The Adoption of Blockchain-Based Decentralized Exchanges

Abstract

We investigate the market microstructure of Automated Market Makers (AMMs), the most prominent type of blockchain-based decentralized exchanges. We show that the order execution mechanism yields token value loss for liquidity providers if token exchange rates are volatile. AMMs are adopted only if their token pairs are of high personal use for investors, or the token price movements of the pair are highly correlated. A pricing curve with higher curvature reduces the arbitrage problem but also investors’ surplus. Pooling multiple tokens exacerbates the arbitrage problem. We provide statistical support for our main model implications using transaction-level data of AMMs.

Keywords: Crypto tokens; FinTech; Decentralized Finance; Market Microstructure.

1 Introduction

Since the emergence of Bitcoin in 2008, practitioners and academics have argued that financial innovations such as tokenization of assets and decentralized ledgers, along with the backbone blockchain technology, will disrupt traditional financial services (see, e.g., Campbell (2016), Yermack (2017), Cong and He (2019), Chiu and Koeppl (2019), Cong, Li, and Wang (2020), Gan, Tsoukalas, and Netessine (2021)). However, despite thousands of crypto tokens have been created and the total capitalization of cryptocurrencies has exceeded 1.7 trillions as of early 2021, no blockchain-based financial service providers has yet truly challenged traditional financial intermediaries. Ironically, most transactions of crypto tokens still rely on unregulated centralized intermediaries that expose investors to the risk of thefts and exit scams (see, e.g., Gandal et al. (2018)).

In the mid of 2020, a new type of blockchain application called decentralized finance, and commonly referred to as DeFi, has emerged (see Harvey, Ramachandran, and Santoro (2021) for an overview). DeFi utilizes open-source smart contracts on blockchains to provide financial services which typically rely on centralized financial intermediaries. One of the most prominent DeFi innovations are decentralized exchanges which run on the Ethereum blockchain. Most of these exchanges utilize an Automated Market Maker (AMM) smart contract, which makes the market according to a deterministic algorithm, instead of utilizing order books and relying on central intermediaries. The largest of these decentralized exchanges, Uniswap, has become the fourth-largest cryptocurrency exchange by daily trading volume, just a few months after its launch (Kharif (2020)).

The AMMs built on blockchains are revolutionary in many ways. First, the settlement of transactions is instantaneous, after they are confirmed and included on the blockchain. Prior to settlement, traders still retain full control of their tokens. This eliminates counterparty risk for the users. Second, users of AMMs do not need to be paired to complete a transaction. Rather, they gain immediate access to available liquidity by interacting with the smart contract. Thirdly, different from traditional centralized exchanges where liquidity providers are typically professional market makers, any token holder can become a liquidity provider by depositing their tokens and earning fees from trading activities.

The mechanism underlying decentralized exchanges is fundamentally different from that of traditional exchanges. Hence, existing market microstructure literature has little to say about promises and pitfalls of this new form of exchanges. Many important questions remain unanswered: Can AMM provide sufficient incentives for provision of liquidity? Will there be any transaction breakdown where the liquidity reserve of the AMM is drained? What kind of tokens are most suitable for AMMs? How does the AMM structure affect trading activities and economic incentives of market participants?

In this paper, we develop a game theoretical model to answer the questions above, and provide empirical support to our main model implications. We show that, even without any information asymmetry, liquidity providers face arbitrage problems if the token exchange rate fluctuates. This stands in contrast with the adverse selection problem that market makers face in a centralized limit-order-book exchange (see, for instance, Glosten and Milgrom (1985)). While market makers in a centralized limit-order-book exchange can alleviate adverse selection through bid-ask spreads, liquidity providers in the AMM can neither charge a bid-ask spread nor front-run because of the order execution structure of blockchain.

We analyze the incentives of liquidity providers and characterize the subgame perfect equilibrium of the game. At equilibrium, if the exchange rate of tokens is too volatile, liquidity providers do not deposit their tokens in the AMM, which leads to a “liquidity freeze”. In such case, the expected fee revenue from providing liquidity is lower than the expected arbitrage loss plus the opportunity cost from holding the tokens to deposit in the AMM. Moreover, a “liquidity freeze” is less likely to occur if investors extract large private benefits from using their tokens on the corresponding platforms, or if the price movement of two tokens are highly correlated. In the former case, investors would have strong incentives to trade, hence resulting in large trading volumes and high fee revenues for liquidity providers; in the latter case, the prices of two tokens are more likely to co-move, thus leading to less arbitrage opportunities. Last, but not least, we argue that a “liquidity freeze” is more likely to occur for tokens with low expected returns, as liquidity providers incur a large opportunity cost for holding those tokens in their portfolios.

Our equilibrium results also help correct the widely spread misconception that the token value loss due to arbitrage is impermanent and vanishes when the exchange rate reverts to its initial value. We argue that the long-established benchmark used to measure the “impermanent loss” is unable to fully account for the opportunity cost of depositing in the AMM. We show that, contrary to the popular belief, liquidity providers’ incentives to deposit in the AMM may become stronger if the expected “impermanent loss” increases and the probability of exchange rate reversion decreases.

We show that if the AMM is largely adopted, both the expectation and variance of transaction fees charged by the blockchain underlying the exchange increase. This imposes negative externalities on other decentralized applications operating on the same blockchain. Higher and more volatile transaction fees may prevent consumers from using these applications or cause high execution delays. Hence, our results indicate that not only does the blockchain affect the DeFi applications built on it, but the DeFi applications also affect the underlying blockchain.

We use our model to analyze the design of an AMM. There currently exist hundreds of AMMs, which mainly differ in terms of the pricing curve used and the number of managed tokens. (See, for instance, Xu et al. (2021)). First, we show that the curvature of the pricing function determines the severity of the arbitrage problem and the fee revenue generated by trading activities. Pricing functions with larger curvature reduce the arbitrage problem, but also decrease investors’ surplus. We construct an optimal pricing function, which maximizes welfare and deposit efficiency, and minimizes the occurrence of a “liquidity freeze”. Second, we explore how pooling more than two different tokens in the AMM affects the occurrence and profitability of exploitable arbitrage opportunities. Our analysis warns against a typical fallacy—pooling more tokens in the AMM reduce the token value loss due to diversification effects. We show that pooling multiple tokens not only increases the probability that an arbitrage occurs but also allows the arbitrageur to extract a larger portion of deposited tokens.

We provide empirical support to the main testable implications of our model using transaction-level data from Uniswap V2 and Sushiswap AMMs. We identify the deposit, withdrawal, and swap orders from the raw transaction history of 80 AMMs offering the most actively traded token pairs, in the period from Dec 22, 2020 to June 20, 2021. Consistently with our theoretical predictions, we find that token exchange rate volatility has a negative effect on deposit flow rate, while trading volume has a positive effect. Both effects are statistically and economically significant. An increase in weekly log spot rate volatility by 0.04 (around one-standard-deviation) decreases the weekly deposit flow rate by 0.06 (around 25% of the standard deviation). Moreover, an increase in trading volume by one standard deviation increases the weekly deposit flow rate by around 35% of the standard deviation.

We exploit the segmentation of AMMs by dividing them into two groups: “stable pairs” and “non-stable pairs”. “Stable pairs” consist of two stable coins which are each pegged to one US dollar, and thus these pairs have very low token exchange rate volatility compared with “unstable pairs”. Consistent with our theoretical predictions, we find that gas fees for transactions of “stable pairs” are 8% lower than those of “non-stable pairs”, and that the weekly volatility of gas fees for “stable pairs” is about 40% lower than for “non-stable pairs”. This implies that the size of (negative) externalities imposed by “stable pairs” on other platforms using the Ethereum blockchain is smaller.

The rest of paper is organized as follows. Section 2 gives institutional details of crypto exchanges and describes the AMM. Section 3 develops the game theoretical model. Section 4 solves for the subgame perfect equilibrium of the model, and analyzes its economic implications. Section 5 discusses the design of AMMs. Section 6 tests statistically the main model implications. We conclude in Section 7.

Literature Review.

Our paper contributes to the so-far scarce, but rapidly growing, literature on blockchain-based decentralized finance. Relevant contributions include Angeris et al. (2021), who show that the AMM can track the market price closely under no-arbitrage conditions; Bartoletti, Chiang, and Lluch-Lafuente (2021) who abstract away from the economic mechanisms behind AMMs, and prove a set of structural properties; Daian et al. (2020) who provide empirical evidence for the existence of arbitrage at AMM. We refer to Harvey, Ramachandran, and Santoro (2021) for an excellent and comprehensive survey of DeFi applications. In their survey, they highlight the potential token value loss faced by liquidity providers, often referred to as “impermanent loss”. We show that the widely accepted measure of “impermanent loss” can be misleading and lead to sub-optimal liquidity management strategy of liquidity providers.

To the best of our knowledge, our paper is the first to explore theoretically and empirically the market microstructure of AMMs and their design. It is worth mentioning two recent complimentary studies to ours. Park (2021) discusses front-running arbitrage, a different form of arbitrage that arises in blockchain-based crypto exchanges, and Lehar and Parlour (2021) compare liquidity provision at a centralized exchange with liquidity provision at an AMM which utilizes a constant product function.

Our results also add to existing literature on crypto trading. Griffins and Shams (2020), Cong et al. (2020), and Li, Shin, and Wang (2018) analyze the trading activities and price manipulations at centralized crypto exchanges. We contribute to this strand of literature by analyzing the economic incentives behind trading and provision of liquidity at decentralized exchanges, whose trading volume has been growing steadily.

Our paper is broadly related to the the stream of literature studying blockchain technologies. Some of these studies investigate miners’ incentives and how blockchain protocols achieve decentralized consensus. Noticeable contributions in this direction include Abadi and Brunnermeier (2018), Biais et al. (2019), Leshno and Strack (2020), Saleh (2020), Budish (2018), Roşu and Saleh (2021), Hinzen, John, and Saleh (2019), and Cong, He, and Li (2020). Hinzen, John, and Saleh (2019) argue that the Bitcoin’s protocol, despite ensuring decentralization, may result in limited adoption of Bitcoin as a payment system. Our results show that while gas fees incentivize miners and guarantee decentralization on the Ethereum blockchain, they also make the arbitrage problem on DeFi exchanges unavoidable and consequently reduces adopting.

A related branch of literature analyzes blockchain in the context of crypto transactions and pricing. Contribution in this direction include Huberman, Leshno, and Moallemi (2021), Sockin and Xiong (2020), Easley, O’Hara, and Basu (2019), Pagnotta (2021), Schilling and Uhlig (2019), Athey et al. (2016), and Irresberger et al. (2020). Unlike these studies which view blockchain as the technology underlying payment systems, we investigate the pros and cons of blockchain as an infrastructure for decentralized exchanges. In their work, Irresberger et al. (2020) highlight the functionality of public blockchain as an infrastructure supporting DeFi applications.

2 Crypto Exchanges

In this section, we provide institutional details of crypto exchanges and discuss the mechanics of AMMs.

2.1 Institutional Details

Tokenization has gained increasing popularity since the introduction of bitcoin in 2008 by Nakamoto (2008). As of January 2021, there are over 4,000 crypto tokens created, distributed, and circulated (Bagshaw (2020)). With the increasing adoption of cryptocurrencies, many exchanges have been created specifically for trading of crypto tokens. Those exchanges usually fall into two categories: centralized exchanges and decentralized exchanges (often called DEX).

A centralized cryptocurrency exchange is a trusted intermediary which monitors and facilitates crypto trades as well as securely stores tokens and fiat currencies. Similar to the equity market, centralized exchanges are often in the form of limit order books, and many of them also provide leverage and derivative trading. However, different from the equity market, most of the centralized cryptocurrency exchanges are unregulated and lack of proper insurance for the assets stored. This presents concerns for safety, trustworthiness, and potential manipulation.111The study of Gandal et al. (2018) highlights price manipulation behavior on crypto exchanges including Mt.Gox which, at its peak, was responsible for more than 70% of bitcoin trading. In early 2014, Mt.Gox suddenly closed its platform and filed for bankruptcy claiming that the platform’s wallet was hacked and a great amount of assets were stolen. Other centralized exchanges subject to thefts and exit scams include Binance, BitKRX, BitMarket, PonziCoin, and so on.

Because of the concerns presented by centralized crypto exchanges, decentralized exchanges are becoming alternative platforms for the purchase and sale of crypto tokens. As of August 2020, DEX account for more than 5% of the total crypto trading, and their market shares have been increasing steadily (McSweeney (2020)). Different from centralized exchanges, DEX are blockchain-based smart contracts which can operate without a trusted central authority. Most of them utilize an AMM smart contract that tracks a constant product function. The two largest DeFi exchanges, Uniswap and Sushiswap, respectively make up for about 50% and 20% of the trading volume at decentralized exchanges (Smith and Das (2021)).

Orders are typically executed on the scale of milliseconds in a centralized exchange (Sedgwick (2018)). Unlike centralized exchanges which facilitate trades and manage all orders using their own infrastructure, decentralized exchanges take in, manage, and execute orders through a blockchain-based platform (typically Ethereum). Instead of sending the order directly to the exchange, users submit their orders222Users maintain full custody of their tokens and can overwrite their orders before they are confirmed. As a result, users are not exposed to counterparty risk, that is, the risk that the exchange defaults on its obligations to deliver tokens after the transaction is confirmed. Upon confirmation, the delivery of tokens is instantaneous. to the blockchain network and attach a transaction fee (the gas price and gas limit in the Ethereum network). The miner that mines the very next block will prioritize orders based on the attached gas price, from highest to lowest, and append them to the blockchain. Since each block has a maximum size, the number of orders a miner can include in a single block is limited. Hence, an order with a too low transaction fee may need to wait a few minutes before being confirmed and executed.

2.2 AMM with Constant Product Function

We provide a brief description of the most common AMM smart contract, which deploys a constant product function. We refer to Adams (2020) for a more extensive overview.

An AMM does not rely on a limit-order book for transactions. Rather, it develops a new market structure called liquidity pool. A liquidity pool allows for a direct exchange of two crypto tokens, say A and B tokens, instead of first selling A tokens for fiat currency and then purchasing B tokens using proceeds from the asset sale. Each liquidity pool typically manages a pair of tokens.333It is also possible to pool multiple tokens together, despite pools with a single pair are the most common. It is worth emphasizing that the trading mechanism of pools with more than two tokens is almost identical to that of pools with a single pair of tokens. We remark that any pair of tokens can form a liquidity pool. Hence, liquidity pools can support trading activities for tokens not yet listed on centralized exchanges.

The liquidity pool works by incentivizing owners to deposit their tokens into the smart contract. Assume a liquidity pool manages the exchange of two tokens, A and B, where each A token is worth and each token is worth . Anyone who owns both A and B tokens can choose to be a liquidity provider by depositing an equivalent value of each underlying token in the AMM and in return, receiving pool tokens which prove his share of the AMM. For example, if the current reserve in the liquidity pool contains tokens A and tokens B, and the current value is 1 dollar for one A token and 2 dollars for one B token, then the liquidity provider must deposit A tokens and B tokens in the ratio 2:1. After depositing tokens A and tokens B, the liquidity provider can claim pool tokens that account for half of the total tokens in the current liquidity reserve. The provider can exit the liquidity pool by trading in his pool tokens, and receiving his share of the liquidity reserve in the AMM. For instance, if the liquidity reserve contains 25 tokens A and 9 tokens B when the liquidity provider exits and no one deposits after her, then she receives 12.5 tokens A and 4.5 tokens B.

Suppose a new investor arrives at the AMM and wants to exchange A for B tokens. To complete such a trade, this investor does not need to search for a counterparty who is willing to exchange B for A tokens. Rather, she directly interacts with the AMM by submitting a swap order through which she deposits an amount of A tokens and withdraws an amount of B tokens. The quantities and satisfy . That is, multiplying the amount of both tokens in the AMM must yield a constant. Formally, assume the initial liquidity reserve in the AMM contains A tokens and B tokens. Then the trade needs to satisfy . In addition to the amount of tokens A exchanged, the investor must pay an additional amount of tokens A as trading fee. Most of this fee is then added to the liquidity pool.444In practice, a small portion of the trading fees may be collected by the underlying platform. This can be incorporated in the model by multiplying the trading fee collected by the liquidity provider with a constant term. Because such an additional feature would not qualitatively change our results, we opted for leaving it out. Hence, the trading fee increases both the total liquidity reserve of the AMM and the AMM share of liquidity providers. Liquidity providers are incentivized to deposit because they earn the trading fee. For Uniswap V2 and Sushiswap, this trading fee is currently set to of the tokens that investors trade in. The ratio between the amount of two tokens in the liquidity pool equals the spot exchange rate when the trading size is infinitesimally small.555It can be easily verified that if , then .

It is worth noticing that the relationship can, in principle, be replaced by , where is an arbitrary pricing curve referred to as the pricing function. AMMs differ in terms of the chosen pricing function. The constant production function is just a special case, where We refer to Xu et al. (2021) for an overview of pricing functions used by different AMMs.

3 Baseline AMM Model

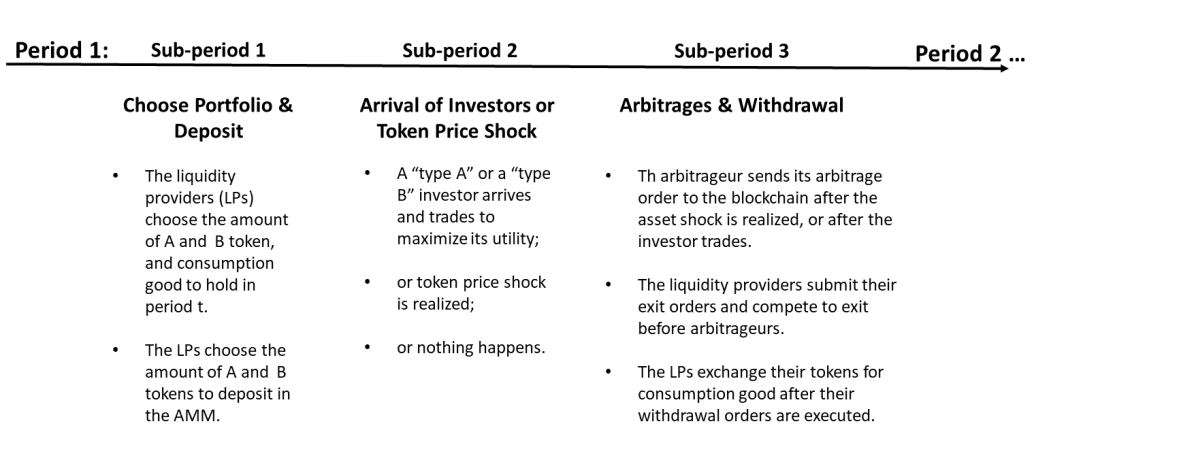

Our baseline model consists of periods indexed by , Each period has 3 sub-periods. There are three kinds of agents: liquidity providers, an arbitrageur, and investors. The discount factor of each agent is equal to .

3.1 The Pricing Function of the AMM

The agents have access to two different tokens, referred to as A and B tokens. The tokens can be used directly on the corresponding platforms A and B. Alternatively, they can be exchanged for a single consumption good used as a numeraire at prices which are public information for all agents. We denote the amount of consumption good that a single A and B token can exchange for at the end of sub-period of period , as and respectively. We will refer to and as the token prices of A and B tokens respectively interchangeably throughout the paper. We will refer to the ratio of token prices, , as the fair value exchange rate.

There is a smart contract built on a blockchain that functions as the AMM for A and B tokens. The smart contract utilizes a twice continuously differentiable pricing function to decide the exchange rate for any trade. If the AMM contains an amount of A tokens and of B tokens, any trade that exchanges A tokens for B tokens needs to satisfy the relation . An additional amount of A tokens needs to be added to the AMM as a trading fee.

Assumption 1.

The function satisfies the following properties:

-

1.

.

-

2.

.

-

3.

for some .

-

4.

, .

The first assumption ensures that a positive amount of A tokens can be exchanged for a positive amount of B tokens from the AMM. The second assumption guarantees that the curve , where is a constant, is convex. This implies that if the demand of A tokens goes up, the exchange rate used to convert from B to A tokens correspondingly increases. Symmetrically, if the demand for B tokens increases, a higher amount of A tokens is required to exchange for a single B token. The third assumption states that the function is homogeneous of degree , and ensures that the exchange rate at the AMM does not change significantly if the amount of deposited tokens goes up. The last condition ensures that the AMM supports trading for any token exchange rate in the interval . These four properties can be verified to hold for the majority of existing AMMs. (see, for instance, Xu et al. (2021)).

3.2 Liquidity Providers

There are liquidity providers, indexed by , and each endowed with a positive amount of consumption good at . We use to denote the initial endowment of liquidity provider , where . The aggregate initial endowment of liquidity providers is .

At sub-period 1 of each period , liquidity providers choose their portfolios. Specifically, they decide whether to exchange their consumption good for A and B tokens, and how much to exchange for. In addition, they decide whether to deposit their tokens in the AMM and how much to deposit. The liquidity providers maximize the amount of consumption good that they can exchange for at the end of period . We also impose the following tie-breaking rule:

Assumption 2.

The liquidity providers do not deposit their tokens if they are indifferent between whether or not to deposit.

We denote the amount of A and B tokens deposited in the AMM at the beginning of period , respectively by and . Liquidity provider deposits and amount of A and B tokens, respectively, where . The AMM requires tokens to be deposited at the current fair value exchange rate666As an example, an AMM which utilizes a constant product function requires the deposited tokens to have equal value, i.e., ., i.e., .

3.3 Investors’ Arrival and Token Price Shocks

In sub-period 2 of each period , after liquidity providers decide on their token holdings and deposit in the AMM, one of the following three mutually exclusive and collectively exhaustive events occurs: “the arrival of an investor”, “the arrival of a token price shock that hits A token or B token”, and “neither a shock hits, nor an investor arrives”.

Investors’ Arrival.

With probability , an investor arrives to the AMM. An investor is characterized by an intrinsic type, that is “type A” or “type B”. A “type A” investor extracts a private benefit of from using one A token on its corresponding platform. A “type A” investor does not use platform B, so she only receives for each B token. Symmetrically, a “type B” investor receives for each B token and for each A token.777For instance, the platform that issues token B20 is Metapurse. On this platform, one can use token B20 to claim ownership of NFT collectibles. The Ethereum network is a platform, where one can use ETH tokens as a cryptocurrency to exchange for goods and other tokens, or to run applications. If an investor prefers to gain exposure to NFT collectibles rather than fiat currencies, then she prefers token B20 over stable coins pegged to USD, such as USDT, USDC. If an investor needs to run applications on Ethereum networks, then she can extract a private benefit from token ETH. If an investor prefers low volatility, high liquidity and wants to exchange her tokens for fiat currencies, then she can extract a private benefit from holding stable coins. The investor arriving to the AMM is of “type A” or of “type B” with equal probability. The investor chooses the traded quantity to maximize her total surplus from the transaction.

Token Price Shock.

In each period , the prices of A and B tokens may be hit by exogenous shocks. With probability , the price changes of A and B tokens are driven by a common shock :

| (1) |

That is, with probability , the common shock causes a price increase of for both A and B tokens.

With probability , the price changes of A and B tokens are caused by independent, idiosyncratic shocks :

| (2) |

That is, with probability , the idiosyncratic shock realizes and increase the price of A tokens by ; with probability , the idiosyncratic shock realizes, and increases the price of B tokens by . Notice that . This means that the expected return of holding B tokens is smaller than the corresponding return of holding A tokens, and thus holding B tokens presents an opportunity cost.

3.4 Arbitrage and Token Withdrawal

The arrival of an investor or the occurrence of a token price shock at sub-period 2 presents an opportunity for the arbitrageur. At sub-period 3 of each period , the arbitrageur submits an arbitrage order and the liquidity provider submits a withdrawal order.

Arbitrage Opportunity

After the investor arrives and trades, the ratio between the amount of A and B tokens deviates from . Since the spot exchange rate is solely decided by the ratio between the amount of tokens, this deviation may present arbitrage opportunities.

Similarly, upon realization of the token price shock, the fair exchange rate of two tokens may change. However, the spot exchange rate in the AMM remains unchanged, and this creates an arbitrage opportunity. The arbitrageur is incentivized to trade in the token not hit by the shock for the token which becomes more valuable after the shock. This, in turn, yields a loss for the liquidity providers, who then have strong incentives to withdraw their tokens ahead of the arbitrageur.

Arbitrageur.

The arbitrageur does not use tokens on either platform and only exchange tokens for consumption good. It takes advantage of the price deviation at the AMM and trades to maximize its profit from arbitrage , where and are respectively the change in the amount of A and B tokens held by the arbitrageur. This trading opportunity can be exploited by the arbitrageur only if its order is confirmed by the blockchain before others. The arbitrageur adds a transaction fee to its order. We will also refer to such fee as “gas fee”888For Ethereum, the total gas fee is equal to the gas price multiplied by the gas amount needed to execute the transaction. The gas price is defined as the amount of ETH paid per unit of gas used, and the gas amount measures the computational resources needed to execute a transaction on Ethereum. The unit of gas price is Gwei, that is, ETH token. Transactions with higher gas prices are confirmed first, because miners prioritize them to maximize their fee revenue. Since transactions executed on the same AMM use similar gas amounts, the transactions with higher gas prices have higher total gas fees. In our model, we assume that the agents directly submit a gas fee instead of a gas price. interchangeably throughout the paper, following its institutional counterpart. The orders will be included on the underlying blockchain and executed in decreasing order of of gas fees, and any tie will be broken uniformly at random. We assume that gas fees attached to unconfirmed orders are observable by everyone.999This assumption is consistent with current practices. All submitted, pending orders to the AMMs are stored at the mempool which is publicly accessible. Following Glosten and Milgrom (1985), we assume that the arbitrageur earns zero profit from each trade net of the paid gas fee.

Assumption 3.

The arbitrageur attaches a gas fee equal to the highest possible profit from an arbitrage order.

Such an outcome can be attained in a competitive environment with many arbitrageurs. Suppose an arbitrageur submits an arbitrage order and attaches a gas fee smaller than the profit earned from the arbitrage. Another arbitrageur can undercut the first order by submitting the exact same order and attaching a slightly higher gas fee. Only if an arbitrageur submits an optimal arbitrage order (i.e., one which maximizes its trading profits) and bids a gas fee equal to its profit, then other arbitrageurs are unable to undercut the submitted order.

Token Withdrawal.

In each period , at sub-period 3, the liquidity provider withdraws his tokens from the AMM by submitting an order and attaching a non-negative gas fee to it. When the withdraw order is executed, the liquidity provider pays the attached gas fee and receives an amount of A tokens and an amount of B tokens, where are the total reserves in the AMM before the first withdrawal. We recall here that is the share of reserves that liquidity provider deposited at the beginning of period . Upon receiving their tokens, liquidity providers exchange them for the consumption good, and period ends. We denote the amount of consumption good that liquidity provider owns at the end of period by . We visualize the timeline of the model in Figure 1.

3.5 States, Actions, Strategy Profiles, and Equilibrium

In this section, we formally define the states, action space, and strategy profiles and payoffs of liquidity providers, investors, and arbitragers.

States.

We denote by the set of possible states. We denote the initial state of the game as . The state at sub-period of period consists of two components:

-

1.

, where are the price of A and B tokens at the end of sub-period of period . is the history of token prices until the end of sub-period of period .

-

2.

, where collect the portfolios of liquidity providers at the end of sub-period of period . and are, respectively, the amounts of A and B token in the AMM that belong to liquidity provider ; is the amount of consumption good he holds; are the amounts of A and B token that liquidity provider holds (apart from his deposit in the AMM).

Action Space.

Liquidity provider chooses the portfolio at sub-period 1 of each period , , and the gas fee attached to the withdrawal order at sub-period 3 of each period . Liquidity provider finances his portfolio at using his endowment at the end of period , i.e. he is subject to the following budget constraint:

When the investors arrive at the AMM, they choose the trading quantities, . At sub-period 3, the arbitrageur chooses the arbitrage order, .

Strategy.

A (pure) strategy of the liquidity provider , consists of four mappings: the first is from the initial state to a portfolio at sub-period 1 of period 1, the second is from to a portfolio at sub-period 1 of period 2, and the third and fourth are from a state to a gas fee , for respectively. We denote the strategy profile of the liquidity providers by .

The strategies of an arriving “type A” and “type B” investor are denoted, respectively, by and . They are mappings from a state to and , i.e., the amount of A and B tokens traded, respectively, by the “type A” and ”type B“ investors. We denote the strategy profile of the investors by .

A (pure) strategy of the arbitrageur is a mapping from a state to the amount of A and B tokens resulting from its arbitrage, respectively and .

Payoffs.

The expected payoff of liquidity provider is , that is, the total amount of consumption good that liquidity provider is expected to possess at the end of period . The expected payoff of the arbitrageur is , that is, the expected total profit from the arbitrage order net of the gas fee paid.

The payoff of an investor arriving at period is defined by her surplus from the transaction, that is, for “type A” investors, and for “type B” investors.

Equilibrium.

The states, the strategy profile, and the payoffs above define our dynamic game. Our equilibrium concept is that of a subgame perfect equilibrium.

4 Equilibrium Trading and Liquidity Provision

We analyze the game theoretical model developed in the previous section. In Section 4.1, we show that the liquidity providers face an arbitrage problem after a token price shock occurs. In Section 4.2, we study the trading strategy of investors. In Section 4.3, we characterize the subgame perfect equilibrium of the game, and study under which conditions liquidity providers do not find it incentive compatible to deposit tokens.

4.1 The Arbitrage Problem

Upon the occurrence of a token price shock in sub-period 2, liquidity providers and the arbitrageur submit their respective orders to the blockchain. An arbitrageur decides the amount of A or B tokens traded in as well as the gas fee attached to the order. A liquidity provider decides the gas fee attached to his exit order only. We show that a liquidity provider will be subject to an arbitrage problem and token value loss, if token prices do not co-move and the price change is large enough.

Recall that the amount of A and B tokens in the AMM at sub-period 2 of period , is denoted respectively, by and . When the common shock occurs and the price of the two tokens co-move, the fair value exchange rate remains unchanged: . However, if a shock hits either token A or token B only, then the fair value exchange rate deviates from the spot exchange rate . Without loss of generality, we assume the shock hits B tokens101010The case where the price shock yields an appreciation of A tokens can be handled symmetrically., and the price rises from to . To profit from this deviation, the arbitrageur submits an order to the AMM and exchanges an amount of A tokens for B tokens. The arbitrageur aims for the optimal arbitrage, i.e., chooses the buy order which solves the following optimization problem:

| (3) | ||||

| s.t. | ||||

where is the trading cost, that is, the value of A tokens traded in plus the trading fee paid to the liquidity providers, and is the value of B tokens received by the arbitrageur from the order. Solving for the optimal arbitrage yields the following result:

Lemma 4.1.

If a price shock hits only one token and the price change of that token exceeds the paid fee, i.e., , then the arbitrageur earns a positive profit from the optimal arbitrage trade. Moreover, such profit and the unique optimal trading size for A tokens and for B tokens are increasing in and decreasing in .

When the prices of two tokens do not co-move, if the realized token price change is sufficiently large, it is profitable for the arbitrageur to exchange the token not hit by the positive price shock for the other more valuable token. The larger the realized price change, the higher the payoff attained from the arbitrage, and the larger the token value loss for liquidity providers. Moreover, the higher the trading fee charged by the AMM, the higher the trading cost for the arbitrageur, which in turn reduces the arbitrage profit and the order size.

The profit of the arbitrageur equals the loss in token value incurred by the liquidity providers. Formally, liquidity provider incurs a token value loss if an optimal arbitrage order is executed. Hence, this liquidity provider has an incentive to submit a withdrawal order to the AMM. To avoid the loss, the withdrawal order must be executed and included in the underlying blockchain before the order submitted by the arbitrageur. This means that the liquidity provider must pay a gas fee higher than the one attached to the arbitrage order. By Assumption 3, the gas fee paid by the arbitrageur for its order matches exactly its gain from the optimal arbitrage. Hence, the arbitrageur makes a zero net profit. Observe that it is never profitable for liquidity provider to pay a gas fee higher than , because he would otherwise incur a cost higher than the loss from arbitrage. Hence, for liquidity providers, the problem is not avoidable by exiting the contract before the arbitrage is exploited.111111One can easily derive the same result by introducing multiple arbitrageurs and modelling competition for first execution as a first-price auction with any tie-breaking rule. For any arbitrageur, the first execution has value , and for liquidity provider , the first execution has a value . At equilibrium, an arbitrageur wins the auction, and the gas fee that the winning arbitrageur pays for the first execution is exactly . In the absence of competition, the liquidity providers can exit with zero additional gas fee after the first execution. This also implies that liquidity providers end up submitting their exit orders with zero gas fee attached, because there is no benefit for bidding up. The next proposition formalizes the above discussion.

Proposition 1.

If and the token price shock hits only one token in sub-period 2 of period , then an optimal arbitrage order is the first order executed in sub-period 3. The arbitrage yields a loss for liquidity provider , and the gas fee attached to the arbitrage order is . If , or the prices of two tokens co-move, then the arbitrageur does not trade.

It is worth noticing that the arbitrage problem in the AMM is fundamentally different from the adverse selection problem arising in typical open limit-order book markets. In a limit-order book market, studied for instance in Glosten and Milgrom (1985) and Glosten (1994), market markers can be adversely selected by other investors who have private information about future realization of asset returns. However, in the AMM, the arbitrage exists even if there is complete information, due to the order execution mechanism of decentralized exchanges built on blockchains. Moreover, market makers in traditional open limit-order book markets can offset the adverse selection problem by placing a bid-ask spread, or they can even front-run the orders when they are able to predict the direction of order flow. In contrast, the AMM does not charge a bid-ask spread, and the liquidity providers are also unable to front-run the arbitrage order because the execution priority is decided by the gas fee attached to the order. As a result, the liquidity providers participating in the AMM are subject to token value loss, and must be compensated with enough trading fees.

A question which often puzzles liquidity providers is as follows: does the token value loss still exist if the token exchange rate reverts back to its initial level in subsequent periods? Some commentators have argued that if the token exchange rate is hit by a shock in the opposite direction, another arbitrage will occur and bring the ratio of deposits back to the initial ratio. Hence, there would be no token value loss from arbitrage. This is the reason why token value loss from arbitrage is often referred to as “impermanent loss” by practitioners (see also Harvey, Ramachandran, and Santoro (2021)).

Definition 1.

The “impermanent loss” is defined as:

| (4) |

where are specified by the following constraints:

In the definition above, are the amount of A and B tokens, respectively deposited in the AMM if the initial fair value exchange rate is . If the fair value exchange rate changes to at the end of the investment horizon, then after the arbitrage is exploited, the amount of A and B tokens in the AMM will be respectively (assuming zero fee). Moreover, the constraint imposed by the pricing curve, , needs to be satisfied. Thus, if are the amount of deposited tokens, is the total value of deposited tokens after the price change. If the tokens are not deposited, is the total value of tokens. The expression in (4) aims at capturing the magnitude of token value loss from depositing relative to not depositing. The “impermanent loss” is indeed zero if the token price reverts, i.e., All this leads to the seemingly logical liquidity management strategy to minimize impermanent loss—whenever a token value occurs, ignore token price movements in short term, continue depositing in the AMM, and wait for the reversion of exchange rate to occur. (see, for instance, Davis (2021)). However, as we show in Section 4.3, the above claim is fallacious.

4.2 Investors’ Trading

Each investor arrives to the exchange and decides the amount of A and B tokens to trade. Moreover, investors’ trades may leave an exploitable arbitrage opportunity for the arbitrageur.

Assume a “type A” investor arrives at sub-period 2 of period . The case of a “type B” investor arriving first follows from symmetry arguments. Since a “type A” investor has personal use for A tokens, she uses B tokens to exchange for A tokens. Formally, when the “type A” investor decides the desired amount of A tokens from the trade, she maximizes her total surplus from the transaction subject to the constraints imposed by the pricing function of the AMM:

| (5) | ||||

| s.t. | ||||

where is the total private benefit of the “type A” investor after trading, and is the total value of B tokens paid by the investor. We use and , to denote the maximum surplus of an arriving “type A” investor, respectively “type B” investor, in period .

Lemma 4.2.

If , then the arriving “type i” investor, , trades and earns a positive surplus from the transaction, i.e., . Moreover, the maximum surplus and the optimal trading quantities of an arriving investor, , are strictly positive, increasing in , and decreasing in . If instead , then the arriving investor does not trade.

Trading generates fees for the liquidity providers, which are then compensated for the arbitrage problem they face. After the investor arrives and trades, the amounts of A and B tokens in the AMM become and , respectively. The trade by the investor alters the ratio of A and B tokens in the AMM, which may lead to an arbitrage opportunity. Again, assume a “type A” investor arrives at . After the investor trades, the spot rate at which A tokens are exchanged for B tokens is higher than the fair value exchange rate:

The arbitrageur then exchanges A for B tokens and chooses the exchange order which solves the optimization problem (3).

4.3 The Adoption of the AMM

In this section, we first characterize the subgame perfect equilibrium of the game. We then provide the conditions under which a “liquidity freeze” occurs at equilibrium.

Proposition 2.

For any , there exists a subgame perfect equilibrium 121212Multiplicity of equilibria only arises if the liquidity providers are indifferent between investing A tokens and B tokens in period 1, and depositing tokens in the AMM in period 1 yields lower expected payoff than investing in either A token or B token. This means that the deposit amounts of A and B tokens in the AMM are the same for all possible equilibria. Moreover, for all the possible equilibria, the expected payoff of all the agents are the same.

We then examine the conditions under which at the equilibrium, the liquidity providers are incentive compatible to deposit their tokens into the decentralized exchange. If none of the liquidity providers deposits their tokens at period , no trading activities occur at that period. We call this market breakdown a “liquidity freeze”. The following proposition characterizes the condition under which a “liquidity freeze” occurs.

Proposition 3.

A “liquidity freeze” occurs surely in period 1 and 2 if and only if , where . Moreover, the threshold is increasing in , and decreasing in .

The above proposition states that when the token exchange rate is sufficiently volatile, the arbitrage problem is severe and a “liquidity freeze” occurs. The comparative static results are intuitive. First, when tokens become more attractive for investors ( increases) and the arrival rate of investors goes up ( increases), the expected trading volume increases and thus liquidity providers collect a higher trading fee. Hence, a “liquidity freeze” is less likely to occur. Second, when the tokens are more likely to be hit by a common shock ( increases) and co-move, arbitrage opportunities are less likely, i.e., the arbitrage problem faced by liquidity providers is less severe. Third, when the token exchange rate is more volatile (magnitude of the price shock and arrival rate of the shock both increase), the arbitrage becomes more costly for liquidity providers, and thus a “liquidity freeze” is more likely. Fourth, when increases, the difference in expected return of the two tokens decreases, and thus the opportunity cost of holding both tokens and providing liquidity decreases. In this way, the incentive of liquidity providers to adopt the AMM becomes stronger.

The above result suggests that the AMM may be more suitable for adoption of pairs whose token prices are highly correlated and not volatile, such as a pair of stable coins. Moreover, adoption is higher for tokens which provide investors with high personal use value, such as BTC and ETH. Because those tokens attract investors who in turn generate high trading volumes, liquidity providers can earn large trading fees and be compensated for the arbitrage problem they face. Last, but not least, adoption is very unlikely for pairs of tokens whose expected returns are low, such as the majority of Altcoins131313Altcoins is the term used to refer to all alternative cryptocurrencies that were launched after the massive success achieved by Bitcoin. which have no value and discernible purpose. This is because owning and providing liquidity for this kind of tokens is very risky and presents large opportunity costs.

Corollary 1.

Suppose that the fair value exchange rate changes from to in period 1. Then, the probability that the fair value exchange rate reverts to in period 2 decreases in , and the expected “impermanent loss” increases in . The expected marginal fee revenue from deposits does not change in . However, in period 2, liquidity providers deposit in the AMM at equilibrium if and only if , and the threshold increases in .

It is a very common misconception that the token value loss from arbitrage is ”impermanent” and will decrease to zero if the exchange rate reverts back to the initial level. This leads to the widely spread liquidity management strategy— after arbitrage loss occurs, if the token exchange rate is likely to revert to its initial level, then it is optimal for the liquidity providers to keep depositing and wait for exchange rate reversion. However, the above corollary shows that this claim is not sound, and the strategy is sub-optimal. As decreases, even though the probability of token exchange rate reversion increases, the expected “impermanent loss” decreases, and the expected marginal fee revenue from deposits is unaffected, liquidity providers’ incentive to deposit becomes weaker. This is because if the token exchange rate reverts in period 2, then the liquidity providers who deposit will only suffer from another token value loss due to arbitrage orders which trade B tokens for A tokens. No matter whether token exchange reverse or not, each realized arbitrage occurred still yields a permanent loss that cannot be offset by the previous arbitrages. In this way, when the reversion probability is high, instead of depositing and waiting for reversion, the optimal action of liquidity providers in period 2 should be holding A tokens in the portfolio and not providing liquidity at the AMM.

The benchmark upon which the widely accepted measure of “impermanent loss” (formally defined in (4)) is based, is misleading: it compares the return of depositing tokens in the AMM with the return of holding the same tokens in a portfolio out of the AMM for the whole time. Maintaining such a fixed portfolio is by no means the optimal strategy ex-ante or the best alternative of depositing tokens for the whole time, and this is why the measure of “impermanent loss” fails to fully account for the opportunity cost of depositing tokens at the AMM. The optimal liquidity management strategy at equilibrium requires the liquidity providers to account for opportunity costs, and decide their portfolio based on the expected return calculation for the following periods. Using this strategy as a benchmark, liquidity providers can quantify the opportunity cost of depositing in the AMM for the entire investment horizon.

Proposition 4.

The expectation and variance of the gas fee in period , 141414 denotes the expectation of the random variable conditional on the information available at the end of sub-period of period . and , are both increasing in the amount of token and deposited by liquidity providers.

The above proposition captures an important, yet undesirable, consequence of AMM adoption. Intuitively, if a large amount of tokens is deposited at the AMM, we expect more profitable arbitrage opportunities and thus gas fee surges due to arbitrageur’s bidding. Hence, as the AMM becomes more popular and widely adopted, the instability of its underlying infrastructure—blockchain–may increase. A surge of gas fees implies that other decentralized applications built on the same blockchain may lose their costumers due to high transaction fees, or significantly delay the execution of orders by their costumers. Additionally, if those fees become less predictable due to larger variance, the usage of the blockchain decreases. This means that the large adoption of the AMM may impose negative externalities on other decentralized applications using the same blockchain infrastructure.

5 The Design of AMMs

Since Uniswap first introduced AMMs with constant product function, numerous AMMs have been developed. They differ in terms of the pricing functions they utilize, the number of different tokens handled, and the charged transaction fees.

In this section, we study how such choices affect the equilibrium outcome. In Section 5.1, we show that the curvature of the curve determines the severity of the arbitrage problem and the deposit efficiency, i.e., the expected trading volume per unit token deposited. We also solve for the optimal curvature of the pricing function, i.e., the curvature at which a “liquidity freeze” is least likely to occur and aggregate welfare maximized. In Section 5.2, we argue why pooling more than two tokens in the AMM does not reduce the arbitrage problem.

5.1 The Curvature of Pricing Curve

We begin by recalling that at sub-period of period , any trade satisfies the relation:

| (6) |

where are, respectively, the amounts of A and B tokens added to (or withdrawn from, if the sign is negative) the AMM. The slope of the curve, , is the negative of marginal exchange rate, and the curvature of the curve at each point captures the rate of change of the marginal exchange rate.

For example, if the pricing function is linear, , then the slope of the curve is and its curvature is 0, i.e., the marginal exchange rate is fixed at the fair rate at sub-period 1 and equal to . Another example is the product function used by Uniswap V2 and Sushiswap, i.e., . The slope of the curve is , which means that the marginal exchange rate depends on the deposited tokens at the AMM. Moreover, the curvature of the exchange rate curve is positive. This implies that the marginal exchange rate from A to B tokens decreases in the amount of A tokens traded in, , which leads to the so called “slippage”.151515“Slippage” occurs when the rate at which A tokens are exchanged for B tokens (respectively if B tokens are exchanged for A tokens), is worse than the spot exchange rate (respectively if B tokens are exchanged for A tokens). The size of the slippage, which is determined by the curvature of the pricing curve, affects the equilibrium outcomes. To see this, consider the following family of pricing functions:

where , and is a scaling coefficient. The curvature of the pricing curve is increasing in . If , the pricing curve is a straight line with zero curvature; if , the pricing curve is the constant product function, and it has the largest curvature among all ’s, .

Lemma 5.1.

Suppose . The following claims hold:

-

1.

the expected arbitrage loss ratio in period t, that is, the expected loss from arbitrage divided by the total value of tokens in the AMM, , decreases in ;

-

2.

the investors’ surplus ratio in period t, that is, the sum of “type A” investor and “type B” investor’s maximum surplus divided by the total value of tokens in the AMM, given by , is decreasing in .

When increases, the curvature of the pricing curve also increases, and the exchange rate adjusts more quickly to the increased exchange amount. This yields a higher slippage for trades of the arbitrageur and of investors. Hence, the amount of a token the arbitrageur or investors exchange for the other token increases. Because trading costs increase, the arbitrageur extracts a lower profit from the arbitrage opportunity, thus the expected token value loss of liquidity providers decreases. This explains why employing a pricing curve with a larger curvature reduces the severity of the arbitrage problem.

A higher curvature does not benefit investors, who see their total trading surplus decrease as a result of higher trading costs. In a few cases, the fee revenue of liquidity providers would decrease if the curvature increases.

Proposition 5.

Suppose that Then there exists a critical threshold such that

-

1.

The expected payoff of liquidity providers at equilibrium is increasing in , for , and decreasing in , for .

-

2.

“Liquidity freeze” is least likely to occur if . That is, for any state , , if there is a “liquidity freeze” at period when , then there is a “liquidity freeze” at period for any other .

When the curvature of the pricing curve is too small, that is, , the exchange rate adjusts very slowly to the exchange amount, and the slippage of trading is very small. In this case, an arriving investor only needs to deposit a very small amount of A (respectively B) tokens to take out all the B (respectively A) tokens in the AMM. As a result, the fee revenue generated by investors’ trades is very small. Moreover, because the slippage has a small size, the arbitrage problem is severe. Hence, increasing the curvature of the pricing function leads to a higher fee revenue and a smaller arbitrage loss for investors, which in turn increases their payoffs. Conversely, when the curvature of the pricing function is too high, that is, , then so is the slippage of trading. Despite making the arbitrage problem less severe, investors become more reluctant to trade, and the fee revenue of liquidity providers is reduced. Hence, decreasing the curvature of the pricing function increases the payoffs of liquidity providers. If , the pricing curve achieves a balance between these two economic forces: generating a higher fee revenue and increasing the severity of arbitrage problem. As a result, liquidity providers have the strongest incentives to deposit their tokens, and the occurrence of a “liquidity freeze” is minimized.

Proposition 6.

Suppose that The equilibrium deposit efficiency in period measured by the expected investors’ trading volume divided by the total value of tokens deposited in period , 161616We define the deposit efficiency to be zero when ., is maximized if . Moreover, the socially optimal pricing curve, i.e., under which aggregate welfare measured by the sum of agents’ expected payoffs is maximized, is attained at .

The arbitrage loss and transaction fees are merely transfers of wealth between agents in our model, whereas the gas fee paid by the arbitrageur to miners of underlying blockchain is a deadweight loss. Hence, the highest social welfare is attained when the aggregated investors’ maximum surplus and liquidity providers’ payoffs are maximized. Both liquidity providers’ payoffs and deposit efficiency are maximized at . Hence, deposits of liquidity providers can support the highest number of trades for investors. Additionally, the amount deposited in the AMM grows the fastest if liquidity providers’ payoffs are maximized. This increases the expected aggregate trading volume and leads to higher social welfare.

5.2 Does Pooling More Tokens Reduce the Arbitrage Problem?

In this section, we analyze how pooling more than two types of tokens in the AMM affects the token value loss of liquidity providers from arbitrage. Many practitioners have the seemingly convincing intuition that pooling more tokens may alleviate the arbitrage problem due to diversification effects. Few AMMs, including Balancer, have been designed based on this intuition. Interestingly, we find that if an AMM manages more than two types of tokens, the arbitrage problem becomes worse.

Assume agents have access to three different tokens: A, B, and C token. There are two AMMs, one handles A and B tokens only, while the other handles all three tokens. Both AMMs utilize a constant product function, that is, for the first AMM, and for the second AMM. We denote the price of a single C token at sub-period of period by .

As in the baseline model, in each period the prices of tokens A, B, and C may move due to exogenous shocks. With probability , the price movements of A, B, and C tokens are driven by a common shock :

| (7) |

With probability , they are determined by independent, idiosyncratic shocks , respectively:

| (8) |

Apart from this adjustment, the model remains the same as the baseline model. The following proposition compares the arbitrage loss of the two AMMs in equilibrium:

Proposition 7.

Suppose for the AMM pooling two tokens and for the AMM pooling three tokens. At period t, the expected arbitrage loss ratio of the AMM pooling A and B tokens, , is smaller than the expected arbitrage loss ratio of the AMM which pools A, B, and C tokens, .

The above result shows that the arbitrageur can extract more profit from the AMM pooling three tokens, leading to a higher loss for the liquidity providers. The reason is twofold. First, an arbitrage opportunity becomes more likely as the number of tokens in the AMM increases. Consequently, the probability of a token value loss for liquidity providers increases. Second, for each realized arbitrage opportunity, the arbitrageur can extract a larger portion of the shocked token from the AMM deposit. Intuitively, if the price of token A increases due to a shock in period , the arbitrageur can only use token B to exchange for token A in the AMM pooling two tokens. The exchanged amount will be such that the marginal benefit of trading is equal to the marginal trading cost. However, in the AMM which pools three tokens, the arbitrageur can use both token B and C to exchange for the appreciated token A, and it will stop trading only when the marginal benefit of trading both B and C tokens for A tokens equals to the marginal trading costs.

The logic described above carries through for AMMs which pool tokens, . The main takeaway is that the arbitrage problem cannot be mitigated by pooling more tokens in the AMM.

6 Empirical Analysis

In this section, we provide empirical support to the main testable implications of our model. We state the implications in Section 6.1. We describe our dataset in Section 6.2. We define the variables used in our empirical validation in Section 6.3. We discuss the results from the regression analysis in Section 6.4.

6.1 Testable Implications

Our model generates the following implications:

-

(1)

An increase in token exchange rate volatility decreases the amount of tokens deposited at the AMM. As shown in Proposition 3, if the volatility171717The standard deviation of a change of the log token exchange rate over one-period is , which clearly increases in the parameter . of the token exchange rate increases, the arbitrage problem becomes more severe, and the liquidity providers have weaker incentives to deposit their tokens. We test this implication by examining how the amount of deposits in AMMs changes with the volatility of the token exchange rate.

-

(2)

A higher trading volume results in a higher amount of tokens deposited at the AMM. As shown in Proposition 3, if the token pairs attract more investors, both volume and trading fees increase, which gives liquidity providers stronger incentives to deposit. We test this implication by relating the change of deposits in AMMs with trading volumes.

-

(3)

Average levels and volatility of gas fees attached to pairs with larger exchange rate volatility are higher. Proposition 4 implies that, as the volatility of the token exchange rate increases, arbitrage opportunities become more profitable. This in turn yields a higher expectation and variance of the gas fee. To test this implication, we group all token pairs into two categories, “stable pairs” and “unstable pairs”, and examine whether transactions in “stable pairs” are associated with lower average levels and volatility of gas fees. “Stable pairs” consist of two stable coins pegged to one US dollar, and have lower price volatility relative to “unstable pairs”.

6.2 Data

The dataset contains histories of all trades, deposits, and withdrawals for a sample of 80 AMMs with actively traded pairs. Among the 80 AMMs, 40 of them are from Uniswap V2, and the rest are from Sushiswap. 7 pairs consist of only stable coins pegged to one US dollar, and they are denoted as “stable pairs”.

For each AMM, the transaction level data include the time stamp, the address of the investor, the gas price attached to the transaction, as well as the name and amount of tokens that the investor trades in or takes out of the AMM. If an investor trades in (takes out) both tokens in a transaction, then we identify the transaction as a deposit (withdrawal); if instead, the investor trades in one token and takes out the other token, we identify the transaction as a swap. We use the history to calculate and track the total liquidity reserve of both tokens in each AMM, and calculate the spot rate of the exchange from the liquidity reserves.

This study covers the 25-week period181818We choose this interval to have enough cross-sectional and time-series observations. A longer time period reduces the amount of AMMs available, as most of the AMMs are set up at the end of 2020. from Dec 22, 2020 to June 20, 2021. The number of AMMs initiated by Dec 22, 2020 is only 30. Among them, 16 are from Sushiswap, and the rest are from Uniswap; in particular, 3 pairs are “stable pairs”, and they all belong to Uniswap.

6.3 Definitions of Variables

We next describe the main variables in our analysis.

Token Exchange Rate Volatility.

We measure the volatility of the token exchange rate for AMM in week using the standard deviation of the log spot rate between two tokens deposited in the AMM , in week . This measurement is invariant with respect to the choice of base token191919In the foreign exchange market, the first element of a currency pair is denoted as the base currency, and the second one is referred to as the quote currency. We follow the same convention for an AMM, and refer to the first token in a pair as the base token, and to the second token as the quote token. of the pair and to scalar multiplication202020Some tokens are more valuable than others, with Bitcoin being a prominent example. A normalized measure makes the volatility of the token exchange rate comparable across pairs of token values.

Deposit Inflow and Outflow.

Denote the pair of tokens in AMM as token and token. We measure the change of deposits for AMM in week as follows:

| (9) |

where , are the total tokens and tokens deposited (if positive), or withdrawn (if negative) by liquidity providers of AMM , with deposit or withdrawal order during week . and are, respectively, the total liquidity reserves of and tokens in AMM at the beginning of week . is positive if the net deposit is larger than the net withdrawal, and negative otherwise.

Trading Volume.

We measure the total trading volume in AMM during week as follows:

| (10) |

where , are, respectively, the total amount of and tokens traded by investors with swap orders at AMM in week , and are, respectively, the total liquidity reserves of and tokens in AMM at the beginning of week . The above measure captures the total trading volume by investors relative to the total reserve in AMM during week .

Gas Price Volatility.

We measure the gas price volatility in AMM during week using the standard deviation of the gas price attached to all transactions executed on AMM in week . All AMMs we consider are built on the same blockchain, i.e., Ethereum, and thus levels and volatility of gas prices are comparable across pairs.

Table 1 presents summary statistics of the data. Most of the variables have large in-sample variations. Since “stable pairs” are pairs of stable coins pegged to one dollar, the log spot exchange rates are very close to 0, and their token exchange rate volatility is much lower than the volatility of “unstable pairs”.

N Mean SD 10th 50th 90th Panel A: Weekly-level Data Log Rate Volatility, All 750 0.049 0.039 0.004 0.042 0.093 Log Rate Volatility, Stable 75 0.004 0.002 0.002 0.003 0.005 Log Rate Volatility, Unstable 675 0.054 0.038 0.015 0.045 0.094 Token Inflow Rate, All 750 0.013 0.273 -0.164 -0.001 0.160 Token Inflow Rate, Stable 75 0.063 0.369 -0.179 -0.002 0.230 Token Inflow Rate, Unstable 675 0.008 0.260 -0.163 -0.001 0.141 Trading Volume , All 750 1.987 1.980 0.200 1.365 4.672 Trading Volume , Stable 75 1.033 1.018 0.173 0.762 2.032 Trading Volume , Unstable 675 2.093 2.032 0.231 1.465 4.794 Gas Price Volatility, All 750 183.045 240.660 29.993 124.363 364.445 Gas Price Volatility, Stable 75 84.888 67.732 17.458 75.391 157.683 Gas Price Volatility, Unstable 675 193.951 250.307 31.922 135.929 383.220 Panel B: Transaction-level Data Gas Price (Gwei), All 4,161,096 136.884 340.908 34 106.000 235.000 Gas Price (Gwei), Stable 223,318 117.471 113.586 40.000 99.000 202.000 Gas Price (Gwei), Nonstable 3,937,778 137.985 349.363 33.000 106.275 237.865 Absolute Value of Log Spot Rate, All 4,161,096 5.792 2.463 1.698 7.142 7.847 Absolute Value of Log Spot Rate, Stable 223,318 0.003 0.003 0.000 0.002 0.005 Absolute Value of Log Spot Rate, Nonstable 3,937,778 6.120 2.098 3.003 7.199 7.865

6.4 Empirical Tests and Results

In this section, we examine the three testable implications listed in Section 6.1.

6.4.1 Exchange Rate Volatility, Trading Volume, and Deposit

We estimate the following panel regressions to measure the impact of token exchange rate volatility and trading volume on deposit flow rates:

| (11) |

| (12) |

| (13) |

where indexes AMMs, indexes time, is the deposit flow rate (inflow if positive and outflow if negative), are respectively the AMM and time fixed effects, is the volatility of the token exchange rate of AMM in week , is the trading volume at AMM in week , and is an error term. We cluster our standard errors at the AMM level. The coefficients quantify the sensitivity of deposit flow on token volatility, and the coefficients give the sensitivity of deposit flow on trading volume.

Table 2 shows a negative, statistically significant relationship between the token exchange rate volatility and the deposit flow rate, which is consistent with our theoretical prediction that . After controlling for trading volume, a one-standard-deviation increase in weekly spot rate volatility (which is equal to 0.04) decreases the deposit flow rate by 25% standard deviations of that variable. Columns (b) and (c) show that there exists a positive, statistically significant relationship between trading volume and deposit flow rate, confirming our theoretical prediction that . After controlling for exchange rate volatility, a one-standard-deviation increase in trading volume (which is equal to 1.98) increases the deposit flow rate by 35% standard deviations of that variable. In summary, Table 2 confirms our model predictions from Section 6.1 that the amount of deposited tokens decreases with the exchange rate volatility, and increases with the trading volume. Additionally, the regression estimates indicate that these effects are economically significant.

| Dependent variable: Deposit Inflow Rate | |||

| (a) | (b) | (c) | |

| Intercept | 0.023 | ||

| (0.077) | (0.073) | (0.070) | |

| Exchange Rate Volatility | |||

| (0.182) | (0.405) | ||

| Trading Volume | |||

| (0.015) | (0.020) | ||

| Week fixed effects? | yes | yes | yes |

| AMM fixed effects? | yes | yes | yes |

| Observations | 750 | 750 | 750 |

| 0.11 | 0.14 | 0.17 | |

| Note: | ∗p0.1; ∗∗p0.05; ∗∗∗p0.01 | ||

6.4.2 Token Exchange Rate Volatility and Gas Price

We examine the impact of token exchange rate volatility on levels and volatility of gas fees. Specifically, we estimate the following two linear models:

| (14) |

| (15) |

where indexes AMMs, indexes time, and indexes transactions. We run regressions at weekly frequency212121We choose weekly, instead of daily frequency, to have enough observations to estimate the volatility of gas price. for the model in equation (14) and at daily frequency for the model in equation (15). is the volatility of gas price at time in AMM , is the gas price of transaction in AMM , are time fixed effects, is the fixed effect for all Uniswap AMM exchanges, is the dummy variable for “stable pairs” which consist of two stable coins pegged to one US dollar, and are error terms. We cluster our standard errors at the AMM level. The coefficients and quantify the differences in levels and volatility of gas fees between “stable pairs” and “unstable pairs”, respectively.

Table 3 indicates that the weekly gas price volatility of “stable pairs” is around 40% lower than that of “non-stable pairs”. Additionally, the gas price level for transactions of “stable pairs” is around 8% lower than that of “non-stable pairs”. In summary, Table 3 supports our model predictions from Section 6.1 that levels and volatility of gas fees are higher for pairs with larger exchange rate volatility. Moreover, the coefficient estimates indicate that these relationships are economically significant.

| Dependent variables: | ||

| Gas Price Volatility | Gas Price | |

| (a) | (b) | |

| Intercept | 189.48∗∗∗ | 137.34∗∗∗ |

| (16.13) | (1.61) | |

| Stable | -64.34∗∗∗ | -10.51∗∗∗ |

| (20.02) | (2.78) | |

| Week fixed effects? | yes | no |

| Day fixed effects? | no | yes |

| Exchange fixed effects? | yes | yes |

| Observations | 750 | 4,161,126 |

| 0.24 | 0.04 | |

| Note: | ∗p0.1; ∗∗p0.05; ∗∗∗p0.01 | |

7 Conclusion

Our paper analyzes the economic incentives behind blockchain-based financial intermediation. We show theoretically and empirically that exploitable arbitrage opportunities created by token exchange rate volatility limits the adoption of blockchain-based AMMs by liquidity providers. We also argue that the adoption of AMMs impose negative externalities on other decentralized applications built on the same underlying blockchain.

Our findings inform the liquidity management strategy of token holders. We argue that they should only deposit into AMMs whose token prices are stable and highly correlated, or whose trading volumes are high. Our results warn against providing liquidity into AMMs which manage Altcoins with no intrinsic value. Importantly, we argue that liquidity providers should not fall prey to the fallacy that token value loss from arbitrage is impermanent and keep depositing if exchange rate reversion is likely. Token exchange rate movements, regardless of the direction, leads to permanent loss, and liquidity providers need to account for the opportunity cost of depositing tokens into AMMs.

Our results have implications for the operation and design of DeFi exchanges. We argue that the curvature of the pricing curve used by the AMM governs the trade-offs between the severity of the arbitrage problem and the investors’ willingness to trade. When these two forces are well balanced, a “liquidity freeze” is least likely to occur, the deposit efficiency is the highest, and social welfare is maximized. Our analysis also sheds light on a common misconception among practitioners, and shows that pooling more than two tokens in the same AMM does not alleviate the arbitrage problem.

Our paper can be extended along several directions. The first extension is to study the governance of AMMs. Typically, decisions for the operations of DeFi projects are proposed, voted and made by investors who hold the governance tokens. However, different voters, such as developers, liquidity providers, and token investors, may have very different incentives, and their votes often lead to socially inefficient protocols, such as those demanding very high transaction fees. This calls for the design of a mechanism which distributes governance tokens to agents so to minimize agency costs. Another desirable extension is to design protocols through which DeFi projects internalize the externalities imposed on the underlying blockchains. Such a protocol would inform the decision of which DeFi projects should be built on the same blockchain versus multiple blockchains. While executing all DeFi projects on a smaller number of blockchains may increase safety, it would also increase congestion and transaction costs. We leave a systematic study of the trade-off between transaction safety and costs for future research.

References

- Abadi and Brunnermeier (2018) Abadi, J., and M. Brunnermeier. 2018. Blockchain Economics. NBER Working Papers 25407, National Bureau of Economic Research, Inc.

- Adams (2020) Adams, H. 2020. Uniswap. https://uniswap.org/blog/uniswap-v2/.

- Angeris et al. (2021) Angeris, G., H. T. Kao, R. Chiang, C. Noyes, and T. Chitra. 2021. An analysis of Uniswap markets. Working Paper.

- Athey et al. (2016) Athey, S., I. Parashkevov, V. Sarukkai, and J. Xia. 2016. Bitcoin pricing, adoption, and usage: Theory and evidence. Stanford University Graduate School of Business Research Paper No. 16-42. Available at SSRN: https://ssrn.com/abstract=2826674.

- Bagshaw (2020) Bagshaw, R. 2020. Top 10 cryptocurrencies by market capitalization. https://finance.yahoo.com/news/top-10-cryptocurrencies-market-capitalisation-160046487.html.

- Bartoletti, Chiang, and Lluch-Lafuente (2021) Bartoletti, M., J. Chiang, and A. Lluch-Lafuente. 2021. A theory of automated market makers in DeFi. Working Paper.

- Biais et al. (2019) Biais, B., C. Bisière, M. Bouvard, and C. Casamatta. 2019. The Blockchain Folk Theorem. The Review of Financial Studies 32:1662–715. ISSN 0893-9454.

- Budish (2018) Budish, E. 2018. The economic limits of bitcoin and the blockchain. Working Paper 24717, National Bureau of Economic Research.

- Campbell (2016) Campbell, R. H. 2016. Cryptofinance. Working paper.

- Chiu and Koeppl (2019) Chiu, J., and T. V. Koeppl. 2019. Blockchain-Based Settlement for Asset Trading. The Review of Financial Studies 32:1716–53. ISSN 0893-9454.

- Cong et al. (2020) Cong, L., X. Li, K. Tang, and Y. Yang. 2020. Crypto wash trading. Working paper.

- Cong and He (2019) Cong, L. W., and Z. He. 2019. Blockchain Disruption and Smart Contracts. The Review of Financial Studies 32:1754–97. ISSN 0893-9454.

- Cong, He, and Li (2020) Cong, L. W., Z. He, and J. Li. 2020. Decentralized Mining in Centralized Pools. The Review of Financial Studies 34:1191–235. ISSN 0893-9454.

- Cong, Li, and Wang (2020) Cong, L. W., Y. Li, and N. Wang. 2020. Token-Based Platform Finance. NBER Working Papers 27810, National Bureau of Economic Research, Inc.

- Daian et al. (2020) Daian, P., S. Goldfeder, T. Kell, Y. Li, X. Zhao, I. Bentov, L. Breidenbach, and A. Juels. 2020. Flash boys 2.0: Frontrunning in decentralized exchanges, miner extractable value, and consensus instability. In 2020 IEEE Symposium on Security and Privacy (SP), 910–27.

- Davis (2021) Davis, D. 2021. What is Impermanent loss? What can I do to avoid it? https://cryptoarena.org/what-is-impermanent-loss/.

- Easley, O’Hara, and Basu (2019) Easley, D., M. O’Hara, and S. Basu. 2019. From mining to markets: The evolution of bitcoin transaction fees. Journal of Financial Economics 134:91–109. ISSN 0304-405X.

- Gan, Tsoukalas, and Netessine (2021) Gan, J. R., G. Tsoukalas, and S. Netessine. 2021. Initial coin offerings, speculation, and asset tokenization. Management Science 67:914–31.