Algorithmic Challenges in Ensuring Fairness

at the Time of Decision

Abstract

Algorithmic decision-making in societal contexts such as retail pricing, loan administration, recommendations on online platforms, etc., often involves experimentation with decisions for the sake of learning, which results in perceptions of unfairness amongst people impacted by these decisions. It is hence necessary to embed appropriate notions of fairness in such decision-making processes. The goal of this paper is to highlight the rich interface between temporal notions of fairness and online decision-making through a novel meta-objective of ensuring fairness at the time of decision. Given some arbitrary comparative fairness notion for static decision-making (e.g., students should pay at most 90% of the general adult price), a corresponding online decision-making algorithm satisfies fairness at the time of decision if the said notion of fairness is satisfied for any entity receiving a decision in comparison to all the past decisions. We show that this basic requirement introduces new methodological challenges in online decision-making. We illustrate the novel approaches necessary to address these challenges in the context of stochastic convex optimization with bandit feedback under a comparative fairness constraint that imposes lower bounds on the decisions received by entities depending on the decisions received by everyone in the past. The paper showcases novel research opportunities in online decision-making stemming from temporal fairness concerns.

1 Introduction

In recent years, a wide range of organizations has deployed sophisticated data-driven algorithms that repeatedly output decisions having a serious impact on human lives. For example, a recommendation engine shows job advertisements to a stream of arriving customers to maximize their click-through-rates and platform engagement [1]; a retail pricing algorithm repeatedly offers a good at different prices over time to arriving customers to learn the most profitable price [2]; a resume screening algorithm screens out unqualified candidates to provide the most lucrative subset to hiring managers [3]. This widespread pursuit of efficiency and optimality has largely ignored a long-standing issue with decision-making with partial information: the perceptions of unfairness that may arise as a result of experimenting with decisions for the purpose of information-gathering in an online framework.

For example, a demand learning algorithm may experiment with different prices over time to determine the optimal price for a good. While such experimentation is necessary to learn the optimal price, arbitrarily changing prices may create a sense of unfairness amongst customers, e.g., a customer may receive a price much higher than a previous customer who arrived before her for no apparent reason. Indeed, there has been extensive research in behavioral sciences investigating consumer perception of price fairness, which has concluded that notions of price fairness essentially stem from comparison: without explicit explanations, customers think they are similar to other customers buying the same item, and thus should pay equal prices [4, 5, 6, 7, 8]. In the above scenario, there is likely no palatable explanation that the firm can provide to justify the temporal disparities that arise in the search for the profit-maximizing price.

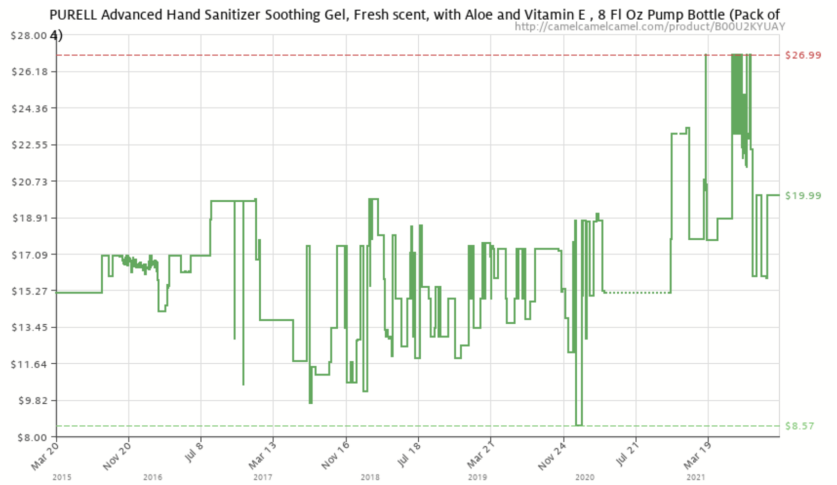

Such issues with increased experimentation are further complicated by the growing litigation and policymaking surrounding algorithmic decisions; e.g., Amazon was recently sued for allegedly price-gouging during the pandemic, as they increased the price of essential goods by more than 450% (e.g., see Figure 1) compared to previously seen prices (McQueen and Ballinger v. Amazon.com111McQueen and Ballinger v. Amazon.com, Inc., 422 U.S. Case 4:20-cv-02782 (2020).). Such misalignment of business practices geared towards profitability, and evolving consumer protection laws (e.g., [9]) raises a natural question for various operational tasks: can firms enforce appropriate fairness desiderata in their online decision-making systems while still achieving good operational performance? In this work, we make two broad contributions to our understanding of this question.

-

(1)

First, we define a general meta-notion of fairness for temporal decision-making called fairness at the time of decision (FTD) to mitigate perceptions of unfairness when an entity receives a decision. In particular, FTD requires that when an entity A receives a decision that affects them at time , comparing this decision to the available data on decisions received by other entities at or before time must not reveal any problematic disparity in the treatment of entity A. This requirement amounts to a basic prerogative from the perspective of any principal who makes these decisions and is interested in guaranteeing immunity to legal claims of discrimination at the time of the decision. The notion of “problematic disparity" can be modeled by any task-specific notion of fairness for static decision-making, generally requiring that each entity gets a decision that is (approximately) as conducive as that received by others. Thus, FTD adapts to the growing literature on task-specific variants of comparative fairness across a variety of operational applications such as demand learning [10], assortment optimization [11], kidney exchange [12], etc. Importantly, since fairness is not required to be guaranteed from the perspective of an entity after the entity receives the decision, FTD generally allows decisions to become more conducive over time, thus allowing room for (constrained) experimentation and learning.

-

(2)

Enforcing FTD across time results in a rich class of online optimization problems where decisions must follow a constrained trajectory. This results in the natural question: Is it even possible to ensure FTD in online decisions without sacrificing performance?” As our second contribution, we exemplify the algorithmic challenges in restricting decision trajectories across time in the context of stochastic convex optimization.

We consider a setup where a principal seeks to optimize real-valued decisions corresponding to groups of populations. Each group corresponds to an a priori unknown (expected) cost function. We assume that higher decisions are more conducive from the perspective of the groups and we consider a generic comparative notion of fairness that we refer to as envy freeness, which imposes lower bounds on the decision received by each group depending on the decisions received by others. We assume a bandit feedback model where the principal only observes the function value at any decision point corrupted by zero-mean sub-Gaussian noise. This setup can, for example, model a dynamic pricing scenario for multiple customer segments under demand uncertainty, where the firm wants to maximize revenue while satisfying a recently proposed notion of price fairness [10] relative to the past sales data at the time of each purchase (the revenue maximization objective can be equivalently posed as a cost minimization objective).

Focusing on the case where the cost functions are known to be smooth and strongly convex, we show that significant and non-trivial algorithmic innovations are necessary to satisfy FTD while achieving good regret bounds. A key challenge arises because of bandit feedback since it entails the construction of accurate gradient estimates while satisfying the FTD constraint. In addition, the approach to optimality as the decisions become more conducive must be cautious since if the algorithm overshoots the optimal point, then it cannot backtrack, again due to the FTD constraint. We first design novel approaches to tackle these challenges for the case of two population groups and we show that our algorithms attain a regret bound, which is known to be the best achievable without the fairness constraint [13]. We then consider the multi-group case beyond two groups, for which we design a simpler regret algorithm, although we conjecture that regret is achievable using similar ideas as the case of two groups at the cost of a significantly more complex algorithm definition. Our analysis thus illustrates the nature of design tradeoffs that arise in satisfying FTD while ensuring low impact on the utility.

We conclude the paper by discussing various open problems in extending FTD to other practical contexts, open problems arising from related temporal fairness notions, and extensions of FTD. We point to a rich space of exciting problems and research opportunities at the interface of temporal fairness and online optimization.

Organization. The paper is organized as follows. We first discuss related literature in the remainder of this section. In Section 2, we introduce a generic static decision-making scenario and an abstract notion of static fairness whose temporal extensions we will consider. In Section 3 we motivate and introduce the notion of fairness at the time of decision. In Section 4 we define the multi-group stochastic convex optimization problem under bandit feedback and we also introduce the comparative notion of envy freeness. In Section 5, we tackle algorithm design for the case where there are two groups of populations. Our main methodological ideas are developed in this section. Algorithm design for the multi-group case is considered in Section 6. In Section 7, we present numerical experiments validating our approaches using a retail pricing dataset. We finally discuss related problems and extensions in Section 8. The detailed proofs of all our results can be found in the Appendix.

1.1 Related Work

Fairness in static decision-making. Notions of fairness in static decision-making typically ensure that various stakeholders are treated equitably [14]. Two broad varieties of notions have appeared in this regard. First is the popular notion of individual fairness [15], which requires that similar individuals must receive similar treatments. Formally, if is the decision received by individual , then individual fairness requires that for any two individuals and , where is some constant, and is a similarity metric that captures some publicly acceptable notion of “distance" between two individuals that dictates the allowable disparity between their decisions. The second notion is group fairness, also known as statistical parity [16, 17], under which one demands parity in certain statistics of the decisions across multiple groups of people, e.g., requiring that two groups of populations in the same role have similar average salaries in an organization. Such parity notions have been proposed in the context of multi-segment pricing recently by [10] and [18]. For example, the notion of price fairness considered by [10] imposes bounds on the price disparity seen across segments, i.e., they require that for any two customer segments and where is some constant. The common aspect of these two notions is that they impose bounds on the degree of envy felt by entities – either individuals or groups – when comparing their decision to others. In Section 2, we consider a generalization of such notions of fairness.

Temporal notions of fairness in dynamic decision-making. Broadly, four different types of temporal notions of fairness have appeared in the literature on online decision-making. The first type of constraint is a time-independent fairness constraint in which a static fairness constraint must be satisfied independently in each period. For example, [19] and [20] consider a multi-segment dynamic pricing problem where the price fairness constraint of [10] must be satisfied in each time period.

In contrast, the second type of fairness constraint is what we refer to as a time-dependent decision-adaptive fairness constraint. FTD is an example of this type of temporal constraint. Such constraint changes depending on the decisions taken in the past, but is agnostic to the outcomes of the decisions. Similar constraints have appeared in recent and parallel literature. For example, [20] requires that the price offered to a particular segment must be close to the prices offered to the same segment over the past time periods (in addition to satisfying the price fairness constraint across segments every time period). Such a sliding-window fairness constraint was also considered by [21] in the context of adaptive supervised learning.

In a similar vein, and the most related to our paper, [22] define the notion of individual fairness in hindsight in the context of contextual bandit problems. This is a temporal version of the static notion of individual fairness that guarantees individual fairness at the time of decision based on some underlying similarity metric. Our meta-objective of FTD is a significant generalization of this notion that goes beyond individual fairness objectives for static decision-making (e.g., unlike individual fairness, we can model additive as well as multiplicative notions of envy-freeness in our framework, with asymmetric allowable disparities across groups). Moreover, the technical analysis of [22] is restricted to a simple and abstract contextual bandit setup where the decision-maker tries to distinguish between a finite set of utility models. Our framework, on the other hand, allows us to consider a general stochastic convex optimization setup that is applicable in a broader variety of settings.

The third type of temporal fairness constraint is what we refer to as a time-dependent outcome-adaptive fairness constraint, where the constraint can change as the outcomes from the decisions change. For example, [23] has introduced a fairness constraint in a contextual bandit setting requiring that preferential treatment be given to an arriving entity only if it is known with high enough certainty that such preferential treatment is justified by current estimates of the mean rewards resulting from the treatment. Thus, as entities are administered decisions over time, certainty in their reward distributions increases, and they can eventually be treated differently. A Bayesian version of this idea was proposed by [24] in the non-contextual bandit setting, in which decisions are constrained to be fair with respect to the posterior reward distributions of the arms at any time. In this way, as the posterior distributions converge to the true distributions, violations of the desired fairness constraint should diminish. In a similar vein, [25] consider a problem of ensuring group fairness in hiring, where uncertainty is modeled using a partial order and decisions are constrained to be consistent with the partial order at any time.

The fourth type of temporal fairness constraint asks for fairness of certain decision statistics, either ex ante or ex post, across arriving entities over time. For example, [26] considers a sequential resource allocation setting where entities arrive over time with certain demands and the goal is to maximize the minimum fill rate. [27] similarly considers the problem of maximizing the minimum service rate across different groups in an online bipartite matching setting. The main difference from the other three types of constraints is that one doesn’t necessarily seek to guarantee comparative fairness for an entity arriving at a point in time, but rather one guarantees fair treatment of groups of entities across time. A general framework for satisfying such time-average fairness constraints in the context of kidney transplantation has been proposed by [28].

Decision-constrained stochastic convex optimization. Our work makes fundamental contributions to decision-constrained stochastic convex optimization under bandit feedback. In general, none of the existing algorithms from the convex optimization toolkit can be easily modified to satisfy FTD. For example, FTD may require that decisions are monotonically increasing in each dimension as we see in Section 5. Even this requirement cannot be met by simple modifications of existing algorithms. In the noiseless bandit feedback setting, Kiefer gave an -regret algorithm, now well known as Golden-Section Search, for minimizing a one-dimensional convex function [29]. This algorithm iteratively uses three-point function evaluations to “zoom in” to the optimum, by eliminating a point and sampling a new point in each round. Its mechanics render it infeasible to implement it in a fashion that respects the monotonicity of decisions. For higher dimensions, a -regret algorithm has been designed by [30]. This algorithm is based on gradient-descent using a one-point gradient estimate constructed by sampling uniformly in a ball around the current point. This key idea recurringly appears in several works on convex optimization with bandit feedback (e.g., [31], [32], [33]). However, due to the randomness in the direction chosen to estimate the gradient, such an approach does not satisfy monotonicity.

For the case of noisy bandit feedback, [13] has shown a lower bound of in the single-dimensional setting that holds for smooth and strongly convex functions and showed that an appropriately tuned version of the well-known Kiefer-Wolfowitz [34] stochastic approximation algorithm achieves this rate. This algorithm uses two-point function evaluations to construct gradient estimates, which are then utilized to perform gradient-descent. Our near-optimal algorithms in Section 5 are the most related to this approach, where we tackle the significant additional challenge that the two-point evaluations need to consistently satisfy monotonicity over time while attaining the same regret bounds (up to logarithmic factors). For the case of convex functions, Agrawal et al. designed an algorithm that achieves the bound under bandit feedback [35]. In the one-dimensional case, their approach is the most related to the golden-section search procedure of [29], and as such, is infeasible to implement in a monotonic fashion.

Though not motivated by fairness concerns, two recent parallel works have considered the problem of ensuring monotonicity of decisions in stochastic optimization under bandit feedback ([36] and [37]).222It may be worth mentioning that the first public drafts of both these works appeared after the first public draft of an earlier version of our paper [38], although it is most likely that the research was conducted in parallel. Assuming that the functions are only known to be Lipschitz and unimodal they find that the optimal achievable regret is , which is higher than the regret achievable without the monotonicity requirement. In contrast, Theorem 2 implies that under the assumption that the cost functions are smooth and strongly convex, the unconstrained optimal regret bound of is attainable while ensuring monotonicity of decisions (up to logarithmic terms). We also note that, because the settings considered by these other works are more pessimistic in their view of the possible cost functions, algorithm-design for optimizing the worst-case turns out to be simpler. In particular, both [36] and [37] show that we cannot do better than the simple approach of sequentially traversing the decision space in a fixed direction and using a fixed step size until the utility keeps increasing (as determined by a sequence of two-point hypothesis tests). In contrast, the problem of leveraging gradient information while maintaining monotonicity, while also ensuring negligible impact on regret, results in several novel and non-trivial aspects of our algorithm design.

2 Fairness in static decision-making

Consider a static decision-making scenario, where there is a finite set of entities representing the stakeholders receiving the decisions. For example, an entity could represent a customer segment (such as “youth”) in a pricing scenario or a job applicant in an applicant-screening scenario. The decisions lie in the set (e.g., the range of prices that can be offered to a customer, or accept/reject decisions for screening). There is a principal (such as a firm or a platform) who chooses a decision rule that maps entities to decisions. We represent such a rule by the vector , where is the decision assigned to entity . There is an evaluator function that measures the utility from a decision rule, which represents some operational performance measure such as social welfare, efficiency, principal utility, etc.

The decision rule is required to satisfy a task-specific notion of comparative fairness. Such a notion typically imposes certain entity-specific equity constraints, which ensure that each entity is treated equitably when compared to others. Consider the following two examples from recent literature.

-

1.

Fair pricing. Consider a product pricing scenario with customer segments. Let be the price offered to segment . To ensure comparative fairness from the perspective of segment , we may require certain upper bounds on the price offered to depending on the prices offered to the other segments. For instance, we may require that , where represents a permissible additive slack that depends on the two segments in comparison; e.g., if the two segments are youth (1) and adults (2), we may require that , i.e., the price offered to the youth segment must be at most that offered to the adults. Similarly, we may require that , i.e., while the adults can be priced higher than the youth, the difference cannot be larger than $. Such a notion of price fairness has been recently proposed by [10] under the assumption that the slacks are non-negative and symmetric (so that the constraints amount to requiring that for all segments ). We will consider such a notion of comparative fairness in the context of stochastic convex optimization in Section 4.1.

-

2.

Fair assortment planning. [11] consider a platform making an assortment planning decision from amongst products/sellers to show to a customer. Each product has some weight that measures how popular the product is to customers; in particular, upon offering the customers an assortment of products, the customers purchase product according to the Multinomial Logit Choice (MNL) model, with probability where . Given a probabilistic assortment choice of the platform, suppose that is the probability that is included in the assortment, referred to as the visibility offered to product . [11] propose a notion of fairness that requires that for every product and for some ,

for all . That is, must get at least as much visibility (with a slack) as after adjusting for their relative differences in popularities, for every .

To generally capture such comparative notions of fairness exemplified by these settings, let’s suppose that for each entity , there exists a set of real-valued functions, , for , each of which maps (a) the decision received by entity , and (b) the profile of decisions received by all the entities, to a real number. We then assume that the fairness notion requires that

| (1) |

For example, imposes a constraint that decision of th entity is at least 0.9 times the maximum decision received by any other entity. The idea is that the entity-specific constraints capture the fairness requirements from the perspective of entity on comparing its decision with the decision profile across all entities. We include the decision for entity twice in the argument of because later when we incorporate time, we may want to compare the decision received by entity at time against that received at some other time .

The static optimization problem of maximizing the utility of a decision rule subject to fairness constraints can then be expressed as follows.

| (2) | ||||

| subject to | (3) |

When and are well-behaved functions, one can find a solution using standard optimization techniques.

3 Fairness at the time of decision in dynamic decision-making

The introduction of time in the above setup makes it more interesting. Suppose that the principal chooses decision rules over a time horizon of multiple periods, . Let’s denote the decision rule at time as . First, note that if there is no reason to choose different decision rules across time periods, e.g., in settings where the utility function is unchanging and known to the principal, then the time dimension is redundant since the principal can simply choose the same static-optimal fair decision rule at each time. However, if (a) is unknown to the principal and the optimal fair decision rule must be learned over time, or (b) if is known but it changes over time, then the ability to change decision rules may be fundamental to attaining good utility. Thus a temporal fairness constraint should ideally allow room for some changes in decisions over time. At the same time, it should satisfy a meaningful desideratum of equity and non-discrimination from the perspective of the entities. We now present our main proposal in this regard.

Definition 1 (Fairness at the time of decision (FTD)).

Consider a static notion of fairness captured by the functions for and . A sequence of decision rules satisfies fairness at the time of decision if for all ,

| (4) |

FTD requires that the fairness constraints from the perspective of entity at time are satisfied not only with respect to the decisions received by others at time , but also with respect to decisions that were received at any time in the past. For example, consider salary administration in an organization where a non-discrimination requirement dictates that women’s average salary for a role must be at least as much as men’s and vice versa (effectively implying that their average salaries should be equal). FTD in such a scenario would require that women’s average salary in the year 2022 must be at least as high as that of men in 2020 (or any year 2022), but men’s average salary in 2020 need not be as high as that of women in 2022. This effectively means that while the average salary of men and women must be identical within a year, it can increase over years. The attractive feature of this definition is that, when the salaries are decided in a year, both the groups are revealed to be treated fairly with respect to all of the past salary data: they get at least as much pay as that received by anyone in the past. However, the salaries may increase further in the later years, leading to the current salary decisions turning out to be unfair in retrospect in light of the future data.

To further appreciate the notion of FTD, we contrast it against other natural temporal extension of static fairness. The first and most basic possibility in this regard is to simply ignore the temporal aspect and ensure that the static fairness constraints are satisfied for each group independently in each time period. That is, we require that for all , , and across all times . This allows for decisions to change arbitrarily between time periods and hence is typically insufficient as a notion of fairness, e.g., it may be difficult to justify that the price of a smartphone seen by a particular customer segment is higher than that seen by the same segment the day before for no apparent reason.

The second possibility lies on the opposite end of the spectrum, requiring that the fairness of a decision must be satisfied with respect to decisions across all times. That is for each ,

| (5) |

While ideal from a fairness perspective, this requirement is too stringent since it often disallows any change in decisions over time [22]. For instance, in the context of salary administration, this requirement means that women’s average salary in the year 2022 must be at least as high as that of men in 2020 and vice versa, effectively implying that the average salaries of men and women must be the same fixed value across all time.

Fairness at the time of the decision thus occupies a convenient middle ground that straddles the extremes of temporal notions of fairness discussed above. As we will see in the next section, FTD leads to technically new challenges in online optimization: it offers enough flexibility in decisions that could potentially allow for some experimentation and learning, and at the same time these intertemporal constraints are novel in the context of online optimization and require new design tools and techniques to assimilate them while ensuring good utility guarantees.

4 Application to multi-group stochastic convex optimization with bandit feedback

We now consider algorithm design for satisfying FTD within the framework of stochastic convex optimization under bandit feedback. We consider the setup of a principal that administers decisions to a finite set of population groups over a horizon of periods. Decisions lie in the set for each group. We further assume that there is a directionality in the conduciveness of decisions from the perspective of the groups, and without loss of generality, we assume that higher decisions are perceived to be better by any group (e.g., a higher salary). Each group is also associated with a cost function (or equivalently a utility function ) that captures the utility to the principal. In terms of our earlier notation, the goal of the principal is to maximize . The setup can, for example, model a firm setting prices for customer segments with revenue function corresponding to group (one can define ), where the prices lie in some set . In this scenario, a lower price is perceived to be better by any customer.

If these cost functions are known to the principal, and if there are no additional constraints on the decisions, then the principal can simply choose the optimal decision of for each segment . We next define the static optimization problem of choosing decisions to minimize cost while satisfying certain comparative fairness constraints.

4.1 Static optimization under envy-freeness

We will consider a static fairness notion of envy freeness while allowing for certain additive disparities. Envy freeness is a commonly studied notion of fairness in the literature on social choice and fair division of resources, which requires that an entity should not envy an allocation received by someone else, i.e., prefer someone else’s allocation over their own allocation [39, 40, 41]. In our setting, since higher decisions are perceived to be better by any group, each group will envy every group that receives a higher decision. Thus, to eliminate envy is to ensure equal decisions across groups. However, instead of eliminating envy, we consider a generalization that allows for certain limits on the envy between any two groups. In particular, we define the “slack” functions defined on ordered pairs of groups: , where we assume that for all . Consider then the following definition.

Definition 2 (Envy Freeness with Additive Slacks).

We say that a decision vector satisfies envy-freeness (EF) with additive slacks if the following inequalities hold:

| (6) |

Despite the existence of slacks, we will refer to this notion as envy freeness (EF) for convenience. These constraints say that, e.g., group should not receive a decision that is much lower than group , with the slack specifying how much difference is permissible. The slack need not be symmetric, i.e., may not necessarily equal . In the pricing example, since lower decisions are more conducive, if is the price received by group , then the corresponding constraint would be that . (Note that the direction of this constraint does not matter from an algorithmic perspective: our algorithms can be trivially modified to temporally satisfy the EF constraint in any fixed direction.) As noted earlier, EF in the context of pricing thus generalizes the price fairness proposal of [20], in which the slack functions are assumed to be symmetric.

Note that the constraints eq. 6 are always feasible since the principal can make the same decision for each group. These constraints are also linear and hence, convex. Let the set of decision vectors in satisfying the EF constraints in eq. 6 be denoted as . Then the problem of cost minimization under the EF constraints is defined as

| (7) |

Assuming that are well-behaved, e.g., convex, the set of optimal fair decisions can be easily computed if these are known. The challenge is in ensuring temporal fairness constraints when are unknown and must be learned over time.

4.2 Ensuring Envy Freeness at the time of decision in multi-group stochastic convex optimization with bandit feedback

We now formulate the problem of stochastic convex optimization with bandit feedback under the constraint of ensuring envy freeness at the time of decision. Consider the setting where the cost functions are unknown to the principal. The principal hopes to learn to administer the solution to (7) under the temporal fairness constraint over a discrete time horizon . We make the following assumptions on the cost functions .

Assumption 1.

We assume that for all , the function is

-

1.

-strongly convex, i.e., for all , and

-

2.

-smooth, i.e., for all ,

for some and known to the principal.

These assumptions are commonly made in the convex optimization literature and they allow us to focus on the difficulties that arise in adapting gradient-driven online optimization procedures to satisfy the FTD constraint. In the context of pricing, the corresponding assumption is that the revenue functions are strongly concave and smooth. This assumption is satisfied under the popular linear demand model that is commonly assumed in the pricing literature [42, 43]. Even beyond linear demand models, we argue in Appendix D that this may be a reasonable assumption in many dynamic pricing scenarios where the firm has past sales data on similar products.

Envy freeness at the time of decision (EFTD). Given the notion of envy freeness for static decision-making, the notion of FTD amounts to the following temporal fairness notion.

Definition 3.

A sequence of decisions is said to satisfy envy freeness at the time of the decision (EFTD) if

| (8) |

The idea is that the decisions received at at time need to satisfy the EF only relative to the decisions administered at times .

Dynamics and feedback. At each time period , the algorithm produces a decision and observes bandit feedback, i.e., the function values for each at the chosen decision potentially corrupted with noise. In particular, we assume that the feedback observed is a random variable , where for each is a sequence of random variables representing the noise in the feedback. Note that the distribution of can potentially depend on . We make the following commonly made assumption on this sequence.

Assumption 2.

For each , and a sequence of decisions , the random variables are independent, have zero mean, and are sub-Gaussian: there exists a constant such that for all . We also assume that they have bounded norm , where .

Objective and constraints. The problem is an online decision-making problem, in that the decision at time is made using the historic information . These decisions are further constrained to respect the EFTD constraint: . The regret incurred by an algorithm is defined to be

| (9) |

where the expectation is over the randomness in , and where recall that denotes the set of decision vectors that satisfy the EF constraint.

Our objective is to design an algorithm that minimizes regret in the worst case over all -strongly convex and -smooth functions while ensuring that the decisions satisfy the EFTD constraint. We say that an algorithm is a -regret algorithm if its regret is at most .

5 A near-optimal EFTD algorithm with two groups

Ensuring EFTD imposes complex constraints across decisions over time. In this section, we tackle the challenges that arise in designing a near-optimal regret algorithm for the simplest case of two population groups. First, let’s examine what the EFTD constraints require in this setting. These constraints can be broken down into two parts:

-

1.

Coordinate-wise monotonicity. We first require that for and for , which means that the decisions on each coordinate must (weakly) increase over time.

-

2.

Cross-coordinate constraints. We also have that and for all , which means that the decision for group at any time can be at most less than the highest decision seen by group so far.333We adopt the convention of “Group ” indicating the group other than Group . So, Group refers to Group 2, and Group refers to Group 1.

Because several ideas will be necessary for designing a near-optimal regret algorithm that satisfies these constraints with just bandit feedback, we break down this problem into parts. First, we will consider a single-group online stochastic optimization problem where the only constraint is to satisfy weak monotonicity. The algorithmic approach we develop for that case will then be used as a component in the two-group case where we additionally have to tackle the cross-coordinate constraints.

5.1 Single group monotonic stochastic optimization with bandit feedback.

In this section, we consider the problem of minimizing a smooth and strongly convex function over the feasible set under noisy bandit feedback, while ensuring that the decisions monotonically (weakly) increase over time and while ensuring low regret. We denote . As we noted earlier in Section 1.1, none of the existing stochastic optimization algorithms designed for this setting satisfy monotonicity.

Algorithmic approach. At their core, our algorithm relies on gradient estimates constructed from monotonic two-point function evaluations (i.e., “secant” information) to improve decisions as in the well-known Keifer-Wolfowitz algorithm for convex optimization with noisy bandit feedback [34]. Due to the monotonicity constraint, the challenge is to ensure that sufficient progress is continually made towards reaching the optimal decision using gradient information while avoiding excessively overshooting the optimum (since backtracking is disallowed). There are two key algorithmic ideas we develop to tackle this challenge: (a) taking gradient steps from a “lagged" point to avoid overshooting the optimum, and (b) adapting the lag size to local gradient estimates to tailor the degree of caution to the distance from the optimum point, while ensuring monotonicity.

Warm-up: the case of noiseless bandit feedback. We first consider algorithm design in the noiseless bandit setting: a decision is made at each time , and for each decision , the algorithm observes . The decisions made by the algorithm are constrained to be monotone: .

We present a monotonic procedure called Lagged Gradient Descent (Lgd) (Algorithm 1) for this setting, which is a variation on classical gradient descent. At each round, we use two queries (one at and one at the “lagged” point ) to estimate the gradient. Since we need to ensure monotonicity of iterates, we need to sample first at the lagged point and next at to get an estimate of the gradient. The size of will depend on the time horizon and be optimized for minimizing the regret of the overall scheme. We then move by an amount proportional to the estimated gradient.

While increasing decisions, even in this non-noisy case, we need to be careful about not excessively overshooting the optimum point, which could result in high regret due to the monotonicity constraint that disallows backtracking. To avoid overshooting, we move proportional to the gradient from the lagged point instead of from . Since the estimated gradient in Lagged Gradient Descent is less steep than the true gradient at , the smoothness of allows us to ensure that we never overshoot. However, since we jump from instead of , a small jump (of a magnitude smaller than ) may violate monotonicity. To avoid this, we jump forward only if the gradient is steep enough; in particular, if the magnitude of the estimated gradient is at least , for some , defined in Theorem 1.

Lemma 1 below shows that the decisions resulting from Lagged Gradient Descent (Lgd) are monotonic, they avoid overshooting, and their convergence rate to the optimum is exponential.

Lemma 1.

Let be an -strongly convex and -smooth function. Let be the non-lagged points generated by Lagged Gradient Descent (Algorithm 1), and assume that . Then, for , the following hold:

-

1.

Decisions increase monotonically toward the optimum: ;

-

2.

The convergence rate is exponential up to halting: , where and .

With this convergence rate established, we can calculate a regret bound for Lgd. We can break the regret of this procedure into three categories: regret during exploration, regret due to stopping (i.e., regret incurred after the “for loop” has ended), and regret due to potential overshooting (which is 0 by Lemma 1). We balance these three to obtain an regret bound.

Theorem 1.

Assume that , and fix and . Then Lagged Gradient Descent (Alg. 1) is a -regret EFTD algorithm for optimizing an -smooth and -strongly convex function in the noiseless bandit setting.

Theorem 1 shows that imposing monotonicity has no (asymptotic) effect on the hardness of the noiseless setting: a non-monotonic constant-regret procedure is already known [29], and Lgd is a monotonic constant-regret procedure.

One important aspect of the noiseless setting is that gradient estimation is easy: one simply requires two samples, and additionally, the gap between the samples can be arbitrarily small, resulting in arbitrarily accurate gradients. As we will discuss in the next section, when noise is introduced, there is a trade-off between the magnitude of and the number of samples required to accurately estimate the gradient. This tension ultimately results in a higher regret bound.

The challenges posed by noisy bandit feedback. Recall that in the noisy bandit setting, upon querying the point , the algorithm observes , where the noise is assumed to be independent, mean zero, and sub-Gaussian of bounded sub-Gaussian norm (Assumption 2). To appreciate the complication added by the noise, let’s suppose we try to replicate the approach in Lagged Gradient Descent, in which we utilize secant calculations with a fixed lag size to estimate the gradient step. In the absence of noise, the secant is always sandwiched between the true gradients at and the lagged point by the mean value theorem. Thus moving from the lagged point using the secant ensures that the algorithm never overshoots the optimum. But when the function evaluations are noisy, multiple function evaluations are necessary to evaluate the secant accurately enough for this sandwich property to hold. In particular, one can show that function evaluations are necessary at the two points to get such an accurate secant estimate (Lemma 4 in the appendix). So, if one uses as in the analysis of noiseless Lgd (Theorem 1), the number of samples required at each point is . Such high sampling rates may be acceptable when the algorithm iterates are very close to the optimum, but will lead to a high (linear) regret when the iterates are farther from the optimum. Thus, clearly, cannot be set to be that small.

At the same time if is too large then the algorithm may stop far from the optimum, since the local gradient may prematurely become small enough relative to the lag size that jumping from a lagged point may violate monotonicity (i.e., the condition is satisfied). Such premature stopping will again cause high regret. Later in Section 6, we will see that one can set a fixed that optimizes this tradeoff and obtain a regret of in the multi-group setting.

However, it turns out that we can do strictly better and obtain the near-optimal regret rate of by choosing the lag sizes adaptively. The key idea is that if the algorithm stops moving with a particular lag size , then we reduce the lag size so that the algorithm can continue to proceed. This ensures that smaller lag sizes and correspondingly higher sampling rates are utilized only when the iterates are closer to the optimum when they do not result in high regret.

This approach, however, presents a crucial challenge: when estimating the secant at a point and a lagged point , the decision of whether the lag size must be reduced from to some smaller quantity must be made before we sample at to insure monotonicity of the iterates. To address this challenge, we design a novel algorithm that respects monotonicity while searching for the correct lag size.

Adaptive Lagged Gradient Descent. We develop a novel procedure called Adaptive Lagged Gradient Descent (Ada-Lgd) (Alg. 2) in this section. In this procedure, there are “non-lagged” iterates, denoted as , and “lagged” iterates denoted in relation to the non-lagged iterates, e.g., for some specified . For any non-lagged iterate such that , we say that is the lag size of .

We now describe how Ada-Lgd reduces the lag sizes in a monotonic manner. Suppose the current lag size is , and we are sampling at . Right after sampling at , we sample at (where for some ). This has the benefit of providing a gradient estimate at . This estimate in turn gives us an estimate of the gradient at , which can be used in deciding whether or not the lag size should indeed be reduced to or lower. If yes, then we continue to sample at and continue the search for the right lag size; else, we finally sample at and continue the secant descent procedure. Such pre-emptive sampling to search for the correct lag size thus guarantees monotonicity.

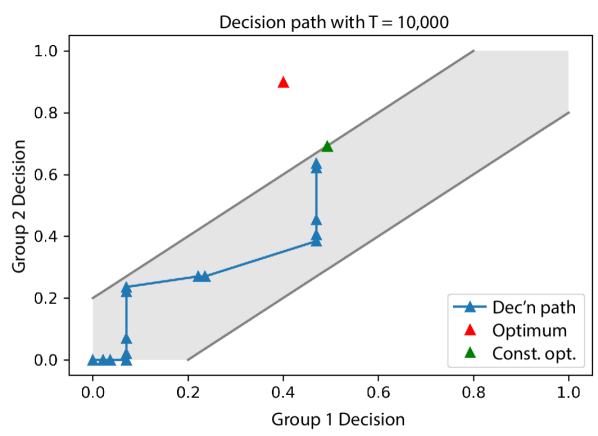

In view of these dynamics, it is useful to think of the iterates with the same lag size as forming a phase, where phases are numbered chronologically: Phase 1 is the phase containing , Phase 2 is the next phase, and so on. The lag size associated to Phase is denoted . Since multiple lag sizes can be skipped between and , it may be the case that . For example, see Figure 2, where the first jump is taken with a lag size of . While sampling at and , since the estimated gradient is not steep enough, the algorithm begins sampling at . The algorithm decreases the lag size twice more before deciding that is an appropriate lag size. In this case, is the “chosen” lagged point. Theorem 2 formalizes the regret guarantee achieved:

Theorem 2.

There are several steps in the proof of Theorem 2, which is presented in Appendix A.2. We first show that all the secant estimates are accurate enough with high probability so that the sandwich property holds, i.e., the secant is indeed sandwiched between the gradients at the two points (Claim 3 in the proof). With this established, we show that overshooting does not occur (Claim 4), that the iterates are monotonic (Claim 5), and that we achieve exponential convergence to the optimum (Claim 6) (again, with high probability) across all the iterates, regardless of lag size. The challenging part is to bound the regret from non-lagged and lagged iterates, which we address separately. For each source of regret, we derive a key phase-dependent regret bound that is inversely proportional to the local gradient in that phase; this bounds the regret from the early phases (Claims 7 and 8). We finally bound the regret from the later phases by leveraging the fact that the iterates are closer to the optimum. Balancing regret between early and late phases yields the regret bound (Claim 9).

5.2 The case of two groups.

Having developed a procedure that achieves near-optimal-regret for single-dimensional monotonic stochastic convex optimization with bandit feedback, we now return to the problem of two groups.

Algorithmic Approach. Assume without loss of generality that (otherwise if both are 0, then we get the single group case).444While we require slacks to be nonnegative, the algorithm allows for negative slacks as well with a minor adjustment. In particular, assuming that the feasible set of decisions is non-empty, we compute the minimum decision on each dimension that is feasible. The algorithm then proceeds from this point. Recall that we have to ensure the constraint and for all . Our overall approach is simply described as a continuous-time procedure in the case where we have access to perfect gradient feedback, i.e., :

-

1.

Coordinate descent phase (continuous-time). Starting with , pick an arbitrary coordinate, say , and increase it while keeping the other coordinate fixed until either (a) , or (b) . Switch the coordinate and repeat until, for both , either or . Once that happens, go to step 2.

-

2.

Combined descent phase (continuous-time). If for both , then we are done – the EF constraint doesn’t bind and the unconstrained optimum is the same as the constrained optimum. Else, there is some such that and (since we assumed at least one slack is non-zero). At that point, we can deduce that the corresponding EF constraint will be tight at the optimum (which means we can again reduce to the single group case). Then define , and continue reducing and jointly until .

-

12(a)

if is a th lagged point (i.e., ) and then

if is a non-lagged point (i.e., ) then

if is the second feasibility iterate (i.e., ) then

It is clear that this continuous-time dynamic finds the constrained optimum while satisfying EFTD. The challenge then is to convert this process into a practical discrete-time procedure with only noisy bandit feedback on each dimension, while ensuring optimal overall regret. To adapt the above continuous-time dynamic to a discrete-time setting with noisy bandit feedback, we use a similar discretization as Ada-Lgd, where for each coordinate, we compute non-lagged iterates and slowly move towards the non-lagged iterates using lagged iterates while searching for the right lag size to estimate the gradient. However, due to the two-group setting, a number of methodological adaptations must be made to overcome the following challenges:

-

(1)

the unconstrained optimality for a particular group, i.e., , can only be approximately detected, which means that more care must be taken before entering the combined phase;

-

(2)

similarly, since the unconstrained optimality for a particular group can only be approximately detected, the trigger for switching between groups in the coordinate descent phase must be adapted as well (recall that reaching optimality for a group triggered the switch to the other group in the continuous-time method);

-

(3)

recall that the analysis of Ada-Lgd depended on controlling the lag sizes and resulting gradient accuracy as the sampling process approached the optimum. Since the two groups may have different derivatives at the current point, their lag sizes may differ significantly as well. This raises an issue as the group with the smaller derivative will spend more time sampling, thus causing the other group to incur regret in the meantime;

-

(4)

moreover, if the two groups have different lag sizes, this disparity must be reconciled when entering the combined phase, where the groups must proceed jointly with a single lag size.

We explain our novel discrete-time bandit algorithm SCAda-Lgd below, which addresses these concerns.

Coordinate descent phase (SCAda-Lgd). In the coordinate descent phase of SCAda-Lgd, each group maintains a queue of points to sample denoted as for group , and the iterate with the minimum value for coordinate is sampled first. As in Ada-Lgd, we call iterates computed using gradient jumps “non-lagged iterates” (i.e, where denotes the estimate of the gradient at ), and we move towards non-lagged iterates using “lagged iterates” (defined by ) to control the accuracy of the gradients. We additionally introduce a new set of iterates, which we refer to as “feasibility iterates," which are used to detect whether or not the combined phase should be initiated. These iterates are used to provide the group with larger lag size (and thus a lower-accuracy gradient estimate) with a higher-accuracy gradient estimate, thus alleviating concern (4) if the combined phase is initiated.

The two groups are optimized in turn, one at a time, and the following values of gradients are used to detect various conditions:

-

(a)

Low gradient accuracy: If the point sampled is the th lagged point555We do not compute the gradient for the first lagged point, since there is no “previous” lagged point with which a difference quotient can be calculated. The samples taken at the first lagged point are only used to estimate the gradients at the next lagged point. (), and the gradient estimate is less than , then we know that we need to sample the next lagged point (with a lower lag size) as well. As was the case for Ada-Lgd, this check allows us to continue converging to the optimum despite the low-gradient condition being met.

-

(b)

Low gradient or Switch to other group: If the point sampled is a non-lagged iterate in group , and the gradient estimated is small enough (i.e., less than ), then we permanently switch to sampling group and never optimize group in the coordinate descent phase again. This is to ensure that group does not incur excessive regret while group is already close to its optimum and thus further improvements to group would take a large number of steps. Otherwise, the next non-lagged and lagged iterates are computed (as in Ada-Lgd) and added to the queue to sample. If the lag size of group is smaller than the lag size of group , then a switch to optimizing group is triggered. This is to prevent the algorithm from devoting too much time to one group without optimizing the other. Intuitively, if the slacks were high enough that the constraints are never tight, then this would ensure that the lag sizes of the two groups differ by at most a factor of , in the coordinate descent phase.

-

(c)

Combined Phase Trigger: When the next points to sample for group are the two feasibility iterates, then a gradient estimate is computed using the function values at these two points. At this stage, we know that group is close to its optimum, since feasibility iterates are only added in such a scenario. So, if the gradient is large enough (i.e., greater than ), then we can infer that group is far from its optimum, and this indicates that the EF constraint is tight at the joint optimum; hence, in this case, the combined descent phase is triggered.

After these checks, it may be the case that (i) a switch to the other group was triggered, or that (ii) there are no more feasible points for group to sample. If either of these situations occurs, then the algorithm will switch groups, adding feasibility iterates to if applicable (that is, if the lag size of group is smaller than the lag size of group ). If neither (i) nor (ii) occur, then we remain on group and repeat this process.

Combined descent phase (SCAda-Lgd). The decisions for the two groups are locked together once the combined phase is initiated. This means that the function can be expressed as a single-variable function for some . Since feasibility iterates were sampled in the group with larger lag size, both groups enter the combined phase with similar-accuracy gradients, which provide the first gradient estimate of . At this point, Ada-Lgd is run on for the remainder of the time horizon.

The following result shows that SCAda-Lgd achieves an order-optimal (up to polylogarithmic factors) regret guarantee.

Theorem 3.

Proof sketch of Theorem 3. As discussed above, SCAda-Lgd (Alg. 3) is composed of (1) a coordinate descent phase, in which Ada-Lgd is run on each group, switching between groups when boundary or low-gradient conditions are met; and (2) a combined phase, where the decisions for one group are locked with respect to the decisions for the other, and the two are optimized simultaneously. Much of the analysis is identical to that of Algorithm 2, so we focus on the differences.

Properly entering the combined phase. Suppose we are sampling at the feasibility check iterates, where the lag size of group 1 is smaller than that of group 2, i.e., . Entering the combined phase when the unconstrained optimum is feasible can result in high regret, as can failing to quickly enter the combined phase when the unconstrained optimum is infeasible. We show that, with high probability, if , the algorithm will enter the combined phase, and if , it will not, for some and . This ensures that the algorithm enters the combined phase when it is known with high confidence that the unconstrained optimum is infeasible.

Controlling the waiting regret. The other major difference from the analysis of Algorithm 2 is the presence of waiting regret: the regret incurred by group 1 while the algorithm is optimizing over group 2, and vice versa. The waiting regret has the potential to be quite large without careful algorithm design. By limiting the amount of time spent on any group in the coordinate descent phase and by permanently moving to the combined phase when gradients become small enough, we can obtain a waiting regret bound of . In particular, given lag sizes of and sampling times , we can bound the waiting regret by . By bounding the number of lag transitions and the number of gradient-scaled jumps taken in any round, we can bound this expression further by . Finally, this expression can be bounded by since optimization stops when the gradient on either dimension is of order . With these two points sorted, the analysis of Algorithm 2 carries through. ∎

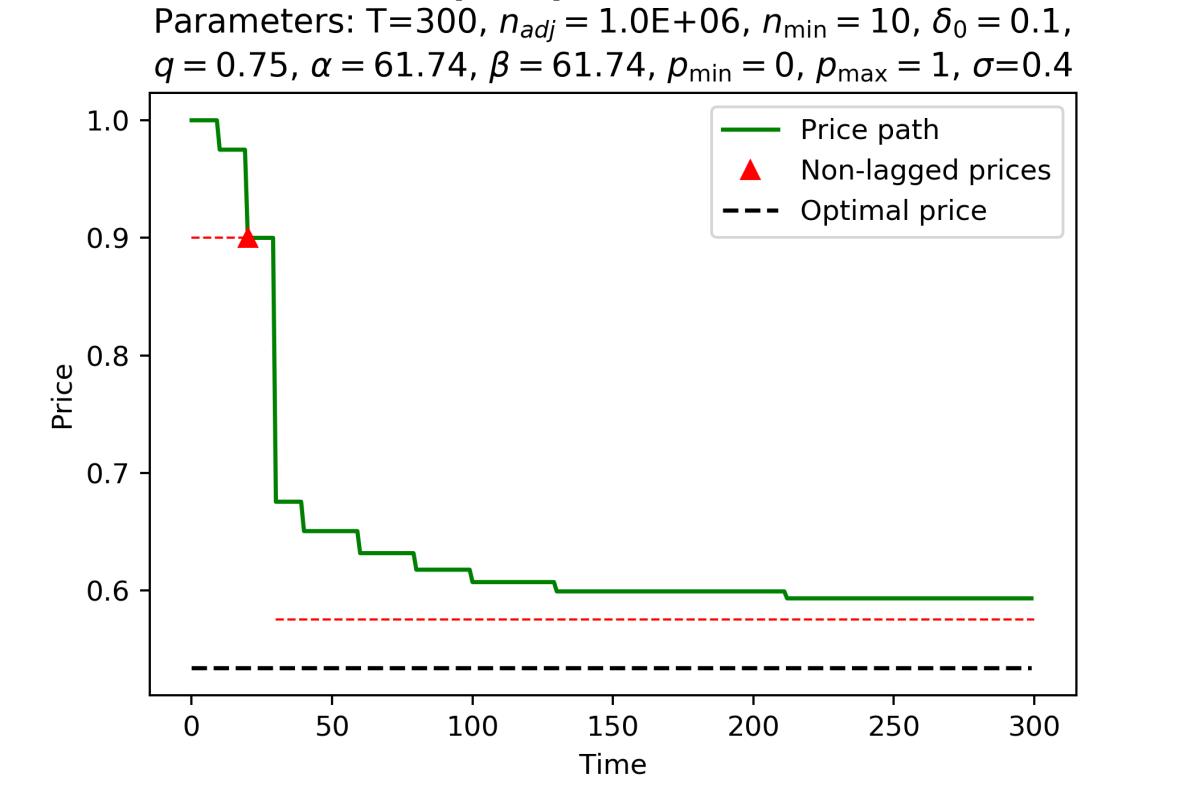

5.2.1 Numerical validation

To validate the EFTD behavior of SCAda-Lgd, we run it on a synthetic example. The functions being optimized are and , which are chosen so that and . A sample decision path for this input over time periods is shown in Figure 3 (right), where the initial decision is , and the decisions increase in both coordinates over time. Note that Group 1 overshot its optimum slightly in this run, but the decision path did not overshoot its joint constrained optimum.

6 A EFTD algorithm for the case of groups

We now consider the multi-group setting beyond two groups. In this case, an overall approach similar to the two-group case can be used when perfect gradient feedback is available. The groups can take turns ascending along their coordinate until they either hit a constraint boundary or meet the local optimality condition . When all groups have stopped moving, each group that has stopped because it hit a constraint boundary can be associated with a group that has stopped because , by tracing the path of tight EF constraints leading up to this group (there could be more than one such group). We can thus partition the groups into disjoint clusters, where each cluster is associated with a set of groups that have stopped because . Each such cluster moves together from that point onwards, with the relative positions of the different groups in the cluster locked. We then continue the procedure with these clusters as the new groups and so on, until all current clusters are at their optimum.

However, in the case where only noisy bandit feedback is available, similar challenges arise as in the two-group setting in converting this high-level approach to a practical algorithm that incurs near-optimal regret. Since we anticipate the details of such an algorithm to be quite cumbersome, we instead consider a simpler approach where we use static lags instead of dynamic lags. In particular, unlike the two-group setting, where a decision for a group is allowed to increase despite meeting the low gradient condition by adaptively choosing a lower lag size, with a static lag, each group (or a cluster) meets the low gradient condition at most once. The algorithm initially considers each group to be its own cluster. Each cluster is optimized in turn sampling at the next feasible point or moving to the boundary if no feasible points exist. If no clusters can move and not all clusters are at a low gradient, then one of the high-gradient clusters is combined with one of its constraining low-gradient clusters, and the process continues. This process, which we call Cycle-then-Combine Lagged Gradient Descent (C2-Lgd), is described formally in Algorithm 4. A sample decision path of this algorithm for the case of three groups is shown in Figure 4.

We show below that this algorithm attains regret. That said, we conjecture that an asymptotically better regret bound of can be obtained using a dynamic-lag approach.

Theorem 4.

We provide a proof sketch here, and a more detailed proof in Appendix B.

Proof sketch. First, note that Algorithm 4 run on a single group would result in regret. To see this, note that the exploration regret is bounded by , and when the algorithm reaches the low-gradient condition, the instantaneous regret is . The total regret is therefore of order , which becomes for .

There are two added complications in analyzing this algorithm compared to the two-group algorithm. First, the stopping regret will depend on , and second, we must consider the effect of multiple groups erroneously combining. We address these complications with the following claims.

Claim 1.

Suppose C2-Lgd has reached a point where each cluster has met the low-gradient condition. Then the regret incurred during the remainder of the time horizon is of order .

To address this first claim, we consider the case where all current clusters have reached a low-gradient condition. In this case, each cluster incurs instantaneous regret of , which contributes a total of to the regret.

Claim 2.

The total regret incurred due to erroneously combining clusters (i.e., combining clusters whose joint unconstrained optimum is in the interior of the feasible region) is of order .

To prove the second claim, suppose two clusters and are erroneously combined, where was at a boundary and had reached a low-gradient condition (see Figure 5). With high probability, we have that has not overshot its optimum, and with high probability, is within of its optimum. In this case, the unconstrained optimum is away from the facet defined by ’s constraint on .

In this case, we can address the regret due to incorrectly combining clusters by “translating” the function . In particular, there is a unique vector which is uniform within each cluster, 0 on clusters other than and , and for which the optimum of the function over (given the current intra-cluster lockings) is on the facet defined by ’s constraint on . In simpler terms, translates the function so that the point in Figure 5 is translated to its projection onto the noted facet.

By the argument above, the entries of are all of order , indicating that is a vector of length . Moreoever, note that the clusters are correctly combined with respect to the translated function. Since clusters can be combined at most times, the cumulative translation is of length . This therefore accounts for an added to the regret.

Combining the regret bouns from Claims 1-2 with the exploration regret, we get a regret bound of order . Plugging in gives the stated result.∎

7 Numerical Experiments

In this section, we present numerical experiments to compare Ada-Lgd to two standard state-of-the-art bandit algorithms (UCB by [44] and that of [33]) on data-derived revenue curves. These simulations aim to demonstrate the non-monotonic behavior of existing algorithms and to validate the sublinear the regret guarantee of Ada-LGD (Alg. 2).

We test the performance of a practical variant of Ada-Lgd using a trans-national UK-based online retail dataset comprised of various products, prices offered, quantities bought, purchase time, and other information (this dataset is available online at https://archive.ics.uci.edu/ml/datasets/online+retail). We restrict the dataset to the products with at least 1000 entries (of which there were 37) and pre-process the data to account for returns, to remove 0-priced entries, and to normalize the prices to be in . For each product, we remove all days for which multiple prices were offered, and use linear regression (fitting a demand curve is a typical task faced by an online retailer; linear regression is a reasonable choice here as the -values of the products have mean and standard deviation , with 13 products having -value greater than ) to generate a demand curve based on per-day average quantities. After this processing, 35 of the 37 products have rich enough data to produce meaningful demand curves, so we restrict to these products. We use the demand curve for product to calculate a revenue curve , which we then scale so that its minimum over is 0 and its maximum over is 1. The feedback generated for on item is , where are independent noise with .

While Ada-LGD (Alg. 2) has optimal (up to logarithmic factors) regret as , its regret can be high for small values of , since the number of samples taken at a point can be large relative to in this regime. To address this issue, we introduce an adjustment factor and a minimum sampling rate . We re-define the sample size in Ada-LGD (Alg. 2) to be .

We benchmark our algorithm against two bandit algorithms: a bandit convex optimization algorithm of [33] which is a sample-based gradient descent algorithm using a self-concordant barrier, and a UCB algorithm Discretize then UCB (Dtu) based on a discretization of . Dtu on input of -discretization obtains a regret of , which is sub-optimal, but nonetheless can have good performance. In our simulations, we use a discretization of 15 prices.

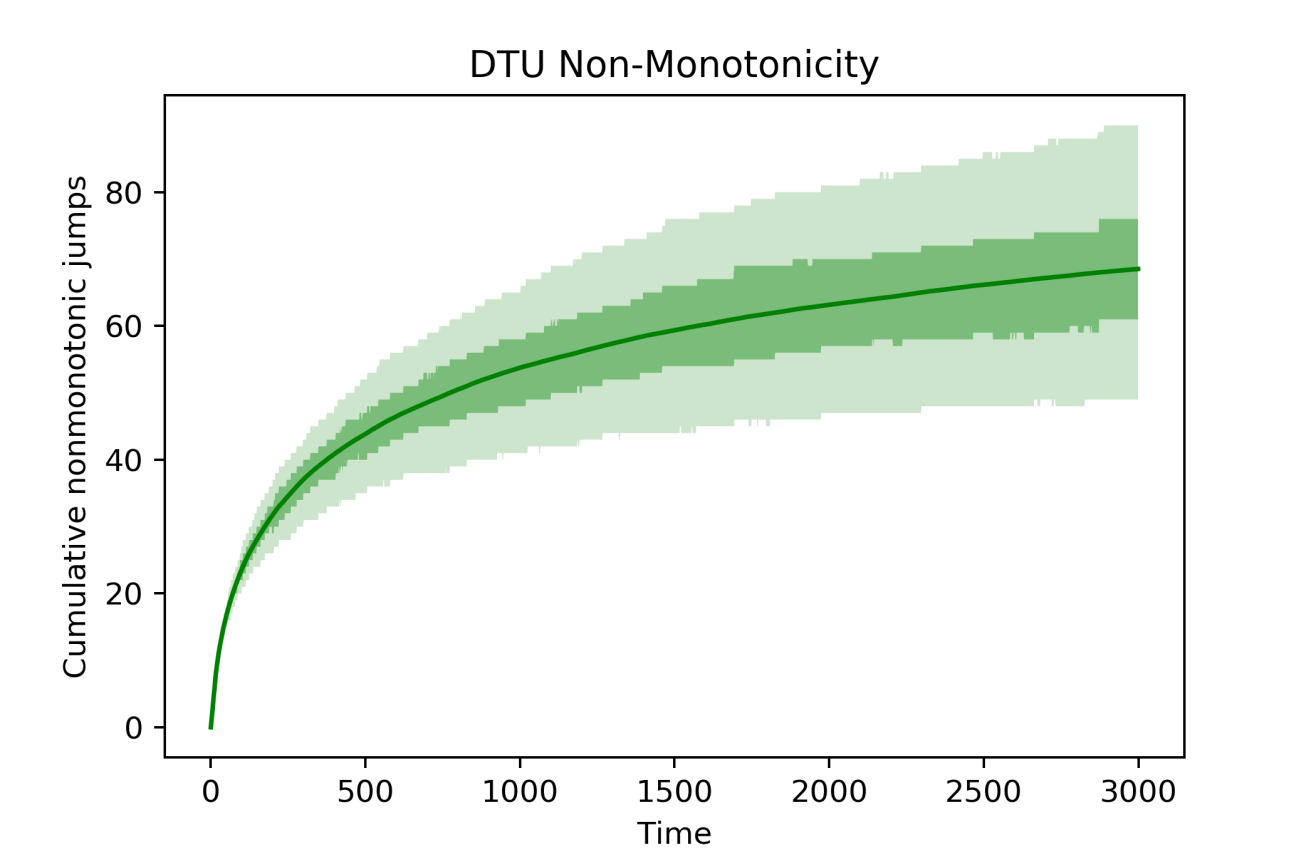

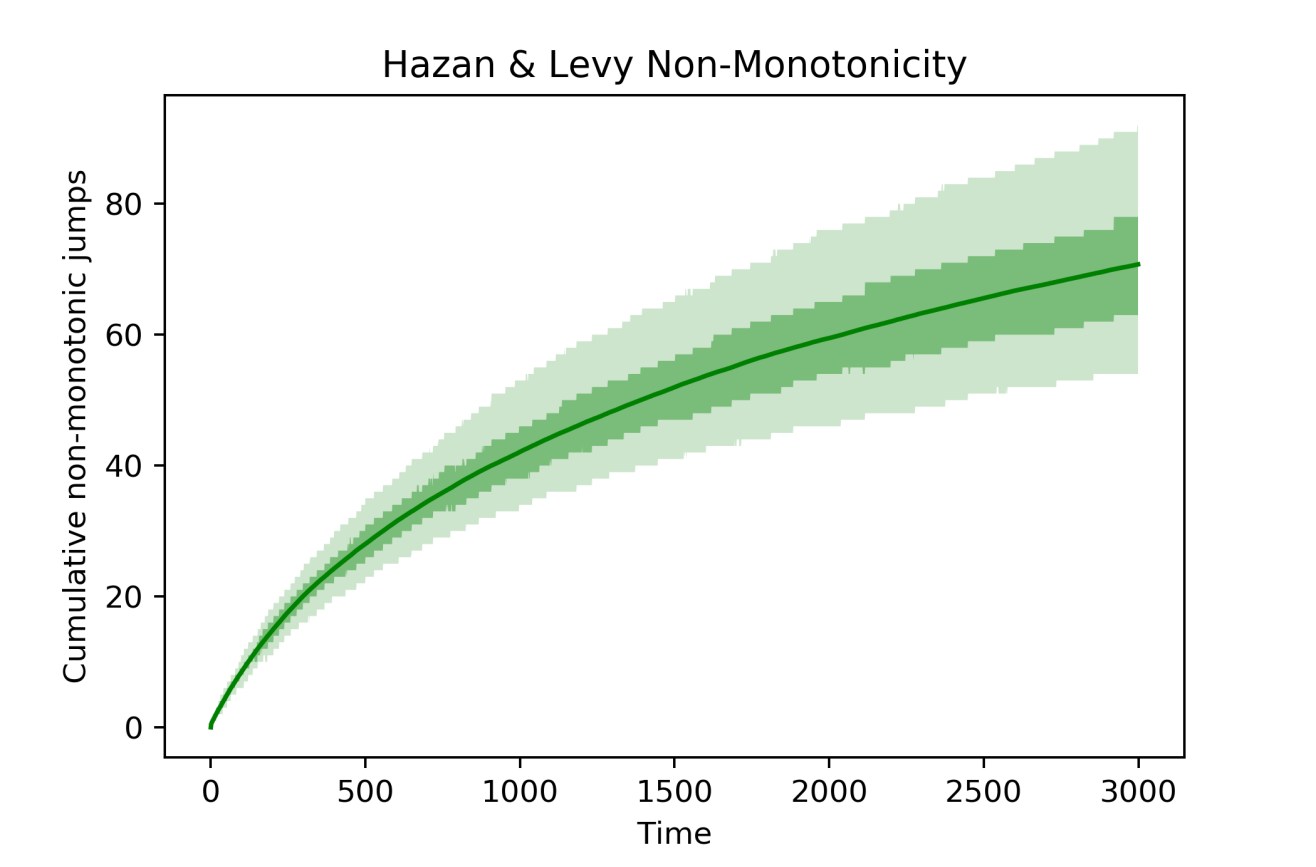

In Figure 6, we first plot the cumulative number of non-monotonic jumps for Hazan & Levy and Dtu. We note that both algorithms ultimately make a similar number of non-monotonic jumps at time 3000, with Dtu making most of these jumps in early time periods. A sample monotonic price path generated by Ada-LGD (Alg. 2) is shown in Figure 6 (right).

8 Discussion and Conclusion

There has been a surge of interest in the academic community and among policymakers alike on the topic of algorithmic fairness. As this discourse develops, various task-specific notions of fairness have been introduced. This is natural since the social backdrop of, say, loan-granting is very different from that of job applicant screening. Hence, the notions of fairness appropriate in various decision-making settings such as pricing, applicant screening, loan-granting, etc., may be different. However, these settings commonly involve decision-making over a period of time, and thus, the aspect of avoiding temporal disparity in decisions is common to most of these tasks. In this paper, we illustrated the rich interplay between temporal fairness desiderata and online decision-making through the novel meta-objective of ensuring fairness at the time of decision. There are several possibilities for extension of our proposal and analysis as we discuss below.

-

1.

Envy freeness with multiplicative slacks. In many scenarios, multiplicative allowable disparities in treatment could be more appropriate than additive disparities. For example, a firm may want to price an item while ensuring that the price disparity between the youth and the general population is not more than 25%. In particular, consider slack functions defined on ordered pairs of groups, and consider the following definition of envy-freeness with multiplicative slacks.

Definition 4 (Envy Freeness with Multiplicative Slacks)).

We say that a decision vector satisfies envy-freeness (EF) with multiplicative slacks if the following inequalities hold:

(10) It would be interesting to extend our algorithm design to satisfy the FTD extension of this kind of a relaxed envy freeness constraint. One setting where our current results extend is the case where there is a function such that . In this case, (10) effectively requires that . In this case, one can redefine the decision space for group as . Our algorithms then readily apply to optimizing in this setting.

-

2.

Slack-monotonicity. In our analysis of envy freeness with additive slacks, we assumed that . This resulted in the temporal monotonicity constraint of ensuring for all and . However, in many scenarios, some changes to within-group decisions across time may be acceptable. In other words, we may have for all , so that we effectively require that is at most lower than the highest decision seen by group until time , thus allowing for a limited amount of backtracking in decisions (similarly, with multiplicative slacks, we may have that ). While it is interesting that this type of slack in the monotonicity constraint isn’t necessary for our setting to attain the unconstrained optimal near-regret rate of , it may nevertheless simplify the algorithm design. Moreover, it may provide crucial flexibility in attaining near-optimal regret rates in harder settings, such as when the functions are only known to be unimodal.

-

3.

Beyond strong convexity. It would be interesting to extend our results beyond the strong convexity assumption. As discussed earlier, for the simplest case of single-dimensional optimization, [36] and [37] have shown that a significant impact on the achievable rate of regret is inevitable under the monotonicity constraint if only unimodality and Lipschitzness of the cost function are assumed. While it seems that smoothness is necessary to obtain the near-optimal regret rate of in our setting (since smoothness is fundamental to controlling overshooting of the optimum), we are hopeful that the strong convexity assumption can be relaxed (to, e.g., just assuming convexity) without impacting the regret guarantee.

-

4.

Extensions to online convex optimization. It would be interesting to consider algorithm design for satisfying FTD in the general context of online convex optimization, which models scenarios where the utility function , though convex, changes over time [45]. In such scenarios, even with perfect gradient feedback (since the utility functions are assumed to be known in each period) it would be interesting to characterize conditions on the arriving functions under which sublinear regret rates can be attained while satisfying FTD.

-

5.

Time decay. Certain fairness goals may not be subsumed by the FTD objective; as such, there is room for generalizing or adapting FTD to better fit specific objectives. For example, one may wish to incorporate a time-decay element to the envy-freeness constraint, which can be achieved by having the slack functions be dependent on the difference in the times at which the decisions were received by the two groups. In particular, we may have that for all , where the slack function now also takes the time difference as input. If is assumed to be increasing in the time difference, this would allow for greater changes in decisions over time.

Finally, we note that temporal considerations can be required or suggested for compliance with laws or policy. For example, applicant-screeners often ensure approximate demographic parity for the purpose of avoiding disparate impact litigation [46], and this constraint constrains current decisions by prior decisions. So-called “mandated progress” legislation, such as affirmative action—which has been adopted and, in some cases, mandated in the U.S., Canada, and France—can similarly be thought of as a temporal constraint in which goals must be set and a current decision is thus constrained by past decisions [47]. In terms of loan-granting, Wells Fargo was recently sued for racial dicrimination in mortgage lending, including offering different average interest rates to Black applicants than white applicants over a period of time [48], which again points to the potential for the use of temporal fairness constraints as a preventative measure for avoiding litigation. Some times these constraints can be enforced due to necessity of protecting consumer rights in the prevelant societal context, e.g., price gouging laws may dictate bounded increase in decisions, during the duration of the pandemic (McQueen and Ballinger v. Amazon.com). In general, the case law surrounding algorithmic approaches to ensuring fairness is not yet well-developed, thus leaving many questions open. However, we believe that it is important to get ahead of such restrictions and to understand the limitations of algorithms to provide guidance to legal scholarship on the possibilities.

References

- [1] S. Bansal, A. Srivastava, and A. Arora, “Topic modeling driven content based jobs recommendation engine for recruitment industry,” Procedia computer science, vol. 122, pp. 865–872, 2017.

- [2] N. B. Keskin and A. Zeevi, “Dynamic pricing with an unknown demand model: Asymptotically optimal semi-myopic policies,” Operations research, vol. 62, no. 5, pp. 1142–1167, 2014.

- [3] A. K. Sinha, A. K. Akhtar, A. Kumar et al., “Resume screening using natural language processing and machine learning: A systematic review,” Machine Learning and Information Processing, pp. 207–214, 2021.

- [4] P. R. Darke and D. W. Dahl, “Fairness and discounts: The subjective value of a bargain,” Journal of Consumer psychology, vol. 13, no. 3, pp. 328–338, 2003.

- [5] L. E. Bolton, L. Warlop, and J. W. Alba, “Consumer perceptions of price (un) fairness,” Journal of consumer research, vol. 29, no. 4, pp. 474–491, 2003.

- [6] J. Heyman and B. A. Mellers, “Perceptions of fair pricing,” 2008.

- [7] K. L. Haws and W. O. Bearden, “Dynamic pricing and consumer fairness perceptions,” Journal of Consumer Research, vol. 33, no. 3, pp. 304–311, 2006.

- [8] L. Xia, K. Monroe, J. Cox, B. Kent, K. Monroe, and J. Jones, “The price is unfair! a conceptual framework of price fairness perceptions,” Journal of Marketing, vol. 68, pp. 1–15, 11 2004.

- [9] CCPA, “TITLE 1.81.5. California Consumer Privacy Act of 2018 (Title 1.81.5 added by Stats. 2018, Ch. 55, Sec. 3.).”

- [10] M. C. Cohen, A. N. Elmachtoub, and X. Lei, “Price discrimination with fairness constraints,” Management Science, 2022.

- [11] Q. Chen, N. Golrezaei, F. Susan, and E. Baskoro, “Fair assortment planning,” Available at SSRN 4072912, 2022.

- [12] G. Farnadi, W. St-Arnaud, B. Babaki, and M. Carvalho, “Individual fairness in kidney exchange programs,” in Proceedings of the AAAI Conference on Artificial Intelligence, vol. 35, no. 13, 2021, pp. 11 496–11 505.

- [13] E. W. Cope, “Regret and convergence bounds for a class of continuum-armed bandit problems,” IEEE Transactions on Automatic Control, vol. 54, no. 6, pp. 1243–1253, 2009.

- [14] A. Sen, “Equality of what?” Globalization and International Development: The Ethical Issues, p. 61, 2013.

- [15] C. Dwork, M. Hardt, T. Pitassi, O. Reingold, and R. Zemel, “Fairness through awareness,” in Proceedings of the 3rd Innovations in Theoretical Computer Science (ITCS). ACM, 2012, pp. 214–226.

- [16] M. B. Zafar, I. Valera, M. Gomez Rodriguez, and K. P. Gummadi, “Fairness beyond disparate treatment & disparate impact: Learning classification without disparate mistreatment,” in Proceedings of the 26th International Conference on World Wide Web, 2017, pp. 1171–1180.

- [17] T. Calders, F. Kamiran, and M. Pechenizkiy, “Building classifiers with independency constraints,” in 2009 IEEE International Conference on Data Mining Workshops. IEEE, 2009, pp. 13–18.

- [18] N. Kallus and A. Zhou, “Fairness, welfare, and equity in personalized pricing,” in Proceedings of the 2021 ACM Conference on Fairness, Accountability, and Transparency, 2021, pp. 296–314.

- [19] X. Chen, X. Zhang, and Y. Zhou, “Fairness-aware online price discrimination with nonparametric demand models,” arXiv preprint arXiv:2111.08221, 2021.

- [20] M. C. Cohen, S. Miao, and Y. Wang, “Dynamic pricing with fairness constraints,” Available at SSRN 3930622, 2021.

- [21] H. Heidari and A. Krause, “Preventing disparate treatment in sequential decision making,” in Proceedings of the 27th International Joint Conference on Artificial Intelligence, 2018, pp. 2248–2254.

- [22] S. Gupta and V. Kamble, “Individual fairness in hindsight,” in Proceedings of the 2019 ACM Conference on Economics and Computation, 2019, pp. 805–806.

- [23] M. Joseph, M. Kearns, J. Morgenstern, and A. Roth, “Fairness in learning: classic and contextual bandits,” in Proceedings of the 30th International Conference on Neural Information Processing Systems, 2016, pp. 325–333.

- [24] Y. Liu, G. Radanovic, C. Dimitrakakis, D. Mandal, and D. C. Parkes, “Calibrated fairness in bandits,” arXiv preprint arXiv:1707.01875, 2017.

- [25] J. Salem and S. Gupta, “Closing the gap: Group-aware parallelization for the secretary problem with biased evaluations,” Available at SSRN 3444283, 2019.

- [26] V. Manshadi, R. Niazadeh, and S. Rodilitz, “Fair dynamic rationing,” in Proceedings of the 22nd ACM Conference on Economics and Computation, 2021, pp. 694–695.

- [27] W. Ma, P. Xu, and Y. Xu, “Group-level fairness maximization in online bipartite matching,” arXiv preprint arXiv:2011.13908, 2020.

- [28] D. Bertsimas, V. F. Farias, and N. Trichakis, “Fairness, efficiency, and flexibility in organ allocation for kidney transplantation,” Operations Research, vol. 61, no. 1, pp. 73–87, 2013.

- [29] J. Kiefer, “Sequential minimax search for a maximum,” Proceedings of the American mathematical society, vol. 4, no. 3, pp. 502–506, 1953.

- [30] Y. Nesterov and V. Spokoiny, “Random gradient-free minimization of convex functions,” Foundations of Computational Mathematics, vol. 17, no. 2, pp. 527–566, 2017.

- [31] J. C. Spall et al., “Multivariate stochastic approximation using a simultaneous perturbation gradient approximation,” IEEE transactions on automatic control, vol. 37, no. 3, pp. 332–341, 1992.

- [32] A. D. Flaxman, A. T. Kalai, and H. B. McMahan, “Online convex optimization in the bandit setting: gradient descent without a gradient,” in Proceedings of the sixteenth annual ACM-SIAM symposium on Discrete algorithms, 2005, pp. 385–394.

- [33] E. Hazan and K. Y. Levy, “Bandit convex optimization: Towards tight bounds.” in NIPS, 2014, pp. 784–792.

- [34] J. Kiefer and J. Wolfowitz, “Stochastic estimation of the maximum of a regression function,” The Annals of Mathematical Statistics, vol. 23, no. 3, pp. 462–466, 1952.

- [35] A. Agarwal, D. P. Foster, D. Hsu, S. M. Kakade, and A. Rakhlin, “Stochastic convex optimization with bandit feedback,” in Proceedings of the 24th International Conference on Neural Information Processing Systems, 2011, pp. 1035–1043.

- [36] S. Jia, A. Li, and R. Ravi, “Markdown pricing under unknown demand,” Available at SSRN 3861379, 2021.

- [37] N. Chen, “Multi-armed bandit requiring monotone arm sequences,” arXiv preprint arXiv:2106.03790, 2021.

- [38] J. Salem, S. Gupta, and V. Kamble, “Taming wild price fluctuations: Monotone stochastic convex optimization with bandit feedback,” arXiv preprint arXiv:2103.09287, 2021.

- [39] D. K. Foley, Resource allocation and the public sector. Yale University, 1966.