Next Generation Models for Portfolio Risk Management: An Approach Using Financial Big Data

Abstract

This paper proposes a dynamic process of portfolio risk measurement to address potential information loss. The proposed model takes advantage of financial big data to incorporate out-of-target-portfolio information that may be missed when one considers the Value at Risk (VaR) measures only from certain assets of the portfolio. We investigate how the curse of dimensionality can be overcome in the use of financial big data and discuss where and when benefits occur from a large number of assets. In this regard, the proposed approach is the first to suggest the use of financial big data to improve the accuracy of risk analysis. We compare the proposed model with benchmark approaches and empirically show that the use of financial big data improves small portfolio risk analysis. Our findings are useful for portfolio managers and financial regulators, who may seek for an innovation to improve the accuracy of portfolio risk estimation.

JEL classification: C13, C32, C55, C58.

Key words and phrases: Value at Risk, financial big data, blessing of dimensionality, principal component analysis, multivariate GARCH, factor model.

1 Introduction

The widespread failure of portfolio risk management models observed in the 2008 financial crisis raises the question of how risk managers can analyze the risks of investment portfolios while taking into account systematic risks caused by a systemic crisis. Extant literature has developed a range of risk measurement methods, for example, Value at Risk (VaR), expected shortfall (ES), entropic Value at Risk (EVaR), and superhedging price (Acerbi and Tasche, , 2002; Ahmadi-Javid, , 2012; Bensaid et al., , 1992; Jorion, , 2000). VaR, in particular, has been widely used to estimate the level of risk by measuring the amount of loss for investments during a given period under normal market conditions (Jorion, , 2000). Especially, the literature documents the development of risk models with VaR to accommodate non-normal market conditions, for example, asymmetric, heavy-tailed stock returns, and volatility clustering (see, e.g., Huisman et al., (1998); Natarajan et al., (2008); Wu and Shieh, (2007); Zoia et al., (2018) for non-normal stock returns; Billio and Pelizzon, (2000); Broda and Paolella, (2009); Engle and Manganelli, (2004); Fantazzini, (2008); McNeil and Frey, (2000) for volatility clustering).

However, the 2008 financial crisis demonstrates that the development of risk models with dynamics for non-normal conditions does not guarantee financial firms to be successful in managing extreme systematic risks. One of the supporting arguments can be that risk managers still consider only stock data in their target portfolio (Fan and Gu, , 2003; Hendricks, , 1996; Patton et al., , 2019). They tend to overlook the risks of the assets that are not included in the portfolio; hence, the portfolio size for risk analysis can be relatively small. This so-called small portfolio risk analysis may not sufficiently capture portfolio risk dynamics, particularly systematic risks inherent in the market.

In this regard, this study highlights a clear message that the use of financial big data can help risk managers take into consideration latent risks that cannot be captured in the portfolios of interest. The contributions of this paper are threefold. First, we propose a dynamic risk model to resolve the above-mentioned problem by capturing systematic risk dynamics. At the core of the proposed model is the use of financial big data to analyze portfolio risks. The use of financial big data can help risk managers take into account a universe of assets larger than the size of their portfolios. This usefulness can lead to a higher accuracy of risk prediction, particularly, when it comes to capturing the systematic risk inherent in the markets. Consequentially, financial regulators can benefit from a high accuracy of risk prediction for market players to maintain the stability of financial markets and thus reduce the probability of a systemic risk occurrence.

One may be concerned about the fact that the use of financial big data can lead multivariate VaR methods to be computationally intensive in parameter estimation, which is called the curse of dimensionality.222For instance, when the BEKK model (Engle and Kroner, , 1995) is conducted on -dimensional log return data, the number of parameters increases with the order. As the dimension increases, the parameter estimation becomes computationally demanding due to the exploding of computation time, which is the NP hard problem. Even if it is possible to estimate the parameters, they are not consistent estimators (Bickel and Levina, , 2008; Engle et al., , 2017). Our second contribution is to address this point in that the proposed model overcomes the curse of dimensionality with a two-step estimation. The first step is to use the principal orthogonal complement thresholding (POET) procedure (Fan et al., , 2013) to estimate the latent factor and idiosyncratic component of the approximate latent factor model (Ait-Sahalia and Xiu, , 2017; Fan and Kim, , 2018; Fan et al., , 2019; Kim et al., , 2018; Li et al., , 2018). The second step is a maximum quasi-likelihood estimation for the Generalized AutoRegressive Conditional Heteroskedasticity (GARCH) parameter with the latent factor estimator from the first step. The estimated GARCH parameters are used to predict one-step ahead portfolio volatility, with which the one-step ahead VaR is predicted under the parametric and non-parametric -based approaches (Brooks and Persand, , 2003; Giot and Laurent, , 2004; Hull and White, , 1998).

Lastly, our contribution is the incorporation of financial big data featuring the blessing of dimensionality (Donoho, , 2000; Fan and Kim, , 2019; Fan et al., , 2013; Li et al., , 2018) by discussing the asymptotic properties of -based approaches. Upon the risk measurement procedure with integrated econometric approaches, our study is the first to suggest how a big data approach can help financial risk management. The proposed model can be particularly helpful for financial firms and regulators, who may be concerned about the stability of financial markets and question how big data can be optimally used for an improved prediction of risks.

The rest of the paper is organized as follows. In Section 2, we introduce the concept of VaR and develop a dynamic risk model. In Section 3, we propose a maximum quasi-likelihood estimation method and study its asymptotic behavior. Section 4 shows how the large volatility matrix can be predicted, how the proposed method can be applied to measure VaR, and how the curse of dimensionality can be solved. In Section 5, we implement the Monte Carlo simulation to check the finite sample performance of the proposed methods and apply the proposed VaR measure to the empirical data. We conclude in Section 6.333All technical proofs are provided in the online supplement (see Appendix A).

2 Model setup

Consider a market consisting of stocks. Let denote the -valued random vector of the assets’ log returns at time . Then, the portfolio is characterized by a vector of asset weights , for example, . We assume that the log returns admit the factor model (Ait-Sahalia and Xiu, , 2017; Bai, , 2003; Carhart, , 1997; Fan et al., , 2013, 2019; Fama and French, , 1992, 1993, 2015) as follows:

| (2.1) |

where is a mean vector, is an -dimensional factor, is a factor loading matrix, and is an idiosyncratic component. We assume that the factor and idiosyncratic component are independent, and without loss of generality, we assume that the mean of and are zero. Usually, the number of market factors is much smaller than the number of assets, so we assume that is finite. Moreover, in this paper, we consider the latent factor model (Ait-Sahalia and Xiu, , 2017; Fan et al., , 2013, 2019; Li et al., , 2018), so and are not observable. In this section, under the latent factor model, we propose a VaR estimation procedure.

2.1 -Based VaR method

One of the most popular risk measures is VaR, which estimates how much a portfolio of assets might lose under normal market conditions. Specifically, VaR at level is defined as the -percentile of a portfolio log return distribution as follows:

| (2.2) |

where denotes the conditional distribution of the portfolio log returns given a filtration representing information to time . When the portfolio log return distribution follows a location-scale family, such as normal distribution and t-distribution, we can obtain VaR from the portfolio conditional mean and conditional volatility given a filtration information to time as follows:

| (2.3) |

where is an -quantile value of the distributions of the standardized . This method is called a -based approach (Jorion, , 2000). The performance of the -based approach depends on three components: the conditional mean , conditional volatility , and quantile . Quantile can be determined using the parametric and non-parametric methods. The parametric method involves the assumption of the parametric distribution for the standardized log return , such as normal distribution or student-t distribution, and is determined based on the -quantile of each distribution. The non-parametric method uses a sample quantile of the historical standardized portfolio log returns . Detailed implementations are described in Section 4.2. However, several empirical studies indicate that the portfolio conditional mean does not have strong time series patterns (Cajueiro and Tabak, , 2004; Fama, , 1998; Malkiel, , 2003; Narayan and Smyth, , 2004), which makes it difficult to predict the mean. In this paper, we simply assume that the mean process is constant over time in order to reduce the model misspecification error. Meanwhile, in the stock market, we observe volatility time series structures, such as volatility clustering (Mandelbrot, , 1963). From this point of view, it is crucial to determine the dynamic structure of the conditional volatility . Thus, in this paper, we focus on how the dynamic volatility structure can be incorporated in VaR. We note that the mean structure would have a significant effect on VaR; hence, a parametric structure of the mean process should be developed. We leave this for future study.

2.2 Small portfolio risk analysis

When analyzing portfolio volatility, we usually investigate only the stock log return data that belong to the portfolio. For example, let be the -dimensional log return vector whose stocks belong to the portfolio. We also denote the conditional co-volatility matrix of by and the -dimensional portfolio weight vector by . Then, the portfolio conditional volatility can be obtained from as follows:

To account for the market dynamics of the portfolio return, researchers have introduced several dynamic models, such as the BEKK (Engle and Kroner, , 1995), CCC (Bollerslev, , 1990), and portfolio univariate GARCH (Bollerslev, , 1986). See also Engle, (2002), Kawakatsu, (2006), Paolella et al., (2021), Paolella and Polak, (2015), and Van der Weide, (2002). The BEKK model with the conditional mean vector has the following structure:

where is an lower triangular matrix, is the square root of the matrix , and are matrices, and is some arbitrary distribution with mean zero and variance one. As in the above BEKK model, the dynamic volatility models have the autoregressive form of the historical squared returns. Empirical studies shows that the volatility is heterogeneous, and these models can explain the market dynamics (Bollerslev, , 1986, 1990; Engle, , 2002; Engle and Kroner, , 1995; Kawakatsu, , 2006; Van der Weide, , 2002). Moreover, the dynamic volatility model helps to improve the measurement of VaR (Engle and Manganelli, , 2004; Giot and Laurent, , 2004; Kuester et al., , 2006). That is, the performance of measuring VaR can be improved by identifying the market dynamics. In financial markets, we often observe that much of the market dynamic structure comes from the systematic risk, which is related to the entire stock market; hence, the systematic risk information is contained in the entire stock. From this point of view, even if we consider only the small number of assets in the portfolio, to account for the market dynamics, we need to investigate the whole stock market and extract the systematic risk information from the stock returns. One of the naive extensions is to use a multivariate volatility model, such as the BEKK and CCC models, for the whole stock market. However, when applying these volatility models to the incorporation of a large number of assets, we face the curse of dimensionality (Bickel and Levina, , 2008; Pakel et al., , 2020; Engle et al., , 2017). Specifically, let be the total number of assets, and then the number of parameters quadratically increases with . Hence, with a large , the estimated model is statistically inconsistent. Furthermore, in practice, the parameter optimization takes exponential computation time, which is known as the non-deterministic polynomial-time (NP) hard problem. Thus, applying the usual multivariate volatility model to a large number of assets is not feasible. In this paper, we discuss how the curse of dimensionality issue can be handled while accounting for the market dynamics.

2.3 High-dimensional dynamic volatility model

In this section, we propose a dynamic factor model under the latent factor structure in (2.1). The factor model implies that the risk of assets stems from factor and idiosyncratic components, which are called systematic and idiosyncratic risks, respectively. An idiosyncratic risk is related to the firm-specific risk; hence, it does not affect the entire market. Moreover, it can be mitigated by the portfolio diversification. By contrast, a systematic risk arises from common market factor, such as interest rate, inflation, oil price, etc. Because systematic risk affects the entire market, we cannot mitigate this risk. From this point of view, we impose a dynamic structure on the factor to account for the market risk. For the idiosyncratic risk, we employ some martingale assumption, for example, the idiosyncratic volatility is constant over time. Then, the conditional expected co-volatility matrix of given the current available information is expressed as follows:

| (2.4) |

where , and represents the idiosyncratic volatility matrix. Under the framework (2.4), the market dynamics can be explained by the factor volatility dynamics.

The latent factor model has an identification problem in . For example, the pair is not distinguishable from for any orthonormal matrix . To uniquely define the latent factor model, we often impose the following identifiability condition (Bai and Li, , 2012; Bai and Ng, , 2013; Fan et al., , 2013; Kim and Fan, , 2019; Li et al., , 2018):

| (2.5) |

The identification condition (2.5) implies that the scaled factor loading matrix and elements of are the eigenmatrix and eigenvalues of the conditional variance of the factor part. Thus, the market dynamics are explained by the dynamic structure of the eigenvalues, whereas its factor loading matrix is constant over time.

To account for the factor dynamics, we employ the famous GARCH model (Bauwens et al., , 2006; Engle and Kroner, , 1995; Engle, , 2002, 2016; Van der Weide, , 2002). The conditional expected volatility of the factor is modeled by the following GARCH structure:

| (2.6) |

where ’s are i.i.d. random variables with mean zero and unit variance; is an -dimensional vector of the conditional expected factor volatility , that is, , where is a vector whose elements are diagonal entries of , is an element-wise squared vector of the factor log return , and is the GARCH parameters. The GARCH model in (2.3) indicates that the conditional expected volatility of the factor is the autoregressive form of the historical squared factor log returns. Thus, we expect that this model can capture the stylized market features, such as the volatility clustering and heavy tail. The empirical study in Section 5.2 also supports this.

The idiosyncratic component comes from the firm-specific risk, so their risk is not strongly connected. Empirical studies show that there are some local factors that affect few other idiosyncratic components (Ait-Sahalia and Xiu, , 2017; Boivin and Ng, , 2006). In light of these, we allow a weak relationship between idiosyncratic components so that the idiosyncratic volatility satisfies the following sparse condition:

| (2.7) |

where , and the sparsity measure diverges slowly with the dimension , for example, . We define . This sparsity condition is widely employed in the large convariance matrix inferences (Ait-Sahalia and Xiu, , 2017; Bickel and Levina, , 2008; Cai and Liu, , 2011; Fan et al., , 2013, 2019; Kim and Fan, , 2019). When the idiosyncratic volatility satisfies the exact sparsity, that is, , the sparsity condition indicates that each asset has at most non-zero idiosyncratic correlations with other assets.

Under the volatility structure (2.4) and (2.3), the VaR of portfolios in (2.3) can be calculated as follows:

To evaluate the above VaR value, we need to estimate the unobserved factor components and the idiosyncratic volatility. However, to incorporate the entire market asset information, we consider a large number of assets and consequently run into the curse of dimensionality problem. In the following section, we discuss how to overcome this issue and introduce an estimation procedure to incorporate the financial big data for risk analysis.

3 Factor dynamics estimation

First, we define the notations. We denote , and by the matrix spectral norm, Frobenius norm, and max norm, respectively. We use as a big-O in probability, as the largest eigenvalue of the square matrix , and as the vectorization of . We also denote the true parameters by .

3.1 Latent factor estimation

To estimate the model parameter , we first need to estimate the latent factor components and . We recall that the conditional volatility matrix is

and the mean conditional volatility matrix is

where . Under the identification and sparsity conditions (2.4) and (2.7), the mean conditional volatility matrix has the low-rank plus sparse structure that is widely used in the high-dimensional factor analysis (Ait-Sahalia and Xiu, , 2017; Fan et al., , 2013, 2019; Kim and Fan, , 2019). With the low-rank plus sparse structure, Fan et al., (2013) introduced the POET estimation procedure to estimate the latent factor volatility and idiosyncratic volatility matrices. To harness the POET procedure, we need a good proxy of the mean conditional volatility matrix. We use the sample covariance matrix with sample mean , and under some mild condition, the martingale convergence theorem implies that the sample covariance matrix converges to . Thus, we apply the POET procedure with the sample covariance matrix to estimate the latent factor components. Specifically, the eigenvalue decomposition admits

| (3.1) |

where and are the largest eigenvalues and eigenvectors of the sample covariance matrix , respectively. Then, the factor loading matrix estimator is , and the mean factor volatility matrix estimator is , where is a diagonal matrix whose diagonal entries are . Note that has a multiplier so that satisfies the condition . Then, the latent factors can be obtained as follows:

| (3.2) |

Theorem S2.1 in the online supplement shows that the convergence rate of is . We note that when the factor is not observable and the number of assets is finite, the latent factors are impossible to estimate. By contrast, Theorem S2.1 shows the blessing of financial big data in the latent factor estimation. Specifically, every asset contains the common market information. Thus, as the number of assets increases, the information for the latent factors also increases. Therefore, more stock samples exhibit a clearer latent signal, and we can estimate the latent factors consistently with the convergence rate .

3.2 Maximum quasi-likelihood estimation

In this section, we propose a model parameter estimation procedure. Specifically, we adopt the following quasi-maximum likelihood estimation (QMLE) method:

| (3.3) |

where is a compact parameter space. Then, the well-developed asymptotic theorems for the QMLE provide the consistency (Comte and Lieberman, , 2003). However, the factors are not observable; hence, to evaluate the quasi-likelihood function, we use the non-parametric factor estimator . For example, the conditional co-volatility is estimated by

| (3.4) |

and we use as the initial value. Note that is the unconditional volatility of the factor. Then, we calculate the quasi-likelihood function with the conditional co-volatility estimator and obtain the maximum quasi-likelihood estimator as follows:

| (3.5) |

Theorem S3.1 in the online supplement shows the consistency of .

4 Large volatility matrix estimation and VaR forecast

4.1 Estimation of the one-step ahead large volatility matrix

In the previous section, we find the blessing of dimensionality in the latent factor estimation. However, when estimating large volatility matrices, we still suffer from the curse of dimensionality. For example, sample volatility matrix estimators are inconsistent when both the number of assets and sample size go to infinity (Bickel and Levina, , 2008; Cai and Liu, , 2011). To overcome the curse of dimensionality, we impose the sparse structure (2.7) on the idiosyncratic volatility matrix. As discussed in Section 2.3, in the stock market, the co-movement of stocks can be explained by the common factor, and the remaining idiosyncratic co-volatilities are weakly correlated. Thus, the sparsity condition is realistic. To estimate the sparse idiosyncratic volatility matrix, we employ the POET procedure (Fan et al., , 2013) as follows. First, we estimate the input idiosyncratic volatility matrix estimator by using the non-pervasive eigen-components as follows:

where the eigenvalues ’s and eigenvectors ’s are defined in (3.1). Then, we apply the thresholding method to the input idiosyncratic volatility matrix estimator as follows:

| (4.1) |

where is an indicator function, and is a shrinkage function satisfying . The examples of the shrink function are the soft thresholding function and the hard thresholding function . The thresholding level will be given in Theorem 4.1. The working principle of the thresholding method is that the co-volatility is zero if the estimated correlation is weak. This makes the estimated idiosyncratic volatility matrix estimator sparse, so the estimated idiosyncratic volatility satisfies the sparse condition.

With the estimated factor volatility and idiosyncratic volatility matrix , we estimate the conditional volatility matrix as follows:

| (4.2) |

We call the conditional volatility matrix estimator the P-GARCH estimator.

The following theorem shows the asymptotic behaviors for the P-GARCH estimator.

Theorem 4.1.

Remark 1.

Theorem 4.1 shows that the P-GARCH is the consistent estimator as long as .

With the realistic low-rank plus sparse structure, we can enjoy the blessing of dimensionality for estimating the factor volatility matrix. Moreover, using the regularization method, as shown in Theorem 4.1, we can overcome the curse of dimensionality.

4.2 One-step ahead VaR forecast from financial big data

In this section, we discuss how the VaR value can be measured with the P-GARCH estimator in (4.2). Using the plug-in method, we estimate the one-step ahead VaR as follows:

| (4.3) |

where is an -quantile, and is a sample mean vector. To evaluate the VaR value, we need to determine the -quantile value. To do this, we assume that the standardized portfolio log returns are i.i.d. Then, when the standardized portfolio log returns follow the standard normal distribution, is the -quantile of the standard normal . When the standardized portfolio log returns follow the multivariate t-distribution with the degrees of freedom , then , where is an -quantile of the t-distribution with the degrees of freedom (Glasserman et al., , 2002). We call them the parametric -based VaR estimator. The performance of the parametric -based VaR estimator depends on the distribution assumption. On the other hand, to obtain distribution robust VaR estimators, we use the non-parametric sample quantile method, which we call the non-parametric -based VaR estimator. For example, is set to be -th smallest value of , where is a ceiling function.

Then, the following theorem shows the convergence rates of VaR.

Theorem 4.2.

In this paper, we focus on investigating the effect of the VaR estimator with the financial big data for a small portfolio. When we do not incorporate financial big data, that is, is finite, the absolute VaR error is not consistent for all parametric and non-parametric estimators. This is because the term does not converge and so the latent factor estimation error is dominant. Therefore, Theorem 4.2 supports that incorporating financial big data leads to the blessing in the VaR forecast by capturing common factor dynamics.

Remark 2.

In this paper, we consider the parametric and non-parametric quantile structures. However, imposing the parametric structure, such as normal and Student distributions, on the standardized returns does not explain the skewness of the asset returns. Furthermore, the empirical quantile approach can have large errors in the extreme tail and does not work well when we calculate other risk meausures, such as expected shortfall. Thus, it is important and interesting to develop a quantile estimation procedure, which is able to account for stylized features of the asset returns, such as skewness and heavy-tailedness. We leave this for future study.

5 Numerical studies

5.1 Simulation study

In this section, we conducted Monte Carlo simulations to check the finite sample performances of the proposed P-GARCH and corresponding VaR model. The data-generating process is analogous to the models (2.1) and (2.4). The number of factors was chosen to be ; the mean of is set to be zero ; and the factor loading matrix was randomly sampled from the first right singular vector of random matrix, which has the elements . The latent factors were generated by the multivariate normal distribution with the conditional expected volatility as follows:

where ,

The idiosyncratic risk was generated from the multivariate normal distribution with the following sparse co-volatility:

| (5.1) |

We varied from 20 to 500 and from 500 to 10,000, and employed the QMLE procedure in Section 3.2 to estimate the GARCH parameters. We repeated the entire procedure 500 times.

| MAE | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 20 | 500 | 0.138 | 0.088 | 0.068 | 5.706 | 9.483 | 12.637 | 14.279 | 18.768 | 21.801 |

| 2000 | 0.060 | 0.047 | 0.042 | 2.816 | 4.343 | 6.830 | 11.338 | 13.448 | 15.169 | |

| 4000 | 0.046 | 0.040 | 0.034 | 2.033 | 3.359 | 5.621 | 9.738 | 10.703 | 14.345 | |

| 6000 | 0.039 | 0.032 | 0.031 | 1.736 | 2.887 | 5.436 | 8.871 | 9.450 | 12.538 | |

| 10000 | 0.030 | 0.031 | 0.029 | 1.333 | 2.825 | 4.947 | 8.279 | 8.912 | 12.923 | |

| 100 | 500 | 0.124 | 0.079 | 0.060 | 5.816 | 8.651 | 12.264 | 13.739 | 16.993 | 19.134 |

| 2000 | 0.056 | 0.040 | 0.028 | 2.594 | 4.306 | 5.933 | 10.340 | 12.012 | 13.912 | |

| 4000 | 0.040 | 0.027 | 0.020 | 1.846 | 2.925 | 3.978 | 9.869 | 10.098 | 12.730 | |

| 6000 | 0.029 | 0.021 | 0.015 | 1.550 | 2.263 | 3.147 | 8.539 | 8.335 | 11.924 | |

| 10000 | 0.023 | 0.018 | 0.012 | 1.047 | 1.874 | 2.606 | 7.993 | 7.731 | 10.932 | |

| 500 | 500 | 0.118 | 0.079 | 0.055 | 5.788 | 8.539 | 11.931 | 14.059 | 16.716 | 18.482 |

| 2000 | 0.058 | 0.039 | 0.027 | 2.734 | 4.208 | 5.619 | 10.161 | 11.007 | 13.436 | |

| 4000 | 0.039 | 0.027 | 0.019 | 1.786 | 2.916 | 3.948 | 8.975 | 9.451 | 12.525 | |

| 6000 | 0.031 | 0.023 | 0.015 | 1.546 | 2.448 | 3.571 | 8.615 | 8.533 | 11.790 | |

| 10000 | 0.024 | 0.018 | 0.012 | 1.057 | 1.764 | 2.456 | 7.932 | 7.477 | 10.843 | |

Note: To save space, we report only the first 3 elements of and are reported. The other results have a similar pattern.

Table 1 shows the mean absolute error (MAE) of the QMLE estimate for various and . For the sake of spatial efficiency, we only documented estimation results with nine parameters.444The estimations with the rest of parameters provide similar results, which are available upon request. The result illustrates that MAEs decreases as the parameter as or increases, which supports the theoretical findings in Theorem S3.1.

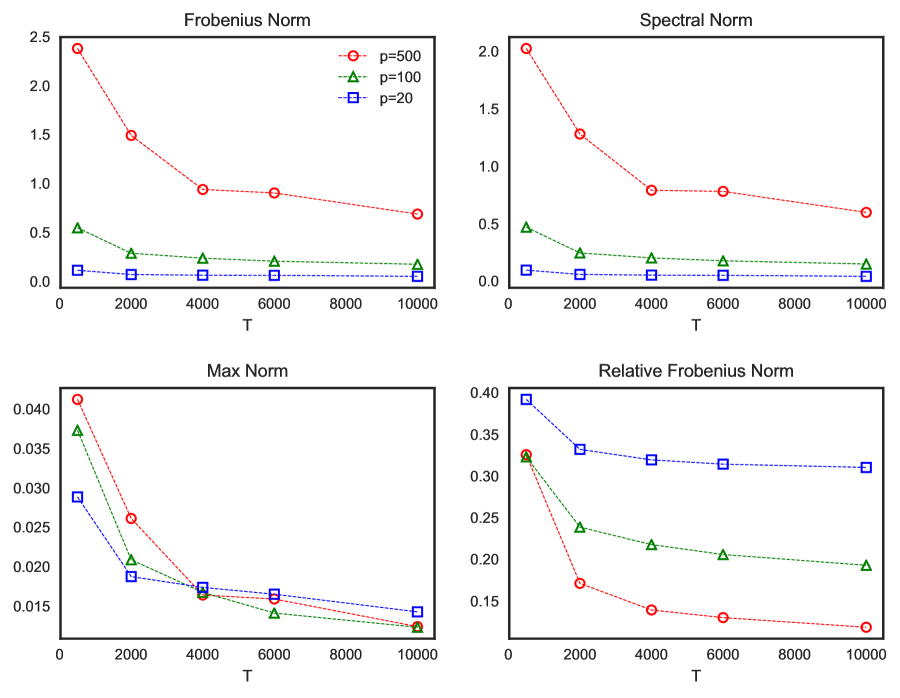

With the estimated parameter , we validated the one-step ahead volatility prediction with several matrix norms. We implemented the thresholding procedure for the idiosyncratic volatility in (4.1) with the tuning parameters and . Figure 1 displays the prediction errors of with the Frobenius, spectral, max, and relative Frobenius norms. We find that the errors are large at for the Frobenius and spectral norms that depend on the dimensionality , whereas the error of the relative Frobenius norm decreases as the dimension p increases. This result thus highlights that the relative Frobenius norm can lead to the blessing of dimensionality, thereby helping risk managers enjoy the use of financial big data for volatility prediction. The max norm shows no significant difference for different , which can be explained by the fact that a large volatility matrix is more likely to have a large max norm error, despite a decrease in the element-wise error. In all cases, the errors decrease as the sample size increases, which supports the theoretical findings in Theorem 4.1.

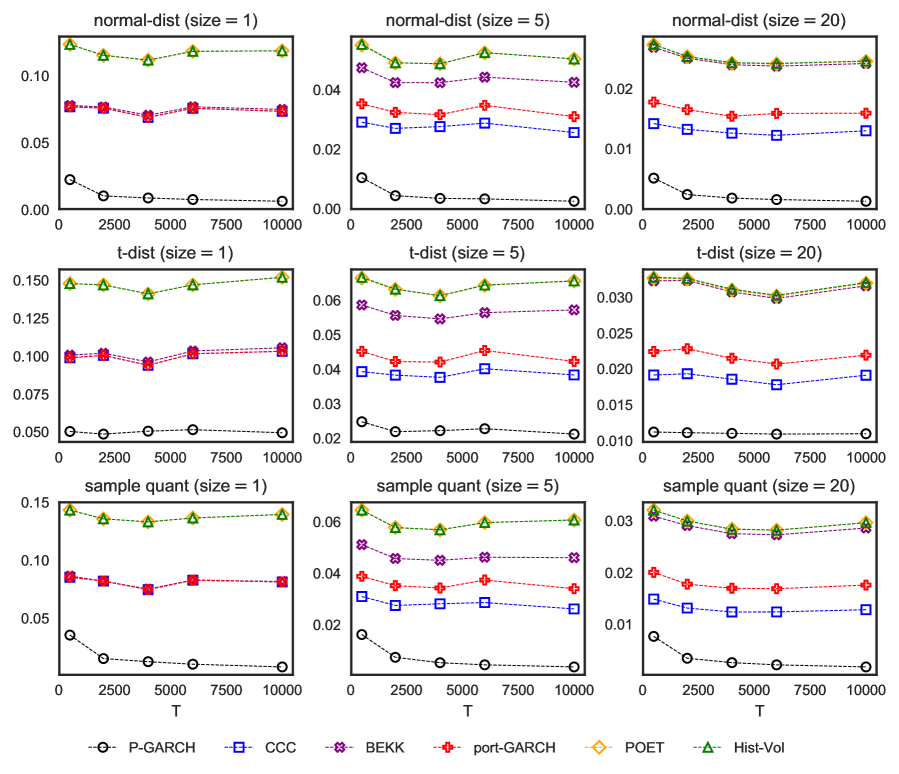

We compared the performance of predicting one-step ahead volatility matrices of the assets in the portfolio to clarify the benefits of using financial big data for small portfolio risk analysis We set the portfolio size as and the total number of assets as . To capture the market dynamics within the portfolios of interest and compare with our proposed model (P-GARCH), we considered the CCC model (Bollerslev, , 1990), and BEKK with diagonal-constraint and variance targeting (Engle and Kroner, , 1995; Pedersen and Rahbek, , 2014). Additionally, in the empirical study, we often impose the static or slow time varying covariance assumption, and under this condition, we adopted POET (Fan et al., , 2013) and historical sample covariance (Hist-Vol). Figure 2 plots the average predicted volatility errors of the portfolio volatility matrix against the sample size under the Frobenius, spectral, max, and relative Frobenius norms. We observe that the P-GARCH model is superior to the other multivariate volatility matrix models by showing much lower errors across different sample sizes. This finding can be explained by the fact that the P-GARCH can address the market dynamics with small portfolios, whereas the others cannot fully address dynamics.

Finally, we compared the VaR forecasting performance with the small portfolio risk analysis methods. We set as 1% and fixed and varied the portfolio size from 1 to 20. We also calculated the small portfolio matrix estimators based on the P-GARCH, CCC, BEKK, POET, and Hist-Vol for the volatility forecast. We compared the considered models with the portfolio univariate GARCH(1,1) model, which is a widely-used approach to modeling a portfolio return (Bollerslev, , 1986). For the -quantile, we considered the normal and student-t distribution with 6 degrees of freedom () for the parametric method, whereas we used the non-parametric method with -th smallest values of the standardized portfolio log returns, as in Section 4.2. The portfolio was set to be equally weighted. The true VaR is , where is the -quantile for the standard normal distribution.

Figure 3 shows the MAEs of the 1%-level VaR forecasts for with 500 replications. We identify that the P-GARCH outperforms the other models for any -based methods and portfolio size. When comparing the quantile estimation methods, given that the true model is based on the normal distribution, the normal distribution-based method shows the best performance. However, the sample quantile-based method shows similar performance as the sample size increases. This is because the sample quantile is a non-parametric consistent estimation procedure; thus, with a large , we can estimate the quantile consistently. Finally, the parametric-based methods, such as P-GARCH, CCC, BEKK, and port-GARCH, usually perform better than the non-parametric methods. However, as the portfolio size increases, the BEKK method performs worse. One possible explanation is that as the portfolio size increases, the BEKK model becomes too complex to estimate model parameters.

5.2 Empirical study

In this section, we examined the performance of one-step ahead VaR forecasting with the empirical data. The data comprise 18 years CRSP daily percentage log returns of S&P 500 constituents from January 1, 2000, to December 31, 2017 (4,523 days). The log returns are calculated from the percentage return of the last sale or closing bid/ask price including dividends. We selected firms that have been ever a constituent of the S&P 500 during this period and filtered out the stocks that have any missing data. This selection process led us to include 492 firms () for the empirical study.

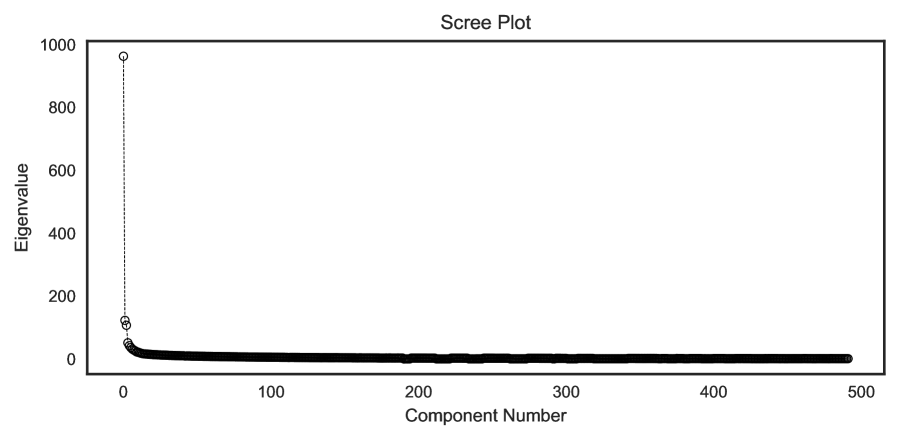

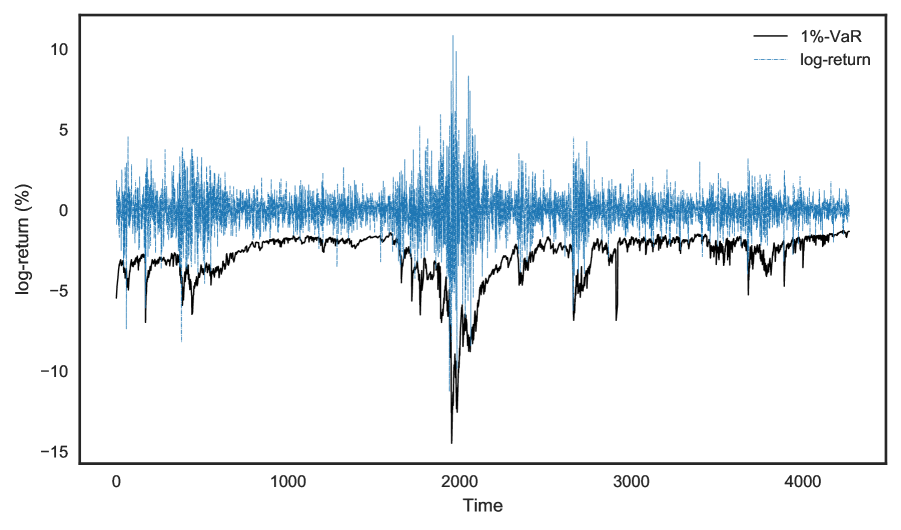

To employ the proposed P-GARCH model, we should determine the number of factors (). Figure 4 shows that the optimal is less than , and the rank estimated by (S1) in the online supplement is also 3. Thus, we determined the possible values of as 1, 2, and 3, which is in line with previous empirical studies (Chan et al., , 1998; Fama and French, , 1992, 1993). For the thresholding step, we used the global industry classification standard (GICS) sector (Fan et al., , 2016). For example, we maintained within-sector volatilities but set others to zero. The equally weighted portfolios of sizes 5 and 20 are randomly sampled from the 492 stocks with 500 repetitions, and the single-asset portfolio contains only one stock from 492 assets. With these portfolios, we predicted VaR with a significance level of , 5%, 2%, and 1% using the parametric and non-parametric methods, as discussed in Section 4.2. For the model fitting, we employed a rolling window scheme with the window size days (1 year). The parameter is updated every 10 days, whereas the VaR forecasting is done every day with the updated log return data. The total forecasting number is 4,270. The estimated parameters of P-GARCH(r=3) for the entire period are 16.32, 0.32, 0.42, 83.99, 0.00, 0.08, 6.65, 48.23, 0.90, 87.04, 5.88, 62.87, 892.7, 0.00, 0.00, 0.01, 944.7, 0.23, 0.01, 0.00, 934.99. The estimated parameter matrix is almost diagonal, which indicates that the recursive structure mainly comes from its own volatility. Similarly, the estimated parameter matrix is also almost diagonal, except for . However, when considering the magnitudes of the first and third eigenvalues, does not affect the first eigenvalue significantly. Thus, the dynamics of the three factors are mainly explained by their own past volatilities. Figure 5 depicts one sample path of the estimated one-step ahead 1%-level VaR under t-distribution with a portfolio size of 5. It shows that predicted VaR of the P-GARCH model can capture the dynamics of extreme loss.

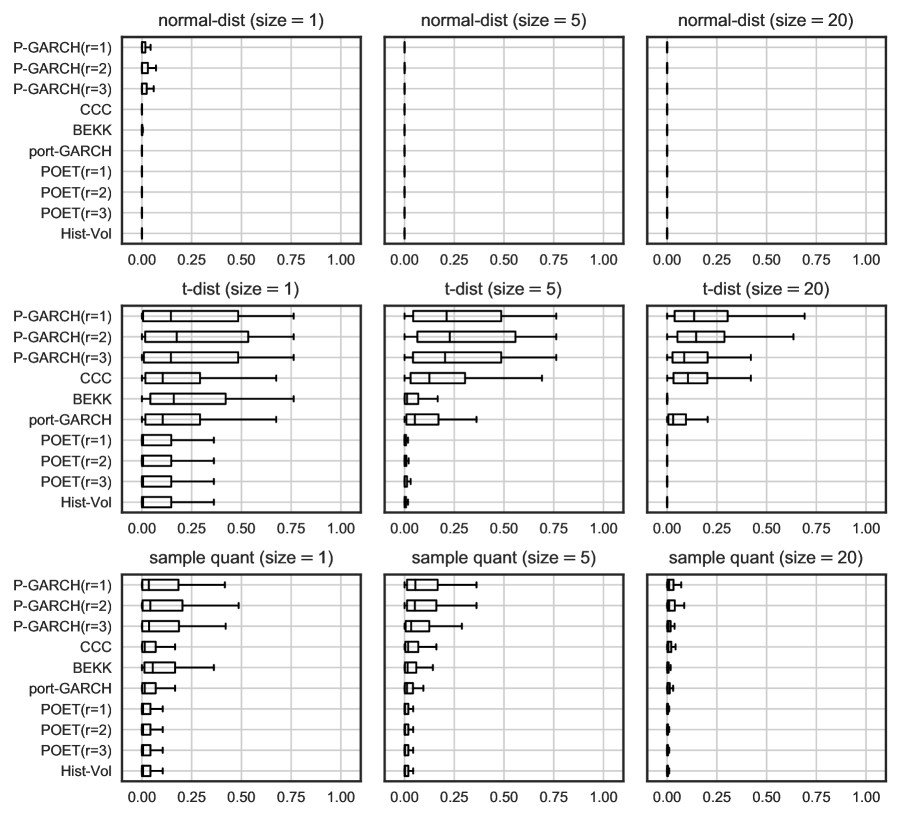

We compared the out-of-sample VaR forecast performances with the small portfolio risk analysis methods considered in Section 5.1. For example, we used the P-GARCH, CCC, BEKK, portfolio GARCH, Hist-Vol, and POET for the volatility prediction and the standard normal quantile, t-quantile with degrees of freedom 6, and sample quantile for the -quantile. To test whether the predicted VaR is correct, we used the unconditional coverage test () (Kupiec, , 1995), the conditional coverage test () (Christoffersen, , 1998), and the dynamic quantile test (DQ) (Kuester et al., , 2006). Table 2 reports the averaged hit rates () and the average -values of the , DQ, and DQ for portfolio sizes of 1, 5, 20 and with the normal distribution, student-t distribution, and sample quantile. Figure 6 presents box plots of individual portfolio’s LRcc -values for portfolio sizes of 1, 5, and 20 and with the normal distribution, t-distribution, and sample quantile. From Table 2 and Figure 6, we find that when comparing the dynamic models and static models, the dynamic models, such as the P-GARCH, BEKK, CCC, and portfolio GARCH, show better performance than the non-parametric models. This indicates that the financial market is not static and that the GARCH-type models can account for the market dynamics. When the dynamic models are compared, the P-GARCH has the highest -values for most of the VaR tests. From this empirical result, we can conjecture that the P-GARCH accounts for the market dynamics by incorporating financial big data, and this leads to improved performance in VaR forecasting for the relatively small portfolio. Finally, when the quantile methods are compared, the t-distribution shows the best performance. Moreover, the normal distribution has the smallest -values for all the portfolio sizes. This pattern coincides with the stylized fact that the log return follows the conditional heavy-tailed distribution (Cont, , 2001).

| Models | DQ | DQ | DQ | DQ | DQ | DQ | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| normal-distribution () | normal-distribution () | normal-distribution () | |||||||||||||||

| P-GARCH(r=1) | 0.016 | 0.043 | 0.040 | 0.024 | 0.021 | 0.018 | 0.002 | 0.003 | 0.001 | 0.001 | 0.019 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| P-GARCH(r=2) | 0.015 | 0.049 | 0.047 | 0.032 | 0.029 | 0.017 | 0.004 | 0.004 | 0.001 | 0.001 | 0.019 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| P-GARCH(r=3) | 0.015 | 0.045 | 0.042 | 0.028 | 0.025 | 0.017 | 0.002 | 0.002 | 0.000 | 0.001 | 0.019 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| CCC | 0.018 | 0.002 | 0.004 | 0.003 | 0.001 | 0.018 | 0.000 | 0.000 | 0.000 | 0.000 | 0.019 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| BEKK | 0.017 | 0.006 | 0.009 | 0.007 | 0.004 | 0.020 | 0.000 | 0.000 | 0.000 | 0.000 | 0.022 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| port-GARCH | 0.018 | 0.003 | 0.004 | 0.003 | 0.001 | 0.019 | 0.000 | 0.000 | 0.000 | 0.000 | 0.021 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| POET(r=1) | 0.018 | 0.008 | 0.007 | 0.001 | 0.001 | 0.021 | 0.000 | 0.000 | 0.000 | 0.000 | 0.023 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| POET(r=2) | 0.018 | 0.008 | 0.007 | 0.001 | 0.001 | 0.020 | 0.000 | 0.000 | 0.000 | 0.000 | 0.022 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| POET(r=3) | 0.018 | 0.008 | 0.007 | 0.001 | 0.001 | 0.020 | 0.000 | 0.000 | 0.000 | 0.000 | 0.022 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| Hist-Vol | 0.018 | 0.008 | 0.007 | 0.001 | 0.001 | 0.020 | 0.000 | 0.000 | 0.000 | 0.000 | 0.022 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| t-distribution () | t-distribution () | t-distribution () | |||||||||||||||

| P-GARCH(r=1) | 0.011 | 0.367 | 0.243 | 0.110 | 0.105 | 0.012 | 0.339 | 0.279 | 0.039 | 0.044 | 0.012 | 0.208 | 0.206 | 0.005 | 0.005 | ||

| P-GARCH(r=2) | 0.011 | 0.405 | 0.262 | 0.121 | 0.117 | 0.012 | 0.377 | 0.309 | 0.060 | 0.061 | 0.012 | 0.190 | 0.202 | 0.014 | 0.012 | ||

| P-GARCH(r=3) | 0.011 | 0.390 | 0.246 | 0.120 | 0.118 | 0.012 | 0.353 | 0.272 | 0.053 | 0.053 | 0.013 | 0.150 | 0.154 | 0.012 | 0.012 | ||

| CCC | 0.013 | 0.202 | 0.195 | 0.093 | 0.060 | 0.013 | 0.212 | 0.208 | 0.012 | 0.016 | 0.013 | 0.125 | 0.153 | 0.001 | 0.001 | ||

| BEKK | 0.012 | 0.264 | 0.250 | 0.090 | 0.078 | 0.014 | 0.065 | 0.066 | 0.000 | 0.001 | 0.016 | 0.004 | 0.004 | 0.000 | 0.000 | ||

| port-GARCH | 0.013 | 0.202 | 0.195 | 0.093 | 0.061 | 0.013 | 0.114 | 0.128 | 0.012 | 0.008 | 0.014 | 0.048 | 0.072 | 0.001 | 0.001 | ||

| POET(r=1) | 0.013 | 0.201 | 0.107 | 0.027 | 0.021 | 0.015 | 0.031 | 0.023 | 0.000 | 0.000 | 0.016 | 0.003 | 0.002 | 0.000 | 0.000 | ||

| POET(r=2) | 0.013 | 0.201 | 0.107 | 0.027 | 0.021 | 0.015 | 0.036 | 0.027 | 0.000 | 0.000 | 0.016 | 0.004 | 0.003 | 0.000 | 0.000 | ||

| POET(r=3) | 0.013 | 0.201 | 0.107 | 0.027 | 0.021 | 0.015 | 0.036 | 0.028 | 0.000 | 0.000 | 0.016 | 0.004 | 0.003 | 0.000 | 0.000 | ||

| Hist-Vol | 0.013 | 0.201 | 0.107 | 0.027 | 0.021 | 0.015 | 0.032 | 0.024 | 0.000 | 0.000 | 0.016 | 0.003 | 0.002 | 0.000 | 0.000 | ||

| sample quantile () | sample quantile () | sample quantile () | |||||||||||||||

| P-GARCH(r=1) | 0.013 | 0.172 | 0.130 | 0.050 | 0.032 | 0.013 | 0.104 | 0.120 | 0.029 | 0.028 | 0.014 | 0.024 | 0.031 | 0.004 | 0.005 | ||

| P-GARCH(r=2) | 0.013 | 0.183 | 0.144 | 0.066 | 0.041 | 0.013 | 0.097 | 0.112 | 0.033 | 0.031 | 0.014 | 0.021 | 0.034 | 0.009 | 0.007 | ||

| P-GARCH(r=3) | 0.013 | 0.152 | 0.125 | 0.050 | 0.031 | 0.013 | 0.075 | 0.088 | 0.025 | 0.027 | 0.015 | 0.012 | 0.021 | 0.005 | 0.005 | ||

| CCC | 0.014 | 0.042 | 0.059 | 0.031 | 0.013 | 0.014 | 0.043 | 0.058 | 0.003 | 0.004 | 0.015 | 0.014 | 0.023 | 0.000 | 0.000 | ||

| BEKK | 0.013 | 0.107 | 0.125 | 0.047 | 0.027 | 0.014 | 0.054 | 0.063 | 0.001 | 0.001 | 0.014 | 0.017 | 0.010 | 0.000 | 0.000 | ||

| port-GARCH | 0.014 | 0.042 | 0.059 | 0.031 | 0.013 | 0.014 | 0.024 | 0.039 | 0.005 | 0.003 | 0.015 | 0.007 | 0.012 | 0.000 | 0.000 | ||

| POET(r=1) | 0.013 | 0.107 | 0.071 | 0.015 | 0.006 | 0.014 | 0.043 | 0.029 | 0.000 | 0.000 | 0.015 | 0.016 | 0.008 | 0.000 | 0.000 | ||

| POET(r=2) | 0.013 | 0.107 | 0.071 | 0.015 | 0.006 | 0.014 | 0.043 | 0.029 | 0.000 | 0.000 | 0.015 | 0.016 | 0.008 | 0.000 | 0.000 | ||

| POET(r=3) | 0.013 | 0.107 | 0.071 | 0.015 | 0.006 | 0.014 | 0.043 | 0.029 | 0.000 | 0.000 | 0.015 | 0.016 | 0.008 | 0.000 | 0.000 | ||

| Hist-Vol | 0.013 | 0.107 | 0.071 | 0.015 | 0.006 | 0.014 | 0.043 | 0.029 | 0.000 | 0.000 | 0.015 | 0.016 | 0.008 | 0.000 | 0.000 | ||

6 Conclusion

In this paper, we aim to develop a dynamic process of portfolio risk measurement with the use of financial big data. The proposed model benefits from the use of financial big data in that it leads risk managers to take into account latent risk factors that are not included in their portfolios. One may be concerned about the curse of dimensionality with regard to the use of financial big data in parameter estimation; however, the proposed approach can overcome this problem with the POET method (Fan et al., , 2013) under the dynamic factor model in a GARCH form. We showed that a large number of assets aids in increasing the accuracy of factor volatility estimation. This finding results from the fact that every asset contains common market information so that an increase in the number of assets enables one to obtain more information on latent risk factors. Thus, the proposed model achieves the blessing of dimensionality in estimating latent common factors.

We tested a finite sample performance of the proposed dynamic volatility model and the corresponding VaR model with Monte Carlo simulations and showed that the results support our theoretical findings. We further investigated the performance of our one-step ahead volatility matrices in the asset portfolio and concluded that our dynamic process with P-GARCH outperforms other competitive models for any -based methods and portfolio size. To guarantee the performance of our predictive model with financial big data, we used S&P 500 constituents with parametric and non-parametric methods. The results illustrated that the predicted VaR of our dynamic volatility model can capture the dynamics of extreme loss, which can be extreme cases from systematic factors in the market. Finally, the empirical study shows that our dynamic model with P-GARCH outperforms the other competitive dynamic models in terms of forecasting the VaR with financial big data for a relatively small portfolio.

The lesson from the 2008 financial crisis and similar systemic events in the financial market of history clearly argues that risk managers in the financial industry may have to take into account latent risks possibly accounting for systematic factors. The portfolios that they aim to analyze may consist of idiosyncratic factors with a limited number of risk factors (or assets); hence, the predicted level of risk in their target portfolios may fail to address the entire risk landscape. This problem can be also of importance for financial regulators in that underestimation of risk capitals based on a small portfolio risk measurement would potentially prevent the financial markets from being stabilized, thereby leading to negative externality to the economy, as observed in 2008 (Kaserer and Klein, , 2019)555The negative externality was realized in 2008 as a huge bailout to, e.g., AIG as described in the introduction. Most of the $374 billion total bailout was provided to financial firms, e.g., AIG, Citigroup and Bank of America, and the government rationale of this financial support was to avoid the collapse of world financial markets potentially creating the risk of another Great Depression (Harrington, , 2009). This negative externality to the economy clearly burdened tax-payers for not only the size of bailout from taxes, but also the negative spillover effect on real economy.. This study contributes to this regard by providing an innovative approach to using financial big data in improve the accuracy of portfolio risks.

In this paper, we only consider the factor dynamics, but several studies have also shown that the idiosyncratic volatilities are also affected by common market factors (Barigozzi and Hallin, , 2016; Connor et al., , 2006; Herskovic et al., , 2016; Rangel and Engle, , 2012; Shin et al., 2021b, ). Thus, it is interesting but difficult to develop idiosyncratic dynamic models. In addition, we consider the -based approach to estimate the VaR values with the parametric and non-parametric quantile structures. However, the parametric structure cannot account for some stylized features, such as the skewness of the asset returns, whereas the empirical quantile approach often has large errors in the extreme tail. Thus, it is important and interesting to develop a quantile estimation procedure that can accomodate the stylized features of the asset returns. Finally, we assume that the mean process is constant over time, but this assumption is often violated in finance practice. Unlike the volatility process, the mean process does not have a strong linear time series structure, which makes the modeling of a dynamic mean process difficult. Thus, a parametric structure of the mean process, which can account for the heterogeneity of the mean process, should be developed. We leave these interesting problems for future study.

Online supplement

Theorems and technical proofs are provided online at Wiley in the Supplementary Material of this article. Readers may refer to the supplementary material associated with this article, available at Wiley (https://onlinelibrary.wiley.com/journal/15396975).

Supplementary Material on “Next Generation Models for Portfolio Risk Management: An Approach Using Financial Big Data”

This appendix provides micelleneous materials, theorems, and technical proofs of the paper entitled “Next Generation of Portfolio Risk Management: An Approach to Using Financial Big Data”.

We first introduce some notations. For a symmetric matrix , is the largest eigenvalue of , is the largest eigenvalue, and is the smallest eigenvalue. is the matrix norm. Denote the Hadamard (or element-wise) product and the element-wise square of a vector . and are the trace and vectorization of , respectively. Denote the indicator function of the event and the standard basis vector. To simplify the notations, we define as a partial derivatives: ; ; ; , where the functions and are differentiable. is a generic constant that may differ from each equations.

Appendix S1 Choice of the rank

In this paper, we assume that the rank is known. However, in practice, the rank is unknown, so it is important to estimate the rank. Ait-Sahalia and Xiu, (2017) introduced the rank estimation procedure as follows:

| (S1) |

where , , and are tuning parameters. Under some technical conditions, we can show its consistency. We note that the overestimated is not harmful because the factor model includes the important factors and the impact of the misspecified factors is relatively small (Fan et al., , 2013). In contrast, when the rank is underestimated, the factor model losses important information.

Appendix S2 Theorems for the latent factor estimation

Assumption 1.

-

(a)

, and are bounded by some constant for all and s.t. .

-

(b)

The minimum eigen-gap satisfies a.s.

Remark 3.

Assumption 1(b) is the pervasive condition that is widely used in the low-rank matrix inferences (Ait-Sahalia and Xiu, , 2017; Fan et al., , 2013, 2018, 2019; Kim and Fan, , 2019; Stock and Watson, , 2002). The pervasive condition with the sparsity condition (2.7) helps to distinguish the latent factor from the idiosyncratic volatility. Additionally, since the common market factor affects the whole asset, its proportion to the total variation is significant. Mathematically, this implies that the corresponding eigenvalues have the order, so the pervasive condition is not restrictive.

The following theorem provides the convergence rates of the latent factor component estimators and .

Theorem S2.1.

Remark 4.

Eigenvectors have the sign problem; for example, and are not distinguishable, where is the column vector of . So we put the sign matrix in (S1) to identify the eigenmatrix.

Remark 5.

Theorem S2.1 shows that the convergence rate of is . The first term is the usual optimal convergence rate for estimating the mean conditional volatility matrix . The second term is the cost to identify the latent factor. This results match with the convergence rate derived in Fan et al., (2011, 2013, 2018). We note that unlike the usual i.i.d. assumption, to manage the heterogeneous volatility structure, we impose the dynamic structure on the covariance matrix. Theorem S2.1 shows the asymptotic properties under the heterogeneous structure.

S2.1 Proof of Theorem S2.1

Lemma S2.1.

Under the assumptions of Theorem S2.1, we have

Proof of Lemma S2.1. We have

where and . Then each element is a martingale difference. Consider . We have

where is the th element of , and the first inequality is due to the Burkholder-Davis-Gundy inequality (Chow and Teicher, , 2012). Thus, we have

We can show other elements similarly.

Proof of Theorem S2.1. First consider (S1). By the Davis-Kahan’s sine theorem (Yu et al., , 2015), we have

| (S3) |

where the last equality is due to Lemma S2.1 and the fact that

where the last inequality is due to the sparsity condition 2.7.

Consider (S2). Without of loss of generality, we assume that is the identity matrix. Algebraic manipulations show

For (I), we have

| (I) | |||

where the fourth inequality is due to the Hölder’s inequality and the last inequality is due to (S2.1). For (II), we have

| (II) | |||

where the last inequality is by the fact that . For (III), we have

| (III) | |||

where is the column of . Similarly, we can show

| (IV) | |||

Therefore, we have

Appendix S3 Theorems for the QMLE estimation procedure

Define

where and .

Assumption 2.

-

(a)

The parameter space is a compact set such that every element is positive; is bounded for all and ; the eigenvalues of and are positive and ; and is the interior point.

-

(b)

’s are non-degenerate random variables.

The below theorem illustrates the convergence rate of the QMLE estimator .

Theorem S3.1.

Remark 6.

S3.1 Proof of Theorem S3.1

Lemma S3.1.

Under the assumptions of Theorem S3.1, let to be a function of and ,

Then, for some true initial value , we have

Lemma S3.1 shows that the effect of the initial value is negligible. Thus, for the mathematical convenience, we assume that . Then we have . To obtain the consistent , it is sufficient to show that uniformly in (Lemma S3.2) and attains a unique global maximum at (Amemiya, , 1985).

Lemma S3.2 (Uniform Convergence).

Under the assumptions of Theorem S3.1, we have

Proof of Lemma S3.2. We have

For the simplicity, we omit the parameter . Consider . We have

where is the element-wise inverse of . Recall . Then by the fact that for all , we have

where , , and the last equality is due to Theorem S2.1. Similarly, we can show that (II) and (III) uniformly converges to zero. Therefore, we have

Now we consider . By Theorem 2.1 in Newey, (1991), uniform convergence is equivalent to the pointwise convergence and stochastic equicontinuity, where the stochastic equicontinuity is satisfied by the Lipschitz condition . Thus, it is enough to show

-

1.

pointwise in ;

-

2.

for all .

Since is a martingale difference, we can show

Now, we show the Lipschitz condition. We have

where the first inequality is due to for all , and the second inequality is due to Hölder’s inequality.

Lemma S3.3 (Uniqueness of ).

Proof of Lemma S3.3. Since has a unique minimizer at , is a unique maximizer of for all . If is not a unique parameter to have , then there exists such that . Then , and

where 0 is a zero matrix. By Assumption 2(b), is invertible a.s., which implies

Therefore, a.s. which is a contradiction.

With the uniqueness solution result, by Lemma S3.2 and Theorem 4.1.2 in Amemiya, (1985), we can show (S2).

Lemma S3.4.

Under the assumptions of Theorem S3.1, for all fixed , and ,

Proof of Lemma S3.4. Notice that

where . For the case of , is trivial. With the case ,

where is the standard basis vector. Thus, . For the case of , we have

where the second inequality is due to for . By choosing , we have

where first inequality is due to the Minkowski’s inequality, and the last inequality follows from and . Similarly, we can show the higher order derivatives bounds.

Lemma S3.5.

Under the assumptions of Theorem S3.1, let . Then we have

Proof of Lemma S3.5. Denote and . Since , we have

-

1.

;

-

2.

;

-

3.

;

-

4.

,

where the last equation is by the fact that

where the last equality is due to Lemma S3.4. Thus, we have

and

| (S3) |

Moreover, we have

and

| (S4) |

where the last equality is due to Lemma S3.4. By combining (S3.1) and (S3.1), we complete the proof.

Lemma S3.6.

Proof of Lemma S3.6. We have

By the mean value theorem and (S2), we have and , respectively. Thus, it is enough to show . Denote . Then, for all , we have

By and Lemma S3.4, we can show . Thus, . Similar to the proof of Lemma S3.5, we can show

| (II) | |||

Moreover, since and ’s are non-degenerate, we can show

Appendix S4 Proof of Theorem 4.1

Assumption 3.

-

(a)

The sample covariance estimator satisfies the concentration inequality, for any given ,

where is a constant only depending on .

-

(b)

There is a constant such that

-

(c)

The smallest eigenvalue of stays away from , and for all , .

-

(d)

.

Remark 7.

Assumption 3(a) is the sub-Gaussian condition. When investigating the high-dimensional inferences, the sub-Gaussian condition is essential. Recently, several robust variance estimation methods have been developed, which can satisfy the sub-Gaussian condition Assumption 3(a) under the finite forth moment condition (Catoni, , 2012; Fan and Kim, , 2018; Minsker, , 2018; Shin et al., 2021a, ). Thus, the sub-Gaussian condition Assumption 3(a) is not restrictive. On the other hand, we can investigate the asymptotic behaviors under sub-Weilbull conditions (Kuchibhotla and Chakrabortty, , 2018; Vladimirova et al., , 2020).

Remark 8.

Assumption 3(b) is called the incoherence condition, which is widely assumed in analyzing the low-rank matrix (Candès and Recht, , 2009; Fan et al., , 2017). The basic intuition is that the factor loading matrix is not to be sparse. That is, the factor affects almost all the stock returns. Thus, under the factor model, the incoherence condition is acceptable.

Lemma S4.1.

Under the assumptions of Theorem 4.1, we have

| (S1) |

Proof of Lemma S4.1. Without loss of generality, we assume that is the identity matrix. Similar to the proofs of Theorem 4.2 in Kim et al., (2018), we have

First consider (I). By the Sherman-Morrison-Woodbury formula (Higham, , 2002), we have

and by denoting ,

Then, since and , we have

| (I) | |||

where the last equality is by the fact that

For (II) and (III), similarly, by Theorem S2.1, we can show

| (II) | |||

and

| (III) | |||

Lemma S4.2.

Under the assumptions of Theorem 4.1, suppose that , and the thresholding level satisfies the condition such that . Then we have

Proof of Lemma S4.2. Let . Similar to the proofs of Section 3 in Fan and Kim, (2018), under the event , we have

where the last equality is due to the sparse condition.

Proof of Theorem 4.1. By Assumption (a)(a), we have

| (S2) |

We denote and the column vectors of and , respectively. Then by Theorem 2.1 in Fan et al., (2017),

where the last equality is due to . Thus, we have

| (S3) |

By combining (S2) and (S4), we have

| (S4) |

which leads to and . Combining Lemmas S4.1 and S4.2, and (S4), we have

where the last equality is by the fact

Appendix S5 Proof of Theorem 4.2

Assumption 4.

-

(a)

The estimated standardized return satisfies the concentration inequality, for any given ,

where and is a constant only depending on .

-

(b)

The cumulative density function of and its inverse function are continuous.

-

(c)

The variance of the portfolio return is bounded and strictly positive.

Remark 9.

Proof of Theorem 4.2. Consider the parametric VaR estimator case. By the definition of VaR in (2.3), we have

Then, since and , we have

| (S1) |

Consider . We have

| (S2) |

where the last is due to Theorem 4.1 and . Combining (S1) and (S5), we have

Consider the non-parametric -based VaR estimator case. Define

where is an -quantile value, and as a cumulative distribution function of . Then the expected value of the absolute difference between and is

Let . Then, since Assumption (a)(a) implies , we have, for large enough ,

where the last equality is due to Assumption (b)(b). Similarly, the bound for can be found. Then . By the Dvoretzky–Kiefer-Wolfowitz inequality (Dvoretzky et al., , 1956), we have . Thus,

Define

Then the -th smallest value of is bounded as follows:

and

Thus, we have

| (S3) |

We also have

| (S4) |

where the inequality is due to the gross exposure condition and , and the last equality is due to , where is the row vector of . Combining results from (S1) to (S5), we have

References

- Acerbi and Tasche, (2002) Acerbi, C. and Tasche, D. (2002). Expected shortfall: a natural coherent alternative to value at risk. Economic notes, 31(2):379–388.

- Ahmadi-Javid, (2012) Ahmadi-Javid, A. (2012). Entropic value-at-risk: A new coherent risk measure. Journal of Optimization Theory and Applications, 155(3):1105–1123.

- Ait-Sahalia and Xiu, (2017) Ait-Sahalia, Y. and Xiu, D. (2017). Using principal component analysis to estimate a high dimensional factor model with high-frequency data. Journal of Econometrics, 201(2):384–399.

- Amemiya, (1985) Amemiya, T. (1985). Advanced econometrics. Harvard university press.

- Bai, (2003) Bai, J. (2003). Inferential theory for factor models of large dimensions. Econometrica, 71(1):135–171.

- Bai and Li, (2012) Bai, J. and Li, K. (2012). Statistical analysis of factor models of high dimension. The Annals of Statistics, 40(1):436–465.

- Bai and Ng, (2013) Bai, J. and Ng, S. (2013). Principal components estimation and identification of static factors. Journal of Econometrics, 176(1):18–29.

- Barigozzi and Hallin, (2016) Barigozzi, M. and Hallin, M. (2016). Generalized dynamic factor models and volatilities: recovering the market volatility shocks. The Econometrics Journal, 19(1).

- Bauwens et al., (2006) Bauwens, L., Laurent, S., and Rombouts, J. V. (2006). Multivariate garch models: a survey. Journal of Applied Econometrics, 21(1):79–109.

- Bensaid et al., (1992) Bensaid, B., Lesne, J.-P., Pages, H., and Scheinkman, J. (1992). Derivative asset pricing with transaction costs 1. Mathematical Finance, 2(2):63–86.

- Bickel and Levina, (2008) Bickel, P. J. and Levina, E. (2008). Covariance regularization by thresholding. The Annals of Statistics, 36(6):2577–2604.

- Billio and Pelizzon, (2000) Billio, M. and Pelizzon, L. (2000). Value-at-risk: a multivariate switching regime approach. Journal of Empirical Finance, 7(5):531–554.

- Boivin and Ng, (2006) Boivin, J. and Ng, S. (2006). Are more data always better for factor analysis? Journal of Econometrics, 132(1):169–194.

- Bollerslev, (1986) Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3):307–327.

- Bollerslev, (1990) Bollerslev, T. (1990). Modelling the coherence in short-run nominal exchange rates: a multivariate generalized arch model. Review of Economics and Statistics, 72(3):498–505.

- Broda and Paolella, (2009) Broda, S. A. and Paolella, M. S. (2009). Chicago: A fast and accurate method for portfolio risk calculation. Journal of Financial Econometrics, 7(4):412–436.

- Brooks and Persand, (2003) Brooks, C. and Persand, G. (2003). Volatility forecasting for risk management. Journal of Forecasting, 22(1):1–22.

- Cai and Liu, (2011) Cai, T. and Liu, W. (2011). Adaptive thresholding for sparse covariance matrix estimation. Journal of the American Statistical Association, 106(494):672–684.

- Cajueiro and Tabak, (2004) Cajueiro, D. O. and Tabak, B. M. (2004). The hurst exponent over time: testing the assertion that emerging markets are becoming more efficient. Physica A: Statistical Mechanics and its Applications, 336(3-4):521–537.

- Candès and Recht, (2009) Candès, E. J. and Recht, B. (2009). Exact matrix completion via convex optimization. Foundations of Computational Mathematics, 9(6):717.

- Carhart, (1997) Carhart, M. M. (1997). On persistence in mutual fund performance. The Journal of Finance, 52(1):57–82.

- Catoni, (2012) Catoni, O. (2012). Challenging the empirical mean and empirical variance: a deviation study. Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, 48(4):1148–1185.

- Chan et al., (1998) Chan, L. K., Karceski, J., and Lakonishok, J. (1998). The risk and return from factors. Journal of Financial and Quantitative Analysis, 33(2):159–188.

- Chen and Tang, (2005) Chen, S. X. and Tang, C. Y. (2005). Nonparametric inference of value-at-risk for dependent financial returns. Journal of Financial Econometrics, 3(2):227–255.

- Chow and Teicher, (2012) Chow, Y. S. and Teicher, H. (2012). Probability theory: independence, interchangeability, martingales. Springer Science & Business Media.

- Christoffersen, (1998) Christoffersen, P. F. (1998). Evaluating interval forecasts. International Economic Review, pages 841–862.

- Comte and Lieberman, (2003) Comte, F. and Lieberman, O. (2003). Asymptotic theory for multivariate garch processes. Journal of Multivariate Analysis, 84(1):61–84.

- Connor et al., (2006) Connor, G., Korajczyk, R. A., and Linton, O. (2006). The common and specific components of dynamic volatility. Journal of Econometrics, 132(1):231–255.

- Cont, (2001) Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative finance, 1(2):223.

- Donoho, (2000) Donoho, D. L. (2000). High-dimensional data analysis: The curses and blessings of dimensionality. AMS math challenges lecture, 1(2000):32.

- Dvoretzky et al., (1956) Dvoretzky, A., Kiefer, J., and Wolfowitz, J. (1956). Asymptotic minimax character of the sample distribution function and of the classical multinomial estimator. The Annals of Mathematical Statistics, pages 642–669.

- Engle, (2002) Engle, R. (2002). Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics, 20(3):339–350.

- Engle, (2016) Engle, R. F. (2016). Dynamic conditional beta. Journal of Financial Econometrics, 14(4):643–667.

- Engle and Kroner, (1995) Engle, R. F. and Kroner, K. F. (1995). Multivariate simultaneous generalized arch. Econometric Theory, 11(1):122–150.

- Engle et al., (2017) Engle, R. F., Ledoit, O., and Wolf, M. (2017). Large dynamic covariance matrices. Journal of Business & Economic Statistics, pages 1–13.

- Engle and Manganelli, (2004) Engle, R. F. and Manganelli, S. (2004). Caviar: Conditional autoregressive value at risk by regression quantiles. Journal of Business & Economic Statistics, 22(4):367–381.

- Fama, (1998) Fama, E. F. (1998). Market efficiency, long-term returns, and behavioral finance. Journal of Financial Economics, 49(3):283–306.

- Fama and French, (1992) Fama, E. F. and French, K. R. (1992). The cross-section of expected stock returns. The Journal of Finance, 47(2):427–465.

- Fama and French, (1993) Fama, E. F. and French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1):3–56.

- Fama and French, (2015) Fama, E. F. and French, K. R. (2015). A five-factor asset pricing model. Journal of Financial Economics, 116(1):1–22.

- Fan et al., (2016) Fan, J., Furger, A., and Xiu, D. (2016). Incorporating global industrial classification standard into portfolio allocation: A simple factor-based large covariance matrix estimator with high-frequency data. Journal of Business & Economic Statistics, 34(4):489–503.

- Fan and Gu, (2003) Fan, J. and Gu, J. (2003). Semiparametric estimation of value at risk. The Econometrics Journal, 6(2):39–69.

- Fan and Kim, (2018) Fan, J. and Kim, D. (2018). Robust high-dimensional volatility matrix estimation for high-frequency factor model. Journal of the American Statistical Association, 113(523):1268–1283.

- Fan and Kim, (2019) Fan, J. and Kim, D. (2019). Structured volatility matrix estimation for non-synchronized high-frequency financial data. Journal of Econometrics, 209(1):61–78.

- Fan et al., (2011) Fan, J., Liao, Y., and Mincheva, M. (2011). High dimensional covariance matrix estimation in approximate factor models. Annals of Statistics, 39(6):3320.

- Fan et al., (2013) Fan, J., Liao, Y., and Mincheva, M. (2013). Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 75(4):603–680.

- Fan et al., (2018) Fan, J., Liu, H., and Wang, W. (2018). Large covariance estimation through elliptical factor models. Annals of statistics, 46(4):1383.

- Fan et al., (2017) Fan, J., Wang, W., and Zhong, Y. (2017). An ℓ∞ eigenvector perturbation bound and its application to robust covariance estimation. The Journal of Machine Learning Research, 18(1):7608–7649.

- Fan et al., (2019) Fan, J., Wang, W., and Zhong, Y. (2019). Robust covariance estimation for approximate factor models. Journal of Econometrics, 208(1):5–22.

- Fantazzini, (2008) Fantazzini, D. (2008). Dynamic copula modelling for value at risk. Frontiers in Finance and Economics, 5(2):72–108.

- Giot and Laurent, (2004) Giot, P. and Laurent, S. (2004). Modelling daily value-at-risk using realized volatility and arch type models. Journal of Empirical Finance, 11(3):379–398.

- Glasserman et al., (2002) Glasserman, P., Heidelberger, P., and Shahabuddin, P. (2002). Portfolio value-at-risk with heavy-tailed risk factors. Mathematical Finance, 12(3):239–269.

- Harrington, (2009) Harrington, S. E. (2009). The financial crisis, systemic risk, and the future of insurance regulation. Journal of Risk and Insurance, 76(4):785–819.

- Hendricks, (1996) Hendricks, D. (1996). Evaluation of value-at-risk models using historical data. Economic Policy Review, 2(1):531–554.

- Herskovic et al., (2016) Herskovic, B., Kelly, B., Lustig, H., and Van Nieuwerburgh, S. (2016). The common factor in idiosyncratic volatility: Quantitative asset pricing implications. Journal of Financial Economics, 119(2):249–283.

- Higham, (2002) Higham, N. J. (2002). Accuracy and stability of numerical algorithms. SIAM.

- Huisman et al., (1998) Huisman, R., Koedijk, K. G., and Pownall, R. A. (1998). Var-x: Fat tails in financial risk management. Journal of Risk, 1(1):47–61.

- Hull and White, (1998) Hull, J. and White, A. (1998). Incorporating volatility updating into the historical simulation method for value-at-risk. Journal of Risk, 1(1):5–19.

- Jorion, (2000) Jorion, P. (2000). Value at risk: The New Benchmark for Managing Financial Risk. McGraw-Hill Professional Publishing.

- Kaserer and Klein, (2019) Kaserer, C. and Klein, C. (2019). Systemic risk in financial markets: how systemically important are insurers? Journal of Risk and Insurance, 86(3):729–759.

- Kawakatsu, (2006) Kawakatsu, H. (2006). Matrix exponential garch. Journal of Econometrics, 134(1):95–128.

- Kim and Fan, (2019) Kim, D. and Fan, J. (2019). Factor garch-itô models for high-frequency data with application to large volatility matrix prediction. Journal of Econometrics, 208(2):395–417.

- Kim et al., (2018) Kim, D., Liu, Y., and Wang, Y. (2018). Large volatility matrix estimation with factor-based diffusion model for high-frequency financial data. Bernoulli, 24(4B):3657–3682.

- Kuchibhotla and Chakrabortty, (2018) Kuchibhotla, A. K. and Chakrabortty, A. (2018). Moving beyond sub-gaussianity in high-dimensional statistics: Applications in covariance estimation and linear regression. arXiv preprint arXiv:1804.02605.

- Kuester et al., (2006) Kuester, K., Mittnik, S., and Paolella, M. S. (2006). Value-at-risk prediction: A comparison of alternative strategies. Journal of Financial Econometrics, 4(1):53–89.

- Kupiec, (1995) Kupiec, P. (1995). Techniques for verifying the accuracy of risk measurement models. The Journal of Derivatives, 3(2).

- Li et al., (2018) Li, Q., Cheng, G., Fan, J., and Wang, Y. (2018). Embracing the blessing of dimensionality in factor models. Journal of the American Statistical Association, 113(521):380–389.

- Malkiel, (2003) Malkiel, B. G. (2003). The efficient market hypothesis and its critics. Journal of Economic Perspectives, 17(1):59–82.

- Mandelbrot, (1963) Mandelbrot, B. (1963). The variation of certain speculative prices. The Journal of Business, 36(4):394–419.

- McNeil and Frey, (2000) McNeil, A. J. and Frey, R. (2000). Estimation of tail-related risk measures for heteroscedastic financial time series: an extreme value approach. Journal of Empirical Finance, 7(3-4):271–300.

- Minsker, (2018) Minsker, S. (2018). Sub-gaussian estimators of the mean of a random matrix with heavy-tailed entries. The Annals of Statistics, 46(6A):2871–2903.

- Narayan and Smyth, (2004) Narayan, P. K. and Smyth, R. (2004). Is south korea’s stock market efficient? Applied Economics Letters, 11(11):707–710.

- Natarajan et al., (2008) Natarajan, K., Pachamanova, D., and Sim, M. (2008). Incorporating asymmetric distributional information in robust value-at-risk optimization. Management Science, 54(3):573–585.

- Newey, (1991) Newey, W. K. (1991). Uniform convergence in probability and stochastic equicontinuity. Econometrica: Journal of the Econometric Society, pages 1161–1167.

- Pakel et al., (2020) Pakel, C., Shephard, N., Sheppard, K., and Engle, R. F. (2020). Fitting vast dimensional time-varying covariance models. Journal of Business & Economic Statistics, pages 1–17.

- Paolella and Polak, (2015) Paolella, M. S. and Polak, P. (2015). Comfort: A common market factor non-gaussian returns model. Journal of Econometrics, 187(2):593–605.

- Paolella et al., (2021) Paolella, M. S., Polak, P., and Walker, P. S. (2021). A non-elliptical orthogonal garch model for portfolio selection under transaction costs. Journal of Banking & Finance, 125:106046.

- Patton et al., (2019) Patton, A. J., Ziegel, J. F., and Chen, R. (2019). Dynamic semiparametric models for expected shortfall (and value-at-risk). Journal of econometrics, 211(2):388–413.

- Pedersen and Rahbek, (2014) Pedersen, R. S. and Rahbek, A. (2014). Multivariate variance targeting in the bekk–garch model. The Econometrics Journal, 17(1):24–55.

- Rangel and Engle, (2012) Rangel, J. G. and Engle, R. F. (2012). The factor–spline–garch model for high and low frequency correlations. Journal of Business & Economic Statistics, 30(1):109–124.

- (81) Shin, M., Kim, D., and Fan, J. (2021a). Adaptive robust large volatility matrix estimation based on high-frequency financial data. Available at SSRN 3793394.

- (82) Shin, M., Kim, D., Wang, Y., and Fan, J. (2021b). Factor and idiosyncratic var-ito volatility models for heavy-tailed high-frequency financial data. Available at SSRN 3921526.

- Stock and Watson, (2002) Stock, J. H. and Watson, M. W. (2002). Forecasting using principal components from a large number of predictors. Journal of the American Statistical Association, 97(460):1167–1179.

- Van der Weide, (2002) Van der Weide, R. (2002). Go-garch: a multivariate generalized orthogonal garch model. Journal of Applied Econometrics, 17(5):549–564.

- Vladimirova et al., (2020) Vladimirova, M., Girard, S., Nguyen, H., and Arbel, J. (2020). Sub-weibull distributions: Generalizing sub-gaussian and sub-exponential properties to heavier tailed distributions. Stat, 9(1):e318.

- Wu and Shieh, (2007) Wu, P.-T. and Shieh, S.-J. (2007). Value-at-risk analysis for long-term interest rate futures: Fat-tail and long memory in return innovations. Journal of Empirical Finance, 14(2):248–259.

- Yu et al., (2015) Yu, Y., Wang, T., and Samworth, R. J. (2015). A useful variant of the davis–kahan theorem for statisticians. Biometrika, 102(2):315–323.

- Zoia et al., (2018) Zoia, M. G., Biffi, P., and Nicolussi, F. (2018). Value at risk and expected shortfall based on gram-charlier-like expansions. Journal of Banking & Finance, 93:92–104.