011). Remanufacturing and energy savings. Environmental science & technology, 45(10):4540–4547.

- Ijomah et al. (2007) Ijomah, W. L., McMahon, C. A., Hammond, G. P., and Newman, S. T. (2007). Development of design for remanufacturing guidelines to support sustainable manufacturing. Robotics and Computer-Integrated Manufacturing, 23(6):712–719.

- Iyengar (2005) Iyengar, G. N. (2005). Robust dynamic programming. Mathematics of Operations Research, 30(2):257–280.

- Kim (2016) Kim, M. J. (2016). Robust control of partially observable failing systems. Operations Research, 64(4):999–1014.

- Kim and Makis (2013) Kim, M. J. and Makis, V. (2013). Joint optimization of sampling and control of partially observable failing systems. Operations Research, 61(3):777–790.

- Kurt and Kharoufeh (2010) Kurt, M. and Kharoufeh, J. P. (2010). Optimally maintaining a markovian deteriorating system with limited imperfect repairs. European Journal of Operational Research, 205(2):368–380.

- Lund and Hauser (2012) Lund, R. T. and Hauser, W. (2012). The database of remanufacturers. Boston University [www. reman. org/Papers/Reman_Database_Lund. pdf].

- Mannor et al. (2007) Mannor, S., Simester, D., Sun, P., and Tsitsiklis, J. N. (2007). Bias and variance approximation in value function estimates. Management Science, 53(2):308–322.

- Moghaddass and Zuo (2014) Moghaddass, R. and Zuo, M. J. (2014). An integrated framework for online diagnostic and prognostic health monitoring using a multistate deterioration process. Reliability Engineering & System Safety, 124:92–104.

- Nilim and El Ghaoui (2005) Nilim, A. and El Ghaoui, L. (2005). Robust control of markov decision processes with uncertain transition matrices. Operations Research, 53(5):780–798.

- Östlin et al. (2009) Östlin, J., Sundin, E., and Björkman, M. (2009). Product life-cycle implications for remanufacturing strategies. Journal of cleaner production, 17(11):999–1009.

- Puterman (2014) Puterman, M. L. (2014). Markov decision processes: discrete stochastic dynamic programming. John Wiley & Sons.

- Satia and Lave Jr (1973) Satia, J. K. and Lave Jr, R. E. (1973). Markovian decision processes with uncertain transition probabilities. Operations Research, 21(3):728–740.

- Savaskan et al. (2004) Savaskan, R. C., Bhattacharya, S., and Van Wassenhove, L. N. (2004). Closed-loop supply chain models with product remanufacturing. Management science, 50(2):239–252.

- Saxena et al. (2008) Saxena, A., Goebel, K., Simon, D., and Eklund, N. (2008). Damage propagation modeling for aircraft engine run-to-failure simulation. In 2008 international conference on prognostics and health management, pages 1–9. IEEE.

- Seitz (2007) Seitz, M. A. (2007). A critical assessment of motives for product recovery: the case of engine remanufacturing. Journal of Cleaner Production, 15(11-12):1147–1157.

- Shi and Min (2014) Shi, W. and Min, K. J. (2014). Product remanufacturing and replacement decisions under operations and maintenance cost uncertainties. The Engineering Economist, 59(2):154–174.

- Silver (1963) Silver, E. A. (1963). Markovian decision processes with uncertain transition probabilities or rewards. Technical report, MASSACHUSETTS INST OF TECH CAMBRIDGE OPERATIONS RESEARCH CENTER.

- Skrainka (2012) Skrainka, M. R. S. (2012). Analysis of the environmental impact on remanufacturing wind turbines. Rochester Institute of Technology.

- Song et al. (2015) Song, S., Liu, M., Ke, Q., and Huang, H. (2015). Proactive remanufacturing timing determination method based on residual strength. International Journal of Production Research, 53(17):5193–5206.

- Sutherland et al. (2008) Sutherland, J. W., Adler, D. P., Haapala, K. R., and Kumar, V. (2008). A comparison of manufacturing and remanufacturing energy intensities with application to diesel engine production. CIRP annals, 57(1):5–8.

- Van Der Laan et al. (1999) Van Der Laan, E., Salomon, M., Dekker, R., and Van Wassenhove, L. (1999). Inventory control in hybrid systems with remanufacturing. Management science, 45(5):733–747.

- Wang et al. (2016) Wang, Y., Hu, J., Ke, Q., and Song, S. (2016). Decision-making in proactive remanufacturing based on online monitoring. Procedia CIRP, 48:176–181.

- White III and El-Deib (1986) White III, C. C. and El-Deib, H. K. (1986). Parameter imprecision in finite state, finite action dynamic programs. Operations Research, 34(1):120–129.

- White III and Eldeib (1994) White III, C. C. and Eldeib, H. K. (1994). Markov decision processes with imprecise transition probabilities. Operations Research, 42(4):739–749.

- Wiesemann et al. (2013) Wiesemann, W., Kuhn, D., and Rustem, B. (2013). Robust markov decision processes. Mathematics of Operations Research, 38(1):153–183.

- Xu et al. (2012) Xu, H., Caramanis, C., and Mannor, S. (2012). A distributional interpretation of robust optimization. Mathematics of Operations Research, 37(1):95–110.

Appendix

A.1 Proof of Proposition 1

The value function defined in (RRmPO) involves solving an inner problem for any given and as follows

| s.t. | (A.1) | |||

The Lagrangian dual problem of (A.1) is

where the Lagrangian function is

The strong duality holds because is a strictly feasible solution to the problem (A.1) and the Slater condition holds. The first order conditions of the Lagrangian function give

| (A.2) |

By substituting (A.2) into the Lagrangian function, the dual problem becomes

Again, the first order conditions give

| (A.3) |

The dual problem can be rewritten as

where is the optimal solution of the dual problem with given and .

A.2 Proof of Proosition 2

Let denote the value function at the th iteration of the robust value iteration algorithm in Section 4.1.1. We will show that is non-increasing in and for any integer by induction. Then, the theorem follows because the robust value iteration algorithm converges to an optimal policy.

We set the initial value as for all and . First, we show that is non-increasing in for all . Because for all , the induction holds at the initial iteration. Assume that is non-increasing in for . Let with and be the optimal solution of the dual problem (5) defined in Theorem 1 for any give state . We consider two cases at iteration . If , we have

| (A.4) | ||||

| (A.5) | ||||

The inequality (A.4) holds because . The inequality (A.5) follows Lemma 4.7.2 in Puterman (2014) because is IFR and is non-increasing in given by the induction hypothesis.

If , we have . Therefore, is non-increasing in given . Similarly, since , is also non-increasing in given . Since , the induction hypothesis holds at iteration .

Next, we show that is non-increasing in for all . Because for all , the induction holds at the initial iteration. Assume for any given , is non-increasing in for . We consider two cases at iteration . If , we have

| (A.6) | ||||

| (A.7) | ||||

The inequality (A.6) holds because and by the induction hypothesis. The Inequality (A.7) follows Lemma 4.7.2 in Puterman (2014) because by Assumption 2(b) and is non-increasing in .

If , we have . Therefore, is non-increasing in for all . Similarly, since , is also non-increasing in for all . Since , the induction hypothesis holds at iteration .

A.3 Proof of Theorem 1

We first show that the optimal policy is of control-limit type for all . Let . We consider two cases: (i) If , then . Because is non-increasing in for all , . Thus, we have and . (ii) If , then , and by Theorem 2, , we have and .

Next, we show the existence of the threshold . This is equivalent to show that if for some , then . Since and , we have and hence .

A.4 Proof of Theorem 2

We first prove that is non-increasing in . This is equivalent to show that if . We prove this by contradiction. Suppose but for some and . Then, we have , and hence,

| (A.8) |

The right hand side (RHS) of Equation (A.8) be rewritten as

| RHS | ||||

| (A.9) |

where inequality (A.9) follows Lemma 4.7.2 in Puterman (2014) because is non-increasing in and in Assumption 2. And the left hand side (LHS) of Equation (A.8) be rewritten as

| (A.10) |

where the first inequality holds because , and the second inequality holds because . By (A.9) and (A.10), we have , which violates condition in Theorem 2(a) and implies that if .

It is straightforward that is non-increasing in because if as shown in the proof of Theorem 1.

A.5 Proof of Proposition 3

Before proving our main results, we first present a lemma that identifies the worst distribution of the following problem:

| (A.11) | ||||

| s.t. | ||||

with given , where and are effective lower and upper bounds defined by equations (8) and (9).

Lemma A.1.

If is non-increasing in , then the optimal solution of the problem (A.11) (i.e., the worst distribution) is as follows:

| (A.12) |

where .

Proof.

We prove Lemma A.1 by introducing a contradiction. Suppose is an optimal solution and there exists an such that . This implies that there exists an such that . Let . We construct a new distribution such that for , , and . It is easy to verify that is feasible to problem (A.11). Because , we have

This means there exists a feasible solution that is no worse than . Thus there exists a contradiction. ∎

We now prove the monotonicity of the value function. We first show that is IFR for any given if and satisfy conditions (10) and (11) for all . Let and be the same defined in Lemma A.1. If , we have

where the first inequality is a result of condition (10). If , we have

where the first inequality is a result of condition (11). Therefore, the result follows. We can similarly show that for all if conditions (12) and (13) for all are satisfied.

Having established the structure properties of transition matrices, we next prove part (a) regarding the monotonicity of with respect to for all .

The proof is based on the robust value iteration algorithm in Iyengar (2005). Let be the value function of the state at the end of iteration . We show that is non-increasing in for all in every iteration and therefore is non-increasing in for all as the algorithm converges.

We prove this by induction. Let the initial values in the robust value iteration algorithm be for all and , then the induction hypothesis holds at the initial iteration. Assume is non-increasing in for for . Let with . We first show that is IFR for any given . At iteration , if ,

| (A.13) | ||||

where inequality (A.13) follows Lemma 4.7.2 in Puterman (2014) because is non-increasing in by the induction hypothesis and is IFR given .

If , . Therefore, is non-increasing in for all . We can similarly prove that is also non-increasing in for all .

Because . Therefore, the induction hypothesis holds at iteration .

The proof of part (b) is similar to that of part (a), and is omitted.

A.6 Proof of Corollary 1

A.7 Proof of Corollary 2

A.8 Proof of Theorem 3

The proof is similar to the proof of Theorem 1.

A.9 Proof of Theorem 4

The proof is similar to the proof of Theorem 2.

A.10 Proof of Theorem 5

Suppose we solve the two problems simultaneously using the robust value iteration algorithm. We first show that starting with a value of 0 for all states in both problems, at the end of each iteration of the algorithm, the value function of will be greater than or equal to the value function of for each state. Let be the value function of the state of problem at the end of iteration . Let , , and denote the ambiguity set, transition probability, and the worst transition probability for state of problem , respectively.

We prove this by induction. Since for , the induction holds at the initial iteration. Now, assume that , for . Then we want to show that . At iteration , if , we have

| (A.14) | ||||

| (A.15) | ||||

| (A.16) |

If , , since for by the induction assumption. If , . Since for all , the induction hypothesis holds at iteration . Because the value function of is always greater than or equal to that of at each iteration of the value-iteration algorithm, the optimal value function of is greater than or equal to that of .

Next, we prove part (a) that for , where and is the threshold defined in Theorems 2 and 4 for . This is equivalent to show if and for all . We prove this by introducing a contradiction. Suppose when . Then we have and . Thus, we have

| (A.17) |

The left-hand-side (LHS) of (A.17) can be rewritten as

| LHS | ||||

| (A.18) | ||||

| (A.19) | ||||

| (A.20) |

The equality (A.18) is obtained by simply rearranging terms. The equality (A.19) holds because and for all following Theorem 1. The equality (A.20) holds because . By (A.17) and (A.20), we must have . However, the inequality does not hold since and leads to a contradiction. Therefore, we have if and .

Next, we prove part (b) that for . This is equivalent to show if . Because and by the induction, we have and thus .

Since if for , part (c) follows.

B.1 Experiment Parameters

The following table provides the experiment parameters used in the experiment that examines the existence of control limit policies when the condition of Theorem 2(a) is violated. Note that for easy parameter control, we redefine the reward as . Parameter values are drawn from their respective uniform distributions.