He et al.

Adaptive Importance Sampling

Adaptive Importance Sampling for Efficient Stochastic Root Finding and Quantile Estimation

Shengyi He

\AFFDepartment of Industrial Engineering & Operations Research, Columbia University, New York, NY 10027, USA, \EMAILsh3972@columbia.edu \AUTHORGuangxin Jiang\AFFSchool of Management, Harbin Institute of Technology, Harbin, Heilongjiang 150001, China,

\EMAILgxjiang@hit.edu.cn

\AUTHORHenry Lam

\AFFDepartment of Industrial Engineering & Operations Research, Columbia University, New York, NY 10027, USA, \EMAILkhl2114@columbia.edu

\AUTHORMichael C. Fu

\AFFThe Robert H. Smith School of Business, Institute for Systems Research, University of Maryland, College Park, MD 20742, USA, \EMAILmfu@umd.edu

In solving simulation-based stochastic root-finding or optimization problems that involve rare events, such as in extreme quantile estimation, running crude Monte Carlo can be prohibitively inefficient. To address this issue, importance sampling can be employed to drive down the sampling error to a desirable level. However, selecting a good importance sampler requires knowledge of the solution to the problem at hand, which is the goal to begin with and thus forms a circular challenge. We investigate the use of adaptive importance sampling to untie this circularity. Our procedure sequentially updates the importance sampler to reach the optimal sampler and the optimal solution simultaneously, and can be embedded in both sample average approximation and stochastic approximation-type algorithms. Our theoretical analysis establishes strong consistency and asymptotic normality of the resulting estimators. We also demonstrate, via a minimax perspective, the key role of using adaptivity in controlling asymptotic errors. Finally, we illustrate the effectiveness of our approach via numerical experiments.

Monte Carlo simulation, importance sampling, adaptive algorithms, quantile estimation, stochastic root finding, stochastic optimization, central limit theorem

1 Introduction

A stochastic root-finding problem refers to the search of a solution to an equation , where the function lacks analytical tractability and can only be accessed via noisy simulation. This problem is intimately related to stochastic optimization, where is then the gradient and we solve the first-order optimality conditions. Such problems are fundamental in many fields, including operations research and data science. Examples include quantile estimation where involves the probability distribution function (Wetherill 1963), continuous-space simulation optimization (Fu 2015), commonly used machine learning algorithms where model parameters are trained via empirical risk minimization (Bottou et al. 2018), and other applications such as the characterizations of convex risk measures as the roots of decreasing functions (Dunkel and Weber 2010).

In this paper, we are interested in situations where the root-finding problem involves extremal or rare-event considerations. A primary example is extreme quantile estimation, in which the target probability level can be very close to 0 or 1 (e.g., ). In this case, crude Monte Carlo can be prohibitively inefficient, as it takes roughly a sample size reciprocal to the target probability level to obtain meaningful statistical information. This phenomenon occurs generally in other examples involving rare events: As long as the solution depends crucially on samples in a region that is infrequently hit, the effectiveness of crude Monte Carlo could be substantially hampered.

To address estimation challenges related to rare events, importance sampling (IS) is commonly used (e.g., Asmussen and Glynn 2007 Chapters 5 and 6; Glasserman 2003 Chapter 4; Rubinstein and Kroese 2016 Chapter 5). IS is a variance reduction technique that draws samples using a distribution distinct from the original (the importance sampler) that hits the rare-event region more often. At the same time, the estimator maintains unbiasedness via a multiplication of the sample output with the so-called likelihood ratio. If the IS distribution is carefully chosen, so that the hitting frequency and the likelihood ratio magnitude are properly controlled, then the estimation efficiency can be significantly boosted. Choosing and analyzing good IS schemes have been a focus in many studies (see, e.g., the surveys Bucklew 2004, Juneja and Shahabuddin 2006, Blanchet and Lam 2012).

Although there exists a rich literature on IS, there are relatively few theoretical results on applying IS to resolve the efficiency issues for crude Monte Carlo in extreme quantile estimation and other root-finding or stochastic optimization problems involving rare events. Most of the literature in IS focuses on the estimation of a target probability or expectation-type risk quantities, and the question is whether the same techniques can be easily adapted for root-finding. To this end, IS is known to be sensitive to the input choice: That is, let us suppose we already have found a good parametric IS distribution class, in the sense that there is a parameter value in the class that achieves high efficiency in the resulting sampler. If this parameter is wrongly chosen, the efficiency could be bad – in some cases even worse than crude Monte Carlo. In other words, choosing good parameter values is crucial to the success of IS. On top of this, this value typically depends highly on the problem specification (e.g., Glynn and Iglehart 1989, Sadowsky 1991, L’Ecuyer et al. 2010).

To illustrate the above, suppose we want to estimate for some high exceedance level and model output . Consider an IS distribution class, say for that is parameterized over . The efficiency of the resulting IS for estimating could be highly sensitive to the choice of , which in turn depends on . That is, we can think of a good or an optimal to be for a specific function . We argue that this can cause significant challenges in root-finding, as the dependence of parameter choice on the target probability’s specification will result in a circular choice in an inverse problem like root-finding. In this example, suppose we would like to use the IS distribution to improve the efficiency in estimating the extreme quantile of . Then in principle we would like to select , where is the quantile. This, however, is clearly not obtainable, as it requires knowledge on the quantile , which is what we want to determine in the first place.

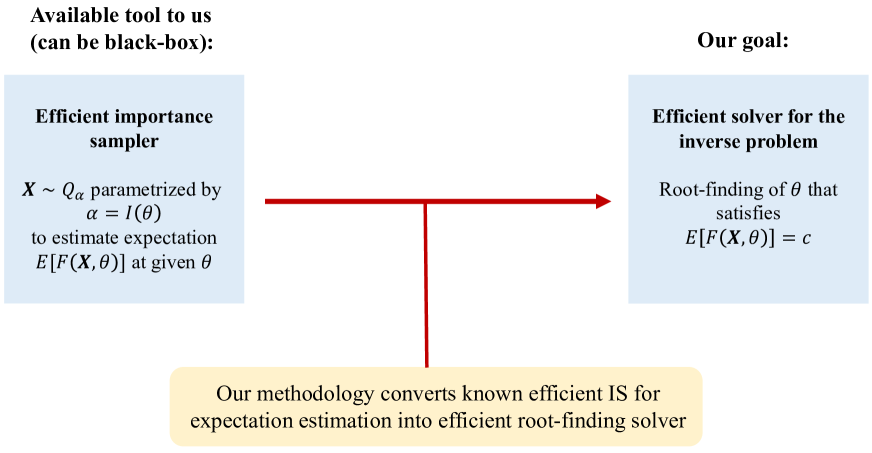

Our main goal in this paper is to provide a mechanism to untie the above circularity. Specifically, given an efficient IS scheme designed to estimate a target probability or expectation, we offer a mechanism to convert this IS into one that is also efficient for the inverse problem of root-finding (see Figure 1). Our conversion mechanism does not require knowledge on how the initial IS works, i.e., the initial IS algorithm can be a black box, and the only thing we know is that it works well for the initial estimation problem.

We propose an adaptive sampling approach that aims to iteratively reach the root and update the IS parameter simultaneously. That is, at each iterative step we use the best myopic parameter value pretending that the target estimation problem is specified by the current root estimate. Using this IS, we generate new samples and update the root, which is then used to update the IS parameter again in a continuing manner.

We support the necessity of the iterative approach above from a minimax perspective. If one does not allow iteration, then, since we do not know the root and hence the proper IS parameter, our root-finding procedure can have a large error in the worst case, as the parameter value that is used can misalign badly with the true root. On the other hand, we demonstrate that our iterative approach may achieve a substantial reduction of estimation error, regardless of the location of the root, by attaining a lower bound on the worst-case error dictated by a weak duality of the minimax error. Put in another way, this means that our approach exhibits the same asymptotic error as if we know the root in advance, and thus is the best possible within the considered class of IS.

We discuss how to embed our adaptive IS into the two main numerical procedures for root-finding and stochastic optimization. First is sample average approximation (SAA), which replaces an unknown expectation with the empirical counterpart and applies deterministic solvers to locate the root (Shapiro 2003). In quantile estimation, this corresponds to using the empirical quantile. The second main approach is stochastic approximation (SA), which can be viewed as a stochastic analog of the quasi-Newton method in deterministic optimization (Quarteroni et al. 2007, Kushner and Yin 2003). SA iteratively updates the solution estimate by taking incremental steps to get closer to the true solution. In quantile estimation, this means adjusting the current quantile estimate by adding or subtracting a step depending on whether the new sample falls above or below the quantile estimate. Our adaptive IS can be embedded easily in both SAA and SA. In SAA, our adaptive approach leads to an iterative run of SAA programs, each with additional new samples. While this could be computationally intense for some problems, this approach is well suited for extreme quantile estimation, as each SAA corresponds simply to finding an empirical quantile. On the other hand, since SA is already an iterative approach, our IS can be naturally embedded at every iteration and does not cause extra computational complexity.

We investigate the consistency and central limit convergence of our adaptive IS embedded in both SAA and SA. These convergence theorems characterize the asymptotic behavior to support the superiority of our approach in performing at the same level as if we know the solution in advance, which is the best possible when using the considered IS class. Our technical developments require developing asymptotic normality results for a variant of SAA constructed from dependent data via martingale differences, and combining with functional complexity measures such as bracketing numbers, which are suitably adapted for our setting. Finally, we conduct experiments to validate our theoretical claims by comparing with other benchmarks.

The rest of this paper is as follows. Section 2 first reviews related literature. Section 3 formulates the stochastic root-finding problems and presents the challenges in applying standard IS via a worst-case analysis on the asymptotic variances. Section 4 presents the main procedures in embedding our adaptive IS in SAA and SA, and provides theoretical guarantees in single-dimensional settings. Section 5 specializes to quantile estimation. Section 6 generalizes our framework to multi-dimensional problems. Section 7 applies our approach on numerical examples, including analyses to verify required assumptions. Section 8 concludes our paper. Proofs of all the theoretical results are provided in the Appendix.

2 Related Work

Our work is related to several others on quantile estimation that, similar to our approach, choose IS distributions adaptively in simulation rounds. Morio (2012) proposes a nonparametric approach using a Gaussian kernel density to build the IS. Egloff and Leippold (2010) updates the IS parameter using an SA procedure similar to our proposed IS embedding, leading to a consistent quantile estimator where the parameter converges to the variance minimizer, but they do not analyze asymptotic variance. Pan et al. (2020) considers adaptive IS for quantile estimation using a two-layer model where the inner layer is a black box, and are able to establish consistency and demonstrate variance reduction empirically by comparing with crude Monte Carlo.

The closest work to ours is Bardou et al. (2009), which considers estimation of Value-at-Risk (VaR) and conditional Value-at-Risk (CVaR), and also views the optimal IS parameter as a solution to a stochastic root-finding problem. An iterative (SA) algorithm is proposed, for which they establish a central limit theorem (CLT) showing that this approach will lead to the smallest asymptotic variance among the chosen IS class. Our work considers a general framework to translate efficient IS from expectation estimation to stochastic root-finding, and generalizes Bardou et al. (2009) in two main directions: (i) We can handle general parametrizations, whereas their work considers only location translations and exponential twists. (ii) We embed our adaptive IS in both SA and SAA, whereas they consider only the SA setting. In particular, our analysis of SAA is substantially more involved and requires developing new tools via empirical process theory.

We also briefly mention some variance reduction in quantile estimation using other adaptive methods. Cannamela and Iooss (2008) uses a reduced model to design the variance reduction scheme. Hu and Su (2008) studies the use of adaptive IS in bootstrap quantile estimation. Other variance reduction approaches for quantile estimation that do not use adaptive methods include classical IS (Glynn 1996, Sun and Hong 2010), control variates (Hsu and Nelson 1990, Hesterberg and Nelson 1998), Latin hypercube sampling (Jin et al. 2003, Dong and Nakayama 2017), stratified sampling (Glasserman et al. 2000, Chu and Nakayama 2012), and splitting (Guyader et al. 2011).

Work on using adaptive IS for expected value estimation is abundant, and we mention just a few here. Au and Beck (1999) uses the Metropolis algorithm combined with kernel method to get an approximation to the optimal IS distribution. Fu and Su (2002) and Egloff et al. (2005) find an optimal importance sampler using SA and then use this sampler to estimate the expectation. Ryu and Boyd (2015) updates the IS sampler simultaneously with the expectation estimation. Cornuet et al. (2012) adaptively chooses the IS density by fitting the moments and reweights all of the past samples in each step. Kollman et al. (1999) and Ahamed et al. (2006) use adaptive IS along the time horizon to estimate the first passage of Markov chains and provide convergence guarantees. A comprehensive review of adaptive IS for expectation estimation can be found in Bugallo et al. (2017).

Since our adaptive method is built on IS samplers for expectation estimation where rare events are involved, our work naturally relates to rare event simulation. Bucklew (2004), Juneja and Shahabuddin (2006) and Blanchet and Lam (2012) provide surveys on the literature. Common approaches to design good IS for rare-event estimation utilize large deviations (Budhiraja and Dupuis 2019) by scrutinizing the exponential twist in the rate function (Nicola et al. 2001, Dupuis et al. 2012, Collamore 2002, Blanchet et al. 2019, Blanchet and Lam 2014), which also leads to the dominating point method (Sadowsky and Bucklew 1990, Dieker and Mandjes 2005, Owen et al. 2019), subsolution approaches (Dupuis et al. 2009, Blanchet et al. 2012a), and mixture-based schemes that are especially useful in heavy-tailed problems (Blanchet and Glynn 2008, Blanchet and Liu 2008, Chen et al. 2019, Blanchet et al. 2012b, Murthy et al. 2015, Hult and Svensson 2012). A more closely related approach to our study is the large body of work on the cross-entropy method (Rubinstein and Kroese 2004, 2016, de Boer et al. 2005), which originally was used to design IS for estimating rare-event probabilities and later was applied also to root-finding and optimization. This approach involves iteratively updating the IS parameters by minimizing the Kullback-Leibler divergence between the considered IS class and a zero-variance estimator. This latter step typically results in an SAA problem constructed from samples drawn from the most recent IS. While our adaptive IS and cross entropy have similar characteristics in using sequential IS updates and SAA formulations, the settings and the formulated SAA are different. The SAA in cross entropy is an empirical counterpart of the Kullback-Leibler divergence minimization. In contrast, our SAA, or SA, arises from the objective function in our target root-finding problem, and we assume a priori availability of a good IS for the corresponding expectation estimation problem. As a result, the guarantees we achieve are also different from the cross-entropy method. Finally, we mention extensions and variants to cross entropy such as model reference adaptive search (Hu et al. 2007) for the optimization setting and methods using, e.g., Markov chain Monte Carlo (Botev et al. 2013, Grace et al. 2014, Chan and Kroese 2012, Botev and L’Ecuyer 2020).

We briefly review methods for stochastic root-finding and optimization problems, where SAA and SA are commonly used. The Robbins-Monro SA (RM-SA) algorithm (Robbins and Monro 1951) is one of the most widely used stochastic root-finding and optimization methods, which can be viewed as a stochastic counterpart to the quasi-Newton iteration in solving deterministic root-finding problems. To increase robustness and alleviate the well-known sensitivity of RM-SA to its stepsize sequence, iterate averaging, first proposed by Polyak and Juditsky (1992), is often used. Other recent variants for improving the practical performance of the SA method include robust SA (Nemirovski et al. 2009), accelerated SA (Ghadimi and Lan 2013), and the secant-tangent averaged SA (Chau et al. 2014, 2020). General finite-time bounds for SA can be found in, e.g., Broadie et al. (2011) and Srikant and Ying (2019). More details of SA can be found in Chau and Fu (2015), Kushner and Yin (2003), Borkar (2009), and the references therein.

The SAA method (Shapiro et al. 2014, Kim et al. 2015), also known as the Monte Carlo sampling method (Shapiro 2003, Shapiro and Nemirovski 2005, Homem-de-Mello and Bayraksan 2014), is another commonly used technique for stochastic root-finding and optimization. Theoretical properties like consistency and asymptotic normality of SAA can be found in Robinson (1996) and Kleywegt et al. (2002). The lines of work Mak et al. (1999), Bayraksan and Morton (2006), Bayraksan and Morton (2011), Freimer et al. (2012), Lam and Zhou (2017) and Lam and Qian (2018) study the statistical properties and estimation of optimality gaps in SAA. To improve computational efficiency, the retrospective approximation method is proposed to generate a sequence of SAA problems with progressively increasing sample size and then solve these problems with decreasing error tolerances (Pasupathy and Schmeiser 2009, Pasuapthy 2010).

Recently, the probabilistic bisection algorithm (PBA), first proposed by Horstein (1963), has been applied to stochastic root-finding problems. Waeber et al. (2013) derives a PBA where the expected absolute residuals converge to zero at a geometric rate, and Frazier et al. (2019) proposes an extended PBA that has a convergence rate arbitrarily close to, but slower than, the rate of SA. Rodriguez and Ludkovski (2020) extends PBA to unknown sampling distributions and location-dependent settings. More methods for stochastic root-finding problems can be found in Pasupathy and Kim (2011), Waeber (2013), and the references therein.

3 Problem Setting and Motivation

We consider a stochastic root-finding problem in the following standard form. Let be a vector-valued function . Let be an unbiased observation for generated from simulation, where and is a random vector with probability distribution . We are interested in finding the unique root to the equation

| (1) |

where denotes the expectation under . Our premise is that the function lacks analytical tractability and can only be accessed via the unbiased simulation output . Important examples that can be cast in the above general formulation include:

Example 3.1 (Quantile estimation)

We are interested in finding the th quantile of a random output, say , that can be simulated. Denote as the cumulative distribution function of . This problem is equivalent to finding the root of

which is (1) with and .

Example 3.2 (Stochastic optimization)

We are interested in an optimization problem

where we have a stochastic gradient estimator with that can be simulated. Then the first-order optimality condition becomes finding the root to

which is (1) with . Under appropriate regularity conditions, such a can be found via techniques such as infinitesimal perturbation analysis (Heidelberger et al. 1988, Ho et al. 1983, Glasserman 1991, L’Ecuyer 1990), the likelihood ratio or the score function method (Glynn 1990, Rubinstein 1986, Reiman and Weiss 1989), measure-valued differentiation (Heidergott et al. 2010), or other variants (e.g., Fu and Hu 1997, Peng et al. 2018). Alternately, when a “direct” unbiased gradient estimator is unavailable, we can also approximate via finite-difference schemes using to define .

To solve (1), the two main approaches in the literature are sample average approximation (SAA) and stochastic approximation (SA). They work as follows. In SAA, we first generate simulation samples from , and approximate (1) by replacing the expectation with its empirical counterpart, namely

Then we apply deterministic root-finding procedures, e.g., the Newton-Raphson method, to obtain the estimated root . Under regularity conditions (Shapiro et al. 2014, Shapiro and Nemirovski 2005), this estimator satisfies the asymptotic normality

| (2) |

where “” means convergence in distribution, is the Jacobian matrix of , and “” denotes the transpose (“” denotes the inverse of the transpose).

In SA, the Robbins-Monro SA (RM-SA) procedure estimates the root by generating a sequence of iterates via the recursion

| (3) |

where is an appropriate stepsize such that

and is an appropriate matrix. In practice, we usually set , where is a prescribed constant. With this choice of stepsize, under regularity conditions (Fabian 1968) we have asymptotic normality (which is also an implication of our Theorem 4.9 later) as follows. Let be an orthogonal matrix such that

is diagonal, then

where .

A variant of the RM-SA algorithm (3) is the Polyak-Ruppert averaging SA (PR-SA; Polyak and Juditsky 1992), motivated by the desire to reduce sensitivity to stepsize in RM-SA. This approach takes bigger steps in (3) (e.g., for ) and, when the iteration stops, averages the historical iterates to obtain

Under proper regularity conditions, SAA and PR-SA achieve the same asymptotic variance, which is optimal among RM-SA when the stepsize constant and is chosen such that (Polyak and Juditsky 1992, Asmussen and Glynn 2007). That is, we have

| (4) |

The methodology that we propose in this paper applies to all three algorithms depicted above.

3.1 Challenges in Incorporating Importance Samplers

In this paper, we consider situations where the root-finding problem (1) involves a rare event. A prime example is extreme quantile estimation, where the root is the quantile corresponding to a very high (or low) probability level. To facilitate presentation of our main ideas, we consider a one-dimensional output, i.e., (also denoted as unbold form ), in this section, and use the extreme quantile (Example 1) as our running example.

In the one-dimensional case, the asymptotic normality (2) is simplified to

In quantile estimation, this is , where is the density of . Typically, when is very close to 0 or 1, is correspondingly tiny and the asymptotic variance becomes very large. Note that the asymptotic normality dictates that the sample size required to achieve a target accuracy level is proportional to the asymptotic variance, so that a large variance implies a large required sample size. In fact, in many situations where the rare-event probability is governed by a large deviations theory (Bucklew 2004), this required sample size is exponentially large in the “rarity parameter”. Such an issue motivates one to consider variance reduction, in particular IS.

The basic idea of IS is to change the probability measure from which random variables are generated, which results in more frequent hits on the important regions. To maintain unbiasedness, the outputs are weighted by the so-called likelihood ratios, which are the Radon-Nikodym derivatives between the IS and the original measures. IS achieves variance reduction by using a generating distribution that has well-controlled likelihood ratios in the target hit region. Consider the estimation of . The crude Monte Carlo estimator for is given by , where are i.i.d. samples drawn from the original distribution . In contrast, IS generates samples from an IS distribution , and estimates by , where , with and the densities of under and , respectively, is the likelihood ratio. This latter estimator is unbiased as we can write . Here, a good choice of the IS sampler should exhibit a small variance of .

However, for root-finding problems, the design of an IS sampler is more challenging. To see this, suppose we want to use some sampler , and we apply SAA, RM-SA and PR-SA. More specifically, with IS, SAA would generate i.i.d. from and estimate the objective function using

from which we output the root, denoted . Under regularity conditions, the behavior of this root estimation is governed by the following CLT:

For RM-SA and PR-SA, the recursion is replaced by

where is independent of the past samples. Under regularity conditions, the errors of the root estimation using these methods are also governed by CLTs. For PR-SA, we know that

For RM-SA, it is known that if the stepsize is chosen as , then

From the above asymptotic normalities, we observe that the asymptotic variance would depend on the choice of through the variance . A good sampler needs to make this variance small. However, this expression for the variance involves , which is unknown a priori as it is exactly what we want to solve. This leads to a circular challenge: On one hand we need a good sampler to efficiently estimate the root; on the other hand, we need the root to decide the efficient sampler. This phenomenon is fundamental in the design of IS for stochastic root-finding problems.

3.2 A Worst-Case Perspective of Asymptotic Variances

To more concretely illustrate the challenge and what our proposed adaptive IS can achieve, we use a worst-case perspective and look at the minimax error. To set up this discussion, suppose that the candidate importance samplers form a parametric family . Let be the family of all possible roots, and we consider the family of root-finding problems in which we find the root of where varies in . Note that, since we do not know the true root in advance, even if we know , we cannot tell what is the that makes beforehand.

Let us consider SAA and PR-SA first. If we use any fixed importance sampler , then when , the estimator has the following asymptotic normality (suppose that for every )

For any fixed sampler determined without knowledge of , we have that the worst-case variance when varies in is

and the minimum possible worst-case asymptotic variance for any fixed IS is given by

On the other hand, suppose we can make use of the root when designing the importance sampler (i.e., we can choose based on ). Then we would choose , and be able to achieve the following worst-case asymptotic variance

The relation between the two asymptotic variances can be seen by a weak duality:

Theorem 3.3

Suppose that for any . Then

This theorem tells us that, if we use a fixed IS scheme, then we will suffer from a loss in efficiency due to a lack of a priori knowledge on the root. The gap between the two sides in Theorem 3.3 could be huge especially if only very limited knowledge of is available beforehand, i.e., is a large set. The key of our proposed approach is to achieve the lower end of the inequality, by using suitable adaptive schemes. In other words, we achieve an asymptotic variance as if we know the root.

We make two remarks. First, we consider the paradigm where we are already given an efficient IS for estimating the expectation (i.e., ), which can be a “black-box” in which we do not need to know any algorithmic details. The expectation estimation problem has been a long-standing focus of variance reduction, and our approach builds on the availability of these good IS schemes from the large literature. Second, we point out that in most practically interesting cases, it may not be easy or worthwhile to obtain an accurate minimizer for , even in expectation estimation problems when is known. This has led to different efficiency notions such as weak or logarithmic efficiency in the rare-event literature (L’Ecuyer et al. 2010). While Theorem 3.3 does not directly capture the comparisons using these specialized notions, our main assertion of achieving an asymptotic variance as if we know the root, which is not attainable using a fixed IS, still holds. Theorem 3.3 makes our main assertion clear by considering the basic setting where the minimization can be accurately solved.

We can do a similar analysis for the RM-SA algorithm, the only difference being that the asymptotic variance of the RM-SA algorithm is sensitive to the stepsize, and so we compare the behaviors of different IS schemes based on the same choice of stepsize, say . For this choice, we have the following weak duality

where the right-hand side (RHS) is the best possible for all fixed IS schemes and the left-hand side (LHS) is the best we can do as if we know the root, which can be achieved using our adaptive IS.

4 Adaptive Importance Sampling

In this section, we first present the main procedures of our adaptive IS to embed in SAA and SA. We then present asymptotic results and connect to our minimax discussion in Section 3.2. As in Sections 3.1 and 3.2, here we focus on the single-dimensional case with , i.e., , to highlight the main ideas of our developments. We generalize to multi-dimensional settings in Section 6 and the Appendix.

4.1 Main Procedures

We want to estimate the root of , where . We suppose there is an available good IS in the class for estimating the expectation for a given , i.e., once is given to us, we can choose with a low variance . Our procedures utilize this choice .

Our procedure is adaptive and consists of iterations to update both the IS parameter and the root estimate simultaneously. More precisely, at each iteration, given the most updated root estimate, we create a new IS sampler with parameter that aims to estimate the expectation with being precisely the most updated root estimate, and use it to draw new samples. From these new samples, we update our root estimate, via either SAA or SA, and repeat the iteration.

Algorithm 1 shows our adaptive IS embedded in SAA. At iteration , we are first given the most updated root estimate , and we set a new IS parameterized by (with some technical adjustment that we discuss momentarily). We use this IS to generate sample . Then, we solve a new SAA problem constructed from all the observed samples with a proper importance weighting, given by (5), to obtain and repeat the process.

For technicality reasons to ensure correct convergence, in Algorithm 1 we add a truncation to the IS parameter set so that it cannot diverge too fast. This means we construct a series of deterministic sets such that and their union contains the optimal IS parameter . Our implemented choice of IS would have parameter , where means a projection to set . For the choice of the truncation sets , if we have some prior knowledge that the optimal IS belongs to some compact set , then we can simply let for each . In particular, for quantile estimation problems, if we have crude knowledge on the possible deterministic range for the true quantile, then the possible value of would belong to a computable compact set that implies the truncation set. If we do not have this prior knowledge, then we can let increase to the whole space: . We also need that does not grow too fast (so that Assumption 4.2.1 in our sequel is satisfied).

| (5) |

Algorithm 2 shows our adaptive IS embedded in SA, where we replace the SAA problem in each iteration with an SA move, with the corresponding importance weight in (6). At the end of the procedure, we either output the final root iterate (RM-SA) or the average (PR-SA). Note that in Algorithm 2 the updating step in each iteration only utilizes the current sample , as opposed to using all past samples as in SAA.

| (6) |

4.2 Theoretical Results

We present our main theoretical results on the consistency and asymptotic normality of our SAA and SA with embedded adaptive IS.

4.2.1 SAA with Adaptive IS.

We first consider SAA, i.e., Algorithm 1. We need several assumptions and intermediate lemmas. The first assumption is about the growth rate of the IS parameter . {assumption} For each , holds for some .

In our algorithm, this is guaranteed by introducing the truncation sets (see the discussion before Algorithm 1). With this assumption, we have pointwise convergence of the estimated objective function in the following lemma, the proof of which is provided in Appendix 10.1. Note that refers to a sample drawn from the adaptive algorithm, i.e., and given , the distribution of is independent of .

Lemma 4.1

Under Assumption 4.2.1, for each , we have

Based on this pointwise convergence, we can show a uniform convergence of over all possible values of . Following the bracketing number approach (see Section 2.4 of van der Vaart and Wellner 1996), we make the following assumption.

{assumption}

Define .

For each , there exists a finite set whose

elements are pairs of functions such that:

(1) For each , there exists such that ;

(2) For each pair of , the limits

exist, and

To verify Assumption 4.2.1, we can also follow similar arguments to bound bracketing numbers as in, e.g., Section 2.7 of van der Vaart and Wellner (1996). We have intentionally stated our assumption in a general way without using any condition like Lipschitz continuity or smoothness of function . That is because, for quantile estimation problems which we consider as an important example, is not even continuous in . On the other hand, if we have some smoothness conditions for , it could help verify this assumption. For example, if the function class is Lipschitz continuous in , in the sense that

for some metric on the index set, and (which can be shown in a similar way as Lemma 4.1), then similar to Theorem 2.7.11 of van der Vaart and Wellner (1996), a sufficient condition for Assumption 4.2.1 is that the -covering number on set , , is finite. Here the covering number is the minimum number of -balls under metric needed to cover , where an -ball centered at under metric means . More concretely, if is the Euclidean distance, then the compactness of would be sufficient for the aforementioned condition. But the compactness of is not necessary because it could be the case that shrink to 0 when and are large.

The following lemma presents the uniform convergence of the estimated objective function. Its proof uses a generalized bracketing number to handle the sum of martingale difference array and is in Appendix 10.2.

Based on the uniform convergence of the sample-averaged objective function, similar in spirit to Theorem 5.7 of van der Vaart (1998), we make the following assumption to ensure the root to is well separated. {assumption} The objective function is differentiable at = with continuously invertible derivative, and is the unique root in the sense that for any ,

With this assumption, and using the uniform convergence derived in Lemma 4.2, we can show the strong consistency of the SAA estimator with adaptive IS. The proof is included in Appendix 10.3.

Theorem 4.3 (Consistency of SAA with embedded adaptive IS)

Next, we will establish a CLT for the estimator using the weak convergence of martingale processes. To develop this, we introduce additional notation and some preliminary technical tools. Let , be the function defined by , and . Furthermore, for each measurable function on the probability space , let

Notice that when varies in , and could be regarded as processes indexed by . We denote as the filtration. We write as the conditional expectation given , and similarly as the conditional variance given . Notice that, for each ,

is a martingale difference array. For each fixed , the standard martingale CLT can give the asymptotic normality for , but for the asymptotic normality of the root, we need a uniform behavior of for in a neighborhood of . To this end, enlightened by Donsker-type theorems and the analysis of the weak convergence of function-valued martingale difference arrays in Nishiyama (2000), we construct the following assumption. {assumption} There exists such that each is a cover of (i.e., ) and . Here for each , is an -ball under -distance . Moreover,

where for a set , is defined as the smallest -measurable function that is greater than . Furthermore,

Here, the first displayed condition requires that each set in the cover should be small enough and the second displayed condition requires that there cannot be too many sets in the cover. The following proposition provides a more transparent sufficient condition for Assumption 4.2.1. With slight abuse of notations, we let be a pseudo-metric on . Notice that in Assumption 4.2.1 we also use to denote the -distance between functions under , and we have that . Let the covering number be the minimum number of balls of radius needed to cover .

Proposition 4.4

Suppose that we are given and , both a.s. Then the following condition is sufficient for Assumption 4.2.1: There exists a such that

and (ii) there exists constant and real-valued function such that for any ,

Here, the first part is a uniform entropy condition that is commonly assumed for Donsker-type theorems. The second can be regarded as a Lipschitz condition for function when is close to and is close to . Similar to the conditions for the martingale CLT (see e.g. Theorem 8.2.8 of Durrett 2019), we introduce our last assumption. {assumption}(Lindeberg’s condition) There exists a such that for every ,

where is the adapted envelope for , i.e., is the smallest -measurable random variable such that .

To verify this assumption, we can bound when and are close to and respectively. We summarize this observation in the following proposition. The proof is in Appendix 11.2.

Proposition 4.5

Suppose that we are given and , both a.s. Suppose that there exist and such that for all . Also suppose . Then Assumption 4.4 holds.

With these assumptions, we can first prove asymptotic equicontinuity for the sum of martingale difference arrays at . That is, for any large and , as long as is small, and should be close enough. Similar to Donsker-type theorems, this would guarantee a uniform behavior in the martingale CLT for all , where is a normal random variable with mean zero and variance determined by . Another main ingredient of our proof is that, since a.s., we have that a.s., thus the variance of would converge to . This tells us the variance of . Then, based on this, we derive the asymptotic normality of the SAA with adaptive IS in the following theorem. The full proof is in Appendix 10.4.

Theorem 4.6 (Asymptotic normality of SAA with embedded adaptive IS)

This theorem tells us that using our adaptive IS, the asymptotic variance would be the same as if we use a fixed sampler , or in other words as if we know the root in advance. In particular, when , we would achieve the asymptotic normality

So the worst-case variance would be the LHS of the weak duality in Theorem 3.3.

4.2.2 SA with Adaptive IS.

Now we turn to SA, i.e., Algorithm 2. For consistency, we adopt the projected ordinary differential equation (ODE) approach in Kushner and Yin (2003). Since , we have that

so iteration (6) has a martingale difference noise. To proceed, we state some assumptions. The first is the boundedness of the conditional variance of the gradient estimator. Let be the error of the estimated objective function. We assume the following. {assumption} There exists a constant such that .

In our adaptive method, can be chosen to make this conditional variance small, so that this assumption is typically readily verifiable. Our next assumption is a one-dimensional version of the constraint set condition (A4.3.2) of Kushner and Yin (2003) and the uniqueness of the root. {assumption} for some , belongs to the interior of , and is the unique root of .

By verifying the conditions of Theorem 5.2.3 in Kushner and Yin (2003) (See Appendix 10.5), we have the consistency of and .

Theorem 4.7 (Consistency of SA with embedded adaptive IS)

Next we present the asymptotic normality of the root estimator, considering first the RM-SA estimator . Following Fabian (1968), we introduce the following assumption on the uniform integrability of the squared noise. {assumption}

Similar to Assumption 4.4, we also have the following sufficient condition to verify Assumption 4.7. The proof is in Appendix 11.2.

Proposition 4.8

Suppose that we are given and , both a.s. Suppose that there exist and such that for all . Also suppose . Then Assumption 4.7 holds.

With these, we have the following CLT for the RM-SA estimator.

Theorem 4.9 (Asymptotic normality of RM-SA with embedded adaptive IS)

The proof of Theorem 4.9 requires reformulating the recursion in our Algorithm 2 in an alternative form used in Fabian (1968). See Appendix 10.6 for the details.

Lastly, we consider the PR-SA estimator . Following Polyak and Juditsky (1992), we have the following asymptotic result, whose proof is in Appendix 10.7.

Theorem 4.10 (Asymptotic normality of PR-SA with embedded adaptive IS)

5 Quantile Estimation with Adaptive Importance Sampling

In this section, we apply our adaptive IS to the quantile estimation problem. Let be a performance function of a stochastic system, and recall that is the cumulative distribution function of . Then the -quantile of is

| (8) |

Henceforth, we assume that is a continuous random variable, so the -quantile of is the root of the equation

| (9) |

Note that in this section, is used in place of as the variable in the root-finding equation.

As discussed in the introduction, when is close to 0 or 1, standard Monte Carlo could perform poorly, where the standard approach means using the empirical quantile, i.e., generating i.i.d. samples , and solving the empirical root-finding problem (9) by plugging in the empirical distribution for . To address the extreme value estimation problem, we apply the adaptive IS approach to the quantile estimation setting, for which we also provide milder and easier-to-verify conditions for the asymptotic analysis.

5.1 Empirical Quantile

The empirical quantile depicted above is the analog of the SAA solution in quantile estimation. Similar to the previous section, the IS distribution is parameterized by , on which we know a black-box function that gives a good IS parameter for estimating . Algorithm 3 presents our adaptive IS embedded in the empirical quantile, where the truncation set is the same as in Algorithm 1 that is used to guarantee strong consistency.

Because of the special monotone structure of the objective function, the assumptions required for the quantile estimation asymptotics are considerably simpler than those used in the general case presented previously. Our first assumption is analogous to Assumption 4.2.1. {assumption} There exist such that .

The next assumption corresponds to the condition in Proposition 4.5 (or 4.8) specialized for the quantile estimation problem. Observe that in Proposition 4.5 corresponds to in the quantile estimation case, which is monotone w.r.t. . {assumption} There exist such that there exists with .

The next assumptions about the smoothness of the variance and objective function are Assumption 4.2 and the condition depicted in Theorem 4.6 specialized to the quantile estimation case. {assumption} For in a neighborhood of , the function

is continuous in .

The distribution function is differentiable at , and the density is strictly positive at .

With these, we have the consistency and asymptotic normality of the quantile estimator .

Theorem 5.1

In the proof of Theorem 5.1, we first verify the conditions for invoking Theorem 4.3 to show strong consistency. Regarding asymptotic normality, instead of using Theorem 4.6 directly, we exploit the special structure of quantile estimation, and the required condition is slightly weaker (the counterpart of Assumption 4.2.1 is not required for Theorem 5.1). While the idea follows generally from Serfling (2009) Theorem A, Section 2.3.3, one notable difference is that to show the weak convergence of the empirical estimate of , we need to use a triangular-array martingale CLT instead of the Berry-Essen bound in Serfling (2009). As a result, we also do not need to assume that the likelihood ratio has bounded third-order moment as required by Berry-Esseen.

5.2 SA with Adaptive IS for Quantile Estimation

Algorithm 4 presents our procedure to embed IS in SA for quantile estimation where, as in Section 4, we consider both the RM-SA quantile estimator and the PR-SA quantile estimator .

| (10) |

Let . The following is Assumption 4.2.2 specialized to quantile estimation. {assumption} There exists a constant such that .

We get the following special case of Theorem 4.9.

Theorem 5.2

We also have asymptotic normality of our adaptive IS embedded in PR-SA for quantile estimation.

Theorem 5.3

Finally, we note that Algorithms 3 and 4, with IS outputs of the form , are designed for the case when is close to 0. When is close to 1, we should use outputs of the form , because the area becomes more important. Correspondingly, we can replace the indicator function in Algorithms 3 and 4 by and by . All our theoretical results continue to hold, as we can view this case equivalently as simply adding a negative sign to .

6 Multidimensional Setting

In Sections 4 and 5, we restricted our discussion to a one-dimensional root . In this section, we generalize our developments to multidimensional settings. Most of these generalizations follow naturally, but one major new issue arises in comparing (asymptotic) performance, since the scalar measure of (asymptotic) variance is now replaced by a matrix. To make this comparison well-defined, we introduce a scalar-valued performance function , and we measure errors in terms of , e.g., can be an approximation of the objective function in a considered optimization problem. With this, the best IS parameter would be an optimal solution to minimize the variance of the approximated objective function.

We study the asymptotic variance using this performance function . By the delta method, and recalling formulas (2) and (4), if is continuously differentiable, we have that for a fixed IS parameter ,

where is the gradient of , and recall that is the Jacobian matrix of .

Since the variance now becomes one-dimensional, we can follow our developed one-dimensional approach and say that a good IS parameter should minimize the quantity

Note that this quantity is exactly the variance when we use

as an IS estimator for the expectation . Similar to the one-dimensional case, this means if given and , then what we want is simply a good sampler for this expectation estimation problem. Suppose we have already an available good IS for this problem, i.e., we know a function that parameterizes a good IS to estimate for given and . Then in Step 4 of Algorithms 1 and 2, we plug in and the estimate

and use to parameterize the IS in the next iteration. Algorithms A.1 and A.2 in Appendix 9.1 provide the respective procedures of our adaptive IS embedded in SAA and SA for this multivariate setting.

We have consistency and asymptotic normality for adaptive IS in the multivariate setting as follows.

Theorem 6.1

Theorem 6.2

(Consistency and asymptotic normality of RM-SA with embedded adaptive IS (multivariate case)). (Full version in Theorem A.4) Under a multidimensional version of the assumptions in Theorem 4.9, let be an orthogonal matrix such that

is diagonal. Then for the root estimate generated by the RM-SA algorithm with embedded adaptive IS, a.s. and

where and .

Theorem 6.3

These results are natural generalizations of those in Section 4. One new challenge in proving these results is to show the consistency of the Jacobian estimate , and we also need an extra assumption (Assumption 9.2.1). The other required assumptions can be regarded as the component-wise generalizations of the assumptions in Section 4. To avoid repetition, we defer the explicit formulations of these assumptions, theorems, and their proofs to Appendices 9.2 - 10.8.

7 Examples

In this section, we consider two sets of examples. The first set comprises toy examples on extreme quantile estimation for a standard normal distribution, an exponential distribution, and a Pareto-tailed distribution. The second set considers estimation of VaR and CVaR for a financial portfolio.

7.1 Toy Examples

We consider quantile estimation for three toy examples: , , . We describe theoretical analysis and numerical results for the first example here, with analogous analysis and results provided for the other two distributions in Appendix 12.

7.1.1 Theoretical Analysis.

Suppose we want to use Monte Carlo samples of to estimate its -quantile, where is large. We use Algorithms 3 and 4. To specify the algorithms, we first give the choice of the IS class (here we are using instead of , as it will be seen that is one-dimensional for this example), the black-box IS function , and the truncation scheme . As is well-known in the IS literature (e.g., Bucklew 2004), a natural choice of is the set of IS samplers derived from exponential shifting, where in the normal case this would be a normal distribution with mean . Moreover, for a given , a good IS estimator for is to set its mean at , i.e., we choose . To complete the algorithm specification, we select the truncation sets . One simple way to do this is to estimate a lower and upper bound for using some concentration inequality, and from a knowledge we can let . If we do not have this bound, then another way is to let grow to . The next proposition gives some conditions for which the required assumptions of our theoretical results would be satisfied.

Proposition 7.1

From Theorems 5.1, 5.2 and 5.3, both SAA and PR-SA exhibit the asymptotic variance

| (11) |

where is the true quantile, is the likelihood ratio, and is the standard normal density. RM-SA with stepsize exhibits the asymptotic variance

We now analyze the variance reduction. The numerator of (11) is bounded by

When , the RHS is bounded by , using a tail bound for the standard normal distribution for . So the asymptotic variance of is bounded by in SAA.

On the other hand, if we use SAA without IS, then the variance of is given by . When is close to 1, we have

so the variance

would grow to infinity exponentially as goes to infinity, where the inequality used another tail bound for the standard normal distribution . Comparing variances in the above cases, we see that our adaptive IS significantly reduces the asymptotic variance when is close to 1.

7.1.2 Numerical Experiments.

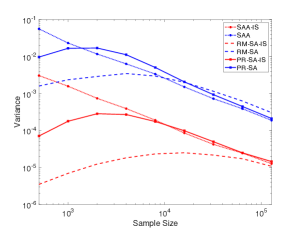

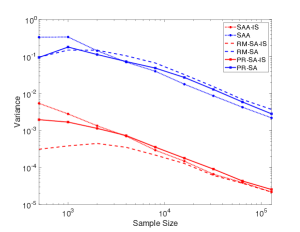

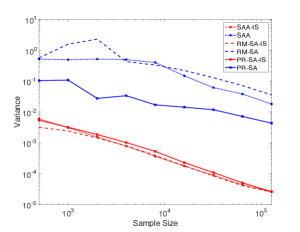

We report numerical experiments to estimate the quantile of the standard normal distribution using our adaptive IS, using the following settings:

-

•

For SAA, we set , where and .

-

•

For RM-SA, we set the stepsize with (the optimal choice of the stepsize parameter), where is the standard normal density and is the true quantile, and the projection set .

-

•

For PR-SA, we set the stepsize with . We average the estimates beginning from the ()th iteration, i.e., for , we set ; for , we set . We set and use the projection set .

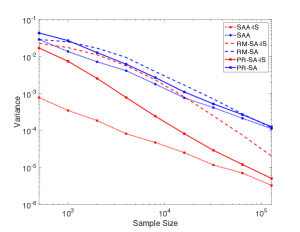

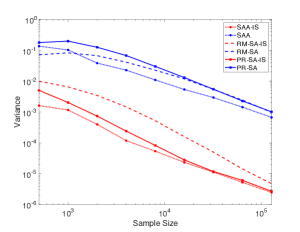

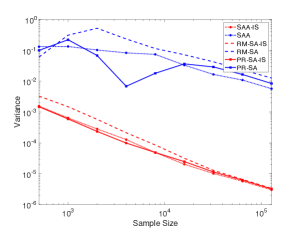

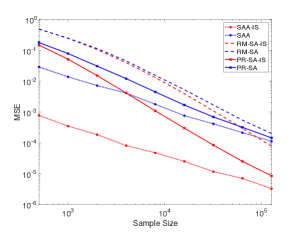

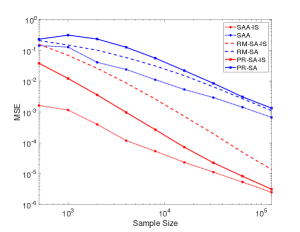

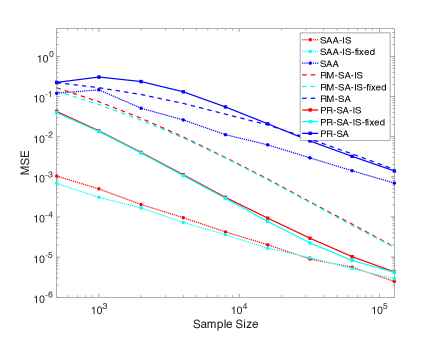

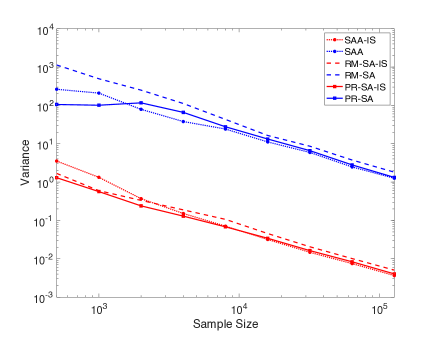

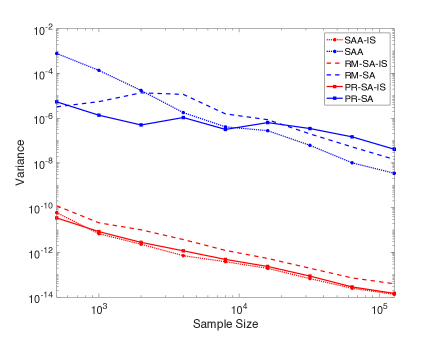

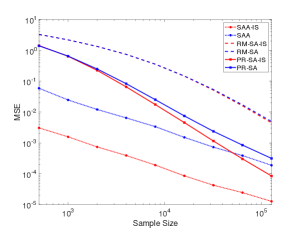

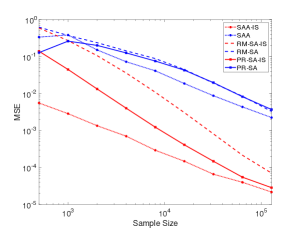

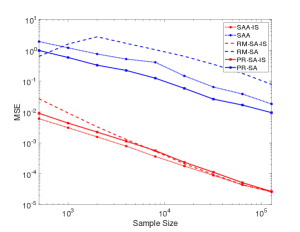

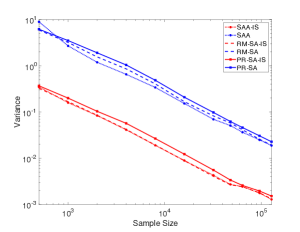

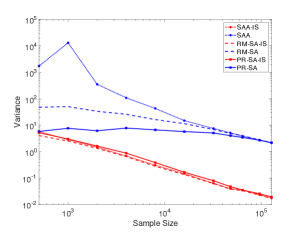

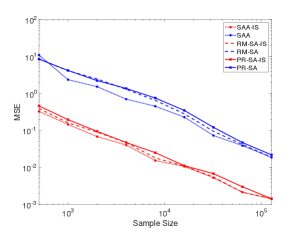

We also run the algorithms under the same setting but without using IS. We set , and vary the total number of simulation samples from to to estimate the quantiles. We repeat the procedure times to estimate the variance and mean squared error (MSE) of the estimated quantiles. Figures 2-3 show the results. Tables 1-3 further show their numerical details, and also the ratios of the variance of the without-IS estimator over the with-IS counterpart.

| Sample Size | SAA-IS | SAA | ratio | RM-SA-IS | RM-SA | ratio | PR-SA-IS | PR-SA | ratio |

|---|---|---|---|---|---|---|---|---|---|

| 500 | 7.80E-04 | 2.89E-02 | 37 | 2.28E-02 | 2.90E-02 | 1.3 | 1.70E-02 | 4.34E-02 | 2.5 |

| 1000 | 3.49E-04 | 1.37E-02 | 39 | 1.75E-02 | 2.51E-02 | 1.4 | 7.44E-03 | 2.70E-02 | 3.6 |

| 2000 | 1.86E-04 | 7.20E-03 | 39 | 1.11E-02 | 1.68E-02 | 1.5 | 2.55E-03 | 1.27E-02 | 5.0 |

| 4000 | 8.19E-05 | 4.14E-03 | 51 | 5.62E-03 | 9.46E-03 | 1.7 | 7.80E-04 | 6.20E-03 | 7.9 |

| 8000 | 4.76E-05 | 1.80E-03 | 38 | 2.34E-03 | 3.92E-03 | 1.7 | 2.44E-04 | 2.70E-03 | 11 |

| 16000 | 2.52E-05 | 7.63E-04 | 30 | 8.11E-04 | 1.68E-03 | 2.1 | 8.20E-05 | 1.10E-03 | 13 |

| 32000 | 1.17E-05 | 4.17E-04 | 36 | 2.49E-04 | 7.13E-04 | 2.9 | 2.92E-05 | 5.25E-04 | 18 |

| 64000 | 7.10E-06 | 2.14E-04 | 30 | 7.45E-05 | 2.80E-04 | 3.8 | 1.21E-05 | 2.69E-04 | 22 |

| 128000 | 3.28E-06 | 1.12E-04 | 34 | 2.05E-05 | 1.20E-04 | 5.9 | 5.08E-06 | 1.26E-04 | 25 |

| Sample Size | SAA-IS | SAA | ratio | RM-SA-IS | RM-SA | ratio | PR-SA-IS | PR-SA | ratio |

|---|---|---|---|---|---|---|---|---|---|

| 500 | 1.62E-03 | 1.37E-01 | 85 | 9.97E-03 | 7.18E-02 | 7.2 | 5.03E-03 | 1.79E-01 | 36 |

| 1000 | 1.17E-03 | 1.03E-01 | 88 | 6.53E-03 | 8.33E-02 | 13 | 2.04E-03 | 2.00E-01 | 98 |

| 2000 | 3.99E-04 | 3.87E-02 | 97 | 3.46E-03 | 6.74E-02 | 20 | 7.39E-04 | 1.26E-01 | 171 |

| 4000 | 1.18E-04 | 2.29E-02 | 193 | 1.47E-03 | 4.13E-02 | 28 | 2.41E-04 | 6.81E-02 | 282 |

| 8000 | 5.37E-05 | 1.10E-02 | 205 | 5.25E-04 | 2.28E-02 | 43 | 8.26E-05 | 3.02E-02 | 365 |

| 16000 | 2.33E-05 | 5.40E-03 | 232 | 1.59E-04 | 1.19E-02 | 75 | 2.80E-05 | 1.31E-02 | 469 |

| 32000 | 1.12E-05 | 2.95E-03 | 263 | 5.02E-05 | 5.44E-03 | 108 | 1.18E-05 | 5.50E-03 | 466 |

| 64000 | 5.24E-06 | 1.44E-03 | 275 | 1.43E-05 | 2.43E-03 | 170 | 6.08E-06 | 2.28E-03 | 376 |

| 128000 | 2.47E-06 | 6.71E-04 | 271 | 4.76E-06 | 9.75E-04 | 205 | 2.71E-06 | 1.02E-03 | 376 |

| Sample Size | SAA-IS | SAA | ratio | RM-SA-IS | RM-SA | ratio | PR-SA-IS | PR-SA | ratio |

|---|---|---|---|---|---|---|---|---|---|

| 500 | 1.56E-03 | 1.32E-01 | 85 | 3.29E-03 | 6.10E-02 | 19 | 1.48E-03 | 1.00E-01 | 68 |

| 1000 | 6.44E-04 | 1.34E-01 | 208 | 1.49E-03 | 3.12E-01 | 210 | 5.97E-04 | 2.21E-01 | 371 |

| 2000 | 2.83E-04 | 1.03E-01 | 363 | 5.78E-04 | 5.22E-01 | 903 | 2.35E-04 | 6.81E-02 | 290 |

| 4000 | 1.28E-04 | 8.30E-02 | 649 | 2.13E-04 | 2.35E-01 | 1100 | 9.86E-05 | 6.85E-03 | 69 |

| 8000 | 4.87E-05 | 7.42E-02 | 1524 | 8.53E-05 | 1.15E-01 | 1346 | 4.88E-05 | 1.81E-02 | 371 |

| 16000 | 2.03E-05 | 3.32E-02 | 1635 | 3.18E-05 | 7.22E-02 | 2274 | 2.46E-05 | 3.65E-02 | 1480 |

| 32000 | 1.01E-05 | 1.66E-02 | 1638 | 1.29E-05 | 4.27E-02 | 3316 | 1.14E-05 | 2.90E-02 | 2541 |

| 64000 | 5.71E-06 | 1.09E-02 | 1909 | 6.53E-06 | 2.34E-02 | 3580 | 6.22E-06 | 1.65E-02 | 2654 |

| 128000 | 2.99E-06 | 5.72E-03 | 1913 | 3.35E-06 | 1.27E-02 | 3786 | 3.23E-06 | 8.44E-03 | 2612 |

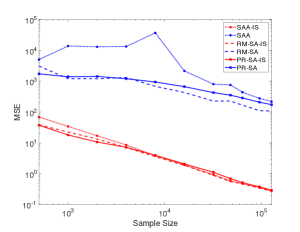

We observe the following: (i) All three procedures (SAA, RM-SA and PR-SA) are improved by the adaptive IS, as clearly indicated in Figures 2 and 3 by comparing the corresponding red and blue curves. Moreover, the variance reduction ratios (ratio between the variances of without-IS and with-IS estimators) increase quickly as approaches 1. For example, in Tables 1-3 where takes , and , respectively, fixing the sample size as , the variance reduction ratio for SAA is , and , respectively. (ii) SAA generally has the smallest variance of the three procedures, and the variance of PR-SA is generally smaller than that of RM-SA. This can be seen by comparing the red curves in Figure 2). More precisely, in Table 1 when , fixing the sample size as 128000 for instance, the variance of SAA-IS is about 16% (3.28E-06/2.05E-05) of the variance of RM-SA-IS and the variance of PR-SA-IS is about 24% (5.08E-06/2.05E-05) of the variance of RM-SA-IS. When , the variances of the three procedures are closer. In Table 3, again fixing the sample size at 128000 for instance, the variance of SAA-IS is about 89% (2.99E-06/3.35E-06) of the variance of RM-SA-IS and the variance of PR-SA-IS is about 96% (3.23E-06/3.35E-06) of the variance of RM-SA-IS. (iii) When is very close to 1 (e.g., and ), the variance reduction ratios increase with the sample size up to some point and then plateau. This observation is clearer for SAA. For example, in Tables 2 and 3, each ratio column tends to increase at first as the sample size increases. When the sample size is more than , the ratios appear roughly unchanged. This could be attributed to that with a large sample size, the IS sampler stabilizes around the optimum and additional samples provide negligible variance reduction improvements.

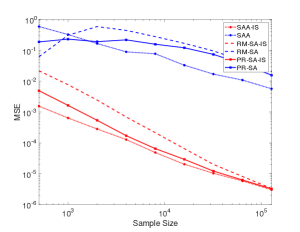

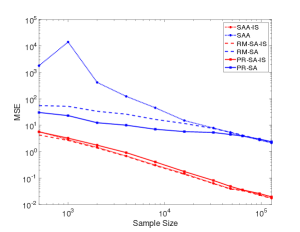

Furthermore, we compare the adaptive IS with the fixed optimal IS where we assume is known and use the IS parameter

This optimal IS is the best we can do among the considered IS class. Using this fixed optimal IS parameter, we run SAA, RM-SA and PR-SA using the same truncation set and stepsize as described in the beginning of this subsection. Figure 4 shows that all of SAA, RM-SA and PR-SA that embed our adaptive IS (represented by the red curves) give variances and MSEs very close to the counterparts with the fixed optimal IS (represented by the light blue curves). This indicates our adaptive IS achieves almost the same variance reduction as the fixed optimal IS, which coincides with the implications of Theorems 4.6, 4.9 and 4.10 (see the discussions right after these theorems).

7.2 VaR and CVaR for a Financial Portfolio

In this example, we estimate the VaR and CVaR of a financial portfolio. Let be the value of a portfolio at time , where are risk factors, and be the loss of this portfolio at time . The -VaR is the -quantile of :

The -CVaR is the expected return on the portfolio in the worst of cases, i.e.,

If has a positive density in the neighborhood of , then -CVaR and -VaR are related by the following equation (Rockafellar and Uryasev 2000):

| (12) |

7.2.1 Choice of IS Sampler and Other Algorithmic Configurations.

We first specify an initial IS to estimate . We use the sampler suggested by Glasserman et al. (2000). Let . To simplify notation, henceforth we drop the dependency on time in and . When is small, the loss of the portfolio can be approximated by

where , , and . Here , and are the Greeks for this portfolio, i.e., is the partial derivative of on , is the gradient of on with , and is the Hessian matrix of on with the th element .

Suppose that has a multivariate normal distribution with mean and covariance matrix . Then following Glasserman et al. (2000), we can write in a diagonalized quadratic form:

where , is a matrix such that , is a diagonal matrix, , and is the th diagonal element of .

The IS sampler is obtained through exponential twisting with likelihood ratio

where is the logarithm of the moment generating function of . Note that such a change of measure is equivalent to changing the distribution of from to , where and . The second moment of the estimator using this sampler is given by

| (13) |

where denotes expectation under IS with twisting parameter .

A good choice of for the estimation of should make small. However, finding the value of to minimize is computationally expensive. Instead, Glasserman et al. (2000) suggested minimizing the upper bound in (13), i.e., we choose

From the convexity of , we know that satisfies the first-order condition

Solving this first-order condition yields , which will serve as our black-box IS function.

For the truncation set needed in our algorithms, we can estimate an upper bound for using

and a lower bound can be derived similarly. With these bounds that give , we can now use our Algorithms 3 and 4 with . The following proposition verifies the conditions needed to provide the asymptotic guarantees of our algorithms.

Proposition 7.2

Finally, from the estimator for , we can estimate CVaR using Equation (12).

7.2.2 Numerical Results on a Portfolio with Ten Risk Factors.

We use the example in Glasserman et al. (2000). Suppose that there are trading days in one year, and we investigate the loss of the portfolio over days, i.e., the risk time period (years). We take the risk-free interest rate as and assume that there are ten uncorrelated underlying assets (risk factors), with all assets having the same initial value of and the same volatility of . The portfolio shorts at-the-money call options and at-the-money put options on each asset, all options having a half-year maturity. The Greeks , , and can be calculated through the Black-Scholes formula, and then the parameters , , , and can be calculated accordingly.

We first estimate the -VaR . We set , and vary the total number of simulation samples from to . We use the following configurations to run the algorithms:

-

•

For SAA, we set for both and .

-

•

For RM-SA, when , we set the stepsize with and the projection set . When , we set and the projection set .

-

•

For PR-SA, we set the stepsize , and the choices of and the projection sets are the same as in RM-SA. Similar to the toy example, we average the estimates beginning from the th iteration with .

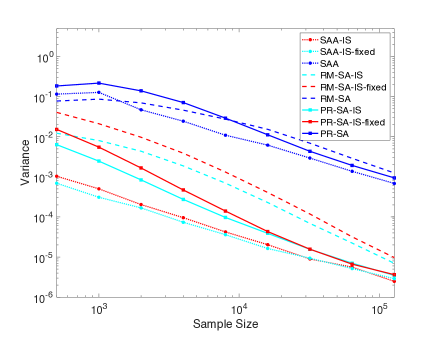

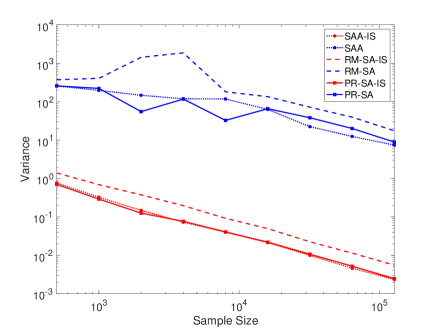

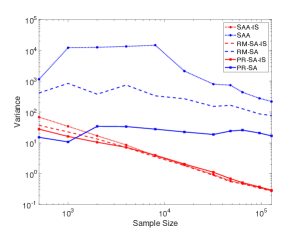

The samples of the loss of the portfolio are calculated through the Black-Scholes formula based on the approximated , where represents the th sample path of these ten underlying assets. We repeat the procedure times to estimate the variance of the estimated -VaRs obtained from the three procedures. The results are shown in Figure 5 and Tables 4 and 5.

| Sample Size | SAA-IS | SAA | ratio | RM-SA-IS | RM-SA | ratio | PR-SA-IS | PR-SA | ratio |

|---|---|---|---|---|---|---|---|---|---|

| 500 | 3.53E+00 | 2.63E+02 | 75 | 1.68E+00 | 1.13E+03 | 673 | 1.30E+00 | 1.05E+02 | 81 |

| 1000 | 1.33E+00 | 2.09E+02 | 157 | 5.98E-01 | 4.94E+02 | 826 | 5.64E-01 | 1.01E+02 | 179 |

| 2000 | 3.69E-01 | 7.89E+01 | 214 | 3.33E-01 | 2.49E+02 | 749 | 2.40E-01 | 1.16E+02 | 486 |

| 4000 | 1.52E-01 | 3.79E+01 | 250 | 1.88E-01 | 1.12E+02 | 594 | 1.29E-01 | 6.57E+01 | 508 |

| 8000 | 7.07E-02 | 2.41E+01 | 341 | 1.07E-01 | 4.30E+01 | 404 | 6.80E-02 | 2.77E+01 | 407 |

| 16000 | 3.18E-02 | 1.11E+01 | 350 | 4.55E-02 | 1.64E+01 | 360 | 3.43E-02 | 1.33E+01 | 387 |

| 32000 | 1.47E-02 | 5.92E+00 | 402 | 2.05E-02 | 8.60E+00 | 419 | 1.63E-02 | 6.60E+00 | 404 |

| 64000 | 7.49E-03 | 2.48E+00 | 331 | 1.01E-02 | 3.76E+00 | 371 | 8.35E-03 | 2.80E+00 | 336 |

| 128000 | 3.65E-03 | 1.26E+00 | 345 | 5.06E-03 | 1.81E+00 | 358 | 4.03E-03 | 1.33E+00 | 329 |

| Sample Size | SAA-IS | SAA | ratio | RM-SA-IS | RM-SA | ratio | PR-SA-IS | PR-SA | ratio |

|---|---|---|---|---|---|---|---|---|---|

| 500 | 7.70E-01 | 2.57E+02 | 333 | 1.40E+00 | 3.72E+02 | 267 | 7.04E-01 | 2.58E+02 | 367 |

| 1000 | 3.27E-01 | 1.97E+02 | 603 | 6.91E-01 | 4.06E+02 | 588 | 2.91E-01 | 2.22E+02 | 764 |

| 2000 | 1.48E-01 | 1.47E+02 | 993 | 3.76E-01 | 1.43E+03 | 3807 | 1.26E-01 | 5.53E+01 | 440 |

| 4000 | 7.30E-02 | 1.19E+02 | 1633 | 1.96E-01 | 1.87E+03 | 9517 | 7.67E-02 | 1.17E+02 | 1526 |

| 8000 | 4.01E-02 | 1.18E+02 | 2940 | 9.24E-02 | 1.81E+02 | 1958 | 4.08E-02 | 3.26E+01 | 800 |

| 16000 | 2.15E-02 | 6.30E+01 | 2937 | 4.97E-02 | 1.35E+02 | 2717 | 2.21E-02 | 6.57E+01 | 2978 |

| 32000 | 1.00E-02 | 2.24E+01 | 2233 | 2.25E-02 | 7.20E+01 | 3199 | 1.07E-02 | 3.82E+01 | 3568 |

| 64000 | 4.62E-03 | 1.25E+01 | 2702 | 1.15E-02 | 3.96E+01 | 3452 | 5.32E-03 | 2.01E+01 | 3776 |

| 128000 | 2.35E-03 | 7.40E+00 | 3147 | 5.56E-03 | 1.75E+01 | 3155 | 2.48E-03 | 8.89E+00 | 3580 |

From Figure 5 and Tables 4 and 5, we reach similar conclusions as in Section 7.1.2: (i) Our adaptive IS can reduce the variance of the VaR estimator significantly for SAA, RM-SA and PR-SA. For example, from Table 5, we see that when and the sample size is 128000, the variance reduction ratio is more than 3000 for all of the three procedures. (ii) SAA has the smallest variance and PR-SA has smaller variance than RM-SA. For example, in Table 5, when , the variance of SAA-IS is about 42% (2.35E-03/5.56E-03) of the variance of RM-SA-IS and the variance of PR-SA-IS about 45% (2.48E-03/5.56E-03) of the variance of RM-SA-IS. (iii) For both SAA and PR-SA, the variance reduction ratios tend to increase as sample size increases and then start to plateau when the sample size is about 32000. This can be seen from the ratio column for SAA and PR-SA in Table 4 or 5. For RM-SA, the ratio is less stable. In Table 5, when the sample size is 4000, the ratio for RM-SA is 9517, which appears to be an outlier, as it is quite large compared to the other ratios; however, when the sample size becomes larger (larger than 32000), the ratio tends to become stable.

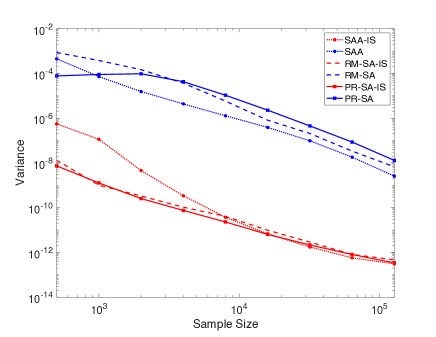

Next, we estimate CVaRs using the estimated . Since we do not have an analytical expression for computing , we use samples to approximate the expectation, i.e., we generate samples of and then plug into the estimated using the three different procedures (SAA, RM-SA, PR-SA) and estimate the variances. By comparing the red curves with corresponding blue curves in Figure 6, we see that our adaptive IS again substantially reduces the variances of all three procedures.

8 Conclusion

In this paper, we propose an adaptive IS scheme to resolve the circular challenge in stochastic root-finding problems involving rare events. The circular challenge arises because, in the presence of rare events, variance reduction via IS is crucial to boost the estimation accuracy to an acceptable level, yet configuring a good IS relies on knowing the root, which is our a priori unknown target. We design an adaptive approach to simultaneously estimate the root and the IS parameters, and embed it in three commonly used root-finding procedures: SAA, RM-SA and PR-SA. We use a worst-case asymptotic variance comparison to show the benefit and necessity of adaptivity, and support our algorithms with theoretical analysis on strong consistency and asymptotic normality. We use extreme quantile estimation as a concrete example, and obtain the corresponding theoretical results under milder conditions than in the general setting. Finally, we demonstrate via numerical experiments the effectiveness of our adaptive IS.

This material is based upon work supported by the National Science Foundation under Grants CAREER CMMI-1834710 and IIS-1849280, the U.S. Air Force Office of Scientific Research under Grant FA95502010211, and the National Natural Science Foundation of China under Grant 71801148. A preliminary version of this work (Lam et al. 2018) was published in the 2018 Proceedings of the Winter Simulation Conference.

References

- Ahamed et al. (2006) Ahamed, T. P. I., V. S. Borkar, S. Juneja. 2006. Adaptive importance sampling technique for Markov chains using stochastic approximation. Operations Research 54(3) 489–504.

- Asmussen and Glynn (2007) Asmussen, S., P. W. Glynn. 2007. Stochastic Simulation: Algorithms and Analysis. Springer Science & Business Media, New York, NY.

- Au and Beck (1999) Au, S.-K., J. L. Beck. 1999. A new adaptive importance sampling scheme for reliability calculations. Structural Safety 21(2) 135–158.

- Bardou et al. (2009) Bardou, O., N. Frikha, G. Pages. 2009. Computing VaR and CVaR using stochastic approximation and adaptive unconstrained importance sampling. Monte Carlo Methods and Applications 15(3) 173–210.

- Bayraksan and Morton (2006) Bayraksan, G., D. P. Morton. 2006. Assessing solution quality in stochastic programs. Mathematical Programming 108(2-3) 495–514.

- Bayraksan and Morton (2011) Bayraksan, G., D. P. Morton. 2011. A sequential sampling procedure for stochastic programming. Operations Research 59(4) 898–913.

- Blanchet and Glynn (2008) Blanchet, J. H., P. W. Glynn. 2008. Efficient rare-event simulation for the maximum of heavy-tailed random walks. The Annals of Applied Probability 18(4) 1351–1378.

- Blanchet et al. (2012a) Blanchet, J. H., P. W. Glynn, K. Leder. 2012a. On Lyapunov inequalities and subsolutions for efficient importance sampling. ACM Transactions on Modeling and Computer Simulation 22(3) No.13.

- Blanchet and Lam (2012) Blanchet, J. H., H. Lam. 2012. State-dependent importance sampling for rare-event simulation: An overview and recent advances. Surveys in Operations Research and Management Science 17(1) 38–59.

- Blanchet and Lam (2014) Blanchet, J. H., H. Lam. 2014. Rare-event simulation for many-server queues. Mathematics of Operations Research 39(4) 1142–1178.

- Blanchet et al. (2012b) Blanchet, J. H., H. Lam, B. Zwart. 2012b. Efficient rare-event simulation for perpetuities. Stochastic Processes and Their Applications 122(10) 3361–3392.

- Blanchet et al. (2019) Blanchet, J. H., J. Li, M. K. Nakayama. 2019. Rare-event simulation for distribution networks. Operations Research 67(5) 1383–1396.

- Blanchet and Liu (2008) Blanchet, J. H., J. Liu. 2008. State-dependent importance sampling for regularly varying random walks. Advances in Applied Probability 40(4) 1104–1128.

- Borkar (2009) Borkar, V. S. 2009. Stochastic Approximation: A Dynamical Systems Viewpoint. Cambridge University Press, Cambridge, UK.

- Botev and L’Ecuyer (2020) Botev, Z. I., P. L’Ecuyer. 2020. Sampling conditionally on a rare event via generalized splitting. INFORMS Journal on Computing Forthcoming.

- Botev et al. (2013) Botev, Z. I., P. L’Ecuyer, B. Tuffin. 2013. Markov chain importance sampling with applications to rare event probability estimation. Statistics and Computing 23(2) 271–285.

- Bottou et al. (2018) Bottou, L., F. E. Curtis, J. Nocedal. 2018. Optimization methods for large-scale machine learning. SIAM Review 60(2) 223–311.

- Broadie et al. (2011) Broadie, M., D. Cicek, A. Zeevi. 2011. General bounds and finite-time improvement for the Kiefer-Wolfowitz stochastic approximation algorithm. Operations Research 59(5) 1211–1224.

- Bucklew (2004) Bucklew, J. A. 2004. Introduction to Rare Event Simulation. Springer Science & Business Media, New York, NY.

- Budhiraja and Dupuis (2019) Budhiraja, A., P. Dupuis. 2019. Analysis and Approximation of Rare Events: Representations and Weak Convergence Methods. Springer, New York, NY.

- Bugallo et al. (2017) Bugallo, M. F., V. Elvira, L. Martino, D. Luengo, J. Miguez, P. M. Djuric. 2017. Adaptive importance sampling: The past, the present, and the future. IEEE Signal Processing Magazine 34(4) 60–79.

- Cannamela and Iooss (2008) Cannamela, C., J. Garnierand B. Iooss. 2008. Controlled stratification for quantile estimation. The Annals of Applied Statistics 2(4) 1554–1580.

- Chan and Kroese (2012) Chan, J. C. C., D. P. Kroese. 2012. Improved cross-entropy method for estimation. Statistics and Computing 22(5) 1031–1040.

- Chau and Fu (2015) Chau, M., M. C. Fu. 2015. An overview of stochastic approximation. M. C. Fu, ed., Handbook of Simulation Optimization, chap. 6. Springer, New York, 149–178.

- Chau et al. (2020) Chau, M., M. C. Fu, J. J. Lee, H. Qu. 2020. Multivariate stochastic approximation using a secant-tangents averaged (STAR) gradient. working paper .

- Chau et al. (2014) Chau, M., H. Qu, M. C. Fu. 2014. A new hybrid stochastic approximation algorithm. Proceedings of the 12th International Workshop on Discrete Event Systems (WODES). IFAC, New York, NY, 241–246.

- Chen et al. (2019) Chen, B., J. H. Blanchet, C.-H. Rhee, B. Zwart. 2019. Efficient rare-event simulation for multiple jump events in regularly varying random walks and compound Poisson processes. Mathematics of Operations Research 44(3) 919–942.

- Chu and Nakayama (2012) Chu, F., M. K. Nakayama. 2012. Confidence intervals for quantiles when applying variance-reduction techniques. ACM Transactions on Modeling and Computer Simulation 22(2) No.10.

- Collamore (2002) Collamore, J. F. 2002. Importance sampling techniques for the multidimensional ruin problem for general Markov additive sequences of random vectors. The Annals of Applied Probability 12(1) 382–421.

- Cornuet et al. (2012) Cornuet, J. M., J. M. Martin, A. Mira, C. P. Robert. 2012. Adaptive multiple importance sampling. Scandinavian Journal of Statistics 39(4) 798–812.

- de Boer et al. (2005) de Boer, P. T., D. Kroese, S. Mannor, R. Rubinstein. 2005. A tutorial on the cross-entropy method. Annals of Operations Research 134 19–67.

- Dieker and Mandjes (2005) Dieker, A. B., M. Mandjes. 2005. On asymptotically efficient simulation of large deviation probabilities. Advances in Applied Probability 37(2) 539–552.

- Dong and Nakayama (2017) Dong, H., M. K. Nakayama. 2017. Quantile estimation with Latin hypercube sampling. Operations Research 65(6) 1678–1695.

- Dunkel and Weber (2010) Dunkel, J., S. Weber. 2010. Stochastic root finding and efficient estimation of convex risk measures. Operations Research 58(5) 1505–1521.

- Dupuis et al. (2009) Dupuis, P., K. Leder, H. Wang. 2009. Importance sampling for weighted-serve-the-longest-queue. Mathematics of Operations Research 34(3) 642–660.

- Dupuis et al. (2012) Dupuis, P., K. Spiliopoulos, H. Wang. 2012. Importance sampling for multiscale diffusions. Multiscale Modeling & Simulation 10(1) 1–27.

- Durrett (2019) Durrett, R. 2019. Probability: Theory and Examples. 5th ed. Cambridge University Press, Cambridge, UK.

- Egloff and Leippold (2010) Egloff, D., M. Leippold. 2010. Quantile estimation with adaptive importance sampling. The Annals of Statistics 38(2) 1244–1278.

- Egloff et al. (2005) Egloff, D., M. Leippold, S. Jöhri, C. Dalbert. 2005. Optimal importance sampling for credit portfolios with stochastic approximation. SSRN working paper: 693441.

- Fabian (1968) Fabian, V. 1968. On asymptotic normality in stochastic approximation. Annals of Mathematical Statistics 39(4) 1327–1332.

- Frazier et al. (2019) Frazier, P. I., S. G. Henderson, R. Waeber. 2019. Probabilistic bisection converges almost as quickly as stochastic approximation. Mathematics of Operations Research 44(2) 651–667.

- Freimer et al. (2012) Freimer, M. B., J. T. Linderoth, D. J. Thomas. 2012. The impact of sampling methods on bias and variance in stochastic linear programs. Computational Optimization and Applications 51(1) 51–75.

- Fu (2015) Fu, M. C., ed. 2015. Handbook of Simulation Optimization. Springer, New York, NY.

- Fu and Hu (1997) Fu, M. C., J. Q. Hu. 1997. Conditional Monte Carlo: Gradient Estimation and Optimization Applications. Kluwer Academic Publishers.

- Fu and Su (2002) Fu, M. C., Y. Su. 2002. Optimal importance sampling in securities pricing. Journal of Computational Finance 5(4) 27–50.

- Ghadimi and Lan (2013) Ghadimi, S., G. Lan. 2013. Optimal stochastic approximation algorithms for strongly convex stochastic composite optimization II: Shrinking procedures and optimal algorithms. SIAM Journal on Optimization 23(4) 2061–2089.

- Glasserman (1991) Glasserman, P. 1991. Gradient Estimation via Perturbation Analysis. Kluwer Academic Publisher, Norwell, MA.

- Glasserman (2003) Glasserman, P. 2003. Monte Carlo Methods in Financial Engineering. Springer, New York, NY.

- Glasserman et al. (2000) Glasserman, P., P. Heidelberger, P. Shahabuddin. 2000. Variance reduction techniques for estimating Value-at-Risk. Management Science 46(10) 1349–1363.

- Glynn (1990) Glynn, P. W. 1990. Likelihood ratio gradient estimation for stochastic systems. Communications of the ACM 33(10) 75–84.

- Glynn (1996) Glynn, P. W. 1996. Importance sampling for Monte Carlo estimation of quantiles. Proceedings of 1996 Second International Workshop on Mathematical Methods in Stochastic Simulation and Experimental Design. Publishing House of St. Petersburg University, St. Petersburg, Russia, 180–185.

- Glynn and Iglehart (1989) Glynn, P. W., D. L. Iglehart. 1989. Importance sampling for stochastic simulations. Management Science 35(11) 1367–1392.

- Grace et al. (2014) Grace, A. W., D. P. Kroese, W. Sandmann. 2014. Automated state-dependent importance sampling for Markov jump processes via sampling from the zero-variance distribution. Journal of Applied Probability 51(3) 741–755.

- Guyader et al. (2011) Guyader, A., N. Hengartner, E. Matzner-Løber. 2011. Simulation and estimation of extreme quantiles and extreme probabilities. Applied Mathematics & Optimization 64(2) 171–196.

- Heidelberger et al. (1988) Heidelberger, P., X.-R. Cao, M. A. Zazanis, R. Suri. 1988. Convergence properties of infinitesimal perturbation analysis estimates. Management Science 34(11) 1281–1302.

- Heidergott et al. (2010) Heidergott, B., F. J. Vázquez-Abad, G. Pflug, T. Farenhorst-Yuan. 2010. Gradient estimation for discrete-event systems by measure-valued differentiation. ACM Transactions on Modeling and Computer Simulation 20(1) No.5.

- Hesterberg and Nelson (1998) Hesterberg, T. C., B. L. Nelson. 1998. Control variates for probability and quantile estimation. Management Science 44(9) 1295–1312.

- Ho et al. (1983) Ho, Y.-C., X.-R. Cao, C. Cassandras. 1983. Infinitesimal and finite perturbation analysis for queueing networks. Automatica 19(4) 439–445.

- Homem-de-Mello and Bayraksan (2014) Homem-de-Mello, T., G. Bayraksan. 2014. Monte Carlo sampling-based methods for stochastic optimization. Surveys in Operations Research and Management Science 19(1) 56–85.

- Horstein (1963) Horstein, M. 1963. Sequential transmission using noiseless feedback. IEEE Transactions on Information Theory 9(3) 136–143.

- Hsu and Nelson (1990) Hsu, J. C., B. L. Nelson. 1990. Control variates for quantile estimation. Management Science 36(7) 835–851.

- Hu et al. (2007) Hu, J., M. C. Fu, S. I. Marcus. 2007. A model reference adaptive search method for global optimization. Operations Research 55(3) 549–568.

- Hu and Su (2008) Hu, J., Z. Su. 2008. Bootstrap quantile estimation via importance resampling. Computational Statistics & Data Analysis 52(12) 5136–5142.