Contrastive Pre-training for Imbalanced Corporate Credit Ratings

Abstract.

The corporate credit rating reflects the level of corporate credit and plays a crucial role in modern financial risk control. But real-world credit rating data usually shows long-tail distributions, which means a heavy class imbalanced problem challenging the corporate credit rating system greatly. To tackle that, inspired by the recent advances of pre-train techniques in self-supervised representation learning, we propose a novel framework named Contrastive Pre-training for Corporate Credit Rating (CP4CCR), which utilizes the self-supervision for getting over the class imbalance. Specifically, we propose to, in the first phase, exert contrastive self-supervised pre-training without label information, which aims to learn a better class-agnostic initialization. Furthermore, two self-supervised tasks are developed within CP4CCR: (i) Feature Masking (FM) and (ii) Feature Swapping(FS). In the second phase, we can train any standard corporate credit rating model initialized by the pre-trained network. Extensive experiments conducted on the real public-listed corporate rating dataset, prove that CP4CCR can improve the performance of standard corporate credit rating models, especially for the class with few samples.

1. Introduction

Credit rating systems have been widely employed in all kinds of financial institutions such as banks and agency securities, to help them to mitigate credit risk. However, the credit assessment process, which is expensive and complicated, often takes months with experts involved to analyze. Therefore, it is necessary to design a model to predict credit level automatically.

The banking industry has developed some credit risk models since the middle of the twentieth century. Initially, logistic regression and hidden Markov model were applied in credit rating (Gogas et al., 2014; Petropoulos et al., 2016). With the progress of science and technology, machine learning, deep learning and hybrid models have shown their power in this field (Wu and Hsu, 2012; Yeh et al., 2012; Pai et al., 2015). With the advent of graph neural networks, some graph-based models (Bruss et al., 2019; Cheng et al., 2019b, a, 2020a, 2020b), were built based on the loan guarantee network to utilize relations between corporations.

Although these models have achieved promising results, they all ignore a fatal problem, the class imbalance problem, which prevents these models from improving continuously. We find out that credit rating agencies, like Standard & Poor’s, Moody’s and CCXI, often give AA, A, BBB to most corporations, and few of them are CC, C. This will incur the class-imbalanced problem, which poses a great challenge to corporate credit rating model.

When the supervised model is limited, these models may fail due to the class-imbalanced problem, self-supervised manners will show their power. Recently, contrastive self-supervised learning brings a new chance to this problem. In the work (Yang and Xu, 2020), they systematically investigate and demonstrate, theoretically and empirically, the class-imbalanced learning can significantly benefit in contrastive self-supervised manners.

Contrastive self-supervised learning attracted the interest of many researchers due to its ability to avoid the cost of annotating large-scale datasets. Mikolov et al. (Mikolov et al., 2013) firstly proposed contrastive learning for natural language processing in 2013. And it started to prevail on several NLP tasks in recent years (Chi et al., 2020; Fang and Xie, 2020; Giorgi et al., 2020). On the one hand, contrastive self-supervised learning had shown its power by four main pretext tasks: color transformation, geometric transformation, context-based tasks, and cross-modal tasks (Jaiswal et al., 2020). On the other hand, in the field of recommendation systems, Yao et al. (Yao et al., 2020) proposed a multi-task self-supervised learning framework for large-scale recommendations. Xie et al. (Xie et al., 2020) developed CP4Rec to utilize the contrastive pre-training framework to extract meaningful sequential information. Besides, it can also alleviate generalization error, spurious correlations and adversarial attacks. That’s why this kind of technology is applied in many fields.

Due to the limitations mentioned before, the application of contrastive self-supervised learning in the corporate credit rating is less well study. Different from previous works, we aim to tackle the class-imbalanced problem and improve the model performance of the class with few samples by leverage self-supervised signals constructed from corporate profile data. In specific, we propose a novel framework named Contrastive Pre-training for Corporate Credit Rating, CP4CCR for brevity. In the pre-training phase, we propose two self-supervised tasks, (i) Feature Masking and (ii) Feature Swapping (FS), to perform self-supervised pre-training. Then in the following phase, any standard corporate credit rating model can perform based on the pre-trained data. To sum up, the main contributions of this work are summarized as follows:

-

Two novel unsupervised tasks of corporate credit rating are proposed to perform contrastive pre-training: (i) Feature Masking and (ii) Feature Swapping (FS).

-

We proposed a new framework named Contrastive Pre-training for Corporate Credit Rating (CP4CCR) to tackle the class-imbalanced problem.

-

Comprehensive experiments on the real public-listed corporate rating dataset demonstrate that our model can improve the performance of common credit rating models experimentally.

2. The Proposed Method: CP4CCR

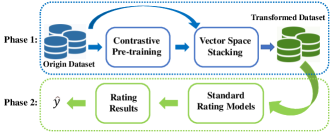

In this section, we introduce the proposed framework: CP4CCR. It includes two phases. The architecture is illustrated in Figure 1.

In the first phase, the original dataset without label information is performed contrastive self-supervised pre-training to learn better initialization. Then to make full use of the original and pre-trained dataset, vector space stacking is proposed. We get the better-transformed dataset at the end of phase 1. Afterward, any standard corporate credit rating model can be applied based on the transformed dataset to predict the credit level in phase 2.

2.1. Notations and Problem Statement

In this paper, we represent column vectors and matrices by italic lower case letters (e.g., ) and bold upper case letters (e.g., ), respectively. And we use calligraphic letters to represent sets (e.g., ).

Let denotes the set of corporations, is the number of corporations. includes the profile of corporation, which has dimensions feature. Every corporation has a corresponding label that represents its credit level. Let denotes the set of labels, and is the number of all unique labels. Corporate credit rating models aim to predict the credit level according the profile of corporation .

2.2. Contrastive Self-supervised Pre-training

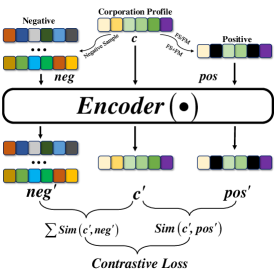

The architecture of the Contrastive Self-supervised Pre-training is described as Figure 2. Positive samples and negative samples are generated by self-supervised learning tasks and negative sampling, respectively. They are all mapped into another vector space through an encoder function to get better initialization. Finally, the encoder model is trained by constructing the contrastive loss between positive samples and negative samples.

Self-supervised Learning Tasks. Inspired by masked-LM used in pre-training for NLP and unordered nature of corporation profile, we propose two methods for generating positive samples: Feature Masking (FM), Feature Swapping (FS), and design three self-supervised learning tasks: FS, FM, FS+FM. During the FS task, we can randomly swap the location of features for times due to the unordered nature of the corporation profile to build the self-supervised task. In addition, as demonstrated in figure 2, FM is designed to mask a subset of input features, therefore, they can only train by partial features . FS+FM is a more complicated task by using FS and FM simultaneously.

Encoder Function. Theoretically, any encoder function which could map a vector space into another vector space can be applied to our framework. In our experiments, we use MLP and Transformer. MLP is easy and simple while Transformer is more powerful but more complicated. It is defined as follows:

| (1) |

where , is the representation of corporation in new vector space, is the dimension of new vector space.

Negative Samples and Contrastive Loss. For negative samples, we can randomly select sample which different from corresponding positive samples. Here we use cosine similarity to measure the distance between the embeddings of two samples. And InfoNce loss is applied to build contrastive loss. The self-supervised pre-training (SSP) loss can be represented as follows:

| (2) |

| (3) |

2.3. Vector Space Stacking

To fully use the information of data, we propose two methods of vector space stacking: Space Concatenation (SC) and Space Fusion (SF). They can be formulated as follows:

| (4) |

| (5) |

where , and due to .

When the new vector space and origin vector space are in different space, in other words, , we can concatenate them together to form a large space. In this space, both origin data and pre-trained data can be used to predict the credit level. What’s more, if , not only Space Concatenation but also Space Fusion can be used to mix two spaces. When CP4CCR will degenerate into the common credit rating model. While , only pre-trained data will be used. The reason why we design this structure will be explained in Section 3 (Experiment).

2.4. Phase 2

After the pre-training in phase 1, the better initialization of data will be got. In this vector space, similar samples will be closer, and dissimilar samples will be far from each other. The border between different classes will be wider. Therefore, this distribution of data will be easy for standard credit rating models to learn, especially for the class with few samples. The result of experiments will demonstrate this point. The training process can be formulated as follows.

| (6) |

| (7) |

| (8) |

where denotes the one-hot encoding vector of ground truth item, is parameter-specific regularization hyperparameters to prevent overfitting, and the model parameters are . The Back-Propagation algorithm is performed to train the model.

3. Experiment

In this section, we aim to answer the following three questions:

RQ1. Could the proposed CP4CCR improve the performance of standard credit rating models?

RQ2. How the proposed CP4CCR infect the data distribution of class with few samples?

RQ3. How do different types of vector space stacking affect the model performance?

3.1. Experimental Configurations

Dataset. We evaluate the proposed CP4CCR on the corporate credit dataset. It has been built based on the annual financial statements of Chinese listed companies and China Stock Market & Accounting Research Database (CSMRA). The results of credit ratings are conducted by the famous credit rating agencies, including CCXI, China Lianhe Credit Rating (CLCR), etc. The financial data of the corporation includes six aspects: profit capability, operation capability, growth capability, repayment capability, cash flow capability, Dupont identity. After the same preprocess as work (Feng et al., 2020b),we get 39 features and 9 rating labels: AAA, AA, A, BBB, BB, B, CCC, CC, C.

Baselines. To evaluate the performance of the proposed CP4CCR, we select several models including KNN, Logistic Regression (LR), Random Forest (RF), Decision Tree (DT), GBDT, AdaBoost, GaussianNB, LDA, SVM (linear), SVM (rbf), MLP and Xgboost due to the particularity of the financial field. But we believe our framework will have more or less improvement based on other corporate credit rating models.

Evaluation Metrics. We adopt three commonly-used metrics for evaluation, including Recall, Accuracy, and F1-score. Let denote the set of credit rating models, and is the set of metrics. For comparing overall improvement on all kinds of rating models, we propose a metric, Overall Performance (OaP), which can be computed as follows:

| (9) |

where means the metric of model under self-supervised pre-training, while uses the origin dataset. On the whole, means CP4CCR has a positive gain on all models, negative gain vice versa.

Hyperparameter Setup. During the data preprocessing, we perform the Feature Masking, Feature Swapping and FS+FM respectively. is set to 4, and negative samples is set to 8. In the experiment, we use the MLP or Transformer as the encoder function. The initial learning rate for Adam is set to 0.001 and will decay by 0.00001.

3.2. Improvement with Baseline Methods (RQ1)

| MLP | Transformer | |

|---|---|---|

| FS | 0.60619 | 1.01328 |

| FM | 0.81989 | 1.03799 |

| FS+FM | 0.86575 | 1.04080 |

To demonstrate the improvement of our proposed framework CP4CCR, we conduct experiments based on the baseline methods. The origin denotes the data without pre-training. Data are pre-trained by three different self-supervised tasks:@FS, @FM, @FS+FM. We find that most baselines are improved by pre-training. Due to the space limit, we omit the sophisticated original result. For clearly verifying, the overall performance (OaP) is displayed in Table 1. Both two encoder functions have a positive gain for data pre-training while the transformer encoder is better. FM is superior to FS, and perform them simultaneously will bring better results.

Besides we find another interesting result, in terms of the powerful encoder (Transformer), different types of pretext tasks bring almost the same positive gain for the model. However, a normal encoder (MLP) has a relative gap between different pretext tasks. It is might that a more powerful encoder is more robust to the pretext tasks. Therefore, we should pay more attention to the design of pretext tasks for the normal encoder, while for the powerful encoder, concentrating on improving the ability of it is a better way.

3.3. Influence on the Class Imbalance(RQ2)

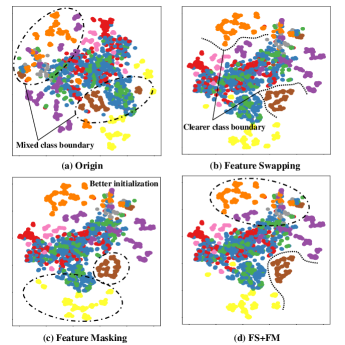

To clearly demonstrate the influence on the class-imbalanced problem, we perform the t-SNE visualization on the original and pre-trained data.

From Figure 3, the original data is usually chaotic. But after contrastive self-supervised learning, the imbalanced problem is mitigated, which results in clearer boundary and better initialization. For example, we can find that there are clear boundaries with feature swapping self-supervised tasks from Figure 3 (b). And in Figure 3 (c) yellow and brown samples get better initialization compared with original data to easily perform downstream tasks (Corporate Credit Rating).

3.4. Different Vector Space Stackings (RQ3)

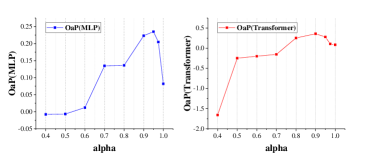

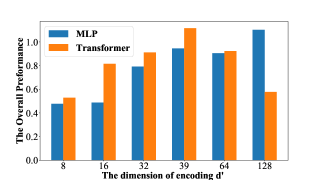

To answer the RQ3, in this section, we analyze how hyper-parameter impacts the metric OvP when the dimensions of origin and new vector space are the same, in other words, . The following Figure 4 shows the result.

We can find that when is too small, space fusion even results in a negative gain. It gets better performance when is about 0.9. And in the whole, the MLP encoder is stable, while the transformer encoder performs better but bigger variance.

What’s more, we analyze the influence on space concatenation when , the variation of OaP follows the changes of encoding dimension . From Figure 5, we can draw some conclusions. When is less than 64, the Transformer encoder performs better than MLP. As increasing, larger vector space brings more positive gain in MLP than Transformer. We believe that increasing leads to more parameters for Transformer encoder which converges difficultly. In addition to considering the time of cost, we believe that a relatively satisfied result is got when with space concatenation.

All in all, both FS and FM have positive gain to get better initialization and clearer boundary. Then Transformer is better than MLP to be the encoder function in the majority of cases. Finally, in terms of different space stackings, space concatenation exactly a great way to mix the original and new data information.

4. Conclusion

In this work, we propose a novel framework named Contrastive Pre-training for Imbalanced Corporate Credit Rating (CP4CCR), which can get better initialization and clearer boundary by contrastive self-supervised learning. In specific, we proposed two self-supervised tasks: Feature Masking and Feature Swapping, and two types of vector space stacking: Space Concatenation and Space Fusion. Extensive experiments demonstrate that our CP4CCR can improve the performance of baseline methods by pre-trained data. What’s more, Transformer is a better encoder function for contrastive self-supervised pre-training. In terms of space stackings, space concatenation is still a better way. We believe this work will bring a new framework to tackle imbalanced corporate credit rating in reality.

References

- Bruss et al. (2019) C Bayan Bruss, Anish Khazane, Jonathan Rider, Richard Serpe, Antonia Gogoglou, and Keegan E Hines. Deeptrax: Embedding graphs of financial transactions. arXiv preprint arXiv:1907.07225, 2019.

- Caron et al. (2020) Mathilde Caron, Ishan Misra, Julien Mairal, Priya Goyal, Piotr Bojanowski, and Armand Joulin. Unsupervised learning of visual features by contrasting cluster assignments. arXiv preprint arXiv:2006.09882, 2020.

- Chen and Long (2020) Binbin Chen and Shengjie Long. A novel end-to-end corporate credit rating model based on self-attention mechanism. IEEE Access, 8:203876–203889, 2020.

- Chen et al. (2020) Ting Chen, Simon Kornblith, Mohammad Norouzi, and Geoffrey Hinton. A simple framework for contrastive learning of visual representations. arXiv preprint arXiv:2002.05709, 2020.

- Cheng et al. (2019a) Dawei Cheng, Yi Tu, Zhen-Wei Ma, Zhibin Niu, and Liqing Zhang. Risk assessment for networked-guarantee loans using high-order graph attention representation. In IJCAI, pages 5822–5828, 2019.

- Cheng et al. (2019b) Dawei Cheng, Yiyi Zhang, Fangzhou Yang, Yi Tu, Zhibin Niu, and Liqing Zhang. A dynamic default prediction framework for networked-guarantee loans. In Proceedings of the 28th ACM International Conference on Information and Knowledge Management, pages 2547–2555, 2019.

- Cheng et al. (2020a) Dawei Cheng, Zhibin Niu, and Yiyi Zhang. Contagious chain risk rating for networked-guarantee loans. In Proceedings of the 26th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 2715–2723, 2020.

- Cheng et al. (2020b) Dawei Cheng, Sheng Xiang, Chencheng Shang, Yiyi Zhang, Fangzhou Yang, and Liqing Zhang. Spatio-temporal attention-based neural network for credit card fraud detection. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 34, pages 362–369, 2020.

- Chi et al. (2020) Zewen Chi, Li Dong, Furu Wei, Nan Yang, Saksham Singhal, Wenhui Wang, Xia Song, Xian-Ling Mao, Heyan Huang, and Ming Zhou. Infoxlm: An information-theoretic framework for cross-lingual language model pre-training. arXiv preprint arXiv:2007.07834, 2020.

- Fang and Xie (2020) Hongchao Fang and Pengtao Xie. Cert: Contrastive self-supervised learning for language understanding. arXiv preprint arXiv:2005.12766, 2020.

- Feng et al. (2020a) Bojing Feng, Haonan Xu, Wenfang Xue, and Bindang Xue. Every corporation owns its structure: Corporate credit ratings via graph neural networks. arXiv preprint arXiv:2012.01933, 2020.

- Feng et al. (2020b) Bojing Feng, Haonan Xu, Wenfang Xue, and Bindang Xue. Every corporation owns its structure: Corporate credit ratings via graph neural networks, 2020.

- Feng et al. (2020c) Bojing Feng, Wenfang Xue, Bindang Xue, and Zeyu Liu. Every corporation owns its image: Corporate credit ratings via convolutional neural networks. arXiv preprint arXiv:2012.03744, 2020.

- Giorgi et al. (2020) John M Giorgi, Osvald Nitski, Gary D Bader, and Bo Wang. Declutr: Deep contrastive learning for unsupervised textual representations. arXiv preprint arXiv:2006.03659, 2020.

- Gogas et al. (2014) Periklis Gogas, Theophilos Papadimitriou, and Anna Agrapetidou. Forecasting bank credit ratings. The Journal of Risk Finance, 2014.

- Golbayani et al. (2020) Parisa Golbayani, Dan Wang, and Ionut Florescu. Application of deep neural networks to assess corporate credit rating. arXiv preprint arXiv:2003.02334, 2020.

- He et al. (2020) Kaiming He, Haoqi Fan, Yuxin Wu, Saining Xie, and Ross Girshick. Momentum contrast for unsupervised visual representation learning. In Proceedings of the IEEE/CVF Conference on Computer Vision and Pattern Recognition, pages 9729–9738, 2020.

- Jaiswal et al. (2020) Ashish Jaiswal, Ashwin Ramesh Babu, Mohammad Zaki Zadeh, Debapriya Banerjee, and Fillia Makedon. A survey on contrastive self-supervised learning. arXiv preprint arXiv:2011.00362, 2020.

- Jaiswal et al. (2021) Ashish Jaiswal, Ashwin Ramesh Babu, Mohammad Zaki Zadeh, Debapriya Banerjee, and Fillia Makedon. A survey on contrastive self-supervised learning. Technologies, 9(1):2, 2021.

- Kim (2005) Kee S Kim. Predicting bond ratings using publicly available information. Expert Systems with Applications, 29(1):75–81, 2005.

- Mikolov et al. (2013) Tomas Mikolov, Ilya Sutskever, Kai Chen, Greg S Corrado, and Jeff Dean. Distributed representations of words and phrases and their compositionality. In Advances in neural information processing systems, pages 3111–3119, 2013.

- Misra and Maaten (2020) Ishan Misra and Laurens van der Maaten. Self-supervised learning of pretext-invariant representations. In Proceedings of the IEEE/CVF Conference on Computer Vision and Pattern Recognition, pages 6707–6717, 2020.

- Pai et al. (2015) Ping-Feng Pai, Yi-Shien Tan, and Ming-Fu Hsu. Credit rating analysis by the decision-tree support vector machine with ensemble strategies. International Journal of Fuzzy Systems, 17(4):521–530, 2015.

- Petropoulos et al. (2016) Anastasios Petropoulos, Sotirios P Chatzis, and Stylianos Xanthopoulos. A novel corporate credit rating system based on student’st hidden markov models. Expert Systems with Applications, 53:87–105, 2016.

- Trinh et al. (2019) Trieu H Trinh, Minh-Thang Luong, and Quoc V Le. Selfie: Self-supervised pretraining for image embedding. arXiv preprint arXiv:1906.02940, 2019.

- Wu and Hsu (2012) Tsui-Chih Wu and Ming-Fu Hsu. Credit risk assessment and decision making by a fusion approach. Knowledge-Based Systems, 35:102–110, 2012.

- Xie et al. (2020) Xu Xie, Fei Sun, Zhaoyang Liu, Jinyang Gao, Bolin Ding, and Bin Cui. Contrastive pre-training for sequential recommendation. arXiv preprint arXiv:2010.14395, 2020.

- Yang and Xu (2020) Yuzhe Yang and Zhi Xu. Rethinking the value of labels for improving class-imbalanced learning. Advances in Neural Information Processing Systems, 33, 2020.

- Yao et al. (2020) Tiansheng Yao, Xinyang Yi, D. Cheng, F. Yu, Ting Chen, Aditya Menon, L. Hong, Ed Huai hsin Chi, Steve Tjoa, J. Kang, and Evan Ettinger. Self-supervised learning for large-scale item recommendations. arXiv: Learning, 2020.

- Yeh et al. (2012) Ching-Chiang Yeh, Fengyi Lin, and Chih-Yu Hsu. A hybrid kmv model, random forests and rough set theory approach for credit rating. Knowledge-Based Systems, 33:166–172, 2012.