Optimal Dynamic Futures Portfolios Under

a Multiscale Central Tendency Ornstein-Uhlenbeck Model

Abstract

We study the problem of dynamically trading multiple futures whose underlying asset price follows a multiscale central tendency Ornstein-Uhlenbeck (MCTOU) model. Under this model, we derive the closed-form no-arbitrage prices for the futures contracts. Applying a utility maximization approach, we solve for the optimal trading strategies under different portfolio configurations by examining the associated system of Hamilton-Jacobi-Bellman (HJB) equations. The optimal strategies depend on not only the parameters of the underlying asset price process, but also the risk premia embedded in the futures prices. Numerical examples are provided to illustrate the investor’s optimal positions and optimal wealth over time.

I Introduction

Futures are standardized exchange-traded bilateral contracts of agreement to buy or sell an asset at a pre-determined price at a pre-specified time in the future. The underlying asset can be a physical commodity, like gold and silver, or oil and gas, but it can also be a market index like the S&P 500 index or the CBOE volatility index.

Futures are an integral part of the derivatives market. The Chicago Mercantile Exchange (CME), which is the world’s largest futures exchange, averages over 15 million futures contracts traded per day.333Source: CME Group daily exchange volume and open interest report, available at https://www.cmegroup.com/market-data/volume-open-interest/exchange-volume.html Within the universe of hedge funds and alternative investments, futures funds constitute a major part with hundreds of billions under management. This motivates us to investigate the problem of trading futures portfolio dynamically over time.

In this paper, we introduce a multiscale central tendency Ornstein-Uhlenbeck (MCTOU) model to describe the price dynamics of the underlying asset. This is a three-factor model that is driven by a fast mean-reverting OU process and a slow mean-reverting OU process. Similar multiscale framework has been widely used for modeling stochastic volatility of stock prices [1]. The flexibility of multifactor models permits good fit to empirical term structure as displayed in the market. Especially in deep and liquid futures markets, such as crude oil or gold, with over ten contracts of various maturities actively traded at any given time, multifactor models are particular useful. In the literature, we refer to [2] for a multifactor Gaussian model for pricing oil futures, and [3] for a multifactor stochastic volatility model for commodity prices to enhance calibration against observed option prices.

Under the MCTOU model, we first derive the no-arbitrage price formulae for the futures contracts. In turn, we solve a utility maximization problem to derive the optimal trading strategies over a finite trading horizon. This stochastic control approach leads to the analysis of the associated Hamilton-Jacobi-Bellman (HJB) partial differential equation satisfied by the investor’s value function. We derive both the investor’s value function and optimal strategy explicitly.

Our solution also yields the formula for the investor’s certainty equivalent, which quantifies the value of the futures trading opportunity to the investor. Surprisingly the value function, optimal strategy and certainty equivalent depend not on the current spot and futures prices, but on the associated risk premia. In addition, we provide the numerical examples to illustrate the investor’s optimal futures positions and optimal wealth over time.

In the literature, stochastic control approach has been widely applied to continuous-time dynamic optimization of stock portfolios dating back to [4], but much less has been done for portfolios of futures and other derivatives. For futures portfolios, one must account for the risk-neutral pricing before solving for the optimal trading strategies. To that end, our model falls within the multi-factor Gassian model for futures pricing, as used for oil futures in [2]. The utility maximization approach is used to derive dynamic futures trading strategies under two-factor models in [5] and [6]. A general regime-switching framework for dynamic futures trading can be found in [7]. As an alternative approach for capturing futures and spot price dynamics, the stochastic basis model [8, 9] directly models the difference between the futures and underlying asset prices, and solve for the optimal trading strategies through utility maximization.

In comparison to these studies, we have extended the investigation of optimal trading in commodity futures market under two-factor models to a three-factor model. Closed-form expressions for the optimal controls and for the value function are obtained. Using these formulae, we illustrate the optimal strategies. Intuitively, it should be more beneficial to be able to access a larger set of securities, and this intuition is confirmed quantitatively. Therefore, we consider all available contracts of different maturities in that market. From our numerical example, the highest certainty equivalent is achieved from trading every contract that is available.

II The Multiscale Central Tendency Ornstein-Uhlenbeck Model

We now present the multiscale central tendency Ornstein-Uhlenbeck (MCTOU) model that describes the price dynamics of the underlying asset. This leads to the no-arbitrage pricing of the associated futures contracts. Hence, the dynamcis under both the physical measure and risk-neutral pricing measure are discussed.

II-A Model Formulation

We fix a probability space . The log-price of the underlying asset is denoted by . Its evolution under the physical measure is given by the system of stochastic differential equations:

| (1) | ||||

| (2) | ||||

| (3) |

where , and are independent Brownian motions under the physical measure .

Under this model, the mean process of log-price is the sum of two stochastic factors, and , modeled by two different OU processes. The first factor is fast mean-reverting. The rate of mean reversion is represented by , with being a small parameter corresponding to the time scale of this process. is an ergodic process and its invariant distribution is independent of . This distribution is Gaussian with mean and variance . In contrast, the second factor is a slowly mean-reverting OU process. The rate of mean reversion is represented by a small parameter .

The three processes , , and can be correlated. The correlation coefficients , , and are constants, which satisfy and .

We specify the market prices of risk as , for , which satisfy

| (4) |

where , and are independent Brownian motions under risk-neutral pricing measure . We introduce the combined market prices of risk , for , defined by

| (5) | ||||

| (6) | ||||

| (7) |

Then, we write the evolution under the risk-neutral measure as:

| (8) |

| (9) | ||||

| (10) |

For convenience, we define

| (11) | ||||

| (12) | ||||

| (13) | ||||

| (14) | ||||

| (15) | ||||

| (19) | ||||

| (23) |

and

| (24) |

Then, the evolution for under measures and can be written concisely as

| (25) |

and

| (26) |

III Futures Pricing and Futures Trading

III-A Futures Pricing

Let us consider three futures contracts , and , written on the same underlying asset with three arbitrarily chosen maturities , and respectively. Recall that the asset price is given by

Then, the futures price at time is given by

| (27) |

for . Define the linear differential operator

| (28) |

where is the nabla operator and Hessian operator satisfies

| (29) |

Then, for , the futures price function solves the following PDE

| (30) |

for , with the terminal condition for , where .

Proposition 2

The futures price is given by

| (31) |

where and satisfy

| (32) | ||||

| (33) |

III-B Dynamic Futures Portfolio

Now consider a collection of contracts of different maturities available to trade, where 2, 3. We note that there are only three sources of randomness, so trading three contracts is sufficient. Any additional contract would be redundant in this model. By Proposition 2, we have

| (40) | ||||

| (41) |

where we have defined

| (42) |

Define

| (43) |

Then, in matrix form, the system of futures dynamics is given by the set of SDE:

| (44) |

where

| (45) | ||||

| (46) |

Here, we assume there be no redundant futures contract, which means any futures contract could not be replicated by other futures contracts, indicating that .

Next, we consider the trading problem for the investor. Let strategy , where the element denotes the amount of money invested in -th futures contract. In addition, we assume the interest rate be zero for simplicity. Then, for any admissible strategy , the wealth process is

| (47) |

We note that the wealth process is only determined by the strategy and it is not affected by factors variable and futures prices .

The investor’s risk preference is described by the exponential utility:

| (48) |

where denotes the coefficient of risk aversion. A strategy is said to be admissible if is real-valued progressively measurable and satisfies the Novikov condition [14]:

| (49) |

The investor fixes a finite optimization horizon , which means that has to be less than or equal to the maturity of the earliest expiring contract, and seeks an admissible strategy that maximizes the expected utility of wealth at :

| (50) |

where denotes the set of admissible controls at the initial time . Since the wealth SDE (47) does not depend on the factors variable and futures prices , the value function does not depend on them either.

To facilitate presentation, we define

| (51) |

Then, following the standard verification approach to dynamic programming [15], the candidate value function and optimal trading strategy is found from the Hamilton-Jacobi-Bellman (HJB) equation

| (52) |

for , along with the terminal condition , for

Theorem 3

The unique solution to the HJB equation (52) is given by

| (53) |

where

| (54) |

The optimal futures trading strategy is explicitly given by

| (55) |

Proof:

We will first use the ansatz

| (56) |

Then, using the relations

| (57) |

and

| (58) |

the PDE (52) becomes

| (59) |

with terminal condition . From the first-order condition, which is obtained from differentiating the terms inside the supremum with respect to and setting the equation to zero, we have

| (60) |

Recall that . Then, is an invertible matrix. Accordingly, we have the optimal strategy (55). Given the fact that is the semi-positive definite matrix for any matrix , the time-dependent component is always non-negative.

Example 4

In order to quantify the value of trading futures to the investor, we define the investor’s certainty equivalent associated with the utility maximization problem. The certainty equivalent is the guaranteed cash amount that would yield the same utility as that from dynamically trading futures according to (50). This amounts to applying the inverse of the utility function to the value function in (53). Precisely, we define

| (65) | ||||

| (66) |

Therefore, the certainty equivalent is the sum of the investor’s wealth and a non-negative time-dependent component . The certainty equivalent is also inversely proportional to the risk aversion parameter , which means that a more risk averse investor has a lower certainty equivalent, valuing the futures trading opportunity less. From (32), (42), (45) and (54), we see that the certainty equivalent depends on the constant matrix , volatility matrix , correlation matrix and market prices of risk . Nevertheless, the certainty equivalent does not depend on the current values of factors .

| 1 | 0.5 | 0.5 | 0.5 | 0.5 |

| 0.05 | 0.01 | 0.8 | 0.02 | 0.3 |

| 0 | 0 | 0 | 0.02 | 0.02 | 0.02 |

|---|---|---|---|---|---|

| 5 |

IV Numerical Illustration

In this section, we simulate the MCTOU process and illustrate the outputs from our trading model. With the closed-form expressions obtained in the Section III, we now generate the futures prices, optimal strategies and wealth processes numerically, using the parameters in Table I. Primarily, we let and be small parameters and we consider trading three futures with maturities year, year and year. Then, our trading horizon will be year, no greater than the futures maturities. We assume 252 trading days in a year and 21 trading days in a month (or 1/12 year). In our figures, we show the corresponding trading days on the axis.

| Parameters | Futures Combinations (Maturity) | |||||||

| 0.563 | 1.58 | 3.25 | 5.36 | 4.65 | 4.41 | 419 | ||

| 0.502 | 1.09 | 1.74 | 3.09 | 2.62 | 2.41 | 417 | ||

| 0.456 | 0.837 | 1.19 | 2.88 | 2.35 | 2.01 | 417 | ||

| 0.561 | 1.56 | 3.23 | 5.34 | 4.64 | 4.40 | 543 | ||

| 0.500 | 1.08 | 1.73 | 3.08 | 2.62 | 2.40 | 542 | ||

| 0.454 | 0.833 | 1.18 | 2.87 | 2.34 | 2.01 | 541 | ||

| 0.565 | 1.59 | 3.27 | 5.39 | 4.66 | 4.42 | 571 | ||

| 0.504 | 1.10 | 1.75 | 3.11 | 2.63 | 2.41 | 569 | ||

| 0.457 | 0.842 | 1.20 | 2.90 | 2.36 | 2.02 | 569 | ||

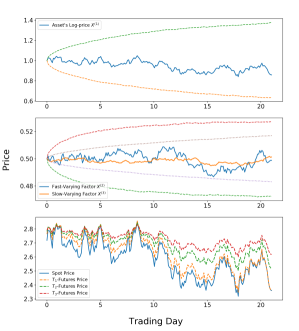

In Figure 1, we plot the simulation paths and confidence intervals for three factors in the top figure and middle figure. As shown in the middle panel, the confidence interval of the slow-varying factor is much narrower than the one for fast-varying factor . At the bottom, we plot the spot price and futures prices. The three paths for the futures prices are highly correlated and -futures price is equal to the asset’s spot price at its maturity date , which is the 21st trading day.

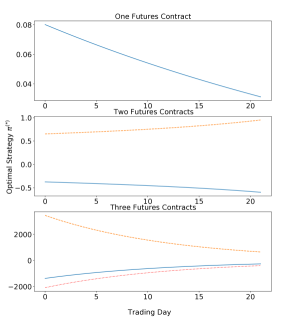

In Figure 2, we plot the optimal strategies as functions of time for different portfolios and different correlation parameters. In each sub-figure, from top to bottom, we show the optimal strategies for one-contract portfolio, two-contract portfolio and three-contract portfolio respectively. The optimal investments on -futures, dashed lines represent the optimal investment on -futures, -futures, and -futures are represented by solid, dashed, and dotted lines respectively. The optimal cash amount invested are deterministic functions for time, but the optimal units of futures held do vary continuously with the prevailing futures price.

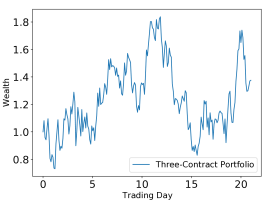

Moreover, the investor takes large long/short positions in three-contract portfolio since all sources of risk can be hedged. We provide sample path for wealth process for three-contract portfolios in the Figure 3.

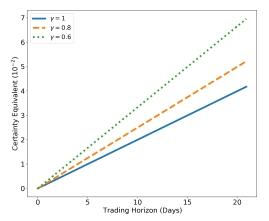

In Figure 4, we see that the certainty equivalent increases as a function of trading horizon , which means that the more time the investor has, the more valuable is the trading opportunity. As the trading horizon reduces to zero, the certainty equivalent converges to the initial wealth , which is set to be 0 in this example, as expected from (66). Also, with a lower risk aversion parameter , the investor has a higher certainty equivalent for any given trading horizon.

Table II shows the certainty equivalents for all possible futures combinations under various correlation configurations. The certainty equivalent is much higher when more contracts are traded. In addition, if there is only one futures contract to trade, the certainty equivalent is increasing with respect to its maturity, see first three columns. The certainly equivalents tend to be higher when and are negative.

V Conclusion

We have studied the optimal trading of futures under a multiscale multifactor model. Closed-form expressions for the optimal controls and value function are derived through the analysis of the associated HJB equation. Using these, we have illustrated the path behaviors of the futures prices and optimal positions. We also quantify the values of the trading different combinations of futures under different model parameters.

References

- [1] J.-P. Fouque, G. Papanicolaou, and R. Sircar, Derivatives in Financial Markets with Stochastic Volatility. Cambridge University Press, 2000.

- [2] G. Cortazar and L. Naranjo, “An N-factor Gaussian model of oil futures prices,” Journal of Futures Markets, vol. 26, no. 3, pp. 243–268, 2006.

- [3] G. Cortazar, M. Lopez, and L. Naranjo, “A multifactor stochastic volatility model of commodity prices,” Energy Economics, vol. 67, pp. 182–201, 2017.

- [4] R. Merton, “Optimum consumption and portfolio rules in a continuous time model,” Journal of Economic Theory, vol. 3, no. 4, pp. 373–413, 1971.

- [5] T. Leung and R. Yan, “Optimal dynamic pairs trading of futures under a two-factor mean-reverting model,” International Journal of Financial Engineering, vol. 5, no. 3, p. 1850027, 2018.

- [6] ——, “A stochastic control approach to managed futures portfolios,” International Journal of Financial Engineering, vol. 6, no. 1, p. 1950005, 2019.

- [7] T. Leung and Y. Zhou, “Dynamic optimal futures portfolio in a regime-switching market framework,” Internation Journal of Financial Engineering, vol. 6, no. 4, p. 1950034, 2019.

- [8] B. Angoshtari and T. Leung, “Optimal dynamic basis trading,” Annals of Finance, vol. 15, no. 3, pp. 307–335, 2019.

- [9] ——, “Optimal trading of a basket of futures contracts,” Annals of Finance, 2020, published online.

- [10] T. Leung, J. Li, X. Li, and Z. Wang, “Speculative futures trading under mean reversion,” Asia-Pacific Financial Markets, vol. 23, no. 4, pp. 281–304, 2016.

- [11] T. Leung and X. Li, Optimal Mean Reversion Trading: Mathematical Analysis and Practical Applications. World Scientific, Singapore, 2016.

- [12] T. Leung and B. Ward, “The golden target: analyzing the tracking performance of leveraged gold ETFs,” Studies in Economics and Finance, vol. 32, no. 3, pp. 278–297, 2015.

- [13] J. Mencia and E. Sentana, “Valuation of VIX derivatives,” Journal of Financial Economics, vol. 108, pp. 367–391, 2013.

- [14] A. A. Novikov, “On an identity for stochastic integrals,” Theory of Probability & Its Applications, vol. 17, no. 4, 1972.

- [15] W. H. Fleming and H. M. Soner, Controlled Markov Processes and Viscosity Solutions. Springer-Verlag, 1993.