Monotonic Alpha-divergence Minimisation for Variational Inference

Abstract

In this paper, we introduce a novel family of iterative algorithms which carry out -divergence minimisation in a Variational Inference context. They do so by ensuring a systematic decrease at each step in the -divergence between the variational and the posterior distributions. In its most general form, the variational distribution is a mixture model and our framework allows us to simultaneously optimise the weights and components parameters of this mixture model. Our approach permits us to build on various methods previously proposed for -divergence minimisation such as Gradient or Power Descent schemes and we also shed a new light on an integrated Expectation Maximization algorithm. Lastly, we provide empirical evidence that our methodology yields improved results on several multimodal target distributions and on a real data example.

1 Introduction

Bayesian inference tasks often induce intractable and hard-to-compute posterior densities which need to be approximated. Among the class of approximating methods, Variational inference methods (for example Variational Bayes Jordan et al., 1999; James Beal, 2003) have attracted a lot of attention as they have empirically been shown to be widely applicable to many high-dimensional machine-learning problems (Hoffman et al., 2013; Ranganath et al., 2014; Kingma and Welling, 2014).

These optimisation-based methods introduce a simpler variational family and find the best approximation to the unknown posterior density among this family in terms of a certain measure of dissimilarity, the most common choice of measure of dissimilarity being the exclusive Kullback-Leibler divergence (Blei et al., 2017; Zhang et al., 2019).

However, the exclusive Kullback-Leibler divergence is known to have some drawbacks. Indeed, its zero-forcing behavior is responsible for returning variational approximations with light tails that severely underestimate the posterior covariance and that are unable to capture multimodality within the posterior density (Minka, 2005; Jerfel et al., 2021; Prangle, 2021). This is especially inconvenient when the variational family does not exactly match the posterior density (Yao et al., 2018; Campbell and Li, 2019) and even more so if one wants to appeal to Importance Sampling methods to approximate integrals of interest in a Bayesian Inference setting (Jerfel et al., 2021; Prangle, 2021).

To avoid this hurdle, advances in Variational Inference turned to more general families of divergences such as the -divergence (Zhu and Rohwer, 1995b, a) and Rényi’s -divergence (Rényi, 1961; van Erven and Harremoes, 2014). These families of divergences both recover the exclusive Kullback-Leibler when and thanks to the hyperparameter , they provide a more flexible framework that can bypass the difficulties associated to the exclusive Kullback-Leibler divergence by choosing (Minka, 2005). For this reason, they have notably been used in Minka (2004); Hernandez-Lobato et al. (2016); Li and Turner (2016); Dieng et al. (2017); Wang et al. (2018); Daudel et al. (2021); Daudel and Douc (2021).

In the spirit of Variational Inference methods based on the -divergence, we propose in this paper to build a framework for -divergence minimisation in a Variational Inference context. The particularity of our work is that our algorithms will ensure a monotonic decrease at each step in the -divergence between the variational and the posterior distributions. In addition, our work will apply to variational families as wide as the class of mixture models. The paper is then organised as follows:

-

In Section 2, we introduce some notation and state the optimisation problem we aim at solving in terms of the posterior density, the variational density and the -divergence.

-

In Section 3, we consider the typical Variational Inference case where belongs to a parametric family. In this particular case, we state in 1 conditions which ensure a systematic decrease in the -divergence at each step for all . We then show in 1 that these conditions are satisfied for a well-chosen iterative scheme and we call the resulting approach the maximisation approach. This approach is particularly convenient, a fact that we illustrate over 1 and 1. Furthermore, we derive in 2 additional iterative schemes satisfying the conditions of 1 under the name gradient-based approach, which we then use to underline the links between our approach and Gradient Descent schemes for -divergence and Rényi’s -divergence minimisation.

-

In Section 4, we extend the results from Section 3 to the more general case of mixture models. We derive in Theorems 2 and 3 conditions to simultaneously optimise the weights and the components parameters of a given mixture model, all the while maintaining the systematic decrease in the -divergence initially enjoyed in Section 3. These conditions are then met in 4 and 5, which respectively generalise the maximisation approach of 1 and the gradient-based approach of 2 to the case of mixture models.

-

Section 5 is devoted to related work. We explain in more detail the links between our framework and existing Variational Inference methods for -divergence minimisation. We also connect our approach to the Power Descent algorithm from Daudel et al. (2021) and provide in 2 additional monotonicity results which go beyond the case . In addition, we obtain that an integrated Expectation Maximization algorithm introduced in Cappé et al. (2008) can be recovered as a special case of our framework.

-

In Section 6, we state generic results that solve our maximisation and gradient-based approaches when the variational family is based on the exponential family. More specifically, we introduce in Section 6.1 additional notation for the exponential family and we recall several of its useful properties. Section 6.2 and Section 6.3 then focus on the maximisation approach and gradient-based approach respectively and notably provide the theoretical justification behind some special cases mentioned earlier in the paper, such as Gaussian densities in 1. Lastly, Section 6.4 extends once again the maximisation approach in order to incorporate variational families that were not previously included in our framework, yet draw on the exponential family (such as multivariate Student’s densities in 5).

-

In Section 7, we focus on the important case of Gaussian Mixture Models (GMMs) and we discuss practical implementations of our algorithms for GMMs optimisation.

2 Notation and Optimisation Problem

Let be a measured space, where is a -finite measure on . Assume that we have access to some observed variables generated from a probabilistic model parameterised by a hidden random variable that is drawn from a certain prior . The posterior density of the latent variable given the data is then given by

where is called the marginal likelihood or model evidence. For many interesting choices of models, sampling directly from the posterior density is impossible and the marginal likelihood is also unknown or too costly to compute.

To address this difficulty, Variational Inference methods approximate the posterior density by a simpler probability density belonging to a given variational family (from which it is easy to sample from). They select the best probability density in by solving an optimisation problem that involves a certain measure of dissimilarity, which is chosen to be the -divergence in this paper due to its advantages compared to the more traditional exclusive Kullback-Leibler divergence (see for example Minka, 2005).

More precisely, let us denote by the probability measure on with corresponding density with respect to . As for the variational family, let us denote by the probability measure on with associated density with respect to . We let be the convex function on defined by , and for all . Then, assuming that both and are absolutely continuous w.r.t. , the -divergence between and (extended by continuity to the cases and as for example done in Cichocki and Amari, 2010) is given by

| (1) |

and the Variational Inference optimisation problem we aim at solving is . Notably, it can easily be proven that this optimisation problem is equivalent to solving

| (2) |

where, for all measurable non-negative function on and for all , we have set

As the unknown constant does not appear anymore in the optimisation problem (2), this formulation is often preferred. Therefore, we consider the general optimisation problem

| (3) |

where is any measurable positive function on . Note that we may drop the dependency on in for notational ease and when no ambiguity occurs.

At this stage, we are left with the choice of the variational family appearing in the optimisation problem (3). The natural idea in Variational Inference and the starting point of our approach is then to work within a parametric family : letting be a measurable space, be a Markov transition kernel on with kernel density defined on , we consider a parametric family of the form

3 An Iterative Algorithm for Optimising

In this section, our goal is to define iterative procedures which optimise with respect to and which are such that they ensure a systematic decrease in at each step. For this purpose, we start by introducing some mild conditions on , and that will be used throughout the paper.

-

(A1)

The kernel density on , the function on and the -finite measure on satisfy, for all , , and .

From this point onwards, and as announced in the previous section, we will drop the dependency on in for notational convenience. Let us now construct a sequence valued in such that the sequence is decreasing. The core idea of our approach will rely on the following proposition.

Proposition 1.

Proof.

We treat the two cases and separately.

-

(a)

Case with for all . This case is immediate since

- (b)

∎

This result then allows us to deduce 1 below.

Theorem 1.

Proof.

At this point, we seek to find iterative schemes satisfying (5). To do so, for all , all and all , we introduce the notation:

| (6) | ||||

Note that under (A1), the normalisation in satisfies , where the right inequality in particular follows from Jensen’s inequality applied to the strictly concave function . We then state our first corollary.

Corollary 1 (Maximisation approach).

Proof.

We now make three comments regarding 1.

-

•

The r.h.s. of (7) can be simplified, yielding the equivalent iterative scheme

provided that for all .

-

•

While it suffices to find any so that (5) holds to obtain a systematic decrease in , defining as in (7) enables us to solve this argmax problem for notable choices of kernel density . A remarkable aspect is indeed that (7) is written as a maximisation problem involving the logarithm of the ratio whereas is not directly expressed in terms of logarithm of this ratio for . As a result, we can use the maximisation approach of 1 to derive simple update rules for . An example and a lemma are provided thereafter to illustrate this fact and more general results regarding exponential families will follow later in Section 6.

- •

We next provide a motivating example where the maximisation approach is applicable.

Example 1 (Maximisation approach for a Gaussian density).

We consider a -dimen-sional Gaussian density, in which case , is the -dimensional Lebesgue measure and , where denotes the mean and covariance matrix of the Gaussian density. We let the parameter set include all possible means in and all possible positive-definite covariance matrices . Finally, denoting by the Euclidean norm, we assume that the non-negative function defined on satisfies

| (8) |

Then (A1) holds. Furthermore, starting from any so that and denoting for all , it holds that: for all and all , there exists such that the argmax problem (7) has a unique solution defined by

| (9) | ||||

where, using the definition of in (6), we set

Here, the detailed derivation of (9) is deferred to Section 6.2 as we focus on interpreting this result in light of 1 (in particular we will see in 6 that the case corresponding to will require an additional non-degenerate condition on ). By 1, the systematic decrease in holds for any choice of sequence valued in in the updates (9). In addition, permits us to build a tradeoff at time between selecting an update close to the current parameter (that is, taking close to zero) and choosing the Gaussian density with exactly the same mean and covariance matrix as (that is, setting ). This is a key idea that is linked to the regularisation term appearing in (7) and that we will revisit several times throughout the paper.

The maximisation approach of 1 is also applicable to the commonly-used mean-field variational family, which approximates the true density by a density with independent components parameterised separately. The following lemma indeed states that the global argmax problem can be separated into component-wise argmax problems in that case.

Lemma 1 (Maximisation approach for the mean-field family).

A generic member of the mean-field variational family is given by with and . Then, starting from and denoting for all , solving (7) yields the following update formulas:

The maximisation approach is not the only way to satisfy (5). Indeed, this can also be achieved by taking a gradient-based approach and relying on additional smoothness conditions (see Section A.1 for the definition of -smoothness), as written in 2.

Corollary 2 (Gradient-based approach).

Proof.

Let us now reflect on the implications of 2. Under common differentiability assumptions, we can write: for all and all

Then, (10) becomes

| (12) |

Under this form, the iterative scheme (12) bears similarities with Gradient Descent iterations for -divergence and Rényi’s -divergence minimisation. Indeed, given a learning rate policy and setting , such Gradient Descent iterations are given respectively by

(we refer to Section A.2 for details regarding how these updates are obtained). Building on this comment, let us now give an example where the conditions on from 2 are satisfied and show how Gradient Descent steps (in that case for Rényi’s -divergence minimisation) can originate from our gradient-based approach.

Example 2 (Gradient-based approach for a Gaussian density).

We consider the case of a -dimensional Gaussian density with , where this time . Further assume that is a convex subset and that , where and denotes the -dimensional identity matrix. Finally, denoting by the Euclidean norm, we assume that the non-negative function defined on satisfies

| (13) |

Then, (A1) holds. Furthermore, denoting and setting for all , the conditions on from 2 are satisfied so that the mean of the Gaussian density can be optimised as follows: for all and all

| (14) |

where (we refer to 8 for the detailed derivation). Setting , the update (14) can notably be seen as a Gradient Descent step for Rényi’s -divergence minimisation with a learning rate , where .

We now make two important comments.

-

•

2 sheds light on the links between our approach and the more traditional Gradient Descent methodology for optimising objective functions based on the -divergence in Variational Inference (Li and Turner, 2016; Dieng et al., 2017).

Unlike the usual Gradient Descent methodology, 2 requires a smoothness condition on . Smoothness conditions are tools that are often used to obtain stronger convergence guarantees for Variational Inference algorithms (see for example Buchholz et al., 2018; Alquier and Ridgway, 2020). Yet, it can be difficult to satisfy these smoothness assumptions in practice, even if some results have been derived for specific variational families when using the exclusive Kullback-Leibler divergence as the objective function (Domke, 2020).

To the best of our knowledge, no such results have been proven for -divergence minimisation. In our case, we obtain that a smoothness condition on translates into a systematic decrease in . As we shall see in the forthcoming section, being able to establish monotonicity results on will come in handy as we try to go beyond the framework considered in Section 3.

-

•

To put things into perspective with the maximisation approach from earlier, observe that the updates on the means in Examples 1 and 2 coincide. The difference between the two examples is due to the fact that the former provides an update for the covariance matrix as well, without sacrificing the monotonicity of the overall algorithm. It is in fact hard to derive a covariance matrix update in the Gaussian case using the gradient-based approach (see Section 6.3 for details). In that sense, the maximisation approach provides an interesting alternative that can bypass this difficult smoothness assumption on . We will further delve into this aspect as we reach Section 6.

So far, the function appearing in 1 considerably eased the derivation of iterative update formulas for well-chosen kernel densities that can exploit this log structure (Examples 1-2 and 1). Yet, these choices of kernel densities can be too restrictive to fully capture complex and multimodal posterior densities. Since working with a larger variational family might lead to more accurate approximations of the posterior density, an idea is then to investigate whether the iterative update formulas from Section 3 can be generalised to the mixture model variational family (for example whether we can extend the updates for a Gaussian kernel from 1 to Gaussian Mixture Models).

As we shall see in the next section, further theoretical developments will be required in order to derive valid iterative schemes that optimise both the mixture weights and the mixture components parameters of a given mixture model.

4 Extension to Mixture Models

Let us first formally define the class of mixture models we are going to be working with. Given , we introduce the simplex of :

we define and we denote . We consider the mixture model variational family given by

| (15) |

that is, we are interested in solving the optimisation problem

with . Let us next denote and for all . For convenience, we also introduce the shorthand notation and

| (16) | ||||

for all , all , all and all .

Our goal in this section is to derive iterative schemes for the mixture weights and the mixture components parameters ensuring that the sequence is decreasing. As 1 holds for any choice of parametric family, a first idea is to apply 1 to the variational family (15), which gives 3 below.

Corollary 3.

Assume (A1). Let , let and starting from an initial parameter set , let be defined iteratively such that for all ,

| (17) |

Further assume that . Then, for all .

Observe that we are in a less favourable situation in 3 with compared to the cases we previously studied in Section 3. Indeed, we now have a ratio of sums inside the function in (17), meaning that the approach from 1 to derive simple iterative schemes does not directly transfer to the variational family (15) for choices of kernel densities identified in Examples 1-2 and 1. However, by carefully exploiting the condition (17), we are able to overcome this difficulty in our second main theorem below.

Theorem 2.

Assume (A1). Let , and starting from an initial parameter set , let be defined iteratively such that for all ,

| (18) | |||

| (19) |

Further assume that . Then, for all .

Proof.

By 3, we can conclude if we show that (18) and (19) together imply (17). To show this, first observe that since the function is convex and , Jensen’s inequality implies that: for all and all ,

that is:

Multiplying by on both sides, integrating with respect to and using the definition of in (16), this in turn implies that: for all ,

As a consequence, the condition

| (20) |

implies (17). The condition (20) in itself is then straightforwardly implied by (18) and (19) and the proof is concluded. ∎

Strikingly, (18) does not depend on nor does (19) depend on in 2. This means that we can treat these two conditions separately and thus that the weights and components parameters of the mixture can be optimised simultaneously. This result was far from immediate by looking at the initial condition (17) and, as we shall see laterly in Section 8, will lead to reduced computational power in practice.

In addition, we have recovered in (19) the key property used in Section 3: compared to the condition (17) which involved the of weighted sums of kernel densities, (19) considers a sum of logs of kernel densities. This suggests that we can extend the updates derived in Section 3 for well-chosen kernel densities to the more general case of mixture models.

Observe finally that the dependency in appearing in (18) is simpler than the dependency in appearing in (19) and that is expressed through the kernel density . As a result, we will first study (18), in the hope of deriving iterative update formulas for the mixture weights that do not require a specific choice of kernel density . Interestingly, while the natural idea is to perform direct optimisation of the left-hand side of (18), we will derive a more general expression for the mixture weights update, which shall induce numerical advantages later illustrated in Section 8.

4.1 Choice of

In the following theorem, we identify an update formula which satisfies (18), regardless of the choice of the kernel density .

Theorem 3.

Proof.

We first check that the integrals appearing in (21) are finite:

| (22) |

Using (16), that , that and Jensen’s inequality applied to the concave function , we have, for any and ,

The bound (22) follows by (A1). Now, to prove (18), we treat the cases and separately.

-

(a)

Case . Since with , we have that

where we have used that . In other words, to obtain (18) in the particular case , it is enough to show

that is, since (22) holds,

(23) Notice then that by definition of when , we can write

[Indeed, setting and for all , we have that and that this quantity is minimal when for .] This implies (23) and settles the case .

-

(b)

For the particular case , we will use that for all and all ,

Indeed, since for all , we can then write that for all ,

(24) Now notice that by definition of we can write

when satisfies . [Indeed setting and for all , we have by convexity of the function that and that this quantity is minimal when for .] We then deduce that taking (it is always possible since by assumption) yields

which in turn yields (18) [since combined with (24) it implies (23) which itself implies (18) as seen in the case ]. This settles the case .

∎

Notice that as a byproduct of the proof of 3, the mixture weights update given by (21) can be rewritten under the form: for all ,

where, setting , we have defined for all ,

More specifically, acts as an upper bound of the left-hand side of (18) and we recover exactly the left-hand side of (18) in the particular case and .

Now that we have established the mixture weights updates (21) in 3, we are interested in deriving update formulas for the sequence satisfying (19), which we will then pair up with (21) in order to apply 2. From this point onwards, all the proofs of the coming results will be deferred to the appendices to ease the reading.

4.2 Choice of

We investigate two different approaches for choosing .

4.2.1 A Maximisation Approach

As done in 1, an idea is to consider an update for of the form

where the function is constructed as a lower bound on of the function that satisfies . In doing so, the function evaluated at is an upper bound of the left-hand side of (19) and implies (19). This leads us to 4 below.

Corollary 4 (Generalised maximisation approach).

Assume (A1). Let , let be valued in and let be such that at all times . Furthermore, let be a non-negative sequence for all . Starting from an initial parameter set , let be defined iteratively for all in such a way that (21) holds and

| (25) |

where we assume that this argmax is uniquely defined at each step. Then, we can apply 2.

The proof of this result is deferred to Section B.1. Under the assumptions of 4, Algorithm 1 leads to a systematic decrease in at each step. This result effectively generalises the monotonicity property from 1 to the case of mixture models and we can deduce simple iterative schemes satisfying (25) for well-chosen kernel densities . To illustrate this, we provide below the extension of 1 to Gaussian Mixture Models (and 1 can be extended in the same way, see Section B.2).

Example 3 (Maximisation approach for Gaussian Mixture Models).

We consider the case of -dimensional Gaussian mixture densities, in which case , is the -dimensional Lebesgue measure and , where denotes the mean and covariance matrix of the -th Gaussian component density. We let the parameter set include all possible means in and all possible positive-definite covariance matrices. Finally, we assume that the non-negative function defined on satisfies (8).

Then (A1) holds. Moreover, starting from any so that and denoting for all and all , it holds that: for all , all and all , there exists such that the argmax problem (25) has a unique solution defined by:

where, using the definition of in (16), we set

The detailed derivation of the mean and covariance updates above is deferred to Section 6.2. The interpretation of these updates is akin to the one already made in 1: acts as a regularisation parameter which, through , permits a tradeoff between an update close to the current parameter and choosing the Gaussian density with exactly the same mean and covariance matrix as . As per written in 4, these updates are compatible with the mixture weights updates (21), resulting in a systematic decrease of .

We next present another possible update formula for .

4.2.2 A Gradient-based Approach

Corollary 5 (Generalised gradient-based approach).

Assume (A1). Let be a convex set, let , let be valued in and let be such that at all times . Furthermore, for all , let be valued in . Starting from an initial parameter set , let be defined iteratively for all in such a way that (21) holds and

| (26) |

where for all , is defined by: for all and all ,

and is assumed to be -smooth. Then, we can apply 2.

The proof of this result is deferred to Section B.3. Under the assumptions of 5, Algorithm 2 ensures a systematic decrease in at each step and 5 thus extends 2 to mixture models. Much like what we did for 2, we want to identify how our updates relate to Gradient Descent-based techniques for optimising . Under common differentiability assumptions, we have: for all , all and all ,

so that (26) becomes

| (27) |

The link with Gradient Descent-based Variational Inference shall become apparent by (i) writing the update formulas that ensue from Gradient Descent iterations for -divergence and Rényi’s -divergence minimisation and (ii) understanding how 2 generalises to Gaussian Mixture Models. Given , an index in and letting , performing one Gradient Descent iteration w.r.t. for -divergence and Rényi’s -divergence minimisation indeed respectively amounts to updating as follows

where is the learning rate (we refer to Section B.4 for details regarding these updates). There is thus a similarity between (27) and the Gradient Descent updates above. To fully comprehend the connection between our gradient-based approach and Gradient Descent steps, we present below the generalisation of 2 to Gaussian Mixture Models. The smoothness assumption on will be satisfied in that example and we will recover a Gradient Descent scheme for Rényi’s -divergence minimisation as a special case.

Example 4 (Gradient-based approach for Gaussian Mixture Models).

We consider the case of -dimensional Gaussian mixture densities with , where this time . Further assume that is a convex subset and that , where and denotes the -dimensional identity matrix. Finally, we assume that the non-negative function defined on satisfies (13).

Then, (A1) holds. Setting and denoting , the function is -smooth for all and all so that the means of the Gaussian densities can be optimised as follows: for all ,

where is defined in (16), and (we refer to 8 for details). In particular, letting be valued in for all ,

(since ). The resulting iterative algorithm is given by the following update at time :

| (28) |

Interestingly, (28) can be seen as a Gradient Descent step w.r.t. for Rényi’s -divergence minimisation with a learning rate . Hence, if we were to solely rely on the Gradient Descent literature, the convergence of the iterative sequence defined by (28) would require the sequence to be constant. This is in contrast with 5, which allows for a simultaneous optimisation of and according to (21) and (28).

We now add on the comments made in Section 3 for the gradient-based methodology (which we built in 2 and have since extended to mixture models in 5):

-

•

A core insight from 5, which is exemplified in 4, is that under a smoothness assumption on our mixture weights iterative updates are compatible with gradient-based updates, themselves linked to the Gradient Descent literature. In other words, we have embedded Gradient Descent-based iterative updates, which only act on , within a larger framework where simultaneous updates for the mixture components parameters and the mixture weights are well-supported theoretically.

-

•

Putting things into perspective with the maximisation approach once again, notice that our previous conclusions from Section 3 still hold. Namely: (i) the updates on the means from Examples 3 and 4 coincide, meaning that contrary to the gradient-based approach, the maximisation approach enables covariance matrices updates on top of means updates (ii) the maximisation approach permits us to bypass the smoothness assumption made in 5. As a whole, these properties make the maximisation approach a compelling alternative to the gradient-based approach.

We presented two approaches to construct iterative schemes that ensure a monotonic decrease in at each step and lead to simple updates formulas for Gaussian Mixture Models. We now describe how our framework can be linked to the existing literature.

5 Related Work

In this section, we detail how our work relates to and improve on previous algorithms proposed for -/Rényi’s -divergence minimisation.

5.1 Rényi Divergence Variational Inference (Li and Turner, 2016)

In Li and Turner (2016), they seek to maximise the Variational Rényi (VR) Bound via (Stochastic) Gradient Ascent. This objective function is derived from Rényi’s -divergence and is given by: for all variational density and all ,

| (29) |

Contrary to us, the work from Li and Turner (2016) does not consider the case where belongs to the mixture models variational family (15), that is .

Yet, a parallel can be drawn in the GMM case between Li and Turner (2016) and our approach by observing that the gradient-based updates on the means in 4 each coincide with a Gradient Ascent step on the objective function (29) for a well-chosen learning rate (since the gradient of is proportional to the gradient of Rényi’s -divergence with a factor , this follows from the remarks made in Section 4.2.2 regarding Gradient Descent steps for Rényi’s -divergence minimisation in the GMM case).

Our work hence provides a theoretical framework which enables simultaneous optimisation of the mixture weights and of the mixture components parameters . In addition, beyond the gradient-based updates, we propose the novel maximisation updates and we allow for covariance matrices optimisation. We also emphasise that our maximisation approach will apply to well-chosen kernels beyond the Gaussian case, as we will detail in Section 6.

5.2 The Power Descent Algorithm (Daudel et al., 2021)

In order to identify the connection between our work and the Power Descent algorithm introduced in Daudel et al. (2021), let us briefly present the latter.

The Power Descent is a gradient-based algorithm that operates on probability measures and performs -divergence minimisation for all . More precisely, equipping with a -field and denoting by the space of probability measures on , the Power Descent optimises with respect to , where for all and all . Given an initial probability measure , it does so by performing several one-step transitions of the Power Descent algorithm:

| (30) |

where, for all and all ,

Daudel et al. (2021) motivated the Power Descent algorithm by establishing a monotonicity result for this algorithm obtained as a particular case of (Daudel et al., 2021, Theorem 1). In their result, the monotonic decrease in of the scheme (30) holds for all , all , all and all such that . We provide below a more general version of their result, where the monotonic decrease in holds for well-chosen values of that are larger than when (we refer to Section B.5 for the proof of this result).

Proposition 2.

Assume that and are as in (A1). Let belong to any of the following cases.

-

(i)

and ;

-

(ii)

and ;

-

(iii)

or and .

Moreover, let be such that and let be such that . Then, the two following assertions hold.

-

(i)

We have .

-

(ii)

We have if and only if .

Building on the monotonicity result provided by (Daudel et al., 2021, Theorem 1) for the Power Descent algorithm - that we generalised in 2 - Daudel et al. (2021) then applied this algorithm to mixture weights optimisation by letting the initial probability measure be a weighted sum of Dirac measures of the form , with and . For that choice of , in (30) can be written as at time and the Power Descent amounts to performing the update

| (31) |

Interestingly, the update (31) corresponds to the update on the mixture weights (21) we have identified in 3 for , and . Steaming from this link between our approach and Daudel et al. (2021), we now make two important comments.

-

•

Benefits of our approach compared to Daudel et al. (2021). The monotonicity result from Daudel et al. (2021) generalised in 2 requires the sequence to be constant when applied to mixture weights optimisation in (31). This restricts the variational family to mixture models with fixed mixture components parameters. To remedy this problem, Daudel et al. (2021) proposed a fully-adaptive algorithm that alternates between an Exploitation step optimising the mixture weights according to (31) and an Exploration step acting on the mixture components parameters. However, they established no theoretical guarantees for their complete Exploitation-Exploration algorithm, as the choice of the Exploration step remained mostly unexplored.

A strong improvement of our approach is then that we provide theoretically-sound updates for , with the particularity that our mixture weights updates relate to the framework of Daudel et al. (2021). In that sense, our approach supplements the work done in Daudel et al. (2021) (albeit by an entirely different proof technique). Furthermore, we do not need to alternate between mixture weights and mixture components parameters updates in our algorithms, as both can be carried out simultaneously (as done in Algorithms 1 and 2). In practice, this will permit us to reduce the computational cost (as the samples will be shared throughout the mixture weights and the mixture components parameters approximated updates, see Section 7).

-

•

A gradient-based mixture weights update. Daudel et al. (2021) establishes that the Power Descent belongs to a family of gradient-based algorithms which includes the Entropic Mirror Descent algorithm, a typical optimisation algorithm for optimisation under simplex constraints, as a special case. Viewed from this angle, the parameter in (31) can be understood as a learning rate with playing the role of the gradient of . Connecting the Power Descent to our framework thus sheds light on the gradient-based nature of the mixture weights update (21) from 3 and provides a better understanding of the role of the parameter appearing in this update. This aspect will be helpful to interpret our numerical experiments in Section 8.

5.3 The M-PMC Algorithm (Cappé et al., 2008)

For any measurable positive function on , the M-PMC algorithm (Cappé et al., 2008) aims at solving the optimisation problem

or equivalently, at minimising the inclusive Kullback-Leibler divergence w.r.t. to , where for all . This is done in (Cappé et al., 2008, Section 2) by introducing the following iterative updates: for all and all ,

Cappé et al. (2008) motivated the two updates above by noticing that they can be seen as integrated versions under the target distribution of the update formulas for the Expectation-Maximisation (EM) algorithm applied to the mixture density parameter estimation problem

meaning that these updates ensure a systematic increase in the integrated likelihood at each step. As these updates also correspond to the case , , , and in Algorithm 1, the M-PMC algorithm is in fact included in our framework and we can interpret our theoretical results in light of this algorithm.

More precisely, we have generalised an integrated EM algorithm by preserving its monotonicity property for a wide range of hyperparameters. A particularly striking fact is that the monotonicity property holds for , hence updates akin to an EM procedure can be derived past the traditional case of likelihood optimisation. As we shall see, the additional layers of flexibility obtained in Algorithm 1 will also have important practical consequences due to the underlying gradient-based structure behind the mixture weights (and the mixture components parameters updates in the GMMs case) we have uncovered.

Table 1 summarises the main improvements of our framework compared to the existing literature and in the coming section, we revisit the maximisation and the gradient-based approaches when the variational family is based on the exponential family.

| Improvements of our framework | |

| Rényi Gradient Descent | Simultaneous optimisation w.r.t. |

| Li and Turner (2016) | (prev. mixture weights optimisation not considered) |

| For GMMs : maximisation approach encompasses Rényi | |

| Gradient Descent and provides covariance matrices updates | |

| Power Descent | Simultaneous optimisation w.r.t. |

| Daudel et al. (2021) | (prev. constant) |

| M-PMC algorithm | Extension of an Integrated EM algorithm to: |

| Cappé et al. (2008) | , , and |

| (prev. , , and ) |

6 Exponential Family Distributions: a Closer Look

In this section, we state generic results for the maximisation and the gradient-based approaches in the important case where the variational family is based on the exponential family. Those results will in particular enable us to show how the update formulas in Examples 3 and 4 are derived, before allowing us to incorporate novel variational families in our framework such as multivariate Student’s densities. To do so, let us first review the exponential family and some of its well-known properties.

6.1 Notation and Useful Definitions

We start with the definition of an exponential family distribution.

Definition 1 (Exponential family).

Let be a -finite measure on , be a Euclidean space endowed with an inner product and its corresponding norm , be a non-negative function defined on and be a measurable function. In its canonical form, a member of the exponential family is defined by the parametric probability density

where

and where the values taken by on the subset are obtained from the normalising constraint . In this setting, is called the dominating measure and the natural statistic. In what follows, denotes the interior of .

Recall now that defines an exhaustive statistic for this model, that is a convex subset of and that is infinitely differentiable in . Moreover, for all , the expectation and covariance operator of under the density are the gradient and the Hessian of taken at , respectively. For later reference, we also recall

| (32) |

and we introduce the following assumption.

-

(B1)

The kernel density defined on is a member of the exponential family as in 1. Moreover, we assume that:

-

(a)

The function on is positive.

-

(b)

There is no affine hyperplane of to which belongs for -almost all .

-

(a)

Notice that the assumption (B1)(B1)(a) can be circumvented by changing the dominating measure and therefore the assumptions (B1)(B1)(a) and (B1)(B1)(b) should be considered together. These assumptions notably imply that the covariance operator of under the density is positive definite and thus so is for all . In addition, one often relies on a non-canonical parameterisation (see for example 1), leading to the kernel density

| (33) |

where maps the parameter space to a subset of . In that case, the assumption (B1)(B1)(a) will ensure that the assumption made on in (A1) holds.

6.2 The Maximisation Approach for the Exponential Family

Recall that the maximisation approach proposed in 1 aims at solving the optimisation problem (7) given by

Furthermore, in the more general case of mixture models described in 4, the maximisation approach leads to the argmax problem (25). This second argmax problem is similar to (7) in the sense that it updates by solving component-wise argmax problems of the same form as (7) (with , , and being replaced by , , and , for ):

Our goal is now to solve the argmax problems above for a member of the exponential family. To do so, we first state a theorem in which the kernel is in its canonical form, that is is the identity mapping in (33) and . Other parameterisations will then be built using this theorem and as a result we will deduce corollaries that include non-canonical parameterisations and that are applicable to the general case of mixture models. All the proofs of the results stated in Section 6.2 are deferred to Section C.2.

Theorem 4.

4 shows the equivalence between the argmax problem (35) and the equation (37) under the canonical parameterisation. From there, using the expression of given in (32) and considering the non-canonical exponential family probability density (33), we can interpret the equation (37) as an equality between two means of the statistic computed under two different distributions. Setting and , we indeed obtain

| (38) |

where is the mixture

As exemplified in the following corollary, an adequate parameterisation may then lead to a simple solution of (38), which in turn provides a solution to the argmax problem

| (39) |

Corollary 6 (Gaussian density).

Let and . Let denote the set of symmetric positive definite matrices. We consider the case of a -dimensional Gaussian density with , where . Let be a probability density function on such that (34) holds, that is in the Gaussian case

Let and . If , assume moreover that is non-degenerate in the sense that its covariance matrix is positive definite. Then (39) has a unique solution defined by and , where is a random variable valued in with density

It now remains to choose adequately to relate (39) to (7), or rather to its generalisation (25). That way, we will in particular get that the update formulas given in Examples 1 and 3 are straightforward consequences of 6. This is the purpose of 7 below, in which we also rewrite the assumption (34) made on under a more convenient form.

Corollary 7.

Let satisfy (B1). Further assume that the kernel is of the form (33) with a one-to-one mapping defined on such that its image is an open subset of . Let and let be such that

| (40) |

holds. Let , and . Then, for all , (34) holds with as defined in (16) and setting , we have that

| (41) |

admits at least a solution if and only if

| (42) |

belongs to the image set , in which case (41) has a unique solution defined by

Since the argmax problem (41) is immune to change of variables thanks to its argmax form, the maximisation approach can be solved using the canonical parameter in 4 and transported to the parameter via the one-to-one mapping as written in 7.

The updates from Examples 1 and 3 then follow from 7, paired up with 6 and with the fact that (40) simplifies to (8) (since in the Gaussian case we have set for all ). More generally, we can always solve the argmax problem (41), that is the argmax problem of 4 with belonging to the exponential family, for large enough.111Under the assumptions of 7, is an open subset of and is a -diffeomorphism on . Hence, is an open subset of . Since in (42) tends to as , ends up belonging to for large enough. The desired result follows by using that the regularisation parameter in 4 can be freely chosen at each step .

We now move on to the study of the gradient-based approach for the exponential family.

6.3 The Gradient-based Approach for an Exponential Family Distribution

Remember that to construct the sequence according to the gradient-based approach from 2 we need to compute the gradient of the function defined in (11) by

and verify that satisfies a -smoothness condition, which leads to updates of the form

with . Furthermore, the extension to mixture models in 5 involves the gradient of functions that resemble (, and are replaced by , and in the definition of above) and where each function is assumed to be -smooth.

Let us now solve the gradient-based approach for a member of the exponential family. Like in the previous section, we start with a result handling the case where the kernel is in its canonical form (that is, is the identity mapping in (33) and ). All the proofs of the results stated in Section 6.3 are deferred to Section C.3.

Proposition 3.

Letting be the line segment in 3, we have that stays in for large enough. Since the Hessian of is continuous on , the inequality in (44) can also be satisfied. Hence, the following gradient step

| (45) |

can always be performed for all and we can always apply the gradient-based approach when the kernel is in its canonical form. When considering non-canonical exponential family probability densities of the form (33) and under some reasonable assumptions on the mapping (for instance, if is a diffeomorphism), one is left with choosing between two alternative ways of exploiting 3:

-

(i)

Apply a gradient step on the canonical parameter using the objective in (43) and translate it into an update of the parameter via a change of variable. In this case, we set , we apply the step (45) and we then perform the change of variable to get back to a parameter in . Overall, this leads to an update of the form

-

(ii)

Apply a gradient step directly on the parameter using the objective

In that case, since where is again as in (43) with , this leads to an update of the form

In both approaches, and the smoothness indices and have to be taken large enough in order to guarantee a decrease of the objective function. In practice, it is not clear which parameterisation leads to the simpler or more efficient algorithm. We investigate a particular setting in the following result.

Corollary 8 (Gaussian density with known covariance matrix).

Let and . We consider the exponential family of a -dimensional Gaussian density with , where and is a (known) covariance matrix in . Let be a probability density function w.r.t. such that (34) holds, that is in the Gaussian case

Set and define the canonical kernel with , and . Then (33) holds and the methods (i) and (ii) lead to the the following gradient-based updates, respectively,

| (46) | ||||

| (47) |

where is the largest eigenvalue of and is the largest eigenvalue of . They correspond to the smoothness indices of and over , respectively.

8 illustrates how, even in a simple framework, the gradient-based updates strongly depend on the parameterisation chosen. They in fact coincide only if is scalar in the above corollary, in which case and above are both equal to the identity matrix.

Following the reasoning of Section 6.2, we can then apply 8 with (and more generally with ). As (34) is implied by (13) (using 8 in Section C.2 and that here ), this enables us to deduce the updates in Examples 2 and 4. Note that we did not introduce a convex subset in 8 (this is due to the fact that the smoothness index is constant over the whole parameter space for both gradient-based updates in that case), which is why does not appear in Examples 2 and 4.

Let us next put into perspective 6, in which we considered a Gaussian density with varying mean vector and covariance matrix, and 8, where the covariance matrix is assumed to be known. While 8 kept the computations straightforward and provided gradient-based updates that do not require to introduce a convex subset , this is no longer the case if we take the same exact setting as in 6. Indeed, when and under the condition (34), the gradient of is given by

The smoothness index is now no longer constant here, which makes it much more involved to choose a convenient convex subset and to bound the smoothness index over it.

At this stage, we can solve the maximisation and gradient-based approaches when the kernel belongs to the exponential family for variational families as large as (finite) mixture models. The maximisation approach appears to be preferable to the gradient-based one as it does not require a smoothness assumption and does not depend on the parameterisation.

In the next section, we investigate how our maximisation approach may further generalise to include extensions of the exponential family distribution such as Student’s distributions, hence further motivating the maximisation approach over the gradient-based approach.

6.4 Extension to Linear Mixture (LM) Models

The goal of this section is to examine what becomes of the maximisation approach for a specific extension of the exponential family distribution, which we will refer to as exponential linear mixture (ELM) family. The ELM family will in particular encompass the Student’s distribution with mean , covariance matrix and degrees of freedom which can be defined as the continuous mixture

where denotes the distribution with degrees of freedom. As a result, building a maximisation approach within the ELM family will lead to new iterative schemes for variational families that go beyond the cases considered thus far. To this end, let us first provide a precise definition of the ELM family we want to study and introduce the main assumptions of this section. All the proofs from Section 6.4 are deferred to Section C.4.

6.4.1 The (E)LM Family: Definition and Notation

Let be an Euclidean space endowed with the inner product and norm . We denote by and the (finite-dimensional) linear spaces of linear operators from to and from to itself, respectively. We now provide the definition of the (E)LM family.

Definition 2 ((E)LM family).

Let be a kernel density w.r.t. the dominating measure , with and let . Set and denote by its Borel -field. Let be a subset of probability measures on satisfying

-

(i)

for all in , the distributions and are equivalent;

-

(ii)

for all and -almost all , the image set is included in .

A member of the linear mixture (LM) family with canonical kernel , mixing class and parameter mapping , is defined for a parameter by the density w.r.t.

| (48) |

If moreover satisfies (B1), we say that is a member of the exponential linear mixture (ELM) family.

Here, Assumption (i) implies that we only need to check Assumption (ii) for one in . As for Assumption (ii), it ensures that for all and all , the function appearing in (48) is a probability density function w.r.t. , so that for all , the function is a probability density function w.r.t. .

Furthermore, the mapping in 2 allows us to introduce various parameterisations. It is also important to note that for , the probability density function only depends on and . As we shall see later, Student’s distributions in particular will fit this general setting. Before that, let us state conditions leading to a systematic decrease in when the kernel is as in 2 and from there, let us see how a maximisation approach for the ELM family can be derived.

6.4.2 Monotonic Decrease Conditions for the (E)LM Family

In the case of an ELM family, we are not able to directly solve the argmax problem (25) as we did for the exponential family in Section 6.2. Instead, given an (E)LM family as in 2, we come back to a monotonic decrease condition of the form

| (49) |

As detailed in the remark below, for selected choices of and of , (49) can indeed be linked to the conditions (5) and (19) appearing in 1 and 2 respectively.

Remark 1.

Let denote the Radon-Nikodym derivative of w.r.t. . We then have the following proposition (we defer the proofs of the results from Section 6.4.2 to Section C.4.1).

Proposition 4 (Conditions for a monotonic decrease within the (E)LM family).

One possible way to obtain (50) is to observe that since the left-hand side of (50) is zero for , (50) is fulfilled by setting

| (53) |

assuming that this argmax is well-defined. This will notably be done later in order to get the update formula (70) of 5 (see the proof of 10 in Section C.4).

As for the updating of , we can again adopt a maximisation approach to derive a convenient . This is the purpose of the following result, where we directly update since is a known mapping in 2.

Corollary 9.

6.4.3 The Maximisation Approach for the ELM Family

Let us show that we can solve an argmax of the form (54) for an adequate choice of by fully exploiting the fact that is a canonical kernel of the exponential family distribution which satisfies (B1) and by relying on additional assumptions to be introduced alongside some helpful notation. Our first assumption is the following.

-

(C1)

The image set is an open subset of and for all , -a.e. is full rank.

(C1) guarantees that, for all , and -almost all in , belongs to , the interior set of (see 9 in Section C.4 for details). This will come in handy in the upcoming derivations and we now introduce some helpful notation, before presenting our next two assumptions. We let denote operator norms, for instance, for any ,

We further denote the adjoint of the linear operator by , for instance, in the case , is defined by

| (55) |

and, for convenience, we also denote

| (56) |

Here, is the function appearing in the definition of an exponential family (1). Recall that is infinitely differentiable on so that by (C1), is well-defined on for -a.e. with . Furthermore, we use and to denote the probability and its corresponding expectation under which the pair has density with respect to . Namely, for any non-negative measurable on ,

| (57) |

We now introduce, for any , two auxiliary functions and , both defined from to , such that the two following conditions hold.

-

(C2)

For all and , we have

-

(C3)

For all and , we have

(C2) and (C3) are made to ensure that the integrals used to solve the argmax problem from 9 will be well-defined. We finally present our last assumption, which corresponds to some sort of identifiability assumption (see 10 in Section C.4 for details). It is used to obtain the uniqueness for the argmax problem we will solve.

-

(C4)

For all and , we have .

We can now state the following result, whose proof can be found in Section C.4.2.

Theorem 5.

Consider an ELM family as in 2 and let . Assume (C1)–(C4) hold. Let be a probability density function w.r.t. such that

| (58) |

define by (52) and set for all such that

| (59) | ||||

| (60) |

Then -a.s., and is well-defined from to and one-to-one on , hence bijective from to its image , and satisfies, for all ,

| (61) |

Moreover, setting , for any , the argmax problem

| (62) |

has at least a solution if and only if

| (63) |

belongs to , in which case (62) has a unique solution defined by

| (64) |

By setting and as well as using (61), (64) can be interpreted as

| (65) |

where denotes the probability having density with respect to and denotes a random variable valued in such that, under , the pair is distributed according to the mixture density

with respect to . Interestingly, the second marginals of these two mixands are . The distribution of under can thus equivalently be defined by saying that and the conditional distribution of given is the mixture with density

Using the definition of on the left-hand side of (65) as well, the latter reads

| (66) |

Hence, 5 along with (66) can be used to solve the argmax problem (54) in the case where (B1) and (C1)–(C4) hold and for with being a non-negative constant. From there, it only remains to find ways to check that the condition (58) on holds. This can notably be done when takes one of the two forms listed in 1 (see 8 in Section C.2 for details) and we now provide an example of particular interest.

Example 5 (Finite mixture of Student’s distributions).

Let be the Lebesgue measure on , with . Let and such that

| (67) |

Let and consider a -mixture family as in (15), with being the density of the Student’s distribution with parameter , given by

Define a sequence valued in where with and such that, for all ,

-

(i)

given valued in , valued in and , is defined by the iterative formula (21);

-

(ii)

given valued in and , is defined by

(68) (69) (70) where, defining as in (16) and denoting the inverse mapping of , we set

(71) (72) (73)

Here, in (73) is the distribution with degrees of freedom and in (70) is well-defined (this follows from 13 in Section C.4.3).

We then have the following result, whose proof is postponed to Section C.4.3.

Corollary 10.

In the setting of 5, if , then, at any time , we have .

We have stated results that solve our maximisation and gradient-based approaches when the variational family is based on the exponential family. However, all the update formulas we have obtained so far involve intractable integrals. In the next section, we focus on the case of Gaussian Mixture Models optimisation seen in Examples 3 and 4 and we investigate how our framework can be used to derive tractable algorithms in that case.

7 Gaussian Mixture Models (GMMs) Optimisation

We consider -dimensional Gaussian mixture densities with , where denotes the mean and covariance matrix of the -th Gaussian component density. By 2, a valid update formula at time for is

| (74) |

Furthermore, as underlined in 3, a valid update at time for the means and the covariances matrices is given by

| (75) | ||||

where , with and . In addition, another possible update for the means is

| (76) |

By virtue of 4, this update can be used in lieu of the means update written in (75) with still in . Since the update (76) is linked to Gradient Descent steps for Rényi’s -divergence minimisation (see 4), we will refer to this update as the Rényi Gradient Descent (RGD) update in the following. One the other hand, the update on the means written in (75) will be referred to as the Maximisation Gradient (MG) update.

Notice that the updates (74), (75) and (76) all involve intractable integrals. However, we can resort to approximate update rules and take advantage of the fact that the integrals appearing in these update formulas are of the form

| (77) |

where is a well-chosen function defined on and where is defined in (16) by for all . Many choices are indeed possible to approximate (77) and for simplicity we restrict ourselves to typical Importance Sampling estimation. Looking at the definition of , a first idea would be to sample i.i.d. random variables according to for and to use the unbiased estimator of (77)

As this sampler depends on , this option becomes very computationally heavy as and increase due to the sampling cost () and to the evaluation cost ( and need to be evaluated times each, where is a sum over ). To reduce this computational bottleneck, it is then preferable to consider sequences of samplers that do not depend on at time . More specifically, we discuss two possibilities.

-

(i)

Best sampler at time (IS-n). Approximated update rules can be obtained by sampling i.i.d. random variables according to the best approximation of we have a time , that is . Then, the samples are shared throughout the mixture weights and mixture components parameters updates. This eases the computational burden, with both a sampling and an evaluation costs of , as an unbiased estimator of (77) is

(78) -

(ii)

Uniform sampler (IS-unif). Approximated update rules can be obtained by sampling according to the uniform sampler and using the unbiased estimator (78). That way, the sampling and evaluation costs are also each. Contrary to IS-n, this sampler ensures a fair sampling among all components, as it entails sampling an index vector uniformly from whereas IS-n samples an index vector according to the mixture weights .

Remark 2.

Approximated update rules for GMMs can be obtained by sampling according to , where is the null vector of dimension . These can be deduced by applying the reparameterisation trick: for all , if with and by observing that an unbiased estimator of (77) is . This choice of relies on the existence of a reparameterisation and while it incurs a gain in terms of sampling cost as we only need samples, the evaluation cost remains .

We thus have access to tractable algorithms that iteratively update both the weights and components parameters of a GMM by optimising the -divergence between the mixture distribution and the targeted distribution. Our framework also allows the use of learning rates that are dependent on . This means that the learning rates can differ for each component parameters update and it paves the way for adaptive learning rates per components. This aspect is left for future work as we will focus on the case according to Algorithm 3 and move on to presenting our numerical experiments.

-

1.

Draw independently samples from the proposal .

-

2.

For all ,

-

(a)

Set and .

-

(b)

Choose one between the (MG) and (RGD) approaches

and set

-

(a)

Remark 3.

Computing the estimator (78) can be expensive for two reasons: (i) involves a sum over so that evaluating this function requires heavier computations as the number of components grows and (ii) bayesian applications with often consider large-scale data sets . To alleviate this computational burden, one can (i) approximate the summation appearing in using subsampling and (ii) use a mini-batch approach to approximate , as detailed in (Li and Turner, 2016, Section 4.3).

8 Numerical Experiments

In our numerical experiments, we are interested in understanding the behaviour of Algorithm 3 in practice. We first investigate the challenging case of multimodal targets, as our framework is designed to handle multimodality thanks to the hyperparameter and to the use of mixture models as a variational family.

8.1 Toy multimodal targets

Let be the -dimensional vector whose coordinates are all equal to , be the identity matrix and be a positive constant (we set ). We consider three multimodal examples:

-

(i)

Equally-weighted Gaussian Mixture Model. The target is a mixture density of two equally-weighted -dimensional Gaussian distributions multiplied by such that

-

(ii)

Imbalanced Gaussian Mixture Model. The target is a mixture density of three -dimensional Gaussian distributions with unequal weights and multiplied by such that

-

(iii)

Equally-weighted Student’s Mixture Model. The target is a mixture density of two equally-weighted -dimensional Student’s distributions with two degree of freedom (i.e. ) multiplied by such that

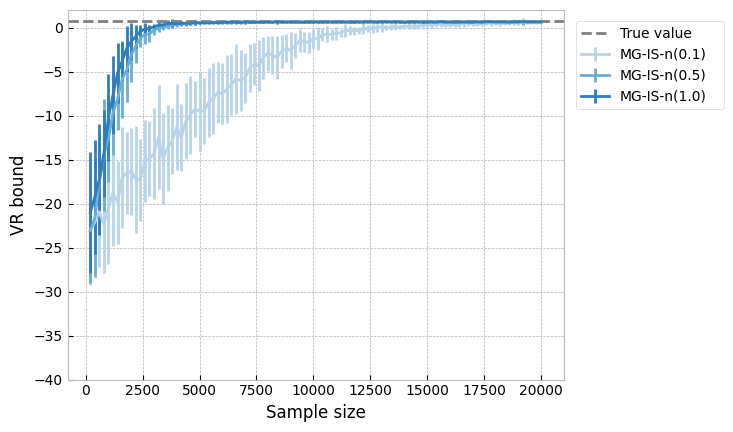

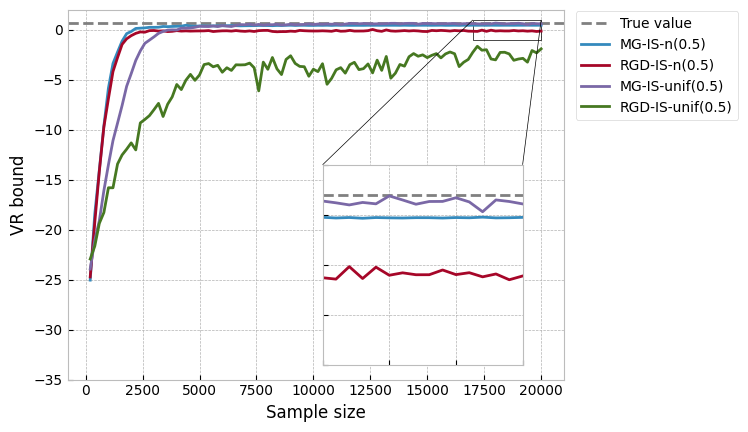

8.1.1 Comparing the RGD and the MG Approaches with

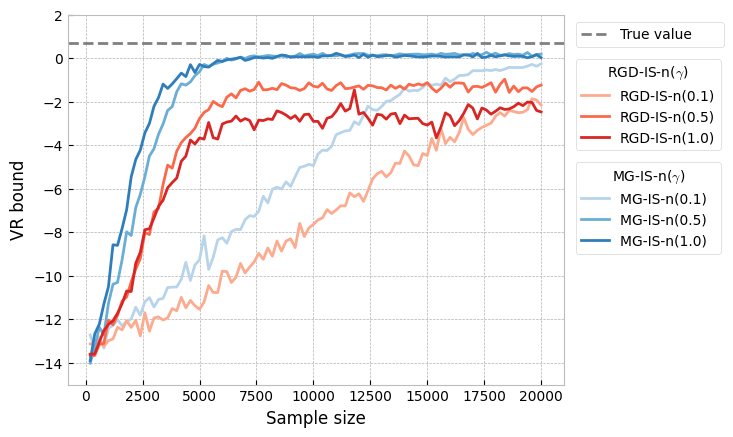

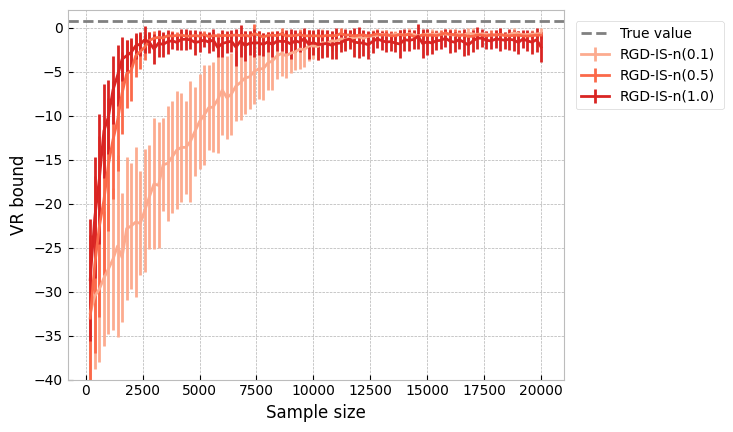

Setting at all times keeps the mixture weights fixed in Algorithm 3. In that case, our RGD approach relates to Gradient Ascent steps on the VR Bound (Li and Turner, 2016) w.r.t. the means of our Gaussian components (see Section 5.1). We then want to compare the performances of the RGD approach (that can be derived from Li and Turner, 2016) to the novel MG approach we have introduced in our work.

Implementation details. The covariance matrices of the mixture components are fixed and equal to with , , , , , the total number of iterations is equal to , is generated by sampling from a centered normal distribution with covariance matrix , and for all time , , and with . The experiments are replicated independently 30 times and the convergence of the RGD and of the MG approaches is monitored for the three multimodal examples (i), (ii) and (iii) by computing a Monte Carlo estimator of the VR Bound (since we have sampled samples from at time , these samples can readily be used to obtain an estimate the VR Bound with no additional computational cost).

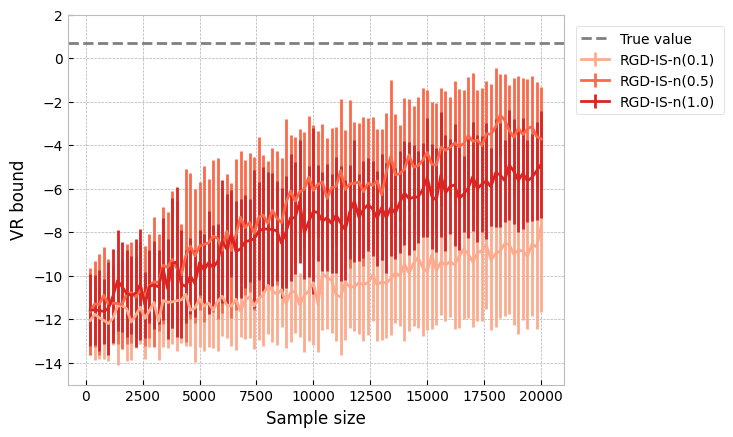

Our results are plotted on Figure 1, where RGD-IS-n() and MG-IS-n() denote the algorithms originating from the RGD and MG approaches (the IS-n and IS-unif samplers are equivalent here), and error bounds plots can be found in Figures 5 and 6 of Appendix D. As minimising is equivalent to maximising the VR Bound when , our theoretical results predict a systematic increase in the VR Bound for the algorithms considered. This is what we observe in Figure 1 and we also see that the choice of plays the role of a learning rate our algorithms: while increasing mostly improves the speed of convergence, it may deteriorate the performances if chosen too large, such as when with the target (iii).

| (i) | ||

|

|

|

| (ii) | ||

|

|

|

| (iii) | ||

|

|

| (i) | RGD-IS-n() | -0.081 | -0.076 | -0.218 | -1.640 | -1.673 | -1.560 |

| MG-IS-n() | -3.702 | -1.875 | -2.711 | -2.760 | -2.771 | -2.788 | |

| (ii) | RGD-IS-n() | -0.211 | -0.072 | -0.015 | -1.401 | -1.437 | -1.515 |

| MG-IS-n() | -2.581 | -2.101 | -1.742 | -2.611 | -2.328 | -1.933 | |

| (iii) | RGD-IS-n() | -0.108 | -0.008 | -0.111 | -1.652 | -1.654 | -1.634 |

| MG-IS-n() | -0.913 | -1.489 | -1.846 | -2.036 | -2.530 | -0.717 |

Furthermore, MG-IS-n() leads to better performances in all but one case compared to RDG-IS-n(). This renders the MG-IS-n() algorithm more suitable overall for capturing the multimodality of the various multimodal targets we considered, a fact that is further supported in Table 2, in which we compare the log of the Mean-Squared Error (logMSE) returned by each algorithm. (The MSE is computed as the average of over 30 independent runs of each algorithm, where stands for the Euclidean norm, with for all and where is the mean of the optimised variational distribution, that is in our setting .)

Let us next pair up the means optimisation with mixture weights optimisation and investigate the impact of the sequence on our algorithms.

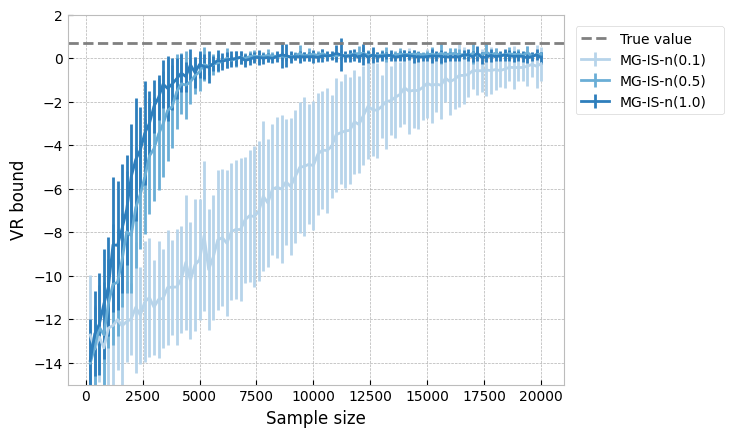

8.1.2 Comparing the RGD and the MG Approaches with

So far, we have demonstrated the viability of our novel MG approach compared to the more usual Rényi’s -divergence-based RGD approach. Yet, we have not taken advantage of the fact that we can perform mixture weights optimisation on top of means optimisation, which is another novelty of our framework compared to traditional Variational Inference methods.

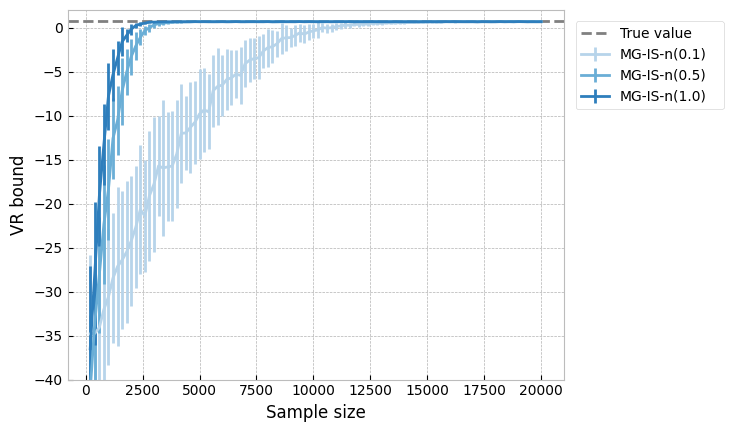

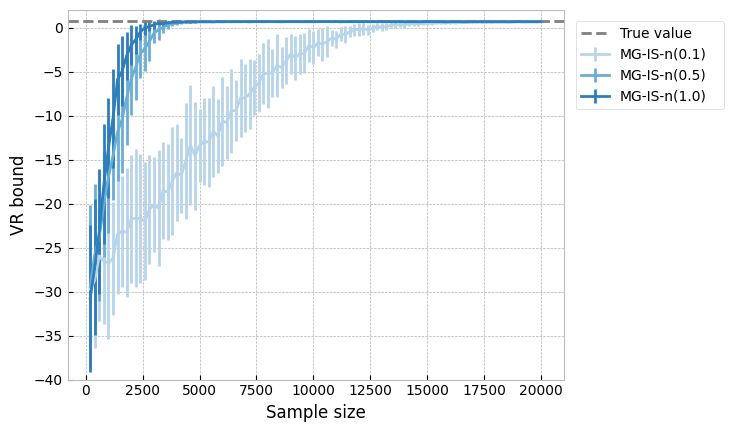

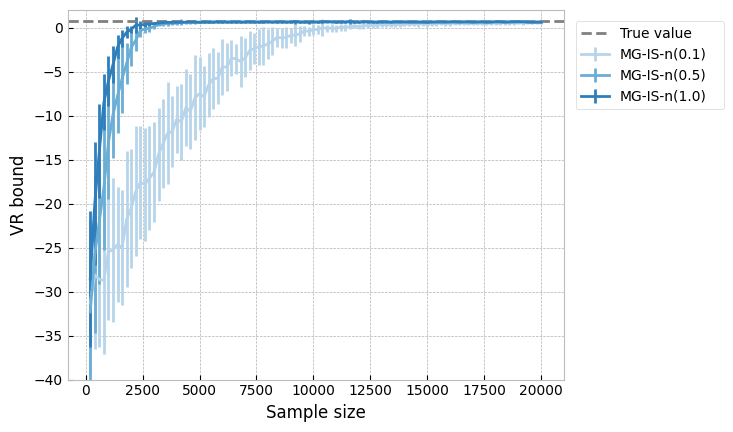

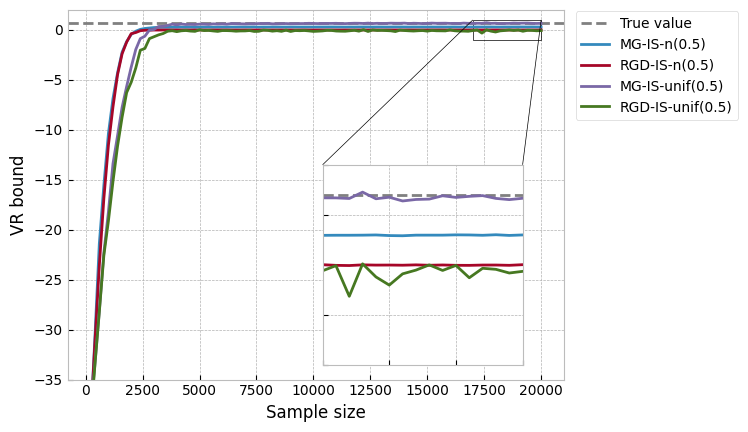

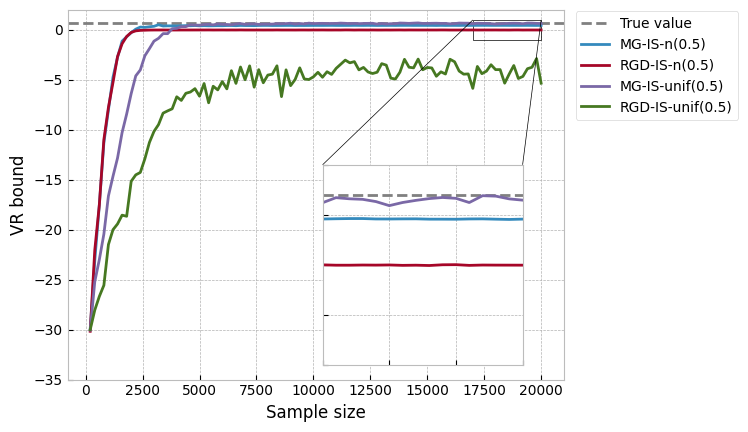

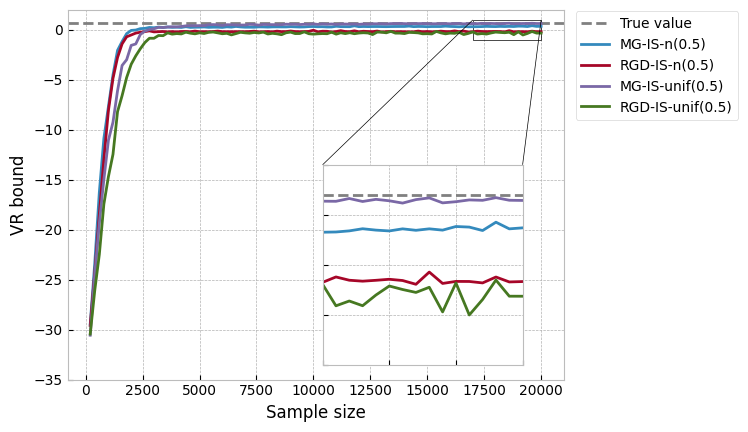

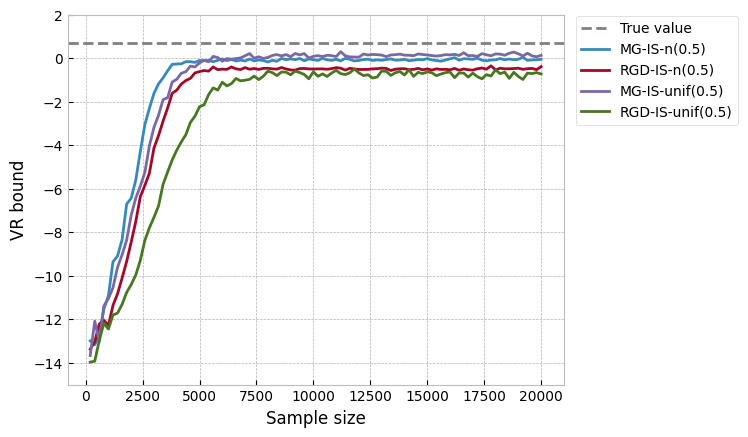

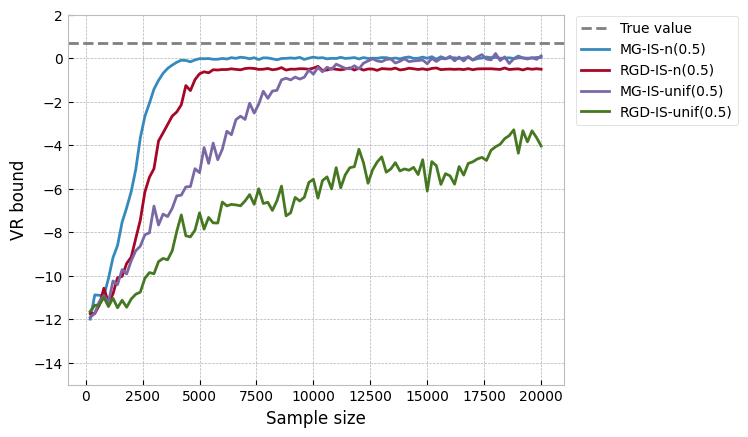

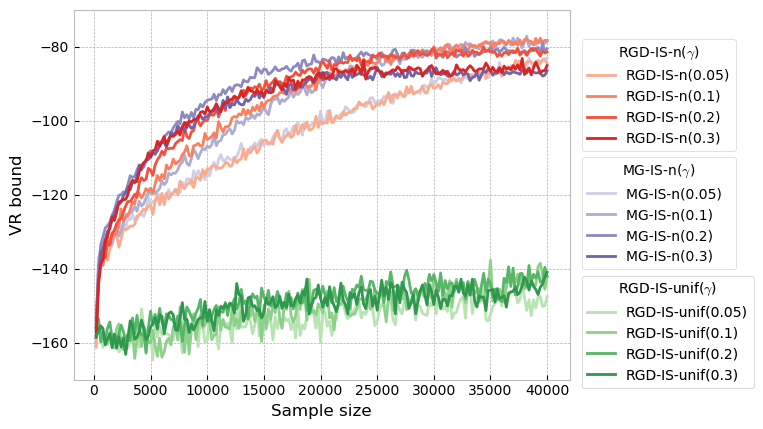

Implementation details. We work with the same implementation details as those described in Section 8.1.1, except for the fact that we will now let at time and we will vary the value of . In addition to the RGD-IS-n and the MG-IS-n algorithms, we also include the RGD-IS-unif and the MG-IS-unif algorithms in our results (that is, the algorithms resulting from pairing up the RGD and MG approaches with the IS-unif sampler).

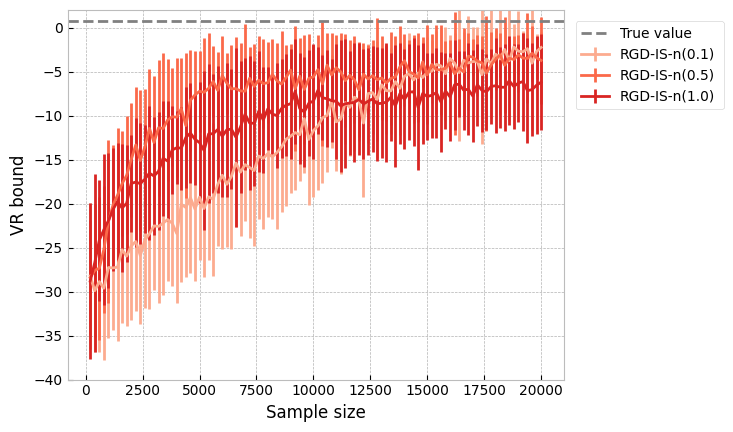

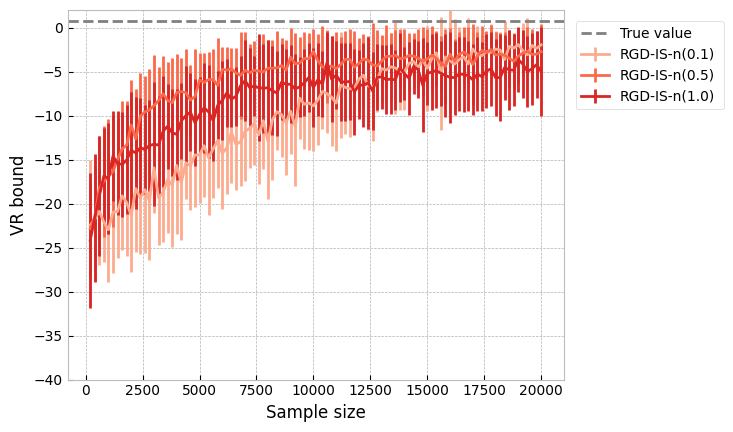

The plots for the averaged Monte Carlo estimate of the VR Bound with and are then available in Figure 2 (and similar plots for are provided in Figures 7 and 8 of Appendix D respectively). According to Figure 2, MG-IS-unif outperforms most of the time the other methods (this trend for MG-IS-unif is further confirmed by looking at the logMSE in Table 3 of Appendix D, which includes the cases for completeness).

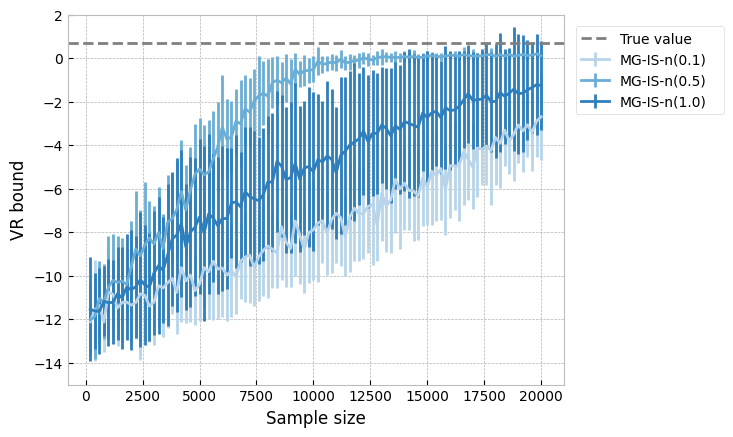

We also plot in Figure 3 the final mixture weights obtained after one typical run of MG-IS-unif() for and (and additional LogMSE results can be found in Table 4 of Appendix D). This is done in order to delve into how impacts the variational density returned at the end of Algorithm 3 (MG-IS-unif was chosen among all four options since it enjoys good empirical performances according to Figure 2).

| (i) | ||

|

|

|

| (ii) | ||

|

|

|

| (iii) | ||

|

|

A key insight from Figure 3 is that optimising the mixture weights permits us to select the components appearing in our mixture model according to their overall contribution in constructing a good approximation of the targeted density.

On the one hand, we enable more flexibility in our variational approximation as we optimise over a set of component parameters with instead of just one component parameter (). On the other hand, we avoid complexifying unecessarily the variational distribution returned at the end of the optimisation procedure since we perform mixture weights optimisation alongside components parameters optimisation. That way, we can bypass the limitation of the case , which may use more components than needed when approximating the targeted density (this is the case here since the targeted densities considered have three modes at best while ).

However, there is a tradeoff to find between the simplicity of the variational density that is returned and its accuracy at describing the targeted density, which is expressed via the choice of the learning rate . Indeed, choosing too large might lead to missing some of the modes while having too small may not discriminate quickly enough between the components. Observe in particular that the number of components too plays a role in how fast the components selection process occurs, as for the same value of , this selection process is slower as increases.

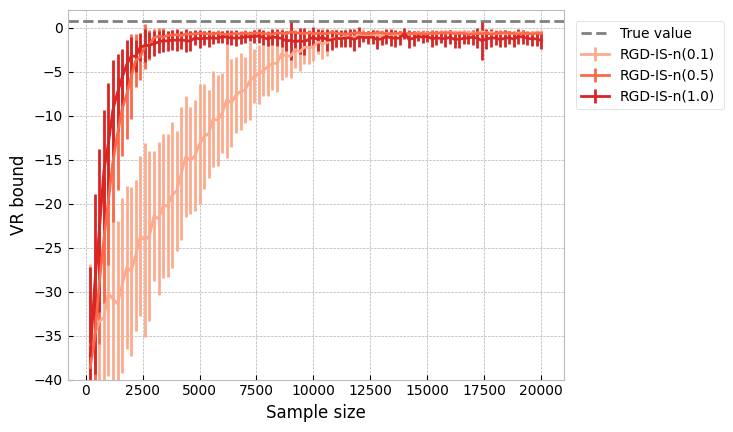

8.2 Bayesian Logistic Regression

We consider the Bayesian Logistic Regression setting from Gershman et al. (2012). Namely, the data is made of binary class labels, , and of covariates for each datapoint, . The latent variable consists of regression coefficients , and a precision parameter . Furthermore, the following model is assumed

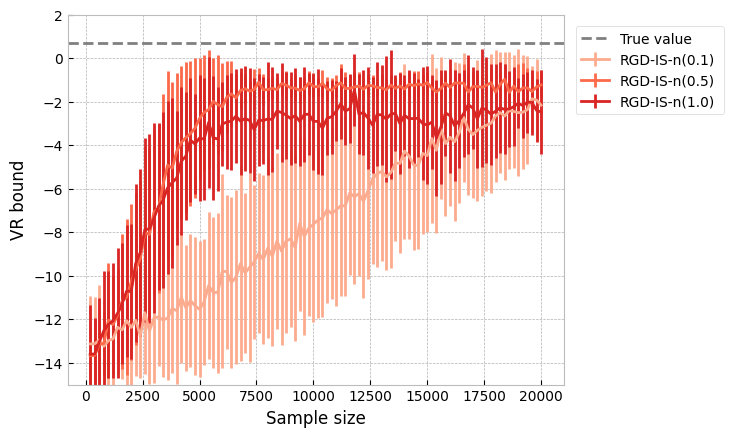

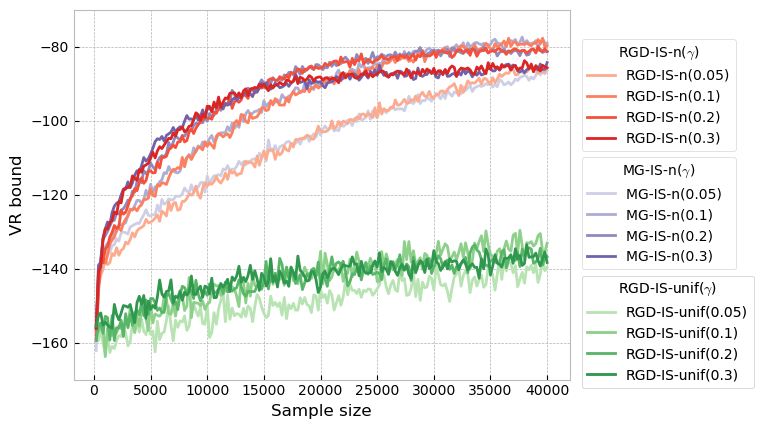

where and , so that . We now want to demonstrate the practicability of our framework in a real data scenario. To this end, we select the Covertype data set ( data points and features, available at https://www.csie.ntu.edu.tw/ ~cjlin/libsvmtools/datasets/binary.html) and we compare the RGD and the MG approaches for this choice of target density.

Implementation details. The covariance matrices of the mixture components are fixed and equal to with , , , , , the total number of iterations is equal to , is generated by sampling from a centered normal distribution with covariance matrix , and for all time , , , where and . Computing constitutes the major computation bottleneck here since . To address this problem, is approximated according to 3 with subsampled mini-batches of size . The experiments are replicated independently times and the convergence of the RGD and of the MG approaches is monitored by computing a Monte Carlo estimator of the VR Bound.

|

|

|

|

|

Our results are plotted in Figure 4, in which we focus on RGD-IS-n() and MG-IS-unif() (those two versions of Algorithm 3 are the most interesting to compare in this particular setting since MG-IS-n() enjoys similar performances to RGD-IS-n() and RGD-IS-unif() underperforms, see Figure 9 of Appendix D for details). We observe that both algorithms are able to learn in a real data scenario for a proper tuning of and that selecting either or too small/large can deteriorate the performance (as per the learning rate behaviour associated to those parameters). Furthermore, MG-IS-unif() can be tuned to outperform RGD-IS-n(), which confirms our previous empirical findings regarding the relevance of the novel MG approach compared to the more traditional RGD one.

9 Conclusion

We introduced a novel methodology to build algorithms ensuring a monotonic decrease in the -divergence at each step. Our methodology enabled simultaneous updates for both the weights and components parameters of a given mixture model, making it suitable for capturing complex multimodal target densities. Our work also connected and improved on different approaches: Gradient Descent for -divergence minimisation, Power Descent and an Integrated EM algorithm. By investigating variational families based on the exponential family, we applied our framework to important classes of models such as Gaussian Mixture Models and Student’s Mixture Models. Finally, we provided empirical evidence that our methodology can be used to enhance the aformentioned existing algorithms.

To conclude, we state several directions to extend our work. Now that we have established a systematic decrease for our iterative schemes, the next step could be to derive convergence results and to compare them with those obtained using typical Gradient Descent schemes. Based on 2, another direction is to generalise the monotonicity property from 3 beyond the case . Lastly, much like it is already the case in traditional Black-Box Variational Inference, we expect that fine-tuning our hyperparameters and resorting to more advanced Monte Carlo methods in the estimation of the intractable integrals appearing in our ideal algorithms will lead to further improved numerical results.

Acknowledgments and Disclosure of Funding

We would like to thank the action editor and the reviewers for helpful comments and suggestions on the paper. Kamélia Daudel acknowledges support of the UK Defence Science and Technology Laboratory (Dstl) and and Engineering and Physical Research Council (EPSRC) under grant EP/R013616/1. This is part of the collaboration between US DOD, UK MOD and UK EPSRC under the Multidisciplinary University Research Initiative.

Appendix A Deferred Proofs and Results for Section 3

A.1 Quantifying the Improvement in one Step of Gradient Descent

Let be a convex set. Here, is the standard inner product on and is the Euclidean norm.

Definition 3.

A continuously differentiable function defined on is said to be -smooth if for all ,

Lemma 2.

Let , let be a -smooth function defined on . Then, for all it holds that

Proof.

By assumption on , we have that for all

In particular, setting yields

Since , we can deduce the desired result.∎

A.2 Gradient Descent for - / Rényi’s -divergence Minimisation in Section 3

Let us first write the definition of the -divergence (resp. of Rényi’s -divergence) between the two absolutely continuous probability measures and

Here, the Rényi divergence is defined following the convention from Cichocki and Amari (2010), alternative definitions may use a different scaling factor.

A.2.1 Gradient Descent for -divergence Minimisation

As underlined in the introduction, minimising the -divergence w.r.t is equivalent to minimising with w.r.t , where we have gotten rid of in the optimisation problem as written in (2). Letting be of the form , the traditional Variational Inference way to optimise with w.r.t corresponds to performing Gradient Descent steps on to construct a sequence that converges towards a local optimum of the function . This procedure involves a well-chosen learning rate policy and sets:

| (79) |

Under common differentiability assumptions,

so that (79) becomes

A.2.2 Gradient Descent for Rényi’s -divergence Minimisation

Considering yet again , minimising Rényi’s -divergence

w.r.t can be done by performing Gradient Descent steps on to construct a sequence that converges towards a local optimum of the function . This procedure involves a well-chosen learning rate policy and sets:

| (80) |

Under common differentiability assumptions and setting ,

so that (80) becomes

Appendix B Deferred Proofs and Results for Section 4

B.1 Proof of 4

B.2 Extension of 1 to Mixture Models

Lemma 3 (Generalised maximisation approach for the mean-field family).

Let

each component of the mixture be a member of the same mean-field variational family so that with . Then, starting from and denoting with for all and all , solving (25) yields the following update formulas: for all and all ,

B.3 Proof of 5

B.4 Gradient Descent for - / Rényi’s -divergence Minimisation in Section 4

We obtain the desired results by adapting the reasoning from Section A.2 to the case

with , meaning that we consider the -divergence (resp. Rényi’s -divergence) between the two absolutely continuous probability measures and :

(we use the convention from Cichocki and Amari (2010) for Rényi’s -divergence).

B.5 Monotonicity Property for the Power Descent

B.5.1 Preliminary Remarks

For convenience, we redefine in this section the function for all by

Then, for all , the iteration is well-defined if we have

| (81) |

Furthermore, Daudel et al. (2021) already established that one transition of the Power Descent algorithm ensures a monotonic decrease in the -divergence at each step for all and all such that under the assumption of 2, which settles the case (iii). Finally, while we establish our results for (i) and (ii) in the general case where , the particular case of mixture models follows immediately by choosing as a weighted sum of dirac measures.

B.5.2 Extending the Monotonicity