Dual Labor Market

and the “Phillips Curve Puzzle”

Abstract

Low inflation was once a welcome to both policy makers and the public. However, Japan’s experience during the 1990’s changed the consensus view on price of economists and central banks around the world. Facing deflation and zero interest bound at the same time, Bank of Japan had difficulty in conducting effective monetary policy. It made Japan’s stagnation unusually prolonged. Too low inflation which annoys central banks today is translated into the “Phillips curve puzzle”. In the US and Japan, in the course of recovery from the Great Recession after the 2008 global financial crisis, the unemployment rate had steadily declined to the level which was commonly regarded as lower than the natural rate or NAIRU. And yet, inflation stayed low. In this paper, we consider a minimal model of dual labor market to explore what kind of change in the economy makes the Phillips curve flat. The level of bargaining power of workers, the elasticity of the supply of labor to wage in the secondary market, and the composition of the workforce are the main factors in explaining the flattening of the Phillips curve. We argue that the changes we consider in the model, in fact, has plausibly made the Phillips curve flat in recent years.

Keywords: Phillips curve; bargaining power; secondary workers.

JEL codes: C60; E31.

1 Introduction

Low inflation was once a welcome to both policy makers and the public. However, Japan’s experience during the 1990’s changed the consensus view on price of economists and central banks around the world; After the financial bubble burst at the beginning of the 1990’s, Japan lapsed into deflation. During the course, the Bank of Japan (BOJ) kept cutting the nominal interest rate down to zero. Facing deflation and zero interest bound at the same time, BOJ had difficulty in conducting effective monetary policy. It made Japan’s stagnation unusually prolonged.

The “Japan problem” made economists aware of long-forgotten danger of deflation. In the prewar period, deflation was a menace to the economy, and its danger was emphasized by famous economists such as Keynes (1931) and Fisher (1933). To prevent deflation, central bank must seek low inflation rather than zero inflation or stable price level. Today, following this idea, many central banks including The US Federal Reserve, BOJ, and European Central Bank target at two percent inflation of consumer price index. However, few central banks have been successful in achieving this goal in any satisfactory way.

Too low inflation which annoys central banks today is translated into the “Phillips curve puzzle”. The benchmark Phillips curve is as follows (Phillips, 1958; Frıedman, 1968):

| (1) |

where and are inflation and the unemployment rate, respectively. is either inflationary expectation or inertia of past inflation. is the natural rate of unemployment or the NAIRU (Non-Accelerating Inflation Rate of Unemployment). According to conventional macroeconomics, Eq. (1) or the Phillips curve determines inflation.

In the US and Japan, in the course of recovery from the Great Recession after the 2008 global financial crisis, the unemployment rate had steadily declined to the level which was commonly regarded as lower than NAIRU, . And yet, inflation stayed low: 0.5% for Japan and 1.5% for the US.

In terms of the Phillips curve, Eq. (1), two things have been pointed out. First, coefficient for inflationary expectations or lagged inflation declined significantly almost to zero in recent years. Blanchard (2018, Figure 7), for example, found that which was almost zero in the early 1960’s, rose sharply to one in the late 1960’s, had stayed there for thirty years, and then declined suddenly to zero at the beginning the 2000’s. While the decline in inflation from the ’90s had been often attributed to better policy management, and even the tern “Great Moderation” was coined (Clarida et al., 2000), more recent analyses identify the anchoring of inflation expectations for the change in the trade-off between inflation and unemployment (Barnichon and Mesters, 2020; Blanchard, 2016). Greenspan (2001) left the following remark: “Price stability is best thought of as an environment in which inflation is so low and stable over time that it does not materially enter into the decisions of households and firms.”

The second factor is a change of coefficient for the unemployment rate in Eq. (1). A decline of entails lower inflation than otherwise when the unemployment rate declines. Some researchers even argue that unemployment no longer has an effect on inflation, at least over some unemployment and inflation range.

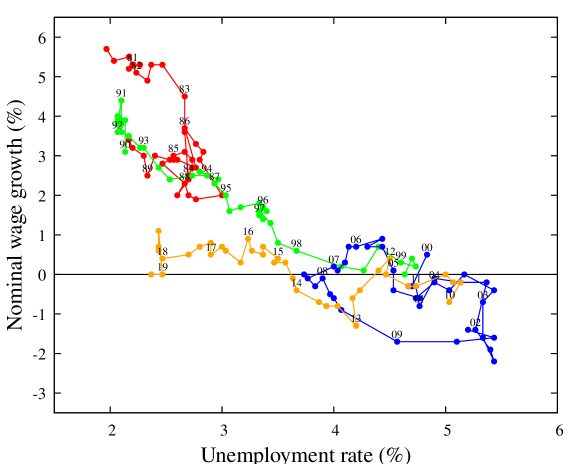

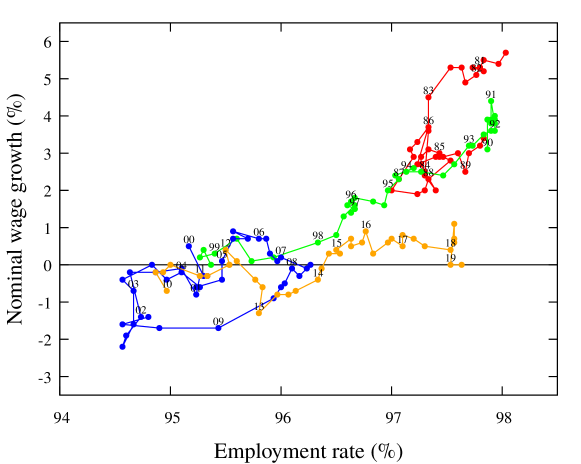

Figure 1 (a) displays Japan’s Phillips curve, namely, the quarterly relation between the unemployment rate and nominal wage growth for 1980.II-2019.II. We can indeed observe that the Phillips curve has flattened in recent years.

(a)

(b)

These are the “Phillips curve puzzle”. In this paper, we leave the first problem untouched: we simply take as zero, and focus on the second problem, namely why gets smaller in Eq. (1). For this purpose, we consider a minimal model of dual labor market (McDonald and Solow, 1981, 1985; Gordon, 2017) to explore what kind of change in the economy makes the Phillips curve flat. In the model, the level of bargaining power of workers, the elasticity of the supply of labor to wage in the secondary market, and the composition of the workforce are the main factors in explaining the flattening of the Philips curve.

Our main contribution is to provide a compact model to jointly consider factors that have been so far mostly investigated separately by the literature. Our main finding is that the change in shape in the relationship between the level of economic activity and inflation can only be explained by the joint effects of these four factors. The structural modifications in the labor market that occurred in Japan over the last three decades have determined the dramatic shift in the relationship between inflation and level of economic activity.

2 The Model

The model assumes a dual labor market consisting of primary labor and secondary workers (McDonald and Solow, 1981, 1985; Gordon, 2017). As inDi Guilmi and Fujiwara (2020), we identify as secondary workers all the employees without a permanent contract (agency, temporary, and part-time).

Firms are heterogeneous in size and efficiency, but adopt the same production function. Each firm produces a homogeneous goods by employing only labor, composed by primary and secondary workers. Specifically, the firm ) employs primary workers with wage and secondary workers with wage . There are primary workers and secondary workers employed.

Primary workers are a fixed endowment for each firm.111The Japanese firm rarely lays off its primary workers. In 2020, for example, in the mid of Covid–19 recession, real GDP fell by unprecedented 28.1%, and yet, the unemployment rate rose slightly only to 2.8%. Accordingly, is a given constant. In contrast, firm freely changes the level of secondary workers. Following the empirical findings of Munakata and Higashi (2016), the wage of secondary workers is determined by the market and is uniform across firms.

The output of firm is determined as follows:

| (2) |

where . is firm-specific total factor productivity (TFP). The parameter quantifies the productivity of secondary labor relative to that of primary labor.

The profit is given by

| (3) |

In order to mimic the firm-level bargaining process that is prevailing in Japan, the primary workers’ wage is set in a two-step process for each employer. Assuming a fixed endowment of primary workers (or insiders) for each firm, in the first stage firm and primary workers determine the number of secondary workers (or outsiders) to be hired. Assuming a perfectly competitive market for secondary workers, firms take the secondary wage as given. Once the number of secondary workers is determined, firms and insiders share the surplus defined by revenue less the wages paid to secondary workers through a Nash bargaining (Mortensen and Pissarides, 1994).

First stage maximization: profit

Firm maximizes its profit (3) by choosing the number of secondary workers or outsiders:

| (4) |

This determines demand for secondary workers of firm as follows:

| (5) |

The total demand for secondary workers in the economy as a whole is then:

| (6) |

where is the following nonlinear sum of :

| (7) |

The level of output of firm is

| (8) |

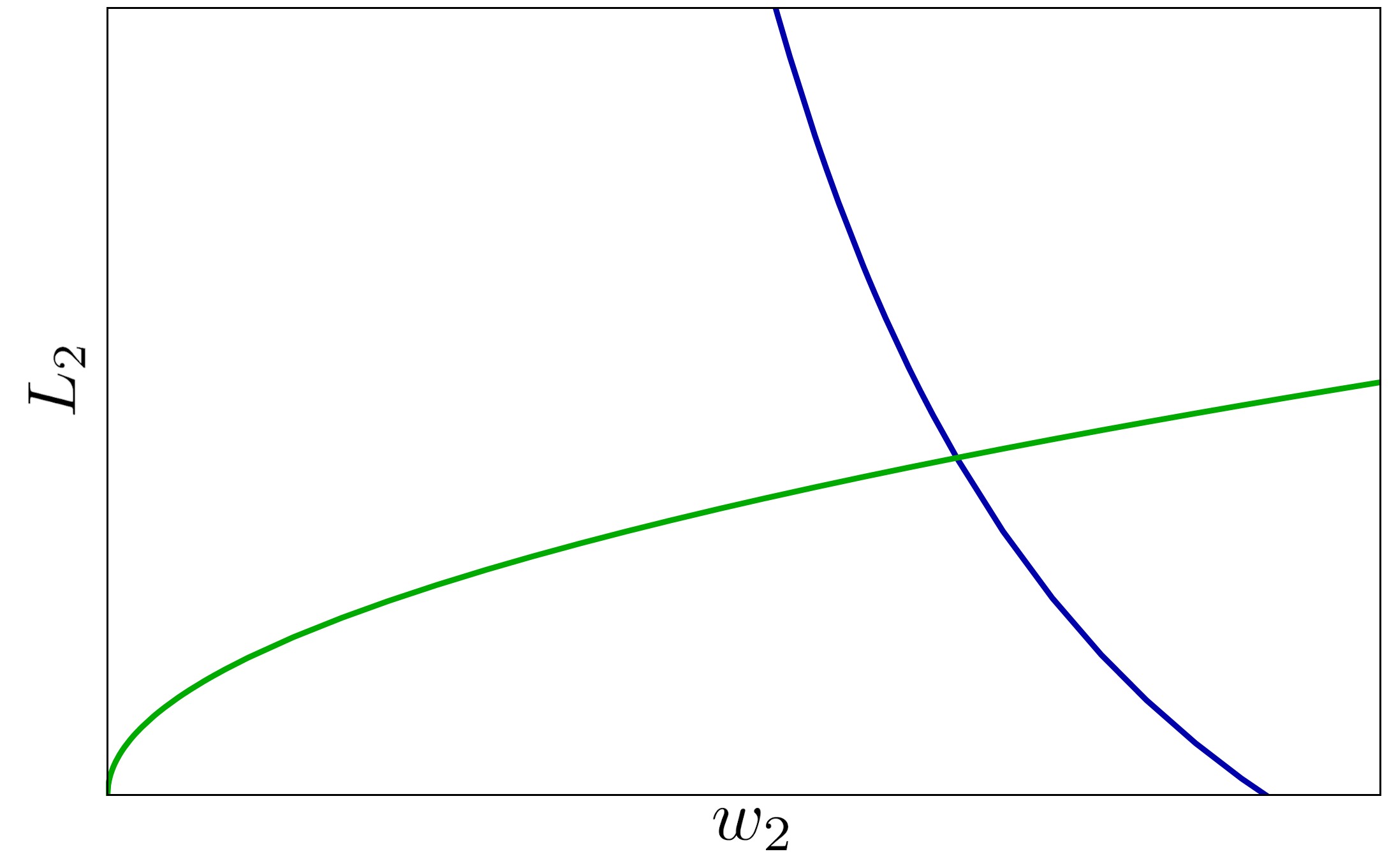

We assume the following supply function of secondary workers :

| (9) |

where is the Frisch elasticity. Matching demand for and supply of secondary workers, , we obtain the following nonlinear equation for :

| (10) |

Demand for and supply of secondary labor as functions of are shown on plane in Fig. 2. It can be shown that the solution of Eq. (10) always exists.

Second stage maximization: primary workers’ wage

Firm and primary workers (insiders) determine the wage of primary workers through a Nash bargaining according to:

| (11) |

where indicates bargaining power of primary workers.

The Nash bargaining determines as follows:

| (12) |

In the following, we study the relationship between the total employment of workers,

| (14) |

and the average wage,

| (15) |

In Eq.(15), is the total earnings of all the workers:

| (16) |

We use the result of the second maximization, Eq.(12). Because and are functions of , we obtain functional relationship between and by eliminating , while keeping other parameters { } fixed. The curve is our Phillips curve, which models the relationship shown in Fig.1(b).

Our Phillips curve is expressed in level of wage (rather than wage inflation) since, as we show below, the rate of change in wage is implied by the wage level.

The parameters and variables of this model are listed in Table 1. The model is extremely parsimonious, with only seven free parameters: . However, because of nonlinearities, its solution is not trivial and able to generate a set of interesting results.

| Output | |

|---|---|

| Nonlinear sum of the total factor productivity (Eq.(7)) | |

| Total number of primary workers | |

| Total number of secondary workers employed (Eq.(5)) | |

| Secondary workers’ productivity coefficient | |

| Output exponent | |

| Supply of secondary workers | |

| Coefficient of labor supply for secondary workers | |

| Elasticity to wage for secondary workers | |

| Nash Bargaining | |

| The wage of the primary workers at firm (Eq. (12)) | |

| The wage of secondary workers (Eq. (10)) | |

| Bargaining power of primary workers | |

3 Solving the Model

Toward the goal of solving the model, we first rewrite Eq.(10) as follows:

| (17) |

By introducing the following scaled variable

| (18) |

we can rewrite Eq.(17) as follows:

| (19) |

where

| (20) |

Recall that solving the model amounts to finding the equilibrium which is equivalent to . Thus, we focus on Eq.(19). We note here that both and are dimensionless quantities in Eq.(19) (see Appendix A). This makes the following analysis straightforward.

With variable , Eqs.(14) and (16) are written as follows:

| (21) | ||||

| (22) |

This leads to the following average wage:

| (23) |

The coefficient is the only factor with the same dimension as . The function is the following dimensionless function of the dimensionless parameters and :

| (24) |

The Phillips curve defined as the relationship between the average wage and employment, , is obtained by eliminating (and ) from Eq. (21) and Eq. (23).

Now, the second term in the parentheses of the right-hand-side of Eq.(19), is the ratio . Therefore, if and measured in efficiency unit are different in order, we may approximate it around the larger term. In other words, if , namely, if the primary workers dominate in efficiency in production, we expand the right hand side around for or equivalently (note that large implies small because of Eq.(20)).

The small- perturbative solution of Eq.(19) is the following:

| (25) |

where . By substituting Eq.(25) into Eqs.(21), (23), and (24), we obtain the followings:

| (26) | ||||

| (27) |

In order to eliminate from these two equations and obtain a relationship between and , we first solve Eq.(26) for small :

| (28) |

Note that this is a perturbative series in . By substituting this expression into Eq.(27), we obtain the following expression of :

| (29) |

Thus, the average wage is a monotonically increasing function of total employment, . Namely, the Phillips curve has the expected sign of slope: it is upward sloping on employment–wage plane, therefore, is downward sloping on wage–unemployment plane. We find from the leading term of this expression that the slope of the curve depends on two key factors, and .

The above analysis assumes . We can make similar analysis in the case of . It is given in Appendix B.

4 Comparative Statics

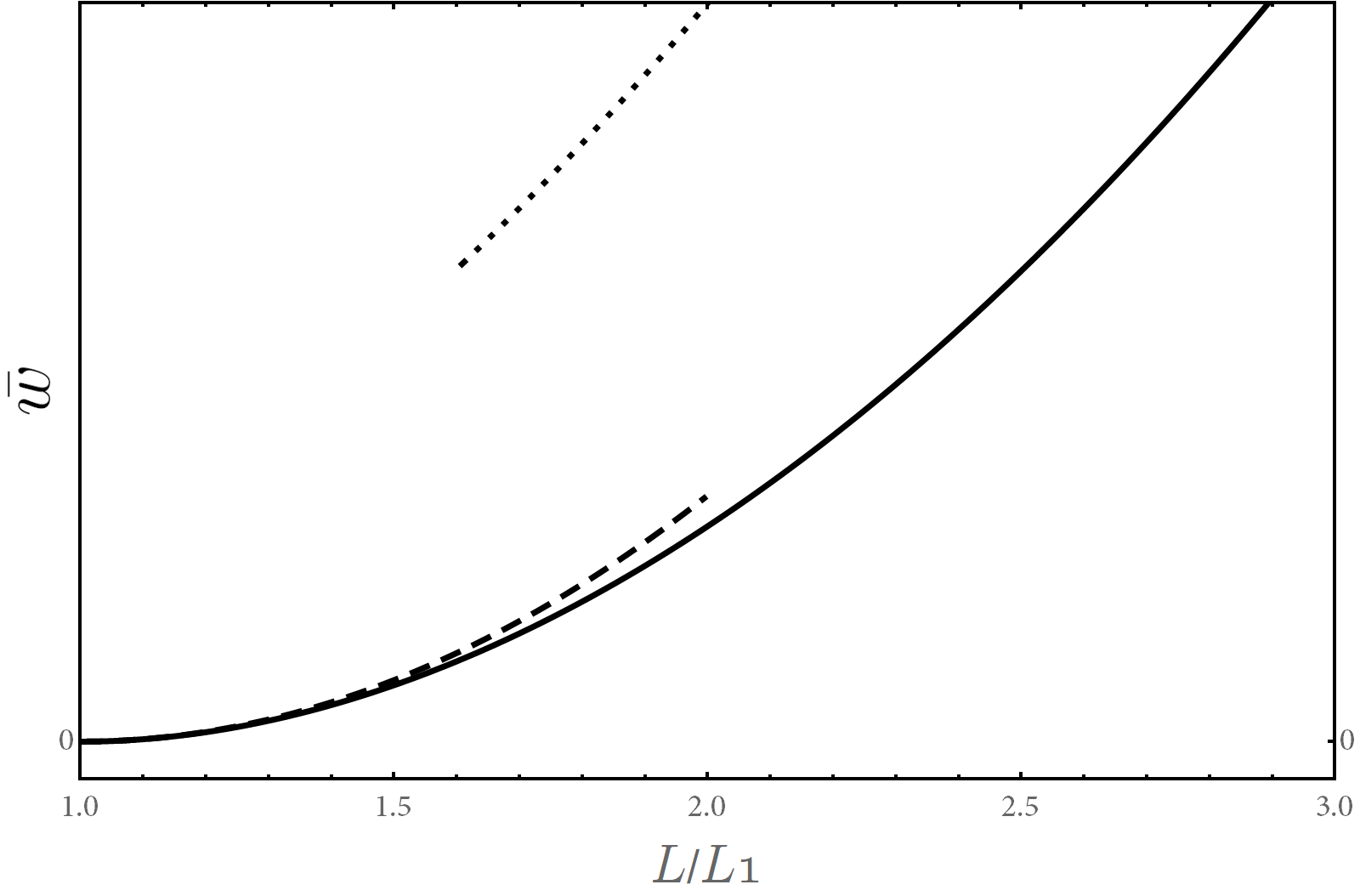

In order to estimate the effects of the parameter, we provide here a numerical comparative statics exercise. For the numerical calculations, the parameters are estimated as follows: (following Di Guilmi and Fujiwara, 2020); (Carluccio and Bas, 2015); (Kuroda and Yamamoto, 2007), while other parameters are calibrated. The Phillips curve is plotted in Fig. 3, where the solid curve is the numerical solution of Eqs. (19), (21), (23) and the dashed and dotted curves are the analytical solutions Eq.(29) and Eq.(43), respectively. We find that the analytical solution (29) for the case when when primary workers are dominant provides a reliable approximation for it mimics well the original function in this range of .

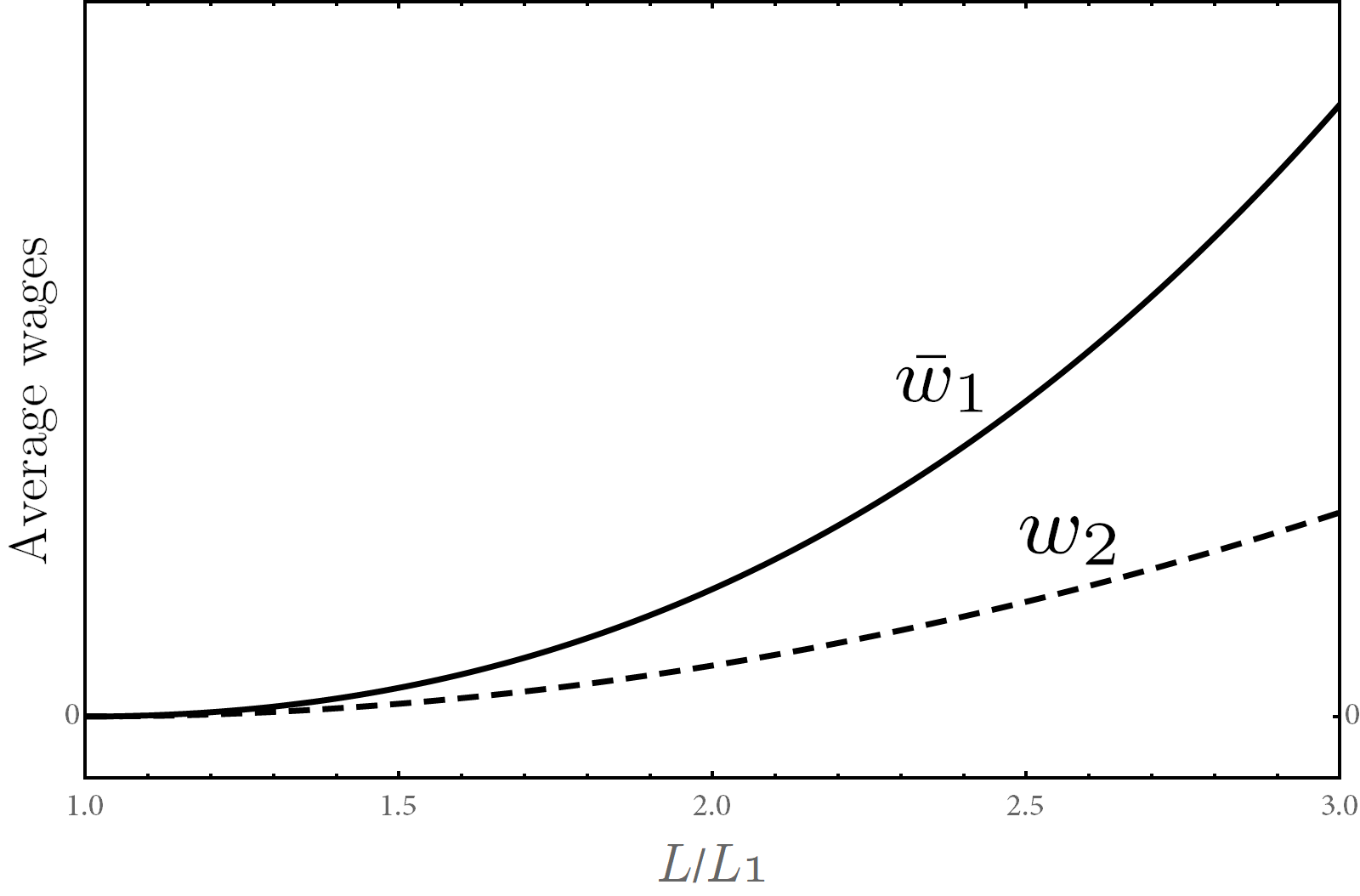

The wages of primary and secondary workers,

| (30) |

and as functions of total employment are shown in Fig. 4. It is interesting to observe that the wages of primary workers determined by Nash bargaining increase more than market–determined wages of secondary workers when the total employment increases.

Our goal is to find the answer for the question why the Phillips curve flattened in recent years. For this purpose, we explore how the slope of Phillips curve depends on parameters , and .

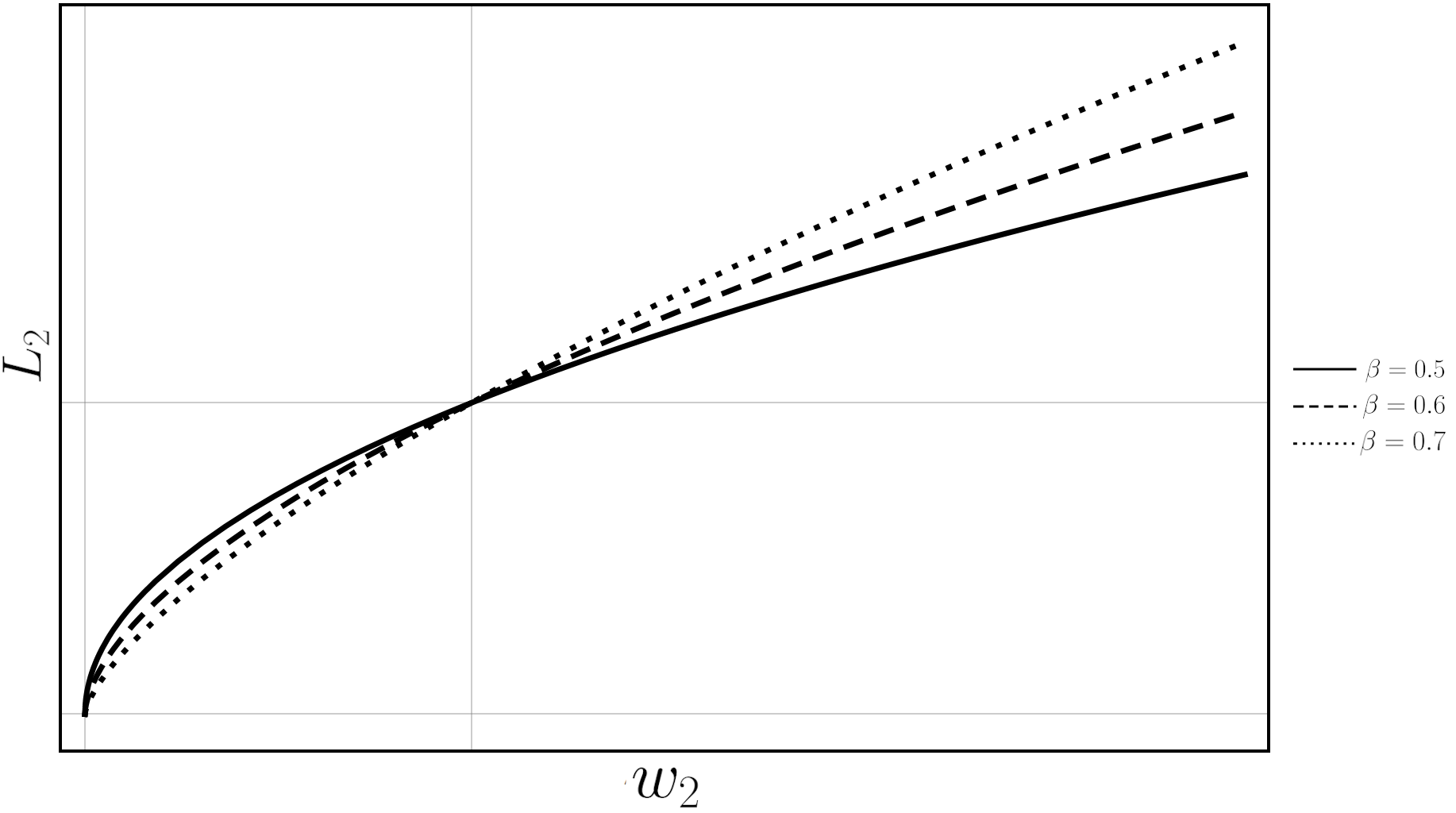

Variations of parameter , however, require careful consideration: in the supply function Eq.(9), the coefficient has a dimension that depends on . Therefore, when changing the value of , keeping the same numerical value of does not make sense. One way of making clear the dimensional consideration is to set so that

| (31) |

Accordingly, the supply function is parametrized by and instead of and . In this parametrization, Eq.(23) is written as follows:

| (32) |

which makes the dimensionality trivial. Using Eq. (32), when varying , we keep constant and vary the value of in in the above equation. This situation is illustrated in Fig. 5.

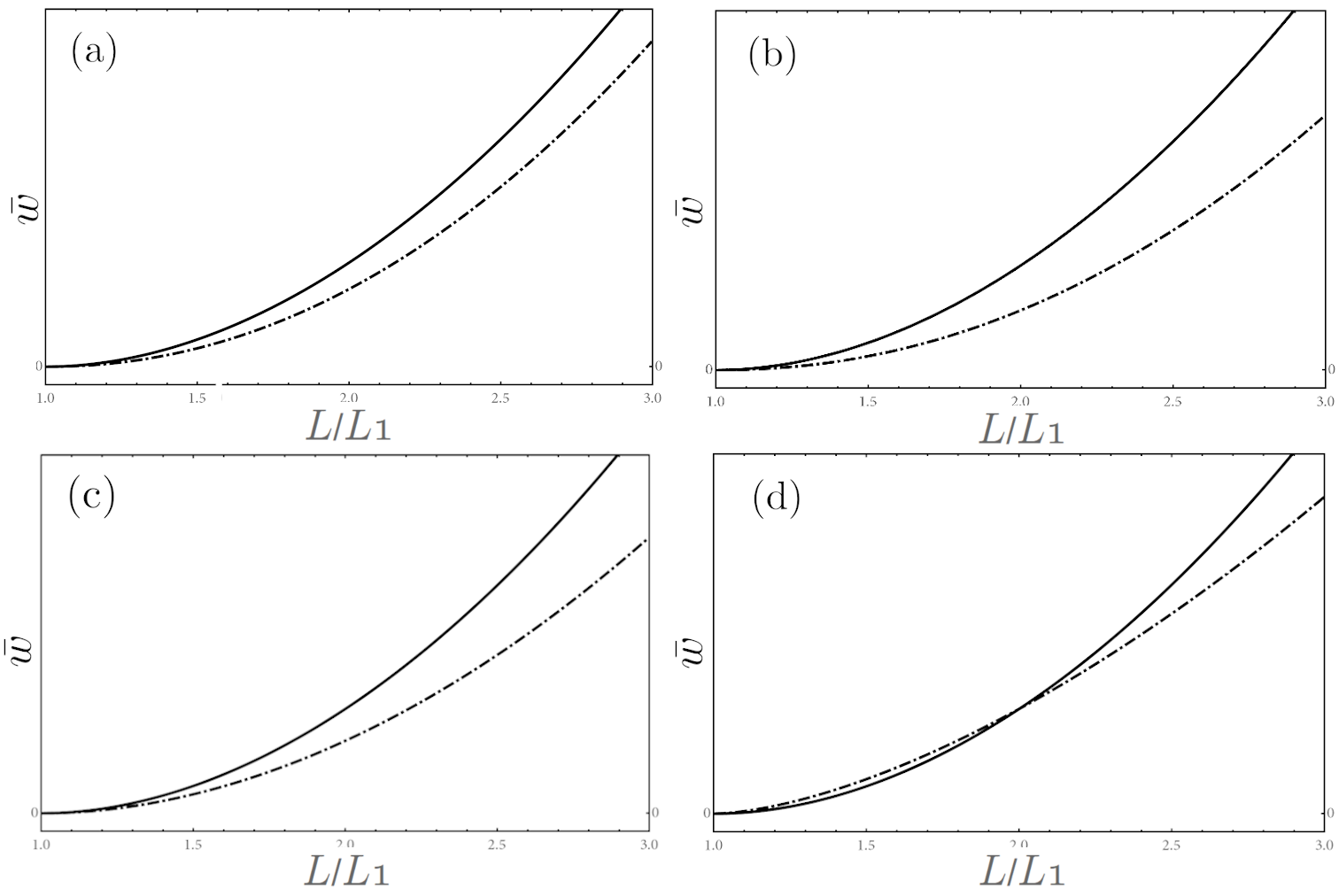

Now, the Philips curve with relatively small changes of the parameters and in the manner explained above are illustrated in Fig. 6 in comparison with the Phillips curve in Fig. 3.

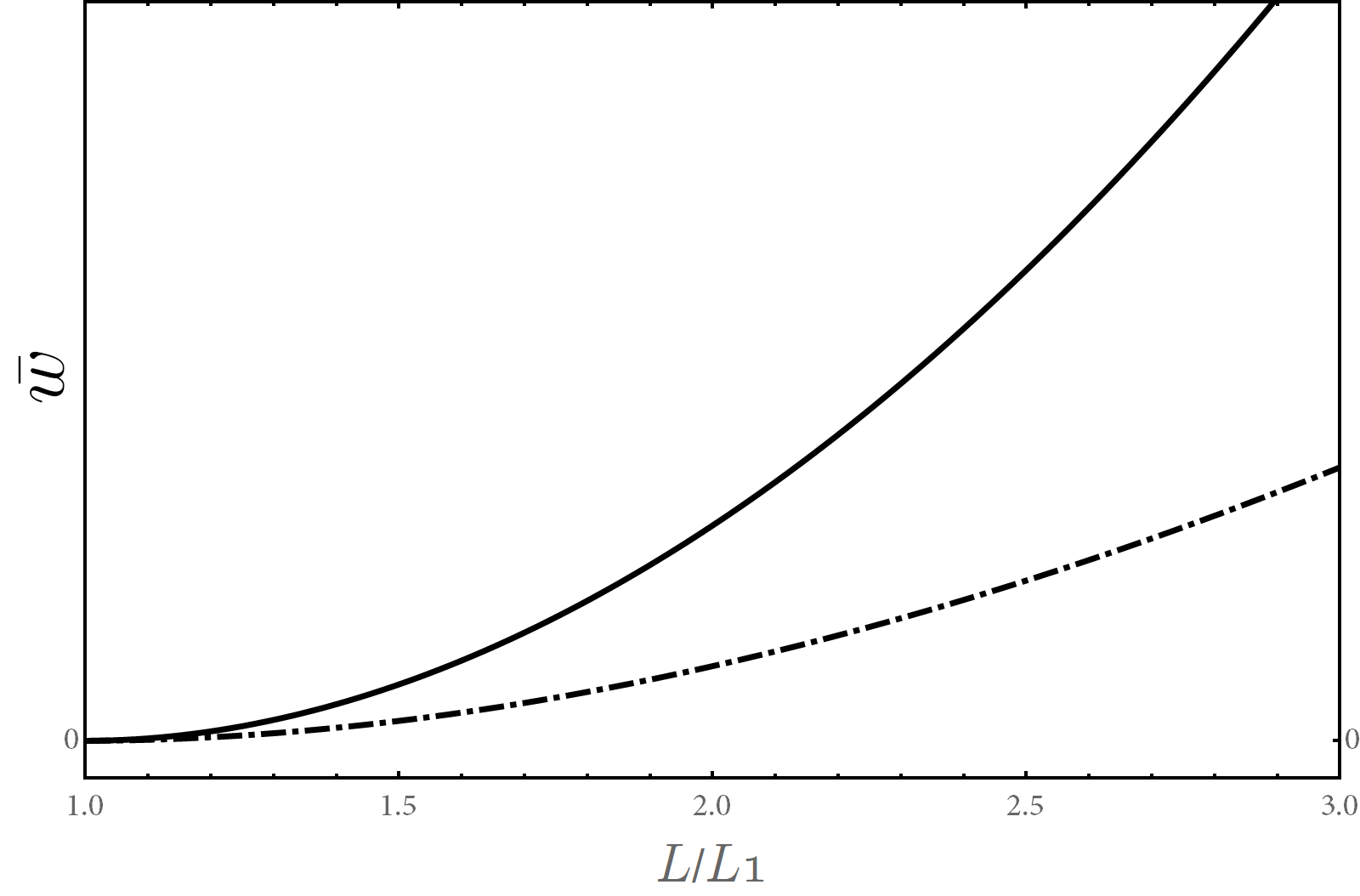

Combining all the effects of changes of four parameters and shown in Fig. 6, we obtain Fig. 7, where we can clearly observe a flattening of the Phillips curve.

5 Discussion

We compare the results obtained in the model with actual data. For this purpose, we focus on the first term in Eq.(29). Take the period 2018–19 (let us denote this time-window as “period II”) when the unemployment rate was about 2.5%, and the nominal wage growth was around 0.5%. The unemployment rate was about 2.5% in the late 80’s (in red in the lower panel of figure 1) to the early 90’s (in green in the lower panel of figure 1, identified as “period I”) but the the nominal wage growth was around 3%. Given 2.5% unemployment rate, the wage growth was lower in period II than in period I by 2,5%: the Philips curve had flattened. We explore how this change is generated in our model.

We first discuss whether the change in the Phillips curve can be explained by varying a single parameter. For example, we want to test whether such a structural change in the curve can be entirely originated by a change in the relative productivity of the two classes of workers. We denote in period I and II by and , respectively. Let us assume that the average wage for one period is given and take one year as the time reference. Taking period I, it increased by 3% next year. In period II, it increases only by 0.5%. Thus the next year’s wage in period II is times that of the next year in period I. This difference can be achieved by increase of the value of by 2.5%, since according to Eq.(29) the average wage is inversely proportional to and . There is no evidence suggesting that productivity of secondary workers had increased that much. Rather, our modes suggests that it is most plausible that the change of the Phillips curve is the result of the combined effects of simultaneous changes in the different parameters. These changes indeed occurred in Japan between period I and period II, as discussed below.

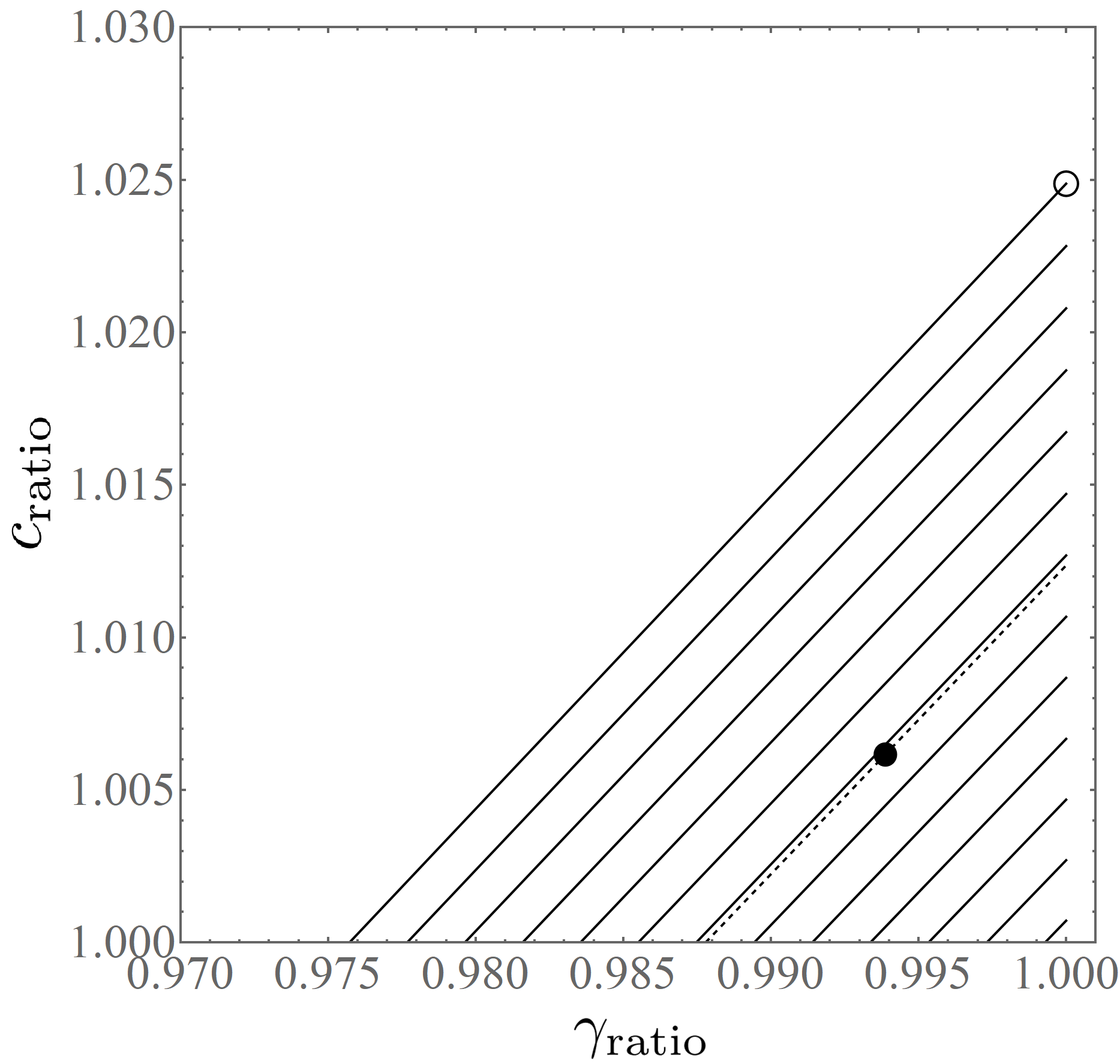

Now, let us discuss how the change between those two periods is explained by simultaneous change in , and , keeping fixed in order to focus on possible structural modifications in the labor market. The ratios of the parameters between two periods (we denote values of parameters in each period with suffix I or II) that explain the change of the wage growth from period I to II satisfy the following:

| (33) |

If we require that the three parameters change by the same ratio, with , we obtain , that is, 0.62% increase in and with 0.61% reduction in . From this we learn that even though change in each parameters is minute, it brings the wage growth down significantly, from 3% to 0.5%. The general solutions to Eq.(33) is illustrated in Fig.8. This computational experiment suggests that the changes in the Japanese Phillips curve should be modeled as a combined effect of relatively marginal changes in the labor market.

The changes of parameters in the model which make the Phillips curve flatter are (1) an increase of productivity of secondary workers relative to primary workers, (2) weaker bargaining power of primary workers, (3) an increase of supply of secondary workers, and (4) an increase of wage elasticity of supply of secondary workers. These are indeed changes which occurred in the Japanese economy over the last thirty years.

The share of secondary or irregular workers in Japan was 15–16% during the late 1980’s, but has steadily increased since then to almost 40% in 2020 (Kawaguchi and Ueno, 2013; Gordon, 2017). After bubble busted at the beginning of the 1990’s, Japanese firms facing unprecedented difficulties had attempted to cut labor cost by replacing highly-paid primary workers with low-wage secondary workers. Historically, secondary workers are considered to have a lower productivity due to less training and lower attachment to the employer (Fukao and Ug Kwon, 2006; Shinada, 2011). However, in face of a dramatic increase in secondary workforce, overall productivity has been mostly stagnant and has not showed the decline that the variation in the proportion of secondary workers would imply. Consequently, in the absence of disaggregated data, it is possible to infer that the relative productivity of secondary workers has improved, reducing the gap with primary workers’ one.

While data about wage elasticity for the different categories of workers are not available, the supply of workers who are more most likely to be employed as secondary has increased, thanks in particular to two factors. First, post-war baby boomers had reached the age of retirement leaving primary jobs and entering secondary labor market. At the same time, in line with what happened in other developed economies, an increase in female participation has created additional availability of workforce, in particular for part-time employment.

The de-unionization of capitalist economies over the last decades is a well-documented phenomenon, which has recently been confirmed by micro-data analysis, as in the cited paper by Stansbury and Summers (2020). However, Japanese unions have faced a higher pressure to restrain wage demand, in comparison to Western economies, in order to limit the loss of jobs following the bust of the double bubble in the stock and real estate markets and the lost decade.

The results have clear policy implications. The inflation target cannot be achieved without structural changes in the labor market, aimed to reverse (or at least to lessen the impact of) the changes discussed above. In particular, the past reforms aimed to make the job market more flexible and the progressive de-unionization observed in virtually all the developed economies should be reconsidered in order to lessen the upward rigidity of wages that is affecting all the employed workforce but especially the secondary workers.

6 Concluding Remarks

The paper presents a parsimonious model of the labor market in which the labor force is composed of temporary and permanent workers. A Phillips curve which includes the structural parameters of the labor market is analytically derived. The slope of the Phillips curve depends on the composition of the workforce, the bargaining power of workers, and the labor supply elasticity to wage of secondary workers. The solution of the model allows for a qualitative assessment of the role of a series of structural change observed in the Japanese economy on the flattening of the Phillips curve.

In terms of policy prescriptions, the results suggest that policy maker cannot achieve target inflation without structural changes in the labor market. The present model can be included in a more comprehensive framework, in order to better highlight the feedback effects among the sluggish dynamic of wages, aggregate demand and demand for labor. Such an extension could be suitable for a more empirically grounded analysis, proving some quantitative assessment on the flattening of the Phillips curve.

Acknowledgements

This study was supported in part by the Project “Macro-Economy under COVID-19 influence: Data-intensive analysis and the road to recovery” undertaken at Research Institute of Economy, Trade and Industry (RIETI), MEXT as Exploratory Challenges on Post-K computer (Studies of Multi-level Spatiotemporal Simulation of Socioeconomic Phenomena), and Grant-in-Aid for Scientific Research (KAKENHI) by JSPS Grant Numbers 17H02041 and 20H02391. We would like to thank Ms. Miyako Ozaki at Research Institute For Advancement of Living Standards for providing us with a part of the data shown in Fig.1.

Appendix A Dimensional Analysis

In this appendix, we discuss the dimensions of various parameters and variables in our model.

Dimensions play important role in various fields of natural science. Basic dimensions in natural science are: Length, Weight, Time and Charge. In any equation that deals with natural quantities, the dimension of the left-hand side has to be equal to the dimension on the right-hand side. For example, “1 [in meter] = 1 [in kilogram]” does not make sense. For this reason, we often learn a lot by simply looking at the dimensions of the constants and variables. This is called “dimensional analysis”.

Also, dimensionless quantities play important roles in analysis: The most famous dimensionless constant is the fine structure constant (in cgs units), where is the unit of electric charge, is the reduced Planck’s constant and is the speed of light. As this quantity is dimensionless, has this value, regardless of whether length is measured in meters or feet, or whether weight is measured in kilogram or pounds, and so on.

Our analysis of the model benefits greatly by the dimensional analysis. Let us examine dimensional properties of quantities in our model. We denote the dimension of the number of workers by , unit of value, like the dollar or yen, by , and time by .

First, the parameters and are dimensionless by their definitions. Dimensions of the fundamental variables are the following:

| (34) | ||||

| (35) | ||||

| (36) |

as is value created per a unit of time (yen per year, for example), are number of workers, and are value per person per time. From these, we find the following dimensions of the parameters:

| (37) | ||||

| (38) |

The former is obtained by the requirement that dimensions of the right-hand side and the left-hand side of Eq.(2) matches, and the latter similarly from Eq.(9). From these, we find that the scaled variable (Eq.(18)) and the parameter (Eq.(20)) are dimensionless. For this reason, the nonlinear equation Eq.(10), which plays a central role in our model but is rather complicated, is simplified to a form much simpler and easier to analyse, Eq.(19).

Appendix B Domination of secondary workers

Large- perturbative solution for Eq.(19) is the following:

| (39) |

This leads to,

| (40) | ||||

| (41) |

The coefficient of the non-leading term in is a complicated function of and , which is not essential for our discussion and is not given here.Perturbative solution of Eq.(40) for is the following:

| (42) |

Note that current assumption is that . Therefore, we find that

| (43) |

where the non-leading term ‘’ is of order of . Again we obtain a monotonically increasing Phillips curve, whose gradient is determined by .

References

- Barnichon and Mesters (2020) Barnichon, R. and Mesters, G. (2020). The phillips multiplier. Journal of Monetary Economics.

- Blanchard (2016) Blanchard, O. (2016). The phillips curve: Back to the ’60s? American Economic Review, 106(5):31–34.

- Blanchard (2018) Blanchard, O. (2018). Should we reject the natural rate hypothesis? Journal of Economic Perspectives, 32(1):97–120.

- Carluccio and Bas (2015) Carluccio, J. and Bas, M. (2015). The impact of worker bargaining power on the organization of global firms. Journal of International Economics, 96(1):162 – 181.

- Clarida et al. (2000) Clarida, R., Galí, J., and Gertler, M. (2000). Monetary Policy Rules and Macroeconomic Stability: Evidence and Some Theory*. The Quarterly Journal of Economics, 115(1):147–180.

- Di Guilmi and Fujiwara (2020) Di Guilmi, C. and Fujiwara, Y. (2020). Dual labor market, inflation, and aggregate demand in an agent-based model of the Japanese macroeconomy. CAMA Working Papers 2020-11, Centre for Applied Macroeconomic Analysis, Crawford School of Public Policy, The Australian National University.

- Fisher (1933) Fisher, I. (1933). The debt-deflation theory of great depressions. Econometrica: Journal of the Econometric Society, pages 337–357.

- Frıedman (1968) Frıedman, M. (1968). The role of monetary policy. American Economic Review, 58(1):1–17.

- Fukao and Ug Kwon (2006) Fukao, K. and Ug Kwon, H. (2006). Why did Japan’s TFP growth slow down in the lost decade? An empirical analysis based on firm-level data of manufacturing firms. The Japanese Economic Review, 57(2):195–228.

- Gordon (2017) Gordon, A. (2017). New and enduring dual structures of employment in japan: The rise of non-regular labor, 1980s–2010s. Social Science Japan Journal, 20(1):9–36.

- Greenspan (2001) Greenspan, A. (2001). Transparency in monetary policy. In Remarks at the Federal Reserve Bank of St. Louis, Economic Policy Conference, St. Louis, Missouri, October 11.

- Kawaguchi and Ueno (2013) Kawaguchi, D. and Ueno, Y. (2013). Declining long-term employment in japan. Journal of the Japanese and International Economies, 28:19–36.

- Keynes (1931) Keynes, J. M. (1931). The consequences to the banks of the collapse of money values (august 1931). In Essays in persuasion. Macmillan.

- Kuroda and Yamamoto (2007) Kuroda, S. and Yamamoto, I. (2007). Estimating Frisch Labor Supply Elasticity in Japan. IMES Discussion Paper Series 07-E-05, Institute for Monetary and Economic Studies, Bank of Japan.

- McDonald and Solow (1981) McDonald, I. M. and Solow, R. M. (1981). Wage Bargaining and Employment. American Economic Review, 71(5):896–908.

- McDonald and Solow (1985) McDonald, I. M. and Solow, R. M. (1985). Wages and Employment in a Segmented Labor Market. The Quarterly Journal of Economics, 100(4):1115–1141.

- Ministry of Health, Labor and Welfare, Japan (2020) Ministry of Health, Labor and Welfare, Japan (2020). Monthly labor Survey. The site is in Japanese. Data: contractual and schedules cash earnings for the establishments with 30 or more employees (quarterly, ratio to the same month of the preceding year).

- Mortensen and Pissarides (1994) Mortensen, D. T. and Pissarides, C. A. (1994). Job creation and job destruction in the theory of unemployment. The Review of Economic Studies, 61(3):397–415.

- Munakata and Higashi (2016) Munakata, K. and Higashi, M. (2016). What Determines the Base Salary of Full-time/Part-time Workers? Bank of Japan Review Series 16-E-11, Bank of Japan.

- Phillips (1958) Phillips, A. W. (1958). The relation between unemployment and the rate of change of money wage rates in the united kingdom, 1861–1957. Economica, 25(100):283–299.

- Shinada (2011) Shinada, N. (2011). Quality of Labor, Capital, and Productivity Growth in Japan: Effects of employee age, seniority, and capital vintage. Discussion papers 11036, Research Institute of Economy, Trade and Industry (RIETI).

- Stansbury and Summers (2020) Stansbury, A. and Summers, L. H. (2020). The declining worker power hypothesis: An explanation for the recent evolution of the american economy. Technical report, National Bureau of Economic Research.

- Statistics Bureau of Japan (2020) Statistics Bureau of Japan (2020). Labor Forth Survey. The site is in Japanese. Data: unemployment rate (monthly, seasonally adjusted, average over each quarters).