Bridging factor and sparse models

Abstract

Factor and sparse models are two widely used methods to impose a low-dimensional structure in high-dimensions. However, they are seemingly mutually exclusive. We propose a lifting method that combines the merits of these two models in a supervised learning methodology that allows for efficiently exploring all the information in high-dimensional datasets. The method is based on a flexible model for high-dimensional panel data, called factor-augmented regression model with observable and/or latent common factors, as well as idiosyncratic components. This model not only includes both principal component regression and sparse regression as specific models but also significantly weakens the cross-sectional dependence and facilitates model selection and interpretability. The method consists of several steps and a novel test for (partial) covariance structure in high dimensions to infer the remaining cross-section dependence at each step. We develop the theory for the model and demonstrate the validity of the multiplier bootstrap for testing a high-dimensional (partial) covariance structure. The theory is supported by a simulation study and applications.

keywords:

[class=MSC]keywords:

, and

1 Introduction

With the emergence of new and large datasets in almost all disciplines, the correct characterization of the dependence among variables is of substantial importance. Usually, to achieve this goal, the literature has followed two seemingly orthogonal tracks over the last two decades. On the one hand, factor models have become an essential tool to summarize information in large datasets under the assumption that the remaining dependence structure is negligible. For instance, panel factor models are now applied to various problems, ranging from forecasting to causal inference and network analysis. However, on the other hand, there have been significant advances in parameter estimation in ultra high-dimensions under the assumption of sparsity or weak sparsity. That is, a variable depends only on a (very) small subset of the other variables. For an overview of these two topics and their exciting developments, see Fan et al. (2020).

In this paper, we take an alternative route and combine the best of the two worlds described above to better characterize the dependence structure in high-dimensional datasets. More specifically, we consider that the covariance structure of a large set of variables, organized in a panel data format, is characterized as a combination of a factor structure, where factors can be either observed, unobserved, or both, and a weakly-sparse idiosyncratic component. This formulation is general enough to accommodate many data-generating processes of interest in economics, finance, epidemiology, and energy/engineering, for example. The proposed methodology has two ingredients: a multi-step estimation procedure and a new test for structure in high dimensional (partial) covariance matrices. The steps of the estimation procedure are as follows. In the first one, we take the original data and remove the effects of any observed factors. These factors can be deterministic terms such as seasonal dummies and/or trends or other observed covariates. The first step can be parametric or nonparametric, low or high dimensional. A latent factor model is then estimated using the residuals from the first stage. In a third step, we model the dependence among idiosyncratic terms as a weakly sparse regression estimated by the Least Absolute Shrinkage and Selection Operator (LASSO). A final additional fourth step can be used to build models for out-of-sample forecasting, taking into account each of the components in the previous steps. At each step, the null hypothesis of no remaining cross-section dependence can be tested by the proposed test for the (partial) covariance structure in high dimensions.

Our approach has many statistical applications. It can enhance high-dimensional prediction, select more interpretable variables, construct counterfactuals for policy evaluations, and depict (partial) correlation networks, among many others.

1.1 Motivation

Let be a random vector generated as , for , , where , with , is not necessarily diagonal. Fix one component of interest , which serves as a response variable. Consider the following predictive models:

| (1.1) |

where and are, respectively, vectors with the elements of and without the -th entry. is a factor augmented regression since it is the same as .

Suppose that we observe both and . Which one of the three models above is best in terms of mean square error () for prediction? Comparison between and is not clear since it depends, among other things, on the magnitude of relative to , where . However, since the -algebras generated by and are both included in the -algebra generated by , it is not surprising that . The same will hold true if we replace the models in (1.1) by their best linear projections, which we denote by for . Therefore, we can write the “gains” of when compared to and :

where is coefficients of the projection of onto ; is excluding the -th row and column; ; ; and is the coefficient of the projection of onto . From the previous expressions, it becomes evident that both and are restrictions on . Broadly speaking, whenever one does not expect to have an exact factor model, there are potential gains of taking into account the contribution of the idiosyncratic components . Therefore, we use as the base model for the estimation methodology described in Section 2.2.

1.2 Main Contributions and Comparison with the Literature

The contributions of this paper are multi-fold. First, our methodology bridges the gap between two apparently competing methods for high-dimensional modeling; see, for example, the discussion in Giannone, Lenza and Primiceri (2021) and Fan, Ke and Wang (2020). This yields a vast number of potential applications and spin-offs. For instance, in Fan, Masini and Medeiros (2020), we apply the methods developed here to evaluate the effects of interventions and contribute to the literature on synthetic controls and related methods by combining the approaches of Gobillon and Magnac (2016), and Carvalho, Masini and Medeiros (2018). Therefore, in our setup, both a common strong factor structure and weak sparsity can coexist.

Second, the methodology proposed here contributes to the forecasting literature. For instance, in the second application considered in this paper, we build forecasting models based on a large cross-section of macroeconomic variables. We call this method the FarmPredict. We show that combining factors and a sparse regression strongly outperforms the traditional principal component regression as in Stock and Watson (2002). Therefore, FarmPredict can be an additional contribution to the forecasting and machine learning toolkit. The method can be easily extended to a multivariate setting combining factor-augmented vector autoregressions (FAVAR) as in Bernanke, Boivin and Eliasz (2005) and sparse vector models as in Kock and Callot (2015) and Masini, Medeiros and Mendes (2019). Our methodology can also be applied in areas beyond economics. For example, it can be useful to construct forecasting models for the spread of infectious diseases, such as COVID-19, by taking into account co-movements and spillovers among different locations.

Third, we show the consistency of factor estimation based on the residuals of a first-step regression. Our results hold for both parametric (linear or nonlinear) and nonparametric first stage. A high-dimensional first stage is also allowed. Note that current results in the literature consider that factors are estimated based on observed data, and our derivations favor a much more flexible and general setup (Bai, 2003; Bai and Ng, 2002, 2006). More specifically, our methodology allows settings where there are both observed and latent factors and trend-stationary data. In the latter, the trend can be first removed by (nonparametric) first-stage regression. Whenever the unobserved factors and the observed covariates are correlated, the method proposed in Pesaran (2006) can be used, and all results follow directly.

Fourth, we contribute to the LASSO literature. LASSO can not be model selection consistent for highly correlated variables. By decomposing covariates into factors and idiosyncratic components, namely the idea of lifting, we decorrelate the variables and make the model selection condition much easier to hold; see, for example, Fan, Ke and Wang (2020). We show the consistency of the estimates based on the residuals of the previous steps. Our results are derived under restrictions on the population covariance matrix of the data and not on the estimated one, as is usual in many papers. See, for example, van de Geer and Bühlmann (2009). Furthermore, we derive our results under much mild conditions than the ones considered in Fan, Ke and Wang (2020).

Fifth, we extend the results in Chernozhukov, Chetverikov and Kato (2013a, 2018) to strong-mixing data in order to construct hypothesis tests for covariance and partial covariance structure in high dimensions.111Giessing and Fan (2020) also extended Chernozhukov, Chetverikov and Kato (2013a). However, their setup differs from ours as they only consider the case of independent and identically distributed data. We also establish the consistency of a new estimator of the partial covariance matrix in high-dimensions and strong-mixing data. Our proposed tests can be used to infer if the (partial) covariance matrix of a high-dimensional random vector is diagonal or block-diagonal. More generally, we can test any pre-defined structure. Furthermore, we show that the test remains valid when we use the residuals from a previous step estimation to compute the covariance matrix. This result allows us to apply the test to the multi-stage estimation procedure proposed here. These are important results for many applications in economics, finance, epidemiology, and many other areas. For instance, our inference procedure can serve as a diagnostic and misspecification tool. For panel data models with interactive fixed effects as in Pesaran (2006), Bai (2009), Moon and Weidner (2015) and Bai and Liao (2017), our test can be directly applied to uncover the dependence structure among cross-sectional units before and after accounting for common factor components. If the factor structure is informative enough, we expect the idiosyncratic covariance matrix to be almost sparse. If this is not the case, we may have possibly underestimated the number of factors. One popular application is in asset pricing, as discussed in Gagliardini, Ossola and Scaillet (2019) and the empirical section of this paper. There are a huge number of proposed factors as described in Feng, Giglio and Xiu (2020). We can apply our methodology to test for omitted factors and estimate network connections among firms, as in Diebold and Yilmaz (2014) and Brownlees, Gudmundsson and Lugosi (2020). Finally, as a diagnostic tool, our paper tackles the same problem as Gagliardini, Ossola and Scaillet (2019). However, we take an alternative solution strategy that relies on a much different set of hypotheses; see also Gagliardini, Ossola and Scaillet (2020).

Although our results are derived under the assumption that the number of factors is known, simulation results presented in the Supplementary Material provide evidence that the test has good finite-sample properties even when the number of factors is determined by data-driven methods commonly found in the literature. In addition, due to factor augmentation, our method is robust to overestimating the number of factors. Over the past years, a vast number of papers proposed different methods to test for covariance structure in high dimensions. See, for example, Cai (2017) and the references therein. To the best of our knowledge, we complement all the previous papers by simultaneously considering high-dimensions, strong-mixing data with mild distributional assumptions, and pre-estimation when constructing tests for both covariance and partial covariance structure.

Finally, it is essential to highlight the theoretical challenges that we tackle in this paper. First, to derive the properties of our proposed test for (partial) covariance structure, we prove a new high dimensional Central Limit Theorem (CLT) for strong mixing sequences. To our knowledge, this CLT is new in the literature and allows us to apply Gaussian approximation results in a much more general framework. Second, as a side result, to develop the test, we first show the consistency of kernel-based estimation of a high-dimensional long-run covariance matrix of strong-mixing processes. This is also a new result with significant consequences for the theory of high-dimensional regression with dependent errors. Second, all the non-asymptotic bounds for our multi-step estimators are derived under the assumption that the distributions of the random variables in the model have polynomial tails, and the estimation errors of previous steps are also taken into account. This introduces several difficulties in proving the results but makes our method well-suited for applications with fat-tailed data, such as those observed in financial applications. Finally, in the derived bounds, the strong mixing coefficient appears explicit and can be allowed to grow with the sample size. This not only introduces technical challenges but makes our results very general.

Summarizing, our approach provides:

-

1.

A systematic way to unify factor and sparse models to construct statistical specifications which use all available information and that can be applied, for example, to

-

(a)

Forecasting in a high-dimensional setting;

-

(b)

Construction of counterfactuals to aggregate data; or

-

(c)

Estimation of partial correlation networks;

-

(a)

-

2.

An inferential procedure to test for general structures in covariance and partial covariance matrices which can be useful, among other things, for:

-

(a)

Test for misspecification in factor models; or

-

(b)

Test for nontrivial links among idiosyncratic units.

-

(a)

1.3 Organization of the Paper

In addition to this Introduction, the paper is organized as follows. We present the model setup and assumptions in Section 2. The theoretical results are presented in Section 3. We discuss the empirical application in Section 4. Section 5 concludes. All proofs, additional discussion, simulation, and empirical results are deferred to the Supplementary Material due to space constraints. Tables and figures in the Supplementary Material are referenced with an “S” before the number.

1.4 Notation

All random quantities (real-valued, vectors and matrices) are defined in a common probability space . We denote random variables by an upper case letter, , and its realization by a lower case letter, . The expected value operator is with respect to the law, such that . Matrices and vectors are written in bold letters . Except for the number of factors, , and the number of covariates, , defined below, all other dimensions are allowed to depend on the sample size (). However, we omit this dependency throughout the paper to avoid clustering the notation prematurely. Also, we write for and denote the cardinality of a set by .

We use to denote the norm for , such that for a -dimensional (possibly random) vector , we have for and . If is a possibly random matrix, then denotes the matrix -induced norm and denotes the maximum entry in absolute terms of the matrix . Note that whenever is random, then for and are random variables. We also reserve the symbol without subscript for the Euclidean norm for both vectors and matrices. We denote the norm of by for , i.e., for and is the essential supremum of (in respect to ). Also, when is a random vector, we define . Note that is random variable while is non-random scalar for .

For any vector , is a diagonal matrix whose diagonal is the elements of . is an indicator function ion the event , i.e, if is true and otherwise. For any matrix (possibly random) , represents the entry for row and column , is the column-vector with all rows of column and is a column-vector with the transpose of all elements of row . We decide not to write as to avoid a cumbersome notation. Finally, for non-negative sequences and , we write if there is a constant independent of such that for all . Also, we write if both and . Similarly, for non-negative random sequences and , we write if for every there is a constant independent of such that for all . Also, , if both and .

2 Setup and Method

2.1 Data Generating Process

We consider a very general panel data model rich enough to nest several important cases in economics, finance, and related areas. We define the following Data Generating Process (DGP).

Assumption 1 (DGP).

For and , the process is generated by covariate-adjusted factor model

| (2.1) |

where is a -dimensional observable (random) vector which may also include a constant term and is typically used for adjustments of heterogeneity, seasonality, and covariate dependence, is a -dimensional vector of common latent factors, and is a zero mean idiosyncratic component.222For simplicity, we assume that all the units have the same number of covariates (). The framework can certainly accommodate situations where depends on . It also includes cross-sectional regression as a specific example. The unknown parameters are , the factor loadings , and the covariance matrix of the idiosyncratic components. Finally, we assume that , and are mutually uncorrelated, but can be serially autocorrelated.

Remark 1.

In Assumption 1 we consider that , the dimension of , is finite and fixed. Furthermore, the relation between and is linear. This is for the sake of exposition. As our theoretical results are written in terms of the consistency rate of the first-step estimation, the DGP can be made much more general by just changing the rates.

Remark 2.

The assumption that , and are mutually uncorrelated can be relaxed. Whenever is correlated with and , and the interest lies of the estimation of the parameters , , the method proposed by Pesaran (2006) can applied in the first-stage of the procedure considered in this paper and our theoretical results will follow. Nevertheless, we provide several examples where the assumption that , and are mutually uncorrelated is reasonable.

Our modeling strategy does not stop at (2.1). Instead, we attempt to further explain and impose dynamics on . The former allows us to use other idiosyncratic components to further explain and hence, increase the information set. The latter builds a dynamic model to facilitate out-of-sample prediction, for instance.

For each , let be a vector whose elements form a (non-empty) subset of , where is a non-negative integer (much) smaller than . This subset of variables attempts to explain further by the following population regression model:

| (2.2) |

where , for and . For simplicity of exposition, we assume that the dimension of is the same for all , which we denote by . Clearly, .

Similarly, for a non-negative integer (much) smaller than , let be a vector whose elements form a (non-empty) subset of , for , which attempts to explain further the latent factor. Consider the following population regression model:

where , for and . Once again, we assume that the dimension of is the same for all , which we denote by , where . Note that we do not necessarily exclude from to contemplate cases when the contemporaneous factor is available in a prediction exercise. For future reference we write (2.3) as

| (2.3) |

where , , and .

Example 1 (Asset Pricing Models).

Suppose is the return of an asset at time and let be a set of observable common risk factors, such as the market returns or Fama-French factors (Fama and French, 1993, 2015). can be a set of additional, non-observable risk factors. Several asset pricing models, such as the Capital Asset Pricing Model (CAPM) or the Arbitrage Pricing Theory (APT) model, are nested into this general framework. The idiosyncratic terms, , can be non-trivially correlated across assets, representing links among firms that are not captured by the common factor structure. In this case, we may be interested in estimating a regression where such that:

The coefficients represent the links among firms after controlling for the factors. The structures of the covariance and partial covariance matrix of also shed light on these potential links.

Example 2 (Networks).

Model (2.1) also complements the network specifications discussed in Barigozzi and Hallin (2016,2017b) and Barigozzi and Brownlees (2019). Furthermore, as discussed in the previous example, the test proposed here can be used to detect network links as in Diebold and Yilmaz (2014), and Brownlees, Gudmundsson and Lugosi (2020). As another example, can be the (realized) volatility of financial assets and can be volatility factors as in Andreou and Ghysels (2021).

Example 3 (FAVAR).

In the case where the index represents a different dependent (endogenous) variable and is a dependent process, model (2.1) turns out to be equivalent to the Factor Augmented Vector Autoregressive (FAVAR) model of Bernanke, Boivin and Eliasz (2005). In this case, may include a constant and seasonal dummies, and . Furthermore, in order to construct -step-ahead out-of-sample forecasts, we can set .

Example 4 (Panel Data Models).

Model (2.1) is the panel model with iterative fixed-effects considered in Gobillon and Magnac (2016), where the authors propose an alternative to the Synthetic Control method of Abadie and Gardeazabal (2003) to evaluate the effects of regional policies. Model (2.1) is also in the heart of the FarmTreat method of Fan, Masini and Medeiros (2020), where the authors set .

2.2 The Method

The method proposed here for estimation, inference, and prediction consists of multiple stages, where the residuals’ covariance structure can be tested at the end of each stage.

-

1.

For each run the regression:

and compute . The first stage may consist of a regression on a constant, a deterministic time trend, and seasonal dummies, for instance, or, as in Example 1, a regression on observed factors. After removing the contribution from the observables, we can use the test for the null hypothesis of no remaining (partial) covariance structure to check if the (partial) covariance of is dense or sparse. If it is dense, we move to Step 2. Otherwise, we jump directly to Step 3. This first parametric, low-dimensional step can be replaced by a nonlinear/nonparametric regression or by a high-dimensional model when, for example, the number of observed factors is large. As pointed out in Remark 2, the Pesaran’s (2006) estimator can be also used whenever correlation between and is allowed. This will be discussed more in the subsequent sections.

-

2.

Write and . This step consists of estimating and , for , through principal component analysis (PCA) 333Another approach is to use the joint estimation as in Agarwal, Negahban and Wainwright (2012). The key difference between the two approaches is the optimization-based approach (fully-iterated) and the one-step approach as well as the different assumptions behind the two approaches. The PCA approach is based on the strong factor assumption with a large eigengap but does not impose the sparse structure on the idiosyncratic component covariance matrix. See Fan, Liao and Mincheva (2013) for additional discussion. of and compute

After estimating the factors and loadings, we apply our testing procedure to check for the remaining covariance structure in . The second-step estimation can be carried out also by dynamic factor models. In Section S.2 we discuss the selection of the number of factors.

-

3.

Now, define be a non-empty subset of where is a non-negative integer (lag). This includes contemporary regression for association studies and lagged regression for prediction of as two specific examples. The third step consists of a sparse regression to estimate the following model for each :

The regression in Step 3 provides useful augmentation for reducing the error in explaining in (2.1) further from to and hence the prediction error for ; see (2.5).

-

4.

(For partial covariance analysis only) Estimate the following sparse regression model for each :

where is the vector without and elements. Let be the residuals. Then compute the partial correlation as the sample correlation of .

-

5.

(For forecasting only) Define where is a non-empty subset of for each ; and is a non-negative integer (lag) 444We write at this generality to accommodate the cross-sectional applications in which no latent factor needs to be predicted as in the principal component regression. In this case, and this step is not needed.. This step is multiple linear regression to estimate the following model for each :

This step aims at establishing a predictive model for latent factors. The estimator will be used in the predictive model defined in (2.5).

2.3 Predictive Models

In a pure prediction exercise, one is usually interested in the linear projection of onto motivated by the discussion in Section 1.1. This results in the factor-augmented regression model (FARM)

| (2.4) |

in which predicts ; see (2.1). This can used for prediction, following the steps described in Section 2.2, by

| (2.5) |

We call the prediction model FarmPredict.

Note that model (2.4) is equivalent to using the predictors and , which augment predictors by using the common factors . The form in (2.4) mitigates the collinearity issues in high dimensions. Model (2.4) also bridges factor regression () on one end and (sparse) regression on the other end with , where is the loading matrix without the th row. In the latter, if we set and (hence, ), model (2.4) becomes a (sparse) regression model:

In this case, (2.4) decorrelates the predictor , which makes the model selection consistency much easier to satisfy and forms the basis of FarmSelect in Fan, Ke and Wang (2020). Our contribution in this specific task is to allow heterogeneity adjustments, resulting in the estimated data . In general, for model (2.4) with sparsity, FarmPredict chooses additional idiosyncratic components to enhance the prediction of the factor regression.

2.4 Covariance Structure and Inference

In several applications, the structure of the idiosyncratic components is the objective of interest. An estimator for could be simply given by

| (2.7) |

The task of estimating is well documented in literature even in high-dimensions; see, for example, Fan et al. (2020), Ledoit and Wolf (2021), and the references therein. Nevertheless, we show that (2.7) can be used within our testing framework.

In order to proper understand the (linear) relation between a pair of , a simple covariance estimate sometimes is not enough. In applications, it is often desirable to directly measure how and are connected. By direct connection, we mean the relation between those units removing the contribution of other variables of . For this purpose, we use the partial covariance between and , defined for any pair as , where and denotes the linear projection of onto the space spanned by all the units except and , which we denote by . As in Peng et al. (2009), we suggest to estimate the partial covariance matrix by

| (2.8) |

where is the residual of the LASSO regression of onto obtained in step 4 for .

We also would like to conduct formal tests on the population structure of . Specifically, we propose a test for the following null hypothesis:

| (2.9) |

for a given subset , where, for a given matrix , the notation denotes the -dimensional vector of indexed by the elements in . Note we allow to diverge as . For testing the structure on the partial covariance matrix, consider:

| (2.10) |

The null hypotheses (2.9) and (2.10) nest several cases of interest. The most common would be to test for a diagonal or a block diagonal structure in and/or . But it also accommodates other structures.555With minor changes, the proposed test can also be used to test the null for some matrix and -dimensional vector where is also a function of . The challenges for testing (2.9) and (2.10) can be summarized as follows:

-

1.

As we allow for both and to diverge as grows, sometimes at a faster rate, we have a high-dimensional test where some sort of Gaussian approximation result for dependent data must be deployed as we also allow the number covariances to be tested to diverge. In this case, a high-dimensional long-run covariance matrix must be estimated if one expects to get the (asymptotic) correct test size.

-

2.

We do not observe or . Instead, we have an estimate of both from a postulated model on observable random variables. Therefore, the estimation error must be considered to claim some sort of asymptotic properties of the test. In fact, it is not uncommon to obtain estimates of both and from a multi-stage estimation procedure as we illustrate later.

We propose to test (2.9) using the statistic

| (2.11) |

The quantiles of are approximated by a Gaussian bootstrap. To describe the procedure, let denote the covariance matrix for the vectorized submatrix , where . Since the process might present some form of temporal dependence (refer to Assumption 2(c)), we estimate using a Newey-West-type estimator. For a given , where is a class of kernel functions described below in (3.6) and bandwidth , is estimated by

| (2.12) |

where is a -dimensional vector with entries given by for , where is the element of defined in (2.7). Finally, let be the conditional -quantile of the Gaussian bootstrap where , i.e.

Theorem 5 demonstrates the validity of Gaussian bootstrap procedure described above, i.e., it states conditions under which the -quantile of the test statistic (2.11) can be approximated by in the appropriate sense.

Similarly, the test statistic for (2.10) is given by

| (2.13) |

Let denote the covariance matrix of where . is estimated by

| (2.14) |

where is a -dimensional vector with entries given by for . Also, let be the conditional -quantile of the Gaussian bootstrap where . Theorem 6 establish conditions for the validity of Gaussian bootstrap to approximate the quantiles of (2.13).

3 Theoretical Results

In this section, we collect all the theoretical guarantees for estimating the model (2.1) by using the proposed multi-stage method described above. Specifically, Subsection 3.1 presents non-asymptotic bounds for the (parametric) estimation, Subsection 3.2 deals similar results concerning forecasting, and Subsection 3.3 deals with inference on the (partial) covariance structure of .

To present the results, it is convenient to use a compact notation. For each , we define the -dimensional vectors and . We also define the matrix of covariates , for each and the matrix of factors , such that (2.1) can be represented as

| (3.1) |

for each cross-sectional unit , where .

We define for each , the -dimensional vectors and ; and the -dimensional vector . Also, set the block diagonal matrix whose block diagonal is given by and the loading matrix . Then, (2.1) can also be represented as panel time series

| (3.2) |

where .

3.1 Estimation

We start by stating the following assumption.

Assumption 2 (Moments and Dependency).

Consider the following:

-

(a)

The stochastic process is weakly stationary for each , where denotes the vector after excluding all deterministic (non-random) components. Furthermore, the strong mixing coefficient of is denoted by .

-

(b)

Define for some integer and let be a finite constant such that , where is the minimum eigenvalue of .

-

(c)

Assume there exists an universal constant such for all , and :

-

(c.1)

for some constants and

-

(c.2)

-

(c.3)

-

(c.4)

.

-

(c.1)

Assumption (2.a) excludes the deterministic components of to accommodate possibly non-random non-stationary, but uniformly bounded covariates as in Assumption (2.c). Assumption (2.b) ensures that the parameter in (2.2) is well defined since, by the Cauchy interlacing theorem, we have . Finally, Assumptions (2.a) and (2.c) allow us to apply a Marcinkiewicz-Zygmund type inequality for partial sums to deal with polynomial tails (see Lemma S.2 in the Supplementary Material).

For each , let denote the unobservable error term in (3.1), the least-squares estimator of and the vector of residuals. Also, set and . We must control for estimation error in the first step of the proposed methodology. The next result gives a bound for the maximum entry of the matrix when the first stage is conducted by OLS in a linear setup. Note that in this case we assume that , and are mutually uncorrelated.

We state the results below in terms of the strong mixing coefficient sequence, whose definition is presented here for convenience. For , define

| (3.3) |

where is the -algebra generated by for . Note that might depend on both and .

Remark 3.

Even though we will treat the number of factors, , and the number of covariates, , fixed (not depending on or ), we kept them explicit in the result above. Furthermore, if we assume that for all , where is a constant that might depend on and is an universal constant, then

Remark 4.

When the first step of the method involves more complicated estimation, such as Pesaran’s (2006) method, instrumental variables, or LASSO, we write , where is a non-negative sequence of and . This approach is adopted systematically in the following theorems.

Define the matrices and ; and the matrix . We can write (2.1) in the matrix form as

| (3.4) |

Notice that where and can be estimated by Principal Component Analysis (PCA), which minimizes with respect to and , subject to . The solution is the matrix whose columns are times eigenvectors of the top eigenvalues of and .

Since we do not observe , in the third step of the method we use instead. Therefore, we must control for the estimation error in the previous steps: . Also, the loading matrix and the factors are not separably identified since for any matrix such that . If we let , where is the diagonal matrix containing the largest eigenvalues of in decreasing order, we have that is identified as is identified.

The result below first appeared in Bai (2003) for the case of diverging and was further extended to hold uniformly in by Fan, Liao and Mincheva (2013). However, both consider the case when the factor model is estimated using the actual data instead of the “estimated” ones (residuals) as in our case. Therefore, the next result is a generalization that takes into account the pre-estimation error term and quantifies how the error impacts the precision of factor analysis.

Assumption 3 (Factor Model).

Assume:

-

(a)

, , and is a diagonal matrix;

-

(b)

All eigenvalues of are bounded away from zero and infinity as ;

-

(c)

; and

-

(d)

.

Remark 5.

Assumption 3 is standard in the literature. Assumption is not restrictive as our approach considers a first-step estimation which may include a constant in the set of regressors. Assumption (3.a) is also needed for identifiability of the factor structure. Assumption (3.c) imposes a strong factor structure.

Theorem 2.

By setting we have the case of no estimation error in the first step. Note that in order to have the error vanishing in probability we must have the pre-estimation error of order (in probability) smaller than .

We have decided not to replace in Theorem 2 with the rate obtained in Theorem 1 as the latter only applies to the least-squares estimator. In some applications, however, the first step of the procedure could be done using a different type of estimator. For instance, a penalized adaptive Huber regression as in Fan, Li and Wang (2017) if the number of features is comparable or even larger than and the tail of the distribution of is heavy. By stating Theorem 2 in terms of a generic rate, it is easier to account for the effect of different estimators. By combining Theorems 1 and 2 we have the following corollary.

Corollary 1.

We propose to estimate (2.3) by LASSO using in place of . Specifically, for a regularization parameter , we denote by a minimizer of given by

| (3.5) |

The next result presents non-asymptotic bounds for the (in sample) prediction error and the -estimation error for the LASSO estimator (3.5) based on the “estimated data” and quantifies how the estimation errors impact on the choice of regularization parameter and rates of convergence.

Theorem 3.

Once again, we purposely avoided replacing in Theorem 3 with the rate of Corollary 1 to make it readily applicable to the case when a different type of factor model was used or, as a matter of fact, any other pre-estimation procedure. By setting equal to , the rate of Corollary 1, we have the next result.

3.2 Forecasting

Recall that in the context of out-of-sample forecasting, our object of interest is for and , which we estimate using . The next result bounds (in probability) the prediction error bound in terms of all estimation errors from previous steps.

Theorem 4.

3.3 Inference on Covariance and Partial Covariance Matrices

We now obtain the null distributions of our test statistics for the structures of the covariance and the partial covariance. Recall the setup and notation of Section 2.4. Further define and as the element of indexed by . Also, for any pair of random vectors of the same dimensional, , say; define the distance in distribution

where is the class of all rectangles in the from for some and .

We assume that the kernel appearing in the covariance estimator defined by (2.12) belongs to the class defined in Andrews (1991) which we reproduce below for convenience

| (3.6) |

This includes most of the well-known kernels used in the literature. To avoid confusion, it is worth pointing out that our tuning parameter , also called bandwidth parameter by Andrews (1991), is supposed to diverge, as opposed to the bandwidth in the density kernel estimation setup, which is expected to shrink to zero.

The following result shows how accurately the covariance matrix elements are estimated and validate the bootstrap method.

Theorem 5.

For , let and be a zero-mean Gaussian vector with the same covariance matrix of , i.e., . Under Assumptions 1–3, if further

-

(a)

is fourth-order stationary process for each ;

-

(b)

The strong mixing coefficient of , , obeys for where and are defined in Assumption 2; and a constant that might depend on ;

-

(c)

the minimum eigenvalue of is greater or equal to , for some , then,

where , and .

Let , then

Let be any positive semi definite estimator of and , then

Remark 7.

The first result in Theorem 5 bounds the Komolgorov distance between the (unobservable) process and a Gaussian process with the same covariance structure. It is a direct consequence of a more general Central Limit Theorem result for high-dimensional alpha mixing sequences (see Theorem S.13 in the Supplementary Material). The second one is similar but controls for the difference between and, therefore, takes into account the estimation error. Finally, the last result ensures a bootstrap validity provided we can estimate the covariance matrix in an appropriate sense.

Remark 8.

Theorem 5 seem complicated. However, they only depend on , , , , and the “quality” of the estimators and . The latter allows a different selection of estimators for any of the stages and the bootstrap procedure. If we were to specialized Theorem 5 to incorporate the rates obtained in Theorem 1 and 2, and set defined by (2.12), we obtain a sufficient condition to ensure the bootstrap validity depending only on and .

Corollary 3.

Under the same conditions of Theorem 5, if defined by (2.12) with , where is defined by (3.6), then, uniformly in ,

where is the bandwidth parameter of the covariance estimator and is the rate appearing in Corollary 1. If further, as :

-

(a)

, where is the rate appearing in the first result of Theorem 5 with replaced by ;

-

(b)

-

(c)

, then,

where the first supremum is over all null hypotheses of the form (2.9) indexed by .

The next theorem shows how well the elements of the partial autocovariance matrix are estimated and gives the conditions under which the bootstrap test is valid. In the calculation the partial covariance (2.8), we use the residual of the LASSO regression of onto . Define for and recall from Section 2.4 that for , , and denotes the covariance of .

Theorem 6.

For , let and be a zero-mean Gaussian vector with the same covariance matrix of , i.e., . Under the same assumptions and notation of Theorem 5, with and replaced by and , respectively in condition (c), we have

where are defined in Theorem 5.

Let , then

Let be any positive semi definite estimator of and , then

Similar comments as those appearing in Remarks 8 apply to Theorem 6 as well, which results in the following corollary.

Corollary 4.

Under the same conditions of Theorem 6, if defined by (2.14) with , where is defined by (3.6), then, uniformly in ,

where is the bandwidth of the covariance estimator, for , is the rate appearing in Corollary 1, and is the rate appearing in Corollary 2 with and replaced by and , respectively, and . If further, as :

-

(a)

, where is the rate in the first result of Theorem 6 with replaced by ;

-

(b)

-

(c)

, then,

where the first supremum is over all null hypotheses of the form (2.9) indexed by .

Remark 9.

As opposed to the case of testing covariance, when testing partial covariance in high dimensions, the sparse structure plays a role in terms of appearing in the conditions (b) and (c). Therefore, these assumptions restrict the cases where the proposed partial covariance test has the correct asymptotic size. For instance, in the case of a complete dense partial covariance structure, we are likely to have of the order of and, therefore, conditions and are not expected to hold.

4 Applications

4.1 Factor Models and Network Structure in Asset Returns

We illustrate our methodology by studying the factor structure of asset returns. We consider monthly close-to-close excess returns from a cross-section of 9,456 firms traded on the New York Stock Exchange. The data starts on November 1991 and runs until December 2018. There are 326 monthly observations in total. In addition to the returns, we also consider 16 monthly factors: Market (), Small-minus-Big (), High-minus-Low (), Conservative-minus-Aggressive (), Robust-minus-Weak (), earning/price ratio, cash-flow/price ratio, dividend/price ratio, accruals, market beta, net share issues, daily variance, daily idiosyncratic variance, 1-month momentum, and 36-month momentum. The firms are grouped according to 20 industry sectors as in Moskowitz and Grinblatt (1999). The following sectors are considered:666The number between parenthesis indicates the number of firms in our sample that belong to each sector. Mining (602), Food (208), Apparel (161), Paper (81), Chemical (513), Petroleum (48), Construction (68), Primary Metals (133), Fabricated Metals (186), Machinery (710), Electrical Equipment (782), Transportation Equipment (166), Manufacturing (690), Railroads (25), Other transportation (157), Utilities (411), Department Stores (67), Retail (1018), Financial (3419), and Other (11).

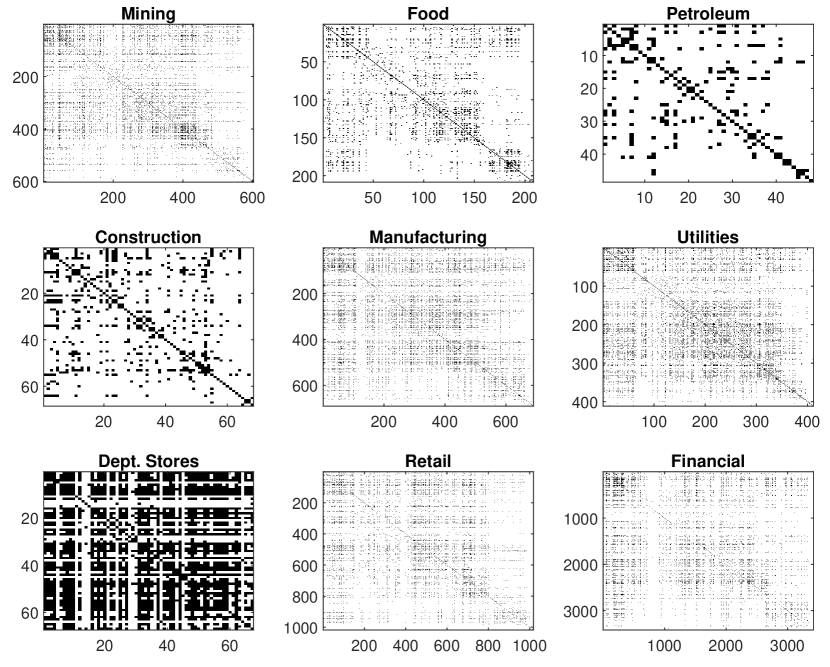

We start the analysis by looking at the correlation matrix for monthly returns of a sample of nine sectors: Mining, Food, Petroleum, Construction, Manufacturing, Utilities, Department Stores, Retail, and Financial. Figure 1 plots the correlations that are larger than 0.15 in absolute value. We test for the null of a diagonal covariance matrix. The null hypothesis is strongly rejected with -value much lower than 1% for all sectors. To conduct the test of the covariance matrix we use the simple sample estimator as described in the paper. However, the correlations plotted in Figure 1 and in the subsequent ones are based on the nonlinear shrinkage estimator proposed by Ledoit and Wolf (2020).

We estimate the correlations between all pairs of returns from specific sectors. The correlations that are higher than 0.15 in absolute value are shown as black dots.

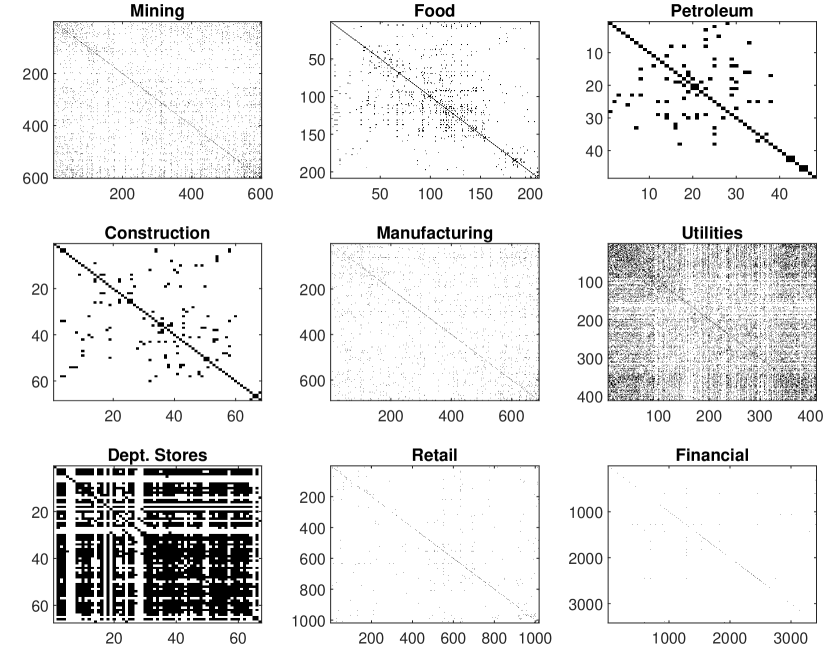

We proceed by regressing the daily returns on the observed 16 factors. Figure 2 presents the estimated correlations for the first-stage residuals, namely factor-adjusted returns. We focus on the nine sectors as before. The first-stage regression is efficient in removing the correlation within specific sectors in some cases. The most notable ones are Financial and Retail, followed by Construction, Petroleum, and Manufacturing. On the other hand, Utilities, Department Stores, Mining, and Food still display a dense covariance matrix.

We estimate the correlations between all pairs of residuals from the first-stage OLS regression on 16 observed factors from specific sectors. The correlations that are higher than 0.15 in absolute value are shown as black dots.

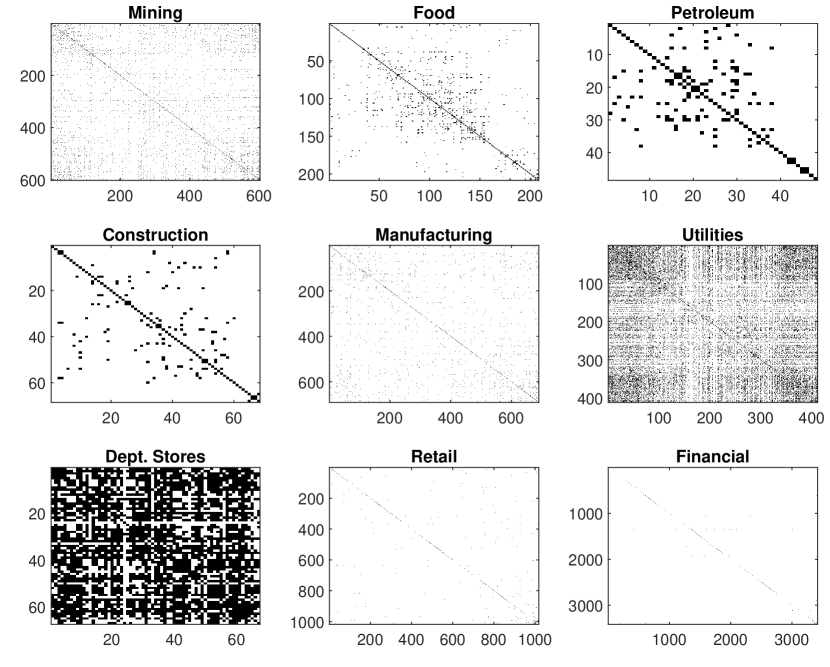

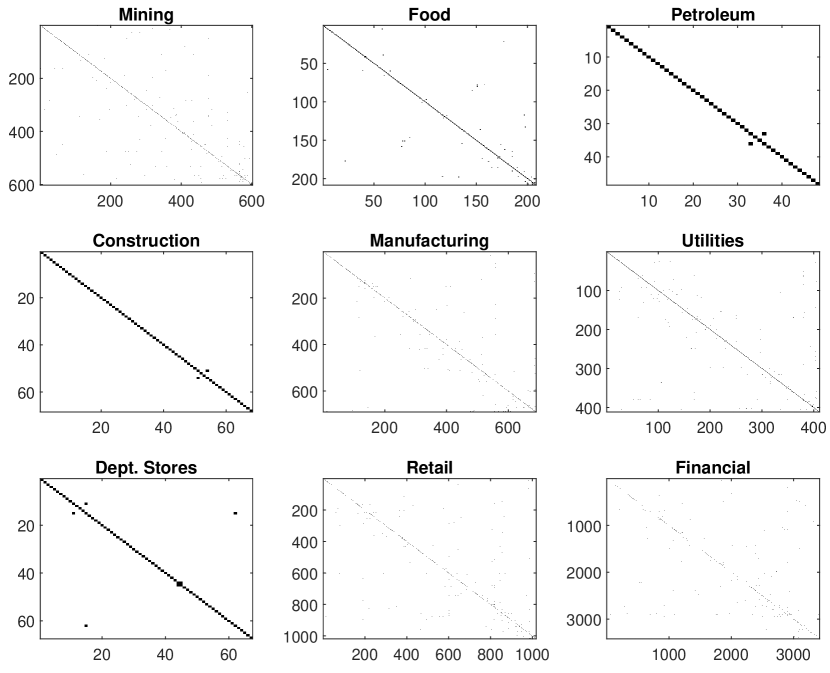

The second step is to conduct a principal component analysis on the residuals of the first stage. The eigenvalue ratio procedure selects two factors, while all four information criteria points to a single factor. We proceed with two factors. Note that, by construction, the principal component factors are orthogonal to all the 16 risk factors considered in the first stage. Figure 3 shows the estimated correlations for the residuals (idiosyncratic component) of the second-stage. The latent factor is not able to reduce the correlations within each sector. However, when we consider the partial correlations the conclusions are much different. As can be seen from Figure 4 that the partial correlation matrices are (almost) diagonal. In addition, we are not able to reject the null of a diagonal covariance matrix at a 5% significance level.

We estimate the correlations between all pairs of residuals from the second-stage principal component analysis from specific sectors. The correlations that are higher than 0.15 in absolute value are shown as black dots.

We estimate the partial correlations between all pairs of residuals from the second-stage LASSO regression from specific sectors. The correlations that are higher than 0.15 in absolute value are shown as black dots.

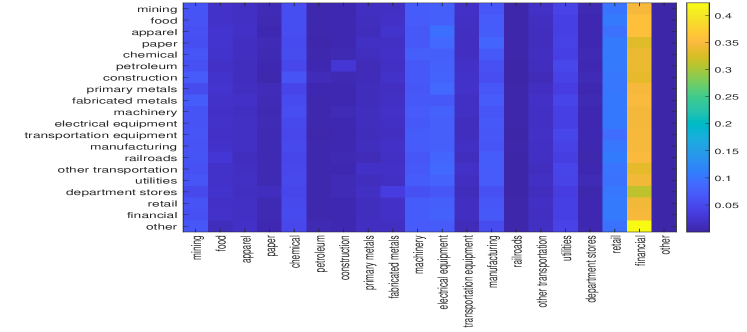

To shed some light on the links among different sectors, we report how often variables from sector are selected in the third-stage LASSO regression for firms in sector . The numbers are normalized by the total number of firms in each sector and are presented in Figure 5. The most interesting fact is that covariates from the financial sector are the ones most frequently selected for all the other sectors. Other sectors, such as Mining, Chemical, Machinery, Electrical Equipment, Manufacturing, and Retail are also frequently selected. This may indicate that there are industry factors, specifically a “financial factor”, that is unmodeled in the first two stages. However, if we augment the set of regressors in the first stage by the value-weighted portfolio from the financial sector, although the remaining dependence among firms is attenuated, particularly for Department Stores, we do not get close to an exact factor model. This finding suggests that there are hidden links among firms.

We report how often the variables from column sectors are selected in the third-stage LASSO regression for firms on row sectors. The numbers are normalized by the total number of firms in each sector.

4.2 Forecasting US Industrial Production

The second application consists of forecasting monthly US industrial production using a large set of monthly macroeconomic variables. We compare four different models: (1) Autoregressive model; (2) Sparse LASSO Regression (SR); (3) Principal Component Regression (PCR); and (4) FarmPredict.

We use variables from the August 2022 vintage of the FRED-MD database, which is a large monthly macroeconomic dataset designed for empirical analysis in data-rich macroeconomic environments. The dataset is updated in real-time through the FRED database and is available from Michael McCraken’s webpage.777https://research.stlouisfed.org/econ/mccracken/fred-databases/. For further details, we refer to McCracken and Ng (2016). .

Our sample extends from January 1960 to December 2019 (719 observations), and only variables with all observations in the period are used (122 variables). The dataset is divided into eight groups: (i) output and income; (ii) labor market; (iii) housing; (iv) consumption, orders, and inventories; (v) money and credit; (vi) interest and exchange rates; (vii) prices; and (viii) stock market. Finally, all series are transformed in order to become stationary.

In order to highlight the gains of exploring all relevant information in the dataset, we construct one-step ahead forecasts for the first-order difference of the logarithm of the monthly industrial production index (IP, growth rate): .

We compare the following models:

-

1.

Autoregressive model (AR):

where are OLS estimates. The value of is selected by BIC.

-

2.

Sparse regression (SR):

are LASSO estimates and with . The penalty parameter is selected by modified BIC as in Wang, Li and Leng (2009).

-

3.

Principal Component Regression (PCR):

where is the estimate of the vector of factors given by the first principal components of with being the sample average of . The parameters of the model are computed by OLS regression of on a constant and lags of . The lag is selected by BIC.

-

4.

AR - Principal Component Regression (AR-PCR):

where is the estimate of the vector of factors given by the first principal components of with being the sample average of . The parameters of the model are computed by OLS regression of on a constant, its own lags and lags of . The lag orders and are selected by BIC.

-

5.

FarmPredict:

where and , . The estimates , , are given by LASSO. The penalty parameter is selected by the modified BIC and the value of is set to 24.

The forecasts are based on a rolling-window framework of a fixed length of 480 observations, starting in January 1960. Therefore, the forecasts start on January 1990. The last forecasts are for December 2019. Note that the AR model only considers information concerning the own past of the variable of interest. SR and PCR/AR-PCR/ expand the information by two opposing routes. While SR uses a sparse combination of the set of variables, PCR and AR-PCR consider a factor structure (dense model). In the case of AR-PCR, lags of the dependent variable are also included. FarmPredict combines these two approaches and uses the full information available. The number of factors is set to 1.

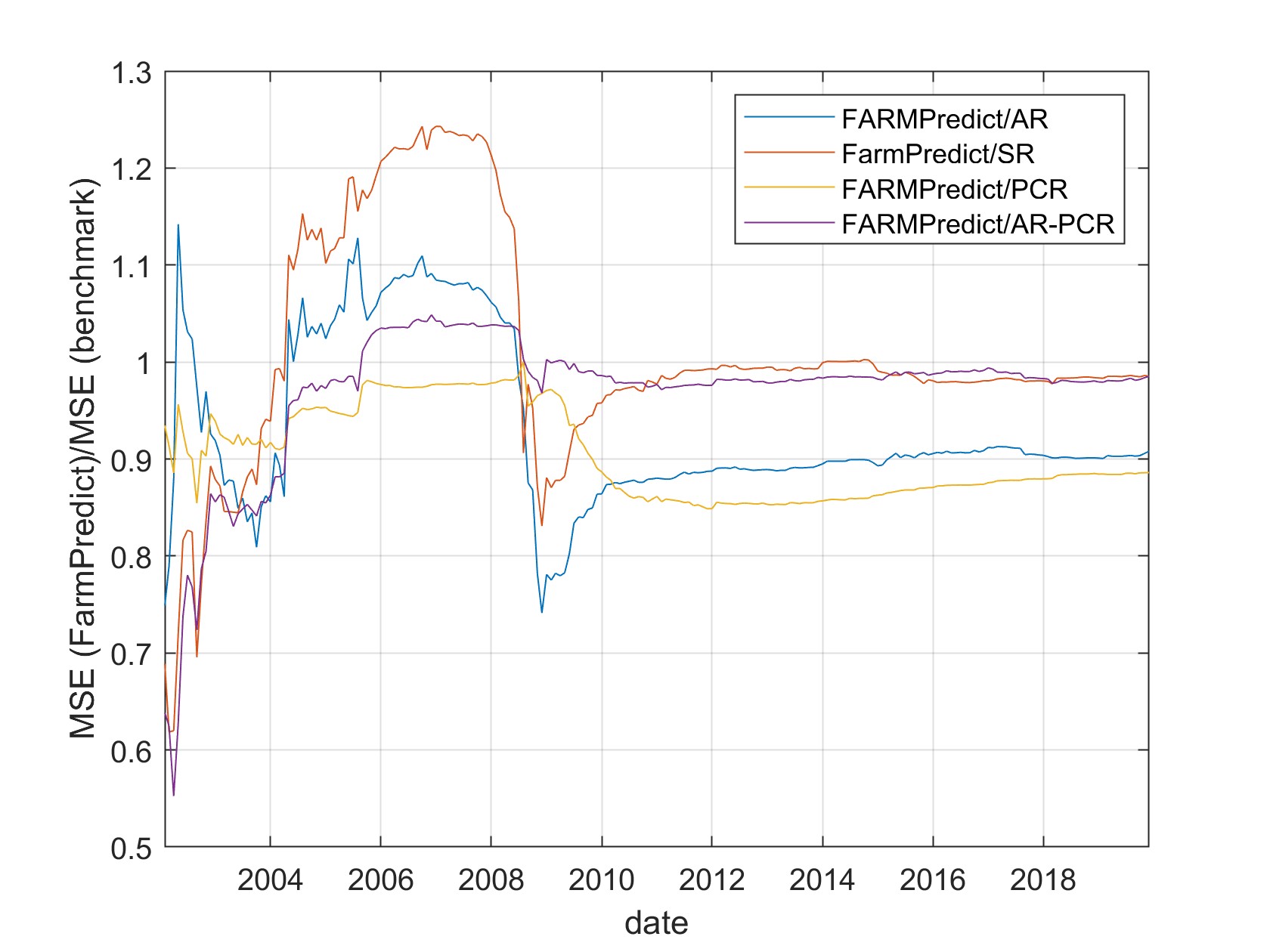

Figure 6 reports the ratios of cumulative MSE of the FarmPredict model against the cumulative MSE of the other benchmarks over the forecasting period. Several conclusions emerge from the plot. First, FarmPredict outperforms the PCR model over the entire out-of-sample period. It is also, in general, superior to the AR, SR, and AR-PCR models, apart from 2004 and 2008. During this period, the economy experienced housing and financial crises. Furthermore, the number of out-of-sample forecasting periods was also quite small. It is clear that the performance of FarmPredict improves drastically after 2008, and over the entire sample, the MSE ratio of the FarmPredict model over the AR benchmark is 0.9080, while the SR, PCR, and AR-PCR models have the following ratios, respectively: 0.9217, 1.0249, and 0.9215.

In the figure we report the cumulative ratios of the mean squared errors (MSE) of the FarmPredict model and the other benchmarks over the rolling windows.

5 Conclusions

We propose a new methodology that bridges the gap between sparse regressions and factor models and evaluates the gains of increasing the information set via factor augmentation. Our proposal consists of several steps. In the first one, we filter the data for known factors (trends, seasonal adjustments, covariates). In the second step, we estimate a latent factor structure. Finally, in the last part of the procedure, we estimate a sparse regression for the idiosyncratic components. We also propose a new test for remaining structures in both high-dimensional covariance and partial covariance matrices. Our test can be used to evaluate the benefits of adding more structure to the model. Our paper has also a number of important side results. First, we proved the consistency of kernel estimation of long-run covariance matrices in high dimensions where both the number of observations and variables grows. Second, we derive the theoretical properties of factor estimation on the residuals of a first-step process. Third, the proposed test can be used as a diagnostic tool for factor models.

We evaluate our methodology with simulations and real data. The simulations show the test has good size and power properties even when the true number of factors is unknown and must be determined from the data. If the number of factors is underestimated, we observe size distortions. In particular, this is the case when the eigenvalue ratio test is used to determine the number of latent factors. The simulations also show that there are major informational gains when combining factor models and sparse regressions in a forecasting exercise. Two applications are considered.

[Acknowledgments] Medeiros gratefully acknowledges the partial financial support from CNPq and CAPES. Fan’s research is partially supported by ONR grant N00014-22-1-2340 and NSF grants DMS-2210833, DMS-2053832, and DMS-2052926. We are grateful to Caio Almeida, Matteo Barigozzi, Gilberto Boareto, Gustavo Bulhões, Giuseppe Cavaliere, Frank Diebold, Bruno Ferman, Marcelo Fernandes, Claudio Flores, Conrado Garcia, Eric Ghysels, Alexander Giessing, Nathalie Gimenes, Marcelo J. Moreira, Henrique Pires, Yuri Saporito, and Rodrigo Targino for helpful comments. We also thank seminar participants at the SofiE online seminar series, Princeton University, the University of Amsterdam, the University of Pennsylvania, the University of Illinois at Urbana-Champaign, the Federal University of São Carlos, Rutgers University, the University of North Carolina at Chapel Hill, the University of Chicago, the University of California at Riverside, and Columbia University for a number of valuable comments. Finally, we are deeply grateful to Michele Lenza, Eduardo F. Mendes, and Michael Wolf for the careful reading of the paper and the many insightful discussions which led to a much-improved version of this manuscript. This manuscript has been also presented at a number of conferences, and we thank all the participants for their very useful comments.

References

- Abadie and Gardeazabal (2003) {barticle}[author] \bauthor\bsnmAbadie, \bfnmA.\binitsA. and \bauthor\bsnmGardeazabal, \bfnmJ.\binitsJ. (\byear2003). \btitleThe Economic Costs of Conflict: A Case Study of the Basque Country. \bjournalAmerican Economic Review \bvolume93 \bpages113–132. \endbibitem

- Agarwal, Negahban and Wainwright (2012) {barticle}[author] \bauthor\bsnmAgarwal, \bfnmAlekh\binitsA., \bauthor\bsnmNegahban, \bfnmSahand\binitsS. and \bauthor\bsnmWainwright, \bfnmMartin J\binitsM. J. (\byear2012). \btitleNoisy matrix decomposition via convex relaxation: Optimal rates in high dimensions. \bjournalThe Annals of Statistics \bvolume40 \bpages1171–1197. \endbibitem

- Andreou and Ghysels (2021) {barticle}[author] \bauthor\bsnmAndreou, \bfnmE.\binitsE. and \bauthor\bsnmGhysels, \bfnmE.\binitsE. (\byear2021). \btitlePredicting the VIX and the volatility risk premium: The role of short-run funding spreads Volatility Factors. \bjournalJournal of Econometrics \bvolume220 \bpages366-398. \endbibitem

- Andrews (1991) {barticle}[author] \bauthor\bsnmAndrews, \bfnmDonald W. K.\binitsD. W. K. (\byear1991). \btitleHeteroskedasticity and Autocorrelation Consistent Covariance Matrix Estimation. \bjournalEconometrica \bvolume59 \bpages817–858. \endbibitem

- Bai (2003) {barticle}[author] \bauthor\bsnmBai, \bfnmJ.\binitsJ. (\byear2003). \btitleInferential Theory for Factor Models of Large Dimensions. \bjournalEconometrica \bvolume71 \bpages2135–171. \endbibitem

- Bai (2009) {barticle}[author] \bauthor\bsnmBai, \bfnmJ.\binitsJ. (\byear2009). \btitlePanel data models with interactive fixed effects. \bjournalEconometrica \bvolume77 \bpages1229–1279. \endbibitem

- Bai and Liao (2017) {barticle}[author] \bauthor\bsnmBai, \bfnmJ.\binitsJ. and \bauthor\bsnmLiao, \bfnmY.\binitsY. (\byear2017). \btitleInferences in panel data with interactive effects using large covariance matrices. \bjournalJournal of Econometrics \bvolume200 \bpages59–78. \endbibitem

- Bai and Ng (2002) {barticle}[author] \bauthor\bsnmBai, \bfnmJ.\binitsJ. and \bauthor\bsnmNg, \bfnmS.\binitsS. (\byear2002). \btitleDetermining the Number of Factors in Approximate Factor Models. \bjournalEconometrica \bvolume70 \bpages191–221. \endbibitem

- Bai and Ng (2006) {barticle}[author] \bauthor\bsnmBai, \bfnmJ.\binitsJ. and \bauthor\bsnmNg, \bfnmS.\binitsS. (\byear2006). \btitleConfidence intervals for diffusion index forecasts and inference for factor augmented regressions. \bjournalEconometrica \bvolume74 \bpages1133–1155. \endbibitem

- Barigozzi and Brownlees (2019) {barticle}[author] \bauthor\bsnmBarigozzi, \bfnmM.\binitsM. and \bauthor\bsnmBrownlees, \bfnmC.\binitsC. (\byear2019). \btitleNETS: Network estimation for time series. \bjournalJournal of Applied Econometrics \bvolume34 \bpages347–364. \endbibitem

- Barigozzi and Hallin (2016) {barticle}[author] \bauthor\bsnmBarigozzi, \bfnmM.\binitsM. and \bauthor\bsnmHallin, \bfnmM.\binitsM. (\byear2016). \btitleGeneralized dynamic factor models and volatilities: Recovering the market volatility shocks. \bjournalEconometrics Journal \bvolume19 \bpagesC33–C60. \endbibitem

- Barigozzi and Hallin (2017) {barticle}[author] \bauthor\bsnmBarigozzi, \bfnmM.\binitsM. and \bauthor\bsnmHallin, \bfnmM.\binitsM. (\byear2017). \btitleA network analysis of the volatility of high-dimensional financial series. \bjournalJournal of the Royal Statistical Society, Series C \bvolume66 \bpages581–605. \endbibitem

- Bernanke, Boivin and Eliasz (2005) {barticle}[author] \bauthor\bsnmBernanke, \bfnmB. S.\binitsB. S., \bauthor\bsnmBoivin, \bfnmJ.\binitsJ. and \bauthor\bsnmEliasz, \bfnmP.\binitsP. (\byear2005). \btitleMeasuring the Effects of Monetary Policy: A Factor-Augmented Vector Autoregressive (FAVAR) Approach. \bjournalThe Quarterly Journal of Economics \bvolume120 \bpages387–422. \endbibitem

- Brownlees, Gudmundsson and Lugosi (2020) {barticle}[author] \bauthor\bsnmBrownlees, \bfnmC.\binitsC., \bauthor\bsnmGudmundsson, \bfnmG. S.\binitsG. S. and \bauthor\bsnmLugosi, \bfnmG.\binitsG. (\byear2020). \btitleCommunity Detection in Partial Correlation Network Models. \bjournalJournal of Business & Economic Statistics. \bnoteforthcoming. \endbibitem

- Cai (2017) {barticle}[author] \bauthor\bsnmCai, \bfnmT. T.\binitsT. T. (\byear2017). \btitleGlobal Testing and Large-Scale Multiple Testing for High-Dimensional Covariance Structures. \bjournalAnnual Review of Statistics and its Application \bvolume4 \bpages4.1–4.24. \endbibitem

- Carvalho, Masini and Medeiros (2018) {barticle}[author] \bauthor\bsnmCarvalho, \bfnmC. V.\binitsC. V., \bauthor\bsnmMasini, \bfnmR.\binitsR. and \bauthor\bsnmMedeiros, \bfnmM. C.\binitsM. C. (\byear2018). \btitleArCo: An Artificial Counterfactual Approach for High-Dimensional Panel Time-Series Data. \bjournalJournal of Econometrics \bvolume207 \bpages352–380. \endbibitem

- Chernozhukov, Chetverikov and Kato (2013a) {barticle}[author] \bauthor\bsnmChernozhukov, \bfnmV.\binitsV., \bauthor\bsnmChetverikov, \bfnmD.\binitsD. and \bauthor\bsnmKato, \bfnmK.\binitsK. (\byear2013a). \btitleGaussian approximations and multiplier bootstrap for maxima of sums of high-dimensional random vectors. \bjournalAnnals of Statistics \bvolume41 \bpages2786–2819. \endbibitem

- Chernozhukov, Chetverikov and Kato (2013b) {bmisc}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmChetverikov, \bfnmDenis\binitsD. and \bauthor\bsnmKato, \bfnmKengo\binitsK. (\byear2013b). \btitleComparison and anti-concentration bounds for maxima of Gaussian random vectors. \bdoi10.48550/ARXIV.1301.4807 \endbibitem

- Chernozhukov, Chetverikov and Kato (2017) {bmisc}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmChetverikov, \bfnmDenis\binitsD. and \bauthor\bsnmKato, \bfnmKengo\binitsK. (\byear2017). \btitleDetailed proof of Nazarov’s inequality. \bdoi10.48550/ARXIV.1711.10696 \endbibitem

- Chernozhukov, Chetverikov and Kato (2018) {bmisc}[author] \bauthor\bsnmChernozhukov, \bfnmV.\binitsV., \bauthor\bsnmChetverikov, \bfnmD.\binitsD. and \bauthor\bsnmKato, \bfnmK.\binitsK. (\byear2018). \btitleInference on causal and structural parameters using many moment inequalities. \endbibitem

- Chernozhukov, Chetverikov and Koike (2020) {bmisc}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmChetverikov, \bfnmDenis\binitsD. and \bauthor\bsnmKoike, \bfnmYuta\binitsY. (\byear2020). \btitleNearly optimal central limit theorem and bootstrap approximations in high dimensions. \bdoi10.48550/ARXIV.2012.09513 \endbibitem

- Diebold and Yilmaz (2014) {barticle}[author] \bauthor\bsnmDiebold, \bfnmF. X.\binitsF. X. and \bauthor\bsnmYilmaz, \bfnmK.\binitsK. (\byear2014). \btitleOn the network topology of variance decompositions: Measuring the connectedness of financial firms. \bjournalJournal of Econometrics \bvolume182 \bpages119–134. \endbibitem

- Fama and French (1993) {barticle}[author] \bauthor\bsnmFama, \bfnmE. F.\binitsE. F. and \bauthor\bsnmFrench, \bfnmK. R.\binitsK. R. (\byear1993). \btitleCommon risk factors in the returns on stocks and bonds. \bjournalJournal of Financial Economics \bvolume33 \bpages3–56. \endbibitem

- Fama and French (2015) {barticle}[author] \bauthor\bsnmFama, \bfnmE. F.\binitsE. F. and \bauthor\bsnmFrench, \bfnmK. R.\binitsK. R. (\byear2015). \btitleA five-factor asset pricing model. \bjournalJournal of Financial Economics \bvolume116 \bpages1–22. \endbibitem

- Fan, Ke and Wang (2020) {barticle}[author] \bauthor\bsnmFan, \bfnmJ.\binitsJ., \bauthor\bsnmKe, \bfnmY.\binitsY. and \bauthor\bsnmWang, \bfnmK.\binitsK. (\byear2020). \btitleFactor-adjusted regularized model selection. \bjournalJournal of Econometrics \bvolume216 \bpages71–85. \endbibitem

- Fan, Li and Wang (2017) {barticle}[author] \bauthor\bsnmFan, \bfnmJ.\binitsJ., \bauthor\bsnmLi, \bfnmQ.\binitsQ. and \bauthor\bsnmWang, \bfnmY.\binitsY. (\byear2017). \btitleEstimation of high dimensional mean regression in the absence of symmetry and light tail assumptions. \bjournalJournal of the Royal Statistical Society, Series B \bvolume79 \bpages247–265. \endbibitem

- Fan, Liao and Mincheva (2013) {barticle}[author] \bauthor\bsnmFan, \bfnmJ.\binitsJ., \bauthor\bsnmLiao, \bfnmY.\binitsY. and \bauthor\bsnmMincheva, \bfnmM.\binitsM. (\byear2013). \btitleLarge covariance estimation by thresholding principal orthogonal complements. \bjournalJournal of the Royal Statistical Society, Series B \bvolume75 \bpages603–680. \endbibitem

- Fan, Masini and Medeiros (2020) {btechreport}[author] \bauthor\bsnmFan, \bfnmJ.\binitsJ., \bauthor\bsnmMasini, \bfnmR. P.\binitsR. P. and \bauthor\bsnmMedeiros, \bfnmM. C.\binitsM. C. (\byear2020). \btitleDo We Exploit all Information for Counterfactual Analysis? Benefits of Factor Models and Idiosyncratic Correction \btypeWorking Paper, \bpublisherPrinceton University. \endbibitem

- Fan et al. (2020) {bbook}[author] \bauthor\bsnmFan, \bfnmJ.\binitsJ., \bauthor\bsnmLi, \bfnmR.\binitsR., \bauthor\bsnmZhang, \bfnmC. H.\binitsC. H. and \bauthor\bsnmZou, \bfnmH.\binitsH. (\byear2020). \btitleStatistical Foundations of Data Science. \bpublisherCRC Press. \endbibitem

- Fang and Koike (2021) {barticle}[author] \bauthor\bsnmFang, \bfnmXiao\binitsX. and \bauthor\bsnmKoike, \bfnmYuta\binitsY. (\byear2021). \btitleHigh-dimensional central limit theorems by Stein’s method. \bjournalThe Annals of Applied Probability \bvolume31 \bpages1660 – 1686. \bdoi10.1214/20-AAP1629 \endbibitem

- Feng, Giglio and Xiu (2020) {barticle}[author] \bauthor\bsnmFeng, \bfnmG.\binitsG., \bauthor\bsnmGiglio, \bfnmS.\binitsS. and \bauthor\bsnmXiu, \bfnmD.\binitsD. (\byear2020). \btitleTaming the Factor Zoo: A Test of New Factors. \bjournalJournal of Finance \bvolume75 \bpages1327–1370. \endbibitem

- Gagliardini, Ossola and Scaillet (2019) {barticle}[author] \bauthor\bsnmGagliardini, \bfnmP.\binitsP., \bauthor\bsnmOssola, \bfnmE.\binitsE. and \bauthor\bsnmScaillet, \bfnmP.\binitsP. (\byear2019). \btitleA diagnostic criterion for approximate factor structure. \bjournalJournal of Econometrics \bvolume212 \bpages503–521. \endbibitem

- Gagliardini, Ossola and Scaillet (2020) {bincollection}[author] \bauthor\bsnmGagliardini, \bfnmP.\binitsP., \bauthor\bsnmOssola, \bfnmE.\binitsE. and \bauthor\bsnmScaillet, \bfnmP.\binitsP. (\byear2020). \btitleEstimation of large dimensional conditional factor models in finance. In \bbooktitleHandbook of Econometrics, (\beditor\bfnmS.\binitsS. \bsnmDurlauf, \beditor\bfnmL.\binitsL. \bsnmHansen, \beditor\bfnmJ.\binitsJ. \bsnmHeckman and \beditor\bfnmR.\binitsR. \bsnmMatzkin, eds.) \bvolumeVolume 7A \bpages219–282. \endbibitem

- Giannone, Lenza and Primiceri (2021) {barticle}[author] \bauthor\bsnmGiannone, \bfnmD.\binitsD., \bauthor\bsnmLenza, \bfnmM.\binitsM. and \bauthor\bsnmPrimiceri, \bfnmG.\binitsG. (\byear2021). \btitleEconomic Predictions with Big Data: The Illusion of Sparsity. \bjournalEconometrica \bvolume89 \bpages2409–2437. \endbibitem

- Giessing and Fan (2020) {bmisc}[author] \bauthor\bsnmGiessing, \bfnmA.\binitsA. and \bauthor\bsnmFan, \bfnmJ.\binitsJ. (\byear2020). \btitleBootstrapping -Statistics in High Dimensions. \endbibitem

- Gobillon and Magnac (2016) {barticle}[author] \bauthor\bsnmGobillon, \bfnmL.\binitsL. and \bauthor\bsnmMagnac, \bfnmT.\binitsT. (\byear2016). \btitleRegional Policy Evaluation: Interactive Fixed Effects and Synthetic Controls. \bjournalReview of Economics and Statistics \bvolume98 \bpages535–551. \endbibitem

- Horenstein (2013) {barticle}[author] \bauthor\bsnmHorenstein, \bfnmS. C. Ahn A. R.\binitsS. C. A. A. R. (\byear2013). \btitleEigenvalue Ratio Test for the Number of Factors. \bjournalEconometrica \bvolume81 \bpages1203–1227. \endbibitem

- Kock and Callot (2015) {barticle}[author] \bauthor\bsnmKock, \bfnmA. B.\binitsA. B. and \bauthor\bsnmCallot, \bfnmL.\binitsL. (\byear2015). \btitleOracle inequalities for high dimensional vector autoregressions. \bjournalJournal of Econometrics \bvolume186 \bpages325–344. \endbibitem

- Ledoit and Wolf (2020) {barticle}[author] \bauthor\bsnmLedoit, \bfnmO.\binitsO. and \bauthor\bsnmWolf, \bfnmM.\binitsM. (\byear2020). \btitleAnalytical nonlinear shrinkage of large-dimensional covariance matrices. \bjournalAnnals of Statistics. \bnoteforthcoming. \endbibitem

- Ledoit and Wolf (2021) {barticle}[author] \bauthor\bsnmLedoit, \bfnmO.\binitsO. and \bauthor\bsnmWolf, \bfnmM.\binitsM. (\byear2021). \btitleThe power of (non-)linear shrinking: A review and guide to covariance matrix estimation. \bjournalJournal of Financial Econometrics. \bnoteforthcoming. \endbibitem

- Masini, Medeiros and Mendes (2019) {btechreport}[author] \bauthor\bsnmMasini, \bfnmR. P.\binitsR. P., \bauthor\bsnmMedeiros, \bfnmM. C.\binitsM. C. and \bauthor\bsnmMendes, \bfnmE. F.\binitsE. F. (\byear2019). \btitleRegularized Estimation of High-Dimensional Vector AutoRegressions with Weakly Dependent Innovations \btypeTechnical Report No. \bnumber1912.09002, \bpublisherarxiv. \endbibitem

- McCracken and Ng (2016) {barticle}[author] \bauthor\bsnmMcCracken, \bfnmM.\binitsM. and \bauthor\bsnmNg, \bfnmS.\binitsS. (\byear2016). \btitleFRED-MD: A Monthly Database For Macroeconomic Research. \bjournalJournal of Business & Economic Statistics \bvolume34 \bpages574–589. \endbibitem

- Medeiros and Mendes (2016) {barticle}[author] \bauthor\bsnmMedeiros, \bfnmM. C.\binitsM. C. and \bauthor\bsnmMendes, \bfnmE. F.\binitsE. F. (\byear2016). \btitle-regularization of high-dimensional time-series models with non-Gaussian and heteroskedastic errors. \bjournalJournal of Econometrics \bvolume191 \bpages255–271. \endbibitem

- Merlevède, Peligrad and Rio (2011) {barticle}[author] \bauthor\bsnmMerlevède, \bfnmFlorence\binitsF., \bauthor\bsnmPeligrad, \bfnmMagda\binitsM. and \bauthor\bsnmRio, \bfnmEmmanuel\binitsE. (\byear2011). \btitleA Bernstein type inequality and moderate deviations for weakly dependent sequences. \bjournalProbability Theory and Related Fields \bvolume151 \bpages435-474. \bdoi10.1007/s00440-010-0304-9 \endbibitem

- Moon and Weidner (2015) {barticle}[author] \bauthor\bsnmMoon, \bfnmR.\binitsR. and \bauthor\bsnmWeidner, \bfnmM.\binitsM. (\byear2015). \btitleLinear regression for panel with unknown number of factors as interactive fixed effects. \bjournalEconometrica \bvolume83 \bpages1543–1579. \endbibitem

- Moskowitz and Grinblatt (1999) {barticle}[author] \bauthor\bsnmMoskowitz, \bfnmT. J.\binitsT. J. and \bauthor\bsnmGrinblatt, \bfnmM.\binitsM. (\byear1999). \btitleDo industries explain momentum? \bjournalJournal of Finance \bvolume54 \bpages1249–1290. \endbibitem

- Negahban et al. (2012) {barticle}[author] \bauthor\bsnmNegahban, \bfnmS. N.\binitsS. N., \bauthor\bsnmRavikumar, \bfnmP.\binitsP., \bauthor\bsnmWainwright, \bfnmM. J.\binitsM. J. and \bauthor\bsnmYu, \bfnmB.\binitsB. (\byear2012). \btitleA unified framework for high-dimensional analysis of -estimators with decomposable regularizers. \bjournalStatistical Science \bvolume27 \bpages538–557. \endbibitem

- Peng et al. (2009) {barticle}[author] \bauthor\bsnmPeng, \bfnmJ.\binitsJ., \bauthor\bsnmWang, \bfnmP.\binitsP., \bauthor\bsnmZhou, \bfnmN.\binitsN. and \bauthor\bsnmZhu, \bfnmJ.\binitsJ. (\byear2009). \btitlePartial correlation estimation by joint sparse regression models. \bjournalJournal of the American Statistical Association \bvolume104 \bpages735–746. \endbibitem

- Pesaran (2006) {barticle}[author] \bauthor\bsnmPesaran, \bfnmM. H.\binitsM. H. (\byear2006). \btitleEstimation and inference in large heterogeneous panels with a multifactor error structure. \bjournalEconometrica \bvolume74 \bpages967–1012. \endbibitem

- Rio (2017) {bbook}[author] \bauthor\bsnmRio, \bfnmEmmanuel\binitsE. (\byear2017). \btitleAsymptotic theory of weakly dependent random processes \bvolume80. \bpublisherSpringer. \endbibitem

- Stock and Watson (2002) {barticle}[author] \bauthor\bsnmStock, \bfnmJ.\binitsJ. and \bauthor\bsnmWatson, \bfnmM.\binitsM. (\byear2002). \btitleForecasting Using Principal Components from a Large Number of Predictors. \bjournalJournal of the American Statistical Association \bvolume97 \bpages1167–1179. \endbibitem

- van de Geer and Bühlmann (2009) {barticle}[author] \bauthor\bparticlevan de \bsnmGeer, \bfnmS. A.\binitsS. A. and \bauthor\bsnmBühlmann, \bfnmP.\binitsP. (\byear2009). \btitleOn the conditions used to prove oracle results for the Lasso. \bjournalElectronic Journal of Statistics \bvolume3 \bpages1360–1392. \endbibitem

- van der Vaart and Wellner (1996) {bbook}[author] \bauthor\bparticlevan der \bsnmVaart, \bfnmA. W.\binitsA. W. and \bauthor\bsnmWellner, \bfnmJ.\binitsJ. (\byear1996). \btitleWeak Convergence and Empirical Processes: With Applications to Statistics. \bpublisherSpringer. \endbibitem

- Wang, Li and Leng (2009) {barticle}[author] \bauthor\bsnmWang, \bfnmH.\binitsH., \bauthor\bsnmLi, \bfnmB.\binitsB. and \bauthor\bsnmLeng, \bfnmC.\binitsC. (\byear2009). \btitleShrinkage tuning parameter selection with a diverging number of parameters. \bjournalJournal of the Royal Statistical Society, Series B \bvolume71 \bpages671–683. \endbibitem

[sections]

CONTENTS

[sections]l1

S.1 Introduction

The goal of this supplement is to provide additional results as well as the proofs of all theoretical results in the main body of the paper.

This Supplementary Material is organized as follows. We start by discussing guidelines for practical implementation of the method in Section S.2. Section S.3 provides some additional simulation results. Section S.4 presents results for the case with geometric mixing and Exponential Tails. Section S.5 contains all the proofs of the results on paper. Finally, Section S.7 collects auxiliary lemmas.

S.2 Guide to Practice

The methodology in this paper involves several steps. The first step consists of identifying known covariates that we may want to control for. It may involve the removal of deterministic trends and seasonal effects, for instance. This can be done either by parametric or nonparametric regressions. It is important to notice, however, that the convergence rates of the estimations in the subsequent steps will be influenced by the convergence rate of the estimation in the first part of the procedure.

After the data are filtered in the first step, one can test for the remaining covariance structure. If the covariance matrix of the filtered data is (almost) diagonal, there is no need to estimate a latent factor structure, and the practitioner may jump directly to the third step. On the other hand, if the covariance of the filtered data is dense, a latent factor model should be considered, and the number of factors must be determined. To determine the number of factors, we consider either the eigenvalue ratio test of Horenstein (2013) or the information criteria put forward in Bai and Ng (2002). The factors can be estimated by the usual methods.

The next step involves a sparse regression in order to estimate any remaining links between idiosyncratic components. Before running the last step, we may test for a diagonal covariance matrix of the idiosyncratic terms. If the null is not rejected, there is no need for additional estimation. In case of rejection, we can proceed with a LASSO regression. We recommend that the penalty term is selected by some Information Criterion (IC) as advocated by Wang, Li and Leng (2009) and Medeiros and Mendes (2016). If out-of-sample forecasting is the goal, an additional final step is necessary. In this case, lags of factors and idiosyncratic terms must be determined. The practitioner may rely on the usual information criteria available.

Finally, concerning the estimation of the long-run matrices, the usual methods discussed in the literature can be used here to select the kernel and the bandwidth. We use the simple Bartlett kernel with bandwidth given as .

S.3 Simulation

In this section, we report simulation results divided into two parts. In the first one, we evaluate the finite-sample properties of the test for the remaining covariance structure. In the second part, we highlight the informational gains when considering both the common factors and the idiosyncratic component. We simulate 1,000 replications of the following model for various combinations of sample size () and number of variables ():

| (S.1) | ||||

| (S.2) | ||||

| (S.3) | ||||

| (S.4) |

where is the indicator function, is a sequence of independent t-distributed random variables with 10 degrees of freedom, and is a sequence of -dimensional mutually independent random vectors t-distributed with 10 degrees of freedom. Furthermore, and are mutually independent for all time periods, factors and variables. For each Monte Carlo replication, the vector of loadings is sampled from a Gaussian distribution with mean -6 and standard deviation 0.2 for and mean 2 and unit variance for . The coefficients , , , and are equal to zero or 0.8, 0.9, -0.7, and 0.5, respectively. We set the number of factors, , equal to 3. can be either 0 or 0.5. Note that equation (S.3) is a special case of equation (2.2) with .

S.3.1 Test for Remaining Covariance Structure

We start by reporting results for the test of no remaining structure on the covariance matrix of . The null hypothesis considered is that all the covariances between the first variable () and the remaining ones are all zero. For size simulations we set in the DGP. To evaluate the effects of factor estimation as well as the methods in selecting the number of factors, we consider the following scenarios: (1) factors are known, and there is no estimation involved; (2) factors are estimated by principal components, but the number of factors is known; (3) the number of factors is determined by the eigenvalue ratio procedure of Horenstein (2013); (4)-(7) the number of factors is determined by one of the four information criteria proposed by Bai and Ng (2002) as defined by

where and .

Table S.1 and S.2 reports the results of the empirical size of test for different significance levels. We consider the case of in Table S.1 and in S.2. The tables present the results when the factors are known in panel (a), the factors are unknown but the number of factors is known in panel (b), or the number of factors is estimated either by the information criterion in panel (c) or the eigenvalue ratio procedure in panel (d).