figuresection tablesection

-expectiles clustering ††thanks: Financial support of the European Union’s Horizon 2020 research and innovation program "FIN-TECH: A Financial supervision and Technology compliance training programme" under the grant agreement No 825215 (Topic: ICT-35-2018, Type of action: CSA), the European Cooperation in Science & Technology COST Action grant CA19130 - Fintech and Artificial Intelligence in Finance - Towards a transparent financial industry, the Deutsche Forschungsgemeinschaft’s IRTG 1792 grant, the Yushan Scholar Program of Taiwan, the Czech Science Foundation’s grant no. 19-28231X / CAS: XDA 23020303 are greatly acknowledged. All correspondence may be addressed to the authors by e-mail at amyli999@hotmail.com.

Abstract

-means clustering is one of the most widely-used partitioning algorithm in cluster analysis due to its simplicity and computational efficiency. However, -means does not provide an appropriate clustering result when applying to data with non-spherically shaped clusters.

We propose a novel partitioning clustering algorithm based on expectiles. The cluster centers are defined as multivariate expectiles and clusters are searched via a greedy algorithm by minimizing the within cluster ’ -variance’. We suggest two schemes: fixed clustering, and adaptive clustering. Validated by simulation results, this method beats both -means and spectral clustering on data with asymmetric shaped clusters, or clusters with a complicated structure, including asymmetric normal, beta, skewed and distributed clusters. Applications of adaptive clustering on crypto-currency (CC) market data are provided. One finds that the expectiles clusters of CC markets show the phenomena of an institutional investors dominated market. The second application is on image segmentation. compared to other center based clustering methods, the adaptive cluster centers of pixel data can better capture and describe the features of an image. The fixed clustering brings more flexibility on segmentation with a decent accuracy. All calculation can be redone via quantlet.com.

Keywords:

clustering, machine learning, simulation study, parameter-tuning

expectiles, partitional clustering

1 Introduction

Clustering is a useful technique to discover and identify homogenous groups of data points in a given sample. As an unsupervised learning algorithm, it aims to extract information on the underlying characteristics via dividing the data into groups that maximize common information. Obviously the information about homogeniety of groups is key in such a sample dividing mechanism. Among the simplest choice is the -means clustering method described by Steinhaus (1956) and Hartigan (1975), which adopt the Euclidean distance as neighbourhood measure, thus leading to spheres as silhouettes and means as centers of clusters. Indeed, while keeping a balance between group size and information gain, -means is the most widely used partitioning algorithm due to its simplicity, efficiency in computing and easiness of interpretation. Successful applications include signal processing, image identification, customer segmentation.

The principle of a partitioning clustering algorithm is to assign data points to the nearest cluster by optimising some objective function. The objective function of -means is the sum of within-group variance, and thus the correspondence cluster centers are the mean of each cluster. Minimizing the objective function is equivalent to maximizing the log-likelihood function with independent Gaussian density. Although -means clustering is often viewed as a "distribution free" algorithm, it is actually partitioning using equal sized spherical contour lines which can be considered as assuming independent identically distributed (i.i.d.) Gaussian clusters. Therefore, -means approach works better for cluster in the symmetric distribution than the skewed ones.

On the other hand, when applied on skewed or asymmetric distributed data whose characteristics may not be fully captured by the first two moments, new methods are required for non-spherical cluster. To account for within-cluster skewness, Hennig et al. (2019) introduce the -quantile clustering algorithm based on the assymmetric absoluate discrepancy. Then they linked their approach to a fixed partition model of genralized asymmetric Laplace distributions. This quantile discrepancy based density relies on both the quantile level and some additional scale/penalty parameter . However, and are assumed the same across different clusters to reduce the computation complexity.

An analogous work on quantile based clustering is proposed in Zhang et al. (2019), where they developed a model-based iterative algorithm to identify subgroups with heterogeneous slopes. In particularly, they consider clustering across multiple quantiles to capture the full picture of heterogeneity. For that accordance, how to specify the appropriate quantile level vector could be a problem for large dimensional data.

This motivates us to consider a novel method, -expectile clustering. This method is based on a similar idea as -means but with an expectile cluster center and aims at minimizing the so-called -variance, which is a weighted quadratic loss to take into account asymmetry. Besides being simple and fast, our algorithm can be applied on wider range of data compared with -means. In particular, we consider two schemes, either with a pre-specify level or an adaptive that may vary across different dimensions or clusters, which accommodates either a fixed cluster shape or a data-driven cluster shape to capture heterogeniety.

To better understand the basic ideas of -expectile clustering, we recall some basic knowledge about tail events. Quantile regression (Koenker and Bassett Jr, 1978) and expectile regression (Newey and Powell, 1987) have been suggested for displaying the whole picture of the conditional distribution of response variable on covariates, especially for data not sufficing the condition of homoskedasticity or conditional symmetry. For a random variable drawn from distribution , a location model of -th tail event measure with could be defined as:

With an assumption on the -th quantile or expectile of the cdf of being zero, is by definition the -th quantile or expectile of accordingly. An estimator of the location model of quantiles and expectiles can be naturally formed:

where the loss function is defined as:

with and respectively.

Although the concept of expectiles is natural analogues of quantiles, expectiles enjoy the computation efficiency over quantiles (Schnabel, 2011). In finance, the expectile might be preferred as a favorable risk measures due to its desirable properties such as coherence and elicitability (Kuan et al., 2009, Ziegel, 2016). Recently, the use of expectiles attracts more and more attention, such as the nonparametric expectile regression by Sobotka and Kneib (2012) and Yang et al. (2018), the principle expectile analysis by Tran et al. (2019). Our proposed -expectile clustering allows us to take into account tail characteristics and asymmetry when identifying homogenous groups of data, while simulation studies and applications justify its excellent performance.

The rest of the paper is organized as follows. In section 2, we will briefly review the classical -means algorithm, and then propose our -expectile clustering in two schemes. In section 3, we present the simulation study that includes data from different distribution and compare the performance of -expectiles clustering with other methods. Section 4 applies our method to real crypto currency market analysis and image segmentation. Codes of all the functions, applications and data are uploaded to quantlet.com.

2 Methodology

2.1 -means clustering

-means clustering is rooted in signal processing, and was described by Hartigan (1975). Suppose the data set comes from a random sample in . A clustering algorithm denoted by generates subsets each with distribution . Any clustering algorithm maps into a membership vector , i.e. , and , .

A clustering criterion is defined via a cost function. In -means clustering, the cost is defined as the sum of squared Euclidean distance between cluster members to the cluster centroids. Indeed the centroids can be considered as location parameters for clusters. In -means clustering, cluster centroids are actually cluster means and the cost function is the sum of within-cluster variance. Let be the -means objective function, be a set of cluster centroids with ,

Clustering is now turned into an optimisation problem and is solved via iteration. For a fixed , partition is achieved by assigning each point to the nearest cluster centroid.

For a fixed membership vector , the centroid can be estimated by taking the within-cluster mean.

If are drawn i.i.d. from an unknown distribution , an equally-weighted Gaussian Mixture Model can be formed by assuming the sample distribution composed by a convex combination of Gaussian distributions with expectation and variance ,

The estimation of this model requires the EM algorithm, and the details are explained in Deisenroth et al. (2020). If let be the -th cluster centrioid, and covariance matrix simply equals to , -means objective function is coincide with the expectation function in EM algorithm of a Gaussian Mixture Model with equal mixture weights. By a "hard" assignment of data points to nearest cluster centroid in -means algorithm as described in MacKay and Mac Kay (2003), the computation of parameter can be easily conducted by independently estimating cluster means. Simoultaneously -means clustering is a distribution-free but distance based clustering technique.

2.2 -expectiles clustering

Now consider a set of data with skewed or asymmetrically distributed clusters, i.e., cluster centroids are not located on means and cluster variances are heterogeneous on different sides around centroids. As said before, it is the information measure of homogeneity that yields the clusters. A distance with cluster centroids offset from means and a distance metric which takes asymmetry into account is certainly a more flexible way of dividing groups.

For that purpose, assume each cluster is a group of data drawn independently from a multivariate distribution , define the cluster centroid as the expectile of cluster distribution, and assign points according to expectile distances.

More precisely, let be a univariate random variable with probability cumulative function and finite mean . For a fixed , the -th expectile of as proposed by Newey and Powell (1987) is identified as the minimizer of the asymmetric quadratic loss

| (1) | |||

| (2) |

where . it is worth noting here that the expectile location estimator can be interpreted as a maximum likelyhood estimator of a normal distributed sample with an unequal weight placed on positive and negative disterbances, showed in Aigner et al. (1976).

For , define , then the multivariate expectile is the solution to the optimization problem:

| (3) |

Here the dependence is taken into account by using the norm. The construction of the multivariate expectiles are related to the dependence structure of each components. The choice of dependence modelling may differ according to the practical goal. For simplification reasons, we only elaborate the case when the dependence structure is ignored. The multivariate expectile now consists of marginal univariate expectiles,

where denotes the -th coloum of matrix (Maume-Deschamps et al., 2016).

The flexibility and power of expectiles in dimension comes from looking at , making the level variable over dimensions. Thus, we obtain

The empirical version reads as:

| (4) |

The idea is now to fix the cluster centroids at the empirical expectile of the -th cluster, i.e. , and consider an asymetrically weighted distance function with norm. For an observation , define -distance

| (5) |

which coincides with loss function (2).

Based on the concept of -distance, instead of specifying an asymmetric form of distribution or , we can form a -expectile objective function by defining an asymmetric -variance as described in Tran et al. (2019),

which yields to an axis-aligned elipsoid unit ball. To include covariance or correlation, usually a matrix form of multivariate expctile will be considered. By introducing a symmetric matrix , one can form a score function as described in Maume-Deschamps et al. (2016),

| (6) |

However, we will not include this case in this paper. We will leave this problem for further works.

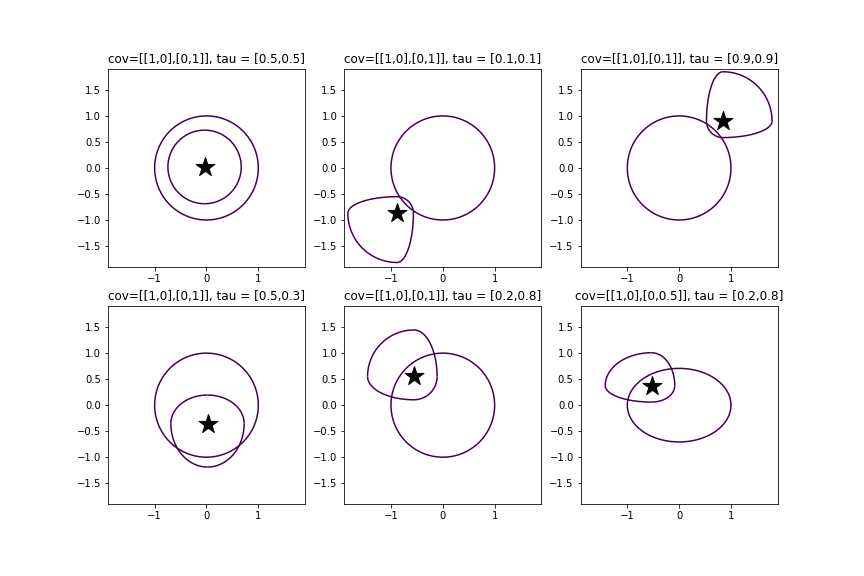

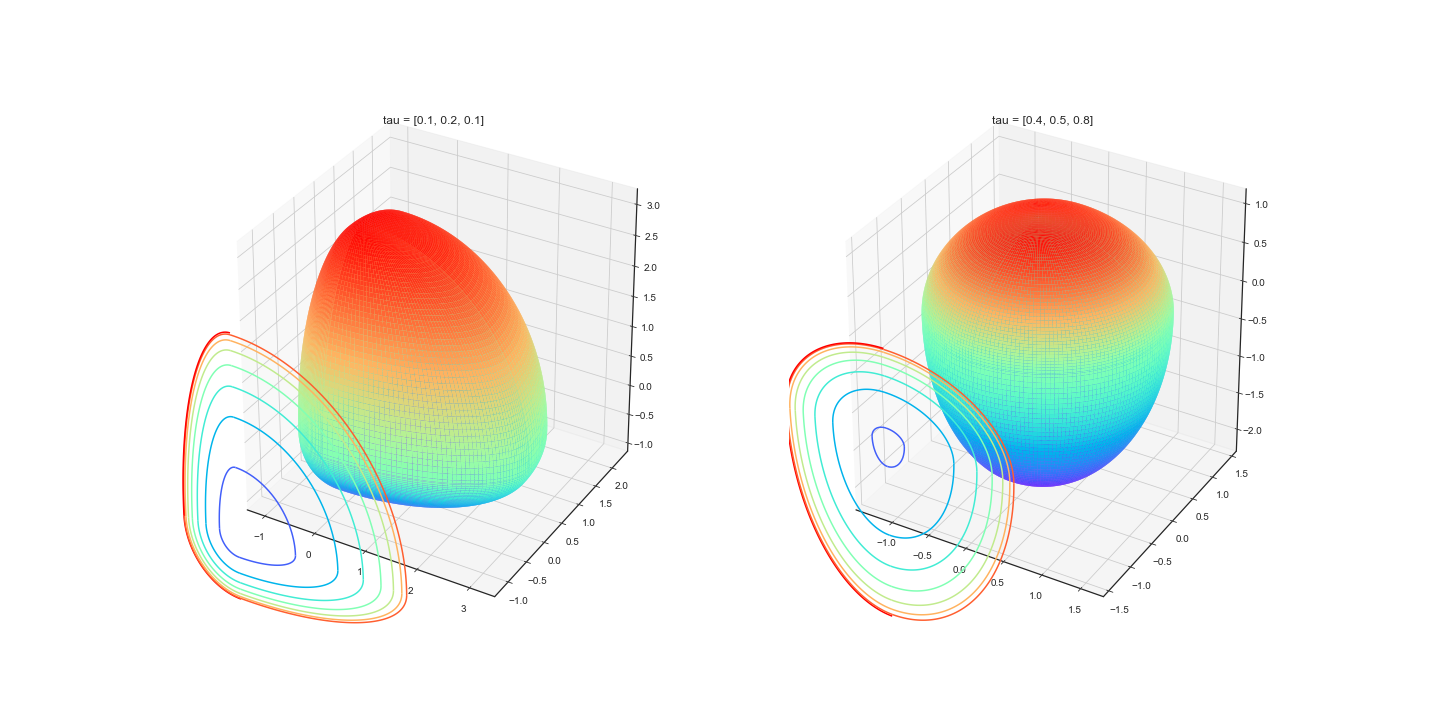

In Figure 1, the contour lines of unit circles of bivariate -variance with various levels on each axis are shown along with unit circles of a symmetric variance in the back. The covariance matrix is the inverse matrix of in function 6. The last sub-plot shows the unit circles with different scales on two axis. These are equivalent to the contour lines of independent bivariate asymmetric normal distributions in comparison with the contour lines of independent normal distributions. Figure 2 shows the 3D contour surface of -variance unit ball with different -levels on each dimension, or the 3D cluster shapes.

2.3 Fixed clustering

With distance (5) and a pre-specified vector, define the objective function

| (7) | ||||

| (8) |

which aims to detect expectile-specified clusters by minimizing the sum of within-cluster -variance.

For known , cluster centroids are found by:

| (9) | ||||

| (10) |

where is a weight function which is related to , the location parameter at the given level.

| (11) |

This implicit dependence of on leads to the application of the Least Absolute Square Estimator (LAWS), a version of the Stochastic Gradient Algorithm. For a fixed , the weight in equation (11) is calculated, therefore a closed form solution of can be expressed as

| (12) |

where

Cluter centroids can be estimated by iteratively repeating the two steps until the location of does not change, see:

The -expectiles clustering algorithm now read as follows:

2.4 Adaptive clustering

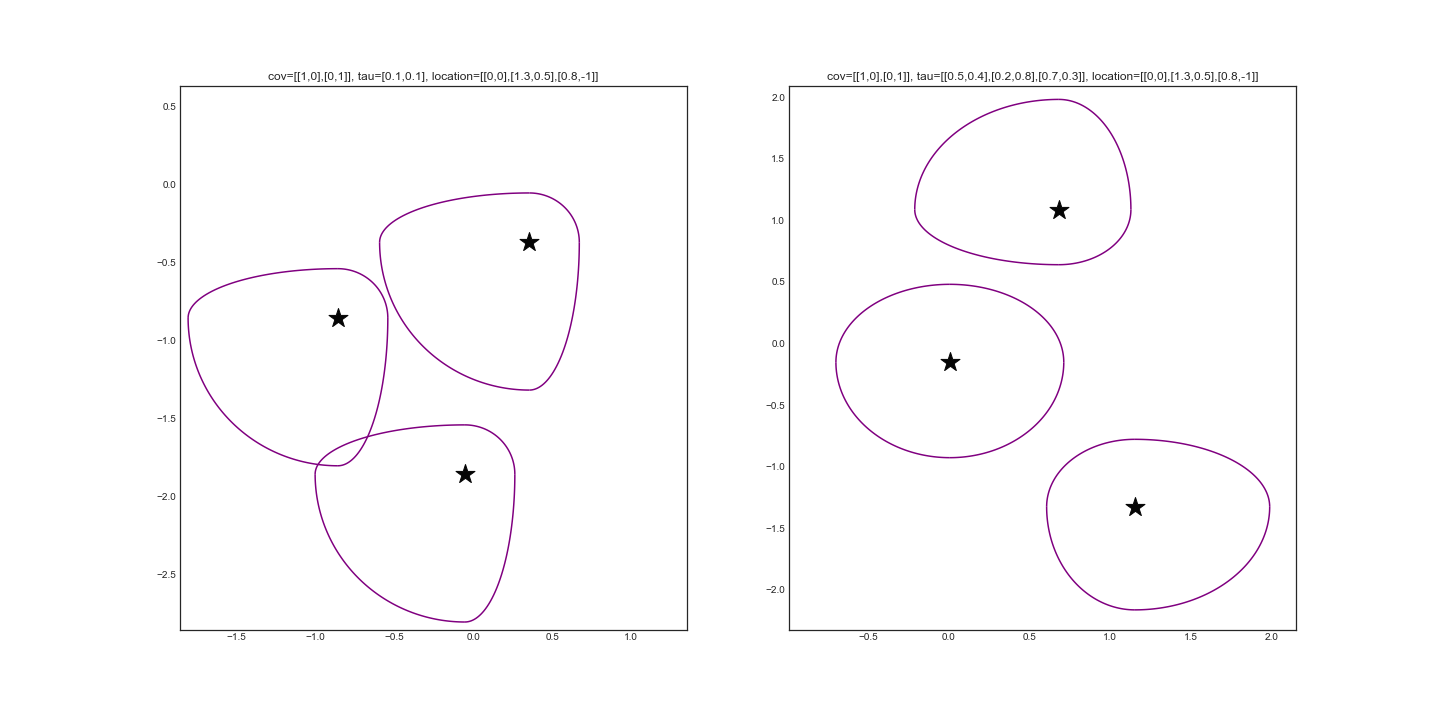

In the last section, clustering with fixed cluster shapes by pre-specifying the vector has been discussed, and this senario is shown in Sub-plot of Figure 3. In comparison, regarding the issue of clusters with different shapes as shown in Sub-plot of Figure 3, we present the result of a fully adaptive algorithm, both for different dimensions and for different clusters. Without pre-defined , we now assume is a matrix. We optimize the following cluster objective function with respect to as well.

| (13) | ||||

| (14) |

For given , to optimize , require

| (15) |

By taking first order condition, we get the unique solution:

| (16) |

where

Then the clustering algorithm for adaptive can be described as:

The clustering algorithm can be implemented as follows:

3 Simulation

To evaluate the performance of -expectiles clustering, we design four simulated samples with clusters. Let , each cluster represented by is an i.i.d. random sample drawn from a -variate distribution in the size of . Each component of the multivariate distribution is assumed to be independent. Data set can be written as . Scale, location and skewness of the distribution can cause the overlapping of multiple clusters which in turn influece the cluster shapes and within-cluster data density, thus hinder the accuracy of grouping results. The simulated samples are designed to reserve some extend of overlap while ensure certain discrimination between clusters, in order to achieve the purpose of evaluating the robustness of the algorithms.

- Sample 1:

-

In the first sample we generate multivariate Gaussian clusters with unit variance and different location parameters. , where is a -dimensional integer vector whose elements are randomly generated in interval , and then shift the location of other clusters by . Clusters are in the same size of .

- Sample 2:

-

To include some asymmetry on the basis of Sample 1, the second sample is designed as a mixture of asymmetric normal distributions. Each cluster is considered as a -dimensional i.i.d. sub-sample, where . The probability density function of can be expressed as following, with as location parameters, and , as standard deviation of two sides around ,

Now let (-expectile of the variable) be the location parameter, and be the overall standard deviation of the variable, the density function of asymmetric normal distribution can be rewritten as:

which means the asymmetric normally distributed variable can be converted from univariate Gaussian distributed variables according to the formula:

in our sample, each . Parameter is given by using random generator with interval , and location parameter is randomly generated in -th cluster, then the location of -th cluster can be shifted by .

- Sample 3:

-

In the third sample we want to test the algorithm on skewed but not leptokurtic clusters, namely -distributed clusters. For variables in cluster, , , and in cluster , , . We generate parameter randomly from interval and from interval , again .

- Sample 4:

-

For the last sample, skewed and leptokurtic clusters are being considered. We set different scenarios:

-

•

skewed generalized -distributed samples. We first generated a random sample with dimension , parameters , location randomly fluctuated with the difference of 0.5 around , . And generate data repeatedly until reaches and .

-

•

multivariate -distributed clusters. For variables in the first cluster, , and when ; , when , where and are integers randomly selected from interval and . In the second cluster, , , , , where and are integers randomly selected from interval and . In the third cluster, , , and , , where and are integers randomly selected from interval and .

-

•

For each of the first three samples, we evaluate combinations of . For the last sample, .

For each simulation setting, we re-generate the data times and test the algorithms each round, and take the average of the Adjusted Rand Index (ARI) of the yielded classification compared with the true cluster membership. Rand Index measures the pair-wised agreement between data clustering. When it is djusted for the chance grouping of elements, this is the Adjusted Rand Index. Given two partitions , , and the contingency table,

the Ajusted Rand Index is defined as:

Other distance based clustering algorithms such as -means denoted by -means, spectral clustering (Shi and Malik, 2000) denoted by spectral, Ward hierarchical clustering (Ward Jr, 1963) denoted by h-ward, and Quantile based clustering (Hennig et al., 2019) are comparing with -expectile clustering with adaptive . Note that Quantile based clustering algorithm allows quantile level (skewness parameter) to change variable-wisedly and introduces a scale/penalty parameter. CU, CS, VU, VS stands for the four modes of Quantile based clustering, corresponding to Common skewness parameter and Unscaled variables, Common skewness parameter and Scaled variable-wise, Variable-wise skewness parameter and Unscaled variables, Variable-wise skewness parameter and Scaled variable-wise. Results are shown in Apendix from Table 3 to table 7, where the demonstrated values are the times of ARI.

The cluster algorithm shows a higher ARI score when the sample sizes are larger and the dimensionalities are higher. Spectral clustering sometimes does not work appropriate on data with outliers which lead to a not fully connected graph. This scenario can be easily occured in a highly skewed sample or sample with large dimensionality.

From Table 3 we can conclude that -expectile, as an algorithm that generalize -means, works as good as but sometimes even better than -means on spherical clusters. Meanwhile it is better than all the other clustering algorithms, incluing Ward hierarchical clustering, spectral clustering, and quantile based clustering.

For asymmetric normal distributed clusters, as Table 4 shows, -expectile outperforms all the listed algorithms. Since the contour lines of the real distribution of the data correspond to the assumption of -expectile cluster shapes, -expectile yields a significantly better result than other algorithms.

For more general skewed distributed clusters as demonstrated in Table 4, 5, 6 and 7, -expectile still has a robust and outstanding performance. It always performs better than -means, only except for some special cases of low-dimensional beta distributed clusters, which may due to the almost sphere cluster shapes and the non-leptokurtic density. On this kind of samples, Ward hierarchical clustering has a moderate but non-robust performance, especially when the dimensionality goes higher. Quantile based clustering, in another hand, has a comparable performance on skewed data with -expectile. Under non-leptokurtic scenario, -expectile performs better, while working on leptokurtic clusters, among the four algorithms of Quantile based clustering, some has superior results but others can be inferior. Criterion of selection among the four algorithms needs to be further studied.

4 Application

4.1 Application of adaptive clustering on CRIX and VCRIX data

An application based on the CRIX and VCRIX data is presented in this section. CRIX (CRyptocurrency IndeX) developed by Trimborn and Härdle (2018) provides a CC market price index weighted by market capitalization with a dynamic changing number of constituents of representative cryptos. The mechanism of selecting CRIX constituents with Akaike Informstion Creterion is introduced in the mentioned paper. VCRIX, developed by Kim et al. (2019) is a volatility index built on CRIX which offers a forecast for the mean annualized volatility of the next 30 days, re-estimated daily by using Heterogeneous Auto-Regressive (HAR) model.

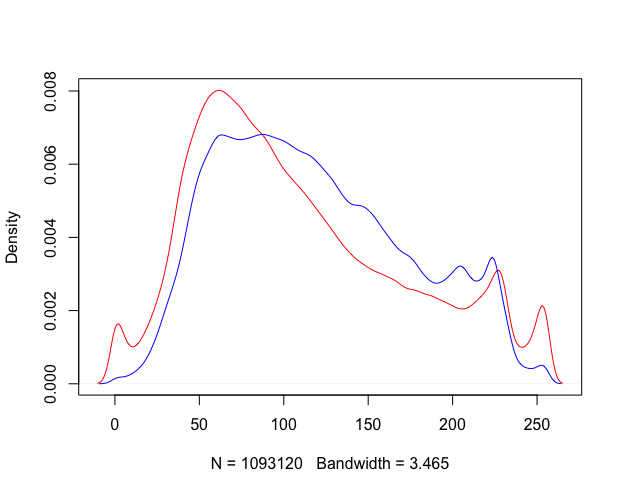

The data are downloaded from thecrix.de, consists of two time series, CRIX and VCRIX, collected daily from 2017-01-02 to 2021-02-09, in total 1497 observations in two dimensions. Here we scaled the data by dividing each varaible by their standard deviations to ensure the data has equal variance. The descriptive statistics and density plots of the two variables are listed as following.

| Min. | 1st Qu. | Median | Mean | 3rd Qu. | Max | Skewness | Kurtosis | JB statistic | |

|---|---|---|---|---|---|---|---|---|---|

| CRIX | 0.080 | 0.621 | 1.056 | 1.246 | 1.443 | 7.257 | 2.450 | 10.988 | 5481.283 |

| VCRIX | 0.801 | 1.814 | 2.225 | 2.458 | 2.884 | 6.565 | 1.370 | 5.360 | 816.166 |

Looking at Table 1, it is evident that neither of the two variables are normally distributed and both of them are skewed. This fact can be seen in Figure 4 as well, due to the longer right tail of the densities of both variables. From the plot of marginal distribution one might suspect several clusters exist.

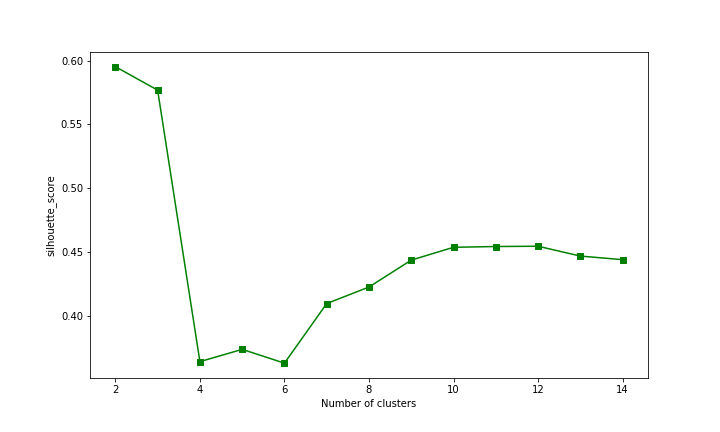

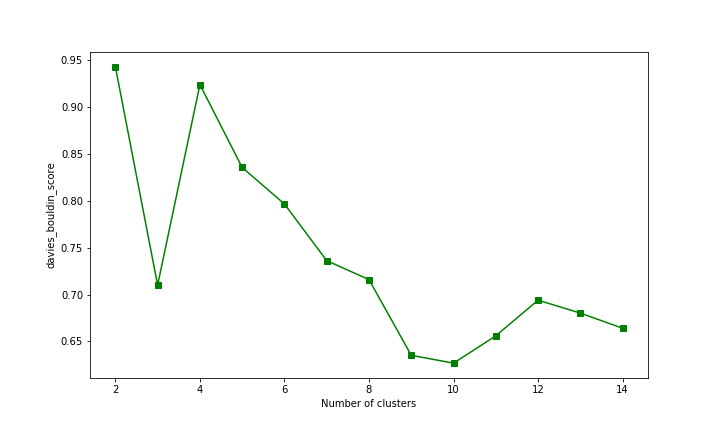

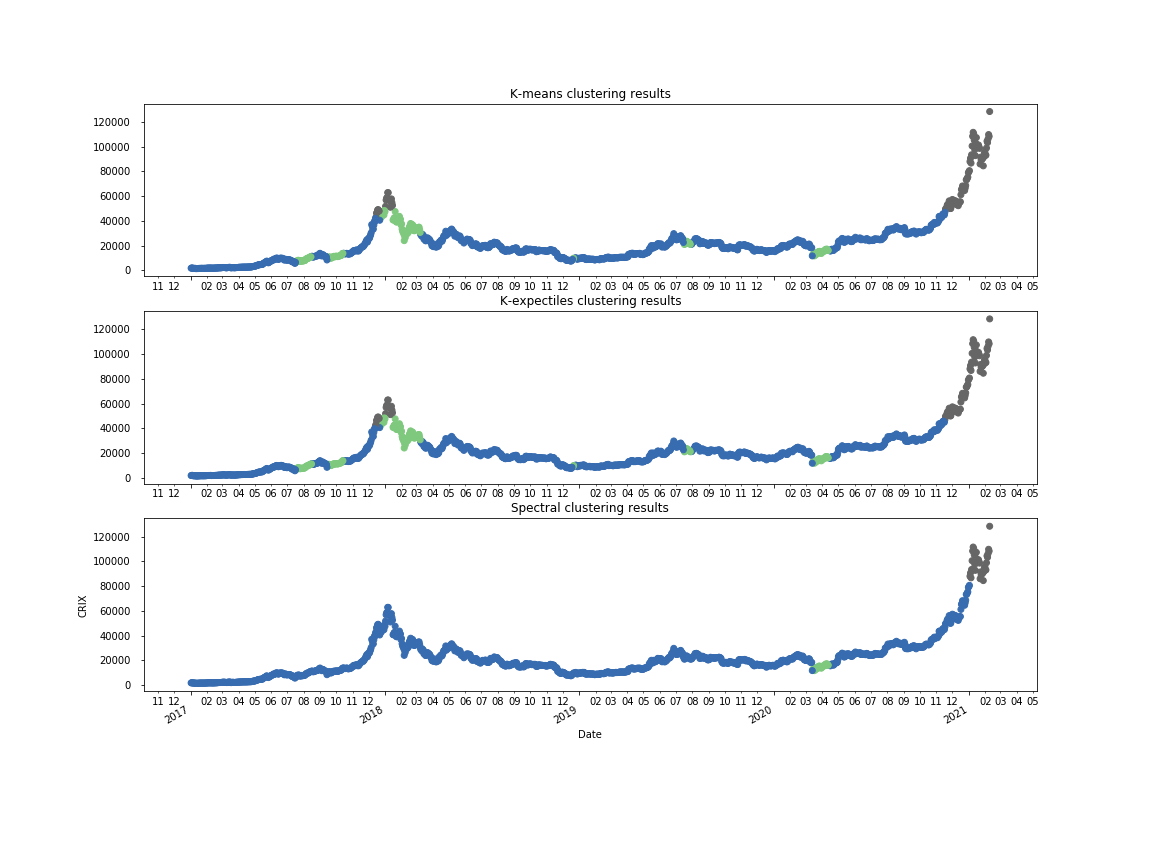

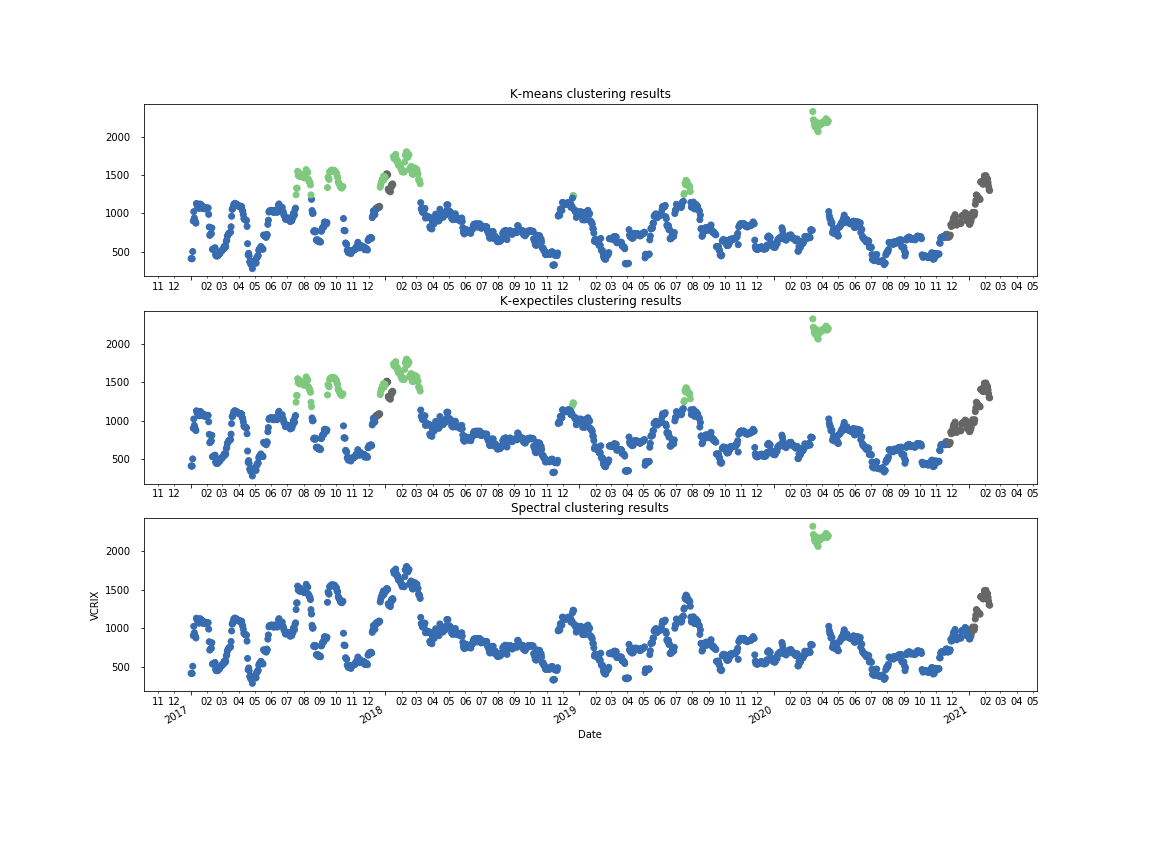

Results of -means clustering, -expectile clustering with adaptive and Spectral clustering are shown in Figure 10. If referring to Figure 4, it seems is a reasonable group number which best reflects the multi-modal property of the marginal density plot. But according to clustering evaluation cretaria including silhouette score and Davies-Bouldin score (Figure 8 and 9), both of them showed that is the optimal cluster number which balances the cluster efficiency and number of clusters from a maximising similarity perspective. Here allow me to presume that a symmetric variance-based clustering algorithm such as -means is not suitable due to the skewness of the whole system. Now we fix and let the algorithm find the optimal location of the cluster center based on the skewness nature of the data, we obtain the parameter in the form of a matrix , corresponding to the blue, green and grey clusters in Figure 10 respectively. It can also be seen that -means and -expectile algorithms result in different locations of cluster centroids, which lead to different cluster memberships. To better evaluate the performance of -expectile clustering, the result of spectral clustering is using as comparison.

Figure 3 shows the shapes and distribution of the three clusters on the two dimensional space consisting of CRIX and VCRIX. From the plot we can observe that the three clusters of - expectile represents different types of correlation between price and volatility index. The three clusters can be described as ’low-price-low-volatility cluster’, ’low-price-high-volatility cluster’, and ’positively correlated price and volatility cluster’, corresponding to color blue, green and grey.

it is worth noting that the grey cluster only appears shortly in the end of 2017 and from the end of 2020 till now. Positive correlation between price and volatility of crypto markets means that the volatility and price drives each other in the same direction. Higher price and higher volatility shows an ’exciting’ signal other than a ’panic’ expectation, this phenomenon mostly occurs in the securities market dominated by individual investors, where increased volatility is a signal of market activation. On the other hand, low-volatility cluster appears in most period of the CC market, which means CC market is highly dominated by instituational investors most of the time. High volatility means unstable market sentiment and high trading volumn, and the green cluster often appears when the price start to change.

4.2 Application of fixed clustering on image segmentation

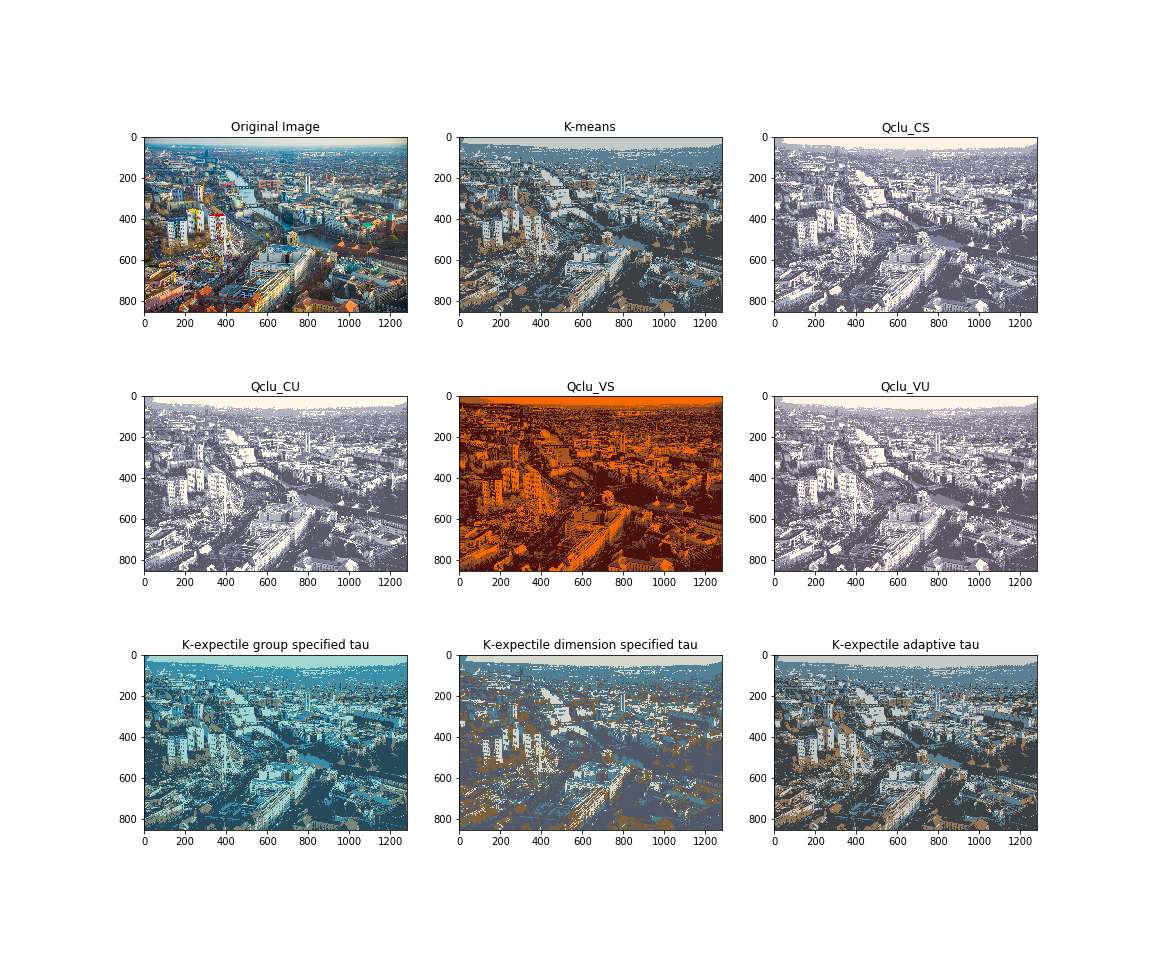

Image segmentation is a technique widely used in image processing, which partition an image into multiple parts sharing similar characteristics. Image segmentation includes separating foreground from background, or clustering regions of pixels based on color or shape. One of the commenly used methods in color-based segmentation is -means clustering. In this case, pixel values are regarded as independent random samples in the 8 bits color space, and divided into discrete regions which has minimal variances. The output of - means segmentation can be visualized by converting all the pixels in a group to the color of the cluster centers.

By applying K-expectile clustering, we expect a more flexible choice of centers and thus a more flexible segmentation output of the image, including an optimising procedure on parameter and two ways to specify , which put more weights on group-wised and dimension-wised tail behavior. With clusters, we set a group-specified as to include groups emphasizes on both left tail and right tail. For dimensions of RGB valued data, we fixed a parameter as to involve information on both tails. To test the performance of K-expectile clustering, we take K-means clustering result as benchmark and bring Quantile based clustering results into comparison.

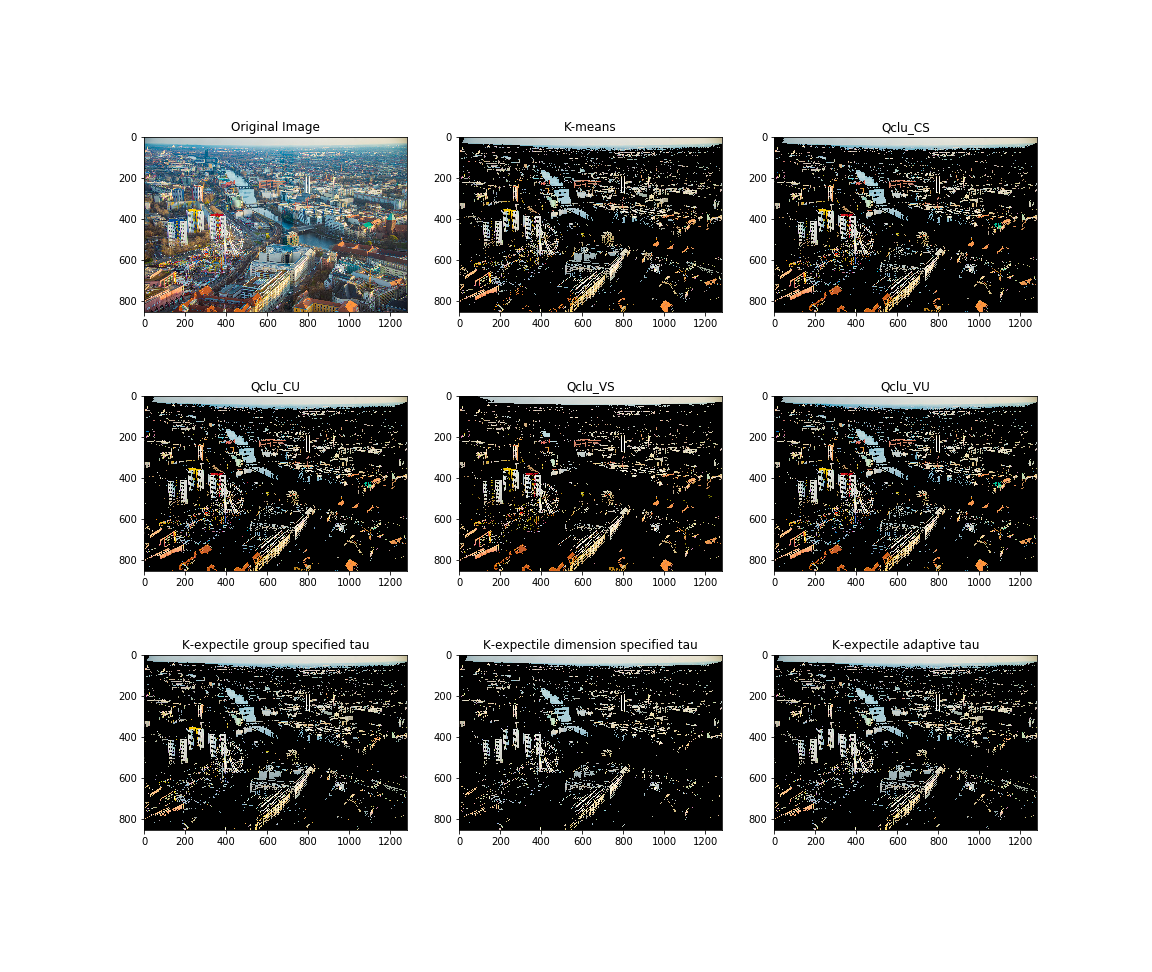

The original image is an aerial photo of Berlin, for pre-processing, we transform the image into pixel values in RGB color space, and flatten the data into a two-dimensional array. Figure 5 shows the original image and the segmented image, which can be considered as filtered image with 4 color clusters. Important information can be extracted from the image by displaying some clusters and mute others. The subplots showed in Figure 6 are image with only one cluster enabled.

To evaluate the performance of segmentation methods, we use two indices, Mean Square Error (MSE) and Peak to Signal Noise Ration (PSNR). Given an monochrome image , Mean Square Error measures how much the approximation differs from it. is defined as:

Peak to Signal Noise Ration is usually used to measure the quality of the compressed image. is the proportion between maximum attainable powers and the corrupting noise that influence likeness of image. It is defined as following:

where is the maximum possible pixel value of the image , which equals to when the sample is in 8 bits. The higher value of and the lower value of , the better the fitting of the approximated image.

Table 2 shows the and values of segmented image using multiple methods. Although is usually calculated on monochrome data, here we take the average MSE on three RGB dimensions. Moreover, we convert both the original image and the segmented image from RGB data into GRAY and YCrCb color space. From the table, it can be concluded that 1) -expectiles with adaptive perform better compare to both -means and quantile based clustering, 2) with pre-specified parameter , in both senario, -expectile clustering gives us a quite moderate result and more flexibility for one to customize the desired segmentation result.

| GREY | YCrCb | RGB | ||||

|---|---|---|---|---|---|---|

| MSE | PSNR | MSE | PSNR | MSE | PSNR | |

| K-means | 509.18 | 21.06 | 839.12 | 18.89 | 742.53 | 28.96 |

| K-expectiles_vtau | 429.47 | 21.80 | 835.66 | 18.91 | 741.17 | 28.97 |

| CS | 2001.30 | 15.12 | 2886.34 | 13.52 | 2841.61 | 23.14 |

| CU | 2217.68 | 14.67 | 3546.76 | 12.63 | 3639.46 | 22.06 |

| VS | 5338.85 | 10.86 | 2799.57 | 13.66 | 2398.98 | 23.87 |

| VU | 2030.67 | 15.05 | 3332.15 | 12.90 | 3507.04 | 22.22 |

| K-expectiles_gp_spec_tau | 519.81 | 20.97 | 1449.73 | 16.51 | 1203.65 | 26.87 |

| K-expectiles_dim_spec_tau | 876.31 | 18.70 | 1304.86 | 16.97 | 1214.55 | 26.83 |

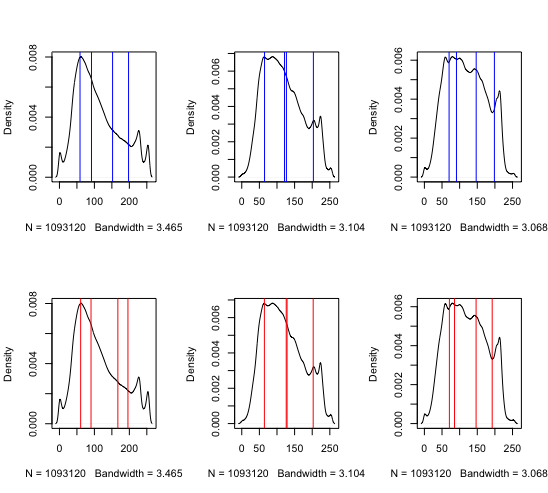

Marginal distribution of R-G-B three dimensional scores has been shown in Figure 7. Blue and red vertical lines are the locations of cluster centers of -means and -expectiles with adaptive . The resulting skewness parameter

, while for -means, equals to for each cluster and each dimension. -expectile clustering again shows more adaptibility to adjust to the skewness of the data.

References

- Aigner et al. (1976) Aigner, D. J., T. Amemiya, and D. J. Poirier (1976): “On the estimation of production frontiers: maximum likelihood estimation of the parameters of a discontinuous density function,” International Economic Review, 377–396.

- Deisenroth et al. (2020) Deisenroth, M. P., A. A. Faisal, and C. S. Ong (2020): Mathematics for machine learning, Cambridge University Press.

- Hartigan (1975) Hartigan, J. A. (1975): Clustering algorithms, John Wiley & Sons, Inc.

- Hennig et al. (2019) Hennig, C., C. Viroli, L. Anderlucci, et al. (2019): “Quantile-based clustering,” Electronic Journal of Statistics, 13, 4849–4883.

- Kim et al. (2019) Kim, A., S. Trimborn, and W. K. Härdle (2019): “VCRIX-A Volatility Index for Crypto-Currencies,” Available at SSRN 3480348.

- Koenker and Bassett Jr (1978) Koenker, R. and G. Bassett Jr (1978): “Regression quantiles,” Econometrica: journal of the Econometric Society, 33–50.

- Kuan et al. (2009) Kuan, C.-M., J.-H. Yeh, and Y.-C. Hsu (2009): “Assessing value at risk with CARE, the conditional autoregressive expectile models,” Journal of Econometrics, 150, 261–270.

- MacKay and Mac Kay (2003) MacKay, D. J. and D. J. Mac Kay (2003): Information theory, inference and learning algorithms, Cambridge university press.

- Maume-Deschamps et al. (2016) Maume-Deschamps, V., D. Rullière, and K. Said (2016): “Multivariate extensions of expectiles risk measures,” arXiv preprint arXiv:1609.07637.

- Newey and Powell (1987) Newey, W. K. and J. L. Powell (1987): “Asymmetric least squares estimation and testing,” Econometrica: Journal of the Econometric Society, 819–847.

- Schnabel (2011) Schnabel, S. (2011): Expectile smoothing: new perspectives on asymmetric least squares. An application to life expectancy, Utrecht University.

- Shi and Malik (2000) Shi, J. and J. Malik (2000): “Normalized cuts and image segmentation,” IEEE Transactions on pattern analysis and machine intelligence, 22, 888–905.

- Sobotka and Kneib (2012) Sobotka, F. and T. Kneib (2012): “Geoadditive expectile regression,” Computational Statistics & Data Analysis, 56, 755–767.

- Steinhaus (1956) Steinhaus, H. (1956): “Sur la division des corps materiels en parties. Bull. Acad. Polon. Sci., C1. III vol IV: 801-804,” .

- Tran et al. (2019) Tran, N. M., P. Burdejová, M. Ospienko, and W. K. Härdle (2019): “Principal component analysis in an asymmetric norm,” Journal of Multivariate Analysis, 171, 1–21.

- Trimborn and Härdle (2018) Trimborn, S. and W. K. Härdle (2018): “CRIX an Index for cryptocurrencies,” Journal of Empirical Finance, 49, 107–122.

- Ward Jr (1963) Ward Jr, J. H. (1963): “Hierarchical grouping to optimize an objective function,” Journal of the American statistical association, 58, 236–244.

- Yang et al. (2018) Yang, Y., T. Zhang, and H. Zou (2018): “Flexible expectile regression in reproducing kernel Hilbert spaces,” Technometrics, 60, 26–35.

- Zhang et al. (2019) Zhang, Y., H. J. Wang, and Z. Zhu (2019): “Quantile-regression-based clustering for panel data,” Journal of Econometrics, 213, 54–67.

- Ziegel (2016) Ziegel, J. F. (2016): “Coherence and elicitability,” Mathematical Finance, 26, 901–918.

5 APPENDIX A: proofs for Section 2

In order to proof the convergence of the algorithm, we first recall the objective function:

Then define

Let be the previous partition, and be previous estimated centroid and parameters, be the new partition,

New partition minimises over all possible partitions:

Hence,.

6 Figures

7 Tables

| =1500 | = 300 | |||||

|---|---|---|---|---|---|---|

| =10 | =50 | =100 | =10 | =50 | =100 | |

| ARI | ARI | ARI | ARI | ARI | ARI | |

| K-expectiles_vtau | 99.36 | 99.60 | 99.87 | 97.00 | 97.99 | 97.99 |

| K-means | 99.36 | 99.60 | 99.60 | 97.00 | 97.99 | 97.99 |

| Spectral | 31.22 | 86.74 | 27.48 | 85.03 | ||

| h-ward | 99.20 | 99.60 | 99.87 | 93.54 | 97.99 | 97.99 |

| CS | 99.24 | 99.60 | 99.87 | 96.61 | 97.99 | 97.99 |

| CU | 99.24 | 99.60 | 99.87 | 96.61 | 97.99 | 97.99 |

| VS | 99.28 | 99.60 | 99.87 | 96.03 | 97.99 | 97.99 |

| VU | 99.20 | 99.60 | 99.87 | 96.61 | 97.99 | 97.99 |

| =1500 | = 300 | |||||

|---|---|---|---|---|---|---|

| =10 | =50 | =100 | =10 | =50 | =100 | |

| ARI | ARI | ARI | ARI | ARI | ARI | |

| K-expectiles_vtau | 93.22 | 99.60 | 99.60 | 92.20 | 97.99 | 97.99 |

| K-means | 91.19 | 99.59 | 99.60 | 81.70 | 97.99 | 97.99 |

| Spectral | -0.02 | |||||

| h-ward | 77.19 | 99.52 | 99.60 | 76.98 | 97.01 | 97.99 |

| CS | 86.61 | 99.58 | 99.60 | 88.98 | 97.99 | 71.74 |

| CU | 80.73 | 99.28 | 94.70 | 72.76 | 93.36 | 76.27 |

| VS | 88.86 | 99.59 | 99.57 | 93.16 | 91.71 | 97.99 |

| VU | 85.74 | 99.55 | 99.60 | 80.41 | 93.73 | 97.99 |

| =1500 | = 300 | |||||

|---|---|---|---|---|---|---|

| =10 | =50 | =100 | =10 | =50 | =100 | |

| ARI | ARI | ARI | ARI | ARI | ARI | |

| K-expectiles_vtau | 94.04 | 99.60 | 99.60 | 93.17 | 97.99 | 97.99 |

| K-means | 94.79 | 99.60 | 99.60 | 93.16 | 97.99 | 97.99 |

| Spectral | 93.63 | 99.60 | 99.60 | 93.17 | ||

| h-ward | 94.80 | 99.60 | 99.60 | 88.88 | 97.99 | 97.99 |

| CS | 68.92 | 96.89 | 82.52 | 92.20 | 97.99 | 65.54 |

| CU | 68.14 | 94.08 | 73.26 | 92.17 | 93.36 | 65.62 |

| VS | 93.28 | 97.47 | 79.84 | 91.98 | 91.71 | 62.46 |

| VU | 94.03 | 94.69 | 73.28 | 92.56 | 93.73 | 46.90 |

| n =1500 | n = 300 | |||||

| p=2 | p=10 | p=50 | p=2 | p=10 | p=50 | |

| ARI | ARI | ARI | ARI | ARI | ARI | |

| K-expectiles_vtau | 96.50 | 97.99 | 97.99 | 95.10 | 97.99 | 97.99 |

| K-means | 96.26 | 97.99 | 97.99 | 94.80 | 97.99 | 97.99 |

| Spectral | 96.21 | 26.31 | 94.81 | 93.10 | 92.43 | |

| h-ward | 96.24 | 97.99 | 97.99 | 94.29 | 97.99 | 97.99 |

| CS | 96.48 | 97.99 | 97.99 | 95.01 | 97.99 | 97.99 |

| CU | 96.08 | 97.99 | 97.99 | 94.57 | 97.99 | 97.99 |

| VS | 96.48 | 97.99 | 97.99 | 95.10 | 97.99 | 97.99 |

| VU | 96.07 | 97.99 | 97.99 | 94.57 | 97.99 | 97.99 |

| n =1500 | n = 300 | |||||

| p=2 | p=10 | p=50 | p=2 | p=10 | p=50 | |

| ARI | ARI | ARI | ARI | ARI | ARI | |

| K-expectiles_vtau | 95.80 | 99.60 | 99.60 | 94.58 | 99.60 | 99.60 |

| K-means | 95.19 | 99.60 | 99.60 | 94.01 | 99.60 | 99.60 |

| Spectral | 94.89 | 26.31 | 93.82 | |||

| h-ward | 96.82 | 99.60 | 99.60 | 95.25 | 99.60 | 99.60 |

| CS | 97.96 | 99.60 | 99.60 | 96.03 | 99.60 | 99.60 |

| CU | 95.42 | 99.60 | 99.60 | 94.19 | 99.60 | 99.60 |

| VS | 97.72 | 99.60 | 99.60 | 95.64 | 99.60 | 99.60 |

| VU | 95.44 | 99.60 | 99.60 | 94.19 | 99.60 | 99.60 |