Splitting the Sample at the Largest Uncensored Observation

Abstract

We calculate finite sample and asymptotic distributions for the largest censored and uncensored survival times, and some related statistics, from a sample of survival data generated according to an iid censoring model. These statistics are important for assessing whether there is sufficient follow-up in the sample to be confident of the presence of immune or cured individuals in the population. A key structural result obtained is that, conditional on the value of the largest uncensored survival time, and knowing the number of censored observations exceeding this time, the sample partitions into two independent subsamples, each subsample having the distribution of an iid sample of censored survival times, of reduced size, from truncated random variables. This result provides valuable insight into the construction of censored survival data, and facilitates the calculation of explicit finite sample formulae. We illustrate for distributions of statistics useful for testing for sufficient follow-up in a sample, and apply extreme value methods to derive asymptotic distributions for some of those.

keywords:

[class=MSC]keywords:

2103.01337 \startlocaldefs \endlocaldefs

and

1 Introduction

In the analysis of censored survival data, it was long considered an anomalous situation to observe a sample Kaplan-Meier estimator (KME) [7] which is improper, i.e., of total mass less than 1. This occurs when the largest survival time in the sample is censored. In some early treatments it was advocated to remedy this situation by redefining the largest survival time in the sample to be uncensored (cf. Gill [3], p.35). Later it was recognized that one or more of the largest observations being censored conveys important information concerning the possible existence of immune or cured individuals in the population. One aim of the present paper is to focus attention on the importance of considering the location and conformation of the censored observations in the sample.

Even in a population in which no immunes are present, it can be the case that the largest or a number of the largest survival times are censored according to whatever chance censoring mechanism is operating in the population. The possible presence of immunes will be signaled by an interval of constancy of the KME at its right hand end, with the largest observation being censored. The length of that interval and the number of censored survival times larger than the largest uncensored survival time are important statistics for testing for the presence of immunes, and for assessing whether there is sufficient follow-up in the sample to be confident of their presence. We focus particularly on the “sufficient follow-up” issue in the present paper.

Our aim is to derive distributional results that lead to rigorous methods for deciding if the population contains immunes and if the length of observation is sufficient. We proceed by calculating finite sample and asymptotic joint distributions for the largest censored and uncensored survival times under an iid (independent identically distributed) censoring model for the data. These calculations are facilitated by a significant splitting result which states that, conditional on knowing both the value of the largest uncensored survival time and the number of censored observations exceeding this observation, the sample partitions into two conditionally independent subsamples. The observations in each subsample have the distribution of an iid sample of censored survival times, of reduced size, from appropriate truncated random variables. See Theorem 2.1 below for a detailed description of this result.

Using this result we are able to calculate expressions for distributions of statistics, such as those mentioned, related to testing for sufficient follow-up. Those distributions are reported in Section 2. In Section 3 we calculate large sample distributions for the statistics under very general conditions on the tails of the censoring and survival distributions. Special emphasis is placed on the realistic situation where the censoring distribution has a finite right endpoint. These results complement analysis in [10] made under the assumption of an infinite right endpoint. That paper is concerned only with asymptotics whereas in the present paper we have the finite sample distributions in Section 2. With these we can calculate moments of rvs, etc.

A discussion Section 4 contains a motivating example outlining how the results can be applied in practice to validate and improve existing procedures. Proofs for the formulae in Section 2 are in Section 5 and the asymptotic results are proved in Section 6. A supplementary arXiv submission [11] contains plots illustrating some of the distributions in Section 2.

For further background we refer to the book by Maller and Zhou [9] which gives many practical examples from medicine, criminology and various other fields of this kind of data and its analysis. See also the review articles by Othus, Barlogie, LeBlanc and Crowley [12], Peng and Taylor [14], Taweab and Ibrahim [17], Amico and Van Keilegom [1], and a recent paper by Escobar-Bach, Maller, Van Keilegom and Zhao [2].

2 Splitting the Sample: Finite Sample Results

2.1 Setting up: the iid censoring model

We assume a general independent censoring model with right censoring and adopt the following formalism. Assume and are two proper, continuous, cumulative distribution functions (cdfs) on . Let be a parameter. Define the iid sequence of triples , where has distribution , has distribution and is Bernoulli with

For each the components , and are assumed mutually independent. The are censoring variables and the represent lifetimes given that they are finite. Define

Then has distribution given as

| (2.1) |

We allow to be infinite to cater for cured or immune individuals in the population.

The auxiliary unobserved Bernoulli random variable (rv) indicates whether or not individual is immune; (resp., ) indicates that is susceptible to death or failure (resp., immune). When , equivalently , all individuals are susceptible; this is the situation in “ordinary” survival analysis (when all individuals in the population are susceptible to death or failure). We do not observe the so we do not know whether an individual is susceptible or immune. Overall, our model is commonly known as the “mixture cure model”.

Immune individuals do not fail so their lifetimes are formally taken to be infinite. Thus we set when , with being the probability individual is immune. The cdf can be interpreted as the distribution of the susceptibles’ lifetimes.

As is usual in survival data, and essential in our study of long-term survivors, potential lifetimes are censored at a limit of follow-up represented for individual by the random variable . The observed lifetime for individual is thus of the form

| (2.2) |

Immune individuals’ lifetimes are, thus, always censored. The distribution of the is . We also observe indicators of whether censoring is present or absent:

Tail or survivor functions of distributions , , and on are denoted by , , and . We note that

| (2.3) |

and

To connect this formalism with the observed survival data, we think of the as representing the times of occurrence of an event under study, such as the death of a person, the onset of a disease, the recurrence of a disease, the arrest of a person charged with a crime, the re-arrest of an individual released from prison, etc. We allow the possibility that only a proportion of individuals in the population are susceptible to death or failure, and the remaining are “immune” or “cured”.

2.2 Splitting the sample: main structural result

In addition to the notation in the previous subsection, let be the largest observed survival time and let be the largest observed uncensored survival time. Since all with probability 1 we can define in terms of the and by .

To state the splitting result, we adopt the convention that for a non-negative random variable and Borel set with , is a random variable with distribution

| (2.4) |

Our splitting theorem says that the sample partitions into

| (2.5) |

Conditional on knowing that and that censored observations exceed , , consists of iid variables with distribution that of , and consists of iid variables with tail function

| (2.6) |

which is the conditional distribution tail of a censored observation given that it is bigger than . (See Eq. (2.13) in [10].) Furthermore, and are conditionally independent. Note that observed lifetimes less than may be either censored or uncensored but observed lifetimes greater than are necessarily censored.

For further precision in stating the splitting result, we need notation for the numbers of censored observations smaller or greater than , the largest uncensored survival time in the sample. On , let

| (2.7) |

By convention we set

and

On we set . Next, let

| (2.8) |

and when , define

| (2.9) | ||||

| (2.10) |

and

| (2.11) |

On , set . When , we do not define or (and of course there’s no need for a notation like since such a number would always be 0.) Lastly, let

| (2.12) |

We also use the notation , .With these definitions and conventions, on the , and take values in , satisfying and , and we have

The precise statement of the main splitting result is contained in the next theorem and proved in Section 5. Theorem 2.1 also contains the distribution in (2.13) needed for later calculations. Let be the right endpoint of the support of the cdf , and similarly define , and .

Theorem 2.1.

[Splitting the Sample at ] For a sample of size ,

(i) The joint distribution of is, for , ,

| (2.13) | |||

| (2.14) |

Remarks. (i) The case in Theorem 2.1 means no censored observation exceeds , so , and the second component in the statement of the theorem is empty.

When , the first component in the statement of the theorem is empty and all observations are censored except for the smallest which is .

2.3 Finite sample distributions of the maximal times

Theorem 2.1 gives a way to think about censored survival data, especially in the presence of a possible immune component, and provides a route to calculating descriptor distributions such as the joint finite sample distribution of and . Recall that is the right endpoint of the support of .

Theorem 2.2.

[Distributions of and ]

(i) The joint distribution of and is given by

| (2.18) | |||

| (2.19) |

(ii) The distribution of is given by

| (2.20) |

where is the distribution of an uncensored lifetime:

| (2.21) |

Remarks. (i) There is no probability mass outside the region so the distribution in (2.18) equals 1 for , . Likewise the distribution in (2.21) equals 1 for .

Note also that Lines 2 and 3 on the RHS of (2.18) include the value for ; there is mass on the interval , as given by the first line on the RHS of (2.18). Illustrative plots of the distributions of and are in the Supplementary Material to the paper.

(ii) has the distribution of the maximum of iid copies of a rv with distribution on . The distribution has mass at 0 corresponding to all observations being censored. (It may seem pedantic to include these degenerate cases but they are important for checking that distributions are proper (have total mass 1).)

The right extreme of the distribution may be strictly less than ; in fact, we have , as is derived in the proof of Theorem 2.2. No uncensored observation, including the sample maximum of the uncensored observations, can exceed the smaller of and . Note that, in general, . We always have , and ; when , so that , then has total mass 1 and ; when we have , and , with the possibility that .

(iii) has the distribution of the maximum of iid copies of a rv with distribution on ; namely,

| (2.22) |

Also important for statistical purposes are the length of the time interval between the largest uncensored survival time and the largest survival time, and the ratio of those times. For them we have the following distributions.

Theorem 2.3.

[Distributions of and ]

Remarks. (i) Setting in (2.23) we see that the distribution of the difference has mass at 0 of

| (2.28) |

while setting in (2.23) and observing that

| (2.29) |

we can check that the total mass is 1 by doing the integration

| (2.30) | |||

| (2.31) | |||

| (2.32) |

Taking in the second term on the RHS of (2.23) and adding this to the RHS of (2.30) we get 1.

2.4 Distributions of the Numbers

The results in Subsection 2.3 are obtained in Section 5 as special cases of the formulae for the joint distributions of , and which we derive there. That analysis can be expanded to obtain more generally the joint distribution of , , and (and then ). This allows derivation of the joint distribution of , and , variables which are also useful in addressing questions of sufficient follow-up.

We omit the details of this more general analysis here, but give a main result concerning the vector . This vector is not as might be thought at first multinomially distributed, but it is, conditional on the value of . This again illustrates the simplicity of exposition gained by conditioning on . For this result, we need some more notation. Define the functions

| (2.33) | |||||

| (2.34) | |||||

| (2.35) |

which are non-negative and (using (2.29)) add to 1 for each .

Theorem 2.4.

[Distributions of Numbers]

(i) We have for , , , the multinomial probability

| (2.36) | |||

| (2.37) | |||

| (2.38) |

(ii) Consequently, conditional on , the marginal rvs , and are binomial with as the number of trials and success probabilities , and respectively.

(iii) Conditional on , the number of censored observations is Binomial , where .

(iv) Conditional on and , the number is Binomial , where

| (2.39) |

Remarks. Note that we keep in Theorem 2.4, so conditioning on as we do implies , thus , and there is at least one uncensored observation. Thus .

3 Asymptotic Results

In practice, samples of survival data can be large enough that asymptotic methods are appropriate. Equations (2.20) and (2.22) suggest the use of extreme value methods to find limiting distributions of and . For applications we are particularly interested in the cases when and/or have finite right endpoints. In the theorem that follows we assume Type III Weibull extreme value domain of attraction conditions on and , where the extreme value shape parameter is negative (as well as a tail balancing condition in Case 2 of the theorem). We refer to [6] and [15] for general extreme value theory.

Theorem 3.1.

[Asymptotic distribution of

]

Recall we assume that and are continuous distributions.

We have the following limiting distributions in cases of interest.

Case 1: Assume and ,

so that .

Suppose in addition that, as , ,

| (3.1) |

where are positive constants and and are slowly varying as . Then an asymptotic independence property holds for the random variables and , namely, for ,

| (3.2) |

for some deterministic norming sequences and , as .

Case 2: Assume and , so that and . Suppose in addition that, as , ,

| (3.3) |

where and are positive constants and is slowly varying as . Then there exists a deterministic sequence as such that, for ,

| (3.4) |

Case 3: Assume and , so that , and assume the first relation in (3.1) holds. Suppose in addition that, in a neighbourhood of , has a density which is positive and continuous at . Then there exist deterministic sequences and as such that and are asymptotically independently distributed with marginal cdfs, respectively,

| (3.5) |

Further, this result remains true under the same assumptions when , and/or when .

In any of Cases 1–3 we have and as .

Remarks. (i) Under the assumptions of Theorem 3.1, and (in Case 1) or (in Case 3) are asymptotically independent with Weibull distributions, or, as a special case, exponential. The required choices of and are specified in the proof of the theorem.

(ii) A common assumption is of an exponential distribution for lifetime survival: , , , and the uniform distribution for censoring, . This situation, or a close approximation to it, is often the case in practice. See for example Goldman [4], [5], who assumes a scenario of patients being accrued to a trial at random times for a fixed period. The survival distribution is assumed exponential and the censoring is uniform over a known period. These distributions for and constitute very good baseline reference distributions for assessing the practicality of theoretical results.

(iii) When , , we have . Thus satisfies (3.1) with , and , while when is exponential. Case 3 of Theorem 3.1 applies.

(iv) For a complementary asymptotic analysis of and when and have infinite right endpoints and are in the domain of attraction of the Gumbel distribution, see [10]. We note that the Gumbel domain also includes distributions with finite end point.

(v) In Case 3 of Theorem 3.1, the requirement that have a positive density in a neighbourhood of can be replaced with the less restrictive assumption that the quantity , (the mass assigned by to the interval ) is of the form , where , and is slowly varying as . The factor is then replaced with in (3.5). The version in (3.5) is recovered under the assumptions of the theorem when is replaced by and . We omit the details.

3.1 Exact vs Asymptotic

Here we give a small illustration of how the results can be used. We concentrate on Case 3 of Theorem 3.1, the case of insufficient follow-up. Table 1 has the 95% quantiles of the distribution of in (2.23) assuming uniform censoring and a unit exponential survival distribution truncated at (a unit exponential with 99% of its mass below ). Sample sizes of , are listed, with denoting the corresponding quantiles from the asymptotic distribution in (3.5). Values of range from 1 (very heavy censoring, insufficient follow-up) to (lighter censoring, but still insufficient follow-up). Susceptible proportion is .

| 50 | 100 | 500 | 5000 | 20000 | ||

|---|---|---|---|---|---|---|

| 0.528 | 0.401 | 0.198 | 0.067 | 0.034 | 0 | |

| 1.004 | 0.796 | 0.425 | 0.151 | 0.079 | 0 | |

| 1.596 | 1.317 | 0.760 | 0.292 | 0.164 | 0 | |

| 2.293 | 1.954 | 1.224 | 0.438 | 0.319 | 0 | |

| 3.73 | 4.01 | 4.43 | 4.74 | 4.81 | 5.77 | |

| 5.02 | 5.62 | 6.72 | 7.55 | 7.90 | 9.51 | |

| 6.52 | 7.59 | 9.81 | 11.92 | 13.39 | 15.67 | |

| 8.11 | 9.77 | 13.68 | 15.49 | 22.56 | 25.84 |

Upper panel, unscaled, lower panel, scaled.

The upper panel in Table 1 has the unscaled 95% quantiles; in the lower panel is scaled by the factor giving the asymptotic distribution in Theorem 3.1 (the second distribution in (3.5)). The approach to the asymptotic distribution is rather slow but faster when censoring is heavy (small ). In a sample situation we could use estimated distributions in place of those assumed.

4 Discussion: Testing for Sufficient follow-up

Maller and Zhou [9] coin the phrase sufficient follow-up and, based on properties of the KME, specify it to be present in a population when . (A rationale for this is in Sections 2.2 and 2.3 of [9]). To perform a test of this, we assume the contrapositive hypothesis, . This implies that , and for this reason we have emphasised the necessity to include distributions with finite right endpoints in our analyses. Cases 3 and 4 of Theorem 3.1 are especially relevant in this context. Notwithstanding this, distributions with infinite right endpoints (such as, for example, the exponential, Weibull or lognormal) are commonly used in practice to model survival times (and, possibly the censoring times). There may indeed be situations in which an infinite right endpoint is not unrealistic (certain individuals can be strictly immune to a disease, in that they can never catch the disease); in other situations the assumption is a close enough approximation for practical purposes. For a comprehensive theory we need to thoroughly explore both possibilities, as in [2] and [10].

Statistics for testing can be constructed from the number of censored survival times larger than the largest uncensored survival time and/or the length of the interval of constancy of the KME at its right hand end. Consequently we have concentrated on finding the distributions of these and similar quantities as an aid to the development of rigorous statistical methods. Apart from providing foundational results for this purpose, Theorem 2.1 gives strong intuitive insight into the structure of a censored sample.

The importance of developing a reliable test for sufficient follow-up is underscored by a recent study of Liu et al. [8], in which such testing is done on a very extensive scale. Those researchers processed follow-up data files for 11,160 patients across 33 cancer types, calculating median follow-up times as well as median times to event (or censorship) based on the observed times for four endpoints (overall survival, disease-specific survival, disease-free interval, or progression-free interval). They classified all resulting KMEs as having sufficient or insufficient follow-up (or noted cases in which tests were inconclusive) in order to give endpoint usage recommendations for each cancer type. They stress: For each endpoint, it is very important to have a sufficiently long follow-up time to capture the events of interest, and the minimum follow-up time needed depends on both the aggressiveness of the disease and the type of endpoint ([8], p.401). See also Othus et al. ([13], p.1038), who ask for … Further research … to identify tests for adequacy of follow-up.

The test statistics used in [8] are

| (4.1) |

suggested by Maller and Zhou ([9], p.81), and a similarly constructed alternative suggested by Shen [16]. Large values of are associated with sufficient follow-up, thus, provide evidence against . We reject and conclude that follow-up is sufficient if the observed value of exceeds its 95-th percentile calculated under the null.

The results in Section 2 can be used to get expressions for the distribution of . Conditional on the event , the RHS of (4.1) is

| (4.2) |

(with if ). Using Theorem 2.1 and Remark (ii) following it, is conditionally distributed as a Binomial rv, where when . Since we know the joint distribution of and from Theorem 2.2, we can obtain formulae for the previously unknown unconditional distribution of , and for similarly constructed statistics. So our present results open up wide areas of statistical application. We leave further development of these ideas till later.

5 Proofs for Section 2

Recall we assume throughout that and are continuous, including at 0 and at their right extremes if these are finite. Thus the (censored) survival times are all distinct with probability 1.

5.1 Proof of Theorem 2.1

A natural split of the sample into values greater than or less than is exploited to prove Theorem 2.1. We need some notation for sample values less than and greater than . First consider sample values greater than . Fix and let

| (5.1) |

be a censored sample from , where and are two independent sequences of iid positive random variables whose components have distributions the same as

| (5.2) |

(Recall the convention in (2.4)). Analogously, let

| (5.3) |

For sample values less than , fix and let be a sequence of iid positive random variables having distribution

| (5.4) |

Having set up this preliminary notation we can commence to prove the statement in Theorem 2.1. Let and denote arbitrary Borel sets in . Take and and consider

| (5.5) | ||||

| (5.6) |

We can calculate this probability as

| (5.7) | |||

| (5.8) |

In this expression, are unequal integers in , distinct from , and exceeds all of the corresponding , and also ; these are the observations, both censored and uncensored, smaller than . The remaining , of which there are , i.e., those with , are the censored observations exceeding , which is the largest uncensored observation in the sample, and those are in .

On the event in (5.7), and , for . Thus, using exchangeability to renumber the observations conveniently, the probability in (5.7) equals

| (5.10) | |||

| (5.11) | |||

| (5.12) |

Condition on and integrate to rewrite this as

| (5.13) | |||

| (5.14) | |||

| (5.15) |

where we see that the observations greater than are independent of those smaller than it, and recall that and . (Notice that since one or other of or attributes no mass to values exceeding , we can replace and by in any of the integrals such as appear in (5.13).)

The first probability in (5.13) is

| (5.16) |

and the first probability in (5.16) is

| (5.17) | |||

| (5.18) |

(using the notation in (5.3)). The second probability in (5.16) is

| (5.19) | |||

| (5.20) |

Consequently the first probability in (5.13) can be written as

| (5.21) |

Using the notation in (5.4), the second probability in (5.13) can be written as

| (5.22) | |||

| (5.23) |

So we can write (5.13) and consequently (5.5) for as

| (5.26) | |||||

When , (5.5) is interpreted as

| (5.27) | |||

| (5.28) |

We can calculate this probability as

| (5.29) | |||

| (5.30) |

which agrees with (5.26) when if we interpret , the empty set.

Thus we see that (5.26) holds for all with the appropriate interpretations. Choosing and in (5.26) and taking complements gives (2.13), and from (2.13) we have

| (5.31) | |||

| (5.32) | |||

| (5.33) |

for . So (5.26) and consequently (5.5) can be rewritten as

| (5.34) | |||

| (5.35) |

Recalling the definitions in (5.1)–(5.4), this gives (2.15).

Remarks. (i) Conditional on , , , the independent components into which the sample splits are

| (5.36) |

where and , . The cases and are included in Theorem 2.1 with appropriate interpretations, as previously noted.

(ii) We can include the case in Theorem 2.1 by deriving the conditional distribution of the observations given . When all observations are censored in which case the second component in (5.36) contains the whole sample and the first component in (5.36) is empty. By convention we then set . Then we can calculate

| (5.37) | |||||

| (5.38) |

and thus, for ,

| (5.39) |

Dividing (5.37) by (5.39) with gives the required conditional distribution as:

| (5.40) |

The next corollary is required for Remark (ii) following Theorem 2.1. Define integers and , and let be the smallest -field making measurable; and likewise let be the smallest -field making measurable.

Corollary 5.1.

Let be any event in and any event in . Then for any Borel , , ,

| (5.43) | |||||

Proof of Corollary 5.1 For a Borel , , , we have

| (5.44) | ||||

| When , an event in is of the form , where are unequal integers in and is Borel in . Then, on the event , we obtain by writing for in . Similarly, we can formulate and . Using these remarks, (5.44) becomes | ||||

| (5.45) | ||||

where the factorisation of the integrand is justified by Theorem 2.1. Now for

| (5.46) | |||

| (5.47) | |||

| (5.48) |

by Theorem 2.1 again. From this we see that (5.45) equals

| (5.49) |

Comparing the LHS of (5.45) with (5.49) shows that

| (5.50) | |||

| (5.51) |

which is (5.43).

5.2 Proof of Theorem 2.2

Part (i) Keep , and , and calculate, using Theorem 2.1,

| (5.52) | ||||

| (5.53) | ||||

| (5.54) |

where if the second probability on the RHS is taken as 1 and if the first probability on the RHS is taken as 1. The first probability on the RHS of (5.52) also equals 1 when . So, recalling the definition of in (5.3), we get

| (5.55) | ||||

| (5.56) |

Next keep and , and use this together with (2.13) to calculate

| (5.57) | |||

| (5.58) | |||

| (5.59) | |||

| (5.60) | |||

| (5.61) | |||

| (5.62) |

(Observe that .)

Add over in (5.57) and recall (2.29) to get

| (5.63) | |||

| (5.64) | |||

| (5.65) | |||

| (5.66) |

Adding in the value for in (5.39) gives

for , and hence the third line on the RHS of (2.18).

For , take in both sides of (5.63) to get

Adding in the value for in (5.39) gives

(as it should), and hence the second line on the RHS of (2.18).

Part (ii) Taking in the first and third lines on the RHS of (2.18) gives

which is (2.20) in terms of the righthand formula in (2.21). The lefthand formula in (2.21) comes from an integration by parts. For the right extreme of the distribution we have . This is established by checking the behaviour of the second integral in (2.21) in the cases: Case 1, , and (a) , or else (b) ; and Case 2, , in which case , and again we may have, (a) , or else (b) .

5.3 Proof of Theorem 2.3

To prove (2.23), take and write

| (5.68) | |||

| (5.69) |

Decompose the component as

Here . For we calculate

| (5.70) | |||

| (5.71) | |||

| (5.72) | |||

| (5.73) |

Taking in (5.70) we find

| (5.74) |

Further decompose in (5.68) as

By (5.67), . To get , we calculate, for ,

The conditional distribution of given follows from (2.20) and (5.63). For we add . But note that is the same as with set equal to 0, so that is given by (with allowed in ). This verifies (2.23).

5.4 Proof of Theorem 2.4

Here we use the découpage de Lévy (e.g., Resnick [15], p.212), which we used in [10] and which we now review. Relative to a sequence , as specified in Section 2, define random indices and by

| (5.81) | ||||

| (5.82) |

The sequences and , select out the subsequences of uncensored and censored observations, respectively. Note that and . The and are iid with respective distributions

| (5.83) |

for Borel . Both subsequences and are comprised of iid random vectors. Furthermore, the three sequences

| (5.84) |

are independent of each other.

Recall the notations for the numbers , , , and in (2.7)–(2.12) for a sample of size . In calculating (2.36), we have a sample of size and condition on with . This means that there is at least once uncensored observation, so . We index the uncensored observations as and the censored observations as .

Part (i) To prove (2.36) we begin by calculating, for nonnegative integers , with , , and , the probability

| (5.85) |

Substituting for the definitions of the numbers in (2.7)–(2.12) we have to calculate for (5.85) the probability of the event

| (5.86) |

(note that the requirement in (5.85) is redundant because we must have ), conditional on the event

| (5.87) |

Denote the sum in (5.86) by

| (5.88) |

As a result of the découpage in (5.84), the variables in (5.87), having index “”, are independent of those in (5.86), having index “”. So the conditioning event in (5.87) is independent of the event in (5.86). Thus the probability in (5.85) equals . With this notation we can write what we have proved so far as

| (5.89) | |||

| (5.90) |

Rewriting the conditional probability in (5.85) using (5.89), and the fact that on , we obtain

| (5.91) | |||

| (5.92) | |||

| (5.93) | |||

| (5.94) | |||

| (5.95) | |||

| (5.96) |

The first probability on the RHS of (5.91) is by (5.88) a binomial with success probability

where is defined in (2.21) and . Recalling the notation in (2.33), we can thus write

A similar computation gives

Thus the first probability on the RHS of (5.91) equals

| (5.97) |

For the second probability on the RHS of (5.91) we have to carry out a computation similar to that in the proof of Theorem 2.1. We find after some calculation

| (5.98) | |||

| (5.99) |

This is valid for .

As a check on (5.98), adding (5.98) over gives the expression in (2.20) for , and differentiating (2.20) gives a formula for . Now divide the formula for into the corresponding differential of (5.98). (Formally, we calculate Radon-Nikodym derivatives.) Then, recalling (2.33), we arrive at

| (5.100) |

Multiplying (5.97) and (5.100) together and setting gives (2.36).

Part (ii) The binomial distributions are immediate from (2.36).

Part (iii) This also follows directly from (2.36) by a convolution calculation.

Part (iv) For this we use the identity

| (5.101) | |||

| (5.102) | |||

| (5.103) |

Here the numerator equals

for which we can obtain a formula from (2.36), and the denominator is given by the binomial distribution in Part (iii). Then it’s easily verified that (5.101) is a binomial probability with defined as in (2.39).

6 Proof of Theorem 3.1

Take any sequences , , , , and use the identity to write, for any ,

| (6.1) | |||

| (6.2) | |||

| (6.3) | |||

| (6.4) |

Recall we assume throughout that and are continuous distributions.

Case 1: Assume and . Then . Assume also (3.1). For define . Then , , and by the first relation in (3.1), as . Similarly we can choose to satisfy , and then as .

Since we can assume and are large enough for for any . Recognizing this we can use (2.18), (2.20), and (2.22) to express the RHS of (6.1) as

| (6.5) | |||

| (6.6) |

Recall and . Hence by (3.1), the relation , and the slow variation of ,

| (6.7) | |||||

| (6.8) |

Here since . Then by a standard approximation

| (6.9) |

For the term in (6.5) use (2.21), and the mean value theorem for integrals to write

| (6.10) |

where . The slow variation of and imply . Since , the RHS of (6.10) has limit . Thus

| (6.11) |

Now for the integral term in (6.5), subtract from 1 the expression in parentheses, recall that , and , and calculate as follows:

| (6.12) | |||

| (6.13) | |||

| (6.14) | |||

| (6.15) | |||

| (6.16) | |||

| (6.17) |

The last equality comes about because for . After a cancellation and multiplying through by , the last expression takes the form

| (6.18) | |||

| (6.19) |

After integrating by parts and use of the mean value theorem, (6.18) becomes

| (6.20) | |||

| (6.21) |

where . For the same and the expression on the RHS of (6.20) has limit

| (6.22) |

Putting together (6.9), (6.11) and (6.22) and recalling (6.1) and (6.5) gives

and hence the independent distributions in (3.1).

Case 2: Assume and , so that , and . Assume also (3.3). In this case we choose just one norming sequence so that , thus , and the component parts on the RHS of (6.1) can be calculated as

| (6.23) | |||

| (6.24) | |||

| (6.25) |

The asymptotic relations follow from (3.3). Similarly, using (6.10),

| (6.26) |

To deal with the second summand in (6.5) in this case, we have to consider two subcases. We set for this part. Suppose first that . Working from the second line of (6.12), we look at

| (6.27) |

This follows from an integration by parts. Using the mean value theorem, the RHS here is

| (6.28) |

where . Multiplying (6.28) by and letting we obtain the limit on the RHS, and hence

| (6.29) |

Thus, via (6.1), putting together (6.23), (6.26) and (6.29) we get

| (6.30) |

The second subcase is when , so . In this case we use the second line on the RHS of (2.18) to write

Case 3: Assume and keep . In this case . Assume also the first relation in (3.1). Once again we calculate the component parts on the RHS of (6.1). This time we have to scale differently. We take to satisfy and as in Case 1, but set . Then and . Thus is bigger than , ultimately, and, for any , we have hence for large enough.

In place of (6.7) we have, by continuity of , the first relation in (3.1), and the relation ,

| (6.31) |

For the part, modify (6.10) to

| (6.32) | |||

| (6.33) | |||

| (6.34) | |||

| (6.35) |

where . To deal with we used the first relation in (3.1) and to deal with we used the mean value theorem, together with the assumption that, in a neighbourhood of , has a density which is positive and continuous at . Letting with , we get from (6.32) and the slow variation of that

| (6.36) |

Finally, in place of (6.12): for any we have for large enough. Use integration by parts, by (2.3), , and the mean value theorem, to calculate

where . With the previous choices of and we find from this that

| (6.37) | |||

| (6.38) |

Put together (6.31), (6.36) and (6.37) and recall (6.1) and (6.5) to get (3.5).

For this case, we can easily check that all the working so far remains true under the same assumptions when , and for none of it is the value of beyond relevant, so the results hold equally well when .

References

- [1] Amico, M. and Van Keilegom, I. (2018) Cure models in survival analysis. Annual Review of Statistics and Its Application, 5, 311–342.

- [2] Escobar-Bach, M., Maller, R.A., Van Keilegom, I. and Zhao, M. (2020) Estimation of the cure rate for distributions in the Gumbel maximum domain of attraction under insufficient follow-up. Biometrika, to appear.

- [3] R.D. Gill. Censoring and stochastic integrals. Mathematical Centre Tracts, 124, Amsterdam: Mathematisch Centrum, 1980.

- [4] Goldman, A. (1984) Survivorship analysis when cure is a possibility: A Monte Carlo study. Stat. Med., 3, 153–163.

- [5] Goldman, A. (1991) The cure model and time confounded risk in the analysis of survival and other timed events. J. Clinical Epidemiology, 44, 1327–1340.

- [6] de Haan, L. and Ferreira, A. (2006) Extreme Value Theory. Springer, New York.

- [7] Kaplan, E.L. and Meier, P. (1958) Nonparametric estimation from incomplete observations. J. Amer. Statist. Assoc., 53, 457–481.

- [8] Liu, J., Lichtenberg, T., Hoadley, K.A., Poisson, L.M., Lazar, A.J., Cherniack, A.D.. Kovatich, A.J., Benz, C.C., Levine, D.A., Lee, A.V., Omberg, L., Wolf, D.M., Shriver, C.D., Thorsson, V. and Hu, H. (2018) An integrated TCGA pan-cancer clinical data resource to drive high-quality survival outcome analytics, Cell, 173(2), 400–416.

- [9] Maller, R.A. and Zhou, X. (1996) Survival Analysis with Long Term Survivors. Wiley, Chichester.

- [10] Maller, R.A. and Resnick, S.I. (2020) Extremes of censored and uncensored lifetimes in survival data. Under revision for Extremes.

- [11] Maller, R.A., Resnick, S.I. and Shemehsavar, S. (2020) Splitting the sample at the largest uncensored observation. arXiv:2103.01337

- [12] Othus, M., Barlogie, B., LeBlanc, M.L, and Crowley, J.J. (2012) Cure models as a useful statistical tool for analyzing survival. Clinical Cancer Research, 18, 311–342.

- [13] Othus, M., Bansal A., Erba, H., Ramsey, S. (2020) Bias in mean survival from fitting cure models with limited follow-up. Value in Health, 23, 1034–1039.

- [14] Peng, Y. and Taylor, J.M.G. (2014) Cure models. In: Klein, J., van Houwelingen, H., Ibrahim, J.G., and Scheike, T.H., Eds, Handbook of Survival Analysis, Handbooks of Modern Statistical Methods series, Chapter 6. Chapman & Hall, Boca Raton, FL, USA., 113–134.

- [15] Resnick, S.I. (2008) Extreme Values, Regular Variation and Point Processes. Springer, New York. Reprint of the 1987 original.

- [16] Shen, Pao-sheng (2000) Testing for sufficient follow-up in survival data. Statistics & Probability Letters, 49, 313–322.

- [17] F. Taweab and N. A. Ibrahim (2014) Cure rate models: a review of recent progress with a study of change-point cure models when cured is partially known. J. Appl. Sci., 14, 609–616.

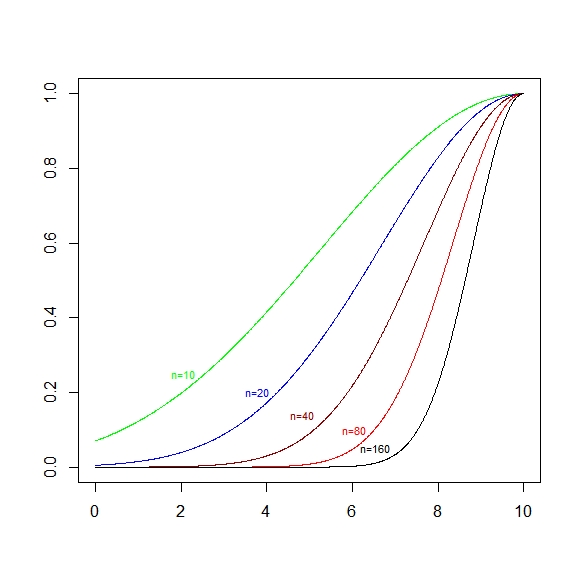

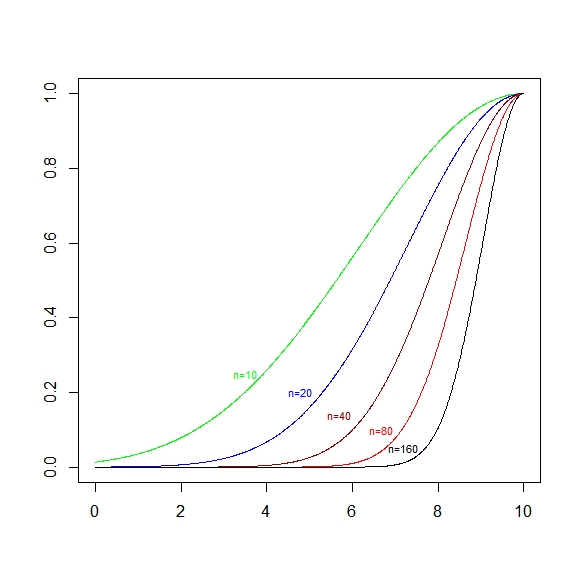

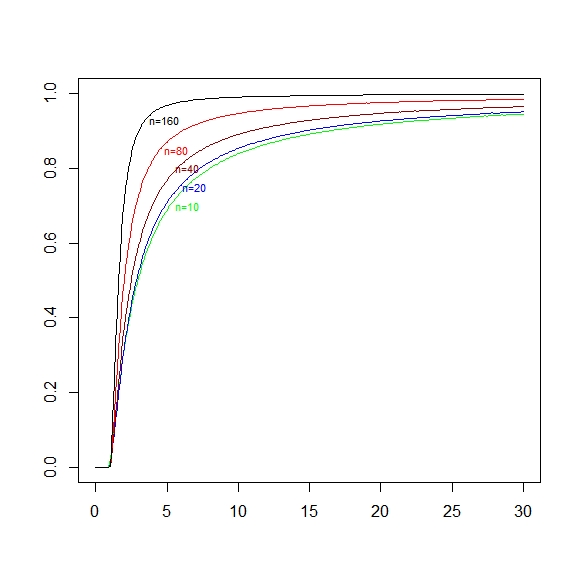

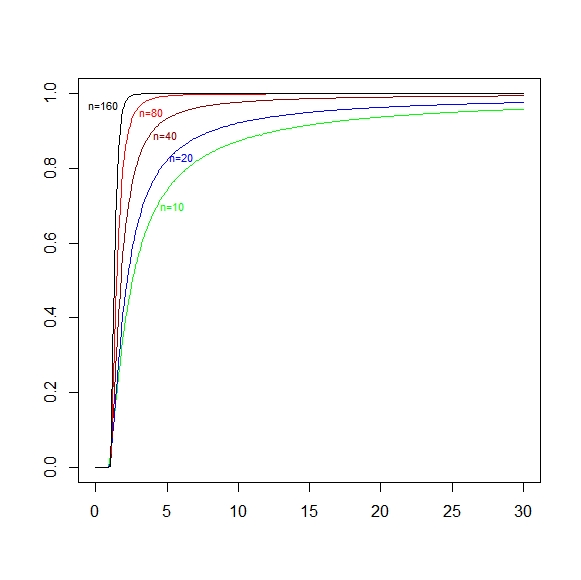

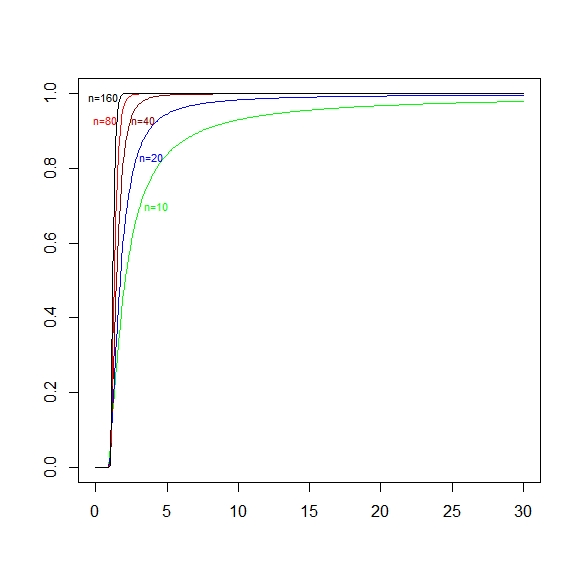

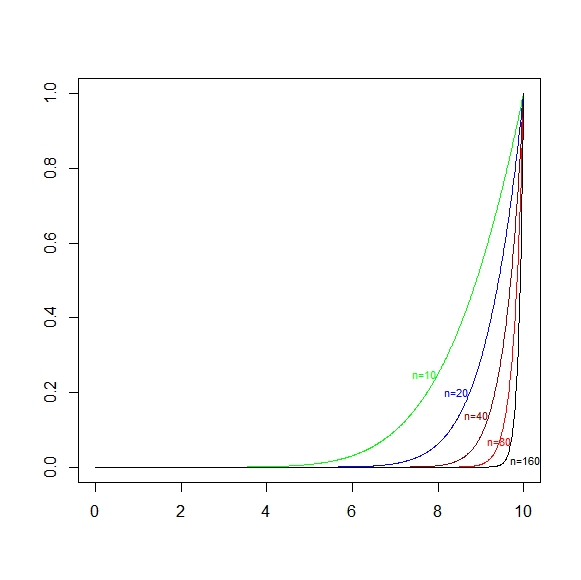

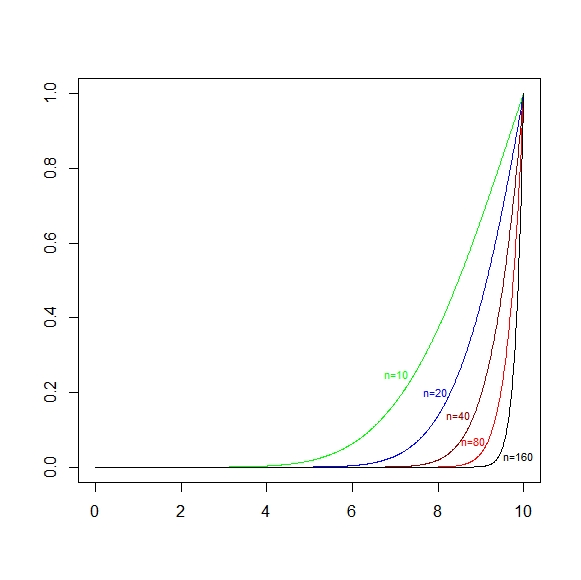

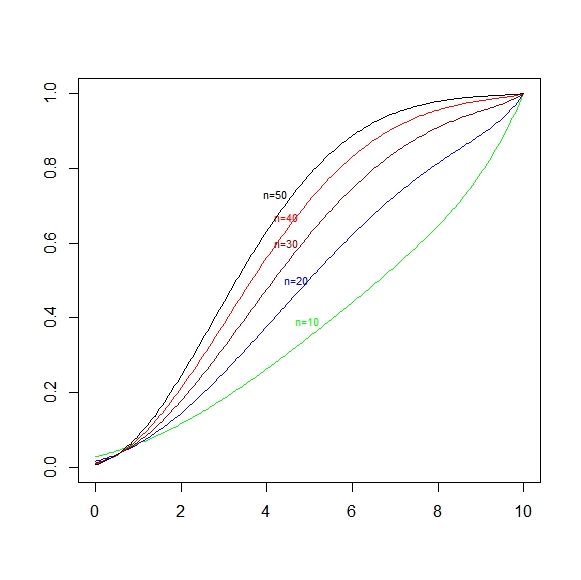

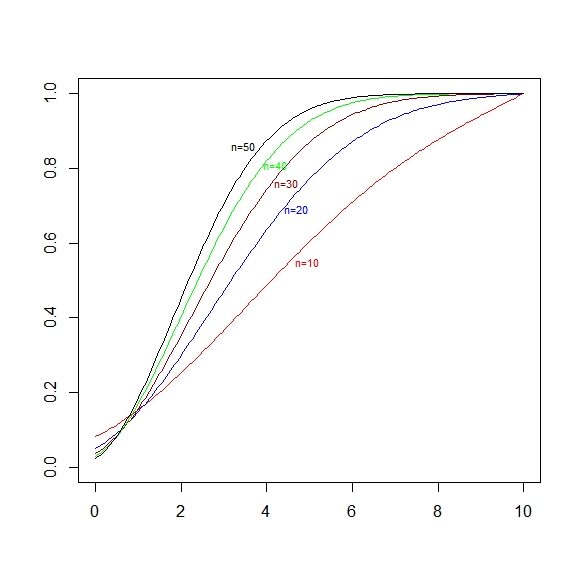

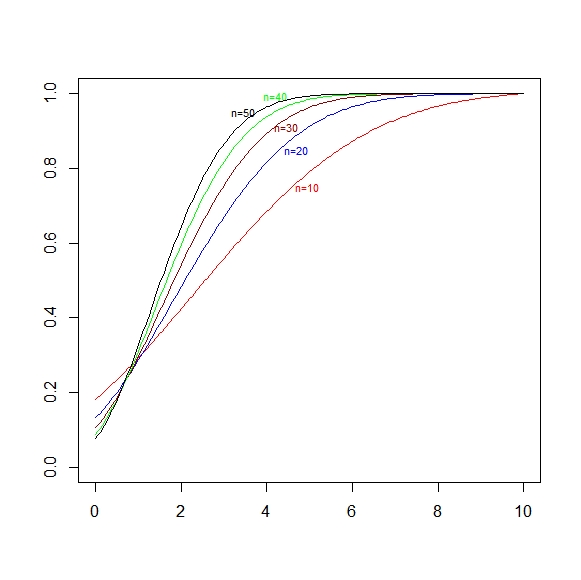

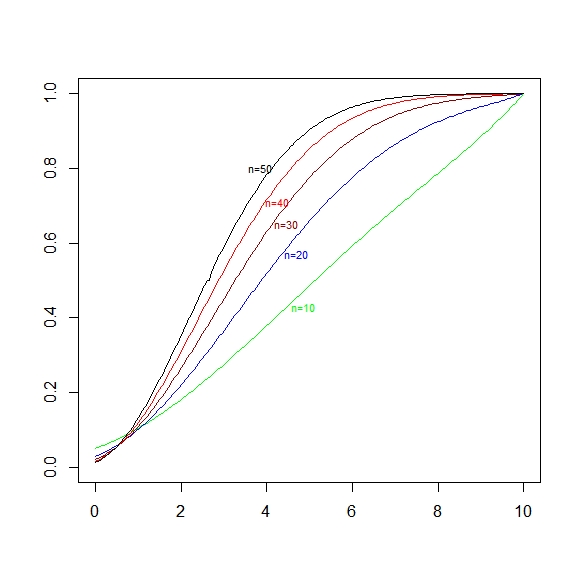

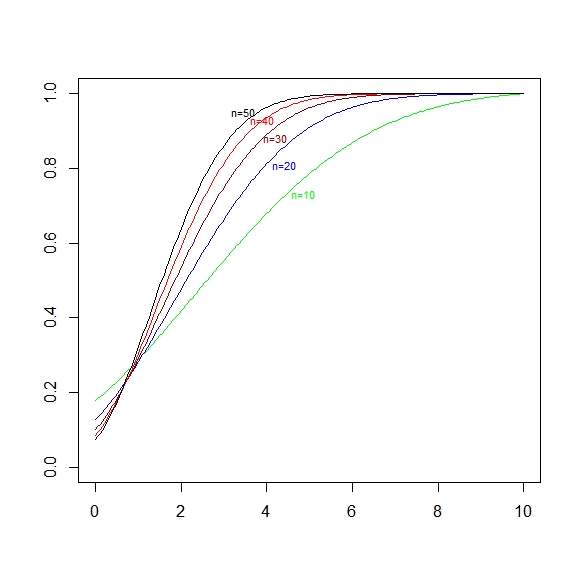

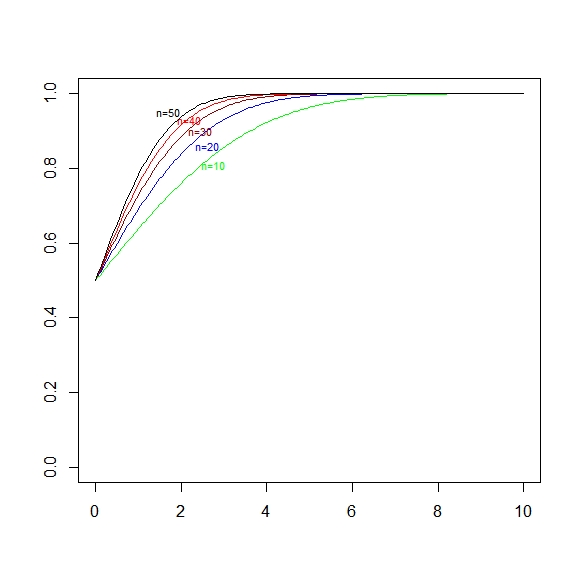

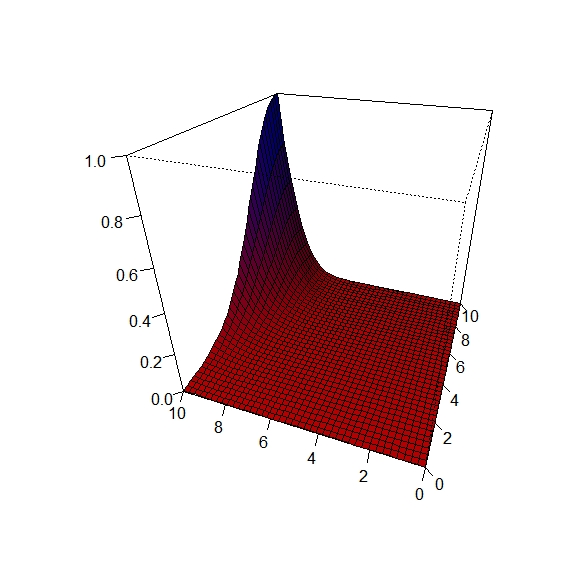

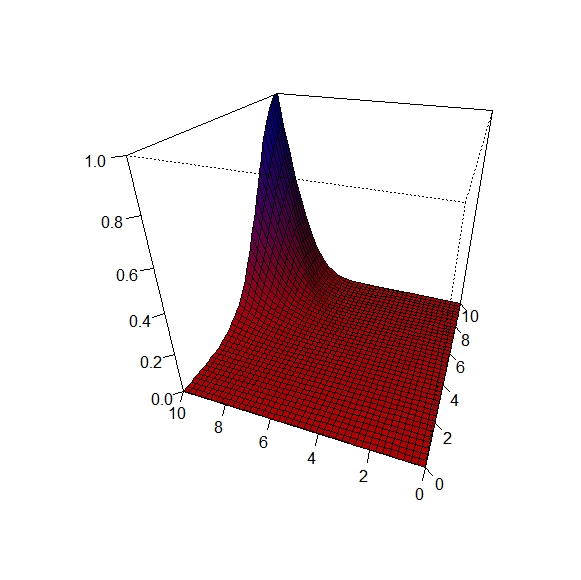

7 Illustrations of cdfs

In this section we plot the cdfs of some of the distributions in Section 2. Most figures have and , with . In this scenario, represents insufficient follow-up, is a marginal case (insufficient), and represents sufficient follow-up. All plots were done using the statistical package R.

, , . Left to right: .