ReferencesSuppReferences

Continuous Record Asymptotic Framework for Inference in Strucutral Change Models

Theory of Low Frequency Contamination from Nonstationarity and Misspecification: Consequences for HAR Inference††thanks: We thank Whitney Newey and Tim Vogelsang for discussions. We also thank Andrew Chesher, Adam McCloskey, Zhongjun Qu and Daniel Whilem for comments.

Abstract

We establish theoretical results about the low frequency contamination (i.e., long memory effects) induced by general nonstationarity for estimates such as the sample autocovariance and the periodogram, and deduce consequences for heteroskedasticity and autocorrelation robust (HAR) inference. We present explicit expressions for the asymptotic bias of these estimates. We distinguish cases where this contamination only occurs as a small-sample problem and cases where the contamination continues to hold asymptotically. We show theoretically that nonparametric smoothing over time is robust to low frequency contamination. Our results provide new insights on the debate between consistent versus inconsistent long-run variance (LRV) estimation. Existing LRV estimators tend to be inflated when the data are nonstationary. This results in HAR tests that can be undersized and exhibit dramatic power losses. Our theory indicates that long bandwidths or fixed- HAR tests suffer more from low frequency contamination relative to HAR tests based on HAC estimators, whereas recently introduced double kernel HAC estimators do not suffer from this problem. Finally, we present second-order Edgeworth expansions under nonstationarity about the distribution of HAC and DK-HAC estimators and about the corresponding -test in the linear regression model.

Abstract

This supplemental material is for online publication only. It introduces the notion of long memory segmented locally stationary processes in Section S.A. Section S.B contains the proofs of the results in the paper and Section S.C contains additional figures.

JEL Classification: C12, C13, C18, C22, C32, C51

Keywords: Edgeworth expansions, Fixed-, HAC standard errors, HAR, Long memory, Long-run variance, Low frequency contamination, Nonstationarity, Outliers, Segmented locally stationary.

1 Introduction

Economic and financial time series are highly nonstationary [see, e.g., Perron (1989), Stock and Watson (1996), Ng and Wright (2013), and Giacomini and Rossi (2015)]. We develop theoretical results about the behavior of the sample autocovariance () and the periodogram () for a short memory nonstationary process.111By short memory nonstationary processes we mean processes that have non-constant moments and whose sum of absolute autocovariances is finite. The latter rules out processes with unbounded second moments (e.g., unit root). For unit root or trending time series, one has to first apply some differencing or de-trending technique. We show that nonstationarity (e.g., time-variation in the mean or autocovariances) induces low frequency contamination, meaning that the sample autocovariance and the periodogram share features that are similar to those of a long memory series. We present explicit expressions for the asymptotic bias of these estimates, showing that it is always positive and increases with the degree of heterogeneity in the data.

The low frequency contamination can be explained as follows. For a short memory series, the autocorrelation function (ACF) displays exponential decay and vanishes as the lag length , and the periodogram is finite at the origin. Under general forms of nonstationarity, we show theoretically that where , and is independent of . Assuming positive dependence for simplicity (i.e., ), this means that each sample autocovariance overestimates the true dependence in the data. The bias factor depends on the type of nonstationarity and in general does not vanish as . In addition, since short memory implies as , it follows that generates long memory effects since as . As for the periodogram, , we show that under nonstationarity as , a feature also shared by long memory processes.

This low frequency contamination holds as an asymptotic approximation. We verify analytically the quality of the approximation to finite-sample situations. We distinguish cases where this contamination only occurs as a small-sample problem and cases where it continues to hold asymptotically. The former involves asymptotically but a consistent estimate of satisfies in finite-sample. We show analytically that using in place of provides a good approximation in this context. This helps us to explain the long memory effects in situations where asymptotically no low frequency contamination should occur. An example is a -test on a regression coefficient in a correctly specified model with nonstationary errors that are serially correlated. Other examples include -tests in the linear model with mild forms of misspecification that do not undermine the conditions for consistency of the least-squares estimator. Further, similar issues arise if one applies some prior de-trending techniques where the fitted model is not correctly specified (e.g., the data follow a nonlinear trend but one removes a linear trend). Yet another example for which our results are relevant is the case of outliers. In all these examples, asymptotically but one observes enhanced persistence in finite-samples that can affect the properties of heteroskedasticity and autocorrelation robust (HAR) inference. Most of the HAR inference in applied work (besides the - and -test in regression models) are characterized by nonstationary alternative hypotheses for which even asymptotically. This class of tests is very large. Tests for forecast evaluation [e.g., Casini (2018), Diebold and Mariano (1995), Giacomini and Rossi (2009, 2010), Giacomini and White (2006), Perron and Yamamoto (2021) and West (1996)], tests and inference for structural change models [e.g., Andrews (1993), Bai and Perron (1998), Casini and Perron (2021c, 2020, 2021b), Elliott and Müller (2007), and Qu and Perron (2007)], tests and inference in time-varying parameters models [e.g., Cai (2007) and Chen and Hong (2012)], tests and inference for regime switching models [e.g., Hamilton (1989) and Qu and Zhuo (2020)] and others are part of this class.

Recently, Casini (2021c) proposed a new HAC estimator that applies nonparametric smoothing over time in order to account flexibly for nonstationarity. We show theoretically that nonparametric smoothing over time is robust to low frequency contamination and prove that the resulting sample local autocovariance and the local periodogram do not exhibit long memory features. Nonparametric smoothing avoids mixing highly heterogeneous data coming from distinct nonstationary regimes as opposed to what the sample autocovariance and the periodogram do.

Our work is different from the literature on spurious persistence caused by the presence of level shifts or other deterministic trends. Perron (1990) showed that the presence of breaks in mean often induces spurious non-rejection of the unit root hypothesis, and that the presence of a level shift asymptotically biases the estimate of the AR coefficient towards one. Bhattacharya et al. (1983) demonstrated that certain deterministic trends can induce the spurious presence of long memory. In other contexts, similar issues were discussed by Christensen and Varneskov (2017), Diebold and Inoue (2001), Demetrescu and Salish (2020), Lamoureux and Lastrapes (1990), Hillebrand (2005), Granger and Hyung (2004), McCloskey and Hill (2017), Mikosch and Stărica (2004) and Perron and Qu (2010). Our results are different from theirs in that we consider a more general problem and we allow for more general forms of nonstationarity using the segmented locally stationary framework of Casini (2021c). Importantly, we provide a general solution to these problems and show theoretically its robustness to low frequency contamination. Moreover, we discuss in detail the implications of our theory for HAR inference.

HAR inference relies on estimation of the long-run variance (LRV). The latter, from a time domain perspective, is equivalent to the sum of all autocovariances while from a frequency domain perspective, is equal to times an integrated time-varying spectral density at the zero frequency. From a time domain perspective, estimation involves a weighted sum of the sample autocovariances, while from a frequency domain perspective estimation is based on a weighted sum of the periodogram ordinates near the zero frequency. Therefore, our results on low frequency contamination for the sample autocovariances and the periodogram can have important implications.

There are two main approaches in HAR inference which relies on whether the LRV estimator is consistent or not. The classical approach relies on consistency which results in HAC standard errors [cf. Newey and West (1987, 1994) and Andrews (1991)]. Inference is standard because HAR test statistics follow asymptotically standard distributions. It was shown early that HAC standard errors can result in oversized tests when there is substantial temporal dependence. This stimulated a second approach based on inconsistent LRV estimators that keep the bandwidth at a fixed fraction of the sample size [cf. Kiefer et al. (2000)]. Inference becomes nonstandard and it is shown that fixed- achieves high-order refinements [e.g., Sun et al. (2008)] and reduces the oversize problem of HAR tests.222See Dou (2019), Lazarus et al. (2020), Lazarus et al. (2018), Ibragimov and Müller (2010), Jansson (2004), Kiefer and Vogelsang (2002, 2005), Müller (2007, 2014), Phillips (2005), Politis (2011), Pötscher and Preinerstorfer (2016, 2018, 2019), Robinson (1998), Sun (2013, 2014a, 2014b) and Zhang and Shao (2013). However, unlike the classical approach, current fixed- HAR inference is only valid under stationarity [cf. Casini (2021b)].

Recent work by Casini (2021c) questioned the performance of HAR inference tests under nonstationarity from a theoretical standpoint. Simulation evidence of serious (e.g., non-monotonic) power or related issues in specific HAR inference contexts were documented by Altissimo and Corradi (2003), Casini (2018), Casini and Perron (2019, 2021c, 2020), Chan (2020), Chang and Perron (2018), Crainiceanu and Vogelsang (2007), Deng and Perron (2006), Juhl and Xiao (2009), Kim and Perron (2009), Martins and Perron (2016), Otto and Breitung (2021), Perron and Yamamoto (2021), Shao and Zhang (2010), Vogelsang (1999) and Zhang and Lavitas (2018) among others]. Our theoretical results show that these issues occur because the unaccounted nonstationarity alters the spectrum at low frequencies. Each sample autocovariance is upward biased () and the resulting LRV estimators tend to be inflated. When these estimators are used to normalize test statistics, the latter lose power. Interestingly, is independent of so that the more lags are included the more severe is the problem. Further, by virtue of weak dependence, we have that as but across . For these reasons, long bandwidths/fixed- LRV estimators are expected to suffer most because they use many/all lagged autocovariances.

To precisely analyze the theoretical properties of the HAR tests under the null hypothesis, we present second-order Edgeworth expansions under nonstationarity for the distribution of the HAC and DK-HAC estimator and for the distribution of the corresponding -test in the linear regression model. Under stationarity the results concerning the HAC estimator were provided by Velasco and Robinson (2001). We show that the order of the approximation error of the expansion is the same as under stationarity from which it follows that the error in rejection probability (ERP) is also the same. The ERP of the -test based on the DK-HAC estimator is slightly larger than that of the -test based on the HAC estimator due to the double smoothing. High-order asymptotic expansions for spectral and other estimates were studied by Bhattacharya and Ghosh (1978), Bentkus and Rudzkis (1982), Janas (1994), Phillips (1977; 1980) and Taniguchi and Puri (1996). The asymptotic expansions of the fixed- HAR tests under stationarity were developed by Jansson (2004) and Sun et al. (2008). Casini (2021b) showed that under nonstationarity the ERP of the fixed- HAR tests can be larger than that of HAR tests based on HAC and DK-HAC estimators thereby controverting the mainstream conclusion in the literature that fixed- HAR tests are theoretically superior to HAR tests based on consistent LRV estimators.

The paper is organized as follows. Section 2 presents the statistical setting and Section 3 establishes the theoretical results on low frequency contamination. Section 4 presents the Edgeworth expansions of HAR tests based on the HAC and DK-HAC estimators. The implications of our results for HAR inference are analyzed analytically and computationally through simulations in Section 5. Section 6 concludes. The supplemental materials [cf. Casini et al. (2021)] contain some additional examples and all mathematical proofs. The code to implement our method is provided in , and languages through a repository.

2 Statistical Framework for Nonstationarity

Suppose is defined on a probability space , where is the sample space, is the -algebra and is a probability measure. In order to analyze time series models that have a time-varying spectrum it is useful to introduce an infill asymptotic setting whereby we rescale the original discrete time horizon by dividing each by Letting we define a new time scale on which as we observe more and more realizations of close to time . As a notion of nonstationarity, we use the concept of segmented local stationarity (SLS) introduced in Casini (2021c). This extends the locally stationary processes [cf. Dahlhaus (1997)] to allow for structural change and regime switching-type models. SLS processes allow for a finite number of discontinuities in the spectrum over time. We collect the break dates in the set . Let A function is said to be left-differentiable at if exists for any . Let be a finite integer.

Definition 2.1.

A sequence of stochastic processes is called segmented locally stationary (SLS) with regimes, transfer function and trend if there exists a representation

| (2.1) |

for , where by convention and . The following technical conditions are also assumed to hold: (i) is a process on with and

where denotes the cumulant spectra of -th order, , for all with that may depend on , and is the period extension of the Dirac delta function ; (ii) There exists a and a piecewise continuous function such that, for each , there exists a -periodic function with , and for all

| (2.2) | ||||

| (2.3) |

(iii) is piecewise Lipschitz continuous.

Assumption 2.1.

(i) is a mean-zero SLS process with regimes; (ii) is twice continuously differentiable in at all , with uniformly bounded derivatives and ; (iii) is Lipschitz continuous at all ; (iv) is twice left-differentiable in at with uniformly bounded derivatives and and has piecewise Lipschitz continuous derivative ; (v) is Lipschitz continuous in

We define the time-varying spectral density as for . Then we can define the local covariance of at the rescaled time with and lag as . The same definition is also used when and . For and it is defined as .

Next, we impose conditions on the temporal dependence (we omit the second subscript when it is clear from the context). Let

where is a Gaussian sequence with the same mean and covariance structure as , is the time- fourth-order cumulant of while is the time- centered fourth moment of if were Gaussian.

Assumption 2.2.

(i) and for all . (ii) For all there exists a function such that for some constant ; the function is twice differentiable in at all with uniformly bounded derivatives and , and twice left-differentiable in with uniformly bounded derivatives and , and piecewise Lipschitz continuous derivative .

3 Theoretical Results on Low Frequency Contamination

In this section we establish theoretical results about the low frequency contamination induced by nonstationarity, misspecification and outliers. We first consider the asymptotic proprieties of two key quantities for inference in time series contexts, i.e., the sample autocovariance and the periodogram. These are defined, respectively, by

| (3.1) |

where is the sample mean and

which is evaluated at the Fourier frequencies . In the context of autocorrelated data, hypotheses testing and construction of confidence intervals require estimation of the so-called long-run variance. Traditional HAC estimators are weighted sums of sample autocovariances while frequency domain estimators are weighted sums of the periodograms. Casini (2021c) considered an alternative estimate for the sample autocovariance to be used in the DK-HAC estimators,333The DK-HAC estimators are defined in Section 5.1. namely,

where satisfying the conditions given below, and

| (3.2) |

with and such that . For notational simplicity we assume that and are even. is an estimate of the autocovariance at time and lag , i.e., . One could use a smoothed or tapered version; the estimate is an integrated local sample autocovariance. It extends to better account for nonstationarity. Similarly, the DK-HAC estimator does not relate to the periodogram but to the local periodogram defined by

where is the (untapered) periodogram over a segment of length with midpoint . We also consider the statistical properties of both and under nonstationarity. Define for with and . Note that

3.1 The Sample Autocovariance Under Nonstationarity

We now establish some asymptotic properties of the sample autocovariance under nonstationarity. We consider the case only; the case is similar. Let

where is defined in (2.1). We use as a shorthand for

Theorem 3.1.

Theorem 3.1 reveals interesting features. It is easier to discuss the case for for which the mean of in each regime is constant. The theorem states that is asymptotically the sum of two terms. The first is the true autocovariance of at lag . The second, , is always positive and increases with the difference in the mean across regimes. Thus, nonstationarity (here in the form of breaks in the mean) induces a positive bias. In the next section, we shall discuss cases in which this bias arises as a finite-sample problem and cases where the bias remains even asymptotically. The result that as implies that unaccounted nonstationarity generates long memory effects. The intuition is straightforward. A long memory SLS process satisfies for some , similar to a stationary long memory process.444In Section S.A in the supplement we define long memory SLS processes that are characterized by the property for some where and is the long memory parameter at time . The theorem shows that exhibits a similar property and decays more slowly than for a short memory stationary process for small lags and approaches a positive constant for large lags. A similar result for was discussed under stationarity in Mikosch and Stărica (2004) to explain long memory in the volatility of financial returns.

Theorem 3.1 suggests that certain deviations from stationarity can generate a long memory component that leads to overestimation of the true autocovariance. It follows that the LRV is also overestimated. Since the LRV is used to normalize test statistics, this has important consequences for many HAR inference tests characterized by deviations from stationarity under the alternative hypothesis. These include tests for forecast evaluation, tests and inference for structural change models, time-varying parameters models and regime-switching models. In the linear regression model, corresponds to the regressors multiplied by the fitted residuals. Unaccounted nonlinearities and outliers can contaminate the mean of and therefore contribute to .

3.2 The Periodogram Under Nonstationarity

Classical LRV estimators are weighted averages of periodogram ordinates around the zero frequency. Thus, it is useful to study the behavior of the periodogram as the frequency approaches zero. We now establish some properties of the asymptotic bias of the periodogram under nonstationarity. We consider the Fourier frequencies for an integer (mod ) and exclude for mathematical convenience.

Assumption 3.1.

(i) For each there exists a such that

where for ; (ii) for all and all for some , (which depends on and ), , and .

Part (i) is easily satisfied (e.g., the special case with ). Part (ii) is satisfied if is strong mixing with mixing parameters of size for some such that This is less stringent than the size condition for some sufficient for Assumption 2.2-(i).

Theorem 3.2.

The theorem suggests that for small frequencies close to the periodogram attains very large values. This follows because the first term of (3.4) is bounded for all . Since are fixed, the order of the second term of (3.4) is . Note that as there are some values for which the corresponding term involving on the right-hand side of (3.4) is equal to zero. In such cases, For other values of as , the second term of (3.4) diverges to infinity. Thus, considering the behavior of as , it generally takes unbounded values except for some for which is bounded below by A SLS process with long memory has an unbounded local spectral density as for some . Since cannot be negative, it follows that is also unbounded as . Theorem 3.2 suggests that nonstationarity consisting of time-varying first moment results in a periodogram sharing features of a long memory series.

3.3 The Sample Local Autocovariance Under Nonstationarity

We now consider the behavior of as defined in (3.2) for fixed as well as for . For notational simplicity we assume that is even.

Theorem 3.3.

(i) for any such that for all , ;

(ii) for any such that for some , we have two sub-cases: (a) if or with , then

(b) if or , then .

Further, if there exists an such that there exists a with satisfying (ii-a), then, as , -a.s., where and as .

The theorem shows that the behavior of depends on whether a change in mean is present or not, and if so whether it is close enough to or not. For a given and , if the condition of part (i) of the theorem holds, then is consistent for [see Casini (2021c)]. If a change-point falls close to either boundary of the window , as specified in case (ii-b), then remains consistent. The only case in which a non-negligible bias arises is when the change-point falls in a neighborhood around sufficiently far from either boundary. This represents case (ii-a), for which a biased estimate results. However, the bias vanishes asymptotically. Since is an average of over blocks , if case (ii-a) holds then as but as . Thus, comparing this result with Theorem 3.1, in practice the long memory effects are unlikely to occur when using . Furthermore, one can altogether avoid this problem by appropriately choosing the blocks . A procedure was proposed in Casini (2021c) using the methods developed in Casini and Perron (2021a).

3.4 The Local Periodogram Under Nonstationarity

We study the asymptotic properties of as for . We consider the Fourier frequencies for an integer (mod ). We need the following high-level conditions. Part (i) corresponds to Assumption 3.1 while part (ii) requires additional smoothness.

Assumption 3.2.

(i) For each with there exist , with for such that

(ii) is continuous in

Theorem 3.4.

(i) for any such that for all , as ;

(ii) for any such that for some we have two sub-cases: (a) if or with and as , then for many values in the sequence as ; (b) if or , then as .

It is useful to compare Theorem 3.4 with Theorem 3.2. Unlike the periodogram, the asymptotic behavior of the local periodogram as depends on the vicinity of to . Since uses observations in the window , if no discontinuity in the mean occurs in this window then is asymptotically unbiased for the spectral density . More complex is its behavior if some falls in . The theorem shows that if is close to the boundary, as indicated in case (ii-b), then is bounded below by , similarly to case (i). If instead falls sufficiently close to the mid-point as indicated in case (ii-a), then for many values in the sequence as provided it satisfies as . Hence, unless is close to the local periodogram behaves very differently from the periodogram . Accordingly, nonstationarity is unlikely to generate long memory effects if one uses the local periodogram. As for , if one uses preliminary inference procedures [cf. Casini and Perron (2021a)] for the detection and estimation of the discontinuities in the spectrum and for the estimation of their locations, then one can construct the window efficiently and avoid being too close to

4 Edgeworth Expansions for HAR Tests Under Nonstationarity

We now consider Edgeworth expansions under nonstationarity for the distribution of the -statistic in the location model based on the HAC and DK-HAC estimator. This is useful for analyzing the theoretical properties of the null rejection probabilities of the HAR tests. As in the literature, we make use of the Gaussianity assumption for mathematical convenience.555This can be relaxed by considering distributions with Gram-Charlier representations at the expenses of more complex derivations without any particular gain in intuition. We relax the stationarity assumption which has been always used in the literature [cf. Jansson (2004), Sun et al. (2008) and Velasco and Robinson (2001)] which has important consequences for the nature of the results. The results concerning the -test based on the HAC estimator are presented in Section 4.1 while those based on the DK-HAC estimator are presented in Section 4.2.

Let be a zero-mean Gaussian SLS process satisfying Assumption 2.1-(i-iv). Let

| (4.1) |

which is valid for all such that where . From Casini (2021c) it follows that .

4.1 HAC-based HAR Tests

The classical HAC estimator is defined as

where is a kernel and a bandwidth parameter. Under appropriate conditions on we have from which it follows that

Let . Note that where has th element

| (4.2) |

such that is a kernel with smoothing number and . For an even function that integrates to one, we define

Note that is periodic of period , even and satisfies . It follows that and . is the so-called spectral window generator. We refer to Brillinger (1975) for a review of these introductory concepts.

We now analyze the joint distribution of and . Let and denote the relative bias and variance, respectively, of . It is convenient to work with standardized statistics with zero mean and unit variance. Write

where . Note that is a centered quadratic form in a Gaussian vector where . The joint characteristic function of is

where , and with being the vector . The cumulant generating function of is

where is the cumulant of Phillips (1980) considered the distribution of linear and quadratic forms under Gaussianity. From his derivations, the nonzero bivariate cumulants are

We introduce the following assumptions about and .

Assumption 4.1.

For all , and has continuous derivatives in a neighborhood of and the th derivative satisfies a Lipschitz condition of order with .

Assumption 4.2.

For all , for some , i.e.,

Assumption 4.3.

, , for and .

Assumption 4.4.

satisfies a uniform Lipschitz condition of order 1 in .

Assumption 4.5.

For , and

Assumption 4.6.

as .

Assumption 4.7.

where and .

Assumption 4.3-4.7 about the kernel and bandwidth are the same as in Velasco and Robinson (2001) in which a discussion can be found. They are satisfied by most kernels used in practice. The bandwidth condition in Assumption 4.6 is sufficient for the consistency of and is strengthened in Assumption 4.7, for some parts of the proofs, which is satisfied by popular MSE-optimal bandwidths [cf. Andrews (1991), Belotti et al. (2021) Whilelm (2015)].

Assumption 4.1-4.2 impose conditions on the smoothness and boundedness of the spectral density. Assumption 4.1 is implied by but it is stronger than necessary because it extends the smoothness restriction to all frequencies. Assumption 4.2 does impose some restrictions on beyond the origin, though it is not particularly restrictive since any arbitrarily close to 1 will suffice.

We now analyze the asymptotic distribution of . Under stationarity this was discussed by Bentkus and Rudzkis (1982) and Velasco and Robinson (2001). We first present a result about the limit of and a result about the bias of .

Lemma 4.1.

Lemma 4.3.

A few examples of are and If then for . In order to develop an Edgeworth expansion to approximate the distribution of , we need to study the cross-cumulants of

Lemma 4.4.

For example, we have and . We now present a second-order Edgeworth expansion to approximate the distribution of , with error and including terms up to order to correct the asymptotic normal distribution. This will imply the validity of that expansion for the distribution of . For , where is any class of Borel sets in , let where is the density of the bivariate standard normal distribution,

and are the univariate Hermite polynomials of order . Let denote a neighborhood of radius of the boundary of a set Let denote the probability measure of

Theorem 4.1 shows that is a valid second-order Edgeworth expansion for the measure . The method of proof is the same as in Velasco and Robinson (2001). We first approximate the true characteristic function and then apply a smoothing lemma [cf. Lemma S.B.2 in the supplement which is from Bhattacharya and Rao (1975)]. The leading term of the approximation error is of order as the second term on the right hand side of (4.3) is negligible if is convex because decreases as a power of . This is the same order obtained for the corresponding leading term under stationarity. Since the higher-order correction terms in depend only on but not on , they are equal to the one obtained under stationarity.

Next, we focus on , i.e., a -statistic for the mean. Proceeding as in Velasco and Robinson (2001), we first derive a linear stochastic approximation to and show that its distribution is the same as that of up to order . Then, we show that the asymptotic approximation for the distribution of the linear stochastic approximation is valid also for with the same error . Using Lemma 4.2-4.3 we can substitute out and in and, by only focusing on the leading terms, we define the following linear stochastic approximation,

Lemma 4.5.

Note that the condition is sufficient for the consistency of . Indeed, for it implies that which coincides with the MSE-optimal bandwidth choice for the quadratic spectral kernel [cf. Andrews (1991)]. The next theorem presents a valid Edgeworth expansion for the distribution of from that of

Theorem 4.2.

Lemma 4.5 and Theorem 4.2 show the form of the correction term to the standard normal distribution, i.e., . The error of the approximation is of order which is the same as the one obtained under stationarity by Velasco and Robinson (2001).

Let denote the distribution function of the standard normal. Setting , and integrating and Taylor expanding , we obtain, uniformly in ,

| (4.5) | ||||

This shows that under the conditions of Theorem 4.2, the standard normal approximation is correct up to order . Consider the location model For the null hypothesis , consider the following -test,

where is the least-squares estimator of . Theorem 4.2 and (4.5) imply that

| (4.6) |

for any where is an odd function. Thus, the error in rejection probability (ERP) of is of order . If is second-order stationary, the results in Velasco and Robinson (2001) imply that the ERP of is also of order . Below we establish the corresponding ERP when the -statistic is instead normalized by and also discuss the ERP of the -test under fixed- asymptotics.

4.2 DK-HAC-based HAR Tests

We now consider the Edgeworth expansion for tests based on the DK-HAC estimator. In order to simplify some parts of the proof here we consider an asymptotically equivalent version of the DK-HAC estimator discussed in Section 5. Let

where is a bandwidth sequence and

with a kernel and a bandwidth. Note that and are asymptotically equivalent and is a special case of with being a rectangular kernel and .

Assumption 4.8.

, , , for and is continuous. The bandwidth sequence satisfies , and where is the index of smoothness of at 0.

Under Assumption 4.3-4.4, 4.6 and 4.8 it holds that [cf. Casini (2021c)] and

| (4.7) |

Note that where with and defined in (4.2). Let

is the local periodogram of . Then, .

We begin by analyzing the joint distribution of and . Let and denote the relative bias and variance of , respectively. It is convenient to work with standardized statistics with zero mean and unit variance. Write

where with Note that is a centered quadratic form in a Gaussian vector where . The joint characteristic function of is

where and . The cumulant generating function of is

where is the cumulant of To obtain more precise bounds in some parts of the proofs we use the following assumption on the cross-partial derivatives of . Let denote the set of continuity points of in , i.e., .

Assumption 4.9.

For has continuous derivatives in in a neighborhood of the derivative satisfying a Lipschitz condition of order .

We now consider the cumulants of the normalized spectral estimate .

Lemma 4.7.

Note that includes the error due to the smoothing over time. This error is of smaller order than . We now consider the cross-cumulants of

Lemma 4.8.

We now present a second-order Edgeworth expansion to approximate the distribution of with error . The expansion includes terms up to order to correct the asymptotic normal distribution. This implies the validity of that expansion for the distribution of . For , let where

and are the univariate Hermite polynomials of order .

Theorem 4.3.

Theorem 4.3 shows that is a valid second-order Edgeworth expansion for the probability measure of The correction differs from in Theorem 4.1. This difference depends on the smoothing over time, i.e., on and . The theorem also suggests that the leading term of the error of the approximation is order of .

Next, we focus on defined in (4.7), i.e., a -statistic based on , and present the Edgeworth expansion. We need the following assumption, replacing Assumption 4.6-4.7, that controls the rate of smoothing over lagged autocovariances and time implied by the bandwidths and , respectively. The assumption is satisfied by, for example, the MSE-optimal DK-HAC estimators proposed by Belotti et al. (2021) and Casini (2021c).

Assumption 4.10.

The bandwidths and satisfy

Theorem 4.4.

Theorem 4.4 shows that the correction term to the standard normal distribution, i.e., , depends on both smoothing directions. The error of the approximation is of order which can be larger than that obtained in Theorem 4.2 for the HAC estimators. Similarly to (4.5), we obtain uniformly in ,

| (4.10) |

where , which suggests that the standard normal approximation is correct up to order . Returning to the location model, consider the -statistic based on ,

Theorem 4.4 and (4.10) imply that

| (4.11) |

for any where is an odd function different from in (4.6). Thus, the ERP of can be larger than that of . This follows from the fact that applies smoothing over two directions. The smoothing over time is useful to more flexibly account for nonstationarity. Its benefits appear explicitly under the alternative hypothesis as we show in the next section whereas the ERP refers to the null hypothesis. One can also show that the ERP of and remain unchanged if prewhitening is applied, though the proofs are omitted since they are similar.

We can further compare the ERP of and to that of the corresponding -test under the fixed- asymptotics. Casini (2021b) showed that the limiting distribution of the fixed- HAR test statistics under nonstationarity is not pivotal as it depends on the true data-generating process of the errors and regressors. This contrasts to the stationarity case for which the fixed- limiting distribution is pivotal and the ERP is of order [see Jansson (2004) and Sun et al. (2008)]. Based on an ERP of smaller magnitude relative to that of HAR tests based on HAC estimators [cf. ], the literature has long suggested that fixed- HAR tests are superior to HAR tests based on HAC estimators. However, this break downs under nonstationarity as shown by Casini (2021b) who established that the ERP of fixed- HAR tests increases by an order of magnitude relative to the stationary case [i.e., from to with ]. Therefore, fixed- HAR tests can have an ERP larger than that of and . Finally, the ERP of the fixed- HAR tests that use the critical value from the distribution valid under stationarity is since the latter is different from the relevant distribution if the data are nonstationarity.

5 Consequences for HAR Inference

In this section we discuss the implications of the theoretical results from Section 3-4. In Section 5.1, we first present a review of HAR inference methods and their connection to the estimates considered in Section 3. We separate the discussion into two parts. In Section 5.2, we discuss HAR inference tests for which the issues of low frequency contamination induce a finite-sample problem, and in Section 5.3 when they persist even asymptotically. For the latter case, in Section 5.4 we provide theoretical results about the power of the tests. Section 5.5 presents a discussion.

5.1 HAR Inference Methods

There are two main approaches for HAR inference which differ on whether the long-run variance (LRV) estimator is consistent or not. The classical approach relies on consistency which results in HAC standard errors [cf. Newey and West (1987, 1994), Andrews (1991) and Casini (2021a)]. Classical HAC standard errors require estimation of the LRV defined as where is defined after (4.1). The form of depends on the specific problem under study. For example, for a -test on a regression coefficient in the linear model we have . Classical HAC estimators take the following form,

| , |

where is given in (3.1) with where are the least-squares residuals, is a kernel and is bandwidth. One can use the the Bartlett kernel, advocated by Newey and West (1987), or the quadratic spectral kernel as suggested by Andrews (1991), or any other kernel suggested in the literature, see e.g. de Jong and Davidson (2000) and Ng and Perron (1996). Under at an appropriate rate, we have Hence, equipped with , HAR inference is standard and simple because HAR test statistics follow asymptotically standard distributions.

HAC standard errors can result in oversized tests when there is substantial temporal dependence [e.g., Andrews (1991)]. This stimulated a second approach based on inconsistent LRV estimators that keep the bandwidth at some fixed fraction of [cf. Kiefer et al. (2000)], e.g., using all autocovariances, so that which is equivalent to the Newey-West estimator with , in which case is an inconsistent estimate of . Because of the inconsistency, inference is nonstandard and HAR test statistics do not have asymptotically standard distributions. The validity of fixed- inference rests on stationarity [cf. Casini (2021b)]. Many authors have considered various versions of . However, the one that leads to HAR inference tests that are least oversized is the original [see Casini and Perron (2021d) for simulation results]. For comparison we also report the equally weighted cosine (EWC) estimator of Lazarus et al. (2020). It is an orthogonal series estimators that use long bandwidths,

with some fixed integer. Assuming satisfies some conditions, under fixed- asymptotics a -statistic normalized by follows a distribution where is the degree of freedom.

Recently, a new HAC estimator was proposed in Casini (2021c). Motivated by the power impact of low frequency contamination of existing LRV estimators, he proposed a double kernel HAC (DK-HAC) estimator, defined by

| , |

where is a bandwidth sequence and defined in Section 3 with replaced by

with a kernel and a bandwidth. Note that and are asymptotically equivalent and the results of Section 3 continue to hold for . More precisely, is a special case of with being a rectangular kernel and . This approach falls in the first category of standard inference and HAR test statistics normalized by follows standard distribution asymptotically. Additionally, Casini and Perron (2021d) proposed prewhitened DK-HAC estimator that improves the size control of HAR tests. The estimator applies a prewhitening transformation to the data before constructing and enjoys the same asymptotic properties. Due to their ability to more flexibly account for nonstationarity, Casini (2021c) and Casini and Perron (2021d) demonstrated via simulations that tests based on and have superior power properties relative to tests based on the other estimators. In terms of size, the simulation results showed that tests based on performs better than those based on and , and is competitive with when the latter works well. We include and in our simulations below. We report the results only for the DK-HAC estimators that do not use the pre-test for discontinuities in the spectrum [cf. Casini and Perron (2021a)] because we do not want the results to be affected by such pre-test. Since the pre-test improves the results, what we report here are the worst-case results for the DK-HAC estimators.

5.2 Small-Sample Low Frequency Contamination

We now discuss situations in which the low frequency contamination arises as a small-sample problem. These comprise situations where asymptotically but a consistent estimate of satisfies in finite-sample. In these situations, one can expect the low frequency contamination to have an effect in small samples.

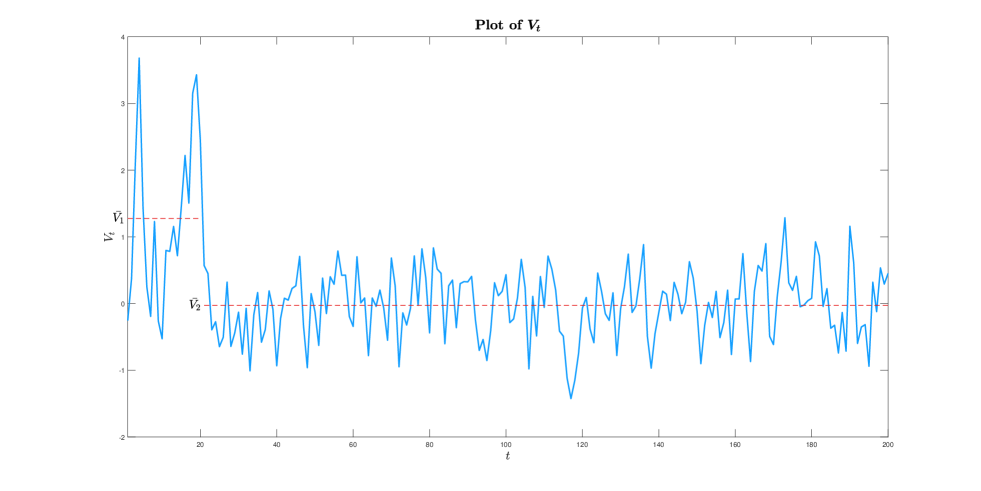

We begin with a simple model involving a zero-mean SLS process with changes in persistence. The combination of nonstationarity and serial dependence generates long memory effects because . We specify as a SLS process given by a two-regimes zero-mean time-varying AR(1), labeled model M1. That is, , for with , and , , for . Note that varies between 0.172 and 0.263. We set and A plot of is reported in Figure 1. Note that for all and so . However, if we replace and in by and respectively, where and , then the estimate of is different from zero and generates a finite-sample bias which can give rise to effects akin to long memory.

We first look at the behavior of the sample autocovariance . We compare it with the theoretical autocovariance . The latter is equal to We can compute numerically using,

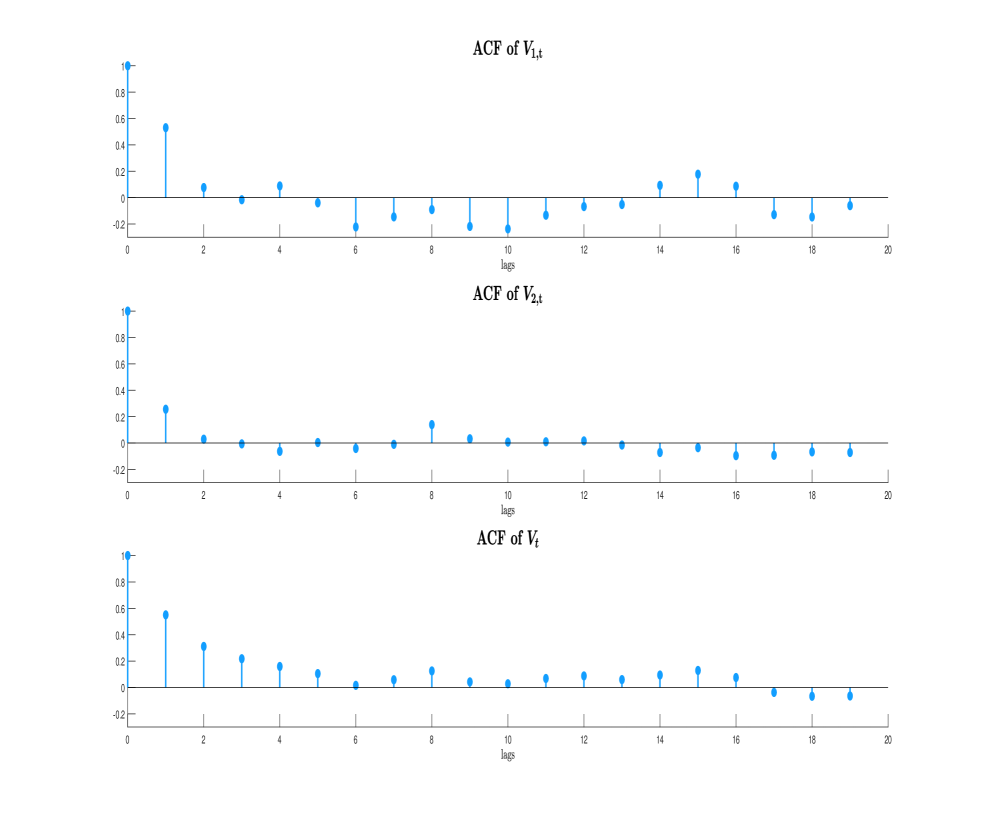

Table 1 reports , and for several values of . Despite noisy autocovariance estimates, it is still possible to discern some patterns. For all , largely overestimates . This is consistent with Theorem 3.1 which suggests that this is due to the bias . This is also supported by the bias-corrected estimate which is accurate in approximating This is especially so for small In general, Theorem 3.1 provides good approximations confirming that suffers from low frequency contaminations. Theorem 3.3 suggests that this issue should not occur for . In fact, is more accurate than (except for ). For the form of is different, because , and is simply given by the autocovariance of for (i.e., the second regime). Thus, for whereas is often small but positive. In contrast, for thereby confirming that does not suffer from low frequency contamination. These results are confirmed in Figure 2 which plots the autocorrelation function (ACF) of (), () and (). Although the ACF of should be a weighted average of the ACF of and of the ACF of in the bottom panel shows much higher persistence than either ACF in the top and mid panels. This is odd since is a highly persistent series. Further, it shows that the dependence is essentially always positive. This is also odd. These features are consistent with our theory which suggests that nonstationarity makes appear more persistent and that the bias is positive. Other examples with similar features involve given by the least-squares regression residuals under mild forms of misspecification that do not undermine the conditions for consistency of the least-squares estimator, e.g., exclusion of a relevant regressor uncorrelated with the included reggressors, or inclusion of an irrelevant regressor. Another example involves obtained after applying some de-trending techniques where the fitted model is not correctly specified (e.g., the data follow a nonlinear trend but one removes a linear trend). A final example is the case of outliers because they influence the mean of and therefore .

What is especially relevant is whether this evidence of long memory feature has any consequence for HAR inference. We obtain the empirical size and power for a -test on the intercept normalized by several LRV estimators for the model with under the null and under the alternative hypothesis. In addition to M1, we consider other models: M2 involves a locally stationary process , , ; M3 is the same as M2 with outliers for where where is the inverse complementary error function, is the median and ;666We follow the literature on outlier detection for continuous functions and use the median absolute deviation to generate the outlier. This notion used in this literature does not deem a value smaller than as an outlier. M4 involves a locally stationary model with periods of strong persistence where , , . varies between 0.7 and 0.05 in M2-M3 and between 0.95 and 0.07 in M4.

We consider the DK-HAC estimators with and without prewhitening (, , ) of Casini (2021c) and Casini and Perron (2021d), respectively; Andrews’ (1991) HAC estimator with and without the prewhitening procedure of Andrews and Monahan (1992); Newey and West’s (1987) HAC estimator with the usual rule to select the number of lags (i.e., ; Newey-West with the fixed- method of Kiefer et al. (2000) (labeled KVB); and the Empirical Weighted Cosine (EWC) of Lazarus et al. (2018). For the DK-HAC estimators we use the data-dependent methods for the bandwidths, kernels and choice of as proposed in Casini (2021c) and Casini and Perron (2021d), which are optimal under mean-squared error (MSE). Let denote the least-squares residual based on where the latter is the least-squares estimate of . We set where

with and and , where and

with being the cardinality of and , We set , is the QS kernel and for

Table 2-5 report the results. The -test normalized by Newey and West’s (1987) and Andrews’ (1991) prewhitened HAC estimators are excessively oversized.777This is not in contradiction with our theoretical results. The prewhitening of Andrews and Monahan (1992) is unstable when there is nonstationarity as shown by Casini and Perron (2021d). The reason is that there is a bias both in the whitening and the recoloring stages. The biases have opposite signs so that here the underestimation of the LRV dominates. Newey-West uses a fixed rule for determining the number of lags. The number of included lags is small. This estimator is known to be largely oversized when the data are stationary with high dependence. Our results say that the included sample autocovariances may be inflated if there is nonstationarity. However, given that the fixed rule selects a small number of lags then nonstationarity results in a smaller oversize problem. Andrews’ (1991) HAC-based test is slightly undersized while KVB’s fixed- and EWC-based tests are severely undersized.888In general, Andrews’ (1991) HAC estimator leads to tests that are oversized when the data are stationary with strong dependence. Here, nonstationarity reduces the oversize problem. It follows from a similar argument as for the Newey-West estimator even though Andrews’ (1991) HAC estimator uses a data-dependent method for the selection of the number of lags. Thus, it selects more lags than the ones suggested by the fixed rule. Consequently, more sample autocovariances are overestimated and this helps to reduce its oversize problem. These outcomes arise from nonstationarity and are consistent with our theoretical analysis of . Since for many large lags , the KVB’s fixed- and EWC’s estimators that include many lags are inflated and reduce the magnitude of the test statistic even under the null hypotheses. The fact that KVB’s fixed- and EWC-based tests have larger size distortions than other tests is consistent with the results in Section 4 which suggest that they have a larger ERP. For the -test on the intercept, can lead to tests that are oversized when there is strong dependence, as shown in Table 2. However, the prewhitened DK-HAC estimators and lead to tests that show very accurate rejection rates. Overall, inspection of the size properties suggests that the DK-HAC-based tests do not suffer from low frequency contamination which, in contrast, affects the tests based on LRV estimators that rely on the full sample estimates or equivalently on (e.g., the EWC). The same issue also affects the power properties of the tests. The KVB’s fixed- and EWC-based estimators suffer from relatively large power losses. The power of tests normalized by Newey and West’s (1987) and Andrews’ (1991) prewhitened HAC are not comparable because they are significantly oversized. The DK-HAC-based tests have the best power, the second best being Andrews’ (1991) HAC-based test.

Turning to M2, Table 3 shows even larger size distortions and power losses for KVB’s fixed- and EWC-based tests. All the DK-HAC-based tests display accurate size control and good power. Newey and West’s (1987) and Andrews’ (1991) prewhitened HAC-based tests are again excessively oversized. Andrews’ (1991) HAC-based test sacrifices some power relative to the DK-HAC-based test even though the margin is not high. For model M3-M4, Table 4-5 show that Andrews’ (1991) HAC-based test also suffers from strong size distortions and power losses, thus sharing the same issues as KVB’s fixed- and EWC-based tests. In model M4, even Newey and West’s (1987) and Andrews’ (1991) prewhitened HAC-based tests are undersized and have relatively low power. The DK-HAC-based tests perform best both in terms of size and power. Table 2-5 suggest that the low frequency contamination can equally arise from different forms of nonstationarity. Overall, the evidence for quite substantial underejection and power losses in model M1-M4 for the existing HAR tests is consistent with our theoretical results. These represent situations where the contamination occurs as a small-sample problem and the ERP is larger for fixed--based HAR tests. In the next section, we show that when the contamination holds asymptotically then the size distortions and power problems can be even more severe.

5.3 General Low Frequency Contamination

We now discuss HAR inference tests for which the low frequency contamination results of Section 3 hold even asymptotically. This means that for all and as . This comprises the class of HAR tests that admit a nonstationary alternative hypotheses. This class is very large and include most HAR tests as discussed in the Introduction. Here we consider the Diebold-Mariano test for the sake of illustration and remark that similar issues apply to other HAR tests.

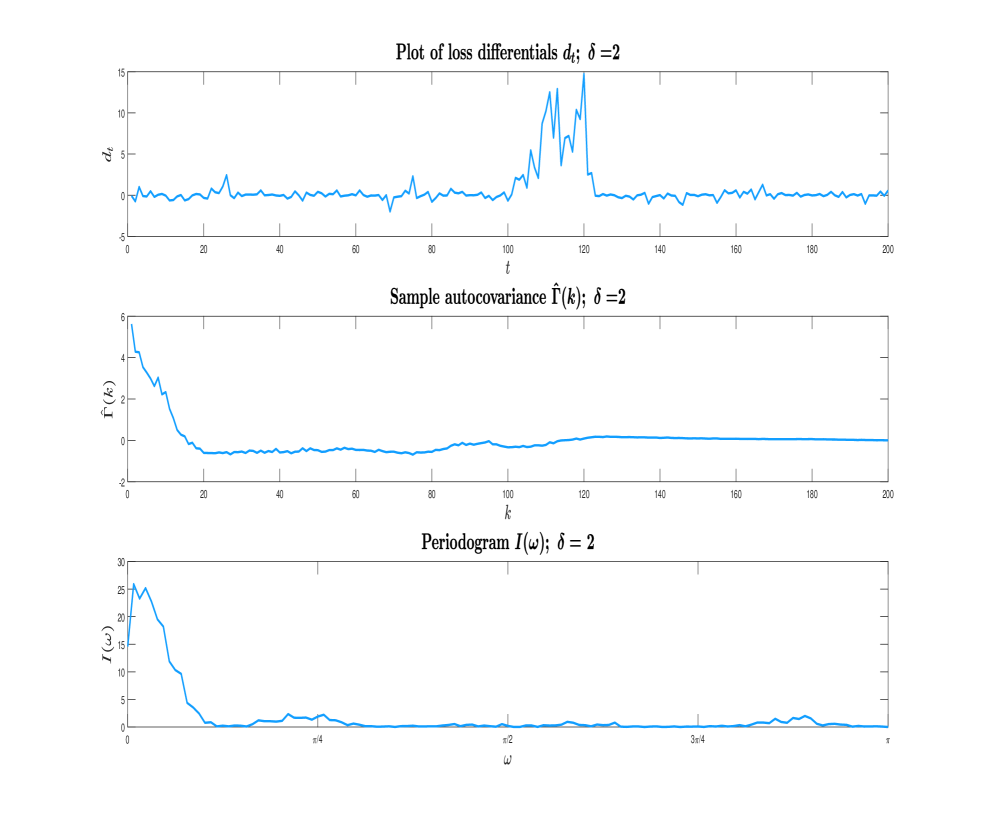

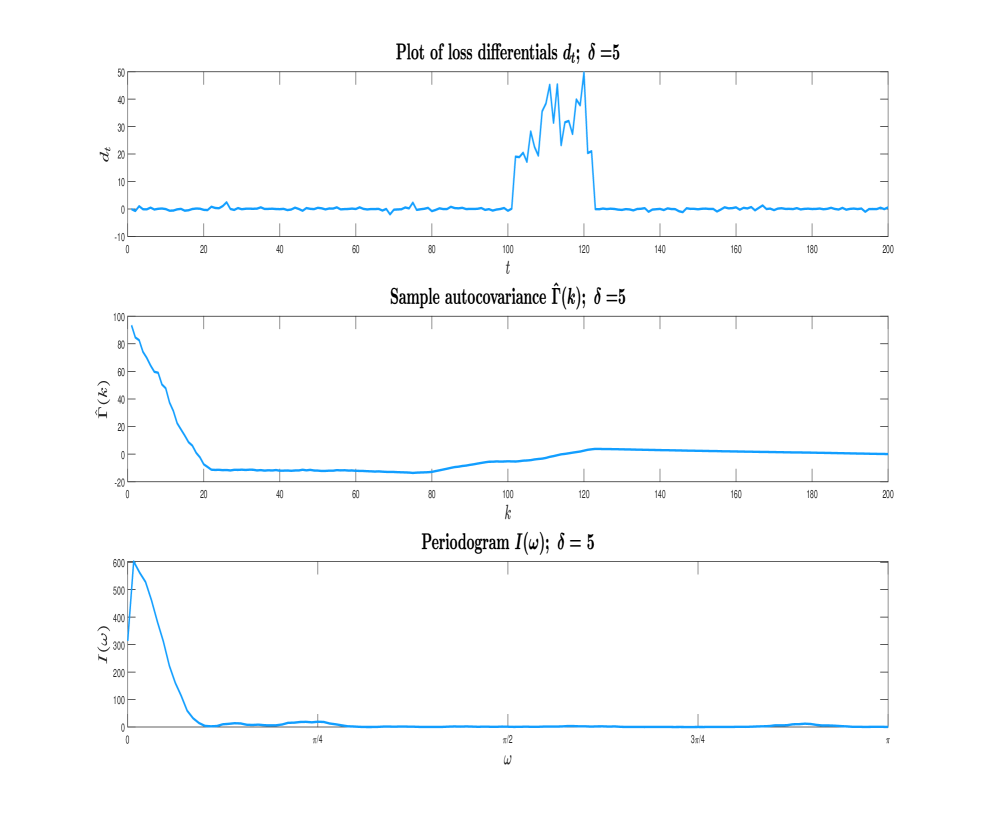

The Diebold-Mariano test statistic is defined as , where is the average of the loss differentials between two competing forecast models, is an estimate of the LRV of the the loss differential series and is the number of observations in the out-of-sample. We use the quadratic loss. We consider an out-of-sample forecasting exercise with a fixed forecasting scheme where, given a sample of observations, observations are used for the in-sample and the remaining half is used for prediction [see Perron and Yamamoto (2021) for recommendations on using a fixed scheme in the presence of breaks]. The DGP under the null hypotheses is given by where , with , and we set and The two competing models both involve an intercept but differ on the predictor used in place of . The first forecast model uses while the second uses where and are independent sequences, both independent from . Each forecast model generates a sequence of -step ahead out-of-sample losses for Then denotes the loss differential at time . The Diebold-Mariano test rejects the null hypotheses of equal predictive ability when is sufficiently far from zero. Under the alternative hypothesis, the two competing forecast models are as follows: the first uses where while the second uses for and for with , where has the same distribution as

We consider four specifications for In the first is subject to an abrupt break in the mean ; in the second is locally stationary with time-varying mean ; in the third specification for and for with ; in the fourth is the same as in the second with in addition two outliers for where where . That is, in the second model is locally stationary only in the out-of-sample, in the third it is locally stationary in both the in-sample and out-of sample and in the fourth model has two outliers in the out-of-sample. The location of the outliers is irrelevant for the results; they can also occur in the in-sample.

Table 6 reports the size and the power of the various tests for all models. We begin with the case (top panel). The size of the test using the DK-HAC estimators is accurate while the test using other LRV estimators are oversized with the exception of the KVB’s fixed- method for which the rejection rate is equal to zero. The HAR tests using existing LRV estimators have lower power relative to that obtained with the DK-HAC estimators for small values of . When increases the tests standardized by the HAC estimators of Andrews (1991) and Newey and West (1987), and by the KVB’s fixed- and EWC LRV estimators display non-monotonic power gradually converging to zero as the alternative gets further away from the null value. In contrast, when using the DK-HAC estimators the test has monotonic power that reaches and maintains unit power. The results for the other models are even stronger. In general, except when using the DK-HAC estimators, all tests display serious power problems. Thus, either form of nonstationarity or outliers leads to similar implications, consistent with our theoretical results.

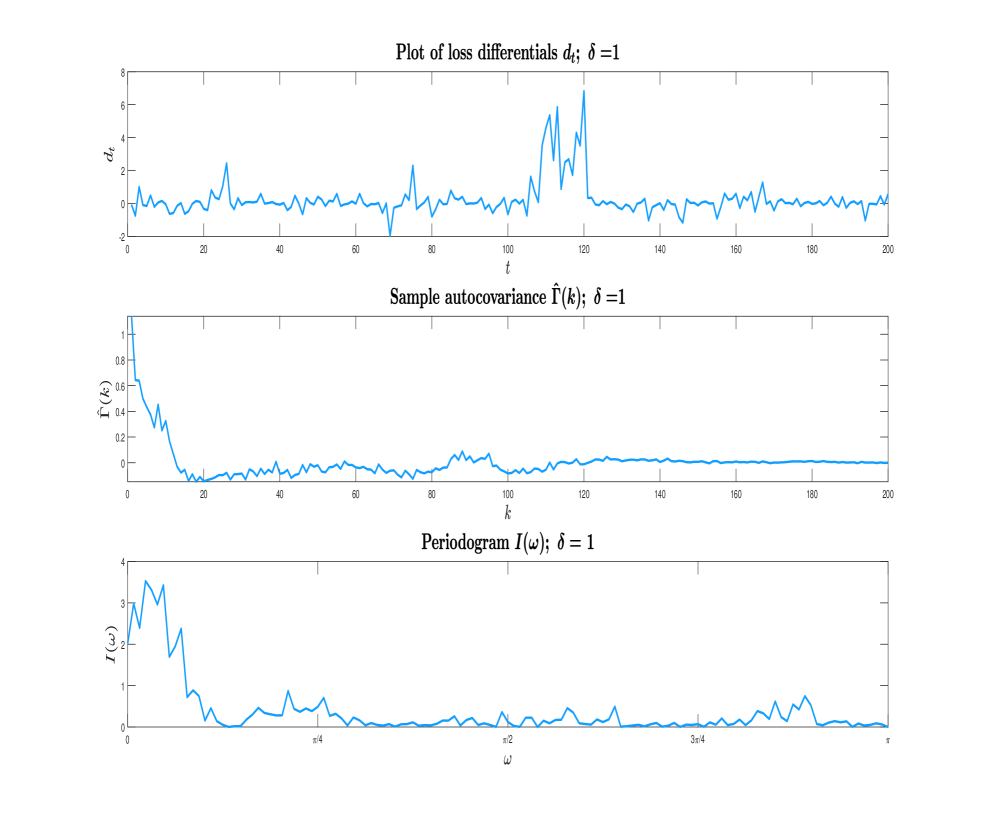

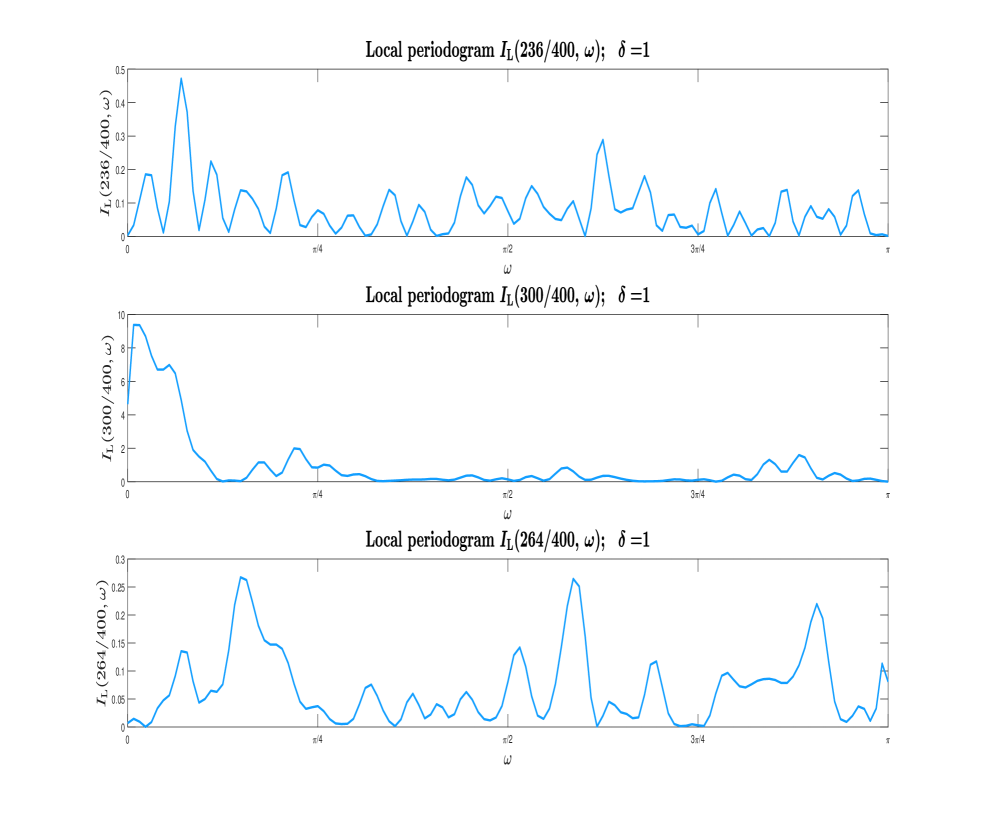

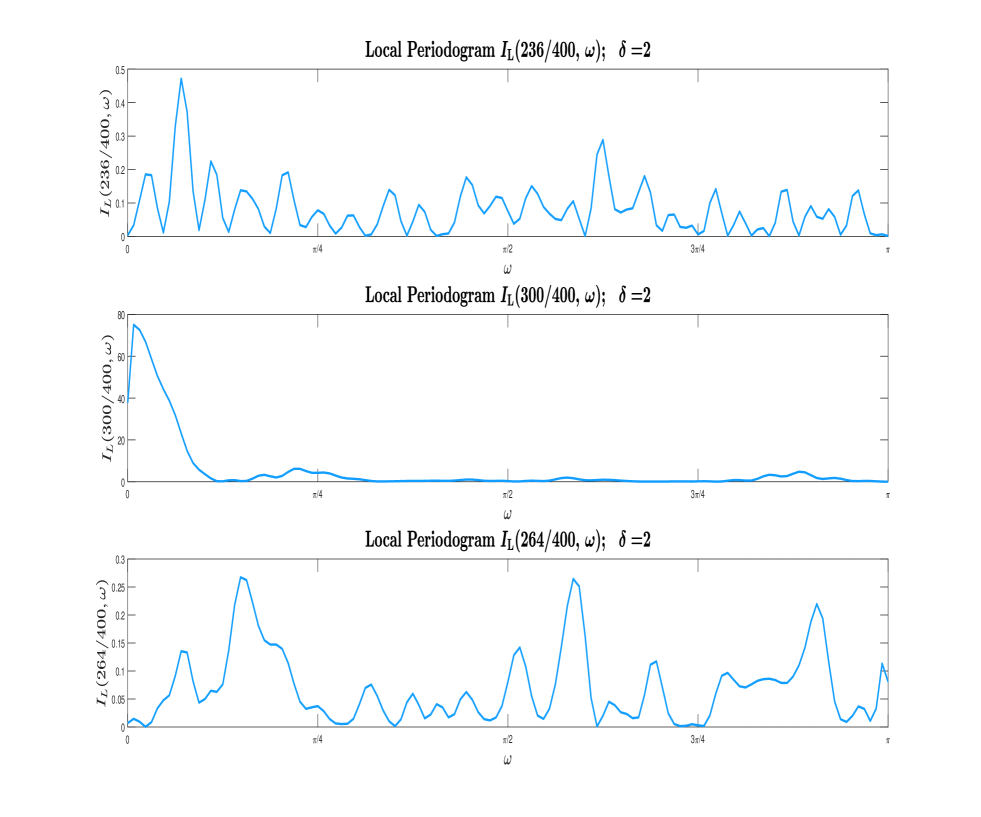

In order to further assess the theoretical results from Section 3, Figure 3 reports the plots of , its sample autocovariances and its periodogram, for . Figure S.1-S.2 in the supplement report the corresponding plots for , respectively. We only consider the case . The other cases lead to the same conclusions. For , Figure 3 (mid panel) shows that decays slowly. As increases, Figure S.1 and S.2 (mid panels), decays even more slowly at a rate far from the typical exponential decay of short memory processes. This suggests evidence of long memory. However, the data are short memory with small temporal dependence. What is generating the spurious long memory effect is the nonstationarity present under the alternative hypotheses. This is visible in the top panels which present plots of for the first specification. The shift in the mean of for is responsible for the long memory effect. This corresponds to the second term of (3.3) in Theorem 3.1. The overall behavior of the sample autocovariance is as predicted by Theorem 3.1. For small lags, shows a power-like decay and it is positive. As increases to medium lags, the autocovariances turn negative because the sum of all sample autocovariances has to be equal to zero [cf. Percival (1992)]. Next, we move to the bottom panels which plot the periodogram of . It is unbounded at frequencies close to as predicted by Theorem 3.2 and as would occur if long memory was present. It also explains why the Diebold-Mariano test normalized by Newey-West’s, Andrews’, KVB’s fixed- and EWC’s LRV estimators have serious power problems. These LRV estimators are inflated and consequently the tests lose power. The figures show that as we raise the more severe these issues and the power losses so that the power eventually reaches zero. This is consistent with our theory since is increasing in (cf. ).

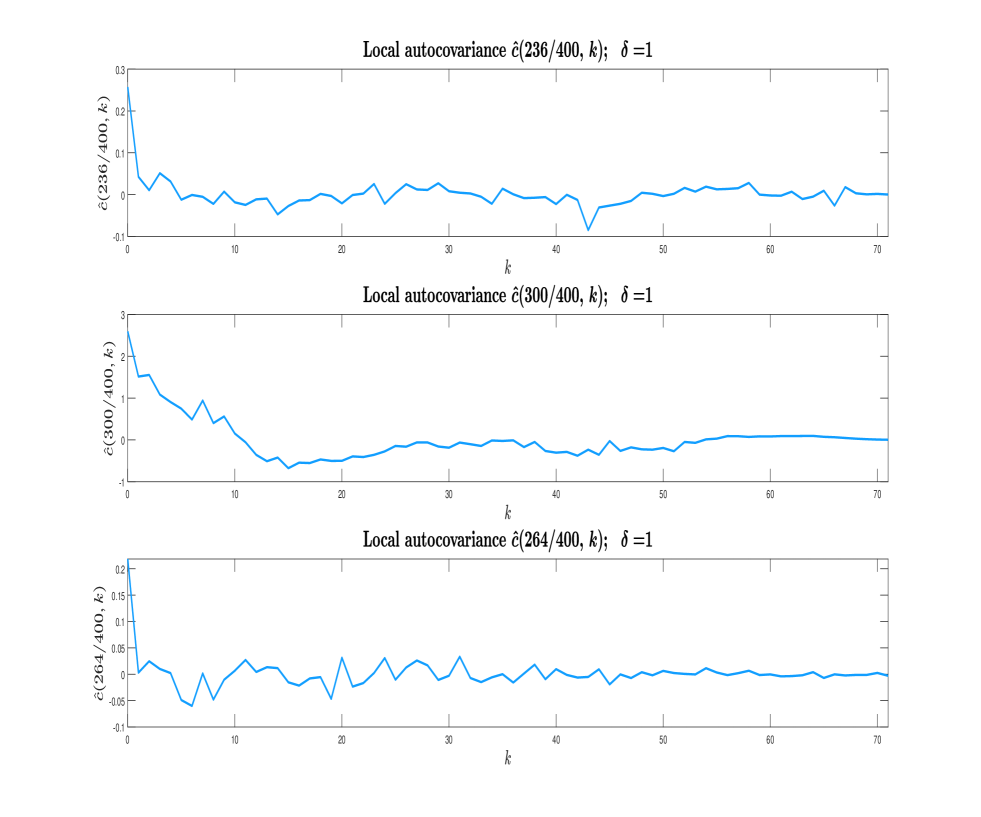

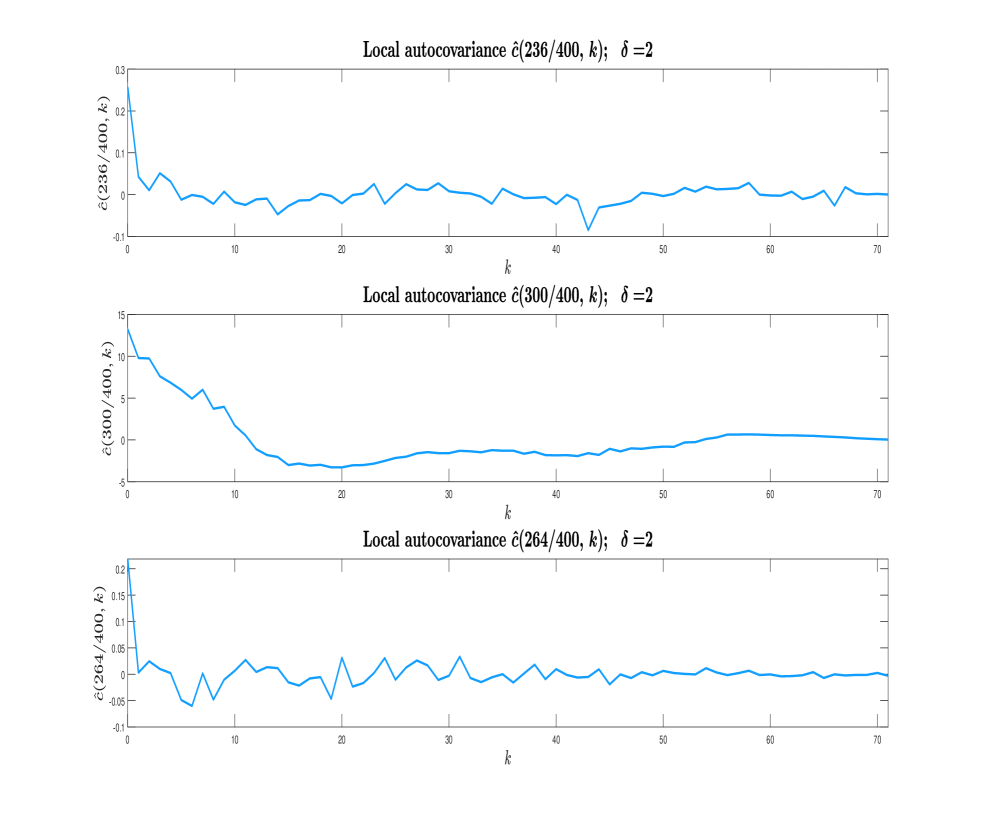

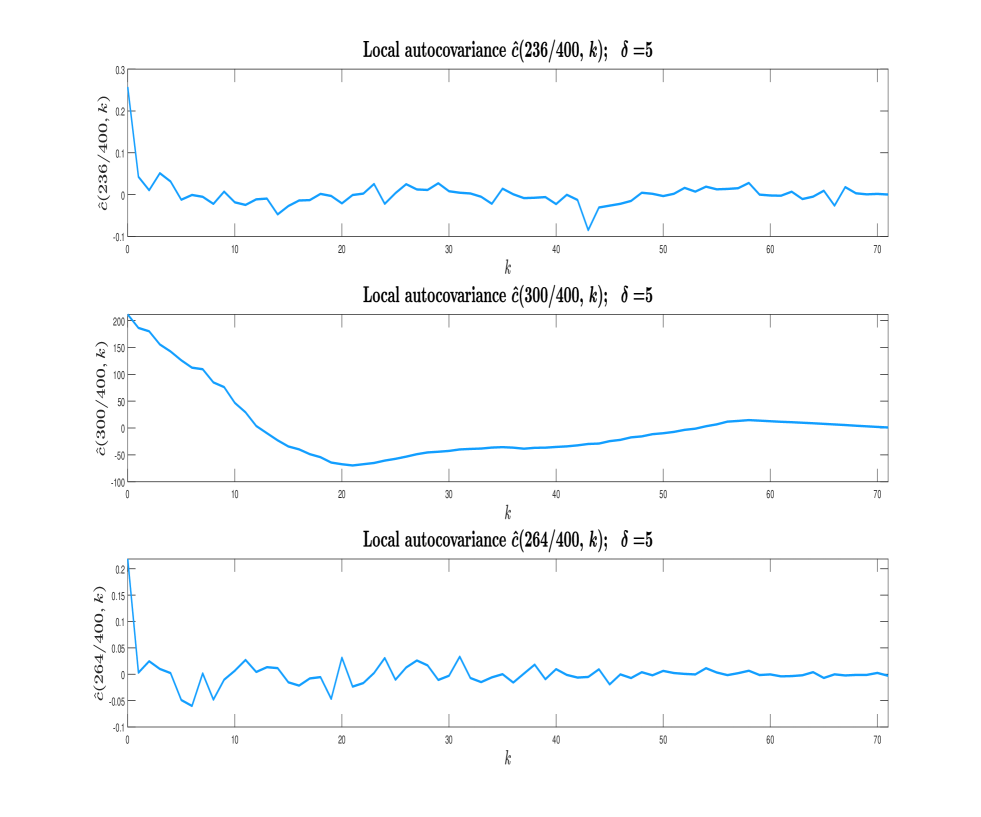

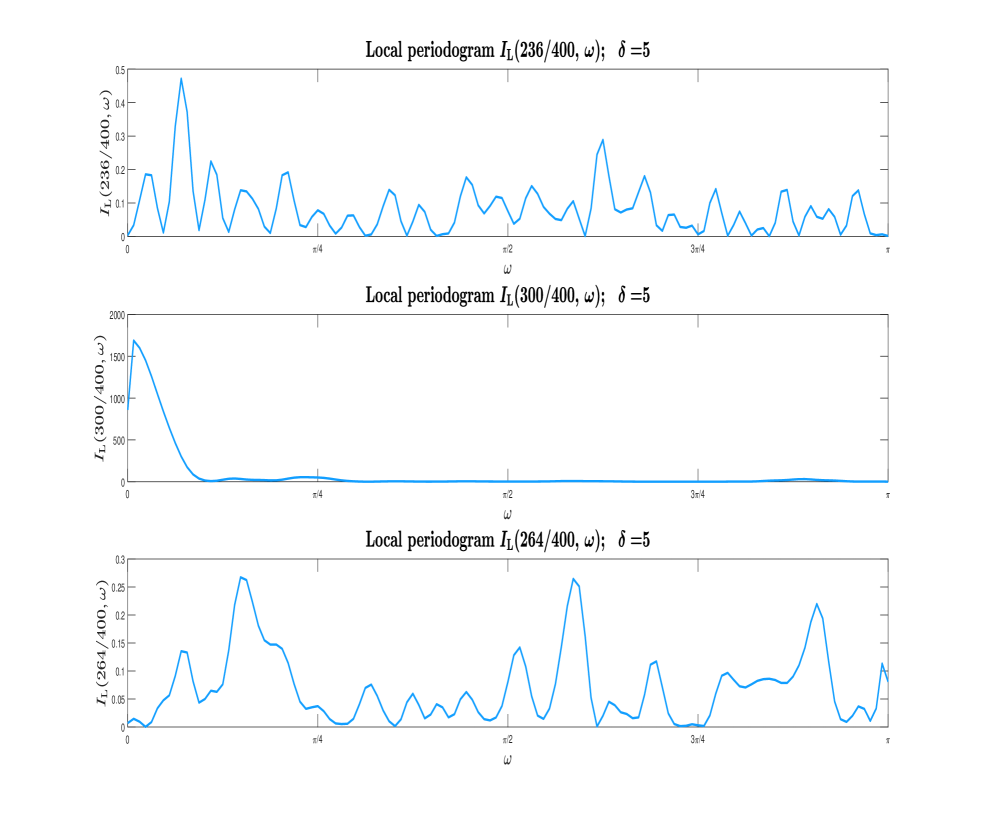

We now verify the results about the local sample autocovariance and the local periodogram from Theorem 3.3-3.4. We set following the MSE criterion of Casini (2021c). We consider (i) , (ii-a) and (ii-b) . Note that cases (i)-(ii-b) correspond to parts (i)-(ii-b) in Theorem 3.3-3.4. We consider and . According to Thereon 3.3-3.4, we should expect long memory features only for case (ii-a). Figure 4-5 and S.3-S.6 in the supplement confirm this. The results pertaining to case (ii-a) are plotted in the middle panels. Figures 4, S.3 and S.5 show that the local autocovariance displays slow decay similar to the pattern discussed above for and that this problem becomes more severe as increases. Such long memory features also appear for . The middle panels in Figure 5, S.4 and S.6 show that the local periodogram at and at a frequency close to are extremely large. The latter result is consistent with Theorem 3.4-(ii-a) which suggests that as . For case (i) and (ii-b) both figures show that the local autocovariance and the local periodogram do not display long memory features. Indeed, they have forms similar to those of a short memory process, a result consistent with Theorem 3.3-3.4 also for cases (i) and (ii-b).

It is interesting to explain why HAR inference based on the DK-HAC estimators does not suffer from the low frequency contamination even if case (ii-a) occurs. The DK-HAC estimator computes an average of the local spectral density over time blocks. If one of these blocks contains a discontinuity in the spectrum, then as in case (ii-a) some bias would arise for the local spectral density estimate corresponding to that block. However, by virtue of the time-averaging over blocks that bias becomes negligible. Hence, nonparametric smoothing over time asymptotically cancels the bias, so that inference based on the DK-HAC estimators is robust to nonstationarity.

5.4 Theoretical Results about the Power

We present theoretical results about the power of for the case of general low frequency contamination discussed in Section 5.3. In particular, we focus on specification (1) (i.e., ). The same intuition and qualitative theoretical results apply to the other specifications of .

Let denote the DM test statistic where , and with and being using the quadratic spectral and Bartlett kernel, respectively. Define the power of as where is the two-sided standard normal critical value and is the significance level. To avoid repetitions we present the results only for and . The results concerning the prewhitening DK-HAC estimator are the same as those corresponding to the DK-HAC estimator while the results concerning the EWC estimator are the same as those corresponding to the KVB’s fixed- estimator. The results pertaining to Andrews’ (1991) HAC estimator (with and without prewhitening) are the same as those corresponding to Newey and West’s (1987) estimator. Let denote the length of the regime in which exhibits a shift in the mean and let be an integer function of with that may depend on .

Theorem 5.1.

Let be a SLS process satisfying Assumption 2.1-(i-iv) and 2.2. Let Assumption 4.3-4.4 hold. Then, we have:

(ii) If , then and

(iii) Under Assumption 4.8, and where is such that as with and .

Note that Assumption 4.7 with refers to the MSE-optimal bandwidth for the Newey and West’s (1987) estimator. The sequence in part (iii) depends on the form of the alternative hypothesis. Theorem 5.1 implies that when the classical HAC estimators or the fixed- LRV estimators are used, the DM test is not consistent and its power converges to zero. The theorem also implies that the power functions corresponding to tests based on HAC estimators lie above the power functions corresponding to those based on fixed-/EWC LRV estimators. This follows from Another interesting feature is that and do not increase in magnitude with because appears in both the numerator and denominator [ enters the denominator through the low frequency contamination term that accounts for the bias in the HAC and fixed- estimators [cf. Theorem 3.1]]. Part (iii) of the theorem suggests that these issues do not occur when DK-HAC estimator is used since the test is consistent and its power increases with and with the sample size as it should be. These results match the empirical results in Table 6 discussed above, thereby confirming the relevance of Theorem 5.1.

5.5 Discussion

In summary, the sample autocovariance and the periodogram are sensitive to nonstationarity in that they may display characteristics typical of long memory when the data are short memory subject to low frequency contamination. In some cases these issues only imply a small-sample problem [cf. Section 5.2]. In others, they have an effect even asymptotically. In either case, the theory in Section 3 provides useful guidance about the properties of the sample autocovariance and the periodogram in finite-samples. It also provides accurate approximations for misspecified models or models with outliers. Since LRV estimates are direct inputs for inference in the context of autocorrelated data, our theory offers new insights for the properties of HAR inference tests. The use of HAC standard errors has become the standard practice, and recent theoretical developments in HAR inference advocated the use of fixed- or long bandwidth LRV estimators on the basis that they offer better size control when there is strong dependence in the data. Our results suggest that care is needed before applying such methods because they are highly sensitive to effects akin to long memory arising from nonstationarity. The concern is then that the use of long bandwidths leads to overestimation of the true LRV due to low frequency contamination. Consequently, HAR tests can dramatically lose power, a problem that occurs also for the classical HAC estimators, though to a lesser extent since they use a smaller number of sample autocovariances.

Our theory also suggests a solution to this problem. This entails the use of nonparametric smoothing over time which avoids combining observations that belong to different regimes. This accounts for nonstationarity and prevents spurious long memory effects.

6 Conclusions

Economic time series are highly nonstationary and models might be misspecified. If nonstationary is not accounted for properly, parameter estimates and, in particular, asymptotic LRV estimates can be largely biased. We establish results on the low frequency contamination induced by nonstationarity and misspecification for the sample autocovariance and the periodogram under general conditions. These estimates can exhibit features akin to long memory when the data are nonstationary short memory. We distinguish cases where this contamination only implies a small-sample problem and cases where the problem remains asymptotically. We show, using theoretical arguments, that nonparametric smoothing is robust. Since the autocovariances and the periodogram are basic elements for HAR inference, our results provide insights on the important debate between consistent versus inconsistent LRV estimation. Our results show that existing LRV estimators tend to be inflated when the data are nonstationarity. This results in HAR tests that can be undersized and exhibit dramatic power losses or even no power. Long bandwidths/fixed- HAR tests suffer more from low frequency contamination relative to HAR tests based on HAC estimators, whereas the DK-HAC estimators do not suffer from this problem.

Supplemental Materials

supplement for online publication [cf. Casini et al. (2021)] introduces the notion of long memory segmented locally stationary processes and contains the proofs of the results in the paper and additional figures.

References

- Altissimo and Corradi (2003) Altissimo, F., Corradi, V., 2003. Strong rules for detecting the number of breaks in a time series. Journal of Econometrics 117, 207–244.

- Andrews (1991) Andrews, D.W.K., 1991. Heteroskedasticity and autocorrelation consistent covariance matrix estimation. Econometrica 59, 817–858.

- Andrews (1993) Andrews, D.W.K., 1993. Tests for parameter instability and structural change with unknown change-point. Econometrica 61, 821–56.

- Andrews and Monahan (1992) Andrews, D.W.K., Monahan, J.C., 1992. An improved heteroskedasticity and autocorrelation consistent covariance matrix estimator. Econometrica 60, 953–966.

- Bai and Perron (1998) Bai, J., Perron, P., 1998. Estimating and testing linear models with multiple structural changes. Econometrica 66, 47–78.

- Belotti et al. (2021) Belotti, F., Casini, A., Catania, L., Grassi, S., Perron, P., 2021. Simultaneous bandwidths determination for double-kernel HAC estimators and long-run variance estimation in nonparametric settings. arXiv preprint arXiv:2103.00060.

- Bentkus and Rudzkis (1982) Bentkus, R.Y., Rudzkis, R.A., 1982. On the distribution of some statistical estimates of spectral density. Theory of Probability and Its Applications 27, 795–814.

- Bhattacharya et al. (1983) Bhattacharya, R., Gupta, V., Waymire, E., 1983. The Hurst effect under trends. Journal of Applied Probability 20, 649–662.

- Bhattacharya and Ghosh (1978) Bhattacharya, R.N., Ghosh, J.K., 1978. On the validity of the formal Edgeworth expansion. Annals of Statistics 6, 434–451.

- Bhattacharya and Rao (1975) Bhattacharya, R.N., Rao, R.R., 1975. Normal Approximation and Asymptotic Expansion. New York: Wiley.

- Brillinger (1975) Brillinger, D., 1975. Time Series Data Analysis and Theory. New York: Holt, Rinehart and Winston.

- Cai (2007) Cai, Z., 2007. Trending time-varying coefficient time series models with serially correlated errors. Journal of Econometrics 136, 163–188.

- Casini (2018) Casini, A., 2018. Tests for forecast instability and forecast failure under a continuous record asymptotic framework. arXiv preprint arXiv:1803.10883.

- Casini (2021a) Casini, A., 2021a. Comment on Andrews (1991) "Heteroskedasticity and autocorrelation consistent covariance matrix estimation". Unpublished Manuscript, Department of Economics and Finance, University of Rome Tor Vergata.

- Casini (2021b) Casini, A., 2021b. The Fixed-b limiting distribution and the ERP of HAR tests under nonstationarity. Unpublished Manuscript, Department of Economics and Finance, University of Rome Tor Vergata.

- Casini (2021c) Casini, A., 2021c. Theory of evolutionary spectra for heteroskedasticity and autocorrelation robust inference in possibly misspecified and nonstationary models. arXiv preprint arXiv:2103.02981.

- Casini et al. (2021) Casini, A., Deng, T., Perron, P., 2021. Supplement to "Theory of low frequency contamination from nonstationarity and misspecification: consequences for HAR inference". arXiv preprint arXiv:2103.01604 .

- Casini and Perron (2019) Casini, A., Perron, P., 2019. Structural breaks in time series, in: Oxford Research Encyclopedia of Economics and Finance,. Oxford University Press.

- Casini and Perron (2020) Casini, A., Perron, P., 2020. Generalized Laplace inference in multiple change-points models. Econometric Theory forthcoming.

- Casini and Perron (2021a) Casini, A., Perron, P., 2021a. Change-point analysis of time series with evolutionary spectra. arXiv preprint arXiv 2106.02031.

- Casini and Perron (2021b) Casini, A., Perron, P., 2021b. Continuous record asymptotics for change-point models. arXiv preprint arXiv:1803.10881.

- Casini and Perron (2021c) Casini, A., Perron, P., 2021c. Continuous record Laplace-based inference about the break date in structural change models. Juornal of Econometrics 224, 3–21.

- Casini and Perron (2021d) Casini, A., Perron, P., 2021d. Minimax MSE bounds and nonlinear VAR prewhitening for long-run variance estimation under nonstattionarity. arXiv preprint arXiv:2103.02235.

- Chan (2020) Chan, K.W., 2020. Mean-structure and autocorrelation consistent covariance matrix estimation. Journal of Business and Economic Statistics, forthcoming.

- Chang and Perron (2018) Chang, S.Y., Perron, P., 2018. A comparison of alternative methods to construct confidence intervals for the estimate of a break date in linear regression models. Econometric Reviews 37, 577–601.

- Chen and Hong (2012) Chen, B., Hong, Y., 2012. Testing for smooth structural changes in time series models via nonparametric regression. Econometrica 80, 1157–1183.

- Christensen and Varneskov (2017) Christensen, B.J., Varneskov, R.T., 2017. Medium band least squares estimation of fractional cointegration in the presence of low-frequency contamination. Journal of Econometrics 97, 218–244.

- Crainiceanu and Vogelsang (2007) Crainiceanu, C.M., Vogelsang, T.J., 2007. Nonmonotonic power for tests of a mean shift in a time series. Journal of Statistical Computation and Simulation 77, 457–476.

- Dahlhaus (1997) Dahlhaus, R., 1997. Fitting time series models to nonstationary processes. Annals of Statistics 25, 1–37.

- Demetrescu and Salish (2020) Demetrescu, M., Salish, N., 2020. (Structural) VAR models with ignored changes in mean and volatility. Unpublished Manuscript, SSRN https://ssrn.com/abstract=3544676.

- Deng and Perron (2006) Deng, A., Perron, P., 2006. A comparison of alternative asymptotic frameworks to analyse a structural change in a linear time trend. Econometrics Journal 9, 423–447.

- Diebold and Inoue (2001) Diebold, F.X., Inoue, A., 2001. Long memory and regime switching. Journal of Econometrics 105, 131–159.

- Diebold and Mariano (1995) Diebold, F.X., Mariano, R.S., 1995. Comparing predictive accuracy. Journal of Business and Economic Statistics 13, 253–63.

- Dou (2019) Dou, L., 2019. Optimal HAR inference. Unpublished Manuscript, Department of Economics, Princeton University.

- Elliott and Müller (2007) Elliott, G., Müller, U.K., 2007. Confidence sets for the date of a single break in linear time series regressions. Journal of Econometrics 141, 1196–1218.

- Giacomini and Rossi (2009) Giacomini, R., Rossi, B., 2009. Detecting and predicting forecast breakdowns. Review of Economic Studies 76, 669–705.

- Giacomini and Rossi (2010) Giacomini, R., Rossi, B., 2010. Forecast comparisons in unstable environments. Journal of Applied Econometrics 25, 595–620.

- Giacomini and Rossi (2015) Giacomini, R., Rossi, B., 2015. Forecasting in nonstationary environments: What works and what doesn’t in reduced-form and structural models. Annual Review of Economics 7, 207–229.

- Giacomini and White (2006) Giacomini, R., White, H., 2006. Tests of conditional predictive ability. Econometrica 74, 1545–1578.

- Granger and Hyung (2004) Granger, C.W.J., Hyung, N., 2004. Occasional structural breaks and long memory with an application to the SP 500 absolute stock returns. Journal of Empirical Finance 11, 399–421.

- Hamilton (1989) Hamilton, J.D., 1989. A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica 57, 357–384.

- Hillebrand (2005) Hillebrand, E., 2005. Neglecting parameter changes in GARCH models. Journal of Econometrics 129, 121–138.

- Ibragimov and Müller (2010) Ibragimov, R., Müller, U.K., 2010. t-statistic based correlation and heterogeneity robust inference. Journal of Business and Economic Statistics 28, 453–468.

- Janas (1994) Janas, D., 1994. Edgeworth expansions for spectral mean estimates with applications to Whittle estimates. Annals of the Institute of Statistical Mathematics 46, 667–682.

- Jansson (2004) Jansson, M., 2004. The error in rejection probability of simple autocorrelation robust tests. Econometrica 72, 937–946.

- de Jong and Davidson (2000) de Jong, R.M., Davidson, J., 2000. Consistency of kernel estimators of heteroskedastic and autocorrelated covariance matrices. Econometrica 68, 407–423.

- Juhl and Xiao (2009) Juhl, T., Xiao, Z., 2009. Testing for changing mean with monotonic power. Journal of Econometrics 148, 14–24.

- Kiefer and Vogelsang (2002) Kiefer, N.M., Vogelsang, T.J., 2002. Heteroskedasticity-autocorrelation robust standard errors using the Bartlett kernel without truncation. Econometrica 70, 2093–2095.

- Kiefer and Vogelsang (2005) Kiefer, N.M., Vogelsang, T.J., 2005. A new asymptotic theory for heteroskedasticity-autocorrelation robust tests. Econometric Theory 21, 1130–1164.

- Kiefer et al. (2000) Kiefer, N.M., Vogelsang, T.J., Bunzel, H., 2000. Simple robust testing of regression hypotheses. Econometrica 69, 695–714.

- Kim and Perron (2009) Kim, D., Perron, P., 2009. Assessing the relative power of structural break tests using a framework based on the approximate Bahadur slope. Journal of Econometrics 149, 26–51.

- Lamoureux and Lastrapes (1990) Lamoureux, C.G., Lastrapes, W.D., 1990. Persistence in variance, structural change, and the GARCH model. Journal of Business and Economic Statistics 8, 225–234.

- Lazarus et al. (2020) Lazarus, E., Lewis, D.J., Stock, J.H., 2020. The size-power tradeoff in HAR inference. Econometrica, forthcoming.

- Lazarus et al. (2018) Lazarus, E., Lewis, D.J., Stock, J.H., Watson, M.W., 2018. HAR inference: recommendations for practice. Journal of Business and Economic Statistics 36, 541–559.

- Martins and Perron (2016) Martins, L., Perron, P., 2016. Improved tests for forecast comparisons in the presence of instabilities. Journal of Time Series Analysis 37, 650–659.

- McCloskey and Hill (2017) McCloskey, A., Hill, J.B., 2017. Parameter estimation robust to low frequency contamination. Journal of Business and Economic Statistics 35, 598–610.

- Mikosch and Stărica (2004) Mikosch, T., Stărica, C., 2004. Nonstationarities in financial time series, the long-range dependence, and the IGARCH effects. Review of Economic and Statistics 86, 378–390.

- Müller (2007) Müller, U.K., 2007. A theory of robust long-run variance estimation. Journal of Econometrics 141, 1331–1352.

- Müller (2014) Müller, U.K., 2014. HAC corrections for strongly autocorrelated time series. Journal of Business and Economic Statistics 32, 311–322.

- Newey and West (1987) Newey, W.K., West, K.D., 1987. A simple positive semidefinite, heteroskedastic and autocorrelation consistent covariance matrix. Econometrica 55, 703–708.

- Newey and West (1994) Newey, W.K., West, K.D., 1994. Automatic lag selection in covariance matrix estimation. Review of Economic Studies 61, 631–653.

- Ng and Perron (1996) Ng, S., Perron, P., 1996. The exact error in estimating the spectral density at the origin. Journal of Time Series Analysis 17, 379–408.

- Ng and Wright (2013) Ng, S., Wright, J.H., 2013. Facts and challenges from the great recession for forecasting and macroeconomic modeling. Journal of Economic Literature 51, 1120–54.

- Otto and Breitung (2021) Otto, S., Breitung, J., 2021. Backward CUSUM for testing and monitoring structural change. arXiv preprint arXiv:2003.02682 .

- Percival (1992) Percival, D., 1992. Three curious properties of the sample variance and autocovariance for stationary processes with unknown mean. The American Statistician 47, 274–276.

- Perron (1989) Perron, P., 1989. The great crash, the oil price shock and the unit root hypothesis. Econometrica 57, 1361–1401.

- Perron (1990) Perron, P., 1990. Testing for a unit root in a time series with a changing mean. Journal of Business and Economic Statistics 8, 153–162.

- Perron and Qu (2010) Perron, P., Qu, Z., 2010. Long-memory and level shifts in the volatility of stock market return indices. Journal of Business and Economic Statistics 28, 275–290.

- Perron and Yamamoto (2021) Perron, P., Yamamoto, Y., 2021. Testing for changes in forecast performance. Journal of Business and Economic Statistics 39, 148–165.

- Phillips (1977) Phillips, P.C.B., 1977. Approximations to some finite sample distributions associated with a first-order stochastic difference equation. Econometrica 45, 463–485.

- Phillips (1980) Phillips, P.C.B.., 1980. Finite sample theory and the distributions of alternative estimators of the marginal propensity to consume. Review of Economic Studies 47, 183–224.

- Phillips (2005) Phillips, P.C.B., 2005. HAC estimation by automated regression. Econometric Theory 21, 116–142.

- Politis (2011) Politis, D.M., 2011. Higher-order accurate, positive semidefinite estimation of large-sample covariance and spectral density matrices. Econometric Theory 27, 703–744.

- Pötscher and Preinerstorfer (2018) Pötscher, B.M., Preinerstorfer, D., 2018. Controlling the size of autocorrelation robust tests. Journal of Econometrics 207, 406–431.

- Pötscher and Preinerstorfer (2019) Pötscher, B.M., Preinerstorfer, D., 2019. Further results on size and power of heteroskedasticity and autocorrelation robust tests, with an application to trend testing. Electronic Journal of Statistics 13, 3893–3942.

- Preinerstorfer and Pötscher (2016) Preinerstorfer, D., Pötscher, B.M., 2016. On size and power of heteroskedasticity and autocorrelation robust tests. Econometric Theory 32, 261–358.

- Qu and Perron (2007) Qu, Z., Perron, P., 2007. Estimating and testing structural changes in multivariate regressions. Econometrica 75, 459–502.

- Qu and Zhuo (2020) Qu, Z., Zhuo, F., 2020. Likelihood ratio based tests for Markov regime switching. Review of Economic Studies 88, 937–968.

- Robinson (1998) Robinson, P.M., 1998. Inference without smoothing in the presence of nonparametric autocorrelation. Econometrica 66, 1163–1182.

- Shao and Zhang (2010) Shao, X., Zhang, X., 2010. Testing for change points in time series. Journal of the American Statistical Association 105, 122–1240.

- Stock and Watson (1996) Stock, J.H., Watson, M.W., 1996. Evidence on structural stability in macroeconomic time series. Journal of Business and Economic Statistics 14, 11–30.

- Sun (2013) Sun, Y., 2013. Heteroscedasticity and autocorrelation robust F test using orthonormal series variance estimator. Econometrics Journal 16, 1–26.

- Sun (2014a) Sun, Y., 2014a. Fixed-smoothing asymptotics in a two-step GMM framework. Econometrica 82, 2327–2370.

- Sun (2014b) Sun, Y., 2014b. Let’s fix it: fixed-b asymptotics versus small-b asymptotics in heteroskedasticity and autocorrelation robust inference. Journal of Econometrics 178, 659–677.

- Sun et al. (2008) Sun, Y., Phillips, P.C.B., Jin, S., 2008. Optimal bandwidth selection in heteroskedasticity-autocorrelation robust testing. Econometrica 76, 175–194.

- Taniguchi and Puri (1996) Taniguchi, M., Puri, M.L., 1996. Valid Edgeworth expansions of M-estimators in regression models with weakly dependent residuals. Econometric Theory 12, 331–346.