MDA for random forests: inconsistency, and a practical solution via the Sobol-MDA

Abstract

Variable importance measures are the main tools to analyze the black-box mechanisms of random forests. Although the mean decrease accuracy (MDA) is widely accepted as the most efficient variable importance measure for random forests, little is known about its statistical properties. In fact, the definition of MDA varies across the main random forest software. In this article, our objective is to rigorously analyze the behavior of the main MDA implementations. Consequently, we mathematically formalize the various implemented MDA algorithms, and then establish their limits when the sample size increases. This asymptotic analysis reveals that these MDA versions differ as importance measures, since they converge towards different quantities. More importantly, we break down these limits into three components: the first two terms are related to Sobol indices, which are well-defined measures of a covariate contribution to the response variance, widely used in the sensitivity analysis field, as opposed to the third term, whose value increases with dependence within covariates. Thus, we theoretically demonstrate that the MDA does not target the right quantity to detect influential covariates in a dependent setting, a fact that has already been noticed experimentally. To address this issue, we define a new importance measure for random forests, the Sobol-MDA, which fixes the flaws of the original MDA, and consistently estimates the accuracy decrease of the forest retrained without a given covariate, but with an efficient computational cost. The Sobol-MDA empirically outperforms its competitors on both simulated and real data for variable selection. An open source implementation in R and C++ is available online.

Keywords: MDA; Random forests; Sensitivity analysis; Sobol indices; Variable importance; Variable selection

1 Introduction

Random forests (Breiman, 2001) are a statistical learning algorithm, which aggregates a large number of trees to solve regression and classification problems, and achieves state-of-the-art performance on a wide range of problems. In particular, random forests exhibit a good behavior on high-dimensional or noisy data, without any parameter tuning, and are also well known for their robustness. However, they suffer from a major drawback: a given prediction is generated through a large number of operations, typically tens of thousands, which makes the interpretation of the prediction mechanism impossible. Because of this complexity, random forests are often qualified as black boxes. More generally, the interpretability of learning algorithms is receiving an increasingly high interest since this black-box characteristic is a strong practical limitation. For example, applications involving critical decisions, typically healthcare, require predictions to be justified. The most popular way to interpret random forests is variable importance analysis: covariates are ranked by decreasing order of their importance in the algorithm prediction process. Thus, specific variable importance measures were developed along with random forests (Breiman, 2001, 2003a). However, we will see that they may not target the right variable ranking to detect influential covariates in a dependent setting, and could therefore be improved. First, we present the objectives of variable importance. Second, we review the existing variable importance measures for random forests, and then conduct a theoretical analysis of their limitations. Finally, we introduce the Sobol-MDA algorithm, a new importance measure for random forests, which mimics the brute force algorithm of retraining the forest without a covariate to measure the accuracy decrease, but with a much higher computational efficiency. The Sobol-MDA is proved to be consistent, and outperforms the existing variable importance competitors for variable selection, as shown in the experiments. An implementation in R and C++ of the Sobol-MDA is available at https://gitlab.com/drti/sobolmda, and is based on ranger (Wright and Ziegler, 2017), a fast implementation of random forests.

2 Context and Objectives

2.1 Variable Importance for Random Forests.

There are essentially two importance measures for random forests: the mean decrease accuracy (MDA) (Breiman, 2001) and the mean decrease impurity (MDI) (Breiman, 2003a). The MDA measures the decrease of accuracy when the values of a given covariate are permuted, thus breaking its relation to the response variable and to the other covariates. On the other hand, the MDI sums the weighted decreases of impurity over all nodes that split on a given covariate, averaged over all trees in the forest. In both cases, a high value of the metric means that the covariate is used in many important operations of the prediction mechanism of the forest. Unfortunately, there is no precise and rigorous interpretation since these two definitions are purely empirical. Furthermore, in the last two decades, many empirical analyses have highlighted the flaws of the MDI (Strobl et al., 2007). Although Li et al. (2019), Zhou and Hooker (2021), and Loecher (2020) recently improved the MDI to partially remove its bias, Scornet (2020) demonstrated that the MDI is consistent under a strong and restrictive assumption: the regression function is additive and the covariates are independent. Otherwise, the MDI is ill-defined. Overall, the MDA is widely considered as the most efficient variable importance measure for random forests (Strobl et al., 2007; Ishwaran, 2007; Genuer et al., 2010; Boulesteix et al., 2012), and we therefore focus on the MDA. Although it is extensively used in practice, little is known about its statistical properties. To our knowledge, only Ishwaran (2007) and Zhu et al. (2015) provide theoretical analyses of modified versions of the MDA, but the asymptotic behavior of the original MDA algorithm (Breiman, 2001) is unknown: Ishwaran (2007) considers Breiman’s forests but simplifies the MDA procedure, whereas Zhu et al. (2015) considers the original MDA but assumes the independence of the covariates and an exponential concentration inequality on the random forest estimate, the latter being proved only for purely random forests, which do not use the data set to build the tree partitions. On the practical side, many empirical analyses provide evidence that when covariates are dependent, the MDA may fail to detect some relevant covariates (Archer and Kimes, 2008; Strobl et al., 2008; Nicodemus and Malley, 2009; Genuer et al., 2010; Auret and Aldrich, 2011; Toloşi and Lengauer, 2011; Gregorutti et al., 2017; Hooker et al., 2021; Mentch and Zhou, 2020). Several proposals (Mentch and Hooker, 2016; Candès et al., 2018; Williamson et al., 2021) were recently made to overcome this issue. Mentch and Hooker (2016) prove the asymptotic normality of random forests, which enables detection of whether the predictions of a forest built without a given covariate are significantly different from the ones of the original forest with all covariates. Alternatively, Candès et al. (2018) introduce model-X knockoffs, which rely on conditional randomization tests, where the relation between a covariate and the response variable is broken without modifying the joint distribution of the covariates. Finally, Williamson et al. (2021) propose to measure the decrease of accuracy between the original procedure and a new run without a given covariate. However, these methods have a much higher computational cost, as many model retrains are involved, and are in particular intractable in high dimension. Furthermore, it is critical to assess that the properties of a variable importance measure are in line with the final objective of the conducted analysis. In the following subsection, we review the possible goals of variable importance, and then introduce sensitivity analysis to deepen the theoretical understanding of the MDA.

2.2 Sensitivity Analysis

In practice, obtaining raw measures of variable importance is rarely the end goal. Rather, practitioners are frequently interested in using such measures to detect influential covariates to either (Genuer et al., 2010): (i) find a small number of covariates with a maximized accuracy, or (ii) detect and rank all influential covariates to focus on for further exploration with domain experts. Depending on which of these two objectives is of interest, different strategies should be used as the following example shows: if two influential covariates are strongly correlated, one must be discarded in the first case, while the two must be kept in the second case. Indeed, if two covariates convey the same statistical information, only one should be selected if the goal is to maximize the predictive accuracy with a small number of covariates, i.e., objective (i). On the other hand, these two covariates may be acquired differently and represent distinct physical quantities. Therefore, they may have different interpretations for domain experts, and both should be kept for objective (ii) of ranking all variables for interpretation.

Sensitivity analysis is the study of uncertainties in a system. The main goal is to apportion the uncertainty of a system response to the uncertainty of the different covariates. Iooss and Lemaître (2015) and Ghanem et al. (2017) provide detailed reviews of global sensitivity analysis. In particular, sensitivity analysis introduces well-defined importance measures of covariate contributions to the response variance: Sobol indices (Sobol, 1993; Saltelli, 2002) and Shapley effects (Shapley, 1953; Owen, 2014; Iooss and Prieur, 2019). These metrics are widely used to analyze computer code experiments, especially for the design of industrial systems. However, the literature about variable importance in the fields of statistical learning and machine learning rarely mentions sensitivity analysis. The reason of this hiatus is clear: until quite recently, sensitivity analysis was focused on independent covariates, whereas such an assumption is generally unreasonable in machine learning contexts. In the last years, Gregorutti (2015) first established a link between sensitivity analysis and the MDA: in the case of independent covariates, the theoretical counterpart of the MDA is the unnormalized total Sobol index, i.e., twice the amount of explained variance lost when a given covariate is removed from the model, which is the expected quantity for both objectives (i) and (ii) in this independent setting. Accordingly, the algorithm from Williamson et al. (2021) also estimates the total Sobol index when the accuracy metric is the explained variance, even when covariates are dependent, and although this connection is not explicitly mentioned. When one is using variable importance to select a small number of covariates while maximizing predictive accuracy, i.e. objective (i), the total Sobol index is clearly the relevant measure to eliminate the less influential covariates, as also suggested by Williamson et al. (2021). Additionally, Owen (2014) reintroduced Shapley effects, originally proposed in game theory (Shapley, 1953). Shapley effects exhibit very interesting properties for objective (ii), of ranking all variables for interpretation, as they equitably allocate the mutual contribution due to dependence and interactions to individual covariates. Shapley effects are now widely used by the machine learning community to interpret both tree ensembles and neural networks. SHAP values (Lundberg and Lee, 2017) also adapt Shapley effects for local interpretation of model predictions, and Lundberg et al. (2018) provide a fast algorithm for tree ensembles. Finally, we refer to Antoniadis et al. (2020) for a review of random forests and sensitivity analysis.

3 MDA Theoretical Limitations

3.1 MDA Definitions

The MDA was originally proposed by Breiman in his seminal article (Breiman, 2001), and works as follows. The values of a specific covariate are permuted to break its relation to the response variable. Then, the predictive accuracy is computed for this perturbed dataset. The difference between this degraded accuracy and the original one gives the importance of the covariate: a high decrease of accuracy means that the considered covariate has a strong influence on the prediction mechanism. However, a review of the literature on random forests and their software implementations reveals that there is no consensus on the exact mathematical formulation of the MDA. We focus on the most popular random forest algorithms: the R package randomForests (Liaw and Wiener, 2002) based on the original Fortran code from Breiman and Cutler, the fast R/C++ implementation ranger (Wright and Ziegler, 2017), the most widely used python machine learning library scikit-learn (Pedregosa et al., 2011) (RandomForestClassifier/RandomForestRegressor), and the R package randomForestSRC (Ishwaran and Kogalur, 2020), which implements survival forests in addition to the original algorithm. To give an order of magnitude, the typical number of users of each of these packages during the year 2020 is about half a million. A close inspection of their code exhibits that essentially three distinct definitions of the MDA are widely used. References and details about the MDA implementation in the package codes are provided in the Supplementary Material. The differences between the three MDA versions are twofold: the MDA can be computed based on the tree error or the whole forest error, and via a test set or out-of-bag samples, as summarized in Table 1. We first introduce the required notations, and then mathematically formalize these different MDA definitions.

| Algorithm | Package | Error Estimate | Data | ||

|---|---|---|---|---|---|

| Train-Test MDA |

|

Forest | Testing dataset | ||

| Breiman-Cutler MDA |

|

Tree | OOB sample | ||

| Ishwaran-Kogalur MDA |

|

Forest | OOB sample |

We define a standard regression setting with the following Assumption 1, as well as the random forest notations below.

Assumption 1.

The response variable follows , where the covariate vector admits a density over bounded from above and below by strictly positive constants, is continuous, and the noise is sub-Gaussian, independent of , and centered. A sample of independent random variables distributed as is available.

The random CART estimate is trained with and , where is used to generate the bootstrap sampling and the split randomization, and is a new observation. The component of used to resample the data is denoted . The random forest estimate aggregates -random CART, each of which is randomized by a component of . In the sequel, we consider a fixed index . Next, we define as the vector where the -th component is permuted between observations. Similarly, is the vector where the -th component is replaced by an independent copy of . Finally, we also introduce , as the random vector without the -th component. Now, we can detail the three MDA definitions, summarized in Table 1.

The most simple approach is taken by scikit-learn where the forest is fit with a training sample and the accuracy decrease is estimated with an independent testing sample . Throughout the article, we call the generalization error of the forest the expected squared error for a new observation, usually estimated with an independent sample. Thus, forest predictions are run for both the test set and its permuted version, and the corresponding mean squared errors are subtracted to give the generalization error increase, called the Train-Test MDA.

Definition 1 (Train/Test MDA).

The Train/Test MDA is defined by

This algorithm is the only MDA version implemented in scikit-learn, and is one possibility in randomForestSRC. Note that the Train/Test-MDA is straightforward to implement with any random forest package by simply running predictions.

In practice, splitting the sample in two parts for training and testing often hurts the accuracy of the procedure, then decreasing the accuracy of the MDA estimate. Since the data is bootstrapped prior to each tree growing, a portion of the sample is left out, which is called the out-of-bag sample and can be used to measure accuracy. Despite the lack of mathematical formulation in the original MDA introduction (Breiman, 2001), it seems clear that for each tree, the generalization error is estimated using its out-of-bag sample and the permuted version. Then, the two errors are subtracted and this difference is averaged across all trees to give the Breiman-Cutler MDA.

Definition 2 (Breiman-Cutler MDA).

If is the -th permuted out-of-bag sample for the -th tree and for , then the Breiman-Cutler MDA (BC-MDA) (Breiman, 2001) is defined by

where is the size of the out-of-bag sample of the -th tree.

Among the four main random forest implementations introduced above, only ranger and randomForestSRC exactly follow this original definition. In randomForests, the final quantity is normalized by the standard deviation of the generalization error differences. However, this procedure is questionable (Díaz-Uriarte and De Andres, 2006; Strobl and Zeileis, 2008): a non-influential covariate would constantly have a standard deviation close to zero, potentially leading to a high normalized MDA.

More importantly, observe that Breiman’s MDA definition is in fact a Monte-Carlo estimate of a random tree decrease of accuracy when a covariate is noised up. Since we are interested in the covariate influence in the entire forest, and not only in a single tree, it seems natural to extend the out-of-bag procedure to estimate the forest error (Ishwaran et al., 2008) as implemented in randomForestSRC: for each observation , we retrieve the random set of trees which do not involve in their construction because of the resampling step, formally defined by

We can take advantage of such batch of trees to define the out-of-bag random forest estimate by averaging the tree predictions considering only trees that belong to , i.e., for ,

It is therefore possible to estimate the random forest error using alone. Recall that for each -random tree, we randomly permute the -th component of the out-of-bag dataset to define , and we stress that the permutation is independent for each tree. Then, we define the permuted out-of-bag forest estimate as

These estimates enable to compute both the out-of-bag error of the forest and the inflated out-of-bag forest error when a covariate is noised up. Finally, the difference between these two errors forms the Ishwaran-Kogalur MDA. From an algorithmic point of view, the only difference with Breiman’s definition is the mechanism to aggregate tree predictions and compute the errors, as highlighted in Algorithms and of the Supplementary Material.

Definition 3 (Ishwaran-Kogalur MDA).

An asymptotic analysis of these three MDA versions, summarized in Table 1, reveals that they do not share the same theoretical counterpart. Consequently, they have different meanings and generate different variable rankings, from which divergent conclusions can be drawn. However, these MDA versions are used interchangeably in practice. The convergence of the MDA is established in the next subsection, and then the different theoretical counterparts are analyzed in the following subsection.

3.2 MDA Inconsistency

The out-of-bag estimate is involved in both the Breiman-Cutler MDA and Ishwaran-Kogalur MDA, but is also used in practice to provide a fast estimate of the random forest error. We begin our asymptotic analysis by a result on the efficiency of the out-of-bag estimate, stated in Proposition 1 below, which shows that the out-of-bag error consistently estimates the generalization error of the forest. This result will be later used to establish the convergence of the Ishwaran-Kogalur MDA. The only difference between the implemented algorithms and our theoretical results, is that the resampling in the forest growing is done without replacement to alleviate the mathematical analysis (Scornet et al., 2015; Mentch and Hooker, 2016; Wager and Athey, 2018). We define the number of subsampled training observations used to build each tree.

Proposition 1.

If Assumption 1 is satisfied, for a fixed sample size and , we have

First observe that, by construction of the set of trees , the out-of-bag estimate aggregates a smaller number of trees than in the standard forest: trees in average. Therefore, the errors of the out-of-bag and standard forest estimates are different quantities. To our knowledge, this is the first result which states the convergence of the out-of-bag error towards the forest error for any fixed sample size, with a fast rate of . This suggests that growing a large number of trees in the forest, which is computationally possible and what is done in practice, ensures that the out-of-bag estimate provides a good approximation of the forest error.

Next, the convergence of the three versions of the MDA holds under the following Assumption 2 of the consistency of a theoretical randomized CART. Since we are interested in the random forest interpretation through the MDA, it seems natural to conduct our analysis assuming that each tree of the forest is an efficient learner, i.e., consistent. To formalize such an assumption, we first define the variation of the regression function within a cell by

and secondly, we introduce the cell of the theoretical CART of depth (randomized with ) in which the observation falls.

Assumption 2.

The randomized theoretical CART tree built with the distribution of is consistent, that is, for all , almost surely,

At first glance, Assumption 2 seems quite obscure since it involves the theoretical CART. However, Scornet et al. (2015) show that Assumption 2 holds if the regression function is additive. Because the original CART (Breiman et al., 1984) is a greedy algorithm, Assumption 2 may not always be satisfied when the regression function has interaction terms. However, it holds if the CART algorithm is slightly modified to avoid splits close to the edges of cells, and the split randomization is slightly increased to have a positive probability to split in all directions at all nodes (Meinshausen, 2006; Wager and Athey, 2018). Indeed in that case, all cells become infinitely small as the tree depth increases, and therefore Assumption 2 holds by continuity of . Such modifications of CART have a negligible impact in practice on the random forest estimate since the cut threshold and the split randomization increase can be chosen arbitrarily small. Notice that such asymptotic regime is specifically analyzed in the next section.

As specified above, is the number of training observations subsampled without replacement to build each tree, and we define as the final number of terminal leaves in every tree. Notice that we can specify in or when needed, but we omit it in general to avoid cumbersome notations. In order to properly define the MDA procedures, the out-of-bag sample needs to be at least of size to enable permutations, i.e., . Finally, we need the following Assumption 3 on the asymptotic regime of the empirical forest as stated in Scornet et al. (2015), which essentially controls the number of terminal leaves with respect to the sample size to enforce the random forest consistency.

Assumption 3.

The asymptotic regime of , the size of the subsampling without replacement, and the number of terminal leaves is such that , for a fixed , , , and .

In the case of the Ishwaran-Kogalur MDA, the number of trees has to tend to infinity with the sample size to ensure convergence. To lighten notations, we drop the dependence of to .

Assumption 4.

The number of trees grows to infinity with the sample size : .

Theorem 1.

Theorem 1 reveals that the theoretical MDA counterparts are not identical across the different MDA definitions. Thus, covariates are ranked according to different criteria depending on the MDA version involved. We deepen this discussion in the following subsection.

3.3 MDA Analysis

The theoretical counterparts of the MDA established in Theorem 1 are hard to interpret since has a different distribution from the original covariate vector whenever components of are dependent. These different MDA versions are widely used in practice to assess the variable importance of random forests, but the relevance of such analyses completely relies on the ranking criteria or , according to Theorem 1. It is possible to deepen the discussion, observing that and are independent conditionally on by construction. It enables to break down the MDA limit using Sobol indices that are well-defined quantity to measure the contribution of a covariate to the response variance.

Definition 4 (Total Sobol Index).

We also introduce a new sensitivity index: the total Sobol index computed for the input vector . We call it the marginal total Sobol index, since the distribution of is the product of the marginal distributions of and . It can take high values even when is strongly correlated with other covariates, as opposed to the original total Sobol index. We derive the main properties of this new sensitivity index below, proved in the Supplementary Material.

Definition 5 (Marginal Total Sobol Index).

The marginal total Sobol index of covariate is defined by

Property 1 (Marginal Total Sobol Index).

If Assumption 1 is satisfied, the marginal total Sobol index satisfies the following properties.

-

(a)

.

-

(b)

If the components of are independent, then we have .

-

(c)

If is additive, i.e. , then we have , and .

Notice that the last property states that for additive regression functions, which may also hold in the general case with interactions. However, such an extension is out of the scope of the article. We also mention that total Sobol indices can be generalized to a group of covariates. It is now possible to break down the MDA limits as the sum of positive terms using total Sobol indices and the following quantity , further discussed below and defined as

Proposition 2.

Importantly, each term of the decompositions of Proposition 2 is positive, and can be interpreted alone. We denote and .

is the non-normalized total Sobol index that has a straightforward interpretation: the amount of explained output variance lost when is removed from the model. This quantity is really the information one is looking for when computing the MDA for objective (i) of finding a small group of the most predictive covariates.

is the non-normalized marginal total Sobol index. Its interpretation is more difficult. Intuitively, in the case of , contributions due to the dependence between and are excluded because of the conditioning on . For , this dependence is ignored, and therefore such removal does not take place. For example, if has a strong influence on the regression function but is highly correlated with other covariates, then is small, whereas is high. For objective (i), one wants to keep only one covariate of a group of highly influential and correlated inputs, and therefore can be a misleading component.

is not a known measure of importance, and seems to have no clear interpretation: it measures how the permutation shifts the average of over the -th covariate, and thus characterizes the structure of and the dependence of combined. is null if covariates are independent. The value of increases with dependence, and this effect can be amplified by interactions between covariates.

Overall, all MDA definitions are misleading with respect to both objectives and since they include in their theoretical counterparts. In the Supplementary Material, we provide an analytical example to show how the MDA can fail to detect relevant covariates when the data has both dependence and interactions. From a practical perspective, it is only possible to conclude in general that the Breiman-Cutler MDA or Ishwaran-Kogalur MDA should be used rather than the Train/Test-MDA. Indeed, on the one hand we only have access to one finite sample in practice, which has to be split in two parts to use the Train/Test-MDA, hurting the forest accuracy. On the other hand, it is possible to grow many trees at a reasonable linear computational cost, and Proposition 1 ensures that the out-of-bag estimate is efficient in this case. With additional assumptions on the data distribution, the Breiman-Cutler MDA and the Ishwaran-Kogalur MDA recover meaningful theoretical counterparts.

Corollary 1.

Thus, Corollary 1 states that when covariates are independent, all MDA versions estimate the same quantity, the unnormalized total Sobol index (up to a factor ), as stated in Gregorutti (2015). However, since the Train/Test-MDA is based on a portion of the training sample, the Breiman-Cutler MDA on the accuracy of a single tree, and the Ishwaran-Kogalur MDA on the accuracy of the forest, the Ishwaran-Kogalur MDA appears to be a more efficient estimate than the two others in this independent setting. Also notice that in the case of independent covariates, the total Sobol index is a relevant measure for both objectives (i) and (ii). Interestingly, when covariates are dependent but without interactions, all MDA versions then estimate the marginal total Sobol index, as stated in the following Corollary.

Corollary 2.

In this correlated and additive setting, the MDA versions now estimate the marginal total Sobol index, which takes the simple form stated in Property 1-(c), but is difficult to estimate with a finite sample because of dependence. The MDA is thus quite relevant for objective (ii) of ranking all variables for interpretation: while contributions due to the dependence between covariates are removed in the total Sobol index, it is not the case here. Also notice that covariates with no influence in the regression function are excluded. If we further assume that the regression function is linear, the MDA limits can be written with the linear coefficients and the input variances as stated in Gregorutti et al. (2015); Hooker et al. (2021).

Remark 1 (Distribution Support).

Our asymptotic analysis relies on Assumption 1, which states that the support of the covariate distribution is a hypercube. Without such geometrical assumption, the support of may differ from the support of in the dependent case. It means that the random forest estimate may be applied on regions with no training samples, resulting in inconsistent forest and MDA estimates, and then in a low predictive accuracy (Hooker et al., 2021). This is an additional source of confusion of the MDA when inputs are dependent, induced by the permutation trick.

4 Sobol-MDA

4.1 Objectives

When covariates are dependent, the MDA fails to estimate the total Sobol index, which is our true objective to solve problem (i) of finding a small group of the most predictive covariates, as shown in Section 3. Therefore, we introduce an improved MDA procedure for random forests: the Sobol-MDA, that consistently estimates the total Sobol index even when covariates are dependent and have interactions. The Sobol-MDA is able to identify the less relevant covariates, as the total Sobol index is the proportion of response explained variance lost when a given covariate is removed from the model. For example, if two influential variables are strongly correlated, the Sobol-MDA takes small values for these two variables, since the model accuracy does not decrease much when one of them is removed. Therefore, a recursive feature elimination procedure based on the Sobol-MDA is highly efficient for our objective (i) of selecting a small number of covariates while maximizing predictive accuracy. Notice that training a random forest without the covariate of interest would also enable to get an estimate of the total Sobol index, and is the approach taken by Williamson et al. (2021). However, the Sobol-MDA only requires to perform forest predictions, which is computationally faster than the forest growing, and scales with the dimension as opposed to this brute force approach from Williamson et al. (2021). Similarly, Mentch and Hooker (2016) detect influential covariates with hypothesis tests based on the asymptotic normality of random forests and a model retrain without the considered covariate. However, this approach is only valid in specific forest settings (Peng et al., 2022), which considerably reduce the accuracy of tree ensembles compared to Breiman’s algorithm, and therefore the ability to identify influential covariates. It is also possible to estimate total Sobol indices with existing algorithms which are not specific to random forests. Indeed, this type of methods only requires a black-box estimate to generate predictions from given values of the covariates. Initially, Mara et al. (2015) introduce Monte-Carlo algorithms for the estimation of total Sobol indices in a dependent setting. The first step of the method is to generate a sample from the conditional distributions of the covariates. However, in our setting defined in Assumption 1, we do not have access to these conditional distributions, and their estimation is a difficult problem when only a limited sample is available. Consequently, the approach of Mara et al. (2015) is not really appropriate for our setting. Notice that the promising approach from Candès et al. (2018) to detect relevant covariates also requires to sample from the conditional distributions of the covariates, and is therefore not adapted to our problem as well. In the sequel, we describe the Sobol-MDA algorithm, along with its main properties.

4.2 Sobol-MDA Algorithm

The key feature of the original MDA procedures is to permute the values of the -th covariate to break its relation to the response, and then compute the degraded accuracy of the forest. Observe that this is strictly equivalent to drop the original dataset down each tree of the forest, but when a sample hits a split involving covariate , it is randomly sent to the left or right side with a probability equal to the proportion of points in each child node. This fact highlights that the goal of the MDA is simply to perturb the tree prediction process to cancel out the splits on covariate . Besides, notice that this point of view on the MDA procedure (using the original dataset and noisy trees) is introduced by Ishwaran (2007) to conduct a theoretical analysis of a modified version of the MDA. Here, our Sobol-MDA algorithm builds on the same principle of ignoring splits on covariate , such that the noisy CART tree predicts , similarly to the tree that is rebuilt by removing from the training data. It enables to recover the proper theoretical counterpart: the unnormalized total Sobol index, i.e., . To achieve this, we leave aside the permutation trick, and use another approach to cancel out a given covariate in the tree prediction process: the partition of the covariate space obtained with the terminal leaves of the original tree is projected along the -th direction, as shown in Figure 1, and the outputs of the cells of this new projected partition are recomputed with the training data. From an algorithmic point of view, this procedure is quite straightforward as we will see below, and enables to get rid of covariate in the tree estimate. Then, it is possible to compute the accuracy of the associated out-of-bag projected forest estimate, subtract it from the original accuracy, and normalize the obtained difference by to obtain the Sobol-MDA for .

Interestingly, to compute SHAP values for tree ensembles, Lundberg et al. (2018) also introduce an algorithm to modify the CART predictions to estimate . More precisely, they propose the following recursive algorithm: the observation is dropped down the tree, but when a split on covariate is hit, is sent to both the left and right children nodes. Then, falls in multiple terminal cells of the tree. The final prediction is the weighted average of the cell outputs, where the weight associated to a terminal leave is given by an estimate of : the product of the empirical probabilities to choose the side that leads to A at each split on covariate in the path of the original tree. At first sight, their approach seems suited to estimate total Sobol indices, but unfortunately, the weights are properly estimated by such procedure only if the covariates are independent. Therefore, as highlighted in Aas et al. (2021), this algorithm gives biased predictions in a correlated setting.

We improve over Lundberg et al. (2018) with the Projected-CART algorithm, formalized in Algorithm in the Supplementary Material: both training and out-of-bag samples are dropped down the tree and sent on both right and left children nodes when a split on covariate is met. Again, each observation may belong to multiple cells at each level of the tree. For each out-of-bag sample, the associated prediction is the output average over all training observations that belong to the same collection of terminal leaves. In other words, we compute the intersection of these terminal leaves to select the training observations belonging to every cell of this collection to estimate the prediction. This intersection gives the projected cell. Overall, this mechanism is equivalent to projecting the tree partition on the subspace span by , as illustrated in Figure 1 for and . Recall that is the cell of the original tree partition where falls, whereas the associated cell of the projected partition is denoted . Formally, we respectively denote the associated projected tree and projected out-of-bag forest estimates as and , respectively defined by

The Projected-CART algorithm provides two sources of improvements over Lundberg et al. (2018): first, the training data points are dropped down the modified tree to recompute the cell outputs, and thus is directly estimated in each cell. Secondly, the projected partition is finer than in the original tree, which mitigates masking effects (when an influential covariate is not often selected in the tree splits because of other highly correlated covariates).

Finally, the Sobol-MDA estimate is given by the normalized difference of the squared error of the out-of-bag projected forest with the out-of-bag error of the original forest. Formally, we define the Sobol-MDA as

where is the standard variance estimate of the response . An implementation in R and C++ of the Sobol-MDA is available at https://gitlab.com/drti/sobolmda and is based on ranger (Wright and Ziegler, 2017), a fast implementation of random forests. Given an initial random forest, the Sobol-MDA algorithm has a computational complexity of , which is in particular independent of the dimension , and quasi-linear with the sample size . On the other hand, the brute force approach from Williamson et al. (2021) has a complexity of , which is quadratic with the dimension and therefore intractable in high-dimensional settings, as opposed to the Sobol-MDA. Additional details are provided in the Supplementary Material.

Remark 2 (Empty Cells).

Some cells of the projected partition may contain no training samples. Consequently, the prediction for a new query point falling in such cells is undefined. In practice, the Projected-CART algorithm uses the following strategy to avoid empty cells. Recall that each level of the tree defines a partition of the input space (if a terminal leave occurs before the final tree level, it is copied down the tree at each level), and that a projected partition can thus be associated to each tree level. When a new observation is dropped down the tree, if it falls in an empty cell of the projected partition at a given tree level, the prediction is computed using the previous level. Notice that empty cells cannot occur in the partitions associated to the root and the first level of the tree by construction. Therefore, this mechanism enforces that the projected tree estimate is well defined over the full covariate space.

4.3 Sobol-MDA Consistency

The original MDA versions do not converge towards the total Sobol index, which is the relevant quantity for our objective (i) of finding a small group of the most predictive covariates, as stated in Proposition 2. On the other hand, the Sobol-MDA is consistent as stated below. Before introducing this convergence result, we need to introduce additional assumptions. Indeed, in Section 3, we show the convergence of the different MDA versions provided that the forest is an efficient estimate, i.e. consistent. To enforce the consistency of random forests, we used Assumption 2 which controls the variation of the regression function in each cell of the theoretical tree: . Because the covariates may be dependent, Assumption 2 does not imply the same property for the projected partition. Therefore, we cannot directly build on Scornet et al. (2015) to prove the consistency of the Sobol-MDA. Thus, we take another route and define a new Assumption 5 which brings two modifications to the random forest algorithm.

Assumption 5.

A node split is constrained to generate child nodes with at least a small fraction of the parent node observations. Secondly, the split selection is slightly modified: at each tree node, the number mtry of covariates drawn to optimize the split is set to with a small probability . Otherwise, with probability , the default value of mtry is used.

Importantly, since and can be chosen arbitrarily small, the modifications of Assumption 5 are mild. Besides, notice that this assumption follows Meinshausen (2006) and Wager and Athey (2018): we slightly modify the random forest algorithm to enforce empirical cells to become infinitely small as the sample size increases. The projected forest inherits this property and an asymptotic analysis from Györfi et al. (2006) gives the consistency of the Sobol-MDA, provided that the complexity of tree partitions is appropriately controlled. If an original tree has terminal leaves, the associated projected partition may have a higher number of terminal leaves, at most . Thus, we introduce Assumption 6, which slightly modifies Assumption 3 with a more restrictive regime for the number of terminal leaves in the original trees.

Assumption 6.

The asymptotic regime of , the size of the subsampling without replacement, and the number of terminal leaves is such that , for a fixed , , , and .

The Projected-CART algorithm ignores the splits based on the -th covariate, and the associated out-of-bag projected forest consistently estimates under Assumptions 1, 5, and 6, which leads to the Sobol-MDA consistency towards the total Sobol index, as stated below.

According to Theorem 2, the Sobol-MDA targets the appropriate quantity for objective (i), of selecting a small number of covariates while maximizing accuracy, whereas original MDA versions target a biased quantity, as stated in Proposition 2. Notice that the brute force approach of retraining the forest without covariate also estimates the total Sobol index, as proved in Theorem of the Supplementary Material. However, the brute force method has a quadratic computational complexity with respect to the dimension , and is thus intractable in high dimensional settings. Since the Sobol-MDA complexity is independent of , our approach is much more computationally efficient and outperforms its competitors, as shown in the next subsections.

4.4 Experiments with Simulated Data

We conduct three batches of experiments. First, we use the analytical example of the Supplementary Material, and show empirically that the Sobol-MDA leads to the accurate importance variable ranking, while original MDA versions do not. Next, we simulate a typical setting where several groups of covariates are strongly correlated and only few covariates are involved in the regression function. In such difficult setting, the Sobol-MDA identifies the relevant covariates, as opposed to its competitors. Finally, we apply the recursive feature elimination algorithm on real data to show the performance improvement of the Sobol-MDA for variable selection.

We first consider the analytical example of the Supplementary Material, where the data has both dependence and interactions. In this example, the covariates are distributed as a Gaussian vector with , and the regression function is given by

Here, we set , , for all covariates . The correlation coefficients are set to and , and other covariance terms are null. Finally, we define the model response as , where is an independent centered Gaussian noise whose variance verifies . Then, we run the following experiment: first, we generate a sample of size and distributed as the Gaussian vector . Next, a random forest of trees is fit with and we compute the Breiman-Cutler MDA, Ishwaran-Kogalur MDA, the algorithm from Williamson et al. (2021) denoted by , and the Sobol-MDA. To enable comparisons, the Breiman-Cutler MDA is normalized by , and the Ishwaran-Kogalur MDA by , as suggested by Proposition 2. To show the improvement of our Projected-CART algorithm, we also compute the Sobol-MDA using the algorithm from Lundberg et al. (2018), denoted . All results are reported in Table 2, along with the theoretical counterparts of the estimates, and the covariates are ranked by decreasing values of the theoretical total Sobol index since it is the value of interest: , then and , and finally and .

| 0.47 | 0.37 (0.03) | 0.47 | 0.43 (0.02) | 0.47 | 0.45 (0.03) | 0.42 (0.06) | 0.43 (0.03) | |

| 0.21 | 0.10 (0.02) | 0.37 | 0.14 (0.01) | 0.10 | 0.08 (0.01) | 0.06 (0.04) | 0.13 (0.01) | |

| 0.21 | 0.09 (0.01) | 0.37 | 0.13 (0.01) | 0.10 | 0.08 (0.01) | 0.06 (0.04) | 0.13 (0.01) | |

| 0.64 | 0.24 (0.02) | 1.0 | 0.29 (0.02) | 0.07 | 0.05 (0.01) | 0.03 (0.04) | 0.22 (0.02) | |

| 0.64 | 0.24 (0.02) | 1.0 | 0.28 (0.02) | 0.07 | 0.05 (0.01) | 0.03 (0.04) | 0.23 (0.01) |

Thus, only the Sobol-MDA computed with the Projected-CART algorithm and Williamson et al. (2021) rank the covariates in the same appropriate order than the total Sobol index. In particular, and have a higher total Sobol index than covariates and because of the stronger correlation between and than between and . For all the other importance measures, and are more important than and . For the original MDA, this is essentially due to the term , which increases with correlation. Since the explained variance of the random forest is in this experiment, all estimates have a negative bias. The bias of the Breiman-Cutler MDA and Ishwaran-Kogalur MDA dramatically increases with correlation. Indeed, a strong correlation between covariates leaves some regions of the input space free of training data. However, the out-of-bag permuted sample may fall in these regions, regions for which the forest has to extrapolate, resulting in a low predictive accuracy, and then in a high bias of the Breiman-Cutler MDA and Ishwaran-Kogalur MDA for correlated covariates. Finally, the Sobol-MDA computed with the algorithm of (Lundberg et al., 2018) is biased as suggested by (Aas et al., 2021), and the bias also seems to increase with correlation.

We then consider the following problem inspired by Archer and Kimes (2008); Gregorutti et al. (2017) and related to gene expressions. The goal is to identify relevant covariates among several groups of many strongly correlated covariates. More precisely, we define , a random vector of dimension , composed of independent groups of covariates. Each group is a centered gaussian random vector where two distinct components have a correlation of and the variance of each component is . The regression function only involves one covariate from each group, and is simply defined by

Finally, we define the model response as , where is an independent gaussian noise (). Next, a sample of size is generated based on the distribution of , and a random forest of trees is fit.

| 0.035 | |

| 0.005 | |

| 0.004 | |

| 0.004 | |

| 0.002 | |

| 0.002 | |

| 0.001 | |

| 0.001 | |

| 0.048 | |

| 0.010 | |

| 0.008 | |

| 0.008 | |

| 0.007 | |

| 0.007 | |

| 0.006 | |

| 0.006 | |

| 0.056 | |

| 0.009 | |

| 0.007 | |

| 0.005 | |

| 0.005 | |

| 0.005 | |

| 0.005 | |

| 0.005 | |

| 0.042 | |

| 0.031 | |

| 0.029 | |

| 0.029 | |

| 0.029 | |

| 0.028 | |

| 0.028 | |

| 0.027 | |

Thus, Tables 3 and 4 show that the Sobol-MDA identifies the five relevant covariates, whereas the Breiman-Cutler MDA, Ishwaran-Kogalur MDA, and Williamson et al. (2021) identify some noisy covariates among the top five. In this additive and correlated example, Corollary 2 states that all MDA algorithms have an appropriate theoretical counterpart to identify the five relevant covariates involved in the regression function, because these five covariates are mutually independent. However, in this finite sample setting, the original MDA versions give a high importance to the covariates of the first group because of their correlation with the most influential covariate . Since the Ishwaran-Kogalur MDA is based on the forest error, it outperforms the Breiman-Cutler MDA, which relies on the tree error. Quite surprisingly, Williamson et al. (2021) is the worst performing algorithm although it uses a brute force approach by retraining the forest without a given covariate to consistently estimate its total Sobol index, the appropriate theoretical counterpart. In fact, the multiple layers of data splitting involved in Williamson et al. (2021) generate a high variance of the associated estimate, whereas the MDA and the Sobol-MDA operate with a given dataset and a given initial forest structure to compute the decrease of accuracy, resulting in finer estimates and a higher performance to detect irrelevant covariates.

4.5 Experiments for Variable Selection with Real Data

The recursive feature elimination algorithm is originally introduced by Guyon et al. (2002) to perform variable selection with SVM. Gregorutti et al. (2017) apply the recursive feature elimination algorithm to random forests with the MDA as importance measure. The principle is to discard the less relevant covariates one by one, and is summarized in Algorithm in the Supplementary Material. Thus, the recursive feature elimination algorithm is a relevant strategy for our objective (i) of finding a small group of the most predictive covariates. At each step of the algorithm, the goal is to detect the less relevant covariates based on the trained model. Since the total Sobol index measures the proportion of explained response variance lost when a given covariate is removed, the optimal strategy is therefore to discard the covariate with the smallest total Sobol index. The Sobol-MDA directly estimates the total Sobol index, and therefore improves the performance of the recursive feature elimination procedure with respect to the original MDA, as shown in the following experiments. Indeed, the original MDA inflates the importance of dependent covariates, which leads to discard influential independent covariates, in favor of covariates which are related to the response only through correlation with others.

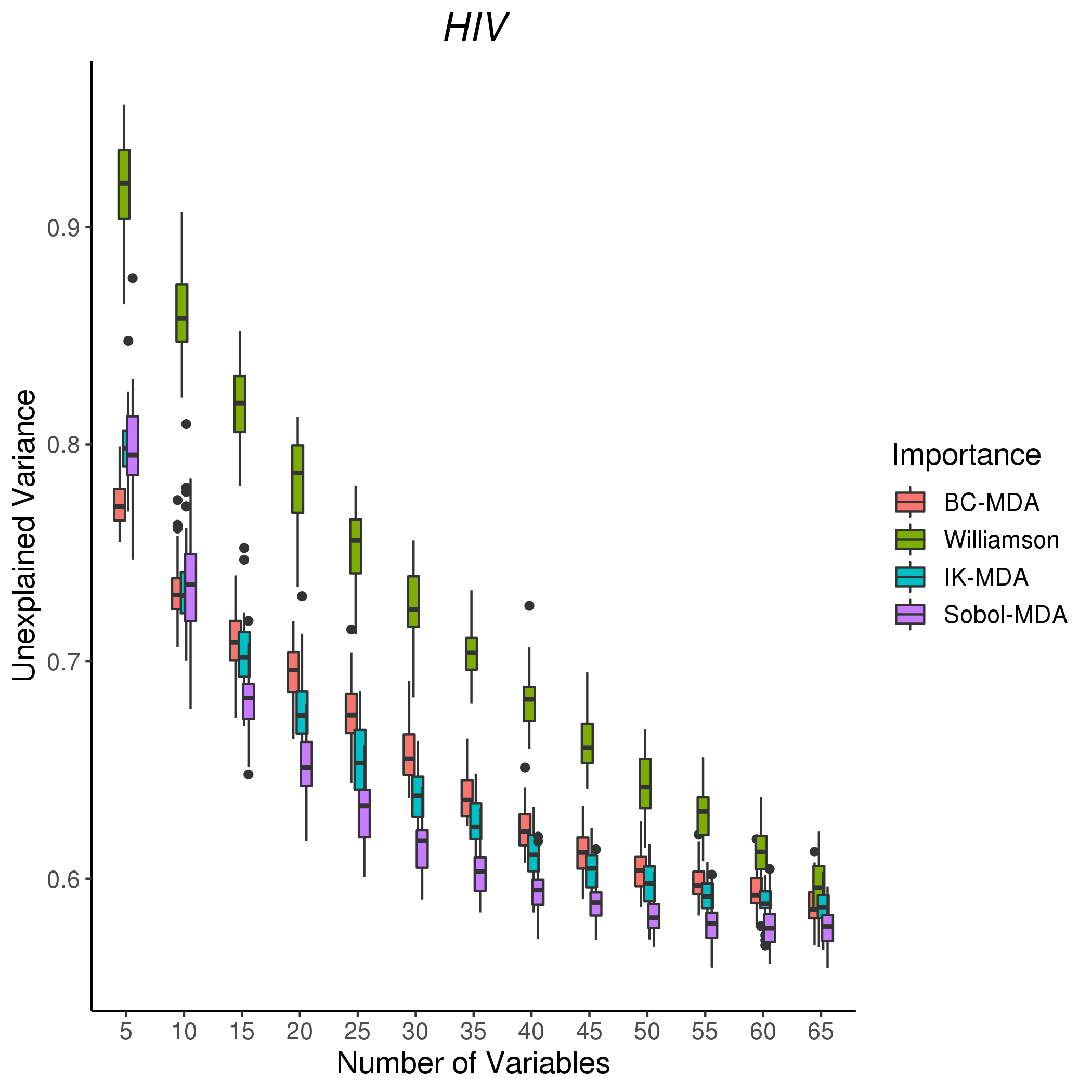

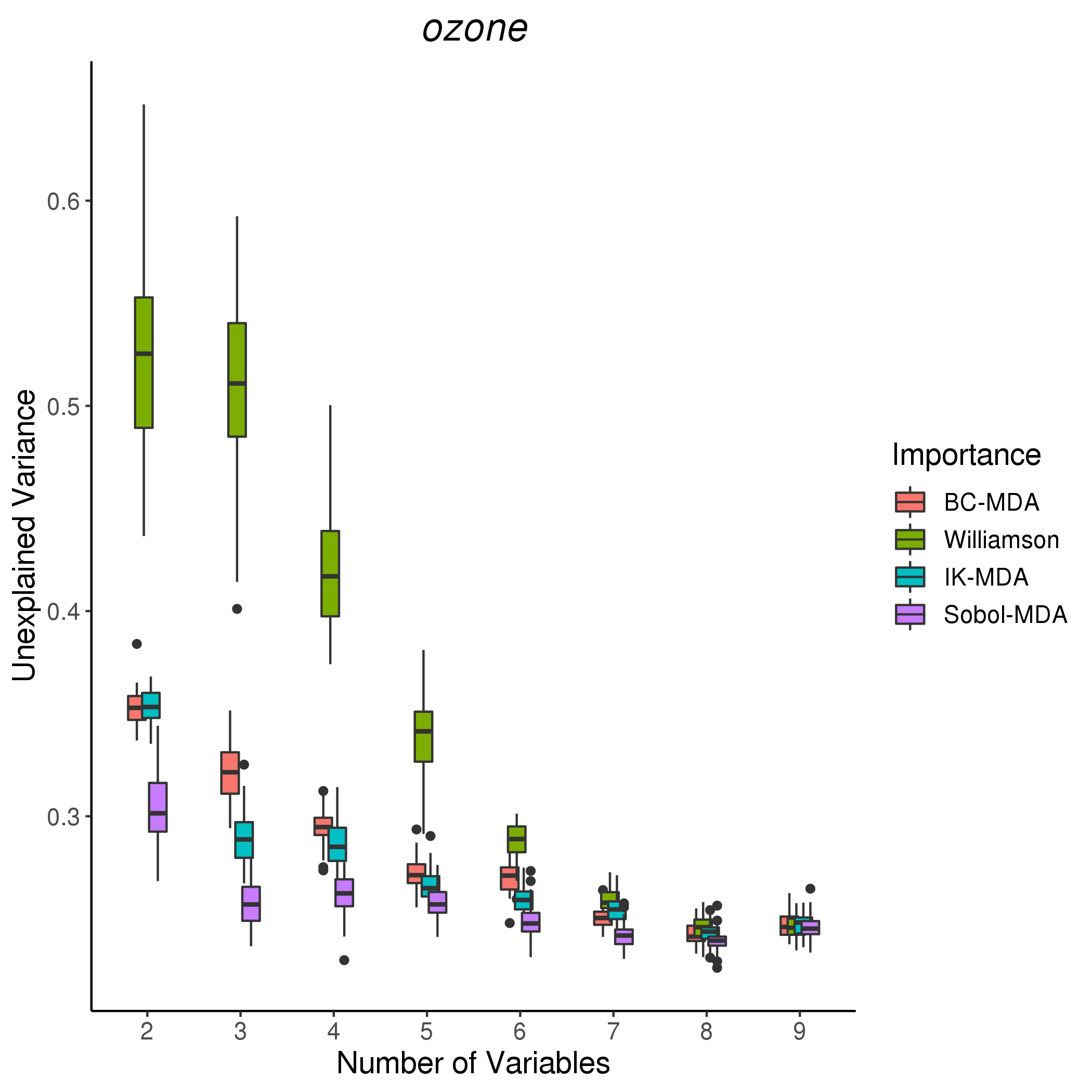

The recursive feature elimination algorithm is illustrated with the “Ozone” data (Dua and Graff, 2017) and the high-dimensional dataset “HIV” as suggested in Williamson et al. (2021), and run using the original MDA, the Sobol-MDA, and Williamson et al. (2021). At each step of the recursive feature elimination algorithm, the explained variance of the forest is retrieved. Following Gregorutti et al. (2017), we do not use the out-of-bag error since it gives optimistically biased results, but use instead a -fold cross-validation, repeated times to get uncertainties: the forest and the associated importance measure are computed with folds, and the error is estimated with the -th fold. Thus, Figure 2 highlights that the Sobol-MDA leads to a more efficient variable selection than all competitors for the “HIV” and “Ozone” datasets. We refer to the Supplementary Material for additional experiments. Notice that the Ishwaran-Kogalur MDA performs better than the Breiman-Cutler MDA, as expected from their theoretical counterparts stated in Proposition 2. Finally the algorithm from Williamson et al. (2021) is the worst performing approach because of the data splitting procedure, as explained in the previous subsection.

Acknowledgement

We thank the referees and the editors for their relevant suggestions to improve the article.

References

- Aas et al. (2021) K. Aas, M. Jullum, and A. Løland. Explaining individual predictions when features are dependent: More accurate approximations to Shapley values. Artificial Intelligence, 298:103502, 2021.

- Antoniadis et al. (2020) A. Antoniadis, S. Lambert-Lacroix, and J.-M. Poggi. Random forests for global sensitivity analysis: a selective review. Reliability Engineering & System Safety, 206:107–312, 2020.

- Archer and Kimes (2008) K.J. Archer and R.V. Kimes. Empirical characterization of random forest variable importance measures. Computational Statistics & Data Analysis, 52:2249–2260, 2008.

- Auret and Aldrich (2011) L. Auret and C. Aldrich. Empirical comparison of tree ensemble variable importance measures. Chemometrics and Intelligent Laboratory Systems, 105:157–170, 2011.

- Benoumechiara (2019) N. Benoumechiara. Treatment of dependency in sensitivity analysis for industrial reliability. PhD thesis, Sorbonne Université ; EDF R&D, 2019.

- Boulesteix et al. (2012) A.-L. Boulesteix, S. Janitza, J. Kruppa, and I.R. König. Overview of random forest methodology and practical guidance with emphasis on computational biology and bioinformatics. Wiley Interdisciplinary Reviews: Data Mining and Knowledge Discovery, 2:493–507, 2012.

- Breiman (2001) L. Breiman. Random forests. Machine Learning, 45:5–32, 2001.

- Breiman (2003a) L. Breiman. Setting up, using, and understanding random forests v3.1. Technical report, UC Berkeley, Department of Statistics, 2003a.

- Breiman et al. (1984) L. Breiman, J.H. Friedman, R.A. Olshen, and C.J. Stone. Classification and Regression Trees. Chapman & Hall/CRC, Boca Raton, 1984.

- Candès et al. (2018) E.J. Candès, Y. Fan, L. Janson, and J. Lv. Panning for gold: ‘Model-X’ knockoffs for high-dimensional controlled variable selection. Journal of the Royal Statistical Society Series B, 80(13):551–577, 2018.

- Díaz-Uriarte and De Andres (2006) R. Díaz-Uriarte and S.A. De Andres. Gene selection and classification of microarray data using random forest. BMC Bioinformatics, 7:1–13, 2006.

- Dua and Graff (2017) D. Dua and C. Graff. UCI machine learning repository, 2017. URL http://archive.ics.uci.edu/ml.

- Genuer et al. (2010) R. Genuer, J.-M. Poggi, and C. Tuleau-Malot. Variable selection using random forests. Pattern Recognition Letters, 31:2225–2236, 2010.

- Ghanem et al. (2017) R. Ghanem, D. Higdon, and H. Owhadi. Handbook of Uncertainty Quantification. Springer, New York, 2017.

- Gregorutti (2015) B. Gregorutti. Random forests and variable selection : analysis of the flight data recorders for aviation safety. PhD thesis, Université Pierre et Marie Curie - Paris VI, 2015.

- Gregorutti et al. (2015) B. Gregorutti, B. Michel, and P. Saint-Pierre. Grouped variable importance with random forests and application to multiple functional data analysis. Computational Statistics & Data Analysis, 90:15–35, 2015.

- Gregorutti et al. (2017) B. Gregorutti, B. Michel, and P. Saint-Pierre. Correlation and variable importance in random forests. Statistics and Computing, 27:659–678, 2017.

- Guyon et al. (2002) I. Guyon, J. Weston, S. Barnhill, and V. Vapnik. Gene selection for cancer classification using support vector machines. Machine learning, 46:389–422, 2002.

- Györfi et al. (2006) L. Györfi, M. Kohler, A. Krzyzak, and H. Walk. A distribution-free theory of nonparametric regression. Springer, New York, 2006.

- Hooker et al. (2021) G. Hooker, L. Mentch, and S. Zhou. Unrestricted permutation forces extrapolation: variable importance requires at least one more model, or there is no free variable importance. Statistics and Computing, 31:1–16, 2021.

- Iooss and Prieur (2019) B. Iooss and C. Prieur. Shapley effects for sensitivity analysis with correlated inputs: comparisons with Sobol’indices, numerical estimation and applications. International Journal for Uncertainty Quantification, 9, 2019.

- Iooss and Lemaître (2015) Bertrand Iooss and Paul Lemaître. A review on global sensitivity analysis methods. In Uncertainty Management in Simulation-Optimization of Complex Systems, pages 101–122. Springer, Boston, 2015.

- Ishwaran (2007) H. Ishwaran. Variable importance in binary regression trees and forests. Electronic Journal of Statistics, 1:519–537, 2007.

- Ishwaran and Kogalur (2020) H. Ishwaran and U.B. Kogalur. Fast Unified Random Forests for Survival, Regression, and Classification (RF-SRC), 2020. URL https://cran.r-project.org/package=randomForestSRC. R package version 2.9.3.

- Ishwaran et al. (2008) H. Ishwaran, U.B. Kogalur, E.H. Blackstone, and M.S. Lauer. Random survival forests. The Annals of Applied Statistics, 2:841–860, 2008.

- Kucherenko et al. (2012) S. Kucherenko, S. Tarantola, and P. Annoni. Estimation of global sensitivity indices for models with dependent variables. Computer Physics Communications, 183:937–946, 2012.

- Li et al. (2019) X. Li, Y. Wang, S. Basu, K. Kumbier, and B. Yu. A debiased MDI feature importance measure for random forests. In Advances in Neural Information Processing Systems, volume 32, pages 8049–8059, New York, 2019. Curran Associates, Inc.

- Liaw and Wiener (2002) A. Liaw and M. Wiener. Classification and regression by randomforest. R News, 2:18–22, 2002.

- Loecher (2020) Markus Loecher. Unbiased variable importance for random forests. Communications in Statistics-Theory and Methods, pages 1–13, 2020.

- Lundberg and Lee (2017) S.M. Lundberg and S.-I. Lee. A unified approach to interpreting model predictions. In Advances in Neural Information Processing Systems, volume 30, pages 4765–4774, New York, 2017. Curran Associates, Inc.

- Lundberg et al. (2018) S.M. Lundberg, G.G. Erion, and S.-I. Lee. Consistent individualized feature attribution for tree ensembles. arXiv preprint arXiv:1802.03888, 2018.

- Mara et al. (2015) T. A Mara, S. Tarantola, and P. Annoni. Non-parametric methods for global sensitivity analysis of model output with dependent inputs. Environmental Modelling & Software, 72:173–183, 2015.

- Meinshausen (2006) N. Meinshausen. Quantile regression forests. Journal of Machine Learning Research, 7:983–999, 2006.

- Mentch and Hooker (2016) L. Mentch and G. Hooker. Quantifying uncertainty in random forests via confidence intervals and hypothesis tests. Journal of Machine Learning Research, 17:841–881, 2016.

- Mentch and Zhou (2020) Lucas Mentch and Siyu Zhou. Getting better from worse: augmented bagging and a cautionary tale of variable importance. arXiv preprint arXiv:2003.03629, 2020.

- Nicodemus and Malley (2009) K.K. Nicodemus and J.D. Malley. Predictor correlation impacts machine learning algorithms: implications for genomic studies. Bioinformatics, 25:1884–1890, 2009.

- Owen (2014) A.B. Owen. Sobol’indices and Shapley value. SIAM/ASA Journal on Uncertainty Quantification, 2:245–251, 2014.

- Pedregosa et al. (2011) F. Pedregosa, G. Varoquaux, A. Gramfort, V. Michel, B. Thirion, O. Grisel, M. Blondel, P. Prettenhofer, R. Weiss, V. Dubourg, J. Vanderplas, A. Passos, D. Cournapeau, M. Brucher, M. Perrot, and E. Duchesnay. Scikit-learn: Machine learning in Python. Journal of Machine Learning Research, 12:2825–2830, 2011.

- Peng et al. (2022) Wei Peng, Tim Coleman, and Lucas Mentch. Rates of convergence for random forests via generalized U-statistics. Electronic Journal of Statistics, 16(1):232 – 292, 2022. doi: 10.1214/21-EJS1958. URL https://doi.org/10.1214/21-EJS1958.

- Saltelli (2002) A. Saltelli. Making best use of model evaluations to compute sensitivity indices. Computer Physics Communications, 145:280–297, 2002.

- Scornet (2020) E. Scornet. Trees, forests, and impurity-based variable importance. arXiv preprint arXiv:2001.04295, 2020.

- Scornet et al. (2015) E. Scornet, G. Biau, and J.-P. Vert. Consistency of random forests. The Annals of Statistics, 43:1716–1741, 2015.

- Shapley (1953) L.S. Shapley. A value for n-person games. Contributions to the Theory of Games, 2:307–317, 1953.

- Sobol (1993) I.M. Sobol. Sensitivity estimates for nonlinear mathematical models. Mathematical Modelling and Computational Experiments, 1:407–414, 1993.

- Strobl and Zeileis (2008) C. Strobl and A. Zeileis. Danger: High power!–exploring the statistical properties of a test for random forest variable importance. In Proceedings of the 18th International Conference on Computational Statistics, Porto, Portugal, 2008.

- Strobl et al. (2007) C. Strobl, A.-L. Boulesteix, A. Zeileis, and T. Hothorn. Bias in random forest variable importance measures: illustrations, sources and a solution. BMC Bioinformatics, 8:25, 2007.

- Strobl et al. (2008) C. Strobl, A.-L. Boulesteix, T. Kneib, T. Augustin, and A. Zeileis. Conditional variable importance for random forests. BMC Bioinformatics, 9:307, 2008.

- Toloşi and Lengauer (2011) L. Toloşi and T. Lengauer. Classification with correlated features: unreliability of feature ranking and solutions. Bioinformatics, 27:1986–1994, 2011.

- Wager and Athey (2018) S. Wager and S. Athey. Estimation and inference of heterogeneous treatment effects using random forests. Journal of the American Statistical Association, 113:1228–1242, 2018.

- Williamson et al. (2021) B.D. Williamson, P.B. Gilbert, N.R. Simon, and M. Carone. A general framework for inference on algorithm-agnostic variable importance. Journal of the American Statistical Association, pages 1–38, 2021.

- Wright and Ziegler (2017) M.N. Wright and A. Ziegler. ranger: a fast implementation of random forests for high dimensional data in C++ and R. Journal of Statistical Software, 77:1–17, 2017.

- Zhou and Hooker (2021) Z. Zhou and G. Hooker. Unbiased measurement of feature importance in tree-based methods. ACM Transactions on Knowledge Discovery from Data, 15:1–21, 2021.

- Zhu et al. (2015) R. Zhu, D. Zeng, and M. R. Kosorok. Reinforcement learning trees. Journal of the American Statistical Association, 110:1770–1784, 2015.

Supplementary Material for “MDA for random forests: inconsistency, and a practical solution via the Sobol-MDA”

1 Analytical Example for the MDA

To illustrate the behavior of the MDA, we take a simple example and analytically derive the MDA limit and its three associated components , , and . This example shows how the MDA is misleading when input variables are dependent. We consider the Breiman-Cutler MDA, denoted by MDA to lighten notations. The TT-MDA or Ishwaran-Kogalur MDA lead to identical conclusions.

The input X is a Gaussian vector of dimension . Its covariance matrix is defined by for , and all covariance terms are null except and . The regression function is given by

Notice that has a simple form to enable an easy interpretation of the importance measures, but that interaction terms are required to highlight the different behaviors of the three MDA components in a correlated setting. Simple calculations give the analytical expression of the MDA limit for as

First, observe that decreases with the correlation between and . Indeed, is the total Sobol index and when these two variables are strongly dependent, the additional information provided by alone is small. In the extreme case, implies that , i.e., can be removed from the model without hurting the model accuracy since all its information is contained in . On the other hand, does not rely on the dependence between and . Indeed, recall that in the case of , contributions due to the dependence between and are excluded because of the conditioning on . For , this dependence is ignored, and therefore such removal does not take place. Therefore, it is clear that the MDA mixes two terms with opposite meanings. Finally, the third term measures how the permutation of shifts the mean value of the regression function averaged over , which is not a quantity of interest to rank variables. However, in a high correlation setting , we have , which means that the meaningless third term is the main contribution of the MDA value of variable . Besides, symmetrically for the other input variables, we have , and the same formula for and with the appropriate parameters. MDA formulas for variables , and are to be found in the last section of the Supplementary Material.

As stated in the introduction, one of the main objective of variable importance analysis is usually to select a small number of variables while maximizing the model accuracy. In our example, we show how the MDA fails for this purpose. Let say we want to remove the less relevant input variable in a setting where the two vectors and are interchangeable (), except that their dependence strengths differ and satisfy . Since the correlation between variables and is higher than between variables and , we should remove or to minimize the information loss, as suggested by the total Sobol index ranking

However, in such setting we have

that would lead to discard or , which is suboptimal—see the last section of the Supplementary Material for computation details. On the other hand, using only or as importance measures gives the accurate variable selection. The term artificially increases the MDA value because of correlation, and is thus misleading for both objectives (i) and (ii).

2 Algorithms

2.1 MDA Algorithm Formulations

Algorithms 1 and 2 respectively provide an algorithmic formulation of the Breiman-Cutler MDA and the Ishwaran-Kogalur MDA.

2.2 Ishwaran-Kogalur MDA by Blocks

The Ishwaran-Kogalur MDA is implemented in randomForestSRC. This package also provides the possibility to define the Ishwaran-Kogalur MDA by blocks: the trees of the forest are divided in a fixed number of blocks. The Ishwaran-Kogalur MDA is estimated for each block and then averaged. Thus, the Breiman-Cutler MDA can be seen as a specific case where the number of blocks is the number of trees , and each block contains only one tree. On the theoretical side, if the number of blocks is fixed and Assumption 4 is satisfied, the number of trees in each block grows to infinity, and therefore Theorem 1-(iii) still holds.

2.3 Sobol-MDA Computational Complexity

Recall that the computational complexity of the brute force approach of Williamson et al. (2021), where a forest is retrained without each input variable, is , which is quadratic with the dimension and therefore intractable in high-dimensional settings.

On the other hand, the original MDA procedure has an average complexity of : to run a balanced tree prediction for a given data point, it is dropped down the levels of the tree, which makes a complexity of for the full out-of-bag sample, repeated for the trees of the forest and the variables. In the Sobol-MDA procedure, the complexity analysis is similar, except that when a point is dropped down the tree, it can be sent to both the left and right children nodes, generating multiple operations at a given tree level and then an additional multiplicative factor of . However, it is not necessary to run the Projected-CART algorithm for each of the covariates. Indeed, when a given observation is dropped down the tree, it meets at most different variables in the original tree path. Therefore, the Projected-CART prediction has to be computed only for covariates for each observation. Thus, the Sobol-MDA algorithm has a computational complexity of , which is in particular independent of the dimension , and quasi-linear with the sample size .

2.4 Projected-CART

We provide below Algorithm 3 for an implementation of the projected random forests.

2.5 Recursive Feature Elimination

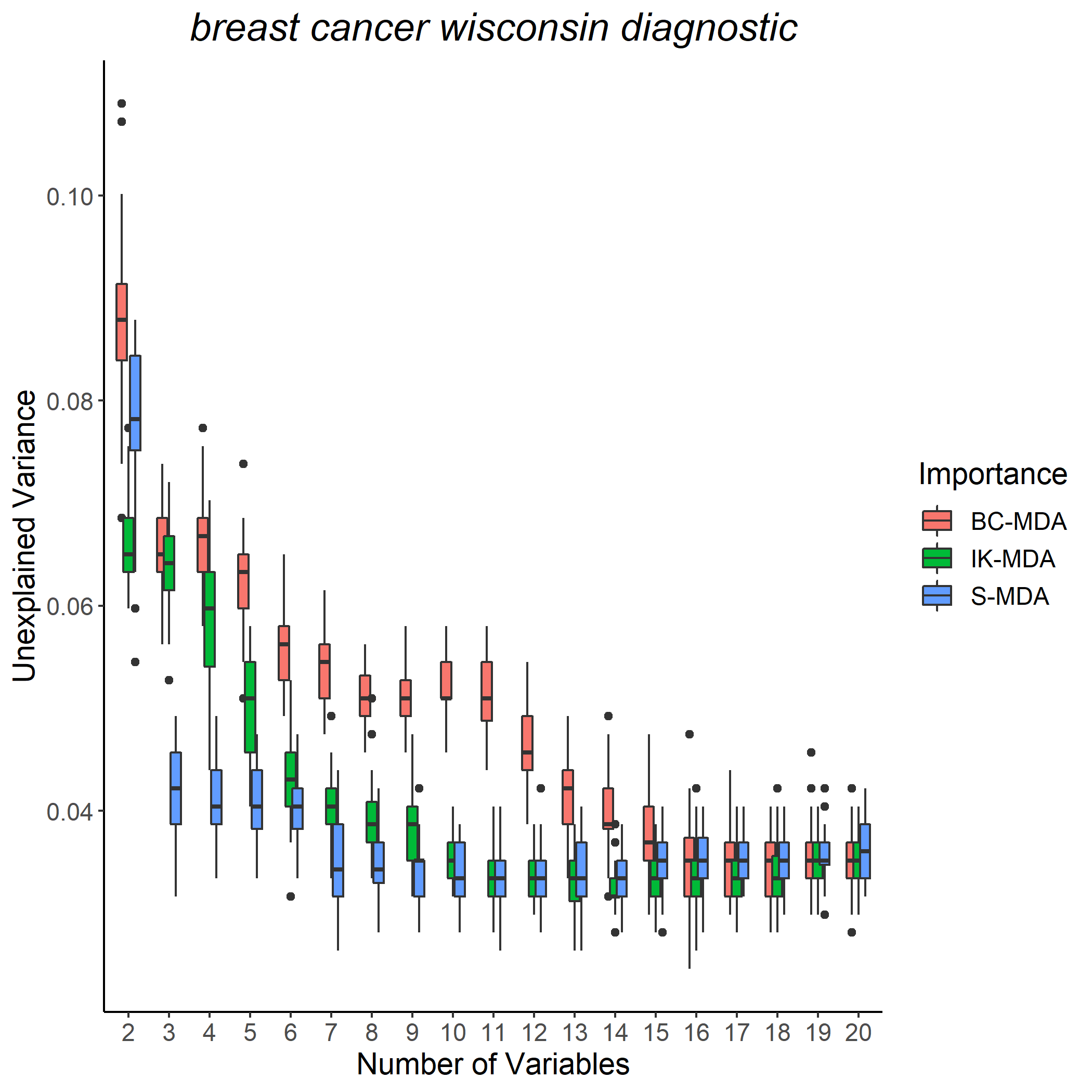

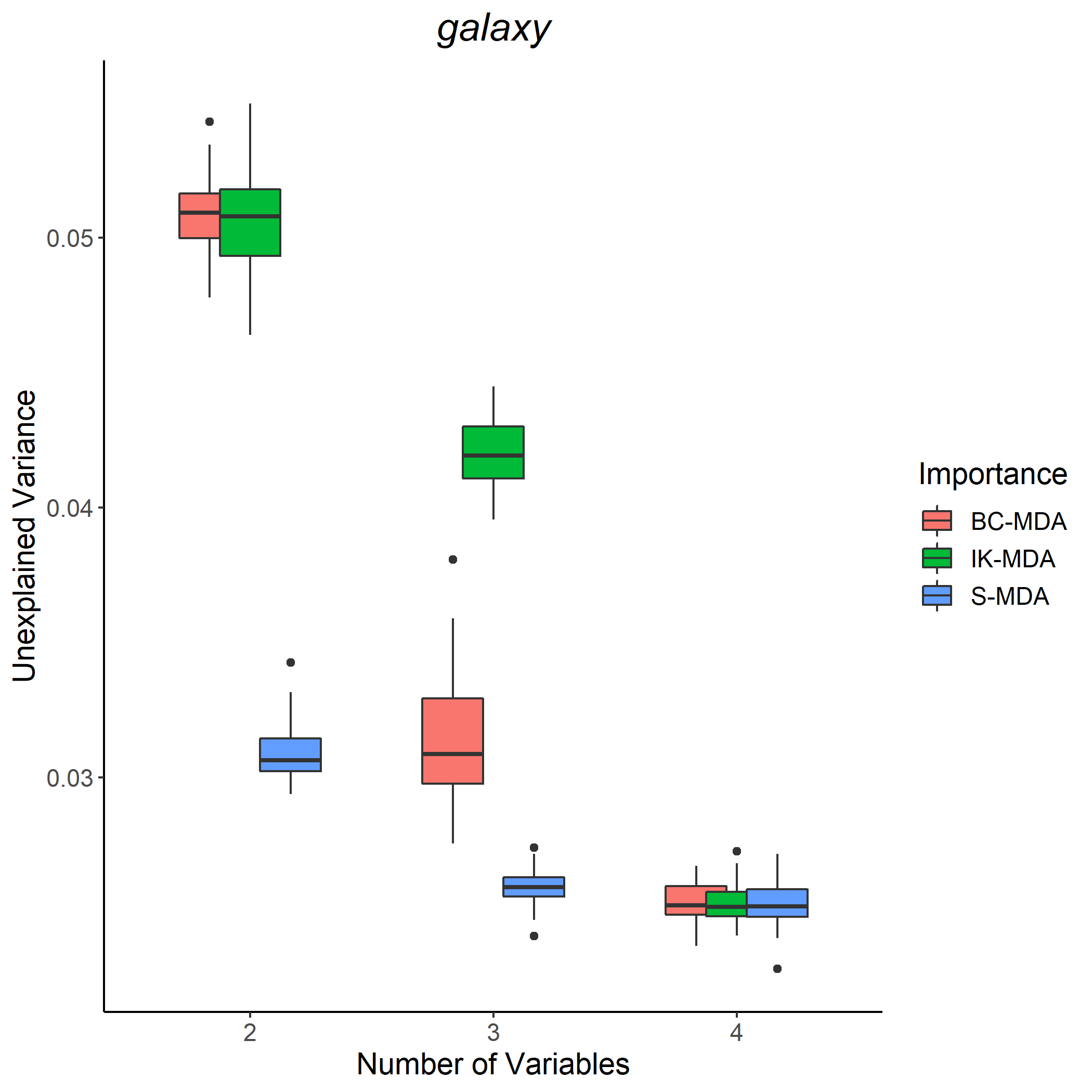

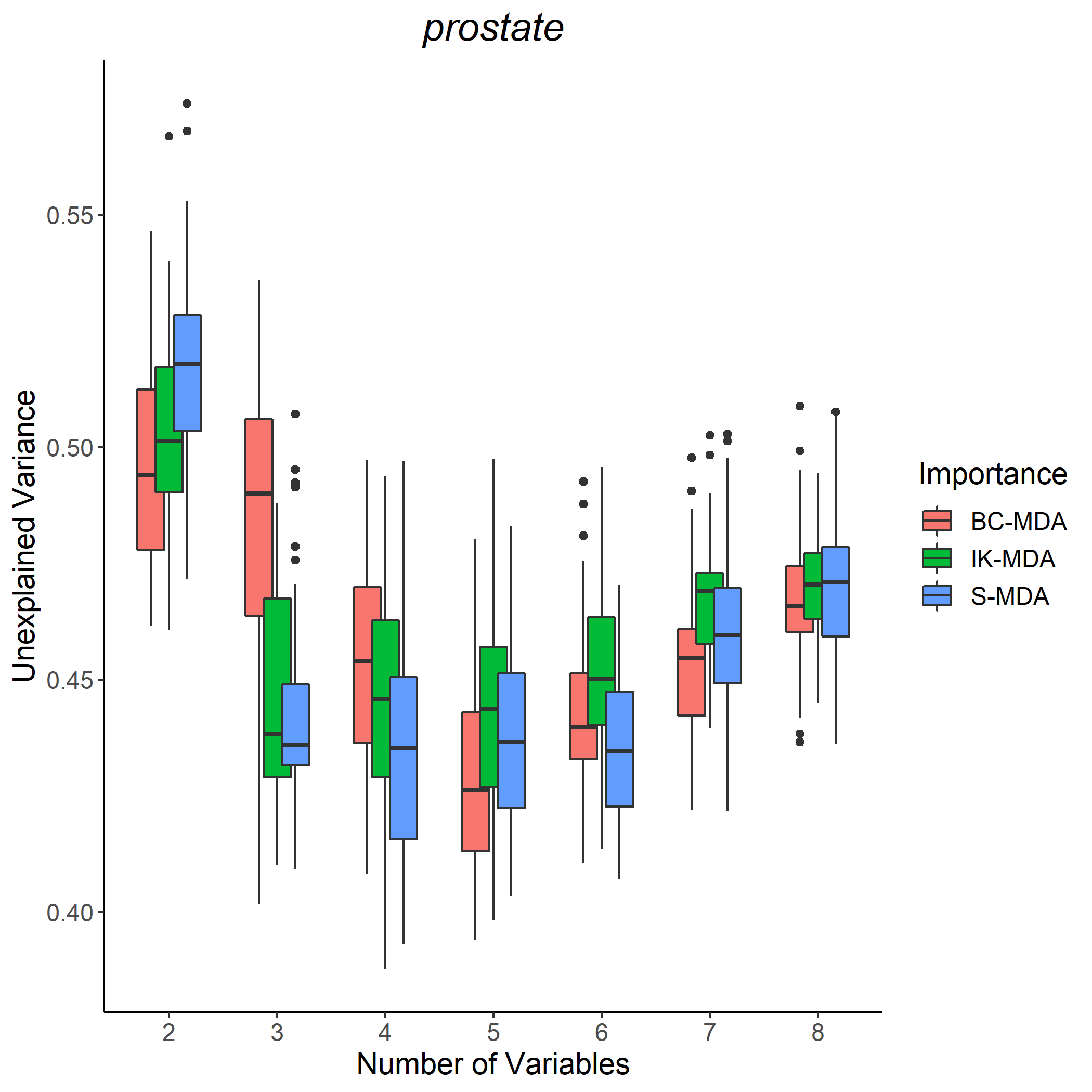

Figures 3 and 4 provide additional experiments to show that the Sobol-MDA leads to a more efficient variable selection than the Breiman-Cutler MDA, Williamson et al. (2021), and the Ishwaran-Kogalur MDA. Notice that Algorithm 4 recalls the RFE procedure. The “Prostate” dataset in Figure 4 is an example where the Sobol-MDA does not significantly improve over the original MDA.

3 Proof of the MDA Consistency

3.1 Assumptions and Theorem 1

Assumption 1.

The response follows

where admits a density over bounded from above and below by strictly positive constants, is continuous, and the noise is sub-Gaussian, independent of X, and centered. A sample of independent random variables distributed as is available.

Assumption 2.

The randomized theoretical CART tree built with the distribution of is consistent, that is, for all , almost surely,

Assumption 3.

The asymptotic regime of , the size of the subsampling without replacement, and the number of terminal leaves is such that , for a fixed , , , and .

Assumption 4.

The number of trees grows to infinity with the sample size : .

Proposition 1.

If Assumption 1 is satisfied, for a fixed and , we have

3.2 Proof of Theorem 1-(i)

Assumptions 1, 2 and 3 are sufficient to slightly extend the -consistency of random forests from Scornet et al. (2015, Theorem 1) to the case where inputs are dependent, and also when the prediction is performed for the permuted sample (i.e, for a query point with a different distribution than the training data). Then, the TT-MDA consistency follows using a standard asymptotic analysis.

Proof of Theorem 1-(i).

We assume that 1, 2, and 3 are satisfied, and fix and .

Firstly, according to Lemma 1, we have

| (3.1) |

and

| (3.2) |

Next, we can break down the Train/Test-MDA as follows

Then, we use the triangle inequality and the previous expression to get the following bound

| (3.3) | ||||

| (3.4) | ||||

| (3.5) | ||||

| (3.6) | ||||

| (3.7) | ||||

| (3.8) | ||||

| (3.9) |

Now, let us consider all the terms on the right hand side one by one.

The first and fourth terms (3.3) and (3.6) do not depend on the forest estimate, but it is not possible to simply apply the law of large numbers since the permutation introduces dependence within samples. For both terms, we prove -convergence, which implies the -convergence we are looking for. For the first term (3.3), we define as

Clearly, we have . Its variance writes

Because of the permutation, each element of the sum is dependent on only two other terms. Therefore, only terms of the double sum are not null, and because is bounded (continuous on a compact), we get

Thus, , which proves -convergence of towards . We can handle the fourth term (3.6) in the same way. For the second term (3.4), by symmetry,

which tends to zero according to (3.2). The sixth term (3.8) is handled similarly using (3.1). Since is bounded, we can bound the third term (3.5)

and since convergence implies convergence, we use (3.2) to obtain the convergence towards of this third term (3.5). For the fifth term (3.7) we first apply the triangle inequality, and by symmetry we get

which tends to zero according to (3.2). Similarly, the last term (3.9) is handled with (3.1). Gathering all previous convergence results on (3.3)-(3.9), we have for all , for all ,

∎

Proof of Lemma 1.

We assume that Assumptions 1, 2, and 3 are satisfied, and fix and . We first introduce the infinite forest estimate defined as where is the randomized CART estimate.

Theorem 1 from Scornet et al. (2015) states the -consistency of infinite random forests. It relies on Assumption 3 for the asymptotic regime of and , and on a modified version of 1, where the regression function is additive and X is uniformly distributed over . Here, we extend this result to any continuous regression function and any positive distribution for X with support on the unit cube. First, the extension to the case where X has any distribution bounded from above and below by positive constants can be easily obtained by several technical adaptations as already highlighted in Scornet (2020). Secondly, notice that the additive structure of the regression function is only required in Scornet et al. (2015) to show the consistency of a theoretical randomized CART. Therefore we can drop the additivity assumption and replace it by Assumption 2. Overall, we can extend Theorem 1 from Scornet et al. (2015): provided that Assumptions 1, 2, and 3 are satisfied, we have

| (3.10) |

Next, this result needs to be extended when the query point X is replaced by . From Assumption 1, X admits a density over . By construction, the random vector is the vector X where the -th component is replaced by an independent copy of . Therefore admits a density , which is the product of the densities of and , i.e., for ,

| (3.11) |

From Assumption 1, is bounded from above and below by positive constants. Thus, it exists such that for all ,

| (3.12) |

Combining (3.12) and (3.11), we obtain that for all , , and consequently,

Now, we write

Taking expectations on both sides and using (3.10), we finally obtain

| (3.13) |

Equations (3.10) and (3.13) state that infinite forests evaluated at X or are consistent. The first of these two results can be extended to get the consistency of a single randomized CART , as shown in Scornet et al. (2015) by an easy adaptation of the infinite forest case. Formally, we obtain

| (3.14) |

The exact same reasoning as for the infinite forest above applies to get the extension to , and thus, we have

| (3.15) |

Now, we expand the final quantity of interest (and its counterpart for ):

Conditional on , the random variables for are iid. Hence

| (3.16) |

Using (3.10) and (3.14), we obtain the final result

which also holds for , using (3.13) and (3.15):

∎

3.3 Proof of Theorem 1-(ii)

Theorem 1-(i) can be quite easily adapted to the BC-MDA (ii).

Proof of Theorem 1-(ii).

We assume that Assumptions 1-3 are satisfied, and fix and . Recall that the Breiman-Cutler MDA is formally defined by

where is the size of the out-of-bag sample of the -th tree.

Since observations are subsampled without replacement prior to the construction of each tree, all out-of-bag samples have the same constant size of . Using the triangle inequality, we have

and by symmetry, this boils down to

Next, we expand the sum in the right hand side and obtain a similar decomposition as the one in the proof of Theorem 1-(i),

Thus, we have the following bound

| (3.17) | ||||

| (3.18) | ||||

| (3.19) | ||||

| (3.20) | ||||

| (3.21) | ||||

| (3.22) | ||||

| (3.23) |

Now, let us consider all the terms on the right hand side one by one.

For the first term (3.17), we define as

Its expectation is

Next, observe that each term of the sum in is dependent on two other terms because of the permutation of the -th component, then we have . By Assumption 3, with a fixed , thus . Since and , converges towards in , which implies -convergence. We can handle the fourth term (3.20) in the same way. For the second term (3.18),

where the last equality results from . The conditioning event means that the observation of index belongs to the out-of-bag sample. Thus, it is strictly equivalent to consider the tree trained with the sample of size with a subsampling size . Furthermore, we can replace the query point by because these two random vectors are iid and both independent of the training data of . Then,

which tends to zero according to the second statement in Lemma 1 for . The sixth term (3.22) is handled similarly using the first part of Lemma 1. Since is bounded, we can bound the third term (3.19)

which tends to zero according to Lemma 1 (with ). Similarly, for the fifth term (3.21), we have

and the convergence towards is again given by Lemma 1. The last term (3.23) is handled in the same way. Gathering all previous convergence results on (3.17)-(3.23), we have for all , for all ,

∎

3.4 Proof of Theorems 1-(iii) and Proposition 1

The obstacle in the asymptotic analysis of the IK-MDA arises from the randomness of , which can even be empty. However, the quadratic risk of the OOB estimate can be bounded using the risk of the standard forest, as stated in the following Lemma.

Lemma 2.

If Assumption 1 is satisfied, for all and , we have

We can draw interesting insights from Lemma 2. First by construction, the OOB estimate aggregates a smaller number of trees than in the standard forest: trees in average. Therefore the risk of the standard forest is inflated by the coefficient to bound the OOB risk. Since the risk of the OOB estimate is bounded by the risk of the standard forest, the -consistency of random forests can be extended to the OOB estimate.

Lemma 3.

Lemma 4.

If and are defined as

for all , we have

and for a fixed sample size ,

Then, we can deduce the consistency of the IK-MDA.

Proof of Theorem 1-(iii).

We assume that Assumptions 1-4 are satisfied, and fix . Recall that Ishwaran-Kogalur MDA is defined as

where is the number of points which do not belong to all trees, and

To lighten derivations, we define . We expand the following expression,

Observe that is bounded between and , and consequently

Then, we follow the proof of Theorem 1-(i) and (ii) with a similar decomposition of the sum of the above expression

We then obtain the following bound

| (3.24) | ||||

| (3.25) | ||||

| (3.26) | ||||

| (3.27) | ||||

| (3.28) | ||||

| (3.29) | ||||

| (3.30) |

Now, let us consider all the terms on the right hand side one by one. For the first term (3.24), we can rewrite

and the multiplicative term in front is upper bounded by by Assumption 3. Next, we can apply the strong law of large numbers to show that the sum converges almost surely towards

Since almost sure convergence implies -convergence, the first term (3.24) converges towards . The fourth term (3.27) is handled similarly with the strong law of large number since the noise is centered and independent of . The second term

converges towards from the second part of Lemma 3 and because . The sixth term (3.29) is handled identically using the first part of Lemma 3. For the third term (3.26), since is bounded (continuous on a compact), we have

which converges towards by Lemma 3. Similarly, for the fifth (3.28) and seventh (3.30) terms, we have the following bound

and we conclude using Lemma 3 again. Overall, we have

∎

Proof of Lemma 2.