Supplement to the paper

Cluster based inference for extremes of time series

Holger Dreeslabel=e1]drees@math.uni-hamburg.de

[Anja Janßenlabel=e2]anja.janssen@ovgu.de

[Sebastian Neblunglabel=e3

[mark]sebastian.neblung@uni-hamburg.de

University of Hamburg, Department of Mathematics,

SPST, Bundesstr. 55, 20146 Hamburg, Germany,

Otto-von-Guericke University of Magdeburg, Faculty of Mathematics, IMST,

Universitätsplatz 2, 39106 Magdeburg, Germany,

Abstract

We continue the simulation study from section 3 of the main paper and provide additional simulation results in another model. Furthermore, we specify the variance example at the end of Section 2 by giving the concrete variance formulas. We verify three conditions of Theorem 2.3 for solutions to stochastic recurrence equations. Moreover, we state a modified version of the sliding block limit theorem from Drees and Neblung (2021) which is used for the proof of Theorem 2.3 of the main paper. Finally, we provide the proofs for equation (2.1), equation (A.4), Remark 2.2, Lemma A.2, Lemma A.9 (ii), Lemma A.10 and Lemma A.12 of the main paper.

62G32,

62M10, 62G05, 60F17,

cluster of extremes, empirical processes, extreme value analysis, time series, uniform central limit theorems,

keywords:

[class=AMS]

keywords:

\cbcolor

black

,

,

To avoid confusion, we continue the section and figure numbering from the main article.

4 Further simulations.

In this section, we present additional simulation results about the finite sample performance of the projection based estimator and its competitors and of the cdf of . We keep the Monte Carlo setting (sample size, threshold, block length, number of Monte Carlo simulations) used in the paper.

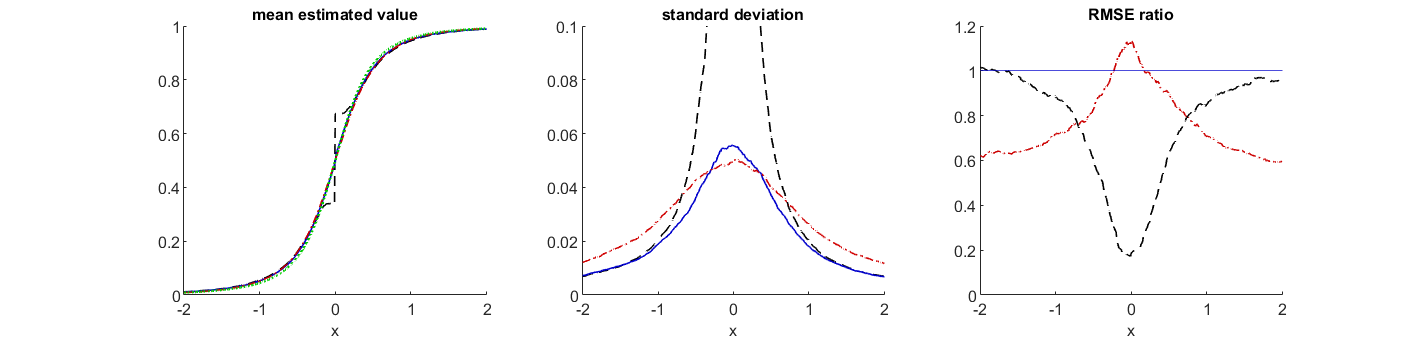

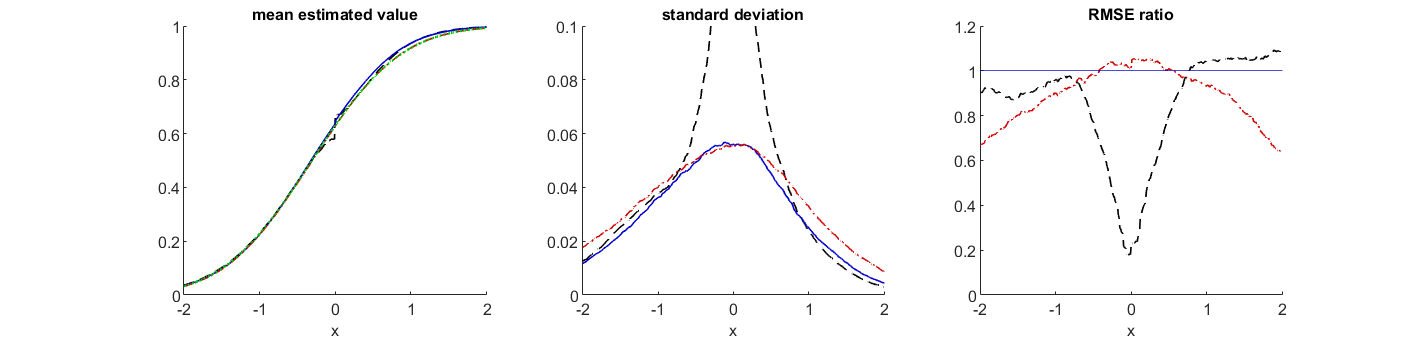

In Section 3, among other things, the estimators are discussed in the GARCHt model for lag , where performs best. Figure 3 shows the corresponding results for smaller lags, namely and , respectively. Because and have point mass at , typically has smallest bias among all estimators for small , which is also reflected in the RMSE.

In contrast, has smallest variance for most values of and this effect becomes more pronounced as the lag increases.

Consequently, the projection based estimator outperforms the backward estimator, in particular as increases, and it has smallest RMSE for and all lags under consideration.

Figure 3: Mean (left), standard deviation (middle) and relative efficiency w.r.t. (right), of (blue solid line), (black dashed line) and (red dashed-dotted line) in the

GARCHt model for lags (top) and (bottom); the true cdf is indicated by the green dotted line.

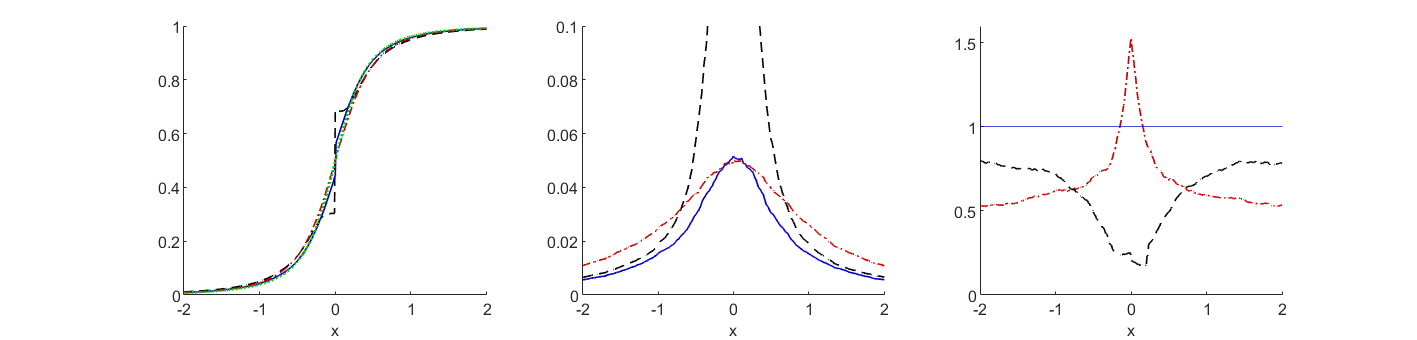

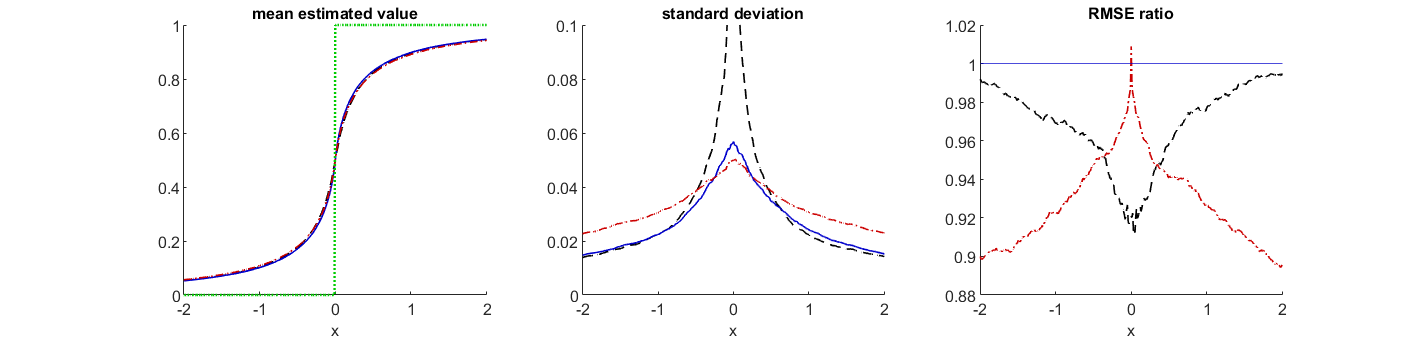

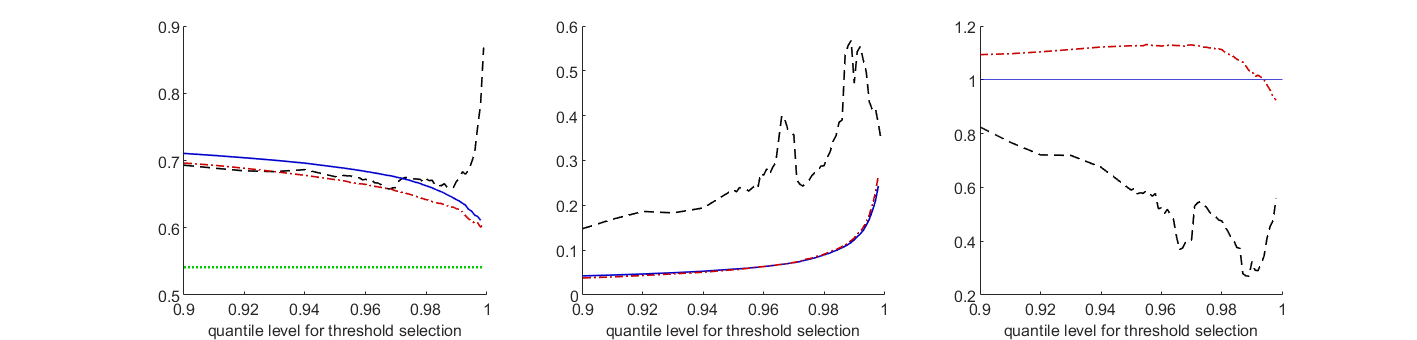

While in the (asymmetric) SRE model (see Figure 2 in the paper for lag 1 and Figure 4 for lags ) the variances of the three estimators behave similarly, the large bias, which is due to the influence of , often dominates the RMSE, leading to an underperformance of . This is particularly true for larger lags and negative , while for and lag 10, has minimal RMSE.

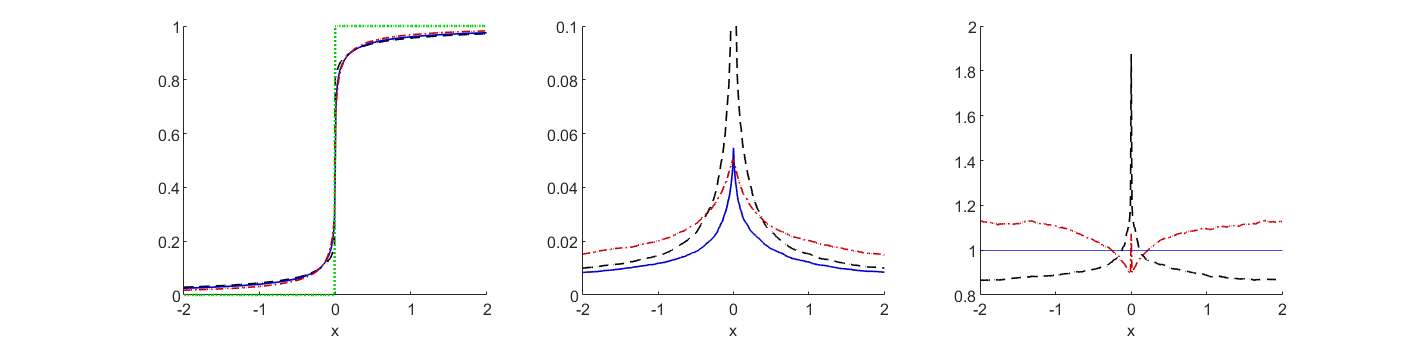

Note that here the difference between the conditional distribution of the exceedances over the threshold and its limit distribution obscures almost all real differences between the estimators. It is thus instructive to compare, in addition, the performance of , and interpreted as estimators of the pre-asymptotic cdf (rather than its limit ), like it was done in Davis et al. (2018) for the backward estimator. The corresponding plots for lag are shown in Figure 5. Of course, in the left plot only the true cdf has changed and the middle plot is exactly the same as in the bottom line of Figure 2, but the RMSE of the projection based estimator is much more strongly reduced than that of the forward estimators for not too close to 0. So, in this setting, overall performs best as an estimator of the pre-asymptotic cdf.

Figure 4: Mean (left), standard deviation (middle) and relative efficiency w.r.t. (right), of (blue solid line), (black dashed line) and (red dashed-dotted line) in the

SRE model for lags (top) and (bottom); the true cdf is indicated by the green dotted line.Figure 5: Mean (left), standard deviation (middle) and relative efficiency w.r.t. (right), of (blue solid line), (black dashed line) and (red dashed-dotted line) as estimators of the pre-asymptotic cdf of given in the

SRE model for lag ; the true cdf is indicated by the green dotted line.

In addition to the GARCHt and the SRE model, here we examine a model with trivial tail process:

•

SV: Consider the stationary stochastic volatility model with where are i.i.d. standard normal random variables and are i.i.d. with Student’s -distribution, independent of . Then is a stationary regularly varying time series with (cf. Davis et al. (2018), Section 4). Since the extremal behavior of is dominated by the i.i.d. heavy-tailed innovations , we have for all , see Davis and Mikosch (2009).

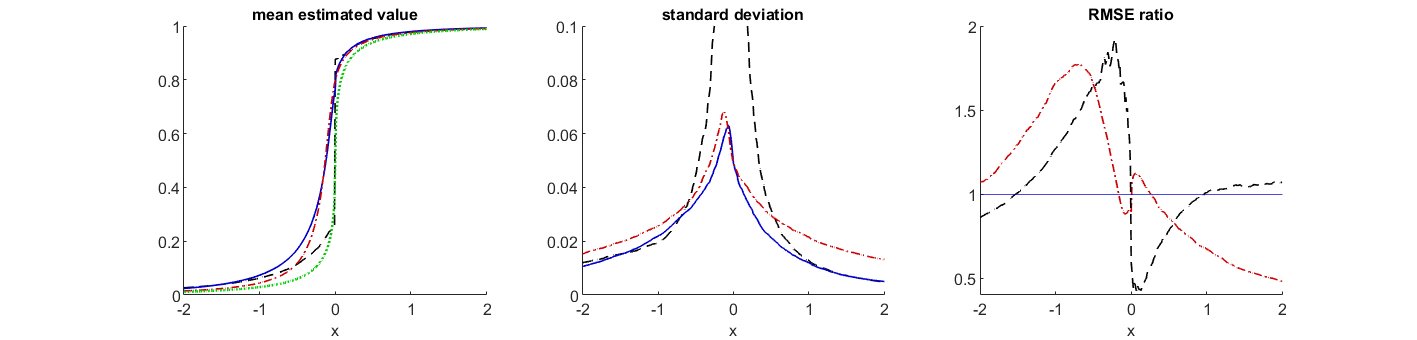

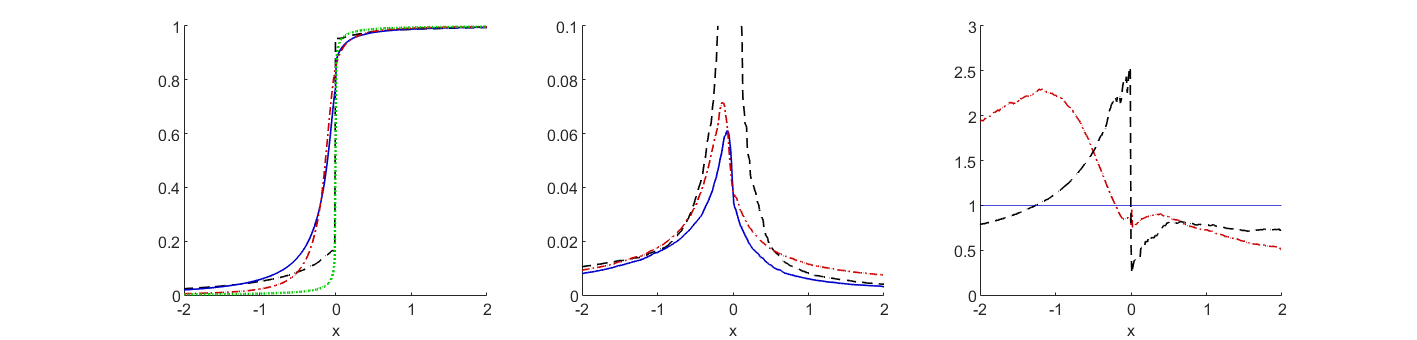

Note that the conditions of Section 2 can only be fulfilled for the family of sets if a neighborhood of 0 is omitted from the range of -values. Nevertheless, here we present the results for the full range (and lags ) in Figure 6.

For lag , the projection based estimator performs best, but the loss of efficiency of the other estimators is less than 10%.

In contrast, for , the has usually a moderately smaller RMSE than , which in turn is preferable to outside a tiny neighborhood of the origin.

Figure 6: Mean (left), standard deviation (middle) and relative efficiency w.r.t. (right), of (blue solid line), (black dashed line) and (red dashed-dotted line) in the

SV model for lags (top) and (bottom); the true cdf is indicated by the green dotted line.

To sum up, usually the projection based estimator has the smallest variance, especially for larger lags. If pre-asymptotic probabilities significantly differ from the corresponding limit probabilities, may have a larger bias and RMSE than the forward estimator and sometimes also than the backward estimator. Overall, though, shows a more robust performance than both these estimators.

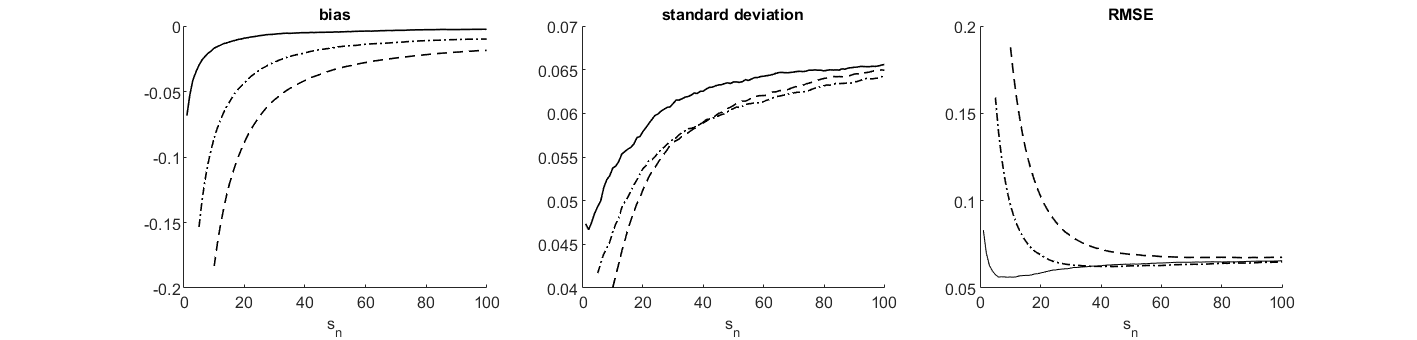

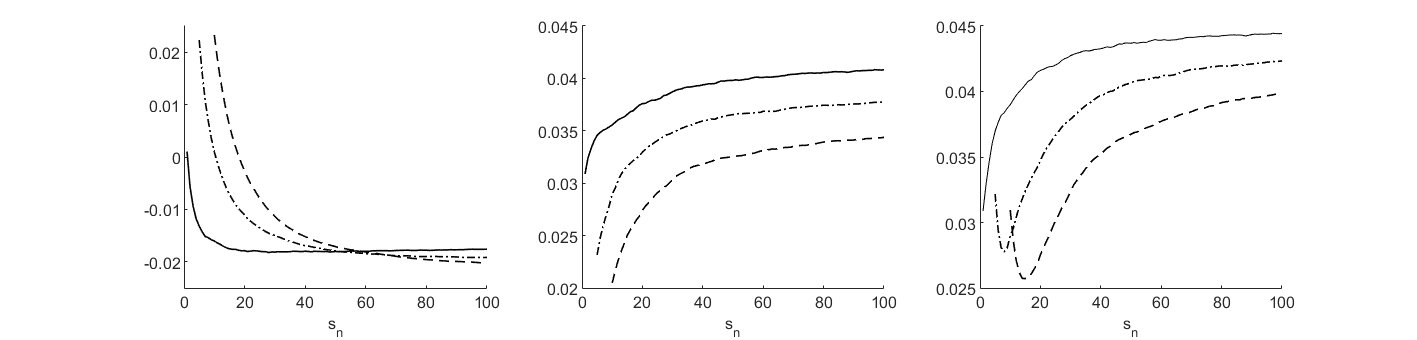

Figure 7: Bias (left), standard deviation (middle) and RMSE (right) of versus , for lag (solid line), lag (dashed-dotted line) and lag (dashed line) with (top) and (bottom) in the

GARCHt model.

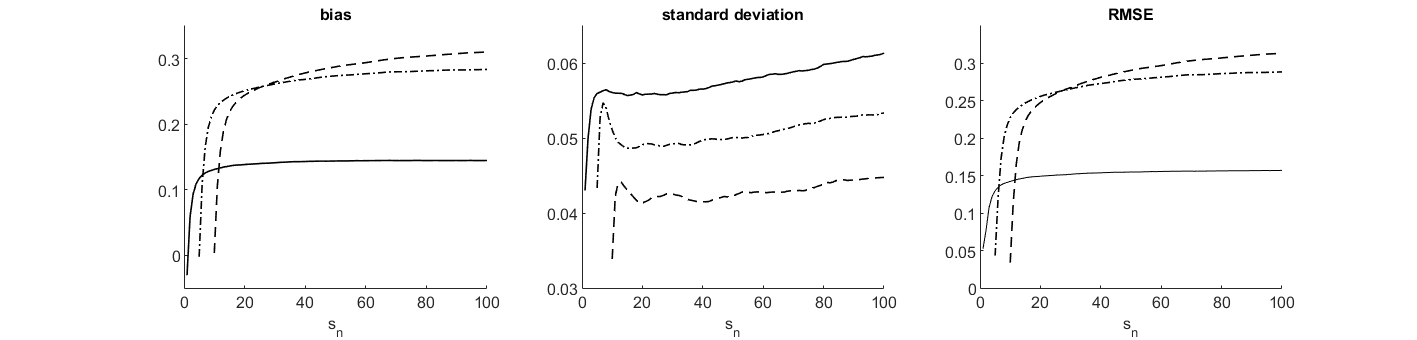

Figure 8: Bias (left), standard deviation (middle) and RMSE (right) of versus , for lag (solid line), lag (dashed-dotted line) and lag (dashed line) with (top) and (bottom) in the

SRE model.

Recall that in the definition of the projection based estimator one has to choose which determines the length of the blocks. Next, we examine the sensitivity of the estimators to changes of the block length.

If blocks are chosen too small than they do not capture the dependence structure of a typical cluster of extremes. Moreover, a point mass at 0 is introduced as an artefact of the artificial clipping of the cluster. On the other hand, if the block length is chosen too large, then almost independent clusters of large observations are compounded, which may lead to a bias and increase the variance, too.

Figure 7 shows the bias, the standard deviation and the RMSE of as function of for the lags and for the GARCHt model and Figure 8 does the same for the SRE model. For the GARCHt model, especially for larger lags, the estimator is clearly biased if is chosen too small (see top left plot in Figure 7), but for the bias is small and the RMSE is quite stable. In the SRE model, in most cases the bias is caused by the deviation of the pre-asymptotic cdf from the limit cdf, discussed above. This negative bias happens to (partly) cancel a positive bias caused by too short a block out if is chosen small, leading to a very small RMSE. Apart from this very specific effect, the RMSE is again rather stable if is not too small. We thus recommend to choose the block length not too small (in particular for larger lags ), but unless an excessively large value is used, the performance of the estimator is not very sensitive to this tuning parameter.

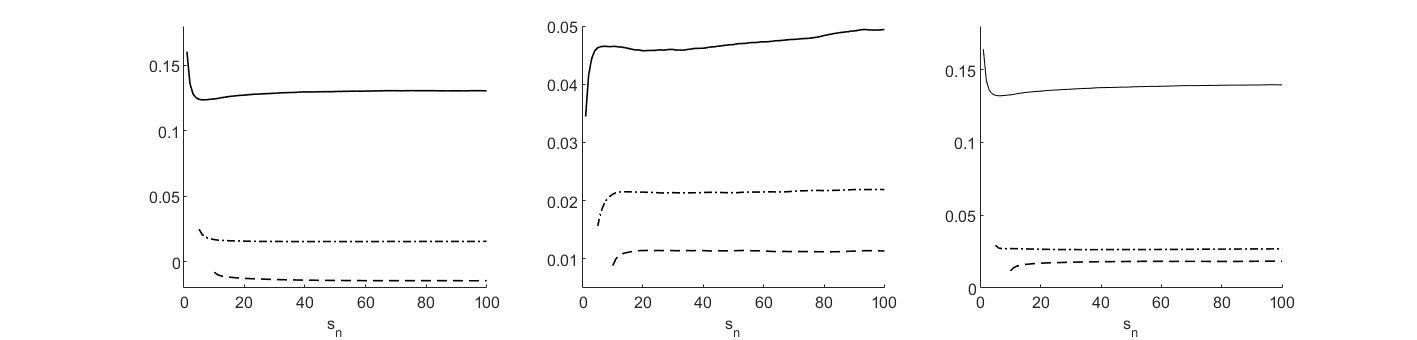

To guide the selection of a reasonable value, a graph analogous to a Hill plot may be useful. In Figure 9, for a single a time series according to the GARCHt model, the value of is plotted versus , for (left) and (right). We suggest to choose in a range where the plots starts to stabilize, which in this case again leads to a value of about 30.

Figure 9: versus for a single realization of the GARCHt model for lag (solid line), lag (dashed-dotted line) and lag (dashed line) with (left) and (right).

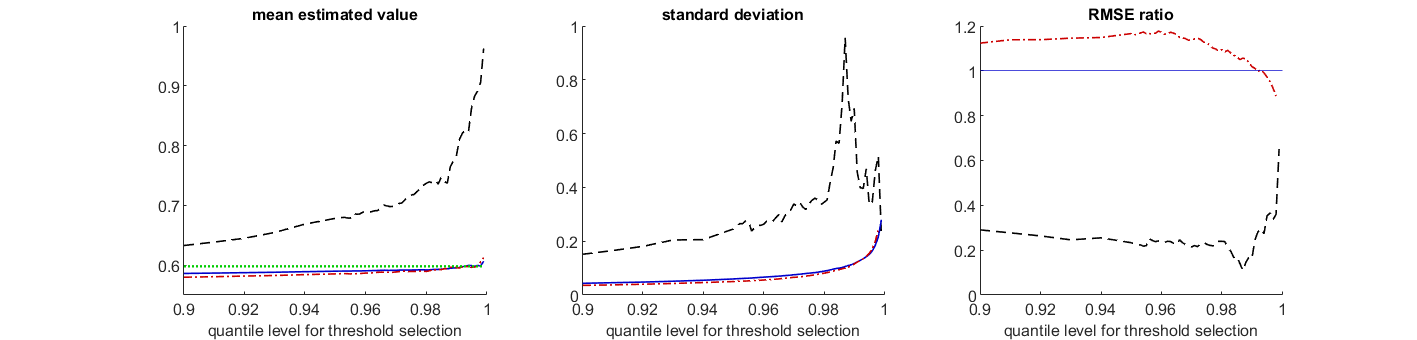

As always when the peaks-over-threshold approach is employed, all three estimators under consideration depend on the

selected threshold . So far, we have fixed this tuning parameter to the empirical -quantile of .

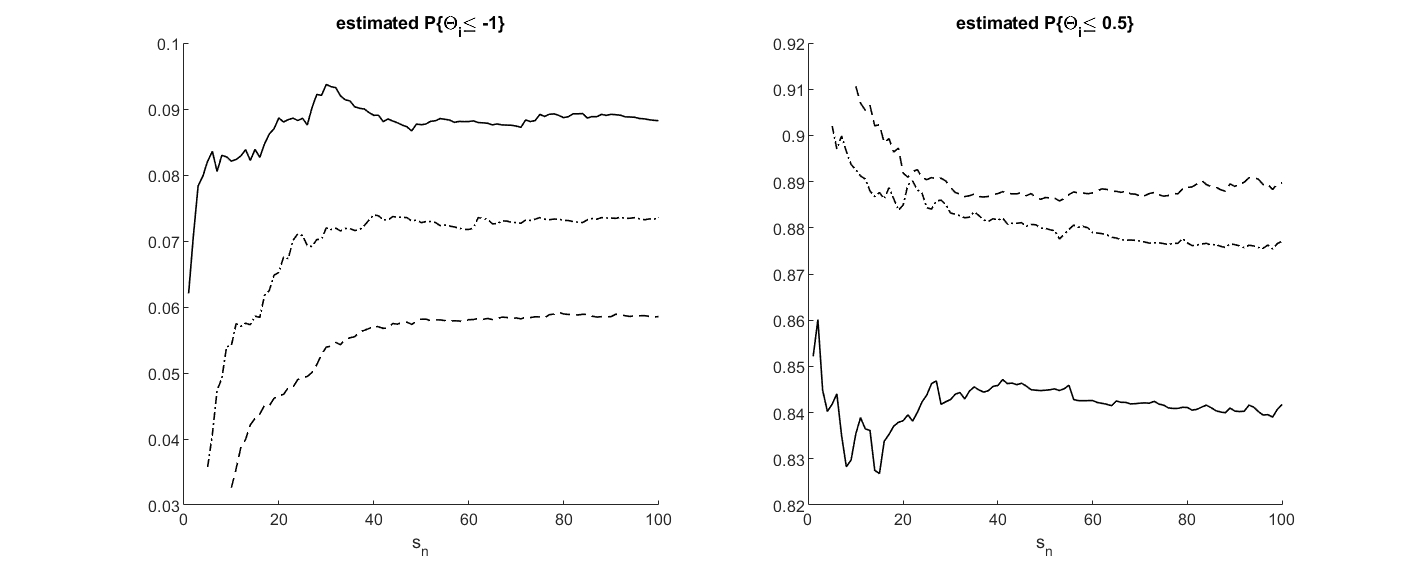

Figure 10 displays the performance of all estimators for the cdf at in the GARCHt and the SRE model for lag 1 for different quantile levels. Unless the threshold is chosen very high, the performance of the projection based estimator and forward estimator seems quite stable. To a lesser extent, this is also true for the backward estimator, but here the performance deteriorates a bit faster. (Note that here we consider a set whose boundary is close to the origin, while the backward estimator is known to perform better for sets clearly bounded away from 0.)

To conclude, apparently the newly proposed estimator is quite insensitive to the choice of the block length, and it is not more sensitive to threshold selection than the direct forward estimator.

Figure 10: Mean (left), standard deviation (middle) and relative efficiency w.r.t. (right) versus , of (blue solid line), (black dashed line) and (red dashed-dotted line) in the

GARCHt model (top) and in the SRE model (bottom) for lag and ; the true cdf is indicated by the green dotted line.

5 Example: comparison of asymptotic variances.

In this section we give further details for the calculation of the covariances in Example 2.4 of the main paper.

Recall that we defined the process by

(5.1)

(5.2)

for some , and and we set and define such that , which results in

(5.3)

The specific choice yields

(5.4)

Likewise, we obtain

(5.5)

(5.6)

(5.7)

According to Theorem 2.3, for sets such that its boundary is disjoint to , the asymptotic variance of equals

with and and given in Theorem 2.3 and (2.2).

Likewise, according to Davis et al. (2018), Theorem 3.1, for with , the asymptotic variance of is given by

where is a centered Gaussian process with covariance specified by the formulas in Theorem 2.3 and

(5.8)

(5.9)

(5.10)

Finally, from Davis et al. (2018), Theorem 3.1, it is known that in this setting the variance of the forward estimator equals

(5.11)

All these expectations can be easily calculated numerically, since the spectral tail process vanishes for and its distribution is discrete with just 4 points of mass.

Note that the asymptotic variances of the backward estimator and the projection based estimator with known can be calculated likewise, by omitting all terms involving or .

6 Verification of (BC), (BC’) and (M) (i) for solutions to stochastic recurrence equations.

In Subsection 2.1 of the main paper we discussed stationary solutions to stochastic recurrence equations

(6.1)

where are random -matrices with non-negative entries and are -valued random vectors so that , are i.i.d. The Conditions (SRE) and (SRE’) have been used to conclude the existence of a stationary regular varying solution and that is an aperiodic, positive Harris recurrent, -irreducible Feller process. Recall

(6.2)

where and are independent of .

Here we give more details why Conditions (BC), (BC’) and (M) (i) are satisfied in this setting.

As in the paper, denotes both the Euclidean norm of a vector and the corresponding operator norm of a matrix.

Recall that for all one has for sufficient large

Since we assume that and only have non-negative entries, the first summand can be bounded by . For the second term, the generalized Markov inequality and (6.3) yield

(6.8)

Hence,

(6.9)

for all . To sum up, we have shown

(6.10)

which is (2.11) in the main paper.

Because of regular variation of , and , we have and . Therefore

and

(6.11)

(6.12)

i.e. condition (BC).

Next observe that, for , from the drift condition , i.e. Assumption 2.1 (iii) of Kulik et al. (2019) which has been established in Subsection 2.1 with some and some , one may conclude by induction that (Douc et al. (2018), Proposition 14.1.8). For all such that , it follows

(6.13)

(6.14)

(6.15)

(6.16)

for sufficiently large .

Define , which for all can be bounded in absolute value by for some constant . The uniform moment bound (6.16) readily shows that the random variables are uniformly integrable, so that the definition of the tail process yields

for all . Moreover, the representation of the forward tail process and (6.3) show that the are summable:

Hence, for all , one can find some such that . Using (6.16) and convergence (2.10), one may conclude for sufficiently large

(6.17)

Let tend to 0 to obtain (BC’).

Finally, (6.16) with , , and shows that the sum on the left-hand side of Condition (M) (i) can be bounded by a multiple of

(6.18)

(6.19)

(6.20)

provided is bounded, because is of larger order than for all .

7 Modified sliding blocks limit theorem.

In this section we present a slightly modified version of a limit theorem for unbounded functions of sliding blocks introduced by Drees and Neblung (2021) (D&N), Theorem 2.4, which is applied in the proof of Theorem 2.3 of the main paper.

To this end, assume that is a triangular array of row-wise stationary random variables, consider a set of functionals defined on vectors of arbitrary length and define for some sequence ,

(7.1)

(7.2)

(7.3)

(7.4)

and for some suitable sequence ; here denotes a random variable with the same distribution as . Moreover, we use the following conditions taken from Section 2 and Appendix A of D&N:

(A1)

is stationary for all .

(A2)

The sequences , , and , , satisfy , , and .

(D0)

The processes , , are separable.

(MX)

for .

(C)

There exists a function such that

(7.5)

()

satisfies

(i)

(ii)

(iii)

for some .

(L)

(D1)

There exists a semi-metric on such that is totally bounded and

(7.6)

(D2)

(7.7)

where denotes the -bracketing number of w.r.t. , i.e. the smallest number such that for each there exists a partition of satisfying

(7.8)

(Here denotes the outer expectation.)

(D3)

Denote by the -covering number of w.r.t. the random semi-metric

(7.9)

with , , independent copies of , i.e. is the smallest number of balls with respect to with radius that is needed to cover . We assume

(7.10)

Condition () is always fulfilled if

(7.11)

Then we can modify Theorem 2.4 of D&N as follows.

Theorem 7.1.

(i)

Suppose the conditions (A1), (A2), (D0), (MX) and (C) are met. Moreover, assume condition (L) is satisfied and

(7.12)

Then the fidis of and of converge to the fidis of the Gaussian process defined in Theorem 2.1 of D&N.

(ii)

If, in addition, is measurable, is the same for all , (7.12) holds for and the conditions (D1) and (D2) or the conditions (D1) and (D3) are fulfilled, then the processes and converge weakly to uniformly.

So, in comparison with Theorem 2.4 of D&N, basically condition (2.8) in that paper, which is the analog to (7.12) with some exponent strictly greater than 2, is replaced with the weaker condition (7.12), a weak technical condition is omitted, and as a compensation condition (L) is added.

The proof is basically the same as for Theorem 2.4 in D&N. We apply Theorem A.1 of D&N to the observations , , and block lengths and to establish fidi-convergence of . Only Condition () must be verified, because (L) is assumed and the remaining conditions follow as in the proof of Theorem 2.1 of D&N.

Since

Hence, equation (7.11) holds, which in turn yields (). Now, the convergence of the fidis of follows from Theorem A.1 of D&N.

Similarly,

(7.17)

so that the fidi-convergence of follows, too.

Part (ii) of the assertion can be concluded by the same arguments as in the proof of Theorem 2.4 of D&N.

∎

8 Proof of (2.1) and (A.4).

First we want to establish (2.1) of the paper, i.e. the convergence

(8.1)

for ,

(8.2)

and , . To this end, we define the approximating functions ,

(8.3)

for all .

As a finite sum of continuous functions, is -a.s. continuous for if and . While the former equality is ensured by (C) and Lemma A.3, the latter follows from , where and are independent and has a Pareto()-distribution. Here we only need the continuity for , but below the general version is used in the proof of (A.4) for the continuity of .

Since is bounded by , the weak convergence defining the tail process implies

(8.4)

One has as for all . Since for all , dominated convergence implies as .

Next, we prove that the difference between and is asymptotically negligible for all as and tend to . While here this result is only needed for , the general version is used in the proof of (A.4) below.

Using (A.18) of the paper, one has for sufficiently large (such that )

(8.5)

(8.6)

(8.7)

(8.8)

For from (TC), Condition (BC) implies

(8.9)

(8.10)

(8.11)

for sufficiently large , due to regular variation of . Therefore,

(8.12)

(8.13)

for sufficiently large and all .

Thus, condition (BC) and (TC) yield

(8.14)

Combine this with (8.4) and to conclude (8.1), i.e. (2.1) of the paper.

Next we verify (A.4) of the paper, i.e.

(8.15)

for all , with defined as with

(8.16)

(8.17)

Again we define approximating functions by

(8.18)

(8.19)

for all .

Observe that and , so that is -a.s. continuous and bounded by . Thus, the definition of the tail process implies

Combining this with (8.20) and as , which holds due to dominated convergence and for all , yields (8.15), i.e. (A.4) of the paper.

9 Proof of Remark 2.2.

We start with part (a). Since and for and , we conclude

(9.1)

(9.2)

(9.3)

(9.4)

where in the last expression the first expectation is finite due to (M) (ii) and the second expectation, because is exponentially distributed. Thus, Condition (M) (ii) implies (2.5) of the paper.

Conversely, (2.5) of the paper implies

(9.5)

(9.6)

Thus, Condition (M) (ii) is equivalent to (2.5) of the main paper.

Next we turn to part (b) of Remark 2.2, which states that (M’) implies (M) (ii) and (TC).

According to (a), it suffices to establish (2.5) of the paper, which follows from the definition of the tail process if we prove uniform integrability of

This, in turn, is implied by the uniform moment bound

(9.7)

for . By Jensen’s inequality, the expectation can be bounded by

(9.8)

On the set , the term in the expectation can be bounded by

(9.9)

(9.10)

Thus, Conditions (M’) (i) and (ii) imply (9.7), and hence in turn condition (M) (ii).

To verify (TC) under (M’) (ii), choose so that . Since, for , the denominator is at least , it directly follows

(9.11)

(9.12)

Because is a bounded function on and thus the sum over with is bounded, Condition (M’) (ii) ensures that (TC) holds.

10 Proof of Lemma A.2.

Next, we give the proof for Lemma A.2 of the main paper. This lemma shows that the well-known anticlustering condition is implied by our condition (BC) which also restricts the size of clusters of extremes.

Lemma 10.1.

If (RV) and (BC) holds, then the so-called anticlustering condition

(10.1)

is satisfied for all .

Proof.

For , the assertion is an immediate consequence of (BC):

(10.2)

(10.3)

For and sufficiently large , stationarity, regular variation and (BC) yield

(10.4)

(10.5)

for all .

Thus, (BC) implies

(10.6)

(10.7)

11 Proof of Lemma A.9, part (ii).

Part (i) of Lemma A.9 was already established in the main paper. Here we prove the second assertion by similar arguments. First, recall the Lemma A.9 (ii):

Lemma 11.1.

Under Conditions (RV), (S) and (M) (ii)

with and defined in Theorem 2.3.

Proof.

In a first step we prove

Direct calculations using with and independent, yield

(11.1)

(11.2)

(11.3)

(11.4)

(11.5)

(11.6)

(11.7)

because the last two expectations can be interpreted as expectations of the same function on w.r.t. and , respectively, and these two distributions coincide.

The remaining part of the proof is similar to the proof of part (i) of Lemma A.9.

Direct calculations show

(11.8)

(11.9)

(11.10)

(11.11)

(11.12)

Similar as for the bound of in the proof of part (i), we obtain

(11.13)

(11.14)

Applying the Hölder inequality for expectations and for sums, we can bound by

(11.15)

According to Remark 2.2 (a), the first expectation is bounded if Condition (M) (ii) is met. The second expectation converges to as by monotone convergence. Hence . Since (2.5) in combination with also implies that for all , monotone convergence yields , too.

By analogous arguments as used for in the proof of part (i), one can show that

(11.16)

(11.17)

(11.18)

so that . Since the bounds on and do not depend on , all convergences hold uniformly in , which proves assertion (ii). ∎

12 Proof of Lemma A.10.

Lemma A.10 of the main paper establishes bounds on the solutions to two optimization problems. For convenience, the lemma is restated here.

Lemma 12.1.

For and let

(12.1)

with for .

Then and

as .

Proof.

We only establish the bound on , as the second assertion follows by similar arguments.

First note that is decreasing on the interval . Thus, if for some , then replacing by increases , i.e. any point of maximum must belong to .

Check that the partial derivative

(12.2)

tends to as . Hence all points of maximum must be in and all partial derivatives must vanish at such points. In particular,

for all , which is equivalent to

and thus to or . Because the second case contradicts , we have shown so far that all coordinates of a point of maximum must be equal.

The condition on the partial derivatives then reads as

(12.3)

This equation has a unique solution . It is easily seen that is of smaller order than and of larger order than as for all . In particular, and thus

(12.4)

as . The maximum of is given by

(12.5)

as .

∎

13 Proof of Lemma A.12.

Lemma A.12 of the paper contains the limit behavior of the covariances between and and the variance of . The proof uses similar ideas as the proof of Lemma A.4.

Lemma 13.1.

Suppose the conditions (RV), (S), (BC), (TC), (C), and (BC’) are satisfied. Then

(i)

(13.1)

(ii)

(13.2)

(13.3)

for all .

Proof.

Regular variation implies

(13.4)

(13.5)

for all (cf. Kulik and Soulier (2020), Section 2.3.3). Therefore, by stationarity we obtain

(13.6)

(13.7)

(13.8)

(13.9)

where the last step follows from Pratt’s Lemma, which may be applied because of (BC’).

Check that

(13.10)

(13.11)

Direct calculations similar to (11.7), using with and independent and yield

(13.12)

(13.13)

(13.14)

(13.15)

(13.16)

(13.17)

(13.18)

(13.19)

for all , which proves assertion (i).

Next we prove

(13.20)

(13.21)

for all , using similar techniques as in the proof of (8.1). In particular, by the same arguments and uniform integrability one obtains, for all ,

(13.22)

(13.23)

Furthermore, because , the Cauchy-Schwarz inequality yields

(13.24)

(13.25)

Because the second expectation converges to , (8.14) shows that

which, in combination with (13.22) and (13.23), yields (13.21) by standard arguments.

Now, by stationarity and Pratt’s lemma,

(13.26)

(13.27)

(13.28)

Similarly as above, we obtain

(13.29)

(13.30)

(13.31)

(13.32)

(13.33)

which concludes the proof of assertion (ii).

∎

References

(1)

Davis et al. (2018)

Davis, R. A., Drees, H., Segers, J. and Warchoł, M.

(2018), ‘Inference on the tail process with

application to financial time series modeling’, Journal of Econometrics205(2), 508–525.

Davis and Mikosch (2009)

Davis, R. A. and Mikosch, T. (2009),

Extremes of stochastic volatility models, in ‘Handbook of Financial

Time Series’, Springer, pp. 355–364.

Douc et al. (2018)

Douc, R., Moulines, E., Priouret, P. and Soulier, P. (2018), Markov Chains, Springer.

Drees and Neblung (2021)

Drees, H. and Neblung, S. (2021),

‘Asymptotics for sliding blocks estimators of rare events’, Bernoulli .

to appear.

Kulik and Soulier (2020)

Kulik, R. and Soulier, P. (2020),

Heavy-Tailed Time Series, Springer.

Kulik et al. (2019)

Kulik, R., Soulier, P. and Wintenberger, O. (2019), ‘The tail empirical process of regularly varying

functions of geometrically ergodic Markov chains’, Stochastic

Processes and their Applications129(11), 4209–4238.