Optimal dynamic regulation of carbon emissions market

A variational approach

Abstract

We consider the problem of reducing the carbon emissions of a set of firms over a finite horizon. A regulator dynamically allocates emission allowances to each firm. Firms face idiosyncratic as well as common economic shocks on emissions, and have linear quadratic abatement costs. Firms can trade allowances so to minimise total expected costs, from abatement and trading plus a quadratic terminal penalty. Using variational methods, we exhibit in closed-form the market equilibrium in function of regulator’s dynamic allocation. We then solve the Stackelberg game between the regulator and the firms. Again, we obtain a closed-form expression of the dynamic allocation policies that allow a desired expected emission reduction. Optimal policies are not unique but share common properties. Surprisingly, all optimal policies induce a constant abatement effort and a constant price of allowances. Dynamic allocations outperform static ones because of adjustment costs and uncertainty, in particular given the presence of common shocks. Our results are robust to some extensions, like risk aversion of firms or different penalty functions.

Keywords: Stochastic optimization, environmental economics, cap and trade, linear quadratic problem, Fréchet differentiability, market equilibrium, social cost minimisation.

AMS subject classifications: 91A65, 91B60, 91B70, 91B76, 49J50, 93E20.

JEL subject classifications: C62, E63, H23, Q52, Q58.

Acknowledgements: We warmly thank Bruno Bouchard, Anna Creti, Paolo Guasoni, Peter Tankov and Nizar Touzi for discussions on the topic.

1 Introduction

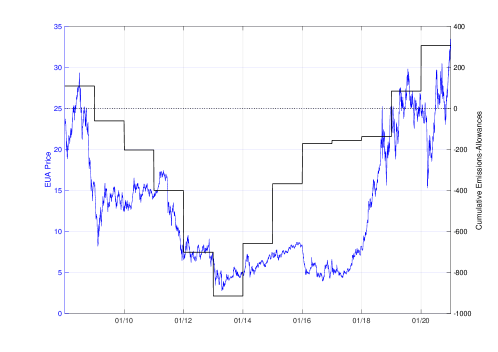

Since its inception in 2005, the European Union Trading System has been a major innovative tool to manage carbon emissions and help EU member states reach their agreed reduction targets. Former examples of cap-and-trade mechanism to reduce pollution include the successful cap-and-trade market for sulfur dioxide and nitrogen oxides in the US (Title IV of Clean Air Act Amendments, 1990). However, the striking novelty of the EU carbon market is the dimension: more than 30 billions euro of value gathering more than 15 thousands stationary installations across 30 countries. The seminal paper by Montgomery (1972) [26] on market for licences has found here a spectacular illustration of the idea that market mechanisms can be efficiently developed to achieve pollution reduction. Nevertheless, after 15 years, it is clear that the EUTS is facing some issues. Figure 1 provides the price of allowances from January, 2008 to June, 2020 and the cumulative difference between total verified emissions per year and total allowances. It shows that the market price of carbon is highly sensitive to the relation between supply (allowances) and demand (emissions). The 2008 financial crisis led a large surplus that lasted until 2013 and led to a depressed market price, which reached less than 5 €/tCO2. During this period, emissions were reduced, not because of firms abatement efforts, but because the world was experiencing a major recession. This phenomenon led the EU to design the Market Stability Reserve mechanism (MSR), to reduce market price volatility and over supply (EU Decision 2015/1814 of October 6, 2015 on EU Directive 2003/87). In a nutshell, the MSR regulates the potential market imbalances either by backloading allowances to the future or providing more allowances through auctions during the current phase and the next ones. This mechanism makes the carbon market regulation a dynamic process.

.

Thus, the MSR mechanism implements the idea that contingent regulation should be preferred to fixed ones. This concept has been vastly supported in the literature, since Weitzman’s (1974) [37] seminal paper on regulation under uncertainty. From there, an intense research activity has focused on dynamic regulation in different settings. Hahn (1989) [17] and more recently Hepburn (2006) [18] both provide surveys on regulation through prices or quantities as well as a framing of the admissible tools to regulators.

In our specific case of carbon market, there exists an extensive literature which analyzes the carbon emissions reduction problem under its many different aspects. The optimality of banking permits from one period to the next has been studied in Rubin (1996) [33], Schennach (2000) [34], Chaton et al. (2015) [4], Lintunen and Kuusela (2018) [25] and Kuusela and Lintunen (2020) [23]. Mechanism designs are proposed in Carmona et al. (2010) [7] in a discrete time model to reduce electricity producers windfall profits. An important stream of the literature on diffusive pollution deals with imperfect competition and strategic interaction among polluters. Requate (1993) [31], Von Der Fehr (1993) [36] and recently Anand and Giraud-Carrier (2020) [1] develop static models of imperfect competition which point out the firms capacity to increase their profit with emissions regulation.

The focus in the present paper is continuous time regulation of the carbon emissions with dynamic allowances allocation, see also Kollenberg and Taschini (2016, 2019), Grüll and Taschini (2011) [16], Pizer (2002) [29] and Pizer and Prest (2020) [30]. However, we leave for future research the coupling of the dynamical aspects of emissions reductions with imperfect competition among polluters.

We regard carbon reduction as a stochastic Stackelberg game. Firms are the Followers, and the regulator is the Leader. The model for firms is a continuous time stochastic model, largely inspired by the Kollenberg and Taschini (2016, 2019) [21, 22] carbon emissions market model. Firms experience individual emissions growth rate, plus idiosyncratic as well as common economic shocks. Abatement costs are heterogeneous and linear-quadratic. Although there are significant uncertainties on the marginal abatement costs of carbon reduction (see Gillingham and Stock (2018) [14] for an introduction on the topic), we make the assumption that at the time scale of carbon market emissions phase, less than ten years, these costs are known and constant. Firms can trade the carbon emissions allowances provided by the regulator, and emissions market imperfection is taken into account by an impact on the price of carbon. The key feature is that each firm is endowed with a bank account, as in the cited papers by Kollenberg and Taschini. The bank account position is the result of the allocation received, the traded permits minus the realised emissions. Further, firms face a terminal quadratic penalty on their bank position at the end of the regulated period - this is a strong incentive to achieve emission reduction. There are quite large uncertainties on the damage cost function induced by carbon emissions (see Hsiang and Kopp’s [19] and Auffhammer [2] papers for a thorough introduction to the uncertainties in carbon emissions damage function). Nevertheless, the convex terminal penalty can be interpreted as the expected future damage costs induced by non-compliant emissions. The objective of the authority is to achieve a given expected carbon emission reduction at least possible expected total cost from abatement, trading and terminal penalty. Dynamic allocation processes available to the regulator are chosen in the space of semimartingales, i.e. processes which are the sum of a diffusion part and a jump component.

Usually, carbon emissions equilibrium price is tackled using forward-backward stochastic differential equations as illustrated in Carmona et al. (2009, 2010, 2011, 2013) [6, 7, 5, 8]. Further, stochastic dynamic Stackelberg games are typically solved using Bellman’s principle and coupled HJB equations. On this, the reader is referred to Bensoussan et. al. (2014) [3] for a survey on the problem and illustrations in the linear quadratic case.

Instead, our approach is in the spirit of Duffie’s utility maximisation via stochastic gradient methods (see Duffie (2001) [9]). Since the objective functions in our problem are linear quadratic, they are Fréchet differentiable over the space of square integrable processes. This smoothness allows for stochastic variational techniques and leads to explicit and compact expressions for the equilibrium price and optimal controls. In fact, using the variational approach we provide closed form expressions for the best response of each firm. Without surprise, the optimal abatement effort equates the marginal abatement cost to the marginal penalty. More surprisingly, the abatement effort process is a martingale irrespectively of the allocation. We obtain in closed form a unique market equilibrium, reached at the trading rates that clear the market. The corresponding equilibrium price is a martingale given by the conditional expectation of the (average of) marginal penalties. Its dynamics are driven by (conditional) expectation of global allocations and emission shocks. Of course, the higher the allocations, the lower the market price, and conversely for shocks. Further, we show that the same methodology can be applied to different situations, like risk-averse firms or alternative terminal penalty function.

Our main findings consist in showing that optimal dynamic policies are not unique, though sharing common properties. All optimal dynamic policies induce a constant abatement effort. As a consequence of constant abatement efforts, the market equilibrium price is also constant. All dynamic allocations provide the same expected allocation. A simple example of optimal dynamic policy consists in, first, debiting the firms accounts by the level of the desired emission reduction and then to credit them at the business-as-usual emission rate, including shocks. By acting in this way, the regulator hedges or protects firms against heavy adjustment costs. Far from being a drawback, the non-uniqueness of the optimal dynamic allocation suggests that by the same tool the regulator could reach other goals on top of the reduction of expected emission at the minimum social cost. An example is adding constraints on the financing of new technologies. We leave this analysis to future research.

Indeed, an accurate comparison with a static allocation mechanism as implemented in the first phases of the EUTS shows that dynamic allocation mechanisms outperform static allocations only in the presence of adjustment costs, business cycles and, in particular, of common shocks. If any of these three features is absent, there is no benefit from the implementation of a dynamic allocation mechanism. Using crude data of verified emission of the industrial sectors involved in the EUTS on the period 2008 to 2012, we calibrated our model. Using the closed formulas then, we calculated the difference in cost between the optimal dynamic allocation described above and three alternative existing policies, namely the static allocation mechanism that prevailed during Phase I and II, a MSR-like mechanism and the pure tax policy. We find significant difference in cost between static and dynamic allocations, approximately when flexibility is low. On the other hand, the pure tax policy induces costs of higher order of magnitude.

The paper is organised as follows. Section 2 describes the stochastic underlying model and formalises the regulator’s problem. Section 3 deals with the firm individual optimisation problem for a fixed allocation process and a given market price process. Section 4 provides the market equilibrium both with and without market impact. Section 5 solves the regulator’s problem. Comparisons with alternative policies, like Market Stability Reserve, pure tax and static allocation are gathered in Section 6. There, numerical illustrations are also given. Finally, the Appendix contains technical results and computationally intensive parts of the proofs of the main Theorems.

2 The model

The regulation of carbon allowances is indeed quite complex. In particular, it occurs over several periods, and allowances can be banked from one period to the other. We abstract from these features and focus on a single period of years at the end of which compliance is assessed, as in Carmona et al. (2010, 2013) [7, 8], Kollenberg and Taschini (2016, 2019) [21, 22], Fell and Morgenstern (2010) [11].

A regulator (the Leader) wishes to reduce the pollution produced by a set of firms (Followers) over a period . To this end, she allocates carbon permits to the firms. Given the received allocation, each firm minimizes its reduction, trade and terminal penalty cost till the system reaches a market equilibrium. Then, the regulator minimizes optimal social cost over possible allocations. The stochastic model formalization goes as follows.

Consider a filtered probability space , in which the filtration is the augmented Brownian filtration generated by a standard dimensional Brownian motion . Fix further correlation factors and let

| (2.1) |

In particular, the correlation between is . The index notation in what follows is self explanatory, in the sense that denotes a process, while refer to constants or deterministic functions. The Business As Usual (BAU) cumulative emissions dynamics for firm are:

| (2.2) |

where and are the average growth rate and standard deviation rate of their emission. Thus, the emission of firm is affected by its own idiosyncratic noise and by the common economic business cycle . A positive shock induces an increase in emissions.

In the BAU case, the expected total emission over the period is where and . The regulation wishes to reduce the expected emissions to

i.e. to achieve percent of reduction compared to BAU. The regulator has several instruments at her disposal (taxes, quotas) but she wishes to implement a dynamic cap–and–trade system working in this way. At she opens for each firm a bank account and allocates permits, summed up in the cumulative process . The -th bank follows the dynamics:

| (2.3) |

In the above, is the abatement rate and is the trading rate in the (liquid) allowances market. When making the effort , the emissions of firm increases at a rate .

Assumptions: Firms controls are square integrable wrt , namely they belong to . The allocation process is a square integrable semimartingale, that is for all , decomposable into square integrable finite variation part and square integrable stochastic integral:

We do not require that the finite variation part of is absolutely continuous wrt . Therefore, the regulator is free e.g. to allocate (credit or debit) permits at discrete instants, which can be fixed or stopping times, and/or at a rate . In addition, the Lebesgue Decomposition Theorem allows the decomposition of into the sum of an absolutely continuous part with respect to the Lebesgue measure, and of singular part . So,

| (2.4) |

Each of the three addenda can be null. As already mentioned, the singular can be e.g. a pure jump part. Namely, a weighted sum of Dirac deltas along a targeted (stochastic) time grid, in which the regulator provides/cancels allowances in a discrete way:

where the dates form an increasing sequence of stopping times and . This covers the case in which there is an initial allocation. In fact,

it is enough take in the grid, and . Given an allowance scheme, the allowance bank of firm gives at all s the net position of the firm in terms of emissions, abatement, allowances trading and allowances endowment by the regulator. A positive economic shock to the emissions induces a decrease in the bank accounts, while an increase in the allocations makes the accounts grow. The bank dynamics can be rewritten as

| (2.5) |

in which is the net allocation process over the trend

Since our results on the optimal regulation depend only on , the trend rate does not necessarily have to be a constant. Here, we set it constant for ease of presentation. For future use, note that

For a given market price of permits and a given (net) allowance scheme , the firm aims to solve its cost minimization problem:

| (2.6) |

In the objective function of firm , the abatement cost function is supposed to be quadratic

to consider both the linear and the adjustment costs, the latter proportional to the square of the abatement rate. This choice is in line with the literature of carbon emission reduction (see Gollier (2020) [15] and reference therein). Further, the linear-quadratic form captures the non decreasing feature of marginal abatement cost. From an investment point of view, it means that there is some irreversibility in the abatement decision. The higher the values of , the higher the flexibility of the abatement process and thus the higher the reversibility of the decision.

About trading costs, we take into account a price impact effect as in the original Kyle (1985) model [24], with constant market depth parameter . The term , with equal for all firms, is the terminal monetary penalty on the bank accounts set by the regulator. The firm is going to pay both if its bank is above or below the compliance zero level. It is a regularized version of the actual terminal (cap) penalty function, which is zero if the firm is compliant and linear otherwise.

The objective of the regulator is to design dynamic allocation schemes to reduce expected emission, while minimising social cost

| (2.7) |

when the firms behave optimally and are at equilibrium, namely when .

So, the problem regulator/firms falls in the category of dynamic stochastic Stackelberg games since the regulator aims at minimizing social cost from optimal firms reduction and trade. Thus, she acts as a Leader while firms act as Followers (see Bensoussan et. al. (2014) [3] for a survey).

3 The firm optimal response

3.1 General result

The focus here is on the single firm cost minimization, for a given exogenous allowances price and a net allocation scheme . We define

| (3.1) |

in which

-

•

is the martingale closed by . It gives, at time , the (conditional) expectation of the firm cumulative (net) endowment . Different intertemporal allocations, with the same cumulative value on the regulatory horizon give rise to the same . From the definition of ,

-

•

the process gives, at time , the conditional expectation of the residual net allocation on .

As anticipated in the Introduction, the firm minimization problem can be tackled by variational methods. In our case, the functional is linear-quadratic:

strictly convex and smooth. The optimal solution is unique and can be obtained by annihilating the stochastic gradient.

By the Riesz Representation Theorem, any linear form on a Hilbert space can be represented by an element of the space itself. Therefore, the differential of can be represented by the gradient, which belongs to . The gradient is then a couple of square integrable, adapted processes on which we are going to write the first order conditions (FOC) in the proof of the next Theorem.

Theorem 3.1.

For a given cumulative, net allocation scheme and for a given allowances price , the i-th firm cost minimization problem (2.6) has a unique, explicit solution in .

(i) The optimal abatement is the solution of the following SDE

| (3.2) | ||||

| (3.3) |

and is therefore a martingale.

(ii) The optimal trade is

| (3.4) |

(iii) Both optimal controls can be rewritten in feedback form in function of the bank state

| (3.5) | ||||

| (3.6) |

in which the expected residual allocation process appears in place of .

Proof. The proof is given in Section A.1. Here, we just anticipate the FOCs written on the gradient of , as they will be explicitly referred to in the rest of the paper. They are

| (3.7) | ||||

| (3.8) |

Let us comment on these findings.

-

(i)

The FOCs can be written

The marginal abatement cost is equal to the (C.E. of the) marginal penalty, and so is the marginal cost of trading, . Consistently with economic intuition, the firm buys (resp. sells) if its marginal abatement cost is higher (resp. lower) than the market price.

-

(ii)

The optimal abatement is a martingale. In fact, it is a stochastic integral, with a bounded, deterministic integrand , of three explanatory martingales: , namely the C.E. of cumulative net allocation over ; the conditional expectation of the integrated price; and the emission noise . A fortiori it is not the full intertemporal structure of the net allocation which matters, as it appears in (2.4). The key quantity here is .

The firm compares the dynamics of the expectation of what will be given during the whole regulatory period, , to noise and to integrated price, and then makes the decision on effort. If there is a positive economic shock everything else being equal, the firm effort increases. It decreases if is positive, i.e. if the firm anticipates an increase in total expected net allocation.

The integrand in the martingale representation for depends on the following parameters: the individual firm adjustment cost of abatement , the common penalty coefficient and market depth coefficient .

When written in feedback form, depends only on the state , on the C.E. of net residual allocation at time , , and on the C.E. of the (residual) integrated price.

Finally, we remark that martingality of would be preserved if the abatement first order cost became a martingale. -

(iii)

The optimal trade is not a martingale, unless is a martingale as well. This will occur at equilibrium (see Section 4).

3.2 Market without frictions

Absence of market frictions is a common assumption in the literature (see Kollenberg and Taschini (2016) [21] or Carmona et. al. (2010) [7] and the references within). TO better compare with this case, let us solve the firm optimisation problem when the market has infinite depth, . The problem becomes

| (3.9) |

If the optimizers exist, we cannot expect that will be unique. The objective function in fact loses strict convexity in the argument. The quadratic terminal penalty however involves the cumulative trade , for which uniqueness will be obtained.

Proposition 3.1.

Problem (3.9) admits a solution if and only if is a martingale. In case is a martingale, the abatement effort of firm is unique and given by:

| (3.10) |

The optimal trade rate is not unique. Any satisfying

| (3.11) |

is optimal, where is the martingale satisfying the Cauchy problem

| (3.12) |

The complete proof follows the same lines as the previous Theorem 3.1. We briefly highlight the main differences. The resulting FOCs are:

| (3.13) | |||

| (3.14) |

If is not a martingale, there are no stationary points and thus no minimizers. When is a martingale, as economic intuition suggests, each firm equates the marginal cost of abatement to the market price . Also, the market price is equal to the conditional expectation of the marginal penalty. In Theorem 3.1, frictions introduce deviation from these equalities. With finite in fact, we saw that the marginal cost of abatement equals the marginal cost of trading, as from (3.7), (3.8). Same holds for the relation between the marginal cost of trading and the marginal penalty.

Further, the FOC equations here

do not involve directly, but only the martingale generated by the total trade:

This is the main novelty, now the optimisation problem is strictly convex only in the total trade . Therefore the optimal and the generated martingale are unique. And, in fact, such martingale is found by replacing in relation (3.14), by its expression as a function of :

| (3.15) |

An application of Lemma A.2, together with evaluation at , gives

| (3.16) | ||||

| (3.17) |

Therefore, any satisfying

is optimal.

4 Market equilibrium

We are now ready to tackle the equilibrium problem of the system of firms. Recall that the noises in the firms activity have a quite general dependence structure, as described at the beginning of Section 3. Fix a net allocation policy of the regulator Define the positive, deterministic function

| (4.1) |

where is defined in (3.1). If firms share the same , all the functions are equal. Market equilibrium consists in finding a price that satisfies the market clearing condition:

| (4.2) |

in which the are given from the system (3.4). The price is then called an equilibrium price. The market equilibrium is described in the following Theorem.

Theorem 4.1.

For a given net cumulative allocation ,

-

(i)

The equilibrium price is the unique solution to the Cauchy problem:

(4.3) The price is therefore a martingale.

-

(ii)

The equilibrium can be written in feedback form as

(4.4) -

(iii)

The optimal controls are the unique solutions of the next Cauchy problems:

(4.5) (4.6) -

(iv)

In feedback form,

(4.7)

Proof. See appendix A.2.

Let us comment on the above results.

-

(i)

The explanatory processes in (4.3) for the equilibrium price are the martingales , . We observe that if all these martingales experience a positive shock, the price decreases. In short, if the regulator promises to all firms more (resp. less) future total net allocation than the effect of their economic shock, the price decreases (resp. increases).

-

(ii)

When the adjustment costs are equal, the deterministic coefficients become equal and can be factorized out in (4.4). The equilibrium price in this case depends then only on the aggregrate quantities

(4.8) -

(iii)

The optimal efforts are obtained from (3.2) exploiting the martingality of . The trade keeps its structure.

When there are no market frictions, we have seen in Section 3.2 that the optimal trade is non unique. However, there is a unique (martingale) equilibrium price , and consequently a unique abatement effort . The equilibrium price depends only on the aggregate quantities as in (4.8), plus the average of adjustment cost coefficient . If denotes an equilibrium triplet, the next Proposition sums up the results in this particular framework. We omit the proof, since it follows from combining Theorem 4.1 (sending to infinity) and Proposition 3.1.

Proposition 4.1.

When there are no market frictions,

-

(i)

The equilibrium price dynamics become

(4.9) in which and Its expression in closed-loop is given by

(4.10) where denotes the average bank account process.

-

(ii)

The abatement effort of firm is unique and given by:

(4.11) -

(iii)

The trading rates are not unique. Any satisfying

(4.12) is optimal, where satisfies the Cauchy problem

(4.13)

5 Optimal dynamic regulation

Market frictions are small compared to the cost of abatement required to achieve the carbon emission reduction targeted by the European Union. As documented by Frino et. al. (2010), the carbon market quality has been constantly increasing with tick size decreasing from 5 c€/t to 1 c€/t and a bid–ask spread of 5 c€/t as of 2008. Nowadays, the value of the bid–ask on the December contract is around 2 c€/t for a quoted carbon price around 30 €/t‡‡‡Source: Thomson-Reuters Refinitiv quotations of the EU EUA December contract., which makes a transaction cost less than 0.06%. Hence, we neglect them in the regulator’s problem and assume hereafter that there are no market frictions.

5.1 Main result

We address now the optimisation problem (2.7) of the regulator when the market is at equilibrium. The regulator faces:

| (5.1) |

in which is the optimal effort of the system given the allocation , while is the system emission under this effort. Using Proposition 4.1 (i) and (ii),

Hence, the reduction constraint on the expected emissions amounts to a constraint on the equilibrium price

| (5.2) |

The relation (5.2) gives the necessary average carbon price required to emerge from the market if the regulator wishes to achieve a carbon emission by a factor . This average price captures all the features of the system in a simple way: it is proportional to the inflexibility of the system, to the average abatement cost , to the growth rate of the emission and to the ambition of reduction .

Equating the constraint on in (5.2) with the expression (4.9) of obtained in Proposition 4.1 (i), we get

| (5.3) |

Thus, the regulator withdraws allowances on average as is negative. This holds regardless of the intertemporal allocation processes from the (detrended) equation (2.4), as the relevant processes are the . If e.g. firms receive allowances in the beginning, so that the banks satisfy , then in the regulator on average will withdraw permits.

Conversely, if initially firms are given

then the regulator will on average credit back permits in . In fact, using the decomposition of ,

and the second addendum must then be positive. By the Predictable Representation Property of the Brownian filtration generated by the noises (see (2.1)), each can be written as

with , . If denotes the integrands vector for firm , the problem can be re-parametrized on controls . With this formulation, we state our main result.

Theorem 5.1.

The social cost minimisation problem

| (5.4) |

has the following solutions structure:

-

(1)

Optimizers , annihilate the volatility of the price. The vectors are non unique. One set of optimizers is obtained by tracking the volatility of each firm separately, thus allocating to the i-th firm exactly the systemic () and idiosyncratic components ():

The optimal martingales become

-

(2)

Expected optimal allocations are also non unique. The regulator is free to allocate permits as long as the expectation of the total number of permits satisfies the constraint . An example is the equal assignment in expectation:

-

(3)

Optimal allocations are, as a consequence, non unique. If the regulator chooses the firm-by-firm volatility tracking and equal assignment in expectation as in item 1) and 2) above, there is an optimal set of net martingale allocations:

-

(4)

As the price has zero volatility, it is constant:

(5.5) -

(5)

Firms optimal abatements are unique and constant

-

(6)

Firms optimal trading rates are non unique. Any satisfying (4.12) is optimal. If the regulator chooses the firm-by-firm individual tracking in item 1) above, the dynamics of the associated are null. If in addition, there is equal endowment in expectation then an optimal solution is trading at a constant rate

-

(7)

The minimum social cost is

(5.6)

Proof. The cost function in (5.4) is convex and differentiable in for all . The Lagrangian is

in which the optimal controls are from Proposition 4.1. From (3.14), for all firms . Substituting the optimal firm abatement controls with as from (3.13), the optimal cost for the firm is

By the martingale property of , the Lagrangian becomes

Also,

Finally,

Optimality conditions:

-

•

. We have to impose

-

•

. The matrix process in the representation of is involved only in the dynamics of . In the Lagrangian, it thus enters only in the quadratic variation. This implies that the minimum wrt is attained when the regulator annihilates the quadratic variation, i.e. the volatility of . From Proposition 4.1, we just need to impose that

in which . Using (2.1), and recalling , the previous equation can be rewritten as

The above boils down to the system:

(5.7) Namely, the regulator allocates on the Brownian motion the aggregate volatility the system has in that shock. Thus, the net effect is that the regulator kills the exposure to shocks in the whole system. Clearly, a particular solution is to kill exposure firm by firm, with , and otherwise as stated in item (1).

-

•

Feasibility is simply

-

•

Price will then be unique, the positive constant

-

•

The optimal efforts are unique and constant, as per (4.11).

-

•

The optimal C.E. of total trade are non unique, because they depend on the C.E of the individual optimal total allocation as detailed in (4.13). If the regulator tracks individual volatility, then and .

-

•

Finally, the expression of the minimum social cost easily follows from the above relations.

Hence, the dynamic regulation effect is a constant market price. However, this condition is not imposed a priori, but it is a consequence of social cost minimisation. Indeed, the level of carbon emission reduction fixes the average level of required effort, and thus the average required price. But price fluctuations induce variations of effort, which in turn produce irreversible cost because of the inflexibility of the system. In fact, social costs are increased by price fluctuations. By annihilating price changes, the regulator avoids firms expensive stop-and-go.

In the optimal policy given in Theorem 5.1, one has

i.e. the regulator provides an initial (negative) allocation and then, credits the whole BAU emissions to the firms. As a consequence, the bank accounts have a deterministic, linear dynamic:

In other optimal schemes, the regulator eliminates all the economic uncertainty involved in the dynamics of the carbon emissions. Regulation does not necessarily kill individual emission noises, but uncertainty is tackled as a whole - as soon as the optimality condition (5.7) is respected.

Although more complex to implement than a tax or a static initial endowment, optimal dynamic policies offer a powerful tool in emissions control. In particular, non-uniqueness of optimal dynamic policies is a key feature in our model. Indeed, because they are non-unique, the regulator can achieve more goals using the same device. This can be obtained by e.g. adding more constraints to the optimal control problem of the regulator. An example could be an additional constraint on the financing of new technologies. We leave these developments for future research.

Remark 5.1 (When there are frictions).

The same procedure used in Theorem 5.1 applies to the case where there are market frictions. In that case, Theorem 4.1 states that the optimal efforts and trading rates are martingales. Also, the terminal values of the bank accounts still are deterministic functions of , as can be easily deduced from (3.7) and (4.7). Therefore the regulator’s general problem (2.7) also amounts to annihilating the volatility of . This goal is uniquely achieved by individual tracking, giving to firm . The dynamic allocation proposed in Theorem 5.1, item (3) is now the unique optimal policy. Optimal efforts and optimal trading rates will also be unique.

5.2 Extensions

Cap-and-trade mechanism

A cap-and-trade mechanism is often described by a terminal penalty in the form of a cap on emissions. This corresponds to a put on the bank, with strike equal to the maximum tolerated emission level . We show that the firm optimization problem can be still be solved by the variational methodology. Suppose the cost function of the agent is

where the cap is the minimum tolerated bank level at the end of the regulated period. After this threshold, the firm pays at maturity per ton exceeding the bank level. This formulation can be seen as continuous time version of the model in Carmona, Fehr an Hinz [6], with the additional features of price impact and quadratic abatement costs. In order to solve

we observe that the functional is finite, strictly convex and coercive on and so there exists a unique optimizer. is also sub-differentiable. In fact, the pointwise (non adapted) subdifferentials of the put expectation are:

in which is a -measurable r.v. Note that when then all the subdifferentials at coincide almost surely, so we can safely choose . The put becomes differentiable. This happens e.g. when the allocation of the regulator does not perfectly track the bank noise. In fact, in this case the distribution of has no atoms thanks to the presence of a diffusion term. In the paper [6], the assumption (19) in Theorem 1 is a very similar condition on the net firm position, which ensures that the subdifferential of the put is in fact unique. To better compare with [6], assume the put is differentiable. The FOCs become:

| (5.8) | ||||

| (5.9) |

and the system admits a unique solution in . At equilibrium, by market clearing the term vanishes in the second FOC and the equilibrium price becomes the average of the conditional expectations of the marginal penalties. If, as in [6] we neglect price impact, at equilibrium one gets the simplified relation

This implies that the sets , coincide a.s. and

and therefore the price can be seen as the marginal penalty of the aggregate put:

and equals the marginal abatement costs.

As in the cited [6], optimal strategies cannot be found in closed form. Nevertheless, we observe that the market equilibrium price is still a martingale, depending on the allocation processes and the abatement efforts are a linear function of the price. As in Theorem 5.1 then, optimal allocations annihilate the volatility of the price.

Risk aversion taken into account

Let us denote by

the random cost incurred in by a single firm. Suppose the agent has a concave utility finite on , smooth and with . Consider the expected utility functional

Assume that the functional is proper, namely there exists a couple in such that the expected utility of the associated cost , , is finite. The agent seeks to solve

Proceeding heuristically, we differentiate under the integral sign and get the (non adapted) gradient

in which is the bivariate process:

Since , then the FOC condition is

which is equivalent to (A.2) and therefore the same we had in the risk neutral case. Thus, the solutions found in Theorem 3.1 are the candidate optimal couple. We only need to check that the associated cost has finite utility. This is straightforward

since here is integrable and is finite on . Therefore, from Theorem 3.1 continues to be the optimal couple even in the presence of risk aversion.

6 Comparison with existing policies

We compare here the optimal dynamic allocation policy suggested in Theorem 5.1 with three alternative existing policies: the initial static allocation, the pure tax system, and a Market Stability Reserve–like allocation mechanism. In each case, we compute the social cost to achieve the same expected total carbon emissions reduction. For ease of presentation, the firms adjustment costs are assumed to be equal

6.1 Static allocation

For the sake of comparison, consider an ETS Phase 2-like mechanism, i.e. a static allocation: an initial endowment and zero intertemporal allocation for all and . Under this policy we now calculate the social cost (5.1), which will necessarily be suboptimal. Denote by the average initial endowment. Since , by Proposition 4.1 (i) rewritten with the equilibrium price is

| (6.1) |

since . The expected emissions under optimal effort given the above price are

Then, under a static allocation the regulator achieves the objective of emission reduction from the BAU trend to by setting

Thus, the initial price becomes identical to (5.5) and the regulator has to allocate on average

| (6.2) |

Note that contrary to the optimal dynamic allocation scheme (Theorem 5.1 (2)), the initial allocation here can be positive. Further, let us compare with the intuitive initial allocation of a cap-and-trade system. There, if regulator wishes to reduce the emissions to , this value will be the aggregate cap. Then, she would set precisely the initial endowment at the cap level per firm. Here instead the optimal initial endowment is lower than this intuitive cap.

The corresponding social cost is:

Let denote , with Since

straightforward computations lead to

| (6.3) |

Thus, the difference in social benefit between the static allocation (6.3) and the optimal allocation in (5.6) is given by

| (6.4) |

Such difference stems from the presence of uncertainty and inflexibility in the system. Further, suppose there are firms with identical and identical , so that we have .

In this case, . Thus, when is large, the volatility tends to zero, unless there is some correlation with the common shocks. In fact, when is non zero the per unit difference in cost does not vanish:

| (6.5) |

Thus, for large, the optimal dynamic policies continue to outperform the static allocation in the presence of common economic shocks.

Further, by the relation (6.1), the price quadratic variation satisfies:

| (6.6) |

which provides a way to estimate the flexibility parameter . Indeed, it satisfies

| (6.7) |

When the term is large (see the numerical illustration below in section 6.4), we have

| (6.8) |

The relation makes more explicit the relation between the volatility of the exogenous economic shocks and the equilibrium market price volatility. The penalty factor and the flexibility parameter act as the transmission belts of the economic shocks to the market price volatility. The higher the flexibility , the greater the compensation of an economic shock in the equilibrium market price.

6.2 Pure tax

As the name suggests, in a pure tax system there is no bank account for net emissions positions, nor allowances. Firm makes abatement effort only because of a proportional tax on total realized emissions from (2.3). Each firm then faces the minimization problem:

| (6.9) |

which admits a unique solution, the constant effort . So, the regulator would set the tax at

| (6.10) |

to induce a reduction of expected total emission of a factor . Without surprise, the tax level is equal to the constant price in (5.5) of the dynamic allocation schemes because there the expected emissions reduction is determined by the average carbon price. The social cost becomes

| (6.11) |

and must be compared with in (5.6). Quick computations show that the tax is more efficient than an optimal dynamic allocation when

| (6.12) |

The difference in cost between the tax system and the optimal dynamic allocation should be understood as follows. In a tax system, firms pay for each ton they emit whereas in the cap-and-trade system, they pay only for those tons which are non-compliant with the targets. Hence, the more the system emits carbon, the more it is socially expensive to set a tax. The relation (6.12) translates this phenomenon into a threshold on the penalty factor, i.e. the damage function.

6.3 MSR–like policy

To cope with the imbalances of the EUTS between realised emissions and total allocations, the EU has launched in 2019 a Market Stability Reserve (MSR). The policy rules under MSR specify that when the number of allowances in circulation falls below a certain threshold value (400 million allowances), the regulator auctions off a share of new allowances (%). Further, if the total number of allowances exceeds another threshold (800 million allowances), the same fraction of allowances are withdrawn from the market.

To make a comparison of the MSR policy with our framework, we consider a continuous time version of this mechanism. We work under identical initial endowments and allocations, since the social cost is a function of the aggregate quantities. So, consider a net allocation scheme with equal initial endowment (but no intertemporal singular for all and ), and identical net allocation rates given by:

| (6.13) |

The rationality behind the above allocation mechanism is that the regulator would like to drive the accounts from to an aggregate position so that by following a linear trajectory. In this scheme, deviations from the average expected trajectory of carbon emissions reduction are considered to be market imbalances and are compensated continuously at a rate proportional to the imbalance. The parameter acts as mean-reversion factor, trying to make the average bank accounts go back to the desired trajectory.

Since the allocation process is fixed, we need to determine such that

| (6.14) |

to ensure that the expected total emissions are reduced by a factor . Under this MSR-like mechanism, the market equilibrium follows the dynamics:

| (6.15) | ||||

| (6.16) | ||||

Since can be found explicitly, we can calculate the initial allocation that ensures a reduction of emission of level :

| (6.17) |

Computations are detailed in Appendix A.3. The complexity of the expression for the induced cost leads us to resort to numerical illustrations, see the next Section.

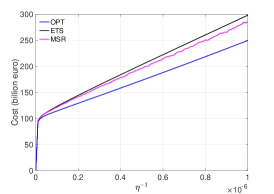

6.4 Numerical illustrations

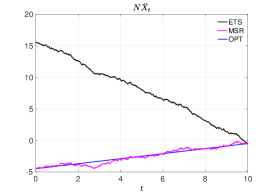

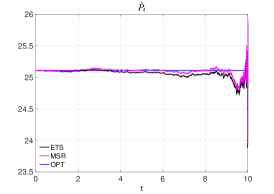

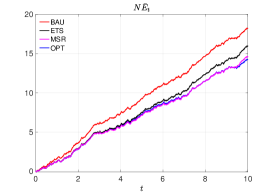

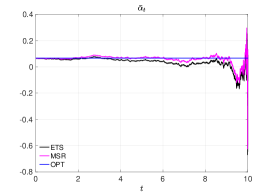

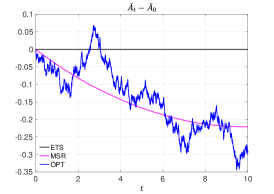

We illustrate here the firms behavior and provide some orders of magnitude of social costs in the various policy schemes above. As a reference situation, we consider an objective of reduction of 20% of carbon emission ( ) over a period of years.

This setup is quite close to the objective of the European Union in their climate policy adopted in 2008 for the Phase 2 of the EU ETS, only we consider a longer period of time, ten years instead of five. We consider the six main sectors covered by the EU ETS (Public Power and Heat, Pulp and Paper, Cement, Lime and Glass, Metals, Oil and Gas, Other), so . The average emission growth rate of the EU 27 members included in the EU ETS is around Gton per year. The average standard deviation of emission rate is Gton/year.

The volatility has been estimated on data provided by the European Environment Agency EU Emission Trading System data viewer. For sake of simplicity, we assume that sectors share an identical emission volatility . To estimate the correlation matrix among sectors, we considered the yearly verified emissions from 2008 to 2012. The result is an average correlation to the common shock of equal for all sectors. The terminal penalty parameter is chosen so to ensure that, in the optimal dynamic scheme, the reduction target is reached with a discrepancy of Gt. This means that verifies with Gt, namely €/ton2.

The estimation of the marginal abatement cost function per firm is the subject of a vivid, current debate amongst economists (see Gillingham and Stock (2018) [14] for an introduction on the topic). Our purpose here is to provide illustrative examples to fix the ideas on the difference in social costs across policies. Thus, we base our choice for on the estimation performed by Gollier (2020) [15] which are in turn based on the MIT Emissions Prediction and Policy Analysis of Morris et. al. (2012) [27]. It leads to taking €/ton and a nominal value of the flexibility parameter ton2€/year. Further, we make a sensitivity analysis of the costs in function of .

| (a) | (b) | (c) |

|

|

|

| (d) | (e) | (f) |

|

|

|

Figure 2 illustrates the behaviour of the different policies in the case of the presence of common shocks. With an average growth rate of 2 Gt per year on a 10 year period with a reduction objective of 20%, it leads to an expected reduction of 4 Gt. The optimal dynamic allocation schemes starts by allocating a debt of approximately 5 Gt to the firms while the static ETS scheme allocates approximately 15 Gt in the system, close to the natural cap of Gt. Both the static and dynamic allocation schemes achieve nearly the same reduction at the end of the regulated period as the trajectories show. But to reach that end, each scheme follows a different path. Under optimal dynamic allocation policies, total bank accounts, total abatement efforts and market equilibrium price are deterministic while the net cumulated allocation is random. Under the static ETS policy the opposite is true, while under the MSR–like policy each process involved is stochastic. Also, in the static policy the volatility is monotone increasing in time. Indeed, the relation (6.1) gives that

Hence, compared to its value at time zero, the volatility at maturity is multiplied by a , which explains the large oscillations observed at maturity. Figure 2 (f) shows the effect the choice on the different allocation schemes. First, we observe the hockey stick form of the costs. When is in the range , the system is flexible enough so that there is no significant difference in cost among the various allocation policies. When goes below , the difference in cost exhibits a linear growth. The discrepancy between the static ETS mechanism and the optimal dynamic scheme becomes approximately % ( billion euros compared to an optimal cost of billion). The fact that the MSR-like policy succeeds in getting close to the optimal trajectory of the bank accounts translates in a reduced cost compared to the static allocation. Thus, in the range of values for the flexibility of the system we picked, we find significant difference in costs between static and optimal dynamic allocation, but not an order of magnitude. The pure tax scheme is excluded from these comparisons because its cost is one order of magnitude higher than the other policies. In fact, even in the base scenario of we get an expected social cost of the allowances policies around billion euros, while the tax social cost is greater than billion euros.

7 Conclusion

We find the optimal dynamic allocation processes that achieve a given expected emission reduction of carbon emissions. They are non-unique, but have the same effect on the system: they induce constant abatement efforts. As a result, the equilibrium market price is also constant. A priori, the regulator is not pursuing any price control mechanism. A posteriori, however, the desired reduction goals naturally lead to that conclusion. The efficiency of optimal dynamic allocations scheme compared to sub-optimal yet intuitive policies strongly depends on the flexibility of the system and on its dependence on common business cycles. Non-uniqueness in the optimal policy suggests that within our framework the regulator can accomplish not only emission reduction at minimal social cost, but also consistently include other features such as the financing of new non-emissive technology. We leave these extensions for future research.

Appendix A Proofs and computations

The following facts will be used in the proofs.

Lemma A.1.

Let be a process in and . Then

Namely, the scalar product of and the pathwise integral equals the scalar product in of and the martingale process closed by , namely .

Proof. The proof is one line:

where the equalities from the second onwards follow from Fubini Theorem and from the properties of conditional expectation. An alternative is to apply integration by parts to the product of the martingale and the bounded variation process . The proof of the next Lemma is straightforward.

Lemma A.2.

Let be a martingale. Then, consider the martingale closed by

which also belongs to . Then,

and the dynamics of are given by

A.1 Proof of Theorem 3.1

For ease of notation, we drop the dependence on of the coefficients and of the controls. We split the cost function in two parts, running cost and terminal cost :

From the structure it is apparent that both and are differentiable. The differential of the running cost

is given by differentiation inside the integral

In the terminal penalty , the bank equals

If we apply the chain rule inside the expectation in , namely to we get the (non adapted) Frechet gradient:

in which is the gradient of w.r.t. . As is a linear map, is simply the constant bidimensional process

Given the regularity of the problem, we can differentiate under the expectation side. This means that the Frechet derivative must verify

To find the two components of , make the scalar product of e.g. the first derivative with a generic :

from which we deduce . Similarly for . Finally,

| (A.1) |

Putting things together, the differential of the cost function

| (A.2) |

The FOC equations for the generic agent write

| (A.3) |

Subtracting the two equations above,

which can be substituted into the first equation:

| (A.4) |

Thus, it is straightforward that the optimal abatement (if it exists) is a martingale, solution of the equation:

| (A.5) |

| (A.6) |

To solve for , we rewrite (A.5) in differential version:

By Lemma A.2, and thus

or

| (A.7) |

where the term between parentheses is (the differential of) a square integrable martingale. The Cauchy problem given by the SDE and the initial condition (A.6) uniquely identifies , since the dynamics of and are exogenous here. The optimal trade is then

| (A.8) |

Note that the optimal trade is a martingale of and only if is a martingale. To conclude, we rewrite the optimal couple as a function of the state . Start again from the first FOC,

and rewrite

An application of Lemma A.2 leads to

Finally, in feedback form reads as

and this concludes the proof, since .

A.2 Proof of Theorem 4.1

(i) Summing up over all the relations (3.4) and using market clearing condition,

| (A.9) |

From Theorem 3.1 (i),

| (A.10) |

Thus,

which shows that must be a martingale. Hence, by Lemma A.2,

which gives the SDE for the equilibrium price in (4.3).

For the initial condition of the equilibrium price dynamics, first using the first FOC in (A.4) written for and substituing as a function of and , we find that

| (A.11) |

Then substituting the value above in (A.9), we get after tedious computions:

| (A.12) |

(ii) The equilibrium price is given by the market clearing condition

According to Theorem 3.1 (ii), we deduce that:

| (A.13) |

from which we deduce that the equilibrium price is a martingale. Recalling that

and using the fact that is a martingale, we get that the equilibrium price is given by:

| (A.14) |

Hence,

| (A.15) |

Further,

| (A.16) |

from which

Hence,

(iii) Using relation (A.10) and the expression of the dynamics of the equilibrium price, the relations are immediate. (iv) Direct consequence of the initial condition on the controls and on the price.

A.3 Computations for the MSR-like mechanism

In our MSR-like mechanism, allocations consists of initial endowment plus net allocation rate of mean-reverting type:

| (A.17) |

The goal is finding to ensure an expected emissions reduction to a factor . From Section 5.1, we know that

| (A.18) |

to ensure the desired reduction. The dynamics of the average bank account verifies

| (A.19) |

where we used the expression of the abatement effort rates given by (4.11) and the market clearing condition. The solution is

| (A.20) |

Exploiting martingality of ,

We now solve for the equilibrium price corresponding to the MSR-like allocation. According to Proposition 4.1 (1),

The residual expected allocation is

Using the solution of the dynamics of (A.20), we have that

Thus, we have:

which we rewrite as

Hence, solving for gives

Thus, under this MSR-like mechanism, the market equilibrium follows the dynamics:

| (A.22) | ||||

| (A.23) |

with given by (A.21).

References

- [1] K. S. Anand, F. C. Giraud-Carier. Pollution Regulation of Competitive Markets. Management Science, 66(9):4193-4206, 2020.

- [2] M. Auffhammer. Quantifying economic damages from climate change. J. of Economic Perspectives, 32(4):33-52, 2018.

- [3] A. Bensoussan, S. Chen, S. P. Sethi. Feedback Stackelberg solutions of infinite-horizon stochastic differential games. Models and Methods in Economics and Management Science, F. El Ouardighi and K. Kogan (eds.), International Series in Operations Research & Management Science 198, 2014.

- [4] C. Chaton, A. Creti, B. Peluchon. Banking and back-loading emission permits. Energy Policy, 82:332-341, 2015.

- [5] R. Carmona, M. Fehr. Risk-neutral models for emission allowance prices and option valuation. Management Science, 57(8):1453-1468, 2011.

- [6] R. Carmona, M. Fehr, J. Hinz. Optimal stochastic control and carbon price formation. SIAM J. on Control and Optimisation, 48(4):2168-2190, 2009.

- [7] R. Carmona, M. Fehr, J. Hinz, A. Porchet. Market design for emission trading schemes. SIAM Review, 52(3):403-452, 2010.

- [8] R. Carmona, F. Delarue, G.-E. Espinosa, N. Touzi. Singular forward-backward stochastic differential equations and emissions derivatives. Ann. of Applied Probabilities, 23(3):1086-1128, 2013.

- [9] Darrell Duffie. Dynamic Asset Pricing Theory. Princeton University Press, 3rd ed., 2001.

- [10] P. Falbo, J. Hinz. Risk aversion in modeling of cap-and-trade mechanism and optimal design of emission markets. Stochastics of Environmental and Financial Economics, F.E. Benth and G. Di Nunno (eds.), Springer Proceedings in Mathematics and Statistics 138, 2014.

- [11] H. Fell, R. D. Morgenstern. Alternative Approaches to Cost Containment in a Cap-and-Trade System. Environmental and Ressource Economics, 47:275-297, 2010.

- [12] H. Fell, D. Burtraw, R. D. Morgenstern, K. L. Palmer. Soft and hard price collars in a cap-and-trade system: A comparative analysis. J. of Environmental Economics and Management, 64:183-198, 2012.

- [13] A. Frino, J. Kruk, A. Lepone. Liquidity and transaction costs in the European carbon futures market. J. Deriv. and Hedge Funds, 16(2):100-115, 2010.

- [14] K Gillingham, J. H. Stock. Quantiffying economic damages from climate change. J. of Economic Perspectives, 32(4):53-72, 2018.

- [15] C. Gollier. The cost–efficiency carbon pricing puzzle. Toulouse School of Economics Working Paper, 18–952, 2020.

- [16] G. Grüll, L. Taschini. Cap-and-trade properties under different hybrid scheme designs. J. of Environmental Economics and Management, 61:107-118, 2011.

- [17] R. W. Hahn. Economic prescriptions for environmental problems: How the patient followed the doctor’s orders. J. of Economic Perspective, 3(2):95-114, 1989.

- [18] C. Hepburn. Regulation by prices, quantities, or both: a review of instrument choice. Oxford Review of Economic Policy, 22(2):226-247, 2006.

- [19] S. Hsiang, R. E. Kopp. An economist’s guide to climate change science. J. of Economic Perspectives, 32(4):3-32, 2018.

- [20] E. Keeler, M. Spence, R. Zeckhauser. The optimal control of pollution. J. of Economic Theory, 4:19-34, 1971.

- [21] S. Kollenberg, L. Taschini. Emissions trading systems with cap adjustments. J. of Environmental Economics and Management, 80:20-36, 2016.

- [22] S. Kollenberg, L. Taschini. Dynamic supply adjustment and banking under uncertainty in an emission trading scheme: The market stability reserve. European Economic Review, 118:213-236, 2019.

- [23] O.-P. Kuusela, J. Lintunen. A Cap-and-Trade Commitment Policy with Allowance Banking. Environmental and Resource Economics, 75:421-455, 2020.

- [24] A. S. Kyle. Continuous auctions and insider trading. Econometrica, 53(6):1315-1336, 1985.

- [25] J. Lintunen, O.-P. Kuusela. Business cycles and emission trading with banking. European Economic Review, 101:397-417, 2018.

- [26] W. D. Montgomery. Markets in licences and efficient pollution control programs. J. of Economic Theory, 5:395-418, 1972.

- [27] J. Morris, S. Paltsev, J. Reilly. Marginal abatement costs and marginal welfare costs for greenhouse gas emissions reductions: Results from the EPPA model. Environmental Modeling and Assessment, 17:325-336, 2012.

- [28] N. Z. Muller, R. Mendelsohn. Efficient pollution control: Getting the prices right. American Economic Review, 99(5):1714-1739, 2009.

- [29] W. A. Pizer. Combining price and quantity controls to mitigate global climate change. J. of Public Economics, 85:409-434, 2002.

- [30] W. A. Pizer, B. Prest. Prices versus quantities with policy updating. J. of the Association of Environmental and Resource Economists, 7(3):483-518, 2020.

- [31] T. Requate. Pollution control in a Cournot duopoly via taxes and permits. J. of Economics, 58(3):255-291, 1993.

- [32] M. J. Roberts, M. Spence. Effluent charges and licenses under uncertainty. J. of Public Economics, 5:193-208, 1976.

- [33] J. D. Rubin. A model of intertemporal emission trading, banking, and borrowing. J. of Environmental Economics and Management, 31:269-286, 1996.

- [34] S. Schennach. The economics of pollution permit banking in the context of title IV of the 1990 clean air act amendments. J. of Environmental Economics and Management, 40:189-210, 2000.

- [35] D. F. Spulber. Effluent regulation and long-run optimality. J. of Environmental Economics and Management, 12:103-116, 1985.

- [36] N. Von der Fehr. Tradable emission rights and strategic interaction. Environmental Resource Economics, 3(2):129–151, 1993.

- [37] M. L. Weitzman. Prices vs. quantities. Review of Economic Studies, 41(4):683-691, 1974.