On the Sensitivity of Singular and Ill-Conditioned Linear Systems

Zhonggang Zeng

Department of Mathematics,

Northeastern Illinois University, Chicago, Illinois 60625, USA.

email: zzeng@neiu.edu.

Research is supported in part by NSF under grant DMS-1620337.

Abstract

Solving a singular linear system for an individual vector solution is an

ill-posed problem with a condition number infinity.

From an alternative perspective, however, the general solution of a

singular system is of a bounded sensitivity as a unique element in an affine

Grassmannian.

If a singular linear system is given through empirical data that

are sufficiently accurate with a tight error bound, a properly formulated

general numerical solution uniquely exists in the same affine

Grassmannian, enjoys Lipschitz continuity and approximates the

underlying exact solution with an accuracy in the same order as the

data.

Furthermore, any backward accurate numerical solution vector is an accurate

approximation to one of the solutions of the underlying singular system.

1 Introduction

Solving linear systems in the matrix-vector form

is one of the most fundamental

problems in scientific computing.

In the literature of numerical analysis,

linear systems are always assumed to be nonsingular with few exceptions.

Numerical solutions of singular

systems are almost never mentioned directly in textbooks.

A rare remark in Meyer’s textbook [25, page 218] accurately reflects the

state of knowledge:

“If is singular, … even a stable algorithm can result in a

significant loss of information. …

[T]he small perturbation due to roundoff

makes the possibility that very likely.

The moral is to avoid floating point solutions of singular systems”

(emphasis added).

In applications such as deblurring images and discrete inverse problems, rank-deficient and

highly ill-conditioned linear systems are approached using the

Tikhonov regularization [11, 12, 13, 27].

As Neumaier states [27]:

“Though frequently needed in applications, the adequate handling of

such ill-posed linear problems is hardly ever touched upon in numerical

analysis text books.”

Singular linear systems are unavoidable in scientific computing and often

need to be solved without knowing the exact matrices and vectors, as shown

in case studies in §3.

The obvious difficulty in solving a singular linear system from empirical

data is the condition number infinity so that the error is unbounded when

solving for an individual vector solution.

While this error analysis in itself is impeccable, the solution of a singular

system is more than an individual vector.

The very notion of the numerical solution to a given system

needs clarification when entries of

serve as empirical data for an underlying singular

linear system .

This paper attempts to analyze the accuracy and sensitivity of solving

singular linear systems from a different perspective:

The solution of a singular linear system is either an empty set or an

affine subspace as a unique element in an affine Grassmannian rather than a

vector.

Using this point of view, the condition number becomes bounded.

A properly formulated general numerical solution in a certain affine

Grassmannian

is of a sensitivity proportional to , never

infinity, with respect to either constrained or arbitrary perturbations

where is the Moore-Penrose inverse of .

Such a numerical solution of a perturbed system

within a viable error tolerance

accurately solves the underlying singular system

and the ratio of solution accuracy to the data error is

bounded by a factor of , not

,

assuming the data error is small with an attainable tight bound.

We shall further demonstrate that the sensitivity of a singular

linear system is measured by

rather than infinity from multiple

perspectives, including homogeneous cases, under constrained perturbations

preserving the singularity and consistency, solving for the

general numerical solutions in an affine Grassmannian, and solving for a

single particular solution.

Furthermore, every backward accurate numerical (vector) solution of a singular

consistent linear system accurately approximates a particular exact solution

regardless of the algorithm used.

The “error” largely falls harmlessly in the kernel of .

This result extends what Peters and Wilkinson discovered in [29]

beyond inverse power iterations.

While any numerical (single-vector) solution may be inaccurate to a

linear system that is genuinely nonsingular and highly ill-conditioned,

we shall prove that a stable numerical (affine subspace) solution may exist

and contain an accurate approximation to the exact solution.

For practical computation, efficient and robust algorithms already exist for

general numerical solutions in affine Grassmannians.

Regularization algorithms such as the Tikhonov method and

truncated SVD [9, §5.5.4][10] produce the

accurate vector component and numerical rank-revealing algorithms [2, 7][9, §5.4.6][18, 19, 20, 31]

provide the numerical kernel as the remaining component.

For the continuity of presentation, lemmas and long proofs are listed

in the appendix.

Additional computating results and software demonstration are given in the

supplementary material.

2 Preliminaries

Column vectors are denoted by boldface lower case letters such as ,

, etc with being a zero vector whose dimension can

be derived from the context.

The vector space of -dimensional complex column vectors is denoted by

.

The vector space of matrices with complex entries is denoted

by .

Matrices are denoted by upper case letters such as , , , etc

with and denote a zero matrix and an identity matrix respectively.

The range, kernel, rank and Hermitian transpose of a matrix are

denoted by , , and respectively.

In this paper, we consider general linear systems

in the form of and we say the system is

singular when so that ,

including non-square cases where or .

The system is consistent if .

For any matrix ,

the -th largest singular value of a matrix is denoted by

.

The numerical rank of a matrix within an error tolerance

is defined as

assuming does not equal to any singular value of .

Let be the singular value decomposition of

where and

.

If within , then the

-projection of is defined as

In this case, the numerical kernel of

within is

where denotes the vector space spanned by vectors in

the list.

The entities , and are

undefined if is a singular value of .

The Moore-Penrose inverse of , denoted by ,

is the unique matrix satisfying the Moore-Penrose conditions

, ,

and

.

Using the singular value decomposition as above and assuming

, the identity [9, §5.5.2]

holds and is the mininum Frobenius norm matrix such that

and are orthogonal projections from onto

and from onto respectively.

We shall frequently use as an alternative

notation for the smallest positive singular value of

with rank .

The set of -dimensional subspaces of is

called the Grassmannian [6][17, page 52]

of index of denoted by .

For any , let

be matrices whose columns form

orthonormal bases for , respectively while

such that

.

The Grassmannian is a metric space with the distance

[9, §2.5.3]

The set of -dimensional affine

subspaces of is called the affine Grassmannian [16, §7.1][21, 22]

of index of denoted by

Here, for any vector and subspace

, the

affine subspace

can be written as

with a unique of the minimum norm where denotes the

unitary complement of any subspace .

The metric

(1)

for every

is a distance in .

For every , denote

the set of vector solutions to the system by

For , the set as the solution

of

uniquely exists as either or

an element in the affine Grassmannian .

The dimension of is either if

it is in or if it is empty [3, page 6].

We define so that the deviation of

solutions can be measured if and only if they are of the same dimension.

The condition number of a square matrix

in the context of solving a linear system is

well-known to be with a convention

when is singular

[9, p. 87].

This condition number is based on the attainable error of the solution

as an individual vector.

The infinity convention can be justified

by

when is singular

and by the interpretation as the reciprocal of the distance to the

singularity [14, Theorem 6.5].

For a rectangular matrix , it is natural to generalize the

condition number as

(see, e.g. [14, p. 382]).

We shall make arguments from multiple perspectives that the infinity

convention may be unnecessary even if is square and singular.

It is easy to see that

is discontinuous at any rank deficient matrix and can not be

approximated from empirical data since

can be arbitrarily large when is small.

For any error tolerance with

, however,

the asymptotic bound

follows from [9, Corollary 8.6.2]

when the data matrix is sufficiently accurate so that

.

Assuming an error bound is attainable

and is sufficiently tight so that ,

the condition number of the -projection

of the data matrix ,

not ,

is an approximation to the underlying condition number

.

3 Models of singular linear systems

We shall elaborate some case studies to show that

solving singular linear systems is not only unavoidable in scientific

computing, but also crucial in many applications.

It may even be beneficial for the systems to be singular.

Moreover, singular linear systems are often not known with exact matrices

and right-hand side vectors in practical computation, and need to be solved

from empirical data.

Example 1 (Multiplicity of a singular solution to a nonlinear system)

For a system of nonlinear equations in the form of

where and

is an analytic function for

, a zero of is multiple if the

Jacobian of at is rank-deficient.

At such a multiple there is a vector space called the

dual space that forms the multiplicity structure of the

zero and the dimension of is the multiplicity.

The multiplicity structure can be determined by solving a

sequence of homogeneous linear systems

(2)

where is the Macaulay matrix whose entries are derivatives

of ’s of orders up to evaluated at .

The solution of (2) in a proper

Grassmannian is isomorphic to the desired dual space

when reaches the so-called depth.

See, e.g., [4] for detailed elaborations and the supplemenary

material for a computing demo.

The exact Macaulay matrix is almost never available since

is generally known approximately through a certain

within an error bound.

The model is to solve the singular system (2) for

the solution in a Grassmannian rather than individual vectors from empirical

data matrix .

Example 2 (Sylvester equation)

This is an application arising in control and system theory[1]

in the form of the Sylvester matrix equation

where , and are matrices depending on a

parameter .

The system may inevitably become singular

when the parameter varies continuously and passes through a certain

whose value may only be obtained approximately.

The following illustrative example is slightly modified from [1]

(c.f. supplementary material).

Let

(3)

When varies continuously, the system

becomes singular but still consistent when hits the value

with the general solution

(4)

Suppose we know with an

error bound .

Can we find a numerical solution of the perturbed system at the

parameter value approximating in (4)

of the underlying system at with an accuracy

roughly 0.0001?

Example 3 (Bézout coefficients)

For polynomials , with a greatest common

divisor , there exist polynomials , known

as the Bézout coefficients (see e.g. [26, §1.3][36]),

such that the Bézout identity

(5)

holds.

Solving the linear equation (5) for the Bézout coefficients

appears in many applications such as computing the Smith normal form

in linear control theory [36],

and the systems are often singular for .

Denote as the vector space of polynomials with degrees up to .

For instance, let be polynomials of degrees,

say with degree of , say , the equation

(5) for is

consistent and rank-deficient by 2.

The rank-deficiency is, in fact, a blessing in turning the general solution

into an invertible transformation

(6)

The exact coefficients of polynomial parameters

and may be unknown beyond their empirical data,

say

with coefficientwise error bound .

Can we accurately calculate the general solution for

of the

equation (5) using the imperfect data

and within an error

in the same order of the data?

A computation/software demo for this example is given in the supplementary

material.

The matrix-vector representation of the

equation (5) in the given data is

(7)

with respect to monomial bases, and the condition number

.

The system (7) in the conventional sense is highly

ill-conditioned since .

Applications are abundant involving singular linear systems.

The output regulation problem arises in the

application of neural networks [23]

for finding the matrix pair satisfying the so-called regulator

equations whose solutions are not necessarily unique.

An illustrative example is as follows (c.f. supplementary material):

(8)

where the unknowns and are matrices.

The system is rank deficient by one.

Furthermore, the matrix parameters

are not known exactly but given by estimation.

For a matrix with a defective

eigenvalue and an associated eigenvector ,

a generalized eigenvector satisfies the singular system

for .

The value of and generally can

only be known approximately.

The problem is to solve the underlying system by solving

from

the data ,

and .

More applications include solving the singular homogeneous linear systems

of Ruppert matrices in numerical factorization of polynomials

[8, 37], numerical elimination of polynomial variables

[38], etc.

The generalized Lyapunov equation

with given matrices , and is singular when is

rank-deficient [33].

A singular linear system that models the atmospheric path delay and the water

vapor constant estimation is given in [30].

Linear systems derived from discretizing the Fredholm and Volterra

integral equations can be considered empirical data of singular systems in the

presense of annihilators [12, §2.4 and page 83]

(c.f. an example in supplementary material).

4 Homogeneous systems with empirical data

A problem is well-posed if its solution satisfies existence,

uniqueness and Lipschitz continuity with respect to the data

or, otherwise, it is an ill-posed problem.

For an singular homogeneous linear system

, the problem

Solve for a single-vector solution

in

(9)

is obviously ill-posed as its solutions are not unique.

However, the problem (9) is not precisely the problem to be solved

in standard linear algebra where all the solutions are in question.

There is a unique solution to the problem

Solve for the solution in

the Grassmannian

(10)

where .

The problem may become somewhat confounding when the exact is

unknown but given through empirical data in

as illustrated in Example 1.

What really is at stake is a nontrivial solution in the

Grassmannian but the data system

is almost always nonsingular with when .

The condition number

can be huge as well

if .

The very problem of solving a homogeneous linear system from empirical data

needs clarification.

Problem 1 (Numerical Solution of a Homogeneous Linear System)

Let be an matrix serving as empirical

data for an underlying homogeneous system where

entries of may or may not be known exactly.

Identify the rank of using and find a numerical

solution of in the Grassmannian

in the form of an orthonormal basis

so that

(11)

From Wedin’s perturbation analysis [34], the numerical kernel

within a proper error tolerance

is an approximation to in

(c.f. Lemma 1 in §A in appendix).

For every , we define

as the numerical solution of the homogeneous system

in the Grassmannian within an error tolerance

where .

Numerical methods for computing as

are well-established, including the singular value decomposition and

other numerical rank-revealing methods

(see, e.g. [11, 20]).

The following theorem summarizes the properties of the

numerical solution as a generalization of the exact solution to the

homogeneous system and as a well-posed computing problem that solves the

underlying system in Problem 1.

The essence and underlying substance of Theorem 1 are based on

Wedin [34].

Theorem 1

Let .

The following properties hold for the numerical solution

of a homogeneous system.

(i)

The exact solution is a special case of the

numerical solution:

(ii)

Computing the numerical solution is a well-posed

problem:

If is well-defined within ,

then uniquely exists in the same Grassmannian

as and enjoys Lipschitz continuity with

(12)

for all with sufficiently small satisfying

(iii)

A homogeneous system can be solved from empirical data with an

accuracy in the same order as the data:

For any serving as empirical data of with

,

there exist with

(13)

such that the numerical solution

within any error tolerance

is in the same Grassmannian as the exact solution

and

(14)

Proof.

A straightforward verification from Wedin’s error bound [34] on

singular subspaces (see Lemma 1 in Appendix A) along with

the identity

for where ,

and

.

By Theorem 1, Problem 1 is solvable if

the data are sufficiently accurate and a tight error bound on data

is attainable, as asserted in the following corollary.

Corollary 1

Let the matrices and be as in Problem 1.

Assume the data in are sufficiently accurate

such that .

Further assume a data error bound is known

and is sufficiently tight so that

.

Then Problem 1 is solvable by setting the error tolerance

and finding an orthonormal basis for the numerical

solution within

.

Proof.

A straightforward verification using Theorem 1.

The error tolerance in Theorem 1 is

an operational parameter that needs to be set up for solving

Problem 1.

If we assume the underlying application allows the data error to a certain

extent, say , the data error bound

in Corollary 1 is expected to be below .

The inequality (13) ensures there is a window for

setting the operational error tolerance at or slightly

larger.

Using the notation of Problem 1, it is reasonable to assume

the data error bound on is known or can be

estimated.

The crucial criterion for operational purpose is

to set at or slightly above according

to Theorem 1, part (iii).

The error tolerance should not exceed

whose exact value or estimation

is not needed if the data error bound is sufficiently tight.

See the supplementary material for examples of setting error tolerances.

For a rank- matrix , the sensitivity of solving

for

in the Grassmannian

from a perturbed data matrix is

from (12) and (14), not infinity or .

The convention for the square singular case

and may

overestimate the sensitivity substantially.

Problem 1 may not be solvable if the data error

is large beyond, say ,

or may not be solved accurately if the data error bound is unknown or

the inherent sensitivity is high.

For solving with ,

there are differences between cases of and .

The solution is of a positive dimension when regardless of

perturbations and, if , the condition

is continuous with respect to small perturbations.

When and is nontrivial, however, the

dimension of degrades to zero for almost all

perturbations and the condition is

discontinuous.

The assertions of Theorem 1 remain the same either

or .

5 Sensitivity of a consistent singular system

Solving a singular system for an individual vector solution is known to have an

unbounded sensitivity under arbitrary perturbations.

From a different perspective, the infinity condition number is not the

sensitivity of the singular system if the singularity is not maintained.

There is an intrinsic stability in solving

when the rank and consistency are preserved.

This point of view is originated in [15] by Kahan who suggests the

perceived hypersensitivity of multiple roots may be a “misconception”

without maintaining the multiplicity.

A consistent linear system with

has a unique solution

in the affine Grassmannian

where is any particular solution.

The sensitivity of the linear system can be based on

the deviation of the solution in with

respect to perturbations of .

From (1), the difference between solutions of two consistent

systems of the same rank can be measured by the metric (1), namely

(15)

Notice that the component

in (15) but the other

component

can be large or small.

One way to avoid an imbalance is to put a weight factor on the

component .

We choose not to use weights for the sake of simplicity of

elaborations and for the reason that the weight can be used

to scale the linear system instead so that we can solve

equivalently.

For convenience, we adopt a specific norm

(16)

in the product space .

The theories in this paper can be adapted to other norms.

With these notations and metrics, the solution of a

singular consistent linear system uniquely

exists in the affine Grassmannian and the sensitivity is

proportional to rather than infinity when the

rank and consistency are preserved, as established in the following

theorem.

Theorem 2

The solution of a consistent linear system is Lipschitz

continuous when the rank and consistency are preserved.

Let and .

Assume the perturbation is constrained

such that:

and

where

and .

Then

(17)

where whenever

.

Proof sketch.

The kernel component of the distance in (17) is bounded by

Wedin’s error estimate [34] (see Lemma 1 in

Appendix A).

Let be a matrix whose coluns form an orthonormal basis for

.

Then the mininum norm solution is the unique least squares

solution of the system

and the standard error bound [24, Theorem 1.4.6] applies.

Detailed proof is in Appendix B.

As a result of (17), the intrinsic sensitivity of solving

a singular system for

the general solution is a constant multiple of

when the rank and consistency are preserved.

As a by-product of establishing Theorem 2, the following corollary

improves the standard normwise

error bound [9, Theorem 5.6.1]

on the minimum norm solution of a full rank underdetermined linear system

by reducing a factor from 2 to .

Corollary 2

Let with and

.

If and are minimum norm solutions of the

underdetermined linear systems and

respectively with

,

then

(18)

Proof.

The inequality (18) follows from (54) in

Appendix B.

Remark 1

The subset of all rank- matrices is a complex analytic

manifold in the topological space [5]

with the topology derived from the Frobenius norm.

Similarly the subset

is a complex analytic manifold in .

Although the problem of solving a singular linear system in general is

ill-posed, Theorem 2 implies the problem of solving

for in

is well-posed on the manifold .

6 The general numerical solution

When a rank-deficient linear system is

given through empirical data , the perturbed matrix

is almost always of full rank and highly ill-conditioned.

Furthermore, the conventional single-vector solution of the data system

is in while the general solution

of the underlying system is in completely different space .

What the problem precisely is and what the numerical solution really means

need to be clarified.

Problem 2 (Numerical Solution of a Linear System)

For given and

serving as empirical data for an underlying linear system

to be solved, find a numerical solution of

that can be identified as the exact solution

of

such that both the backward error and the forward error

(19)

(20)

are in the same order of the data accuracy.

The accuracy requirement (20) stipulates that both

and

are in the same affine Grassmannian or both empty.

It is natural to choose within a proper

and as the orthogonal

projection of onto .

The solution is acceptable as

the numerical

solution of if its backward error

is below the error tolerance or the empty set.

Definition 1 (General Numerical Solution)

Let , and

be an error tolerance within which is well defined.

With respect to a norm on

, the general numerical solution

of the linear system within is

defined as

where is the -projection of

and is

the orthogonal projection of onto the range

of .

The solution is undefined

if equals to a singular value of or

.

We can now establish the following theorem on the general numerical solution.

Theorem 3

At any ,

the following properties of the general numerical solution hold

with respect to the norm (16).

(i)

An exact general solution is a special case of

general numerical solution: The identity

holds

for all if ,

or otherwise.

(ii)

Computing the general numerical solution is a well-posed

problem: Assume is well-defined within a certain

.

There is a depending on and

such that, for every with a sufficiently small norm,

there exists a unique

satisfying the Lipschitz continuity

(21)

(iii)

A singular linear system can be solved from

empirical data with an accuracy in the same order as the data: (a)

Assume and let .

For any empirical data pair satisfying

where

and for any error tolerance satisfying

(22)

there exists a unique general numerical solution

with a backward error bound

and a forward error bound

(23)

(b) Assume .

For any ,

there is a constant such that

at any empirical data

pair satisfying

.

Proof sketch.

The assertion (i) and the unique existence in the assertion (ii) directly

follow from Definition 1.

The Lipschitz continuity (21) is a variation of

the error estimate for the truncated SVD solution by

Hansen [10, inequality (26a)] as an extension of Wedin error

analysis [35].

The bound on the minimum norm solution component of the distance in

the inequality (23) follows from Hansen

[10, inequality (27a)] and the

the bound on the numerical kernel is established by Wedin [34].

Detailed proof is given in Appendix B.

For Problem 2, assume the underlying linear system

in Problem 2 is known to be consistent

in applications such as Example 3, the

solvability the system from empirical data

is given in the following corollary of Theorem 3.

Corollary 3

Let and be as in

Problem 2 where the underlying linear system

is consistent.

Assume the data matrix is sufficiently accurate

with .

Further assume an error bound

is attainable

and is sufficiently tight so that

.

Then Problem 2 is solvable by calculating

with the error tolerance

where is the orthogonal projection

of onto .

Furthermore

We reiterate that the sensitivity of solving

from empirical data is measured by

not infinity or when the underlying matrix is

singular where .

Problem 2 may still be difficult if data are inaccurate, if the

intrinsic condition is large, or if

the window for setting the error tolerance is too narrow.

The general numerical solution can be computed using existing rank-revealing

tools such as [18, 20]

and UTV/ULV decomposition[9, §5.4.6] in the following template:

set the error tolerance at or slightly above the

error bound

ifthen

–

calculate whose columns form an

orthonormal basis for the numerical kernel

–

solve for a particular solution

by any backward accurate method such as

or Tikhonov

regularization

–

output .

else

–

calculate a decomposition

with

, and

–

solve for and

obtain the truncated SVD solution .

–

output:

end if

As we shall establish in §7,

the particular solution component of in

the above template can be computed by any backard accurate numerical algorithm

including Tikhonov regularization and truncated SVD.

Computation of general numerical solution is implemented in the

Matlab package NAClab [40] as the functionality

LinearSolve (c.f. [39] and the supplementary material).

The general guideline for the error tolerance is to set it at or slightly

larger than a known data error bound if the

application allows such an adjustment.

We conclude this section with the following example.

Example 4

Revisiting the linear system in Example 3, the data error bound can

be estimated as

where is the underlying matrix since the

entrywise error bound is .

The error tolerance can be set at or slightly larger than the

error bound, say .

The numerical solution of the system (5) within

in the affine Grassmannian is a representation of

(c.f. supplementary material).

The general numerical solution

is of a healthy sensitivity

,

not the infinite or the large

.

The three components of

form an invertible polynomial transformation matrix as shown in (6)

with the numerical inverse

Remark 2

An system with is inconsistent

for almost all and its least squares solution is usually

studied in the literature.

In fact, the least squares solution can be considered whenever

even if .

There are substantial differences between the conventional solution

and the least squares solution.

In Theorem 3 and throughout this paper, our elaboration is

restricted to the conventional solution so that

for inconsistent systems and the nonempty

set of least squares solutions is beyond the scope.

The sensitivity of the least squares solution is well-known

to be (see, e.g. [14, §20.1]) in contrast to

for the (conventional) solution in Theorem 3.

7 Particular solution of a singular linear system

There are many applications where only a particular solution is needed among

the infinitely many solutions of a singular linear system

and it makes little difference which particular

solution is obtained.

For such applications, the problem of finding a

numerical particular solution can be stated as follows.

Problem 3 (Numerical Particular Solution)

Assume a linear system is consistent

where the entries of and may be known through empirical

data of limited accuracy.

Find a numerical particular solution

that approximates an exact solution

with the error

at an acceptable level.

There are regularization approaches such as the Tikhonov method

[9, §6.1.5][11, 27]

that can produce

approximate particular solutions with high backward accuracy.

For any backward accurate numerical solution of the system

in the sense that there is a pair

such that

and is at an acceptable level,

we shall call a numerical particular solution of

.

The following theorem asserts that every numerical particular solution

approximates one of the exact solutions.

Theorem 4

Let with and .

Assume is a backward accurate numerical solution of

in the sense that

is an exact solution of

with .

Then approximates an exact solution

with an error bound

(24)

assuming where ,

, or

(25)

if .

Proof sketch. Let and .

Write where

and

.

Choose a particular solution

from .

Since

approximates , ,

and

approximates , hence is an approximation to the

particular solution of so the theorem holds.

Detailed proofs of (24) and (25) are in

Appendix B.

For the case in Theorem 4, the objective is

to solve the homogeneous system .

The inequality (25) includes three cases:

Case (i): and .

The inequality (25) is trivial and perhaps meaningless

since .

Case (ii): and .

Then we can normalize to be a unit vector so that

(25) becomes

(26)

Case (iii): .

The case is relevant in practical computation by setting the right-hand side

as a nonzero random vector of a moderate norm and obtaining a

numerical particular solution as an exact solution of

with a small ,

leading to the inverse power iteration.

The norm is almost always large due to the condition

number .

As it turns out pleasantly, the large is exactly

what is needed as (25) becomes

(27)

The larger the norm achieves, the more accurate

is to a particular nontrivial solution of

the homogeneous system .

Once again, the sensitivity of solving a singular linear system

is

,

not infinity in the sense of finding a numerical particular solution.

Particular solutions of can vary arbitrarily but their

deviations can only stretch in .

As the following corollary states, the high sensitivity is near

a direction in and such a sensitivity may be harmless after all.

Corollary 4

Let with and .

Assume and are both backward accurate numerical

particular solutions of in the sense that

and

with sufficiently small

and .

Then there is an such that

(28)

Proof.

Apply the inequality (25) on and

that satisfies

.

Theorem 4 extends the accuracy result for the inverse iteration in

spite of the large condition number.

In [29], Peters and Wilkinson described what they called

“exaggerated fears” in the early days of computer age when the inverse

iteration

(29)

at an approximation to an eigenvalue of was proposed

for calculating an eigenvector as a nontrivial

solution to the homogeneous system :

Although [inverse iteration is] basically a simple concept its numerical

properties have not been widely understood.

If really is very close to an eigenvalue, the matrix

is almost singular and hence a typical step in the iteration involves the

solution of a very ill-conditioned set of equations. …

The period when inverse iteration was first considered was notable for

exaggerated fears concerning the instability of direct methods for solving

linear systems and ill-conditioned systems were a source of particular

anxiety.

[Few] numerical analysts discuss inverse iteration with any

confidence.

It is counterintuitive, and pleasantly surprising nonetheless,

that ill-condition is not harmful in computing the eigenvector.

As pointed out in [29] and by Parlett

[28, §4.3] that errors mainly lie in and are not

really errors at all:

[R]oundoff errors can give rise to complely erroneous “solutions” to very

ill-conditioned systems of equations. …

Indeed some textbooks have cautioned users not take [] too close to any

eigenvalue. …

Fortunately these fears are groundless and furnish a nice example of confusing

ends with means. …

The error ,

which may be almost as large as the exact solution of

[], is almost entirely in the direction of [the

eigenvector].

…

The result is alarming if we had hoped for an accurate solution of

[(29)] (the means) but is a delight in the search for

[the eigenvector] (the end).

Theorem 4 concludes, in fact, that the fears of solving a highly

ill-conditioned linear system may also be exaggerated for non-homogeneous

systems as well when the underlying system

is consistent and singular, as long as the numerical solution is

backward accurate and the intrinsic sensitivity measure

is moderate.

The variation between any two numerical particular solutions can be large

but the difference falls harmlessly in the kernel of .

In other words, the “error” is actually a part of the solution.

Example 5

The system in (7) is a

representation of the underlying system with

from the entrywise error bound .

Rounded to five digits after the decimal point,

two numerical particular solutions and

by turncated SVD and

Matlab “”, respectively, are

with both residuals

and

roughly within the data error bound.

The two numerical particular solutions are far apart with

as predicted by the

large condition number .

However, the underlying system is

consistent and singular with a healthy sensitivity

.

Both and are accurate approximations to

different exact solutions with estimate error bounds and

respectively, and actual relative errors are

and in the same level

of the data error.

8 Bona fide ill-conditioned linear systems

A linear system is truely ill-conditioned when

is large regardless of its rank.

When is of full column rank, and the condition

number is huge, the solution uniquely exists but in general

can not be computed accurately from perturbed data using whatever algorithm.

The system is de facto rank-deficient in a practical sense.

Even in such cases, a stable general numerical solution may still be

attainable in an affine Grassmannian from empirical data, and the underlying

solution can be accurately approximated by a vector in the affine subspace as

the general numerical solution.

Theorem 5

Assume , and

.

Let be any integer with .

For any serving as

empirical data of with

(30)

there is an

with such that

(31)

Proof sketch.

Since is a backward accurate solution of the linear system

, Theorem 4

applies from a reversed perspective.

The detailed proof is in Appendix B.

In the following example, the underlying system is

ill-conditioned but truly nonsingular.

All known numerical algorithms including regularization methods

produce solutions that are inaccuate as single vectors but highly accurate

as the vector component of a general numerical solution that

is perfectly conditioned and contains accurate approximations to

the underlying exact solution.

Example 6

Consider the polynomial division problem in the form of the

equation

for the quotient and the constant remainder .

There is a unique solution which consists of and

.

The corresponding linear system is of the form where

with the exact solution

that is attainable in symbolic computation using the exact data in

rational number format.

In Matlab single precision arithmetic, the system is represented as

perturbed data

where and

.

The singular values

indicate that it is practically impossible to calculate the single-vector

solution with any meaningful accuracy using such data.

Table 1 shows three sample numerical solutions:

by a straightforward application of the Matlab command

Ab, a Tikhonov regularization solution

at, say

and the truncated SVD solution

with an error tolerance

that is roughly

where is

the unit roundoff.

As expected from the condition number ,

none of the solutions can be considered accurate as a single vector.

On the other hand, the general numerical solution

is almost perfectly

conditioned at

.

The three solutions , and that are inaccurate

as individual vectors are all accurate as the component

of the general numerical solution

with where

(32)

All for are nearly identical in the

affine Grassmannian and each contains a particular vector

that is an accurate approximation to the exact

solution as shown in the bottom part of Table 1.

The errors are all within

the bound predicted by (31).

Table 1: For in Example 6,

numerical solutions , and

by Matlab “”, Tikhonov regularization and truncated SVD

respectively in comparison with the exact solution ,

as well as the accuracies of , and as

a component of the general numerical solution.

The linear system in Example 6 is

nonsingular in theory but practically underdetermined in numerical computation.

Suppose an additional piece of information becomes

available, say the remainder .

One can impose such a constraint on the general numerical solution

at the trailing component as

, obtaining

corresponding to a numerical solution with a relative error

in the same order of the data.

Appendix A Lemmas

Lemma 1

Let with .

Assume .

(i)

(Wedin)

If ,

then

(33)

for any .

(ii)

If and

, then

(34)

Proof.

Assertion (i) is established by Wedin [34]

(also see [32, Theorem 4.4] and [10, Theorem 3.3]).

To prove (ii), let the singular value decompositions of and

be

respectively where .

Then

and thus

Lemma 2

Let be a subspace of and be a matrix whose columns

form an orthonormal basis for .

For every subspace of of the same dimension as

with , there is a matrix whose columns form

a basis for such that

Proof.

Let be any matrix whose columns form an

orthonormal basis for and be a unitary matrix.

Then, for any unit vector ,

leading to

,

implying is invertible so that columns of

form a basis for , and

that is

less than or equals to .

Lemma 3

Let with .

(i)

For every ,

let be a matrix whose columns form an

orthonormal basis for .

Then

(40)

where if or otherwise.

(ii)

Assume columns of span .

For any , let and

be the

least squares solution of the linear system

(41)

Then if or

if where

is the orthogonal projection of onto .

Furthermore,

(42)

for any with

and .

Proof. For the case of , we can write in its

singular value expansion

and where

and are left and right singular vectors

respectively with a unitary matrix .

Write .

Then

whose extrema subject to

are

and

,

leading to ((i)) and (40) in the assertion (i).

The case is similar.

To prove (ii), write the singular value decomposition

where

and

.

Then is the solution of the normal equation

.

Namely, we have an orthogonal decomposition

(44)

implying and thus

.

Since , hence

.

Namely is a particular solutions of the

system .

Also,

Finally, if , then so

in (44), implying .

Consequently from (42).

The following lemma is a variation of

Theorem 5.1 in [35] by Wedin and its extension in

Theorem 3.4 in [10] by Hansen.

Lemma 4 (Wedin, Hansen)

Let and .

Assume, for a , we have

and .

There is a constant

(45)

such that, for any and

with

(46)

the following inequality holds:

(47)

As a special case,

further assume and .

Then

(48)

Proof.

The assumption implies

and thus

following (46)

so that as well.

Then it is straightforward to verify (47) from

the inequality (26a) in [10] using

The inequality (48) follows from

[10, inequality (27a)]

and .

Lemma 5

At any and

within which

is well-defined, there is a such that

is well-defined with the same dimension

as if .

Proof.

Write and .

Since is well-defined, we have

.

Thus

ensures .

Let and

.

Then

where and .

If is empty, then

and thus

when is sufficiently small so that

as well.

When and

is sufficiently small, we also have

and

so that

has the identical dimension as .

Appendix B Proofs of theorems and corollaries

Proof of Theorem 2. (p. 2)

Let whose columns form an orthonormal basis for

.

By Lemma 2, there is an

whose columns form a basis for such that

.

For , denote

and .

Then and

by Lemma 3 part (ii).

By from Lemma 1

part (ii), [24, Theorem 1.4.6, page 30] and Lemma 3 part (i),

so ,

and thus is of the same

dimension as .

Since ,

the backward error of

is bounded above by

from (B).

Thus (23) follows from (33) in Lemma 1 and

(48) in Lemma 4,

leading to the assertion (iii).

We now prove the assertion (b) of part (iii).

If is empty, then

whenever .

By Lemma 5, there is a such that

for every

with

.

Thus

with both backward and forward errors as zero.

Proof of Theorem 4. (p. 4)

Let

be the singular value

decomposition where is with .

Then is a solution to

implies

and

where

and .

Then with

for any between

and .

By Lemma 4 with , we have

Let columns of form an orthonormal basis for .

Since ,

(56)

by Lemma 1 which, combined with , implies

and thus

Let .

Then is a particular solution to and

.

We have

leading to (24).

For the case , the bound (25) follows from

(56)

Proof of Theorem 5. (p. 5)

Let

and

be singular value decompositions of and respectively

where .

Denote ,

,

, ,

and

.

Then, with ,

leading to

Let with

Then

while, similar to the proof of Theorem 4 from (30),

[1]K. E. Avrachenkov and J. B. Lasserre, Analytic perturbation of

Sylvester matrix equations, IEEE Trans. on Automatic Control, 47 (2002),

pp. 1116–1119.

[2]J. Barlow, H. Erbay, and I. Slapnicar, An alternative algorithm

for the refinement of ULV decompositions, SIAM J. Matrix Anal. Appl., 27

(2005), pp. 198–211.

[3]M. Coornaert, Topological Dimension and Dynamical Systems,

Springer, Switzerland, 2015.

[4]B. Dayton, T.-Y. Li, and Z. Zeng, Multiple zeros of nonlinear

systems, Mathematics of Computation, 80 (2011), pp. 2143–2168.

[5]J. W. Demmel and A. Edelman, The dimension of matrices (matrix

pencils) with given Jordan (Kronecker) canonical forms, Linear Alg. and

its Appl., 230 (1995), pp. 61–87.

[6]A. Edelman, T. A. Arias, and S. T. Smith, The geometry of

algorithms with orthogonality constraints, SIAM J. Matrix Anal. Appl., 20

(1998), pp. 303–353.

[7]R. D. Fierro, P. C. Hansen, and P. S. K. Hansen, UTV Tools:

Matlab templates for rank-revealing UTV decompositions, Numerical

Algorithms, 20 (1999), pp. 165–194.

[8]S. Gao, Factoring multivariate polynomials via partial

differential equations, Math. Comp., 72 (2003), pp. 801–822.

[9]G. H. Golub and C. F. Van Loan, Matrix Computations, The John

Hopkins University Press, Baltimore and London, 4th ed., 2013.

[10]P. C. Hansen, The truncated SVD as a method for

regularization, BIT, 27 (1987), pp. 534–553.

[11]P. C. Hansen, Rank-Deficient and Discrete Ill-Posed Problems,

SIAM, Philadelphia, 1997.

[12]P. C. Hansen, Discrete Inverse Problems. Insight and Algrithms,

SIAM, Philadelphia, 2010.

[13]P. C. Hansen, J. G. Nagy, and D. P. O’Leary, Deblurring Images,

Matrices, Spectra, and Filtering, SIAM, Philadelphia, 2006.

[14]N. J. Higham, Accuracy and Stability of Numerical Algorithms,

SIAM, 2nd ed., 2002.

[15]W. Kahan, Conserving confluence curbs ill-condition.

Technical Report 6, Computer Science, University of California,

Berkeley, 1972.

[16]D. A. Klain and G.-C. Rota, Introduction to Geometric Probability,

Cambridge University Press, Cambridge, 1997.

[17]V. Lakshmibai and J. Brown, The Grassmannian Variety, Springer,

New York, 2015.

[18]T.-L. Lee, T.-Y. Li, and Z. Zeng, A rank-revealing method with

updating, downdating and applications, Part II, SIAM J. Matrix Anal.

Appl., 31 (2009), pp. 503–525.

[19]T.-L. Lee, T.-Y. Li, and Z. Zeng, RankRev — A Matlab package

for computing numerical ranks, Numerical Algorithms, 77 (2018),

pp. 559–576.

[20]T.-Y. Li and Z. Zeng, A rank-revealing method with updating,

downdating and applications, SIAM J. Matrix Anal. Appl., 26 (2005),

pp. 918–946.

[21]L.-H. Lim, K. S.-W. Wong, and K. Ye, Numerical algorithms on the

affine Grassmannian, SIAM J. Matrix Anal. Appl., 40 (2019) pp. 371-393,

DOI 10.1137/18M1169321.

[22]L.-H. Lim, K. S.-W. Wong, and K. Ye, The Grassmannian of affine

subspaces.

arXiv:1807.10883.

[23]T. Liu and J. Huang, A discrete-time recurrent neural network

for solving rank-deficient matrix equations with an application to output

regulation of linear systems, IEEE Trans. on Neural Networks and Learning

systems, 29 (2018), pp. 2271–2277.

[24]Åke Björck, Numerical Methods for Least Squares

Problems, SIAM, Philadelphia, 1996.

[25]C. D. Meyer, Matrix Analysis and Applied Linear Algebra, SIAM,

Philadelphia, 2000.

[26]T. Mora, Solving Polynomial Equation Systems I: The

Kronecker-Duval Philosophy, Cambridge Univ. Press, London, 2003.

[27]A. Neumaier, Solving ill-conditioned and singular linear systems:

A tutorial on regularization, SIAM Review, 40 (1998), pp. 636–666.

[28]B. N. Parlett, The Symmetric Eigenvalue Problem, Prentice-Hall,

Englewood Cliffs, N.J., 1980.

[29]G. Peters and J. H. Wilkinson, Inverse iteration, ill-conditioned

equations and Newton’s method, SIAM Review, 21 (1979), pp. 339–360.

[30]A. Saqellari-Likoka and V. Karathanassi, An approach for

solving rank-deficient systems that enable atmospheric path delay and water

vapor content estimation, IEEE Trans. Geoscience and Remote Sensing, 46

(2008), pp. 3187–3195.

[31]G. W. Stewart, UTV decompositions, in Numerical Analysis,

1993, D. F. Griffith and G. Watson, eds., Pitman Research Notes in

Mathematical Sciences, New York, 1994, 1994.

[32]G. W. Stewart and J. Sun, Matrix Perturbation Theory, Academic

Press, Inc, Boston, San Diego, New York, London, Sydney, Tokyo, Toronto,

1990.

[33]T. Stykel, Numerical solution and perturbation theory for

generalized Lyapunov equations, Linear Alg. and Its Appl., 349 (2002),

pp. 155–185.

[34]P.-Å. Wedin, Perturbation bounds in connection with singular

value decomposition, BIT, 12 (1972), pp. 99–111.

[35]P.-Å. Wedin, Perturbation theory for pseudo-inverses, BIT,

13 (1973), pp. 217–232.

[36]J. Wilkening and J. Yu, A local construction of the Smith

normal form of a matrix polynomial, J. Symbolic Computation, 46 (2011),

pp. 1–12.

[37]W. Wu and Z. Zeng, The numerical factorization of polynomials,

J. Foundation of Computational Mathematics, 17 (2017), pp. 259–286.

[38]Z. Zeng, A polynomial elimination method for numerical

computation, Theoretical Computer Science, 409 (2008), pp. 318–331.

[39]Z. Zeng, Intuitive interface for solving linear and nonlinear

system of equations, in Mathematical Software — ICMS 2018, J. H.

Davenport, M. Kauers, G. Labahn, and J. Urban, eds., LNCS 10931, Springer

International AG, 2018, pp. 495–506.

[40]Z. Zeng and T.-Y. Li, NAClab: A Matlab toolbox for numerical

algebraic computation, ACM Communications in Computer Algebra, 47 (2013),

pp. 170–173.

Online Supplement to

“On the Sensitivity of Singular and Ill-Conditioned

Linear Systems”

Zhonggang Zeng111Department of Mathematics,

Northeastern Illinois University, Chicago, Illinois 60625, USA.

email: zzeng@neiu.edu.

Research is supported in part by NSF under grant DMS-1620337.a

Abstract. This online supplement provides a software demo of the

package NAClab and additional computing examples for calculating

numerical solutions of singular and ill-conditioned linear systems.

In this online supplementary material, we briefly introduce the software

package NAClab in the context of solving singular linear systems

for the general numerical solution elaborated in the paper

On the sensitivity of singular and ill-conditioned linear systems.

All the example numbers point to the examples in the paper and all the

citation numbers point to the references of the paper.

1. NAClab functionality LinearSolve

NAClab222http://homepages.neiu.edu/zzeng/naclab.html

is a software package of Matlab functions for

numerical algebraic computation [40].

We implemented the computation of general numerical solution

as a functionality LinearSolve [39]

in a simple call with input , and :

>> [x0, N, lcnd, res] = LinearSolve(A, b, theta)

The output x0, N, lcnd and res carries

, spanned by the orthonormal columns

of , the sensitivity estimate

and the residual respectively.

The functionality LinearSolve follows from the high-rank case of

the template in §6.

Furthermore, LinearSolve provide a mechanism to solve a linear system

in the form of

where is a linear transformation and

are vector spaces of

column vectors, matrices, or polynomials in a call syntax

where L is a Matlab (anonymous) function for evaluating

the linear transformation along with domain and

parameter in cell arrays representing the domain

and parameters of .

Consider a system of polynomial equations that is

known through empirical data in the perturbed system

with

and the coefficientwise error bound .

A multiple zero

is computed using the NAClab polynomial system solver psolve and

the depth-deflation method [4] with an error bound

As briefly elaborated in Example 1 and in [4],

the multiplicity structure can be computed via solving a sequence of

homogeneous linear systems for from Macaulay matrices serving

as empirical data.

The NAClab functionality MacaulayMatrix is built for generating

the Macaulay matrices.

To construct, say , use the following statements:

>> f = {’x^3+y-0.7698’,’x+y^3-0.7698’}; % cell array of polynomials in character strings >> var = {’x’,’y’}; % cell array of variable names in character stings >> z = [.57735,.57735]; % approximate zero >> M = MacaulayMatrix(z, f, var, 2); % generate the Macaulay matrix >> single(full(M)) % display the matrix in single precision ans = 0 1.0000000 0.9999990 0 0 1.7320499 0 0.9999990 1.0000000 1.7320499 0 0 0 0 0 1.0000000 0.9999990 0 0 0 0 0.9999990 1.0000000 0 0 0 0 0 1.0000000 0.9999990 0 0 0 0 0.9999990 1.0000000

It is a straightforward to verify that the entrywise error on

is bounded by on 8 entries.

As a result, we have an error bound for the error tolerance

Set the error tolerance slightly larger at

Then a one-line call of LinearSolve produces the matrix whose

columns form an orthonoral basis for the numerical solution

in the Grassmannian

.

>> [z,N,lcnd,res] = LinearSolve(M,zeros(6,1),2e-4); % solve M*z = 0 within 2e-4 >> single(N) % display solution basis in single precision ans = 1.0000000 -0.0000000 0.0000000 0 -0.7828174 0.2320854 0 0.5924006 0.5618970 0 0.1099370 -0.4584060 0 -0.1099372 0.4584060 0 0.1099374 -0.4584059

The multiplicity of is thus 3, with the dual space

accurately represented by the basis

so that those differential operators vanish on the entire ideal generated

by the polynomial system at the zero point .

The linear equation can be written as

where is a linear transformation

with the domain is and parameters

, and in (3),

The linear system can be solved by constructing the representation matrix and

vectors for and and solving the resulting matrix-vector

equation.

LinearSolve in NAClab provides an intuitive WYSIWYG approach

for solving the equation directly.

The matrix-vector representation is generated internally.

At the hypothetical with an error bound 0.0001

of a system, it clearly safe to say the 2-norm data error bound

is that can be used as the error

tolerance for the general numerical solution.

>> L = @(X,t) [1 -1; 1 -1]*X+X*[-5/3+t 1; -1 -1/3+2*t]; % the linear transformation L >> C = [1 0; 2 -1]; % the right-hand side >> domain = {ones(2,2)}; % domain of 2x2 matrices >> parameter = {0.6666}; % parameter t = 0.6666 >> [x0, N, lcnd, res] = LinearSolve({L,domain,parameter}, C, 1e-3);% solve L(X)=C within 1e-3 x0 = [2x2 double] N = {1x1 cell} {1x1 cell} lcnd = 1.573435327501125 res = 2.499756923490804e-05

The underlying singular linear system is quite well conditioned with a

sensitivity measure roughly 1.6 along with a residual , implying the general numerical solution carried in x0 and N

are as accurate as the data.

>> x0{1} % display the truncated SVD solution ans = 0.249983334213952 -0.250004166457633 -0.750004165972904 -0.249974998284764 >> N{1}{1} % display the 1st kernel component ans = -0.662148424976858 0.483868243696442 -0.483822831115126 0.305526519527407 >> N{2}{1} % display the 2nd kernel component ans = 0.558171384891092 0.126097939805073 -0.126073928483796 0.810339052016092

The result is an accurate approximation to the exact solution (4).

The linear system (8) can be considered as the equation

where is the linear transformation

along with parameters

In preparation for calling LinearSolve, define the linear transformation,

its domain and the parameter array:

>> L = @(X,U,A,B,C,D) {X*A-B*X-C*U, D*X}; % the linear transformation function >> A = [1 1; 0 1]; B = [0 1 0; 0 0 1; 2 -1 0]; C = [0; 0; 1]; D = [1 0 -1]; % parameters A,B,C,D >> E = [2 1; -1 1; 0 0]; F = [-1 0]; % right side E and F >> domain = {ones(3,2), ones(1,2)}; % domain of 3x2 and 1x2 matrices >> parameter = {A,B,C,D}; % parameter cell array

The data are exact but floating point arithmetic will introduce entrywise

error arround the unit roundoff so that

we can set the error tolerance slightly larger, say .

A simple call to find the general numerical solution within the error

tolerance:

>> [Z, N, lcnd, res] = LinearSolve({L,domain,parameter}, {E, -F}, 1e-10) % solve L(X,U) = (E,-F) Z = [3x2 double] [1x2 double] N = {1x2 cell} lcnd = 11.987437447750866 res = 1.332267629550188e-15

The sensitivity measure approximately 11.99 along with the residual

indicate that the numerical solution is accurate.

>> Z{1} % display X component of the

truncated SVD solution ans = 1.999999999999999 -0.333333333333333 0 0.666666666666666 0.999999999999999 -0.333333333333333 >> Z{2} % display U component of the

truncated SVD solution ans = -2.999999999999999 1.999999999999998 >> N{1}{1} % display the X component of the kernel basis| ans = 0 -0.577350269189626 0 -0.577350269189626 0 -0.577350269189626 >> N{1}{2} % display the U component of the kernel basis| ans = 0 0

Namely, the general numerical solution is an accurate approximation to

The package NAClab provides a library of polynomial operation

functionalities, such

as pplus(...) for adding polynomials and ptimes(...) for

multiplying polynomials, so that the linear transformation can be defined

as a Matlab (anonymous) function:

>> L = @(u1,u2,u3,f1,f2,f3) ... % linear transformation (u1,u2,u3) -> u1*f1 + u2*f2 + u3*f3 pplus(ptimes(u1,f1),ptimes(u2,f2),ptimes(u3,f3));

To set the error tolerance, consider the entrywise error bound

on 55 nonzero entries and

Thus the error tolerance can be set slightly larger at, say .

We can then define the domain and parameter cell arrays and execute

LinearSolve to calculate the Bézout coefficients:

The sensitivity is healthy at 20.3 with a residual so

that the error on the computed general numerical solution is at the same order

of the data error.

The output z0 carries the numerical truncated SVD solution

as shown above.

The components and

of the general numerical solution are in the output N consists of

an orthonormal basis of the numerical kernel of the linear transformation

such as the result shown in Example 4.

Notice that the output in z0 and N carries polynomial in

WYSIWYG style as character strings.

There is no need for a reverse representation and interpretation of

a solution in column vectors.

Computation of the numerical inverse of the polynomial transformation

matrix shown at the end of Example 4 is out the scope of this

paper.

6. An application in solving an integral equation with

an annihilator

Consider a Volterra integral equation of the first kind in the form of

(57)

for finding on the interval from the given kernel function

and the right-hand side function defined on the same interval.

The equation is singular if there exists an annihilator

such that for

.

As described in [12, pp. 82-83], the kernel333There is apparently a typo in [12, p. 83] about the kernel

(58).

(58)

corresponds to an annihilator , the delta function at .

For integer , stepsize and nodes

, ,

the equation (57) can be discretized by the linear spline

approximation

and represented by a linear system where the variable

in , the right-hand side

vector and the coefficient

matrix with

As an experiment with the kernel (58) where , the

right-hand side function

of the equation (57) corresponds to a known general solution

where is an arbitrary constant.

By any standard numerical integration method such as the composite Simpson’s

rule, the matrix and the right-hand side vector can be

generated easily.

Notice that the system is underdetermined with the size

in addition to being empirical data of a singular equation

(57).

We choose not to add an extra equation to square the system for the

consideration of the inherent singularity in the underlying problem.

For , a simple call of LinearSolve produces the

truncated SVD solution z, the matrix K whose columns form an

orthonormal basis for , the sensitivity measure lcnd

defined as , and the

residual res:

>> [z,K,lcnd,res] = LinearSolve(A, b, 1e-6); % solve A*z = b >> lcnd % the sensitivity lcnd = 2.469428269074639e+04 >> res % the residual res = 8.371530784514738e-10

The numerical kernel is of dimension three.

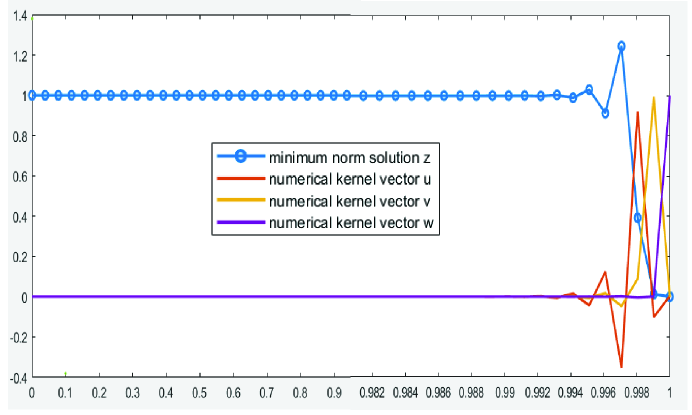

Figure 1 shows the plot of the truncated SVD solution

and the numerical kernel vectors , and .

trunc. SVD

basis for

solution

0

0

1.0000025

0.0000000

-0.0000000

-0.0000000

1

0.0009766

0.9999977

-0.0000000

0.0000000

0.0000000

2

0.0019531

1.0000017

-0.0000000

-0.0000000

-0.0000000

3

0.0029297

0.9999994

0.0000000

0.0000000

-0.0000000

4

0.0039063

1.0000004

-0.0000000

-0.0000000

0.0000000

1007

0.9833984

1.0000002

-0.0000001

-0.0000000

0.0000000

1008

0.9843750

0.9999998

0.0000004

0.0000001

-0.0000000

1009

0.9853516

1.0000010

-0.0000011

-0.0000002

0.0000000

1010

0.9863281

0.9999978

0.0000032

0.0000004

-0.0000000

1011

0.9873047

1.0000067

-0.0000093

-0.0000013

0.0000000

1012

0.9882813

0.9999813

0.0000268

0.0000037

-0.0000001

1013

0.9892578

1.0000541

-0.0000770

-0.0000106

0.0000003

1014

0.9902344

0.9998449

0.0002211

0.0000303

-0.0000009

1015

0.9912109

1.0004460

-0.0006352

-0.0000870

0.0000025

1016

0.9921875

0.9987195

0.0018246

0.0002500

-0.0000072

1017

0.9931641

1.0036784

-0.0052409

-0.0007182

0.0000206

1018

0.9941406

0.9894347

0.0150535

0.0020628

-0.0000591

1019

0.9951172

1.0303428

-0.0432346

-0.0059230

0.0001698

1020

0.9960938

0.9129785

0.1240610

0.0169516

-0.0004872

1021

0.9970703

1.2462977

-0.3529420

-0.0470151

0.0013861

1022

0.9980469

0.3926255

0.9206328

0.0892117

-0.0036175

1023

0.9990234

0.0127561

-0.1016541

0.9947379

0.0003994

1024

1.0000000

0.0000008

0.0039290

0

0.9999923

Table 2: The general numerical solution

that approximates the

exact underlying solution for the

equation (57)

Figure 1: The general numerical solution

that approximates the

exact underlying solution for the

equation (57)

Table 2 shows the actual digits in single precision of the general

numerical solution.

The condition number

is huge whereas the sensitivity of the general numerical solution

is manageable and much lower

at .

Given the residual , we can make a rough error estimate

of the general numerical solution as

that can be considered accurate for such an application.

The accuracy estimate can also be justified as follows.

The obvious particular solution of the equation (57)

can be approximated by a numerical particular solution:

>> y = K\(1-z); % solve K*y+z = 1 y = 0.561958104442570 1.049493278421724 0.997798939791854 >> norm(Z+K*u-1,1)*h % error of the numerical particular solutoin ans = 1.090344305094233e-07

Namely, the particular solution can be accurately approximated

by a numerical particular solution with error bound .

On the other hand, the solution to the homogeneous equation corresponding to

(57) is

The following Matlab statement sequence shows that a numerical kernel vector

approximates with an error measure ,

as the error estimate suggests.

>> y = K\(1-z); % solve K*y+z = 1 y = >> epsilon = 1e-5; % a tiny epsilon >> h = 1/n; % stepsize >> t = 0:h:1; % the nodes in t >> v = K\(1./(epsilon*sqrt(pi)*exp(((t-1)/epsilon).^2))) % solve K*v = delta_epsilon v = 1.0e+04 * 0.022167287609456 0.000000000000000 5.641852287123326 >> norm(K*v -1./(epsilon*sqrt(pi)*exp(((t-1)/epsilon).^2)),1)*h ans = 7.764167138103457e-05

Although the underlying system is underdetermined in addition to being

singular, the general numerical solution

accurately reveals that the equation (57) with the specific kernel (58) can be accurately solved

in an interval for a small since the annihilator

represented by is identically zero in

that interval.

The singularity of the underlying equation compounded by the representation

linear system being underdetermined is not detrimental at all if we compute

the general numerical solution and, in particular, consider the numerical

kernel as an integral part of the solution.