Dynamic covariate balancing:

estimating treatment effects over time with potential local projections111Previous versions are available at

https://arxiv.org/abs/2103.01280.

We thank Isaiah Andrews, Graham Elliott, Jesse Shapiro, Yixiao Sun, Kaspar Wüthrich for continuous feedback. We also thank participants at the 2019 conference of the Institute for Pure & Applied Mathematics, UCSD metrics lunch, Microsoft Research, Stanford, SEA 2022, Econometric NASM 2023, where this paper has been previously presented and Dmitry Arkhangelesky, Guido Imbens, Lihua Lei, Ashesh Rambachan, Jonathan Roth, Pedro Sant’Anna, Jann Spiess in particular for helpful comments. We thank Jake Carlson and Isaac Meza Lopez for excellent research assistance.

The method is implemeted in the R package DynBalancing.

All mistakes are our own.

First version: March, 2021)

Abstract

This paper studies the estimation and inference of treatment histories in panel data settings when treatments change dynamically over time. We propose a method that allows for (i) treatments to be assigned dynamically over time based on high-dimensional covariates, past outcomes, and treatments; (ii) outcomes and time-varying covariates to depend on treatment trajectories; (iii) heterogeneity of treatment effects. Our approach recursively projects potential outcomes’ expectations on past histories. It then controls the bias by balancing dynamically observable characteristics. We study the asymptotic and numerical properties of the estimator and illustrate the benefits of the procedure in an empirical application.

Keywords: Causal Inference, Local Projections, High Dimensions, Treatment Effects, Panel Data.

JEL Code: C10.

1 Introduction

Researchers collect a panel of independent observations observed over a finite number of periods in an observational study. The dataset encompasses time-varying covariates, outcomes, and time-varying treatments. The primary objective is to conduct inference on the average effect of exposure to different treatment histories, such as the effect of being treated for a certain number of periods.

The first challenge is that treatments change dynamically over time. In a survey of all articles in 2021 top-5 economics journals, more than of studies with time-varying treatments exhibit treatment dynamics, a figure similar in magnitude to the number of papers utilizing Difference-in-Differences (DiD) designs ().444This is based on the authors’ calculation. Top-5 economics journals are American Economic Review, Econometrica, Journal of Political Economy, Quarterly Journal of Economics, Review of Economic Studies. Recent work has extended DiD or related methods for when potential outcomes depend on a treatment path (see De Chaisemartin and d’Haultfoeuille, 2022; Roth et al., 2023), but these approaches require parallel trends across groups with different treatment paths. If units can dynamically choose treatments in response to their previous outcomes (or treatments), this will lead to violations of the parallel trends assumption (Ghanem et al., 2022; Marx et al., 2022). We, therefore, introduce an approach that is valid when treatment decisions at period can depend on the history of outcomes and treatments prior to . The second challenge is that treatment dynamics are difficult to estimate. Individuals may select into treatment arbitrarily based on high-dimensional covariates, outcomes, and treatments, e.g., when maximizing future expected utilities (Heckman and Navarro, 2007). This motivates a method that does not impose modeling assumptions on selection into treatment mechanisms (i.e., propensity score).

This paper studies the estimation and inference of the effects of treatment histories when potential outcomes (and covariates) depend on present and past treatments. Individuals dynamically select into treatment based on past (time-varying) covariates, outcomes, and treatments. There are no unobserved confounders after controlling for high-dimensional past characteristics (Ding and Li, 2019). Researchers remain agnostic on the propensity score.

We leverage a model on the potential outcomes’ conditional expectations as an (approximately) linear function of previous potential outcomes and (high-dimensional) covariates in each period. Our model is motivated by local projection frameworks (Jordà, 2005; Montiel Olea and Plagborg-Møller, 2021). Local projections impose a (linear) model on observed outcomes conditional on each period observables and do not require estimating how each time-varying covariate changes in response to treatments – which would be prone to large estimation error in high dimensions. However, different from standard local projections, our model is imposed on expected potential instead of observed outcomes. This difference is important here because of treatments’ serial correlation and selection into treatment based on past outcomes and covariates: a model on realized outcomes imposes restrictions on the distribution of the treatment assignments, whereas a potential outcome model does not. Building on the literature on marginal structural models (Robins et al., 2000), we identify the parameters of interest by recursively projecting outcomes’ conditional expectations over past histories, allowing for dynamic selection into treatment.

Our estimation method, Dynamic Covariate Balancing (DCB), estimates the parameters of the model by using recursive penalized projections through lasso (Hastie et al., 2015). It then reweights observations to guarantee balance between treated and control units. Balancing covariates is intuitive and common in practice: in cross-sectional studies, treatment, and control units are comparable when the two groups have similar characteristics (Imai and Ratkovic, 2014; Li et al., 2018; Hainmueller, 2012). We generalize covariate balancing in the absence of dynamics of Zubizarreta (2015); Athey et al. (2018); Ben-Michael et al. (2018); Hirshberg and Wager (2017) to a dynamic setting. We show that balancing with potential local projections corresponds to constructing weights sequentially in time by first balancing treated and control units’ covariates in the first period and then balancing histories in the next periods reweighted by the weights obtained in the previous period. The estimated balancing weights solve a sequence of quadratic programs to minimize the weights’ variance.

Our estimation procedure guarantees a vanishing bias of order faster than and a parametric rate of convergence of the estimated treatment effect in high-dimensional settings. In addition, the optimization problem over the set of balancing weights admits a feasible solution, with the true propensity score being one such solution (and without requiring knowledge of it). This result highlights the benefits of balancing over propensity score reweighting here: the proposed balancing weights have a smaller variance than inverse probability weights and – by leveraging an (approximate) high-dimensional linear outcome model – do not require the correct specification of the propensity score.555Typical methods in high dimensions require conditions on the product of the rates of estimators for the propensity score and coefficients of the linear model to be faster than , and also require consistent estimation of both the outcome model and propensity score model (what known as rate-doubly robustness, see e.g., Athey and Wager, 2021). Compared to estimating the propensity score with a semi-parametric model, our guarantees do not depend on the estimation error of the propensity score (only require that the estimation error of the coefficients is ), by leveraging the high dimensional linear outcome model. This is an advantage especially in dynamic settings: the propensity score defines the joint probability that units are assigned to a given treatment history, and therefore inverse probability weights can exhibit large variance in finite sample (see e.g., Figure 9). Finally, we provide guarantees for inference. Relative to cross-sectional studies, our dynamic structure necessitates novel considerations for identification, balancing, and derivations, that require analyzing joint distributions of correlated residuals from sequential projections.

We illustrate our method in an empirical application using data from Acemoglu et al. (2019) on studying the effects of democracy on economic growth. Here, the authors assume a dynamic selection model. Whereas effects are in magnitude and sign consistent with Acemoglu et al. (2019), we show that standard local projections and Acemoglu et al. (2019)’s linear regression lead to significantly smaller point estimates compared to our approach. We also show that (A)IPW methods lead to a more substantial imbalance (and bias) compared to DCB due to the instability of the propensity score in both high and low-dimensions.

Our problem connects to the literature on DiD methods, local projections, and dynamic treatments. We provide a formal comparison in Section 2.4 and an overview below.

Different from the literature on DiD (Roth, 2022; Rambachan and Roth, 2023; Imai and Kim, 2016; Goodman-Bacon, 2021; de Chaisemartin and d’Haultfoeuille, 2019; Callaway and Sant’Anna, 2019; Abraham and Sun, 2018; Athey and Imbens, 2022), here we allow for dynamic selection into treatment, violated under parallel trends assumed in this literature (Marx et al., 2022; Ghanem et al., 2022). Different from the time-series literature (Plagborg-Møller, 2019; Montiel Olea and Plagborg-Møller, 2021; Stock and Watson, 2018), this paper uses information from panel data and allows for arbitrary dependence of outcomes, covariates, and treatment assignments over time. This difference motivates the recursive identification and estimation strategy proposed here. For instance, in the context of local projections, Rambachan and Shephard (2019) show that the causal interpretability of local projections relies on independent assignments over time. Here, we consider serially correlated treatments that depend on past outcomes. Finally, in a more recent work Dube et al. (2023) study local projections with DiD designs. Different from the current paper, the authors do not consider recursive projections or balancing methods, and they assume parallel trends.

Our paper provides the first dynamic balancing equations under a local projection model. In econometrics, Arkhangelsky and Imbens (2019) propose balancing assuming no treatment dynamics, whereas here, treatment dynamics require different (and novel) balancing conditions. In the statistics literature, we generalize balancing in static settings (e.g. Ben-Michael et al., 2018) to dynamic settings. In the context of dynamics, different from Imai and Ratkovic (2015), who estimate a single set of balancing weights over all possible combinations of time periods and covariates, here the number of moment conditions grows linearly with and not exponentially. Unlike Zhou and Wodtke (2018), who extend entropy balancing of Hainmueller (2012) to dynamic settings, we do not estimate one model for each covariate in the past (which is prone to large estimation error in high dimensions). DCB explicitly characterizes the high-dimensional model’s bias in a dynamic setting to avoid overly conservative moment conditions, while Kallus and Santacatterina (2018) design conservative balancing conditions for the worst-case bias. Different from Yiu and Su (2018), we do not require estimating the propensity score. Our insight with respect to all these references (both for high and low dimensional settings) is that by leveraging a potential local projection model and computing balancing weights sequentially, balancing reduces to few and easy-to-compute dynamic restrictions. This insight is even more relevant with high-dimensional covariates, which none of these references study for dynamic treatments.

Our approach connects to the literature on dynamic treatments. A typical approach in the dynamic treatment literature is to estimate a dynamic choice model, i.e., propensity score (e.g. Heckman and Navarro, 2007; Heckman et al., 2016). Here, we leverage the potential outcome model to estimate treatment effects consistently without necessitating consistent estimation of the treatment assignment mechanism. References in bio-statistics include Robins (1986), Robins et al. (2000), Hernán et al. (2001), Boruvka et al. (2018), Blackwell (2013), Bang and Robins (2005) (for a review, Vansteelandt et al., 2014). Bojinov and Shephard (2019), Bojinov et al. (2020) study IPW estimators from a design-based perspective.

Doubly robust estimators for dynamic treatments have been studied by Nie et al. (2021); Zhang et al. (2013); Jiang and Li (2015); Tchetgen and Shpitser (2012); Babino et al. (2019). These methods use information from the estimated propensity score. Therefore, in high dimensions, they are sensitive to the misspecification of the propensity score (e.g., Farrell, 2015). Similarly, in studies regarding high-dimensional panel data, researchers require correct specification of the propensity score (Lewis and Syrgkanis, 2020; Zhu, 2017; Shi et al., 2018; Chernozhukov et al., 2018; Bodory et al., 2020; Belloni et al., 2016; Chernozhukov et al., 2017), or impose homogeneous treatment effects (Krampe et al., 2020; Kock and Tang, 2015) (Lewis and Syrgkanis (2020) also provide bounds on how misspecification of the propensity score affect rates of convergence). Bodory et al. (2020) propose doubly robust estimators that leverage product of rates assumptions (and consistent estimation of the propensity score). More generally, prior works that formally study properties of dynamic AIPW methods in high dimensions require product of rates conditions for the estimated propensity score and conditional mean function, and consistent estimation of both. The reader may refer to follow-up work of Bradic et al. (2021), who provide an extensive study of doubly-robust methods under these conditions in high dimensions. Different from all these references, our framework does not require consistent estimation of the propensity score, relevant, for example, when individuals select into treatment when maximizing an unobserved utility function. Finally, in work subsequent to the current paper, Chernozhukov et al. (2022) generalize balancing with dynamics for arbitrary influence functions, allowing for non-linear outcome models. Our focus on the potential local projection model is motivated by its wide use in applications.

2 Dynamics and potential local projections

This section introduces the setup and main assumptions in the presence of two time periods. We extend our framework to multiple time periods in Section 4.1.

Researchers observe a panel with copies of a random vector666In practice, the panel can be either balanced or unbalanced. See Section 5.

where are binary treatments at time , respectively, denote covariates and the outcome at time . We allow for arbitrary nonstationarity and dependence over time for a given unit. Whenever we omit the index (e.g., writing ), we refer to the vector of observations for all units. Covariates, treatments and outcomes realize as in Figure 1. We refer to and as vectors of ones and zeros of dimension .

2.1 Estimand

Potential outcomes are functions of the entire treatment history. Define the potential outcome at time , under treatment in the first period and in the second period. Our goal is to conduct inference on the estimand(s)

for given treatment histories . For example, researchers may be interested in estimating which denotes the total effect of treating an individual for two consecutive periods (Athey and Imbens, 2022); or the direct effect , which denotes the effect of increasing the treatment in the first period only. Our framework allows for generic for arbitrary histories . Figure 2 shows that the treatment effects typically capture two sources of dynamics: the direct effect of the treatment on the outcomes and the indirect effect through intermediate covariates and outcomes.

2.2 Sequential selection into treatment

Treatment histories may affect (intermediate) outcomes and covariates. Let be the intermediate potential outcome and potential covariates for a treatment history . Here, denotes baseline covariates.

Assumption 1 (No Anticipation).

For , let (i) , and (ii) .

Assumption 1 has two implications: (i) intermediate potential outcomes only depend on past but not future treatments; (ii) the treatment status at has no contemporaneous effect on covariates.777No anticipation was first introduced in duration models in Abbring and Van den Berg (2003). Assumption 1 allows for anticipatory effects governed by expectations (Heckman and Navarro, 2007) (e.g., individuals may select into treatment based on expected future utilities), but it prohibits anticipatory effects based on the future treatment realizations (see Bojinov and Shephard, 2019; Athey and Imbens, 2022, for a discussion). Also, Assumption 1 does not impose restrictions on treatments .

Example 2.1 (Observed outcomes).

In the rest of our discussion, we index potential outcomes and covariates by past treatment history under Assumption 1. We define the vector of past treatment assignments, covariates, and outcomes in the previous period. We refer to

as the potential history under treatment status in the first period. Here, can include interaction terms, omitted for brevity.

Assumption 2 (Sequential Ignorability).

Assume that for all ,

Sequential ignorability is common in the literature on dynamic treatments (Robins et al., 2000). It states that treatment in the first period is exogenous conditional on baseline covariates, and the treatment in the second period is exogenous conditional on all observable characteristics at time . Sequential ignorability assumes no unobserved factors after controlling for high dimensional observable characteristics and arbitrary past information. Sequential ignorability differs from and complements parallel trend restrictions in the DiD literature, which would not allow for dynamic selection into treatment (Ghanem et al., 2022; Roth et al., 2023). The choice between a DiD design or a dynamic treatment design depends on the nature of selection into treatment, with the dynamic treatment design most suited when treatments are likely to change over time based on past information.

A class of economic models satisfying Assumption 2 are discrete choice models under conditional independence assumptions considered in Heckman et al. (2016), Heckman and Navarro (2007), Rust (1994), to cite some. As noted in Heckman et al. (2016), conditional independence assumptions “are especially well motivated if analysts have rich data on the determinants of choices,” here formalized by assuming that covariates are high dimensional.888Experiments in marketing, political campaigns or medical treatments are other examples where sequential ignorability have often been invoked (e.g. Blackwell, 2013; Acemoglu et al., 2019; Boruvka et al., 2018).

Example 2.1 Cont’d

2.3 Potential local projections

Following in spirit, Jordà (2005), we approximate the expectation of potential outcomes as linear functions of (high-dimensional) past characteristics. Different from Jordà (2005), linearity is imposed on expected potential instead of realized outcomes. Define

the conditional expectation of the potential outcome, given baseline covariates (), and given the history at time , respectively.

Assumption 3 (Model).

For some

Assumption 3 allows for heterogeneity in the treatment history , and the dimensions can be large (grow with , either or both because of additional covariates or also covariates transformations). As for marginal structural models (Robins et al., 2000), the model in Assumption 3 has two advantages. First, it does not require estimating a structural model for each time-varying-covariate, that would be prone to large estimation error in high dimensions. Second, it is agnostic on the treatment assignment mechanism because the model is imposed on potential outcomes. Time fixed-effects are directly incorporated in the model, since coefficients (and intercepts) can vary with time.

The proof is in Appendix A.1. Lemma 2.1 builds on results in the literature on marginal structural models (Robins et al., 2000; Bang and Robins, 2005; Tran et al., 2019). The connection we make between marginal structural models and local projections in economics is a contribution of independent interest. Lemma 2.1 motivates a recursive identification (and estimation) strategy, where we first project the observed outcome on the information in the second period. We then project its conditional expectation on information in the first period while controlling for the treatment in the second period (see Section 3).

Example 2.2 (Linear Model).

Let also contain an intercept. Consider the following set of conditional expectations

for some arbitrary parameters and . In the above display, denote unknown matrices in . The model satisfies Assumption 3.999Model with time-varying covariates have also been studied in more recent work of Caetano et al. (2022). Caetano et al. (2022) study DiD estimators with time-varying covariates assuming parallel trends instead of dynamic selection into treatment, hence presenting an analysis different (and complementary) to ours. ∎

Remark 1 (Linearity in high-dimensions as an approximation to the true model).

In the same spirit of Belloni et al. (2014), our results also directly extend to the case where we relax Assumption 3 and assume only approximate linearity up to an order where is an arbitrary sequence which depends on with .101010We do not include in Assumption 3 for expositional convenience, as we would need to carry over the throughout the text. None of the results, however, remain unchanged with the additional for , see Theorem 4.4, where we show that convergence rates of the estimator is of order . The approximation error of the linear model typically differs from the estimation error rate of the estimated coefficients which we will assume to be of order (for example Belloni et al., 2014, , Page 9, require the approximation of order with fixed sparsity). This setting embeds empirical applications where many covariates (and their transformation) can approximate the conditional mean function as linear. Linearity here also allows us to (re)interpret existing estimators widely used in applications such as local projections. We note that even estimators that use the propensity score require consistent estimation of the coefficients of a linear model in high-dimensions, what known as rate doubly-robustness (e.g. Athey and Wager, 2021).∎

2.4 Examples and comparisons with local projections and DiD

We pause here to compare our assumptions with those of local projections and DiD.

Different from standard local projections, here we assume and identify a local projection model for potential outcomes instead of realized outcomes (see Jordà, 2005; Montiel Olea and Plagborg-Møller, 2021, for reviews of these models). To illustrate this difference, consider a two periods settings without time-varying covariates, and

| (2) |

Under Equation (2), we can write

| (3) | ||||

The first equation is a reduced form corresponding to regressing the outcome at time on past treatments and covariates, the second equation is its equivalent also controlling for (see Alloza et al., 2020), and the third is the reduced form for potential outcomes.

The first equation in (3) shows that the interpretation of the parameters of the local projection of the observed outcome onto depends on properties of . Once we project onto , the estimated coefficient for denotes the effect of treating an individual at time only if and are independent. The second equation shows that controlling for may lead to omitted variable bias on the coefficient multiplying if future treatments depend on past outcomes. Therefore, standard local projections recover estimands whose interpretation depends on the distribution of the treatments, whereas the treatments’ distribution may change with a change in policy (see e.g. Wolf and McKay, 2022, for an insightful discussion). A third possible approach and different from the specifications in (3) is to estimate each equation for and obtain the desired through products and sums of the coefficients. This approach is prone to large estimation error with high-dimensional time-varying covariates because it estimates a separate model for each covariate.111111This follows similarly to discussion motivating local projections over vector auto-regression models (Jordà, 2005; Montiel Olea and Plagborg-Møller, 2021). Our approach leverages the potential outcome model in the third equation in (3), whose parameters do not depend on the realized treatments .

Our problem also connects to the literature on two-way fixed effects and Difference-in-Differences (see Roth et al., 2023, for an overview). This literature focuses on staggered adoption, whereas treatments here can change arbitrarily over time. In particular, the parallel trend assumption in DiD designs prohibits dynamic selection into treatment considered here (see Ghanem et al., 2022; Marx et al., 2022, for a discussion). Using Equation (3) for a simple illustration, we can interpret a version of parallel trends as

| (4) |

violated when future assignments depend on past outcomes (and therefore ). Therefore, DiD designs are suited in the presence of unobserved additive unit-level confounders but lack of dynamic selection different from (and complementary to) our framework.

3 Estimation with dynamic balancing in two periods

This section studies estimation in two periods. We defer to Section 5 a complete guide for practice, including discussion about the model, tuning parameters, and complexity.

3.1 Estimation of the coefficients

We first estimate the regression coefficients with Algorithm 1. The algorithm recursively projects the estimated conditional mean functions on past histories. Specifically, we first estimate a linear model for conditional on the history . We then estimate a linear model for the predicted value of – controlling for its treatment at time – and projecting this onto covariates at time .

We use lasso for penalization (Hastie et al., 2015). The algorithm considers two separate model specifications. The first allows for arbitrary heterogeneity in observable characteristics. This specification is cumbersome for longer time horizons because the effective sample size shrinks exponentially with the number of periods (see the discussion in Section 5). The second specification assumes separable treatment effects, and it is more parsimonious. It is possible to model heterogeneity in treatment effects in the second specification by including interaction terms between observable characteristics and treatments. We require that the parameters of the estimated model converge to the true parameters of the linear model for each regression at a rate of order . This condition is typically attained for lasso and discussed in detail in Section 4.2 (Assumption 6 (i) and discussion therein). Therefore, given the convergence rate requirement, a more parsimonious model such as the linear model in Algorithm 1 imposes stronger restrictions on the estimation error of the parameters.

3.2 Dynamic covariate balancing

Given the estimated coefficients , and following previous literature on doubly-robust scores (Tchetgen and Shpitser, 2012; Zhang et al., 2013; Jiang and Li, 2015; Nie et al., 2021), we propose an estimator that exploits linearity while reweighting observations to guarantee balance. Formally, we consider an estimator

| (5) | ||||

The estimator in (5) uses regression adjustments over each period, and reweight observations by weights (inputs of the estimator). The construction of such estimator leverages properties of influence functions (Tchetgen and Shpitser, 2012). We will omit the arguments in whenever clear from the context.

A first choice of the weights are inverse probability weights (IPW). As for multi-valued treatments (Imbens, 2000), these weights for the first and second period can be written as

| (6) |

However, in high dimensions, IPW weights require the correct specification of the propensity score, which in practice may be unknown. Also, in small sample, such weights are sensitive to poor overlap (high variance), because inverse probability weights denote the entire treatment history. Motivated by these considerations, we leverage the local projection model and propose replacing IPW with more stable weights.

We start studying covariate balancing conditions induced by the local projection model. By denoting the sample average of covariates , we can write

| (7) |

where

| (8) |

and

Lemma 3.1 (Covariate balancing conditions).

The following holds

Element is equivalent to what is discussed in Athey et al. (2018) in one period setting. Element depends on the additional error induced by dynamics in the second period. The estimation error depends on the product between the imbalance of covariates characterized by the expressions in and the estimation error of the coefficients, in the spirit of strong doubly-robustness properties. Therefore the above suggests controlling the norms

| (9) |

By imposing that the first norm converges to zero, the weights in the first-period balance covariates in the first period only. The second condition requires that histories in the second period are balanced, given the weights in the previous period.

The remaining terms in (7) are mean zero under the following conditions.

Lemma 3.2 (Balancing error).

The proof is in Appendix A.3. Lemma 3.2 conveys a key insight: if we can guarantee that each component in Equation (9) is sufficiently small, is centered around the target estimand plus a small estimation error (since ). Lemma 3.2 imposes the following intuitive conditions. The balancing weights in the first period are non-zero only for those units whose assignment in the first period coincide with the target assignment , and similarly for in the second period. Moreover, we can only balance based on information observed before the realization of potential outcomes but not based on future information. A special case of weights satisfying such conditions are IPW weights in (6).

Algorithm 2 presents the algorithmic details in two periods. In the first period, we balance baseline covariates between the treated and control groups as in Athey et al. (2018). Second, we estimate for the desired treatment history . The weights are not zero only for individuals with treatment history as discussed in Lemma 3.2. The estimated weights balance observable characteristics between different treatment groups at time , after reweighting with the weights estimated in the previous period. We choose weights that sum to one, are positive, and do not assign the largest weight to a few observations. For each period, the optimization problem solves a quadratic program recursively that minimizes the weights’ variances (and with scalable computational complexity). In Section 5 we provide more details about its implementation.

Finally, note that the advantages of balancing are well understood both in high and low dimensional scenarios (Zubizarreta, 2015). Here, because we consider an arbitrary class of weights (i.e., without imposing parametric assumptions on such weights, see Bruns-Smith et al., 2023), our residual balancing procedure improves balance (and improve the estimator’s performance) in both high and low dimensional settings.

4 Complete algorithm and theoretical guarantees

In this section, we present the complete algorithm with multiple time periods and formal theoretical guarantees for estimation and inference.

4.1 Multiple time periods

| (11) | ||||

Algorithm 3 generalizes our procedure to finite periods. Let . Define

| (12) |

This estimand denotes the difference in potential outcomes for two treatment histories . We define the information at time after excluding the treatment assignment . We denote

| (13) |

the vector containing information from time one to time , after excluding the treatment assigned in the present period . Interaction components may also be considered, omitted here for brevity. We let the potential history (as a function of the treatment history) be

The following assumption generalizes Assumptions 1-3 from the two-period setting.

Assumption 4.

For any , and ,

-

(A)

(No-anticipation) The potential history is constant in ;

-

(B)

(Sequential ignorability) ;

-

(C)

(Potential projections) For some ,

Condition (A) imposes non-anticipation each period (Boruvka et al., 2018). Condition (B) states that treatment assignments are randomized based on the past only. Condition (C) states that the conditional expectation of the potential outcome at time is linear in . Identification follows similarly to Lemma 2.1, omitted for brevity.

For given weights , and coefficients , we estimate with

| (14) | ||||

Coefficients are estimated recursively as in the two periods setting (see Algorithm 1). Estimation of the weights follows from the following lemma.

Lemma 4.1.

Suppose that if . Then

| (15) | ||||

where

The proof is in Appendix A.2. Lemma 4.1 decomposes the estimation error into three components. First, (), depends on the estimation error of the coefficient and on balancing properties of the weights. () suggests imposing balancing conditions on

each period. The components characterizing the estimation error are , and (). In the following lemma, we provide conditions such that () is mean zero.

Lemma 4.2.

Let Assumption 4 hold. Suppose that the sigma algebra . Suppose in addition that if . Then

The proof is in Appendix A.3.

4.2 Theoretical properties and inference

Next, we study the theoretical properties of the estimator in finite periods. We consider a high dimensional regime where the dimension covariates in each period can grow to infinity, as long as .121212The dimension of covariates can grow either because of additional controls of because of transformations of covariates (either case is allowed here). We impose the following conditions.

Assumption 5 (Overlap and tails’ conditions).

Assume that for each . Assume also that is Sub-Gaussian given and similarly is Sub-Gaussian.

The first condition is the overlap condition, standard in the causal inference literature (Imbens and Rubin, 2015). The second condition is a tail restriction. The sub-gaussianity restriction is imposed to obtain an exponential concentration of the covariates’ means. Such a condition can be relaxed to assuming that the product of the inverse probability weights times the covariates is sub-exponential – holding, for example, under the overlap restriction and sub-exponential covariates – at the expense of more tedious derivations.

Theorem 4.3 (Existence of feasible weights).

Theorem 4.3 has important implications. Inverse probability weights tend to be unstable in a small sample for moderately large periods. The algorithm thus finds weights that minimize the small sample variance, with the IPW weights being one possible solution.

Corollary 1.

Under the conditions in Theorem 4.3, for some , , with probability , , for .

Corollary 1 formalizes the result that IPW weights have larger variance than balancing weights (even in the presence of overlap).

In summary, Theorem 4.3 shows that the true propensity score is a feasible solution for the proposed program. The theorem does not require researchers to know or estimate the propensity score. Instead, the theorem shows that the program will be able to recover the true propensity score (without knowledge of it) if the propensity score has the smallest variance across all balancing weights. In settings where the score is unstable and has a large variance, our method will balance covariates using more robust balancing weights.

Assumption 6.

Let the following hold: for every , ,

-

(i)

, for a finite constant , ;

-

(ii)

Let . For a finite constant , , , almost surely. In addition, is a sub-gaussian random variable.

-

(iii)

, almost surely, for some constant .

Assumption 6 imposes the consistency in estimating the outcome models. Condition (i) is attained for many high-dimensional estimators, such as the lasso method, under regularity assumptions; see, e.g., Bühlmann and Van De Geer (2011). An example and derivation for condition (i) for Lasso is included in Example A.1 (see Appendix A.4).131313Appendix A.4 shows that the restrictions on the degree of sparsity required in dynamic settings are more stringent than those obtained in settings, with the error scaling faster in the sparsity degree. The reason is because of recursively projecting conditional expectations, the estimation error cumulates over each iteration. Appendix A.4 presents details about lasso. The remaining conditions impose moment assumptions, attained for sub-gaussian random variables.141414Sub-gaussianity of imposes restrictions on the tail behavior of the endline outcome, and it is invoked to consistently estimate the variance of the average treatment effect.

Theorem 4.4 shows that the proposed estimator guarantees parametric convergence rate with high-dimensional covariates.

Theorem 4.5 (Asymptotic Inference).

Theorem 4.6 (Inference on ATE).

Let the conditions in Theorem 4.5 hold. Let Then, whenever with ,

The proof is in Appendix B.

Remark 2 (Tighter/Gaussian confidence bands).

The confidence band depends on a chisquared random variable with degrees of freedom. In Appendix B.2 we show that under additional conditions we can get

and hence, tighter confidence bands. The assumptions needed is that converge almost surely to (some) finite constant. This condition imposes restrictions on the degree of dependence of the optimal weights, and holds for a bernoulli design. In addition, this condition also holds whenever we parametrize the weights as a function of and impose appropriate restriction on the complexity of function classes , , as for choices of riesz representers in Chernozhukov et al. (2022).151515For example, it holds when balancing weights are smooth functions of arbitrary parameter such that solving Algorithm 3 is such that for some arbitrary . We do not use the critical quantile of a standard Gaussian random variable in Theorem 4.6 because of the possible lack of almost sure convergence of , when either we have limited overlap in finite sample or we impose no functional form restrictions on such weights (see Section 5 for more details). ∎

Remark 3 (Variance conditional on ).

It is possible to use chi-squared distribution with (instead of ) degrees of freedoms if the estimand of interest is the ATE conditional on baseline covariates instead of the unconditional ATE. In this case he variance should not account for the last term . We use such a variance estimator in our numerical study and application, since in our application units are countries, motivating our focus on the treatment effect conditional on countries’ baseline characteristics. ∎

5 Guide to practice

The complete Algorithm 3 is implemented off-the-shelf in the R-package DynBalancing.

It requires researchers to specify four main parameters: the length of the treatment history considered (i.e., carry-over effects), two treatment histories of length , to compare, the model used to estimate the coefficients (linear or fully interacted) as in Algorithm 1, and whether to consider a pooled regression.

Choosing the length of the treatment history

In the presence of short panels, selecting the length of the treatment history is natural, i.e., studying a treatment path that spans the entire panel. However, with long panels, this may reduce the effective sample size used to estimate causal effects or be infeasible. By selecting a treatment history shorter than the number of periods (i.e., ), we estimate causal effects of the form

| (17) |

for given treatment histories . Equation (17) estimates the effect of exposing an individual to two different treatment histories only over the last periods and average over previous treatment assignments. Our analysis and estimation follow similarly to what is discussed in Algorithm 3, with the difference that we construct balancing weights starting from period and proceed sequentially until time (observable characteristics before time can be used as additional controls). Similarly, the estimator in Equation (14) only uses information from time to , hence reducing the effective length of the time periods. As in Imai et al. (2018), the focus on estimands in Equation (17) makes our procedure robust to long panels.

Choice of the model specification (linear or fully interacted)

The estimation error in periods depends on modeling assumptions. For the fully interacted model, scales exponentially with since this model requires running regressions over the subsample with treatment histories . The linear model avoids that the effective sample size shrinks exponentially in but imposes homogeneity restrictions of treatment effects as in Acemoglu et al. (2019). Therefore, researchers must choose the model, considering the trade-off between the variance (increasing in the length of the treatment history) and bias (due to treatment effect heterogeneity). Considering linear specification with interaction terms with covariates is also possible when researchers expect heterogeneity through observable characteristics.

Pooled regression

When pooled is true, we consider a regression

where denotes fixed effects, and an estimand as in Equation (17), pooling together effects estimated in different periods. For given treatment history length , it uses each observation (including information about past histories until time ) as separate observations, assuming stationarity in treatment effects. We then cluster standard errors at the individual level to allow for correlation in time for each unit. In practice, we recommend reporting results both from a pooled and not pooled regression as robustness checks.

Inference

Theorem 4.5 and Remark 2 present two choices of critical values: a more conservative choice using the square-root of a chi-squared critical value, and the Gaussian critical value. Our package reports both. In our numerical studies (Section 6), the Gaussian quantile performs well under strong sparsity and strong overlap, but its corresponding coverage deteriorates as overlap decreases. Instead, the chi-squared critical quantile presents valid coverage throughout all the designs. We recommend that researchers use Gaussian critical quantiles in settings with moderate or good overlap of treatment assignments, such as when treatments correlate strongly over time. We recommend the chi-squared quantiles otherwise.

Researchers can also choose between the conditional or unconditional variance on baseline covariates. When researchers are interested in sample average causal effects, e.g., effects conditional on countries’ characteristics, we recommend the former, otherwise the latter.

Remark 4 (Tuning parameters).

Similarly to balancing in one-dimensional setting (Athey et al., 2018), Algorithm 3 requires choosing tuning parameters for Equation (11). A complete description is in Algorithm 4 and uses a data-adaptive procedure (i.e., researchers do not need to specify the tuning parameters). In a nutshell, we choose (here is the dimension of covariates at time ) as prescribed by the theoretical analysis in Section 4.2. To guarantee balance with many covariates, we first select the smallest constant for covariates with non-zero estimated coefficients and second the smallest constant for the remaining covariates until a feasible solution is reached. This choice minimizes the estimator’s bias and, within the set of weighting estimators with the smallest bias, selects the one with the smallest variance while prioritizing balance on covariates with non-zero coefficients. Section 6 illustrates the benefits of this procedure. ∎

Remark 5 (Computational complexity).

The program in Algorithm 3 is a sequence of quadratic programs with linear constraints. Its computational complexity scales polynomially with . Figure 6 provides an example showing that the computational time is between a few seconds and a few minutes for on a personal laptop (the running time also includes running the data-adaptive procedure to choose the tuning parameters). ∎

Remark 6 (Unbalanced panels).

Our method allows for imbalanced panels since estimation is performed sequentially (both for the coefficients and weights). If some observations are missing over some periods, the algorithm will exclude such units when estimating the coefficients and weights for that period(s) but not for the remaining ones. ∎

6 Numerical Experiments

This section collects results from numerical experiments.We estimate

We let the baseline covariates be drawn from as i.i.d. with . Covariates in the subsequent period are generated according to an auto-regressive model Treatments are drawn from a logistic model that depends on all previous treatments and past covariates: with

| (18) |

and , for . Here, controls the association between covariates and treatment assignments. We consider values of , . We let , with , similarly to balancing conditions presented in Athey et al. (2018). The larger corresponds to weaker overlap (see Table 1).

| T=2 | T=3 | T=2 | T=3 | T=2 | T=3 | |||

| Min | 0.012 | 0.004 | 0.0002 | 0.001 | 0.00000 | |||

| 1st Quantile | 0.126 | 0.049 | 0.105 | 0.031 | 0.079 | 0.018 | ||

| Median | 0.218 | 0.097 | 0.216 | 0.097 | 0.216 | 0.094 | ||

| 3rd Quantile | 0.248 | 0.126 | 0.259 | 0.153 | 0.277 | 0.183 | ||

| Max | 0.175 | 0.377 | 0.226 | 0.429 | 0.286 | |||

We generate the outcome according to the following equations:

where elements of are i.i.d. and . We consider three different settings: Sparse with , Moderate with moderately sparse and the Harmonic setting with . We set .

6.1 Methods

We consider the following competing methodologies. Augmented IPW, with known propensity score and with estimated propensity score. The method replaces the balancing weights in Equation (5) with the (estimated or known) propensity score. Estimation of the propensity score is performed using a logistic regression (denoted as aIPWl) and a penalized logistic regression as in Negahban et al. (2012) (denoted as aIPWh).161616See for example Nie et al. (2021) and Bodory et al. (2020) for a discussion on doubly-robust estimators. For both AIPW and IPW we consider stabilized inverse probability weights. We also compare to existing balancing procedures for dynamic treatments. Namely, we consider Marginal Structural Model (MSM) with balancing weights computed using the method in Yiu and Su (2018); Yiu and Su (2020). The method consists of estimating Covariate-Association Balancing weights CAEW (MSM) as in Yiu and Su (2018); Yiu and Su (2020).171717These methods consist of balancing covariates reweighted by marginal probabilities of treatments (estimated with a logistic regression), and use such weights to estimate marginal structural model of the outcome linear in past treatment assignments. We follow Section 3 in Yiu and Su (2020) for its implementation. (We do not also compare to Imai and Ratkovic 2015 for MSM since it is intractable in high-dimensions). We also consider “Dynamic” Double Lasso that estimates the effect of each treatment assignment separately, after conditioning on the present covariate and past history for each period using the double lasso discussed in one period setting in Belloni et al. (2014).181818See Lewis and Syrgkanis (2020) for related procedures. Naive Lasso runs a regression controlling for covariates and treatment assignments only. Sequential Estimation estimates the conditional mean in each time period sequentially using the lasso method, and it predicts end-line potential outcomes as a function of the estimated potential outcomes in previous periods. We also consider two “intuitive” but biased estimators. We define DiD switchback as a difference-in-differences estimator that takes the difference between the outcome at time and the outcome at time for those units that switched from control to treatment in the last period, subtracts the difference of the outcomes for time and for those units under control for all periods. It then multiplies the estimated effect by the number of periods of interest to make (since we are interested in the overall effect of being exposed to treatment for all periods).191919We note that one could consider different variants of difference in means or difference-in-differences estimators. The reader may refer to De Chaisemartin and d’Haultfoeuille (2022) for a discussion. Finally, we define Simple LP (Local Projection) the estimator that projects onto baseline covariates and treatment and take the coefficient multiplying as the estimated effect, while penalizing the coefficients for via Lasso. For Dynamic Covariate Balancing, DCB choice of tuning parameters is data adaptive, and it uses a grid-search method discussed in Appendix C.202020The grid-search procedure consists of finding the smallest feasible constraint-value through grid search, while choosing more stringent constants for those variables whose estimated coefficients are non-zero. We estimate coefficients as in Algorithm 1 for DCB and (a)IPW, with a linear model in treatment assignments. Estimation of the penalty for the lasso methods is performed via cross-validation.

6.2 Results

We consider and set the sample size to be . The regression in the first period contains covariates, in the second period covariates, and in the third covariates.

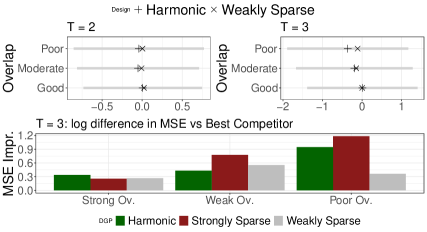

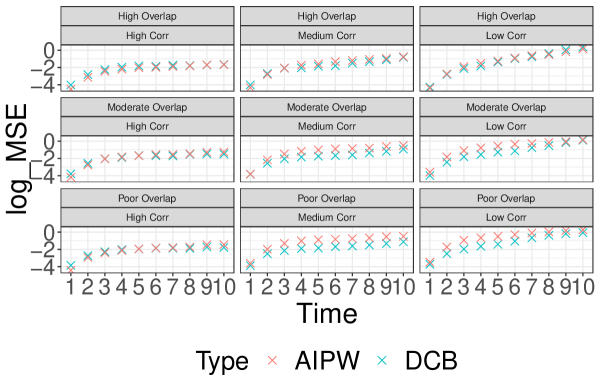

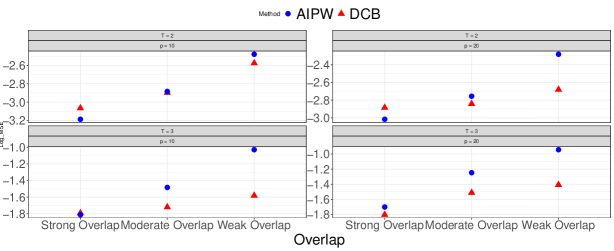

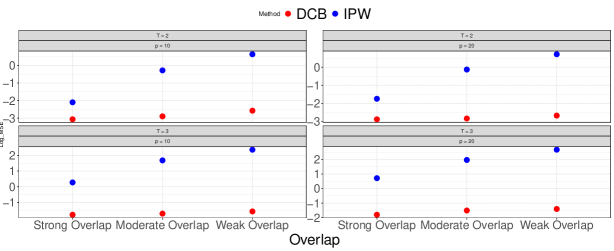

In Table 2 we collect results for the average mean squared error for estimating the average treatment effect in two and three periods. Throughout all simulations, the proposed method significantly outperforms any other competitor, with one single exception for , good overlap and harmonic design. It also outperforms using known propensity score, consistently with our findings in Theorem 4.3, where we show that the propensity score is a feasible solution of DCB weights (and in the absence of knowledge of the propensity score). Improvements are particularly significant when (i) overlap deteriorates; (ii) the number of periods increases from two to three. This can also be observed in the panel at the bottom of Figure 4, where we report the decrease in MSE (in logarithmic scale) when using our procedure for . In Appendix D we present results with misspecified models.

| sparse | mod | harm | sparse | mod | harm | sparse | mod | harm | |||

| aIPW∗ | 0.131 | ||||||||||

| DCB | 0.099 | 0.077 | 0.085 | ||||||||

| aIPWh | |||||||||||

| aIPWl | |||||||||||

| IPWh | |||||||||||

| Seq.Est. | |||||||||||

| Lasso | |||||||||||

| CAEW | |||||||||||

| Dyn.D.Lasso | |||||||||||

| DiD Switchback | |||||||||||

| Simple LP | |||||||||||

| aIPW∗ | |||||||||||

| DCB | |||||||||||

| aIPWh | |||||||||||

| aIPWl | |||||||||||

| IPWh | |||||||||||

| Seq.Est. | |||||||||||

| Lasso | |||||||||||

| CAEW | |||||||||||

| Dyn.D.Lasso | |||||||||||

| DiD Switchback | |||||||||||

| Simple LP | |||||||||||

In the top panel of Figure 4 we report the length of the confidence interval and the point estimates. The length increases with the number of periods, and point estimates are more accurate for a non-harmonic (more sparse) setting.

| Sparse | Moderate | Harmonic | Sparse | Moderate | Harmonic | ||||||||

| Ho | He | Ho | He | Ho | He | Ho | He | Ho | He | Ho | He | ||

| : Coverage Probability | |||||||||||||

| = | 1.00 | 0.98 | 1.00 | 0.99 | 0.99 | 0.96 | 0.99 | 0.99 | 1.00 | 1.00 | 1.00 | 0.96 | |

| = | 0.99 | 0.99 | 0.99 | 0.98 | 0.97 | 0.95 | 1.00 | 0.99 | 0.99 | 0.98 | 0.99 | 0.93 | |

| = | 1.00 | 0.99 | 0.99 | 0.99 | 0.96 | 0.94 | 0.99 | 0.97 | 0.99 | 0.97 | 0.98 | 0.93 | |

| : Coverage Probability | |||||||||||||

| = | 1.00 | 0.99 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | 0.99 | 0.99 | 0.99 | |

| = | 1.00 | 1.00 | 0.99 | 0.99 | 1.00 | 0.99 | 1.00 | 0.99 | 1.00 | 1.00 | 0.97 | 0.96 | |

| = | 1.00 | 1.00 | 1.00 | 1.00 | 0.98 | 0.97 | 1.00 | 0.99 | 1.00 | 0.99 | 0.99 | 0.97 | |

| : Coverage Probability with Gaussian quantile | |||||||||||||

| = | 0.96 | 0.94 | 0.98 | 0.94 | 0.97 | 0.90 | 0.98 | 0.92 | 0.90 | 0.79 | |||

| = | 0.97 | 0.94 | 0.91 | 0.85 | 0.98 | 0.92 | 0.98 | 0.91 | 0.75 | 0.64 | |||

| = | 0.99 | 0.96 | 0.89 | 0.84 | 0.92 | 0.85 | 0.94 | 0.86 | 0.73 | 0.61 | |||

Finally, we report finite sample coverage of the proposed method, DCB in Table 3 for estimating and (for ) in the first two panel with (see Table 4 in the Appendix for the confidence intervals’ length).212121Results for present over-coverage of the chi-squared method, and correct or under-coverage (albeit less severe than ) when considering a Gaussian critical quantile. The former is of interest when the effect under control is more precise and its variance is asymptotically neglegible compared to the estimated effect under treatment (e.g., many more individuals are not exposed to any treatment). The latter is of interest when both and are estimated from approximately a proportional sample. In the third panel, we report coverage when instead a Gaussian critical quantile (instead of the square root of a chi-squared quantile discussed in our theorems) is used. We observe that our procedure can lead to correct (over) coverage, while the Gaussian critical quantile leads to under-coverage in the presence of poor overlap and many variables, but correct coverage with fewer variables and two periods only.

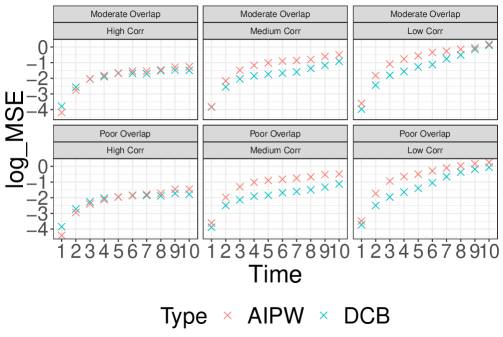

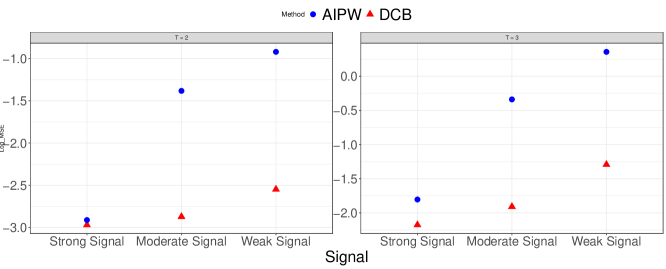

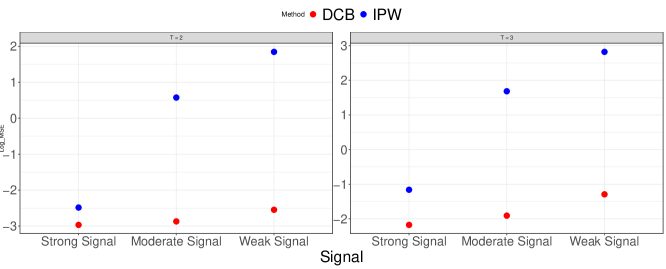

We compare DCB and AIPW with high dimensional covariates with a longer time period. Namely, in Figure 5, we collect results for . We generate data using a sparse model, over two-hundred replications. The outcome at time depends on the contemporaneous treatment, covariates, and previous outcome at time . To simulate a scenario where a strong correlation occurs between treatments over a long time period, we generate

where similarly to the propensity score model Equation (18), . Here controls overlap together with , where has a similar role of the overlap constant in previous simulations.222222We take as this plays approximately the same role of in previous simulations from a simple linear approximation of with respect to . In the figure we report results for (denoted as “High, Medium and Low correlation” respectively), and . In Figure 5, we observe that for very strong time dependence between treatments (i.e., there are limited or no dynamics in assignments) the two methods are comparable. When instead, there are relatively more dynamics in treatment assignments the proposed method significantly improves in mean-squared error, with larger improvements in the presence of poorer overlap. In the Appendix, Figure 10 we provide results also for very good overlap (), where the methods mostly provide comparable results on average.

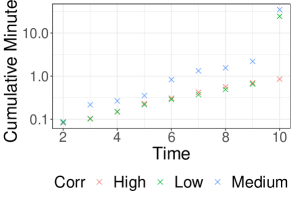

Finally, in Figure 6 we presents an example of computational time of the method as varies, showing that the time for is between few seconds and ten minutes on a personal computer. For the computational time is 60 minutes (on a single core, 30 on two cores) in our empirical application.

6.3 Additional numerical studies and misspecified model

In Appendix D we study settings with a misspecified outcome model, low dimensional covariates and settings where the signal of the coefficients decay in the spirit of Wüthrich and Zhu (2023). We show that our findings in the current section are robust to these alternative designs. In particular, in contexts with misspecified models (Appendix D.1) we observe that DCB outperforms AIPW, with a known propensity score. The main reason is due to the instability of the inverse probability weights in dynamic settings. Because these weights define the joint probability of treatment assignments, these can exhibit instability (poor overlap) in small samples, increasing the variance of the AIPW estimator (which we observe in Appendix D.1 as we decompose the bias and variance of each estimator). These findings further motivate the advantages of DCB.

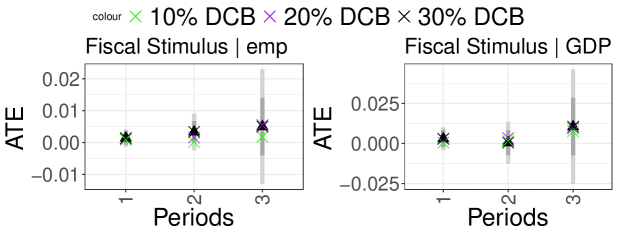

7 Empirical application

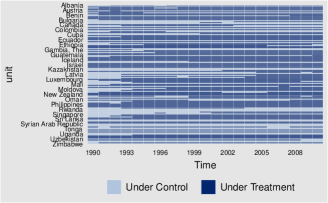

In this section, we present an empirical application for studying the effect of democracy on GDP growth using data from Acemoglu et al. (2019). Acemoglu et al. (2019) studied dynamic treatment effects of democracy under GDP growth under sequential ignorability (Assumption 1 in Acemoglu et al., 2019). Figure 7 illustrates the dynamics of treatments. Many units switch treatment over time, violating standard event studies designs, and motivating an approach for dynamic treatments, for example considered in Acemoglu et al. (2019). We revisit the study of Acemoglu et al. (2019) and illustrate the advantages of our method.

7.1 Data and estimation

The data consist of an extensive collection of countries observed between and .232323Data available at https://www.journals.uchicago.edu/doi/suppl/10.1086/700936. We consider observations starting from . After removing missing values, we run regressions with 141 countries. The outcome is the log-GDP in the country in period as in Acemoglu et al. (2019). We use the same treatment specification as in Acemoglu et al. (2019), which is binary and constructed using a political index. We study the effect of exposing countries at time to democracy for in years before (and including) versus not exposing them to democracy for the previous years. Namely, the estimand is the -long run effect of democracy, after averaging over past assignments as discussed in Section 5.242424Formally, the estimand defines We let to study the impact from one to twenty years of democracy.

For each country, we condition on lag outcomes in the past four years as in the preferred specification of Acemoglu et al. (2019), and past four treatments. We consider a pooled regression (see Section 5) and two alternative specifications. The first is parsimonious and includes dummies for different regions (continents) and different intercepts for different periods. Note that, similarly to what discussed in Zubizarreta (2015), even with a parsimonious specification, residual balancing can substantially improve the finite sample performance of the estimator, as we show in the right panel of Figure 8. The second one controls for the past four outcomes, past four treatments, for the geographical region, and histories based on colonial history and regimes types as defined in the data from Acemoglu et al. (2019).252525To replicate the results, these are the columns of data in Acemoglu et al. (2019) named “Region 60”, “Region DA,” “Region REG.” Note that our specification does not include country fixed effects, as our (and Robins (1986)’s) framework assumes that treatments are exogenous conditional on past information. To control for confounding bias that may arise from country specific characteristics (and time) our second specification controls for a large vector of country’s characteristics. We therefore see our second specification as more robust to possible confounding mechanisms. Coefficients are estimated as in Algorithm 1 with model linear.262626Note that in principle, it is possible to penalize only some but not all coefficients, in the spirit of group lasso methods (Hastie et al., 2015). We omit this for brevity.

7.2 Results

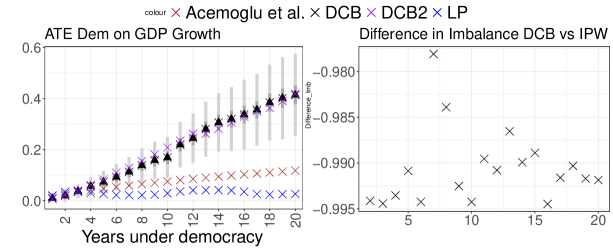

Figure 8 collects our results. Democracy has a statistically insignificant effect over the first few years and a statistically significant positive impact on long-run GDP growth after six years. Point estimates are in sign and magnitude consistent with what found by Acemoglu et al. (2019), and results are robust across the two specifications for DCB.

We compare our method to three alternative specifications: (i) the AIPW method that uses the same estimation method we propose in Algorithm 1 for estimating the conditional mean function, and the propensity score via penalized generalized linear models as in Negahban et al. (2012); (ii) the linear estimator reported by Acemoglu et al. (2019) (Table 2, Column 3), where dynamic effects are estimated by propagating the effect over past outcomes at each period, as suggested by Acemoglu et al. (2019); the simple local projection, that projects the outcome on the treatment and the past outcome periods before, controlling for country, time fixed effects and lagged outcome at time (this specification follows similarly to the regression specifications in macro-economic applications as in Auerbach et al., 2020).

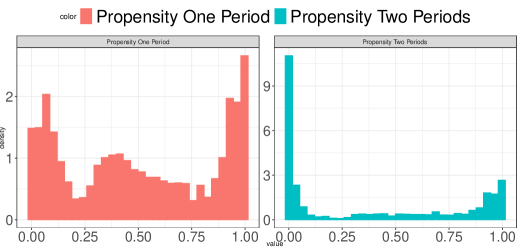

The simple local projection approach reports the smallest point estimates compared to all methods. This result is consistent with our theoretical discussion: local projections average over the distribution of future assignments. Therefore, the causal effects estimated by the local projection differ from the target long-run effect, which instead fixes future treatment assignments. This difference illustrates the benefits of recursive projections in the presence of dynamic selection into treatment, when the goal is to estimate long-run treatment effects.272727The simple local projection presents growing effects in the first few periods and a positive effect with decreasing marginal effects for longer periods. This behavior can be explained by the positive treatment correlations in Figure 7: because of positive treatment correlation, short-term effects may be driven by positive future treatments, whereas long-term effects may be decreasing due to weaker correlation over time. The effect estimated as in Acemoglu et al. (2019) is larger than the local projection method but significantly smaller than the effect estimated through DCB. Therefore, the specification in Acemoglu et al. (2019) may capture some but not all the long-run effects. After controlling for imbalance with DCB, average treatment effects are twice as large. To investigate differences with (A)IPW methods, the right panel in Figure 8 presents comparisons in terms of the imbalance over the lagged outcome at time when using balancing or inverse probability weights. As Acemoglu et al. (2019) note, “Besides controlling for the fact that democratizations are more frequent after economic crises, the lags of GDP per capita summarize the impact of a range of economic factors that affect both growth and democracy, such as commodity prices, agricultural productivity, and technology. Indeed, many of these economic factors should have an impact on future GDP, primarily through their influence on current GDP.” Therefore, an imbalance in lagged GDP may suggest the presence of bias. We report the relative improvement in absolute imbalance (average across the potential outcomes under treatment and control) and observe substantial gain over using inverse probability weights. Such gains illustrate the advantage of balancing in small sample. Finally, Figure 9 complements Figure 8 showing instability of inverse probability weights.

8 Discussion

This paper studies the problem of inference on dynamic treatments via covariate balancing. We consider a potential local projection model with high-dimensional covariates, and we introduce novel balancing conditions that allow for the optimal -consistent estimation. Simulations and empirical applications illustrate the method’s advantages.

Several questions remain open. First, the asymptotic properties crucially rely on cross-sectional independence while allowing for general dependence over time. Future work should addres extensions where cross-sectional -ness does not necessarily hold. Second, our asymptotic results assume a fixed period. Future work should study settings with large (see e.g., Section 5). It would also be interesting to study whether conditions on overlap might be replaced by alternative (weaker) assumptions.

Finally, dynamic treatment regimes and parallel trends impose different (and complementary) assumptions for causal inference. Reconciling these two frameworks and proposing methods that are robust to either condition remains an open research question.

References

- Abbring and Van den Berg (2003) Abbring, J. H. and G. J. Van den Berg (2003). The nonparametric identification of treatment effects in duration models. Econometrica 71(5), 1491–1517.

- Abraham and Sun (2018) Abraham, S. and L. Sun (2018). Estimating dynamic treatment effects in event studies with heterogeneous treatment effects. Available at SSRN 3158747.

- Acemoglu et al. (2019) Acemoglu, D., S. Naidu, P. Restrepo, and J. A. Robinson (2019). Democracy does cause growth. Journal of Political Economy 127(1), 47–100.

- Alloza et al. (2020) Alloza, M., J. Gonzalo, and C. Sanz (2020). Dynamic effects of persistent shocks. arXiv preprint arXiv:2006.14047.

- Arkhangelsky and Imbens (2019) Arkhangelsky, D. and G. Imbens (2019). Double-robust identification for causal paneldata models. arXiv preprint arXiv:1909.09412.

- Athey and Imbens (2022) Athey, S. and G. W. Imbens (2022). Design-based analysis in difference-in-differences settings with staggered adoption. Journal of Econometrics 226(1), 62–79.

- Athey et al. (2018) Athey, S., G. W. Imbens, and S. Wager (2018). Approximate residual balancing: debiased inference of average treatment effects in high dimensions. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 80(4), 597–623.

- Athey and Wager (2021) Athey, S. and S. Wager (2021). Policy learning with observational data. Econometrica 89(1), 133–161.

- Auerbach et al. (2020) Auerbach, A., Y. Gorodnichenko, and D. Murphy (2020). Local fiscal multipliers and fiscal spillovers in the usa. IMF Economic Review 68, 195–229.

- Babino et al. (2019) Babino, L., A. Rotnitzky, and J. Robins (2019). Multiple robust estimation of marginal structural mean models for unconstrained outcomes. Biometrics 75(1), 90–99.

- Bang and Robins (2005) Bang, H. and J. M. Robins (2005). Doubly robust estimation in missing data and causal inference models. Biometrics 61(4), 962–973.

- Belloni et al. (2014) Belloni, A., V. Chernozhukov, and C. Hansen (2014). Inference on treatment effects after selection among high-dimensional controls. The Review of Economic Studies 81(2), 608–650.

- Belloni et al. (2016) Belloni, A., V. Chernozhukov, C. Hansen, and D. Kozbur (2016). Inference in high-dimensional panel models with an application to gun control. Journal of Business & Economic Statistics 34(4), 590–605.

- Ben-Michael et al. (2018) Ben-Michael, E., A. Feller, and J. Rothstein (2018). The augmented synthetic control method. arXiv preprint arXiv:1811.04170.

- Blackwell (2013) Blackwell, M. (2013). A framework for dynamic causal inference in political science. American Journal of Political Science 57(2), 504–520.

- Bodory et al. (2020) Bodory, H., M. Huber, and L. Lafférs (2020). Evaluating (weighted) dynamic treatment effects by double machine learning. arXiv preprint arXiv:2012.00370.

- Bojinov et al. (2020) Bojinov, I., A. Rambachan, and N. Shephard (2020). Panel experiments and dynamic causal effects: A finite population perspective. arXiv preprint arXiv:2003.09915.

- Bojinov and Shephard (2019) Bojinov, I. and N. Shephard (2019). Time series experiments and causal estimands: exact randomization tests and trading. Journal of the American Statistical Association, 1–36.

- Boruvka et al. (2018) Boruvka, A., D. Almirall, K. Witkiewitz, and S. A. Murphy (2018). Assessing time-varying causal effect moderation in mobile health. Journal of the American Statistical Association 113(523), 1112–1121.

- Bradic et al. (2021) Bradic, J., W. Ji, and Y. Zhang (2021). High-dimensional inference for dynamic treatment effects. arXiv preprint arXiv:2110.04924.

- Bruns-Smith et al. (2023) Bruns-Smith, D., O. Dukes, A. Feller, and E. L. Ogburn (2023). Augmented balancing weights as linear regression. arXiv preprint arXiv:2304.14545.

- Bühlmann and Van De Geer (2011) Bühlmann, P. and S. Van De Geer (2011). Statistics for high-dimensional data: methods, theory and applications. Springer Science & Business Media.

- Caetano et al. (2022) Caetano, C., B. Callaway, S. Payne, and H. S. Rodrigues (2022). Difference in differences with time-varying covariates. arXiv preprint arXiv:2202.02903.

- Callaway and Sant’Anna (2019) Callaway, B. and P. H. Sant’Anna (2019). Difference-in-differences with multiple time periods. Available at SSRN 3148250.

- Chernozhukov et al. (2017) Chernozhukov, V., M. Goldman, V. Semenova, and M. Taddy (2017). Orthogonal machine learning for demand estimation: High dimensional causal inference in dynamic panels. arXiv preprint arXiv:1712.09988.

- Chernozhukov et al. (2018) Chernozhukov, V., C. Hansen, Y. Liao, and Y. Zhu (2018). Inference for heterogeneous effects using low-rank estimations. arXiv preprint arXiv:1812.08089.

- Chernozhukov et al. (2022) Chernozhukov, V., W. Newey, R. Singh, and V. Syrgkanis (2022). Automatic debiased machine learning for dynamic treatment effects and general nested functionals. arXiv preprint arXiv:2203.13887.

- Chodorow-Reich (2019) Chodorow-Reich, G. (2019). Geographic cross-sectional fiscal spending multipliers: What have we learned? American Economic Journal: Economic Policy 11(2), 1–34.

- de Chaisemartin and d’Haultfoeuille (2019) de Chaisemartin, C. and X. d’Haultfoeuille (2019). Two-way fixed effects estimators with heterogeneous treatment effects. Technical report, National Bureau of Economic Research.

- De Chaisemartin and d’Haultfoeuille (2022) De Chaisemartin, C. and X. d’Haultfoeuille (2022). Difference-in-differences estimators of intertemporal treatment effects. Technical report, National Bureau of Economic Research.

- Ding and Li (2019) Ding, P. and F. Li (2019). A bracketing relationship between difference-in-differences and lagged-dependent-variable adjustment. Political Analysis 27(4), 605–615.

- Dube et al. (2023) Dube, A., D. Girardi, O. Jorda, and A. M. Taylor (2023). A local projections approach to difference-in-differences event studies. Technical report, National Bureau of Economic Research.

- Farrell (2015) Farrell, M. H. (2015). Robust inference on average treatment effects with possibly more covariates than observations. Journal of Econometrics 189(1), 1–23.

- Ghanem et al. (2022) Ghanem, D., P. H. Sant’Anna, and K. Wüthrich (2022). Selection and parallel trends. arXiv preprint arXiv:2203.09001.

- Goodman-Bacon (2021) Goodman-Bacon, A. (2021). Difference-in-differences with variation in treatment timing. Journal of Econometrics.

- Hainmueller (2012) Hainmueller, J. (2012). Entropy balancing for causal effects: A multivariate reweighting method to produce balanced samples in observational studies. Political Analysis 20(1), 25–46.

- Hastie et al. (2015) Hastie, T., R. Tibshirani, and M. Wainwright (2015). Statistical learning with sparsity: the lasso and generalizations. CRC press.

- Heckman et al. (2016) Heckman, J. J., J. E. Humphries, and G. Veramendi (2016). Dynamic treatment effects. Journal of econometrics 191(2), 276–292.

- Heckman and Navarro (2007) Heckman, J. J. and S. Navarro (2007). Dynamic discrete choice and dynamic treatment effects. Journal of Econometrics 136(2), 341–396.

- Hernán et al. (2001) Hernán, M. A., B. Brumback, and J. M. Robins (2001). Marginal structural models to estimate the joint causal effect of nonrandomized treatments. Journal of the American Statistical Association 96(454), 440–448.

- Hirshberg and Wager (2017) Hirshberg, D. A. and S. Wager (2017). Augmented minimax linear estimation. arXiv preprint arXiv:1712.00038.

- Imai and Kim (2016) Imai, K. and I. S. Kim (2016). When should we use linear fixed effects regression models for causal inference with longitudinal data? Unpublished working paper. Retrieved September 19.

- Imai et al. (2018) Imai, K., I. S. Kim, and E. Wang (2018). Matching methods for causal inference with time-series cross-section data.

- Imai and Ratkovic (2014) Imai, K. and M. Ratkovic (2014). Covariate balancing propensity score. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 76(1), 243–263.

- Imai and Ratkovic (2015) Imai, K. and M. Ratkovic (2015). Robust estimation of inverse probability weights for marginal structural models. Journal of the American Statistical Association 110(511), 1013–1023.

- Imbens (2000) Imbens, G. W. (2000). The role of the propensity score in estimating dose-response functions. Biometrika 87(3), 706–710.

- Imbens and Rubin (2015) Imbens, G. W. and D. B. Rubin (2015). Causal inference in statistics, social, and biomedical sciences. Cambridge University Press.

- Jiang and Li (2015) Jiang, N. and L. Li (2015). Doubly robust off-policy value evaluation for reinforcement learning. arXiv preprint arXiv:1511.03722.

- Jordà (2005) Jordà, Ò. (2005). Estimation and inference of impulse responses by local projections. American economic review 95(1), 161–182.

- Kallus and Santacatterina (2018) Kallus, N. and M. Santacatterina (2018). Optimal balancing of time-dependent confounders for marginal structural models. arXiv preprint arXiv:1806.01083.

- Kock and Tang (2015) Kock, A. B. and H. Tang (2015). Inference in high-dimensional dynamic panel data models. arXiv preprint arXiv:1501.00478.

- Krampe et al. (2020) Krampe, J., E. Paparoditis, and C. Trenkler (2020). Impulse response analysis for sparse high-dimensional time series. arXiv preprint arXiv:2007.15535.

- Lewis and Syrgkanis (2020) Lewis, G. and V. Syrgkanis (2020). Double/debiased machine learning for dynamic treatment effects via g-estimation. arXiv preprint arXiv:2002.07285.

- Li et al. (2018) Li, F., K. L. Morgan, and A. M. Zaslavsky (2018). Balancing covariates via propensity score weighting. Journal of the American Statistical Association 113(521), 390–400.

- Marx et al. (2022) Marx, P., E. Tamer, and X. Tang (2022). Parallel trends and dynamic choices. arXiv preprint arXiv:2207.06564.

- Montiel Olea and Plagborg-Møller (2021) Montiel Olea, J. L. and M. Plagborg-Møller (2021). Local projection inference is simpler and more robust than you think. Econometrica 89(4), 1789–1823.

- Nakamura and Steinsson (2014) Nakamura, E. and J. Steinsson (2014). Fiscal stimulus in a monetary union: Evidence from us regions. American Economic Review 104(3), 753–792.

- Negahban et al. (2012) Negahban, S. N., P. Ravikumar, M. J. Wainwright, B. Yu, et al. (2012). A unified framework for high-dimensional analysis of -estimators with decomposable regularizers. Statistical science 27(4), 538–557.

- Nie et al. (2021) Nie, X., E. Brunskill, and S. Wager (2021). Learning when-to-treat policies. Journal of the American Statistical Association 116(533), 392–409.

- Plagborg-Møller (2019) Plagborg-Møller, M. (2019). Bayesian inference on structural impulse response functions. Quantitative Economics 10(1), 145–184.

- Rambachan and Roth (2023) Rambachan, A. and J. Roth (2023). A more credible approach to parallel trends. Review of Economic Studies, rdad018.

- Rambachan and Shephard (2019) Rambachan, A. and N. Shephard (2019). A nonparametric dynamic causal model for macroeconometrics. Available at SSRN 3345325.

- Robins (1986) Robins, J. (1986). A new approach to causal inference in mortality studies with a sustained exposure period—application to control of the healthy worker survivor effect. Mathematical modelling 7(9-12), 1393–1512.

- Robins et al. (2000) Robins, J. M., M. A. Hernan, and B. Brumback (2000). Marginal structural models and causal inference in epidemiology.

- Roth (2022) Roth, J. (2022). Pretest with caution: Event-study estimates after testing for parallel trends. American Economic Review: Insights 4(3), 305–322.

- Roth et al. (2023) Roth, J., P. H. Sant’Anna, A. Bilinski, and J. Poe (2023). What’s trending in difference-in-differences? a synthesis of the recent econometrics literature. Journal of Econometrics.

- Rust (1994) Rust, J. (1994). Structural estimation of markov decision processes. Handbook of econometrics 4, 3081–3143.

- Shi et al. (2018) Shi, C., A. Fan, R. Song, and W. Lu (2018). High-dimensional a-learning for optimal dynamic treatment regimes. Annals of statistics 46(3), 925–957.

- Stock and Watson (2018) Stock, J. H. and M. W. Watson (2018). Identification and estimation of dynamic causal effects in macroeconomics using external instruments. The Economic Journal 128(610), 917–948.

- Tchetgen and Shpitser (2012) Tchetgen, E. J. T. and I. Shpitser (2012). Semiparametric theory for causal mediation analysis: efficiency bounds, multiple robustness, and sensitivity analysis. Annals of statistics 40(3), 1816.

- Tran et al. (2019) Tran, L., C. Yiannoutsos, K. Wools-Kaloustian, A. Siika, M. Van Der Laan, and M. Petersen (2019). Double robust efficient estimators of longitudinal treatment effects: Comparative performance in simulations and a case study. The international journal of biostatistics 15(2).

- Vansteelandt et al. (2014) Vansteelandt, S., M. Joffe, et al. (2014). Structural nested models and g-estimation: the partially realized promise. Statistical Science 29(4), 707–731.

- Wainwright (2019) Wainwright, M. J. (2019). High-dimensional statistics: A non-asymptotic viewpoint, Volume 48. Cambridge University Press.

- Wolf and McKay (2022) Wolf, C. K. and A. McKay (2022). What can time-series regressions tell us about policy counterfactuals? Technical report, National Bureau of Economic Research.

- Wüthrich and Zhu (2023) Wüthrich, K. and Y. Zhu (2023). Omitted variable bias of lasso-based inference methods: A finite sample analysis. The review of economics and statistics 105(4), 982–997.

- Yiu and Su (2018) Yiu, S. and L. Su (2018). Covariate association eliminating weights: a unified weighting framework for causal effect estimation. Biometrika 105(3), 709–722.

- Yiu and Su (2020) Yiu, S. and L. Su (2020). Joint calibrated estimation of inverse probability of treatment and censoring weights for marginal structural models. Biometrics.

- Zhang et al. (2013) Zhang, B., A. A. Tsiatis, E. B. Laber, and M. Davidian (2013). Robust estimation of optimal dynamic treatment regimes for sequential treatment decisions. Biometrika 100(3), 681–694.