[datatype=bibtex] \map \step[fieldset=issn, null] \step[fieldset=doi, null] \step[fieldset=url, null] \step[fieldset=urldate, null]

Matching with Trade-offs:

Revealed Preferences over Competing Characteristics

Abstract

We investigate in this paper the theory and econometrics of optimal matchings with competing criteria. The surplus from a marriage match, for instance, may depend both on the incomes and on the educations of the partners, as well as on characteristics that the analyst does not observe. Even if the surplus is complementary in incomes, and complementary in educations, imperfect correlation between income and education at the individual level implies that the social optimum must trade off matching on incomes and matching on educations. Given a flexible specification of the surplus function, we characterize under mild assumptions the properties of the set of feasible matchings and of the socially optimal matching. Then we show how data on the covariation of the types of the partners in observed matches can be used to test that the observed matches are socially optimal for this specification, and to estimate the parameters that define social preferences over matches.

Keywords: matching, logit, generalized linear models, revealed preferences, contingency tables.

JEL codes: C78, D61, C13.

Introduction

Louisa was naturally ill-tempered and cunning; but she had been taught to disguise her real disposition, under the appearance of insinuating sweetness, by a father who but too well knew that to be married would be the only chance she would have of not being starved, and who flattered himself that with such an extraordinary share of personal beauty, joined to a gentleness of manners, and an engaging address, she might stand a good chance of pleasing some young man who might afford to marry a girl without a shilling.

Jane Austen, Lesley Castle (1792).

Starting with [1], most of the economic theory of one-to-one matching has focused on the case when the surplus created by a match is a function of just two numbers: the one-dimensional types of the two partners. As is well-known, if the types of the partners are one-dimensional and are complementary in producing surplus then the socially optimal matches exhibit positive assortative matching. Moreover, the resulting configuration is stable, it is in the core of the corresponding matching game, and it can be implemented by the celebrated [10] deferred acceptance algorithm.

While this result is both simple and powerful, its implications are also quite unrealistic. If we focus on marriage and type is education for instance, then positive assortative matching has the most educated woman marrying the most educated man, then the second most educated woman marrying marrying the second most educated man, and so on. In practice the most educated woman would weigh several criteria in deciding upon a match; even in the frictionless world studied by theory, the social surplus her match creates may be higher if she marries a man with less education but, say, a similar income. Since income and education are only imperfectly correlated, the optimal match must trade off assortative matching along these two dimensions. This point is quite general: with multiple types, the stark predictions of the one-dimensional case break down.

Empirical analysts of matching have long felt the need to accommodate the imperfect assortative matching observed in the data, of course. This can be done by introducing noise, in the form of heterogeneity in creation of surplus that is unobserved by the analyst (see [5].) Models with multidimensional types can also be estimated from the data, as in [4]. But as far as we know, there has been little theoretical work exploring the properties of optimal or equilibrium matches in such models. We show in this paper that these properties can be summed up in simple measures of covariation of types across partners; we analyze the set of values of such measures that can be rationalized by a matching model; and we show how to estimate this set from data and to test that the observed matching is socially optimal111A word on terminology: like most of the literature, we call a “match” the pairing of two partners, and a “matching” the list of all realized matches..

While we use the language of the economic theory of marriage in our illustrations, nothing we do actually depends on it. The methods proposed in this paper apply just as well to any one-to-one matching problem—or bipartite matchings, to use the terminology of applied mathematics. In fact, we can even extend them to problems in which the sets of partners are determined endogenously—as with same-sex unions. This is investigated in Section 7, where we consider possible extensions of our setting.

We do require, however, that utility be transferable across partners. Our primitive function is indeed the surplus created by a match. We posit that it is an unknown function of the types of the partners only, plus preference shocks that are observed by all participants but not by the analyst—in the nature of unobserved heterogeneity. When utility is transferable, all optimal matchings must maximize the joint surplus; and so does the equilibrium of the assignment game.

As is well-known, this model is too general to be empirically testable: even without unobserved heterogeneity, any observed assignment can be rationalized by a well-chosen surplus function. This is a consequence of a more general theorem by [2]. [8] shows that on the other hand, some collections of matchings are not rationalizable: if the analyst can observe identical populations on several assignments, then these assignments must be consistent with each other in a sense that his paper makes precise. But we are unlikely to have such data at hand in general.

Relatedly, analysts sometimes observe several subpopulations which are matching independently and yet have the same surplus function. [9] shows that under a “rank-order condition” on the unobserved heterogeneity, it is then possible to identify several important features of the surplus function, and in particular how important complementarity is on various dimensions.

While analyzing complementarity is also one of our goals here, many of the applications we have in mind do not fit Fox’s assumption that there be enough variation across subpopulations with identical surplus. Marriage markets, for instance, seem to be either so disconnected that their surplus functions are unlikely to be similar, or too connected to make it possible to ignore matching across markets. In this paper, we will posit that we are only given data on one instance of a matching problem, such as the marriage market in the US in the 1980s, or the market for CEOs. Our data will consist of the values of the observable types of both partners in each realized match, and of the types of unmatched individuals. Since the optimal/equilibrium matching is determined on the basis of both the observable and the (to us) unobservable types, we will need to impose assumptions that allow us to integrate over the distribution of the unobservable types in a manageable way. Our aim is to start from the observable matching (the distribution of matches across observable types) and to recover information on the observable surplus function (the average surplus of matches for given observable types of both partners.)

To achieve this, we first resort to a separability assumption that rules out interactions between the unobservable types of the partners in the surplus form a match. This was used by [5], and then generalized by [4] who showed that the matching equilibrium then boils down to a series of parallel discrete choice models. While this is an important step on the way to a solution, the resulting model is still too rich to be taken to the data. We need to restrict the distribution of unobserved heterogeneity, and we do this by adopting again [5]’s assumption that gives rise to multinomial logits. Under these assumptions, we prove that the cross-differences of the surplus function over observable types are nonparametrically identified from the data. In particular, we can test for complementarities between any two observable dimensions of the types of the partners, such as the education of the wife and the income of the husband. We can also identify the relative strengths of such complementarities across different dimensions.

If the analyst is lucky enough to have very rich data, then unobserved heterogeneity is almost irrelevant and the observable matching maximizes the observable surplus function. On the other hand, if data is so poor that unobserved heterogeneity dominates, then the analyst should observe something that, to him, looks like completely random matching. We show that under our assumptions, this amounts to maximizing the mutual information of the match distribution—a statistical object that here measures covariation of partner types. Moreover, for any intermediate amount of unobserved heterogeneity, the observable matching maximizes a straightforward linear combination of the observable surplus and of mutual information.

This observation suggests a strategy: approximate the observable surplus function with a linear expansion over some known basis functions, with unknown “assorting weights”. Then all relevant information can be expressed in terms of the average values of these basis functions across couples, and our results have a very neat geometrical interpretation. Take the abstract space where each point represents an hypothetical set of values for all the basis functions. All feasible matchings generate points within a polytope in this space. We first show that even with our restrictive assumptions, any point in this polytope is rationalizable: if the variance of unobserved heterogeneity is well-chosen, then there exist assorting weights for which the optimal matching generates exactly these covariations. Fortunately, this combination of heterogeneity and assorting weights is in general unique as we shall see: this allows us to introduce several consistent and asymptotically normal estimators of both the assorting weights and the variance of the unobserved heterogeneity. Moreover, models without any unobserved heterogeneity can only generate points on the boundary of the polytope, and so the homogeneous model is testable.

This paper thus proves both a negative and a positive result. The negative part is that even if we assume separable heterogeneity with a multinomial logit structure, the model still cannot be rejected. The positive part is that given any theory about the way the observable types enter the surplus function (as embodied in a set of basis functions), we exhibit well-behaved estimators of the unknown parameters; and we can quantify how much heterogeneity is needed to rationalize the data. Moreover, our methods can be used heuristically, to explore ways to understand what goes on in matching markets—and how they change across time and space. Standard statistical techniques could for instance be put to work to find the basis functions that explain the largest share of the variation in the data. Such a methodological stance is reminiscent of revealed preferences in consumer theory; in fact the analogy is very sharp, as the underlying theoretical structure is the same.

Our depiction of matching markets of course abstracts from many features of real-world markets. We focus on static, frictionless markets, as in much of the literature on marriage markets. Models of matching on job markets, for instance, have on the whole adopted a much more dynamic perspective, in which job flows in fact provide a lot of information on the underlying parameters. In the applications we have in mind, the surplus function may involve many more dimensions and we do not want to restrict it too much a priori. The basic lack of identification mentioned at the beginning of this introduction would become even more severe if we introduced dynamics or frictions, unless these additional features are drastically simplified. We leave this for further research. The paper also currently focuses on discrete characteristics; we are exploring possible extensions to continuous types.

Section 1 sets up the matching model we study in the paper, along with the assumptions on the specification of the observable surplus and the process that drives unobserved heterogeneity. In section 2 we build on these assumptions to derive our main analytical results, and we give them a geometric interpretation on section 3. Section 4 introduces our tests and estimators and derives their asymptotic properties. We conclude by sketching extensions of our methods.

Since much of what we do uses convexity, we recall some definitions and basic results in Appendix A. All proofs are collected in Appendices B and C. Finally, we should note that there are close parallels between the analysis we develop in the present paper and familiar notions in thermodynamics and statistical physics. E.g the social utility of a matching evokes (minus) the internal energy of a physical system, and the standard error of unobservable heterogeneity parallels its physical temperature. Since the analogy may prove to be as useful to others as it was to us, we elaborate on it in Appendix D.

Summary of the notation used in the paper. For the reader’s convenience, we regroup here the notation introduced in the text. We consider matches between men and women. is the set of permutations of . A man has a full type , where the econometrician observes but not ; we use for a woman. is a random vector with distribution , and is distributed according to ; we use and for a woman. We denote the set of probability distributions with margins and ; we use for the full types. We denote the product measure which matches men and women randomly. A feasible matching generates a probability , which assesses the odds that a man with full type is married to a woman with full type . A man with full type and a woman with full type generate together a full surplus . We call the observable surplus; in some of the paper we take it to be the structural quadratic form .

1 The Assignment Problem

Throughout the paper, we assume that two subpopulations and of equal size must be matched each man (as we will call the members of ) must be matched with one and only one member of (we will call them women.) Thus we do not model the determination of the unmatched population (the singles) in this paper; we take it as data. We elaborate on this point in our concluding remarks. Note also that we assumed bipartite matching: the two subpopulations which define admissible partners are exogenously given. This assumption can also be relaxed; see Section 7.

Throughout the paper, we illustrate results on the education/income example sketched in the Introduction, which we denote (ER).

1.1 Population characteristics

Each man has an -dimensional type of observable characteristics, and a vector of unobserved characteristics . Denote the full description of man ’s characteristics, which we call his full type. Each woman similarly has an -dimensional type of observed characteristics, and a full type .

We denote (resp. ) the distribution of full types (resp. ) in the subpopulation (resp. ), and (resp. ) the distribution of observable types (resp. .) Thus is a probability distribution on and is a distribution on . In observed datasets we will have a finite number of men and women, so that and are the empirical distributions over the characteristics samples of the men and the women , respectively.

Take the education/income example: there , the first dimension of types is education (dropout or graduate), and the second dimension is income class , which takes values to . describes both the number of graduates among men and the distributions of income among graduate men and among dropout men.

1.2 Matching

The intuitive definition of a matching is the specification of “who marries whom”: given a man of index , it is simply the index of the woman he marries, . Imposing that each man be married to one and only one woman at a given time translates into the requirement that be a permutation of , which we denote . This definition is too restrictive in so far as we would like to allow for some randomization. This could arise because a given type is indifferent between several partner types; or because the analyst only observes a subset of relevant characteristics, and the unobserved heterogeneity induces apparent randomness.

A feasible matching (or assignment) is therefore defined in all generality as a joint distribution over types of partners and , such that the marginal distribution of is and the marginal distribution of is . We denote the set of such joint distributions. Note that when and are univariate, a feasible matching can be equivalently specified through a copula.

A matching is said to be pure if all conditional distributions and are point mass distributions. In a pure matching , there exists an invertible map such that a man with type almost surely marries a woman of type , and conversely, a woman with type almost surely marries a man of type . (Of course, in the discrete case this map can be represented as a permutation on indices.)

In the education/income example (ER), a pure matching is described by numbers; but the marginals impose constraints, so that numbers are to be determined.

1.3 Surplus of a match

The basic assumption of the model is that matching man of type and woman of type generates a joint surplus , where is a deterministic function. Along with most of the matching literature, we assume that

Assumption (O): Observability. Each agent observes the full characteristics and of all men and all women, but the econometrician only observes the subvectors and .

Assumption (O) rules out asymmetric information between participants in the market, as the economics of matching with incomplete information is a subject of its own. On the other hand, we do not need to assume full information as the notation seems to imply: could for instance be reinterpreted as the expectation of a random variable conditional on , as long as all participants evaluate it in the same way.

Given Assumption (O), we need to define the observable surplus as the best predictor of conditional on and , that is

and we can write the decomposition

where is the idiosyncratic surplus.

Assumption (S): Separability. Let and have the same observable type: . Similarly, let and be such that . Then

While much of the literature on matching emphasizes complementarity, assumption (S) in fact requires that conditional on observable types, the surplus exhibit no complementarity across unobservable types.

It is easy to see that imposing assumption (S) is equivalent to requiring that the idiosyncratic surplus from a match must be additively separable, in the following sense:

where and are two deterministic functions and

Then the surplus function can be rewritten as

Note that the model is invariant if one rescales the three terms on the right-hand side by the same positive constant. Later on we will normalize these three components.

As proved in [4], assumption (S) implies that at the optimum (or equilibrium), a given individual (say, a man ) has a preference for a particular class of observable characteristics (say ), but he is indifferent between all partners which have the same but a different .

In fact, the optimal matching is characterized by two functions of observable characteristics and that sum up to such that if a man is matched with a woman of characteristics , he will get utility

while his match gets utility

[4] showed that given assumption (S), the matching problem boils down to a set of discrete choice models for each type of man and of woman: for instance, man is matched in equilibrium to a woman whose observable type maximizes

over all values in the support of .

While this is already quite useful, we need to add more restrictions on the specification of the components of the idiosyncratic surplus and .

1.4 Specifying the idiosyncratic surplus

Following [5] and [4], we introduce the following assumption222We define the scale factor to be 1 for the standard Gumbel, which has variance ; thus e.g. has variance .:

Assumption GUI: Gumbel Unobserved Interactions. It is assumed that:

- There are an infinite number of individuals with a given observable type in the population

- Fix the observable characteristics of a man, and let be the possible values of the observable characteristics of women. Then the vector of preference shocks are distributed as independent and centered Gumbel random variables with scale factor ;

similarly,

- Fix the observable characteristics of a man, and let be the possible values of the observable characteristics of men. Then the vector of preference shocks are distributed as independent and centered Gumbel random variables with scale factor .

In short: men of a given observable type have conditionally Gumbel iid draws of the ’s for different individuals; and conversely for women of a given observable type.

We use (GUI) for the Independence of Irrelevant Alternatives property: without it, the odds ratio of the probability that a man with observable type ends up in a match with a woman of observable type rather than with would also depend on the types of other women, and the model would become unmanageable.

(GUI) underlies the standard multinomial logit model of discrete choice. It has well-known limitations, one of which is that it does not extend directly to continuous choice. We are currently exploring alternative specifications that would allow us to deal with continuous characteristics; but at this stage, we assume

Assumption (DD): The distributions of observed types and are discrete, with probability mass functions and .

In the (ER) example for instance, is the proportion of men who are dropouts and whose income lies in class 3. For simplicity, we now denote the possible values of types of men, and for women.

1.5 Specifying the observable surplus

We now introduce sets of assumptions on the observable surplus ranging from non-restrictive (NPOI below, suited for nonparametric identification) to more restrictive (SLOI below, convenient for a more concise analysis).

Let us first impose a normalization convention on the observable surplus. Notice that the optimal matching (but not the value of the social surplus) is left unchanged if we add an additively decomposable function to . Therefore, without any loss of generality, we impose some identifying restriction on , using the two-way ANOVA decomposition, accoding to which any vector admits the following orthogonal decomposition in as

where and . We shall therefore often take the following convention when using a nonparametric approach:

Convention (ZMOI): Zero-mean Observable interactions. The observable surplus satisfies

It will sometimes be useful to assume more structure on the function (the observable joint surplus.) To do this, we consider given basis assorting functions whose values are interpreted as the utility benefit of interaction between type and type . Given assorting weights , we focus on observable surplus functions which are linear combinations of the basis assorting functions with weights . That is,

Assumption (SLOI): Semilinear Observable Interactions. The observable surplus function can be written

| (1.1) |

where the sign of each is unrestricted.

Note that in the discrete case which we restrict to in this paper, this general form is absolutely not restrictive. Indeed, one can choose and chose so that captures interaction between observable man type and observable woman type . We shall refer to this specification as the:

Specification (NPOI): Nonparametric Observable Interactions. The observable surplus function is expanded in all generality

| (1.2) |

in which case social weight coincide with .

However we favor parsimonious models for the sake of analysis, so in general we shall only assume (SLOI), unless explicitely stated.

To return to the education/income example (ER): we could for instance assume that a match between man and woman creates a surplus that depends on the similarity of the partners in both education and income dimensions. The corresponding specification would be (with education levels coded as ):

This specification only has parameters, while an unrestricted specification would have . Such an unrestricted specification would for instance allow the effect of matching partners in income class 3 to depend on both of their education levels.

An even more restrictive, “diagonal” specification would be

In this last form, it is clear that the relative importance of the ’s reflects the relative importance of the criteria. Thus measures the preference for matching partners who are both in income class , while measures the preference for matching dropouts. The relative values of these numbers indicate how social preferences value complementarity of incomes of partners more, relative to complementarity in educations. We will not need to assume such a diagonal structure in the following, although our results easily specialize to this case.

1.6 Summary: the model specification

Under assumptions (O), (S), (SLOI) and (GUI), the model is fully parametrized; its parameters can be collected in a vector

where is the assorting weight matrix, and (resp. ) is the scale factor of the unobservable characteristics of the men (resp. of women). Without loss of generality, all components of can be multiplied by any positive number; hence we shall need to impose some normalization on .

Most of the results in the next section in fact only require assumptions (O), (S) and (GUI), with a general function . In this case is just , and again it is defined up to a scale factor.

As we will see, the total heterogeneity plays a key role in our results; thus we introduce a specific notation for it:

2 Solving for the Optimal Matching

In this section we only assume (O), (S), and (GUI), and we consider the problem of optimal matching:

| (2.1) |

Our modeling strategy in this section and the next is to assume that the number of men and women in the population is large enough that averages can be replaced with expectations. When we describe our estimators in section 5, we of course take into account the fact that we only have a finite sample.

2.1 The heterogeneous model

Let us provide some intuition before we state a formal theorem. Under (O), (S) and (GUI), standard formulæ of the multinomial logit model give the expected utility of a man of observable type at the optimal matching:

Therefore the expected social surplus from the optimal matching is simply333Since this formula may not be entirely transparent, we develop one term below: (adding the equivalent formula for women of observable type ):

Now recall that is the mean utility of a man with observable type who ends up being matched to a woman with observable type at the optimum. As in the general development of the theory of matching, is the value of the multiplier of the population constraints; and as such, it (along with ) is the unknown function in the dual program in which the expression for the social surplus above is minimized over all such that . We now state this as a theorem (proved in the Appendix):

Theorem 1 (Social welfare-primal version)

Assume (O), (S), (GUI) and (DD). Then

| (2.2) |

where the constraint set is defined by the inequalities

At an optimal matching, men with observable type will be found in matches with women with observable types such that . The expected utility of men with observable type matched with women of observable type is .

This theorem also has a primal version, of course. While deriving it takes a bit more work (again, see the Appendix), the intuition is simple. First, if there were no unobserved heterogeneity (with close to zero) the optimal matching would coincide with the optimal observable matching , which solves

Going to the polar opposite, in the limit when goes to infinity only unobserved heterogeneity would count; and since it is just noise, the optimal matching would simply assign partners randomly, yielding the product measure .

As it turns out, when takes any intermediate value the optimal matching maximizes a weighted sum of these two extreme cases:

Theorem 2 (Social welfare-dual version)

Under the assumptions of Theorem 1

| (2.3) |

where and are the entropies of and given by

and is the mutual informationof joint distribution , given by

The mutual information is nothing else than the Kullback-Leibler divergence of from the independent product to . Recall two important information-theoretic properties of :

-

1.

The map is strictly convex.

-

2.

One has

the left handside becoming an equality in particular in the case of a pure matching, and the right handside inequality becoming an equality in the case where , as we shall see below.

Mutual information is a measure of the covariation of types and . Now is the independent product of and , which corresponds to a completely random matching . Thus a large positive indicates that the matching induces strong correlation across types; if and only if . If is very large then the Theorem suggests that should be minimized, which can only occur for the independent matching ; whereas if is negligible then should be chosen so as to maximize the expected observable surplus . This corroborates the intuition given earlier.

Now the optimal matchings coincide with the solutions to this maximization problem. Since we only observe the realized over observable variables, Theorem 2 defines the empirical content of the model: a combination of the parameters is identified if and only if the solution depends non-trivially on it.

We already knew that can be rescaled by any positive constant without altering the solution. We can now go one step further: while all components of figure in this theorem, and only enter through their sum . Thus and as announced, and are not separately identified.

Accordingly, we redefine the parameter vector as

or under (SLOI).

2.2 The homogeneous limit

In this section we consider the limit behavior of our model when goes to zero, so that unobservable heterogeneity vanishes. We denote

By taking the limit in Theorem 1, we obtain:

Theorem 3 (Homogeneous social welfare)

Assume (O) and (DD); then

a) The value of the social optimum when is given both by

| (2.4) |

and by

| (2.5) |

where the constraint set is given by

A matching is optimal for if and only if the equality

holds -almost surely, where and solve the optimization problem (2.5).

Thus in the limit we recover the standard primal and dual formulation of the matching problem; since all men with observable characteristics have the same tastes, they all obtain the same utility at the optimum and becomes a function of only, which we denoted above; and this is just the Lagrange multiplier on the population constraint

which is implicit in the notation .

3 Qualitative properties of the optimum

In this section we first introduce the various statistics on which our analysis shall rest. We then provide comparative statics which help understanding the influences on the model parameters on these statistics; last, we study the influence on qualitative properties of the equilibria such as uniqueness and purity of the equilibria.

3.1 Matching summaries

Feasible summaries. Recall that under (SLOI), there exists an unknown vector such that the observable surplus function takes the form

with known basis functions . Now consider a hypothetical matching ; under this matching, the basis functions have expected values

We call each a covariation. Take the (ER) example; then

-

•

is the proportion of matches among graduate partners under

-

•

is the expected income of a graduate man’s wife multiplied by the proportion of graduate men; is defined similarly

-

•

and is the expected product of the partners’ incomes.

Random matching, as represented by , plays a special role in our analysis, as it obtains in the limit when heterogeneity becomes very large. We denote the corresponding covariations as . At the polar opposite is the matching that obtains in the homogenous limit ; we denote the implied covariations . Note that does not depend on , but does.

We know from Theorem 2 that under (SLOI), the observable optimal matching maximizes

Thus the vector summarizes all the relevant information about matching . We call each such vector a matching summary; matching summary vectors are set in summary space, which is a subset444Remember that for any feasible matching. of .

Given an observed matching, it is of course very easy to estimate the associated covariation vector and mutual information. Again, the model is scale-invariant and we may impose an arbitrary normalization on . For that purpose we choose a vector and we impose . Later we make the choice of more specific.

Given population distributions and , we define the set of feasible summaries as the set of summary vectors that are generated by some feasible matching , that is

Similarly, define the covariogram as the set of covariations that are implied by some feasible matching; that is,

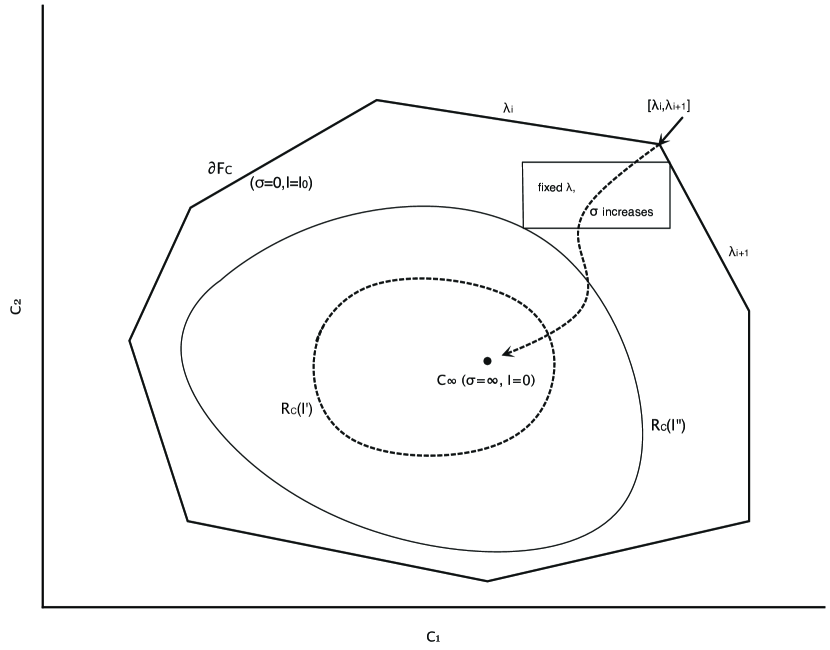

Covariograms provide us with a nice graphical representation of the properties of a matching. Figure 1 illustrates their relevant properties, and the reader should refer to it as we go along. To fit it within two dimensions, we assume that there are only two basis functions; e.g. in the (ER) example we could have

so that (resp. ) measures the preference for assortative matching on educations (resp. income classes.)

Proposition 1

Under (O), (S), (GUI) and (SLOI), the sets and are nonempty closed convex sets, and their support functions are and , respectively.

As will soon become clear, the boundaries of the convex sets and have special significance in our analysis. For now, let us simply note that the boundary of exhibits kinks when these distributions of characteristics are discrete—which is always the case in our setting. The reason for these kinks is that in the discrete case, the optimal matching for homogenous types is generically stable under a small perturbation of the assorting weights ; starting from almost every ’s, a small change in leaves covariations unchanged. Any such value of generates a covariation vector on a vertex of the polytope. On the other hand, there exist a finite number of values of where the optimal matching problem has multiple solutions, with corresponding multiple covariations; each such value of generates a facet of the polytope. This is shown on Figure 1 with all in an interval generating the same covariations in the homogeneous case. Remarkably, such kinks disappear as soon as there is enough positive amount of heterogeneity; we will come back to this in section 3.3.

3.2 Rationalizable boundary

The previous discussion suggests an intimate connection between the boundaries of the sets described above and optimal matchings. To make this clear, we now define the set of rationalizable summaries as the set of -uples such that and are covariations and mutual information corresponding to an optimal matching for some parameter values :

Obviously, rationalizable summaries are feasible and . This definitions allow us to state that rationalizable summaries and extreme feasible summaries coincide. Or, to put it more formally:

Proposition 2

is the frontier of in .

Mutual information level sets. Now consider a covariation vector in the covariogram , and define the rationalizing mutual information

clearly from the definition of and positive homogeneity of , we see that the implicit mutual information function

| (3.1) |

so is the Legendre-Fenchel transform of which is strictly convex; in particular is a function. Conversely, for any mutual information we define and the set of rationalizable covariations by

It follows directly from the convexity of that is the boundary of the set , which is convex and increasing (for inclusion) with respect to .

Note the two limiting cases: when mutual information is zero (corresponding to random matching), then , where . When , consists of the extreme points of the covariogram .

The following result combines the linearity embodied in (SLOI) and the convex structure of the problem:

Proposition 3

Under (O), (S), (GUI) and (SLOI),

a) The social welfare function is positive homogeneous of degree one in . It is convex on and strictly convex on its interior.

b) The subdifferential of at is given by the set of -uples

generated by an optimal matching when parameter values vary.

In particular, when the optimal matching is unique for some , then is differentiable at and

in which case we define

c) The function is on the interior of , and one has

As a corollary, the limiting homogeneous case also has interesting comparative statics, which closely parallel the results above. When the mutual information does not play a role anymore in Theorem 2; so we focus on the covariogram ; and we define . Note in particular that the boundary of the covariogram—which is the polygon in Figure 1—consists of the set of the covariation vectors when varies.

Corollary 1 (Homogeneous comparative statics)

Under (O), (S), (GUI) and (SLOI),

a) The function is convex and positive homogeneous of degree one in .

b) The subdifferential of at is given by the set of -uples

generated by an optimal matching when varies and .

In particular, when the solution is unique for some , then is differentiable at and

Our basic result is that any vector of covariations that is feasible (that belongs to ) can be rationalized for a well-chosen value of total heterogeneity. This is a byproduct of the following result, which sums up the relationships between the sets we introduced:

Proposition 4

Under (O), (S), (GUI) and (SLOI),

a) The sets are the set of extreme points of nested closed and convex sets that expand from to as mutual information goes from 0 to .

b) Any point belongs to exactly one frontier , associated to the mutual information .

c) For a point such that is smooth, letting ; then along

| (3.2) |

Proposition 4 is illustrated on figure 1. Note that when we fix and increase from 0 to , the summary vector for the optimal matching moves continuously from to ; thus part a) tells us that increasing for given moves us from a point on the boundary of to .

Proposition 4 may come as a surprise to the reader: we have imposed quite a few assumptions on the way, and yet it seems that our model still cannot rule out any feasible covariation of types across partners! (Observing a that is outside of is impossible by construction.) Proposition 4 tells us that observing in the interior of rejects the homogeneous model; but that any such can be rationalized by adding the right amount of unobserved heterogeneity.

The interpretation of part c) is simplest when the matrix is diagonal. With several dimensions for types, the optimal matching must sacrifice some covariation in one dimension to the benefit of some covariation in another. The implied sacrifice ratio, quite naturally, is exactly the ratio of the assorting weights along these dimensions. Take for instance the homogeneous case with only two characteristics, and set and . Then the function is decreasing, and the function is increasing. Therefore, when one puts more weight on the second dimension, the covariation of the characteristics in the second dimension increases, while the covariation on the first dimension decreases. Quite intuitively, in the limit where all the weights are put on one dimension, the classical Beckerian theory of positive assortative matching obtains.

More precisely, [3] have shown in an -type homogeneous model that when and for , if is the -optimal matching, and , then the joint distribution of the first characteristics converges towards the maximally correlated distribution. Equivalently, and become comonotonic in the limit, just as in classical positive assortative matching.

3.3 Uniqueness and purity

Uniqueness. As mentioned earlier, the boundary of has kinks when types are discrete. In the homogeneous model (), the optimal matching is pure for almost all values of . Start from such a value . A small change in the value of will not change the optimal matching , or the covariations it generates. Pick some direction in -space and move further away for . At some point , the optimal matching will change to a different pure matching, say ; but this new pure matching will vary with the direction we used to move away from . This is what generates kinks. Note also that in , any matching that is a convex combination of and of is also optimal. So kinks are related to non-uniqueness of the optimal matching. More formally:

Proposition 5

Assume (DD): the distributions and are discrete. Then feasible set is a polytope with a finite number of vertices that correspond to pure matchings.

When there is enough observed heterogeneity, the optimal matching is unique. Indeed, [6] have shown that when the total heterogeneity is large enough (so that is small enough), the solution to Eq. (4.1) is unique.

Purity. A matching is pure if a given type of man cannot be matched to more than one type of women and conversely. Intuition suggests that given sufficient heterogeneity, the optimal matching will not be pure, and its probability weights will react to even small changes in . In fact, we have an even stronger result: even tiny levels of heterogeneity will make the optimal matching impure. To see this, reason by contradiction: take a and any given for which the optimal matching is pure. The objective function is

Note that the derivative with respect to any is infinite in and is finite anywhere else. Since is pure, for any there is only one for which is nonzero. Subtract a positive from each such , and spread it over all zero elements. The new joint distribution is still a feasible matching, and the gain in social surplus from formerly zero probabilities outweighs the loss from other matches. Therefore a pure matching cannot be optimal.

4 Identification

The results in the previous sections give a very useful description of the optimal matchings, and they show that and cannot be identified separately. On the other hand, we have not provided a proof of identification of the remaining parameters yet. We now set out to do so make use for identification purposes of the geometrical interpretation of the matching problem when the observable surplus is a linear combination of known basis functions—this is assumption (SLOI), which we impose throughout this section.

4.1 Nonparametric idenfication

Remember that given assumptions (O) and (S), there exist two functions such that the optimal matching obtains when man maximizes over and woman maximizes over . Now if is the observable component of an optimal matching, it was showed in Section 2 that given assumption (GUI),

Now and depend on and are not easy to characterize as we will see; but we know that they sum up to , so that

In this formula and still depend on in a complex way; but they only appear in terms that depend only on characteristics of one partner. This means that the surplus function is identified up to an additive function of the form .

To state this more formally, define the cross-difference operator as

for any function of . Then we have:

Theorem 4 (Cross-differences are identified up to scale)

Assume (O), (S), (GUI) and (DD). For with , one has:

(i) There exists a unique optimal observable matching which maximizes the social welfare (2.3).

(ii) There exist three vectors , and , and a constant normalized by , which are unique solutions to the following system

| (4.1) |

Further, the constant so defined coincides with the value of the social welfare .

(iii) The probability defined in (ii) coincides with the optimal matching solution of (2.3).

This result expresses that by adjusting the functions and at the right level, one manages to satisfy the “budget constraint” that the matching has the right marginals distributions : hence, these functions and can be interpreted as “shadow prices” of men and women’s observable characteristics.

Theorem 4 has another consequence: the complementarity of dimensions of the observable types of the partners in can be tested directly on , since and have the same sign. Moreover, the relative strengths of complementarities along dimensions and at a point can be estimated by evaluating for values of that differ from along these dimensions.

Theorem 4 immediately gives us an estimator of the observable joint surplus function , up to additive functions of and of . But adding any combination to the joint surplus does not change the optimal matching, as long as we are determined not to have singles—as we assume throughout the paper; and the positive scale factor is irrelevant. So for instance is a perfectly good estimator of if consistently estimates .

When we add a parametric structure under (SLOI), Theorem 4 also gives us an estimator of the assorting weights and the total heterogeneity 555Recall that and are not separately identified.. In fact, the cross-difference operator is linear and so under (SLOI),

if the cross-differences of the are linearly independent, then observing gives us the ’s (along with overidentifying restrictions.) This is a very weak requirement; having linearly dependent basis functions would indeed be a modelling mistake.

This can be very simple in practice; to illustrate, take the diagonal version of the (ER) example. Then if in man and woman are both dropouts, keeping their income classes unchanged and moving them to graduate level in generates

On the other hand, taking man and woman to have different education levels in and swapping their educations to create (again keeping income classes fixed) generates

Therefore we obtain for instance

which is readily estimated from the observed matching.

These results are reminiscent of those in [9], although we obtained them under quite a different set of assumptions: we do not use variation across subpopulations, neither does his rank-order condition apply to our model. Note also that when specialized to one-dimensional types, our result yields that of [16] on testing complementarity of the surplus function by examining log-supermodularity of the match distribution.

4.2 Parametric identification

Our parametric identification strategy will be either based on the knowledge of the matching summaries , which are the sufficient statistics for our model, or of just the covariation , with the assumption that lies on the efficient frontier, that is . In either cases, positive homogeneity imposes the need for a normalization of the parameter .

4.2.1 The normalization rule

Once again, is only identified up to a positive scale factor. Take (SLOI) for instance: was only used to specify the objective function, and so it can be multiplied by any positive constant without any side-effect. In particular, for . Therefore is is quite clear that cannot be identified without fixing some normalisation. So we normalize by the choice

| (4.2) |

where as we recall, .

Our general approach will be to identify the parameter value , and then rescale

4.2.2 Identification of

Note that , therefore, because of the normalization convention, is identified by

| (4.3) |

4.2.3 Identification of

As described above, we look for identifying among the parameters of the form . Remember

so by the enveloppe theorem, is such that . Hence, is identified by

| (4.4) |

4.3 Comparative statics

We define the best additive projector of a vector as

where and minimize

We have immediately that and , and introducing the residue

we get and . The decomposition

is the two-way ANOVA decomposition of . The following proposition will be the fundamental tool for inference. It expresses that the projection residue in the two-way ANOVA decomposition of is the score function .

Proposition 6 (Score function)

Under (O), (S), (GUI), and (SLOI), the score function is given by

that is , where and are solution to Equation (4.1).

As a result, we get an expression for the computation of the Hessian of the social welfare function at fixed .

Proposition 7 (Fisher information matrix)

Under (O), (S), (GUI), and (SLOI), wherever is derivable, we get

where

is the Fisher information matrix. Further,

| (4.5) |

5 Inference

We now turn to the problem of inference. Our data will consist of matched characteristics of pairs , and our null hypothesis is that they were generated by an optimal matching consistent with assumptions (O), (S), (GUI), and (SLOI). Given a proposed specification for the basis functions , and our estimates of the marginal distributions of types and , we would therefore like to infer the values of and which come closest to rationalizing the observed matching. We use our theory to answer two questions:

-

1.

is the observed matching optimal?

-

2.

which parameter vector best rationalizes the observed matching (exactly if the observed matching is optimal, approximately if it is not)?

The primary object of our investigation will be the empirical moments of ,

Let denote the expectation of under the joint distribution of . Standard asymptotic theory of the empirical process ([17]) implies the convergence in distribution

where , being a -Brownian bridge. In particular,

for all .

We shall call the value of the social surplus at parameter obtained with the empirical distributions of observable types and .

Normalization. Recall that because of positive homogeneity, models and are observationally indistinguishable. Just as in the previous section, we impose the normalization convention . When we describe estimators below, we first compute an estimator of the assorting weights for total heterogeneity ; we denote it . We then shall get an estimator of the mutual information . To obtain the normalized estimator in each case, the reader should divide the vector by the scalar .

The results we obtained in sections 2 and 4 suggest two estimation strategies, which we will now define and compare.

5.1 Nonparametric inference

Theorem 4 and its corollary immediately suggest a very simple nonparametric approach. In this discrete case, a nonparametric estimator is readily obtained, by counting the proportion of matches between a man of characteristics and a woman of characteristics . We could pick arbitrary functions and and define

without any reference to basis functions—imposing on the way. Then if we further assume (SLOI) with basis functions , we can apply minimum-distance techniques to recover an estimator , which minimizes some norm

Note that as usual, the minimum value of the norm allows us to construct a test statistic for the hypothesis that is a linear combination of the .

More generally, we know that under (O), (S) and (GUI) only,

thus a nonparametric estimate can be used as a heuristic device to decide on a set of basis functions, and/or to test for the adequacy of such a set.

We now turn to parametric estimators.

5.2 Parametric inference: The Moment Matching Estimator

Our second estimator is based solely on the statistics of the matching covariations . It rests on identification of provided by Eq. (4.4). Therefore is taken as a maximizer of

| (5.1) |

over all possible . This being a strictly concave function, its minimizer is unique; further efficient computation is available. Letting the value of expression (5.1) at the optimal value , we obtain the Moment Matching (MM) estimator, denoted and , by setting

Now if our data was generated by an optimal matching for parameters , the empirical covariations would coincide with the optimal correlations . By construction, the MM estimator is the value of assorting weights such that the predicted covariations coincide with the observed covariations. The Moment matching estimator is consistent and asymptotically Gaussian, and

Theorem 5

Under (O), (S), (GUI) and (SLOI),

where is the Brownian bridge characterized at the beginning of this section and the matrix is the Fisher information matrix expressed above in (4.5). In particular, the MM estimator is asymptotically efficient.

6 Computational issues

With the exception of the semiparametric estimator (SP), our inferential methods require solving for the optimal matching for potentially large populations, and a large number of parameter vectors during optimization. This may seem to be a forbidding task: there exist well-known algorithms to find an optimal matching, and they are reasonably fast; but with large populations the required computer resources may still be large.

Fortunately, it turns out that introducing (our type of) heterogeneity actually makes computing optimal matchings much simpler; this is a boon for the ML and MM estimators666The BP estimator is designed for the homogeneous case and so the following does not apply to it..

To see this, choose a parameter vector and return to the characterization of optimal matchings in equation 2.3, in the continuous case (CD) for simplicity. Dividing by and taking the logarithm, optimal matchings can also be obtained by solving the following minimization program:

Now define a set of probabilities by

and note that given any choice of parameters and known marginals , the probability itself is known.

Determining the optimal matchings therefore boils down to finding the joint probabilities with known marginals and which minimize the Kullback-Leibler distance to :

| (6.1) |

Equivalently, we are looking for the Kullback-Leibler projection of on .

This is a well-known problem in various fields, and algorithms to solve it have been around for a long time. National accountants, for instance, use RAS algorithms to fill cells of a two-dimensional table whose margins are known; here the choice of reflects prior notions of the correlations of the two dimensions of the table. These RAS algorithms belong to a family called Iterative Projection Fitting Procedures (IPFP). They are very fast, and are guaranteed to converge under weak conditions. We only describe the application of IPFP to our model here; we direct the reader to [14] for more information.

The intuition of equation 6.1 is quite clear: the random matching, which is optimal when is very large, has . For smaller ’ s the probability of a match between and must increase with the surplus it creates, ; and given our assumption (GUI) on the distribution of unobserved heterogeneity, it should not come as a surprise that the corresponding factor is multiplicative and exponential.

To describe the algorithm, we split into777It can be shown that at the optimum where .

The functions and of course will only be determined up to a common constant. The algorithm iterates over values . We start from and . Then at step we compute

and

Two remarks are in order here: first, we could just as well start from and and modify the iteration formulæ accordingly. Second and just as in other Gauss-Seidel algorithms, it is important to update one component based on the other updated component: the right-hand sides have and .

If is a fixed point of the algorithm, then

Comparing this formula to Theorem 4 shows the benefit of this reparameterization, since and have a simple interpretation: they represent (up to a common additive constant) the expected utilities of a man of observable characteristics and of a woman of observable characteristics . This can be seen by checking, for instance, that

Thus the IPFP algorithm gives us not only the optimal matching, but also these expected utilities.

The simplification does not stop there. In fact, given data on couples, the marginal assigns probability to each of , and similarly for women. Define a matrix by , and vectors , . Then we end up with the shockingly simple and inexpensive formulæ:

7 Possible extensions and concluding remarks

Our theory so far relies on several strong assumptions. Some of them are easy to relax; we discuss three of them, before turning to potential extensions.

Single households. So far we have not allowed for unmatched individuals. In an optimal matching, some men and/or women may remain single, as of course some must if there are more individuals on one side of the market. The choice of the socially optimal matching can be broken down into the choice of the set of individuals who participate in matches and the choice of actual matches between the selected men and women. Our theory applies without any change to the second subproblem; that is, all of our results extend to and as selected in the first subproblem.

From the point of view of statistical inference, we may lose some efficiency in doing so; we note here that when the unobserved heterogeneity in preferences over partners is separable from the utility of marriage itself, our method does not incur any efficiency loss.

Non-bipartite matching. Bipartite matching refers to the fact that each individual is exogenously assigned in one category—in our terminology, husband or wife. Our analysis in fact is very easy to extend so as to incorporate same-sex unions, and thus to rationalize endogamy in the gender dimension.

To do so, we just need to add one (observed) characteristic, in the form of gender. If for instance gender becomes the first dimension of the characteristics vector, then the observed surplus has an assorting weight that reflects the more typical preference for the opposite sex; while heterogenous preferences and will automatically take into account the dispersion of individual preference for same-sex unions.

Continuous distributions. While we have assumed discrete characteristics, we expect the main thrust of our arguments to carry over to the case where the distributions of the characteristics are continuous. We are working on such an extension; this will require adapting the (GUI) assumption to one that is better-suited to continuous choice.

Revealed Preferences. As mentioned in the section on the Boundary Projection estimator, the Lagrange multiplier is known in the theory of revealed preferences as Afriat’s efficiency index. The analogy in fact goes deeper. Recall the basic theorem on revealed preferences:

Proposition 8 (Afriat)

The following conditions are equivalent:

(i) The observed quantity-price vectors are consistent with maximization of a single utility function;

(ii) There exist scalars such that

is maximized over when for all .

This is reminiscent of a multidimensional matching problem in which prices correspond to the characteristics of men, consumptions to those of women , and there is no unobserved heterogeneity. We are currently exploring this nalogy.

Screening. In the theory of screening, a “type” refers to a set of individual characteristics that are privately observed. Assume that utilities are additively separable in transfers, with

and

Then given quantity-transfer pairs that presumably correspond to different types, it can be shown that

is maximized over when for all .

This again suggests that our methods may help in estimating screening models.

Appendix A Facts from Convex Analysis

A.1 Basic results

We only sum up here the concepts we actually use in the paper; we refer the reader to [11] for a thorough exposition of the topic.

Take any set ; then the convex hull of is the set of points in that are convex combinations of points in . We usually focus on its closure, the closed convex hull, denoted .

The support function of is defined as

for any in . It is a convex function, and it is homogeneous of degree one. Moreover, where is the closed convex hull of , and .

A point in is an extreme point if it does not belong in any open line segment joining two points of .

Now let be a convex, continuous function defined on . Then the gradient of is well-defined almost everywhere and locally bounded. If is differentiable at , then

for all . Moreover, if is also differentiable at , then

When is not differentiable in , it is still subdifferentiable in the following sense. We define as

Then is not empty, and it reduces to a single element if and only if is differentiable at ; in that case .

A.2 Generalized Convexity

In order to make the paper self-contained, we present basic results on the theory of generalized convexity, sometimes called the theory of -convex functions. This theory extends many results from convex analysis and, in particular, duality results, to a much more general setting. We refer to [19], p. 54–57 (or [18], pp. 86–87) for a detailed account888A cautionary remark is in order here: the sign conventions vary in the literature, so our own choices may differ from those of any given author..

Let be a function from the product of two sets to .

Definition 1

Consider any function . Its generalized Legendre transform is defined by

Conversely, take any function ; then its generalized Legendre transform is defined by

A function is called -convex if it is not identically and if there exists such that

Recall that the usual Legendre transform is defined as

thus it coincides with the generalized Legendre transform when is bilinear, and then -convexity boils down to standard convexity.

Our analysis rests on the following fundamental result, which generalizes standard convex analysis.

Proposition 9

For every function ,

with equality if and only if is -convex.

-

Proof

Take any ; then

taking shows that .

Conversely, if then , with . But for any function , the triple transform coincides with . To see this, write

Now for all and ,

as is easily seen by taking ; therefore

Applying this to the such that concludes the proof.

QED.

Appendix B Proofs

B.1 Proof of Theorem 1

In order to prove Theorem 1, some preparation is needed. Remember our shorthand notation , and . For any function , fix and use the theory of generalized convexity briefly recalled in Appendix (A.2) to define

the generalized Legendre transform of with respect to the partial surplus function . We define in the same manner

Similarly, for two functions and , we define

Lemma 1

Let be the set of pairs of functions such that

Then

-

Proof of Lemma 1

By the Kantorovich duality theorem ([19] Theorem 5.10),

(B.1) where is the set of pairs of functions such that

Note the following two facts about the right-hand side of this equality:

-

1.

Since

the infimum in (B.1) can be taken over the pair of functions that satisfy

or

At the optimum this must hold with equality. Going back to Definition 1, it follows that is -convex for every ; and using Proposition 9, we can substitute with , that is:

Given a similar argument on , the objective function can be rewritten as

-

2.

Also note that the constraint of the minimization problem in (B.1) is also

which follows directly from the fact that

Now define

Given points 1. and 2. above, we can rewrite the value as

QED.

-

1.

We are now in a position to prove the theorem.

-

Proof of Theorem 1

Start by drawing two samples of size of men and women from their population distributions and ; we denote the corresponding values of the observed characteristics and . Call and the corresponding sample distributions; e.g. assigns a mass

to the value of observable characteristics of men. The Law of Large Numbers implies that and converge in distribution to and , the population distributions of the observable types. Now we have for any possible

As gets large enough, each of the possible values of observable characteristics of women is included in the sample ; then the in the above expression runs over all such possible values . But under (GUI), conditional on the random variables are independent Gumbel random variables with scaling factor , so we get

hence, taking the limit and integrating over ,

and similarly

QED.

B.2 Proof of Theorem 2

-

Proof

By theorem (1), we have

for which we form the Lagrangian

where

Clearly, and in the inner minimization problems satisfy

(B.3) note that these equations imply that and , so that . Rearranging terms,

and noticing that gives the desired result.

B.3 Proof of Theorem 3

B.4 Proof of Theorem 4

-

Proof

(i) For , the map is strictly convave and finite, on the convex domain ; thus there exists a unique maximizing (2.3).

(ii) Let be the set of pairs of functions such that , and for , let be the partition

Introduce

as a result and are probability vectors. By the strict concavity of , there exists a unique vector such that

and .

B.5 Proof of Proposition 3

-

Proof

a) The convexity of follows from the fact that it is the supremum of expression which are linear with respect to .

b) As a result, by the enveloppe theorem, the subdifferential of at is the set of such that . When this set consists of a single point, is differentiable at and

B.6 Proof of Proposition 1

-

Proof

Non-emptiness is obvious. Now is convex: Let and be two feasible cross-product matrices in . We first show that for any , is in . By definition of , there exist and in such that and . Let . Then , and , thus . Now we prove that is closed: Let be a sequence in converging to , and let be the associated matching. By Theorem 11.5.4 in [7], as is uniformly tight, has a weakly converging subsequence in ; call its limit. Then is the cross-product associated to , so that . Finally, is a closed convex set as it is the upper graph of the function defined in Eq. (3.1).

B.7 Proof of Proposition 2

-

Proof

is the reunion of the subgradients of which was seen in Prop. 1 to be the support function of : hence is the frontier of .

B.8 Proof of Proposition 3

-

Proof

a) Positive homogeneity and convexity of degree one follows from the fact that is the support function of . Strict convexity for follows from the strict convexity of . Part b) follows directly from the enveloppe theorem. Part c) results of being the Legendre transform of which is strictly convex, hence it convex on , differentiable on its interior, and by the enveloppe theorem, .

B.9 Proof of Proposition 4

-

Proof

a) The sets are extreme points of the sets which are closed convex sets. One has which corresponds to , and . Clearly, one has . Finally, the form vanishes along , so one has , hence the result.

Appendix C Proof of Proposition 6

-

Proof

By equation (4.1), we have

hence . But we have that

thus for all and

hence , while , therefore

is the orthogonal decomposition of on , hence .

Appendix D Proof of Proposition 7

-

Proof

We have

hence

Further, by the orthogonality of and ,

QED.

Appendix E Proof of Theorem 5

-

Proof

We have , hence at first order . But as is the Legendre transform of , it results that by Proposition 7.

Appendix F Connections to Statistical physics

There is in fact, a very close parallel between our theory and Statistical physics and Thermodynamics. We refer to [13] for more on Statistical physics, and to [12] for connection with Information theory. To give hints to the parallel, let us just mention that the social welfare is the analog of a total energy; the term is the analog of an internal energy; is the analog of an entropy; the parameter is the analog of a temperature. A pure matching is the equivalent of a solid state; the points of nondifferentiability of are analog to critical points.

Note that equation 4.1 is known in the mathematical physics literature as the Schrödinger-Bernstein equation, cf. [15] and references therein. It was first studied by Erwin Schrödinger as part of his research program in time irreversibility in Statistical Physics. Interestingly, it also bears some connections with the better-known “Schrödinger equation” in Quantum mechanics of the same inventor. In fact, as discovered by Zambrini, a dynamic formulation of this equation is the Euclidian Schrödinger equation which arises in Ed Nelson’s formulation of “Stochastic Mechanics,” an Euclidian analog of quantum mechanics. For more on this topic, see [13], Chap. 19.

References

- [1] G. Becker “A theory of marriage, part I” In Journal of Political Economy 81, 1973, pp. 813–846

- [2] C. Blair “Every finite distributive lattice is a set of stable matchings” In Journal of Combinatorial Theory, Series A 37, 1984, pp. 353–356

- [3] G. Carlier, A. Galichon and F. Santambrogio “From Knothe’s transport to Brenier’s map and a continuation method for optimal transport” preprint available on http://arxiv.org/abs/0810.4153, 2008

- [4] P.-A. Chiappori, B. Salanié, A. Tillman and Y. Weiss “Assortative Matching on the Marriage Market: A Structural Investigation” mimeo Columbia University, 2008

- [5] E. Choo and A. Siow “Who Marries Whom and Why” In Journal of Political Economy 114, 2006, pp. 175–201

- [6] C. Decker, B. Stephens and R. McCann “When do systematic gains uniquely determine the number of marriages between different types in the Choo-Siow matching model? Sufficient conditions for a unique equilibrium” mimeo University of Toronto, 2009

- [7] R.. Dudley “Real Analysis and Probability” Cambridge University Press, 2002

- [8] F. Echenique “What matchings can be stable? The testable implications of matching theory” In Mathematics of Operations Research 33, 2008, pp. 757–768

- [9] J. Fox “Identification in Matching Games”, 2009

- [10] D. Gale and L. Shapley “College Admissions and the Stability of Marriage” In American Mathematical Monthly 69, 1962, pp. 9–14

- [11] J.-B. Hiriart-Urrut and C. Lemaréchal “Fundamental of Convex Analysis” Springer, 2001

- [12] M. Mézard and A. Montanari “Information, Physics, and Computation” Oxford University Press, 2009

- [13] G. Parisi “Statistical Field Theory” Perseus Books, 1988

- [14] L. Rüschendorf “Convergence of the iterative proportional fitting procedure” In Annals of Statistics 23, 1995, pp. 1160–1174

- [15] L. Rüschendorf and W. Thomsen “Closedness of Sum Spaces and the Generalized Schrˆdinger Problem” In Theory of Probability and its Applications 42, 1998, pp. 483–494

- [16] A. Siow “Testing Becker’s Theory of Positive Assortative Matching”, 2009

- [17] A. Vaart “Asymptotic Statistics” Cambridge University Press, 1998

- [18] Cédric Villani “Topics in Optimal Transportation” American Mathematical Society, 2003

- [19] Cédric Villani “Optimal Transport, Old and New” Springer, 2009