The Effect of Network Topology on Credit Network Throughput

Abstract.

Credit networks rely on decentralized, pairwise trust relationships (channels) to exchange money or goods. Credit networks arise naturally in many financial systems, including the recent construct of payment channel networks in blockchain systems. An important performance metric for these networks is their transaction throughput. However, predicting the throughput of a credit network is nontrivial. Unlike traditional communication channels, credit channels can become imbalanced; they are unable to support more transactions in a given direction once the credit limit has been reached. This potential for imbalance creates a complex dependency between a network’s throughput and its topology, path choices, and the credit balances (state) on every channel. Even worse, certain combinations of these factors can lead the credit network to deadlocked states where no transactions can make progress. In this paper, we study the relationship between the throughput of a credit network and its topology and credit state. We show that the presence of deadlocks completely characterizes a network’s throughput sensitivity to different credit states. Although we show that identifying deadlocks in an arbitrary topology is NP-hard, we propose a peeling algorithm inspired by decoding algorithms for erasure codes that upper bounds the severity of the deadlock. We use the peeling algorithm as a tool to compare the performance of different topologies as well as to aid in the synthesis of topologies robust to deadlocks.

1. Introduction

The global economy relies on digital transactions between entities who do not trust one another. Today, such transactions are handled by intermediaries who extract fees (e.g., credit card providers). A natural question is how to build financial systems that limit the need for such middlemen.

Credit networks (similarly, debit networks) are systems in which parties can bootstrap pairwise, distributed trust relations to enable transactions between parties who do not trust each other. The core idea is that even if Alice does not trust Charlie directly, if they both share a pairwise trust relationship with Bob, then Alice and Charlie can execute a credit- (or debit-) based transaction through Bob. The trust relationships that comprise such a network can be based on prior experience or observations111One of the earliest examples is the hawala system (Maimbo et al., 2003), a credit network in existence since the 8th century, which relies on the past performance of a large network of money brokers. (e.g., credit scores in a credit network), or they can be based on escrowed funds that are managed either by a third party or an algorithm (debit networks). Recent debit/credit networks from the blockchain community establish pairwise trust relationships through cryptographically secured data structures stored on a blockchain. Prominent examples include payment channel networks (PCNs) (Poon and Dryja, 2016; rai, [n.d.]; Decker and Wattenhofer, 2015) such as the Lightning Network (Poon and Dryja, 2016) and the Ripple credit network (Moreno-Sanchez et al., 2018).

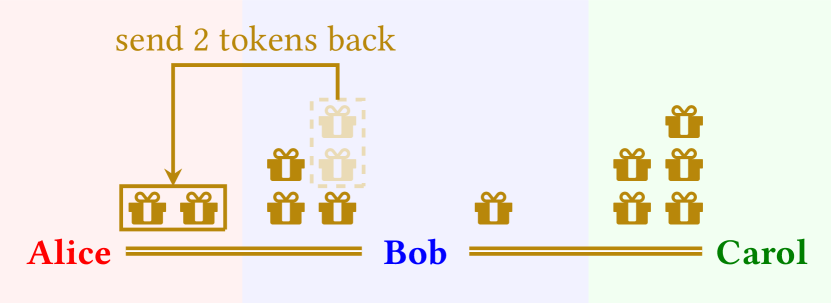

Fig. 1 depicts the operation of a pairwise trust channel (or a payment channel) in PCNs. If Alice and Bob want to establish a payment channel, they each cryptographically escrow some number of tokens into a contract that is stored on the blockchain and ensures the money can only be used to transact between them for a predefined time period. In Fig. 1(a), Alice commits 3 tokens and Bob commits 2 tokens to a payment channel for a week. While the channel is active, Alice and Bob can exchange funds between themselves without committing to the public ledger. However, once the active period expires (or once either of the participants choose to close the channel), Alice and Bob commit the final state of the channel back to the blockchain. The cryptographic construction of these channels ensures that neither Alice nor Bob can default on their obligation.

PCNs are a network of these pairwise payment channels; if Alice wants to transact with Carol, she can use Bob as a relay (Fig. 1(b)). We call (Alice, Carol) a demand pair, and the flow of money over route (Alice, Bob, Carol) a flow (defined more precisely in Section 3). No party incurs risk of nonpayment because PCNs are implemented as debit networks, with settlement processed on the public blockchain. PCNs are viewed as an important class of techniques for improving the scalability of legacy blockchains with slow consensus mechanisms (Torpey, 2016).

Like traditional communication networks, a central performance metric in credit and debit networks is throughput: the total number of transactions a credit network can process per unit time. However, reasoning about credit network throughput is more difficult than in traditional communication networks because of imbalanced channels. That is, because channels impose upper limits on credit (respectively debit) in either direction, transactions cannot flow indefinitely in one direction over a channel. For instance, in Fig. 1(c), once Alice sends 3 tokens to Bob, she cannot send any more tokens to Bob (or Carol). If Bob sends some money back to Alice, she would then again have credit to send new payments to Bob or route payments via Bob (Fig. 1(d)).

Imbalanced channels can affect the throughput of credit networks in unusual ways that depend on topology, user transaction patterns, and transaction routes. An imbalanced channel can harm throughput in other parts of the network due to dependencies between flows (e.g., an imbalanced channel blocks a flow, which prevents that flow from balancing other channels, blocking more flows and so on). Certain configurations of imbalanced channels can even lead to deadlocks where no transactions can flow over certain edges or even the whole network. Recovering from degraded throughput caused by imbalanced channels requires settlement mechanisms outside of the credit network, such as performing “on-chain” transactions on the blockchain to add funds to a channel. These mechanisms incur higher cost and overhead compared to transactions within the credit network and should be avoided.

In this work, we study the role of network topology and channel imbalance on the throughput of credit networks. While system designers cannot directly control the topology of a decentralized network, existing PCNs (e.g., Lightning Network) indirectly influence network topology, for example, with “autopilot” systems that recommend new channels to participants based on a peer’s channel degree, size, and longevity (ln-, [n.d.]b, [n.d.]a). These systems currently lack an understanding of how network topology and channel imbalance impacts the throughput in credit networks. Our goal is to bridge this gap, paving the way for future autopilot systems that encourage high-throughput topologies with minimal deadlocks. We make the following contributions:

-

(1)

We present a synchronous round-by-round model to study the throughput of a credit network for a given demand pattern, routing, and channel balance state. We use this model to formulate the best- and worst-case throughput of a credit network as a function of its starting channel balance state as optimization problems. The best-case throughput is easy to compute using a linear program, but determining the worst-case throughput is non-trivial and requires identifying the worst configuration of channel balances. Since transaction patterns and the likelihood of different balance states in credit networks are unknown, we instead study the worst-case throughput in an effort to bound the throughput achievable by a topology.

-

(2)

We introduce the notion of deadlocks — configurations of channel balances that irrevocably prevent transactions over a subset or all channels in the network. We show that deadlocks precisely capture scenarios in which a credit network’s throughput is sensitive to the channel balances, i.e., if a topology is deadlock-free, then its throughput does not depend on the initial state of the channels.

-

(3)

We show that the problem of determining whether a given network topology can be deadlocked given a fixed set of demand flows over the topology is NP-hard. Nevertheless, we propose a “peeling algorithm” inspired by decoding algorithms for erasure codes (Luby, 2002) that can be used to bound the number of deadlocked channels in the network. We show empirically that these bounds are very accurate for a variety of topologies, providing a computationally-efficient algorithm to estimate the worst-case throughput.

-

(4)

We compare standard random graph topologies and a subset of the actual Lightning Network topology in terms of best- and worst-case throughput for randomly-sampled transaction demands. We find that different topologies have different benefits. For example, scale-free graphs have fewer deadlocks and achieve better worst-case throughput than random regular and Erdos-Renyi graphs when the network contains fewer flows, but achieve lower throughput when the network is heavily utilized.

-

(5)

We take initial steps towards synthesizing deadlock-resilient topologies by exploiting the surprising connection with erasure codes. In particular, we build on prior approaches for designing efficient LT codes (Luby, 2002; Luby et al., 2001) to synthesize topologies with better robustness to deadlocks than existing topologies for a randomized transaction demand model.

2. Motivation

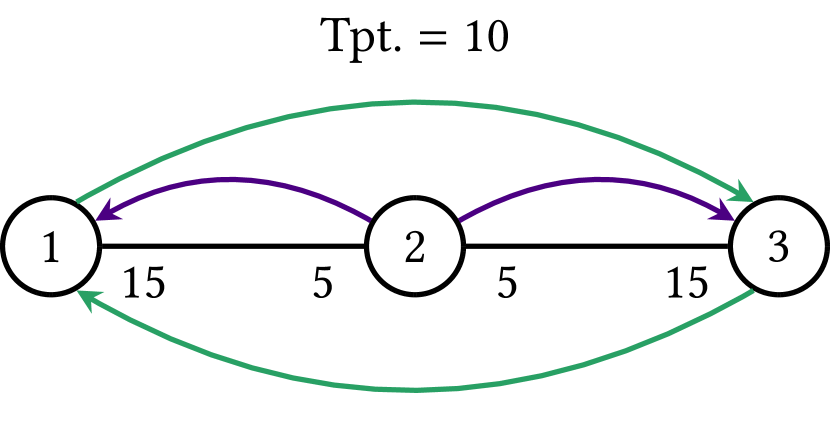

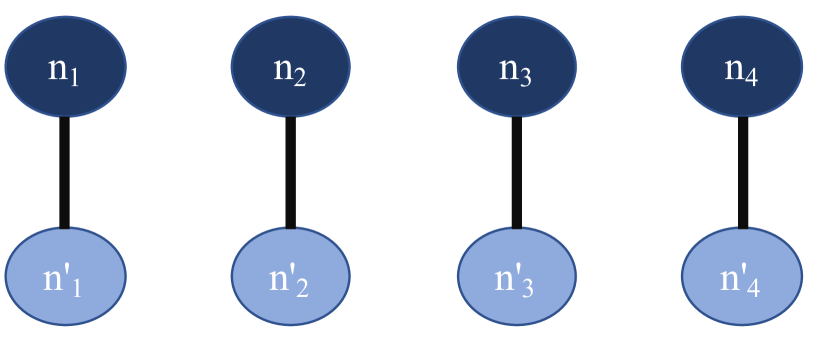

As a motivating example, consider the line topology in Fig. 2 where nodes and have balancing demands to each other, forming a circulation and node has one-directional (DAG) demands going out to and . In steady state, regardless of the balances of the two channels, we only expect the green flows to contribute to throughput because tokens moved by one green flow is restored by the other, permitting more transactions. In Fig. 2(a), both channels are perfectly balanced, and nodes and can send at most 10 tokens to each other without changing the balances on either channel. If we defined a throughput metric for the maximum transaction amount possible in a round when send as many tokens as available without changing channel balances at the end of the round, the throughput in the perfect balance state would be (each green flow moves tokens).

However, if the purple DAG flows were active for a short amount of time in Fig. 2(a), causing 5 tokens on each channel to move to nodes 1 and 3, we would end up in Fig. 2(b). Once in Fig. 2(b), no amount of future flows between the shown sender-receiver pairs can ever restore the credit network to state Fig. 2(a). In other words, Fig. 2(a) is not reachable from Fig. 2(b). In particular, node cannot send more than 5 tokens in a given round to node since it needs funds on the channel and vice-versa. Sending exactly 5 tokens in a round from each end (node 1 to node 3 and vice versa) leaves us back at Fig. 2(b) without any ability to get to Fig. 2(a). Consequently, the steady-state throughput in Fig. 2(b) is instead of in Fig. 2(a).

Worse still, once in Fig. 2(b), if the DAG flows are active for longer, causing the remaining 5 tokens on node on each channel to move outwards, we end up in Fig. 2(c). Notice that Fig. 2(c) is a deadlock; none of the four flows can make any progress. Consequently, there is no way to get out of Fig. 2(c) to any of the other balance states for the credit network. In other words, the steady-state throughput for Fig. 2(c) is , and the only state reachable from Fig. 2(c) is itself.

The implications of Fig. 2 are concerning: for the same amount of escrowed funds in every channel in a credit network, the throughput can vary depending on the starting state. In other words, the throughput of the credit network in Fig. 2 is sensitive to the balance state. When every channel is perfectly balanced, the transaction throughput is highest. If the network stayed in in such a state and only routed circulation flows, the throughput would remain high (Sivaraman et al., 2020). However, transient DAG flows can alter the credit network state in ways that it cannot recover from, permanently harming its throughput. Better routing or rate control cannot eliminate this problem. While a scheme like Spider (Sivaraman et al., 2020) may delay the onset of deadlocks by throttling flows experiencing congestion or more effective load-balancing across multiple paths, DAG demands like the purple flows in Fig. 2 would eventually move the topology to states with reduced or even zero throughput. We formalize the notions of throughput, balance states, and deadlocks in §3 and §4.

3. Model and Metrics

We model the credit network as a graph . The vertices of the graph denote the nodes, or users, of the credit network while the edges denote pairwise channels. Each channel is an undirected edge and is denoted by the pair of nodes constituting the edge. Physically, these channels represent a credit relation between the endpoints. Each channel is associated with two balances and that denote the maximum number of tokens that is willing to credit () and vice versa () in the channel. These can be thought of as escrowed funds that are allocated to each channel when it is established. Each channel has a capacity that denotes the total credit limit of the channel;222We use the notation to denote undirected edges, and to denote directed edges for nodes . that is, . We assume a static network, i.e., all channel capacities are fixed, and the channels remain open and funded with the same amount of tokens for the entire duration under consideration.

We capture the current state of the credit network using a balance vector , containing the balance information of all the channels. For every channel , the vector contains only one entry corresponding to the balance at either or ’s end in the channel as follows. Let be an ordering of the channels in , with the nodes within each channel also ordered such that for any channel . Similarly let be an ordering containing edges in a direction reverse to that in . Now, the -th entry of for contains the balance of the -th channel in . This allows us to visualize the entire network state space as an -dimensional polytope with each perpendicular axis representing balance on a distinct channel. Similar to the balance vector, let the vector contain the capacities of all the channels, with the -th entry of containing the total capacity of the -th channel in . These definitions allow us to represent the balances on the reverse edges or those channels in using the vector .

Definition 0.

(Boundary, Corner, and Interior Balance States.) A channel is imbalanced when all of its escrowed funds are on one end of the channel, i.e., either or . A balance state is located on the boundary of the polytope when one or more of the channels is imbalanced. A corner of the polytope is a point on the boundary where all channels are imbalanced in one of the two directions. In contrast, if none of the balances on either end of any of the channels is 0, such a balance state is an interior balance state. The set of all interior balance states is denoted by . Similarly, denotes the set of all boundary balance states, while denotes the set of all corner states.

Transactions attempted in the credit network follow a demand pattern captured through a binary matrix where if sender wants to transact with receiver . Such a sender-receiver pair can use one or more paths to transact. Let denote an ordering of all paths (across all sender-receiver pairs with demand) in the network through which tokens can be routed.

We assume that transactions in the credit network occur synchronously over rounds or epochs; every transaction starts and completes within the same round. We further assume that a transacting sender-receiver pair has unbounded demand; tokens can always flow from a sender to a receiver if feasible. We also assume that tokens are infinitely divisible. Suppose is the balance state of the credit network at the beginning of a round. Let denote a flow vector, with the -th entry of being the number of tokens sent along path during the round. For the flow vector to be feasible, we require the total number of tokens sent on any channel from towards to not exceed , since only tokens are available for use along channel (in to direction) during the round. To define feasibility of a flow precisely, let routing matrix be such that if the directed edge is part of path and otherwise. The -th column () of corresponds to the -th path while the -th row () corresponds to the -th directed edge in . We similarly define routing matrix over the directed edges in . These routing matrices essentially capture which edges are involved in which paths. With this notation, for a flow to be feasible we must have

| (1) |

When such a feasible flow is sent, at the end of the round a node ’s balance in channel is decremented by the total amount of tokens sent from towards and incremented by the tokens sent from towards during the round. To compute this balance change, we define as . For an edge and path , we have

| (2) |

Letting be the balance state of the network at the end of the round, we then have

| (3) |

Tab. 1 summarizes the notation and provides an example for the credit network state described in Fig. 2(b). The flow sends tokens from node to , and tokens from node to , transferring all of the available tokens on the channel. Sending such a feasible flow results in the new balance state with no remaining tokens at ’s end of the channel.

This process of token transfer allows us to define a set of reachable states from a starting state . We say a state is reachable from in rounds if there exists a sequence of flows for such that

| (4) | ||||

| (5) | ||||

| (6) | ||||

| (7) |

with and . A sequence of flows , that satisfies equations (4)–(7) for a given initial state is called a feasible flow sequence for initial state .

Definition 0.

(Set of reachable states.) For a credit network with capacity and initial balance state , the set of states reachable from is given by

| (8) |

We say a flow is achievable from state if there exists a feasible flow sequence from such that .

Definition 0.

(Set of achievable flows.) The set of flows achievable from state is given by

| (9) |

3.1. Metrics: Best- and Worst-Case Throughput

We measure the performance of a credit network by its throughput. However, the throughput of a credit network depends on many factors, including the demand imposed by users. Prior work (Sivaraman et al., 2020) has shown that a demand matrix can be separated into circulation and directed acyclic graph (DAG) components.333The demand matrix considered in prior work (Sivaraman et al., 2020) is real-valued with the entries denoting how much demand sender-receiver pairs have. In contrast, the demand matrix we consider is binary-valued (§3) denoting only the presence or absence of demand between sender-receiver pairs. Nevertheless, the concept of decomposing a demand matrix into circulation and DAG components is general and applicable to our model also. The circulation represents the portion of the demand that can be routed in a balanced manner and sustained in the long term. The circulation can be extracted from the demand matrix by computing the largest union of all cyclic demand pairs ( has demand to , has demand to , who has demand back to ). The remaining demand pairs form the DAG component. With a circulation demand, transactions can be routed such that every token sent on channel from to is compensated by another token from to , thus maintaining channel balance. This allows a circulation demand to be sustained indefinitely. In contrast, a DAG demand sends one-way traffic on some channels, eventually leaving them imbalanced and unable to sustain more transactions in the same direction. Thus, the DAG portion of the demand cannot be sustained long-term without rebalancing. Rebalancing is a technique to arbitrarily modify the balance of a channel using a mechanism external to the credit network itself (e.g., “on-chain” transactions on a blockchain). Rebalancing usually comes at a substantial cost (high transaction fees, confirmation delay) and should be avoided to the extent possible.

![[Uncaptioned image]](/html/2103.03288/assets/x9.png)

| Symbol | Meaning | Example |

| Initial balance state | ||

| Capacities | ||

| Set of paths | ||

| Fwd. routing matrix | ||

| Bwd. routing matrix | ||

| Feasible flow | ||

| Balance state after sending | ||

| One-step tpt. | 10 | |

| Steady-state tpt. | 10 | |

| Max. tpt. | 20 | |

| Min. tpt. | 0 |

Our goal is to study the throughput of a credit network in the absence of external rebalancing. Consequently our throughput metrics automatically attribute throughput only to the circulations (the long-term throughput of DAG demands is zero without rebalancing). However, we emphasize that our model is general and supports DAG demands. In particular, transient DAG demands transition the credit network to different states, possibly changing its long-term (circulation) throughput. In fact, even circulation demands can appear “DAG-like” over short time scales. We study the impact of such state transitions on the long-term throughput of the credit network.

We define the one-step throughput of a state to be the maximum flow that is feasible to send within an epoch starting from , while ensuring that the balances of all channels remain unchanged after the epoch. Since the balance state does not change, can be achieved in every epoch by repeating the same set of flows.

Definition 0.

(One-step throughput.) The one-step throughput at state is defined as

| (10) |

The one-step throughput is maximized when the channel capacity is equally divided between constituent nodes for all channels, i.e., .

We are interested in the maximum steady-state throughput of the network starting from a state . This depends not only on but also on the states reachable from . In particular, a credit network starting from state can undergo a series of state transitions facilitated by flows present in the demand to reach a state with higher . It can then achieve throughput in every subsequent epoch. This motivates the following definition.

Definition 0.

(Steady-state throughput.) The steady-state throughput of a state is defined as

| (11) |

In Fig. 2(b), the balance on the middle node cannot be increased unilaterally because the green flows that contribute to steady-state throughput are tied to each other. As a result, the maximum throughput is constrained by the available tokens on each side of node . This means that because no state with higher throughput is reachable from (Tab. 1) 444By Definition 10, is the optimal value of a linear programming problem with a compact feasible set. Because the feasible set is related to in a continuous way, the resulting is always a continuous function. In contrast, is typically discontinuous, because the sets of reachable states and may differ drastically from each other, even if and are arbitrarily close (particularly in the neighborhood of the boundaries of ). Since we haven’t established the closedness of the set of reachable states , we use a supremum definition of steady-state throughput instead of a maximum..

Without loss of generality, we use throughput of a state to refer to the steady-state throughput of a state in the rest of this paper. Note that the maximum throughput across all states is also attained at : .

To account for the sensitivity of a credit network’s throughput to the balance state, we propose analyzing the lowest throughput it would yield across all possible balance states . We call this lowest throughput value worst-case throughput and denote it by . Unlike average-case analysis, considering the worst case lets us compare the resilience of different topologies without making assumptions about the distribution of balance states. Since channel balances are private information, little is known about the balance states observed in credit networks in practice.

Definition 0.

(Worst-case Throughput) The worst-case throughput of a credit network with capacity and a balance space are defined as

| (12) |

4. Throughput Sensitivity and Deadlocks

Best- and worst-case throughput depend on the transaction demand pattern. But since the transaction patterns are unknown a priori, our goal is to design credit network topologies such that is close to for most or all transaction patterns. It is important to ensure that such a design does not compromise on throughput. In other words, it is not desirable to have in exchange for a very low relative to the escrowed collateral.

Verifying conditions in which is difficult, because although we know that is attained at , it is unclear a priori which states achieve . In this section, we show that if a topology does not admit deadlocks, then it is always the case that . We call such a topology insensitive to the starting balance.

A channel is said to be deadlocked at a particular state if no feasible flow can alter its balance in either direction.555Notice a subtle difference between our definition of deadlocks and that in (Malavolta et al., 2017b; Werman and Zohar, 2018). They define a deadlock as a set of flows that starts executing during a round, but cannot complete because (a) different flows utilize the same channels, and (b) a poorly-chosen processing ordering for the path edges for different flows blocks all flows from making progress. Our model does not capture such deadlocks because we assume flows complete instantaneously within a round. The collection of all such channels forms the deadlocked channel set for a state . A state represents a deadlock if .

Definition 0.

(Deadlocked Channel Set) Let denote the set of deadlocked channels under balance state . Formally,

where denotes the entry corresponding to channel in the vector .

Since no feasible flow at can alter the balance values of the deadlocked channels , all such channels have the same balance values across all reachable states from . Formally, if and is a state reachable from , then we must have , where and denote the balances of channel in vectors and respectively. This effectively means that the deadlocked channels cannot sustain any flow and thus, make no contributions towards throughput. In other words, for all if there exists an such that or . We formally state and prove these properties in App. A.2.

It is straightforward to verify that for every interior point , there exists such that tokens can be transmitted over some flow in the network. Hence, for any state , ; in other words, deadlocks can only happen at the boundary points of . At every boundary point, a nonempty subset of channels is imbalanced in one of the two directions, so flows using those channels in the imbalanced direction(s) are blocked.

However, merely having imbalanced channels at a boundary point of polytope does not imply the existence of deadlocks at that point. Consider the two corner balance states and shown in Fig. 2(c) and Fig. 2(d) respectively. is a deadlock in that none of the four flows can make any progress, no other state in is reachable from , and . In contrast, is a good boundary point that can achieve the best-case throughput . For example, node can send tokens to node in one round, node can then send the tokens back to node 3 in the next round, and so on. The credit network returns to every two rounds, achieving a throughput of 20 tokens per round. Further, at , sending tokens from node to would return the credit network to the perfectly balanced state ; thus . Effectively, the credit network can escape boundary to reach any state in .

It turns out that to assess a topology’s sensitivity to the starting balance state, it is enough to check if its boundary points can be deadlocked. Intuitively, if there are no deadlocks then every boundary point, and in particular every corner point of the polytope, can be made balanced by moving into an interior point. Since the set of directions along which the corner points can transition to interior points spans the entire state space, this implies one can move in every direction in the polytope. As a result, the credit network must be able to transition from any balance state to any other balance state without being stuck. Such a credit network can always reach its throughput-maximizing state from any other state. In other words, the throughput of such a topology should be insensitive to the starting balance state. In contrast, if a credit network has deadlocks, the largest deadlock (i.e., the deadlock involving the most channels) should lead to the maximum unused collateral and such states would have the lowest throughput. Therefore, the maximum throughput that can be extracted using only the remaining channels in the largest deadlock state constitutes the worst-case throughput of a credit network. The rest of this section formally describes these two results.

Theorem 1.

(Insensitive Throughput) If a credit network with balance state space is deadlock-free, i.e., for any boundary state , there exists an interior point such that , then for any state , .

Proof Sketch (Full proof in App. A.3).

We introduce the notion of feasible directions from a balance state. A unit vector is a feasible direction from if there exists such that . We list some useful properties about feasible directions below, and provide proofs in App. A.2.

Let be an arbitrary interior state. By assumption, every corner state has a corresponding reachable interior state. The transition from a given corner state to its reachable interior state produces a set of feasible directions which is located in an open orthant of the space. Further, the feasible direction corresponding to a particular corner occupies a distinct orthant that is not shared by the feasible directions from any other corner state.

By property 3, the feasible directions of every corner are included in the

the feasible directions of .

By property 1, the set of ’s feasible directions contains the convex hull of all of

these sets of directions, which maps exactly to the full space .

Furthermore, by property 2, any other interior state is reachable from , including the center state . For simplicity, we skip the extension to boundary states and refer it to App. A.3.

Since globally maximizes the one-step throughput , we have for any , .

While a credit network might not be entirely deadlock-free, Theorem 1 can also be applied to any sub-network of the original credit network that does not have deadlocks. A sub-network is embedded within a subgraph of the original topology and only permits paths whose edges are entirely within the subgraph. If this sub-network is deadlock-free, then it enjoys throughput insensitivity within the balance states of the sub-network. In addition, its throughput lower bounds the maximum throughput achievable from an arbitrary initial state in the original credit network.

At the same time, every credit network with deadlocks has a set of balance states that maximizes the number of deadlocked channels. For any , the set of channels deadlocked equals a fixed set that contains all other sets of deadlocked channels across every balance state . The channels outside form a deadlock-free sub-network. The throughput of the original credit network is at least the throughput achievable on this sub-network, regardless of the initial balance state of the original network. We state this formally in Theorem. 2 and prove it in App. A.4.

Theorem 2.

A state has the worst throughput , if the number of deadlocked channels in is the largest across all states, i.e., . Furthermore, the throughput of a worst throughput state can be computed by considering a state where

Then, .

5. Designing Deadlock-free topologies

§4 suggests that to fully utilize the collateral in a credit network, the credit network needs to be deadlock-free. In this section, we first show that determining whether an arbitrary topology is deadlock-free is NP-hard (§5.1). Next, we propose and analyze a “peeling algorithm” that bounds the number of deadlock-free edges in a credit network (§5.2). The peeling algorithm provides a computationally-efficient way to estimate , and reveals a surprising connection between designing deadlock-free topologies and LT Codes (Luby, 2002; Popovski et al., 2012), a well-known class of erasure codes.

5.1. Deadlock Detection Problem

Detecting a deadlock on a credit network is equivalent to finding a balance configuration such that one or more channels is imbalanced and one or more of the imbalanced channels is deadlocked. A full deadlock involves all edges of the credit network while a partial deadlock can involve any non-empty proper subset of credit network edges.

Definition 0.

(Full and Partial Deadlock) A balance state is a full deadlock on the credit network if and a partial deadlock if

Theorem 3.

(Hardness Result) Given a credit network with channel capacity for each , demand matrix and set of paths for satisfying the demand, finding a balance state such that is NP-hard.

Proof Sketch (Full proof in App. A.5)

When a channel is imbalanced with , the channel cannot support flow in the direction unless the balance state is altered. As a result, all flows using from to are blocked. If all flows using a channel in both directions are blocked, then the channel is deadlocked. We use this intuition to present a reduction from the Boolean Satisfiability Problem (SAT) to the full deadlock-detection problem for credit networks. We consider a boolean expression in Conjunctive Normal Form (CNF) and construct a credit network such that, each variable is mapped to a unique channel and each clause is mapped to a unique path in the constructed network. The truth value of a literal is associated with whether or not the balance at a particular end of a channel is zero, while the truth value of a clause relates to whether or not a particular path is blocked by some channel. The boolean expression is therefore satisfiable if and only if there exists a full deadlock in the credit network, proving the -hardness claim.

Note that a straightforward mapping of variables to channels, and clauses to paths results in a disconnected network with invalid paths. To make our constructing valid, we introduce a polynomial number of auxiliary variables (and accompanying clauses), in a way that preserves the connection between the satisfiability of the initial CNF and the existence of deadlocks in the constructed network. We defer more details about our reduction technique to App. A.5. Our reduction can be easily extended to establish that detecting a partial deadlock is also -hard.

5.2. Peeling Algorithm

Although it is NP-hard to check if a topology is deadlock-free, it is possible to identify subsets of edges that are provably deadlock-free in polynomial time. We design such an algorithm inspired by the peeling algorithm used to decode LT codes (Luby, 2002). The key insight of our peeling algorithm is the following: if an edge has a dedicated flow in either direction, tokens can move freely in the direction of the flow, as long as there are tokens available at the origin end. We call such flows “length 1” flows, since they traverse a single edge. If an edge has two such flows in both directions, it can never be deadlocked. The peeling algorithms progressively finds edges with length 1 flows (which cannot be deadlocked), and eliminates them as potential bottlenecks for all flows that traverse them; this can be viewed as “peeling” these edges from these flows. Once it is established that none of the edges in a flow can be deadlocked, the flow can be removed from consideration. This process continues until all edges in the topology can move in either direction, or none of remaining flows traverses edges that can be peeled, causing the process to terminate unsuccessfully. We describe the terminology borrowed from LT Codes in §5.2.1 and define the deadlock peeling algorithm in §5.2.2.

5.2.1. LT Process

LT codes are a rateless code, designed for channel coding under changing or unknown channel conditions (Luby, 2002). LT codes map a sequence of input bits to a sequence of encoded bits . Each encoded bit is the XOR of a subset of input bits: , where set indexes a subset of input symbols, chosen at random. The LT encoding procedure can be represented as a bipartite graph, where each input symbol , corresponds to a node on the right, and each encoded symbol , to a node on the left. An edge exists between input node and encoded node iff . The degree of an encoded node denotes the number of XORed input symbols, .

Decoding the encoded symbols proceeds iteratively. A degree 1 encoded symbol can be immediately decoded to identify the associated input symbol since the encoded symbol’s value matches the input symbol. Such a degree 1 encoded symbol is released to cover or decode its associated input symbol. The input symbol is then added (if not already present) to the ripple , a set of covered input symbols that are yet to be processed. At every time step, an (unprocessed) input symbol is chosen at random from the ripple and processed: its value is XORed with every encoded symbol that it is a neighbor of (i.e., for which ). This reduces the degree of every such encoded symbol, subsequently releasing more encoded symbols that become degree 1. However, the newly covered neighbors of degree 1 flows increase the size of the ripple only if they were previously uncovered. This routine (LT process) of releasing encoded symbols, covering input symbols and adding them to the ripple, and processing input symbols from the ripple, continues until either the ripple runs empty or all input symbols are successfully decoded.

Since encoded symbols incur communication overhead, it is desirable to minimize their quantity. A key factor affecting the number of encoded symbols is the choice of the degree distribution for the encoded symbols. However, if minimizing the number of encoded symbols leads to a ripple that vanishes before the algorithm terminates, the decoding process fails altogether. Prior work (Luby, 2002; Popovski et al., 2012) has focused extensively on the design of degree distributions that achieve a ripple size that is neither redundant nor so small that the ripple disappears before the LT process completes. For example, under a robust soliton distribution (Luby, 2002), LT codes recover input symbols with probability at least from encoded symbols.

5.2.2. Deadlock Peeling

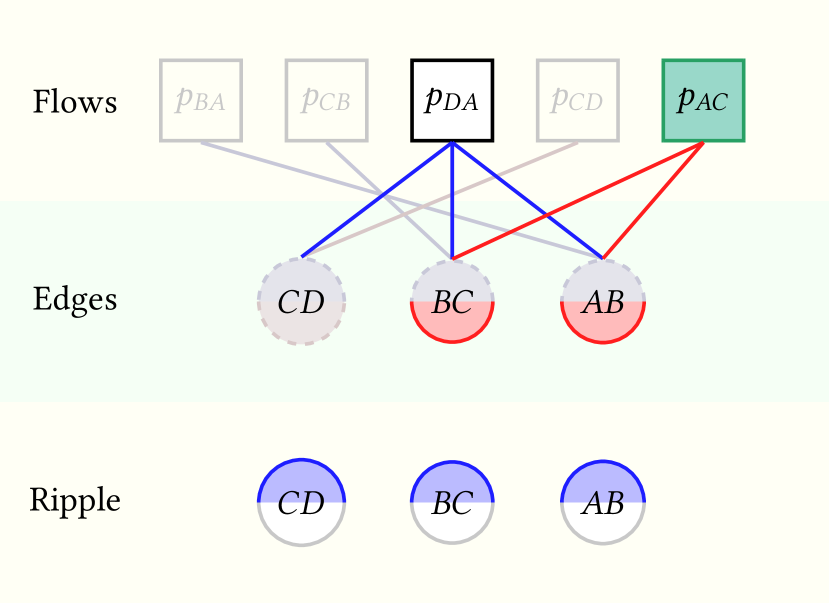

The idea of peeling in LT codes can be extended to detecting deadlocks with a few modifications. Here, channels correspond to input symbols. A channel can be used (and covered) in one of two directions. We will consider the two directions blue and red with the red direction corresponding to usage of the edges in the same direction as and blue denoting the directions specified by . A flow (an encoded symbol) uses one or more channels (input symbols), each in one of the two directions; the degree of the flow is the path length, or the number of channels used by the flow. The deadlock peeling process can be represented as a bipartite graph, where each flow , corresponds to a node in the top partition, and each channel , to a node in the bottom partition. An edge exists between channel and flow iff either or is part of ; the edge is red if and blue if . Figures 4 and 4 show the the bipartite graph construction for their associated credit network topologies and paths.

Fig. 5 shows the deadlock peeling process for the example credit network in Fig. 4. A flow of degree 1 can be released to cover and add to the ripple its last channel in the direction opposite to the direction in use. In other words, a flow of degree 1 using the edge in the blue direction , can be released to cover in the red direction . Newly covered channels are added to the ripple . Covering in the direction signifies that the channel can always support flows in the direction because flow would restore tokens back to the end regardless of ’s current balance state. Fig. 5(a) shows the impact of releasing the initial degree flows. At every subsequent time step, a randomly chosen channel (and its associated color) is processed from the ripple. Processing a channel is similar to the LT process; the degree of every flow that uses the channel in the processed color is reduced by 1. This may lead to new flows being released to cover more channels (Fig. 5(b)). However, only the previously uncovered channels increase the ripple size (e.g. blue in Fig. 5(c)). This peeling process continues as long as the ripple is non-empty and at least one remaining flow is of degree 1. As is the case with the LT process, to establish that the entire topology is deadlock free, the ripple should not vanish before the entire peeling process is complete. Consequently, prior analyses (Luby, 2002; Popovski et al., 2012) that design good degree distributions become relevant for the deadlock peeling process also.

The deadlock peeling process differs from the LT process in one key aspect. Unlike the LT process, flows of degree cannot be removed immediately from the bipartite graph. A flow is removed only after it reaches degree when every channel that it uses is covered in the color opposite to the direction of use. The intuition behind this is that a flow of degree is unconstrained and can move tokens on all the channels it uses (restoring balance if the opposite direction was imbalanced). Note the important distinction here that a flow of degree covers (or frees) only the last remaining channel in the opposite direction while a flow of degree covers all of its channels in the opposite direction (Figures 5(c), 5(d), 5(e)). Algorithm 1 in App. B.2 summarizes the deadlock peeling process.

The deadlock peeling process cannot always detect all deadlock-free edges: the number of edges it successfully peels is a lower bound on the actual number of deadlock-free edges in a topology. This is because it identifies patterns of bidirectional dedicated flows on the channels in a topology. Such flows, while guaranteed to render the associated channels deadlock-free, are not required for deadlock-freeness. For example, the topology in Fig. 4 is deadlock-free but it has no length 1 flows. Hence, the peeling algorithm terminates on this topology without peeling any channels.

Empirical evaluation of the deadlock peeling process. While we know that the deadlock peeling process is a lower-bound on the true number of deadlock-free edges in a topology (and consequently its associated ), it is useful to know how good of a lower-bound it is. Since the deadlock detection problem is NP-hard, we formulate an Integer Linear Program (ILP) to identify the largest deadlock on a given topology. We describe the ILP in App. B and compare it to the output of the deadlock peeling process. Since the ILP is slow, we evaluate it on small samples of four different topologies (described in §6.1) consisting of only nodes.

In Fig. 6, the number of channels unpeeled (line) matches the maximum deadlock reported by the ILP (points on the same lines) in all cases, suggesting that the deadlock peeling process provides not just a lower-bound, but rather an accurate approximation. Hence, in our evaluation (§6.2), we use the deadlock peeling process to peel as many channels as it can and compute the worst-case throughput as the one-step throughput of the sub-network consisting of all the peeled edges.

6. Evaluation

We empirically evaluate a number of standard topologies for their throughput and deadlock characteristics to understand their performance. We describe our evaluation setup in §6.1, define metrics in §6.2, and compare existing topologies in §6.3. We use the peeling algorithm to understand the behavior of different topologies and propose a preliminary synthesis approach in §6.4.

6.1. Setup

Baseline Topologies. We compare the performance of credit networks based on random graphs and a graph based on the Lightning Network for their throughput and deadlock behaviors. We use five random graph types: a Watts Strogatz small-world graph (sma, [n.d.]) with 10% rewiring probability, a Barabási-Albert scale-free graph (sca, [n.d.]), a power-law graph whose degree distribution follows a power-law, an Erdős-Rényi graph (er, [n.d.]), and a random regular graph.

We sample 5 different random graphs with 500 nodes and about 2000 edges for each graph type. To simulate a topology with properties similar to the Lightning Network, a PCN currently in use, we retrieved a snapshot of the topology on Oct. 5, 2020 using a c-lightning (c-l, [n.d.]) node running on the Bitcoin Mainnet. The original full topology has over 5000 nodes and 29000 edges. Similar to prior work (Sivaraman et al., 2020), we snowball sample (Hu and Lau, 2013) the full topology to generate a PCN with 452 nodes and 2051 edges. We also evaluate stars with 500 nodes as an example of a topology with good throughput and deadlock properties at the cost of being highly centralized. The throughput of all credit networks is normalized to a constant collateral distributed equally amongst all their channels.

Demand Matrix and Path Choice. We generate demand matrices by sampling a fixed number of unique source-destination pairs from the set of nodes in the graph. The results in this section use demand pairs sampled uniformly at random, but we include results with demand pairs sampled with a skew towards “heavy-hitting” nodes in App. B.3. Every non-zero entry in the demand matrix adds one sender-receiver pair and allows the shortest path between them to move tokens in the credit network across rounds 666Our throughput metrics only depend on the total number of permissible paths. Adding more edge-disjoint paths for a given demand pair and sampling more demand pairs both increase the total paths; we use the latter approach in our evaluations.. We refer to such a path as a flow in this section since it maps to a single flow node in the bipartite graph associated with the peeling algorithm. Unlike prior work (Sivaraman et al., 2020), we do not explicitly control for a circulation demand since we are interested in the effect of DAG demands on circulation throughput. As the demand matrix becomes more dense, the amount of circulation demand naturally grows. Unless otherwise mentioned, we sample 4 different demand matrices per random instance of the random graphs, to generate 20 unique points over which we average the throughput and deadlock behavior. Since there is only one instance of the star, Lightning Network and our synthesized topology, we use 20 different demand matrices instead. We only present results for demand density ranges that shows variation between the topologies. If the demand matrix is too sparse, there is not enough demand for any topology to perform well; if it is too dense, just routing one-hop demands (between end-points of every edge in the network) uses all the available collateral in the credit network ().

6.2. Metrics

Maximum Throughput. We first compute the maximum per-epoch throughput that a topology achieves when none of its channels are imbalanced or constrained. Recall that the throughput of a credit network is maximized at its perfect balance state . Further, . We use an LP solver to compute based on the constrained optimization problem in Eq. 10.

Worst-case Throughput. The worst-case throughput of a credit network is the minimum steady-state throughput achievable in an epoch from any state in its balance polytope 777Our definitions of and assume the ability to send the maximum feasible amount between a sender-receiver pair using an ideal routing algorithm. This allows us to reason about throughput without concerning ourselves with the precise dynamics of any routing algorithm such as transaction sizes or splitting.. We know from Theorem. 2 that is achieved at the state with the largest deadlock . Though detecting deadlocked states on an arbitrary topology is NP-hard, we use our approximate deadlock peeling process (§5.2) to identify the deadlock-free channels and compute the worst-case throughput as where if is reported as a deadlock-free channel, and otherwise.

Fraction of Channels Unpeeled. In addition to the above throughput metrics, we also report the fraction of the channels in the topology that the deadlock peeling process fails to peel. This acts as an upper-bound for the true number of deadlocked channels in a given topology.

6.3. Performance of Random Topologies

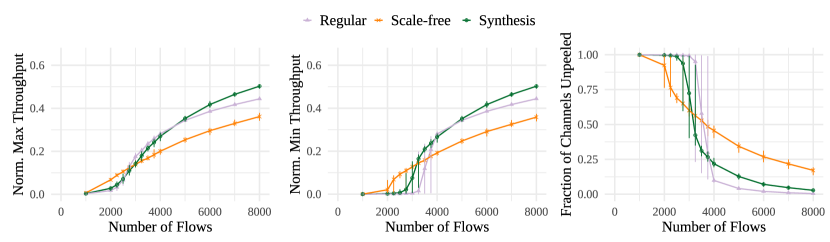

Fig. 7 shows the best-case throughput and the worst-case throughput achievable across all starting balance states for a set of random topologies with 500 nodes and an LN topology with 452 nodes for a fixed collateral budget for 2500–25000 demand pairs sampled uniformly at random. Stars outperform all the other topologies by over 50% even at the midpoint of the range. However, stars are highly centralized topologies (i.e., the hub has degree ); consequently, they are undesirable for decentralized use cases of credit networks. The value is comparable across most topologies; the small-world topology alone stands as an outlier because it has 50% longer paths than other topologies which results in lower throughput.

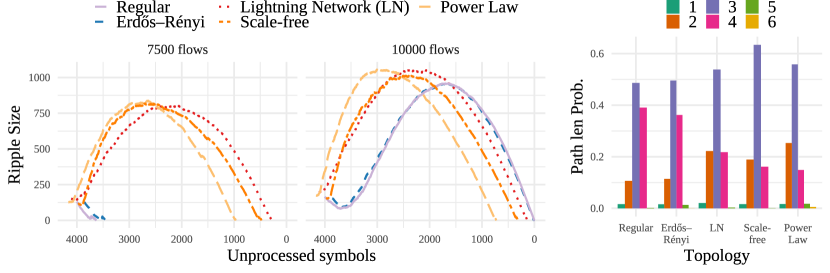

Fig. 7 also shows the variation in the values and the fraction of unpeeled channels across topologies. For instance, we notice that the Lightning Network, power-law and scale-free topologies have much better with fewer flows when compared to the other random graphs suggesting that they exhibit less throughput sensitivity to the channel balance state. At 7500 demand pairs, both Lightning Network and scale-free topologies peel 20-70% more channels than the small-world, Erdős-Rényi, and random regular topologies and correspondingly have 7-9x higher . However, the hardship that the scale-free graph faces in peeling the last 10% of its channels manifests as a 12% hit to its when compared to the Lightning Network, particularly with a denser demand matrix. This effect is even more pronounced in the power-law graph. In contrast, the Erdős-Rényi and random regular topologies do not peel as well with fewer flows, but quickly improve to peel all channels, on average, with 12500 demands. Beyond this point, their is comparable with the Lightning Network. The small-world topology peels only 50% of the flows even with 12500 demands which when compounded with its long paths leads to very low over the entire range. Fig. 13 in App. B.3 shows similar trends across topologies even when demand matrices are skewed in that some “heavy-hitter” nodes are more likely to both send and receive transactions.

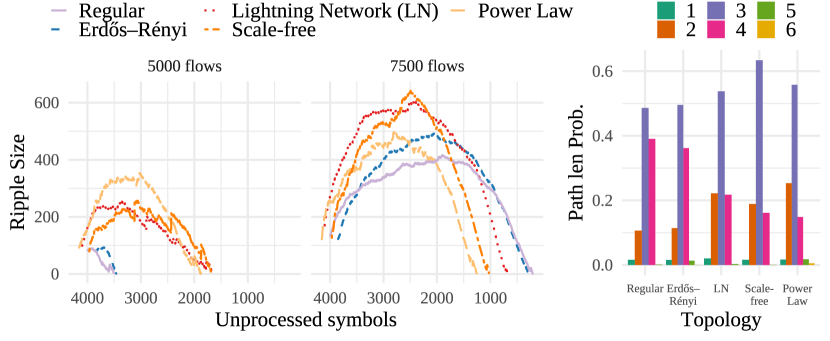

Explaining the relative behavior of topologies. Given the apparent correlation between and the fraction of channels peeled, we now consider the effect of topology on the evolution of the deadlock peeling process. Fig. 8 shows the evolution of the ripple size at 7500 and 10000 demand pairs, along with the path length distributions for the random regular, Erdős-Rényi, Lightning Network, power-law and scale-free topologies. We consider the total number of symbols at the start to be twice the number of channels in the topology, one for each direction of a channel. Each peeling step involves processing one channel in one of the two directions. A processed symbol may lead to the release of some flow nodes and consequently, add more directed channels to the ripple.

In Fig. 8, all topologies start with similar initial ripple sizes because they have the same sparsity. In other words, a randomly sampled demand is equally likely to be of length 1 (span only one edge) across all topologies. However, their ripple evolution patterns quickly diverge. The Lightning Network, power-law and scale-free topologies experience fast initial ripple growth, attributed to the 20% degree 2 flows (with path length 2) and up to 60% flows of degree 3. These short flows are likely to be released early, helping the deadlock peeling process pick up a robust ripple size. In contrast, at 7500 demands, the ripple vanishes quickly for the random regular and Erdős-Rényi topologies due to 10% fewer degree flows. Yet, the ripples in Lightning Network, power-law and scale-free topologies vanish before the entire topology is peeled, with 250 and 500 directed channels respectively unpeeled. This behavior happens with 10000 demands too, albeit to a lesser extent. However, at 10000 flows, Erdős-Rényi and random regular topologies offset the initial dip in the ripple size compared to the remaining topologies; they experience later peaks, but peel the entire topology. The poor tail behavior of the scale-free topology can be attributed to its 6% less channel coverage for the same number of demand pairs: the presence of hubs means edges far away from the hub tend to be less used. Such channels are difficult to peel without a large increase in the number of flows that ensures the relevant edges see enough token movement. A similar analysis of the ripple evolution for flows sampled in a skewed manner is shown in Fig. 14 in App. B.3.

Predicting Performance using LT Codes. Since the deadlock peeling process was inspired by the design on LT Codes, we evaluate whether the analysis of LT Codes predicts the performance of the deadlock peeling process. We use the same 5 random graphs from Fig. 8 at 7500 flows and view their predicted ripple evolution in an LT code with the same degree distribution. The predicted ripple evolution computes the probability that a flow of degree is released and adds a symbol to the ripple when there are unprocessed symbols remaining. Extending this to the expected ripple addition at every step helps build a ripple evolution curve prediction (Eq. 6 of (Popovski et al., 2012)) 888The trajectories use a slightly different expression (Eq. 21) for the expected symbols added that accounts for overlaps between symbols covered by the release of different flows at the same step..

We notice in Fig. 9 that the prediction for the Lightning Network, power-law and scale-free topologies are closer to each other but different from the Erdős-Rényi and random regular graphs. Like the real ripple evolution (Fig. 8), the initial growth rate for the Lightning Network, power-law and scale-free topologies is faster than the other two graphs. Interestingly, the prediction suggests that Erdős-Rényi and random regular topologies will have difficulty peeling at 7500 flows: the predicted ripple sizes approach with around 3000 unprocessed symbols remaining. Such a ripple evolution is not robust to the variance encountered during a typical peeling process as we observe in Fig. 8 where the ripple decreases drastically early on and vanishes. The prediction is more optimistic than the real evolution: the peak ripple sizes are higher and all topologies peel all their edges. In reality, the deadlock peeling process does not peel all the edges even in the Lightning Network, power-law and scale-free topologies. This difference is anticipated since the LT Codes analyses (Luby, 2002; Popovski et al., 2012) rely on an i.i.d. bipartite encoding graph where flows (encoded symbols) choose channels (input symbols) uniformly at random. On real graphs, the channels traversed by flows are correlated; in fact, correlation between edges of flows makes it very hard to peel the last 6% of channels in the scale-free topology. Further, we found that with a skewed demand matrix, the correlations become stronger and the predictions made using the i.i.d. bipartite graph model deviate from reality more significantly (Fig. 14). Hence, a full analysis of the deadlock peeling process should take into account correlations induced by the topology structure and demand pattern (we leave this to future work). As a first step to understanding the value of such an analysis, we next investigate whether the LT code analysis can be used to synthesize good topologies for uniform random demand matrices, where fortuitously LT code predictions are reasonably accurate.

6.4. Topology Synthesis

Generating a path length distribution. Our goal is to find topologies that require fewer demand pairs to render a topology deadlock-free. We start with an approach for LT Codes (Popovski et al., 2012), which fixes a desired ripple evolution and numerically computes a degree distribution that closely approximates it. In our setting, the degree distribution corresponds to a distribution over path lengths in the credit network. Like (Popovski et al., 2012), we choose a ripple evolution of the form where is the number of unprocessed symbols and is the ripple size when symbols remain unprocessed. For a target graph with 300 nodes and 1500 edges, this ensures a ripple of at the start of the peeling algorithm, decaying slowly to halfway and eventually to towards the end of the algorithm.

Next, we choose a path length distribution for the topology that achieves the desired ripple evolution. Prior work shows that the expected number of symbols added to the ripple at each LT process step is a linear function of the path length distribution (Popovski et al., 2012). The linear transformations and constants correspond to the release probabilities and the desired ripple addition at each step of the algorithm respectively. For completeness, we outline the equations in App. B.4.3. We minimize the -norm of the difference between the expected and desired ripple size. Since our degree distributions map to paths on a graph, we constrain the maximum path length and bound path length probabilities based on the maximum node degree (to enforce decentralization). We also ensure that the number of length paths does not exceed the number of edges and that the path length probabilities decrease from length onwards. Solving this least-squares optimization problem with linear constraints yields a path length distribution.

Synthesizing a matching topology. There are potentially many ways to synthesize a topology with a given shortest-path length distribution. Our approach exploits a known link between the distribution of shortest path lengths for a random graph and its pairwise joint degree distribution (Melnik and Gleeson, 2016; Stanton and Pinar, 2012).999The pairwise joint degree distribution of a graph evaluated at and specifies the probability that a randomly sampled edge connects nodes of degree and . We first set up an optimization using MATLAB to generate a joint degree distribution whose path length distribution minimizes the -norm of the distance from the target path length distribution (output from the previous subsection). Given a joint degree distribution, we use established methods to generate a random graph that matches the joint degree distribution (nxj, [n.d.]a; Gjoka et al., 2015). This approach is more expressive than the well-known configuration model (Fosdick et al., 2018), and can (approximately) recover Erdős-Rényi, scale-free, small-world and random regular graphs.

Results. Our target topology has 300 nodes and 1500 edges. We first use the numerical optimizer to find a path length distribution that peels well. We observe that permitting a large maximum node degree generates path length distributions that the downstream MATLAB optimization routine fails to match well, generating graphs with only 60% of the desired edges. Thus, we ensure that the maximum node degree is 10 and no path is longer than 10 edges. The output distribution from the numerical optimizer is shown in Fig. 10. When using the MATLAB optimization routine to generate a joint degree distribution, we observe that setting the maximum node degree to 20, average degree to 10, and maximum path length to 10 ensures a close match to the desired path length distribution while avoiding extremely long paths during the synthesis step. We then synthesize a graph with the desired node distribution and take its largest connected component. The resulting topology has 271 nodes and 1513 channels, and achieves a path length distribution close to the one desired (Fig. 10). To evaluate how well the synthesized topology performs, we compare it to 5 instances of random regular and scale-free topologies with 300 nodes and about 1500 channels in Fig. 11. The maximum throughput achieved by the synthesized topology is comparable to the random regular graph and up to 15% better than the scale-free graph, particularly with more demand pairs. The and the fraction of channels unpeeled of the synthesized topology strikes a balance between the random regular and scale-free graphs. It is less sensitive than the random regular topology, notably with fewer demand pairs, achieving better 10–20% better and peeling 25–50% more channels. While it is more sensitive than the scale-free graph with sparser demand, it compensates with a 15% larger at denser demands. This approach shows promise in generating topologies that show good peeling properties and throughput insensitivity. We leave it to future work to explore generalizing this to different demand models to generate even better topologies.

Remark. While the above synthesis shows promise, most credit networks are formed by individual nodes’ connectivity decisions, rather than by a centralized authority. However, router nodes in credit networks are incentivized to support high throughput via routing fees, and some PCNs already include peer recommendation systems that suggest peers to connect to (ln-, [n.d.]a, [n.d.]b). While we leave the details to future work, we envision building on these systems to encourage desirable topologies. For example, a credit network software client could “score”, or suggest, peers such that the overall topology obeys a given joint degree distribution.

7. Related Work

Network Topology Design. The peer-to-peer networking literature (Lua et al., 2005) has studied the design of structured (Stoica et al., 2001; Maymounkov and Mazieres, 2002; Ratnasamy et al., 2001) and unstructured topologies (Kim and Srikant, 2013; bit, [n.d.]), particularly for efficient content-retrieval. Meanwhile, fat tree (Al-Fares et al., 2008), Clos (Greenberg et al., 2009), small world (Shin et al., 2011), and random graph (Singla et al., 2012) topologies have been designed to maximize throughput in datacenters. Adapting these ideas to credit networks is hard due to their centralization—e.g., in a fat tree (Al-Fares et al., 2008) with top-of-rack (ToR) switches, the aggregation and core switches require a degree of .

Credit Network Performance. There has been substantial recent interest in quantifying credit network performance, broadly defined as transaction throughput or success rate; prior work has studied the impact of several categories of influencing factors, including routing and scheduling protocols (Sivaraman et al., 2018; Wang et al., 2019; Sivaraman et al., 2020; Malavolta et al., 2017b; Werman and Zohar, 2018), privacy constraints (Roos et al., 2017; Malavolta et al., 2017a; Tang et al., 2020; Tikhomirov et al., 2020), defaulting agents (Ramseyer et al., 2020), and network topology (Dandekar et al., 2011; Dandekar et al., 2015; Aumayr et al., 2020; Khamis and Rottenstreich, [n.d.]). Prior work exploring the effects of credit network topology on transaction success rate (Dandekar et al., 2011) assumed sequential transactions and a full demand matrix. In this setting, maximum throughput can be trivially achieved with length-1 flows, so no deadlocks are observed.

Demand-aware design of payment channel network topologies (Dandekar et al., 2015) poses the problem as an ILP: given a channel budget, a set of nodes, and a demand matrix, the ILP finds an adjacency matrix that either maximizes the number of connected demand pairs (Aumayr et al., 2020) or minimizes the number of channels added and the average path length (Khamis and Rottenstreich, [n.d.]). This approach ignores the effects of channel imbalance, which causes the deadlock-related problems explored in this work.

Erasure Codes. Sparse graph codes have been studied for decades in channel coding (Gallager, 1962; Byers et al., 1998; MacKay, 1999; Luby et al., 2001; Richardson et al., 2001; Luby, 2002; Shokrollahi, 2006). We identify a parallel between such codes and detecting deadlocked edges in a topology. However, despite a rich literature on sparse graph codes, our setting cannot fully utilize most existing constructions for two reasons. First, we need to be able to change the number of flows (encoding symbols) flexibly, without requiring a totally new encoding. We therefore use rateless codes (Luby et al., 2001; Luby, 2002; Shokrollahi, 2006); specifically, our peeling algorithm builds closely on Luby’s LT codes (Luby, 2002). Second, our encoding procedure must respect the topology constraints of the underlying graph; we cannot assign channels uniformly at random to flows, as in classical sparse graph codes. To our knowledge, this constraint has not been previously studied. This is why our theoretical predictions for the number of flows needed to peel a graph (from (Luby, 2002)) are lower than the number needed in practice (§6). More broadly, this suggests an interesting direction of further study on error-correcting codes that obey encoding constraints imposed by a graph topology.

8. Conclusion

In this paper, we studied the effects of topology and channel imbalance on the throughput of credit networks. We demonstrated a close relation between worst-case throughput and the presence of deadlocks, and proposed a heuristic peeling algorithm for identifying the presence of deadlocks. Important directions for future work include synthesizing graphs that are: (a) easy to peel, (b) exhibit high throughput, and (c) limit the maximum degree of any node. While we have made progress on that front, we were not able to find topologies that perform substantially better than random graphs. Hence, an interesting question is whether this is even possible. Another interesting direction is to analyze the peeling algorithm given the correlations induced (in the bipartite graph) by an arbitrary topology and demand pattern. Further, this work assumes perfect routing; in practice it is unclear whether one can actually achieve . Designing decentralized routing protocols that are tailored to good credit network topologies and understanding their performance with respect to these upper bounds will be important in practice. Finally, designing suitable incentive/recommendation mechanisms to achieve a desired topology in a decentralized manner is an important problem.

Acknowledgements.

We thank our anonymous reviewers for their detailed feedback. This work was supported in part by an AFOSR grant FA9550-21-1-0090; NSF grants CNS-1751009, CNS-1910676, and CIF-1705007; a Microsoft Faculty Fellowship; awards from the Cisco Research Center and the Fintech@CSAIL program; and gifts from Chainlink, the Sloan Foundation, and the Ripple Foundation.References

- (1)

- c-l ([n.d.]) [n.d.]. Amount-independent payment routing in Lightning Networks. https://medium.com/coinmonks/amount-independent-payment-routing-in-lightning-networks-6409201ff5ed.

- sca ([n.d.]) [n.d.]. Barabási-Albert Graph. https://networkx.github.io/documentation/networkx-1.9.1/reference/generated/networkx.generators.random_graphs.barabasi_albert_graph.html.

- bit ([n.d.]) [n.d.]. BitTorrent. https://www.bittorrent.com.

- er ([n.d.]) [n.d.]. Erdős-Rényi Graph. https://networkx.org/documentation/stable//reference/generated/networkx.generators.random_graphs.erdos_renyi_graph.html.

- nxj ([n.d.]a) [n.d.]a. Joint-Degree Graph. https://networkx.org/documentation/stable/reference/generated/networkx.generators.joint_degree_seq.joint_degree_graph.html.

- nxj ([n.d.]b) [n.d.]b. Joint-Degree Graph Validation. https://networkx.org/documentation/stable/reference/generated/networkx.generators.joint_degree_seq.is_valid_joint_degree.html.

- fmi ([n.d.]) [n.d.]. MATLAB optimizer. https://www.mathworks.com/help/optim/ug/fmincon.html.

- rai ([n.d.]) [n.d.]. Raiden Network. https://raiden.network/.

- ln- ([n.d.]a) [n.d.]a. The Node Operator’s Guide to the Lightning Galaxy, Part 1. https://lightning.engineering/posts/2019-07-30-routing-quide-1/.

- ln- ([n.d.]b) [n.d.]b. The Node Operator’s Guide to the Lightning Galaxy, Part 2: Node Scoring and Pathfinding. https://lightning.engineering/posts/2019-11-07-routing-guide-2/.

- sma ([n.d.]) [n.d.]. Watts-Strogatz Graph. https://networkx.github.io/documentation/networkx-1.9/reference/generated/networkx.generators.random_graphs.watts_strogatz_graph.html.

- Al-Fares et al. (2008) Mohammad Al-Fares, Alexander Loukissas, and Amin Vahdat. 2008. A scalable, commodity data center network architecture. ACM SIGCOMM computer communication review 38, 4 (2008), 63–74.

- Aumayr et al. (2020) Lukas Aumayr, Esra Ceylan, Matteo Maffei, Pedro Moreno-Sanchez, Iosif Salem, and Stefan Schmid. 2020. Demand-Aware Payment Channel Networks. arXiv preprint arXiv:2011.14341 (2020).

- Byers et al. (1998) John W Byers, Michael Luby, Michael Mitzenmacher, and Ashutosh Rege. 1998. A digital fountain approach to reliable distribution of bulk data. ACM SIGCOMM Computer Communication Review 28, 4 (1998), 56–67.

- Dandekar et al. (2011) Pranav Dandekar, Ashish Goel, Ramesh Govindan, and Ian Post. 2011. Liquidity in credit networks: A little trust goes a long way. In Proceedings of the 12th ACM conference on Electronic commerce. 147–156.

- Dandekar et al. (2015) Pranav Dandekar, Ashish Goel, Michael P Wellman, and Bryce Wiedenbeck. 2015. Strategic formation of credit networks. ACM Transactions on Internet Technology (TOIT) 15, 1 (2015), 1–41.

- Decker and Wattenhofer (2015) Christian Decker and Roger Wattenhofer. 2015. A fast and scalable payment network with bitcoin duplex micropayment channels. In Symposium on Self-Stabilizing Systems. Springer, 3–18.

- Fosdick et al. (2018) Bailey K Fosdick, Daniel B Larremore, Joel Nishimura, and Johan Ugander. 2018. Configuring random graph models with fixed degree sequences. Siam Review 60, 2 (2018), 315–355.

- Gallager (1962) Robert Gallager. 1962. Low-density parity-check codes. IRE Transactions on information theory 8, 1 (1962), 21–28.

- Gjoka et al. (2015) Minas Gjoka, Bálint Tillman, and Athina Markopoulou. 2015. Construction of simple graphs with a target joint degree matrix and beyond. In 2015 IEEE Conference on Computer Communications (INFOCOM). IEEE, 1553–1561.

- Greenberg et al. (2009) Albert Greenberg, James R Hamilton, Navendu Jain, Srikanth Kandula, Changhoon Kim, Parantap Lahiri, David A Maltz, Parveen Patel, and Sudipta Sengupta. 2009. VL2: A scalable and flexible data center network. In Proceedings of the ACM SIGCOMM 2009 conference on Data communication. 51–62.

- Hu and Lau (2013) Pili Hu and Wing Cheong Lau. 2013. A survey and taxonomy of graph sampling. arXiv preprint arXiv:1308.5865 (2013).

- Khamis and Rottenstreich ([n.d.]) Julia Khamis and Ori Rottenstreich. [n.d.]. Demand-aware Channel Topologies for Off-chain Blockchain Payments. ([n. d.]).

- Kim and Srikant (2013) Joohwan Kim and Rayadurgam Srikant. 2013. Real-time peer-to-peer streaming over multiple random hamiltonian cycles. IEEE transactions on information theory 59, 9 (2013), 5763–5778.

- Lua et al. (2005) Eng Keong Lua, Jon Crowcroft, Marcelo Pias, Ravi Sharma, and Steven Lim. 2005. A survey and comparison of peer-to-peer overlay network schemes. IEEE Communications Surveys & Tutorials 7, 2 (2005), 72–93.

- Luby (2002) Michael Luby. 2002. LT codes. In The 43rd Annual IEEE Symposium on Foundations of Computer Science, 2002. Proceedings. IEEE, 271–280.

- Luby et al. (2001) Michael G Luby, Michael Mitzenmacher, Mohammad Amin Shokrollahi, and Daniel A Spielman. 2001. Efficient erasure correcting codes. IEEE Transactions on Information Theory 47, 2 (2001), 569–584.

- MacKay (1999) David JC MacKay. 1999. Good error-correcting codes based on very sparse matrices. IEEE transactions on Information Theory 45, 2 (1999), 399–431.

- Maimbo et al. (2003) Mr Samuel Munzele Maimbo, Mr Mohammed El Qorchi, and Mr John F Wilson. 2003. Informal Funds Transfer Systems: An analysis of the informal hawala system. International Monetary Fund.

- Malavolta et al. (2017a) Giulio Malavolta, Pedro Moreno-Sanchez, Aniket Kate, and Matteo Maffei. 2017a. SilentWhispers: Enforcing Security and Privacy in Decentralized Credit Networks.. In NDSS.

- Malavolta et al. (2017b) Giulio Malavolta, Pedro Moreno-Sanchez, Aniket Kate, Matteo Maffei, and Srivatsan Ravi. 2017b. Concurrency and privacy with payment-channel networks. In Proceedings of the 2017 ACM SIGSAC Conference on Computer and Communications Security. 455–471.

- Maymounkov and Mazieres (2002) Petar Maymounkov and David Mazieres. 2002. Kademlia: A peer-to-peer information system based on the xor metric. In International Workshop on Peer-to-Peer Systems. Springer, 53–65.

- Melnik and Gleeson (2016) Sergey Melnik and James P Gleeson. 2016. Simple and accurate analytical calculation of shortest path lengths. arXiv preprint arXiv:1604.05521 (2016).

- Moreno-Sanchez et al. (2018) Pedro Moreno-Sanchez, Navin Modi, Raghuvir Songhela, Aniket Kate, and Sonia Fahmy. 2018. Mind your credit: Assessing the health of the ripple credit network. In Proceedings of the 2018 World Wide Web Conference. 329–338.

- Poon and Dryja (2016) Joseph Poon and Thaddeus Dryja. 2016. The Bitcoin Lightning Network: Scalable Off-chain Instant Payments. draft version 0.5 9 (2016), 14.

- Popovski et al. (2012) Petar Popovski, Jan Ostergaard, et al. 2012. Design and analysis of LT codes with decreasing ripple size. IEEE Transactions on Communications 60, 11 (2012), 3191–3197.

- Ramseyer et al. (2020) Geoffrey Ramseyer, Ashish Goel, and David Mazières. 2020. Liquidity in credit networks with constrained agents. In Proceedings of The Web Conference 2020. 2099–2108.

- Ratnasamy et al. (2001) Sylvia Ratnasamy, Paul Francis, Mark Handley, Richard Karp, and Scott Shenker. 2001. A scalable content-addressable network. In Proceedings of the 2001 conference on Applications, technologies, architectures, and protocols for computer communications. 161–172.

- Richardson et al. (2001) Thomas J Richardson, Mohammad Amin Shokrollahi, and Rüdiger L Urbanke. 2001. Design of capacity-approaching irregular low-density parity-check codes. IEEE transactions on information theory 47, 2 (2001), 619–637.

- Roos et al. (2017) Stefanie Roos, Pedro Moreno-Sanchez, Aniket Kate, and Ian Goldberg. 2017. Settling payments fast and private: Efficient decentralized routing for path-based transactions. arXiv preprint arXiv:1709.05748 (2017).

- Shin et al. (2011) Ji-Yong Shin, Bernard Wong, and Emin Gün Sirer. 2011. Small-world datacenters. In Proceedings of the 2nd ACM Symposium on Cloud Computing. 1–13.

- Shokrollahi (2006) Amin Shokrollahi. 2006. Raptor codes. IEEE transactions on information theory 52, 6 (2006), 2551–2567.

- Singla et al. (2012) Ankit Singla, Chi-Yao Hong, Lucian Popa, and P Brighten Godfrey. 2012. Jellyfish: Networking data centers randomly. In 9th USENIX Symposium on Networked Systems Design and Implementation (NSDI 12). 225–238.

- Sivaraman et al. (2018) Vibhaalakshmi Sivaraman, Shaileshh Bojja Venkatakrishnan, Mohammad Alizadeh, Giulia Fanti, and Pramod Viswanath. 2018. Routing Cryptocurrency with the Spider Network. In Proceedings of the 17th ACM Workshop on Hot Topics in Networks. ACM, 29–35.

- Sivaraman et al. (2020) Vibhaalakshmi Sivaraman, Shaileshh Bojja Venkatakrishnan, Kathleen Ruan, Parimarjan Negi, Lei Yang, Radhika Mittal, Giulia Fanti, and Mohammad Alizadeh. 2020. High Throughput Cryptocurrency Routing in Payment Channel Networks. In 17th USENIX Symposium on Networked Systems Design and Implementation (NSDI 20). 777–796.

- Stanton and Pinar (2012) Isabelle Stanton and Ali Pinar. 2012. Constructing and sampling graphs with a prescribed joint degree distribution. Journal of Experimental Algorithmics (JEA) 17 (2012), 3–1.

- Stoica et al. (2001) Ion Stoica, Robert Morris, David Karger, M Frans Kaashoek, and Hari Balakrishnan. 2001. Chord: A scalable peer-to-peer lookup service for internet applications. ACM SIGCOMM Computer Communication Review 31, 4 (2001), 149–160.

- Tang et al. (2020) Weizhao Tang, Weina Wang, Giulia Fanti, and Sewoong Oh. 2020. Privacy-utility tradeoffs in routing cryptocurrency over payment channel networks. Proceedings of the ACM on Measurement and Analysis of Computing Systems 4, 2 (2020), 1–39.

- Tikhomirov et al. (2020) Sergei Tikhomirov, Pedro Moreno-Sanchez, and Matteo Maffei. 2020. A quantitative analysis of security, anonymity and scalability for the lightning network. In 2020 IEEE European Symposium on Security and Privacy Workshops (EuroS&PW). IEEE, 387–396.

-

Torpey (2016)

Kyle Torpey.

2016.

Greg Maxwell: Lightning Network Better Than

Sidechains for Scaling Bitcoin.

https://bitcoinmagazine.com/articles/greg-maxwell-lightning-network-better-than-sidechains-for-scaling-

bitcoin-1461077424/. - Wang et al. (2019) Peng Wang, Hong Xu, Xin Jin, and Tao Wang. 2019. Flash: efficient dynamic routing for offchain networks. In Proceedings of the 15th International Conference on Emerging Networking Experiments And Technologies. 370–381.

- Werman and Zohar (2018) Shira Werman and Aviv Zohar. 2018. Avoiding deadlocks in payment channel networks. In Data Privacy Management, Cryptocurrencies and Blockchain Technology. Springer, 175–187.

Appendix A Theoretical Results

A.1. Basic Properties

Proposition 4.

For any state , is a convex set and .

Proposition 5.

For a balance state , if , then for any .

Proposition 6.

For any and , we have and .

Proposition 7.

.

Proposition 8.

The center state has maximized . Precisely, .

Proposition 9.

Proposition 10.

If , then for all whose decomposition is a sequence of flows , we have

-

(1)

For all , ;

-

(2)

For all and (index of path) where , .

A.2. Supporting Theorems

Lemma 11.

If for some , , then for all , we have .

Proof.

Since , , a sequence of flows and a sequence of transient states , where , , and for all ,

Consider new flows for and . Starting from state , we send flows and obtain transient states , where for all ,

Note that . Staring with , we have

Therefore, combining with , we know is a valid sequence of flows that leads to a reachable state from . In other words,

Lemma 12.

Let and be the intersection with the boundary of state space with the direction along to . Let . For all , and for all , .

Proof.