A closed-form approximation for pricing geometric Istanbul options

Abstract

The Istanbul options were first introduced by Michel Jacques in 1997. These derivatives are considered as an extension of the Asian options. In this paper, we propose an analytical approximation formula for a geometric Istanbul call option (GIC) under the Black-Scholes model. Our approximate pricing formula is obtained in closed-form using a second-order Taylor expansion. We compare our theoretical results with those of Monte-Carlo simulations using the control variates method. Finally, we study the effects of changes in the price of the underlying asset on the value of GIC.

keywords:

Options pricing, Istanbul options, Geometric average , First hitting time , Taylor approximation , Control variates1 Introduction

The Istanbul option (IO) is an exotic option whose payoff depends on whether the price of the underlying asset has reached or not a certain threshold previously fixed named barrier. If this barrier is reached before maturity, an Asian option (AO) is activated and the average is calculated from the first moment when the price of the underlying asset reaches the barrier until the maturity. However, if the barrier is not reached, a standard European option (EO) is activated at maturity. The IO can therefore be seen as an hybrid option that has the characteristics of both AO and EO. This option is also similar to the AO with barrier studied by Forsyth and Vetzal (1999) and Hsu et al. (2012), the main difference being that in IO the calculation of the average is activated from the first hitting time of the barrier and not from the acquisition date of the contract.

If we consider a Black and Scholes (1973) model, the valuation of products such as the arithmetic Asian options (AAOs) becomes very difficult since the hypothesis of taking the underlying asset price is a geometric Brownian motion does not allow to obtain a closed-form pricing formula because the distribution of the sum of log-normal random variables is not known in theory. However, the price of AAO can be approximated in practice by Monte-Carlo (MC) simulations with variance reduction techniques (see Zhang (2009), Mehrdoust (2015) and Lu et al. (2019)). It is also possible to approach the price of AAO with a Taylor expansion as in Ju (2014).

For the geometric Asian option (GAO), the pricing formula is known in closed-form (see Kemna and Vorst (1990) for the call and Angus (1999) for more examples of payoffs). Recently, the GAOs with barrier have been studied by Aimi and Guardasoni (2017) and Aimi et al. (2018). The price of this type of options has no closed-form expression and is increasingly the subject of financial research. The options involving a geometric average are also studied in the context of stochastic volatility (for examples, see Wong and Cheung (2004) and Hubalek and Sgarra (2011)).

In Jacques (1997), the arithmetic Istanbul call option (AIC) is study in continuous and discrete time trading. The price of AIC is obtained through a log-normal approximation with the moment-matching method (for more details on this approach, see Levy (1992)). In this article, we focus our attention on the pricing problem of the geometric Istanbul option (GIO) in continuous time trading. We consider only the case of a call option with an up-barrier and a fixed strike price. We also suppose that the terms of the contract do not guarantee any payment of dividend or rebate at maturity.

This article is organized as follows. In section 2, we describe the continuous-time economic model chosen for our study and its theoretical properties. In section 3, we show with the strong Markov property that the price formula of GIC can be written in semi-closed form. Then, we propose an analytic approximation formula of this price using a second-order Taylor expansion. In section 4, we compare our theoretical results with those of MC simulations using the control variates (CV) method to reduce the variance of MC estimator. We also compare the price of GIC with AIC, and analyze the price sensitivity of GIC to changes in the price of the underlying asset. Finally, in section 5, we conclude with a summary of the main results obtained in this article.

2 Financial model description

We consider a standard Black and Scholes model of frictionless markets where there is no arbitrage opportunity, the risk-free interest rate and volatility are constant. The underlying stock price follows a geometric Brownian motion

| (1) |

where is the trading period, is the initial stock price, is the risk-neutral drift rate and a one-dimensional standard Brownian motion under the risk-neutral probability .

In this article, the constant is an up-barrier fixed in the terms of the contract. The first hitting time of by the process is a random variable noted and defined as

| (2) |

We also use the following notations :

and .

and are the Gaussian density and distribution functions, respectively.

and is an indicator function.

The payoff of GIC at maturity can be written as , where is the strike price and is a random variable defined as

| (3) |

From definitions (2) and (3), we can see that the price of geometric Istanbul and geometric Asian call options coincide when . Note that the geometric Istanbul put option whose a payoff at equal to is not priced here. As we will see, our analytical approximation method can be perfectly applied in the case of a put option.

3 Pricing of geometric Istanbul options

According to the risk-neutral pricing formula in continuous time111For more theoretical details and discussions on the general formula for pricing of derivative products under the assumptions of the continuous Black and Scholes model, see Harrison and Pliska (1981)., the price (or ) at time 0 of GIO corresponds to expected value of its discounted payoff at maturity, this price will be noted for call option by . Thus, we have

| (4) |

where is expectation operator under -measure.

The probability distribution of is essential in order to obtain an analytical formula of . We notice that this distribution is known when is not reached before . In this case, the distribution corresponds to the joint distribution of the geometric Brownian motion and its first hitting time of . So, only the distribution when is reached before is unknown and need to be calculated.

For , we have

| (5) |

Let us introduce a process , , defined by . According to the strong Markov property on event , the process is a standard Brownian motion under -measure. This process is started at zero and completely independent of stopping time .

Now we can write

| (6) | ||||

where

| (7) |

is the probability density function of first hitting time of by the process (see formula 2.0.2 in Borodin and Salminen (2002)). Note that the equality (6) follows from the fact that the random variable is Gaussian for with a zero mean and a variance equal to (see Zhang et al. (2015)).

Then, the distribution of when is reached before , is given by the following formula

| (8) |

The derivative of formula (8) with respect to gives

| (9) | ||||

where is an infinitesimal quantity.

Remark 1.

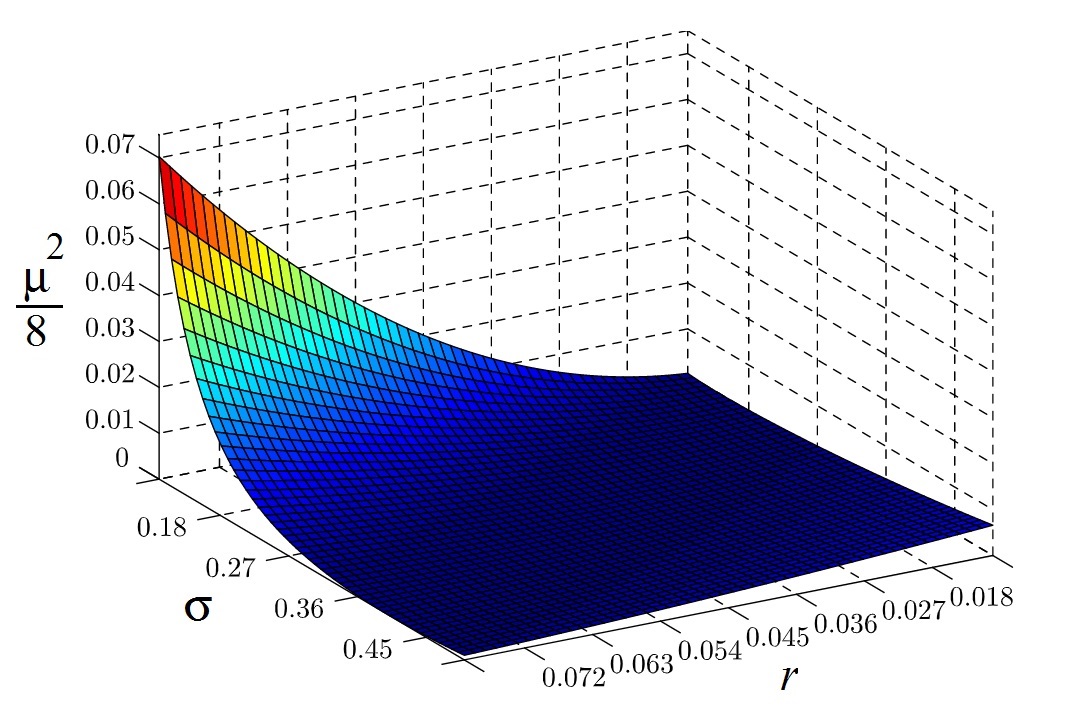

The integral in (9) does not admit a closed-form expression; however, it is possible to approach it numerically with Gaussian quadrature methods (see Brass and Petras (2011)). As illustrated in Figure 1, the quantity is very small for a wide range of parameters and . This observation will allow us to obtain an analytical approximation of (9) using a Taylor series expansion around zero.

Lemma 1.

For , and , if is around zero, then we have

where .

Proof.

See C. ∎

Theorem 1.

Suppose that . We have

| (10) |

where

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

Proof of Theorem 1 1.

We start by rewriting formula (4) as

| (11) |

where is a price of an up-and-out barrier call option at time 0. The first term in (11) is written as follows

| (12) |

Using Lemma 1, we obtain the following approximation

where

and

Since , then has a zero value. It is sufficient to calculate the quantities and with formulas (19) and (20) to have the desired result.

Theorem 2.

Suppose that . We have

| (13) |

where

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

and is a price of an up-and-out barrier call option at time 0.

4 Numerical analysis

In this section, we compare our analytical approximation formulas (10) and (13) with MC simulations. In our simulation procedure, we use the CV as a variance reduction technique of estimator obtained by crude MC method. We analyze two types of simulations errors, namely, the standard error and the relative error noted by S.E. and R.E., respectively. Our calculation algorithms are implemented with R software version 3.5.1 on a PC, Dell, Intel(R) core(TM) i3, 1.70GHZ and running under Windows 8. To simulate the price (4), we start by discretizing the interval into points, , with the discretization step . The simulation of model (1) is given by the following recursion formula

| (14) |

where is i.i.d. standard Gaussian random variables. In order to obtain a realization of the random variable , the time integral in (3) is approximated with trapezoidal rule as follows

| (15) |

where is discret version of first hitting time . The number of paths used in our MC simulations is 10000. We take as a control variate the payoff of a geometric Asian call option (GAC) since the payoff of this option depends on , which gives a high correlation with the payoff of our option. Our controlled estimator for is given by

| (16) |

where and are a crude MC estimators for and respectively and is a parameter that minimizes the variance of .222We take , where and are the payoffs of geometric Istanbul and geometric Asian calls option, respectively. Note that the exact value of is unknown we approximate it using the sample variance and covariance.

In Table 2, we provide a comparison between the approximate price (10) and the one obtained by MC simulations with the CV technique for different input parameters. The results obtained show that our approximation is efficient and could be applied in finance since the relative errors do not exceed . The results in Table 2 also show that the option price increases as approaches . Similarly, for Table 2, the relative errors obtained with formula (13) are all strictly less than . This confirms once again that the price we provide for GIC is stable to changes in input parameters. We also observe from the results in Table 2 that the option price decreases as approaches . It remains to be noted that in both Tables 2 and 2 the option price increases for longer expiration date, which is expected because the price of any type of option depends directly on its time-value.

| Approx. | MCV | R.E. | Approx. | MCV | R.E. | Approx. | MCV | R.E. | |||||

| (S.E.) | (%) | (S.E.) | (%) | (S.E.) | (%) | ||||||||

| Notes: The input parameters are taken as follows: and . We note by ”Approx.” the price of geometric Istanbul call option obtained with formula (10) and by ”MCV” the Monte-Carlo estimator of the price of the same option using the control variates method. We also note by”S.E.” the standard error of MCV and by ”R.E.” the relative error wich is given in percentage with the following formula: . | |||||||||||||

| Approx. | MCV | R.E. | Approx. | MCV | R.E. | Approx. | MCV | R.E. | |||||

| (S.E.) | (%) | (S.E.) | (%) | (S.E.) | (%) | ||||||||

| Notes: The input parameters are taken as follows: and . We note by ”Approx.” the price of geometric Istanbul call option obtained with formula (13) and by ”MCV” the Monte-Carlo estimator of the price of the same option using the control variates method. We also note by”S.E.” the standard error of MCV and by ”R.E.” the relative error wich is given in percentage with the following formula: . | |||||||||||||

In Table 3, we analyze the robustness of approximation formulas (10) and (13) when the maturity date is long. Our analysis consists in adopting the same MC simulations strategy by increasing the maturity each time while fixing all the inputs. The results thus obtained show that the relative errors do not exceed , which means that our analytical approximations remain both stable and efficient for long-term contracts.

| Maturity | 2 | 3 | 4 | 5 | 6 |

| R.E. with approx. formula (10) | 0.8260% | 1.2073% | 1.4955% | 0.4393 | 1.0083% |

| R.E. with approx. formula (13) | 0.4017% | 0.9485% | 1.2925% | 0.7768 | 1.2080% |

| Notes: The maturities are taken in years (first row), we consider contracts with a lifetime ranging from 2 to 6 years. For formula (10) (second row), the input parameters are: , , , and . For formula (13) (third row), the input parameters are: , , , and . | |||||

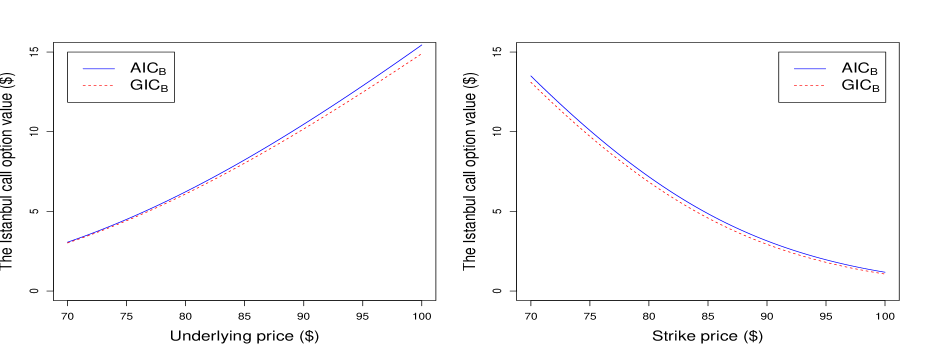

In Figure 2, we compare the price of the GIC to the AIC. As in Jacques (1997), we use the log-normal approximation method to estimate the price in the arithmetic case. For the geometric case, we use our analytical approximation formulas (10) and (13). The numerical results show that a GIC is relatively cheaper than a AIC. We also observe, on the left side of Figure 2, that the price of the Istanbul call option rises when the barrier is close to the current price for both types of averages. This observation is explained by the fact that the closer the barrier is to the current price, the higher the probability that it will be reached, thus increasing the theoretical value of the option. Furthermore, on the right side of Figure 2, we can see that the price of the Istanbul call option decreases as the strike price moves away from the current price, this is due to the fact that the probability of the option expire in-the-money becomes progressively lower as the strike price becomes higher than the current price.

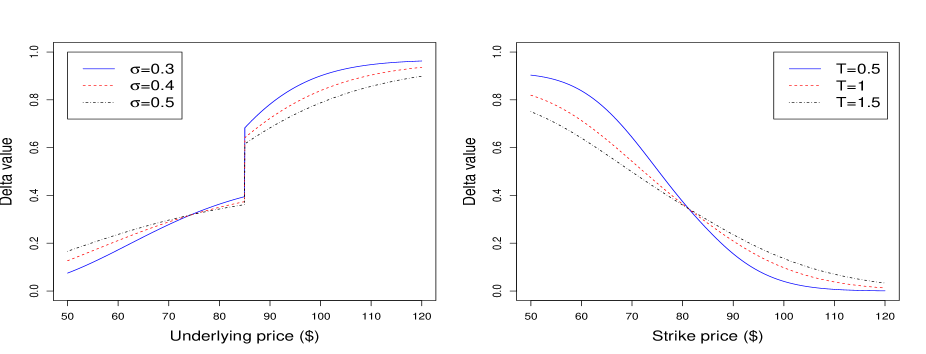

We end this section with a study on the sensitivity of the price of an GIC to changes in the price of the underlying asset. For this purpose, we analyze an important risk measure which is the Delta (). This theoretical quantity is used by options traders to develop good investment strategies.333The Delta is considered by some traders as an approximation of the probability that the option will expire in-the-money. In our case, the of a geometric Istanbul call option corresponds to the partial derivative of (4) with respect to . In Figure 3, on the left side, we calculate the values relative to the price of the underlying asset while increasing the volatility at each plot. On the right side, we fixed the underlying asset and calculate the values relative to the strike price while increasing the maturity at each plot. As shown in Figure 3, the value of depends on three main factors: moneyness, volatility, and maturity. It should be noted that is constantly changing during the trading period and therefore does not predict the maturity value of the underlying asset price.

5 Conclusion

In this paper, we addressed the pricing problem of geometric Istanbul options under the standard Black-Scholes model. A closed-form analytical approximation formula has been proposed for the price of a call option with a fixed strike price. The numerical results obtained by Monte-Carlo simulations using the control variates method have shown that our analytical approximation is very efficient for a wide range of input parameters and can therefore be used in finance. In addition, we have shown through a comparative study that geometric Istanbul call options have a more attractive price compared to those with an arithmetic average treated by Michel Jacques in 1997. Finally, we illustrated, graphically, the price sensitivity of a geometric Istanbul call option to changes in the price of the underlying asset.

Future research on Istanbul options could follow two directions. The first would be to make changes to the input parameters, such as studying the case of a floating strike price, the adoption of a down-barrier or studying the case of a harmonic average. The second interesting approach would be to extend the concept of Istanbul options to more complex economic models such as the exponential Levy model, the CEV model, the Heston model, etc.

Appendix A Some formulas of indefinite integrals of Gaussian functions

| (17) |

where and .

| (18) | ||||

where .

| (19) |

where .

| (20) |

where .

Appendix B A closed-form expressions of two integrals used in this article

| (21) |

where and .

| (22) |

where and .

Appendix C Proof of Lemma 1

By a second-order Taylor series expansion around zero, we have

| (23) |

from equation (23), we have

| (24) |

where

| (25) | |||

| (26) | |||

| (27) |

We start with the evaluation of (25), which can also be written as

| (28) |

thanks to the formula (17), we obtain

For formula (26), we start with the following relationship

| (29) |

by integration with respect to , we obtain

| (30) |

where is a function independent of . The limit of (30) when tends to zero gives

| (31) |

using the formula (21), we get and therefore

Similarly, to obtain a closed-form expression of (27), we note that

| (32) |

The integration with respect to taking and using formula (18) gives

| (33) |

where is a function that depends only on and . The limit of (33) when tends to gives

| (34) |

Using the formula (22), we get and therefore

Finally, it is sufficient to replace the formulas (25), (26) and (27) in (24) to obtain the desired result.

References

- Aimi et al. (2018) Aimi, A., Diazzi, L., Guardasoni, C., 2018. Efficient bem-based algorithm for pricing floating strike asian barrier options (with matlab ® code). Axioms 7, 40.

- Aimi and Guardasoni (2017) Aimi, A., Guardasoni, C., 2017. Collocation boundary element method for the pricing of geometric asian options. Engineering Analysis with Boundary Elements 92.

- Angus (1999) Angus, J.E., 1999. A note on pricing asian derivatives with continuous geometric averaging. Journal of Futures Markets 19, 845–858.

- Black and Scholes (1973) Black, F., Scholes, M., 1973. The pricing of options and corporate liabilities. Journal of Political Economy 81, 637–654.

- Borodin and Salminen (2002) Borodin, A.N., Salminen, P., 2002. Handbook of Brownian motion: facts and formulae. Springer.

- Brass and Petras (2011) Brass, H., Petras, K., 2011. Quadrature Theory: The Theory of Numerical Integration on a Compact Interval. Mathematical surveys and monographs, American Mathematical Society.

- Forsyth and Vetzal (1999) Forsyth, P., Vetzal, K., 1999. Discrete asian barrier options. Journal of Computational Finance 3.

- Harrison and Pliska (1981) Harrison, J., Pliska, S.R., 1981. Martingales and stochastic integrals in the theory of continuous trading. Stochastic Processes and their Applications 11, 215 – 260.

- Hsu et al. (2012) Hsu, W.W.Y., Lu, C., Kao, M., Lyuu, Y., Ho, J., 2012. Pricing discrete asian barrier options on lattices , 1–8.

- Hubalek and Sgarra (2011) Hubalek, F., Sgarra, C., 2011. On the explicit evaluation of the geometric asian options in stochastic volatility models with jumps. Journal of Computational and Applied Mathematics 235, 3355 – 3365.

- Jacques (1997) Jacques, M., 1997. The istanbul option: where the standard european option becomes asian. Insurance: Mathematics and Economics 21, 139–152.

- Ju (2014) Ju, N., 2014. Pricing asian and basket options via taylor expansion. J. Comput. Finance 5.

- Kemna and Vorst (1990) Kemna, A.G.Z., Vorst, A.C.F., 1990. A pricing method for options based on average asset values. Journal of Banking & Finance 14, 113–129.

- Levy (1992) Levy, E., 1992. Pricing european average rate currency options. Journal of International Money and Finance 11, 474 – 491.

- Lu et al. (2019) Lu, K.J., Liang, C.J., Hsieh, M.H., Lee, Y.H., 2019. An effective hybrid variance reduction method for pricing the asian options and its variants. The North American Journal of Economics and Finance .

- Mehrdoust (2015) Mehrdoust, F., 2015. A new hybrid monte carlo simulation for asian options pricing. Journal of Statistical Computation and Simulation 85, 507–516.

- Poularikas (1998) Poularikas, A., 1998. Handbook of Formulas and Tables for Signal Processing. Electrical Engineering Handbook, CRC Press.

- Shreve (2004) Shreve, S.E., 2004. Stochastic calculus for finance 2, Continuous-time models. Springer.

- Wong and Cheung (2004) Wong, H.Y., Cheung, Y.L., 2004. Geometric asian options: valuation and calibration with stochastic volatility. Quantitative Finance 4, 301–314.

- Zhang et al. (2015) Zhang, B., Yu, Y., Wang, W., 2015. Numerical algorithm for delta of asian option. The Scientific World Journal 2015, 692–847.

- Zhang (2009) Zhang, H., 2009. Pricing asian options using monte carlo methods. Uppsala University, Project Report.