Original Article \paperfieldJournal Section \corraddressCuneyt Gurcan Akcora, Departments of Computer Science and Statistics, University of Manitoba, Winnipeg, MB R3T-2N2, Canada \corremailcuneyt.akcora@umanitoba.ca \fundinginfoNSF DMS 1925346, NSF ECCS 2039716, RGPIN-2020-05665

Blockchain Networks: Data Structures of Bitcoin, Monero, Zcash, Ethereum, Ripple and Iota

Abstract

Blockchain is an emerging technology that has enabled many applications, from cryptocurrencies to digital asset management and supply chains. Due to this surge of popularity, analyzing the data stored on blockchains poses a new critical challenge in data science.

To assist data scientists in various analytic tasks on a blockchain, in this tutorial, we provide a systematic and comprehensive overview of the fundamental elements of blockchain network models. We discuss how we can abstract blockchain data as various types of networks and further use such associated network abstractions to reap important insights on blockchains’ structure, organization, and functionality.

keywords:

blockchain, bitcoin and litecoin, ethereum, monero, zcash, ripple, iota1 Introduction

On October 31, 2008, an unknown person called Satoshi Nakamoto posted a white paper titled “Bitcoin: A Peer-to-Peer Electronic Cash System” to the Cyberpunks mailing list. In eight pages [1], Satoshi explained the network, transactions, incentives, and other building blocks of a digital currency that he called Bitcoin.

Bitcoin solves the problem of sending and receiving digital currency on the world wide web. However, the idea of a digital currency is as old as the Internet. For similar purposes, traditional banks and Internet companies have created online payment services, such as Paypal, Visa, and Master. However, a trusted entity intermediates currency flows in these solutions and updates user balances as transactions are processed. Blockchain removes the trusted entity and provides a framework to process transactions and maintain user balances correctly and securely.

Bitcoin and blockchain have been used interchangeably in the past, but Bitcoin is just one financial application among many other use cases of blockchain technology.

Blockchain stores a limited number of transactions (i.e., coin transfers) in a data structure called a block, which is in turn stored in a public ledger. We may consider the ledger as a notebook that has information to calculate user balances written in it. Blockchain represents a user with a blockchain address as a fixed-length string of characters (e.g., 1aw345….). A transaction can be as simple as sending bitcoins from one address to another, along with the required digital signatures. Transaction size increases if more addresses are involved. Blocks contain executed transactions. Block sizes (which determine the number of transactions in a block) are usually small (e.g., 1MB in Bitcoin that allows approximately 3000 transactions).

Blockchain uses an underlying peer-to-peer network to transmit blocks and proposed transactions between blockchain users worldwide. We will elaborate on “users” in later sections; however, users of the first blockchain, Bitcoin, are ordinary web users who can join the network by downloading and installing an application called a wallet.

A copy of the ledger is stored locally at every participant (i.e., node) of the peer-to-peer Bitcoin network. Every user is supposed to check its blockchain copy to learn about user balances. Bitcoin ledger is extended by appending a new block to the end of the chain every 10 minutes through a process that is called mining. The mining is where transaction approval/verification and coin creation occur, and blockchain removes financial institutions from this process and allows ordinary users to serve in their role. Mining is achieved by solving a cryptographic puzzle by trial and error. A valid solution is a proof that the miner has completed some work and effort to find the answer to the puzzle. The answer itself is an integer called nonce that once appended to the end of block content, the hash of the content satisfies a predetermined difficulty goal. The nonce and the resulting hash are known as proof-of-work, which has its roots in a research article [2].

Mining of each block is an open competition worldwide. Any user may compete to solve the puzzle to earn a handsome sum called the block reward, creating new bitcoins. This process is similar to fiat money printing; however, coins are created in predefined quantities (50 BTC in 2009, the amount halves every four years) at each block and given to the miner. Mining is, by purpose, designed to be difficult so that miners will not litter the blockchain with blocks. However, the difficulty is adaptive and depends on the number of miners and their computing power. Furthermore, Bitcoin uses an adaptive difficulty level to reduce the frequency of block mining. The blockchain peer-to-peer network participants will receive the latest block in time and be aware of its transactions. Awareness prevents malicious users from spending the same coin multiple times. For example, Bitcoin updates the mining difficulty to create a ten-minute gap between two blocks on average, and Ethereum aims at 12-15 seconds per block.

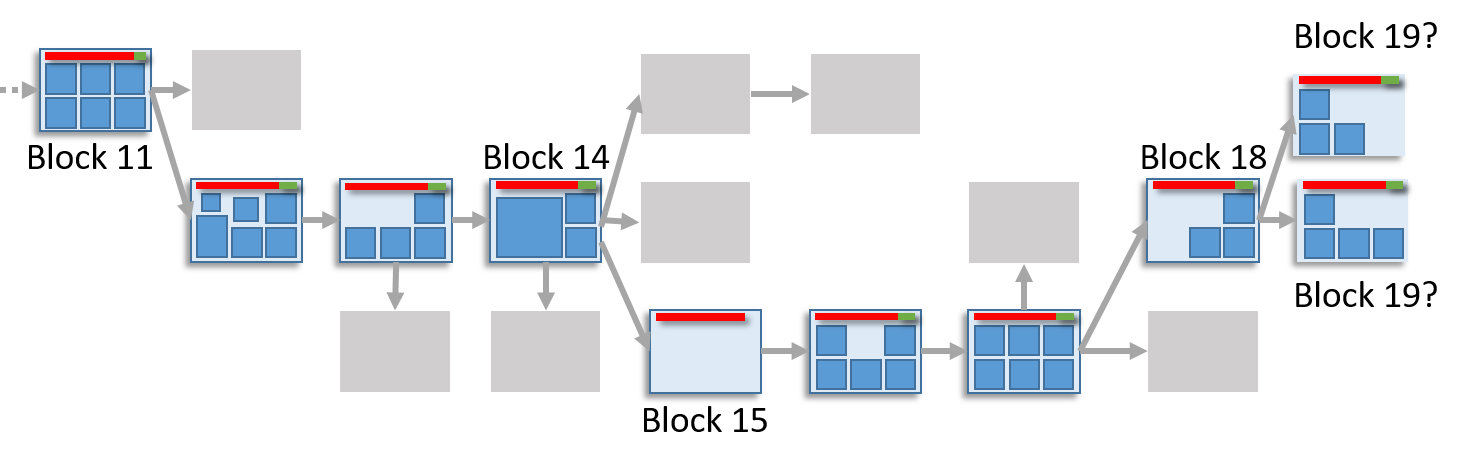

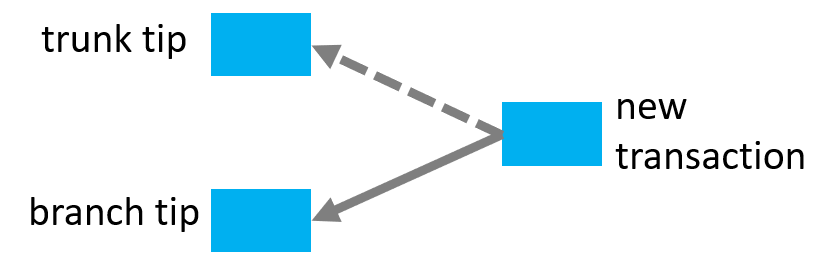

As nodes compete worldwide, miners create candidate blocks and append them to the chain. The competition is resolved by adopting the candidate that appears on the longest blockchain (see Figure 1). As miners append more blocks to the longest chain, the earlier blocks are deemed less likely to change, i.e., data in earlier blocks are considered final.

In Figure 1 a blockchain has 19 blocks (the latest block, has two competing candidates). The longest chain is called the canonical path, and blocks on the chain are deemed valid (i.e., to ). Gray boxes show stale blocks that have failed to be a part of the blockchain. An arrow shows a parent-child relationship between blocks. For example, is the parent of ( is mined later than ).

Blockchains proliferate, and the ecosystem is in evolution. A diverse set of blockchains have proposed novel mechanisms in storing data and representing users, coin transfers, smart-contract operations, and more. As a result, mining blockchain data requires domain expertise which may seem daunting to data scientists.

In this survey, we take a holistic view and define salient characteristics of six significant blockchains in terms of their data structures: Bitcoin, ZCash, Monero, Ethereum, Ripple, and IOTA. As Bitcoin is the first blockchain, we first teach the UTXO blockchains and design choices of Nakamoto that have significantly affected how new blockchains function and store data. The Ethereum section covers the basics of smart contracts, tokens, and other decentralized finance constructs. In the Ripple and IOTA sections, we teach their use cases beyond cryptocurrency and platform aspects. We conclude the survey with an overview of graph types found in these blockchains.pears on the longest blockchain

2 A Taxonomy of Blockchains and Transaction Networks

After Bitcoin’s popularity, various improvements to blockchain have been suggested and implemented in other digital currencies. Bitcoin, so far, has been very conservative in changes to its core technology. A few common points stand out between all blockchain implementations in mining, coding capabilities, and data scalability solutions.

We can broadly classify blockchains as i) private or public blockchains and ii) currency or platform blockchains. A third discussion point is about first vs. second layer technologies that determine how much data blockchains should store on-chain.

Private, Consortium vs. Public. Most blockchains, such as Bitcoin and Ethereum, are permissionless. They store data publicly, and any user can mine a block (Ethereum 2.0, when implemented, will change the mining algorithm). Anyone can join the Blockchain network and download blocks to view the transactions in them. When used by companies, a public blockchain would reveal sensitive corporate data to outsiders. Instead, private blockchains, such as Hyperledger fabric by IBM [3], have been developed to restrict block mining rights or data access to one participant (i.e., private blockchain) or a few verified participants (i.e., consortium blockchain).

Currency vs Platform. Bitcoin and other cryptocurrencies store coin transactions in blocks as data. However, blockchain is oblivious to the type of stored data, which can be multimedia files, weblogs, digitized books, and any other data that we can fingerprint by using a hash function. A hash function takes an unlimited length of data and creates a fixed length (e.g., 256 bits in SHA-256) representation using mathematical operations.

In 1997, Nick Szabo, an American computer scientist, had envisioned embedding what he called smart contracts as “contractual clauses in the hardware and software to make a breach of contract expensive” [4]. Almost 20 years later, Blockchain enthusiasts saw a path to implement this vision. Blockchain platforms Neo (2014), Nem (2015), Ethereum (2015), and Waves (2016) have stored and run software code, called smart contracts, on a blockchain. Smart contracts are written in Turing-complete language. However, the block gas limit restricts what transactions can include in the code. For example, on Ethereum, a smart contract cannot be arbitrarily long to encode an algorithm. As a result, blockchain opponents argue that the Ethereum gas limit prevents Turing-complete smart contracts.

The benefits of storing code on a blockchain are multi-fold. Every blockchain network node can read smart contracts, and transactions can execute contracts by sending call messages to them, and all blockchain nodes will run the contract with the message. These aspects mean that smart contracts allow unstoppable, unmodifiable, and publicly verifiable code execution as transactions between blockchain participants. Any blockchain classification can be flexed to allow public-private functionalities. For example, Hyperledger Fabric uses smart contracts in permissioned settings. The Ripple credit network is a permissioned blockchain that restricts block mining but stores data publicly.

First vs. Second Layer Technologies. Over time, blockchains started to run into scalability issues due to limited block sizes and increased user participation. Blockchains developed initial solutions, such as SegregatedWitness,111https://en.bitcoin.it/wiki/Segregated_Witness to leave some of the encryption signatures and other non-transactional data out of blocks to make space for more transactions. Scalability efforts have culminated in second layer solutions, such as the Lightning Network [5], where the network executes most of the transactions off-the-blockchain. The first layer (i.e., the blockchain itself) only stores a summary of transactions that occur on the second layer. Second layer networks, such as the Lightning Network, are a hot research area in network analysis that can be the topic of an extensive review article on its own. Due to space limitations, this manuscript will only teach blockchain networks that we can extract from the first layer, i.e., the blockchain itself.

Blockchains have come to contain various data such as sensor messages on IOTA, software code on Ethereum, and international banking transactions on Ripple. We give an outline by considering two major blockchain types: cryptocurrencies and platforms. Cryptocurrencies are designed to store financial transactions between addresses. A Blockchain platform stores financial transactions as well but furthermore stores software code in smart contracts.

Blockchains can further be categorized into two broad categories in terms of transaction type: account-based (e.g., Ethereum) and unspent transaction output (UTXO)-based (e.g., Bitcoin, Litecoin) blockchains. Traditionally cryptocurrencies are UTXO-based, whereas platforms are account-based. The difference between UTXO and account-based models has a profound impact on blockchain networks. In the first type of account-based blockchains, an account (i.e., address) can spend a fraction of its coins and keep the remaining balance. An analogy to account-based blockchains is a bank account that makes payments and keeps the remaining balance in the account. A transaction has exactly one input and one output address (an address is a unique identifier on the blockchain transaction network). We may use an address to receive and send coins multiple times. The resulting network is similar to traditional social networks, which implies that we can apply social network analysis tools directly to account networks. In turn, the second type (i.e., UTXO-based blockchains), such as Bitcoin, are the earliest and most valuable blockchains. Bitcoin constitutes around 45-60% of total cryptocurrency market capitalization. Litecoin has approximately 2% capitalization. On UTXO based blockchains, nodes (i.e., addresses) are mostly one-time-use only, complicating network analysis. See Section 8 for issues that complicate network analyses.

Remark 2.1.

A blockchain platform uses smart contracts to implement complex transactions, resulting in a diverse set of networks. Traditionally, blockchain platforms have followed an account-based blockchain model. For this reason, we use the terms account blockchain and blockchain platform interchangeably. However, in theory, a platform can also employ a UTXO transaction model. Similarly, a cryptocurrency could use an account-based transaction model. The reader must discern the distinction between account and UTXO based blockchain networks.

| UTXO | Account | DAG | Platform | Cryptocurrency | Private | Public | |

|---|---|---|---|---|---|---|---|

| Bitcoin | \checkmark | \checkmark | \checkmark | ||||

| ZCash | \checkmark | \checkmark | \checkmark | ||||

| Monero | \checkmark | \checkmark | \checkmark | ||||

| Ripple | \checkmark | \checkmark | \checkmark | ||||

| Ethereum | \checkmark | \checkmark | \checkmark | ||||

| IOTA | \checkmark | \checkmark | \checkmark | \checkmark |

Table 1 shows the focus of this manuscript and lists the blockchains that we will cover. Specifically, we teach two projects that differ from cryptocurrencies and platforms in critical aspects: Ripple and IOTA. Ripple is a credit network that predates blockchain fame. Ripple keeps a ledger of transactions where participants can trade user-issued currencies along with the native cryptocurrency of the Ripple, which is called XRP. The Ripple network moves currencies across the world, and financial institutions mainly use it. Recently, Ripple has also implemented smart contracts (called Hooks). We include Ripple in this manuscript since Ripple uses key blockchain technologies, such as hash-based identities and smart contracts, although not a blockchain by definition. IOTA Tangle is a directed acyclic graph of transactions. However, the underlying transaction model is UTXO based. IOTA relegates mining to each transaction’s creator and does not incur a transaction fee. Although IOTA has its associated cryptocurrency, mainly Internet-of-Things devices use IOTA to share and store data in industrial applications.

3 Bitcoin, Monero and ZCash: UTXO Networks

A cryptocurrency transaction is a construct that consumes one or more outputs of previous transactions and creates one or more outputs. As Bitcoin is a good representative of cryptocurrencies, we will use its data to teach this section. Note that Litecoin data is in the same format as Bitcoin, and in the past, we could have parsed them by using the same software library (e.g., Bitcoin4J). We will conclude the section with Monero and Zcash networks.

Bitcoin stores sequential block data in blk*.dat files on the disk. For example, block1 is serialized and appended into the blk00000.dat file. Next, Bitcoin appends a magic byte to separate block 1 from the upcoming block 2 in the dat file. For example, the Bitcoin mainnet uses 0xD9B4BEF9 as the magic byte. As the number and size of transactions in a block determine the block size, each dat file may contain a different number of blocks.

Each block contains one coinbase transaction and zero or more spending transactions. A coinbase transaction is the first transaction of the block and contains the block reward plus a sum of fees from the block’s transactions, if any. Note that a transaction may leave nothing as a transaction fee but still get mined in the block. The Bitcoin protocol sets the mining reward. If a miner records the block reward higher than the set amount, the network will reject the block. However, if the miner sets the block reward less than the set amount, the block will be accepted, and the miner will have lost bitcoins. In reality, these bitcoins are lost to the protocol, and the total bitcoin supply decreases from 21 million bitcoins.

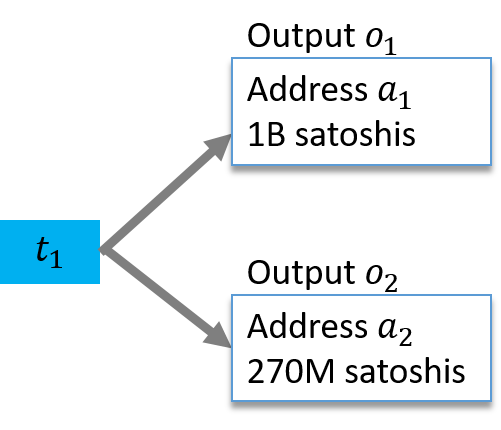

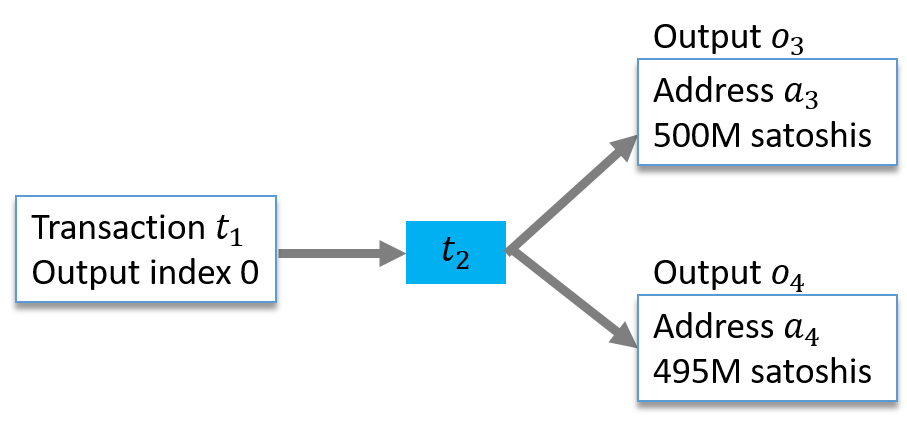

A coinbase transaction has no input but one or more outputs (Figure 2). In a sense, in a coinbase transaction, the miner can write itself a check in the amount of mining reward plus transaction fees. A coinbase transaction increases the total bitcoin supply by the mining reward amount. This is where new coins are created in Bitcoin. For this reason, a coinbase transaction lists no input. All other transactions must list one or more inputs that are being spent. Usually, a coinbase transaction has a single output address, and the address belongs to the miner. Some mining pools pay their miners in coinbase transactions. Such transactions may have hundreds of output addresses where each address belongs to an individual pool member. In Figure 2 the coinbase transaction has two outputs that total 1.270B satoshis, out of which 1.25B (12.5 bitcoins) are the mining reward, whereas 20M are the sum of transaction fees. Satoshi is the subunit of bitcoin (as Cent is the subunit of US dollar), and one bitcoin contains 100 million satoshis. As Figure 2 shows, an output has two useful information: amount and address. An address can next use the received output of in a spending transaction. Figure 3 shows the associated spending transaction that consumes and creates two new outputs.

A look at Figure 3 reveals an interesting point about how Bitcoin records transactions. Transaction gives the consumed output with its previous transaction id (the hash of , which created this output) and the output index. From this information, we can deduce that we are spending the zeroth output of , but this does not tell us the amount or address (). By only linking the previous transaction , we can learn the corresponding amount and address.

From Figure 2 we see that the zeroth output of holds 1B satoshis. We will denote the satoshi amount in an output with , i.e., . Next, in Figure 3 500M and 495M satoshis are sent to and . The difference between satoshis are implicitly left (by the transaction creator) as the transaction fee. The miner’s job is to validate that output amounts are greater than or equal to the input amounts. Furthermore, the miner must observe all previous blocks and ensure that another transaction has not already spent . If the miner makes a mistake and includes an invalid (e.g., already spent output, too great an output amount) transaction, the network will reject the miner’s block.

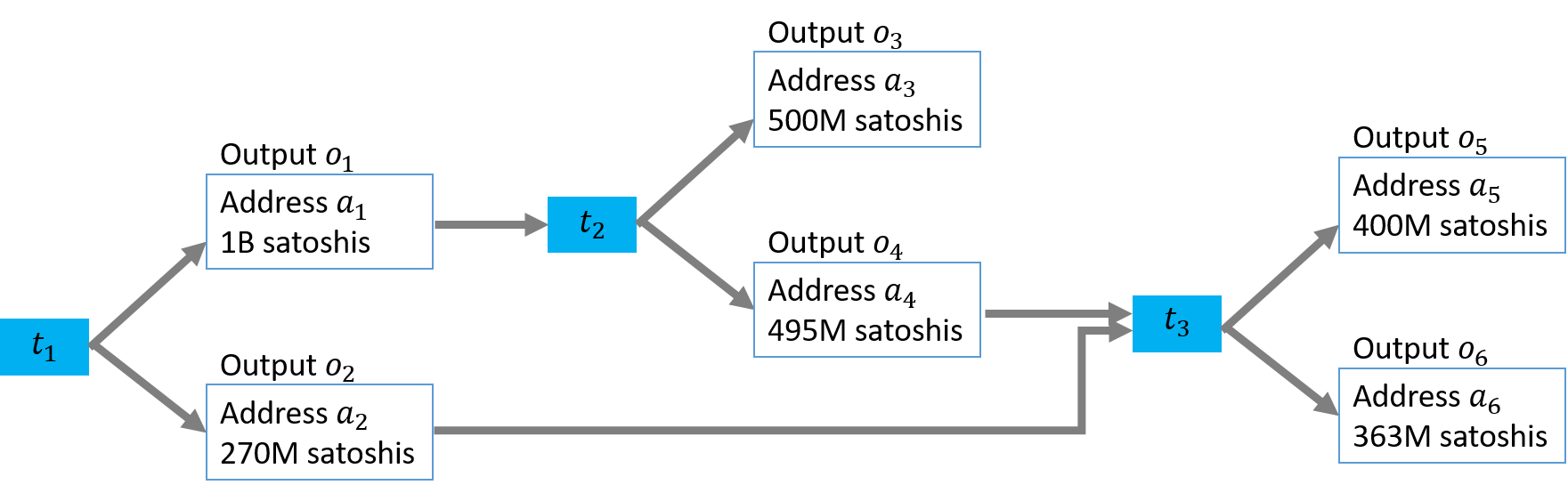

In practice, starting from an output, it is possible to go back in time and trace the lineage of a coin to reach a coinbase transaction. For example, the output linked graph in Figure 4 shows the third transaction , which has two inputs. The output which has two lineages: and . However, the lineage can be obscured by mixing schemes [6].

As well as multiple outputs, a Bitcoin transaction allows multiple inputs. The owner of each input must sign its portion of the transaction to prove an authorized coin transfer. A many-to-many transaction is an interesting data type that we do not encounter in banking and finance; multiple addresses merge their coins and send them to multiple receiving addresses. For the output, a Bitcoin address can be created for free and shared with the sender. Output addresses of a transaction need not belong to the same real-life entity: and may belong to people who have never met in real life.

The same reasoning is less likely to apply to input addresses. There can be multiple scenarios considering the inputs.

-

•

The user behind signs the input of and sends the partially signed transaction to the user behind , who signs its input and finally sends the transaction to the mempool. This scenario implies that the users are different people but know and communicate with each other.

-

•

The user behind signs the input of and sends the partially signed transaction to a public forum where other users can add their inputs, and the transaction is finally sent to the mempool by one of them. This scenario implies that the users are different people, do not know but communicate with each other.

-

•

A single user owns both and . The user signs both inputs and sends the transaction to the mempool.

The tree cases mean that we can never be sure about the joint ownership of inputs. However, in practice, most of the time, all input addresses belong to the same user. We can use this information to link addresses across transactions.

Remark 3.1.

When a transaction sends coins to an address, the address appears in the transaction, but the public key of the receiver address is unknown. The receiver discloses their public key only when spending the received coins, and any user in the network can hash the key to verify that the hash equals the address. The matching hash is additional proof that the assets belong to the receiver. In a P2PSH (pay to script hash) address (which starts with ’3’), the owner must show the script whose hash equals the address.

3.1 Graph Rules for UTXO Blockchains

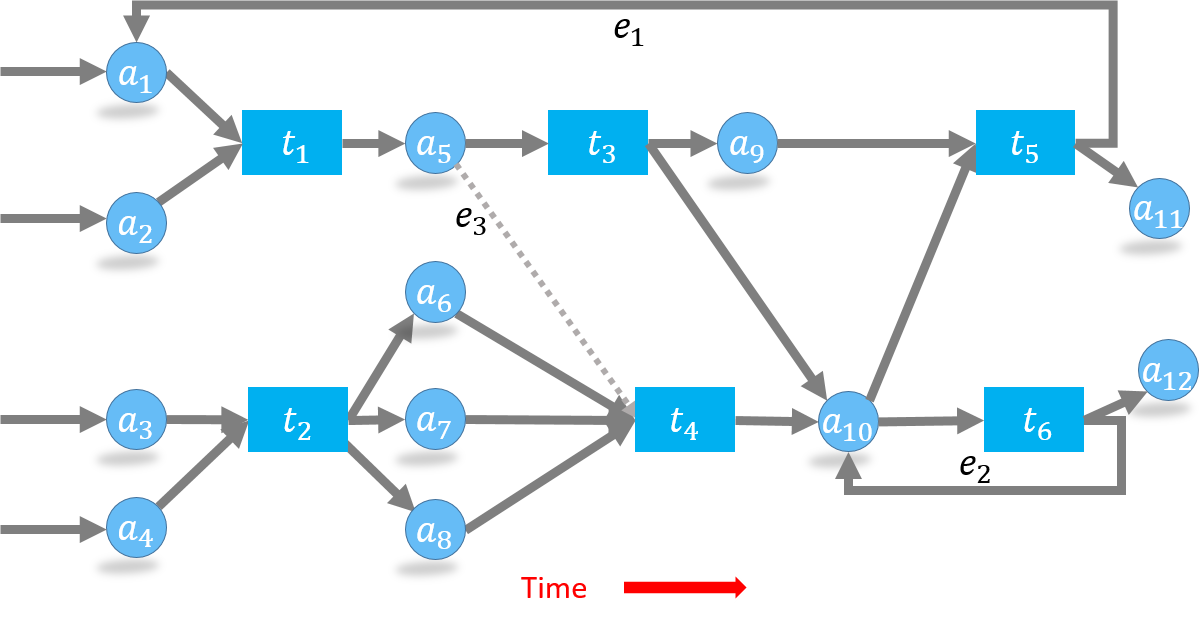

Before modeling the Bitcoin network, we emphasize three graph rules that restrict how transactions can transfer coins. These rules are due to Bitcoin design choices made by Satoshi Nakamoto. For clarity, we will replace outputs with the associated addresses and work with the toy graph shown in Figure 5.

-

1.

Balance Rule: Bitcoin transactions consume and create outputs. Outputs are indivisible units; we can spend each output in one transaction only. Consequently, we must spend coins received from one output in a single transaction. Any amount that we do not send to an output address is considered a transaction fee, and the miner collects the change as the transaction fee. To spend a portion of the coins in output and keep the change, we must create a new address and send the remaining balance to this new address. Another option is to use our existing address as one of the output addresses and re-direct the balance (as done in edge in Figure 5). As a community practice, reuse of the spender’s address (i.e., address reuse) is discouraged. As a result, most address nodes appear in the graph two times: first when they receive coins and second when they spend them.

-

2.

Source Rule: We can merge input coins from multiple transactions and spend them in a single transaction (e.g., the address receives coins from and to spent in and in Fig. 5). However, could have spent all its coins in a single transaction as well.

-

3.

Mapping Rule: In a transaction the input-output address mappings are not explicitly recorded. For instance, consider the transaction in Fig. 5. The output to address may come from either or . We can make an analogy with lakes where in-flowing rivers (inputs) bring water (coins) to the lake (transaction), and outgoing emissaries (outputs) take the water (coin) out.

Besides the three rules, in our research, we have encountered the following Bitcoin spending practices:

-

•

A transaction may list the same address in multiple outputs. We have encountered transactions where all outputs have the same address. As the address must be recorded more than once, this (spam) practice unnecessarily increases the transaction size.

-

•

In time, an address may receive outputs from multiple transactions. Typically, an address collects all outputs and spends them at once. In rare cases, an address can receive outputs again after it has spent its coins. For example, edge in Figure 5 brings an output to after has spent its coins in .

-

•

Address reuse, as shown in , is widespread. Although the community frowns upon address reuse, users are still reluctant to create a new address for change. Hierarchically deterministic wallets facilitate automated address creation (https://en.bitcoin.it/wiki/Deterministic_wallet). However, address reuse did not abate.

-

•

Community practice is to wait for six confirmations (blocks) after receiving a transaction output before spending it. The practice protects bitcoin buyers against history reversion attacks. Thereby, we must spend coins of an output in a minimum of six blocks after they are received ( minutes later). A day sees 144 blocks; a coin should move at most 24 times (in 24 blocks). In reality, however, once a transaction reaches the mempool, it can be considered final, and absent a double-spending, its coins can be used in another transaction immediately, even in the same block.

-

•

It is possible to have ordered transactions in a single block, where and consumes the outputs generated by . As a result, some coins move in the Blockchain network more than 144 times a day.

Remark 3.2.

In theory, Monero, Dash, and ZCash privacy coins are UTXO blockchains; their Blockchain networks are similar to Bitcoin’s. In practice, privacy coins employ cryptographic techniques to hide node and edge attributes in the blockchain network. For example, ZCash hides information in its shielded pool, whereas Monero adds decoy UTXOs to the input UTXO set. This section explains how to model the blockchain network when the node and edge attributes are public (as in Bitcoin).

Data scientists model Bitcoin transaction networks as address or transaction graphs. Address graph omits transactions, and the transaction graph omits addresses. Both approaches are influenced by traditional social network analysis, which employs graphs with one node type only. Additionally, one can extract chainlet substructures from the blockchain network. In the following sections, we will cover these graph models.

3.2 UTXO Transaction graph

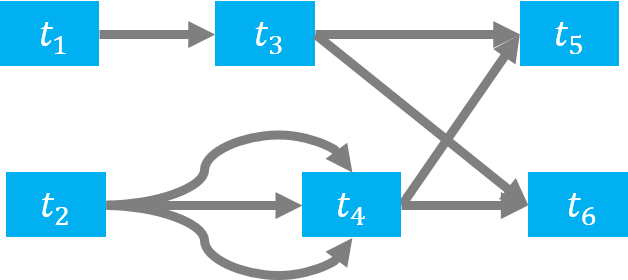

Transaction graphs omit address nodes from the transaction network and create edges among transactions only. Figure 6 shows the transaction graph of the network shown in Figure 5. The most important aspect of the transaction graph is that a node can appear only once. There will be no future edges that reuse a transaction node.

The transaction graph contains far fewer nodes than the network it models. We can immediately observe a few drawbacks from Figure 6. By omitting addresses, we lose the information that and are connected by . The address reuse of is hidden in the transaction graph as well. Additionally, unspent transaction outputs are not visible; we cannot know how many outputs are there in and . Similarly, if had an unspent output, we would not learn this information from the graph. In Bitcoin, many outputs stay unspent for years; the transaction graph will ignore all of them.

The advantages of the transaction graph are multiple. First, we may be more interested in analyzing transactions than addresses. For example, anti-money laundering tools aim at detecting mixing transactions, and once they are found, we can analyze the involved addresses next. Many chain analysis companies focus their efforts on identifying e-crime transactions. Second, the graph order (node count) and size (edge count) are smaller, which is better for large-scale network analysis. The reduction is because, on UTXO networks, transaction nodes are typically less than half the number of address nodes. For example, Bitcoin contains 400K-800K unique daily addresses but 200K-400K transactions only. As we will explain in the next section, the address graph contains many more edges than the transaction graph.

3.3 UTXO Address Graph

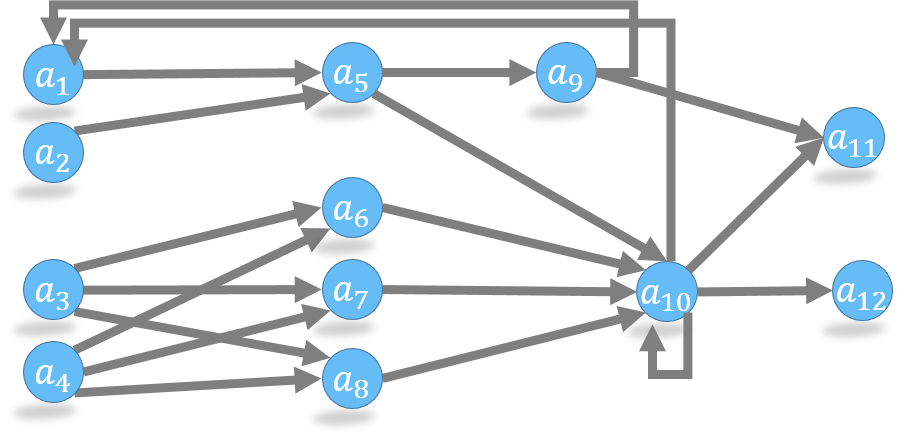

The address graph is the most commonly used graph model for UTXO networks. The address graph omits transactions and creates edges between addresses only. Address nodes may appear multiple times, which implies that addresses may create new transactions or receive coins from new transactions in the future.

Address graphs are larger than transaction graphs in node and edge counts. As the mapping rule states, a UTXO transaction does not explicitly create an edge between input and output addresses in the blockchain transaction network. When omitting the intermediate transaction node, we cannot know how to connect input-output address pairs. As a result, data scientists create an edge between every pair. For example, in Figure 7 we create six edges between inputs () and outputs (). If there are few addresses in the transaction, this may not be a big problem. However, large transactions can easily end up creating millions of edges. For example, the highest number of inputs in a Bitcoin transaction was 20000 (821 on Litecoin), whereas the highest number of outputs in Bitcoin was 13107 (5094 on Litecoin). The address graph approach will have to create one million edges for a transaction with one thousand inputs and one thousand outputs.

Graph size is not the only problem. The address graph loses the association of input or output addresses. For example, the address graph in Figure 7 loses the information that edges and were used in a single transaction; address graph edges would be identical if the addresses had used two separate transactions to transfer coins to and . We can solve this issue by adding an attribute (e.g., transaction id) to the edge; however, this requires additional edge features.

Address graph edge weighting is done as follows. Consider a transaction with its input addresses and output addresses . We will denote the amount an address sends to or receives from as . Amount of coins in an address is denoted as . The edge between an input address and an output address is assigned an edge weight as

Example 3.3.

Consider a transaction with input addresses and amounts as , bitcoin. The transaction has two output addresses and their associated amounts as , bitcoin. The transaction fee is left as the difference between inputs and outputs: bitcoin. When creating the address graph, is weighted as , whereas .

Compared to the transaction graph, the address graph loses less information from the Blockchain network. For example, the address graph does not fail to record past address reuse (edge from to ) and change address reuse (as self-loop at ). Furthermore, unspent output addresses remain visible in the graph.

Remark 3.4.

Address reuse: A blockchain address can be used in multiple transactions as a coin sender or receiver. However, address reuse is discouraged. Ideally, a Bitcoin user should create a new address each time it receives bitcoins in a transaction. Address clustering methods aim at linking multiple addresses to identify real-life entities behind the addresses.

Once we create the address graph, we may be inclined to run traditional network science tools and algorithms on it. However, some of these methods are ineffective in blockchain networks. We can count address clustering, motif analysis, and core decomposition among these methods. UTXO networks are sparse and devoid of closed triangles. Furthermore, address reuse is discouraged on UTXO blockchains as a community practice; most addresses appear in two transactions (i.e., receiving and spending coins). As a result, off-the-shelf Data Science algorithms and software libraries are relatively inefficient on address graphs.

For example, network motif analysis [7] aims at finding repeating subgraphs of specific orders (usually three nodes). Searching for motifs in Figure 7 will try to find shapes without considering how specific addresses appear together as inputs or outputs. Addresses , and will most likely never form a triangle. Also, a triangle between , and is very unlikely. As a second example, motifs do not consider which addresses can be active. For instance, once spends its output in a transaction without receiving a new output, it will never create another edge in the future. Keeping such nodes in memory and searching for their future edges are unnecessary.

Past address reuse is discouraged, but motifs do not use this information and search for (non-existent) edges to past addresses in a large address graph. As a third example, consider that many coins are moved in the network more than 100 times a day, and each time they are received in newly-created addresses. The resulting graph will be huge, but there will be almost no closed edge triangles.

Due to these issues, we argue that we should model UTXO networks as a forward branching tree rather than networks. More importantly, Data Scientists should develop tools to incorporate domain practices such as aversion to address-reuse.

3.4 Monero and Zcash Transaction Networks

Monero and Zcash are two UTXO based cryptocurrencies that hide transaction details from the public. For this reason, Monero and Zcash are called privacy coins.

3.4.1 Monero Networks

Monero (created in 2014) uses ring signatures to hide inputs of a transaction. In a ring signature scheme [8], any one of the members of the ring can sign a document. Any third party can publicly verify the signature but cannot deduce which ring participant signed it. Monero treats each transaction input as a document that ring members will sign. The process to create a transaction is carried out as follows:

-

1.

Choose one or more of your UTXOs that you want to spend in a transaction.

-

2.

For each UTXO that you plan to spend, choose 10 foreign UTXOs (i.e., ring member UTXOs that do not necessarily belong to you) that you will use as decoys.

-

3.

Prepare the ring signature by using the private key of your address.

-

4.

After signing each input, forward the transaction to the Peer-to-Peer network.

The reader should note that decoy UTXOs can belong to any other user, and the transaction creator does not need the consent of these users to include their UTXOs as decoys in a ring. Choosing the best decoy UTXOs to hide the identity of the actual input UTXO is an active research area.

Monero initially allowed using 0-decoys, i.e., not adding any decoys to the ring. In this case, a Monero transaction was equivalent to a Bitcoin transaction where all information is public. Monero also allowed a user to set the ring size, which could be very big. Privacy research has shown the drawbacks of this liberal approach [9, 10]. First, 0-decoy transactions jeopardize the privacy of other blockchain users [10] since a 0-decoy transaction input reveals that no other transaction could have spent it. As a result, we can remove the input from the rings of future transactions. Second, we can use a meta-analysis on similar ring sizes and link transactions of the same user.

Monero banned 0-decoy transactions in 2016, incremented the mandatory ring size from 5 to 7 and eventually to 11. With the RingCT update, Monero has also hidden UTXO addresses and amounts. As a result, very few pieces of transactions are visible to the public, making it an ideal privacy coin. Figure 8 shows a Monero address-transaction graph. Note that although inputs list 11 member rings, outputs are listed individually. However, the receiving address and received amount are hidden in the UTXO. Monero uses commitments and range-proofs to make sure that amounts are spent correctly (See Chapter 4 in [11]).

3.4.2 Zcash Networks

Zcash uses zero-knowledge proofs to hide information about some transactions. In cryptography, a zero-knowledge proof is a method by “which one party can prove to another party that they know a value , without conveying any information apart from the fact that they know the value ”. 222https://z.cash/technology/

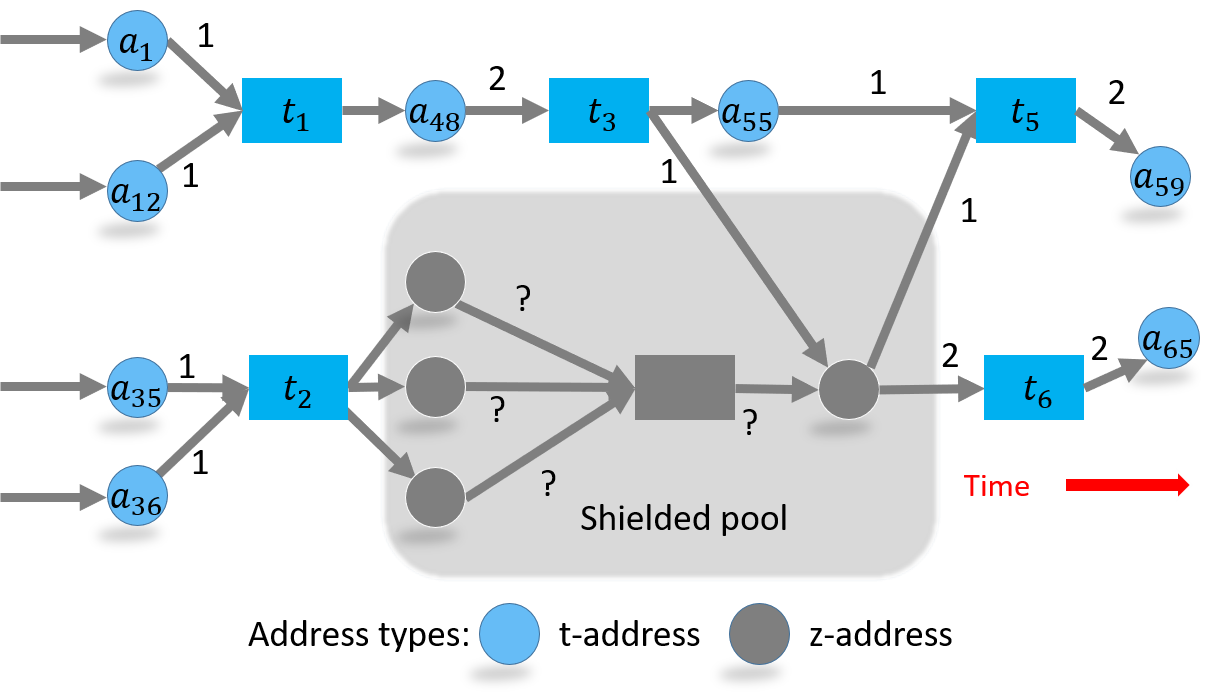

We can broadly categorize Zcash transactions into shielded and public transactions. Public transactions are identical to Bitcoin transactions where amounts, addresses, and all other pieces of information are public. Shielded transactions hide all transaction information from the public by using zero-knowledge proofs. Addresses that are used in public transactions are called t-addresses and start with the letter “t” such as t1K2UQ5VzGHGC1ZPqGJXXSocxtjo5s6peSJ. Shielded transactions use shielded (also called private) addresses that start with the letter “z”.

With and addresses, there are five Zcash transactions types. We will show these types by using Figure 9, and explain them as follows:

-

1.

-to- (public) transactions: all transactions details are public ( in Figure 9).

-

2.

-to- (shielding) transactions: address and its sending amount are public, address is encrypted ( in Figure 9).

-

3.

-to- (de-shielding) transactions: address and amount it receives are public, address is encrypted ( in Figure 9).

-

4.

-to- (private) transactions: the addresses, transaction amount, and the memo field are all encrypted and not publicly visible, i.e., (without an index) in the shielded pool of Figure 9.

-

5.

-to- (mixed) transactions: -addresses are involved, but there are public inputs or outputs in the transaction ( and in Figure 9).

A few design choices have made an impact on Zcash transactions. First, the Zcash protocol includes a consensus rule that coinbase rewards must be sent to a shielded address, and typically these coins are forwarded to -addresses very soon. Second, Zcash initially used a zero-knowledge scheme that supported at most two hidden inputs and two hidden outputs. As a result, including more than two input or output addresses required more cryptographic work, which was costly. A newer scheme called sapling does not have this limitation.

Both Monero and Zcash are much more costly than Bitcoin in terms of computational costs and resource usage. Monero transactions store ten decoys for each actual input, which considerably increases transaction size on disk, and Zcash transaction validation takes too much memory and time. As a result, online exchanges avoid storing balances of -addresses. However, Monero and Zcash both use UTXO models that we can analyze by graph analysis tools developed for Bitcoin.

3.5 Chainlets for UTXO Transaction Networks

Subgraph encoding on the Blockchain network is an alternative to address and transaction graph approaches.

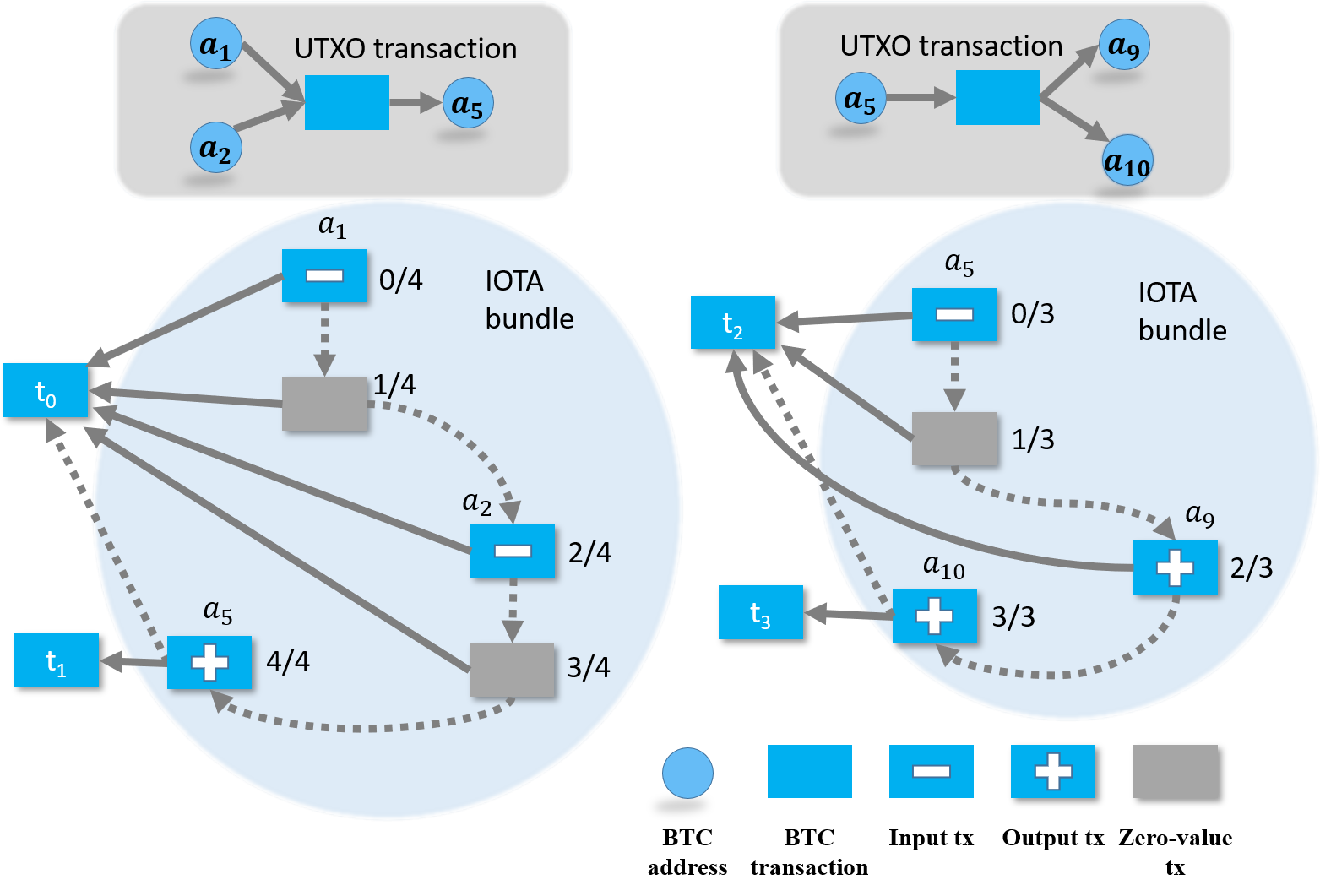

In traditional graphs, we consider nodes and edges the building blocks because nodes are created in time and may establish new edges at various time points. However, UTXo transactions create multiple edges at once. That is, we can think of a transaction itself as a building block of the network. With its nodes and edges, a transaction represents an immutable decision that is encoded as a substructure on the UTXO network. Rather than using individual edges or nodes, we can use this substructure as the building block in network analysis. If we consider multiple transactions and their connections through addresses, we may extend the substructure idea to blockchain subgraphs by considering multiple transactions. We use the term chainlet to refer to such subgraphs [13].

Consider a UTXO network with transaction and address nodes. The node set . An edge connects an address to a transaction (i.e., ) or a transaction to an address (i.e., ). This implies that there are no edges between two nodes of the same type.

A UTXO chainlet is a subgraph of , if and . If is a subgraph of and contains all edges such that , then is called an induced subgraph of .

Let -chainlet be a subgraph of with nodes of type “transaction”. If there exists an isomorphism between and , , we say that there exists an occurrence of in . A is called a blockchain -chainlet.

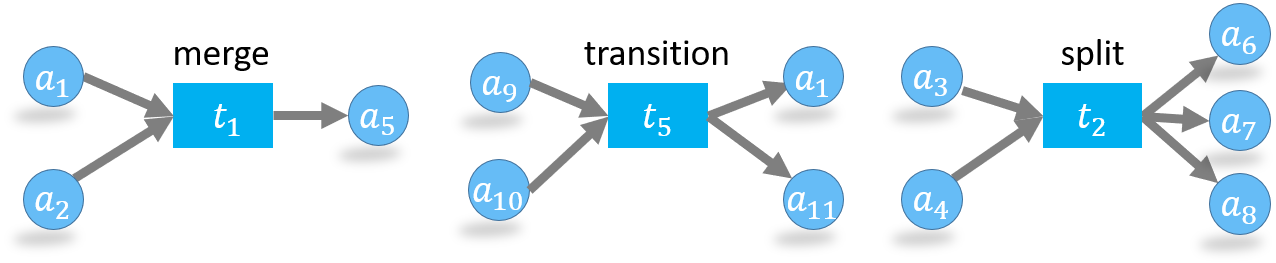

As a starting point, we can focus on the first order chainlet (), which consists of a single transaction node and the address nodes. The first order chainlet is, by definition, a substructure of the network. We denote a chainlet of inputs and outputs with . A natural classification of first-order chainlets can be made regarding the number of inputs and outputs since there is only one transaction involved. We can quickly identify three main types of first-order chainlets.

If the transaction merges input UTXOs, it will have a higher number of inputs than outputs. We call these merge chainlets, i.e., such that , which show an aggregation of coins into fewer addresses. Two other classes of chainlets are transition and split chainlets with and , respectively, as shown in Figure 10. We refer to these three chainlet types as the aggregate chainlets.

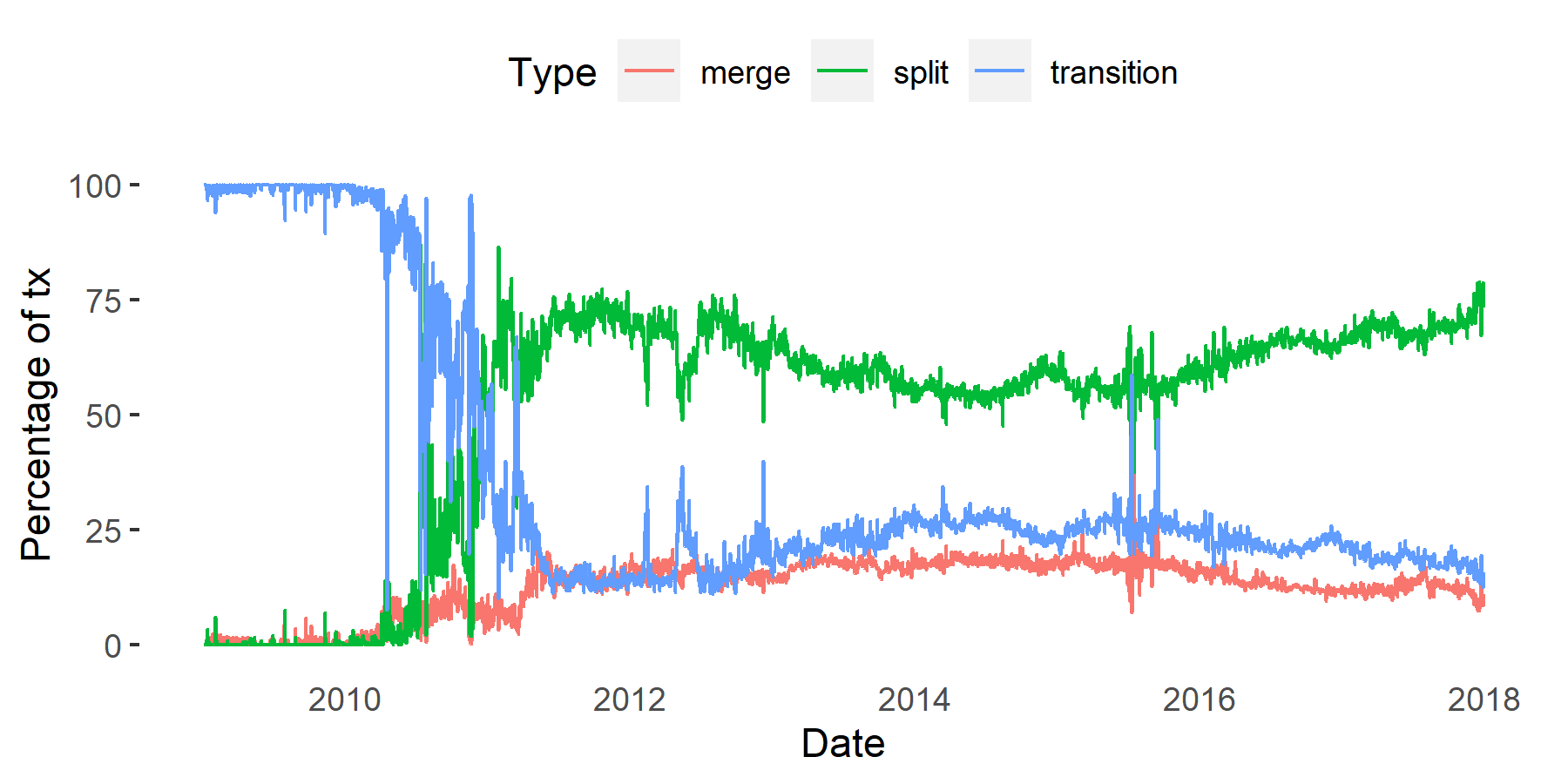

Figure 11 visualizes the percentage of aggregate Bitcoin chainlets in time. For example, the transition chainlets are those for . Figure 11 shows that the Bitcoin network, starting as an unknown project, stabilized only after summer 2011. From 2014 and on-wards, the split chainlets continued to rise steadily, compared to merge and transition chainlets. Spam attacks on the Bitcoin blockchain, which created too many transactions on the mempool to slow down transaction processing and force a block size increase, were visible around late 2015.

Extending this discussion, higher-order chainlets, as shown in Figure 12, can be classified in terms of their shapes.

3.6 Occurrence and Amount Information in Chainlets

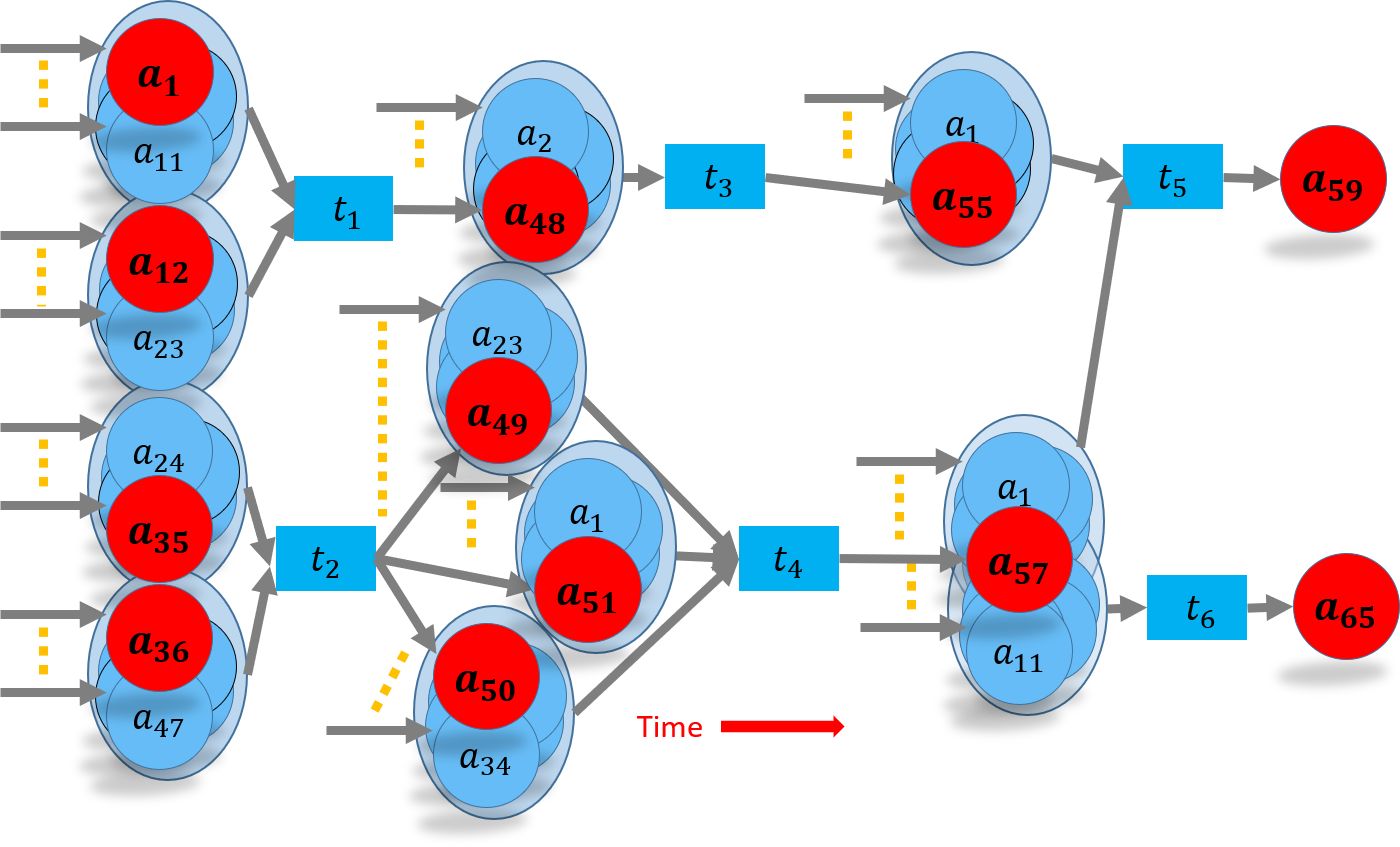

Chainlets provide two lenses to look at the transaction network; we can consider amounts or counts of chainlets.

For a given time granularity, such as one day, we can take snapshots of the blockchain network and extract chainlets from it. From the Blockchain network snapshot for a given granularity (e.g., daily), we mine two information for each chainlet type: amount to store volume of coin transfers by using the chainlet and occurrence to store instances (i.e., counts) of the chainlet.

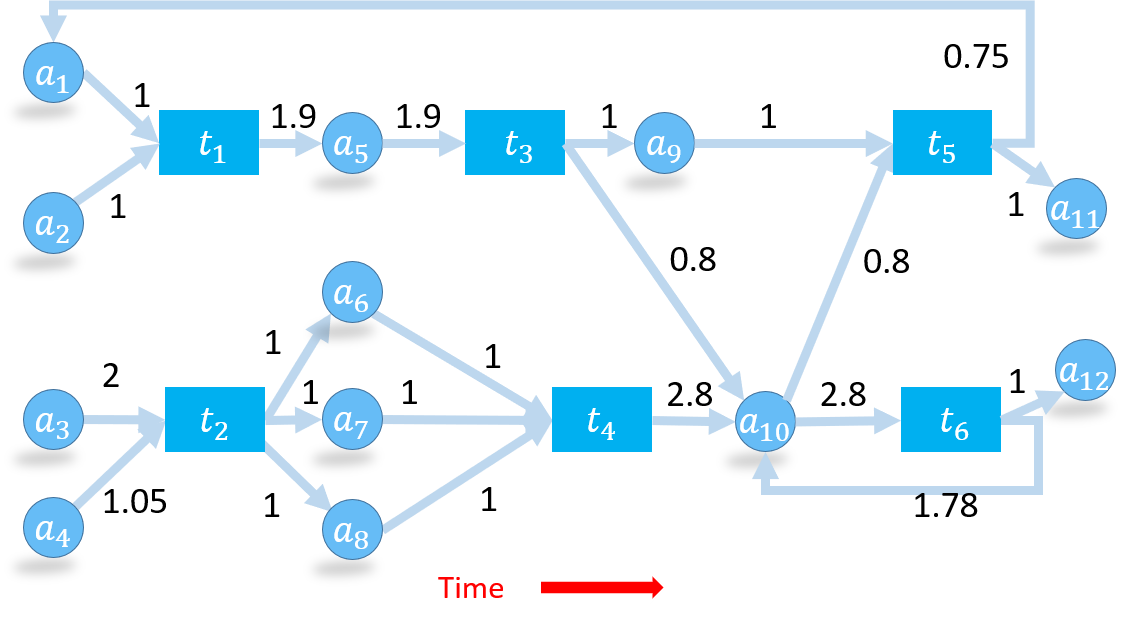

For example, Figure 13 contains six transactions and 12 addresses. However, if we look at the first order chainlets, we find five unique chainlets: Transaction creates a split chainlet . Transaction creates split chainlet . Transactions and create split chainlets . Transaction creates merge chainlet . Transaction creates transition chainlet .

From these chainlets, we can create two matrices to hold occurrence and amount information as

where and store the number and transferred amount of chainlets of the type , respectively, where and . For example, transactions and are stored in . The amounts output in these transactions are .

Remark 3.5.

A coinbase transaction has no input address but output addresses. If we plan to use the occurrence matrix to store coinbase transactions, we need to extend the matrix with as well. Coinbase transactions would then be stored in .

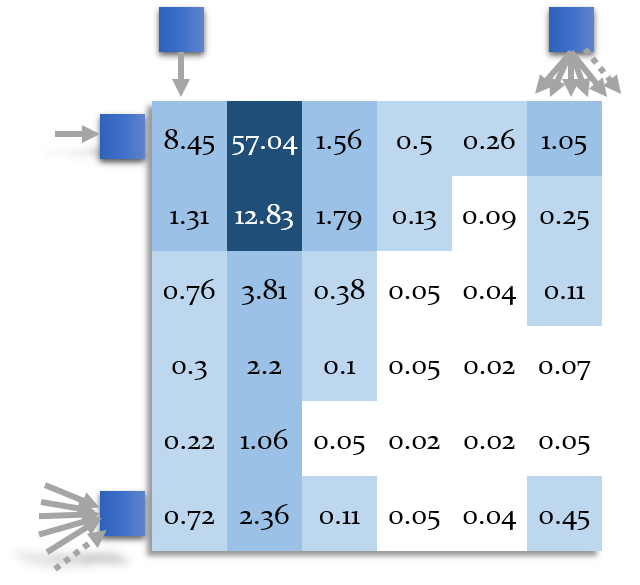

For the transaction network in Figure 13, suffices to store the matrices since transactions have at most three input addresses and three output addresses. However, in a real blockchain matrix, dimensions can easily reach thousands. UTXO blockchains restrict the number of input and output addresses in a transaction by limiting the block size (1MB in Bitcoin), but the number of inputs and outputs can still reach thousands. As a result, we can have large chainlets (e.g., , or ). Consider the case where we choose to create to store the occurrence and amount matrices with 1 million cells. Having so many cells is neither useful nor practical since most transaction types will not exist in the network. In turn, corresponding matrix cells in occurrence and amount would hold many zero values, implying that the matrices would be very sparse. As an alternative, we can choose a suitable value for matrix dimensions.

For the optimal matrix dimension , we have analyzed the history of Bitcoin and Litecoin. We have found that % 91.38 of Bitcoin and % 91.27 of Litecoin chainlets have of 5 (i.e., s.t., and ) in average for daily snapshots. This value reaches % 98.10 and % 96.14 for of 20, for the respective coins. We have selected of 20 since it can distinguish a sufficiently large number (i.e., 400) of chainlets and still offers a dense matrix.

The choice of requires a strategy to deal with transactions whose dimensions are bigger than . We record these chainlets in the last columns/rows of the matrices, which are defined as follows:

Definition 3.6.

Amount Matrix. We denote the total amount of coins transferred by a chainlet in a graph snapshot as . Amount of coins transferred by chainlets in the graph snapshot are stored as an -matrix such that for

Definition 3.7.

Occurrence Matrix. We denote the total number of chainlet in a graph snapshot as . Chainlet counts obtained from the graph snapshot are stored as an -matrix such that for

Example 3.8.

Consider the following example matrices

If we define for this example, ,, , and ,, , values must be stored inside the matrices. The updated matrices are

Extreme Chainlets: In occurrence and amount matrices, choosing an value, such as , means that a chainlet with more than 20 inputs/outputs (i.e., s.t., or ) is recorded in the -th row or column. That is, we aggregate chainlets with large dimensions that would otherwise fall outside matrix dimensions. We use the term extreme chainlets to refer to these aggregated chainlets on the -th row and column.

Extreme chainlets are large transactions that may involve more than 10 thousand addresses and are also large in coin amounts. We see two behavior in extreme chainlets. In the first case, chainlets are of the type ; less than 20 input addresses (usually one or two) sell coins to more than 20 addresses. An example is the Bitcoin transaction a79b970c17d97557357ec0661a2b9de44724440e1c635e1b603381c53ece725d in 2018. These extreme chainlets are split-chainlets which may indicate selling behavior.

In the second case, chainlets are of the type . This chainlet type is useful in finding large coin buys. Usually, an online exchange collects coins of many individual sellers and creates an extreme chainlet that has few (usually one or two) output addresses.

4 Ethereum: Account Networks

Account blockchains, such as Ethereum, do not use the UTXO data structure of Bitcoin. Unlike UTXO coin transactions involving as few as two or as many as thousands of addresses, coin transactions on account blockchains involve only two addresses: sender and receiver.

Many design choices behind account blockchains originate from the most popular account-based blockchain Ethereum. In this section, we will teach account networks by using Ethereum as our data source. However, the reader will find similar, if not the same, network and graph models in other account blockchains.

A major difference between UTXO and account blockchains is the type and variety of networks. UTXO networks are transaction and lightning networks, whereas, on account blockchains, we can observe the following networks:

-

1.

Coin transaction network. Similar to the UTXO transaction network, this network is created from the coin (ether) transfers between addresses. Network edges only carry the native currency (coin) of the blockchain.

-

2.

Token transaction networks. Asset trading networks that are created by internal smart contract transactions.

-

3.

Trace network. Interactions between all address types. The name trace implies that a transaction triggers a cascade of calls to smart contracts or externally owned addresses.

In this section, we discuss the three networks and their building blocks separately. We begin by first outlining network node and edge types.

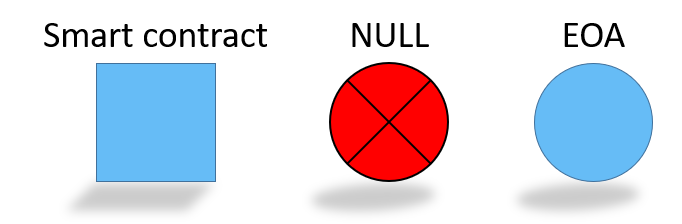

It is useful to re-consider the Ethereum address types. In account networks, we classify addresses into two node types and one special address.

-

1.

Externally owned address (EOA) has a private key. An EOA is managed by a real-life entity such as an investor or a centralized exchange. An entity may create and use multiple EOAs at the same time. Typically, an EOA is used over a long time in many transactions.

-

2.

Smart contract address does not have a private key. We can only distinguish Smart contract addresses by searching for smart contract code at the address.

-

3.

Null address 0x000.. node that has two use cases. First, a smart contract is created by using the NULL address as the receiver. Second, the NULL address is used to dispose of crypto assets. Any coin or asset sent to the address cannot be reclaimed and considered burned. The address may have a private key, but finding it by trial is considered impossible.

Figure 15 visualizes the three-node symbols that we will use to teach account networks.

4.1 Account Transaction Network

The account transaction network contains coin transfers between the three node types. The network edges always start from an EOA because a contract address or a NULL address cannot initiate a transaction. However, a smart contract can send coins to an EOA when a trace initiates the transfer (we will cover traces shortly). Specifically, transaction network edges are from i) EOA to EOA, ii) EOA to contract, iii) EOA to NULL address. iv) contract to EOA.

Network edges may have i) coin amount, ii) account nonce, iii) gas price, and iv) timestamp features.

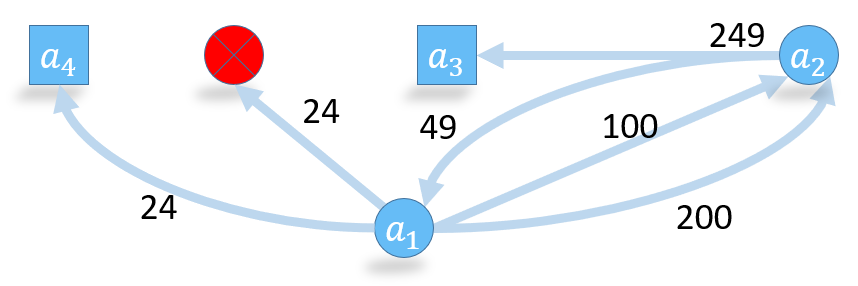

The coin amount in an edge is in subunits (Wei). Account nonce is a number that orders transactions initiated by an EOA. Miners must mine transactions of an address in nonce order. For example, in Table 2 creates four transactions with nonce values 0 to 3. A future transaction of with nonce 5 has to wait because the transaction of nonce 4 has not been mined. Nonce order ensures that the network cannot have out-of-order or missing edges. However, miners can mine multiple transactions from an EOA in the same block according to the nonce order.

Although we mention transaction time as an edge feature, transactions do not have timestamps themselves. The timestamp comes from the timestamp of the block that contains the transaction. Transactions of a block are ordered in the block by the miner, and online explorers record the order as the block index. However, even the miner cannot truly know when a transaction was created.

Another edge feature could be the used gas field of the transaction. However, the feature is not useful for the transaction network because the gas cost equals the base fee (currently 21000 gas) for coin transfers. The input data field of the transaction is empty for coin transfer transactions.

Figure 16 shows an example account transaction network. Table 2 gives the edge table of this network.

We easily model the account transaction network as a directed and weighted multigraph (i.e., multiple edges exist between node pairs). Although address creation is cheap, address reuse is not discouraged on Ethereum, and a node may appear in multiple blocks and send and receive coins for an extended period. Furthermore, smart contracts have permanent addresses. These factors help us track node behavior and network dynamics in time.

| block height | from | to | amount (wei) | nonce | block index | timestamp |

|---|---|---|---|---|---|---|

| 10646423 | 100 | 0 | 1 | Aug-12-2020 05:11:17 PM +UTC | ||

| 10646423 | 200 | 1 | 2 | Aug-12-2020 05:11:17 PM +UTC | ||

| 10646424 | 249 | 0 | 1 | Aug-12-2020 05:11:18 PM +UTC | ||

| 10646424 | 49 | 1 | 2 | Aug-12-2020 05:11:18 PM +UTC | ||

| 10646425 | NULL | 24 | 2 | 1 | Aug-12-2020 05:11:26 PM +UTC | |

| 10646426 | 24 | 3 | 1 | Aug-12-2020 05:11:43 PM +UTC |

4.2 Token Transaction Networks

A token is created by deploying a smart contract where the token’s features and business logic are defined. Any blockchain participant can create a token and facilitate its trade. The token’s contract defines meta attributes about the token, such as its symbol, total token supply, or decimals. Only the address of a token is unique in the blockchain; multiple tokens can have the same symbol, which creates confusion in trades.

Currently, there are more than a hundred thousand tokens on Ethereum [16]. We consider each token to have its network and set of traders.

A token’s current supply is the number of token instances created by the smart contract. If the instances are given unique ids, the token is considered non-fungible (as in the ERC 721 standard); each instance has its characteristics, owner, and price. Otherwise, one token instance will be equal to any other; the token is considered to be fungible (as in the ERC 20 standard). In this section, we will consider networks of fungible tokens, but we can easily extend our analysis to the non-fungible case.

A token transaction network has EOA, NULL, and smart contract addresses as nodes. We outline the following three types of transactions that a Data Scientist must know to analyze token networks.

-

•

The creation transaction that assigns an address for the token initializes its smart contract and state variables.

-

•

A trade transaction that moves some tokens between addresses.

-

•

A management transaction that can only be initiated by the smart contract creator (or any address that the owner specifies). The transaction may delete the contract or forward its balance (in ether or token) to another address. We will study management transactions in Section 4.3.

| token | block height | from | to | amount (Gwei) | tx fee (Gwei) | input data |

|---|---|---|---|---|---|---|

| Binance: BNB Token | 3978343 | 0x00c5…454 | 0xb8c7…d52 | 0 | 32643080 | […..] |

| ChainLink: LINK Token | 4281611 | 0xf550…780 | 0x5149…6ca | 0 | 21895728 | […..] |

| Tether USD | 4634748 | 0x3692…d57 | 0xdac1…ec7 | 0 | 12683176 | […..] |

Table 3 lists the creation transactions of three popular tokens on Ethereum. The from field lists the contract creator; this address is the owner of the token. Contract creation is expensive, and the transaction fee increases with more elaborate contracts. The contract code appears in the input data field of the transaction.

Remark 4.1.

Usually, the transaction that creates a smart contract carries no ether (as shown with 0 amounts in Table 3). The actual payload is the smart contract code written in the input data field of the transaction.

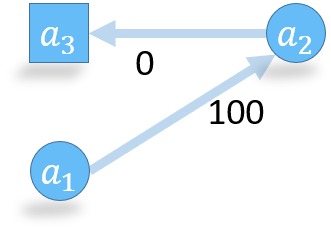

Token networks evolve with changing user balances that we denote as edges between addresses. However, token transfers are internal transactions which are not broadcast to the network in the form of an ordinary Ethereum transaction. In other words, what we call a token trade is, in reality, an update of balances in smart contract variables of the token. It is as simple as changing the values of two keys in a hashmap.

We will explain the observed transactions and states with the help of Figure 17. A token trade involves the following steps.

-

1.

Address owns tokens that are issued by . could have received tokens through various channels. For example, may have bought them in an earlier transaction, or the tokens might have been given to by the owner of .

-

2.

A price per token is agreed upon between or by any off-the-blockchain channel or through a clause in the contract (e.g., the contract sets token price as 50 Wei).

-

3.

pays an ether amount (100 Wei in Figure 17(a)) by creating a transaction, where is the receiver and the input data field of the transaction is blank. Here sends the transaction to the network to be mined.

-

4.

downloads the latest blocks and sees that 100 Weis have been sent to its address from . In turn, uses the conversion rate and decides to send 2 tokens to .

-

5.

creates a transaction where the receiver is , and the transferred ether amount is 0. However, the input data lists as the recipient of two tokens. Typically the input data is a call to the transfer function of the smart contract at with two parameters: to_address: and amount:. sends this transaction to the network to be mined.

-

6.

At every node of the Ethereum network, the Ethereum Virtual Machine executes the transaction of step 5. The smart contract at decreases the balance of by two tokens and increases the balance of by two tokens. This balance update, which is an internal transaction, is recorded as an edge from to in the token network of Figure 17(c), but not sent to the network as a transaction. This step fails if does not own two tokens.

-

7.

downloads and observes the transaction from to . The node at can run the transaction in its local Ethereum Virtual Machine to ensure that tokens are transferred without any error.

As Figure 17 shows, transaction and token networks have different views from the two mined transactions. Without running a virtual machine and executing the transactions, we cannot observe the internal transactions nor create the token transaction network.

Token networks attract trades and traders every day. As Ethereum addresses (both EOA and contract) are reused in multiple days, a token network may see the same node trading in multiple days. However, daily token networks are sparse and consist of disconnected components, and very few traders appear in a token’s network every day.

Some traders appear in networks of multiple tokens, making token networks an ideal setting for studying multi-layer networks. Each token network constitutes a layer with edges and nodes, and nodes overlap between layers.

4.3 Trace Network

Ethereum stores an ecosystem of addresses, smart contracts, and decentralized organizations. In transaction and token networks, we studied financial relationships between addresses. This section now shifts our focus to relationships, call-dependencies, inheritances, and other interactions between Ethereum addresses. A trace network stores these relationships where nodes are EOA and smart contract addresses, and edges are interactions between EOA-contract, contract-EOA, and contract-contract pairs.

An EOA creates a transaction that is directed to the address of a smart contract. The smart contract can execute a function and terminate or call functions of other smart contracts. The contract can also move coins to EOAs. The trace can be extended until the transaction gas limit is exhausted. All the addresses that are involved in this call/interaction chain create a trace. In graph terms, a trace is a hyper-edge (i.e., an edge that connects more than two nodes).

A trace can involve every operation that a smart contract can execute. For example, a trace can create a smart contract, call a smart contract function, or delete a smart contract. As such, we can label parts of the trace with the executed operation.

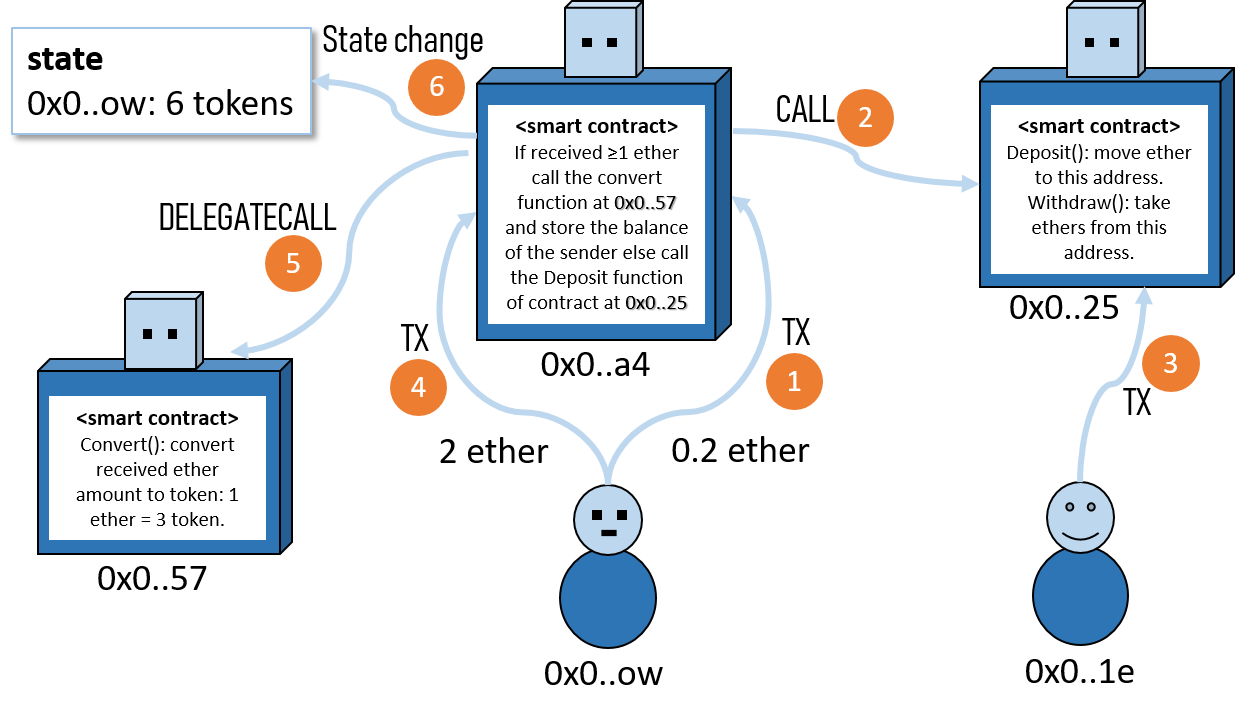

Example 4.2.

We construct a trace network from a toy scenario given in Figure 18. We show addresses with their first and last characters (e.g., 0x0..57). Figure 18 contains three smart contracts (0x0..57, 0x0..a4 and 0x0..25) and two externally owned accounts (0x0..ow and 0x0..1e). Edges denote transactions or message calls. Transactions are created by externally owned accounts explicitly and mined in blocks, whereas message calls are not.

In this example, a contract acts as a salesman for a cryptoasset: 0x0..a4 receives ethers from addresses, and stores their amount of token in its storage. The contract has a rule that the minimum deposit amount is 1 ether. 0x0..ow is not aware of this rule at first and creates a transaction that sends 0.2 ethers to 0x0..a4, which calls a deposit function at 0x0..25 that seizes the amount and stores it in the address. 0x0..1e can observe in the blockchain as a transaction, but is a message call that requires 0x0..1e to execute the contract call to discover.

Usually contracts have withdraw functions that allow the contract creator to remove the deposited ethers from the contract. In 0x0..1e makes a contract call transaction to withdraw these ethers.

0x0..ow learns about the minimum amount rule, and sees that its 0.2 ethers are forfeited. 0x0..ow makes yet another attempt to buy tokens by sending 2 ethers again in transaction . This time, 0x0..a4 accepts the amount, and DELEGATECALLS a conversion function from 0x0..57. which directly stores a state variable that records account 0x0..57 has 6 tokens (three for each ether).

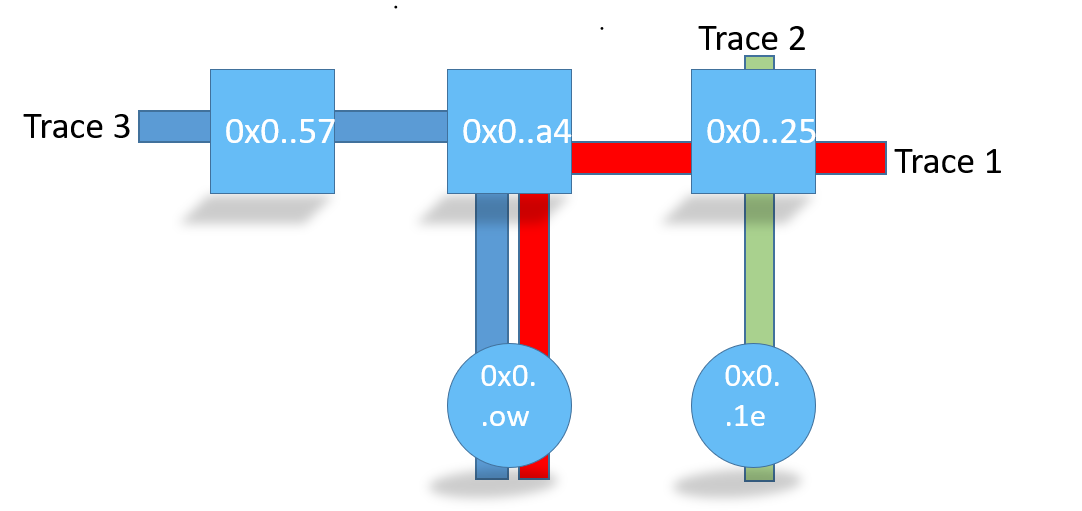

So far, three transactions ( , and ) have been initiated by EOAs and mined in blocks. We observe the following three traces from the three transactions:

-

1.

Trace 1: 0x0..ow 0x0..a4 0x0..25

-

2.

Trace 2: 0x0..1e 0x0..25

-

3.

Trace 3: 0x0..ow 0x0..25 0x0..57

Note that creates a state change (an internal transaction) but it is not recorded in the trace network.

Placing all these traces (hyper-edges) together, we obtain the hypergraph shown in Figure 19.

Remark 4.3.

The Ethereum virtual machine executes every transaction in order and executes calls accordingly. There is no concurrency in Ethereum transaction execution; EVM does not make two calls simultaneously. When a contract calls two contracts sequentially, EVM will make the second call only after the first contract call (and any further contract calls it makes) ends.

In theory, traces can reach large sizes in the shape of trees with many branches. However, the transaction fee grows with additional calls and prevents the creation of huge traces. Note that even when a transaction sets a high gas limit to pay a big transaction fee, the transaction will not be mined if the gas used exceeds the Ethereum block gas limit (currently 12.5K). If a trace creates a call loop, this may deplete smart contract balances before the transaction gas limit is reached.

We can understand smart contract behavior by trace network analysis. For example, we can study the network to discover unexpected call branches in smart contracts.

5 Ripple: Credit Networks

Ripple (www.ripple.com) and Stellar (www.stellar.org) are two credit networks that closely resemble the ancient Hawala system (in Arabic, hawala means to transfer or trust). The main idea of Hawala is to allow a money sender to use connections of people who trust each other to make a payment in a distant geographical location. Merchants have historically used these types of networks to transfer money between countries [17].

We model credit networks as directed, weighted graphs that we build from trust lines between address pairs. A trust line is a directed edge between two addresses, which implies that the source address trusts the target address. We can add weight (i.e., money amount) to the edge to show the limits of that trust. In a credit network built from trust lines, a directed edge is a promise by the source node that it will let the target node use a loan amount in a future transaction. Trust lines can be deleted or updated for amounts in time.

It is helpful to explain a few confusion points in Ripple to a blockchain researcher. Ripple uses the term ledger instead of a block. Transactions have multiple types and may involve financial constructs (e.g., checks), user-issued currencies (e.g., USD), and path-based settlements. The reader should remember that Ripple contains elaborate business logic in its building blocks (e.g., transactions). Before we delve into Ripple, we will use a few scenarios to explain how we can use a network of trust lines to make a payment.

Remark 5.1.

Academic articles have conflicting views on how to represent a trust line as a directed graph edge. Here, we follow the notation used in the official Ripple documentation, i.e., the edge is from the lender (source) to the borrower (target). The lender trusts the borrower.

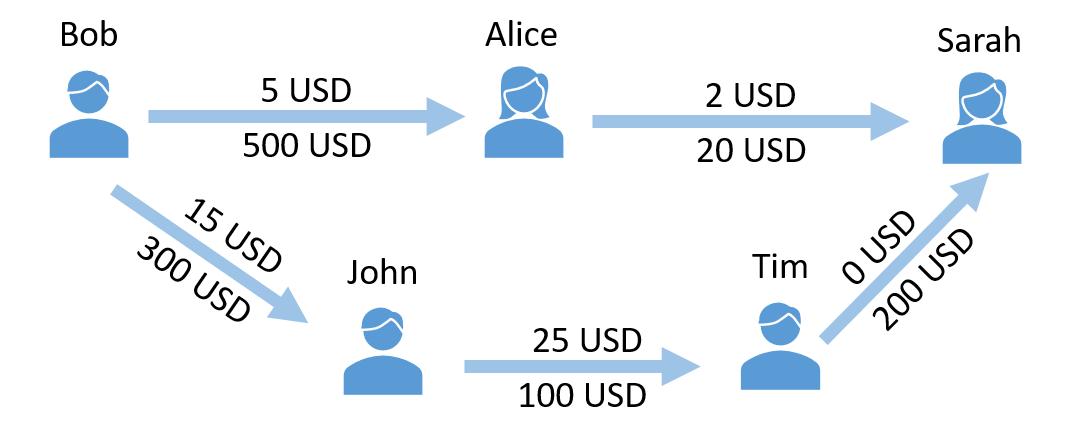

Figure 20 shows two trust lines between Alice, Charlie, and Bob. Each edge has two edge features. First, a value below the edge (500 USD for both edges) is the maximum credit amount (known as the limit) that Charlie and Bob trust with Alice that Alice can use in future transactions. Second, a value above the edge (5 and 15 USD) is the balance amount that Alice has already used with Charlie and Bob. For example, Alice can use 485 in a future transaction by using the trust line from Bob.

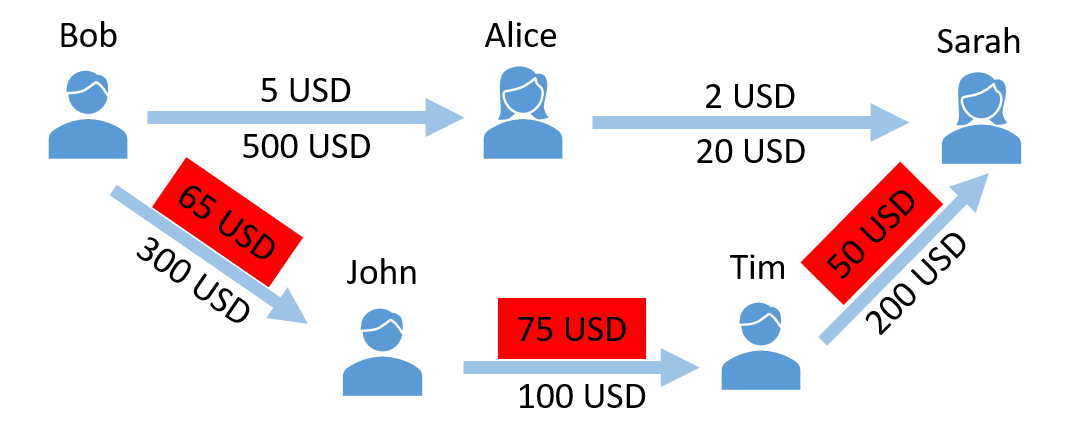

Users may create the Ripple trust line due to two reasons. First, Alice may have paid 500 USD to Charlie and Bob each in an off-the-Ripple transaction. Second, Charlie and Bob may have trusted Alice based on her reputation and created trust lines for her to use. In practice, the amounts are almost always due to the first reason, i.e., offline deposits. By default, Ripple limits are lower-bounded by 0 and upper-bounded by . A high limit creates credit risks for the lender. We make a Ripple trust graph from such trust lines. We can delete an existing trust line by setting its trust limit to zero. We can use trust lines to make payments to third addresses over a path that traverses individual trust lines in the same currency, such as USD. Traveling trust lines is known as rippling. Figure 21 will help the reader learn basic rippling across trust lines.

5.1 Ripple Networks

On cryptocurrencies, a single type of coin, such as bitcoin, is traded between addresses. Similarly, Ripple has its currency called XRP with a drop sub-unit (1 XRP = 1 million drops). However, Ripple also allows users to issue currencies and create trust lines in the issued currencies.

Ripple officially recognizes two main currency types: i) Ripple (abbreviated as XRP) and ii) user-issued currencies. Academic articles further divide user-issued currencies into country currencies (e.g., US dollar, European Euro, Japanese Yen), cryptocurrencies (e.g., Bitcoin), and fictional currencies such as tokens. For example, in Figure 20, USD amount is a user-issued currency. User-issued digital tokens are fictional currencies with no outside backing. Traders must be aware that such tokens have no inherent value.

XRP is issued natively and has no issuer. All other currencies are represented as “currency.issuer” in transactions. We represent a currency with i) three characters such as USD, EUR, or ii) less frequently by a 40 character string. USD issued by address1 is USD.address1 on the Ripple ledger (also called the XRP Ledger). Multiple issuers can issue a currency: USD.address1 and USD.address2 are considered two different currencies, even though they are both USD currencies. However, in rippling user issued currencies of the same denomination (e.g., USD) are considered to be the same currency. Trust in the issuer determines the fungibility of a user-issued currency. If Alice does not trust address1 but trusts address2, 1 USD.address1 will not be worth 1 USD.address2 for Alice. Accordingly, Alice may refuse to participate in rippling transactions that bring her USD.addres2 amounts.

Each Ripple address needs to store a non-trivial XRP amount as a reserve that it cannot spend; otherwise, Ripple considers the address deleted. The reserve requirement (currently 20 XRP) discourages multiple address creation and usage. If a security breach occurs, a user may change its address; however, best practice reuses the same address for multiple transactions.

Info 1

A currency issuer may set a transfer fee for every transaction in that currency between other addresses. The fee is similar to earning a commission for every transaction in the currency. The issuer of a popular currency thus accumulates transfer fees, which reduces the amount of offline liability it must hold to exist as an entity in the Ripple network.

The issuer can also freeze all transactions of its currency (XRP cannot be frozen by anyone). However, holders of the currency can still redeem the currency by returning it to the issuer and getting paid outside of the XRP Ledger. However, in real life, the issuer may have already gone bankrupt or may ignore redeeming requests. Every address on the ledger must make its own trust decisions by considering these issues and create/allow trust lines accordingly.

We outline Ripple Ledger address types in Figure 22 as a gateway, cold wallet (issuing address), hot wallet (operational addresses), market maker, and wallets (i.e., ordinary traders). Gateways are the currency issuers of the Ripple network and link the XRP Ledger to the rest of the world. All network nodes can buy Ripple or any other issued currency by paying money (e.g., US dollars) to the gateway (outside the Ripple ledger). The following steps, taken verbatim from the Ripple documentation, explain the six necessary steps.

-

1.

A customer sends money to a gateway’s offline accounts. This could be fiat money, Bitcoin, or any other asset not native to the XRP Ledger.

-

2.

The gateway takes custody of the money and records it.

-

3.

The gateway issues a balance in the XRP Ledger, denominated in the same currency, to an address belonging to the customer. This is done by creating a trust line to the customer’s Ripple address.

-

4.

The customer uses the issued currency in the XRP Ledger, such as by sending cross-currency payments or trading in the decentralized exchange.

-

5.

A customer (not necessarily the one who deposited the money initially) sends the issued currency to the gateway’s XRP Ledger address.

-

6.

The gateway confirms the customer’s identity who sent the balance in the XRP Ledger funds and gives the corresponding amount of money outside the XRP Ledger to that customer.

An institution may use both cold and hot wallets on the XRP ledger. Connected to the Internet, a hot wallet signs ordinary transactions, and the cold wallet stores currencies offline and is used less frequently.

A market maker is an address that converts a currency to another and takes a conversion fee through its offer, which is broadcast to the ledger in an offer create transaction. The offer may immediately consume earlier offers and gain the market maker what currency it desires. If the offer is not fully consumed, it is stored in the ledger as an offer object that can be used in future payments or consumed by future offers (of other addresses). Offers must be updated in real-time as currency conversion rates change (for country currencies, the conversion rate must be updated according to international exchange rates). A standing exchange offer is canceled in an offer cancel transaction.

We will teach Ripple networks in two subsections: Ripple trust graph and Ripple payment graph. The trust graph stores trust lines and balances. The payment graph utilizes the trust graph to process transactions.

5.2 Ripple trust graph

We create the Ripple trust graph from trust lines issued by addresses. In our basic examples of Figures 20 and 21, trust lines were not reciprocal. However, in Ripple, both addresses can create a trust line to each other in a currency. Furthermore, two addresses can have trust lines in multiple currencies.

Ripple creates a single RippleState object to connect two accounts per currency, sorts the account addresses numerically, and labels the numerically lower address as low account and the other as the high account. Assume that Alice and Bob have trust lines in USD and EUR amounts. Ripple creates two RippleState objects for Alice and Bob; one for EUR and one for USD.

The object has high and low limit fields to record the limit from high low and low high trust lines. However, the net balance is a single value shared by the addresses, and Ripple stores the net balance of the trust line from the low account’s perspective.

Remark 5.2.

So far, we have used trust lines between Ripple users (e.g., John Sarah) in our payment scenarios. However, ordinary users do not issue currencies on Ripple, which means that actual trust lines connect currency issuer-user pairs (gateway Sarah).

We can check the currency issuer in a RippleState with balance. If the balance is positive, the high account is the issuer. If the balance is negative, the low account is the issuer. Often, the issuer has its limit set to 0, and the other account has a positive limit, but this is not reliable because limits can be increased or decreased without affecting an existing balance.

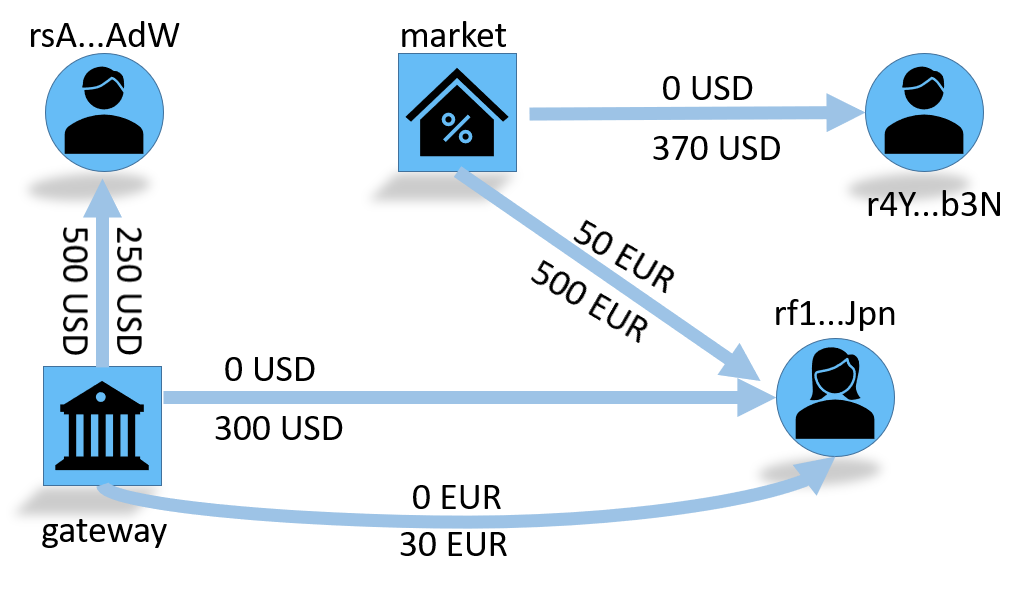

The Ripple trust graph is a directed, weighted multi-graph where an edge has four features: currency name (i.e., type of the edge), balance, low limit, and high limit. Multiple currency edges can connect node pairs. For example, in Figure 23 the gateway and rf1…Jpn have trust lines in USD and EUR currencies. We give the graph data of this figure in Table 4 where we have not excluded 0 high limits.

| low | high | currency | balance | low limit | high limit |

|---|---|---|---|---|---|

| gateway | rSA…Adw | USD | 250 | 500 | 0 |

| gateway | rf1…Jpn | USD | 0 | 300 | 0 |

| gateway | rf1…Jpn | EUR | 0 | 30 | 0 |

| market | rf1…Jpn | EUR | 50 | 500 | 0 |

| market | r4Y…b3n | USD | 0 | 370 | 0 |

A trust line deactivates in three cases. First, the lender may remove the trust line by updating trust parameters in a TrustSet transaction. Second, the lender may freeze the trust line temporarily. Third, the currency issuer can freeze all transactions of the currency (except for the redeeming transaction). In two cases, a node may hold a balance on a trust line greater than the limit, that is, when the node acquires more of that currency through trading and when the node decreases the limit on the trust line. The average node degree is less than four in the trust graph, and the clustering coefficient is around 0.10.

5.3 Ripple payment graph

The Ripple trust graph shares edge features with the Ripple payment graph. Additionally, the payment graph stores a node feature called reserve (i.e., XRP balance of the node). We cannot use the reserve amount in transactions. In addition to the base reserve, the reserve amount increases for every object (such as a trust line) that we create. The reserve increase applies only to the node extending trust, not to the node receiving it.

We create the Ripple payment graph from 1) direct payments, 2) path-based settlements, and 3) a few other financial constructs. We will teach these payment types before giving a graph model for the payment graph.

5.3.1 Direct payments

A direct payment is an XRP transfer between two Ripple addresses and does not require a trust line. Regardless of what trust lines exist in the trust graph, two ripple addresses can send to and receive XRP from each other.

The XRP balance of an address must not fall below the total required reserve. Otherwise, the address is not allowed to create some types of transactions. When an address’s XRP balance falls below the reserve, the address may issue OfferCreate transactions to buy more XRP or other currencies on its existing trust lines. However, these transactions cannot create credit that we can use to buy XRP to satisfy the reserve requirement (i.e., when the account balance the required reserve). For example, the address may pay a transaction fee and create an offer for XRP on the ledger. Once a buyer consumes the offer, the address will receive its XRP payment and satisfy the reserve requirement.

When an address is below the reserve requirement, it can send new OfferCreate transactions to acquire more XRP or other currencies on its existing trust lines. These transactions cannot create new trust lines, nor Offer objects in the ledger, so they can only execute trades that consume existing Offers.

5.3.2 Path-based settlements

A path-based settlement transaction connects a source and a destination node pair via a network path through rippling. For example, in Figure 23 the node rsA…AdW can make a payment to rf1…Jpn through the gateway. We can make a payment by consuming exchange offers along the path. For example, if the sender wants to make a payment in USD, the path can use trust lines that follow USDEURUSD, where the arrow indicates a currency exchange. Traversing exchanges is called bridging. If the transaction offers a better cost, currencyXRP and XRPcurrency conversions can automatically be executed on the path as well. This is called auto-bridging.

A path-based settlement can explicitly write one or more paths (called a pathset) in a payment transaction. All paths in a pathset must start and end with the same currency, and the sender can also leave path selection to Ripple.

Pathfinding is difficult because user XRP balances and trust lines change every few seconds as new ledgers (i.e., blocks of transactions) are validated. As a result, Ripple is not designed to compute the absolute best path. The simplest possible path to connect the steps of the transaction is called the default path. In addition to the paths written in the transaction, Ripple can choose to use the default path. The sender must set the tfNoDirectRipple flag to avoid the default path and force Ripple to use the paths of the pathset.

In a path-based settlement, we can set a few fields of the transaction to restrict path selection. These are the Account (sender), Destination (receiver), Amount (currency and amount to be delivered), and SendMax (currency and amount to be sent, if specified) variables of the transaction. The variables shape the path in these ways:

-

•

The Account (sender) is set to be the first step of the path.

-

•

If the SendMax variable is set to be a currency issuer, the issuer must be the second step of the path.

-

•

If the Amount variable is set to be a currency issuer, the issuer must be the second-to-last step of the path.

-

•

The path ends at the Destination address.

The actual cost of a path-based payment can change between submission and execution of a transaction based on updated information (e.g., the limit of a trust line) from transactions.

A path-based payment can fail for multiple reasons; first, the receiving address may not have the reserve XRP amount. Ripple checks whether the payment would deliver enough XRP to meet the reserve requirement in such a case. If not, the payment fails. Next, the receiving address may have limitations on receiving payments, such as Deposit Authorization or RequireDest (We will cover these constructs shortly). 333Currency issuers set such rules. Third, the paths that the sender specifies may have dried up (i.e., trust line limits are exceeded).