A Novel Multi-Period and Multilateral Price Index

Consuelo R. Nava1, Maria Grazia Zoia2∗

1 Department of Economics and Statistics “Cognetti de Martiis”, Univeristà degli Studi di Torino, Lungo Dora Siena 100A, Torino, Italy. Email: consuelorubina.nava@unito.it

2 Department of Economic Policy, Università Cattolica del Sacro Cuore, Largo Gemelli 1, 20123, Milano, Italy. Corresponding Author. Tel:+390272342948; fax: +390272342324. Email: maria.zoia@unicatt.it

∗ Corresponding author

Abstract

A novel approach to price indices, leading to an innovative solution in both a multi-period or a multilateral framework, is presented. The index turns out to be the generalized least squares solution of a regression model linking values and quantities of the commodities. The index reference basket, which is the union of the intersections of the baskets of all country/period taken in pair, has a coverage broader than extant indices. The properties of the index are investigated and updating formulas established. Applications to both real and simulated data provide evidence of the better index performance in comparison with extant alternatives.

JEL code: C43; E31; C01.Keywords: multi-period index, multilateral index, GLS solution, updating formulas, country-product dummy index.

1 Introduction

Multi-period and multilateral price indices, used to compare sets of commodities over time and across countries respectively, are of prominent interest for statisticians (see, e.g., Biggeri and Ferrari,, 2010). Several approaches to the problem have been carried out in the literature.

One of these is the axiomatic approach (see, e.g., Balk,, 1995, and the references quoted therein), which rests on the availability of both quantities and prices and aims at obtaining price indices enjoying suitable properties (Fisher,, 1921, 1922).

A second approach hinges on the economic theory111This approach is also known as preference field approach or functional approach (Divisia,, 1926). (see, among others, Diewert,, 1979; Caves et al.,, 1982, for a review) and rests on the idea that consumption choices come from the optimization of a utility function under budget constraints. Here, prices play the role of independent variables, while quantities arise as solutions to an optimization problem in accordance with the preference scheme OF decision makers.

A third approach is the stochastic one (see Clements et al.,, 2006; Diewert,, 2010, for a review), which can be traced back to the works of Jevons, (1863, 1869) and Edgeworth, (1887, 1925). Thanks to Balk, (1980) and Clements and Izan, (1987), this approach has been recently reappraised, and its role in inflation measurements duly acknowledged (see, e.g., Asghar and Tahira,, 2010, and references quoted therein). In this framework, prices are assumed to be affected by measurement errors whose bias effect must be duly minimized.

The stochastic approach (hereafter, SA) turns out to be somewhat different from other approaches, insofar as it is closely related to regression theory (Theil,, 1960; Clements and Izan,, 1987). In fact, the SA enables the construction of tests and confidence intervals for price indices, which provide useful pieces of information (Clements et al.,, 2006). Furthermore, the SA has less limits than other approaches222The SA, differently from the index number theory does not need to account for the economic importance of single prices. and clears the way to further extensions, as shown in Diewert, (2004, 2005); Silver, (2009); Rao and Hajargasht, (2016).

In this paper, we devise a multi-period/multilateral price index, MPL index henceforth, within the stochastic framework. The derivation of the MPL index, which is the solution to an optimization problem, calls for quantities and values of the commodities (not prices), like Walsh, (1901). In fact, the MPL index is obtained by applying generalized least squares (GLS) methods to a regression model linking values and quantities of the commodities. In the two-period (country) case the index turns out to be the ratio of weighted sums with harmonic means of the squared quantities as weights. Depending on the choice of the objective function to optimize, the commonly used indices, namely Laspeyeres, Paasche, Marshall-Edgeworth, Walsh and Geary Khamis, arise as special cases.

The reference basket of the MPL index, namely the set of commodities for all periods/countries, is made up of the union of the intersections of all the couples of year/country baskets in pairs. This implies that the price index of a commodity can be always computed once the latter is present in at least two periods/countries. Thus, the reference basket turns out to be more representative than the ones commonly used by the majority of statistical agencies, which either align the reference basket to that of the first period, or make it tally with the intersection of the commodity sets of all periods/countries. Eventually, such a reference basket is likely to be scarcely representative of the commodities present in each period/country. In this sense, just like hedonic (Pakes,, 2003), GESKS (Balk,, 2012) and country/time-product-dummy (CPD/TPD) approaches with incomplete price tableau (Rao and Hajargasht,, 2016), the MPL index does not drop any observation on the account of having no counterpart in the reference basket. Indeed, unlike the aforesaid approaches, the MPL index is built on quantities and values, not on prices. Accordingly, the lack of a commodity in a period/country implies setting its quantity and value equal to zero in that period/country, not its price which, being not observed, must be considered unknown but not necessarily null. Neither any preliminary computation of binary price indices, as in the GESKS approach (Ivancic et al.,, 2011), nor the use of any type of weighting matrix for dealing with missing values or quantities, as in the case of CPD/TPD indices, are needed.

The updating of the MPL index is easy to accomplish and suitable formulas, tailored to the multi-period or multilateral nature of the data, are provided. In fact, while the inclusion of fresh values and quantities, of a set of commodities corresponding to an extra period, does not affect the previous values of the MPL index, the inclusion of a new country affects all former MPL indices. Hence, two updating formulas have been proposed for the MPL index: one for the multi-period case and another for the multilateral case. Closed-form expressions for the standard errors of the MPL estimates are provided and the properties of the estimators are duly investigated. An empirical comparison of the MPL index to CPD/TPD index – a multilateral/multi-period index that, like the MPL one, can be read as a solution to an optimization problem – provides evidence of an easier implementation and greater efficiency of the former index.

To sum up, a threefold novelty characterizes the paper. First, it proposes a price index, which proves effective either for the multi-period or the multilateral case.

Second, updating formulas tailored to the multilateral and the multi-period version of the index are provided.

Third, the grater simplicity of use and efficiency of the said index is highlighted in comparison with well-known standard multilateral/multi-period indices.

Furthermore, the approach employed to build the MPL index yields the so called reference prices, which are the prices expected to be paid for the commodities in the base time/country. The latter together with the values of MPL index allow to determine the prices of those commodities that, for whatever reason, can not be observed in a given period or country.

The MPL index proves to be particularly useful when i) there is the need of a reference basket more representative than the mere intersection of the baskets involved in all periods/countries or in presence of ii) historical data; iii) when the prices of some commodities in some periods/countries are unknown. In a multi period-perspective, this may occur, for instance, when some commodities enter or leave the basket as a consequence of a technological change. The knowledge of prices is lacking in the periods that are antecedent the inclusion of commodities in the basket or in the periods that are subsequent their exclusion from the basket. In a multilateral perspective, this happens when a commodity is not dealt in yet on the market of a given country.

The paper is organized as follows. In Section 2, within the SA, we devise the MPL index according to a minimum-norm criterion as well as its updating formulas for the multi-period and the multilateral cases, respectively. Section 3 is devoted to the properties of the MPL index. Section 4 provides an application of the MPL index to the Italian cultural supply data to shed light on its potential as both a multi-period and a multilateral index. To gain a better insight into the performance of the MPL index, a comparison with the CPD/TPD indices is made by using both real and perturbed data. Section 5 enriches previous empirical evidences with a simulation example, while Section 6 completes the paper with some concluding remarks and hints. For the sake of easier readability, an Appendix has been added with proofs and technicalities.

2 The MPL index as solution to an optimization problem

In this section, taking the SA as the reference frame, we derive a multi-period/multilateral price index whose reference basket – over a set of periods or across a set of countries – is the union of the intersections of the commodity baskets of various periods/countries, taken in pairs. Such a reference basket proves to be an effective solution for several reasons. First, it is broader and more representative than the ones built on the intersection of commodities which are present in all periods/countries. Second, the price index is well defined, provided each commodity is present in at least two baskets.333Some similarities arise with the chaining rule (Forsyth and Fowler,, 1981; von der Lippe,, 2001) where the price index is a measure of the cumulative effect of adjacent periods from 0 to 1, 1 to 2, , to . Thus, chain indices compare the current and the previous periods in order to evaluate the evolution over many periods (for a comparison of this approach with the fixed base one see Diewert, (2001)). However, chain indices, unlike the MPL index, leave unresolved the reference basket updating and are not applicable in a multilateral perspective. The computation of the MPL price index hinges on quantities and values of the commodities, not prices. The lack of a commodity in a given period/country entails that both its quantity and value vanish in that period/country.

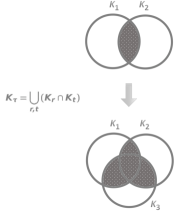

Figure 1 shows the reference basket corresponding to the usual approach as compared with that devised in the paper for the case of two and three periods/countries.

According to the SA, the MPL index is worked out as solution of an optimization problem consisting in finding an hyperplane lying as close as possible to the points whose coordinates are the commodities prices in periods. In fact, it hinges on the idea that in each time/country , the commodity prices move proportionally to a set of reference prices to within “small” discrepancies, that is

| (1) |

or

| (2) |

Here is the actual price vector of the commodities at period/country , is the vector of the unknown (time invariant) reference prices, is a scalar factor acting as price index at period/country and is the discrepancy vector, that is a vector of error terms. As per Eq. (2), in each period/country , the prices can be represented by a point in a -dimensional space. Accordingly, the prices in periods/countries, namely , can be represented by points in a -dimensional space. If all prices move proportionally, these points would lie on a hyperplane, , and, in particular, on a straight line crossing the origin for . In general, this is only approximately true and a price “line” crossing the origin is chosen with the property of fitting the observed price points, by minimizing the deviations of the data from the “line”. In compact notation, Eq. (1) can be more conveniently reformulated as follows

| (3) |

where is the vector of the price indices and is the vector of the (unknown) reference prices. According to Eq. (3), the problem of determining a set of price indices can be read as the problem of approximating the price matrix, , with a matrix of unit rank, , defined as the outer product of a vector of price indices by a virtual price vector. Moving from prices to values, the matrix of the values of commodities in periods/countries has the following representation

| (4) |

where is the matrix of the quantities of commodities in periods/countries and stands for the Hadamard (element-wise) product. According to Eq. (4), the values of commodities at time or for the -th country can be represented as

| (5) |

where and are the -th columns of and respectively, and is added to embody the error term inherent in the model specification of Eq. (4). The above formula, taking into account the identity

can be re-written as

| (6) |

where takes the role of the deflator, and denotes a diagonal matrix with diagonal entries equal to the elements of .444The matrix is defined as follows: Eq. (6) expresses the value, , of each commodity at time (discounted by a factor ) as the product between the (time invariant) reference price, , and the corresponding quantity, , plus an error term, . By assuming , its inverse tallies with the price index in Eq. (5). Over periods/countries, the model can be written as

| (7) |

where is a diagonal matrix with diagonal entries equal to the elements of .

With no lack of generality, we assume that the first period is the base period (that is =), and write the first equation separately from the others . The system takes the form

| (8) |

or equivalently, the form

| (9) |

After some computations555Use has been made of the relationships where is a diagonal matrix whose diagonal entries are the elements of the vector and is the transition matrix from the Kronecker to the Hadamard product (Faliva,, 1996). , the system can be more conveniently rewritten in the form

| (10) |

Here, , is a vector whose elements are the diagonal entries of as specified in Eq. (8), and denotes the transition matrix from the Kronecker to the Hadamard product.666The matrix is defined as follows where represents the dimensional -th elementary vector. An estimate of the vector can be obtained by applying generalized least squares (GLS), by taking

| (11) |

where and is a block diagonal matrix

| (12) |

In this connection, we have the following result.

Theorem 1.

The GLS estimate of the deflator vector is given by

| (13) |

where is the matrix whose -th columns is and . The vector , whose entries are the reciprocals of non-null elements of the GLS estimate of and zero otherwise, is the MPL index of commodities over periods or between countries.777 The vector is defined as follows (14)

Proof.

See Appendix 1.1. ∎

The following corollaries provide estimates of the deflator vector for special cases of interest.

Corollary 1.

Let us assume that the error terms of the system in Eq. (10) are stationary. Accordingly, the diagonal blocks, of the matrix are the same, i.e. for all . Then, the GLS estimate of the deflator vector, , is

| (15) |

where is the matrix whose column is and .

Proof.

The proof is given in Appendix 1.2. ∎

The case is worth considering because it sheds light on the index structure. When assuming stationary and uncorrelated error terms, the matrix reduces to a diagonal matrix, i.e. , and the price index turns out to be simply the ratio of weighted price averages, as stated in the following corollary.

Corollary 2.

Let the matrix be diagonal and . Then the MPL index for a set of commodities is

| (16) |

Here is the price vector of the commodities at time and is the weight vector whose -th entry is

| (17) |

Proof.

See Appendix 1.3. ∎

In case the diagonal entries of are all equal, say equal to 1, then Eq. (16) would tally with the OLS version of the MPL index. In this case the weights of the index would be function of the harmonic mean of the squared quantities

| (18) |

Two considerations are worth making about Eq. (16). The first is that most well-known price indices can be viewed as particular cases of the MPL index. In fact, they can be obtained from Eq. (16) for particular choices of the scalars , as proved in the following corollary.

Corollary 3.

By taking

| (19) |

then and the MPL index tallies with the Laspeyeres index, , i.e.

| (20) |

By taking

| (21) |

then and the MPL index turns out to tally with the Paasche index, , i.e.

| (22) |

By taking

| (23) |

then and the MPL index turns out to tally with the Marshal-Edgeworth index, i.e.

| (24) |

By taking

| (25) |

then and the MPL index turns out to tally with the Walsh index, , i.e.

| (26) |

where is a vector whose entries are the square roots of those of the vector .

By taking

| (27) |

and considering the square roots of the quantities in the index computation, then and the MPL index turns out to tally with the Geary-Khamis index (Drechsler,, 1973), , i.e.

| (28) |

where is a vector whose -th entry is .

Proof.

The proof is simple and follows straight forward. Therefore, it is omitted. ∎

The other consideration is that the index can be obtained as solution of an optimization problem specified as in the following corollary.

Corollary 4.

With reference to the following model

| (29) |

where is a vector of random terms, the index is solution of the optimization problem

| (30) |

where is a (semi)norm of and is given by

| (31) |

with is a vector whose the -th entry, , is specified as in Eq. (17).

Proof.

See Appendix 1.4. ∎

Eq. (29), together with Figure 1, is useful to show that the index basket is the union of the intersection of the commodities that are present in at least two periods/countries and, accordingly, it does not include commodities which are not present in at least two periods/countries. In fact, simple computations prove that weights pertaining commodities not fulfilling this condition turn out to be null. Consequently, the value of the index does not change if computed leaving out them, as shown by the following example.

Example 1.

Let us consider the case of three commodities in two periods and assume that the first commodity is missing in both periods (i.e. ). Then, let us assume that for each for simplicity. Simple computations prove that the weight, as defined in Eq. (18), associated to the first coefficient turns out to be null

The same happens if the first commodity is missing in just one period, for instance the second one () As in the previous case, the coefficient vanishes

Accordingly, in both cases the first commodity can be left out from the computation of the index. In fact, the value of the latter does not change if computed by considering only the second and the third commodities.

As a by-product of Theorem 1, we state the following result.

Corollary 5.

The variance-covariance matrix of the deflator vector, , given in Theorem 1 is

| (32) |

where

The -th diagonal entry of the above matrix provides the variance of the deflator in the -th period/country, given by

| (33) |

where , and denote the -th column of the matrix , and , respectively.

Proof.

See Appendix 1.5. ∎

As for the deflator vector , its moments and confidence intervals can be easily obtained within the theory of linear regression models, from the result given in Corollary 5. As the price index vector turns out to be the reciprocal of the said deflator (see Eq. 13), its statistical behavior can be derived from the former, following the arguments put forward, for example, in Geary, (1930); Curtiss, (1941) and Marsaglia, (1965), merely to quote a few, on ratios (in particular reciprocals) of random variables. The following corollary provides an approximation of the variance of , obtained by using the first Taylor expansion of the variance of a ratio of two random variables.

Corollary 6.

The variance of the MPL index is

| (34) |

In the above equation where are the GLS residuals of Eq. (10) and is an estimate of .

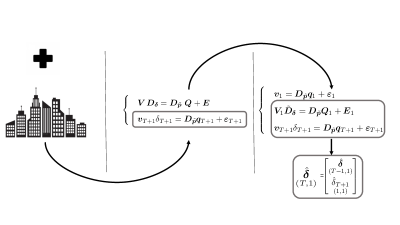

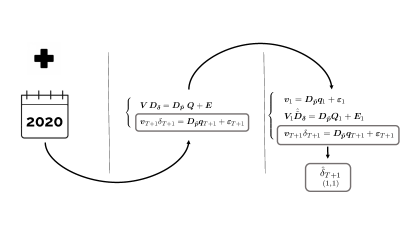

2.1 The MPL update

The following two theorems provide updating formulas for the price index . The former proves suitable when the index is used as a multilateral price index,while the latter is appropriate when it is employed as a multi-period index. In the former case, values and quantities of the commodities included in the reference basket are assumed available for an additional country. In the latter case, it is supposed that values and quantities of the commodities included in the reference basket become available at time . It is worth noting that the approach used to update the index guarantees the temporal fixity issue requiring that its historical values must not be affected by the inclusion of values and quantities pertaining a new period. Spatial fixity, demanding that results for a core set of countries must be unaffected by the inclusion of new countries, is not preserved by the updating method here proposed. This property can be easily fulfilled by updating the index with the same approach used for the multi-period index.

Theorem 2.

Should the values and quantities of commodities of a reference basket become available for a new additional country, say the -th, then, the updated multilateral version of the MPL index, , turns out to be the vector of the reciprocals, as defined in Eq. (13), of the following deflator vector

| (35) |

Here the symbols are defined as in Theorem 1. The terms , denote the vector of values and quantities of commodities of the new -th country, respectively and with variance-covariance matrix of the disturbances at time .

Proof.

See Appendix 1.6. ∎

Theorem 3.

Should the values and quantities of commodities of a reference basket become available for time , then, the updated value of the multi-period version of the MPL index at time turns out to be the reciprocal of the deflator value at time

| (36) |

where and is defined as in Eq. (13).

Proof.

See Appendix 1.7. ∎

Figure 2 highlights the difference between the updating process of the deflator, and thus of the price index, depending on whether it is used in the multilateral or in the multi-period case.

3 Properties of the MPL index

Let us assume for simplicity and denote with a generic index number where and are prices and quantities at time . Without lack of generality, is assumed to be the base period. Following Predetti, (2006), Martini, (1992) and Fattore, (2010), the main properties of an index number can be summarized as follows:

-

P.1

Strong identity: .

-

P.2

Commensurability: where is a vector with non-null entries and is the vector of reciprocals of the entries of .

-

P.3

Proportionality: with .

-

P.4

Dimensionality: with .

-

P.5

Monotonicity: and with where is the unit vector.

Moreover, also the following properties are worth mentioning:

-

P.6

Positivity: , with positive constant;

-

P.7

Inverse proportionality in the base period: ;

-

P.8

Commodity reversal property: invariance of the index with respect to any commodity permutation;

-

P.9

Quantity reversal test: a change in the quantity order does not affects that remains invariant . Therefore the index price does not change.

-

P.10

Base reversibility (symmetric treatment of time) ;

-

P.11

Transitivity ;

-

P.12

Monotonicity: If , then .

Proposition 1.

The MPL index satisfies all properties.

Proof.

See Appendix 1.8. ∎

4 The Italian cultural supply: an application of the MPL index

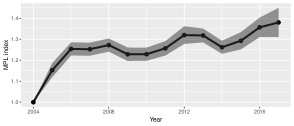

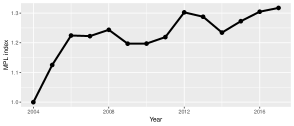

In this section, we provide an application of the MPL index to Italian cultural supply data, such as revenues and the number of visitors to museums (i.e. monuments, archeological sites, museum circuits, ). The availability of temporal and geographical data on Italian culture provides a stimulating basis for ascertaining the potential of the MPL price-index methodology set forth in this paper. The flexibility of the MPL index paves the way to moving beyond ISTAT (and similar) analyses, which are confined to price indices on the supply of data on Italian culture like access to museums and entertainment sectors, aggregated at the national level (ISTAT,, 2020). In addition, to evaluate the performance of the MPL index, we have made a comparison with the CPD/TPD price indices (Diewert,, 2005; Rao and Hajargasht,, 2016), using both real and simulated data. Reference has been made to this approach because, under the log-normality assumption of the error term, the maximum likelihood estimator of the said price index tallies with the least square one, likewise the MPL index. As for the nature of the data, note that Italian cultural heritage is at the top of various world-class lists and plays a key role in the Italian economy (see, e.g., Symbola,, 2019).888The Italian heritage supply chain accounts for 4,889 museums and the like; it generated almost 200 million euro of revenues in 2017 and employs 38.300 people (ISTAT,, 2019). Lately, local cultural supply has evolved significantly. Indeed, most of the Italian museum circuits were founded relatively recently.999Approximately 2,300 sites (45.5%) of the Italian cultural supply chain were opened between 1960 and 1999, while 2,200 sites (38.6%) were opened in 2000, taking advantage of the investments for economic recovery and infrastructure enhancement made for Italian cultural heritage sites (ISTAT,, 2016). In the following analysis, we have considered the ranking of the top 30 Italian cultural institutions (museums and the like) according to the highest number of annual visitors since 2004 (data source: www.statistica.beniculturali.it). Among these, only 20 of the internationally renowned institutions remained ranked in the top 30 on a yearly basis. The other 10 positions were held by museums and institutions which only temporarily experienced an outstanding flow of visitors. These observations led to a twofold issue. First, the need to set-up a price index finalized at registering changes in the period under consideration. Second, a dynamic updating method of the index in order to preserve the information associated with the 10 positions not consistently present in the top 30 ranking (aspects which are not considered in the approaches usually adopted by most statistical agencies). The multi-period version of the MPL price index proves suitable for this scope. Hence, it has been applied to the data set which collects the number of visitors and revenues of the 30 leading Italian cultural institutions which, from 2004 to 2017, were ranked at least two times in the top 30.101010All analyses in this investigation have been made with our own codes, written in R.

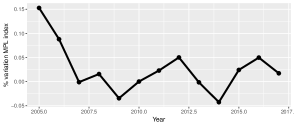

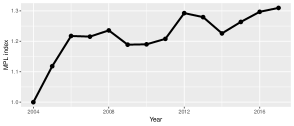

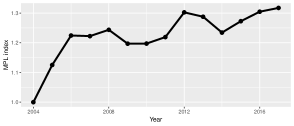

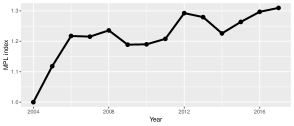

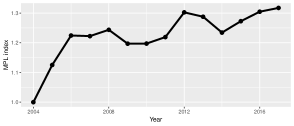

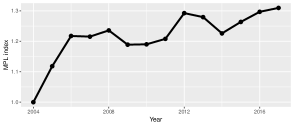

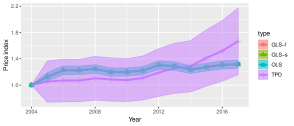

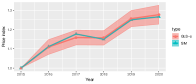

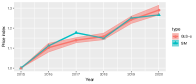

Figure 3 shows the MPL price index together with its annual percentage variations for the period 2004–2017: 2004 being the base year and 2017 the year used for updating the index. Here the computation of the index has been done by assuming non spherical, and in particular heteroschedastic and uncorrelated (GLS-d) error terms. Looking at the graph, we can note that in the early years of the new Millennium, when important investments started being made in the Italian cultural sector, the prices of museums (and the like) tickets grew (Figure 3). Thereafter, the price dynamic became more moderate and then tapered in 2009 and 2014 when, the so called “W” recession, namely the international financial and debt crisis in European peripheral countries, hit Italy.

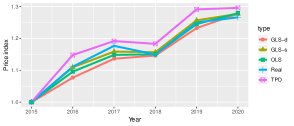

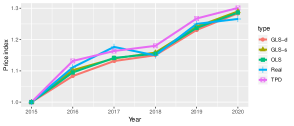

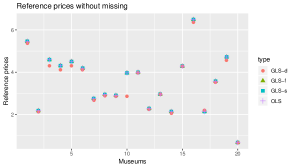

The MPL has been also computed under other specifications of the error terms and by taking into account the possibility of missing commodities. In particular, it has been also worked out by assuming heteroschedastic and correlated (GLS-f), stationary (GLS-s) and spherical error terms (OLS), both in the case when the commodities are present in all period (case of complete price tableaux) and when some of them are missing (case of incomplete price tableaux). In Appendix 2.1 the graphs of the MPL index in all these cases are shown.

For the sake of further evidence from an empirical standpoint, the MPL has been also compared to the TPD index.

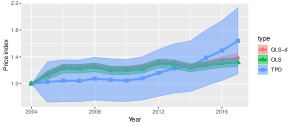

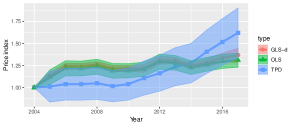

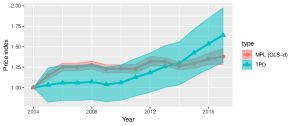

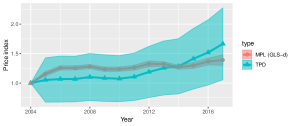

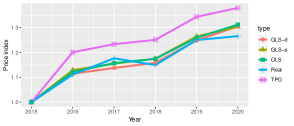

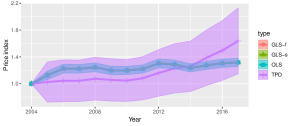

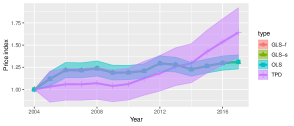

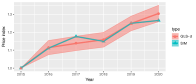

Figure 4 shows both the MPL, computed under the assumption of heteroschedastic and uncorrelated error terms, and TPD price indices together with their confidence bounds. In the left panel the price indices have been computed only for those museums whose prices are available at all times. This has led to a drop in the number of museums/monuments/archaeological sites from 36 to 17 (note that this case corresponds to the “standard” reference basket). The right panel shows these indices computed with data from 36 museums ranked in the top 30 at least twice together with their confidence bounds. In this case, when not all items (museums) are priced in all periods, TPD estimates have been obtained by using the time version of the weighted CPD (Rao and Hajargasht,, 2016, pp. 420-421). Looking at both panels we see that the two indices are aligned, but that the MPL one always fall within the confidence bounds of TPD indices. This result provides evidence of the MPL greater efficiency, due to its lower standard errors. For completeness, in Appendix 2.1 the estimated reference prices, under the different error specifications, have been displayed.

The availability of data on visitors and revenues in 2017 for museums, monuments, archaeological sites, and museum circuits in the North-West, North-East, Centre and South (which includes the two islands Sicily and Sardinia) has allowed the computation of the multilateral version of the MPL index. Looking at the data, we see that almost half (46.3%) are located in the North, while 28.5% in the Centre, and 25.2% in the South and Islands. The Regions with the highest number of cultural institutions are Tuscany (11%), followed by Emilia-Romagna (9.6%), Piedmont (8.6%) and Lombardy (8.2%) (ISTAT,, 2016). However, alongside the more famous attractions, Italy is home to a wide and rich array of notable locations of cultural interest. A considerable percentage of these places (17.5%) are found in municipalities with less than 2,000 inhabitants, but which can have up to four or five cultural sites in their small area. Almost a third (30.7%) are distributed in 1,027 municipalities with a population varying from 2,000 to 10,000, and a bit more than half (51.8%) are situated in 712 municipalities with a population of 10,000 to 50,000. Italy is, therefore, characterized by a strongly polycentric cultural supply distributed throughout its territory, even in areas considered as marginal from a geographic stance.

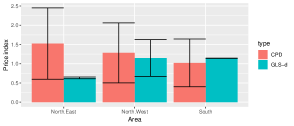

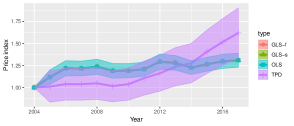

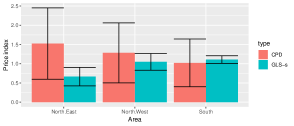

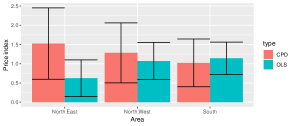

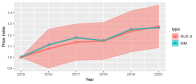

Table 1 reports, in the first three rows, the MPL index, computed under the assumption of stationary (GLS-s), non-spherical (GLS-d) and spherical (OLS) error terms, for three areas (North-West, North-East and Centre) considering the Centre as base area. The following three rows show updated values of the MPL index, computed for the GLS-s, GLS-d and OLS specifications of the error terms, when the South-Islands are added to the data-set. As for the multi-period case, a comparison of the MPL estimates with the CPD ones is provided. The last row of Table 1 shows CPD estimates in the case of full price tableau, as all commodities are priced in the four geographic areas. Figure 5 shows both the MPL and CPD indices together with their confidence bounds. The comparison of the CPD and MPL indices computed under other specifications for the error terms (GLS-f and OLS) is provided in Appendix Appendix 2.2. Once again, the estimates of the MPL index turn out to be more accurate than those provided by the CPD approach, as the former have standard errors lower than the latter. As in the comparison with the TPD index, the confidence bounds of CPD indices always include MPL estimates, thus suggesting the compatibility of the MPL index with the estimates provided with the CPD one. It is worth noting that in 2017, access to cultural sites in Southern Italy cost the most: almost twice as much as in the North-Eastern area. While the disparity could be ascribed to several factors, such as different costs of managing museums and similar institutions, tourism flows, etc: that type of analysis goes beyond the scope of the current investigation.

| North West | North East | Centre | South | |

|---|---|---|---|---|

| MPL-GLS-s | 1.070 (0.021) | 0.634 (0.018) | 1.000 | |

| MPL-GLS-d | 1.162 (0.165) | 0.632 (0.011) | 1.000 | |

| MPL-OLS | 1.072 (0.200) | 0.621 (0.194) | 1.000 | |

| Updated MPL-GLS-f | 1.048 (0.078) | 0.665 (0.087) | 1.000 | 1.107 (0.036) |

| Updated MPL-GLS-d | 1.148 (0.174) | 0.631 (0.008) | 1.000 | 1.143 (0.001) |

| Updated MPL-OLS | 1.070 (0.176) | 0.622 (0.174) | 1.000 | 1.142 (0.153) |

| CPD | 1.524 (0.337) | 1.283 (0.284) | 1.000 | 1.021 (0.226) |

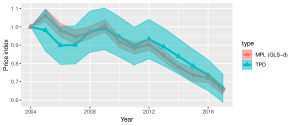

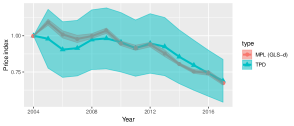

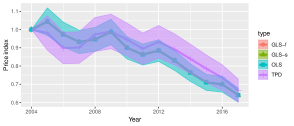

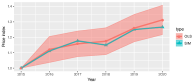

Finally, in order to investigate more thoroughly the performance of the MPL index as compared to the TPD one, a simulation analysis has been performed based on the perturbation of the original value matrix . In particular, one thousand simulations have been carried out by using perturbed values (and prices as a by-product) and assuming fixed quantities (i.e. equal to the original ones). Next, the simulated values (and prices) have been used to compute MPL and TPD indices in different settings: with and without missing quantities (and accordingly prices in the TPD model). The final MPL and TPD indices have been obtained as averages of all indices computed on simulated values (and prices). Two types of simulations have been carried out. First, simulated values from the -nd to the -th period (base period values, , being kept fixed) have been obtained by adding random perturbations, drawn from Normal laws with different means and variances, to the original values of . The plots in Figure 6 show both the MPL and the TPD indices obtained by using these simulated data together with the associated confidence bounds. As before the MPL index has been computed under the assumption of heteroschedastic and uncorrelated error terms (GLS-d).

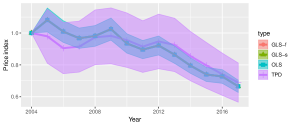

Then, following another approach, simulated values, from the -nd to the -th period (base period values, , being kept fixed), have been obtained from simulated values of the previous period with the addition of perturbation terms, drawn from Normal laws with given means and variances. Plots in Figure 7 show both the MPL, and the TPD indices, for the case of complete and incomplete price tableau, together with the associated confidence bounds. As before the MPL index has been computed under the assumption of heteroschedastic and uncorrelated error terms (GLS-d). Looking at these figures, we see that in both cases, the MPL estimates are in line with the TPD ones, but are more accurate than the latter as their tighter confidence bounds show.

In Appendix 2.3, a comparison of the TPD and the MPL indices, always computed on data simulated and by assuming other specifications for the error terms, (GLS-f, GLS-s and OLS), is provided.

5 A simulation example

To further illustrate the potentialities of the MPL index, the latter has been computed by using a simulated data set built as follows. For given , and , the values have been computed according to Eq. 5. The random terms of this equation have been generated from a standard Normal distribution. These elements represent the ingredients of the system in Eq. 10 used to work out the MPL index. The aim of this simulation is to see the capability of the MPL and TPD indices to reproduce the values of the “true” index . Let’s assume that the quantities, , the reference prices, and the values of the price index, , of four commodities from 2015 to 2020 are specified as follows

Then, with these data at hand, the values computed as in Eq. 5 result to be

while the price matrix, needed to compute the TPD index, hereafter, is

The matrices and have been used to compute both the MPL and the TPD indixes, in a multi-period perspective. In particular, the MPL index has been computed under several specification of the error terms and, more precisely, stationary (GLS-s), heteroschedastic and uncorrelated (GLS-d), spherical (OLS) error terms.

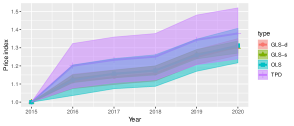

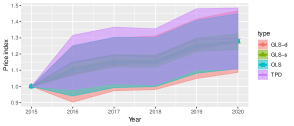

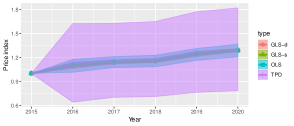

We propose three different examples in which the MPL is compared with the TPD in the following cases

-

1.

complete price tableau, implying a reference basket including the complete set of the four commodities;

-

2.

incomplete price tableau, assuming missing the second and forth commodity, (that is and ), with a “standard” reference basket, (see the left-hand side of Figure 1) that, accordingly includes only the first and the third commodities;

-

3.

incomplete price tableau assuming missing the second and forth commodity, (that is and ), with the “MPL” reference basket, (see the right-hand side of Figure 1), that includes commodities present in at least two periods, namely all the four commodities.

The rows of Table 2 provides the sum of the squares of the differences between the estimated indices (GLS-s, GLS-d, OLS, and TPD) and the index for the three cases . Looking at this table, we see that the MPL index, whatever is the specification assumed for the error terms, provides always the best fit to the index . Thus, for any specification of the error terms, the MPL index exhibits an higher performance than the TPD, except for the GLS-d in the third case. In Appendix 3, the graphs of both the TPD and MPL indixes are provided under different specifications for the error terms (GLS-s, GLS-d; OLS). In all cases the MPL estimates turn out to be more accurate, as they have lower variances and, consequently, they are always included in a confidence band of the TPD (see Figure 16).

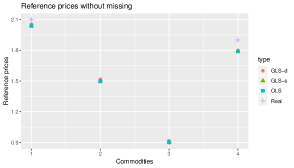

These examples are also particularly interesting to highlight the role played by the reference prices , which are the prices that consumers are expected to pay for the commodities in the base period/country.

Reference prices prove useful

to obtain estimates of the prices of those commodities which, being missing in the basket, can not be determined.

This case occurs in the third example with incomplete price tableau and reference basket including the complete set of commodities. In this case, if a commodity, say , is missing in a period, say , then its price, even if different from zero, turns out to be undetectable.

However, in the MPL approach, it can be determined, through the estimates of both its associated reference price and price index , as follows

.

This strategy has been used to estimate the prices of the second and fourth commodity in the third case.

To assess the goodness of the estimates

, , in reproducing

the real prices , ,

the sum of the squares between observed and estimated prices have been computed for all commodities, either included in the basket or missing. The results, reported in Table 3 in Appendix 3, are very satisfactory.

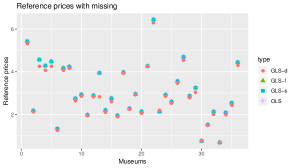

Looking at Figure 17 in Appendix 3, which compares the estimates of the reference prices with the “real” ones, it is clear that the MPL proves able to suitably estimate the reference prices for all commodities, also for the missing ones.

Figure 18 compares the values of the MPL and TPD indexes to the real price index of this experiment. Interestingly, differently from the TPD, the MPL better captures the trend of the “real” price index over time, avoiding a TPD overestimation issue (see Table 2) in all cases (except for the GLS-d incomplete price tableau with the novel basket).

Finally, in Table 4 in Appendix 3 “real” prices have been compared with their estimates obtained by using the MPL and the TPD index, given by and for the former and the latter, respectively. The better performance of the MPL compared to the TPD one in reproducing the sequences of prices emerges from Table 4, providing the sum of the squares of the differences between the real prices and the ones estimated by the two indexes.

| Data | GLS-s | GLS-d | OLS | TPD | |||

|---|---|---|---|---|---|---|---|

|

0.00308 | 0.00311 | 0.00333 | 0.04327 | |||

|

0.00053 | 0.00327 | 0.00126 | 0.00520 | |||

|

0.00219 | 0.00352 | 0.00212 | 0.00301 |

6 Conclusion

The paper works out a novel price index that can be used either as a multi-period or as a multilateral index. This index, called MPL index, is obtained as a solution to an “ad hoc” minimum-norm criterion, within the framework of the stochastic approach. The computation of the MPL index does not require the knowledge of commodity prices, but only their quantities and values. The reference basket of the MPL index, over periods or across countries, is more informative and complete than the ones commonly used by statistical agencies, and easy to update. The updating process is twofold depending on the multi-period or the multilateral use of the index. An application of the MPL index to the Italian cultural supply data provides proof of its positive performance. A comparison between the MPL and the CPD/TPD index on both real and simulated data provides evidence of the greater efficiency of the MPL estimates.

Thus, the MPL index is very promising both in the multi-period and the multilateral perspective, also considering the simple and efficient way of updating the index series (Diewert and Fox,, 2020).

The approach here proposed can be extended along several paths. For instance, the application of the MPL index for a multilateral comparison across countries using different currencies would require a suitable adjustment to ensure comparability among countries. This could be done by using a set of purchasing power parities to convert the different currencies into a common one. In this case, the MPL index could be built by employing “international” quantities and “country volumes” as suggested by (Balk,, 1996). Furthermore, the MPL approach could be employed to construct price indexes across both space and time as in (Hill,, 2004). Both these research lines are being investigated.

Acknowledgements

We sincerely thank Prof. E. Diewert for his valuable and constructive suggestions, as well as precious comments during the development of this article.

All remaining errors, typos or inconsistencies of this work are of our own.

References

- Asghar and Tahira, (2010) Asghar, Z. and Tahira, F. (2010). Measuring inflation through stochastic approach to index numbers for Pakistan. Pakistan Journal of Statistics and Operation Research, 5(2):91–106.

- Balk, (1980) Balk, B. M. (1980). A method for constructing price indices for seasonal commodities. Journal of the Royal Statistical Society. Series A (General), 143(1):68–75.

- Balk, (1995) Balk, B. M. (1995). Axiomatic price index theory: a survey. International Statistical Review/Revue Internationale de Statistique, 63(1):69–93.

- Balk, (1996) Balk, B. M. (1996). A comparison of ten methods for multilateral international price and volume comparison. Journal of official Statistics, 12(2):199.

- Balk, (2012) Balk, B. M. (2012). Price and quantity index numbers: models for measuring aggregate change and difference. Cambridge University Press.

- Biggeri and Ferrari, (2010) Biggeri, L. and Ferrari, G. (2010). Price Indexes in Time and Space. Springer.

- Caves et al., (1982) Caves, D. W., Christensen, L. R., and Diewert, W. E. (1982). The economic theory of index numbers and the measurement of input, output, and productivity. Econometrica, 50(6):1393–1414.

- Clements et al., (2006) Clements, K. W., Izan, H. I., and Selvanathan, E. A. (2006). Stochastic index numbers: a review. International Statistical Review, 74(2):235–270.

- Clements and Izan, (1987) Clements, K. W. and Izan, H. Y. (1987). The measurement of inflation: a stochastic approach. Journal of Business & Economic Statistics, 5(3):339–350.

- Curtiss, (1941) Curtiss, J. (1941). On the distribution of the quotient of two chance variables. The Annals of Mathematical Statistics, 12(4):409–421.

- Diewert, (1979) Diewert, W. E. (1979). The economic theory of index numbers: a survey. Department of Economics, University of British Columbia.

- Diewert, (2001) Diewert, W. E. (2001). The consumer price index and index number theory: a survey. Department of Economics UBC, Discussion paper, 01(02).

- Diewert, (2004) Diewert, W. E. (2004). On the Stochastic Approach to Linking the Regions in the ICP. Department of Economics, University of British Columbia.

- Diewert, (2005) Diewert, W. E. (2005). Weighted country product dummy variable regressions and index number formulae. Review of Income and Wealth, 51(4):561–570.

- Diewert, (2010) Diewert, W. E. (2010). On the stochastic approach to index numbers. Price and productivity measurement, 6:235–62.

- Diewert and Fox, (2020) Diewert, W. E. and Fox, K. J. (2020). Substitution bias in multilateral methods for cpi construction. Journal of Business & Economic Statistics, pages 1–15.

- Divisia, (1926) Divisia, F. (1926). L’indice monétaire et la théorie de la monnaie (suite et fin). Revue d’économie politique, 40(1):49–81.

- Drechsler, (1973) Drechsler, L. (1973). Weighting of index numbers in multilateral international comparisons. Review of Income and Wealth, 19(1):17–34.

- Edgeworth, (1887) Edgeworth, F. Y. (1887). Report of the committee etc. appointed for the purpose of investigating the best methods of ascertaining and measuring variations in the value of the monetary standard. memorandum by the secretary. Report of the British Association for the Advancement of Science, 1:247–301.

- Edgeworth, (1925) Edgeworth, F. Y. (1925). Memorandum by the secretary on the accuracy of the proposed calculation of index numbers. Papers Relating to Political Economy, 1.

- Elandt-Johnson and Johnson, (1980) Elandt-Johnson, R. C. and Johnson, N. L. (1980). Survival models and data analysis. John Wiley & Sons.

- Faliva, (1996) Faliva, M. (1996). Hadamard matrix product, graph and system theories: motivations and role in econometrics. In Camiz, S. and Stefani, S., editors, Proceeding of the conference on Matrices and Graphs, Theory and Applications to Economics, pages 152–175. World Scientific.

- Faliva and Zoia, (2008) Faliva, M. and Zoia, M. G. (2008). Dynamic model analysis: advanced matrix methods and unit-root econometrics representation theorems. Springer Science & Business Media.

- Fattore, (2010) Fattore, M. (2010). Axiomatic properties of geo-logarithmic price indices. Journal of Econometrics, 156(2):344–353.

- Fisher, (1921) Fisher, I. (1921). The best form of index number. Quarterly Publications of the American Statistical Association, 17(133):533–551.

- Fisher, (1922) Fisher, I. (1922). The making of index numbers: a study of their varieties, tests, and reliability. Houghton Mifflin.

- Forsyth and Fowler, (1981) Forsyth, F. and Fowler, R. F. (1981). The theory and practice of chain price index numbers. Journal of the Royal Statistical Society. Series A (General), 144(2):224–246.

- Geary, (1930) Geary, R. C. (1930). The frequency distribution of the quotient of two normal variates. Journal of the Royal Statistical Society, 93(3):442–446.

- Hill, (2004) Hill, R. J. (2004). Constructing price indexes across space and time: the case of the european union. American Economic Review, 94(5):1379–1410.

- ISTAT, (2016) ISTAT (2016). I musei le aree archeologiche e i monumenti in Italia. ISTAT.

- ISTAT, (2019) ISTAT (2019). I musei le aree archeologiche e i monumenti in Italia. ISTAT.

- ISTAT, (2020) ISTAT (2020). Consumer prices: provisional data. ISTAT.

- Ivancic et al., (2011) Ivancic, L., Diewert, W. E., and Fox, K. J. (2011). Scanner data, time aggregation and the construction of price indexes. Journal of Econometrics, 161(1):24–35.

- Jevons, (1863) Jevons, W. S. (1863). A Serious Fall in the Value of Gold Ascertained: And Its Social Effects Set Forth. E. Stanford.

- Jevons, (1869) Jevons, W. S. (1869). The depreciation of gold. Journal of the Statistical Society of London, 32:445–449.

- Marsaglia, (1965) Marsaglia, G. (1965). Ratios of normal variables and ratios of sums of uniform variables. Journal of the American Statistical Association, 60(309):193–204.

- Martini, (1992) Martini, M. (1992). I numeri indice in un approccio assiomatico. Giuffrè.

- Pakes, (2003) Pakes, A. (2003). A reconsideration of hedonic price indexes with an application to pc’s. American Economic Review, 93(5):1578–1596.

- Predetti, (2006) Predetti, A. (2006). I numeri indici. Teoria e pratica dei confronti temporali e spaziali. Giuffrè Editore.

- Rao and Hajargasht, (2016) Rao, D. P. and Hajargasht, G. (2016). Stochastic approach to computation of purchasing power parities in the international comparison program (icp). Journal of econometrics, 191(2):414–425.

- Silver, (2009) Silver, M. (2009). The hedonic country product dummy method and quality adjustments for purchasing power parity calculations. In IMF Working Paper WP/09/271. International Monetary Fund, Washington DC.

- Stuard and Ord, (1994) Stuard, A. and Ord, J. K. (1994). Kendall’s Advanced Theory of Statistics (Distribution Theory, Vol. 1). Halsted Press, New York.

- Symbola, (2019) Symbola (2019). Io sono cultura 2019, l’italia della qualità e della bellezza sfida la crisi. I Quaderni.

- Theil, (1960) Theil, H. (1960). Best linear index numbers of prices and quantities. Econometrica: Journal of the Econometric Society, 28(2):464–480.

- von der Lippe, (2001) von der Lippe, P. M. (2001). Chain indices: A study in price index theory. Metzler-Poeschel.

- Walsh, (1901) Walsh, C. M. (1901). The measurement of general exchange-value, volume 25. Macmillan.

Appendix

1 Proofs of Theorems and Corollaries

1.1 Proof of Theorem 1

Proof.

In compact form, the model in Eq. (10) can be written as

| (A.1) |

where

and

The generalized least square estimator of the vector is given by

| (A.2) |

where, is as defined in Eq. (11).

Some computation prove that,

where is the dimensional -th elementary vector and is a matrix whose -th column is .

Furthermore111111Note that

where .

| (A.3) |

1.2 Proof of Corollary 1

1.3 Proof of Corollary 2

Proof.

When , and . Then, by assuming stationary disturbances, i.e for , the following holds

| (A.7) |

and

Accordingly, the GLS estimate of the deflator turns out to be

Then, by denoting with and the quantity and the value of the -th good at time and by assuming diagonal the matrix , with diagonal entries , some computations yield

| (A.8) |

The reciprocal of Eq. (A.8) yields the GLS estimate of the index. ∎

1.4 Proof of Corollary 4

1.5 Proof of Corollary 5

1.6 Proof of Theorem 2

Proof.

When the values, , and the quantities, , of commodities in a reference basket become available for the -th additional country, the reference equation system for updating the MPL index becomes

After some computations, the above system can be also written as

or, in compact form, as

where

with

Here and are as defined in Eq. (11) and .

Following the same argument of Theorem 1, we obtain that

and

where and are defined as in Theorem 1 and .

Then, upon nothing that

where is the upper off diagonal block of the inverse matrix , partitioned inversion leads to

Then, pre-multiplying by yields the estimator . The reciprocal of the (non-null) elements of this estimator provides the values of the updated multilateral version of the MPL index. ∎

1.7 Proof of Theorem 3

Proof.

When the values, , and the quantities, , of commodities of a reference basket become available at time , the updating of the multi-period version of the MPL index must not change its past values with meaningful computational advantages. In order to get the required updating formula, let us rewrite Eq. (7) as follows

| (A.10) |

where is specified as follows

Here denotes the estimate of , defined as in Eq. (8), that is

where the entries , are the elements of the vector given in Eq. (13). The system in Eq. (A.10) can be also written as

| (A.11) |

The application of the operator to the left hand-side block of equations in Eq. (A.11) yields

| (A.12) |

where with 131313Note that, differently from the proof of Theorem 2, the vector does not enter in the updating estimation process as it is considered given. and is equal to .

It is worth noting that Eq. (A.12) can also be written in vector form as

where

and

with

where is as defined in Eq. (11) and .

The GLS estimator of the vector is given by

where

and

where is a matrix whose -th column is .

Now, upon nothing that

where is the upper off diagonal block of the inverse matrix , partitioned inversion leads to

Then, pre-multiplying by yields the estimator of given in Theorem 3. The reciprocal of this estimator provides the updated value of the multi-period version of the MPL index. ∎

1.8 Proof of the MPL index properties

Proof.

In this Appendix the main properties enjoyed by the MPL index, , as defined in Eq. (16), are proved. To this end, let denote the MPL price index with and vectors of prices and quantities at time .

- P.1

-

P.2

Commensurability: Let and and denote with , and the -th entries of and and respectively.

Then, simple computations prove that the following holds for the th weight, , of the MPL index

where is as defined in (17). This means that and, accordingly

-

P.3

Proportionality: Simple computations prove that when , the weights of the MPL index become

(A.13) Thus

-

P.4

Dimensionality: When and the weights of the MPL index are as in Eq. (A.13). Accordingly

-

P.5

Monotonicity: Let be a vector with entries greater than 1, that is where is the unit vector. Let and note that the entries of are greater than those of , namely . Furthermore, when are the prices of the second period, the weights of the MPL index become where is the -th element of . Accordingly, and the MPL index becomes

Similarly setting , with specified as before, the weights of the MPL index do not change and the index becomes

as the entries of are greater than those of , namely .

It is worth noticing that the MPL index enjoys also the following properties:

-

P.6

Positivity: When , the MPL index becomes

(A.14) -

P.7

Inverse proportionality in the base period: For the proof see Eq. (A.14).

-

P.8

Commodity reversal property: It follows straightforward that the index price is invariant with respect to any permutation :

-

P.9

Quantity reversal test: Simple computations prove that the index price does not change as a consequence of a change in the quantity which affects only the weights .

-

P.10

Base reversibility (symmetric treatment of time): This property is satisfied by the MPL index under a suitable choice of the weights. Setting , or where is a variable or more simply a constant term , leads to weights, , of the MPL index that does not depend on prices

Hence, by denoting with the vector whose -th entry is , simple computations prove that

-

P.11

Transitivity: For a particular choice of and by using the square roots of the quantities, we have proved that the MPL index tallies with the GK index which satisfies all tests for multilateral comparison proposed by Balk, (1996) except for the proportionality one.

-

P.12

Monotonicity: If then the following holds for the weights of the MPL index

Hence

∎

2 Empirical application of MPL: graphics

2.1 MPL index and the cultural supply: a multi-period perspective

2.1.1 Incomplete and complete price tableau

2.2 MPL index and the cultural supply: a multilateral perspective

2.3 MPL index and cultural supply: a simulation

3 Simulations

| Data | GLS-s | GLS-d | OLS | |||

|---|---|---|---|---|---|---|

|

0.0152 | 0.0134 | 0.0165 | |||

|

0.0016 | 0.0005 | 0.0008 | |||

|

0.0083 | 0.0038 | 0.0055 |

| Data | GLS-s | GLS-d | OLS | TPD | |||

|---|---|---|---|---|---|---|---|

|

0.1337 | 0.0940 | 0.1324 | 0.7602 | |||

|

0.0243 | 0.0291 | 0.0227 | 0.0661 | |||

|

0.0772 | 0.0660 | 0.0724 | 0.1471 |