Modeling Price Clustering in High-Frequency Prices

Vladimír Holý

Prague University of Economics and Business

Winston Churchill Square 4, 130 67 Prague 3, Czech Republic

Corresponding Author

Petra Tomanová

Prague University of Economics and Business

Winston Churchill Square 4, 130 67 Prague 3, Czech Republic

March 16, 2024

Abstract:

The price clustering phenomenon manifesting itself as an increased occurrence of specific prices is widely observed and well-documented for various financial instruments and markets. In the literature, however, it is rarely incorporated into price models. We consider that there are several types of agents trading only in specific multiples of the tick size resulting in an increased occurrence of these multiples in prices. For example, stocks on the NYSE and NASDAQ exchanges are traded with precision to one cent but multiples of five cents and ten cents occur much more often in prices. To capture this behavior, we propose a discrete price model based on a mixture of double Poisson distributions with dynamic volatility and dynamic proportions of agent types. The model is estimated by the maximum likelihood method. In an empirical study of DJIA stocks, we find that higher instantaneous volatility leads to weaker price clustering at the ultra-high frequency. This is in sharp contrast with results at low frequencies which show that daily realized volatility has a positive impact on price clustering.

Keywords:

High-Frequency Data, Price Clustering, Generalized Autoregressive Score Model, Double Poisson Distribution.

JEL Codes:

C22, C46, C58.

1 Introduction

Over the last two decades, there has been a growing interest in modeling prices at the highest possible frequency which reaches fractions of a second for the most traded assets. The so-called ultra-high-frequency data possess many unique characteristics which need to be accounted for by econometricians. Notably, the prices are irregularly spaced with discrete values. Other empirical properties of high-frequency prices which can be incorporated into models include intraday seasonality, jumps in prices, price reversal and the market microstructure noise. For related models, see, e.g. Russell and Engle (2005), Robert and Rosenbaum (2011), Barndorff-Nielsen et al. (2012), Shephard and Yang (2017), Koopman et al. (2017), Koopman et al. (2018) and Buccheri et al. (2020).

We focus on one particular empirical phenomenon observed in high-frequency prices – price clustering. In general, price clustering refers to an increased occurence of some values in prices. A notable type of price clustering is an increased occurrence of specific multiples of the tick size, i.e. the minimum price change. For example, on the NYSE and NASDAQ exchanges, stocks are traded with precision to one cent but multiples of five cents (nickels) and ten cents (dimes) tend to occur much more often in prices. In other words, while one would expect the distribution of the second digit to be uniform, the probability of 0 and 5 is actually higher than 0.1 for each. This behavior can be captured by some agents trading only in multiples of five cents and some only in multiples of ten cents. It is well documented in the literature that this type of price clustering is present in stock markets (see, e.g. Lien et al., 2019), commodity markets (see, e.g. Bharati et al., 2012), foreign exchange markets (see, e.g. Sopranzetti and Datar, 2002) and cryptocurrency markets (see, e.g. Urquhart, 2017). Moreover, price clustering does not appear only in spot prices but in futures (see, e.g. Schwartz et al., 2004), options (see, e.g. ap Gwilym and Verousis, 2013) and swaps (see, e.g. Liu and Witte, 2013) as well. From a methodological point of view, almost all papers on price clustering deal only with basic methods and descriptive statistics of the phenomenon. The only paper, to our knowledge, that incorporates price clustering into a price model is the recent theoretical study of Song et al. (2020) which introduced the sticky double exponential jump diffusion process to assess the impact of price clustering on the probability of default.

Our goal is to propose a discrete dynamic model relating price clustering to the distribution of prices and to study the high-frequency behavior of price clustering. We take a fundamentally very different approach than Song et al. (2020) and incorporate the mechanism of an increased occurrence of specific multiples of the tick size directly into the model. This allows us to treat the price clustering phenomenon as dynamic and driven by specified factors rather than given. We also operate within the time series framework rather than the theory of continuous-time stochastic processes. In contrast to the existing literature on price modeling, we do not model log returns or price differences but rather prices themselves. Prices are naturally discrete and positive. When represented as integers, they also exhibit underdispersion, i.e. the variance lower than the mean. To accommodate for such features, we utilize the double Poisson distribution of Efron (1986). It is a less known distribution as noted by Sellers and Morris (2017) but was utilized in the context of time series by Heinen (2003), Xu et al. (2012) and Bourguignon et al. (2019). Modeling prices directly enables us to incorporate price clustering in the model. Specifically, we consider that prices follow a mixture of several double Poisson distributions with specific supports corresponding to agents trading in different multiples of the tick size. This mixture distribution has a location parameter, a dispersion parameter and parameters determining portions of trader types. In our model, we introduce time variation to all these parameters. We consider the location parameter to be equal to the last observed price resulting in zero expected returns. For the dispersion parameter, we employ dynamics in the fashion of the generalized autoregressive conditional heteroskedasticity (GARCH) model of Bollerslev (1986). Specifically, we utilize the class of generalized autoregressive score (GAS) models of Creal et al. (2013) and Harvey (2013) which allows to base dynamic models on any underlying distribution. In the high-frequency literature, the GAS framework was utilized by Koopman et al. (2018) for discrete price changes and Buccheri et al. (2020) for log prices. To account for irregularly spaced observations, we include the last trade duration as an explanatory variable similarly to Engle (2000). Finally, we relate the trader portion parameters to the volatility process and other variables such as the price, the last trade duration and the volume. The resulting observation-driven model is estimated by the maximum likelihood method.

In the empirical study, we analyze 30 Dow Jones Industrial Average (DJIA) stocks in the first half of 2020. We first focus on price clustering from a daily perspective which is a common approach in the price clustering literature. Using a panel regression with fixed effects, we find a positive effect of daily volatility measured by realized kernels of Barndorff-Nielsen et al. (2008) on price clustering. This finding is in line with the results of ap Gwilym et al. (1998); Davis et al. (2014); Box and Griffith (2016); Hu et al. (2017); Blau (2019); Lien et al. (2019) among others. Next, we estimate the proposed high-frequency price model and arrive at a different conclusion – the instantaneous volatility obtained by the model has a negative effect on price clustering. The main message of the empirical study is therefore that the degree of aggregation plays a pivotal role in the relation between price clustering and volatility. While high daily realized volatility correlates with high price clustering, high instantaneous volatility has the opposite effect. The other explanatory variables have the expected effect in both the daily and high-frequency cases – the volume has a positive effect on price clustering while the price and the last trade duration are insignificant.

The rest of the paper is structured as follows. In Section 2, we review the literature dealing with high-frequency price models and price clustering. In Section 3, we propose the dynamic model accommodating for price clustering based on the double Poisson distribution. In Section 4, we use this model to study determinants of price clustering in high-frequency stock prices. We conclude the paper in Section 5.

2 Literature Review

2.1 Some High-Frequency Price Models

In the literature, several models addressing specifics of ultra-high-frequency data have been proposed. One of the key issues is irregularly spaced transactions and discreteness of prices. The seminal study of Engle and Russell (1998) proposed the autoregressive conditional duration (ACD) model to capture the autocorrelation structure of trade durations, i.e. times between consecutive trades. Engle (2000) combined the ACD model with the GARCH model and jointly modeled prices with trade durations. Russell and Engle (2005) again modeled prices jointly with trade durations but addressed discreteness of prices and utilized the multinomial distribution for price changes.

Another approach is to model the price process in continuous time. Robert and Rosenbaum (2011) considered that the latent efficient price is a continuous Itô semimartingale but is observed at the discrete grid through the mechanism of uncertainty zones. Barndorff-Nielsen et al. (2012) considered the price process to be discrete outright and developed a continuous-time integer-valued Lévy process suitable for ultra-high-frequency data. Shephard and Yang (2017) also utilized integer-valued Lévy processes and focused on frequent and quick reversal of prices.

Transaction data at a fixed frequency can also be analyzed as equally spaced time series with missing observations. In this setting, Koopman et al. (2017) proposed a state space model with dynamic volatility and captured discrete price changes by the Skellam distribution. Koopman et al. (2018) continued with this approach and modeled dependence between discrete stock price changes using a discrete copula. Buccheri et al. (2020) also dealt with multivariate analysis and proposed a model for log prices accommodating for asynchronous trading and the market microstructure noise. The latter two papers utilized the GAS framework.

2.2 Price Clustering

The first academic paper on price clustering was written by Osborne (1962), where the author described the price clustering phenomenon as a pronounced tendency for prices to cluster on whole numbers, halves, quarters, and odd one-eighths in descending preference, like the markings on a ruler. Since then, there have been many studies focusing on this phenomenon – from Niederhoffer (1965) to very recent papers of Li et al. (2020), Song et al. (2020), and Das and Kadapakkam (2020) – showing that price clustering is remarkably persistent in time and across various markets.

Song et al. (2020) pointed out that, however, all studies are entirely focused on empirically examining price clustering in different financial markets. Except for the purely theoretical paper of Song et al. (2020) proposing the sticky double exponential jump-diffusion process to analyze the probability of default for financial variables, the studies related to price clustering are based on basic general methods and do not aim to incorporate the phenomenon into the dynamic price model.

The prevalent approach to price clustering examination is a linear regression model estimated by ordinary least squares (OLS) method. Ball et al. (1985), Kandel et al. (2001), and from the recent literature Urquhart (2017), Hu et al. (2019) and Li et al. (2020), used the classical regression with dummy variables to estimate frequency of each level of rounding. The vast of the literature regressed price clustering on explanatory variables such as volatility and trade size, where price clustering is defined as the excess occurrence of multiples of nickles or dimes (see, e.g. Schwartz et al., 2004 and Ikenberry and Weston, 2008 followed by Chung and Chiang, 2006, Brooks et al., 2013, and Hu et al., 2017) or simply their frequency (see, e.g. Palao and Pardo, 2012 and Davis et al., 2014). However, different definitions of the dependent variable representing price clustering can be found in the literature. Baig et al. (2019) defined the clustering as a sum of round clustering at prices ending by digit 0 and strategic clustering measured as a number of trades which decimals are equal to or . ap Gwilym and Verousis (2013) defined the dependent variable as the percentage of price observations at integers, whereas ap Gwilym et al. (1998) estimated the percentage of trades that occur at an odd tick. Ahn et al. (2005) regressed abnormal even price frequencies in transaction and quote prices on the firm and trading characteristics, and similarly, Chiao and Wang (2009) performed the analysis on the limit-order data. Cooney et al. (2003) estimated cross-sectional regressions of the difference in the percentage of even and odd limit orders on stock price and proxies for investor uncertainty.

Several extensions of the OLS method were employed to overcome certain issues. Verousis and ap Gwilym (2013) and Mishra and Tripathy (2018) argued that one encounters a simultaneity issue between trade size and price clustering when striving to examine a causal relationship between them. Hence, Verousis and ap Gwilym (2013) followed by Mishra and Tripathy (2018) used the two-stage least squares (2SLS) method. Moreover, to reflect the endogeneity of quote clustering in the spread model and the endogeneity of the spread in the quote clustering model, Chung et al. (2004, 2005) estimated a structural model using three-stage least squares (3SLS) method. Meng et al. (2013) used the 3SLS method to formally examine the hypothesis of a substitution effect between price clustering and size clustering in the CDS market. Finally, Mbanga (2019) estimated robust regressions that eliminate gross outliers to examine the day-of-the-week effect in Bitcoin price clustering.

Another direction arises from the need to analyze panel data. The prevailing approach is a fixed effects regression. Das and Kadapakkam (2020) included both firm and time fixed effects, whereas Box and Griffith (2016) included fixed effects only for time and report that once they also included firm fixed effects, the results remained unchanged. Blau, 2019 and Blau and Griffith (2016) included month and year fixed effects respectively, and used robust standard errors that account for clustering across both the cross-sectional observations and time-series observations. On the other hand, Ohta (2006) picked random effects model over the fixed effects model based on the results from the Hausman specification test.

A substantial part of the literature models price clustering as a binary variable. For that case, the straightforward approach is to use the logit or probit model. From one of the first papers using logistic regression to analyze price clustering, Ball et al. (1985) modeled three dependent variables taking value 1 if the price is rounded to the whole dollar, half-dollar, or quarter, respectively. Christie and Schultz (1994) estimated logistic regressions that predict the probability of a firm being quoted using odd eighths. Aitken et al. (1996) employed multivariate logistic regression to model three binary dependent variables that are equal to one if the final digit is 0; 0 or 5; and 0, 2, 4, 6, or 8 (even numbers), respectively. Brown and Mitchell (2008) examined the influence of Chinese culture on price clustering by logistic regressions where a binary dependent variable is equal to 1 if the last sale price ends in 4 and 0 if it ends in 8 since many Chinese consider the number 8 as lucky while 4 is considered as unlucky. From the literature employing probit models, Kahn et al. (1999) analyzed the propensity to set retail deposit interest rates at integer levels and Sopranzetti and Datar (2002) analyzed the propensity for exchange rates to cluster on even digits. Moreover, Capelle-Blancard and Chaudhury (2007) models a binary dependent variable that is equal to one if the transaction price ends with , whereas Liu (2011) and Narayan and Smyth (2013) set the variable equal to one if the price ends at either 0 or 5, and 0 otherwise. Alexander and Peterson (2007) followed by Lien et al. (2019) used a bivariate probit model to take into account the dependence between price and trade-size clustering.

Finally, Blau (2019) estimated a vector autoregressive process and examined the impulses of price clustering in response to an exogenous shock to investor sentiment. Besides the classical regression approaches, Harris (1991) and Hameed and Terry (1998) analyzed the cross-sectional data by static discrete price model.

To the best of our knowledge, the literature still lacks a discrete dynamic model to study the high-frequency behavior of the price clustering. Thus, in the next section, we propose a novel model which models high-frequency prices directly at the highest possible frequency and allows us to study the main drivers of price clustering such as price, volatility, volume, and trading frequency in the form of trade durations.

3 Dynamic Price Clustering Model

3.1 Double Poisson Distribution

Let us start with the static version of our model for prices. In the first step, we transform the observed prices to have integer values. For example, on the NYSE and NASDAQ exchanges, the prices are recorded with precision to two decimal places and we therefore multiply them by 100 to obtain integer values. The minimum possible change in the transformed prices is 1. Empirically, the transformed prices exhibit strong underdispersion, i.e. the variance lower than the mean. In our application, the transformed prices are in the order of thousands and tens of thousands while the price changes are in the order of units and tens. We therefore need to base our model on a count distribution allowing for underdispersion. For a review of such distributions, we refer to Sellers and Morris (2017). Although not without its limitations, the double Poisson distribution is the best candidate for our case as the alternative distributions have too many shortcomings. For example, the condensed Poisson distribution is based on only one parameter, the generalized Poisson distribution can handle only limited underdispersion and the gamma count distribution as well as the Conway–Maxwell–Poisson distribution do not have the moments available in a closed form.

The double Poisson distribution was proposed in Efron (1986) and has a location parameter and a dispersion parameter . We adopt a slightly different parametrization than Efron (1986) and use the logarithmic transformation for the dispersion parameter making unrestricted. For , the distribution reduces to the Poisson distribution. Values result in underdispersion while values result in overdispersion. Let be a random variable and an observed value. The probability mass function is given by

| (1) |

where is the normalizing constant given by

| (2) |

The log likelihood for observation is then given by

| (3) |

Unfortunately, the normalizing constant is not available in a closed form. However, as Efron (1986) shows, it is very close to 1 (at least for some combinations of and ) and can be approximated by

| (4) |

Zou et al. (2013) notes that approximation (4) is not very accurate for low values of the mean and suggest approximating the normalizing constant alternatively by cutting off the infinite sum, i.e.

| (5) |

where should be at least twice as large as the sample mean. In our case of high mean, approximation (4) is sufficient while approximation (5) would be computationally very demanding and we therefore resort to the former one. The expected value and variance can be approximated by

| (6) |

The score can be approximated by

| (7) |

The Fisher information can be approximated by

| (8) |

3.2 Mixture Distribution for Price Clustering

Next, we propose a mixture of several double Poisson distributions corresponding to trading in different multiples of tick sizes accommodating for price clustering. We consider that there are three types of traders – one who can trade in cents, one who can trade only in multiples of 5 cents and one who can trade only in multiples of 10 cents. In Appendix A, we treat a more general case with any number of trader types and tick size multiples. The distribution of prices corresponding to each trader type is based on the double Poisson distribution modified to have support consisting only of multiples of while keeping the expected value and the variance regardless of . For a detailed derivation of the distribution, see Appendix A. The distribution of prices for trader type is given by

| (9) |

where denotes the double Poisson distribution and is equal to 1 if is divisible by and 0 otherwise. Note that for , it is the standard double Poisson distribution. Finally, the distribution of all prices is the mixture

| (10) |

where the parameter space is restricted by , , , and . Parameters , , are the portions of trader types and parameters with have the same interpretation as in the double Poisson distribution. The log likelihood for observation is given by

| (11) | ||||

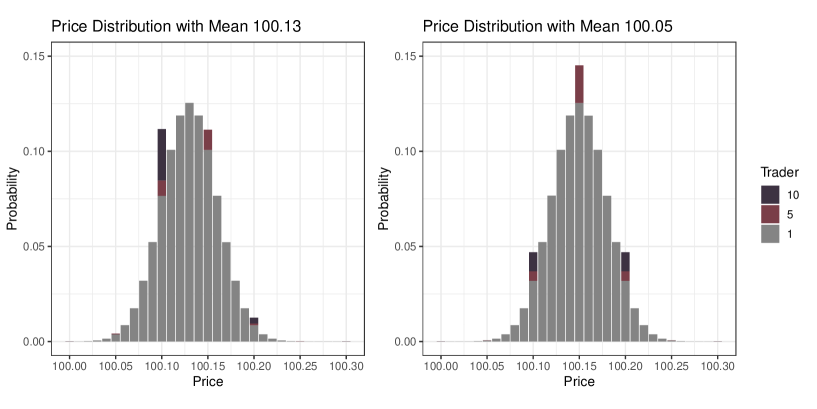

Note that the last logarithm in (11) is not dependent on parameters and besides the normalizing constant making the approximation of the score quite simple. Additionaly, parameters , and appear only in the last logarithm in (11) making the approximation of the score for parameters and independent of parameters , and . The approximations of the expected value and the variance as well as the score and the Fisher information for the parameters and of the mixture distribution are therefore the same as for the regular double Poisson distribution presented in (6), (7) and (8) respectively when assuming . Figure 1 illustrates the probability mass function of the mixture distribution.

3.3 Dynamics of Time-Varying Parameters

Finally, we introduce time variation into parameters . We denote the random prices as , and the observed values as , . We also utilize observed trade durations , and observed volumes , . We assume that follow the mixture double Poisson distribution proposed in Section 3.2 with time-varying parameters , , , and . The dynamics of the location parameter is given by

| (12) |

This means that the expected value of the price is (approximately) equal to the last observed price, i.e. the expected value of the return is zero. This is a common assumption for high-frequency returns (see, e.g. Koopman et al., 2017).

For the dynamics of the dispersion parameter , we utilize the generalized autoregressive score (GAS) model of Creal et al. (2013), also known as the dynamic conditional score (DCS) model by Harvey (2013). The GAS model is an observation-driven model providing a general framework for modeling time-varying parameters for any underlying probability distribution. It captures dynamics of time-varying parameters by the autoregressive term and the score of the conditional density function. Blasques et al. (2015) investigated information-theoretic optimality properties of the score function and showed that only parameter updates based on the score will always reduce the local Kullback–Leibler divergence between the true conditional density and the model-implied conditional density. Creal et al. (2013) suggested to scale the score based on the Fisher information. As the Fisher information for the parameter is constant in our case, the score is already normalized and we therefore omit the scaling. Using (7) and (12), we let the dispersion parameter follow the recursion

| (13) |

where is the constant parameter, is the autoregressive parameter, is the score parameter and is the duration parameter. This volatility dynamics corresponds to the generalized autoregressive conditional heteroskedasticity (GARCH) model of Bollerslev (1986). Similarly to Engle (2000), we also include the preceding trade duration as an explanatory variable to account for irregularly spaced observations. To prevent extreme values of durations, we use the logarithmic transformation.

The portions of trader types are driven by process

| (14) |

where is the autoregressive parameter, is the parameter for the logarithm of the expected price, is the parameter for the logarithm of the variance of the price process , is the parameter for the logarithm of the preceding trade duration, and is the parameter for the logarithm of the volume . The portions of trader types are then standardized as

| (15) |

where and are parameters capturing representation of 5 and 10 trader types. The model can be straightforwardly extended to include additional explanatory variables in (13) and (14).

3.4 Maximum Likelihood Estimation

The proposed model based on the mixture distribution for price clustering (10) with dynamics given by (12), (13) and (15) can be straightforwardly estimated by the conditional maximum likelihood method. Let denote the static vector of all parameters. The parameter vector is then estimated by the conditional maximum likelihood

| (16) |

where is given by (11).

For the numerical optimization in the empirical study, we utilize the PRincipal AXIS algorithm of Brent (1972). To improve numerical performance, we standardize the explanatory variables to unit mean. We also run the estimation procedure several times with different starting values to avoid local maxima.

4 Empirical Results

4.1 Data Sample

The empirical study is conducted on transaction data extracted from the NYSE TAQ database which contains intraday data for all securities listed on the New York Stock Exchange (NYSE), American Stock Exchange (AMEX), and Nasdaq Stock Market (NASDAQ). We analyze 30 stocks that form the Dow Jones Industrial Average (DJIA) index in June 2020. The extracted data span over six months from January 2 to June 30, 2020, except for Raytheon Technologies (RTX)111The RTX company results from the merge of the United Technologies Corporation and the Raytheon Company on April 3, 2020. for which the data are available from April 3, 2020.

We follow the standard cleaning procedure for the NYSE TAQ dataset described in Barndorff-Nielsen et al. (2009) since data cleaning is an important step of high-frequency data analysis (Hansen and Lunde, 2006). Before the standard data pre-processing is conducted, we delete entries that are identified as preferred or warrants (trades with the non-empty suffix indicator). Then we follow a common data cleaning steps and discard (i) entries outside the main opening hours (9:30 – 16:00), (ii) entries with the transaction price equal to zero, (iii) entries occurring on a different exchange than it is primarily listed, (iv) entries with corrected trades, (v) entries with abnormal sale condition, (vi) entries for which the price deviated by more than 10 mean absolute deviations from a rolling centered median of 50 observations, and (vi) duplicate entries in terms of the time stamp. In the last step, we remain the entry with mode price instead of the originally suggested median price due to avoiding distortion of the last decimal digit of prices.

The first and last step has a negligible impact on our data and steps ii, iv, and vi have no impact at all. However, the third step causes a large deletion of the data which is, however, in line with Barndorff-Nielsen et al. (2009). The basic descriptive statistics after data pre-processing are shown in Appendix B. Number of observations ranges from (TRV) to (MSFT). Price clustering in terms of the excess occurrence of multiples of five cents and ten cents in prices ranges from 1.45 % (KO) to 11.52 % (BA). First, we analyze the price clustering using a common approach of fixed effects model on daily data in Section 4.2 to investigate whether the results for our dataset are in line with the existing literature. Then, we estimate the proposed dynamic price model in Section 4.3.

4.2 Analysis Based on Daily Data

In this section, we investigate the main determinants of price clustering for which pervasive evidence is documented in the literature, namely price, volatility, trading frequency (which we measure in terms of trade durations), and volume. We use a panel regression with fixed effects to take into account the unobserved heterogeneity in both dimensions – stocks and days.

Let us define price clustering as the excess relative frequency of multiples of five cents and ten cents in prices of stock at day . We model as

| (17) |

where is a stock specific effect for the stock , is a time effect for day , and is the error term. Parameters – corresponds to logarithmic explanatory variables, where is an average price, is an average duration and is an average volume, where all averages are calculated for each stock at each day . Daily volatility is estimated by realized kernel estimator of Barndorff-Nielsen et al. (2008). We use Parzen kernel as suggested by Barndorff-Nielsen et al. (2009). See Holý and Tomanová (2021) for a comprehensive overview of quadratic covariation estimators.

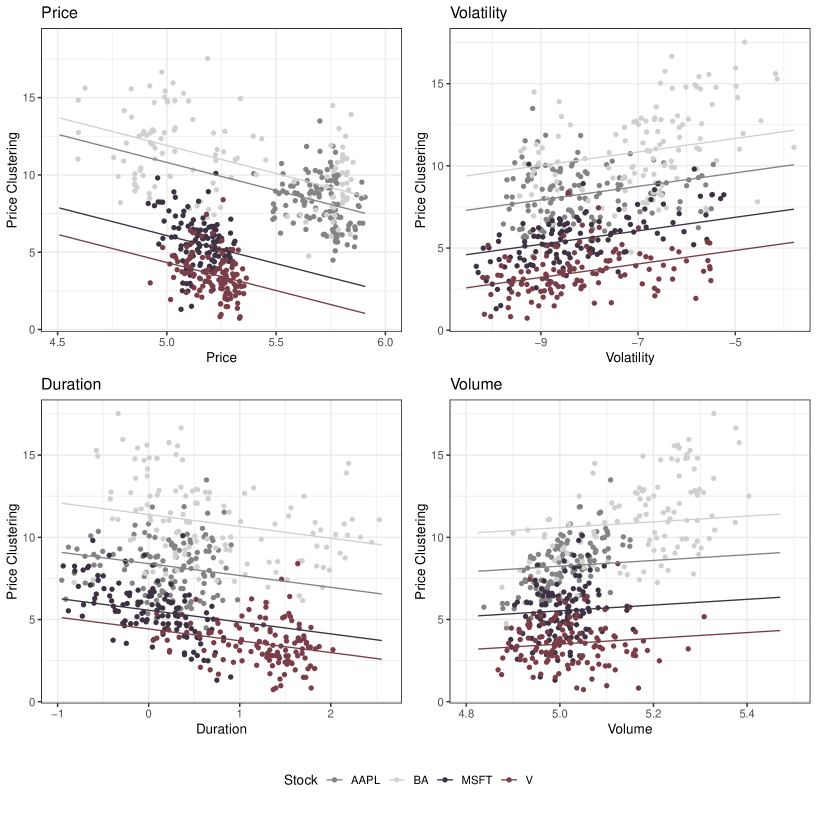

Table 1 reports estimated coefficients of three variants of the fixed effects model. The first variant models price clustering on price, volatility and duration, i.e. model in (17) where volume is skipped. The second model considers only the price, duration and volume as the explanatory variables, and the third one is the full model in (17). We test the significance of the estimated coefficients using robust standard errors for which observations are clustered in both dimensions to account for serial as well as cross-sectional correlation. The results show that only volatility and volume are significant drivers of the price clustering in the full model (Model III). However, once the volatility is dropped from the model, the average daily duration becomes highly significant (Model II). A similar result applies for the price (Model I) which becomes highly significant once the volume is dropped from the full model. For illustration, Figure 2 shows fitted lines from univariate regressions with stock specific effects222Time effects are dropped for better visibility which does not alter the main result. for two stocks traded on NASDAQ – Apple Inc. (AAPL) and Microsoft (MSFT) – and two stocks traded on NYSE – Boeing (BA) and Visa Inc. (V).

| Variable | I | II | III |

|---|---|---|---|

| price | |||

| volatility | |||

| duration | |||

| volume | |||

| ∗p0.05; ∗∗p0.01; ∗∗∗p0.001 | |||

4.3 High-Frequency Analysis

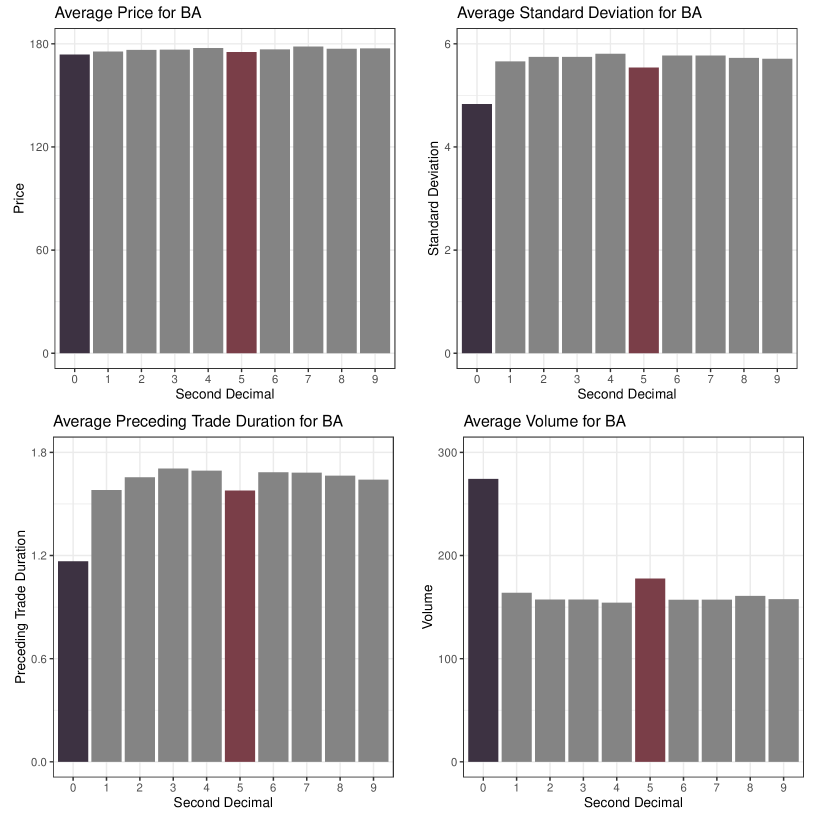

Let us analyze the price clustering phenomenon at the highest possible frequency. First, we take a brief look at the relation between the individual explanatory variables and price clustering. We focus on the BA stock as its price clustering is the most pronounced. Figure 3 shows the average expected price, the average instantaneous variance obtained from the dynamic model, the average duration preceding the trade, and the average volume broken down by the second decimal of the price for the BA stock. We can clearly see that for prices ending with 0 and 5, the average variance and the average trade duration is much lower than for the other digits while the average volume is much higher. Note that succeeding durations show very similar behavior to preceding durations suggesting that price clustering tends to occur when trading is more intense.

Next, we estimate three versions of the proposed price clustering model for each of the 30 stocks. In the first version, we assume that there is no price clustering and set . In the second version, we set only and assume that there is price clustering present but is constant over time and does not depend on any variables. The third version is the dynamic model presented in Section 3.3 without any restrictions. We report the average log-likelihood and the Akaike information criterion (AIC) of the models in Table 2. We can see that adding price clustering to the model and subsequently adding dynamics to price clustering is very much worth of the extra few parameters as AIC is distinctly the lowest for the dynamic model for all stocks.

From now on we focus on the model with dynamic price clustering. Table 3 reports the estimated coefficients. For all stocks, the coefficients in the volatility process , , , and have the same signs and fairly similar values demonstrating the robustness of the model. Parameter is negative, which means that with longer durations, dispersion parameter is lower and the instantaneous variance is higher. We attribute this behavior to the presence of a large amount of extremely short durations associated with small price changes. Note that for example, the BA stock has 50 percent of durations shorter than 0.1 seconds and 19 percent shorter than 0.0001 seconds. Engle (2000) observed the opposite relation between trade durations and volatility but based his results on data with a much lower frequency and without durations shorter than 1 second. This might indicate a change in the data structure over the years and a complex non-linear relation between trade durations and volatility. This topic is, however, beyond the scope of this paper.

Regarding the dynamics of price clustering, the autoregressive parameter is stable across all stocks. The parameter for the expected price significantly varies for different stocks suggesting its low informative value. This is in line with the daily analysis in which prices were found insignificant. The parameter for the instantaneous variance is positive for all stocks. The portion of one cent traders is therefore higher with higher variance and price clustering tends to occur when prices are less volatile. This is the most interesting result as it deviates from the behavior observed in the daily analysis. The parameter for the preceding trade duration significantly varies for different stocks, similarly to . When the preceding trade duration is the only explanatory variable included in the model, however, is positive for all stocks. Recall that durations have a positive effect on instantaneous variance as is positive for all stocks. This implies that durations have an effect on instantaneous variance which in turn has an effect on price clustering. However, when controlling for instantaneous variance, durations do not bring additional information to explain price clustering. These observations are in line with the daily analysis. Finally, the parameter for the volume is negative for all stocks. As in the daily analysis, higher volume is clearly associated with higher price clustering.

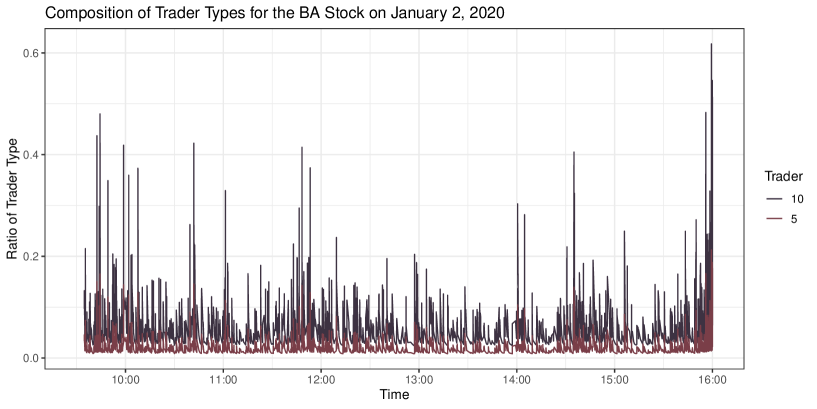

We omit parameters and controlling strength of price clustering from Table 3 as they are not very informative for readers. It is far better to look at the average values of trader portions , and reported in Table 4. The average portion of ten-cent traders ranges from 0.48 percent for the TRV stock to 10.54 percent for the BA stock. The average portion of five-cent traders ranges from 0.34 percent for the TRV stock to 3.63 percent for the BA stock. An example of the progression of trader type ratios is shown in Figure 4 for the BA stock on the first trading day of 2020.

| No PC | Static PC | Dynamic PC | ||||

|---|---|---|---|---|---|---|

| Stock | Lik. | AIC | Lik. | AIC | Lik. | AIC |

| AAPL | -2.3548 | -2.3292 | -2.2953 | |||

| AXP | -2.5117 | -2.5054 | -2.5008 | |||

| BA | -2.8677 | -2.8146 | -2.7980 | |||

| CAT | -2.6144 | -2.6090 | -2.6066 | |||

| CSCO | -0.4650 | -0.4636 | -0.4606 | |||

| CVX | -2.1513 | -2.1476 | -2.1444 | |||

| DIS | -2.1382 | -2.1295 | -2.1231 | |||

| DOW | -1.6701 | -1.6685 | -1.6668 | |||

| GS | -3.1560 | -3.1500 | -3.1460 | |||

| HD | -3.1018 | -3.0969 | -3.0935 | |||

| IBM | -2.4432 | -2.4393 | -2.4360 | |||

| INTC | -0.8455 | -0.8442 | -0.8407 | |||

| JNJ | -2.3836 | -2.3809 | -2.3794 | |||

| JPM | -2.0310 | -2.0264 | -2.0220 | |||

| KO | -1.2238 | -1.2230 | -1.2212 | |||

| MCD | -2.9611 | -2.9563 | -2.9526 | |||

| MMM | -2.7229 | -2.7180 | -2.7149 | |||

| MRK | -1.7024 | -1.7011 | -1.6998 | |||

| MSFT | -1.7431 | -1.7315 | -1.7096 | |||

| NKE | -2.1331 | -2.1310 | -2.1292 | |||

| PFE | -0.8423 | -0.8415 | -0.8398 | |||

| PG | -2.3049 | -2.3024 | -2.3007 | |||

| RTX | -1.7279 | -1.7238 | -1.7207 | |||

| TRV | -2.7871 | -2.7861 | -2.7848 | |||

| UNH | -3.3882 | -3.3834 | -3.3816 | |||

| V | -2.6542 | -2.6485 | -2.6434 | |||

| VZ | -1.3165 | -1.3156 | -1.3141 | |||

| WBA | -1.1807 | -1.1787 | -1.1748 | |||

| WMT | -2.1291 | -2.1262 | -2.1233 | |||

| XOM | -1.1969 | -1.1951 | -1.1895 | |||

| Stock | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| AAPL | 6.09 | 0.08 | 0.29 | -0.40 | 0.66 | -0.33 | 0.61 | -0.11 | -0.69 |

| AXP | 5.32 | 0.10 | 0.35 | -0.28 | 0.34 | 1.05 | 0.05 | 0.06 | -0.74 |

| BA | 5.00 | 0.09 | 0.30 | -0.29 | 0.39 | -0.14 | 0.18 | 0.03 | -0.71 |

| CAT | 5.60 | 0.04 | 0.26 | -0.27 | 0.25 | -0.28 | 0.29 | -0.00 | -0.71 |

| CSCO | 6.11 | 0.17 | 0.08 | -0.35 | 0.81 | 0.28 | 0.40 | -0.08 | -0.37 |

| CVX | 5.79 | 0.11 | 0.35 | -0.26 | 0.36 | 0.70 | 0.28 | 0.02 | -0.64 |

| DIS | 6.05 | 0.12 | 0.33 | -0.25 | 0.39 | 0.45 | 0.21 | 0.05 | -0.64 |

| DOW | 5.71 | 0.15 | 0.33 | -0.22 | 0.34 | 0.55 | 0.18 | 0.04 | -0.70 |

| GS | 4.89 | 0.05 | 0.27 | -0.31 | 0.29 | 1.06 | 0.12 | 0.02 | -0.90 |

| HD | 5.01 | 0.08 | 0.29 | -0.28 | 0.29 | 0.64 | 0.10 | 0.05 | -0.83 |

| IBM | 5.79 | 0.08 | 0.32 | -0.28 | 0.32 | 0.33 | 0.10 | 0.06 | -0.80 |

| INTC | 6.29 | 0.14 | 0.13 | -0.35 | 0.74 | 0.38 | 0.34 | -0.06 | -0.63 |

| JNJ | 5.76 | 0.13 | 0.40 | -0.25 | 0.23 | 1.12 | 0.08 | 0.05 | -0.74 |

| JPM | 5.76 | 0.17 | 0.44 | -0.26 | 0.33 | 0.48 | 0.67 | -0.07 | -0.56 |

| KO | 5.97 | 0.25 | 0.33 | -0.18 | 0.55 | -0.05 | 0.62 | 0.01 | -0.43 |

| MCD | 5.16 | 0.08 | 0.34 | -0.27 | 0.31 | 1.69 | 0.02 | 0.06 | -0.88 |

| MMM | 5.55 | 0.05 | 0.29 | -0.27 | 0.25 | 0.93 | 0.06 | 0.06 | -0.87 |

| MRK | 5.89 | 0.20 | 0.40 | -0.23 | 0.45 | 0.20 | 0.71 | -0.09 | -0.53 |

| MSFT | 6.37 | 0.11 | 0.27 | -0.38 | 0.72 | 0.17 | 0.39 | -0.05 | -0.72 |

| NKE | 6.01 | 0.10 | 0.35 | -0.25 | 0.29 | 0.45 | 0.05 | 0.08 | -0.70 |

| PFE | 5.19 | 0.38 | 0.28 | -0.15 | 0.70 | 0.36 | 0.34 | 0.03 | -0.33 |

| PG | 5.84 | 0.11 | 0.40 | -0.23 | 0.41 | -0.13 | 1.35 | -0.25 | -0.53 |

| RTX | 6.12 | 0.15 | 0.34 | -0.24 | 0.32 | -0.50 | 0.02 | 0.10 | -0.65 |

| TRV | 5.07 | 0.05 | 0.30 | -0.30 | 0.96 | -0.66 | 0.57 | -0.14 | -0.02 |

| UNH | 4.58 | 0.07 | 0.28 | -0.27 | 0.39 | 0.08 | 0.11 | 0.03 | -0.73 |

| V | 5.91 | 0.06 | 0.32 | -0.27 | 0.32 | 0.65 | 0.09 | 0.06 | -0.91 |

| VZ | 5.79 | 0.27 | 0.38 | -0.19 | 0.44 | 2.53 | 0.71 | -0.05 | -0.53 |

| WBA | 5.82 | 0.12 | 0.18 | -0.34 | 0.68 | 0.38 | 0.26 | -0.00 | -0.62 |

| WMT | 6.19 | 0.12 | 0.38 | -0.24 | 0.34 | -2.33 | 0.15 | 0.08 | -0.71 |

| XOM | 6.11 | 0.24 | 0.31 | -0.18 | 0.57 | -0.51 | 0.98 | -0.06 | -0.52 |

| Stock | |||||

|---|---|---|---|---|---|

| AAPL | 291.80 | 8.43 | 92.37 | 0.72 | 6.91 |

| AXP | 98.43 | 7.01 | 95.05 | 1.81 | 3.15 |

| BA | 175.80 | 6.85 | 85.84 | 3.63 | 10.54 |

| CAT | 117.91 | 6.99 | 95.40 | 1.85 | 2.75 |

| CSCO | 42.22 | 10.26 | 98.07 | 0.54 | 1.38 |

| CVX | 88.26 | 7.62 | 96.26 | 1.32 | 2.42 |

| DIS | 112.50 | 7.90 | 94.18 | 2.25 | 3.56 |

| DOW | 36.46 | 7.69 | 97.36 | 1.36 | 1.29 |

| GS | 193.14 | 6.40 | 95.49 | 1.06 | 3.45 |

| HD | 215.44 | 6.63 | 95.72 | 1.44 | 2.84 |

| IBM | 124.05 | 7.38 | 96.01 | 1.64 | 2.34 |

| INTC | 57.72 | 9.82 | 97.83 | 0.65 | 1.52 |

| JNJ | 140.37 | 7.63 | 96.78 | 1.36 | 1.85 |

| JPM | 103.65 | 8.03 | 95.47 | 2.54 | 1.98 |

| KO | 48.33 | 8.88 | 98.29 | 0.67 | 1.04 |

| MCD | 183.86 | 6.74 | 96.12 | 0.72 | 3.16 |

| MMM | 149.92 | 7.02 | 95.87 | 1.17 | 2.96 |

| MRK | 79.28 | 8.43 | 97.69 | 1.23 | 1.08 |

| MSFT | 169.29 | 9.11 | 94.57 | 0.84 | 4.59 |

| NKE | 88.58 | 7.67 | 96.89 | 1.60 | 1.51 |

| PFE | 34.46 | 9.30 | 98.07 | 1.01 | 0.91 |

| PG | 116.41 | 7.61 | 96.82 | 1.87 | 1.31 |

| RTX | 62.28 | 8.13 | 95.83 | 2.06 | 2.11 |

| TRV | 111.57 | 6.59 | 99.18 | 0.34 | 0.48 |

| UNH | 271.73 | 6.29 | 96.01 | 1.08 | 2.91 |

| V | 180.13 | 7.34 | 95.59 | 1.03 | 3.37 |

| VZ | 55.60 | 8.85 | 97.90 | 1.13 | 0.97 |

| WBA | 45.73 | 8.91 | 97.49 | 0.72 | 1.79 |

| WMT | 118.65 | 7.98 | 96.57 | 1.56 | 1.87 |

| XOM | 45.82 | 8.86 | 97.02 | 1.54 | 1.44 |

4.4 Implications

Several hypotheses have been established to explain the price clustering phenomenon. The attraction hypothesis of Goodhart and Curcio (1991) essentially states that there exists a particular preference (basic attraction) for certain numbers, especially for the rounded ones. The negotiation hypothesis of Harris (1991) assumes that traders use discrete price sets to lower the costs of negotiating. Once the set of prices is reduced, the traders reach agreements more easily since the amount of information that must be exchanged between negotiating traders decreases. Christie and Schultz (1994) argued in the collusion hypothesis that the lack of odd-eighth quotes on NASDAQ cannot be explained by the negotiation hypothesis, trading activity, or other variables thought to impact spreads, which suggests that NASDAQ dealers might implicitly collude to maintain wide spreads. However, assessing these hypotheses is out of the scope of our paper. In this section, we focus only on the most studied hypothesis in the literature – the price resolution hypothesis.

The price resolution hypothesis of Ball et al. (1985) considers the source of price clustering to be the uncertainty. It states that when the amount of information in the market is low and the volatility becomes higher, the market participants incline to round their prices, and consequently, the price clustering increases. This hypothesis was confirmed by many studies. The studies found that price clustering increases with volatility using different data and measures. For example, Ahn et al. (2005) computed the volatility as the inverse of the daily return standard deviation, while Ikenberry and Weston (2008) used the standard deviation of returns over the sample period, Box and Griffith (2016) used the standard deviation of 15-minute continuously compounded midpoint returns over the trading day, Schwartz et al. (2004) used the difference in the high and low prices for the day, and Lien et al. (2019) utilized the transitory volatility defined as the coefficient of variation of intraday trade prices. Davis et al. (2014) found that price clustering is positively related to volatility, however, only when a non–high-frequency trading firm provides liquidity. On the contrary to the vast majority of the literature, Blau (2019) reported based on panel regressions that the volatility is negatively related to price clustering, where the volatility is measured as the standard deviation of residual returns obtained from estimating a Fama and French 3-factor model.

Our results from the daily analysis show that the realized volatility is highly significant and positively related to the price clustering. This finding is in line with the price resolution hypothesis. Interestingly, instantaneous volatility obtained from the proposed dynamic price model has a negative effect on price clustering. The results do not contradict since they explore price clustering from different perspectives. The result based on daily data holds for low-frequency traders whose price resolution is influenced by the uncertainty in a negative way, i.e. the higher daily volatility, the higher price clustering. On the other hand, the presence of high-frequency traders is typically associated with increased volatility (see, e.g., Roşu, 2019; Shkilko and Sokolov, 2020; Boehmer et al., 2020). Moreover, high-frequency traders generally do not incline to price rounding (see Davis et al., 2014). Consequently, the higher the instantaneous volatility is, the higher portion of high-frequency traders is, which lowers the price clustering.

5 Conclusion

We have proposed a dynamic price model to capture agents trading in different multiples of the tick size. In the literature, this empirical phenomenon known as price clustering was mostly approached only by basic descriptive statistics rather than a proper price model. By analyzing 30 DJIA stocks from both daily and high-frequency perspectives, we have revealed dissension between the two time scales. While daily realized volatility has a positive effect on price clustering, instantaneous volatility obtained by the proposed model has a negative effect. We argue that volatility on lower frequency affects low-frequency traders through the resolution hypothesis while volatility on higher frequency affects only high-frequency traders who do not tend to price clustering.

We believe the model to be sufficient for its purpose – capturing price clustering and allowing to explain it. For the model to be able to compete with other high-frequency price models, however, it would have to be improved. The main limitation lies in the underlying distribution. We have yet to study how well the double Poisson distribution, which we have used, captures the observed prices. However, due to our specific problem, we require the distribution to be defined on positive integers and allow for underdispersion. The range of possible alternatives is therefore severely limited as it is not a typical situation in count data analysis. Furthermore, the specification of the dynamics could be enhanced. We could include a separate model for durations and we could add a seasonality component to the volatility. One possible direction for the future research is therefore to assess the suitability of the double Poisson distribution for prices, extend the specification of the proposed dynamic model and compare it with various models for price differences.

Concerning the empirical study, our focus has been on the price variance, whether it is daily realized volatility or instantaneous variance. Nevertheless, we have also included the expected price, the preceding trade duration, and the volume as explanatory variables. These are the most common variables in the price clustering literature. However, other factors such as the spread and the investor sentiment could also be considered. In the context of the proposed high-frequency price model, any variable could be straightforwardly included in the price clustering dynamics. Analyzing the effects of these factors is the second possible direction of the future research.

Acknowledgements

Computational resources were supplied by the project "e-Infrastruktura CZ" (e-INFRA LM2018140) provided within the program Projects of Large Research, Development and Innovations Infrastructures.

Funding

This research was supported by the Czech Science Foundation under project 19-02773S, the Internal Grant Agency of the Prague University of Economics and Business under project F4/53/2019, and the Institutional Support Funds for the long-term conceptual development of the Faculty of Informatics, Prague University of Economics and Business.

Appendix A Derivation of Distribution for Specific Trader Types

Let there be types of traders that can trade only in multiples of the tick size respectively. For trader type , we derive the distribution of prices . We require the distribution to be based on the double Poisson distribution, to have the support consisting of multiples of , to have the expected value and to have the variance . We can modify any integer distribution to have support consisting only of multiples of as

| (18) |

where is equal to 1 if is divisible by and 0 otherwise. We assume that follows the double Poisson distribution with parameters and , i.e. . The expected value of is

| (19) | ||||

The variance of is

| (20) | ||||

Our last requirements with lead to the system of equations

| (21) | ||||

with the solution

| (22) |

Everything together gives us the distribution

| (23) |

Note that the mixture distribution of all prices

| (24) |

has approximately the same expected value and variance as the distribution of . This is based on the identity

| (25) | ||||

where is any function satisfying that are the same for all .

Appendix B Descriptive Statistics of Cleaned Data

| Stock | #Trades | Mean P | SD P | Mean D | SD D | PC [%] |

|---|---|---|---|---|---|---|

| AAPL | ||||||

| AXP | ||||||

| BA | ||||||

| CAT | ||||||

| CSCO | ||||||

| CVX | ||||||

| DIS | ||||||

| DOW | ||||||

| GS | ||||||

| HD | ||||||

| IBM | ||||||

| INTC | ||||||

| JNJ | ||||||

| JPM | ||||||

| KO | ||||||

| MCD | ||||||

| MMM | ||||||

| MRK | ||||||

| MSFT | ||||||

| NKE | ||||||

| PFE | ||||||

| PG | ||||||

| RTX | ||||||

| TRV | ||||||

| UNH | ||||||

| V | ||||||

| VZ | ||||||

| WBA | ||||||

| WMT | ||||||

| XOM |

References

- Ahn et al. (2005) Ahn, H.-J., Cai, J., Cheung, Y. L. 2005. Price Clustering on the Limit-Order Book: Evidence from the Stock Exchange of Hong Kong. Journal of Financial Markets. Volume 8. Issue 4. Pages 421–451. ISSN 1386-4181. {https://doi.org/10.1016/j.finmar.2005.07.001}.

- Aitken et al. (1996) Aitken, M., Brown, P., Buckland, C., Izan, H. Y., Walter, T. 1996. Price Clustering on the Australian Stock Exchange. Pacific-Basin Finance Journal. Volume 4. Issue 2-3. Pages 297–314. ISSN 0927-538X. {https://doi.org/10.1016/0927-538x(96)00016-9}.

- Alexander and Peterson (2007) Alexander, G. J., Peterson, M. A. 2007. An Analysis of Trade-Size Clustering and Its Relation to Stealth Trading. Journal of Financial Economics. Volume 84. Issue 2. Pages 435–471. ISSN 0304-405X. {https://doi.org/10.1016/j.jfineco.2006.02.005}.

- ap Gwilym and Verousis (2013) Gwilym, O., Verousis, T. 2013. Price Clustering in Individual Equity Options: Moneyness, Maturity, and Price Level. Journal of Futures Markets. Volume 33. Issue 1. Pages 55–76. ISSN 0270-7314. {https://doi.org/10.1002/fut.21547}.

- ap Gwilym et al. (1998) Gwilym, O., Clare, A., Thomas, S. 1998. Extreme Price Clustering in the London Equity Index Futures and Options Markets. Journal of Banking & Finance. Volume 22. Issue 9. Pages 1193–1206. ISSN 0378-4266. {https://doi.org/10.1016/S0378-4266(98)00054-5}.

- Baig et al. (2019) Baig, A., Blau, B. M., Sabah, N. 2019. Price Clustering and Sentiment in Bitcoin. Finance Research Letters. Volume 29. Pages 111–116. ISSN 1544-6123. {https://doi.org/10.1016/j.frl.2019.03.013}.

- Ball et al. (1985) Ball, C. A., Torous, W. N., Tschoegl, A. E. 1985. The Degree of Price Resolution: The Case of the Gold Market. Journal of Futures Markets. Volume 5. Issue 1. Pages 29–43. ISSN 0270-7314. {https://doi.org/10.1002/fut.3990050105}.

- Barndorff-Nielsen et al. (2012) Barndorff-Nielsen, O. E., Pollard, D. G., Shephard, N. 2012. Integer-Valued Lévy Processes and Low Latency Financial Econometrics. Quantitative Finance. Volume 12. Issue 4. Pages 587–605. ISSN 1469-7688. {https://doi.org/10.1080/14697688.2012.664935}.

- Barndorff-Nielsen et al. (2008) Barndorff-Nielsen, O. E., Hansen, P. R., Lunde, A., Shephard, N. 2008. Designing Realized Kernels to Measure the ex post Variation of Equity Prices in the Presence of Noise. Econometrica. Volume 76. Issue 6. Pages 1481–1536. ISSN 0012-9682. {https://doi.org/10.3982/ecta6495}.

- Barndorff-Nielsen et al. (2009) Barndorff-Nielsen, O. E., Hansen, P. R., Lunde, A., Shephard, N. 2009. Realized Kernels in Practice: Trades and Quotes. Econometrics Journal. Volume 12. Issue 3. Pages 1–32. ISSN 1368-4221. {https://doi.org/10.1111/j.1368-423X.2008.00275.x}.

- Bharati et al. (2012) Bharati, R., Crain, S. J., Kaminski, V. 2012. Clustering in Crude Oil Prices and the Target Pricing Zone Hypothesis. Energy Economics. Volume 34. Issue 4. Pages 1115–1123. ISSN 0140-9883. {https://doi.org/10.1016/j.eneco.2011.09.009}.

- Blasques et al. (2015) Blasques, F., Koopman, S. J., Lucas, A. 2015. Information-Theoretic Optimality of Observation-Driven Time Series Models for Continuous Responses. Biometrika. Volume 102. Issue 2. Pages 325–343. ISSN 0006-3444. {https://doi.org/10.1093/biomet/asu076}.

- Blau (2019) Blau, B. M. 2019. Price Clustering and Investor Sentiment. Journal of Behavioral Finance. Volume 20. Issue 1. Pages 19–30. ISSN 1542-7560. {https://doi.org/10.1080/15427560.2018.1431887}.

- Blau and Griffith (2016) Blau, B. M., Griffith, T. G. 2016. Price Clustering and the Stability of Stock Prices. Journal of Business Research. Volume 69. Issue 10. Pages 3933–3942. ISSN 0148-2963. {https://doi.org/10.1016/j.jbusres.2016.06.008}.

- Boehmer et al. (2020) Boehmer, E., Fong, K., Wu, J. 2020. Algorithmic Trading and Market Quality: International Evidence. Journal of Financial and Quantitative Analysis. ISSN 0022-1090. {https://doi.org/10.1017/S0022109020000782}.

- Bollerslev (1986) Bollerslev, T. 1986. Generalized Autoregressive Conditional Heteroskedasticity. Journal of Econometrics. Volume 31. Issue 3. Pages 307–327. ISSN 0304-4076. {https://doi.org/10.1016/0304-4076(86)90063-1}.

- Bourguignon et al. (2019) Bourguignon, M., Rodrigues, J., Santos-Neto, M. 2019. Extended Poisson INAR(1) Processes with Equidispersion, Underdispersion and Overdispersion. Journal of Applied Statistics. Volume 46. Issue 1. Pages 101–118. ISSN 0266-4763. {https://doi.org/10.1080/02664763.2018.1458216}.

- Box and Griffith (2016) Box, T., Griffith, T. 2016. Price Clustering Asymmetries in Limit Order Flows. Financial Management. Volume 45. Issue 4. Pages 1041–1066. ISSN 0046-3892. {https://doi.org/10.1111/fima.12136}.

- Brent (1972) Brent, R. P. 1972. Algorithms for Minimization Without Derivatives. Englewood Cliffs. Prentice-Hall. ISBN 978-0-13-022335-7. {https://books.google.com/books?id=Ee5QAAAAMAAJ}.

- Brooks et al. (2013) Brooks, R., Harris, E., Joymungul, Y. 2013. Price Clustering in Australian Water Markets. Applied Economics. Volume 45. Issue 6. Pages 677–685. ISSN 0003-6846. {https://doi.org/10.1080/00036846.2011.610747}.

- Brown and Mitchell (2008) Brown, P., Mitchell, J. 2008. Culture and Stock Price Clustering: Evidence from The Peoples’ Republic of China. Pacific-Basin Finance Journal. Volume 16. Issue 1-2. Pages 95–120. ISSN 0927-538X. {https://doi.org/10.1016/j.pacfin.2007.04.005}.

- Buccheri et al. (2020) Buccheri, G., Bormetti, G., Corsi, F., Lillo, F. 2020. A Score-Driven Conditional Correlation Model for Noisy and Asynchronous Data: An Application to High-Frequency Covariance Dynamics. Journal of Business & Economic Statistics. ISSN 0735-0015. {https://doi.org/10.1080/07350015.2020.1739530}.

- Capelle-Blancard and Chaudhury (2007) Capelle-Blancard, G., Chaudhury, M. 2007. Price Clustering in the CAC 40 Index Options Market. Applied Financial Economics. Volume 17. Issue 15. Pages 1201–1210. ISSN 0960-3107. {https://doi.org/10.1080/09603100600949218}.

- Chiao and Wang (2009) Chiao, C., Wang, Z. M. 2009. Price Clustering: Evidence Using Comprehensive Limit-Order Data. Financial Review. Volume 44. Issue 1. Pages 1–29. ISSN 0732-8516. {https://doi.org/10.1111/j.1540-6288.2008.00208.x}.

- Christie and Schultz (1994) Christie, W. G., Schultz, P. H. 1994. Why do NASDAQ Market Makers Avoid Odd-Eighth Quotes? The Journal of Finance. Volume 49. Issue 5. Pages 1813–1840. ISSN 0022-1082. {https://doi.org/10.1111/j.1540-6261.1994.tb04782.x}.

- Chung and Chiang (2006) Chung, H., Chiang, S. 2006. Price Clustering in E-Mini and Floor-Traded Index Futures. Journal of Futures Markets. Volume 26. Issue 3. Pages 269–295. ISSN 0270-7314. {https://doi.org/10.1002/fut.20196}.

- Chung et al. (2004) Chung, K. H., Van Ness, B. F., Van Ness, R. A. 2004. Trading Costs and Quote Clustering on the NYSE and NASDAQ after Decimalization. Journal of Financial Research. Volume 27. Issue 3. Pages 309–328. ISSN 0270-2592. {https://doi.org/10.1111/j.1475-6803.2004.00096.x}.

- Chung et al. (2005) Chung, K. H., Kim, K. A., Kitsabunnarat, P. 2005. Liquidity and Quote Clustering in a Market with Multiple Tick Sizes. Journal of Financial Research. Volume 28. Issue 2. Pages 177–195. ISSN 0270-2592. {https://doi.org/10.1111/j.1475-6803.2005.00120.x}.

- Cooney et al. (2003) Cooney, J. W., Van Ness, B., Van Ness, R. 2003. Do Investors Prefer Even-Eighth Prices? Evidence from NYSE Limit Orders. Journal of Banking & Finance. Volume 27. Issue 4. Pages 719–748. ISSN 0378-4266. {https://doi.org/10.1016/S0378-4266(01)00262-X}.

- Creal et al. (2013) Creal, D., Koopman, S. J., Lucas, A. 2013. Generalized Autoregressive Score Models with Applications. Journal of Applied Econometrics. Volume 28. Issue 5. Pages 777–795. ISSN 0883-7252. {https://doi.org/10.1002/jae.1279}.

- Das and Kadapakkam (2020) Das, S., Kadapakkam, P. R. 2020. Machine over Mind? Stock Price Clustering in the Era of Algorithmic Trading. The North American Journal of Economics and Finance. Volume 51. Pages 100831/1–100831/15. ISSN 1062-9408. {https://doi.org/10.1016/j.najef.2018.08.014}.

- Davis et al. (2014) Davis, R. L., Van Ness, B. F., Van Ness, R. A. 2014. Clustering of Trade Prices by High-Frequency and Non-High-Frequency Trading Firms. Financial Review. Volume 49. Issue 2. Pages 421–433. ISSN 0732-8516. {https://doi.org/10.1111/fire.12042}.

- Efron (1986) Efron, B. 1986. Double Exponential Families and Their Use in Generalized Linear Regression. Journal of the American Statistical Association. Volume 81. Issue 395. Pages 709–721. ISSN 0162-1459. {https://doi.org/10.1080/01621459.1986.10478327}.

- Engle (2000) Engle, R. F. 2000. The Econometrics of Ultra-High-Frequency Data. Econometrica. Volume 68. Issue 1. Pages 1–22. ISSN 0012-9682. {https://doi.org/10.1111/1468-0262.00091}.

- Engle and Russell (1998) Engle, R. F., Russell, J. R. 1998. Autoregressive Conditional Duration: A New Model for Irregularly Spaced Transaction Data. Econometrica. Volume 66. Issue 5. Pages 1127–1162. ISSN 0012-9682. {https://doi.org/10.2307/2999632}.

- Goodhart and Curcio (1991) Goodhart, C., Curcio, R. 1991. The Clustering of Bid/Ask Prices and the Spread in the Foreign Exchange Market. Working Paper. {https://www.fmg.ac.uk/publications/discussion-papers/clustering-bidask-prices-and-spread-foreign-exchange-market}.

- Hameed and Terry (1998) Hameed, A., Terry, E. 1998. The Effect of Tick Size on Price Clustering and Trading Volume. Journal of Business Finance & Accounting. Volume 25. Issue 7-8. Pages 849–867. ISSN 0306-686X. {https://doi.org/10.1111/1468-5957.00216}.

- Hansen and Lunde (2006) Hansen, P. R., Lunde, A. 2006. Realized Variance and Market Microstructure Noise. Journal of Business & Economic Statistics. Volume 24. Issue 2. Pages 127–161. ISSN 0735-0015. {https://doi.org/10.1198/073500106000000071}.

- Harris (1991) Harris, L. 1991. Stock Price Clustering and Discreteness. Review of Financial Studies. Volume 4. Issue 3. Pages 389–415. ISSN 0893-9454. {https://doi.org/10.1093/rfs/4.3.389}.

- Harvey (2013) Harvey, A. C. 2013. Dynamic Models for Volatility and Heavy Tails: With Applications to Financial and Economic Time Series. First Edition. New York. Cambridge University Press. ISBN 978-1-107-63002-4. {https://doi.org/0.1017/cbo9781139540933}.

- Heinen (2003) Heinen, A. 2003. Modelling Time Series Count Data: An Autoregressive Conditional Poisson Model. Working Paper. {https://ssrn.com/abstract=1117187}.

- Holý and Tomanová (2021) Holý, V., Tomanová, P. 2021. Streaming Approach to Quadratic Covariation Estimation Using Financial Ultra-High-Frequency Data. Working Paper. {https://arxiv.org/abs/2003.13062}.

- Hu et al. (2017) Hu, B., Jiang, C., McInish, T., Zhou, H. 2017. Price Clustering on the Shanghai Stock Exchange. Applied Economics. Volume 49. Issue 28. Pages 2766–2778. ISSN 0003-6846. {https://doi.org/10.1080/00036846.2016.1248284}.

- Hu et al. (2019) Hu, B., McInish, T., Miller, J., Zeng, L. 2019. Intraday Price Behavior of Cryptocurrencies. Finance Research Letters. Volume 28. Pages 337–342. ISSN 1544-6123. {https://doi.org/10.1016/j.frl.2018.06.002}.

- Ikenberry and Weston (2008) Ikenberry, D. L., Weston, J. P. 2008. Clustering in US Stock Prices After Decimalisation. European Financial Management. Volume 14. Issue 1. Pages 30–54. ISSN 1354-7798. {https://doi.org/10.1111/j.1468-036X.2007.00410.x}.

- Kahn et al. (1999) Kahn, C., Pennacchi, G., Sopranzetti, B. 1999. Bank Deposit Rate Clustering: Theory and Empirical Evidence. The Journal of Finance. Volume 54. Issue 6. Pages 2185–2214. ISSN 0022-1082. {https://doi.org/10.1111/0022-1082.00185}.

- Kandel et al. (2001) Kandel, S., Sarig, O., Wohl, A. 2001. Do Investors Prefer Round Stock Prices? Evidence from Israeli IPO Auctions. Journal of Banking & Finance. Volume 25. Issue 8. Pages 1543–1551. ISSN 0378-4266. {https://doi.org/10.1016/s0378-4266(00)00131-x}.

- Koopman et al. (2017) Koopman, S. J., Lit, R., Lucas, A. 2017. Intraday Stochastic Volatility in Discrete Price Changes: The Dynamic Skellam Model. Journal of the American Statistical Association. Volume 112. Issue 520. Pages 1490–1503. ISSN 0162-1459. {https://doi.org/10.1080/01621459.2017.1302878}.

- Koopman et al. (2018) Koopman, S. J., Lit, R., Lucas, A., Opschoor, A. 2018. Dynamic Discrete Copula Models for High-Frequency Stock Price Changes. Journal of Applied Econometrics. Volume 33. Issue 7. Pages 966–985. ISSN 0883-7252. {https://doi.org/10.1002/jae.2645}.

- Li et al. (2020) Li, X., Li, S., Xu, C. 2020. Price Clustering in Bitcoin Market - An Extension. Finance Research Letters. Volume 32. Pages 101072/1:101072/9. ISSN 1544-6123. {https://doi.org/10.1016/j.frl.2018.12.020}.

- Lien et al. (2019) Lien, D., Hung, P. H., Hung, I. C. 2019. Order Price Clustering, Size Clustering, and Stock Price Movements: Evidence from the Taiwan Stock Exchange. Journal of Empirical Finance. Volume 52. Pages 149–177. ISSN 0927-5398. {https://doi.org/10.1016/j.jempfin.2019.03.005}.

- Liu (2011) Liu, H.-C. 2011. Timing of Price Clustering and Trader Behavior in the Foreign Exchange Market: Evidence from Taiwan. Journal of Economics and Finance. Volume 35. Issue 2. Pages 198–210. ISSN 1055-0925. {https://doi.org/10.1007/s12197-009-9096-0}.

- Liu and Witte (2013) Liu, H.-C., Witte, M. D. 2013. Price Clustering in the U.S. Dollar/Taiwan Dollar Swap Market. Financial Review. Volume 48. Issue 1. Pages 77–96. ISSN 0732-8516. {https://doi.org/10.1111/j.1540-6288.2012.00353.x}.

- Mbanga (2019) Mbanga, C. L. 2019. The Day-of-the-Week Pattern of Price Clustering in Bitcoin. Applied Economics Letters. Volume 26. Issue 10. Pages 807–811. ISSN 1350-4851. {https://doi.org/10.1080/13504851.2018.1497844}.

- Meng et al. (2013) Meng, L., Verousis, T., Gwilym, O. 2013. A Substitution Effect Between Price Clustering and Size Clustering in Credit Default Swaps. Journal of International Financial Markets, Institutions and Money. Volume 24. Issue 1. Pages 139–152. ISSN 1042-4431. {https://doi.org/10.1016/j.intfin.2012.11.011}.

- Mishra and Tripathy (2018) Mishra, A. K., Tripathy, T. 2018. Price and Trade Size Clustering: Evidence from the National Stock Exchange of India. The Quarterly Review of Economics and Finance. Volume 68. Pages 63–72. ISSN 1062-9769. {https://doi.org/10.1016/j.qref.2017.11.006}.

- Narayan and Smyth (2013) Narayan, P. K., Smyth, R. 2013. Has Political Instability Contributed to Price Clustering on Fiji’s Stock Market? Journal of Asian Economics. Volume 28. Pages 125–130. ISSN 1049-0078. {https://doi.org/10.1016/j.asieco.2013.07.002}.

- Niederhoffer (1965) Niederhoffer, V. 1965. Clustering of Stock Prices. Operations Research. Volume 13. Issue 2. Pages 258–265. ISSN 0030-364X. {https://doi.org/10.1287/opre.13.2.258}.

- Ohta (2006) Ohta, W. 2006. An Analysis of Intraday Patterns in Price Clustering on the Tokyo Stock Exchange. Journal of Banking & Finance. Volume 30. Issue 3. Pages 1023–1039. ISSN 0378-4266. {https://doi.org/10.1016/j.jbankfin.2005.07.017}.

- Osborne (1962) Osborne, M. F. M. 1962. Periodic Structure in the Brownian Motion of Stock Prices. Operations Research. Volume 10. Issue 3. Pages 345–379. ISSN 0030-364X. {https://doi.org/10.1287/opre.10.3.345}.

- Palao and Pardo (2012) Palao, F., Pardo, A. 2012. Assessing Price Clustering in European Carbon Markets. Applied Energy. Volume 92. Pages 51–56. ISSN 0306-2619. {https://doi.org/10.1016/j.apenergy.2011.10.022}.

- Robert and Rosenbaum (2011) Robert, C. Y., Rosenbaum, M. 2011. A New Approach for the Dynamics of Ultra-High-Frequency Data: The Model with Uncertainty Zones. Journal of Financial Econometrics. Volume 9. Issue 2. Pages 344–366. ISSN 1479-8409. {https://doi.org/10.1093/jjfinec/nbq023}.

- Roşu (2019) Roşu, I. 2019. Fast and Slow Informed Trading. Journal of Financial Markets. Volume 43. Pages 1–30. ISSN 1386-4181. {https://doi.org/10.1016/j.finmar.2019.02.003}.

- Russell and Engle (2005) Russell, J. R., Engle, R. F. 2005. A Discrete-State Continuous-Time Model of Financial Transactions Prices and Times: The Autoregressive Conditional Multinomial-Autoregressive Conditional Duration Model. Journal of Business & Economic Statistics. Volume 23. Issue 2. Pages 166–180. ISSN 0735-0015. {https://doi.org/10.1198/073500104000000541}.

- Schwartz et al. (2004) Schwartz, A. L., Van Ness, B. F., Van Ness, R. A. 2004. Clustering in the Futures Market: Evidence From S&P 500 Futures Contracts. Journal of Futures Markets. Volume 24. Issue 5. Pages 413–428. ISSN 0270-7314. {https://doi.org/10.1002/fut.10129}.

- Sellers and Morris (2017) Sellers, K. F., Morris, D. S. 2017. Underdispersion Models: Models That Are "Under the Radar". Communications in Statistics - Theory and Methods. Volume 46. Issue 24. Pages 12075–12086. ISSN 0361-0926. {https://doi.org/10.1080/03610926.2017.1291976}.

- Shephard and Yang (2017) Shephard, N., Yang, J. J. 2017. Continuous Time Analysis of Fleeting Discrete Price Moves. Journal of the American Statistical Association. Volume 112. Issue 519. Pages 1090–1106. ISSN 0162-1459. {https://doi.org/10.1080/01621459.2016.1192544}.

- Shkilko and Sokolov (2020) Shkilko, A., Sokolov, K. 2020. Every Cloud Has A Silver Lining: Fast Trading, Microwave Connectivity, and Trading Costs. The Journal of Finance. Volume 75. Issue 6. Pages 2899–2927. ISSN 0022-1082. {https://doi.org/10.1111/jofi.12969}.

- Song et al. (2020) Song, S., Wang, Y., Xu, G. 2020. On the Probability of Default in a Market with Price Clustering and Jump Risk. Mathematics and Financial Economics. Volume 14. Issue 2. Pages 225–247. ISSN 1862-9679. {https://doi.org/10.1007/s11579-019-00253-x}.

- Sopranzetti and Datar (2002) Sopranzetti, B. J., Datar, V. 2002. Price Clustering in Foreign Exchange Spot Markets. Journal of Financial Markets. Volume 5. Issue 4. Pages 411–417. ISSN 1386-4181. {https://doi.org/10.1016/S1386-4181(01)00032-5}.

- Urquhart (2017) Urquhart, A. 2017. Price Clustering in Bitcoin. Economics Letters. Volume 159. Pages 145–148. ISSN 0165-1765. {https://doi.org/10.1016/j.econlet.2017.07.035}.

- Verousis and ap Gwilym (2013) Verousis, T., Gwilym, O. 2013. Trade Size Clustering and the Cost of Trading at the London Stock Exchange. International Review of Financial Analysis. Volume 27. Pages 91–102. ISSN 1057-5219. {https://doi.org/10.1016/j.irfa.2012.08.007}.

- Xu et al. (2012) Xu, H. Y., Xie, M., Goh, T. N., Fu, X. 2012. A Model for Integer-Valued Time Series with Conditional Overdispersion. Computational Statistics & Data Analysis. Volume 56. Issue 12. Pages 4229–4242. ISSN 0167-9473. {https://doi.org/10.1016/j.csda.2012.04.011}.

- Zou et al. (2013) Zou, Y., Geedipally, S. R., Lord, D. 2013. Evaluating the Double Poisson Generalized Linear Model. Accident Analysis and Prevention. Volume 59. Pages 497–505. ISSN 0001-4575. {https://doi.org/10.1016/j.aap.2013.07.017}.