1 Introduction

Given two random vectors and , canonical correlation analysis (CCA) has been one of the most classical methods to study the correlations between them since the seminal work by Hotelling [24]. More precisely, CCA seeks two sequences of orthonormal vectors, such that the projections of and onto these vectors have maximized correlations. These correlations are referred to as canonical correlation coefficients (CCCs),

which can be characterized as the square roots of the eigenvalues of the population canonical correlation (PCC) matrix

|

|

|

where , , and are the population covariance and cross-covariance matrices defined by

|

|

|

|

|

|

In this paper, we consider the following standard signal-plus-noise model for and :

|

|

|

(1.1) |

where and are two independent noise vectors with i.i.d. entries of mean zero and variance one, is a shared signal vector with i.i.d. entries of mean zero and variance one (which yields a rank- correlation), and and are two arbitrary deterministic matrices. Under the model (1.1), the PCC matrix is given by a rank- matrix

|

|

|

(1.2) |

and we denote the non-trivial eigenvalues of as .

We can study and the population CCCs via their sample counterparts, i.e., the sample canonical correlation (SCC) matrix and the sample CCCs. More precisely, let , , be i.i.d. samples of .

We stack them (as column vectors) into two matrices

|

|

|

(1.3) |

where is a convenient scaling, with which we can write the sample covariance and cross-covariance matrices concisely as

|

|

|

and , and are respectively , and matrices with i.i.d. entries of mean zero and variance .

Then, we define the SCC matrix as

|

|

|

and denote their eigenvalues by

The square roots of these eigenvalues are referred to as sample canonical correlation coefficients. Equivalently, the sample CCCs are the cosines of the principal angles between the two subspaces spanned by the rows of and , respectively. If while and are fixed, it is easy to see that the SCC matrix converges to the PCC matrix almost surely by the law of large numbers, and hence every sample CCC converges almost surely to the corresponding population CCC.

On the other hand, in this paper, we focus on the high-dimensional setting with a low-rank signal: and as for some constants and , and is a fixed integer that does not depend on . In this case, the behavior of the SCC matrix deviates greatly from that of the PCC matrix.

Related work. In the null case with , the eigenvalue statistics of the SCC matrix have been well-understood. If and are Gaussian matrices, then the eigenvalues of reduce to those of a double Wishart matrix, which belongs to the famous Jacobi ensemble [26]. It was shown in [40] that, almost surely, the empirical spectral distribution (ESD) of the double Wishart matrix converges weakly to a deterministic probability distribution (cf. (2.14) below). By analyzing the joint eigenvalue density of the Jacobi ensemble, Johnstone [26] proved that the largest eigenvalues of double Wishart matrices satisfy the Tracy-Widom law asymptotically. Alternatively, the Tracy-Widom law of double Wishart matrices can also be obtained as a consequence of the results in [23] for F-type matrices. In the general non-Gaussian case, the convergence of the ESD of was proved in [45], the CLT of the linear spectral statistics for was proved in [46], and the Tracy-Widom law of the largest eigenvalue of was proved in [22] under the assumption that the entries of and have finite moments up to any order. The moment assumption for the Tracy-Widom law was later relaxed to the finite fourth moment condition in [43].

Some arguments in the literature for the null case are based on the fact that the subspaces spanned by the rows of and are approximately uniformly (Haar) distributed random subspaces, which, however, does not hold for the non-null case with . This makes the study of the non-null case more challenging. Assuming that and are both Gaussian matrices, the asymptotic behaviors of the likelihood ratio processes of CCA under the null hypothesis of no spikes (i.e., ) and the alternative hypothesis of a single spike (i.e., ) were studied in [27]. If either or is fixed as , the asymptotic distributions of the sample CCCs were derived in [21] under the Gaussian assumption. On the other hand, if and are both proportional to , the limiting distributions of the sample CCCs have been established under the Gaussian assumption in [4], which we discuss in more detail now.

BBP transition. Suppose , and are independent random matrices with i.i.d. Gaussian entries. Bao et al. [4] proved that for any , the behavior of undergoes a sharp transition across the threshold defined by

|

|

|

(1.4) |

More precisely, the following dichotomy occurs:

-

(1)

if , then sticks to the right edge (cf. (2.15) below) of the limiting bulk eigenvalue spectrum of the SCC matrix, and converges weakly to the Tracy-Widom law;

-

(2)

if , then lies around a fixed location (cf. (2.16) below), and converges weakly to a centered normal random variable.

Following the notation in random matrix theory literature, we call in case (2) an outlier. The above abrupt change of the behavior of when crosses is generally referred to as a BBP transition, which dates back to the seminal work of Baik, Ben Arous and Péché [2] on spiked sample covariance matrices. The phenomenon of BBP transition has been observed in many random matrix ensembles deformed by low-rank perturbations. Without attempting to be comprehensive, we refer the reader to [11, 10, 18, 29, 30, 36] about deformed Wigner matrices, [1, 2, 3, 9, 19, 25, 35] about spiked sample covariance matrices, [12, 42, 44] about spiked separable covariance matrices, and [5, 6, 7, 13, 14, 41, 47] about several other types of deformed random matrix ensembles. The SCC matrix considered in this paper can be regarded as a low-rank perturbation of the SCC matrix in the null case with .

Main results and basic ideas. A natural question is whether the above BBP transition holds universally if we only assume certain moment conditions on the entries of , and . Answering this question is not only theoretically interesting from the point of view of random matrix theory, but also crucial for modern applications of CCA in e.g., statistical learning, wireless communications, financial economics and population genetics. In this paper, we solve this problem and prove that the BBP transition occurs as long as the entries of and satisfy the bounded -th moment condition (with denoting an arbitrarily small positive constant). More precisely, we obtain the following results when .

-

(i)

In Theorem 2.3, assuming that the entries of , and have bounded moments up to any order, we prove that converges weakly to a centered normal random variable.

-

(ii)

In Theorem 2.4, we prove the CLT for under a relaxed bounded -th moment condition on the entries of and a bounded -th moment condition on the entries of .

On the other hand, when , the Tracy-Widom law of was proved in [34]. For the reader’s convenience, we will state it in Theorem 2.5.

The proof in [4] depends crucially on the fact that multivariate Gaussian distributions are rotationally invariant under orthogonal transforms, which makes it hard to be extended to the non-Gaussian case. To circumvent this issue, we employ an entirely different approach—a linearization method developed in [43]. More precisely, we define a random matrix that is linear in and (cf. equation (3.2) below) and call its inverse as resolvent. We found that the eigenvalues of the SCC matrix are precisely the solutions to a determinant equation in terms of a linear functional of (cf. equation (3.4) below). Moreover, an (almost) optimal local law for this linear functional was obtained in [43]. In [34], we obtained a large deviation estimate on the outlier sample CCCs: if , then converges to with convergence rate (which is slightly larger than the correct order of fluctuation ). With the local law and the large deviation estimate as main inputs, we can reduce the problem to proving the CLT for a (different) linear functional of , denoted by (cf. Section 4.3).

The main technical part of our proof is to show that converges weakly to a centered Gaussian random variable. Our basic idea is to use the classical moment method, that is, showing that the moments of match those of a Gaussian random variable asymptotically. One method to calculate the moments of is to use the simple identity and apply a cumulant expansion formula (cf. Lemma A.1 below) to the resulting expression. However, the calculation for this strategy will be rather tedious. Instead, we adopt a strategy in [29, 30], that is, we first prove the CLT in an “almost Gaussian” case (i.e., a case where most of the entries of and are Gaussian), and then show that the general case is sufficiently close to the almost Gaussian case. This strategy allows us to divide the lengthy calculation into several parts that are more manageable. In particular, the resolvent expansion formula can be replaced by a simpler Gaussian integration by parts formula. We refer the reader to Section 3 for a more detailed review of our proof.

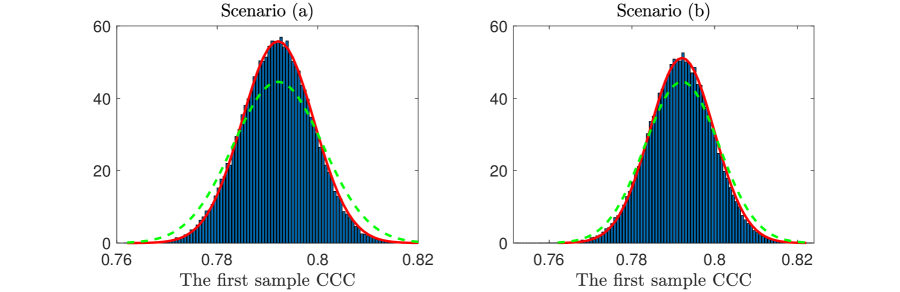

Finally, we remark that the limiting variance of depends on the fourth cumulants of the entries of , and in an intricate way, which has not been identified in the Gaussian case. We also perform simulations to verify this deviation from the CLT result in [4] (cf. Figure 1).

Organizations. The rest of this paper is organized as follows. In Section 2, we define the model and state the main results, Theorem 2.3 and Theorem 2.4, on the limiting distributions of the outlier sample CCCs. In Section 3, we introduce the linearization method, define the resolvent, and give a brief overview of the proof strategy for Theorem 2.3 and Theorem 2.4. The proof of Theorem 2.3 will be given in Sections 4–8. In Section 4, we use the linearization method to reduce the problem to showing a CLT for a linear functional of the resolvent. In Section 5, we establish the CLT of the outlier sample CCCs in an almost Gaussian case, where most of the entries of and are Gaussian. Section 6 contains the proof of Lemma 5.5, which is a key lemma for the proof in Section 5, while Section 7 gives the proof of Theorem 6.4, which is used in the proof of Lemma 5.5. In Section 8, we complete the proof of Theorem 2.3 by showing that the general setting of Theorem 2.3 is close to the almost Gaussian case asymptotically. Finally, utilizing Theorem 2.3 and a comparison argument, we complete the proof of Theorem 2.4 in Section 9.

Conventions.

For two quantities and depending on , the notation means that for some constant , and means that for a positive sequence as . We use the notation if and the notation if and . Given a matrix , we use to denote the operator norm, to denote the Frobenius norm, and to denote the maximum norm. Given a vector , stands for the Euclidean norm. In this paper, we often write an identity matrix as or without causing any confusion.

Acknowledgements. I want to thank Zongming Ma for bringing this problem to my attention and for valuable suggestions. I also want to thank Edgar Dobriban, David Hong and Yue Sheng for fruitful discussions. I am grateful to the editor, the associated editor and an anonymous referee for their helpful comments, which have resulted in a significant improvement.

3 Overview of the proof

In this section, we give a brief overview of the proof for Theorem 2.3.

The starting point of our proof is the following self-adjoint linearization trick developed in [34, 43], that is, a is an eigenvalue of if and only if the following equation holds:

|

|

|

(3.1) |

Inspired by this equation, we define the following self-adjoint block matrix

|

|

|

(3.2) |

and call its inverse the resolvent:

|

|

|

(3.3) |

In this paper, we extend the argument to with being the branch with positive imaginary part. Similar to equation (3.1), it is not hard to see that is not an eigenvalue of the null SCC matrix if and only if . Hence, for , using (1.3), (2.3), (2.4) and (2.5), we can rewrite (3.1) as

|

|

|

|

|

|

|

|

(3.4) |

where we have used the identity for any two matrices and of conformable dimensions. Here, , and are , and matrices defined as

|

|

|

By the anisotropic local law in Theorem 4.8, in equation (3.4) can be replaced by a deterministic matrix, denoted by , up to a small error:

|

|

|

(3.5) |

where

|

|

|

Using the definition of in equation (4.14) below, we can check that if we set in (3.5), then the resulting deterministic equation has a solution if is supercritical. Moreover, Theorem 4.8 shows that with high probability (cf. Definition 4.1 (iv)) for any constant . With this fact, we proved in [34] that with high probability. Thus, performing a Taylor expansion of equation (3.5) around , we obtain that with high probability,

|

|

|

This equation suggests that the limiting distribution of should be determined by that of . In fact, through calculations in Section 4.3, we find that is related to a more complicated linear function of given in (4.32). We refer the reader to Proposition 4.11 below for a precise statement.

Now, roughly speaking, our problem has been reduced to showing the CLT for a linear function of . Through a direct calculation, we can further reduce the problem to showing the CLT of a matrix of the form (cf. equation (4.42))

|

|

|

(3.6) |

where is a matrix independent of and . To illustrate the basic idea, we describe the strategy of the proof for the following quantity:

|

|

|

(3.7) |

where is a -dimensional vector independent of and .

In general, to show that in (3.6) converges weakly to a Gaussian matrix, we can adopt the Cramér-Wold device, that is, we will show that

|

|

|

is asymptotically Gaussian for any fixed vector of parameters . This can be proved using the same strategy as the proof of the CLT for , which we will discuss now.

In order to prove that is asymptotically Gaussian, we will show that its moments match those of a Gaussian random variable as . It suffices to prove the zero mean condition and the induction relation: for any fixed integer ,

|

|

|

(3.8) |

for some deterministic parameter , which determines the variance of the limiting Gaussian distribution. We will describe some basic ideas for the proof of (3.8), while the mean condition can be regarded as a special case with .

Using the definition of , we can write that , and hence

|

|

|

Using the definitions of (cf. equation (4.15)), we can write into a sum of terms of three types (cf. equation (6.11) below)

|

|

|

where , , are vectors that are independent of (and whose forms are irrelevant for our discussion below), and the matrices are block identity matrices defined as

|

|

|

(3.9) |

We only consider type B terms, while type C terms can be handled in exactly the same way. We need to calculate terms of the form

|

|

|

(3.10) |

Assume for now that the entries of are Gaussian. Then, applying Gaussian integration by parts to , we obtain that

|

|

|

|

|

|

|

|

By the definition of , its derivative with respect to can be evaluated as

|

|

|

We can calculate the terms I and II using this identity. Then, the resulting expressions can be estimated using the anisotropic local law, Theorem 4.8, on and the anisotropic local laws on , , which will be provided by Theorem 6.4 below. Through our calculations, we find that the term I will cancel certain type A terms up to an error, while the term II will contribute to the first term on the right-hand side of (3.8).

In general, when the entries of are not Gaussian, we can replace Gaussian integration by parts by a cumulant expansion formula in Lemma A.1, with which we get an expansion of (3.10) with higher order derivatives of . Then, we need to estimate them using anisotropic local laws on and . However, due to the intricate form of as an inverse of a block matrix, the estimation of first order derivative terms is already quite complicated. The estimation of higher order derivative terms will be even more tedious. In particular, to get the fourth cumulant terms in (2.27), we need to study terms coming from the third order derivative of , which leads to a much lengthier calculation than that in the Gaussian case. To have a more tractable proof, we will adopt a strategy in [29, 30]: we first consider an almost Gaussian case where most of the entries of and are Gaussian, and then show that the general case is sufficiently close to the almost Gaussian case in the sense of the limiting CLT of in (3.6). The merit of this strategy is that we can divide the proof into several parts that are relatively easier to handle, as we will explain now.

First, given the matrix appearing in , we will construct almost Gaussian matrices and by changing most entries of and to i.i.d. Gaussian random variables, while keeping the rest entries unchanged. The locations of Gaussian entries depend on the indices of “small” entries in (see Proposition 5.1 for more details). Then, we can define , and by replacing and with and in definitions (3.2), (3.3) and (3.6). Under this construction, we can show that has the same asymptotic distribution as through a resolvent comparison argument developed in [29, Section 7]. Since this is a relatively standard argument in the random matrix theory literature, we will not discuss it here and refer the reader to Section 8 for more details.

Now, to conclude the proof, it remains to prove the CLT of . We first decompose each of and into several different blocks—a large block consisting of Gaussian entries only and several small blocks that also contain non-Gaussian entries. Using the Schur complement formula and concentration estimates for large random vectors, after some calculations, we can rewrite into two parts, where one part is of the form (3.6) with a resolvent consisting of the large Gaussian blocks in and , and the other part is a quadratic form of the small blocks in and (see equation (5.21) below). We have discussed the proof for the former part using Gaussian integration by parts and local laws. On the other hand, the latter part can be handled directly using the classical CLT. This completes the proof for the almost Gaussian case in principle, but the calculations of the limiting covariance functions of the two parts (cf. Sections 5.4 and 5.5) are rather tedious. However, these calculations are straightforward algebraic calculations, and the reader can use a computer algebra system to check them.

Our main result for the almost Gaussian case is summarized in Proposition 5.1, and its proof in Sections 5–7 constitutes the main theoretical contribution of this paper. More precisely, Section 5 constructs the almost Gaussian setting and calculates the limiting covariance function; Section 6 proves the CLT of (3.6) in the Gaussian case; Section 7 proves an sharp anisotropic local law on .

Finally, Theorem 2.4 follows from Theorem 2.3 combined with a comparison argument. More precisely, suppose we have two ensembles of random matrices and , where and satisfy the moment assumption (2.31) and and satisfy (2.8). Then, using the resolvent comparison method developed in [31], we can show that the asymptotic distributions of and are the same as long as the first four moments of the entries and entries match those of the entries and entries. In the proof of Theorem 2.3, we have shown the CLT of . Together with the comparison result, it implies that satisfies the same CLT, and thus concludes Theorem 2.4. Both the construction of according to the moment matching conditions and the resolvent comparison method have been well-understood in the random matrix theory literature. We refer the reader to Section 9 for more details.

6 Proof of Lemma 5.5

In this section, we give the proof of Lemma 5.5, which, as we have seen, is a key step in the proof of Proposition 5.1. Under the setting of Lemma 5.5, we need to study the CLT of the matrix

|

|

|

|

It is easy to check that the matrices , , and are respectively , , and random matrices independent of , and they satisfy that

with high probability,

|

|

|

(6.1) |

|

|

|

(6.2) |

These conditions all follow from (5.20) and (5.11). For simplicity of notations, we permute the columns of and study the CLT of

|

|

|

(6.3) |

Moreover, with a slight abuse of notation, we rename as and study the CLT of the following matrix under the conditions (6.1) and (6.2):

|

|

|

|

(6.4) |

where

|

|

|

Since , we have where is a negligible error. Hence, without loss of generality, we still assume that the dimensions of and are and in order to simplify notations.

In our proof, in order to avoid singular behaviors of on exceptional low-probability events, we will use a regularized resolvent defined as follows.

Definition 6.1 (Regularized resolvent).

For we define the regularized resolvent as

|

|

|

The main reason for introducing the regularized resolvent is that it satisfies the deterministic bound:

|

|

|

(6.5) |

This estimate has been proved in Lemma 3.6 of [43]. In particular, if we choose for a constant , then (6.5) justfies the assumption of Lemma 4.2 (iii), which will be used in the proof when we bound expectations of polynomials of regularized resolvent entries. With a standard perturbation argument, we can easily control the difference between and .

Claim 6.2.

Suppose there exists a high probability event on which for belonging to some subset. Then, we have that

|

|

|

(6.6) |

Proof.

For , we define

|

|

|

Taking the derivative with respect to , we immediately obtain that

|

|

|

(6.7) |

Thus, applying Gronwall’s inequality to

|

|

|

we get that on Then, using (6.7) again, we get (6.6).

∎

Note that the bound (6.6) is purely deterministic on , so we do not lose any probability in this claim. Moreover, such a small error is negligible for our proof.

In the following proof, we will use the regularized resolvent with , and prove the CLT for with replaced by . The argument in the proof of Claim 6.2 then allows us to show that satisfies the same asymptotic distribution. In the proof, it is helpful to keep in mind that the bound (6.5) always holds with , and hence Lemma 4.2 (iii) can be applied without worry. To ease the notation, we also introduce the following notion of generalized entries.

Definition 6.3 (Generalized entries).

For , and an matrix , we shall denote

|

|

|

(6.8) |

where is the standard unit vector along the -th coordinate axis.

For , we denote the -th column vector of by .

With the Cramér-Wold device, it suffices to prove that

|

|

|

is asymptotically Gaussian for any fixed vector of parameters denoted by . By (4.19), we have the rough bound . For our purpose, it suffices to show that the moments of match those of a centered Gaussian random variable asymptotically. This follows immediately from the following claims: (i) the mean of satisfies

|

|

|

(6.9) |

and (ii) for any fixed integer , we have that

|

|

|

(6.10) |

for a deterministic parameter as a function of . Moreover, the covariance of is also determined by .

As described in Section 3, our main tool for the proof of (6.9) and (6.10) is Gaussian integration by parts. Using the identity and equation (4.15), we get that

|

|

|

(6.11) |

We first prove (6.9). With (6.11), we can write that

|

|

|

|

|

|

|

|

|

|

|

|

(6.12) |

where we have abbreviated . For the sum in line (6.12), we expand it as

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(6.13) |

where in the second step we used Gaussian integration by parts with respect to and ,

|

|

|

and the identities

|

|

|

(6.14) |

for any vectors . With the notations in (4.5), we can rewrite (6.13) as

|

|

|

|

|

|

|

|

|

|

|

|

(6.15) |

where recall that is defined in (3.9).

We claim that

|

|

|

(6.16) |

whose proof will be postponed until we complete the proof of Lemma 5.5. Moreover, , , satisfy the anisotropic local laws in Theorem 6.4 below, which implies that for any deterministic unit vectors ,

|

|

|

(6.17) |

Now, plugging (6.15) into (6.12) and using (6.16) and (6.17), we obtain that

|

|

|

(6.18) |

which implies (6.9).

It remains to prove (6.10). With (6.11), we expand as

|

|

|

|

|

|

|

|

|

(6.19) |

|

|

|

(6.20) |

|

|

|

(6.21) |

|

|

|

(6.22) |

|

|

|

(6.23) |

Again, we apply Gaussian integration by parts to the terms in (6.20)–(6.23). First, as we have seen in the case, the terms containing , , and will cancel the first term in (6.19), leaving an error of order as in (6.18). Thus, we get that

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(6.24) |

|

|

|

(6.25) |

|

|

|

(6.26) |

|

|

|

(6.27) |

To calculate the terms (6.24)–(6.27), we need to use the anisotropic local law of , . We first define the deterministic matrix limits of :

|

|

|

(6.28) |

where the functions are defined by

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(6.29) |

On the other hand, the functions are defined by

|

|

|

Here, we recall that is defined in (1.4), , are defined in (4.6)–(4.9), is defined in (4.13), and is defined in (4.29).

Theorem 6.4.

Suppose Assumption 2.1 holds. For any deterministic unit vectors , we have that

|

|

|

(6.30) |

We will prove Theorem 6.4 in Section 7. Again, by the argument in the proof of Claim 6.2, (6.30) also holds for with . Now, we use this estimate to calculate (6.24)–(6.27) term by term. First, for (6.24), using (6.14) we get that

|

|

|

(6.31) |

Now, using the local law (4.19), (6.1) and the first equation in (4.10), we get that

|

|

|

(6.32) |

Moreover, using (6.1), (6.2) and the local law for in Theorem 6.4, we get that

|

|

|

(6.33) |

where we used the notation

|

|

|

and let for . Plugging (6.32) and (6.33) into (6.31), we get that

|

|

|

(6.34) |

Similarly, we can get that

|

|

|

(6.35) |

For (6.26), we have that

|

|

|

(6.36) |

Using (4.19) and (6.2), we get that

|

|

|

(6.37) |

Using the local law for in Theorem 6.4 and (6.2), we get that

|

|

|

(6.38) |

Plugging (6.37) and (6.38) into (6.36) gives that

|

|

|

(6.39) |

Similarly, we can get that

|

|

|

(6.40) |

Combining (6.34), (6.35), (6.39) and (6.40), we obtain that

|

|

|

where is a function of defined by

|

|

|

|

|

|

|

|

|

|

|

|

This concludes (6.10). Combining (6.9) and (6.10), we have shown that is asymptotically Gaussian with zero mean, which indicates that converges weakly to a centered Gaussian matrix by the Cramér-Wold device. Then, the argument in the proof of Claim 6.2 shows that converges to the same limit. Using the definitions of , , in (6.29), we obtain from that

|

|

|

(6.41) |

where are Gaussian matrices as defined in Lemma 5.5, and through direct calculations, we can check that are given by

|

|

|

(6.42) |

In the above calculation, we also used that for ,

|

|

|

Finally, combining (6.41) with (6.3), we can obtain the asymptotic distribution in (5.22), upon renaming the matrices and the coefficients . This concludes Lemma 5.5.

Before the end of this section, we give the proof of (6.16).

Proof of (6.16).

By the proof of Claim 6.2, it suffices to prove the estimate for for . In the following proof, we denote with . By the averaged local law (4.21), we have

|

|

|

(6.43) |

where we also used that due to (2.19). Thus, to show (6.16), it suffices to prove that

|

|

|

|

(6.44) |

|

|

|

|

(6.45) |

The estimate (6.44) follows directly from the definitions in (4.6)–(4.9). We still need to prove (6.45). It follows from the spectral decomposition of the resolvent, which we introduce next.

First, recalling the notations in (2.12), we define

|

|

|

(6.46) |

and the resolvent

|

|

|

where the two blocks and are defined as

|

|

|

(6.47) |

By Theorem 2.10 of [8], we have the following bounds on the extreme eigenvalues of and :

|

|

|

(6.48) |

|

|

|

(6.49) |

Next, consider a singular value decomposition of ,

|

|

|

(6.50) |

where ’s are the eigenvalues of the null SCC matrix , and ’s and ’s are respectively the left and right singular vectors. Then, the singular value decomposition is given by

|

|

|

(6.51) |

We denote the block of by , the block by , the block by , and the block by .

Using the Schur complement formula, we can check that

|

|

|

(6.52) |

|

|

|

(6.53) |

|

|

|

(6.54) |

Now, we are ready to prove (6.45). We only give the proof for , and all the other cases can be proved in exactly the same way.

Using the rigidity estimate (4.4), we get that with high probability,

|

|

|

(6.55) |

Then, using (4.5), (6.51), (6.52), (6.55), and (6.48), we obtain that

|

|

|

where is the standard unit vector along the -th direction.

∎

8 Proof of Theorem 2.3

With Proposition 5.1 and Proposition 4.11, we see that (2.23) holds in the almost Gaussian case. Hence, to conclude Theorem 2.3, it suffices to show that the general case is sufficiently close to the almost Gaussian case regarding the outliers. In particular, by (4.37), (4.38) and (5.6), we only need to show that the asymptotic distribution of in (5.7)

for general and is the same as that of defined for almost Gaussian and .

Corresponding to (5.1) and (5.2), we define the index set (“” stands for “small”)

|

|

|

Corresponding to (3.2) and (3.3), we define a new self-adjoint block matrix and its resolvent as

|

|

|

where and are defined through

|

|

|

(8.1) |

Here, and are i.i.d. Gaussian random variables independent of and with mean zero and variance . Note that and satisfy the setting of Proposition 5.1.

Define the set of pairs of indices

|

|

|

We choose a bijective ordering map on :

|

|

|

Similar to (7.29), we introduce simplified notations

|

|

|

(8.2) |

For any , we define the matrix such that

|

|

|

Correspondingly, we define

|

|

|

Under the above definition, we have and . For , we can write that

|

|

|

(8.3) |

where is a matrix defined by

|

|

|

(8.4) |

and is a random matrix with zero -th and -th entries. In particular, is independent of and .

For simplicity of notations, for any we denote that

|

|

|

(8.5) |

Then, given any function , we can write that

|

|

|

(8.6) |

We will estimate each term in the sum using resolvent expansions. More precisely, by (8.3) we have that

|

|

|

For any fixed , we can expand till order as

|

|

|

(8.7) |

We can also expand in terms of as

|

|

|

(8.8) |

We can get similar expansions for and by replacing with . We will combine these resolvent expansions with the Taylor expansion of to estimate the right-hand side of (8.6).

In the following proof, we use the regularized resolvent in Definition 6.1 with . We can also define and in a similar way. By (6.5), , and satisfy the deterministic bound

|

|

|

(8.9) |

Again, because of this bound, Lemma 4.2 (iii) can be used tacitly, and we will not emphasize this fact again in the following proof.

Using the expansion (8.8) for a sufficiently large (for example, will be enough), , the anisotropic local law (4.19) for , and the bound (8.9) for , we can obtain that for any deterministic unit vectors ,

|

|

|

(8.10) |

Moreover, using the same argument as in the proof of Claim 6.2, we can easily show that

|

|

|

(8.11) |

where is defined as (recall the notations in (5.7))

|

|

|

(8.12) |

By replacing with or , we can also define or .

Then, we will use the following comparison lemma to complete the proof of Theorem 2.3.

Lemma 8.1.

Fix any with . We abbreviate

|

|

|

The matrices and are defined similarly by replacing with and , respectively. Let be a function with bounded partial derivatives up to third order, and be an arbitrary deterministic sequence of symmetric matrices. Then, we have that

|

|

|

(8.13) |

|

|

|

(8.14) |

where satisfies , and we denote

|

|

|

and

|

|

|

(8.15) |

Proof.

The proof of this lemma is almost the same as the one for Lemma 7.13 of [29], where the main inputs are the local laws (4.19) and (8.10), the simple identity (8.6), and the resolvent expansions (8.7) and (8.8). The cosmetic modifications are mainly due to the fact that our local law takes a different form than the one in Theorem 2.2 of [29]. So we ignore the details.

∎

Combining Proposition 4.11, Proposition 5.1 and Lemma 8.1, we can conclude the proof of Theorem 2.3.

Proof of Theorem 2.3.

We fix any function and satisfying (5.4) and (5.5). Using (8.13) and (8.14), we get that

|

|

|

(8.16) |

where means the partial expectation with respect to , , and (for simplicity, we did not add and to the subscript). Since for and for , it is easy to check that

|

|

|

where is the matrix with entries . Thus, for any fixed and , applying (8.13) with replaced by , we get that

|

|

|

Plugging it into (8.16), we get that

|

|

|

On the other hand, we have the Taylor expansion

|

|

|

Comparing the above two equations, we get that

|

|

|

(8.17) |

We iterate (8.17) starting at and and obtain that

|

|

|

(8.18) |

where we also used the bound , which can be verified directly using the definition (8.15). Now, using (5.35), we can bound that

|

|

|

Plugging it into (8.18), we obtain that

|

|

|

This shows that has the same asymptotic distribution as in the almost Gaussian case. Combining this fact with (8.11), Proposition 4.11 and Proposition 5.1, we conclude (2.23) when is smooth. Extension to any bounded continuous follows from a standard argument. ∎

9 Proof of Theorem 2.4

In this section, we present the proof of Theorem 2.4 based on a comparison with Theorem 2.3. We first truncate the entries of , and using the moment condition (2.31). Choose a constant small enough such that and for a constant . Then, we introduce the following truncation on the entries of and :

|

|

|

In other words, we restrict ourselves to the following event:

|

|

|

Combining the condition (2.31) with Markov’s inequality and using a simple union bound, we get that

|

|

|

(9.1) |

Using (2.31) and integration by parts, it is easy to verify that

|

|

|

which implies

|

|

|

(9.2) |

Moreover, we trivially have that

|

|

|

Similar estimates also hold for the entries of and . Now, we introduce the matrices

|

|

|

Note that by (9.2), we have the estimates

|

|

|

(9.3) |

and similar estimates also hold for , , and . Now, we define SCC matrices and by replacing with in (2.10) and (2.11). With the estimate (9.3), we can readily bound the differences between the eigenvalues of and those of using Weyl’s inequality.

Lemma 9.1.

Under the above setting, we have that

|

|

|

Proof.

This lemma is an easy consequence of (9.3) and the singular value bounds in (6.48) and (6.49) (which hold by Theorem 9.3 (iv) below). Moreover, the probability bound is due to (9.1).

∎

By the above lemma, it suffices to prove that Theorem 2.4 holds under the following assumptions on , which correspond to the above setting for .

Assumption 9.2.

Assume that , and are independent , and matrices, whose entries are real i.i.d. random variables satisfying (2.1), (2.2), the bounded fourth moment condition

|

|

|

(9.4) |

and the following bounded support condition with :

|

|

|

(9.5) |

Moreover, we assume that Assumption 2.1 (iii)–(iv) hold.

The local laws in Section 4.2 can be extended to the above setting. More precisely, we have proved the following theorem in [34, 43].

Theorem 9.3.

Suppose Assumption 9.2 holds.

-

(i)

(Outliers: Theorem 2.9 of [34]) If , then we have that

|

|

|

(9.6) |

On the other hand, for any with , we have that

|

|

|

(9.7) |

-

(ii)

(Anisotropic local law: Theorem 3.9 of [34]) For any fixed and deterministic unit vectors , the following estimate holds for all :

|

|

|

(9.8) |

-

(iii)

(Eigenvalue rigidity: Theorem 2.5 of [43]) The eigenvalue rigidity estimate (4.4) holds.

-

(iv)

(Singular value bounds: Lemma 3.3 of [43]) For any constant , the bounds (6.48) and (6.49) hold with high probability.

For the above results to hold, it is not necessary to assume that the entries of , and are identically distributed, that is, only independence and moment conditions are needed.

Moreover, Lemma 5.3 can also be extended.

Lemma 9.4 (Lemma 3.8 of [17]).

Let , be independent families of centered independent random variables, and , be families of deterministic complex numbers. Suppose the entries , have variances at most and satisfy the bounded support condition (9.5). Then, the following large deviation bounds hold:

|

|

|

|

|

|

|

|

|

|

|

|

where and

Following the arguments in Section 4.3 and using Theorem 9.3, we can obtain a similar equation as (4.33):

|

|

|

(9.9) |

Then, using (9.9) and (9.6), as in Proposition 4.11, we can get that

|

|

|

(9.10) |

for a constant depending on only. Again, the proof is the same as the one for Proposition 4.5 in [30], so we omit the details. We also remark that this proof is the only place where we need to use the well-separation condition (2.32).

With (9.9), the problem is once again reduced to showing the CLT of in (4.42). Using Lemma 9.4, we can obtain a similar estimate as in (4.26):

|

|

|

(9.11) |

Thus, similar to (5.4), we can introduce an partial orthogonal matrix such that

|

|

|

(9.12) |

With (9.12) and (9.8), we can check that

|

|

|

where the matrix is defined in (5.7). Thus, to prove Theorem 2.4, it suffices to prove the CLT for . As in Section 8, to avoid singular behaviors of the resolvent on exceptional low-probability events, we will use the regularized resolvent in Definition 6.1 with throughout the rest of the proof. However, for simplicity of notations, we still use the notation to denote the regularized resolvents in the following proof, while keeping in mind that the bound (6.5) holds for all resolvent entries appearing below with , and hence Lemma 4.2 (iii) can be applied without worry. Finally, we remark that the rest of the proof will be conditional on and , i.e., they are regarded as deterministic matrices unless specified otherwise.

Given any random matrices and satisfying Assumption 9.2, we can construct matrices and , whose entries have the first four moments matching those of the entries of and , but with a smaller support .

Lemma 9.5 (Lemma 5.1 of [32]).

Suppose , and satisfy Assumption 9.2. Then, there exist independent random matrices , and satisfying Assumption 9.2,

such that the condition (9.5) holds with replaced by . Moreover, they satisfy the following moment matching conditions:

|

|

|

(9.13) |

Note that , and satisfy the setting of Theorem 2.3. By replacing with in (3.2), (3.3) and (5.7), We can define , and . In Section 8, we have proved the CLT for . The rest of the proof is devoted to showing that has the same asymptotic distribution as .

Proposition 9.6.

Suppose Assumption 9.2 holds. Let and be two random matrices constructed as in Lemma 9.5. Then, there exists a constant such that for any function , we have

|

|

|

To prove this proposition, we will use the continuous comparison method introduced in [31]. We first introduce the following interpolation between and .

Definition 9.7 (Interpolating matrices).

Introduce the notations and . Let and be the laws of and , respectively. For , we define the interpolated law

|

|

|

Let be a collection of random matrices such that for any fixed , is a triple of independent random matrices, and the matrix has law

|

|

|

(9.14) |

Note that we do not require to be independent of for . For , and , we define the matrix through

|

|

|

(9.15) |

In a similar way, we can define a collection of random matrices for with and . We require that for any fixed , is independent of . For , and , we define in the same way as (9.15).

We also introduce the resolvents

|

|

|

Using (9.14) and fundamental calculus, it is easy to derive the following basic interpolation formula.

Lemma 9.8.

For any differentiable function , we have that

|

|

|

(9.16) |

provided all the expectations exist.

We shall apply Lemma 9.8 to for the function in Proposition 9.6, where is defined by replacing with . The main work is to show the following estimate for the right-hand side of (9.16).

Lemma 9.9.

Under the assumptions of Proposition 9.6, there exists a constant such that

|

|

|

(9.17) |

|

|

|

(9.18) |

for all .

Combining Lemma 9.8 and Lemma 9.9, we conclude Proposition 9.6.

The proof of Lemma 9.9 is based on an expansion approach. As in (8.7) and (8.8), for any , , and , we have the resolvent expansion

|

|

|

(9.19) |

where is the matrix defined by as in (8.4). With this expansion, we can readily obtain the following estimate: if is a random variable satisfying , then for any deterministic unit vectors , we have that

|

|

|

(9.20) |

In fact, to prove this estimate, we will apply the expansion (9.19) for a sufficiently large , say , with and , so that . Then, to bound the resulting expansion on the right-hand side of (9.19), we will use , , the anisotropic local law (9.8) for , and the rough bound in (6.5) for in the last term.

Proof Lemma 9.9.

We only give the proof of (9.17), while (9.18) obviously can be proved in the same way.

For simplicity of notations, we only provide the proof for a simpler version of (9.17),

|

|

|

(9.21) |

where is defined as

|

|

|

for some deterministic unit vectors satisfying that

|

|

|

(9.22) |

The proof for (9.17) is the same, except that we need to use multivariable Taylor expansions.

Here, the condition (9.22) is due to the corresponding bound on ,

|

|

|

by (9.12) and the bounded support condition in (9.5).

In the following proof, for simplicity of notations, we fix a and denote while ignoring from the argument. Recall that . Using (9.19) with and the local law (9.20), we get that for a random variable satisfying ,

|

|

|

(9.23) |

where

|

|

|

By (9.20), we have for . On the other hand, for , using (9.20) and (9.22), we can get a better bound

|

|

|

(9.24) |

Combining this bound with , we immediately obtain from (9.23) the rough bound

|

|

|

(9.25) |

Now, fix an integer . Using (9.23) and (9.25), the Taylor expansion of up to the -th order gives that for ,

|

|

|

|

|

|

|

|

|

where means the sum over satisfying

|

|

|

(9.26) |

Here, for the terms with , we have , so they are included into the error.

Now, using the moment matching condition (9.13), we get that

|

|

|

where we used that for . Thus, to show (9.21), we only need to prove that for any fixed and satisfying (9.26),

|

|

|

(9.27) |

for some constant . For the proof of (9.27), we will consider three different cases.

Case 1: Suppose for all . Then, we have and

|

|

|

(9.28) |

On the other hand, using (9.19) with and (9.20), we get that

|

|

|

(9.29) |

Similarly, we have that

|

|

|

(9.30) |

Inserting (9.29) and (9.30) into the definition of , we immediately get that

|

|

|

(9.31) |

We claim that for any deterministic unit vector ,

|

|

|

(9.32) |

We postpone its proof until we complete the proof of Lemma 9.9. Combining (9.28), (9.31) and (9.32), we can bound that

|

|

|

|

|

|

Case 2: Suppose there are at least two ’s such that . Without loss of generality, we assume that for some . Then, we have

, which gives that

|

|

|

(9.33) |

where in the second step we used

|

|

|

Applying (9.29) and (9.30) to (9.24), we can bound that

|

|

|

|

|

|

|

|

(9.34) |

Now, using (9.32) and (9.34), we get that

|

|

|

Combining this bound with (9.33), we get that

|

|

|

Case 3: Finally, suppose there is only one such that . Without loss of generality, we assume that and for . Thus, we have

, which gives that

|

|

|

|

|

|

|

|

|

|

|

|

(9.35) |

where in the first step we used (9.31), and in the second step we used (9.34) and

|

|

|

Applying (9.32) and Cauchy-Schwarz inequality to (9.35), we get that

|

|

|

Combining the above three cases, we conclude (9.27) with , which further implies (9.21). With similar arguments, we can conclude (9.17) and (9.18). ∎

Proof of (9.32).

(9.32) is a simple corollary of the spectral decomposition of the resolvent in (6.51).

Using the rigidity estimate (4.4) given by Theorem 9.3 (iii), we get that

|

|

|

(9.36) |

Combining it with the SVD (6.51), we see that with high probability. Then, using (6.52)–(6.54) and (6.48)–(6.49) given by Theorem 9.3 (iv), we obtain that

with high probability. Thus, we have that for any unit vector ,

|

|

|

(9.37) |

where denotes the conjugate transpose of . If is the regularized resolvent, then we can apply Claim 6.2 to get that

|

|

|

The above argument also works for the resolvent , which concludes (9.32).

∎

Finally, we can complete the proof of Theorem 2.4 using Proposition 9.6.

Proof of Theorem 2.4.

First, suppose , and satisfy Assumption 9.2, and let , and be random matrices constructed in Lemma 9.5. Then, Theorem 2.4 holds for the SCC matrix defined with , because they satisfy the assumptions of Theorem 2.3. By Proposition 9.6 (recall that it is proved for the regularized resolvents following the convention stated above Lemma 9.5), we have that

|

|

|

By the argument in the proof of Claim 6.2, this implies that and also have the same asymptotic distribution. Moreover, by classical CLT, the asymptotic distribution of is still given by (4.41), which only depends on the first four moments of entries. Hence, by (9.10), we can conclude Theorem 2.4 for the SCC matrix defined with satisfying Assumption 9.2. Finally, using the cut-off argument at the beginning of this section and Lemma 9.1, we conclude Theorem 2.4.

∎

Appendix A Proof of Lemma 5.6

In this section, we provide a proof of Lemma 5.6 using the Stein’s method and cumulant expansions. With a slight abuse of notation, we consider the following matrix

|

|

|

where is a random matrix with i.i.d. entries satisfying (2.1) and (2.8),

and are two deterministic matrices satisfying and , and is an deterministic matrix satisfying and

|

|

|

(A.1) |

for some constant . Moreover, we assume that and for a small enough constant . Then, we claim that is asymptotically Gaussian with zero mean. Note that the items (i)–(iv) of Lemma 5.6 all follow from this general claim. In particular, if the entries of are i.i.d. Gaussian, then the condition (A.1) is not necessary, because we can rotate as , where the orthogonal matrix is chosen such that (A.1) holds for and the distribution of is unchanged: .

It is trivial to see that . To show that is asymptotically Gaussian, with the Cramér-Wold device, we need to prove that

|

|

|

is asymptotically Gaussian for any fixed vector of parameters denoted by . For this purpose, we use the Stein’s method [37], i.e. we will show that for any ,

|

|

|

(A.2) |

for some deterministic parameter .

This gives the CLT for , which implies that converges weakly to a centered Gaussian matrix, whose covariances can be determined through .

For simplicity, we denote , such that the entries of are i.i.d. random variables with mean zero and variance one. Moreover, for any fixed , there is a constant such that

|

|

|

(A.3) |

We will prove (A.2) with the following cumulant expansion formula, whose proof can be found in [33, Proposition 3.1] and [28, Section II].

Lemma A.1.

Let for some fixed . Suppose is a centered random variable whose first moments are finite. Let be the -th cumulant of . Then, we have that

|

|

|

(A.4) |

where the error term satisfies that for any ,

|

|

|

(A.5) |

We now expand the left-hand side of (A.2) as

|

|

|

|

|

|

|

|

(A.6) |

We first study the first term on the right-hand side of (A.6). For any fixed , we apply the expansion (A.4) with and to get that

|

|

|

|

|

|

|

|

|

(A.7) |

where is the third cumulant of , satisfies (A.5) for the function , and

|

|

|

(A.8) |

Here, we used (A.1) in the second step. The expectation of the first term on the right-hand side of (A.7) is

|

|

|

|

|

|

(A.9) |

where we used Lemma 5.3 to bound that

|

|

|

(A.10) |

Next, using (A.8) and , we can bound that

|

|

|

|

|

|

|

|

|

(A.11) |

where we used Cauchy-Schwarz inequality in the second step.

Finally, we bound by taking for a small constant . We need to bound

|

|

|

Using the compact support condition of , it is easy to check that

|

|

|

|

|

|

|

|

and

|

|

|

On the other hand, applying Markov’s inequality to (A.3), we obtain the bound

|

|

|

Combining the above three estimates, we obtain that

|

|

|

|

|

|

|

|

|

|

|

|

(A.12) |

where we used (A.1) in the second step. Now, plugging (A.9), (A.11) and (A.12) into (A.7), we obtain that

|

|

|

|

|

|

|

|

|

(A.13) |

Then, we calculate the second term on the right-hand side of (A.6). For any , we need to study

|

|

|

We only consider the hardest case with , and the case can be handled in a similar way. For any fixed , we apply the expansion (A.4) with and to get that

|

|

|

|

|

|

|

|

|

|

|

|

(A.14) |

where is the fourth cumulant of , satisfies (A.5) for the function , and we have abbreviated that

|

|

|

(A.15) |

Using (A.8), we can bound that

|

|

|

|

Similarly, we can get the bounds

|

|

|

|

|

|

On the other hand, with Lemma 5.3, we obtain the estimates

|

|

|

Using these two estimates and (A.10), we get that

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Finally, can be estimated in a similar way as ,

We omit the details of its proof. Combining the above estimates and using Lemma 4.2 (iii), we obtain that

|

|

|

for a deterministic . Combining this equation with (A.13), we obtain (A.2), which concludes Lemma 5.6.