On the Convergence of Step Decay Step-Size for Stochastic Optimization

Abstract

The convergence of stochastic gradient descent is highly dependent on the step-size, especially on non-convex problems such as neural network training. Step decay step-size schedules (constant and then cut) are widely used in practice because of their excellent convergence and generalization qualities, but their theoretical properties are not yet well understood. We provide the convergence results for step decay in the non-convex regime, ensuring that the gradient norm vanishes at an rate. We also provide the convergence guarantees for general (possibly non-smooth) convex problems, ensuring an convergence rate. Finally, in the strongly convex case, we establish an rate for smooth problems, which we also prove to be tight, and an rate without the smoothness assumption. We illustrate the practical efficiency of the step decay step-size in several large scale deep neural network training tasks.

1 Introduction

We focus on stochastic programming problems on the form

| (1) |

Here, is a random variable drawn from some source distribution over an arbitrary probability space and is a closed, convex subset of . This problem is often encountered in machine learning applications, such as training of deep neural networks. Depending the specifics of the application, the function can either nonconvex, convex or strongly convex; it can be smooth or non-smooth; and it may also have additional structure that can be exploited.

Despite the many advances in the field of stochastic programming, the stochastic gradient descent (SGD) method [Robbins and Monro, 1951, Nemirovski et al., 2009] remains important and is arguably still the most popular method for solving (1). The SGD method updates the decision vector using the following recursion

| (2) |

where is an unbiased estimation of the gradient (or subgradient) and is the step-size (learning rate).

The step-size is a critical parameter which controls the rate (or speed) at which the model learns and guarantees that the SGD iterates converge to an optimizer of (1). Setting the step-size too large will result in iterates which never converge; and setting it too small leads to slow convergence and may even cause the iterates to get stuck at bad local minima. As long as the iterates do not diverge, a large constant step-size promotes fast convergence but only to a large neighborhood of the optimal solution. To increase the accuracy, we have to decrease the step-size.

The traditional approach is to decrease the step-size in every iteration, typically as or . Both these step-size schedules have been studied extensively and guarantee a non-asymptotic convergence of SGD [Moulines and Bach, 2011, Lacoste-Julien et al., 2012, Rakhlin et al., 2012, Hazan and Kale, 2014, Shamir and Zhang, 2013, Gower et al., 2019]. However, from a practical perspective, these step-size policies often perform poorly, since they begin to decrease too early. Gower et al. [2019] have proposed to use a constant step-size for the first iterates (where is the condition number) and then shift to a step-size to guarantee convergence for strongly convex functions. However, this strategy requires knowledge of the condition number and is not suitable for the nonconvex setting.

For non-convex problems, such as those which arise in training of deep neural networks, the most popular step-size policy in practice is the step decay step-size [Krizhevsky et al., 2012, He et al., 2016, Huang et al., 2017]. This step-size policy starts with a relatively large constant step-size and then cuts the step-size by a fixed number (called decay factor) at after a given number of epochs. Not only does this step-size result in a faster initial convergence, but it also guarantees that the SGD iterates eventually converge to an exact solution. In Yuan et al. [2019], the step decay step-size (which they call stagewise step decay) was shown to accelerate the convergence of SGD compared to polynomially decay step-sizes, such as and . Ge et al. [2019] prove significant improvements of the step decay step-size over any polynomial decay step-size for least squares problems. In fact, the step decay step-size is the default choice in many deep learning libraries, such as TensorFlow [Abadi et al., 2015] and PyTorch [Paszke et al., 2017]; both use a decay rate of and user-defined milestones when the step-size is decreased. The milestones are often set in advance by experience. If we know some quantities or a certain conditions to characterize when the function is optimized, it will be ideal to decide when to drop the step-size. However, it is hard and time-consuming to get access to these quantities or conditions in practice.

Ge et al. [2019] assume that the SGD algorithm will run for a fixed number of iterations. They then analyze a step decay step-size with decay rate applied every iterations and establish a near-optimal convergence rate for least-squares problems. However, its non-asymptotic convergence for general strongly convex functions, convex functions or nonconvex functions is not analyzed. Motivated by this, in this paper, we focus on SGD with the step decay step-size which uses a general decay factor () rather than the fixed number [Ge et al., 2019, Yuan et al., 2019, Davis et al., 2019a, b]. This is more relevant in practice.

1.1 Main Contributions

This work establishes novel convergence guarantees for SGD with the step decay step-size on smooth (nonconvex), general convex, and strongly convex optimization problems. More precisely, we make the following contributions:

-

•

We propose a non-uniformly probability rule for selecting the output in the nonconvex and smooth setting. Based on this rule,

-

–

we establish a near-optimal rate for SGD with the step decay step-size;

-

–

we improve the results for exponential decay step-size [Li et al., 2020];

-

–

we remove the factor in the best known convergence rate for the classic step-size.

-

–

-

•

For the general convex case, we prove that the step decay step-size at the last iterate can achieve a near-optimal convergence rate (up to a factor).

-

•

For strongly convex problems, we establish the following error bounds for the last iterate under step-decay:

-

–

for smooth problem, which we also prove to be tight;

-

–

without the smoothness assumption.

-

–

1.2 Related Work

For SGD, the best known bound for the expected error of the iterate is of when the objective is convex and smooth with Lipschitz continuous gradient [Nemirovski et al., 2009, Ghadimi and Lan, 2013], and of when the objective is also strongly convex [Moulines and Bach, 2011, Rakhlin et al., 2012]. Without any further assumptions, these rates are known to be optimal. If we restrict our attention to diminshing step-sizes, , the best known error bound for strongly convex and nonsmooth problems is of [Shamir and Zhang, 2013], which is also tight [Harvey et al., 2019a]. This rate can be improved to by averaging strategies [Rakhlin et al., 2012, Lacoste-Julien et al., 2012, Shamir and Zhang, 2013] or a step decay step-size [Hazan and Kale, 2014]. For smooth nonconvex functions, Ghadimi and Lan [2013] established an rate for SGD with constant step-size . Recently, Drori and Shamir [2020] have proven that this error bound is tight up to a constant, unless additional assumptions are made.

The step decay step-size was used for deterministic subgradient methods in Goffin [1977] and Shor [2012]. Recently, it has been employed to improve the convergence rates under various conditions: local growth (convex) [Xu et al., 2016], Polyak-Lójasiewicz (PL) condition [Yuan et al., 2019], sharp growth (nonconex) [Davis et al., 2019a]. Davis et al. [2019b] also apply the step decay scheme to prove the high confidence bounds in stochastic convex optimization. Most of these references consider the proximal point algorithm which introduce a quadratic term to the original problem. In contrast, we study the performance of step decay step-size for standard SGD. Compared to Hazan and Kale [2014] and Yuan et al. [2019], where the inner-loop size is growing exponentially, we use a constant value of , which is known to work better in practice. In the extreme case when , step-decay reduces to the exponentially decaying step-size which Li et al. [2020] have recently studied under the PL condition and a general smoothness assumption.

A number of adaptive step-size selection strategies have been proposed for SGD (e.g., [Duchi et al., 2011, Tieleman and Hinton, 2012, Kingma and Ba, 2015, Loshchilov and Hutter, 2019, Loizou et al., 2020]), some of which result in step-decay policies [Vaswani et al., 2019, Lang et al., 2019, Zhang et al., 2020]. For example, Lang et al. [2019] develop a statistical procedure to automatically determine when the SGD iterates with a constant step-size no longer make progress, and then halve the step-size. Empirically, this automatic scheme is competitive with the best hand-tuned step-decay schedules, but no formal guarantees for this observed behaviour are given.

The remaining part in this paper are organized as follows. Notation and basic definitions are introduced in Section 2. In Section 3, we analyze the convergence rates of step decay step-size on nonconvex case and propose a novel non-uniform sampling rule for the algorithm output. The convergence for general convex and strongly convex functions are investigated in Sections 4 and 5, respectively. Numerical results of our algorithms are presented and discussed in Section 6. Finally, conclusions are made in Section 7.

2 Preliminaries

In this part, we will give some definitions and notations used throughout the paper.

Definition 1.

-

(1)

The stochastic gradient oracle is variance-bounded if for any input vector , the oracle returns a random vector such that .

-

(2)

The stochastic gradient oracle is bounded if for any input vector , the oracle returns a random vector such that for some fixed .

Definition 2 (-smooth).

The function is differentiable and -smooth on if there exists a constant such that . It also implies that for any .

Especially, when is non-differentiable on , we define is -smooth with respect to if with .

The smooth property with respect to has been considered by Rakhlin et al. [2012].

Definition 3 (-strongly convex).

The function is -strongly convex on if with .

Definition 4 (Convex).

The function is convex on if for any and .

Throughout the paper, we assume the objective function is bounded below on and let denote its infimum. If is strongly convex, let be the unique minimum point of and .

Notations: Let denote the set of and without specific mention. We use and to denote the nearest integer to the real number from below and above. For simplicity, we assume that , , , and are all integers.

3 Convergence for Nonconvex Problems

In this section, we provide the first convergence bounds for SGD with step-decay step-sizes on non-convex problems. We also show that our technical approach can be used to improve the best known convergence bounds for both i) standard step-sizes and ii) exponential decay step-sizes.

Before proceeding, it is useful to illustrate the main theoretical novelty that allows us to derive the result. Typically when we study the convergence of SGD for non-convex problems, we analyse a random iterate drawn from with some probability [Ghadimi and Lan, 2013, Ghadimi et al., 2016, Li et al., 2020]. For example, Ghadimi and Lan [2013] provide the following result.

Proposition 3.1.

Suppose that is -smooth on and the stochastic gradient oracle is variance-bounded by . If the step-size , then

| (3) |

where is randomly chosen from with probability . 111 In Ghadimi and Lan [2013], . If is far smaller than , we have . For simplicity, we rewrite the probability as to show the results.

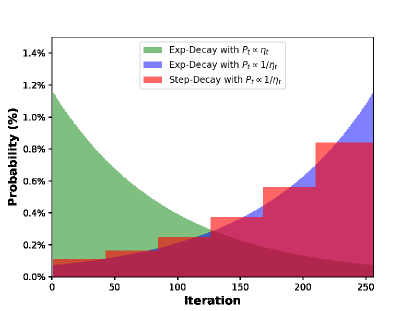

Since is decreasing, means that initial iterates are given higher weights in the average in Equation (3) than the final iterates. This contradicts the intuition that the gradient norm decreases as the algorithm progresses. Ideally, we should do the opposite, i.e. put high weights on the final iterates and low weights on the initial iterates. This is exactly what we do to obtain convergence bounds for step decay step-size: we use the probability instead of . This is especially important when the step-sizes decrease exponentially fast, like in step decay and exponential decay step-sizes. For example, suppose that and . Then with we pick the output from the first 10 iteration with probability. On the other hand, with we pick the output from the last 10 iterations with probability. We illustrate this better in Figure 1.

In the following three subsections we perform such an analysis to 1) provide convergence bounds for step decay step-size (where no bounds existed before) 2) provide improved convergence rate results for exponential decay step-size, and 3) improve the convergence bound for step-size.

3.1 Convergence Rates under the Step Decay Step-size

The step decay step-size (termed Step-Decay) is widely used for training of deep neural networks. This policy decreases the step-size by a constant factor at every iterations; see Algorithm 1. Despite its widespread use, we are unaware of any convergence results for this algorithm in the non-convex regime. Next, we will establish the first such guarantees for an iterate of step decay SGD drawn by the method described above.

In practical deep neural network training, is typically a hyper-parameter selected by experience. To make theoretical statements we must consider a particular choice of . In our theoretical and numerical results we focus on . Note that we can use to obtain the desired . We have the following main result.

Theorem 3.2.

Suppose that the non-convex objective function is -smooth on and upper bounded by 222The function is upper bounded by if for any . and the stochastic gradient oracle is variance-bounded by . If we run Algorithm 1 with , , , and then

where and .

The theorem establishes the first convergence guarantee for step decay step-size on non-convex problems. It ensures a convergence rate towards a stationary point, which is is comparable to the results for step-size in Ghadimi and Lan [2013] or Proposition 3.1. However, as illustrated in our experiments in Section 6, step decay step-size converges faster in practice and tends to find stationary points that generalize better.

In the extreme case when , the step decay policy produces a constant step-size. In this case, Theorem 3.2 matches the existing convergence bounds for SGD in Ghadimi and Lan [2013]. Moreover, in the deterministic case when , Theorem 3.2 yields the standard convergence rate result for deterministic gradient descent [Nesterov, 2004, Cartis et al., 2010, Ghadimi et al., 2016].

A clear advantage of Theorem 3.2 over, e.g., Proposition 3.1, is that it possible to reduce the effect of the noise in the convergence bound by proper parameter tuning. In particular, the following result is easily derived from Theorem 3.2 (proved in the supplementary material).

Corollary 3.3.

If we set , then under the assumptions of Theorem 3.2 we have

The corollary shows us that if we choose in step decay, then the convergence bound will be unaffected by the noise variance . This is in contrast to Proposition 3.1 and step-sizes, where an increased results in a worse upper bound. However, as the proof of Corollary 3.3 reveals, the bound is only tight in the the regime where both noise variance and iteration counts are large.

3.2 A Special Case: Exponentially Decaying Step-Size

An interesting special case occurs when we set in the step decay step-size. In this case, the step-size will decay exponentially, . The first convergence rate results for such step sizes, which we will call Exp-Decay, have only recently appeared in the preprint Li et al. [2020]; we compare our work to those results below.

Clearly, for , the exponential decay factor cannot be chosen arbitrarily: if is too large, then will vanish in only a few iterations. To avoid this, we choose a similar form of the decaying factor as Li et al. [2020] and set , where . The intuition is that at the final iteration the step-size is on the order of (setting ), and thus does not vanish over the iterations. We are now ready to prove the algorithm’s convergence.

Theorem 3.4.

Suppose that the non-convex objective function is -smooth and upper bounded by , and that the stochastic gradient oracle is variance-bounded by . If we run Algorithm 1 with , , , , and , then

where is randomly drawn from with probability . In particular, yields

| (4) |

Theorem 3.4 establishes the convergence of Exp-Decay to a stationary point. With , Exp-Decay yields the rate of , which is comparable to the results in Li et al. [2020]. However, in Li et al. [2020], the -rate is obtained under the (arguably impractical) assumption that the initial step-size is bounded by . This means that the initial step-size will be small if we plan on running the algorithm for a large number of iterations . This is in conflict to the original motivation for using exponentially decaying step-sizes, namely to allow for large initial step-sizes which decrease as the algorithm progresses. On the other hand, our results in Theorem 3.4 only require that the initial step-size is bounded by , which matches the largest fixed step-sizes that ensure convergence.

Another advantage of Theorem 3.4 is that it uses the output probability , instead of as in Li et al. [2020]. As discussed in the beginning of the section (and in Figure 1), means that the output is much more likely to be chosen during the final iterates, whereas with the output is more likely to come from the initial iterates. Therefore, Theorem 3.4 better reflects the actual convergence of the algorithm, since in practice it is typically the final iterate that is used as the trained model. We illustrate this better in our experiments in Section 6.

3.3 Improved Convergence for the Step-Size

The next theorem demonstrates how the idea of using the output distribution instead of can improve standard convergence bounds for step-sizes.

Theorem 3.5.

Suppose that the objective function is -smooth and upper bounded by , and that the stochastic gradient oracle is variance-bounded by . If , then

where is randomly drawn from the sequence with probabilities .

4 Convergence for General Convex Problems

We now establish the first convergence rate results for the step decay step-size in the general convex setting. More specifically, we consider a possibly non-differentiable convex objective function on a closed and convex constraint set . For this problem class, we analyze the projected SGD with step decay step-size detailed in Algorithm 2.

We have the following convergence guarantee:

Theorem 4.1.

Suppose that the objective function is convex on and . The stochastic gradient oracle is bounded by . If we run Algorithm 2 with , , , then we have

where and . Moreover, we have the following bound on the final iterate:

Theorem 4.1 establishes an convergence rate for both the the average objective function value and the objective function value at the final iterate. This convergence rate is comparable to the results obtained for other diminishing step-sizes such as under the same assumptions [Shamir and Zhang, 2013].

5 Convergence for Strongly Convex Problems

We will now investigate the convergence of the step decay step-sizes in the strongly convex case. The algorithm is the same as for general convex problems (Algorithm 2).

5.1 Strongly Convex and -Smooth Functions

We first consider the case when the objective function is strongly convex and -smooth (with respect to ).

Theorem 5.1.

Assume that the objective function is -strongly convex on and the stochastic gradient oracle is bounded by . If we run Algorithm 2 with , , , and , then we have

where and . Further, if the objective function is -smooth with respect to then we can bound the objective function as follows

The theorem provides an theoretical guarantee for the last iterate under step decay step-size.333Note that for all and converges to as goes to infinity. This bound matches the convergence rate of Ge et al. [2019] for strongly convex least squares problems. Therefore, Theorem 5.1 can be considered a generalization of the result in Ge et al. [2019] to general smooth and strongly convex problems.

Under some step-sizes, e.g. , it is possible to get an convergence rate for SGD for smooth and strongly convex problems Moulines and Bach [2011], Rakhlin et al. [2012], Hazan and Kale [2014]. However, our next result shows that the rate in Theorem 5.1 is tight for Algorithm 2.

Theorem 5.2.

Consider Algorithm 2 with and . For any and , there exists a function , where , that is both 1-strongly convex and 1-smooth such that

with probability at least , where .

5.2 Strongly Convex and Non-Smooth Functions

For general, not necessarily smooth, strongly convex functions we have the following result.

Theorem 5.3.

Suppose that the objective function is -strongly convex on and the stochastic gradient oracle is bounded by . If we run Algorithm 2 with , , , and , then we have

where , , , , .

The theorem shows that even without the smoothness assumption, we can still ensure convergence at the rate . We can improve the rate to with an averaging technique, as illustrated next.

6 Numerical Experiments

In this section, we evaluate the practical performance of step decay step-size and compare it against the following popular step-size policies: 1) constant step-size, ; 2) step-size, ; 3) step-size ; 4) Exp-Decay Li et al. [2020], with for . In each experiment, we perform a grid search to select the best values for the free parameters as well as for the step decay step-size parameter . More details about the relationship between the different step-size policies are given in the supplementary material.

6.1 Experiments on MNIST with Neural Networks

First, we consider the classification task on MNIST database of handwritten digits444http://yann.lecun.com/exdb/mnist/ using a fully-connected 2-layer neural network with 100 hidden nodes (784-100-10).

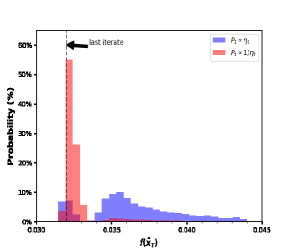

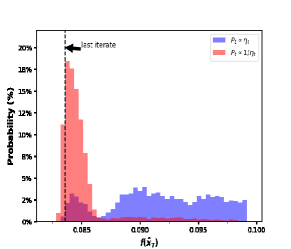

The last iterate is usually chosen as the output of each algorithm in practice. The theoretical output (in Theorem 3.2) is drawn from all the previous iterates with probability . To get an insight into the relationship between the last iterate and theoretical output in Theorem 3.2, we randomly choose 6000 iterates (10% of the total iterates) with probability , record their exact training loss and testing loss, and calculate the probabilities (shown in Figure 2). We can see that the theoretical output can reach the results of the last iterate with high probability, no matter training loss or testing loss.

In the same way, in order to show the advantages of probability over , we also implement Step-Decay with probability in Figure 2. We can see that the output with probability is more concentrated at the last phase and has a higher probability, especially, in terms of loss, compared to the result of probability .

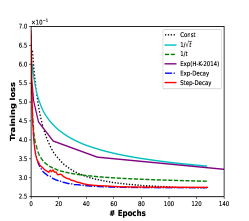

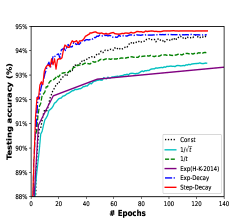

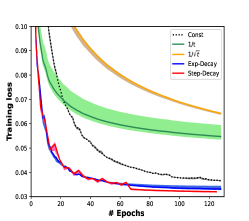

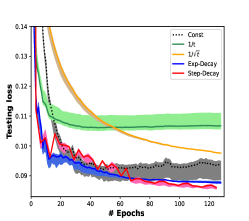

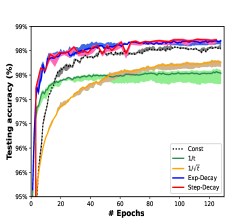

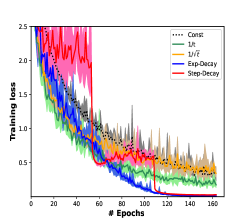

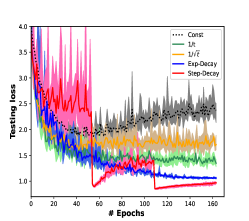

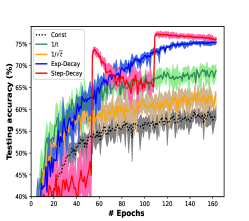

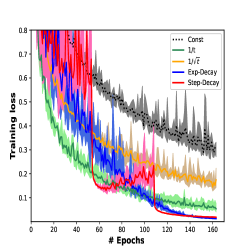

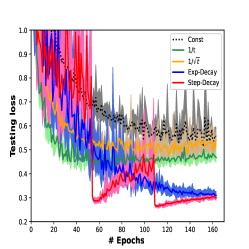

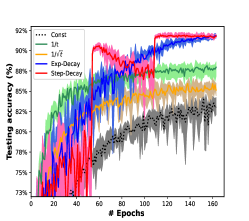

The performance of the various step-size schedules is shown in Figure 3. It is observed that Exp-Decay and Step-Decay performs better than other step-sizes both in loss (training and testing) and testing accuracy. Step-Decay has an advantage over Exp-Decay in the later stages of training where it attains a lower training and testing loss.

6.2 Experiments on CIFAR10 and CIFAR100

To illustrate the practical implications of the step decay step-size, we perform experiments with deep learning tasks on the CIFAR555https://www.cs.toronto.edu/~kriz/cifar.html dataset. We will focus on results for CIFAR100 here, and present complementary results for CIFAR10 in the supplementary material. To eliminate the influence of stochasticity, all experiments are repeated 5 times.

We consider the benchmark experiments for CIFAR100 on a 100-layer DenseNet [Huang et al., 2017]. We employ vanilla SGD without dampening and use a weight decay of 0.0005. The optimal step-size and algorithm parameters are selected using a grid search detailed in the supplementary material. The results are shown in Figure 4. We observe that Step-Decay achieves the best results in terms of both testing loss and testing accuracy, and that it is also fast in reaching a competitive solution. Another observation is that as the iterates proceeds in each phase, its testing loss and accuracy is getting worse because its generalization ability is weakened. Therefore, deciding when to stop the iteration or reduce the step-size is important.

Finally, we compare the performance of Exp-Decay and Step-Decay on Nesterov’s accelerated gradient (NAG) [Nesterov, 1983, Sutskever et al., 2013] and other adaptive gradient methods, including AdaGrad [Duchi et al., 2011], Adam [Kingma and Ba, 2015] and AdamW [Loshchilov and Hutter, 2019]. The results are shown in Table 1. All the parameters involved in step-sizes, algorithms, and models are best-tuned (shown in supplementary material). The shows 95% confidence intervals of the mean accuracy value over 5 runs. We can see that compared to the Exp-Decay step-size, Step-Decay can reach higher testing accuracy on Adam, AdamW and NAG. We therefore beleieve that Step-Decay step-size is more likely to be extended and applied to other methods.

| Method | CIFAR100-DenseNet |

|---|---|

| Testing accuracy | |

| AdaGrad | 0.6197 0.00518 |

| Adam + Exp-Decay | 0.6936 0.00483 |

| Adam + Step-Decay | 0.7041 0.00971 |

| AdamW + Exp-Decay | 0.7165 0.00353 |

| AdamW + Step-Decay | 0.7335 0.00261 |

| NAG + Exp-Decay | 0.7531 0.00606 |

| NAG + Step-Decay | 0.7568 0.00156 |

6.3 Experiments on Regularized Logistic Regression

We now turn our attention to how the step-decay step-size and other related step-sizes behave in the strongly convex setting. We consider the regularized logistic regression problem on the binary classification dataset rcv1.binary () from LIBSVM 666https://www.csie.ntu.edu.tw/~cjlin/libsvmtools/datasets/, where a 0.75 partition is used for training and the rest is for testing.

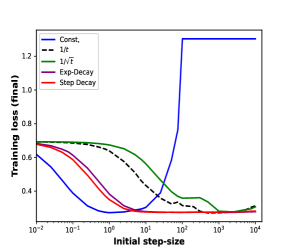

Figure 5(a) shows how a constant step-size has to be well-tuned to give good performance: if we choose it too small, convergence will be painstakingly slow; if we set it too large, iterates will stagnate or even diverge. This effect is also visualized in blue in Figure 5(b), where only a narrow range of values results in a low training loss for the constant step-size. In contrast, the initial step-size of both Exp-Decay and Step-Decay can be selected from a wide range () and still yield good results in the end. In other words, Exp-Decay and Step-Decay are more robust to the choice of initial step-size than the alternatives. A more thorough evaluation of all the considered step-sizes on logistic regression can be found in Supplementary D.3.

7 Conclusion

We have provided theoretical guarantees for SGD under the step decay family of step-sizes, widely used in deep learning. Our first results established a near-optimal rate for step decay step-sizes in the non-convex setting. A key step in our analysis was to use a novel non-uniform probability distribution for selecting the output of the algorithm. We showed that this approach allows to improve the convergence results for SGD under other step-sizes as well, e.g., by removing the term in the best known convergence rate for step-sizes. Moreover, we established near-optimal (compared to the min-max rate) convergence rates for general convex, strongly convex and smooth, and strongly convex and nonsmooth problems. We illustrated the superior performance of step-decay step-sizes for training of large-scale deep neural networks. In the experiments, we observed that as the iterates proceeding in each phase, their generalization abilities are getting worse. Therefore, it will be an interesting to study how to best select the size of inner-loop (instead of constant or exponentially growing) to avoid the loss of generalization.

References

- Abadi et al. [2015] M. Abadi, A. Agarwal, P. Barham, E. Brevdo, Z. Chen, C. Citro, G. Corrado, A. Davis, J. Dean, M. Devin, et al. Tensorflow: Large-scale machine learning on heterogeneous distributed systems. Software available from tensorflow.org, 2015.

- Cartis et al. [2010] C. Cartis, N. I. Gould, and P. L. Toint. On the complexity of steepest descent, newton’s and regularized newton’s methods for nonconvex unconstrained optimization problems. SIAM Journal on Optimization, 20(6):2833–2852, 2010.

- Davis et al. [2019a] D. Davis, D. Drusvyatskiy, and V. Charisopoulos. Stochastic algorithms with geometric step decay converge linearly on sharp functions. arXiv:1907.09547, 2019a.

- Davis et al. [2019b] D. Davis, D. Drusvyatskiy, L. Xiao, and J. Zhang. From low probability to high confidence in stochastic convex optimization. arXiv:1907.13307, 2019b.

- Drori and Shamir [2020] Y. Drori and O. Shamir. The complexity of finding stationary points with stochastic gradient descent. In International Conference on Machine Learning, pages 2658–2667. PMLR, 2020.

- Duchi et al. [2011] J. Duchi, E. Hazan, and Y. Singer. Adaptive subgradient methods for online learning and stochastic optimization. Journal of Machine Learning Research, 12(Jul):2121–2159, 2011.

- Ge et al. [2019] R. Ge, S. M. Kakade, R. Kidambi, and P. Netrapalli. The step decay schedule: A near optimal, geometrically decaying learning rate procedure for least squares. In Advances in Neural Information Processing Systems, pages 14977–14988, 2019.

- Ghadimi and Lan [2013] S. Ghadimi and G. Lan. Stochastic first-and zeroth-order methods for nonconvex stochastic programming. SIAM Journal on Optimization, 23(4):2341–2368, 2013.

- Ghadimi et al. [2016] S. Ghadimi, G. Lan, and H. Zhang. Mini-batch stochastic approximation methods for nonconvex stochastic composite optimization. Mathematical Programming, 155(1-2):267–305, 2016.

- Goffin [1977] J.-L. Goffin. On convergence rates of subgradient optimization methods. Mathematical Programming, 13(1):329–347, 1977.

- Gower et al. [2019] R. M. Gower, N. Loizou, X. Qian, A. Sailanbayev, E. Shulgin, and P. Richtárik. SGD: General analysis and improved rates. In International Conference on Machine Learning, pages 5200–5209. PMLR, 2019.

- Harvey et al. [2019a] N. J. Harvey, C. Liaw, Y. Plan, and S. Randhawa. Tight analyses for non-smooth stochastic gradient descent. In Conference on Learning Theory, pages 1579–1613. PMLR, 2019a.

- Harvey et al. [2019b] N. J. Harvey, C. Liaw, and S. Randhawa. Simple and optimal high-probability bounds for strongly-convex stochastic gradient descent. arXiv:1909.00843, 2019b.

- Hazan and Kale [2014] E. Hazan and S. Kale. Beyond the regret minimization barrier: optimal algorithms for stochastic strongly-convex optimization. Journal of Machine Learning Research, 15(1):2489–2512, 2014.

- He et al. [2016] K. He, X. Zhang, S. Ren, and J. Sun. Deep residual learning for image recognition. In Proceedings of the IEEE conference on computer vision and pattern recognition, pages 770–778, 2016.

- Huang et al. [2017] G. Huang, Z. Liu, L. Van Der Maaten, and K. Q. Weinberger. Densely connected convolutional networks. In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, pages 4700–4708, 2017.

- Kingma and Ba [2015] D. P. Kingma and J. L. Ba. ADAM: A method for stochastic optimization. In International Conference on Learning Representations, 2015.

- Klein and Young [2015] P. Klein and N. E. Young. On the number of iterations for dantzig–wolfe optimization and packing-covering approximation algorithms. SIAM Journal on Computing, 44(4):1154–1172, 2015.

- Krizhevsky et al. [2012] A. Krizhevsky, I. Sutskever, and G. E. Hinton. Imagenet classification with deep convolutional neural networks. In Advances in Neural Information Processing Systems, pages 1106–1114, 2012.

- Lacoste-Julien et al. [2012] S. Lacoste-Julien, M. Schmidt, and F. Bach. A simpler approach to obtaining an convergence rate for the projected stochastic subgradient method. arXiv:1212.2002, 2012.

- Lang et al. [2019] H. Lang, L. Xiao, and P. Zhang. Using statistics to automate stochastic optimization. In Advances in Neural Information Processing Systems, pages 9540–9550, 2019.

- Li et al. [2020] X. Li, Z. Zhuang, and F. Orabona. A second look at exponential and cosine step sizes: Simplicity, convergence, and performance. arXiv:2002.05273, 2020.

- Loizou et al. [2020] N. Loizou, S. Vaswani, I. Laradji, and S. Lacoste-Julien. Stochastic Polyak step-size for SGD: A adaptive learning rate for fast convergence. arXiv:2002.10542, 2020.

- Loshchilov and Hutter [2019] I. Loshchilov and F. Hutter. Decoupled weight decay regularization. In International Conference on Learning Representations, 2019.

- Moulines and Bach [2011] E. Moulines and F. R. Bach. Non-asymptotic analysis of stochastic approximation algorithms for machine learning. In Advances in Neural Information Processing Systems, pages 451–459, 2011.

- Nemirovski et al. [2009] A. Nemirovski, A. Juditsky, G. Lan, and A. Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM Journal on Optimization, 19(4):1574–1609, 2009.

- Nesterov [2004] Y. Nesterov. Introductory lectures on convex optimization: A basic course, volume 87. Springer Science & Business Media, 2004.

- Nesterov [1983] Y. E. Nesterov. A method for solving the convex programming problem with convergence rate o (1/k^ 2). In Dokl. akad. nauk Sssr, volume 269, pages 543–547, 1983.

- Paszke et al. [2017] A. Paszke, S. Gross, S. Chintala, G. Chanan, E. Yang, Z. DeVito, Z. Lin, A. Desmaison, L. Antiga, and A. Lerer. Automatic differentiation in PyTorch. In NIPS 2017 Autodiff Workshop: The Future of Gradient-based Machine Learning Software and Techniques, Long Beach, CA, US, 2017.

- Rakhlin et al. [2012] A. Rakhlin, O. Shamir, and K. Sridharan. Making gradient descent optimal for strongly convex stochastic optimization. In International Conference on Machine Learning, pages 1571–1578, 2012.

- Robbins and Monro [1951] H. Robbins and S. Monro. A stochastic approximation method. The Annals of Mathematical Statistics, pages 400–407, 1951.

- Shamir and Zhang [2013] O. Shamir and T. Zhang. Stochastic gradient descent for non-smooth optimization: Convergence results and optimal averaging schemes. In International Conference on Machine Learning, pages 71–79, 2013.

- Shor [2012] N. Z. Shor. Minimization methods for non-differentiable functions, volume 3. Springer Science & Business Media, 2012.

- Sutskever et al. [2013] I. Sutskever, J. Martens, G. Dahl, and G. Hinton. On the importance of initialization and momentum in deep learning. In International Conference on Machine Learning, pages 1139–1147. PMLR, 2013.

- Tieleman and Hinton [2012] T. Tieleman and G. Hinton. Lecture 6.5-rmsprop, coursera: Neural networks for machine learning. Technical Report, University of Toronto, 2012.

- Vaswani et al. [2019] S. Vaswani, A. Mishkin, I. Laradji, M. Schmidt, G. Gidel, and S. Lacoste-Julien. Painless stochastic gradient: Interpolation, line-search, and convergence rates. In Advances in Neural Information Processing Systems, 2019.

- Xu et al. [2016] Y. Xu, Q. Lin, and T. Yang. Accelerated stochastic subgradient methods under local error bound condition. arXiv:1607.01027, 2016.

- Yuan et al. [2019] Z. Yuan, Y. Yan, R. Jin, and T. Yang. Stagewise training accelerates convergence of testing error over SGD. Advances in Neural Information Processing Systems, 32:2608–2618, 2019.

- Zhang et al. [2020] P. Zhang, H. Lang, Q. Liu, and L. Xiao. Statistical adaptive stochastic gradient methods. arXiv:2002.10597, 2020.

Supplementary Material for "On the Convergence of Step Decay Step-Size for Stochastic Optimization"

A. Proofs of Section 3

Before presenting the proofs of Section 3, we state and prove the following useful lemma.

Lemma 7.1.

Suppose that is -smooth on and the stochastic gradient oracle is variance-bounded by . If , consider the SGD algorithm, we have

Proof.

Recall the SGD iterations , where . By the smoothness of on , we have

| (5) |

The stochastic gradient oracle is variance-bounded by , i.e., . Taking expectation on both sides of (5) and applying and the variance-bounded assumption gives

| (6) |

where the second inequality follows the fact that gradient is unbiased (). We thus have that

Since , we have . Using this inequality, shifting to the left side, and re-arranging (6) gives

∎

Proof.

Proof.

(of Theorem 3.2) In this case, we analyze the convergence of Algorithm 1 with and . Invoking the result of Lemma 7.1, at the current iterate , the following inequality holds:

Dividing both sides by yields

| (8) |

At each inner phase for , the step-size is a constant. Applying (8) repeatedly for gives

| (9) |

Since the output of Algorithm 1 is randomly chosen from all previous iterates with probability ,

| (10) |

By the update rule in Algorithm 1, the last point of the loop is the starting point of the next loop, i.e., for each . Applying the assumption that the objective function is upper bounded by for all ,

Plugging this inequality into (10) and substituting and , we obtain that

Therefore, by changing the base of to be natural logarithm, the theorem is proved. ∎

Proof.

(of Theorem 3.4) Based on Lemma 7.1, at the current iterate , we have

Dividing the above inequality by and summing over to gives

| (11) |

Applying the assumption that the objective function is upper bounded by and recalling the definition of the exponential decay step-size [Li et al., 2020], i.e., where and , we find

| (12) |

Next, we estimate the sum of from to :

| (13) |

where the last inequality follows from the fact that for all .

Proof.

(of Theorem 3.5) In this case, we consider the diminishing step-size . By Lemma 7.1:

| (14) |

In the same way as Theorems 3.2 and 3.4, we divide (14) by and sum over to to obtain

| (15) |

Recalling that the output is randomly chosen from the sequence with probability and applying (Proof.), yields

where the last inequality holds because . The proof is complete. ∎

B. Proofs of Section 4

Proof.

(of Theorem 4.1) The convexity of yields for any , where . Also, by convexity of , we have for any points and . Using these inequalities and applying the assumption that the stochastic gradient oracle is bounded by , i.e., , for any , we have

| (16) |

Shifting to the left side gives

| (17) |

Now, consider the final phase (let ) and and apply (17) recursively from to to obtain

| (18) |

Combining the assumption that for some finite with the expression for the step-size in the final phase, , we have

| (19) |

We have thus proven the first part of Theorem 4.1. Next, based on the above results, we prove the error bound for the last iterate. We focus on the last phase and apply (17) recursively from to to find

| (20) |

Introduce . Inequality (20) implies that

| (21) |

By the definition of , we have . Using this formula and applying (21) gives

Dividing by , we get

Using the above inequality repeatedly for , we have

| (22) |

Recalling the definition of and applying (19) into the above inequality, we obtain

The proof is complete. ∎

C. Proofs of Section 5

Proof.

(of Theorem 5.1 ) In this case, we consider the step decay step-size (see Algorithm 2) with and . By the -strongly convexity of on , we have

| (23) | ||||

| (24) |

Due to the fact that minimizes on , we have for all and . In particular, for we have . Plugging this into (24) and re-arranging (23) and (24) gives

| (25) |

By the convexity of , we have for any and . Then applying the update rule of Algorithm 2 and using these inequalities gives

| (26) |

where the third inequality follows from the stochastic gradient oracle is bounded by , i.e., satisfies that and . In this case, the time horizon is divided into phases and each is of length . Recursively applying (26) from to in the phase and using the assumption gives

| (27) |

Repeating the recursion (27) from to , we get

| (28) |

where the second inequality follows from the fact that for any and . Recalling the formula for the step decay step-size, in the phase, and that and , we can estimate the two sums that appear in (28) as follows:

Using these inequalities in (28) gives

| (29) |

Next, we turn to bound the right-hand side of (29). Let . If , we prefer to divide the second term into two parts. First, we estimate this term for :

| (30) |

where the third inequality uses that . Next, we estimate the term for :

| (31) |

where the second inequality uses that . Incorporating (30) and (31) into (29) gives

Changing the base of to the natural logarithm, that is , we arrive at the desired result. ∎

Before proving the lower bound of Algorithm 2, we state an utility lemma.

Lemma 7.2.

[Klein and Young, 2015] Let be independent random variables taking values uniformly from and . Suppose , then

The lemma was proposed by Klein and Young [2015] (see lemma 4) to show the tightness of the Chernoff bound. Recently it has been used to derive a high probability lower bound of the step-size [Harvey et al., 2019b]. We will now use Lemma 7.2 to prove the following high probability lower bound of the step decay scheme in Algorithm 2 for .

Proof.

(of Theorem 5.2) We consider the one-dimensional function , where . This function is -strongly convex and -smooth on . For any point , the gradient oracle will return a gradient where . We apply the step decay step-size with to using and . Then the last iterate satisfies

| (32) |

Letting , we have that and . For and , we pick . Then the final iterate can be estimated as

For , it holds that for all . Define where is uniformly chosen from . Then for any . Hence, this gradient oracle satisfies the assumptions. Now,

| (33) |

Invoking Lemma 7.2 with and gives

| (34) |

with probability at least . Since we know the optimal function value , the the desired high probability lower bound follows.∎

Proof.

(of Theorem 5.3) Recalling the iterate updates of Algorithm 2, for any , we have

| (35) |

where the second inequality follows since for any and the third inequality follows from the fact that the gradient oracle is bounded and unbiased. In the following analysis, we focus on the final phase, that is . Let be the integer in . Extracting the inner product and summing over all from to gives

| (36) |

By the convexity of on , we have . Plugging this into (36), we get

| (37) |

We pick in (37) to find

| (38) |

Let which is the average of the expected function values at the last iterations of the final phase . The above inequality implies that

By the definition of , we have and . Using these formulas and applying (38) gives

which, after dividing by , yields

Applying the above inequality recursively for , we get

| (39) |

It only remains to estimate . At the phase, the iterate starts from . We pick and in (37) so that

| (40) |

Note that in order to estimate , we have to bound first. From inequality (28) of Theorem 5.1, we know that the distance between the starting point of the phase and can be bounded as follows:

| (41) |

We now follow the proof of Theorem 5.1 to estimate . Substituting the step-size for , and , we have

Therefore, using these inequalities in (41) gives

Incorporating the above results and substituting and into (39), we have

By changing the base of to be natural logarithm, i.e., , the proof is finished. ∎

Proof.

(of Theorem 5.4) Recall inequality (35) in the proof of Theorem 5.3: for any it holds that

By the convexity of , we have , so the above inequality implies that

| (42) |

Let and . By applying (42) repeatedly and summing over all and , we have

| (43) |

Let

Since is convex and each iterate belongs to , we have . By the convexity of and (43) it then follows that

| (44) |

Next, we turn to estimate . By (28) with , we have

| (45) |

Next, we estimate the summation of from to

| (46) |

Incorporating (46) into the second term of (45) gives

| (47) |

where the inequality follows from the fact that . Letting in (46), we have

| (48) |

Plugging (47) and (48) into (45), we get

| (49) |

Incorporating (49) into (44) and using and gives

which concludes the proof. ∎

D. The Details of the Setup in Numerical Experiments

In this section, we provide some details for the numerical experiments in Section 6 and give some complementary experimental results.

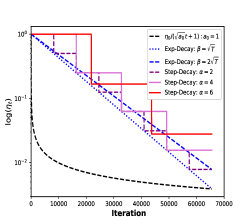

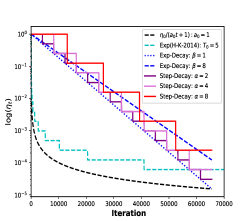

To better understand the relationship between all the considered step-sizes, we draw Figure 6 to show the step-size (-axis is ) versus the number of iterations (starting from the same initial step-size). In the left picture, we show the many step-sizes, studied in Sections 6.1 and 6.2, which finally reach the order of for the nonconvex and convex cases. In the strongly convex case (the right picture), we show the step-sizes which are based on the order of . We also add yet another kind of exponentially decaying step-size (called Exp(H-K-2014)) proposed by Hazan and Kale [2014]: , and , where .

From Figure 6(a), we observe that Exp-Decay for can be regarded as a lower bound of Step-Decay. From another viewpoint, we can see that when the decay factor is very close to 1, the proposed Step-Decay will reduce to Exp-Decay for . A similar relationship can also be observed from Figure 6(b).

D.1 The Details of the Experiments on MNIST

The MNIST dataset consists of a training set of 60,000 examples and a testing set of 10,000 examples. We train MNIST on a fully connected two-layer network (784-100-10). The regularization parameter is and the mini-batch size is 128. We run 128 epochs, which implies that the number of iterations is equal to the training size .

In order to fairly compare the considered step-sizes, the initial step-size is chosen from the search grid . For and , the initial step-size is , and is tuned by searching for the final step-size over the grid ; in our experiments, it turned out that the best value of was 0.01. The best initial step-size was found to be for both Exp-Decay and Step-Decay. Similarly, the parameter for Exp-Decay is selected to make sure that its final step-size is tuned over the grid ; the best tuning of was found to be 0.05. For Step-Decay, the decay factor is empirically chosen from an interval and the search grid is in units of 1 after . The outer-loop size is which is numerically better than its ceil. The best choice was found to be ().

D.2 The Details of the Experiments on CIFAR10 and CIFAR100

The benchmark datasets CIFAR10 and CIFAR100 both consist of 60000 colour images (50000 training images and the rest 10000 images for testing). The maximum epochs called for the two datasets is 164 and batch size is .

First, we employ a 20-layer Resident Network model [He et al., 2016] called ResNet20 to train CIFAR10. We use vanilla SGD without dampening and a weight-decay of 0.0005. The hyper-parameters are selected to work best according to their performance on the test dataset.

For all evaluated step-sizes, the initial step-size . For the constant step-size, the best choice was achieved by . For the step-size, the initial step-size and the parameter is tuned such that reaches the search grid (the grid search yielded ). We tuned the step-size in the same way as the step-size: the initial step-size and . For Exp-Decay, and is chosen such that the final step-size reaches the search grid for step-size (resulting in ). For Step-Decay, the best initial step-size is achieved at and .

The numerical results on CIFAR10 is shown in Figure 7. We can see that the sudden jumps in step-size helps the algorithm to get a lower testing loss and higher accuracy (red curve) compared to other step-sizes.

Next, we give the details about how to select the optimal values of the parameters, , and for CIFAR100. The initial step-size is chosen from for all step-sizes. For the constant step-size, we found and a weight-decay of 0.0001. For the step-size, and was set such that is searched over the grid above, which yielded . For , and is set to make sure that is tuned from the set for step-size, resulting in . For Exp-Decay, and is chosen such that reaches the grid (resulting in ). For the Step-Decay, the initial step-size and the decay factor .

Next, we detail the parameters tuning for the algorithms in Table 1. The maximum epochs called was 164 and the batch size was 128. This implies that . The weight-decay was set to 0.0005 for Adam and NAG. The best initial step-size for AdaGrad was found to be (weight-decay is 0); For Adam, we found the parameters ()=(0.9, 0.99). The weight-decay was set to 0.025 for AdamW while the other parameters were the same as for Adam. For NAG, the momentum parameter was set to 0.9. For Exp-Decay: the best-tuned was and for NAG; and for Adam and AdamW; For Step-Decay: the optimal was found to be 6 for all methods including Adam, AdamW and NAG while the best for NAG and for Adam and AdamW.

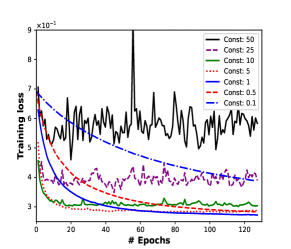

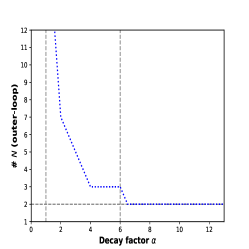

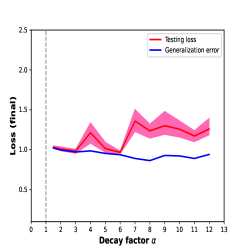

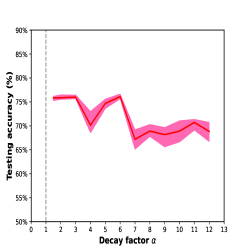

In Figure 8(a), we show how the number of outer-loop iterations changes with the decay factor . The decay factor is an important hyper-parameter for Step-Decay. To figure out the decay factor affects the performance, we plot the testing loss and generalization error (the absolute value of the difference between training loss and testing loss), as well as the testing accuracy in Figures 8(b) and 8(c), respectively. All results are repeated 5 times. The best choice of the decay factor is found to be , according to the best performance on testing loss and accuracy. It is observed that performs better and is more stable than . The main reason is that the length of each phase for is larger than that of so that it loses its advantages in the end (the generalization is weakened). Moreover, suppose that the number of outer-loop iterations is fixed, for example at (where ) or (where ), we can see that the testing loss is getting better if we increase the decay factor.

D.3 Numerical Details for Regularized Logistic Regression

In this part, we present the numerical results for all considered step-sizes on regularized logistic regression. The initial step-size is best-tuned from the search grid for all step-sizes. For the constant step-size, the initial step-size is . For , , Exp(H-K-2014), Exp-Decay [Li et al., 2020] and Step-Decay, the initial step-size is 10. We tune for and step-sizes such that the final step-size is searched over the grid (). Similarly, the parameter of Exp-Decay [Li et al., 2020] is chosen such that is searched over the grid (). The initial period for Exp(H-K-2014) is . For Step-Decay, the decay factor is chosen to be .

Compared to the polynomially diminishing step-sizes (e.g. , ), we can observe that Exp-Decay and Step-Decay not only yields rapid improvements initially, but they also converge to a good solution in the end.