A Simple Unified Framework for High Dimensional Bandit Problems

Abstract

Stochastic high dimensional bandit problems with low dimensional structures are useful in different applications such as online advertising and drug discovery. In this work, we propose a simple unified algorithm for such problems and present a general analysis framework for the regret upper bound of our algorithm. We show that under some mild unified assumptions, our algorithm can be applied to different high dimensional bandit problems. Our framework utilizes the low dimensional structure to guide the parameter estimation in the problem, therefore our algorithm achieves the comparable regret bounds in the LASSO bandit, as well as novel bounds in the low-rank matrix bandit, the group sparse matrix bandit, and in a new problem: the multi-agent LASSO bandit.

1 Introduction

Stochastic multiarmed contextual bandits are useful models in various application domains, such as recommendation systems, online advertising, and personalized healthcare (Auer, 2002b; Chu u. a., 2011; Abbasi-Yadkori u. a., 2011). Under this setting, the agent chooses one specific arm at each round and observes a reward, which is modeled as a function of an unknown parameter and the context of the arm. In practice, such problems are often high-dimensional, but the unknown parameter is typically assumed to have low-dimensional structure, which in turns implies a succinct representation of the final reward.

For example, in high dimensional sparse linear bandits, also known as the LASSO bandit problem (Bastani und Bayati, 2020), both the contexts and the unknown parameter are high-dimensional vectors, while the parameter is assumed to be sparse with limited nonzero elements. There has been a line of research on LASSO bandits, such as Abbasi-Yadkori u. a. (2011), Alexandra Carpentier (2012), Bastani und Bayati (2020), Lattimore u. a. (2015), Wang u. a. (2018), Kim und Paik (2019), Hao u. a. (2020a), and Oh u. a. (2021). Different algorithms are proposed for this problem, and different regret analyses based on various assumptions are provided.

When the unknown parameter becomes a matrix, some recent research have worked on low-rank matrix bandits. For example, Katariya u. a. (2017a, b) and Trinh u. a. (2020) considered the rank-1 matrix bandit problems, but their results cannot be extended to higher ranks. Jun u. a. (2019) studied the bilinear bandit problems where the reward is modelled as a bilinear product of the left arm, the parameter matrix, and the right arm. Kveton u. a. (2017) first studied the low-rank matrix bandit, but required strong assumptions on the mean reward matrix. Lu u. a. (2021) extended the work by Jun u. a. (2019) to a more generalized low-rank matrix bandit problem but their action set was fixed. Hao u. a. (2020b) further studied the problem of low-rank tensor bandits.

Despite the recent progress in all the above high dimensional bandit problems, both experimentally and theoretically, prior works are scattered and different algorithms with different assumptions are proposed for these problems. Although in LASSO Bandits, people have already given logarithmic dependence on the high dimension, we are surprised that such dependence has not been shown for other problems and polynomial dependence on the high dimensions still exists. An interesting question here is: does there exist a unified algorithm that works in all the high dimensional bandit problems, and if so, does such an algorithm hold a desirable regret bound in the different settings in terms of the dimensional dependence? In this work, we provide affirmative answers to these questions.

Our work is inspired by the literature on traditional high dimensional statistical analysis (Negahban u. a., 2012) and modern high dimensional bandit algorithms (Kim und Paik, 2019; Oh u. a., 2021). The only similar prior work we are aware of is the framework by Johnson u. a. (2016), but they analyzed a completely different problem setting. Their algorithm is not only much more complicated than ours, but also requires very strong assumptions on the arm sets as well as low-dimensional structural information of the unknown parameter.

In particular, we want to highlight the following contributions of our paper:

-

•

We present a simple and unified algorithm framework named Explore-the-Structure-Then-Commit (ESTC) for high dimensional stochastic bandit problems and provide a problem-independent regret analysis framework for our algorithm. We show that to ensure a desirable regret, one simply needs to ensure that the two special events defined in Section 3 happen with high probability after the exploration stage under mild assumptions.

-

•

We demonstrate the usefulness of our framework by applying it to different high dimensional bandit problems. We show that under a mild unified assumption, our algorithm can achieve desirable regret bounds. We first prove that our algorithm achieves comparable regret bounds in the LASSO bandit problem as a sanity check; we then provide novel bounds in the low-rank matrix bandit and the group sparse matrix bandit which also depend logarithmicly on the dimensions. We also show that a simple extension of our algorithm can achieve group sparsity with a desirable regret bound in a new problem: the multi-agent LASSO bandit. We summarize our results and compare them with the most relevant existing works in Table 1. 111For the first regret upper bound by Hao u. a. (2020a), i.e. , we have contacted the authors personally and confirmed that there is a mistake in the proof of Theorem 4.2 in their paper. The term is missing in the original theorem. Explanations are provided in Appendix A.

-

•

Our novel framework provides new proofs for different high dimensional bandit problems. Although prior works such as Hao u. a. (2020a) has proved similar results in the LASSO Bandit case, the proof techniques for low-rank matrix bandit and group-sparse matrix bandit are highly different and novel, which are also part of the contributions in this paper, e.g., proofs for Lemma 4.2, 4.3, C.2, C.3, and C.4. Interested readers can refer to the Appendix for more details.

| LASSO | Regret Bound | Arm Set | Assumptions |

|---|---|---|---|

| Lattimore u. a. (2015) | fixed | action set is a hypercube | |

| Bastani und Bayati (2020) | CBL | compatibility, margin, optimality | |

| Wang u. a. (2018) | CBL | compatibility, margin, optimality | |

| Kim und Paik (2019) | contextual | compatibility | |

| Oh u. a. (2021) | contextual | compatibility, symmetry, covariance | |

| Oh u. a. (2021) | contextual | RE condition, symmetry, covariance | |

| Hao u. a. (2020a) | fixed | action set spans | |

| Hao u. a. (2020a) | finite, fixed | action set spans , minimum signal | |

| Hao u. a. (2020a) | finite, fixed | action set spans | |

| This paper (sanity check) | contextual | RE condition | |

| Low-rank | |||

| Jun u. a. (2019) | fixed | the reward function is bilinear | |

| Johnson u. a. (2016) | fixed | prior knowledge of parameter | |

| Lu u. a. (2021) | fixed | sub-Gaussian sampling distribution | |

| This paper | contextual | RE condition | |

| Group-sparse | |||

| Johnson u. a. (2016) | fixed | prior knowledge of parameter | |

| This paper | contextual | RE condition | |

| Multi-agent | |||

| This paper | contextual | RE condition |

2 Preliminaries

In this section, we establish some important preliminary notations and definitions in this paper.

Notations. Given a subspace of , its orthogonal complement is defined as . The matrix inner product for two matrices of the same size are defined as We use for vector norms and for matrix norms. Given a norm , we use the notation to represent the projection of a vector onto , i.e., , and similarly for . The dual of a norm is defined to be . For the regularization norm , we denote its dual to be . We use to hide the non-dominating factors in big- notations. We frequently use the notation for to denote the set of integers . For the reader’s reference, a complete list of all the norms and their duals used in this paper is provided in Appendix A.

Multiarmed Contextual Bandits. In modern multiarmed contextual bandit problems, a set of contexts for each arm is generated at every round , and then the agent chooses an action from the arms. The contexts are assumed to be sampled i.i.d from a distribution with respect to , but the contexts for different arms can be correlated (Chu u. a., 2011). After the action is selected, a reward for the chosen action is received, where is a deterministic function, is an unknown parameter, and is a zero-mean random noise term which is often assumed to be sub-Gaussian or even conditional sub-Gaussian in a few cases. In this paper, we focus on bandit problems where is high dimensional but with low-dimensional structure such as a sparse vector, a low-rank matrix, and a group-sparse matrix.

Let denote the optimal action at each round. We measure the performance of all algorithms by the expectation of the regret, denoted as

The goal for all the bandit algorithms studied in this paper is to ensure a sublinear expectation of the regret with respect to , so that the average regret converges, thus making the chosen actions nearly optimal. Moreover, we require the regret bounds to depend on the low-dimensional structure constraint of the parameter, for example, the number of non-zero elements for a sparse vector, rather than polynomially depend on the high dimension(s), so that the algorithm utilizes the low-dimensional structure of the parameter to reduce the regret.

Optimization Problem. We use the shorthand notations and to represent all the contexts of the chosen actions and the rewards received up to time . Many algorithms designed for multiarmed bandit problems involve solving an online optimization problem with a loss function and a regularization norm , i.e.,

| (1) |

where is the regularization parameter chosen differently in different algorithms and is the parameter domain. We also often use the notation to represent . The solution in Eqn. (1) is a regularized estimate of based on the currently available data. The reason to use the regularization is that it can hopefully identify the low-dimensional structure of so that can converge to fast and the action chosen by the algorithm becomes optimal after a few rounds.

High Dimensional Statistics. Our general theory applies to -estimators, i.e., the loss has the form , where each is a convex and differentiable loss function and is a decomposable norm. -estimators and decomposable norms are well-accepted concepts in the high dimensional statistics literature (Negahban u. a., 2012). We first establish the definition of a decomposable norm.

Definition 1.

Given a pair of subspaces , the norm is said to be decomposable with respect to the subspace pair iff

We present a few examples of the pair of subspaces and the decomposable regularization, each corresponding to one application of our general theory in Section 4.

Example 1.

(Sparse Vectors and the Norm). Let be a sparse vector with nonzero entries, we denote to be the set of non-zero indices of (i.e., the support). The pair of subspaces are chosen as .Then norm is decomposable with respect to i.e., for all , since and have non-zero elements on different entries.

Example 2.

(Low Rank Matrices and the Nuclear Norm). Let be a low rank matrix with rank . We define the pair of subspace as

where and represent the space of the left and right singular vectors of the target matrix . Note that in this case . Then the nuclear norm is decomposable with respect to , i.e., for all .

Example 3.

(Group-sparse Matrices and the Norm). Let be a matrix with group sparse rows, i.e., each row is nonzero only if , and . Similar to Example 1, we define the pair of subspace as

The orthogonal complement can be defined with respect to the matrix inner product. Then the norm, defined as , is decomposable with respect to .

Given the decomposable regularization , it is shown in Negahban u. a. (2012) that when the regularization parameter , the error belongs to a constraint set defined as follows.

Definition 2.

For any decomposable on the subspace pair , the constraint set is defined as

Such a set restrains the behavior of the error when the regularization parameter is correctly chosen. Next we present the definition of restricted strong convexity on the loss function .

Definition 3.

The loss function is said to be restricted strongly convex (RSC) around with respect to the norm with curvature and tolerance function if

In the high dimensional statistics literature, restricted strong convexity is often ensured by a sufficient number of samples for some specific distributions of such as the Gaussian distribution (Negahban u. a., 2012). In the online case, we need some special assumptions to guarantee that restricted strong convexity holds after a number of rounds. In addition, the following subspace compatibility constant plays a key role in restricting the distance between the true parameter and its estimate by the low dimensional structural constraint, hence generating a desirable regret bound.

Definition 4.

For a subspace , the subspace compatibility constant with respect to the pair is given by

For instance, for the norm pair and defined as in Example 1 because for by the Cauchy-Schwarz inequality.

3 Main results

In this section, we present our simple and general algorithm, as well as its analysis framework. Let be a constant to be specified later, we define the following two probability events and

where represents a correctly chosen regularization parameter and means that is RSC with respect to the undefined norm with curvature and tolerance at round . As we will show below, ensuring that these two events happen with high probability is of vital importance.

3.1 Oracle inequality

We first present a general oracle inequality between the estimate and the true parameter, which is extended from the results in Negahban u. a. (2012).

Lemma 3.1.

(Oracle Inequality) If at round , the probability event holds and the event holds for all , then for the solution of Eqn. (1), the difference satisfies the bound

Remark 3.1.

The proof of Lemma 3.1 is provided in Appendix F for completeness. Lemma 3.1 states an oracle inequality for each choice of the pair of norms , and the corresponding subspaces where is decomposable. The difference converges to zero if both and decreases when increases, and therefore the estimate becomes more and more accurate as rounds progress.

3.2 The general algorithm

Now we present our Explore-the-Structure-Then-Commit (ESTC) algorithm for high dimensional contextual bandit problems. Our algorithm consists of two stages: the exploration stage where arms are randomly picked and the commit stage where the best arm explored is chosen. Algorithm 1 shows our procedure in detail.

Remark 3.2.

Similar algorithms have been proposed in some recent papers. For example, Hao u. a. (2020a) proposed an Explore-the-Sparsity-Then-Commit algorithm, but it was only designed and analyzed for fixed action sets and for LASSO bandits. Oh u. a. (2021) proposed a sparsity-agnostic algorithm in the LASSO bandit problem, which does not need the sparsity parameter , but they required much more assumptions than ours in the multi-arm case . Lu u. a. (2021) proposed a Low-ESTR algorithm that solved the same optimization problem as our Section 4.2 in the low-rank matrix bandit, but they require the lowOFUL algorithm by Jun u. a. (2019) and the algorithm is designed for fixed action sets.

Remark 3.3.

Our algorithm generalizes over the prior efforts on different high dimensional bandit problems. The advantages of our algorithm are that (1). it is very simple, (2). it does not require strong assumptions, and (3). it can be applied to different problems while it remains unclear whether prior works can be extended to all the problems we discuss here. Furthermore, we provide comparable regret bounds for existing problems and novel results for new problems (see Table 1, Section 4, and 5).

3.3 Regret analysis

To analyze the regret of Algorithm 1, we impose some weak assumptions on the reward function and the norm of the context. The two assumptions are listed below for the general theorem, and we will demonstrate how they can be easily guaranteed in the specific applications in Section 4.

Assumption 1.

is normalized with respect to the norm ., i.e. for some constant .

Assumption 2.

is -Lipschitz over and -Lipschitz over with respect to . i.e.,

Remark 3.4.

Assumption 1 is very standard in the contextual bandit literature, see e.g., Chu u. a. (2011); Bastani und Bayati (2020); Kim und Paik (2019); Lu u. a. (2021), where the norm or the Frobenius norm of the contexts is assumed to be either bounded by or a constant . In the case where is normalization-invariant (e.g., the linear case), Assumption 1 can be achieved without loss of generality through normalization of the contexts and the rewards. Assumption 2 can also be easily guaranteed with the help of Assumption 1 for linear models, as well as for some generalized linear models whose link functions has bounded derivatives such as the logistic model. Given Assumptions 1 and 2, we present our novel problem-independent theorem of the regret bound.

Theorem 3.1.

Proof Sketch. Instead of assuming a particular form of the model or the shape of the parameter , our proof techniques utilizes the property of all high dimensional bandit problems solved by Algorithm 1 and thus contributes to a general bound. As far as we are aware, no such general analysis have been proved before. The proof starts by showing the instant regret at round is bounded almost surely.

which can be used to bound the regret in and when and do not happen. Then notice that when , our choice of action in the commit phase implies that , we can therefore transform the problem of bounding the regret into a problem of bounding the distance between and by proving that under event and , for

Therefore for any constant , either

or , which means that either the instantaneous regret is bounded by , or the distance is large. The proof is finished by taking to be the upper bound in Lemma 3.1 multiplied by a constant, and taking expectations and summations over .

Remark 3.5.

The full proof is provided in Appendix A. The above regret bound may seem to be complicated at first sight, but we can interpret it in the following way. In the initial exploration rounds, since we pull arms randomly to collect more samples, we have to consider the worst case scenario and bound the regret linearly in . After enough exploration at , when the two events or do not happen, no conclusions can be made on the distance between the estimator and the target , contributing to the second term . When both events happen, and are close enough and we can carefully bound the regret with the help of Lemma 3.1, which generates the third term . Theorem 3.1 indicates that the expected regret upper bound of Algorithm 1 depends on the probability of , after a chosen round , as well as the choice of and . Therefore, to obtain a sublinear regret, we only need to ensure that the following two things happen in the specific applications.

-

1.

are high probability events.

-

2.

are carefully chosen so that term is sublinear

For instance, suppose that term (b) is finite, , and , then the expected regret is of size by simple algebra. Such a result is desirable since the regret bound is sublinear with respect to , and it depends on the subspace compatibility constant instead of the dimension size, so we utilize the low-dimensional structure in . The final regret bound in Theorem 3.1 will become clearer when we discuss its specific applications.

3.4 High probability events

Finally, we address the two high probability events as they are needed to prove a final regret bound. As we will show in Section 4, the probability of the event is often decided by the choice of and the model structure. No further assumptions are needed for to hold with high probability in all the problems in this paper. However, does not necessarily hold with high probability even after a large number of rounds, and we need another assumption to guarantee its validity.

Assumption 3.

(Restricted Eigenvalue Condition) Let denote the matrix where each row is a context vector from an arm. The population Gram matrix satisfies that there exists some constant such that , for all .

Remark 3.6.

In the case where the contexts are matrices, Assumption 3 represents that the population Gram matrix built from the vectorized contexts satisfies the aforementioned condition. To perform vetorization, we simply need to stack the columns of the matrices and then use the vectorized contexts to obtain the matrix . We emphasize that Assumption 3 is very general and mild because it is only a requirement on the population, which is satisfied for many distributions, for example, the uniform distribution on a Euclidean unit ball. Apart from Assumption 3, prior works either need many more assumptions such as symmetric distribution and balanced co-variance in (Oh u. a., 2021), or very complicated algorithms to make a high probability event (Kim und Paik, 2019). Our algorithm, however, is simple and general and it can be applied to different problems with only Assumption 3.

Remark 3.7.

Another popular assumption in the LASSO bandit problem is the compatibility condition (Bastani und Bayati, 2020; Kim und Paik, 2019), which would replace the norm in Assumption 3 by the norm (the regularization norm in the LASSO bandit problem). Although the compatibility condition is slightly weaker than the restricted eigenvalue condition, we can easily replace the norms in all our arguments by the norm and still obtain the favorable properties similar to Lemma 3.1. The final regret bound may slightly differ from our results in Section 4.1 in terms of multiplicative constants if we use the compatibility condition, but the proof idea is the same. We use the RE condition in our paper because it is currently unknown whether the compatibility condition can be extended to the matrix bandit case. We leave it as a future work direction.

4 Applications on existing problems

In this section, we present some specific applications of our general framework. Each subsection is organized in the following way. We first clarify all the unspecified notations in the framework, such as the loss, the regularization norm, the compatibility constant, and so on. Then we present a lemma to give the proper choice of the regularization parameter in each problem. Given the lemma, we derive corollaries of Theorem 3.1 to present the final regret bound of the corresponding algorithm. We emphasize that even though we focus on linear models in all examples for clarity, it is easy to extend our results to nonlinear models that satisfy Assumption 1 and 2. For example, results for generalized linear models whose link functions are Lipschitz can be easily obtained. Validation experiments that support the correctness of our regret upper bounds are provided in Appendix G

4.1 LASSO bandit

We first consider the LASSO bandit problem. In this case, the reward is assumed to be a linear function of the context of the chosen action and the unknown parameter , i.e., , where is a (conditional) sub-Gaussian noise. In the LASSO bandit problem, the unknown parameter is assumed to be sparse with only non-zero elements and . This naturally leads to the use of regularization.

To fit the problem into our framework so that we can get a regret bound, we first clarify the corresponding notations. The loss function and the regularization are defined to be

In this case, we let be defined as in Example 1, then regularization is decomposable with respect to this pair of spaces. We choose the norm in as the norm, and thus the compatibility constant . Following Chu u. a. (2011), we assume that the contexts and the parameter are all normalized so that , . Therefore Assumption 1 and 2 are satisfied automatically. Now, we present the following lemma, which provides the choice of in the LASSO Bandit problem.

Lemma 4.1.

Suppose the noise is conditional -sub-Gaussian. For any , use

in Algorithm 1, then with probability at least , we have

Given the above lemma, it is easy to apply Theorem 3.1 to get a specific regret bound in the LASSO bandit. Corollary 4.1 follows from taking in Lemma 4.1 and .

Corollary 4.1.

The expected cumulative regret of the Algorithm 1 in the LASSO bandit problem is upper bounded by

Remark 4.1.

The proofs and the specific algorithm are provided in Appendix B. Note that most of the regret bound depends polynomially on the size of the support and only logarithmicly on the high dimension . Therefore, Algorithm 1 converges much faster than directly applying linear bandit algorithms such as LinUCB (Chu u. a., 2011) to the sparse setting, which satisfies our requirement. Corollary 4.1 indicates that the regret bound is of size , which matches the regret upper bound proved by Hao u. a. (2020a) on the fixed action set and the minimax lower bound up to a logarithmic factor (Hao u. a., 2020a).

Remark 4.2.

Some recent papers have proved better dependence in terms of the total number of rounds with more complexly-designed algorithms, e.g. Kim und Paik (2019) or more assumptions, e.g. Oh u. a. (2021). Specifically, they have provided regret bounds. However, as mentioned by Hao u. a. (2020a), these works all need to be sufficiently large as an additional requirement. In the so-called data-poor regime where is limited, an regret is unavoidable and thus our regret is optimal (Hao u. a., 2020a). Moreover, since vectors are 1-column matrices, such lower bounds are also unavoidable in the low-rank and group-sparse matrix bandit problems. Our result on LASSO bandit serves as a sanity check of the logarithmic dependence on the dimension and our main goal is to show such dependence in the other problems.

4.2 Low-Rank matrix bandit

Next, we consider the implications of our general theory in the low-rank matrix bandit problems. In this case, the reward is assumed to be a linear function of the low rank matrix and the context matrix , i.e., , where . We specify the loss function and the regularization norm to be

By Example 2, the nuclear norm regularization is decomposable on defined by the left and right singular vector spaces of . Note that in this case because the space contains matrices with rank at most . The norm we choose in the event is the Frobenious norm. Also, we assume without loss of generality that the matrices are normalized, so that , . Therefore, Assumption 1 and 2 are automatically satisfied. Similar to Lemma 4.1, the following lemma provides a good choice of for the low-rank matrix bandit.

Lemma 4.2.

Suppose the noise is -sub-Gaussian. At each round , for any , use

in Algorithm 1, then with probability at least , we have

Similarly, we can obtain the regret bound by setting in Lemma 4.2 and .

Corollary 4.2.

The expected cumulative regret of the Algorithm 1 in the low-rank matrix bandit problem is upper bounded by

Remark 4.3.

The proofs and the corresponding matrix bandit algorithm are provided in Appendix C. The regret bound in Corollary 4.2 is of size , which polynomially depends on the low rank structure but only logarithmicly on the dimensions and is thus better than directly applying linear bandit algorithms to the problem, which is again desirable. We emphasize that our result cannot be directly compared with some prior results, because papers such as Lu u. a. (2021); Jun u. a. (2019) consider a fixed set of the context matrices instead of a generating distribution , which is different from our setting. Although our dependence on the total number of rounds is , we have logarithmic dependence on the sum of the dimensions and thus it is more desirable than bounds that have polynomial dependence on when the dimensions are large.

4.3 Group-sparse matrix bandit

Finally, we also apply our general framework to the group-sparse matrix bandit problem. Similar to the low-rank matrix bandit case, we assume that the expected reward is a linear function of the context matrix and the optimal parameter , i.e., . Define to be the set of non-zero rows in and assume that , so the matrix is group sparse. We again specify the sum of squared errors to be the loss, but use the norm as the regularization norm.

Note that if , the above problem is equivalent to the LASSO bandit case, because we only need to vectorize all the matrices by stacking their columns. Then becomes the mean squared error and becomes the regularization, thus we only consider here. Define the subspaces using as in Example 3, then the norm regularization is decomposable.

Similarly, we assume without loss of generality that the matrices are normalized with respect to the Frobenious norm, so that Assumption 1 and 2 are satisfied automatically. We define the function . This notation is used because we need slightly different choices of for and . Also, the compatibility constant , which varies for different . Similarly, we provide the following lemma for a good choice of the parameter in group-sparse matrix bandits.

Lemma 4.3.

Suppose that is -sub-Gaussian. At each round , for any , use

in Algorithm 1, then with probability at least , we have .

Given the above lemma, we can similarly derive a desirable regret bound.

Corollary 4.3.

With the two functions of

the expected cumulative regret of the Algorithm 1 in the group-sparse matrix bandit problem is upper bounded by

Remark 4.4.

The proofs and the algorithm are provided in Appendix D. The regret bound in Corollary 4.3 depends on the choice of the regularization norm. For example, if , then is the group-LASSO regularization and the final regret bound is . Besides, the regret bound only has logarithmic dependence on , so it is desirable since we assume that the matrix is group sparse with . Again, we emphasize that the regret bound is not directly comparable to Johnson u. a. (2016) since they consider a fixed action set. Although we have dependence on , our regret bound is more desirable when the dimension is high and our logarithmic dependence on is preferred.

5 Application on a new problem: the multi-agent LASSO bandit

Apart from direct applications, our general analysis framework can also inspire less-direct use cases. Here we briefly present a novel application where our framework guides a new algorithm and a new regret bound.

Suppose there are agents solving LASSO bandit problems synchronously, and each agent receives a stochastic reward at every round . Here, the contexts for each problem are similar and thus the parameters are required to be group-sparse instead of just sparse. The major challenges in this problem are that, first, there are multiple actions and multiple rewards at each round. Second, the Lipschitzness assumption may only be guaranteed for each agent, but not for the whole problem. Therefore, we propose a variant of our algorithm (shown in Algorithm 5 in Appendix E where the agents jointly solve the following optimization problem.

Note that the above problem also has the form of Eqn. (1). Therefore, following the same logic in our analysis framework, we prove two high probability events that correspond to the correctly chosen regularization parameter and the restricted strong convexity in this multi-agent problem, and then an regret bound is proved in Appendix E.

Theorem 5.1.

Remark 5.1.

Although the bound in Theorem 5.1 is the same as applying the LASSO bandit algorithm to each agent independently, our regularization can ensure group-sparsity in the parameter, which cannot be guaranteed in the former case. Again, such a regret bound is desirable since we only have logarithmic dependence on , and .

References

- Abbasi-Yadkori u. a. (2011) \NAT@biblabelnumAbbasi-Yadkori u. a. 2011 Abbasi-Yadkori, Yasin ; Pal, David ; Szepesvari, Csaba: Online-to-Confidence-Set Conversions and Application to Sparse Stochastic Bandits. In: Proceedings of the Fifteenth International Conference on Artificial Intelligence and Statistics, 2011

- Alexandra Carpentier (2012) \NAT@biblabelnumAlexandra Carpentier 2012 Alexandra Carpentier, Remi M.: Bandit Theory meets Compressed Sensing for high dimensional Stochastic Linear Bandit. In: Proceedings of the Fifteenth International Conference on Artificial Intelligence and Statistics (AISTATS) (2012)

- Auer (2002b) \NAT@biblabelnumAuer 2002b Auer, Peter: Using confidence bounds for exploitationexploration trade-offs. In: Journal of Machine Learning Research (2002b), S. 3:397–422

- Bastani und Bayati (2020) \NAT@biblabelnumBastani und Bayati 2020 Bastani, Hamsa ; Bayati, Mohsen: Online Decision-Making with High-Dimensional Covariates. In: Operation Research (2020), S. 68 (1), 276–294

- Bobkov u. a. (2015) \NAT@biblabelnumBobkov u. a. 2015 Bobkov, Sergey ; Nayar, Piotr ; Tetali, Prasad: Concentration Properties of Restricted Measures with Applications to Non-Lipschitz Functions. 2015

- Buhlmann und Van De Geer (2011) \NAT@biblabelnumBuhlmann und Van De Geer 2011 Buhlmann, Peter ; Van De Geer, Sara: Statistics for high-dimensional data: methods, theory and applications. Springer Science Business Media, 2011

- Chu u. a. (2011) \NAT@biblabelnumChu u. a. 2011 Chu, Wei ; Li, Lihong ; Reyzin, Lev ; Schapire, Robert: Contextual Bandits with Linear Payoff Functions. In: Proceedings of the Fourteenth International Conference on Artificial Intelligence and Statistics (AISTATS) (2011)

- Hao u. a. (2020a) \NAT@biblabelnumHao u. a. 2020a Hao, Botao ; Lattimore, Tor ; Wang, Mengdi: High-Dimensional Sparse Linear Bandits. In: Advances in Neural Information Processing Systems, 2020

- Hao u. a. (2020b) \NAT@biblabelnumHao u. a. 2020b Hao, Botao ; Zhou, Jie ; Wen, Zheng ; Sun, Will W.: Low-rank Tensor Bandits. 2020

- Johnson u. a. (2016) \NAT@biblabelnumJohnson u. a. 2016 Johnson, Nicholas ; Sivakumar, Vidyashankar ; Banerjee, Arindam: Structured Stochastic Linear Bandits. 2016

- Jun u. a. (2019) \NAT@biblabelnumJun u. a. 2019 Jun, Kwang-Sung ; Willett, Rebecca ; Wright, Stephen ; Nowak, Robert: Bilinear Bandits with Low-rank Structure. In: Proceedings of the 36th International Conference on Machine Learning. Long Beach, California, USA : PMLR, 09–15 Jun 2019 (Proceedings of Machine Learning Research), S. 3163–3172

- Katariya u. a. (2017b) \NAT@biblabelnumKatariya u. a. 2017b Katariya, Sumeet ; Kveton, Branislav ; Szepesvari, Csaba ; Vernade, Claire ; Wen, Zheng: Stochastic Rank-1 Bandits. In: Proceedings of the 20th International Conference on Artificial Intelligence and Statistics, 2017b

- Katariya u. a. (2017a) \NAT@biblabelnumKatariya u. a. 2017a Katariya, Sumeet ; Kveton, Branislav ; Szepesvári, Csaba ; Vernade, Claire ; Wen., Zheng: Bernoulli rank-1 bandits for click feedback. In: Proceedings of the 26th International Joint Conference on Artificial Intelligence, 2017a

- Kim und Paik (2019) \NAT@biblabelnumKim und Paik 2019 Kim, Gi-Soo ; Paik, Myunghee C.: Doubly-Robust Lasso Bandit. In: Advances in Neural Information Processing Systems 32 (2019), S. 5877–5887

- Kveton u. a. (2017) \NAT@biblabelnumKveton u. a. 2017 Kveton, Branislav ; Szepesvari, Csaba ; Rao, Anup ; Wen, Zheng ; Abbasi-Yadkori, Yasin ; Muthukrishnan, S.: Stochastic Low-Rank Bandits. 2017

- Lattimore u. a. (2015) \NAT@biblabelnumLattimore u. a. 2015 Lattimore, Tor ; Crammer, Koby ; Szepesvari, Csaba: Linear Multi-Resource Allocation with Semi-Bandit Feedback. In: Advances in Neural Information Processing Systems Bd. 28, Curran Associates, Inc., 2015, S. 964–972

- Lu u. a. (2021) \NAT@biblabelnumLu u. a. 2021 Lu, Yangyi ; Meisami, Amirhossein ; Tewari, Ambuj: Low-Rank Generalized Linear Bandit Problems. In: Proceedings of The 24th International Conference on Artificial Intelligence and Statistics, 2021

- Negahban u. a. (2012) \NAT@biblabelnumNegahban u. a. 2012 Negahban, Sahand N. ; Ravikumar, Pradeep ; Wainwright, Martin J. ; Yu, Bin: A Unified Framework for High-Dimensional Analysis of -Estimators with Decomposable Regularizers. In: Statistical Science (2012), S. 27(4):538–557

- Oh u. a. (2021) \NAT@biblabelnumOh u. a. 2021 Oh, Min-Hwan ; Iyengar, Garud ; Zeevi, Assaf: Sparsity-Agnostic Lasso Bandit. In: Meila, Marina (Hrsg.) ; Zhang, Tong (Hrsg.): Proceedings of the 38th International Conference on Machine Learning Bd. 139, PMLR, 18–24 Jul 2021, S. 8271–8280

- Recht (2011) \NAT@biblabelnumRecht 2011 Recht, Benjamin: A Simpler Approach to Matrix Completion. In: Journal of Machine Learning Research 12 (2011), Nr. 104, S. 3413–3430

- Trinh u. a. (2020) \NAT@biblabelnumTrinh u. a. 2020 Trinh, Cindy ; Kaufmann, Emilie ; Vernade, Claire ; Combes, Richard: Solving Bernoulli Rank-One Bandits with Unimodal Thompson Sampling. In: Proceedings of the 31st International Conference on Algorithmic Learning Theory, 2020

- Wang u. a. (2018) \NAT@biblabelnumWang u. a. 2018 Wang, Xue ; Wei, Mingcheng ; Yao, Tao: Minimax Concave Penalized Multi-Armed Bandit Model with High-Dimensional Covariates. In: Proceedings of the 35th International Conference on Machine Learning, 2018

Supplementary Materials to ”A Simple Unified

Framework for High Dimensional Bandit Problems”

Appendix A Notations and the Main Theorem

A.1 List of Norms

For a vector ,

-

•

is the norm of , i.e., , which is self-dual.

-

•

is the norm of , i.e., , whose dual norm is the norm.

-

•

is the norm of , i.e., , whose dual norm is the norm.

For a matrix

-

•

is the Frobenius norm of , i.e., , which is self-dual.

-

•

is the nuclear norm of , which is defined as , where ’s are the singular values of . The dual norm of the nuclear norm is the induced operator norm.

-

•

is the operator norm of induced by the vector norm , i.e., . An important property of is that , where ’s are the singular values of . The dual norm of the induced operator norm is the nuclear norm.

-

•

is the norm of . For example if , this corresponds to the group lasso regularization. The dual norm of norm is the norm, defined as , with the relationship .

-

•

is the element-wise maximum norm of , which is defined as .

A.2 Explanations for the Regret Bound by Hao u. a. (2020a)

For the results in this subsection, we have personally contacted the authors and confirmed that the logarithmic term is missing in their proof. For clarity, we follow their notations where they have used instead of for the total number of rounds and instead of for the exploration rounds. The other notations are either the same as ours (e.g. sparsity level of the target vector is denoted by , dimension size is denoted by ) or just constants (e.g., is the maximum reward, which is 1 in our case). Please refer to the original paper for more detailed notations. Now in their “Section B.3: Proof of Theorem 4.2: regret upper bound”, on page 17, the authors have proved that the regret is upper bounded by the following terms in “Step 3: optimize the length of exploration”.

With probability at least .

| (2) |

In the final step, Hao u. a. (2020a) have taken and compute the final regret bound. However, they have ignored the term on the numerator of the fractional under the square root sign. In other words, when taking , we get

| (3) | ||||

A.3 Proof of Theorem 3.1

Proof. By the Lipschitzness of over with respect to , and the boundedness of , we have

Then we can decompose the one-step regret from round into three parts as follows,

where is the indicator function. The last equality is due to the choice of , and thus we know that . We focus on the second indicator function now. By the Lipschitzness of over , we have

Substitute the above inequality back and take expectation on both sides of the one-step regret from round , we get

For and any constant , the expectation is bounded by

Now take to be the upper bound of in Lemma 3.1, i.e., . We know by Lemma 3.1 that . Then the expected cumulative regret becomes

A.4 Regret Bound with the Regularization Norm

In this subsection, we provide a regret bound when Assumption 1 and 2 are assumed base on the regularization norm , which would correspond to, for example, using norm and the compatibility condition in LASSO bandit. The regret bound we derive in Corollary A.1 can be easily extended to the LASSO bandit, the low-rank matrix bandit and the group-sparse matrix bandit problems. We first provide the second oracle inequality (Negahban u. a., 2012).

Lemma A.1.

(Oracle Inequality) If the probability event holds and holds for , where . Further suppose that , then the difference satisfies the bound

Assumption 4.

We assume is normalized with respect to the norm ., i.e., for some constant .

Assumption 5.

Here we assume similar Lipschitzness conditions on and boundedness on , as what we have done in Section 3. We assume is -Lipschitz over and -Lipschitz over with respect to the norm . i.e.,

We show that based on such conditions, we can get a similar result as in Theorem 3.1.

Corollary A.1.

Proof. By the Lipschitzness of over with respect to , and the boundedness of , we have

Then we can decompose the one-step regret from round into three parts as follows

where is the indicator function. The last equality is due to the choice of , and thus we know that . We focus on the second indicator function now. By the Lipschitzness of over , we have

Substitute the above inequality back and take expectation on both sides of the one-step regret from round , we get

For and any constant , the expectation is bounded by

Now take to be the upper bound of in Lemma A.1, i.e., . We know by Lemma A.1 that . Then the expected cumulative regret becomes

Appendix B Proof for the LASSO Bandit

B.1 Notations and Algorithm

We first clarify the notations we use throughout the proof for the LASSO bandit. We use the notations , to represent the context matrix, the reward and the error vectors respectively, i.e., . The loss function now becomes . The derivative of evaluated at can be computed as

The Bregman divergence can therefore be computed as

Therefore the event is equivalent to . The event (RSC condition) is equivalent to

Based on the above Bregman divergence, we define the matrix as follows .

B.2 Technical Lemmas

The following two Bernstein-type inequalities are very useful in our analysis.

Lemma B.1.

(Lemma EC.1 of Bastani und Bayati (2020)) Let be a martingale difference sequence, and suppose that is -sub-Gaussian in an adapted sense, i.e., for all almost surely. Then, for all , we have

Lemma B.2.

(Lemma EC.4. of Bastani und Bayati (2020)) Let be i.i.d. random vectors in with for all Let and . Then for any , we have

B.3 Proof of Lemma 4.1

Proof. Denote to be the -th column of the matrix . Since we assume that each , then the matrix is column normalized, i.e., . From the union bound, we know that for any constant , we have

Note that is a martingale difference sequence adapted to the filtration , because . Also note that each is -sub-Gaussian, therefore

Hence we can use Lemma B.1 and thus

If we take , then with probability , we conclude that

B.4 Proof of Lemma B.3

Lemma B.3.

Suppose Assumption 3 is satisfied, then with probability at least , we have , for all and , where is a constant that depends on .

First, we introduce the following two technical lemmas.

Lemma B.4.

( Lemma 9 of Oh u. a. (2021)) Suppose that , , and that the matrix satisfies the restricted eigenvalue condition with . Moreover, suppose the two matrices are close enough such that where Then

Proof. The proof here modifies the proof by Oh u. a. (2021), and we provide it for completeness. By the Cauchy-Schwartz inequality, we have

For , we have the inequality . Thus

Therefore since we assume that , we have

By some simple algebra on the above inequality, we know that

Lemma B.5.

(Distance Between Two Matrices) Define , where is defined in Assumption 3. Then for all , we have

Proof. Since we sample uniformly in the exploration stage, we know that the contexts are i.i.d., and thus for any constant , by Lemma B.2 we have

Now our choices of and are to let both terms concerning and to be small, i.e.,

Solving the two inequalities leads to

then we have the following inequality

Finally, we provide the proof of Lemma B.3.

Proof. The proof follows from combining Lemma B.4 and Lemma B.5. Since we have that the restricted eigenvalue condition holds for by Assumption 3 , i.e.,

Also, the two matrices , are close enough when is large by Lemma B.5,

with high probability when . Therefore

B.5 Proof of Corollary 4.1

Now given the results in Lemma 4.1, Lemma B.3 and Theorem 3.1, we can easily derive an upper bound for our LASSO bandit algorithm. We specify all the constants here. For example, the Lipschitz constants , the bound of the norm , and we set , where is a constant defined in Lemma B.5. The restricted strong convexity holds with . The compatibility constant . Also, so .

Proof. Using Theorem 3.1, we can get the following upper bound

Note that . Since we take in Lemma 4.1, . Furthermore,

Also by our choice of , we know that

where the last equality is by the fact that is bounded above by a constant when . Therefore we arrive to the following bound

Matching the two dominating terms, we get the choice of and the regret upper bound

Appendix C Proof for the Low-Rank Matrix Bandit

C.1 Notations and Algorithm

We first establish the notations and the corresponding algorithm in low rank matrix bandit problems. We use the shorthand vector notations such that , and . For any matrix , denotes the vectorization of the matrix by stacking all rows of the matrix into a vector, i.e., if has entries

then , and .

The loss function now becomes , and the derivative with respect to can be computed as

where the differentiation is based on the chain rule of matrix calculus and the following facts

Therefore the Bregman divergence in the low rank matrix setting is

Note that one important property of the above Bregman divergence is

Based on the above discussions, we define the matrix as follows

Also by Assumption 3, we know that for any

C.2 Technical Lemmas

The following matrix version of the Bernstein inequality is useful in our analysis of matrix bandits.

Lemma C.1.

(Theorem 3.2 of Recht (2011)) Let be independent zero-mean random matrices of dimension Suppose and M almost surely for all Then for any , we have

C.3 Proof of Lemma 4.2

Proof. The requirement on in terms of the spectral norm of is

Here we define the high probability event , and we first concentrate on the probability of the event conditioned on fixed matrices . By the definition of sub-Gaussian random variables.

where the first inequality is due to the union bound. Hence if we take , then . Under the event , the operator norm of each can be bounded by

Moreover, under the event , we have the following bounds

Therefore we have

where the last inequality is by Lemma C.1 with the corresponding upper bound constants computed above. Now we can further bound the probability using a specific choice of , i.e., we want that

Reversing the above inequality, we get

Therefore if we take , then the above inequality holds. This claim is true because

Note that and hence , and thus if we use

then we have

C.4 Proof of Lemma C.2

Lemma C.2.

Suppose Assumption 3 is satisfied, then with probability at least , we have , for all and , where is a constant that depends on .

First, we introduce the following two technical lemmas.

Lemma C.3.

Suppose that , , and the matrix satisfies the strongly convex condition with . Moreover, suppose the two matrices are close enough such that where Then

Proof. The proof here is inspired by the proof of Lemma 6.17 in Buhlmann und Van De Geer (2011) and Lemma B.4 in Appendix B. A similar argument can be made using the nuclear norms since . That is, the RSC condition can also be assumed in terms of the nuclear norm. Interested readers may take a deeper look at them by replicating all the lemmas in this section. Note that

where the first inequality is by Cauchy-Schwarz and the second inequality is by the definition of the matrix induced norm . Therefore since we assume that , we know that

Therefore

Lemma C.4.

(Distance Between Two Matrices) Define , where is defined in Assumption 3. Then for all , we have

Proof. Since we sample uniformly in the exploration stage, we know that the contexts are i.i.d., and thus for any constant , by Lemma B.2 we have

Note that by the property of matrix norms, we have , therefore we get

Now our choices of and is to let

which leads to the following choices

Then we have the following inequality

Finally, we provide the proof of Lemma C.2.

Proof. The proof follows from Lemma C.3 and Lemma C.4. Since we have that the restricted eigenvalue condition holds for by Assumption 3 , i.e.,

Also, the two matrices , are close enough when is large by Lemma C.4,

with high probability when . Therefore

C.5 Proof of Corollary 4.2

Now given the probability of and in Lemma 4.2 and Lemma C.2, we can easily derive a regret upper bound for our low rank matrix bandit algorithm. We specify all the constants here, for example, the Lipschitz constants , the bound of the norm , and we set , where is a constant defined in Lemma C.4. The restricted strong convexity holds with . The compatibility constant . Also, so .

Proof. Using Theorem 3.1, we can get the following upper bound

Since we take in Lemma 4.2, then . Furthermore

Also by our choice of , we know that

where the last equality is by the fact that is bounded above by a constant when . The last summation term in the regret can be written as

Therefore we arrive to the following final regret bound

Matching the two dominating terms, we get the choice of and the regret upper bound

Appendix D Proof for the Group-sparse Bandit

D.1 Notations and Algorithm

We first clarify the notations we use through out this section. As we discuss in Section 4, is used to denote the matrix whose columns are vectors with similar supports, so that . Similarly, we use the shorthand vector notations such that , and . By our results in the low-rank matrix bandit problem, the derivative with respect to is

Therefore the event is equivalent to

D.2 Proof of Lemma 4.3

Proof. The proof here basically follows from Lemma 5 in Negahban u. a. (2012), except for the function which we introduce later. From the union bound, we know that for any constant , we have

Next, we establish a tail bound for the random variable . Let be the -th row of and define .

For any two -sub-Gaussian vectors , we have

Now if , we have

If , then we have a different inequality

Therefore if we define , we have . Thus the function is Lipschitz with constant . Based on the concentration inequality of measure for Lipschitz functions (Bobkov u. a., 2015; Negahban u. a., 2012), we know that

By Lemma 5 in Negahban u. a. (2012), we know that the mean is bounded by , therefore

By change of variables and the union bound, we can get the claim in the lemma. .

D.3 Proof of Corollary 4.3

Now given the probability of and in Lemma 4.3 and Lemma C.2, we can derive a regret upper bound for our group-sparse matrix bandit algorithm. Similarly, We specify all the constants here, for example, the Lipschitz constants , the bound of the norm , and we set , where is the constant defined in Lemma C.4. The restricted strong convexity holds with . The compatibility constant . Also, so .

Proof. Using Theorem 3.1, we can get the following upper bound

Since we take in Lemma 4.3, . Furthermore,

Also by our choice of , we know that

where the last equality is by the fact that is bounded above by a constant when . The last summation term in the regret can be written as

Therefore we arrive to the following bound

Matching the two dominating terms, we get the choice of

| (4) |

and the following regret upper bound

where and .

Appendix E Proof for the Multi-agent LASSO

E.1 Notations and Algorithm

Define and as the set of zero rows, then by our setting . Let the loss be the sum of squared error function and the regularization function be the norm. More formally,

Define as in Example 3, then the norm is decomposable and . For each agent , we use the notations , to represent the context matrix, the reward and the error vectors, i.e., . The derivative with respect to can be computed as

Note that if we take partial derivatives, we get

Therefore . Now we can compute the Bregman divergence as follows.

Therefore the event is equivalent to

The event (RSC condition) is equivalent to

E.2 Useful Lemmas

Lemma E.1.

(Good Choice of Lambda) Suppose that is -sub-Gaussian. For any , use

at each round in Algorithm 5, then with probability at least , we have .

Proof. From the union bound, we know that for any constant , we have

Note that the -th row of consists of , which are all -sub-Gaussian random variables.

For any two -sub-Gaussian vectors , we have

Now if , we have . If , then we have a different inequality . Therefore if we define , we have . Thus the function is Lipschitz with constant . Based on the concentration inequality of measure for Lipschitz functions (Bobkov u. a., 2015; Negahban u. a., 2012), we know that

By similar arguments as in the proof of Lemma 4.3, we know that

By change of variables and the union bound, we can get the results in the lemma. .

Lemma E.2.

Proof. Note that the RSC condition (event ) is equivalent to

By the results in Lemma B.3 in the LASSO bandit problem, we know that with high probability

when , where is defined in Lemma B.5. Therefore by the Frechet inequality, we know that

E.3 Proof of Theorem 5.1

Proof. By the boundedness of and , we know that

Then we can decompose the one-step regret from round across different agents into three parts as follows

where is the indicator function. The last equality is due to the choice of , and thus we know that . We focus on the second indicator function now. By the Lipschitzness of over , we have

where the last inequality is by the Cauchy-Schwarz Inequality. Substitute the above inequality back and take expectation on both sides of the one-step regret from round , we get

For and any constant , the expectation is bounded by

By Lemma E.2, the RSC condition is satisfied when , where is defined in Lemma B.5. Now take to be the upper bound of in Lemma 3.1, i.e., . We know by Lemma 3.1, the expected cumulative regret becomes

The last term can be bounded as

Take and match the two dominating terms, we get the choice of , Therefore the final regret bound is of size

Appendix F Proofs Related to the Oracle Inequalities

Recall the definition of the constraint set . We define the subset with bounded norm . Also define the function as

F.1 Proof of Lemma 3.1

First, we introduce the following two lemmas from Negahban u. a. (2012)

Lemma F.1.

(Lemma 3 of Negahban u. a. (2012)) For any vectors , and a decomposable norm on , we have the following inequality

Lemma F.2.

(Lemma 4 of Negahban u. a. (2012)) If for all vectors for a constant , then

Now, we provide the proof of Lemma 3.1

Proof. Note that , by the restricted strong convexity of on , we have

where the second inequality is by Lemma F.1. The fourth inequality is by the generalized Cauchy Schwarz inequality. The fifth inequality is because of our setting . The last inequality is because of the triangle inequality . Now by the subspace compatibility constant, we know that

where the last inequality is because and because the projection operation is non-expansive. Therefore we can continue to lower bound in the following way.

Now since we take , by the same algebraic manipulations in Negahban u. a. (2012), we have . Now by Lemma F.2, we know that

The second oracle inequality in Lemma A.1 can be proved easily by the triangle inequality decomposition and the definition of . That is

If , then . Therefore we know that

Appendix G Validation Experiments

In this section, we provide some experiments in order to validate our claims in the theoretical results. We choose to run our algorithms in the different high dimensional bandit problems and validate the corresponding regret upper bounds in Corollary 4.1, Corollary 4.2, Corollary 4.3 and Theorem 5.1. For each problem, we plot the cumulative regret as well as , where is the upper bound derived in the specific application. For each setting in each problem, we run the algorithm for 10 independent runs and plot the mean results with one standard deviation error bars.

-

•

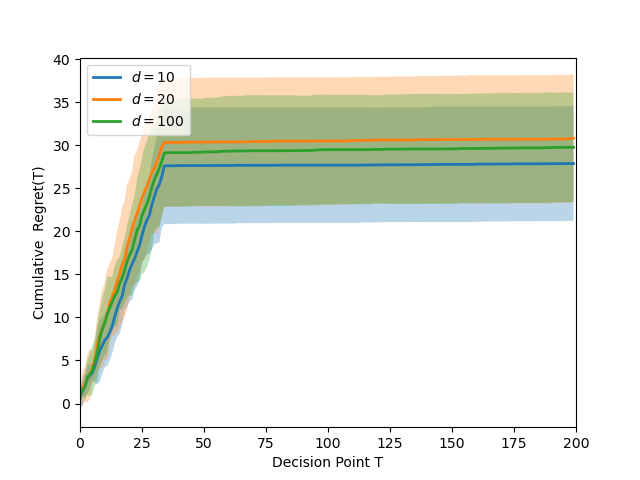

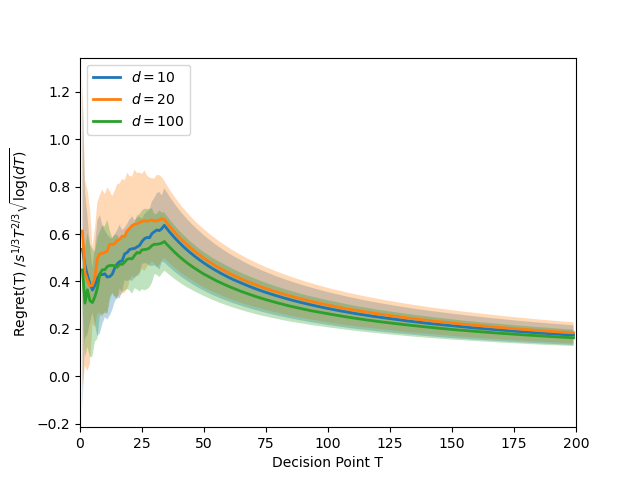

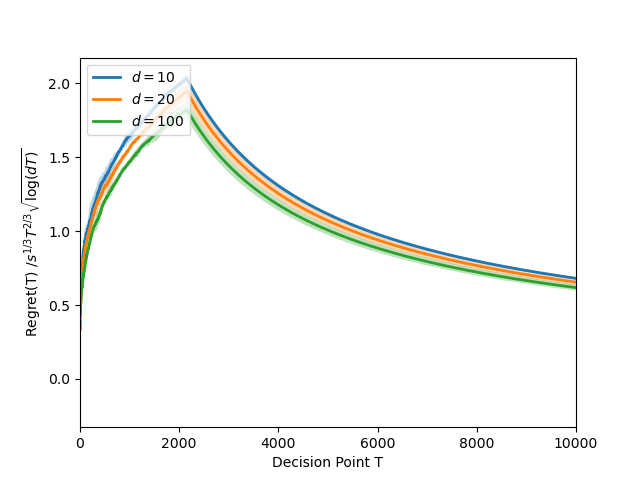

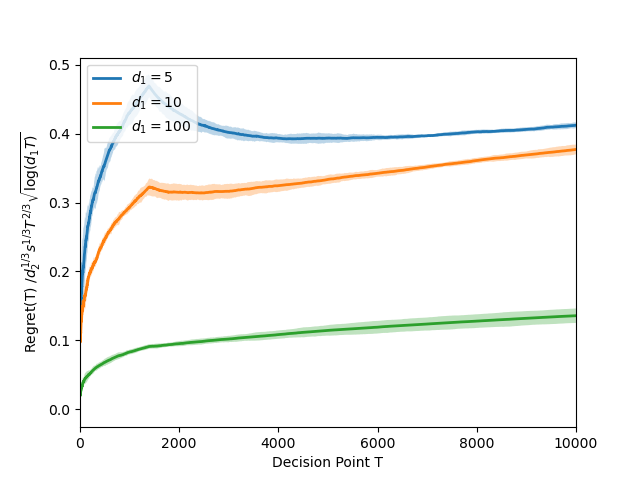

LASSO Bandit. We generate our true by randomly choosing its non-zero indices, and then generate each of its non-zero values uniformly randomly from [0,1] and then perform the normalization. We set so that there are ten different contexts available at each round. The contexts are generated from the zero-mean and identity-covariance normal distribution. We choose three different dimension sizes . The sparsity level is chosen to be in all three settings. The experiment results are shown in Figure 1. As we can observe, the figures show that the regret is at most a constant times , which only depends on the dimension logarithmically and thus satisfies our requirement. Therefore, our bound correctly delineate the order of the regret.

-

•

Low-rank Matrix Bandit. We first randomly generate vectors of dimension , and then we generate our true by randomly choosing its rows from the generated vectors, and thus the matrix is low-rank. We set so that there are ten different contexts available at each round. The contexts are generated from the zero-mean and identity-covariance normal distribution. We choose three different dimension sizes . The rank is chosen to be in all three settings. The experiment results are shown in Figure 2. As we can observe, the figures show that the regret is at most a constant times , which only depends on the dimensions logarithmically and thus satisfies our requirement. Therefore, our bound correctly delineate the order of the regret.

-

•

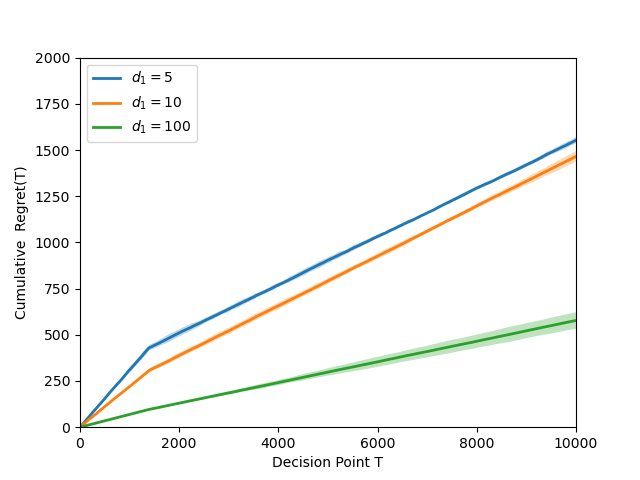

Group-sparse Matrix Bandit. We first randomly generate row indices from the set , where and then we generate our true by setting the selected rows in to be non-zero and generated uniform randomly from . The other rows are set to be zero. We then perform the normalization. We set so that there are ten different contexts available at each round. The contexts are generated from the zero-mean and identity-covariance normal distribution. We choose three different row dimensions . The group-sparsity is chosen to be in all three settings. The experiment results are shown in Figure 3. As we can observe, the figures show that the regret is at most a constant times , which only depends on the dimension logarithmically and thus satisfies our requirement. Therefore, our bound correctly delineate the order of the regret.

In conclusions, all the experimental results validate all our claims in Section 4.