Time-uniform central limit theory

and asymptotic confidence sequences

Abstract

Confidence intervals based on the central limit theorem (CLT) are a cornerstone of classical statistics. Despite being only asymptotically valid, they are ubiquitous because they permit statistical inference under very weak assumptions, and can often be applied to problems even when nonasymptotic inference is impossible. This paper introduces time-uniform analogues of such asymptotic confidence intervals. To elaborate, our methods take the form of confidence sequences (CS) — sequences of confidence intervals that are uniformly valid over time. CSs provide valid inference at arbitrary stopping times, incurring no penalties for “peeking” at the data, unlike classical confidence intervals which require the sample size to be fixed in advance. Existing CSs in the literature are nonasymptotic, and hence do not enjoy the aforementioned broad applicability of asymptotic confidence intervals. Our work bridges the gap by giving a definition for “asymptotic CSs”, and deriving a universal asymptotic CS that requires only weak CLT-like assumptions. While the CLT approximates the distribution of a sample average by that of a Gaussian at a fixed sample size, we use strong invariance principles (stemming from the seminal 1960s work of Strassen and improvements by Komlós, Major, and Tusnády) to uniformly approximate the entire sample average process by an implicit Gaussian process. As an illustration of our theory, we derive asymptotic CSs for the average treatment effect using efficient estimators in observational studies (for which no nonasymptotic bounds can exist even in the fixed-time regime) as well as randomized experiments, enabling causal inference that can be continuously monitored and adaptively stopped.

toc

1 Introduction

The central limit theorem (CLT) is arguably the most widely used result in applied statistical inference, due to its ability to provide large-sample confidence intervals (CI) and -values in a broad range of problems under weak assumptions. Examples include (a) nonparametric estimation of means, such as population proportions, (b) maximum likelihood and other M-estimation problems [58], and (c) modern semiparametric causal inference methodology involving (augmented) inverse propensity score weighting [44, 56, 24, 8]. Crucially, in some of these problems such as doubly robust estimation in observational studies, nonasymptotic inference is typically not possible, and hence the CLT yields asymptotic CIs for an otherwise unsolvable inference problem.

While the CLT makes efficient statistical inference possible in a broad array of problems, the resulting CIs are only valid at a prespecified sample size , invalidating any inference that occurs at data-dependent stopping times, for example under continuous monitoring. CIs that retain validity in sequential environments are known as confidence sequences (CS) [10, 41] and can be used to make decisions at arbitrary stopping times (e.g. while adaptively sampling, continuously peeking at the data, etc.). CSs are an inherently nonasymptotic notion, and thus essentially every published CS is nonasymptotic, including the recent state-of-the-art [19, 17, 65].

This paper presents a new notion: an “asymptotic confidence sequence”. For the familiar reader, this might at first seem almost paradoxical, like an oxymoron. Further, it is not obvious how to posit a definition that is simultaneously sensible and tractable, meaning whether it is possible to develop such asymptotic CSs (whatever it may mean). We believe that we have formulated the “right” definition, because we accompany it with a universality result that parallels the CLT — a universal asymptotic CS that is valid under the exact same moment assumptions required by the CLT. This enables the construction of asymptotic CSs in a huge number of new situations where the distributional assumptions are weak enough to remain out of the reach of nonasymptotic techniques even in fixed-time settings. The width of this universal asymptotic CS scales with the variance of the data, just like the empirical variance used in the CLT — such variance-adaptivity is only achievable for nonasymptotic methods in very specialized settings [65].

Before proceeding, let us first briefly review some notation and key facts about CSs.

1.1 Time-uniform confidence sequences (CSs)

Consider the problem of estimating the population mean from a sequence of iid data that are observed sequentially over time. A nonasymptotic -CI for is a set111We use overhead dots to denote fixed-time (pointwise) CIs and overhead bars to denote time-uniform CSs. with the property that

| (1) |

The coverage guarantee (1) of a CI is only valid at some prespecified sample size , which must be decided in advance of seeing any data — peeking at the data in order to determine the sample size is a well known form of “-hacking”. However, it is restrictive to fix beforehand, and even if clever sample size calculations are carried out based on prior knowledge, it is impossible to know a priori whether will be large enough to detect some signal of interest: after collecting the data, one may regret collecting too little data or collecting much more than would have been required.

CSs provide the flexibility to choose sample sizes data-adaptively while controlling the type-I error rate (see Fig. 1). Formally, a CS is a sequence of CIs such that

| (2) |

The statements (1) and (2) look similar but are markedly different from the data analyst’s or experimenter’s perspective. In particular, employing a CS has the following implications:

-

(a)

The CS can be (optionally) updated whenever new data become available;

-

(b)

Experiments can be continuously monitored, adaptively stopped, or continued;

-

(c)

The type-I error is controlled at all stopping times, including data-dependent times.

In fact, CSs may be equivalently defined as CIs that are valid at arbitrary stopping times, i.e.

| (3) |

A proof of the equivalence between (2) and (3) can be found in Howard et al. [19, Lemma 3].

As mentioned before, while nonparametric CSs have been developed for several problems, they have thus far been nonasymptotic. Nonasymptotic inference for means of random variables requires strong assumptions on the distribution of the data [1]. These assumptions often take the form of a parametric likelihood [64, 17], known bounds on the random variables themselves [19, 65], on their moments [63], or on their moment generating functions [19].

These added distributional assumptions make existing CSs to be quite unlike CLT-based CIs which (a) are universal, meaning they take the same form — up to a change in influence functions — and are computed in the same way for most problems, and (b) are often applicable even when no nonasymptotic CI is known, such as in doubly robust inference of causal effects in observational studies. Our work bridges this gap, bringing properties (a) and (b) to the anytime-valid sequential regime by making one simple modification to the usual CIs. Just as CLT-based CIs yield approximate inference for a wide variety of problems in fixed- settings, our paper yields the same for sequential settings.

1.2 Contributions and outline

The primary contributions of this paper are in rigorously defining “asymptotic confidence sequences” (AsympCSs) in Definition 2.1 and deriving explicit constructions thereof which are as easy to implement and apply as the CLT. Additionally, we develop a Lindeberg-type asymptotic CS that is able to capture time-varying means under martingale dependence (Section 2.4). In Section 2.5, we give a definition of asymptotic time-uniform coverage (akin to coverage of asymptotic CIs) and show how sequences of our AsympCSs have this property. In Section 3 we illustrate how the asymptotic CSs of Section 2.1 enable anytime-valid doubly robust inference of causal effects in both randomized experiments and observational studies (Section 3). To be clear, we are not focused on deriving new semiparametric estimators; we simply demonstrate how doubly robust causal inference — a problem for which no known CSs exist — can now be tackled in fully sequential environments using the existing state-of-the-art estimators combined with our time-uniform bounds (Theorems 3.1 and 3.2). In Section 4, we provide a simulation study to assess empirical widths and type-I error rates of our asymptotic CSs and compare them to some existing (nonasymptotic) CSs in the literature. Finally, we apply the asymptotic CSs of Section 3 to a real observational data set by sequentially estimating the effects of fluid intake on 30-day mortality in sepsis patients. In sum, this work greatly expands the scope of anytime-valid inference, and does so via technically nontrivial derivations.

2 Time-uniform central limit theory

We first define what it means for a sequence of intervals to form an asymptotic confidence sequence (AsympCS). Then, we derive a “universal” AsympCS222We use the term universal in the same way that the CLT and the law of large numbers are considered universality results [52], as they describe macroscopic behaviors that are independent of most microscopic details of the system. in the sense that the AsympCS does not depend on any features of the distribution beyond its mean and variance. This universal AsympCS is fundamentally related to Gaussians — much like classical asymptotic confidence intervals based on the CLT — since it stems from Brownian motion approximations and so-called strong invariance principles. Finally, similar to CIs based on martingale CLTs, we derive a Lindeberg-type martingale AsympCS that can track a moving average of conditional means.

2.1 Defining asymptotic confidence sequences

As mentioned in Section 1, the literature on CSs has focused on the nonasymptotic regime where strong assumptions must be placed on the observed random variables, such as boundedness, a parametric likelihood, or upper bounds on their MGFs. On the other hand, in batch — i.e. fixed-time — statistical analyses, the CLT is routinely applied to obtain approximately valid CIs in large samples, as it requires weak finite moment assumptions and has a simple, universal closed-form expression. Here, we define and present “asymptotic confidence sequences” as time-uniform analogues of asymptotic CIs, making similarly weak moment assumptions and providing a universal closed-form boundary.

The term “asymptotic confidence sequence” may at first seem paradoxical. Indeed, ever since their introduction by Robbins and collaborators [10, 42, 28, 29], CSs have been defined nonasymptotically, satisfying the time-uniform guarantee in equation (2). So how could a bound be both time-uniform and asymptotically valid? We clarify this critical point soon, with an analogy to classical asymptotic CIs. Similar to asymptotic CIs, AsympCSs trade nonasymptotic guarantees for (a) simplicity and universality, and (b) the ability to tackle a much wider variety of problems, especially those for which there is no known nonasymptotic CS. Said differently, AsympCSs trade finite sample validity for versatility (exemplified in Section 3 with a particular emphasis on modern causal inference).

Indeed, there is a clear desire for time-uniform methods with CLT-like simplicity and versatility, especially in the context of causal inference. For example, Johari et al. [21, Section 4.3] use a Gaussian mixture sequential probability ratio test (SPRT) to conduct A/B tests (i.e. randomized experiments) for data coming from (non-Gaussian) exponential families and mentions that CLT approximations hold at large sample sizes. Similarly, Yu et al. [66] develop a mixture SPRT for causal effects in generalized linear models, where they say that their likelihood ratio forms an “approximate martingale”, meaning its conditional expectation is constant up to a factor of . Moreover, Pace and Salvan [34] suggest using Robbins’ Gaussian mixture CS as a closed-form “approximate CS” and they demonstrate through simulations that the time-uniform coverage guarantee tends to hold in the asymptotic regime. However, all of these approaches justify time-uniform inference with approximations that only hold at a fixed, pre-specified sample size, and yet inferences are being carried out at data-dependent sample sizes. This section remedies the tension between fixed- approximations and time-uniform inference by defining AsympCSs such that Gaussian approximations must hold almost surely for all sample sizes simultaneously. The AsympCSs we define will also be valid in a wide range of nonparametric scenarios (beyond exponential families, parametric models, and so on).

To motivate the definition of an AsympCS that follows, let us briefly review the CLT in the batch (non-sequential) setting. Suppose with mean and variance . Then the standard CLT-based CI for takes the form

| (4) |

where is the sample mean and is the -quantile of a standard Gaussian (e.g. for , we have ). The classical notion of “asymptotic validity” is

| (5) |

While the above is the standard definition of an asymptotic CI, we can arrive at a different definition by noting that a stronger statement can be made under the same conditions. Indeed, there exist333Technically, writing (6) may require enriching the probability space so that both and can be defined (but without changing their laws). See Einmahl [14, Equation (1.2)] for a precise statement. iid standard Gaussians such that

| (6) |

Thus, one could define to be an asymptotic -CI if there exists some (unknown) nonasymptotic -CI such that

| (7) |

Statements of the form (6) are known as “couplings” and appear in the literature on strong approximations and invariance principles [14, 26, 27]. While justifications and derivations of CLT-based CIs like (4) are not typically presented using couplings, it is indeed the case that (6) implies the classical asymptotic validity guarantee (5). However, we deliberately highlight the alternative definition of asymptotic CIs because it ends up serving as a more natural starting point for defining asymptotic confidence sequences. In particular, we will define asymptotic CSs so that the approximation (7) holds uniformly over time, almost surely (though we do so using a slightly more general setup).

Definition 2.1 (Asymptotic confidence sequences).

Let be a totally ordered infinite set including a minimum value . We say that is a -asymptotic confidence sequence (AsympCS) for a sequence of parameters if there exists a (typically unknown) nonasymptotic -CS for — i.e. satisfying

| (8) |

and such that becomes an arbitrarily precise almost-sure approximation to :

| (9) |

In words, Definition 2.1 says that an AsympCS is an arbitrarily precise approximation of some nonasymptotic CS as — capturing the intuition of having a time-uniform validity in large samples. Throughout the paper, we will mostly focus on the case where and .

It is important to note that alternate definitions to ours fail to be coherent in different ways. As one example, we could have hypothetically defined a sequence of intervals to be a -AsympCS if , analogously to asymptotic CIs which satisfy . In words, we could have posited that if we just start peeking late enough, then the probability of eventual miscoverage would indeed be below . Unfortunately, even for nonasymptotic CSs constructed at any level , the former limit is zero, so this inequality would be vacuously true, regardless of , even if . (Ideally, a nonasymptotic CS should also be an -AsympCS for any , but not an asymptotic -AsympCS for every .) However, we do show that sequences of our AsympCSs have a guarantee of this type if peeking starts late enough (see Section 2.5), but we delay these definitions until later as they are more involved.

Remark 1 (Why almost surely?).

One may wonder why it is necessary to define AsympCSs so that almost surely (rather than in probability, for example). Since CSs are bounds that hold uniformly over time with high probability, convergence in probability is not the right notion of convergence, as it only requires that the approximation term be small with high probability for sufficiently large fixed , but not for all uniformly. It is natural to try to extend convergence in probability to time-uniform convergence with high probability — i.e. — but it turns out (Section B.3) that this is equivalent to almost-sure convergence .

Going forward, we may omit “a.s.” from and and instead simply write and , respectively to simplify notation. Now that we have defined AsympCSs as time-uniform analogues of asymptotic CIs, we will explicitly derive AsympCSs for the mean of iid random variables with finite variances (i.e. under the same assumptions as the CLT).

2.2 Warmup: AsympCSs for the mean of iid random variables

We now construct an explicit AsympCS for the mean of iid random variables by combining a variant of Robbins’ (nonasymptotic) Gaussian mixture boundary [41] with Strassen’s strong approximation theorem [50]. Before presenting the main result, let us review both Robbins’ boundary and Strassen’s result, and discuss how they can be used in conjunction to arrive at the AsympCS in Theorem 2.2.

2.2.1 Robbins’ Gaussian mixture boundary

The study of CSs began with Herbert Robbins and colleagues [10, 41, 42, 28, 29], leading to several fundamental results and techniques including the famous Gaussian mixture boundary for partial sums of iid Gaussian random variables [41] (see also Howard et al. [19, §3.2]) which we recall here. Suppose are iid standard Gaussian random variables. Then for any ,

| (10) |

Notice that the above boundary scales as for any . In fact, Robbins [41, Eq. 11] noted that (10) holds not only for Gaussian random variables, but for those that are -sub-Gaussian, and hence pre-multiplying the boundary by yields a -sub-Gaussian time-uniform concentration inequality, serving as a time-uniform analogue of Chernoff or Hoeffding inequalities. The connections between these fixed-time and time-uniform concentration inequalities are made explicit in Howard et al. [19]. Nevertheless, Eq. 10 requires a priori knowledge of unlike CLT-based CIs which we aim to emulate in the time-uniform regime. The following strong Gaussian approximation due to Strassen [50] will serve as a technical tool allowing the nonasymptotic sub-Gaussian bound in (10) to be applied to partial sums of arbitrary random variables with finite variances.

2.2.2 Strassen’s strong approximation

Strassen [50] initiated the study of strong approximation (also called strong invariance principles or strong embeddings) which blossomed into an active and impactful corner of probability theory research over the subsequent years, culminating in now-classical results such as the Komlós-Major-Tusnády embeddings [26, 27, 31] and other related works [51, 13, 32, 7].

In his 1964 paper, Strassen [50, §2] used the Skorokhod embedding [49] (see also [4, p. 513]) to obtain the following strong invariance principle which connects asymptotic Gaussian behavior with the law of the iterated logarithm. Concretely, let be an infinite sequence of iid random variables from a distribution with mean and variance . Then on a potentially richer probability space,444A richer probability space may be needed to describe Gaussian random variables, if for example, are -valued on a probability space with whose probability measure is dominated by the counting measure. This construction of a richer probability space imposes no additional assumptions on , and is only a technical device used to rigorously couple two sequences of random variables, and appears in essentially all papers on strong invariance principles, not just Strassen [50]. there exist standard Gaussian random variables whose partial sums are almost-surely coupled with those of up to iterated logarithm rates, i.e.

| (11) |

Notice that the law of the iterated logarithm states that while (11) states that the same partial sum is almost-surely coupled with an implicit Gaussian process — i.e. replacing with . It may be convenient to divide by and interpret (11) on the level of sample averages rather than partial sums, in which case the right-hand side becomes . Let us now describe how Strassen’s strong approximation can be combined with Robbins’ Gaussian mixture boundary to derive an AsympCS under finite moment assumptions akin to the CLT.

2.2.3 The Gaussian mixture asymptotic confidence sequence

Given the juxtaposition of (10) and (11), the high-level approach to the derivation of AsympCSs becomes clearer. Indeed, the essential idea behind Theorem 2.2 is as follows. By Strassen’s strong approximation, we couple the partial sums with implicit partial sums of Gaussians , and then use Robbins’ mixture boundary to obtain a time-uniform high-probability bound on the deviations of , noting that the coupling rate is asymptotically dominated by the concentration rate , leading to asymptotic validity in the formal sense of Definition 2.1.

Theorem 2.2 (Gaussian mixture asymptotic confidence sequence).

Suppose is an infinite sequence of iid observations from a distribution with mean and finite variance. Let be the sample mean, and the sample variance based on the first observations. Then, for any prespecified constant ,

| (12) |

forms a -AsympCS for .

The full proof of Theorem 2.2 can be found in Appendix A.1. We can think of as a user-chosen tuning parameter which dictates the time at which (12) is tightest, and we discuss how to easily tune this value in Section B.2. A one-sided analogue of (12) can be found in Section B.1.

While (12) may look visually similar to Robbins’ (sub)-Gaussian mixture CS [41] — written explicitly in Howard et al. [19, Eq. (14)] — it is worth pausing to reflect on how they are markedly different. Firstly, Robbins’ CS is a nonasymptotic bound that is only valid for -sub-Gaussian random variables, meaning for some a priori known , while Theorem 2.2 does not require the existence of a finite MGF at all (much less a known upper bound on it). Secondly, Robbins’ CS uses this known (possibly conservative) in place of in (12), and thus it cannot adapt to an unknown variance, while (12) always scales with . In simpler terms, Theorem 2.2 is a time-uniform analogue of the CLT in the same way that Robbins’ CS is a time-uniform analogue of a sub-Gaussian concentration inequality (e.g. Hoeffding’s or Chernoff’s inequality [16, 18]).

It is important not to confuse Theorem 2.2 with a martingale CLT as the latter still gives fixed-time CIs in the spirit of the usual CLT but under different assumptions on the martingale difference sequence (however, we do present an analogue of Theorem 2.2 under martingale dependence in Theorem 2.5).

2.2.4 An asymptotic confidence sequence with iterated logarithm rates

As a consequence of the law of the iterated logarithm, a confidence sequence for centered at cannot have an asymptotic width smaller than . This is easy to see since

This raises the question as to whether can be improved so that the optimal asymptotic width of is achieved. Indeed, we can replace Robbins’ Gaussian mixture boundary with Howard et al. [19, Eq. (2)] (or virtually any other Gaussian boundary for that matter) in the proof of Theorem 2.2 to derive such an AsympCS, but as the authors discuss, mixture boundaries such as the one in Theorem 2.2 may be preferable in practice, because any bound that is tighter “later on” (asymptotically) must be looser “early on” (at practical sample sizes) due to the fact that all such bounds have a cumulative miscoverage probability . Nevertheless, we present an AsympCS with an iterated logarithm rate here for completeness.

Proposition 2.3 (Iterated logarithm asymptotic confidence sequences).

We omit the proof of Proposition 2.3 as it proceeds in a similar fashion to that of Theorem 2.2. In fact, both of these AsympCSs are simply instantiations of a more general principle for deriving AsympCSs by combining strong approximations with time-uniform boundaries for the approximating process, an approach that we discuss in the following section.

2.3 A general framework for deriving asymptotic confidence sequences

The proofs of both Theorem 2.2 and Proposition 2.3 follow the same general structure, combining strong approximations with time-uniform boundaries along with some other almost-sure asymptotic behavior. Abstracting away the details specific to these particular results, we provide the following four general conditions under which many AsympCSs can be derived, including those from the previous section but also Lyapunov- and Lindeberg-type AsympCS that we will derive in Section 2.4).

In what follows, let be a totally ordered infinite set that includes a minimum value (for example, one may think about as or with ). Then, consider the following four conditions where we use the “Condition G-X” enumeration as a mnemonic for the X condition in the section on General frameworks for AsympCSs).

Condition G-1 (Strong approximation).

On a potentially enriched probability space, there exists a process starting at that strongly approximates up to a rate of , i.e.

| (13) |

Condition G-2 (Boundary for the approximating process).

The process forms a -boundary for the process given in (13):

| (14) |

Condition G-3 (Strong approximation rate).

Condition G-4 (Almost-sure approximate boundary).

The -boundary for is almost-surely approximated by the sequences , i.e.

| (16) |

Deriving new AsympCSs then reduces to the conceptually simpler but nevertheless nontrivial task of satisfying the requisite conditions above. For example, in the previous section, we satisfied G-1 via Strassen [50], G-2 via Robbins [41], G-3 via the combination of Strassen [50] and Robbins [41], and G-4 via the strong law of large numbers (SLLN). The only difference between Theorem 2.2 and Proposition 2.3 was in what boundaries were being used for and . More generally under Sections G-1–G-4, we have the following abstract Lemma for AsympCSs.

Lemma 2.4 (An abstract AsympCS for well-approximated processes).

We provide a short proof of Lemma 2.4 in Section A.2. In the following section, we will use the general recipe of Lemma 2.4 to obtain AsympCSs for time-varying means from non-iid random variables under martingale dependence as in the Lindeberg CLT [30, 4].

2.4 Lindeberg- and Lyapunov-type AsympCSs for time-varying means

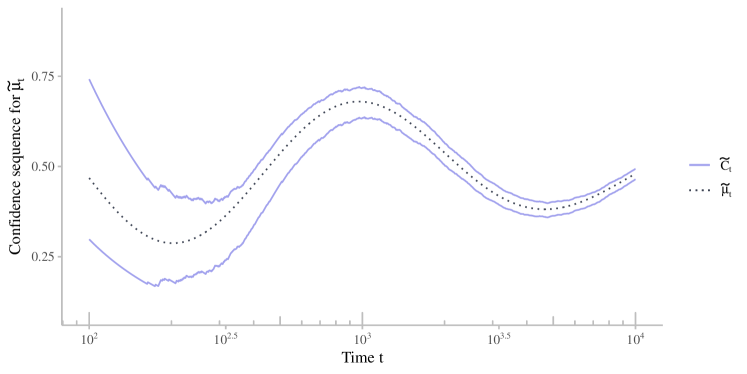

The results in Theorem 2.2 and Proposition 2.3 focused on the situation where the observed random variables are independent and identically distributed, as this is one of the most commonly studied regimes in statistical inference. In practice, however, we may not wish to assume that means and variances remain constant over time, or that observations are independent of each other. Nevertheless, an analogue of Theorem 2.2 still holds for random variables with time-varying means and variances under martingale dependence. In this case, rather than the CS covering some fixed , it covers the average conditional mean thus far: — to be made precise shortly.555Throughout this section and the remainder of the paper, we use the overhead tilde (e.g. , , and ) to emphasize that these quantities can change over time. For example, Fig. 2 explicitly displays means and CSs with sinusoidal behaviors resembling a tilde.

Given the additional complexity introduced by considering time-varying conditional distributions, we will first explicitly spell out the conditions required to achieve a time-varying analogue of Theorem 2.2. Note however, that these conditions are no more restrictive, meaning that they reduce to the conditions of Theorem 2.2 in the iid regime. Suppose is a sequence of random variables with conditional means and variances given by and , respectively. First, we require that the average conditional variance either does not vanish, or does so superlinearly; equivalently, we require that the cumulative conditional variance diverges.

Condition L-1 (Cumulative variance diverges almost surely).

For each , let be the conditional variance of . Then,

| (19) |

Eq. 19 can also be interpreted as saying that the average conditional variance does not vanish faster than (if at all), meaning . For example, L-1 would hold if for some or in the iid case where . Second, we require a Lindeberg-type uniform integrability condition on the tail behavior of .

Condition L-2 (Lindeberg-type uniform integrability).

For each , let be the conditional variance of . Then there exists some such that

| (20) |

Notice that Eq. 20 is satisfied if all conditional moments are almost surely uniformly bounded for some , meaning a.s. for all and for some constant , or more generally under a Lyapunov-type condition that states a.s. for some .666We show that the Lyapunov-type condition implies L-2 in Section B.5. Third and finally, we require a consistent variance estimator.

Condition L-3 (Consistent variance estimation).

Let be an estimator of constructed using such that

| (21) |

Note that in the iid case, (21) would hold using the sample variance by the SLLN. More generally for independent but non-identically distributed data, L-3 holds as long as the variation in means vanishes — i.e. — but we will expand on this later in Corollary 2.6. Given Sections L-1, L-2, and L-3, we have the following AsympCS for the time-varying conditional mean .

Theorem 2.5 (Lindeberg-type Gaussian mixture martingale AsympCS).

At a high level, the proof of Theorem 2.5 (found in Section A.3) follows from the general AsympCS procedure of Lemma 2.4 by using L-2 and Strassen’s 1967 strong approximation [51] (not to be confused with his 1964 result that we used in Theorem 2.2) to satisfy Conditions G-1 and G-3, and a variant of Robbins’ mixture martingale for non-iid random variables — that appears to be new in the literature — along with Conditions L-1 and L-3 to satisfy Conditions G-2 and G-4.

Notice that if the data happen to be iid, then is asymptotically equivalent to given in Theorem 2.2 (here, “asymptotic equivalence” simply means that the ratio of the two boundaries converges a.s. to 1). In other words, Theorem 2.5 is valid in a more general (non-iid) setting, but will essentially recover Theorem 2.2 in the iid case. Fig. 2 illustrates what may look like in practice. Note that when are independent with , and , it is nevertheless the case that forms a -AsympCS for under the same assumptions as Theorem 2.2. In this sense, we can view as “robust” to deviations from independence and stationarity.777Here, the term “robust” should not be interpreted in the same spirit as “doubly robust”, where the latter is specific to the discussions surrounding functional estimation and causal inference in Section 3. A one-sided analogue of Theorem 2.5 is presented in Proposition B.2 within Section B.1.

As a near-immediate corollary of Theorem 2.5, we have the following Lyapunov-type AsympCS under independent but non-identically distributed random variables.

Corollary 2.6 (Lyapunov-type AsympCS).

Suppose is a sequence of independent random variables with individual means and variances given by and , respectively. Suppose that in addition to L-1 and the Lyapunov-type condition , we have the following regularity conditions:

| (23) |

for some . In other words, the higher moments of , the running mean , and the “variation in means” all cannot diverge too quickly relative to . Then using the sample variance for , forms a -AsympCS for the running average mean .

Clearly, the conditions of (23) are trivially satisfied if means and variances are uniformly bounded over time. Since Sections L-1 and L-2 hold by the assumptions of Corollary 2.6, the proof in Section A.4 simply shows how the conditions in (23) imply L-3.

As suggested by Section 2.3, we can combine Lemma 2.4 with essentially any other Gaussian boundary, and indeed there are others that can yield Lindeberg- and Lyapunov-type AsympCSs but we do not enumerate any more here, though we do mention one inspired by Robbins [41, Eq. (20)] in passing in Section 2.6. The next section discusses how all of the aforementioned AsympCSs satisfy a certain formal asymptotic coverage guarantee.

2.5 Asymptotic coverage and type-I error control

While the AsympCSs derived thus far serve as sequential analogues of CLT-based CIs, it is not immediately obvious whether AsympCSs enjoy similar asymptotic coverage (equivalently, type-I error) guarantees. We will now give a positive answer to this question by showing that after appropriate tuning, our AsympCSs have asymptotic -coverage uniformly for all as (to be formalized in Definition 2.7).

Recall that in the discussion preceding the definition of AsympCSs (Definition 2.1), we appealed to the rather strong fact that for an asymptotic confidence interval , there exists a nonasymptotic CI such that . In particular we said that is an AsympCS if there exists a nonasymptotic CS such that . Placing these guarantees side-by-side, our definition of AsympCSs was motivated by the fact that

| (24) |

However, another property of asymptotic CIs is that their coverage is at least in the limit:

| (25) |

but what is the time-uniform analogue of (25)? Since any single AsympCS will simply have some coverage, we provide the following definition as a time-uniform analogue of (25) for sequences of AsympCSs that start later and later.

Definition 2.7 (Asymptotic time-uniform coverage).

Let be a sequence of AsympCSs for and let . We say that has asymptotic time-uniform -coverage for if

| (26) |

and we say that this coverage is sharp if the above inequality is an equality .

To the best of our knowledge, the existing literature lacks a concrete definition of asymptotic time-uniform coverage (or type-I error control) like Definition 2.7, but sequences of AsympCSs satisfying (26) have been implicit in Robbins [41] and Robbins and Siegmund [42] as well as the recent preprint of Bibaut et al. [2]. However, these prior works use boundaries that do not resemble those in the present paper, and hence it is an open question as to whether our AsympCSs satisfy Definition 2.7 in some sense. In the remainder of this section, we give a positive answer to this open question by providing (sharp) coverage guarantees for our AsympCSs. Furthermore, in Section 2.6 we will strictly improve on aforementioned bounds by Robbins [41], Robbins and Siegmund [42], and Bibaut et al. [2] by uniformly tightening their AsympCSs and weakening their assumptions, obtaining those bounds as corollaries.

In order to obtain asymptotic time-uniform coverage, we will need a stronger variant of L-3 so that variances are estimated at polynomial rates (rather than at arbitrary rates).

Condition L-3- (Polynomial rate variance estimation).

There exists some such that

| (27) |

Note that while L-3- is stronger than L-3, it is still quite mild. For instance, if is uniformly bounded, then (27) simply requires that (i.e. at any polynomial rate, potentially much slower than ). Moreover, in the iid case with at least finite absolute moments, L-3- always holds by the non-iid Marcinkiewicz-Zygmund SLLN (see [35, p. 272]).

Our goal now is to show that sequences of AsympCSs given in Theorem 2.5 have asymptotic time-uniform coverage, and we will achieve this by effectively tuning them for later and later start times. Recall that Section B.2 allows us to choose the parameter so that the AsympCS is tightest at some particular time — we will now choose based on the first peeking time as

| (28) |

Then, let be the Gaussian mixture AsympCS with plugged into the expression of the boundary for all :

| (29) |

In other words, should be thought of as an AsympCS that only starts after time , and is vacuous beforehand. The following theorem formalizes the coverage guarantees satisfied by this sequence of AsympCSs as .

Theorem 2.8 (Asymptotic -coverage for Gaussian mixture AsympCSs).

The proof can be found in Section A.7. Notice that in the iid setting, as , is asymptotically equivalent to given by

| (31) |

where . A quick inspection of the proof will reveal that (31) also satisfies the coverage guarantee provided in Theorem 2.8 under the condition that . In summary, (31) can be thought of as an analogue of (29) for the AsympCSs that were derived in Theorem 2.2.

2.6 Asymptotic confidence sequences using Robbins’ delayed start

As is clear from Lemma 2.4, virtually any boundary for Gaussian observations can be used to derive an AsympCS as long as an appropriate strong invariance principle can be applied under the given assumptions — indeed, Theorem 2.2, Proposition 2.3, Theorem 2.5, and Corollary 2.6 are all instantiations of the general phenomenon outlined in Lemma 2.4.

Another AsympCS that may be of interest to practitioners is one that leverages Robbins’ CS for means of Gaussian random variables with a delayed start time [41, Eq. (20)]. In a nutshell, Robbins calculated a lower bound on the probability that a centered Gaussian random walk would remain within a particular two-sided boundary for all times given some starting time . That is, he showed that for iid standard Gaussians , letting , and for any ,

| (32) |

where and and are the CDF and PDF of a standard Gaussian, respectively. In particular, setting so that yields a two-sided -boundary for the Gaussian random walk , and indeed, a solution to always exists and is trivial to compute due to the fact that is monotonically decreasing, starting at and . In a followup paper, Robbins and Siegmund [42] extended the ideas of Robbins [41] to a large class of boundaries for Wiener processes so that the probabilistic inequality in (32) can be shown to be an equality when is replaced by the absolute value of a Wiener process (which would imply the inequality in (32) for iid standard Gaussians as a corollary). Using this fact within the general framework of Lemma 2.4 combined with the strong invariance principle of Strassen [51] and the techniques found in the proof of Theorem 2.8 yields the following result.

Proposition 2.9 (Delayed-start AsympCS).

Consider the same setup as Theorem 2.8 so that have conditional means and variances given by and . Then under Section L-1, L-2, and L-3, we have that for any ,

| (33) |

(and all of otherwise) forms a -AsympCS for , where is chosen so that . Furthermore, under L-3-, has sharp asymptotic time-uniform -coverage in the sense of Definition 2.7.

The proof is provided in Section A.9. Similar to the relationship between Theorem 2.8 and (31), we have that if variances happen to converge almost surely, then as a corollary of Proposition 2.9, the sequence given by

| (34) |

has asymptotic time-uniform coverage as in Definition 2.7. This can be seen as a generalization and improvement of results implied by Robbins [41] and Robbins and Siegmund [42]. In followup work to ours by Bibaut et al. [2], the authors derive similar results to Robbins [41] and Robbins and Siegmund [42] yielding an AsympCS that can be written as a looser version of (34) (in fact, it was their paper that inspired us explicitly write down Definition 2.7 and to show that it holds more generally). We elaborate on the details of these connections in Section B.6.

3 Illustration: Causal effects and semiparametric estimation

Given the groundwork laid in Section 2, we now demonstrate the use of AsympCSs for conducting anytime-valid causal inference. Since it is an important and thoroughly studied functional, we place a particular emphasis on the average treatment effect (ATE) for illustrative purposes but we discuss how these techniques apply to semiparametric functional estimation more generally in Section 3.5. The literature on uncertainty quantification for semiparametric functional estimation often falls within the asymptotic regime and hence AsympCSs form a natural time-uniform extension thereof.

It is important to note that obtaining AsympCSs for the ATE is not as simple as directly applying the theorems of Section 2.1 to some appropriately chosen augmented inverse-probability-weighted (AIPW) influence functions (otherwise the illustration of this section would have been trivial). Indeed, satisfying the conditions of the aforementioned theorems — and Lemma 2.4 in particular — in the presence of potentially infinite-dimensional nuisance parameters is nontrivial and the analysis proceeds rather differently from the fixed- setting. Nevertheless, after introducing and carefully analyzing sequential sample-splitting and cross-fitting (Section 3.1), we will see that efficient time-uniform inference for the ATE is still possible.

To solidify the notation and problem setup, suppose that we observe a (potentially infinite) sequence of iid variables from a distribution where denotes the subject’s triplet and are their measured baseline covariates, is the treatment that they receive, and is their measured outcome after treatment. Our target estimand is the average treatment effect (ATE) defined as

| (35) |

where is the counterfactual outcome for a randomly selected subject had they received treatment . The ATE can be interpreted as the average population outcome if everyone were treated versus if no one were treated . Under standard causal identification assumptions — typically referred to as consistency, positivity, and exchangeability (see e.g. Kennedy [24, §2.2]) — we have that can be written as a (non-counterfactual) functional of the distribution :

| (36) |

Throughout the remainder of this section, we will operate under these identification assumptions and aim to derive efficient AsympCSs for using tools from semiparametric theory. At a high level, we will construct AsympCSs for by combining the results of Section 2 with sample averages of influence functions for and in the ideal case, these influence functions will be efficient (in the semiparametric sense).

3.1 Sequential sample-splitting and cross-fitting

Following Robins et al. [43], Zheng and van der Laan [67], and Chernozhukov et al. [8], we employ sample-splitting to derive an estimate of the influence function on a “training” sample, and evaluate on values of in an independent “evaluation” sample. Sample-splitting sidesteps complications introduced from “double-dipping” (i.e. using to both construct and evaluate ) and greatly simplifies the analysis of the downstream estimator. Since the aforementioned authors employed sample splitting in the batch (non-sequential) regime while we are concerned with settings where data are continually observed in an online stream over time, we modify the sample-splitting procedure as follows. We will denote and as the “training” and “evaluation” sets, respectively. At time , we assign to either group with equal probability:

Note that at time , is not re-randomized into either split — once is randomly assigned to one of or , they remain in that split for the remainder of the study. In this way, we can write and and think of these as independent, sequential observations from a common distribution . To keep track of how many subjects have been randomized to and at time , define

| (37) |

where we have left the dependence on implicit.

Remark 2.

Strictly speaking, under the iid assumption, we do not need to randomly assign subjects to training and evaluation groups for the forthcoming results to hold (e.g. we could simply assign even-numbered subjects to and odd-numbered subjects to ). However, the analysis is not further complicated by this randomization, and it can be used to combat bias in treatment assignments when the iid assumption is violated [12].

3.1.1 The sequential sample-split estimators

After employing sequential sample-splitting, the sequence of sample-split estimators for are given by

| (38) |

where is given by (188) with replaced by which is built solely from . The sample-splitting procedure for constructing is summarized pictorially in Fig. 3. In the batch setting for a fixed sample size, (38) is often referred to as the augmented inverse probability weighted (AIPW) estimator [45, 46] (an instantiation of so-called “one-step correction” in the semiparametrics literature) and we adopt similar nomenclature here.

3.1.2 The sequential cross-fit estimators

A commonly cited downside of sample-splitting is the loss in efficiency by using subjects instead of when evaluating the sample mean . An easy fix is to cross-fit: swap the two samples, using the evaluation set for training and the training set for evaluation to recover the full sample size of [43, 67, 8]. That is, construct solely from and define the cross-fit estimator as

| (39) |

and the associated cross-fit variance estimate

| (40) |

where is the -sample variance of the pseudo-outcomes at time and similarly for (we deliberately omit the subscript on in Eq. 40). All of the results that follow are stated in terms of the cross fit estimators but they also hold using instead. With the setup of Section B.7 and Section 3.1 in mind, we are ready to derive AsympCSs for , first in randomized experiments.

3.2 Asymptotic confidence sequences in randomized experiments

Consider a sequential randomized experiment so that a subject with covariates has a known propensity score given by

Consider the cross-fit AIPW estimator as given in (39) but with estimated propensity scores — and — replaced by their true values , and with and being possibly misspecified estimators for . That is, we will assume that converges to some function , which need not coincide with . In what follows, when we use or in writing or , we are referring to large-sample properties of the estimator (and hence could be replaced by or without loss of generality).

Theorem 3.1 (Confidence sequences for the ATE in randomized experiments).

Let be the cross-fit AIPW estimator as in (39). Suppose for each where is some function (but need not be ), and hence for some influence function . Suppose that propensity scores are bounded away from 0 and 1, i.e. for some , and suppose that . Then for any constant ,

| (41) |

forms a -AsympCS for .

The proof in Appendix A.5 combines an analysis of the almost-sure convergence of with the AsympCS of Theorem 2.2. Notice that since is consistent for a function , we have that is converging to some influence function of the form

| (42) |

In practice, however, one must choose . As alluded to at the beginning of Section 3, the best possible influence function is the EIF defined in (188), and thus it is natural to attempt to construct so that . The resulting confidence sequences would inherit such optimality properties, a point which we discuss further in Section B.8.

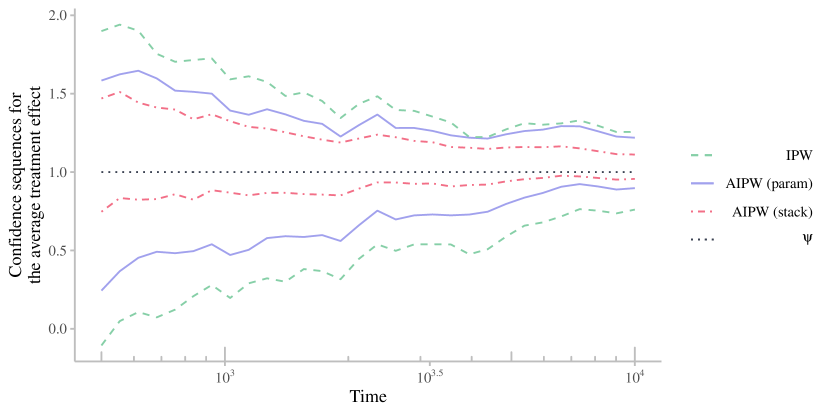

Since is simply a conditional mean function, we can use virtually any regression techniques to estimate it. Here we will consider the general approach of stacking introduced by Breiman [5] and further studied by Tsybakov [54] and van der Laan et al. [57] (see also [38, 39]) under the names of “aggregation” and “Super Learning” respectively. In short, stacking uses cross-validation to choose a weighted combination of candidate predictors where the weights are chosen based on data in held-out samples. Importantly, the candidate predictors can simultaneously include both flexible machine learning methods (e.g. random forests [6], generalized additive models [15], etc.) as well as simpler parametric ones and yet for large samples (and under certain conditions), the stacked predictor will have a mean squared error that scales with that of the best of the predictors up to an additive term [54, 60]. This advantage can be seen empirically in Fig. 4 where the true regression functions and are non-smooth and nonlinear in . We wish to emphasize that such advantages via stacking are not new — we are only highlighting the observation that similar phenomena carry over to AsympCSs.

So far, the use of flexible regression techniques including the ensemble method of stacking were used only for the purposes of deriving sharper AsympCSs in sequential randomized experiments. In observational studies, however, consistent estimation of nuisance functions at fast rates is essential to the construction of valid fixed- CIs, and indeed the same is true for AsympCSs.

3.3 Asymptotic confidence sequences in observational studies

Consider now a sequential observational study (e.g. we are able to continuously monitor but do not know exactly, or we are in a sequentially randomized experiment with noncompliance, etc.). The only difference in this setting with respect to setup is the fact that is no longer known and must be estimated. As in the fixed- setting, however, this complicates estimation and inference. The following theorem provides the conditions under which we can construct AsympCSs for using the cross-fit AIPW estimator in observational studies.

Theorem 3.2 (Confidence sequence for the ATE in observational studies).

Consider the same setup as Theorem 3.1 but with no longer known. Suppose that regression functions and propensity scores are consistently estimated in at a product rate of , meaning that

Moreover, suppose that where is the efficient influence function (188) and that . Then for any constant ,

forms a -AsympCS for .

The proof in Appendix A.5.2 proceeds similarly to the proof of Theorem 3.1 by combining Theorem 2.2 with an analysis of the almost-sure behavior of . Notice that the nuisance estimation rate of is slower than which is usually required in the fixed- regime, but we do require almost-sure convergence rather than convergence in probability.

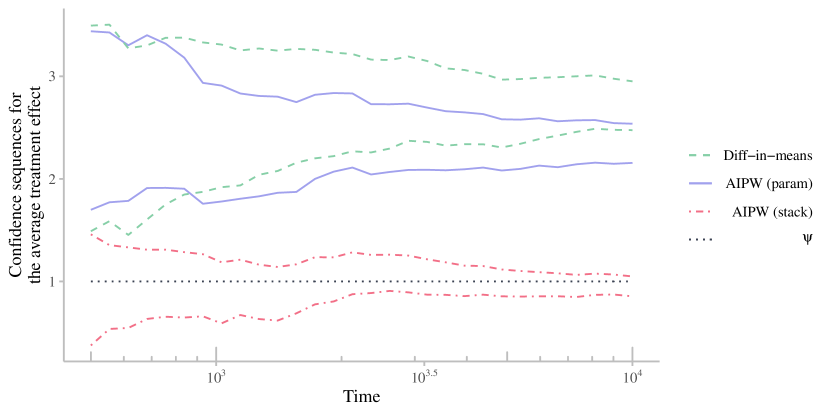

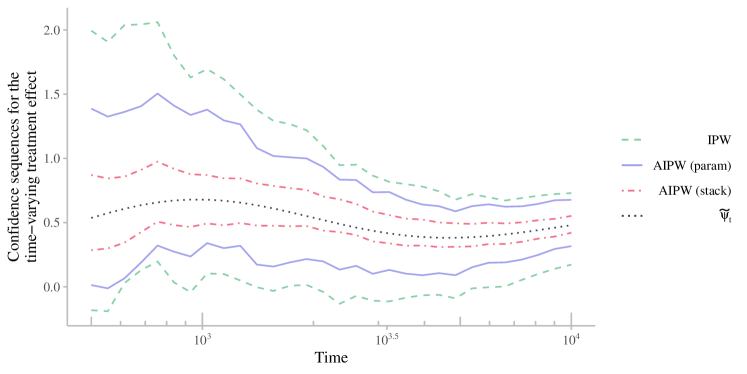

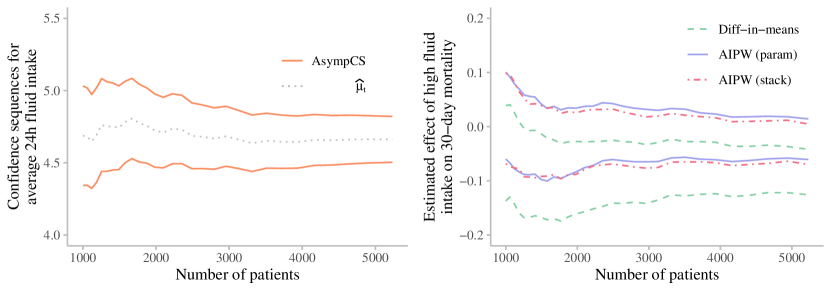

Unlike the experimental setting of Section 3.2, Theorem 3.2 requires that and consistently estimate and , respectively. As a consequence, the stacking-based AIPW AsympCS is both the tightest of the three and is uniquely consistent for (see Fig. 5).

3.4 The running average of individual treatment effects

The results in Sections 3.2 and 3.3 considered the classical regime where the ATE is a fixed functional that does not change over time. Consider a strict generalization where distributions — and hence individual treatment effects in particular — may change over time. In other words,

| (43) |

where the equality holds under the familiar causal identification assumptions discussed earlier. Despite the non-stationary and non-iid structure, it is nevertheless possible to derive AsympCSs for the running average of individual treatment effects — or simply, the running average treatment effect — using the Lyapunov-type bounds of Corollary 2.6. However, given this more general and complex setup, the assumptions required are more subtle (but no more restrictive) than those for Theorems 3.1 and 3.2; as such, we explicitly describe their details here but handle the randomized and observational settings simultaneously for brevity.

Condition -1 (Regression estimator is uniformly well-behaved in ).

We assume that regression estimators converge in to any function uniformly for i.e.

| (44) |

for each .

-1 simply requires that the regression estimator must converge to some function , which need not coincide with true regression function . In the iid setting where all have the same distribution, we would simply drop the , recovering the conditions for Theorems 3.1 and 3.2.

Condition -2 (Convergence of average nuisance errors).

Let be an estimator of the regression function , and an estimator of the propensity score . We assume that the average bias shrinks at a rate, i.e.

| (45) |

Note that -2 would hold in two familiar scenarios. Firstly, in a randomized experiment (Theorem 3.3) where is known by design, we have that is always zero, satisfying -2 trivially. Second, in an observational study where the product of errors vanishes at a rate faster than , for each and for both , we also have that their average product errors vanish at the same rate (45). With these assumptions in mind, let us summarize how running average treatment effects can be captured in randomized experiments.

Theorem 3.3 (AsympCSs for the running average treatment effect).

Suppose are independent triples and that Sections -1 and -2 hold. Finally, suppose that the conditions of Corollary 2.6 hold, but with replaced by the influence functions . Then,

| (46) |

forms a -AsympCS for the running average treatment effect .

The proof can be found in Section A.6, and it is not hard to see that both Theorems 3.1 and 3.2 are particular instantiations of Theorem 3.3. The important takeaway from Theorem 3.3 is that under some rather mild conditions on the moments of , it is possible to derive an AsympCS for a running average treatment effect (see Fig. 6 for what these look like in practice). Nevertheless, under the commonly considered regime where the treatment effect is constant , we have that (46) forms a -AsympCS for . Note that unlike Theorems 3.1 and 3.2, Theorem 3.3 actually does require the use of the cross-fit AIPW estimator and would not capture if the sample-split version were used in its place.

Remark 3 (Avoiding sample splitting via martingale AsympCSs).

The reader may wonder whether it is possible to simply plug in a predictable estimate of — i.e. so that only depends on — and employ the Lindeberg-type martingale AsympCS of Theorem 2.5 in place of Corollary 2.6, thereby sidestepping the need for sequential sample splitting and cross-fitting altogether. Indeed, such an analogue of Theorem 3.3 is possible to derive, but the conditions required are less transparent than those we have provided above, and such a result may overload the current paper, so we omit it.

3.5 Extensions to general semiparametric estimation and the Delta method

The discussion thus far has been focused on deriving confidence sequences for the ATE in the context of causal inference. However, the tools presented in this paper are more generally applicable to any pathwise differentiable functional with positive (and finite) semiparametric information bound. Here we list some prominent examples in causal inference:

-

•

Modified interventions: ;

-

•

Complier-average effects: ;

-

•

Time-varying: ;

-

•

Controlled mediation effects: ,

where is an instrumental variable, is a mediator, and the notation is shorthand for the tuple . Some examples outside of causal inference include

-

•

Expected density: ;

-

•

Entropy: ;

-

•

Expected conditional variance: ,

-

•

Expected conditional covariance: ,

where is the density of the random variable .

All of the aforementioned problems, including estimation of the ATE in Section 3 can be written in the following general form. Suppose and let be some functional (such as those listed above) of the distribution . In the case of a finite sample size , is said to be an asymptotically linear estimator [53] for if

| (47) |

where is the influence function of . When the sample size is not fixed in advance, we may analogously say that is an asymptotically linear time-uniform estimator if instead,

| (48) |

with being the same influence function as before. For example, in the case of the ATE with , we presented an efficient estimator which took the form,

| (49) |

where is the uncentered efficient influence function (EIF) defined in (188). In order to justify that the remainder term is indeed , we used sequential sample splitting and additional analysis in the randomized and observational settings (see the proofs in Sections A.5 and A.5.2 for more details). In general, as long as an estimator for has the form (48), we may derive AsympCSs for as a simple corollary of Theorem 2.2.

Corollary 3.4 (AsympCSs for general functional estimation).

Suppose is an asymptotically linear time-uniform estimator of with influence function , that is, satisfying (48). Additionally, suppose that for some . Then,

| (50) |

forms a -AsympCS for . Moreover, if is replaced by as in Eq. 31 to obtain

| (51) |

then has asymptotic time-uniform coverage as , meaning

| (52) |

Clearly, the boundaries of Sections 2.2.4 or 2.6 could be used here in place of Theorem 2.2, though for the boundary in Proposition 2.3, we would need to strengthen the rate in (47) to . If computing additionally involves the estimation of a nuisance parameter such as in Theorems 3.1 and 3.2, this must be handled carefully on a case-by-case basis where sequential sample splitting and cross fitting (Section 3.1) may be helpful, and higher moments on may be needed. We now derive an analogue of the Delta method for asymptotically linear time-uniform estimators.

Proposition 3.5 (The Delta method for AsympCSs).

Let be an asymptotically linear time-uniform estimator for as in Eq. 47, and let be a continuously differentiable function with first derivative . Then, is an asymptotically linear time-uniform estimator for with influence function given by , i.e.

| (53) |

In particular, Proposition 3.5 can be combined with Corollary 3.4 to obtain Delta method-like AsympCSs with asymptotic time-uniform coverage guarantees. The short proof in Section A.8 is similar to the proof of the classical Delta method but with the almost-sure continuous mapping theorem used in place of the in-probability one, and with the law of the iterated logarithm used in place of the central limit theorem.

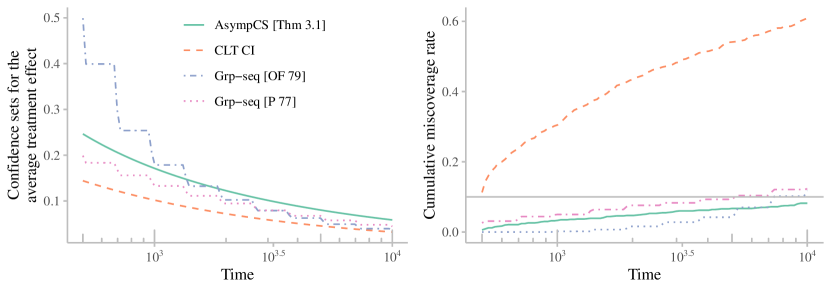

4 Simulation study: Widths and empirical coverage

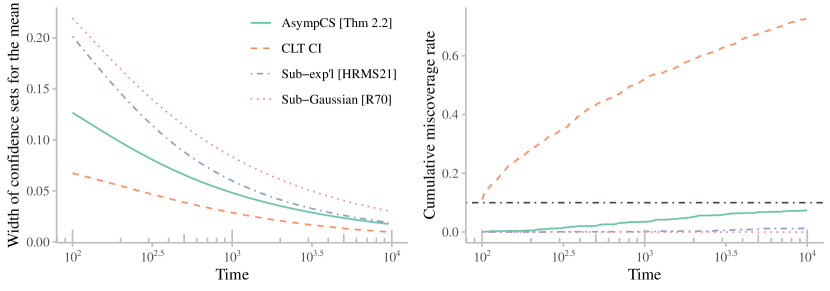

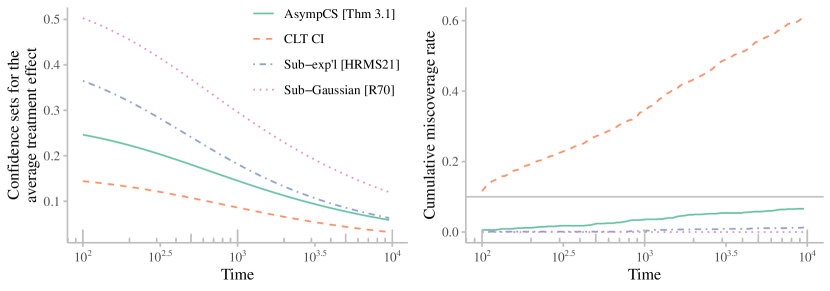

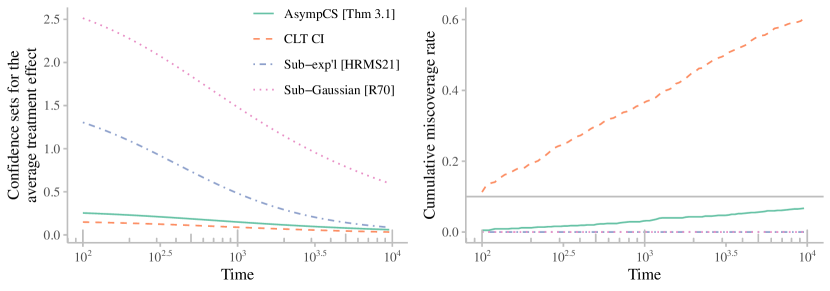

We now provide a brief simulation study focusing on the setting where are bounded random variables (with known bounds) and the parameters of interest may include means or treatment effects. We consider this setting as it is well-studied, allowing us to draw on a rich literature containing several nonasymptotic CSs to which we will compare AsympCSs (though it is important to keep in mind that there are many unbounded problems for which nonasymptotic CSs do not exist, and we discuss these at the end of the section). In particular, we will compare the AsympCSs of Theorems 2.2 and 3.1 to Robbins’ sub-Gaussian mixture CS [41] (see also [19, §3.2]), the empirical Bernstein CSs of Howard et al. [19, Thm 4 and Cor 2], and CLT-based CIs. Of course, CLT-based CIs are not time-uniform and are only included for reference. We consider three cases of parameter estimation for bounded random variables:

(a) Estimating the mean of bounded random variables

(b) Estimating the ATE in a completely randomized Bernoulli experiment

(b) Estimating the ATE in a completely randomized Bernoulli experiment

(c) Estimating the ATE in an experiment with personalized randomization

(c) Estimating the ATE in an experiment with personalized randomization

- (a)

-

(b)

The second considers average treatment effect estimation in a randomized experiment with -valued outcomes where everyone is randomly assigned to treatment or control with probability . Since all propensity scores are equal to , we have that estimates of the influence functions in (42) from Section 3.2 are bounded in , and hence the techniques of Robbins [41] and Howard et al. [19] are applicable (as suggested by Howard et al. [19, §4.2]).

-

(c)

The third and final simulation considers a similar setup to (b) with the key difference that propensity scores are now covariate-dependent (“personalized”). In this case, as suggested by Howard et al. [19, §4.2], note that estimates of the influence functions (42) lie in where , permitting the application of Robbins [41] and Howard et al. [19] as before.888Note that Howard et al. [19, §4.2] use a more conservative bound of but it is not hard to see that this can be improved to . Consequently, we are ultimately comparing our AsympCSs to a strictly tighter nonasymptotic CS than the one proposed by Howard et al. [19, §4.2].

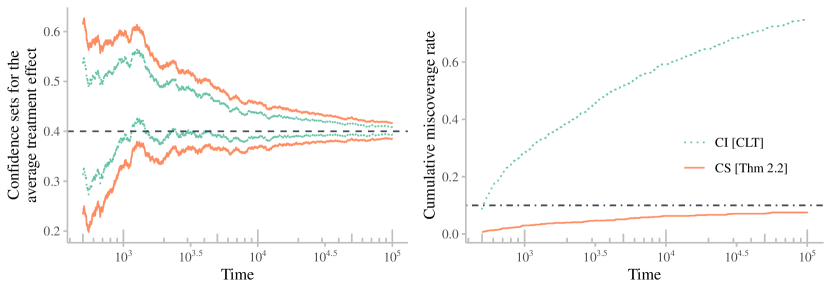

Notice that in all three scenarios, CLT-based CIs have cumulative miscoverage rates that quickly diverge beyond while those of CSs — both asymptotic and nonasymptotic — never exceed before time . (Note that a longer time horizon of is considered only for AsympCSs and CLT-based CIs in Fig. 1, but is omitted here due to the computational expense of Howard et al. [19, Thm 2] at large .) Moreover, notice that nonasymptotic CSs appear to be conservative, while our AsympCSs are much tighter and have miscoverage rates approaching (as expected in light of Theorem 2.8).

These particular simulation scenarios illustrate situations where AsympCSs are increasingly beneficial over nonasymptotic bounds. First, estimating means of bounded random variables (Fig. 7(a)) is a problem for which several nonasymptotic CIs and CSs exist, and indeed both the bounds of Robbins [41] and especially Howard et al. [19] fare well in this setting. The relatively small variance of Uniform(0, 1) random variables, however, means that asymptotic methods can quickly tighten in this setting while the empirical Bernstein CSs of Howard et al. [19] take a while to adapt to the variance (while those of Robbins [41] never will).

However, AsympCSs are particularly well-suited to the settings of ATE estimation in Figs (b) and (c) where almost-sure bounds on observed random variables can be quite large in comparison to their variances. Fig. 7(b) considers the setting where all propensity scores are equal to which is the “easiest” regime for nonasymptotic methods, meaning the influence function bounds are as tight as possible. Even here, AsympCSs are tighter than the nonasymptotic bounds. On the other hand, Fig. 7(c) considers a setting where propensity scores are highly covariate-dependent, and hence the almost sure bounds on propensity scores must hold for all possible (in this simulation, ). In this setting we see that AsympCSs drastically outperform nonasymptotic CSs without inflating miscoverage rates. Taking this to the logical extreme, it is possible to construct scenarios where is closer and closer to 0, but influence function variances remain bounded. In other words, it is possible to consider scenarios where AsympCSs are arbitrarily tighter than nonasymptotic CSs, without inflating miscoverage rates.

Finally, we remark that while AsympCSs demonstrate substantial benefits over nonasymptotic CSs in terms of tightness, we wish to also highlight their benefits of versatility, and in particular, note that there are many settings for which no simulations could be run since AsympCSs provide the first time-uniform solution in the literature. For example, as a consequence of Bahadur and Savage [1], it is impossible to derive nonasymptotic CSs (or CIs) for the mean of random variables without prior bounds on their moments. By contrast, AsympCSs can handle mean estimation under finite (but unknown) moment assumptions. It is also impossible to derive nonasymptotic CS (and CIs) for the ATE from observational studies (without substantial and unrealistic knowledge of nuisance function estimation errors) but Section 3.3 outlines the first time-uniform solution in the literature. In both of these settings, we cannot run simulations akin to Fig. 7 since there are no prior CSs to compare to.

5 Real data application: effects of IV fluid caps in sepsis patients

Let us now illustrate the use of Theorem 3.2 by sequentially estimating the effect of fluid-restrictive strategies on mortality in an observational study of real sepsis patients. We will use data from the Medical Information Mart for Intensive Care III (MIMIC-III), a freely available database consisting of health records associated with more than 45,000 critical care patients at the Beth Israel Deaconess Medical Center [23, 37]. The data are rich, containing demographics, vital signs, medications, and mortality, among other information collected over the span of 11 years.

Following Shahn et al. [47], we aim to estimate the effect of restricting intravenous (IV) fluids within 24 hours of intensive care unit (ICU) admission on 30-day mortality in sepsis patients. In particular, we considered patients at least 16 years of age satisfying the Sepsis-3 definition — i.e. those with a suspected infection and a Sequential Organ Failure Assessment (SOFA) score of at least 2 [48]. Sepsis-3 patients can be obtained from MIMIC-III using SQL scripts provided by Johnson and Pollard [22], but we provide detailed instructions for reproducing our data collection and analysis process on GitHub.999 github.com/WannabeSmith/drconfseq/tree/main/paper_plots/sepsis This resulted in a total of 5231 sepsis patients, each of whom received out-of-hospital followup of at least 90 days.

We considered IV fluid intake within 24 hours of ICU admission . To construct a binary treatment , we dichotomized so that . The 30-day mortality was defined as 1 if the patient died within 30 days of hospital admission, and 0 otherwise. Baseline covariates included for modelling consisted of the patients’ age and sex, whether they are diabetic, modified Elixhauser scores [61], and SOFA scores. We are interested in the causal estimand,

| (54) |

which is the difference in average 30-day mortality that would be observed if all sepsis patients were randomly assigned an IV fluid level according to the lower truncated distribution versus the upper truncated distribution [11]. While this is technically a stochastic intervention effect, we have that under the same causal identification assumptions discussed in Section 3, is identified as

| (55) |

which is the same functional considered in the previous sections. Therefore, we can estimate under the same assumptions and with the same techniques as Section 3.3. Similar to the simulated data analysis of Fig. 4 and Fig. 5, we produced AsympCSs for using difference-in-means, parametric AIPW, and stacking-based AIPW estimators to demonstrate the impacts of different modeling choices on estimation (see Fig. 8).

Remark 4.

These simple binary treatment and outcome variables were used for simplicity so that the methods outlined in Section 3.3 are immediately applicable, but as discussed in Section 3.5, our AsympCSs may be used to sequentially estimate other causal functionals.

Our stacking-based AIPW AsympCSs cover the null treatment effect of 0 from the to the observed patient, and thus we cannot conclude with confidence whether 6L IV fluid caps have an effect on 30-day mortality in sepsis patients. Interestingly, the width and center of AsympCSs based on both stacking and parametric estimators are roughly equal, which is in contrast to the simulations provided in the previous sections. This could be due to the fact that the true regression or propensity score functions lie in the parametric models considered by “AIPW (param)” or because they are good approximations. Since this analysis is not a simulation, we cannot know with certainty one way or another. Nevertheless, because our stacked estimator uses the parametric (linear and logistic regression) models as candidate predictors, the stacking-based AsympCS is guaranteed to asymptotically match the parametric one if the parametric models are correctly specified. As such, there is little reason to use the parametric AIPW AsympCS alone.

Note that these stacking-based AsympCSs nearly drop below 0 after observing the patient’s outcome. If we were using fixed-time confidence intervals, we would need to resist the temptation to resume data collection (e.g. to see whether the null hypothesis could be rejected with a slightly larger sample size) as this would inflate type-I error rates (as seen in Fig. 1). On the other hand, our AsympCSs permit exactly this form of continued sampling.

6 Conclusion

This paper introduced the notion of an “asymptotic confidence sequence” as the time-uniform analogue of an asymptotic confidence interval based on the central limit theorem. We derived an explicit universal asymptotic confidence sequence for the mean from iid observations under weak moment assumptions by appealing to the strong invariance principle of Strassen [50]. These results were extended to the setting where observations’ distributions (including means and variances) can vary over time under martingale dependence, such that our confidence sequences capture a moving parameter — the running average of the conditional means so far. We then applied the aforementioned results to the problem of doubly robust sequential inference for the average treatment effect in both randomized experiments and observational studies under iid sampling. Finally, we showed how these causal applications remain valid in the non-iid setting where distributions change over time, in which case our confidence sequences capture a running average of individual treatment effects. The aforementioned results will enable researchers to continuously monitor sequential experiments — such as clinical trials and online A/B tests — as well as sequential observational studies even if treatment effects do not remain stationary over time.

Acknowledgements

IW-S thanks Tudor Manole for early conversations regarding strong approximation theory. AR acknowledges funding from NSF Grant DMS1916320, NSF Grant DMS2053804, an Adobe faculty research award, and an NSF DMS (CAREER) 1945266. EK gratefully acknowledges support from NSF Grant DMS1810979. The authors thank Ziyu (Neil) Xu, Dae Woong Ham, Eric J. Tchetgen Tchetgen, and the CMU causal inference working group for helpful discussions.

References

- Bahadur and Savage [1956] Raghu R Bahadur and Leonard J Savage. The nonexistence of certain statistical procedures in nonparametric problems. The Annals of Mathematical Statistics, 27(4):1115–1122, 1956.

- Bibaut et al. [2022] Aurélien Bibaut, Nathan Kallus, and Michael Lindon. Near-optimal non-parametric sequential tests and confidence sequences with possibly dependent observations. arXiv preprint arXiv:2212.14411, 2022.

- Bickel et al. [1993] Peter J Bickel, Chris AJ Klaassen, Ya’acov Ritov, and Jon A Wellner. Efficient and adaptive estimation for semiparametric models, volume 4. Johns Hopkins University Press Baltimore, 1993.

- Billingsley [1995] Patrick Billingsley. Probability and measure (3rd ed.). John Wiley & Sons, 1995.

- Breiman [1996] Leo Breiman. Stacked regressions. Machine learning, 24(1):49–64, 1996.

- Breiman [2001] Leo Breiman. Random forests. Machine learning, 45(1):5–32, 2001.

- Chatterjee [2012] Sourav Chatterjee. A new approach to strong embeddings. Probability Theory and Related Fields, 152(1-2):231–264, 2012.

- Chernozhukov et al. [2018] Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21(1):C1–C68, 2018.

- Corless et al. [1996] Robert M Corless, Gaston H Gonnet, David EG Hare, David J Jeffrey, and Donald E Knuth. On the Lambert W function. Advances in Computational mathematics, 5(1):329–359, 1996.

- Darling and Robbins [1967] D. A. Darling and Herbert E. Robbins. Confidence sequences for mean, variance, and median. Proceedings of the National Academy of Sciences of the United States of America, 58 1:66–8, 1967.

- Díaz and van der Laan [2012] Iván Díaz and Mark van der Laan. Population intervention causal effects based on stochastic interventions. Biometrics, 68(2):541–549, 2012.

- Efron [1971] Bradley Efron. Forcing a sequential experiment to be balanced. Biometrika, 58(3):403–417, 1971.

- Einmahl [1989] Uwe Einmahl. Extensions of results of Komlós, Major, and Tusnády to the multivariate case. Journal of multivariate analysis, 28(1):20–68, 1989.

- Einmahl [2009] Uwe Einmahl. A new strong invariance principle for sums of independent random vectors. Journal of Mathematical Sciences, 163(4):311–327, 2009.

- Hastie and Tibshirani [1990] Trevor J Hastie and Robert J Tibshirani. Generalized additive models, volume 43. CRC press, 1990.

- Hoeffding [1963] Wassily Hoeffding. Probability Inequalities for Sums of Bounded Random Variables. Journal of the American Statistical Association, 58(301):13–30, 1963.

- Howard and Ramdas [2022] Steven R Howard and Aaditya Ramdas. Sequential estimation of quantiles with applications to A/B-testing and best-arm identification. Bernoulli, 2022.

- Howard et al. [2020] Steven R. Howard, Aaditya Ramdas, Jon McAuliffe, and Jasjeet Sekhon. Time-uniform Chernoff bounds via nonnegative supermartingales. Probability Surveys, 17:257–317, 2020.

- Howard et al. [2021] Steven R Howard, Aaditya Ramdas, Jon McAuliffe, and Jasjeet Sekhon. Time-uniform, nonparametric, nonasymptotic confidence sequences. The Annals of Statistics, 2021.

- Jennison and Turnbull [1999] Christopher Jennison and Bruce W Turnbull. Group sequential methods with applications to clinical trials. CRC Press, 1999.

- Johari et al. [2017] Ramesh Johari, Pete Koomen, Leonid Pekelis, and David Walsh. Peeking at A/B tests: Why it matters, and what to do about it. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 1517–1525, 2017.

- Johnson and Pollard [2018] Alistair Johnson and Tom Pollard. sepsis3-mimic, May 2018. URL https://doi.org/10.5281/zenodo.1256723.

- Johnson et al. [2016] Alistair EW Johnson, Tom J Pollard, Lu Shen, Li-wei H Lehman, Mengling Feng, Mohammad Ghassemi, Benjamin Moody, Peter Szolovits, Leo Anthony Celi, and Roger G Mark. MIMIC-III, a freely accessible critical care database. Scientific data, 3:160035, 2016.

- Kennedy [2016] Edward H Kennedy. Semiparametric theory and empirical processes in causal inference. In Statistical causal inferences and their applications in public health research, pages 141–167. Springer, 2016.

- Kennedy et al. [2020] Edward H Kennedy, Sivaraman Balakrishnan, and Max G’Sell. Sharp instruments for classifying compliers and generalizing causal effects. Annals of Statistics, 48(4):2008–2030, 2020.

- Komlós et al. [1975] János Komlós, Péter Major, and Gábor Tusnády. An approximation of partial sums of independent rv’-s, and the sample df. i. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 32(1-2):111–131, 1975.

- Komlós et al. [1976] János Komlós, Péter Major, and Gábor Tusnády. An approximation of partial sums of independent rv’s, and the sample df. ii. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 34(1):33–58, 1976.

- Lai [1976a] Tze Leung Lai. Boundary crossing probabilities for sample sums and confidence sequences. The Annals of Probability, pages 299–312, 1976a.

- Lai [1976b] Tze Leung Lai. On confidence sequences. The Annals of Statistics, 4(2):265–280, 1976b.

- Lindeberg [1922] Jarl Waldemar Lindeberg. Eine neue herleitung des exponentialgesetzes in der wahrscheinlichkeitsrechnung. Mathematische Zeitschrift, 15(1):211–225, 1922.

- Major [1976] Péter Major. The approximation of partial sums of independent rv’s. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 35(3):213–220, 1976.

- Morrow and Philipp [1982] Gregory Morrow and Walter Philipp. An almost sure invariance principle for hilbert space valued martingales. Transactions of the American Mathematical Society, pages 231–251, 1982.

- O’Brien and Fleming [1979] Peter C O’Brien and Thomas R Fleming. A multiple testing procedure for clinical trials. Biometrics, pages 549–556, 1979.

- Pace and Salvan [2020] Luigi Pace and Alessandra Salvan. Likelihood, replicability and robbins’ confidence sequences. International Statistical Review, 88(3):599–615, 2020.

- Petrov [2022] Valentin V Petrov. Sums of independent random variables. In Sums of Independent Random Variables. De Gruyter, 2022.

- Pocock [1977] Stuart J Pocock. Group sequential methods in the design and analysis of clinical trials. Biometrika, 64(2):191–199, 1977.

- Pollard and Johnson [2016] Tom J Pollard and Alistair EW Johnson. The MIMIC-III Clinical Database. http://dx.doi.org/10.13026/C2XW26, 2016.

- Polley and van der Laan [2010] Eric C Polley and Mark J van der Laan. Super learner in prediction. U.C. Berkeley Division of Biostatistics Working Paper Series, (Working paper 222), 2010.

- Polley et al. [2011] Eric C Polley, Sherri Rose, and Mark J van der Laan. Super learning. In Targeted learning, pages 43–66. Springer, 2011.

- Ramdas et al. [2020] Aaditya Ramdas, Johannes Ruf, Martin Larsson, and Wouter Koolen. Admissible anytime-valid sequential inference must rely on nonnegative martingales. arXiv preprint arXiv:2009.03167, 2020.

- Robbins [1970] Herbert Robbins. Statistical methods related to the law of the iterated logarithm. The Annals of Mathematical Statistics, 41(5):1397–1409, 1970.

- Robbins and Siegmund [1970] Herbert Robbins and David Siegmund. Boundary crossing probabilities for the Wiener process and sample sums. The Annals of Mathematical Statistics, pages 1410–1429, 1970.

- Robins et al. [2008] James Robins, Lingling Li, Eric Tchetgen Tchetgen, Aad van der Vaart, et al. Higher order influence functions and minimax estimation of nonlinear functionals. In Probability and statistics: essays in honor of David A. Freedman, pages 335–421. Institute of Mathematical Statistics, 2008.

- Robins et al. [1994] James M Robins, Andrea Rotnitzky, and Lue Ping Zhao. Estimation of regression coefficients when some regressors are not always observed. Journal of the American Statistical Association, 89(427):846–866, 1994.

- Rotnitzky et al. [1998] Andrea Rotnitzky, James M Robins, and Daniel O Scharfstein. Semiparametric regression for repeated outcomes with nonignorable nonresponse. Journal of the American Statistical Association, 93(444):1321–1339, 1998.

- Scharfstein et al. [1999] Daniel O Scharfstein, Andrea Rotnitzky, and James M Robins. Adjusting for nonignorable drop-out using semiparametric nonresponse models. Journal of the American Statistical Association, 94(448):1096–1120, 1999.

- Shahn et al. [2020] Zach Shahn, Nathan I Shapiro, Patrick D Tyler, Daniel Talmor, and H Lehman Li-wei. Fluid-limiting treatment strategies among sepsis patients in the icu: a retrospective causal analysis. Critical Care, 24(1):1–9, 2020.

- Singer et al. [2016] Mervyn Singer, Clifford S Deutschman, Christopher Warren Seymour, Manu Shankar-Hari, Djillali Annane, Michael Bauer, Rinaldo Bellomo, Gordon R Bernard, Jean-Daniel Chiche, Craig M Coopersmith, et al. The third international consensus definitions for sepsis and septic shock (sepsis-3). Jama, 315(8):801–810, 2016.