Sturt

A nonparametric algorithm for optimal stopping based on robust optimization

A nonparametric algorithm for optimal stopping based on robust optimization

Bradley Sturt

\AFFDepartment of Information and Decision Sciences

University of Illinois at Chicago, \EMAILbsturt@uic.edu

Optimal stopping is a fundamental class of stochastic dynamic optimization problems with numerous applications in finance and operations management. We introduce a new approach for solving computationally-demanding stochastic optimal stopping problems with known probability distributions. The approach uses simulation to construct a robust optimization problem that approximates the stochastic optimal stopping problem to any arbitrary accuracy; we then solve the robust optimization problem to obtain near-optimal Markovian stopping rules for the stochastic optimal stopping problem.

In this paper, we focus on designing algorithms for solving the robust optimization problems that approximate the stochastic optimal stopping problems. These robust optimization problems are challenging to solve because they require optimizing over the infinite-dimensional space of all Markovian stopping rules. We overcome this challenge by characterizing the structure of optimal Markovian stopping rules for the robust optimization problems. In particular, we show that optimal Markovian stopping rules for the robust optimization problems have a structure that is surprisingly simple and finite-dimensional. We leverage this structure to develop an exact reformulation of the robust optimization problem as a zero-one bilinear program over totally unimodular constraints. We show that the bilinear program can be solved in polynomial time in special cases, establish computational complexity results for general cases, and develop polynomial-time heuristics by relating the bilinear program to the maximal closure problem from graph theory. Numerical experiments demonstrate that our algorithms for solving the robust optimization problems are practical and can outperform state-of-the-art simulation-based algorithms in the context of widely-studied stochastic optimal stopping problems from high-dimensional option pricing.

robust optimization; optimal stopping; options pricing.

First version: March 4, 2021. Revisions submitted on June 17, 2022 and December 21, 2022. Accepted for publication on March 16, 2023.

1 Introduction

Consider the following class of stochastic dynamic optimization problems: A sequence of random states are incrementally revealed to a decision maker. After observing the state in each period, the decision maker chooses whether to continue to the next period or stop and receive a reward that depends on the current state. The problem is to find a control policy, called a stopping rule, for selecting when to stop the process to maximize the expected reward.

Such optimal stopping problems are widely studied and arise in a variety of domains like finance, promotion planning (Feng and Gallego 1995), and organ transplantation (David and Yechiali 1985). In particular, optimal stopping has considerable importance to industry for the pricing of financial derivatives. With a record trading volume that exceeded seven billion contracts in 2020, equity options are among the most widely-traded type of financial derivative (Reuters 2021), and financial firms depend on solving optimal stopping problems to determine accurate prices for American-style options, the most common type of equity option.

In this paper, we study a general class of optimal stopping problems in which the sequence of random states is driven by a non-Markovian probability distribution. We recall that a sequence of random states is non-Markovian if the state in the next time period (e.g., a stock’s price tomorrow) has a probability distribution which depends both on the state in the current time period (e.g., the stock’s price today) as well as the states in the past periods (e.g., the stock’s price yesterday). This class of optimal stopping problems has witnessed a surge of interest as financial firms increasingly use non-Markovian probability distributions to accurately model the volatility patterns of stocks (Gatheral et al. 2018, Leão et al. 2019, Becker et al. 2019, Bezerra et al. 2020, Goudenège et al. 2020, Bayer et al. 2020). Optimal stopping problems with non-Markovian probability distributions also occur when using popular dimensionality-reduction techniques for pricing high-dimensional basket options (Bayer et al. 2019, p. 372) and pricing options when the probability distribution of underlying assets is accessed via a black-box simulator constructed from historical data (Ciocan and Mišić 2020, §5.5).

Despite their importance in practice, non-Markovian optimal stopping (NMOS) problems are “not easy to solve” (Leão et al. 2019, p. 982). The difficulty of these problems arises because the optimal decision in each period may depend on the entire history of the state process. In principle, an NMOS problem can be transformed into an equivalent Markovian optimal stopping problem by converting the original sequence of random states into a Markovian stochastic process where the new state in each period includes the entire state history of the original process. Unfortunately, the enlarged state space will be high-dimensional when the optimal stopping problem has many periods, and the difficulty of solving a Markovian optimal stopping problem explodes in the dimensionality of the state space.

To contend with the curse-of-dimensionality that arises in NMOS problems, a natural approximation technique is to search only for stopping rules that are Markovian. Rather than depending on the entire history of the original sequence, a Markovian stopping rule makes a decision in each period based only on the current original state and knowledge that the sequence of random states was not stopped in any of the previous time periods. In general, the best Markovian stopping rule for an NMOS problem is not guaranteed to be an optimal stopping rule for the NMOS problem. However, recent numerical evidence demonstrates that Markovian stopping rules can lead to highly accurate approximations of optimal stopping rules in NMOS problems from options pricing; see Goudenège et al. (2020, §9.2), Ciocan and Mišić (2020, §5.5), Bayer et al. (2020, §3.5).

As far as we are aware, only two papers until now have suggested methods that are theoretically capable of finding the best Markovian stopping rules to NMOS problems. Belomestny (2011a) analyzes simulation-based methods which optimize directly over spaces of Markovian stopping rules and suggests a nonparametric space of Markovian stopping rules based on -nets; however, he does not propose any concrete algorithms for optimizing over this nonparametric space of Markovian stopping rules. Ciocan and Mišić (2020) propose optimizing over Markovian stopping rules which are restricted to decision trees with fixed depth. Due to the computational intractability of optimizing over all decision trees of fixed depth, the authors develop greedy heuristics which are shown to limit the range of attainable decision trees, and overcoming this limitation of the heuristics “is not obvious, especially in light of the structure of the optimal stopping problem that is leveraged to efficiently optimize split points in our construction” (Ciocan and Mišić 2020, p. 22).

We take a different approach to the aforementioned literature, and in doing so make our contributions to optimal stopping, by drawing on the traditionally unrelated field of robust optimization. Over the past two decades, robust optimization has emerged as a leading tool in operations research for dynamic decision-making when uncertainty is driven by unknown or ambiguous probability distributions (Ben-Tal et al. 2009, Delage and Iancu 2015). In this paper, we show that robust optimization can be combined with simulation to develop algorithms for finding Markovian stopping rules to NMOS problems with known probability distributions. Compared to Belomestny (2011a) and Ciocan and Mišić (2020), our approach for optimal stopping does not restrict the space of Markovian stopping rules to any parametric class, and we develop concrete algorithms that are guaranteed to yield -optimal Markovian stopping rules for general classes of NMOS problems.

In greater detail, this paper introduces a new approach for computing Markovian stopping rules for NMOS problems with known probability distributions that is based on a combination of simulation and robust optimization. At a high level, our approach is comprised of the following steps:

- Step 1:

-

We use Monte-Carlo simulation to generate sample paths of the sequence of random states.

- Step 2:

-

From those sample paths, we construct a robust optimization problem that approximates the NMOS problem.

- Step 3:

-

We solve the robust optimization problem to obtain stopping rules for the NMOS problem.

The robust optimization problem constructed in Step 2 can be interpreted as a proxy or surrogate for the NMOS problem. Indeed, if the number of simulated sample paths in Step 1 is sufficiently large, then every Markovian stopping rule that is optimal for the robust optimization problem constructed in Step 2 is guaranteed with high probability to be an -optimal Markovian stopping rule for the NMOS problem; see §2.4. Thus, the approach comprised of the above steps enables the task of computing near-optimal Markovian stopping rules for an NMOS problem to be reduced to the task of solving a robust optimization problem.

With respect to the robust optimization literature, Step 2 of our approach follows a recent paper by Bertsimas, Shtern, and Sturt (2023, henceforth referred to as BSS22). In that paper, the authors showed that a general class of stochastic dynamic optimization problems with unknown probability distributions can in principle be approximated to arbitrary accuracy by a robust optimization problem constructed from historical data. In particular, our work draws on BSS22 in two specific ways. First, our robust optimization problem constructed in Step 2 is a variant of a robust optimization formulation that is proposed in BSS22. Second, by focusing on the application of optimal stopping, we strengthen theoretical developments from BSS22 to prove under relatively mild and verifiable assumptions that the optimal objective value and optimal Markovian stopping rules of the robust optimization problem from Step 2 converge almost surely to those of the NMOS problem as the number of simulated sample paths in Step 1 grows to infinity (Theorems 2.2-2.4 in §2.4). For the interested reader, a discussion of our improvements to the theoretical convergence guarantees from BSS22 is provided at the beginning of Appendix 9.

In contrast to BSS22, the key novelty of the present paper lies not in showing that robust optimization can be used to construct approximations of stochastic dynamic optimization problems; rather, the main contributions of the present paper are algorithmic. Indeed, in order for a combination of simulation and robust optimization to yield near-optimal algorithms for a class of stochastic dynamic optimization problems with known probability distributions, it is not sufficient to construct a robust optimization problem that approximates the stochastic problem to arbitrary accuracy: one must also have exact or provably near-optimal algorithms for solving the robust optimization problem. However, up to this point, there have been no exact algorithms in the literature for solving the type of robust optimization problems proposed by BSS22 in any class of stochastic dynamic optimization problems where uncertainty unfolds over two or more periods. In particular, because solving the type of robust optimization problems from BSS22 requires optimizing over infinite-dimensional spaces of control policies, it has been unknown in any application whether optimal control policies for these robust optimization problems even exist, let alone whether they can ever be tractably computed. These hurdles have, practically speaking, prevented the robust optimization techniques from BSS22 from being combined with simulation to develop algorithms for computing near-optimal control policies for any class of stochastic dynamic optimization problems with known probability distributions until now.

In this paper, we resolve the aforementioned gaps in the robust optimization literature by establishing the first characterization of optimal control policies for the type of robust optimization problems proposed by BSS22 in an application where uncertainty unfolds over two or more periods (Theorem 3.1 in §3). Specifically, we consider the task of solving the robust optimization problems constructed in Step 2 over the infinite-dimensional space of all Markovian stopping rules. Using a novel pruning technique, we prove in Theorem 3.1 that optimal Markovian stopping rules for these robust optimization problems not only exist, but also have a structure that is simple and finite-dimensional. In fact, our characterization reveals that optimal Markovian stopping rules for these robust optimization problems can be compactly parameterized by integer variables , where is the number of simulated sample paths chosen in Step 1 and is the number of periods in the NMOS problem.

Leveraging the structure of optimal Markovian stopping rules for the robust optimization problems constructed in Step 2, we develop exact and heuristic algorithms for solving the robust optimization problem in Step 3. Specifically, we make the following algorithmic contributions:

- (a)

- (b)

- (c)

- (d)

- (e)

In summary, our exact and heuristic algorithms allow us to solve the robust optimization problem constructed in Step 2. Since the robust optimization problem constructed via Steps 1 and 2 serves as an approximation of the NMOS problem to any arbitrary accuracy, our algorithms for solving the robust optimization problem in turn allow us to compute near-optimal Markovian stopping rules for the NMOS problem.

We conclude with numerical experiments that demonstrate the value of our robust optimization-based algorithms in several settings. First, we consider a simple one-dimensional non-Markovian optimal stopping problem with fifty periods, and we compare the robust optimization algorithm to existing methods based on approximate dynamic programming (Longstaff and Schwartz 2001) and parametric stopping rules (Ciocan and Mišić 2020). The experiments show that our method can find stopping rules that significantly outperform those found by the other techniques, while maintaining a comparable computational cost. In particular, the experiments reveal that our method can strictly outperform alternative algorithms for finding Markovian stopping rules to NMOS problems that are based on backwards recursion. Second, we consider a widely-studied and important problem of pricing high-dimensional Bermudan barrier options with over fifty periods. Across several variants of this problem, we demonstrate that our combination of robust optimization and simulation can find stopping rules that match, and in some cases significantly outperform, those from state-of-the-art algorithms by Longstaff and Schwartz (2001), Ciocan and Mišić (2020) as well as the duality-based pathwise optimization method of Desai et al. (2012).

The rest of our paper has the following organization. §1.1 provides a review of methods for solving optimal stopping problems with Markovian and non-Markovian probability distributions. §2 formalizes the problem setting and introduces our robust optimization-based method. §3 characterizes the structure of optimal policies for the robust optimization problem. §4 develops tractable algorithms and computational complexity results for the robust optimization problem. §5 illustrates the performance of our algorithms in numerical experiments. Unless stated otherwise, all technical proofs can be found in the appendices.

1.1 Other Related Literature

Many methods based on approximate dynamic programming (ADP) have been developed for optimal stopping problems with high-dimensional Markovian stochastic processes. The most popular ADP methods for these optimal stopping problems are based on Monte-Carlo simulation and regression, which originate with Carriere (1996), Longstaff and Schwartz (2001) and Tsitsiklis and Van Roy (2001). Given sample paths of the entire stochastic process, these methods use backwards recursion and regression to obtain approximations of the value function, and exercise policies are then obtained by proceeding greedily with respect to the approximate value functions. The efficacy of regression-based methods hinges on selecting a parametrization of basis functions for the value function that strikes a balance between approximation quality and sample complexity. Nonparametric choices for the basis functions, e.g., Lagurerre polynomials, are discussed in the aforementioned works and subsequently analyzed in works such as Clément et al. (2002), Glasserman and Yu (2004), Egloff (2005), Belomestny (2011b) and Zanger (2020). In §5, we provide numerical comparisons of our proposed algorithms to ADP techniques in the context of NMOS problems.

A variety of other nonparametric methods have been developed for solving optimal stopping problems with Markovian probability distributions, such as quantization-based approximations of value functions (Bally and Pages 2003) and scenario tree discretizations of the sequence of random states (Broadie and Glasserman 1997). Recent works have also considered using deep learning to learn the continuation function, including Becker et al. (2019) and Goudenège et al. (2020). The efficacy of deep learning algorithms for optimal stopping hinges on carefully selecting the topology of the neural network and choosing the right tuning algorithm, and performing these tasks effectively in the context of optimal stopping is an ongoing area of research (Fathan and Delage 2021). Methods to compute upper bounds on optimal stopping problems grew in interest due to the independent works of Haugh and Kogan (2004) and Rogers (2002), and duality-based algorithms to obtain upper bounds which combine simulation and suboptimal stopping rules were first proposed by Andersen and Broadie (2004). Other works that harness dual representations to solve optimal stopping and other stochastic dynamic optimization problems include Brown et al. (2010), Desai et al. (2012), Belomestny (2013), and Goldberg and Chen (2018), among many others. In §5, we provide numerical comparisons of our proposed algorithms to the duality-based pathwise optimization method of Desai et al. (2012).

In the context of non-Markovian optimal stopping, methods have been developed which address settings that are different from ours in non-trivial ways. Leão et al. (2019) and Bezerra et al. (2020) develop discretization schemes for NMOS problems over continuous time and restrict the class of probability distributions to those based on the Brownian motion. In contrast to these works, our paper develops algorithms for finding Markovian stopping rules for discrete-time optimal stopping problems, and we do not require any parametric assumptions on the probability distributions of the underlying stochastic processes. NMOS problems can also be addressed by the scenario tree method of Broadie and Glasserman (1997) and the recursive-dual algorithm of Goldberg and Chen (2018), provided that one can perform Monte-Carlo simulation on the conditional probability distribution of the stochastic process in each time period. In contrast to these methods, the algorithms in this paper require only the ability to simulate sample paths of the entire stochastic process and are shown in numerical experiments to be practically tractable in low-dimensional NMOS problems with dozens of time periods. Within the optimal stopping literature, our method is most closely related to a class of simulation-based methods which optimize directly over spaces of deterministic stopping rules, as explored by Garcıa (2003), Andersen (1999), Belomestny (2011a), Gemmrich (2012), Ciocan and Mišić (2020), and Glasserman (2013, §8.2). We discuss connections between our approach and this stream of literature in §2.3, and a discussion of the challenges of using dynamic programming to find the best Markovian stopping rules for NMOS problems can be found in Appendix 7.

Finally, we note that prior research in operations research and economics have studied robust optimal stopping problems in which the goal is to find stopping rules that perform well under worst-case probability distributions (Bayraktar and Yao 2014, Riedel 2009) or under worst-case state trajectories (Iancu et al. 2021). That stream of research differs significantly from ours, as that stream of research does not consider robust optimization problems that are approximations of stochastic optimal stopping problems with known probability distributions.

2 Robust Optimization for Stochastic Optimal Stopping

2.1 Problem Setting

We consider stochastic optimal stopping problems defined by the following components:

States:

Let denote a sequence of random states, where the state in each period is a random vector of dimension . For example, the state in each period may represent the prices of multiple assets at that point in time. The joint probability distribution of this stochastic process is assumed to be known and accessible through a simulator which generates independent sample paths of the entire stochastic process.

Policies:

Let represent a collection of exercise policies, where the exercise policy in each period is a measurable function of the form . Speaking intuitively, each exercise policy is a partitioning of the state space into regions for stopping and continuing. From the exercise policies, the corresponding Markovian stopping rule is a function that maps a realization of the stochastic process to a stopping period:

Throughout this paper, a minimization problem with no feasible solutions is defined equal to .111We remark that the Markovian stopping rule is a non-anticipative control policy, meaning that the event does not depend on the future states for each period . To see why this is the case, consider any two realizations of the sequence of random states and , and suppose for a given period that the two realizations satisfy for all . Then we readily observe from our definition of Markovian stopping rules and from algebra that the Markovian stopping rule satisfies if and only if is satisfied.

Rewards:

Let be a known and deterministic function that maps a stopping period and a realization of the entire stochastic process to a reward. The assumption that the reward function is nonnegative is common in many applications of optimal stopping, and we assume throughout the paper that a stochastic process that is never stopped yields a reward of zero: . It follows from the definition of the reward function that the reward from stopping on any period may in general depend on the states of the stochastic process in previous or future time periods.

Problem:

With the above notation and inputs, the goal of this paper is to solve stochastic optimal stopping problems of the form

| (OPT) |

where the optimization is taken over the space of all Markovian stopping rules. In the following sections, we introduce and analyze a new simulation-based method for solving this class of stochastic dynamic optimization problems.

2.2 The Robust Optimization Approach

Our proposed approach for solving stochastic optimal stopping problems of the form (OPT) consists of the following steps. We first simulate sample paths of the stochastic process . Let denote the number of sample paths, and let the values of the sample paths be denoted by

We assume that the sample paths are independent and identically distributed realizations of the entire (possibly non-Markovian) stochastic process. We next choose the following robustness parameter:

The purpose of the robustness parameter will become clear momentarily, and a discussion on how to choose the number of sample paths and the robustness parameter is deferred until §2.5. With these parameters, let the uncertainty set around sample path on period be defined as

For notational convenience, denote the uncertainty set around sample path across all periods by

Hence, we observe that the role of the robustness parameter is to control the size of these sets. Given the sample paths and choice of the robustness parameter, our approach obtains an approximation of (OPT) by solving the following robust optimization problem:

| (RO) |

By solving the above robust optimization problem, we obtain exercise policies . These exercise policies constitute our approximate solution to the stochastic optimal stopping problem (OPT).

Remark 2.1

In the above formulation of the robust optimization problem (RO), the sample paths in the objective function are allowed to be perturbed by an adversary in the evaluation of the Markovian stopping rule, , but not in the evaluation of the reward, . This is a deviation from the robust optimization formulation from BSS22, presented below as (RO’), in which the worst-case reward over each uncertainty set has the form :

| (RO’) |

The difference between the objective functions of (RO) and (RO’) turns out to be inconsequential from the perspective of establishing convergence guarantees (see §2.4) or characterizing the structure of optimal Markovian stopping rules (see §3). However, (RO) is significantly simpler from the perspective of algorithm design. For the interested reader, an extended discussion on the similarities and differences between (RO) and the alternative robust optimization formulation (RO’) can be found in Appendix 8.

2.3 Background and Motivation

In contrast to traditional robust optimization or distributionally robust optimization, our motivation behind adding adversarial noise to the sample paths in (RO) is not to find stopping rules which have worst-case performance guarantees, are attractive in risk-averse settings, or perform well the presence of an ambiguous probability distribution. Rather, this paper proposes using robust optimization purely as an algorithmic tool for solving stochastic optimal stopping problems of the form (OPT) when the joint probability distributions are known. The present section elaborates on this motivation and positions our use of robust optimization within the optimal stopping literature.

For the sake of developing intuition, let us suppose for the moment that the robustness parameter of the uncertainty sets in (RO) was set equal to zero. In this case, for any fixed exercise policies , the expected reward of those exercise policies,

would be approximated in (RO) by the sample average approximation:

For these fixed exercise policies, we observe that the sample average approximation is a consistent estimator of the expected reward. In other words, for the fixed exercise policies , it follows from the strong law of large numbers under relatively mild assumptions222For example, Assumptions 2.4 and 2.4 in §2.4. that will converge almost surely to as the number of simulated sample paths is taken to infinity.

However, it is well known in the optimal stopping literature that these desirable asymptotic properties of are generally not retained when considering the problem of optimizing over the space of all exercise policies. For instance, Ciocan and Mišić (2020, EC.1.2) provide simple examples in which the following statements hold almost surely:

| (1) |

The asymptotic suboptimality of the optimal objective value and optimal policies for the problem can be intuitively understood as a type of overfitting. To see why line (1) occurs, we recall for any fixed choice of exercise policies that the sample average approximation is an unbiased estimate of the expected reward . However, when simultaneously considering the space of all exercise policies, there exists for each with high probability a collection of exercise policies that satisfies . The problem will thus be biased towards choosing those exercise policies, which in general will be suboptimal for the problem . Because the set of all is an infinite-dimensional space, the gap between the objective values and does not converge to zero uniformly over the set of all as the number of sample paths tends to infinity.

To circumvent this overfitting in the context of optimal stopping in line (1), a vast literature has focused on restricting the functional form of exercise policies to a finite-dimensional space, such as Garcıa (2003), Andersen (1999), Belomestny (2011a), Gemmrich (2012), Ciocan and Mišić (2020). In this approach, the choice of the parameterization for the space of exercise policies must be made very carefully. On one hand, the effective dimension of the restricted space of exercise policies must be small relative to the number of simulated sample paths to ensure that the sample average approximation problem finds the parametric exercise policies that are ‘best-in-class’ with respect to the stochastic optimal stopping problem (Belomestny 2011a, §3). On the other hand, the parameterization must be chosen appropriately in order for the sample average approximation problem to obtain a good approximation of (OPT). Choosing such an appropriate parameterization “may be counterfactual in some cases”, as explained by Garcıa (2003, p. 1859), “since we may not have a good understanding of what the early exercise rule should depend on.”

Our approach, in view of the above discussion, provides an alternative means to circumvent overfitting. The proposed robust optimization problem allows the space of exercise policies to remain general, and thus relieves the decision maker from the need to select and impose a parametric structure on the exercise policies. Moreover, we show in the following section that our use of robust optimization provably overcomes the asymptotic overfitting described in line (1).

2.4 Optimality Guarantees

In this subsection, we establish theoretical justification for our combination of robust optimization and simulation that is presented in §2.2. Specifically, we strengthen convergence guarantees from BSS22 to the specific problem of optimal stopping to prove that the optimal objective value and optimal exercise policies of (RO) converge almost surely to those of the stochastic optimal stopping problem (OPT) under mild and verifiable conditions. Establishing these convergence guarantees in the context of optimal stopping is necessary to ensure that (RO) will provide a high-quality approximation of the stochastic optimal stopping problem (OPT) when the robustness parameter is sufficiently small and the number of simulated sample paths is sufficiently large.

To establish our theoretical results, we make four relatively mild assumptions on the stochastic optimal stopping problem (OPT). Our first assumption, denoted below by Assumption 2.4, concerns the structure of the reward functions in the optimal stopping problem, and can be roughly interpreted as a requirement that the reward function changes continuously as a function of the states: {assumption} almost surely, where

From a practical standpoint, it is easy to see that Assumption 2.4 holds whenever the functions are continuous, and it can also hold in important stochastic optimal stopping problems with discontinuous reward functions.333To illustrate, consider Robbin’s problem (Bruss 2005), in which the reward functions are discontinuous and the probability distribution is . To show that Assumption 2.4 is satisfied, we observe that the random variable is strictly positive with probability one, which implies that for all .

Our second and third assumptions concern the structure of the probability distribution in (OPT). Specifically, Assumption 2.4 enforces that the stochastic process has a light tail, and Assumption 2.4 says the stochastic process is drawn from a continuous probability distribution. {assumption} The stochastic process satisfies for some . {assumption} The stochastic process has a probability density function. Let us reflect on the practical restrictiveness of these two assumptions. The second assumption, Assumption 2.4, is a standard light-tail assumption on the stochastic process which is satisfied, for example, if the stochastic process is bounded or has a multivariate normal distribution. This assumption greatly simplifies our analysis, as it allows us to invoke a convergence result by BSS22 in our proofs (see Appendix 9). We impose the third assumption, Assumption 2.4, to ensure that there exist arbitrarily near-optimal Markovian stopping rules for (OPT) that satisfy a certain technical continuity structure that we can exploit in our proof. As far as we can tell, these assumptions on the probability distribution are relatively mild and routinely satisfied in applications of optimal stopping in the context of the options pricing literature. Nonetheless, we do not preclude the possibility that these assumptions on the probability distribution can be weakened while still establishing convergence guarantees.

Our fourth and final assumption imposes boundedness on the reward function. This assumption, presented below as Assumption 2.4, leads to a considerably simpler proof and statement of the results, but can generally be relaxed to reward functions bounded above by an integrable, Lipschitz-continuous function. {assumption} The reward function satisfies for all and .

We emphasize that each of the aforementioned four assumptions on the stochastic optimal stopping problem (OPT) can be verified a priori. In particular, they do not require any knowledge of the structure of optimal exercise policies for the stochastic optimal stopping problem (OPT). As a result, each of these assumptions can be verified using the information typically available in practice. We note that these assumptions are considerably weaker than those in BSS22, which require knowledge of the structure of optimal control policies to establish convergence results.

Under the above conditions, the following theorems provide justification for using the robust optimization problem as a proxy for the stochastic optimal stopping problem. In a nutshell, the following Theorems 2.2-2.4 show that (RO) will, for all sufficiently small choices of the robustness parameter and all sufficiently large choices of the number of simulated sample paths, yield a near-optimal approximation of (OPT). Stated another way, the following theorems show that our use of robust optimization provably overcomes the asymptotic overfitting described in line (1) of §2.3. While the following theorems do not specify how to choose the robustness parameter and number of simulated sample paths for any particular optimal stopping problem, we provide guidance (§2.5) and numerical evidence (§5) which suggest that these parameters can be found effectively in practice. A discussion of the technical innovations as well the proofs of the following theorems in this subsection can be found in Appendix 9.

Our first theorem shows that the optimal objective value of the robust optimization problem (RO) will converge almost surely to that of the stochastic problem (OPT) as the robustness parameter tends to zero and the number of sample paths tends to infinity. In the following result, we use the notation to denote the objective value of the robust optimization problem (RO) corresponding to exercise policies .

Our second theorem shows that the expected reward of the optimal exercise policies for the robust optimization problem (RO) will converge almost surely to the optimal objective value of the stochastic problem (OPT). We let denote optimal exercise policies for (RO), and we remark that the existence of optimal exercise policies for the robust optimization problem will be established in §3.

Because we will develop algorithms that solve the robust optimization problem approximately as well as exactly, it is imperative for us to have theoretical guarantees that hold for any Markovian stopping rule that can be found by the robust optimization problem. To this end, our third and final theorem of this section shows that the (in-sample) robust objective value will asymptotically provide a low-bias estimate of the expected reward, and this bound holds uniformly over all exercise policies. The result yields theoretical assurance, provided that the robustness parameter is sufficiently small and the number of sample paths is sufficiently large, that searching for exercise policies with high robust objective values will typically result in exercise policies with high expected rewards .

2.5 Implementation Details

In anticipation of algorithmic techniques for solving the robust optimization problem (RO) in the remainder of the paper, it remains to be specified how the parameters of the robust optimization problem (the number of simulated sample paths and the robustness parameter ) should be selected in practice. For the sake of concreteness, we conclude §2 by briefly providing guidance for choosing these parameters and applying the robust optimization approach in practice. The procedures described below are formalized in Algorithm LABEL:fig:heuristic and implemented in our numerical experiments in §5.

As described previously, this paper addresses stochastic optimal stopping problems in which the probability distributions are known. Consequently, the decision-maker is granted flexibility in choosing the number of sample paths to simulate. On one hand, we have established in the previous section that larger choices of the number of simulated sample paths will generally lead to tighter approximations of the stochastic optimal stopping problem. On the other hand, larger choices of require a greater computation cost in performing the Monte-Carlo simulation and creates a robust optimization problem of a larger size. To balance these tradeoffs in particular applications, we recommend using a straightforward procedure of starting out with a small choice of and iteratively increasing the number of simulated sample paths until the total computational cost meets the allocated computational budget.

Given a fixed number of sample paths, the choice of the robustness parameter can have a significant impact on the policies produced by the robust optimization problem. To this end, we recommend solving (RO) over a grid of possible choices for the robustness parameter. Because the probability distribution is known, we can generate a second set of ‘validation’ sample paths to select the best choice of the robustness parameter. Specifically, for each choice of the robustness parameter, one solves the robust optimization problem to obtain exercise policies. The expected reward of the exercise policies is then estimated using the validation set of sample paths. Finally, we select the value of the robustness parameter (and the corresponding exercise policies) which maximizes the average reward with respect to the validation set.

In summary, we have described straightforward and easy-to-implement heuristics for choosing the parameters of the robust optimization problem. Applying the heuristics and solving the robust optimization problem yields exercise policies for the stochastic optimal stopping problem, and an unbiased estimate of the expected reward of these exercise policies can similarly be obtained by simulating a set of ‘testing’ sample paths (see Algorithm LABEL:fig:heuristic). Because the exercise policies obtained from the robust optimization problem are feasible for the stochastic optimal stopping problem, the expected reward of these exercise policies is thus a lower bound on the optimal objective value of the stochastic optimal stopping problem. Finally, we remark that under a stronger assumption in which one has the ability to perform conditional Monte Carlo simulation, the exercise policies obtained from solving the robust optimization problem can be combined with the method of Andersen and Broadie (2004) to obtain an upper bound on the optimal objective value of the stochastic optimal stopping problem.

3 Characterization of Optimal Markovian Stopping Rules

In §2, we showed that our combination of robust optimization and simulation (§2.2) can yield an arbitrarily close approximation of the stochastic optimal stopping problem (§2.4-§2.5). In this section, we develop the key technical result of this paper, Theorem 3.1, which will enable us to design exact and heuristic algorithms for solving the robust optimization problem. Specifically, Theorem 3.1 establishes the existence and characterizes the structure of optimal Markovian stopping rules for the robust optimization problem (RO). In §3.1 and §3.2, we present the statement of Theorem 3.1 and provide a sketch of its proof. In §3.3, we use the characterization of optimal Markovian stopping rules to transform (RO) from an optimization problem over an infinite-dimensional space of exercise policies into a finite-dimensional optimization problem over integer decision variables (Theorem 3.7).

3.1 Statement of Theorem 3.1

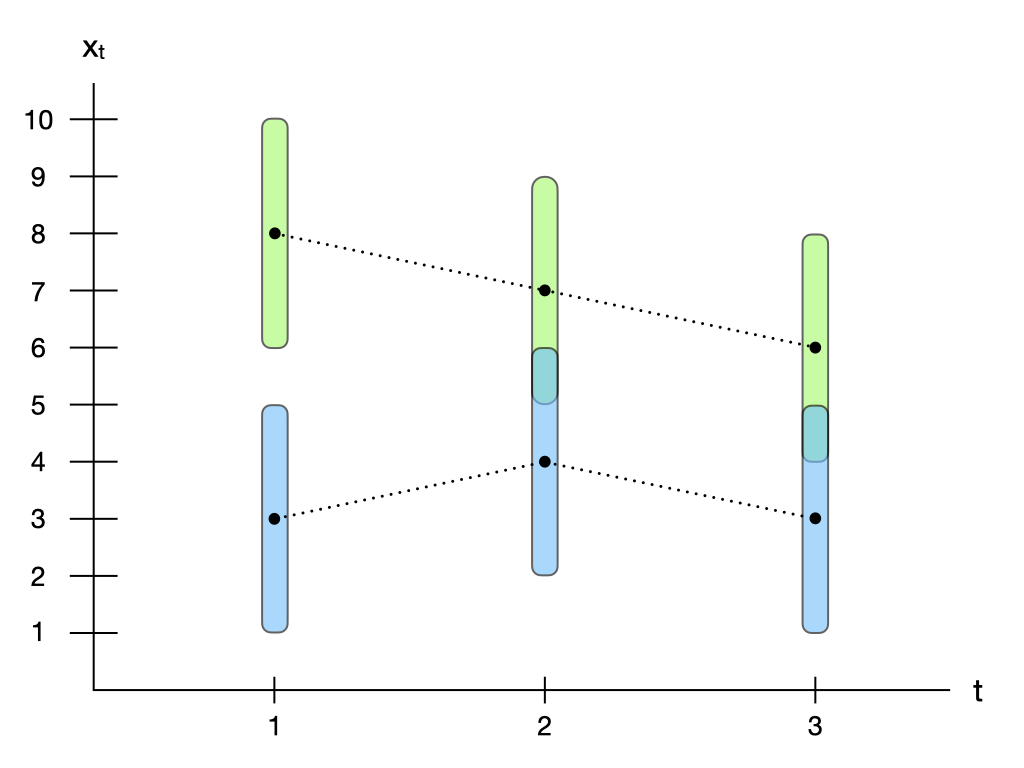

We begin by introducing the notation that will be used in our characterization of the structure of optimal Markovian stopping rules for the robust optimization problem (RO). Consider any instance of the robust optimization problem (RO). For any choice of integers , we define as the exercise policy that satisfies the following equality for each period and each state :

| (2) |

To develop intuition of the above exercise policy, we remark for each sample path that the integer can be interpreted as a selection of one of the uncertainty sets . Specifically, if , then we observe from the above definition that the exercise policy will satisfy for all . More generally, we observe that the exercise policy will satisfy for period and state if and only if there exists an uncertainty set such that the state is contained in the uncertainty set, , and the integer corresponding to the th sample path is equal to the current period, . A visualization of the exercise policy is found in Figure 1.

Let the set of all exercise polices generated by integers be denoted by

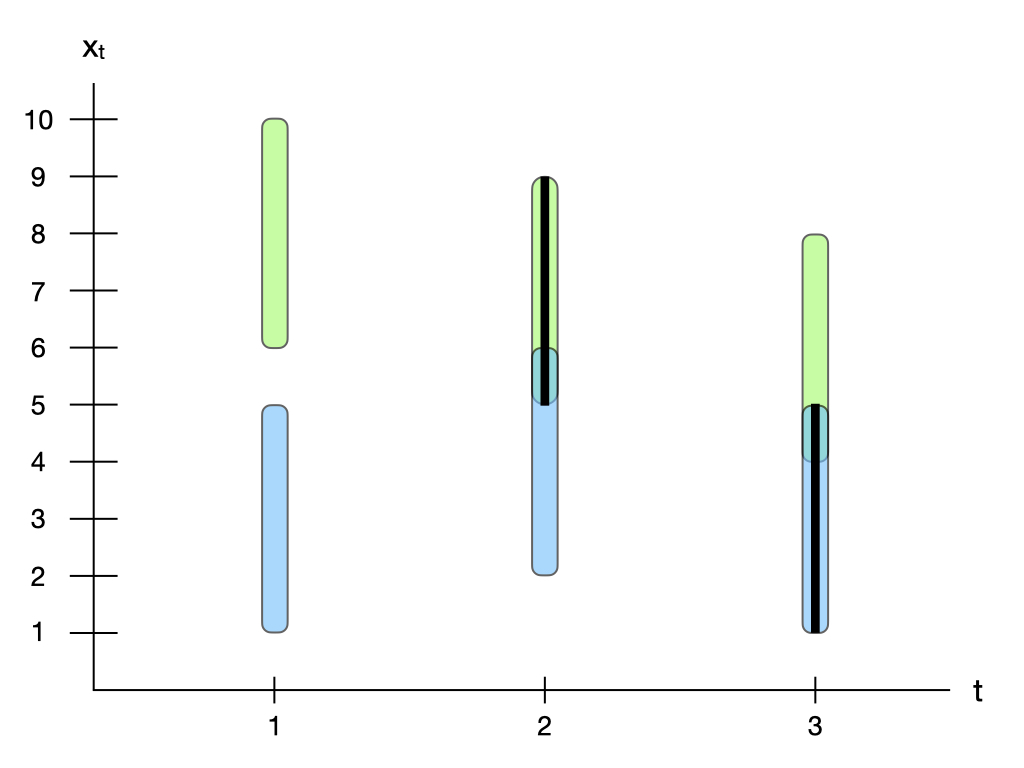

It is clear from the above definition that each of the exercise policies is parameterized by integers ; thus, we readily observe that the cardinality of is always finite and upper bounded by . Moreover, we observe that the definition of the set of exercise policies is sample-path dependent, in the sense that depends on the number and realizations of the simulated sample paths and on the choice of the robustness parameter . In Figure LABEL:fig:exhaustive, we present a visualization of the set of exercise policies .

In view of the above notation, we now present our main result:

Theorem 3.1

There exists that is optimal for (RO).

The above theorem shows that there always exists an exercise policy in the set that is optimal for the robust optimization problem. The result is significant because it will allow us to transform (RO) from an optimization problem over an infinite-dimensional space of exercise policies into a finite-dimensional combinatorial optimization problem over the set . Moreover, Theorem 3.1 is important because it establishes the existence of optimal Markovian stopping rules for the robust optimization problem (RO).

3.2 Proof Sketch of Theorem 3.1

Our proof of Theorem 3.1 follows an exchange argument that is rooted in a technique that we refer to as pruning. The technique consists of starting with an initial exercise policy and then modifying the exercise policy to reduce the size of the stopping regions . By carefully pruning (i.e., reducing the size of) the stopping regions of the initial exercise policy , we will show that any initial exercise policy can be transformed into a new exercise policy with the same or better objective value in the robust optimization problem (RO).

To discuss the proof in greater detail, we begin by stating two preliminary lemmas:

Lemma 3.2

The optimal objective value of (RO) is equal to the optimal objective value of

| (ROT) |

Lemma 3.3

Consider any that satisfies the constraints of (ROT), and define

Then the following equality holds for each :

The first preliminary lemma shows that a structural constraint can be imposed onto the exercise policies in the robust optimization problem (RO) without any loss of optimality. In particular, Lemma 3.2 says that we can restrict to exercise policies in which the resulting Markovian stopping rule satisfies for each trajectory in each of the uncertainty sets .444Recall that the definition of a Markovian stopping rule is . Therefore, we readily observe for each sample path that an exercise policy satisfies for all if and only if there exists a period that satisfies for all . The second preliminary lemma develops a convenient representation of the objective function of (ROT). Specifically, Lemma 3.3 shows for each sample path that the quantity in the objective function of (ROT) is equal to the the minimum among all periods for which the uncertainty set has a nonempty intersection with the stopping region .

Equipped with the above preliminary lemmas, we now formally define the pruning technique that underpins our proof of Theorem 3.1.

Definition 3.4

Let be an exercise policy that is feasible for (ROT). We say that is a pruned version of if the stopping regions of are a subset of the stopping regions of , i.e.,

and if the following equality holds for each sample path :

Speaking intuitively, an exercise policy is a pruned version of an exercise policy if the stopping regions of are a subset of the stopping regions of and if for each sample path . The significance of Definition 3.4 in combination with Lemma 3.3 is established by the following Lemma 3.5; specifically, the following Lemma 3.5 shows that if is a pruned version of , then the robust objective value associated with is greater than or equal to the robust objective value associated with .

Lemma 3.5

If is a pruned version of , then .

In summary, we have shown in Lemma 3.2 that the robust optimization problem (RO) is equivalent to the robust optimization problem (ROT). Moreover, for every initial exercise policy that is feasible for (ROT), Lemma 3.5 shows that the objective value associated with is less than or equal to the objective value associated with every exercise policy that is a pruned version of . The final step of our proof of Theorem 3.1 is given by the following lemma:

Lemma 3.6

The above lemma implies that if is a feasible exercise policy for (ROT), then there always exists an exercise policy that is a pruned version of . Hence, we conclude from Lemmas 3.2, 3.5, and 3.6 that there always exists an exercise policy that is optimal for (RO). The omitted details of the proofs of Theorem 3.1 and Lemmas 3.2, 3.3, 3.5, and 3.6 are found in Appendix 10.

3.3 Reformulation of (RO) as a Finite-Dimensional Optimization Problem

We conclude §3 by using our characterization of optimal Markovian stopping rules (Theorem 3.1) to develop a reformulation of (RO) as a finite-dimensional optimization problem over integer decision variables . The reformulation from this subsection is important because it establishes a natural combinatorial interpretation of the robust optimization problem (RO), which will provide the foundation for our algorithmic developments in §4.1 and §4.2.

Our finite-dimensional reformulation is presented as the following optimization problem (IP):

| (IP) |

The decision variables in the above optimization problem are the integers . We further observe that the inner minimization problems in (IP) involves constraints that depend on whether the intersection is nonempty for each pair of sample paths and each period . An important insight is that these intersections can be precomputed; that is, given the construction of the uncertainty sets from §2.2, we can efficiently precompute the set of all pairs of sample paths and periods that satisfy .555We recall from §2.2 that each uncertainty set is a hypercube. Thus, determining whether is nonempty for each pair of sample paths and each period can be precomputed in a total of computation time.

Theorem 3.7

The proof of Theorem 3.7, which is found in Appendix 10, follows readily from Lemmas 3.2, 3.3, 3.5, and 3.6. Stated in words, the above theorem shows, for any given feasible solution for the optimization problem (IP), that the objective value associated with the exercise policy in the optimization problem (RO) is greater than or equal to the objective value associated with in the optimization problem (IP). Because the above theorem also shows that optimal objective value of (RO) is equal to the optimal objective value of (IP), it follows immediately from Theorem 3.7 that any optimal solution for (IP) can be transformed into an optimal solution for (RO).

4 Computation of Optimal Markovian Stopping Rules

In this section, we use our characterization of optimal Markovian stopping rules from §3 to develop exact and heuristic algorithms for solving the robust optimization problem (RO). In §4.1, we use this finite-dimensional reformulation of (RO) to design exact algorithms and hardness results for solving the robust optimization problem. In §4.2, we propose and analyze an efficient heuristic algorithm for approximately solving the robust optimization problem. We emphasize that the algorithms and analysis in this section are general and do not require any of the assumptions that were made in §2.4.

4.1 Exact Algorithm

In §3.3, we developed a finite-dimensional optimization problem (IP) with integer decision variables that is equivalent to the infinite-dimensional robust optimization problem (RO). Specifically, we showed that the optimal objective values of the optimization problems (IP) and (RO) are always equal. Moreover, we readily observe from Theorem 3.7 that any optimal solution for (IP) can further be transformed into an optimal exercise policy for (RO) through the transformation described by line (2) in §3. Harnessing this optimization problem (IP), we now design exact algorithms for solving the robust optimization problem (RO).

We begin our discussion by considering the case of (IP) when there are two periods. Optimal stopping problems with two periods has been studied in the literature as a testbed for understanding the complexity of solving optimal stopping problems, e.g., Glasserman and Yu (2004). We defer the proof of the following result to §4.2.4.

Theorem 4.1

If , then (IP) can be solved in time.

Continuing with our discussion on the theoretical tractability of (IP), we next consider problems with three or more periods. The following negative result shows that the computational tractability of (IP) in the case of two periods established in Theorem 4.1 does not generally extend to optimal stopping problems with three or more periods. The proof of the following result, which is found in Appendix 11, consists of a reduction from MIN-2-SAT, which is shown to be strongly NP-hard by Kohli et al. (1994).

Theorem 4.2

(IP) is strongly NP-hard for any fixed .

Motivated by the above hardness result, we proceed to develop an exact algorithm for solving (IP) by reformulating it as a zero-one bilinear program over totally unimodular constraints. This reformulation, presented below as (BP), is valuable for three primary reasons. First, it is well known that bilinear programs can generally be transformed into mixed-integer linear optimization problems using linearization techniques; see Appendix 12 for details. Thus, for robust optimization problems with small values of and , the exact reformulation from this section can directly solved by off-the-shelf commercial optimization software. Second, the exact reformulation (BP) will provide the foundation for our heuristic algorithm for the robust optimization problem in the following §4.2. Third, the exact reformulation (BP) is relatively compact, requiring only decision variables and constraints. In particular, the mild dependence of the size of the exact reformulation on the number of simulated sample paths is attractive in practical settings where the number of simulated sample paths is much larger than the number of time periods.

Our reformulation of (IP) as a zero-one bilinear program over totally unimodular constraints (BP) requires the following additional notation. For each sample path , we define the following set:

The above set can be interpreted as the set of distinct values among and . For notational convenience, let the elements of be indexed in ascending order, , and let be defined for each period as the unique index that satisfies the equality . We readily observe that the quantities and can be efficiently precomputed for each sample path and period . With the above notation, our exact reformulation of (IP) is stated as follows:

| (BP) | ||||||

| subject to |

Let us reflect on the structure of the above optimization problem. First, we observe that (BP) is a bilinear program because its objective function is the sum of products of decision variables and . Second, we observe that the bilinear program (BP) is comprised of binary decision variables as well as continuous decision variables . In particular, we readily observe from the structure of the constraints of (BP) and from the fact that each quantity is strictly positive that there always exists an optimal solution for (BP) in which each decision variable is equal to zero or one. For this reason, (BP) will be henceforth referred to as a zero-one bilinear program without any ambiguity in terminology. Finally, we remark that the constraints of (BP) are totally unimodular, which implies that every extreme point of the polyhedron defined by the constraints of (BP) is integral (Conforti et al. 2014, §4.2). We will utilize the total unimodularity of (BP) in §4.2 when designing our heuristic algorithm for the robust optimization problem.

We next show that (BP) is indeed equivalent to (IP). In the following Theorem 4.3, we establish this equivalence and show that any feasible solution for (BP) can be transformed into a feasible solution for (IP) with the same or greater objective value. The proof of Theorem 4.3, as well as the proofs of the subsequent lemmas in §4.1, are found in Appendix 13.

Theorem 4.3

The above theorem shows for each sample path that the decision variables in (BP) can be interpreted as an encoding of an integer for (IP). In other words, given any feasible solution for (BP), Theorem 4.3 shows how to construct a feasible solution for (IP) such that the objective value associated with in the optimization problem (IP) is greater than or equal to the objective value associated with in the optimization problem (BP). Because the above theorem also shows that optimal objective value of (IP) is equal to the optimal objective value of (BP), it follows immediately from Theorem 4.3 that any optimal solution for (BP) can be transformed into an optimal solution for (IP).

We conclude §4.1 by providing intuition for the role of the decision variables in the optimization problem (BP). To do this, we outline the two key steps of our derivation of (BP). Indeed, recall that the optimization problem (IP) is comprised of integer decision variables . The first step in our derivation of (BP) is to introduce binary decision variables for each sample path to represent each integer decision variable . Specifically, consider the following nonlinear binary optimization problem:

| (BP-1) | ||||||

| subject to |

where the function is defined for each sample path as

To make sense of the function , we remark that each quantity will be equal to one if and only if is the earliest period for sample path that satisfies the equality . With this observation, the first step in our derivation of (BP) is comprised of the following lemma:

Lemma 4.4

The above lemma establishes the equivalence of (IP) of (BP-1), and it shows that any feasible solution for (BP-1) can be transformed into a feasible solution for (IP) with the same or greater objective value. In the second and final step in our derivation of (BP), denoted below by Lemma 4.5, we show that each function can be represented as the optimal objective function of a linear optimization problem.

Lemma 4.5

For each sample path , is equal to the optimal objective value of the following linear optimization problem:

| (3) | ||||||

| subject to |

4.2 Heuristic Algorithm

In §4.1, we developed an exact reformulation of the robust optimization problem (RO) as a zero-one bilinear program over totally unimodular constraints (BP). That bilinear program can be solved by off-the-shelf software for mixed-integer linear optimization; see Appendix 12. Thus, the previous subsection can be viewed as a concrete and easily implementable exact algorithm for solving the robust optimization problem.

Building upon (BP), we now turn to the task of developing efficient algorithms that can approximately solve the robust optimization problem. Specifically, the main contribution of §4.2 is a practical heuristic for solving the robust optimization problem with computation time that is polynomial in both the number of sample paths and the number of periods . The proposed heuristic is thus significantly more computational tractable than solving (BP), which was shown in Theorem 4.2 to be NP-hard. Moreover, we will provide theoretical and empirical evidence that the proposed heuristic can perform surprisingly well, both with respect to approximation quality and computational tractability. All omitted proofs of results from §4.2 can be found in Appendix 14.

This subsection is organized as follows. In §4.2.1, we discuss the high-level motivation and intuition behind our proposed heuristic for the robust optimization problem. In §4.2.2 and §4.2.3, we formalize the heuristic and offer a strongly polynomial-time algorithm for implementing it. In §4.2.4, we provide theoretical guarantees which show that the approximation gap of the heuristic cannot be arbitrarily bad and, in some cases, is guaranteed to be equal to zero. We study the empirical performance of the heuristic in the subsequent §5.

4.2.1 Preliminaries.

Our heuristic for approximately solving the robust optimization problem is motivated by the structure of the exact reformulation (BP) from §4.1 for the robust optimization problem. Recall that (BP) is a zero-one optimization problem with a bilinear objective function and totally unimodular constraints. Because the constraints of (BP) are totally unimodular, the computational difficulty of solving (BP) can thus be attributed to the nonlinearity of its objective function. The proposed heuristic, which is formalized in §4.2.2, aims to contend with this difficulty by approximating the nonlinear objective function of (BP) with a linear function.

To describe the motivation behind our heuristic in greater detail, consider any function that is linear in the vectors and is a lower bound on the objective function of the optimization problem (BP) for all that satisfy the constraints of (BP). That is, let be a linear function that satisfies the following condition:

| (4) |

Then it follows immediately from the condition on line (4) that a conservative, lower-bound approximation of the optimization problem (BP) is given by the following optimization problem:

| (H) | ||||||

| subject to |

Indeed, we observe that the constraints of (H) are identical to the constraints of (BP). The only difference between these two optimization problems is that the nonlinear objective function of (BP) has been replaced with the linear function that satisfies the condition from line (4). Therefore, we conclude that every optimal solution for the optimization problem (H) will be a feasible solution for the optimization problem (BP), and the optimal objective value of (H) will always be less than or equal to the optimal objective value of (BP).

Given any linear function that satisfies the condition from line (4), the above optimization problem (H) is useful because it provides a means to computing approximate solutions for (BP). Indeed, the fact that (H) and (BP) have the same constraints implies that any optimal solution for (H) is a feasible solution for (BP). Moreover, it is always theoretically possible to choose the function such that every optimal solution for (H) is an optimal solution for (BP), as shown by the following Proposition 4.6. We thus conclude that solving the optimization problem (H) has the potential to yield high-quality approximate solutions for (BP).

Proposition 4.6

The optimization problem (H) is ultimately attractive compared to (BP) from the perspective of computational tractability. Indeed, we observe that (H) is a zero-one linear optimization problem over totally unimodular constraints. This implies that the integrality constraints on the decision variables can be relaxed without loss of generality; that is, (H) can be solved as a linear optimization problem in which each constraints are replaced with (Conforti et al. 2014, §4.2). The optimization problem (H) is thus particularly convenient from an implementation standpoint: as a linear optimization problem, (H) can be easily formulated and solved directly by commercial linear optimization solvers such as CPLEX or Gurobi.

In fact, the optimization problem (H) can be solved very efficiently by exploiting the relationship between (H) and the maximal closure problem. The maximal closure problem is a problem from combinatorial optimization that has been widely studied in the operations research literature dating back to Rhys (1970) and Picard (1976), with applications ranging from project scheduling to open-pit mining.666For further background on the maximal closure problem, we refer the interested reader to Hochbaum (2004). The goal in the maximal closure problem is to find a maximum-weight closure in a directed graph, where a closure is defined as a subset of vertices without edges that leave the subset. In particular, it follows immediately from Picard (1976, §3) that the linear optimization problem (H) with decision variables and constraints is equivalent to computing the maximal closure of a directed graph with nodes and edges. An important algorithmic property is that maximal closure problems can be solved by computing the maximum flow in the directed graph (Picard 1976, §4). Thus, as we will formalize in §4.2.3, the optimization problem (H) can be solved with running time that is strongly polynomial with respect to both the number of simulated sample paths and the number of time periods .777We note that Proposition 4.6 does not contradict our hardness result for the robust optimization problem (RO) from Theorem 4.2, as the right choice of the linear function in Proposition 4.6 may be difficult to identify.

4.2.2 Description of Heuristic.

In §4.2.1, we discussed the high-level motivation and intuition behind our proposed heuristic. In view of that motivation, we now formally describe our proposed heuristic for approximately solving the optimization problem (BP). Specifically, our proposed heuristic consists of solving the optimization problem (H) with a particular linear objective function, denoted below by .

To formally describe our proposed heuristic, we require the following notation. Recall that is the number of periods in the optimal stopping problem. For each sample path , let be defined as the period in which the sample path achieves its maximum reward, and if there are multiple optimal solutions, we choose the optimal solution that is smallest. To simplify our notation, let us define as the set that contains the period in which sample path achieves its maximum reward as well as the last period of the optimal stopping period.

With this additional notation, the proposed heuristic obtains approximate solutions for the optimization problem (BP) by solving the optimization problem (H) with the objective function

In other words, our heuristic for solving the optimization problem (BP) consists of solving the optimization problem (H) with objective function given by . The optimal solution for (H) with objective function constitutes a feasible solution for (BP), since the constraints of (H) and (BP) are identical. This solution can thus be transformed into a Markovian stopping rule using the transformations described in Theorem 3.7 and 4.3.

Remark 4.7

We readily observe that the function is linear in and . Moreover, it follows from algebra that is less than or equal to the objective function of (BP) for all feasible solutions of (BP); that is, the linear function satisfies the condition from line (4).888To see why is a lower bound on the objective function of (BP), consider any arbitrary vectors that satisfy the constraints of (BP). Since feasibility for the optimization problem (BP) implies that is a binary vector, we observe that the equality holds for each , , and . Therefore, a lower-bound approximation of the objective function of the optimization problem (BP) can be obtained by replacing each term with if and with if . Thus, we conclude that solving the optimization problem (H) with objective function will provide a lower-bound approximation of the optimization problem (BP), and any optimal solution for (H) will be a feasible solution for (BP).

Our motivations for using the heuristic outlined above are two-fold. First, we find that the optimization problem (H) with the objective function is highly tractable from both a theoretical and empirical standpoint on realistic sizes of robust optimization problems. Second, we provide theoretical and empirical evidence that the above heuristic can find high-quality and in some cases optimal solutions for (BP). We elaborate on the theoretical aspects of these two motivations in §4.2.3 and §4.2.4, and we explore the empirical performance of the heuristic in the subsequent §5.

4.2.3 Algorithms for Implementing Heuristic.

In §4.2.1, we argued generally that the optimization problem (H) with any linear objective function can be solved in strongly polynomial time by reducing (H) to a maximal closure problem. We now formalize those earlier arguments to derive an explicit, strongly polynomial-time algorithm for solving the optimization problem (H) in the particular case where . Specifically, the main contribution of §4.2.3 is the development of an algorithm that achieves the running time that is specified in the following proposition:

Proposition 4.8

If , then (H) can be solved in time.

The above proposition establishes the computational tractability of our heuristic by demonstrating that an optimal solution for the optimization problem (H) with objective function can be computed with running time that is polynomial in both the number of simulated sample paths as well as the number of time periods. In particular, if the number of periods is held constant, then the running time in Proposition 4.8 scales cubically in the number of simulated sample paths . Such a tractability guarantee is ultimately important from a practical perspective: indeed, in the following §5, we will present numerical experiments which show that our heuristic can run in seconds on realistic problem sizes with over fifty periods and thousands of sample paths. An outline of the proof of Proposition 4.8 is found throughout the rest of §4.2.3.

To develop an algorithm with the computation time that is specified in Proposition 4.8, we begin by deriving a compact reformulation of (H) when the objective function satisfies . The compact reformulation is denoted below as the optimization problem (). To derive this compact reformulation, we first show that many of the decision variables in the optimization problem (H) can, without loss of generality, be removed from (H) when the objective function satisfies . In particular, our compact reformulation will utilize the following lemma:

Lemma 4.9

If , then there exists an optimal solution for (H) that satisfies and satisfies for each sample path and period .

The above lemma demonstrates that the optimal values for many of the decision variables of (H) can be known in advance when the objective function satisfies . Hence, Lemma 4.9 implies that each decision variable can be fixed to its optimal value and removed from (H) when , except for the decision variables in which the sample path and period satisfy and . In view of Lemma 4.9, we now consider the following optimization problem:

| () | ||||||

| subject to |

It can be shown using straightforward algebra that the above optimization problem () is equivalent to the optimization problem (H) when the objective function of (H) satisfies and when the decision variables in (H) are restricted to satisfy and for all and ; see proof of the following Lemma 4.10 for details. Hence, it follows from Lemma 4.9 that any optimal solution for () can be transformed into an optimal solution for (H) when the objective function satisfies . We formalize the equivalence of (H) and () in the following Lemma 4.10:

Lemma 4.10

To summarize, we have shown in Lemmas 4.9 and 4.10 that solving the optimization problem (H) can be reduced to solving the optimization problem () when the objective function of (H) satisfies . More precisely, we have shown that any optimal solution for () can be transformed into an optimal choice for the decision variables in (H) when the objective function of (H) satisfies . By applying the transformations described in Theorems 3.7 and 4.3, we can construct exercise policies from the decision variables whose robust objective value in the robust optimization problem is greater than or equal to the optimal objective value of ().

From a computational tractability standpoint, the optimization problem () is ultimately attractive because it has significantly fewer decision variables and fewer constraints than the optimization problem (H). Indeed, we observe from inspection that () has decision variables and constraints, whereas (H) has decision variables and constraints. Because of the same reasoning as given in §4.2.1, the integrality constraints on the decision variables can also be relaxed without loss of generality; that is, (H) can be solved as a linear optimization problem in which each constraints are replaced with . Thus, () can be easily formulated and solved directly by commercial linear optimization solvers.

We conclude §4.2.3 by using the above optimization problem () to outline the proof of Proposition 4.8. Specifically, our proof of Proposition 4.8 consists of reformulating () as a maximal closure problem in a directed graph. We then use the efficient maximum-flow algorithm of Orlin (2013) to solve the maximal closure problem. The remaining details for the proof of Proposition 4.8 are found in Appendix 14.

4.2.4 Approximation Guarantees.

We conclude §4.2 by performing a theoretical analysis of the approximation quality of the proposed heuristic () for the optimization problem (BP). Our motivation here is to understand whether the proposed heuristic is ever guaranteed to find optimal solutions for (BP) and, conversely, whether it is ever possible for the gap between the optimal objective values of () and (BP) to be arbitrarily large. Our answers to these theoretical questions are presented below in Propositions 4.11, 4.12, and 4.13.

We begin by focusing on optimal stopping problems in which the number of periods is equal to two. We recall from Theorem 4.1 in §4.1 that any instance of the robust optimization problem with two periods can be solved exactly in strongly polynomial-time. We will now prove Theorem 4.1 by establishing that the approximation gap between () and (BP) is always equal to zero when the number of periods is equal to two:

Proposition 4.11

If , then the optimal objective values of () and (BP) are equal.

Our takeaways from the above proposition are two-fold. First, Proposition 4.11 shows that there indeed exist settings in which the proposed heuristic is guaranteed to find optimal solutions for (BP). Second, Proposition 4.11 in combination with Theorems 3.7 and 4.3 implies that solving the robust optimization problem (RO) can reduced to solving the optimization problem () when . Therefore, we observe that the proof of Theorem 4.1 follows immediately from Propositions 4.8 and 4.11.

We next develop a general bound on the gap between the optimal objective values of () and (BP) that holds for any fixed number of periods . For notational convenience, we let denote the optimal objective value of (BP) and denote the optimal objective value of ().

Proposition 4.12

.

The above proposition can be viewed as valuable from a theoretical perspective, as it shows that the gap between the optimal objective values of () and (BP) can never be arbitrarily large. Indeed, we recall from Remark 4.7 and Lemma 4.10 that the optimal objective value of () is always less than or equal to the optimal objective value of (BP). Thus, Proposition 4.12 establishes that there exist bounds on the gap between the optimal objective values of () and (BP) that are independent of the choice of the number of simulated sample paths , the choice of the robustness parameter that controls the size of the uncertainty sets, the reward function, etc.

Our third theoretical guarantee in §4.2.4, stated below as Proposition 4.13, provides a bound on the gap between the optimal objective values of () and (BP) that does not depend on the number of periods . Our theoretical bound in Proposition 4.13 will require that the reward function of the NMOS problem satisfies the following regularity condition:

There exists a constant such that, for each period , the reward function satisfies for all . The above assumption stipulates for each period that the reward function is Lipschitz-continuous with respect to the state . The above assumption is relatively mild in applications such as options pricing when the reward function depends only on the current state in each period.999For example, we observe that Assumption 4.2.4 is satisfied by the reward function in the multi-dimensional barrier option pricing problem from §5.2 when the state space in the optimal stopping problem is augmented as . We will impose Assumption 4.2.4 in the following Proposition 4.13 to eliminate pathological situations in which slight perturbations of sample paths lead to drastic changes in reward. Once again, for notational convenience, we let and denote the optimal objective values of the optimization problems () and (BP), respectively.

Proposition 4.13

If Assumption 4.2.4 holds, then .

Compared to the bound from Proposition 4.12, we observe that the bound from Proposition 4.13 is attractive when the robustness parameter is relatively small and when the number of simulated sample paths is relatively small compared to the number of periods . For example, we observe that will hold whenever the number of sample paths is subexponential in the number of periods .

In summary, Propositions 4.11, 4.12, and 4.13 establish under mild and verifiable conditions that the approximation gap between the proposed heuristic () and the robust optimization problem (RO) cannot be arbitrarily large and, in some cases, is guaranteed to be equal to zero. Ultimately, the practical value of the proposed heuristic () lies in its performance in the context of optimal stopping applications. In the following §5, we provide numerical evidence that () can indeed find high-quality stopping rules for realistic stochastic optimal stopping problems in practical computation times.

5 Numerical Experiments

In this section, we perform numerical experiments to compare our robust optimization approach and three state-of-the-art benchmarks from the literature (Longstaff and Schwartz 2001, Ciocan and Mišić 2020, Desai et al. 2012). The first two benchmarks serve as representatives of two classes of approximation methods for stochastic optimal stopping problems (approximate dynamic programming and parametric exercise policies) which, similarly as the robust optimization approach, only require the ability to simulate sample paths of the entire sequence of random states. The third benchmark is representative of state-of-the-art duality-based methods for stochastic optimal stopping problems. All experiments were conducted on a 2.6 GHz 6-Core Intel Core i7 processor with 16 GB of memory. All methods are implemented in the Julia programming language and solved using the JuMP library and Gurobi optimization software.

5.1 A Simple Non-Markovian Problem

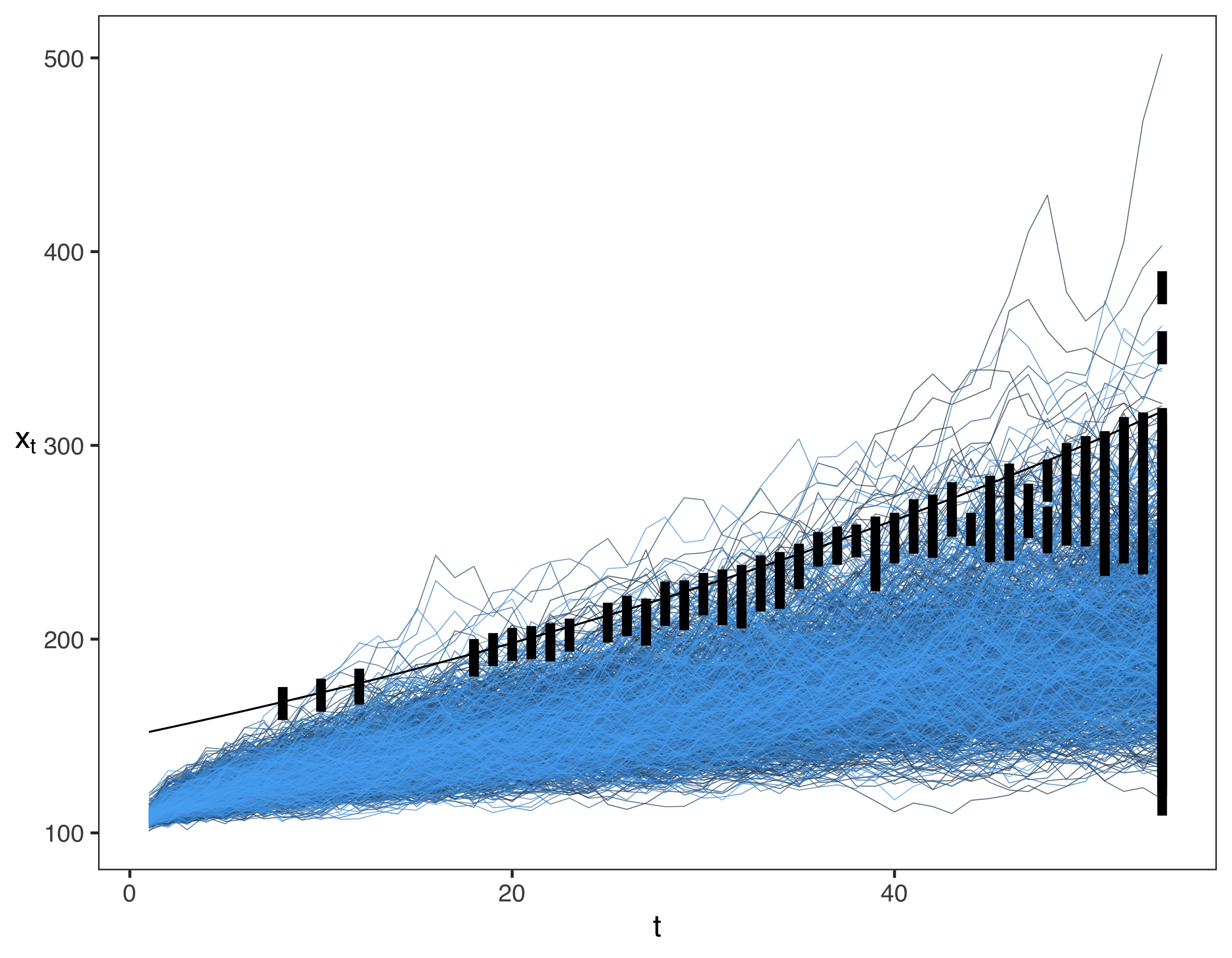

To demonstrate the value of our robust optimization approach, we begin by investigating a simple, one-dimensional stochastic optimal stopping problem with a non-Markovian probability distribution. The optimal stopping problem of consideration involves a state space which is equal to the real numbers () and a reward function of in each period . For any fixed duration , the joint probability distribution of the stochastic process is given by

where the random parameter is selected once per sample path and is unobserved. Simulated sample paths of this non-Markovian stochastic process are visualized in Figure LABEL:fig:nonmarkov_trajectories. We perform numerical experiments on the following methods:

-

•

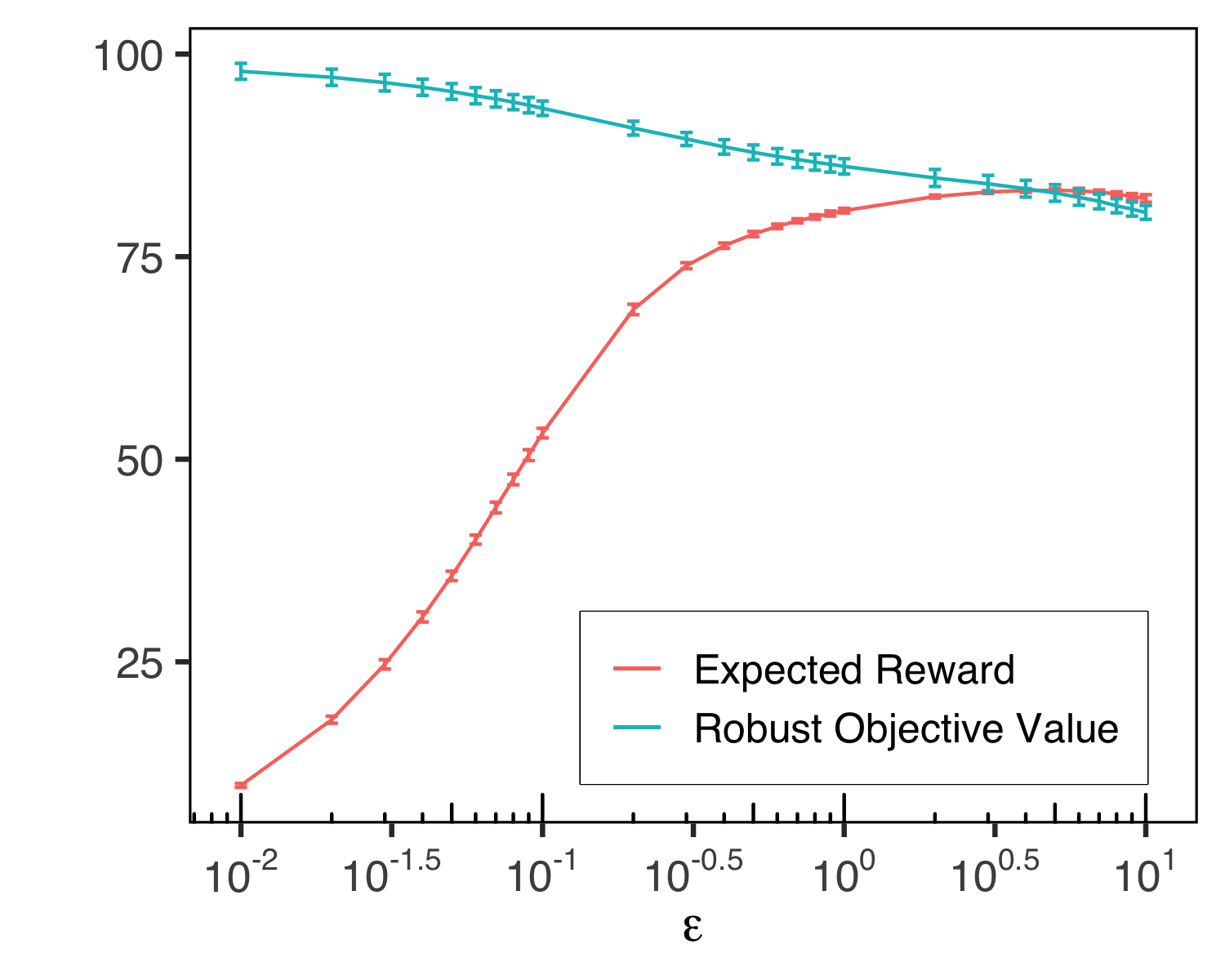

Robust Optimization (RO): The robust optimization approach is used here to approximate (OPT) over the non-Markovian stochastic process , and thus aims to find the best Markovian stopping rules for the stochastic optimal stopping problem. The method was run with robustness parameters for and otherwise, and the robust optimization problem is solved approximately using our proposed heuristic () from §4.2.3.

-

•

Least-Squares Regression (LS): We implement the method of Longstaff and Schwartz, which employs least-squares regression to approximate the continuation value function (i.e., the expected reward from not stopping) in each period using backwards recursion. To apply this method, we first transform each non-Markovian sample path into an augmented Markovian sample path of the form by adding the full history into the state in each period: . The regression step requires a specification of basis functions, and we consider the following categories of basis functions.

Full-History:

This category of basis functions uses the entire vector of states observed up to that point. The basis functions that we consider in this category are One (the constant function 1), Prices (the states observed up to that point, ), and Prices2 (the product of each pair of states observed up to that point, ).

Markovian: