Zero-Sum Semi-Markov Games with State-Action-Dependent Discount Factors

Zhihui Yu1, Xianping Guo1, Li Xia2 1School of Mathematics, Sun Yat-Sen University, Guangzhou, China

2Business School, Sun Yat-Sen University, Guangzhou, China email: mcsgxp@mail.sysu.edu.cnemail: xiali5@sysu.edu.cn; xial@tsinghua.edu.cn

Abstract

Semi-Markov model is one of the most general models for stochastic dynamic systems.

This paper deals with a two-person zero-sum game for semi-Markov

processes. We focus on the expected discounted payoff criterion with

state-action-dependent discount factors. The state and action spaces are

both Polish spaces, and the payoff function is -bounded. We

first construct a fairly general model of semi-Markov games

under a given semi-Markov kernel and a pair of strategies. Next,

based on the standard regularity condition and the

continuity-compactness condition for semi-Markov games, we

derive a “drift condition” on the semi-Markov kernel and suppose

that the discount factors have a positive lower bound, under which

the existence of the value function and a pair of optimal

stationary strategies of our semi-Markov game are proved by using

the Shapley equation. Moreover, when the state and action spaces are

both finite, a value iteration-type algorithm for computing the

value function and -Nash equilibrium of the game is

developed. The convergence of the algorithm is also proved. Finally,

we conduct numerical examples to demonstrate our main results.

Game theory is a fundamental mathematical model to study strategic

interactions among rational decision-makers. It has wide

applications in many fields, such as social science, computer

science, management science, and economic systems. In the early

period of game theory, it focuses on matrix games with two

persons and zero sum, where each participant’s gains or losses are

exactly balanced by those of the other. When the system state

evolves over time, matrix games are transformed into

two-person zero-sum stochastic games.

The study of zero-sum stochastic games is initiated by

Shapley (1953), and many extensions of that work have been

investigated in the literature. As is well known, it can be roughly

classified into the following four main groups. The first group is

discrete-time Markov games

(Hernández-Lerma and Lasserre, 2000; Küenle and Schurath, 2003; Sennott, 1994), which can be

considered as an extension of discrete-time Markov control

processes, that is, the decision epoch is the fixed discrete-time

point and the state-action process is discrete. The second group

deals with stochastic differential games

(Basar, 1999; Borkar and Ghosh, 1996; Kushner, 2003; Ramachandran, 1999), where the

evolution of state variables is governed by stochastic differential

equations. The third group deals with continuous-time Markov

games (Guo and Hernández-Lerma, 2003, 2005, 2007; Neyman, 2017) in which the

sojourn times between consecutive decision epochs are exponentially

distributed and the players can select their actions continuously in

time. The fourth group is semi-Markov games (SMGs)

(Jaskiewicz, 2002; Lal and Sinha, 1992; Luque-Vásquez, 2002; Minjárez-Sosa and Luque-Vásquez, 2008; Mondal et al., 2016),

where the state process is continuous over time, the sojourn time

between two consecutive decision epochs follows any distribution and

players take actions just at the moment when the state changes.

In certain sense, we may argue that semi-Markov processes can model

almost every possible stochastic dynamic system, since the sojourn

time can be any distribution and the Markovian property can be

satisfied by state augment. Therefore, it is important to study

semi-Markov games which can be used to formulate wide varieties of

decision-making problems in social and economic systems. In this

paper, we focus on the study of two-person zero-sum SMGs.

Lal and Sinha (1992) deal with two-person zero-sum SMGs under both

expected discounted and long-run average payoff criterion, where the

state space is denumerable and the payoff function is bounded. For

the discounted case, they prove the existence of the value function

and a pair of optimal stationary strategies by using the

Shapley equation. For the long-run average case, they further

establish the optimality equation and propose a standard ergodic

condition under which the existence of the value function and a pair

of optimal stationary strategies are ensured through solving the

optimality equation in a unified manner. Jaskiewicz (2002)

studies the two-person zero-sum SMGs under the long-run average

payoff criterion with a more general model, where the state and

action spaces are both Borel spaces and the payoff function is

-bounded. This paper derives some generalized geometric

ergodicity conditions on the transition probabilities under which

the optimality equation has a solution which can be obtained by

solving some -perturbed SGMs. This paper also proves

the existence of the value function and a pair of optimal stationary

strategies of the SMGs. There is further literature work on

two-person zero-sum SMGs that extends the similar results to the

expected discounted payoff criterion. Luque-Vásquez (2002)

considers the -stage SMGs as well as the infinite horizon case

with Borel state and action spaces and -bounded payoff

function. The existence of the value function and a pair of optimal

stationary strategies are also shown under suitable assumptions on

the transition law. Moreover, Minjárez-Sosa and Luque-Vásquez (2008) study the

discounted zero-sum SMGs with unknown holding time distribution

for one player. They propose a state-action independent condition on

to get independent observations during the evolution of the

system, under which they combine suitable methods of statistical

estimation of with control procedures to construct an

asymptotically discount optimal pair of strategies.

Most of the literature work on game theory focuses on the existence

of Nash equilibrium. However, how to efficiently solve a

stochastic dynamic game and compute a pair of optimal stationary

strategies are especially important for practical implementation of

game theory. The classic algorithmic study on game theory focuses on

static games, where the matrix game and the bimatrix game can be

solved by linear programming and quadratic programming, respectively

(Barron, 2013). Recently, there are emerging investigations that

aim to study the efficient computation for stochastic dynamic games

using approximation or learning algorithms. Littman (1994)

proposes a minimax-Q algorithm to solve discrete-time two-person

zero-sum Markov games, which is essentially motivated by the

standard Q-learning algorithm with a minimax operator in Markov

games replacing the max operator in reinforcement learning.

Al-Tamimi et al. (2007) utilize the method of Q-learning and

approximate dynamic programming (ADP) to solve a discrete-time

linear system quadratic zero-sum game, and the proof of the

convergence of the algorithm is also given. Vamvoudakis and Lewis (2012)

deal with a continuous-time two-person zero-sum game with infinite

horizon cost for nonlinear systems with known dynamics. They propose

a “synchronous” zero-sum game policy iteration algorithm to solve

the game through learning the Hamilton-Jacobi-Isaacs (HJI) equation

in real time. Moreover, a persistence of excitation condition is

given under which the convergence to the optimal saddle point and

the stability of the system are also guaranteed. Mondal et al. (2016)

study the AR-AT (Additive Reward-Additive Transition) two-person

zero-sum SMGs, where the state and action spaces are both finite.

They prove that such game can be formulated as a vertical linear

complementarity problem (VLCP), which can be solved by the

Cottle-Dantzig’s algorithm.

All the above literature work on SMGs assumes that the discount

factor is a constant, which may not always hold. For example,

considering the application in economics, the discount factor

(interest rate) may depend both on economy environments and

decision-makers’ actions. That is, the interest rate usually varies

in different financial markets and monetary policies, where

financial markets can be considered as states and monetary policies

are actions taken by the government. Thus, it is necessary and

reasonable to study the SMGs with state-action-dependent

discount factors. Problems with non-constant discount factors have

been studied for Markov decision processes (MDP)

(Minjárez-Sosa, 2015; Ye and Guo, 2012) and two-person zero-sum discrete-time

Markov games (González-Sánchez et al., 2019). In this paper, we aim at studying

the two-person zero-sum SMGs with expected discounted payoff

criterion in which the discount factors are state-action-dependent.

The objective is to find a pair of optimal strategies to maximize

the payoff of player (P1) and minimize the payoff of player

(P2). More precisely, we deal with the SMGs specified by five

primitive data: the state space ; the action spaces for P1

and P2, respectively; the semi-Markov kernel ; the

discount factor ; and the payoff function .

The state space and action spaces are all Polish spaces,

and the payoff function is -bounded. With

these data, we construct an SMG model with a fairly general problem

setting. Then we impose suitable conditions on the model parameters

shown in Assumptions 1-4, under which we establish

the Shapley equation and prove the existence of the value function

and a pair of optimal stationary strategies of the game. Our proof

is quite different from González-Sánchez et al. (2019) since we directly search

for Nash equilibrium in history-dependent strategies instead of

turning to Markov strategies. In addition, when the state and action

spaces are both finite, we derive a value iteration-type

algorithm to approach to the value function and Nash equilibrium of

the game based on the Shapley equation. The convergence of the

algorithm is also proved. Finally, we conduct numerical examples on

investment problem to demonstrate the main results of our paper.

The contributions of this paper can be summarized as follows. (1) We

construct the two-person zero-sum SMG model with expected discounted payoff

criterion in which the discount factors are state-action-dependent. To the

best of our knowledge, our work is the first one that the discount

factor is regarded as a variable in stochastic semi-Markov games,

which could complement the theoretical study on SMGs. (2) We derive

a “drift condition” (see Assumption 3) on the semi-Markov

kernel, which is more general than the counterpart in the literature

work (Luque-Vásquez, 2002), as stated in Remark 4. (3)

We propose a value iteration-type algorithm to compute the value

function and -Nash equilibrium of the SMG. This

algorithm can be viewed as a combination of the value iteration of

MDP and the linear programming of

matrix games. Moreover, the convergence and the error-bound of the

algorithm are also guaranteed.

The rest of this paper is organized as follows. In

Section 2, we introduce the model of SMG as well as the

optimality criterion. In Section 3, we impose suitable

conditions on the model parameters under which the existence of the

value function and a pair of optimal stationary strategies are

proved by using the Shapley equation. A value iteration-type

algorithm for computing the -Nash equilibrium is

developed in Section 4, and some numerical examples are

conducted to demonstrate our main results in Section 5.

Finally, we conclude the paper and discuss some future research

topics in Section 6.

2 Two-Person Zero-Sum Semi-Markov Game Model

Notation: If is a Polish space (that is, a complete

and separable metric space), its Borel -algebra is denoted

by , and denotes the family of

probability measures on endowed with the topology

of weak convergence.

In this section, we introduce a two-person zero-sum SMG model with expected

discounted payoff criterion and state-action-dependent discount factors,

which is denoted by the collection

where the symbols are explained as follows.

is the state space which is a Polish space,

and and are action spaces for P1 and P2, respectively, which

are also supposed to be Polish spaces.

and are Borel subsets of and

, which represent the sets of the admissible actions for P1 and

P2 at state , respectively. Let

be a measurable Borel subset of .

is a semi-Markov kernel which

satisfies the following properties.

(a) For each fixed ,

is a probability measure on , whereas for each

fixed ,

is a real-valued Borel function on .

(b) For each fixed and

, is a non-decreasing

right-continuous real-valued Borel function on such

that .

(c) For each fixed ,

denotes the distribution function of the sojourn time at state

when the actions are chosen. For each and , when P1 and P2 select actions and , respectively, denotes the

joint probability that the sojourn time in state is not greater

than and the next state belongs to D.

is a measurable function from to

which denotes the state-action-dependent discount factor.

and are two

real-valued functions on , which represent the payoff function

for P1 and P2, respectively.

If for all , then the

model is called a two-person zero-sum SMG. Otherwise, the game is

nonzero-sum. In this paper, we focus on the zero-sum case. We denote

, and regard P1 as the maximizer and P2 as the

minimizer. The evolution of SMGs with the expected discounted payoff

criterion carries on as follows.

Assume that the game starts at the initial state at the

initial decision epoch . The two players choose

simultaneously a pure action pair according to the variables and , then P1

and P2 receive immediate rewards

, respectively.

Consequently, after staying at state up to time

, the system moves to a new state

according to the transition law

. Once the state transition to

occurs at the st decision epoch , the entire

process repeats again and the game evolves in this way.

Thus, we obtain an admissible history at the th decision epoch

When the game goes to infinity, we obtain the history

where , for all . Moreover, let be the class of all admissible

histories of the system up to the th decision epoch,

endowed with a Borel -algebra.

To introduce our expected discounted payoff criterion discussed in this

paper, we give the definitions of strategies as follows.

Definition 1.

A randomized history-dependent strategy for P1 is a sequence of

stochastic kernels that satisfies

the following conditions:

(i) for each ,

is a Borel function on , and for each

, is a probability

measure on A;

(ii) is concentrated

on , that is

We denote by the set of all the randomized

history-dependent strategies for P1 for simplicity.

Definition 2.

(1) A strategy is called a randomized Markov

strategy if there exists a sequence of stochastic kernels

such that

(2) A randomized Markov strategy

is called stationary if is independent of ; that

is, if there exists a stochastic kernel on given

such that

(3) Moreover, if is a Dirac measure for all , then the stationary strategy

is called a pure

strategy.

We denote by , and the sets

of all the randomized Markov strategies, randomized stationary strategies and pure

strategies for P1, respectively.

The sets of all randomized history-dependent strategies ,

randomized Markov strategies , randomized stationary

strategies , pure strategies for P2 are

defined similarly, with in lieu of . Clearly,

and .

For each , by the

Tulcea’s theorem (Hernández-Lerma and Lasserre, 1996), there exists a unique

probability space and a stochastic process

such that for each and , we have

Corresponding to the stochastic process with probability space , we define an underlying

continuous-time state-action process

as

where , , are

some isolated points, ,

and is an indicator function on any set .

Definition 3.

The stochastic process is called a semi-Markov game.

Next, we will show the definition of the expected discounted payoff criterion in this paper, where denotes the expectation operator associated with .

Definition 4.

For each , the initial state and discount factor , the expected discounted payoff criterion for

player is defined as follows:

(1)

Remark 1.

Since , we just need to consider the expected discounted payoff criterion for

P1. Let

This paper focuses on the study of the value function and Nash

equilibrium of the SMG. So we need the following concepts.

Definition 5.

The upper value and lower value of the expected discounted payoff SMG are defined as

respectively. Obviously, for all . Moreover, if it holds that for all , then the common function is called the value function of the game and denoted by .

Definition 6.

Assume that the game has a value . Then a strategy

is said to be optimal for P1 if

Similarly, is

said to be optimal for P2 if

If is optimal for player (), then we can

call a pair of optimal strategies

(Nash equilibrium).

Remark 2.

is a pair of optimal strategies if and only if

Remark 2 is an effective method to verify whether a pair of

strategy is a Nash equilibrium, which is widely

used in the literature; see, for instance,

Luque-Vásquez (2002), and the references therein.

3 Optimality Analysis

In this section, we give some suitable assumptions on the model

parameters under which the existence of the value function and a

pair of optimal stationary strategies are guaranteed. The related

proofs are also discussed.

Given a measurable function , a function on is said to be -bounded if it has finite -norm which is defined as

such a function can be referred to as a weight function. For convenience, we write the Banach space of all -bounded measurable functions on .

Next, we give some hypotheses to guarantee the existence of a pair

of optimal strategies.

Assumption 1.

There exist constants and such that

Remark 3.

Assumption 1 is a regularity condition which indicates that for each fixed and , we have

which avoids possibility of infinitely many decision epochs during the finite time interval; see, for instance, Lal and Sinha (1992), Luque-Vásquez (2002), and the references therein .

To guarantee the finiteness of the expected discounted payoff

defined in (1), we propose the following assumption.

Assumption 2.

(a) There exists a constant such that for all .

(b) There exists a measurable function and a nonnegative constant such that for all ,

Below we give an important consequence of Assumption 1 and

Assumption 2(a).

Lemma 1.

If Assumptions 1&2(a) hold, then there exists a

constant such that for each ,

We call Assumption 3 the “drift condition”, which

is needed to ensure that the Shapley operator (defined later in

(6)) is a contraction operator as well as our main results.

Particularly, if , where denotes the state transition probability,

(3) degenerates into , which is the same as the Assumption 3(b) of

Luque-Vásquez (2002). Thus, our Assumption 3 is

more general than the counterpart in the literature Luque-Vásquez (2002).

Combining Lemma 1 with Assumption 3, it is easy to derive

(4)

Moreover, we impose the following continuity-compactness conditions

to ensure the existence of a pair of optimal stationary strategies of our SMG model.

Assumption 4.

(a) For each fixed , and are both compact sets.

(b) For each fixed , is upper semi-continuous on and is lower semi-continuous on .

(c) For each fixed , and , the functions

are continuous on and , respectively.

(d) For each fixed , is continuous on .

(e) The function is continuous on .

Remark 5.

Assumption 4 is similar to the standard continuity-compactness hypotheses for Markov control processes; see, for instance, Hernández-Lerma and Lasserre (1999), and the references therein. It is commonly used for the existence of minmax points of games.

By Lemma in Nowak (1984), if Assumption 4(a) holds, then the probability spaces are also compact for each .

We now introduce the following notations: for each given function and , we write

(5)

For each fixed and probability measures , we denote

whenever the integral is well defined.

We define an operator on by

(6)

which is called the Shapley operator. A function is said to be a solution of the Shapley equation if

In order to explore the existence of a pair of optimal stationary

strategies, we also need to define another operator on

by

where is a pair of stationary strategies.

Before stating our main results, we need the following lemmas:

Lemma 2.

Suppose that Assumptions 1-4 hold, then for each given function , the function is in and

(7)

Moreover, there exists a pair of stationary strategies such that

(8)

Proof.

By Assumption 2 and formulation (4), for each given function and

, we can easily get

The above inequality yields , which implies

is in , and so .

On the one hand, by Assumption 4, it follows that

is upper semi-continuous in , then for each

fixed , by the Fatou’s theorem, the

function

is also upper semi-continuous in . Moreover, since the

probability measures on endowed with the topology

of weak convergence, by Theorem in Ash et al. (2000), the

function is upper semi-continuous in

. Similarly, is lower

semi-continuous in . Thus, by Theorem in

Ash et al. (2000), the supremum and the infimum are indeed attained in

(6), which means

Then, by the Fan’s minimax Theorem (Fan, 1953), we obtain

(7).

On the other hand, it is clear that is both concave and convex in with respect to and in with respect to . Hence, by the well-known measurable selection theorem (Nowak, 1985), there exists a pair of stationary strategies that satisfies (8).

∎

Lemma 3.

Both and are contraction operators with modulus less than .

Proof.

First, it is easy to verify that the operator is monotonically increasing. Let , by the definition of -norm, , it follows that for each fixed , we have

(9)

where the last inequality is followed by formulation (4).

Furthermore, taking maximum of and minimum of on both sides of the inequality (9), we have

i.e.

Similarly, interchanging and , we obtain

Combining the two inequalities above, we have

i.e.

which implies is a contraction operator with modulus

. Using the same arguments, we can prove that

is also a contraction operator with modulus

.

∎

Since and are both contraction operators, then there

exist unique functions and such that and

by the Banach’s fixed

point theorem.

Lemma 4.

For each and ,

where , and which denotes the translation of strategy.

Proof.

where the third and fourth equalities are ensured by the property of conditional expectation. The

fifth equality follows from the strong Markovian property.

Hence,

which is required.

∎

Now, if we set and specially, which are both

stationary strategies, from Lemma 4, we have

which implies that the function is the unique fixed point

of the contraction operator .

Lemma 5.

Suppose that Assumptions 1-3 hold, let , then for each , , we have

Proof.

For and , we have

where the first and second equalities are ensured by the property of conditional expectation. The last

inequality follows from formulation (4).

Through iteration we have

which means that the first inequality in (11) holds.

(b) ()

Suppose that is a pair of optimal stationary strategies, then for each , we have

For each fixed , let

with and

, then by Lemma 4, for each

, we have

which yields

Similarly, we can prove

Combining the last two inequalities, we obtain the desired result.

()

This part holds, which has been proved in part .

∎

4 Algorithm

In this section, we develop an iterative algorithm to approach to

the value function and Nash equilibrium of our two-person zero-sum

stochastic SMG, where numerically solving matrix games is

iteratively utilized at every state in a form of value iteration.

First, we introduce some concepts about matrix games

(Barron, 2013).

A two-person zero-sum static game in a matrix form means that there

is a matrix of real numbers so that if P1,

the row player chooses to play row , while P2, the column player

chooses to play column , then the payoff to P1 is and

the payoff to P2 is . Every row and column represents a

pure strategy adopted by P1 and P2, respectively. Both players aim to choose strategies that maximize their individual

payoffs. To guarantee the

optimality, we have to consider mixed strategies, where a player

chooses a row or column according to some probability distributions.

Definition 7.

A mixed strategy is a vector for P1,

and for P2, where

The components and represent the probabilities that row will

be chosen by P1 and column

will be chosen by P2, respectively. Denote the set of mixed strategies with

components by

Definition 8.

Let be a mixed strategy for P1, and

be a mixed strategy for P2, then the

expected payoff to P1 is

In a two-person zero-sum game, the expected payoff to P2 is

.

Both players aim to choose strategies that maximize their individual

payoffs. P1 wants to choose a strategy to maximize the payoff in the

matrix, while P2 wants to choose a strategy to minimize the payoff

in the matrix.

Definition 9.

The upper and lower values of the matrix game are defined as

If , then the common value is called the value of the

game and denoted by .

Moreover, a saddle point in mixed strategies is a pair , which satisfies

By Theorem in Barron (2013), we know that any matrix

game has a unique value as well as at least one saddle point. There

is a method of formulating the matrix game as a linear program as

follows (Barron, 2013):

P1 aims to choose a mixed strategy

to maximize the payoff

(12)

P2 aims to choose a mixed strategy

to minimize the payoff

(18)

We can use the classic algorithms to solve the two linear programs

(12) and (18), such as simplex method or interior

point method. Note that the optimal values of solved by

(12) and (18) are always equal. Therefore, the

optimal strategies of P1 and P2 and the value of the game can be

obtained in a straightforward way.

Next, we utilize the above technique of solving matrix games to

study the computation of two-person zero-sum stochastic SMGs, where a value iteration-type algorithm is developed to

approach to the value function and Nash equilibrium

. To this end, we need to introduce the

following concept.

Definition 10.

Assume that the SMG has a value function . Then a pair of strategies

is said to be an -Nash equilibrium of the game

if

Moreover,

is called the -value function of the

game.

Consider the mathematical model of SMG discussed in this paper. In

order to numerically approach to the value function and Nash

equilibrium, we simplify the general state and action spaces as

finite case for convenience. Without loss of generality, we assume

that and

, for any . Under

Assumptions 1-4 mentioned in Section 3,

we obtain the Shapley equation as follows

(19)

For each fixed and given function , let

be an -dimensional matrix with elements defined

as

where is defined in (5). We further define as an

-dimensional vector and as

an -dimensional vector, which are all mixed strategies. According

to (4), we have

(20)

which can be viewed as a matrix game for the value function at

each state .

However, we cannot directly solve (20) since the value

function is unknown. Below, we develop Algorithm 1

to iteratively compute a series of matrix games whose values can

asymptotically approach to at each state . From the

lines 11-12 of Algorithm 1, we can see that at the th

iteration, we can obtain and by using

linear programming (12) and (18) to solve the game

with matrix whose element is

, where

, , , and . This

iterative procedure of computing a series of is similar to the

classic value iteration algorithm in the MDP theory. Furthermore, we

give a theorem (Theorem 2) to prove the convergence of Algorithm 1.

1Algorithm parameter: a small threshold determining accuracy of estimation; model parameters given by Assumption 1, given by Assumption 2(a), and given by Assumption 3, with and ; a measurable function given by Assumption 2(b)

2Initialize: for all arbitrarily

3repeat

4

5Loopforeach do

6

7fordo

8fordo

9

10

11 Solving the game with matrix

12

13

14

15

16

17until;

18Output:

19

and

Algorithm 1Value iteration-type algorithm to solve the two-person zero-sum SMG

Remark 6.

For the case where the state and action spaces are both

countable, we generally choose for convenience(see Example 1). And the line of Algorithm 1 is simplified to .

Theorem 2.

Under Algorithm 1, for any given and initial

value , there exists a non-negative integer

such that

, which

implies that Algorithm 1 can converge within

iterations. Moreover, the strategy pair

output by Algorithm 1

is an -Nash equilibrium, where

.

Proof.

According to the iterative formula of Algorithm 1, we have

which by iteration yields

For each given and initial value , if , choose , and we have

otherwise, if , choose , and we have

Combining the two cases above, choose and we have , which implies that Algorithm 1 can converge within

iterations.

Moreover, since is the unique solution of the Shapley equation, we have

thus,

taking , and we have

which implies that is an -Nash equilibrium by Definition 10.

∎

Therefore, with Algorithm 1, we can iteratively approach

to the value function and Nash equilibrium of our SMG problem

through recursively solving linear programming (12) and

(18) at each state . Theorem 2 guarantees the

convergence of Algorithm 1. We can implement

Algorithm 1 with discretization techniques for computers

to solve practical problems, as illustrated in the next section.

5 Numerical Experiment

In this section, we conduct numerical examples to illustrate our

main results derived in Sections 3&4. First, we

give an example to demonstrate that

Assumptions 1-4 ensuring the existence of the

value function and Nash equilibrium of SMGs are easy to verify in

practice.

Example 1.

Consider a system with a model of SMG which is defined as follows:

The state space and the action spaces with admissible action sets for each .

The semi-Markov kernel is given by:

where is a positive constant and is a probability distribution.

The payoff function is denoted by which is bounded. Moreover, the discount factor is defined as .

Now, we verify that the conditions on the existence of a pair of

optimal stationary strategies described in

Assumptions 1-4 are satisfied in this example. To

this end, we need the following hypothesis:

Assumption 5.

There exist positive constants and such that for

each , we have for each

and for each .

With this hypothesis, we directly have the following result.

Proposition 1.

Suppose that Assumption 5 holds, then Example 1 satisfies Assumptions 1-4, which means the SMG has a pair of optimal stationary strategies.

Proof.

Obviously, Assumption 2 holds by choosing

and . Since and

are discrete, Assumption 4 holds. Next we verify

Assumptions 1&3. According to the semi-Markov

kernel , we have

Therefore, Assumption 3 is also verified. Hence, the SMG of

Example 1 has a pair of optimal stationary strategies.

∎

Next, we give another example about investment problem to

demonstrate the numerical computation of Algorithm 1 to

solve the value function and a pair of optimal stationary strategies

of the game.

Example 2.

Consider an investment problem with three

states , which denotes the benefit, medium and loss

economy environments, respectively. At each state, the investor will buy some assets while the market-maker will sell. The interest rate depends on the economy environments as well as the number of assets that investor buys and market-maker sells. In state , the investor buys a certain amount of assets from and the market-maker sells

from , which leads to

a payoff to the investor and to the market-maker, where .

Then the system moves to a new state with probability

after staying at state for a random time which

follows exponential-distribution with parameter . In

state , the investor buys a certain amount of assets from

and the market-maker sells from , which leads to a payoff

to the investor and to the market-maker,

where . Then the

system moves to a new state with probability after

staying at state for a random time uniformly distributed in

with parameter . For this

system, the decision makers aim to find a pair of optimal

strategies.

First, we establish a model of SMG for this example as follows.

We set , ,

for each and the semi-Markov

kernel is given by:

To take numerical calculation for this example, we assume that the

values of model parameters are shown in Table 1.

Table 1: The values of model parameters

state

1

2

3

action

0.98

0.96

0.92

0.9

0.78

0.76

0.73

0.7

0.86

0.84

0.89

0.82

40

24

18

33

12

8

10

17

3

5

2

6

20

30

11

13

7

8

6.5

4

0.34

0.44

0.55

0.15

0

0

0

0

0.46

0.48

0.39

0.3

0.45

0.24

0.43

0.4

0.5

0.43

0.32

0.62

0

0

0

0

0.55

0.76

0.57

0.6

0.5

0.57

0.68

0.38

0.54

0.52

0.61

0.7

0

0

0

0

Under these data, we can verify that

Assumptions 1-4 hold by using Proposition 1. Thus, the existence of the

value function and Nash equilibrium of the SMG are ensured by

Theorem 1. Moreover, by Assumption 5 and proposition 1, we can choose , from which we obtain .

Next, we use Algorithm 1 to find the

value function and a pair of optimal stationary strategies of the

game. The detailed steps are listed as follows.

Step 1: Initialization.

Let , and ; set a small threshold

, and we have .

Step 2: Iteration.

For , , we have

Then, for each state , we solve the linear program

If , then

the iteration stops, is the -value function and

is

-Nash equilibrium of the SMG; Otherwise, set

and go to Step 2.

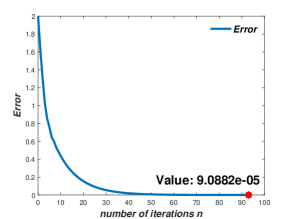

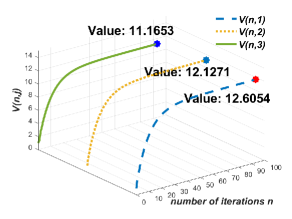

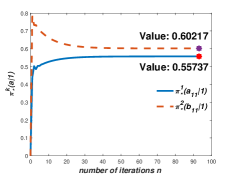

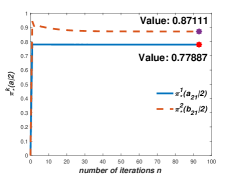

We use Matlab to implement the iteration algorithm for this example.

It takes about seconds to stop at the rd iteration. The

curves of the error of two successive iterations, the value

function, and the strategy pair of players with respect to the

iteration times are illustrated by Figures 2-3.

Figure 1: The error

Figure 2: The value function of the game

Figure 3: The optimal strategy pair

Based on the experimental results, we have the following

observations:

When the state is benefit, the investor should take action with probability and with probability , while the market-maker should take action with probability and with probability ;

When the state is medium, the investor should take action with probability and with probability , while the market-maker should take action with probability and with probability ;

When the state is loss, the investor should always take action while the market-maker should always take action ;

If both investor and market-maker use the optimal

strategies, the investor will obtain a profit at benefit

state, at medium state and at loss state, while the

market-maker will lose the same amount, respectively.

Remark 7.

In this example, we choose a uniformly distributed sojourn time at

state to show that arbitrary distributions are permitted for the

sojourn time of semi-Markov processes. Other distributions can also

be chosen for the sojourn time according to practical situations.

Moreover, if all the sojourn times are exponentially distributed,

the semi-Markov games degenerate into discrete-time Markov games.

6 Conclusion

In this paper, we concentrate on the two-person zero-sum SMG with expected

discounted payoff criterion in which the discount factors are

state-action-dependent. We first construct the SMG model with a fairly

general definition setting. Then we impose suitable conditions on

the model parameters, under which we establish the Shapley equation

whose unique solution is the value function and prove the existence

of a pair of optimal stationary strategies of the game. While the

state and action spaces are finite, a value iteration-type algorithm

for approaching to the value function and Nash Equilibrium is

developed. Finally, we apply our results to an investment problem, which demonstrates that our algorithm performs well.

One of the future research topics is to deal with the nonzero-sum

case of this game model. We wish to find sufficient conditions under

which we use the similar arguments to establish the Shapley equation

and prove the existence of a pair of optimal stationary strategies

for such game. In addition to the value iteration algorithm, the

policy iteration algorithm is also widely used to solve MDPs.

Therefore, it is also promising to develop a policy iteration-type

algorithm to solve the two-person zero-sum SMGs. Moreover,

considering the limitations of computing resources, the dynamic

programming algorithm is difficult to implement in reality when the

scale of the game becomes huge. Another future research topic is to

develop data-driven learning algorithms to approximately solve the

game problems, such as the combination with multi-agent

reinforcement learning approaches.

Acknowledgements

This work was supported in part by the National Natural Science

Foundation of China (11931018, 61573206).

References

Al-Tamimi et al. (2007)

Al-Tamimi A, Lewis FL, Abu-Khalaf M (2007) Model-free Q-learning designs for linear discrete-time zero-sum games with application to H-infinity control.Automatica 43(3):473–481

Ash et al. (2000) Ash RB, Robert B, Doleans-Dade CA, Catherine A (2000) Probability and Measure Theory. Academic Press

Barron (2013)

Barron EN (2013) Game Theory: An Introduction, vol 2. John Wiley & Sons

Basar (1999)

Basar T (1999) Nash equilibria of risk-sensitive nonlinear stochastic

differential games. Journal of Optimization Theory and Applications 100(3):479–498

Borkar and Ghosh (1996)

Borkar VS, Ghosh MK (1996) Stochastic differential games: occupation measure based approach. Journal of Optimization Theory and Applications

88(1):251–252

Fan (1953)

Fan K (1953) Minimax theorems. Proceedings of the National Academy of Sciences of the United States of America 39(1):42–47

González-Sánchez et al. (2019)

González-Sánchez D, Luque-Vásquez F, Minjárez-Sosa JA (2019) Zero-Sum Markov Games with Random State-Actions-Dependent Discount Factors: Existence of Optimal Strategies. Dynamic Games and Applications 9(1):103–121

Guo and Hernández-Lerma (2003)

Guo X, Hernández-Lerma O (2003) Zero-sum games for continuous-time Markov chains with unbounded transition and average payoff rates. Journal of Applied Probability 40(2):327–345

Guo and Hernández-Lerma (2005)

Guo X, Hernández-Lerma O (2005) Zero-sum continuous-time Markov games with unbounded transition and discounted payoff rates. Bernoulli 11(6):1009–1029

Guo and Hernández-Lerma (2007)

Guo X, Hernández-Lerma O (2007) Zero-sum games for continuous-time jump Markov processes in Polish spaces: discounted payoffs. Advances in Applied Probability 39(3):645–668

Hernández-Lerma and Lasserre (1996)

Hernández-Lerma O, Lasserre JB (1996) Discrete-Time Markov Control Processes. Springer Science & Business Media

Hernández-Lerma and Lasserre (1999)

Hernández-Lerma O, Lasserre JB (1999) Further Topics on Discrete-Time Markov Control Processes. Springer Science & Business Media

Hernández-Lerma and Lasserre (2000)

Hernández-Lerma O, Lasserre JB (2000) Zero-sum stochastic games in Borel spaces: average payoff criteria. SIAM Journal on Control and Optimization 39(5):1520–1539

Jaskiewicz (2002)

Jaskiewicz A (2002) Zero-sum semi-Markov games. SIAM Journal on Control and Optimization 41(3):723–739

Küenle and Schurath (2003)

Küenle HU, Schurath R (2003) The optimality equation and

-optimal strategies in Markov games with average reward

criterion. Mathematical Methods of Operations Research

56(3):451–471

Kushner (2003)

Kushner HJ (2003) Numerical approximations for stochastic differential games: the ergodic case. SIAM Journal on Control and Optimization 42(6):1911–1933

Lal and Sinha (1992)

Lal AK, Sinha S (1992) Zero-sum two-person semi-Markov games. Journal of Applied Probability 29(1):56–72

Littman (1994)

Littman ML (1994) Markov games as a framework for multi-agent reinforcement learning. In: Machine Learning Proceedings, Elsevier, pp 157–163

Luque-Vásquez (2002)

Luque-Vásquez F (2002) Zero-sum semi-Markov game in Borel spaces with discounted payoff. Morfismos 6(1):15–29

Minjárez-Sosa (2015)

Minjárez-Sosa JA (2015) Markov control models with unknown random

state–action-dependent discount factors. Top 23(3):743–772

Minjárez-Sosa and Luque-Vásquez (2008)

Minjárez-Sosa JA, Luque-Vásquez F (2008) Two person zero-sum

semi-Markov games with unknown holding times distribution on one side: a discounted payoff criterion. Applied Mathematics and Optimization 57(3):289–305

Mondal et al. (2016)

Mondal P, Sinha S, Neogy SK, Das AK (2016) On discounted AR–AT semi-Markov games and its complementarity formulations. International Journal of Game Theory 45(3):567–583

Neyman (2017)

Neyman A (2017) Continuous-time stochastic games. Games and Economic Behavior 104:92–130

Nowak (1984)

Nowak AS (1984) On zero-sum stochastic games with general state space I.Probability and Mathematical Statistics 4(1):13–32

Nowak (1985)

Nowak AS (1985) Measurable selection theorems for minimax stochastic

optimization problems. SIAM Journal on Control and Optimization

23(3):466–476

Ramachandran (1999)

Ramachandran K (1999) A convergence method for stochastic differential games with a small parameter. Stochastic Analysis and Applications 17(2):219–252

Sennott (1994)

Sennott LI (1994) Zero-sum stochastic games with unbounded costs: discounted and average cost cases. Zeitschrift für Operations Research 39(2):209–225

Shapley (1953)

Shapley LS (1953) Stochastic games. Proceedings of the National Academy of Sciences 39(10):1095–1100

Vamvoudakis and Lewis (2012)

Vamvoudakis KG, Lewis FL (2012) Online solution of nonlinear two-player

zero-sum games using synchronous policy iteration. International

Journal of Robust and Nonlinear Control 22(13):1460–1483

Ye and Guo (2012)

Ye L, Guo X (2012) Continuous-time Markov decision processes with

state-dependent discount factors. Acta Applicandae Mathematicae

121(1):5–27