A New Method to Determine the Presence of Continuous Variation in Parameters of Biological Growth Curve Models

Abstract

Quantitative assessment of the growth of biological organisms has produced many mathematical equations and over time it has become an independent research area. Many efforts have been given on statistical identification of the correct growth model from a given data set. This generated several model selection criteria as well. Every growth equation is unique in terms of mathematical structures; however, one model may serve as a close approximation of the other by appropriate choice of the parameter(s). It is still a challenging problem to select the best estimating model from a set of models whose shapes are similar in nature. Our efforts in this manuscript are to reduce the efforts in model selection by utilizing an existing model selection criterion in an innovative way that reduces the number of model fitting exercises substantially. In this manuscript, we have shown that one model can be obtained from the other by choosing a suitable continuous transformation of the parameters. This idea builds an interconnection between many equations that are available in the literature. As the by product of this exercise, we also get several new growth equations, out of them large number of equations can be obtained from a few key models. Given a set of training data points and the key models, we utilized the idea of interval specific rate parameter (ISRP) proposed by Bhowmick et al. (2014) to obtain a suitable mathematical model for the data. The ISRP profile of the parameters of simpler models indicates the nature of variation in parameters with time, thus, enable the experimenter to extrapolate the inference to more complex models. Our proposed methodology significantly reduced the efforts involved in model fitting exercises. Connections have been built amongst many growth equations, which were studied independently to date by researchers. We believe that this work would be helpful for practitioners in the field of growth study. The proposed idea is verified by using simulated and real data sets. In addition, theoretical justifications have been provided by investigating the statistical properties of the estimators.

keywords:

Relative growth rate , Interval specific rate parameter , Parameter estimation , Multivariate delta method , Parameter sensitivity.1 Introduction

Growth curve models serve as the mathematical framework for the qualitative studies of growth in many areas of applied science and due to its extensive use in the recent studies several new models were developed over a long period of time (Tsoularis and Wallace, 2002; Bhowmick et al., 2014). There are many important applications of such models, viz. modelling of physiological age of animal or group of animals with respect to time (Bridges et al., 2000); study of growth comparison for different genotypes with respect to an expected growth behaviour (Perotto et al., 1992); predicting the extinction pattern in natural populations (Bhowmick et al., 2015). In the growth curve analysis the parameters in the model are assumed to be fixed but unknown quantity. So if , represents a growth process, then the parameter (scalar or vector valued) is assumed to be a constant; is size at time . The parameters are estimated by using non-linear least squares method that provides the confidence interval based on -distribution. However, it might happen that the parameter is not fixed and vary with respect to time (Banks, 1994). Now the problem is, if the experimenter has observed data over a time period then there is an uncertainty about the parameter being fixed or varying with time. Even if the information is known (from the biological theory) that a particular model parameter varies with time, but it’s empirical estimation is a difficult task. The goal of this manuscript: (1) to revisit the theory of parameter variation in the context of growth curve models and demonstrate its importance in growth curve analysis; (2) to develop statistical methods to detect whether any parameters of the growth model has undergone continuous variation with time by using the data; (3) To develop an appropriate way for the best model selection to obtain better insights about the growth process.

To understand the research problem, studied in this paper, we consider the exponential model as the test bed. The exponential growth model is given by , where is the rate parameter. Now, suppose if we artificially simulate observations using the gompertz growth model and plot the corresponding RGR values (logged difference in ’s) against time. The scatterplot would appear to be a monotonically decreasing function of time. Given the mathematical relationship between gompertz and exponential model, the scatterplot can be described “as an exponential model with continuously decaying rate parameter ”. Fortunately, the inter-relation between exponential and gompertz is known (Banks, 1994; Kot, 2001). Hence, it can be easily guessed that the parameter is decreasing with time. Thus, looking into the behaviour of RGR, we can guess whether the parameter is varying or not. The nature or pattern of variation in with time allow us to choose the correct continuous function . The problem is that such inter-relations are very difficult to be identified between growth models and may become mathematically cumbersome as well. Hence, it is difficult to identify the type of variation in the parameter empirically, and most importantly, difficulty in choosing the final transformed model after the type of variation being considered in the parameter. The problem becomes more difficult if multiple parameters are present in the model and one or few of them vary with time. In this paper, we attempt to solve this problem with the help of Interval Specific Rate Parameter (ISRP) proposed by Bhowmick et al. (2014), which is briefly discussed later in this manuscript.

The organization of the rest of the paper is as follows: In Section 2, we briefly describe the development of extended families of growth models by varying parameters. Then in Section 3, we introduce the concept of continuously varying parameters in four different models, namely exponential, logistic, theta-logistic and confined exponential. Also we explore possible connections between growth models by varying parameters continuously. The statistical properties of ISRP of the model parameters with a simulation study for parameters of logistic growth model and their continuous variation is described in Section 4. In Section 5, the utility of proposed method has been demonstrated by using three real life data sets, namely (a) cattle growth data (Kenward, 1987), (b) cumulative sales of LCD-TV data (Trappey and Wu, 2008) and (c) cumulative number of COVID-19 cases for Germany (https://ourworldindata.org/coronavirus). Lastly we conclude the discussion with some remarks and possible future directions. The mathematical form of distribution of ISRP of the parameters for some growth models have been provided in the appendix.

2 Literature survey

In the literature, the idea of considering a continuously varying parameters with time probably dated back to the study of experimental data by Utida (1957) in a host-parasitoid system. Turner et al. (1969) were the first one to consider an explicit time dependent function for the carrying capacity in the logistic growth model (Verhulst, 1838). The authors assumed the carrying capacity , at time , to be an increasing function with a slower rate parameter and as , where is the maximum population size. Basically, the functional form of is logistic with a slower rate of increase as compared to the rate parameter of underlying logistically growing population and the modified growth model was applied to the US population growth for illustration. Turner et al. (1976) further proposed a “generic growth model” from which many commonly known growth equations can derived as a special or limiting case. This is probably the first unification of existing growth equations, in the sense of Chakraborty et al. (2019), that provided a compact representation of a class of growth functions (Fig. 1, Turner et al. (1976)). Consideration of varying parameters with time was not only limited to the dynamics of single populations, but, to the predator prey models (Cushing, 1977) and higher dimensional models as well (Ikeda and Yokoi, 1980). Using the bifurcation theory, Cushing (1977) investigated the dynamics of predator-prey models by modifying the birth rate of prey and death rate of predator as periodic functions of time.

It is interesting to note that in the literature, the logistic growth has received huge attention from the researchers and several studies have been carried out by parametrizing the two fundamental parameters, intrinsic growth rate () and the carrying capacity of the environment (). Coleman (1979) was the first to consider the aperiodic time-dependent functional form for both and that essentially makes autonomous logistic growth equation to a non-autonomous one. The author basically considered two types of variation in : in one situation, varies slowly with time and in the other scenario, fluctuates at an arbitrary rate, but remains close to a constant. Further investigation along this direction was carried out by Hallam and Clark (1981) who reparametrized the equations proposed by Coleman (1979) to model the population with small growth rates in a deteriorating environmental conditions. Beck (1982) considered logistically growing to model the population genetics of cystic fibrosis disease and probably, he was the first one to consider time-dependent form of to model diseases population genetics. Another application of varying parameter was considered by Ebert and Weisser (1997) to model the parasite growth in host body in which the authors considered logistically growing carrying capacity with time. In the context of habitat selection of marine fishes and associated ideal free distribution, Shepherd and Litvak (2004) discussed the biological implications of three different possibilities of variation in and , namely: (1) constant and variable , (2) variable and constant and (3) varying and . Use of continuously varying parameters in growth modelling is not only limited to the biological systems, but, it has been used in other domains as well. Trappey and Wu (2008) analyzed 22 time series data of electronic products and showed that time varying logistic growth models (with ) gives 70% better performance than simple logistic and gompertz models for short product life cycle datasets.

There are some important innovations in growth curve modelling. For example, Sharif and Ramanathan (1981) combined the confined exponential model (Banks, 1994) and logistic growth equation to describe the time pattern of the diffusion process for technological innovations. The author observed a serious limitation due to assumption of constant population of potential adopters (similar to the carrying capacity) in the model. The limitation was overcome by considering the number of potential adaptors to vary with time assuming some known functional form. According to Meyer and Ausubel (1999), the technological adoption process can be modelled by logistic growth equation. The author used the data on technological evolution from two countries, England and Japan, and showed that a sigmoid type function for was a better choice to analyze the data than the assumption of constant . Following the idea of Meyer and Ausubel (1999), Safuan et al. (2011) assumed the confined exponential function for to study the growth of microbial biomass under occlusion of the skin. The author later obtained the exact solution of the non-autonomous logistic equation considering time dependent form of (Safuan et al., 2013). A schematic diagram of the literature is depicted in Table 1.

| Reference | Growth model | Varying parameter | Type of variation | Biological justification or explanation |

|---|---|---|---|---|

| Utida (1957) | Host-parasite model | Rate of reproduction () | Density dependent | Impact of fluctuating environment on |

| Turner et al. (1969) | Generalized logistic model | Maximum population size () | Sigmoidally varying with time | depends on technological advances such as housing and food sources |

| Nisbet and Gurney (1976) | Logistic delay model | Intrinsic growth rate (), carrying capacity () | Periodically varying with time | Impact of periodically varying environment |

| Cushing (1977) | Predator-prey model | Net birth rate of prey and predator ( and ) | Periodically varying with time | Impact of oscillating behaviour of the environment |

| Coleman (1979) | Logistic model | Intrinsic growth rate (), carrying capacity () | Time dependent | Modelling the effect of environmental changes on populations |

| Ikeda and Yokoi (1980) | Theoretical model of fish population | Nutrient amount, carrying capacity, death rates | Increasing function of pollution load | impact of nutrient enrichment and pollution on fish population dynamics |

| Sharif and Ramanathan (1981) | Binomial innovation diffusion model | Population adaptors () | Time dependent | Demands for innovation changes with time due to some factors |

| Hallam and Clark (1981) | Logistic model | Intrinsic growth rate (), carrying capacity () | Time dependent | Impact of deteriorating environment |

| Beck (1982) | Logistic model | Carrying capacity () | Logistically growing with time | Modelling the population genetics of cystic fibrosis |

| Arrigoni and Steiner (1985) | Logistic model | Carrying capacity () | Periodically varying with time | Impact of fluctuating environment |

| Reference | Growth model | Varying parameter | Type of variation | Biological justification or explanation |

|---|---|---|---|---|

| Ebert and Weisser (1997) | Logistic model | Carrying capacity () | Sigmoidally varying with time | Modelling the parasite growth |

| Meyer and Ausubel (1999) | Logistic model | Carrying capacity () | Sigmoidally varying with time | Carrying capacity of a system depends on invention and diffusion of technologies |

| Lakshmi (2003) | Malthusian growth model | Maximum sustainable population () | Periodically varying with time | Modelling the impact of oscillating population dynamics of a system |

| Leach and Andriopoulos (2004) | Verhulst model | Natural rate of replication (), carrying capacity () | Periodically varying with time | To consider temporal variation of carrying capacity and replication rate |

| Shepherd and Litvak (2004) | Population density models, Constant density models and Basin models | Intrinsic growth rate (), carrying capacity () | Density dependent | Impact of habitat selection, ideal free distribution and environmental effects |

| Lakshmi (2005) | Malthusian growth model | Maximum sustainable population () | Periodically varying with time | Oscillating population model |

| Rogovchenko and Rogovchenko (2009) | Pearl–Verhulst model | Intrinsic growth rate and carrying capacity | Periodically varying with time | Modelling the effect of periodic environmental fluctuations |

| Safuan et al. (2011) | Logistic model | Carrying capacity () | Confined exponential function of time | Modelling the drastically changes in cutaneous bacteria population |

| Safuan et al. (2013) | Logistic model | Carrying capacity () | Time dependent | Impact of environmental changes |

The stochastic variation of parameters is not being considered here.

The time dependent variations in the model parameters can be classified into two broad categories: periodic and non-periodic. Till now we have discussed the literature available for non periodic variations of time only. We now mention some literature in which the parameters were assumed as periodic function of time. Nisbet and Gurney (1976) was the first to consider periodic functional form in the single population dynamics. Considering time varying periodic functional form for both and in logistic delay model with time delay , the author investigated the dynamics numerically. Arrigoni and Steiner (1985) further investigated the logistic growth model considering periodically varying functional form of . Lakshmi (2003) considered the time varying parameter ‘maximum sustainable population’ (which is similar to carrying capacity ), as: , in the Malthusian growth model (Freedman, 1980) to model the oscillating population dynamic system. Prompted by the work done by Lakshmi (2003), Leach and Andriopoulos (2004) also considered periodic time-varying parameters to introduce the possibility of chaos into the Verhulst model (Verhulst, 1838). Also considering various forms of and , the author solved the model and investigated the behaviour, stability and properties of solution with comparison of the solution obtained by Lakshmi (2003). Following Leach and Andriopoulos (2004), Lakshmi (2005) extended her proposed work in Lakshmi (2003) and showed that is also periodic for any periodic form of , where is the population at given time . Rogovchenko and Rogovchenko (2009) modified the work done by Lakshmi (2003), Leach and Andriopoulos (2004) and Lakshmi (2005) and briefly examined the periodic variation in intrinsic growth rate (). They assumed the model framework proposed by Hallam and Clark (1981) and examined the existence of a unique positive asymptotically stable periodic solution of the system for for all .

The literature on growth curves is not only limited to the variation in parameters with respect to time; several studies are also available in which the size dependent variations are also explicitly considered. For example, López-Ruiz and Fournier-Prunaret (2005) used density dependent variations in parameters in a predator-prey system. Also there are evidence of stochastic variation in parameters as well Dubkov and Spagnolo (2008); Méndez et al. (2010); Anderson et al. (2015); Yoshioka (2019). However we do not delve deep into the stochastic analogue in this manuscript.

3 Model extension by continuous variation of parameters

Banks (1994) discussed a number of models in which the parameters varied continuously. In this section, we find the possible relationship between two growth models by varying parameter with time (continuously) and density. We have considered four different models as basic models, namely: (a) exponential growth model, (b) logistic growth model, (c) theta-logistic growth model and (d) confined-exponential growth model. The details analysis is given below and the findings are also represented diagrammatically in Fig. 1.

| Parent Model: Exponential Model | ||||

|---|---|---|---|---|

| Srl. | Analytical Solution | Asymptotic size | Model identification | |

| . | Normal Distribution (Banks, 1994) | |||

| . | Power Law Exponential (Banks, 1994) | |||

| . | Linear Model (Banks, 1994) | |||

| . | Hyperbolic Model (Banks, 1994) | |||

| . | Gompertz Model (Banks, 1994) | |||

| . | Korf Model (Korf, 1939) | |||

| . | Linearly increasing | |||

| . | Hyperbolically varying | |||

| . | Hyperbolically varying | |||

| Parent Model: Logistic Model | |||||

|---|---|---|---|---|---|

| Srl. | Analytical Solution | Asymptotic size | Model identification | ||

| . | Exponential Model (Banks, 1994) | ||||

| . | Hyperbolically Varying (Banks, 1994) | ||||

| . | Linearly Growing | ||||

| . | Linearly Decaying | ||||

| . | Extended Logistic Model (Chakraborty et al., 2017) | ||||

| . | Exponentially Decaying | ||||

| . | Exponentially Growing | ||||

| . | Hyperbolically Varying | ||||

| . | Periodically Varying | ||||

| . | Periodically Varying | ||||

We did not consider the variation , (used in Banks (1994)) as it does not give biologically realistic model.

| Parent Model: theta-logistic Model | ||||||

|---|---|---|---|---|---|---|

| Srl. | Analytical Solution | Asymptotic size | Model identification | |||

| . | Logistic Model (Verhulst, 1838) | |||||

| . | Gompertz Model (Gompertz, 1825) | |||||

| . | and | Richards Model (Richards, 1959) | ||||

| . | Koya-Goshu Model (Koya and Goshu, 2013) | |||||

| . | Linearly Increasing | |||||

| . | Linearly Decreasing | |||||

| . | Extended Gompertz Model (Bhowmick et al., 2014) | |||||

| . | Von Bertalanffy Model (Von Bertalanffy, 1949) | |||||

| . | Generalized Von Bertalanffy Model (Von Bertalanffy, 1960) | |||||

| . | and | Generalized Gompertz Model (Chakraborty et al., 2017) | ||||

| . | Crescenzo-Spina Model (Crescenzo and Spina, 2016) | |||||

| . | Second-order Exponential Polynomial(Chakraborty et al., 2019) | |||||

| Parent Model: Confined Exponential Model | |||||

|---|---|---|---|---|---|

| Srl. | Analytical Solution | Asymptotic size | Model identification | ||

| . | Extreme Minimal Value Distribution (Banks, 1994) | ||||

| . | Weibull Distribution (Weibull et al., 1951) | ||||

| . | Logistic Model (Verhulst, 1838) | ||||

| . | Linearly Decaying | ||||

| . | Linearly Increasing | ||||

| . | Exponentially Decaying | ||||

| . | Hyperbolically Varying | ||||

| . | Periodically Varying | ||||

| . | Periodically Varying | ||||

| . | Linearly Increasing | ||||

| . | Exponentially Increasing | ||||

| . | Exponentially Decaying | ||||

We did not consider the variation , (used in Banks (1994)) as it does not give biologically realistic model.

| Srl. | Parent Model | New Model | Asymptotic size | Model identification | |||

|---|---|---|---|---|---|---|---|

| . | Logistic | - | Linearly Varying | ||||

| . | Theta-Logistic | Co-operation Model (Bhowmick et al., 2015) | |||||

| . | Theta-Logistic | Marusic-Bajzer Model (Marusic and Bajzer, 1993) | |||||

| . | Theta-logistic | Exponentially increasing () |

Banks (1994) showed that after varying intrinsic growth rate () in exponential model, one can build connections with normal distribution, power law exponential model, linear model, hyperbolic model and gompertz model. In this paper, the extended models which are obtained by continuous transformation of the growth coefficient () is depicted in Table 2. In Table 3, we considered continuously variation in intrinsic growth rate and carrying capacity in logistic growth model. Considering continuous variation in , Banks (1994) built some connections between logistic model with other existing growth models. We mainly focus on the variation in the parameter and built connection with extended logistic model studied by Chakraborty et al. (2017). The exercises have also been carried out on the theta-logistic and confined exponential model and the derived connections are depicted in Table 4 and Table 5 respectively. Connections have been found between theta-logistic model with logistic model, gompertz model, Richards model, Koya-Goshu model, extended gompertz model, Von Bertalanffy model, generalized Von Bertalanffy model, generalized gompertz model, Crescenzo-Spina model and second order polynomial model.

Noteworthy to mention that by applying the above transformations many new growth equations are obtained. It is to be noted that for each of the previous cases, the final differential equation (after replacing by or by ) can be solved analytically or solutions are available using some special functions. The differential equations must be solved numerically to obtain the size profile in case the analytical solution is not available. In Table 6, we consider few cases in which the analytical expression for the size variable is not available. The detail discussion for each extended growth equation is discussed in the supporting information.

4 ISRP and statistical identification of varying parameters

Bhowmick et al. (2014) proposed the concept of Interval Specific Rate Parameter (henceforth, ISRP) which performed better in selecting the true model more accurately than the Fisher’s RGR (Pal et al., 2018). For every model the authors have identified a key parameter (called the rate parameter), and obtained its interval specific estimates based on the longitudinal data set up. If the underlying model is true, then the rate parameter should remain same over different time intervals. The advantage of using ISRP is, it can detect crucial intervals where the growth process is erratic and unusual. It may help experimental scientists to study more closely the effect of the parameters responsible for the growth of the organism/population under study.

4.1 Asymptotic distribution of the estimator

In this sub section we shall derive the distribution of ISRP estimator of and under some assumptions using Multivariate Delta Method (Wasserman, 2004; Casella and Berger, 2002). This distribution will be the key mechanism to identify whether the parameter has undergone any continuous variation over time.

4.1.1 The data structure and model set up

To derive this distribution, we consider the data matrix , where

whose rows are assumed to be independent and identically distributed (iid) random variables following -variate normal distribution with mean vector and variance covariance matrix . If we take , then and , for all ; denotes the transpose of a matrix . We have considered time points. We consider logistic growth model as test bed model for simulation study and under this model

| (1) |

As existence of second order moments is assumed, so taking , where , we can apply Multivariate central limit theorem (Timm, 2002) by which we get

| (2) |

Now the estimator of ISRP of based on time points , , denoted as , is given by (Pal et al., 2018),

| (3) |

We aim to obtain the sampling distribution of using Multivariate delta method (Wasserman, 2004). In terms of variables , and the function can be written as

| (4) |

By using Multivariate central limit theorem for , we obtain

Here the mean function under logistic growth law is given by eqn. (1) and is a differentiable function at . Now we have to find the at the point to apply Multivariate delta method. Taking partial derivatives of with respect to , and and evaluate the above partial differential equations at the point , we obtain

where the values of ’s, are provided in eqn. (1). Using matrix notation, we obtain

Now by using Multivariate delta method, the distribution of is given as

The estimator of ISRP of the parameter based on the triplet , , denoted by , is given by (Pal et al., 2018),

| (5) |

Since is a function of the random variable , one may argue that the distribution can be derived by using the delta method with taking some function of the form . However, note that the co-variance structure between and is not known. Hence, the function was chosen using the original random variables whose covariance structure is known. In terms of , the function is given as

| (6) |

Taking partial derivatives of with respect to the real variables , and and evaluating it at the point , we obtain

where the values of ’s, are provided in eqn. (1). Using matrix notation, we get

where and . By using Multivariate delta method, the distribution of is given as

The expression for partial derivatives which are required for the computations of interval specific estimators for all the models are given in Appendix A.

4.2 Simulation study

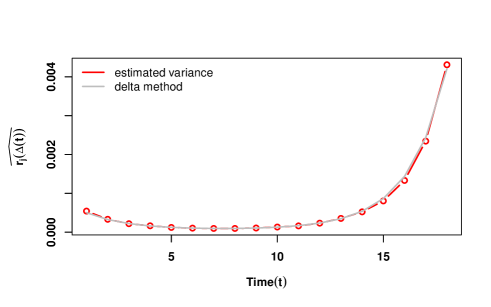

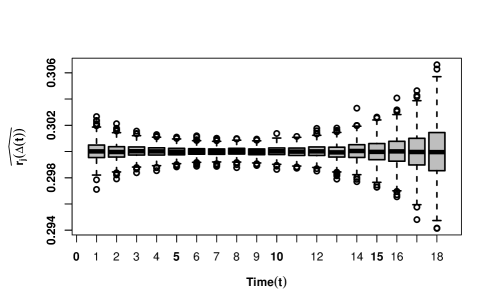

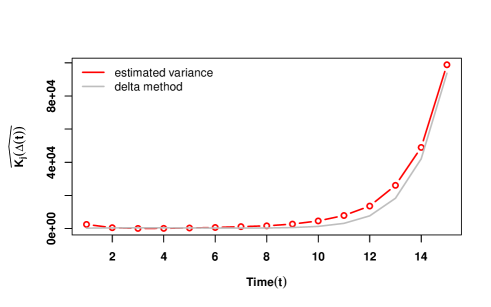

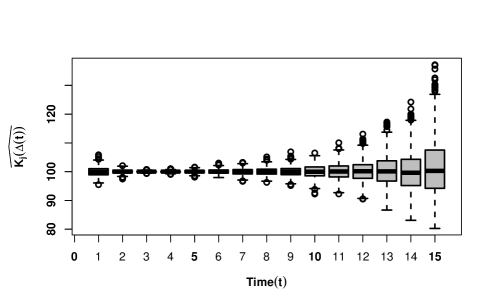

In this section the theoretical results are verified by using the simulation study. To check the accuracy of delta method is approximating the sampling distribution of for , we used computer simulation. We simulated the growth trajectories for individuals for times points where each trajectory was generated from the multivariate normal distribution with logistic mean function and variance-covariance matrix with Koopman structure (Koopmans, 1942). Based on this data, we obtained the estimate of which acts as a single realization from the sampling distribution of . The process was replicated 1000 times to obtain 1000 realizations from the distribution of to visualize the distribution by using the histograms. The histograms obtained from simulation study clearly suggested the agreement with normal distribution with estimated mean and and variance obtained from the delta method. The close agreement between the approximate distribution by using delta method and simulated sampling distribution is depicted in Fig. 2(a), 2(b) for and in Fig. 2(c), 2(d) for . The parameter choices are kept as , and the covariance matrix is the Koopman structure.

In addition, even if the data were simulated from the other growth model, the normal approximation of the sampling distribution of the estimators remain unchanged. For example, we carried out the same simulation study using the extended version of the logistic growth model with and and evaluated the under the assumption of the logistic model. The associated patterns in ISRP profiles are depicted in Fig. 3(a) (power function) and Fig. 3(b) (linear function). The simulation study was carried out in software R. All the necessary codes are being provided in the online supporting material.

Remark 1.

For simulation, we have considered the co-variance matrix having Koopmans (Koopmans, 1942) correlation structure. According to this structure the correlation between and will be small if the time points and are far apart. This is quite natural in growth processes. Similar structure is considered by many other researchers (Pal et al., 2018; Chakraborty et al., 2019).

5 Real data analysis

In this section we establish the utility of the discussed method using some real data sets from different domains. The examples have been selected here from three different domains for illustration purpose only. Analysis of domain specific data sets and providing meticulous analysis is beyond the scope of our current study. We have considered representative examples from animal growth, retail marketing and epidemiology.

5.1 Case study - I

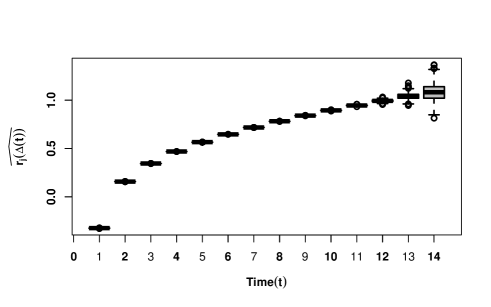

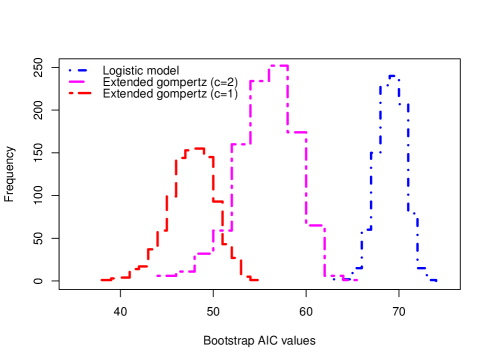

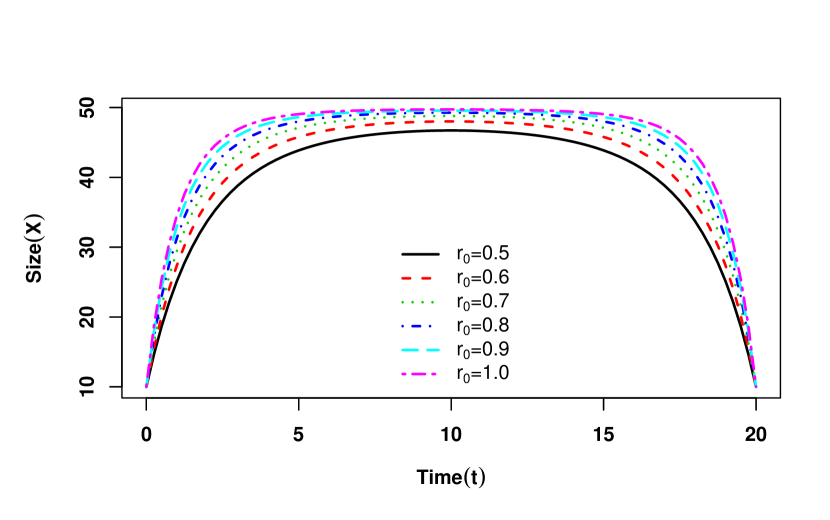

For illustration, we considered the data sets on cattle growth which was analyzed by Kenward (1987). The cattle data contains the weight of individual cattle at 11 time points over a 133 days period. The animals were given two treatments, namely A and B for intestinal parasites. For the demonstration purpose, we considered the data of animals which were given treatment A which were 30 in total. Here we make an attempt to choose the appropriate mean growth profile based on the data. The measurement schedules are rescaled to . The Grey coloured curves in in Fig. 4(a) and Fig. 4(b) depicts the RGR and Size profile of individual animal respectively. Given the mean size profile a sigmoid shape growth curve would be an appropriate choice to start the analysis. However, the RGR profile indicates that the logistic growth model is not appropriate for describing the growth pattern. RGR first increases and then decreases. So, according to our proposal in this manuscript, we start with the base model as exponential and the empirical investigation suggests that the growth coefficient is varying as a function of time as , where , , are positive. Such a choice of the RGR profile was investigated in Bhowmick et al. (2014) and Bhowmick and Bhattacharya (2014). Since for non-integer value of the exact solution can not be obtained, so we consider the final model for and only. The corresponding models are known as extended gompertz model which has a growth equation described in Bhowmick et al. (2014). The logistic model, extended gompertz model ( and ) were fitted to the size profiles and the corresponding AIC values are 68.9423, 46.14059 and 55.42874, respectively (Fig. 4(b)). Thus the best model turns out to be the exponential model with continuously varying growth coefficients . To be more precise with our conclusion, we created bootstrap data sets by randomly selecting rows of the data with replacement. All three designated models were fitted to each bootstrap sample and corresponding AIC values were recorded. The bootstrap distribution of the AIC for each models gives strong indication for the selection of the extended gompertz model with (Fig. 5).

5.2 Case study - II

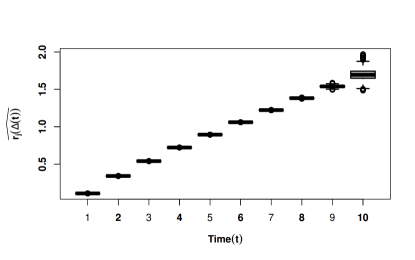

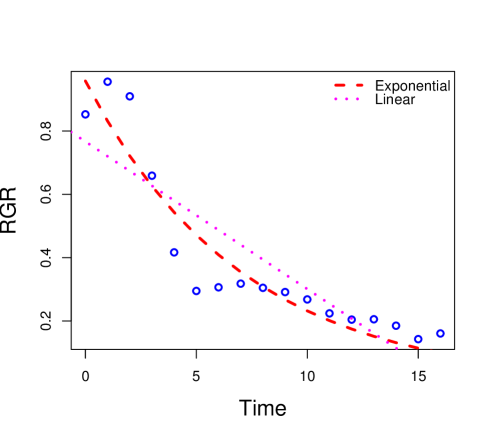

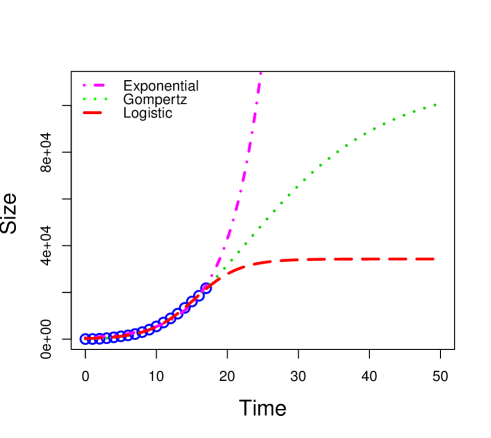

For illustration of the method, we have considered the data set of cumulative sales of LCD-TV from Trappey and Wu (2008). The data gives the cumulative quarterly sales from 2003 to 2007 (in thousand) which were collected from Market Intelligence Center Taiwan by Trappey and Wu (2008). For simplicity, the measurement schedules are rescaled as . The dataset clearly indicates an exponential growth in sales during the period 2003-2007. However, the plot of relative growth rate gives the actual picture (Fig. 6(a)). It is evident from Fig. 6(a), that the logged difference is a decreasing function with respect to time, which indicates that exponential growth is not an appropriate model to choose. Rather it suggests that, the exponential model with an intrinsic growth rate which is a decreasing function of time may be a better choice. So, for the analysis we fitted the exponential and linear function of intrinsic growth rate. Exponential decay of the form () has been found to be more appropriate than a linear choice of based on the Akaike Information Criteria (AIC). AIC of exponential fit is -27.85451 and AIC of linear fit is -14.5925 and the difference in AIC values (Burnham and Anderson, 2002). Hence, gompertz model is the appropriate choice for the given data. In Fig. 6(b), we have fitted all the three models, viz, exponential, gompertz and logistic and obtained the AIC values as 295.0443, 221.4758 and 247.4407, respectively. Smallest AIC for Gompertz model indicates the preference of this model than other two. The models are also compared using the root mean squared error and the conclusion remained same. The analysis was carried out using nonlinear least squares method using nls function available in R. Complete source codes are provided in the supporting online material.

5.3 Case study - III

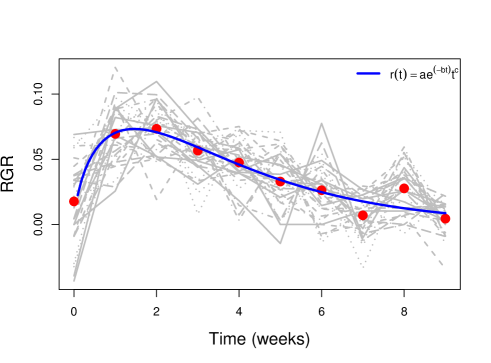

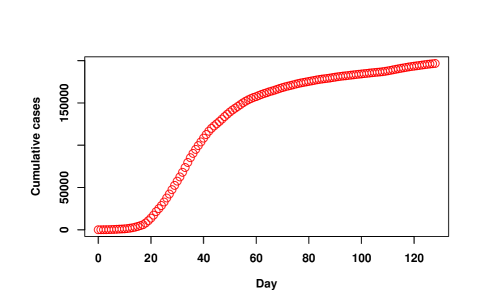

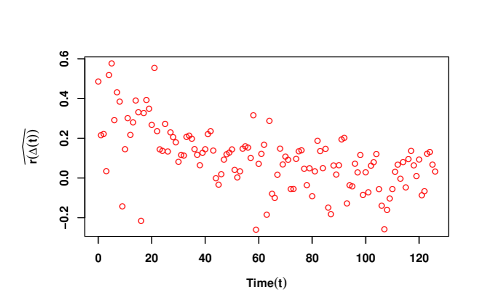

In the third case study, we have taken the data of cumulative COVID-19 cases in Germany. The data set being considered from (https://ourworldindata.org/coronavirus). The data contains cumulative affected cases of COVID-19 from 31st December 2019 to 8th July 2020. Till 27th Jan 2020, there were no cases reported in Germany. For the ease in the selection criterion, we have taken 5 days moving average of the data. It has been observed that till day 62, dated 29th Feb 2020, there were minor changes observed in the data, due to which for fitting the model the data is being considered from 1st march 2020 to 8th June 2020, which is 129 days in total. For simplicity, the measurement schedules are rescaled as .

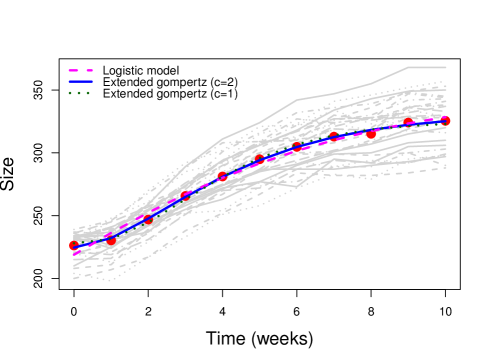

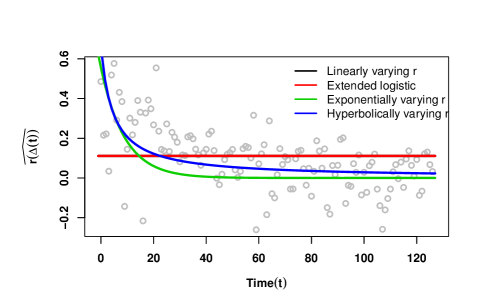

From the size profile (Fig. 7(a)) of the data, it can be clearly seen that logistic growth model seems to be the best choice to start our analysis with. But from the size profile, it is hard to conclude whether or not any variation is present in (intrinsic growth rate). So for getting insight about any variation present in parameter , we plotted ISRP profile (Fig. 7(b)) of by making use of the formula in Bhowmick et al. (2014).

| RMSE and AIC values of continuous variations of parameter fitted on ISRP of | |||||

| Srl. | Type of variation | RMSE values | AIC values | Parameter estimates (with confidence interval) | Confirmed pattern of ISRP |

| . | Linearly varying | 0.1582315 | -101.8885 | , | No linear variation |

| . | Extended logistic | 0.1582315 | -101.8885 | , | No variation |

| . | Exponentially varying | 0.1539704 | -108.8223 | , | Exponentially increasing |

| . | Hyperbolically varying | 0.1385250 | -135.6726 | , | Variation present and best fitted form |

| RMSE and AIC values of continuously varying model for cumulative COVID data sets | |||

| Srl. | Model | RMSE values | AIC values |

| . | Logistic model (constant ) | 6992.228 | 2658.045 |

| . | Linearly growing | 24123.600 | 2979.550 |

| . | Linearly decaying | 24062.943 | 2978.901 |

| . | Extended logistic | 4793.885 | 2562.661 |

| . | Exponentially decaying | 57103.655 | 3201.863 |

| . | Exponentially growing | 61851.387 | 3222.469 |

| . | Hyperbolically varying | 4684.953 | 2556.731 |

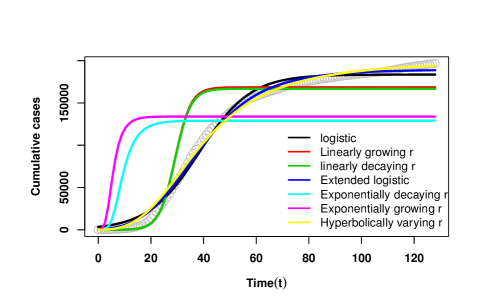

We have obtained the empirical estimate of ISRP of by assuming that the data generating process was logistic. To check whether there is any significant variation in , we fitted the continuous functions given in Table 3 and selected the best model based on AIC and RMSE values (Table 8). As there is no sign of presence of periodic variation in data, we have not considered any kind of periodic variation in as well as as in final fitting. Based on the summary in Table 8, we observed that the parameter was subjected to hyperbolic variation with respect to time (Fig. 8(a)). Hence, we suspect that the actual data generation process is not logistic, rather logistic growth with hyperbolically varying . To support our claim, we fitted derived growth equations (in Table 3 ) to the cumulative number of cases and found that the logistic model with hyperbolically varying growth coefficient is the best choice amongst all the models (both RMSE and AIC (Table 8) support the conclusion )(Fig. 8(b)). The analysis was carried out using nonlinear least squares method using nls2 function available in R. Complete source codes are provided in the supporting online material.

Based on these three case studies, we conclude that ISRP profile acts as a key indicator for selecting the best growth model.

6 Discussion

The main idea of this paper is essentially based on the concept of ISRP developed by Bhowmick et al. (2014), subsequently studied by Pal et al. (2018). Their original work was motivated towards the selection of the best model amongst a class of nonlinear models. In this approach, main criteria is that experimenter should be able to identify the key rate parameter () for every model. However, if we are in a situation in which the parameter varies continuously, then it puts us into the following problems in applications: (1) One needs to make a very good guess about the final model and the analyst should be able to express the RGR of the final model in the form , for some real valued function ; (2) The final model might turn out to be very complicated in nature so that the computation of ISRP becomes difficult and some parameters may not have an explicit expression of ISRP as well. It can be easily understood that both the tasks are quite difficult and may lead wrong conclusion. Our proposed idea apparently resolved both these issues as discussed below.

Firstly, it reduces the search space of selecting the best model by investigating only a few models. As depicted in Fig. 1 and in Table 2, 3, 4, 5 and 6, most of the models can be obtained from four models (Exponential Model, Logistic Model, Theta-Logistic Model, Confined Exponential Model). So, an experimenter does not need to compute ISRP of all the models which is itself may be a tedious computational process. Only ISRP profile from these four models will give the clue for the selection of the underlying model. Thus, this work further reinforces the use of ISRP and generalizes its application in model selection at a reduced effort.

The other important observation is that ISRP profile of parameter is very informative in a sense that, it depicts homogeneity or heterogeneity across different growth trajectories with respect to the parameter of interest, for example, whether the parameter varies or not, can be traced only in some particular time period. If we observe the ISRP profile of (Fig. 2(b)), we notice that till time point , the variation are small, and the same thing happens when it varies continuously (Fig. 3(a), 3(b)). Hence one could argue that information about the parameter in the data are contained during specific time interval only. Beyond that, data points are not informative as they show very high variability with respect to the parameter of interest.

Recently, Chakraborty et al. (2019) proposed a unification function to unify a large number of equations. In their unifying function, different choices of parameters lead to different models, thus giving a compact representation of several growth equations. It is worth mentioning that from a mathematical perspective, the unifying function serves a great purpose, but from a statistical point of view it may pose difficulty in dealing with real data sets as the unifying function itself is heavily parametrized by several fixed but unknown real valued parameters. Thus, if we plot a network similar to Fig. 1, the network will have only one key node (with unifying function) and all other models will be leaf with no connection between them. Thus in application, essentially an experimenter need to resolve a difficult estimation problem to obtain a simpler equation. On the contrary, our approach in this manuscript starts with the investigation of simpler models and extrapolate to complex models (if required at all). In addition the network type plot, depicted in Fig. 1 is more informative than a plot with single key node, because Fig. 1 depicts connection between close approximating models as well, hence giving more broader picture. Hence, if we describe the approach in Chakraborty et al. (2019) as a “complex to simple” strategy, then our approach is “simple to complex”.

The distribution of the interval specific estimators also depends on the covariance structure of the statistical model. The Koopman covariance structure is homoschedastic which assumes equal population variance for all time points. However, in reality, this may not be always true. For example, Diniz et al. (2012) considered the multiplicative heteroschedasticity and estimated the parameters of Von Bertalanffy model under a fully Bayesian set up. Such instances are abundant in growth studies. Louzada et al. (2014) analyzed the growth data under both normal and skew-normal distribution of the error structure with homoschedastic, homoschedastic of lag 1 (Koopman) and multiplicative heteroschedastic covariance matrix. Till date the distributions of ISRP has only been investigated under the homoschedastic covariance matrix with autocorrelation lag 1. It would be an interesting research avenue to study the distribution of the interval estimators under different assumptions of covariance error structure by means of theoretical interest and broader application of the methods presented in this manuscript and by Bhowmick et al. (2014) and Pal et al. (2018).

It is to be noted that in Fig. 3(a), the values of ISRP () with respect to time is indicative of deviation from linearity at the initial phase of the growth only. This is quite natural as the impact of the growth coefficient is more prominent at the early stage and as the process evolve, the information about will be lost. Basically, before the lag phase starts, logistic growth essentially behaves like exponential only. A similar idea has been discussed in the context of estimating the patterns of density dependence for natural populations (Clark et al., 2010). The theta-logistic curve was calibrated using a large number of data sets by Sibly et al. (2005). In the model, the per capita growth rate () is modelled by , where is the intrinsic growth rate and this model have the maximum when the population size is small. In other words, unless the population sizes are observed at low population densities, estimation of will not be reliable. So, if the population size fluctuates around the carrying capacity, then the estimated model can be one of these types: linear, concave upward or concave downward (Clark et al., 2010). Thus, it may lead to dubious inference regarding the fate of the populations. Similar is the idea here, at early stage of growth the parameter plays crucial role, or in other words, observations taken at the early stage of growth are more informative about rather than later stage.

Innovation of interval specific rate parameter is not only useful in better approximation of growth rates, but to understand parameter sensitivity as well in a growth process. If the parameter varies continuously, its identification can be done using interval specific estimates. Similar to the continuously varying parameters, growth models with randomly varying parameters are also significantly available in growth literature. It would be our future endeavor to explore the domain of randomly varying parameters and their impacts in modeling and assessment using real data sets. In addition, it would be our future endeavor to develop general purpose programs that will integrate the connections among growth curve models and guide correct model selection based on the patterns of interval estimates of the model parameters.

7 Conclusion

Theory of growth curve modelling is fundamental to understand any biological process. Building a good approximating model for the underlying growth process requires a good identification of the parameters in the model. In this manuscript, we give a detailed historical development of this domain and justified the need of an unifying study specifically targeting this problem. By extending the idea of Banks (1994), we have identified that several existing growth models in the literature can be connected. We shown here that such connections between growth equations significantly reduce the efforts in choosing an optimal model. Using the idea of Interval Specific Estimator by Bhowmick et al. (2014), we proposed a statistical method to identify whether the parameter in the model varies with time. Our proposed methodology significantly reduced the efforts involved in model fitting exercises. We believe that this work would be helpful for the practitioners in the field of growth study. The proposed idea is verified by using simulated and real data sets from two different domains (biology and marketing). We believe that this idea is unique and it contains a novel message for the scientific community, in particular for applied researchers.

8 Acknowledgement

Karim is thankful to the Council of Scientific & Industrial Research (CSIR), Government of India for the financial support in the form of junior research fellowship (Grant No. 09/991(0057)/2019-EMR-\@slowromancapi@). Authors are thankful to Ayan Paul for valuable discussions and assisting in computations.

References

- Anderson et al. (2015) Anderson, C., Jovanoskia, Z., Towersa, I., Sidhua, H., 2015. A simple population model with a stochastic carrying capacity. 21st International Congress on Modelling and Simulation .

- Arrigoni and Steiner (1985) Arrigoni, M., Steiner, A., 1985. Logistic growth in a fluctuating environment. Journal of Mathematical Biology 21, 237–241.

- Banks (1994) Banks, R.B., 1994. Growth and Diffusion Phenomena. Springer.

- Barker and Sibly (2008) Barker, D., Sibly, R.M., 2008. The effects of environmental perturbation and measurement error on estimates of the shape parameter in the theta-logistic model of population regulation. Ecological Modelling 219, 170 – 177.

- Beck (1982) Beck, K., 1982. A model of the population genetics of cystic fibrosis in the United States. Mathematical Biosciences 58, 243 – 257.

- Bhowmick et al. (2016) Bhowmick, A.R., Bandyopadhyay, S., Rana, S., Bhattacharya, S., 2016. A simple approximation of moments of the quasi-equilibrium distribution of an extended stochastic theta-logistic model with non-integer powers. Mathematical Biosciences 271, 96 – 112.

- Bhowmick and Bhattacharya (2014) Bhowmick, A.R., Bhattacharya, S., 2014. A new growth curve model for biological growth: Some inferential studies on the growth of Cirrhinus mrigala. Mathematical Biosciences 254, 28 – 41.

- Bhowmick et al. (2014) Bhowmick, A.R., Chattopadhyay, G., Bhattacharya, S., 2014. Simultaneous identification of growth law and estimation of its rate parameter for biological growth data: a new approach. Journal of Biological Physics 40, 71–95.

- Bhowmick et al. (2015) Bhowmick, A.R., Saha, B., Chattopadhyay, J., Ray, S., Bhattacharya, S., 2015. Cooperation in species: Interplay of population regulation and extinction through global population dynamics database. Ecological Modelling 312, 150 – 165.

- Bridges et al. (2000) Bridges, T.C., Turner, L.W., Gates, R.S., Smith, E.M., 2000. Relativity of Growth in Laboratory Farm Animals: I. Representation of Physiological Age and the Growth Rate Time Constant. American Society of Agricultural Engineers 43, 1803–1810.

- Burnham and Anderson (2002) Burnham, K., Anderson, D., 2002. Model selection and multimodel inference: a practical information-theoretic approach. Springer Verlag.

- Casella and Berger (2002) Casella, G., Berger, R.L., 2002. Statistical inference. volume 2. Duxbury Pacific Grove, CA.

- Chakraborty et al. (2017) Chakraborty, B., Bhowmick, A.R., Chattopadhyay, J., Bhattacharya, S., 2017. Physiological responses of fish under environmental stress and extension of growth (curve) models. Ecological Modelling 363, 172 – 186.

- Chakraborty et al. (2019) Chakraborty, B., Bhowmick, A.R., Chattopadhyay, J., Bhattacharya, S., 2019. A Novel Unification Method to Characterize a Broad Class of Growth Curve Models Using Relative Growth Rate. Bulletin of Mathematical Biology 81, 2529–2552.

- Clark et al. (2010) Clark, F., Brook, B.W., Delean, S., Reşit Akçakaya, H., Bradshaw, C.J., 2010. The theta-logistic is unreliable for modelling most census data. Methods in Ecology and Evolution 1, 253–262.

- Coleman (1979) Coleman, B.D., 1979. Nonautonomous logistic equations as models of the adjustment of populations to environmental change. Mathematical Biosciences 45, 159 – 173.

- Crescenzo and Spina (2016) Crescenzo, A.D., Spina, S., 2016. Analysis of a growth model inspired by Gompertz and Korf laws, and an analogous birth-death process. Mathematical Biosciences 282, 121 – 134.

- Cushing (1977) Cushing, J., 1977. Periodic Time-Dependent Predator-Prey Systems. SIAM Journal on Applied Mathematics 32, 82–95.

- Diniz et al. (2012) Diniz, C.A.R., Louzada-Neto, F., Morita, L.H.M., 2012. The multiplicative heteroscedastic Von Bertalanffy model. Brazilian Journal of Probability and Statistics 26, 71–81.

- Dubkov and Spagnolo (2008) Dubkov, A.A., Spagnolo, B., 2008. Verhulst model with lévy white noise excitation. The European Physical Journal B 65, 361–367.

- Ebert and Weisser (1997) Ebert, D., Weisser, W.W., 1997. Optimal killing for obligate killers: the evolution of life histories and virulence of semelparous parasites. Proceedings of the Royal Society of London. Series B: Biological Sciences 264, 985–991.

- Freedman (1980) Freedman, H.I., 1980. Deterministic mathematical models in population ecology. volume 57. Marcel Dekker Incorporated.

- Gilpin and Ayala (1973) Gilpin, M.E., Ayala, F.J., 1973. Global Models of Growth and Competition. Proceedings of the National Academy of Sciences 70, 3590–3593.

- Gompertz (1825) Gompertz, B., 1825. Xxiv. on the nature of the function expressive of the law of human mortality, and on a new mode of determining the value of life contingencies. in a letter to francis baily, esq. f. r. s. & amp;c. Philosophical Transactions of the Royal Society of London 115, 513–583.

- Hallam and Clark (1981) Hallam, T., Clark, C., 1981. Non-autonomous logistic equations as models of populations in a deteriorating environment. Journal of Theoretical Biology 93, 303 – 311.

- Ikeda and Yokoi (1980) Ikeda, S., Yokoi, T., 1980. Fish population dynamics under nutrient enrichment — a case of the East Seto Inland Sea. Ecological Modelling 10, 141 – 165.

- Kenward (1987) Kenward, M.G., 1987. A method for comparing profiles of repeated measurements. Journal of the Royal Statistical Society. Series C (Applied Statistics) 36, 296–308.

- Koopmans (1942) Koopmans, T., 1942. Serial Correlation and Quadratic Forms in Normal Variables. The Annals of Mathematical Statistics 13, 14–33.

- Korf (1939) Korf, V., 1939. Contribution to mathematical definition of the law of stand volume growth. Lesnicka Prace 18, 339–379.

- Kot (2001) Kot, M., 2001. Elements of Mathematical Ecology. Cambridge Univ. Press, Cambridge, UK.

- Koya and Goshu (2013) Koya, P.R., Goshu, A.T., 2013. Generalized mathematical model for biological growths. Open Journal of Modelling and Simulation 1, 42.

- Lakshmi (2003) Lakshmi, B., 2003. Oscillating population models. Chaos, Solitons & Fractals 16, 183 – 186.

- Lakshmi (2005) Lakshmi, B., 2005. Population models with time dependent parameters. Chaos, Solitons & Fractals 26, 719 – 721.

- Leach and Andriopoulos (2004) Leach, P., Andriopoulos, K., 2004. An oscillatory population model. Chaos, Solitons & Fractals 22, 1183 – 1188.

- López-Ruiz and Fournier-Prunaret (2005) López-Ruiz, R., Fournier-Prunaret, D., 2005. Indirect Allee effect, bistability and chaotic oscillations in a predator–prey discrete model of logistic type. Chaos, Solitons & Fractals 24, 85 – 101.

- Louzada et al. (2014) Louzada, F., Ferreira, P.H., Diniz, C.A., 2014. Skew-normal distribution for growth curve models in presence of a heteroscedasticity structure. Journal of Applied Statistics 41, 1785–1798.

- Malthus (1798) Malthus, T.R., 1798. An Essey on the Principle of population, as It Affects the future Improvement of Society with Remarks on the Speculations of Mr. Godwin. Condorcet, and Other Writers. J. Johnson in St Paul’s Churchyard, London .

- Marusic and Bajzer (1993) Marusic, M., Bajzer, Z., 1993. Generalized Two-Parameter Equation of Growth. Journal of Mathematical Analysis and Applications 179, 446 – 462.

- Méndez et al. (2010) Méndez, V., Llopis, I., Campos, D., Horsthemke, W., 2010. Extinction conditions for isolated populations affected by environmental stochasticity. Theoretical Population Biology 77, 250 – 256.

- Meyer and Ausubel (1999) Meyer, P.S., Ausubel, J.H., 1999. Carrying Capacity: A model with Logistically Varying Limits. Technological Forecasting and Social Change 61, 209 – 214.

- Nisbet and Gurney (1976) Nisbet, R., Gurney, W., 1976. Population dynamics in a periodically varying environment. Journal of Theoretical Biology 56, 459–475.

- Pal et al. (2018) Pal, A., Bhowmick, A.R., Yeasmin, F., Bhattacharya, S., 2018. Evolution of model specific relative growth rate: Its genesis and performance over Fisher’s growth rates. Journal of Theoretical Biology 444, 11 – 27.

- Perotto et al. (1992) Perotto, D., Cue, R., Lee, A., 1992. Comparison of nonlinear functions for describing the growth curve of three genotypes of dairy cattle. Canadian Journal of Animal Science 72, 773–782.

- Richards (1959) Richards, F.J., 1959. A Flexible Growth Function for Empirical Use. Journal of Experimental Botany 10, 290–301.

- Rogovchenko and Rogovchenko (2009) Rogovchenko, S.P., Rogovchenko, Y.V., 2009. Effect of periodic environmental fluctuations on the Pearl–Verhulst model. Chaos, Solitons & Fractals 39, 1169 – 1181.

- Sæther et al. (1998) Sæther, B.E., Engen, S., Islam, A., McCleery, R., Perrins, C., 1998. Environmental stochasticity and extinction risk in a population of a small songbird, the great tit. The American Naturalist 151, 441–450.

- Safuan et al. (2011) Safuan, H., Towers, I.N., Jovanoski, Z., Sidhu, H., 2011. A simple model for the total microbial biomass under occlusion of healthy human skin. Modelling and Simulation Society of Australia and New Zealand , 733–739.

- Safuan et al. (2013) Safuan, H.M., Jovanoski, Z., Towers, I.N., Sidhu, H.S., 2013. Exact solution of a non-autonomous logistic population model. Ecological Modelling 251, 99 – 102.

- Sharif and Ramanathan (1981) Sharif, M., Ramanathan, K., 1981. Binomial innovation diffusion models with dynamic potential adopter population. Technological Forecasting and Social Change 20, 63 – 87.

- Shepherd and Litvak (2004) Shepherd, T.D., Litvak, M.K., 2004. Density-dependent habitat selection and the ideal free distribution in marine fish spatial dynamics: considerations and cautions. Fish and Fisheries 5, 141–152.

- Sibly et al. (2005) Sibly, R.M., Barker, D., Denham, M.C., Hone, J., Pagel, M., 2005. On the regulation of populations of mammals, birds, fish, and insects. Science 309, 607–610.

- Timm (2002) Timm, N., 2002. Applied Multivariate Analysis: Springer Texts in Statistics. Springer-Verlag New York Incorporated.

- Trappey and Wu (2008) Trappey, C.V., Wu, H.Y., 2008. An evaluation of the time-varying extended logistic, simple logistic, and gompertz models for forecasting short product lifecycles. Advanced Engineering Informatics 22, 421 – 430. PLM Challenges.

- Tsoularis and Wallace (2002) Tsoularis, A., Wallace, J., 2002. Analysis of logistic growth models. Mathematical Biosciences 179, 21 – 55.

- Turner et al. (1969) Turner, M.E., Blumenstein, B.A., Sebaugh, J.L., 1969. 265 note: A generalization of the logistic law of growth. Biometrics 25, 577–580.

- Turner et al. (1976) Turner, M.E., Bradley, E.L., Kirk, K.A., Pruitt, K.M., 1976. A theory of growth. Mathematical Biosciences 29, 367 – 373.

- Utida (1957) Utida, S., 1957. Cyclic Fluctuations of Population Density Intrinsic to the Host-Parasite System. Ecology 38, 442–449.

- Verhulst (1838) Verhulst, P., 1838. Notice sur la loi que la population suit dans son accroissement. Correspondances Mathématiques et Physiques. 10, 113–121.

- Von Bertalanffy (1949) Von Bertalanffy, L., 1949. Problems of Organic G rowth. Nature 163.

- Von Bertalanffy (1960) Von Bertalanffy, L., 1960. In fundamental aspects of normal and malignant growth. Elsevier, Amsterdam 35, 137–295.

- Wasserman (2004) Wasserman, L., 2004. All of statistics: A concise course in statistical inference brief contents. Simulation 100, 461.

- Weibull et al. (1951) Weibull, W., et al., 1951. A statistical distribution function of wide applicability. Journal of applied mechanics 18, 293–297.

- Yoshioka (2019) Yoshioka, H., 2019. A simplified stochastic optimization model for logistic dynamics with control-dependent carrying capacity. Journal of Biological Dynamics 13, 148–176.

- Zhao and Tang (2011) Zhao, T., Tang, S., 2011. Impulsive harvesting and by-catch mortality for the theta logistic model. Applied Mathematics and Computation 217, 9412 – 9423.

Appendix A Expression of the required partial derivatives for computation of variance of interval estimators by Delta Method

A.1 Logistic model

-

1.

Variance of :

For compact representation, we shall use matrix notations. From eqn.(4), we obtain thatIn matrix notation, we have the following expression for :

The expression of the vector of partial derivatives after evaluating at is given in the main text.

-

2.

Variance of :

In real variable, eqn.(6) is written as:where is constant. We define and . Taking logarithm on , we obtain

Taking partial derivative with respect to , we obtain:

So, finally we obtain that,

Final expressions of all the required partial derivatives are as follows:

In matrix notation, we have the following expression for :

A.2 Exponential model

The exponential model (Malthus, 1798) is given by

| (7) |

and the solution is given by

In this model, only one variable is present and the ISRP of is given by (Pal et al., 2018)

In real variable is written as:

Now taking partial derivative of with respect to and , we obtain

Using eqn. (2), where , the distribution of is given as:

where

A.3 Theta-logistic model

The theta-logistic model is given by

| (8) |

and the solution is given by

In this model, two variables and and one limiting constant are present. Here, we only calculate the variance of and only.

- 1.

-

2.

Variance of :

The ISRP of is given by (Pal et al., 2018),After simplification is given as :

where is constant. In terms of real variable the function is written as:

Now, we define and . Taking logarithm on , we obtain

Taking partial derivative with respect to , we obtain:

So, finally we obtain that,

Final expressions of all the required partial derivatives are as follows:

Using eqn. (2), where , the distribution of is given as:

where

A.4 Confined exponential model

The confined exponential model is given by

| (9) |

where is the population size at time ; and are the intrinsic growth rate and carrying capacity (asymptotic size) respectively,) and the solution is given by

In this model, two variables and are present.

- 1.

-

2.

In real variable, is written as:

where is constant. We define . Taking logarithm on , we obtain

Taking partial derivative with respect to , we obtain:

So, finally we obtain that,

Final expressions of all the required partial derivatives are as follows:

Using eqn. (2), where , the distribution of is given as:

where

Appendix B Supporting online information

B.1 Analytical expression exist

We first discuss about the cases where after varying the parameter analytical expression of the solution of the model exists.

B.1.1 Variation in exponential growth model

We start our discussion by the oldest candidate in the growth curve literature, the exponential model (Malthus, 1798). Banks (1994) showed that after varying the parameter () in the exponential model (eqn. 7), one can build connections with the normal distribution, gompertz growth, linear growth, hyperbolic growth and power law exponential model. So, we do not discuss them here. We will concentrate on the other type of variation which are not available in existing literature.

-

1.

; :

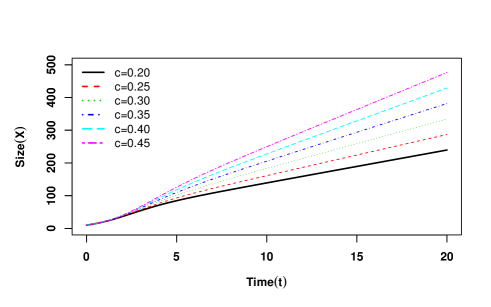

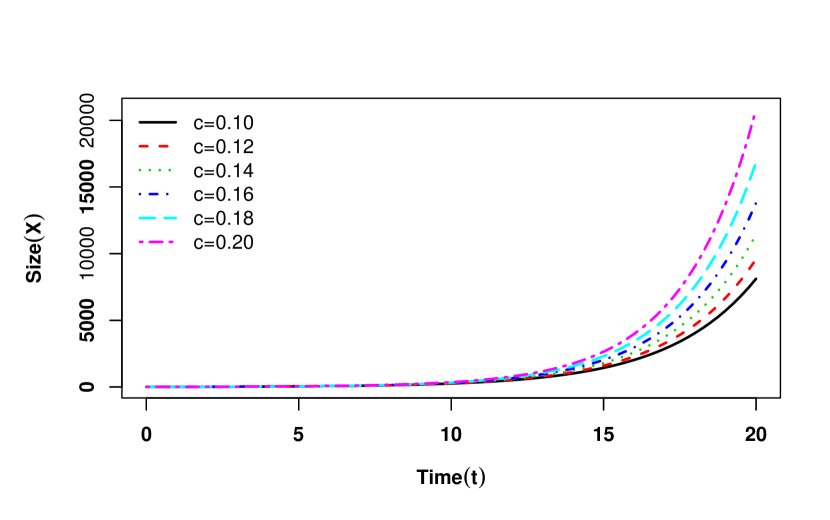

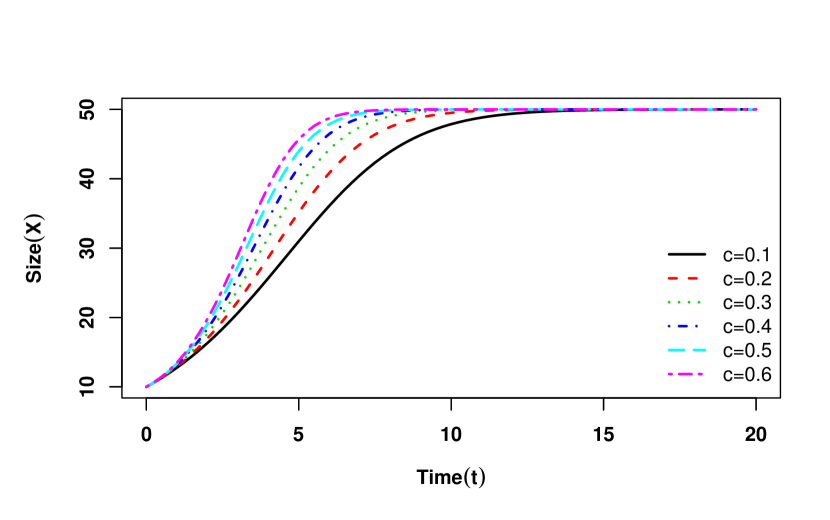

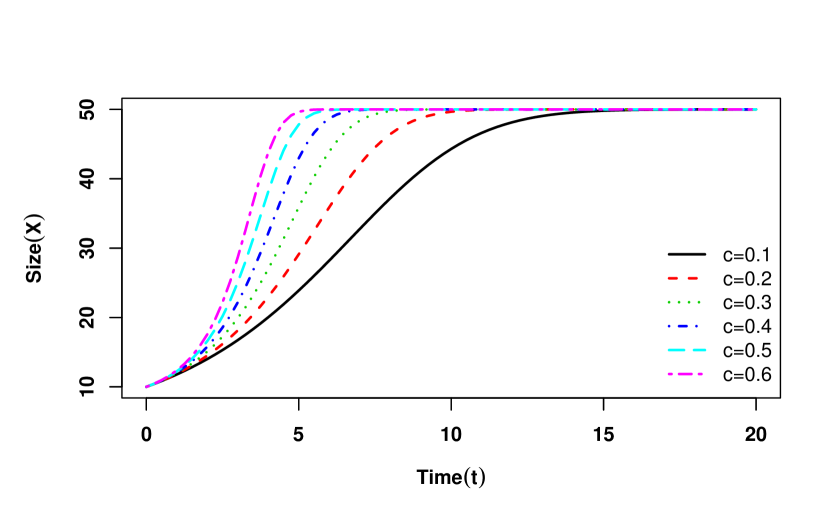

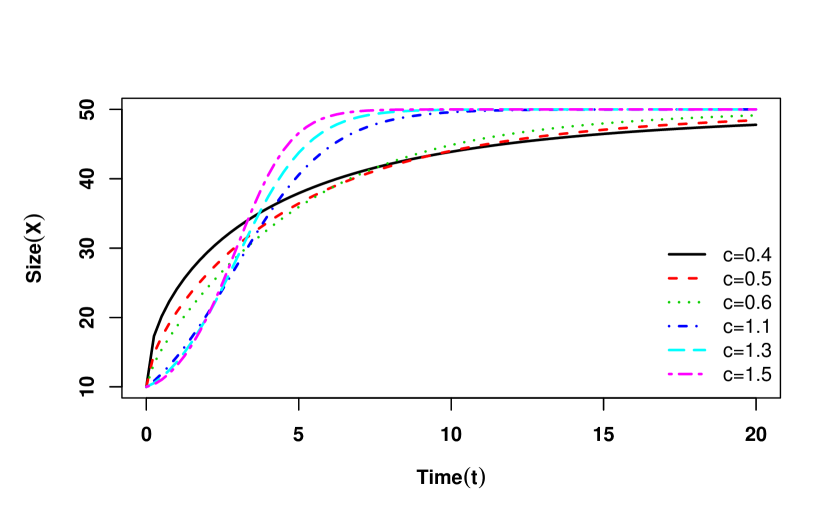

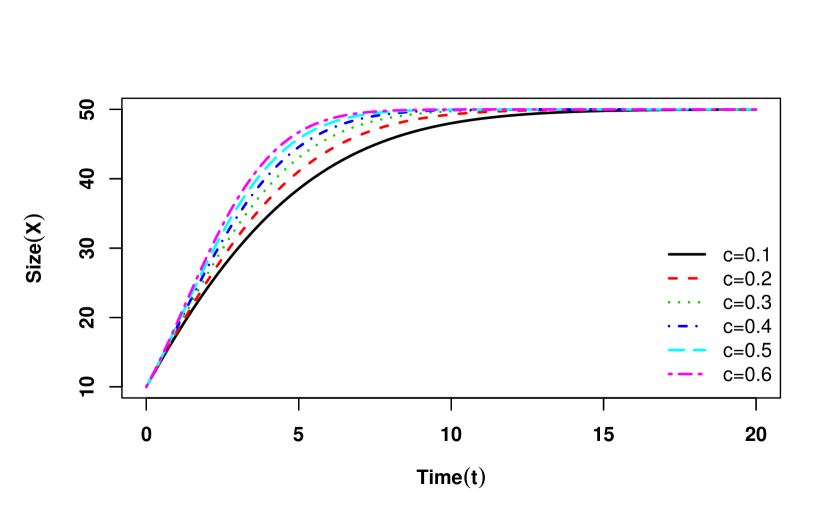

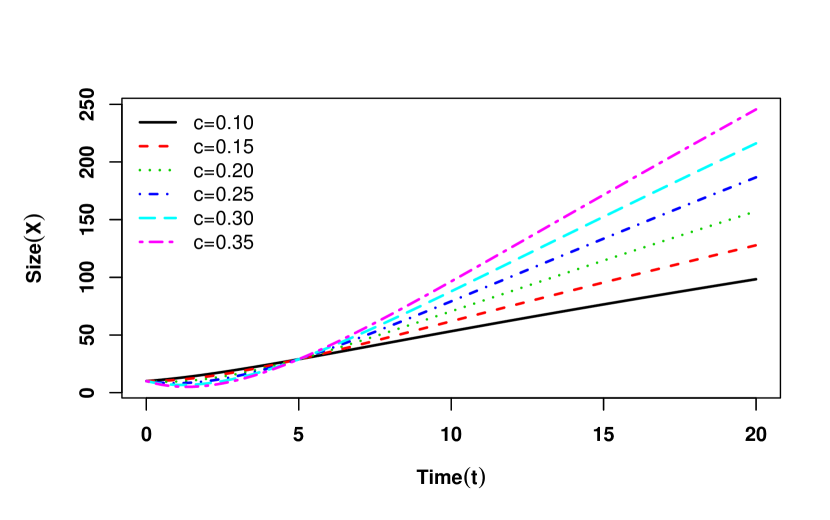

If we take this type of variation in the parameter then the eqn. (7) turns out to Korf model (Korf, 1939) (Table 2; srl. ) for which the asymptotic size tends towards and behaves like exponential model (Fig. 1(a)) and as increases increases and goes towards asymptotic size at a much faster rate. - 2.

-

3.

; :

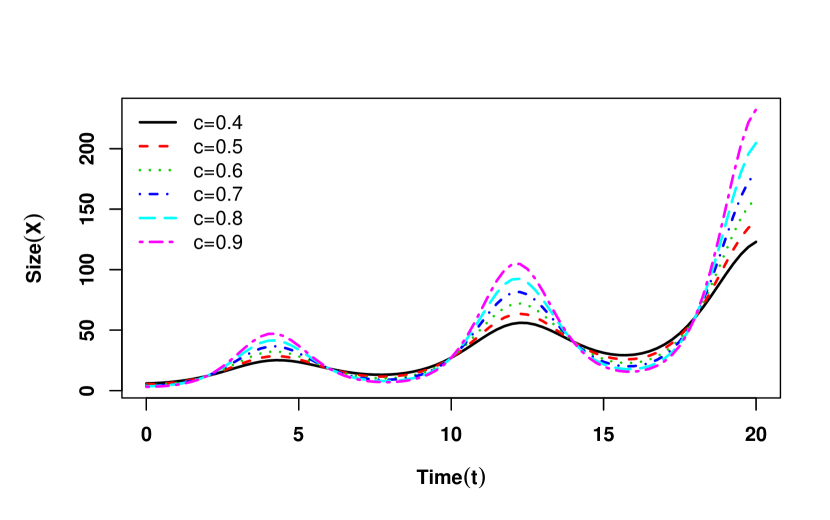

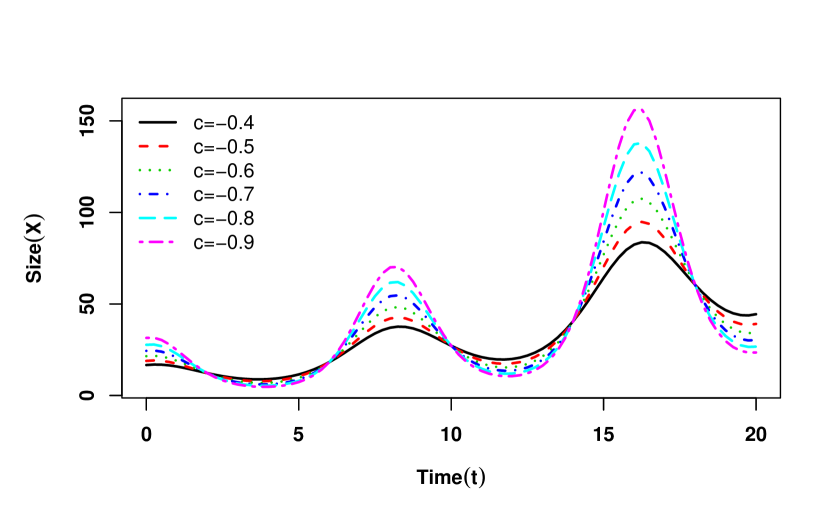

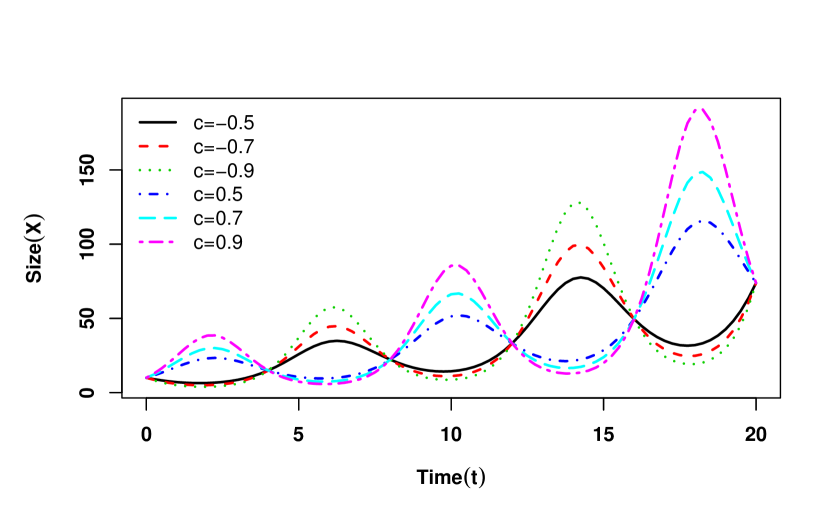

For periodically varying function of , eqn. (7) turns into a new model (Table 2; srl. ) whose asymptotic size remains but goes towards it periodically. If we keep increasing the value of we can see much bigger period in population size () and also goes towards the asymptotic size at a much faster rate (Fig. 1(c), 1(d)). If we take cosine function instead of sine function then also we get a new model (Table 2; srl. ) having similar behaviour (Fig. 1(e)).

B.1.2 Variation in logistic growth model

The logistic model is given by (Verhulst, 1838)

| (10) |

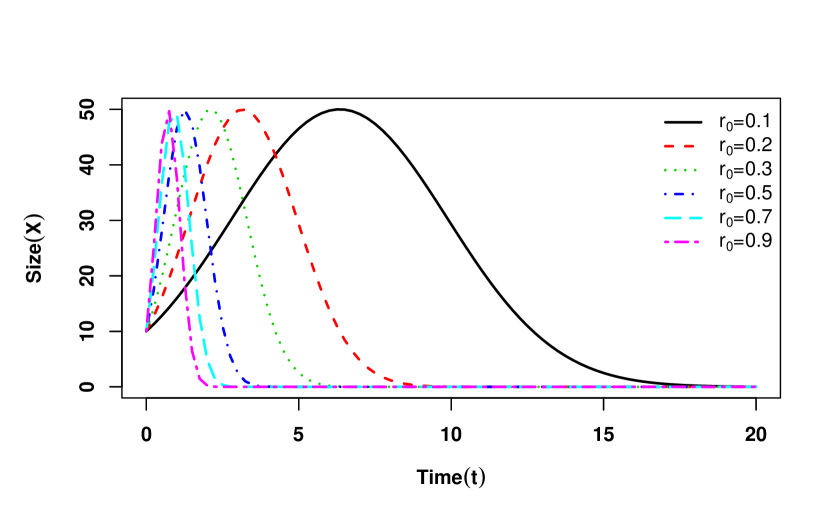

where be the population size at time , and be the intrinsic growth rate and carrying capacity (asymptotic size). Banks (1994) discussed the dynamics of the logistic equation by varying as function of time. Here, we discuss the growth behaviour of logistic equation by varying the parameter . Apart from the connection to different existing growth equations some new models are also obtained. In the following, we categorically discuss different cases.

- 1.

-

2.

; () :

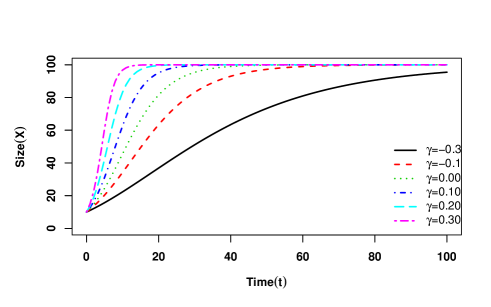

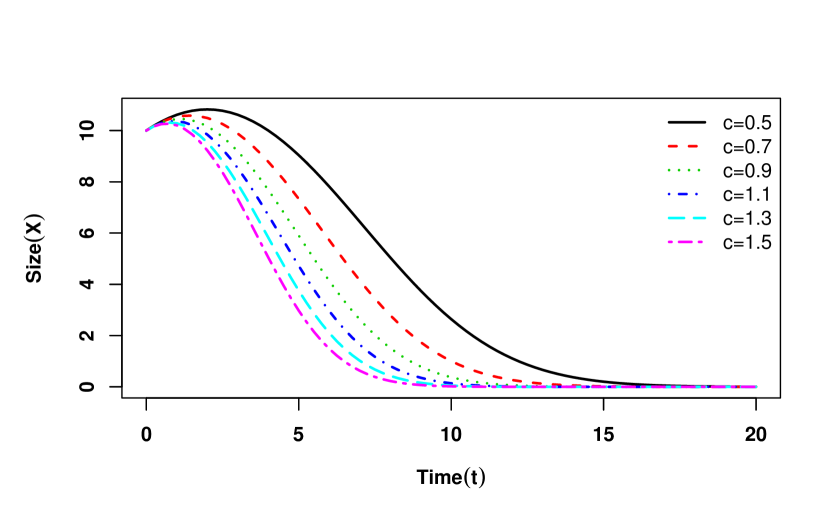

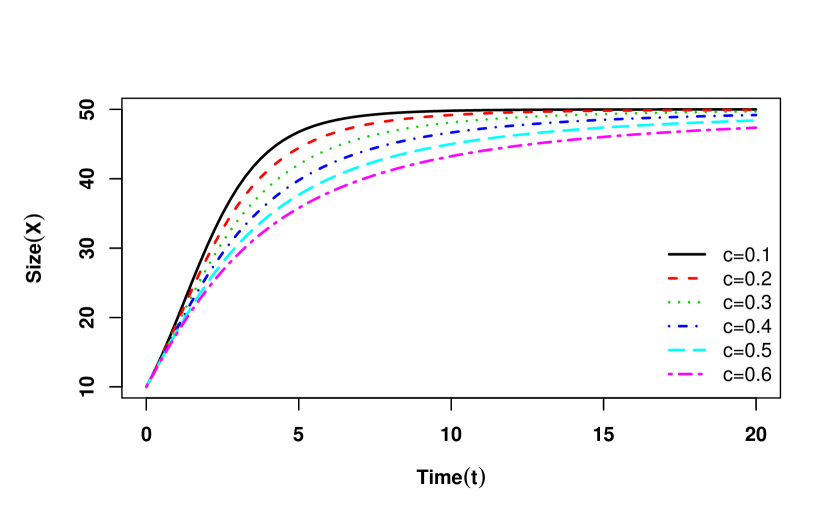

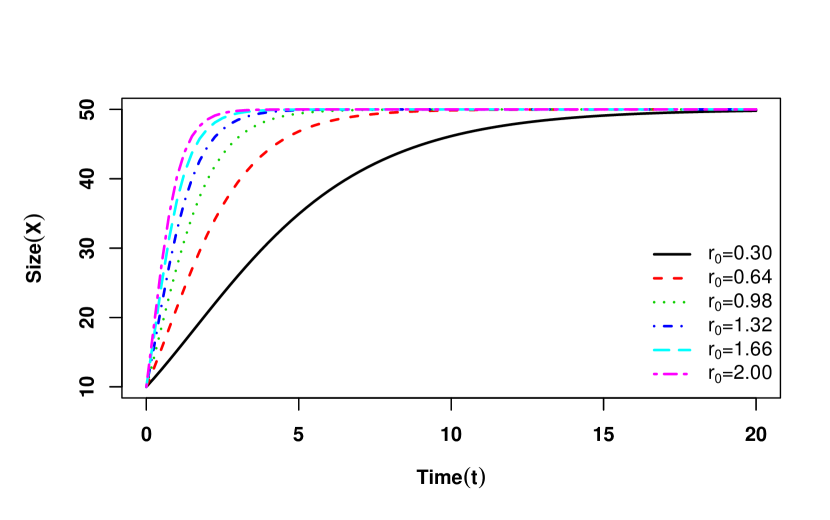

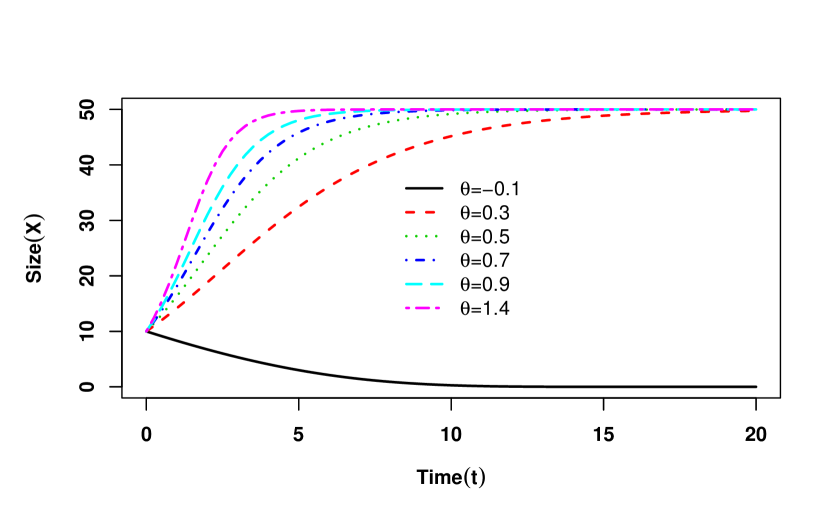

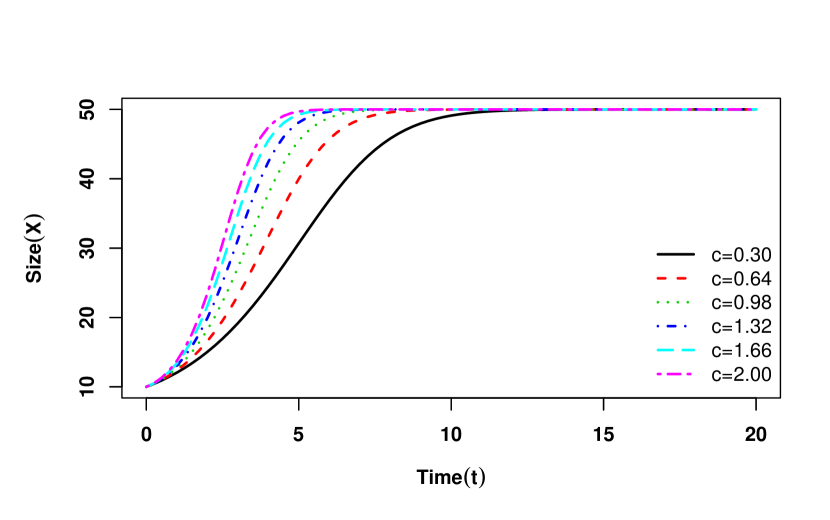

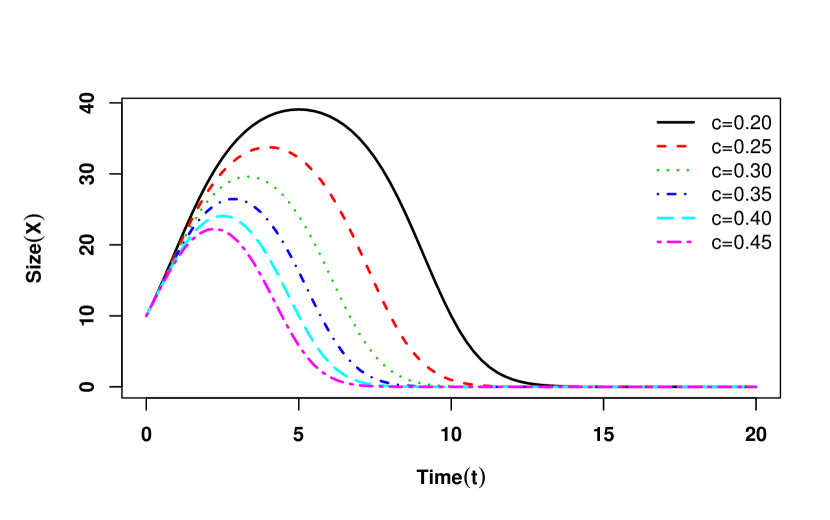

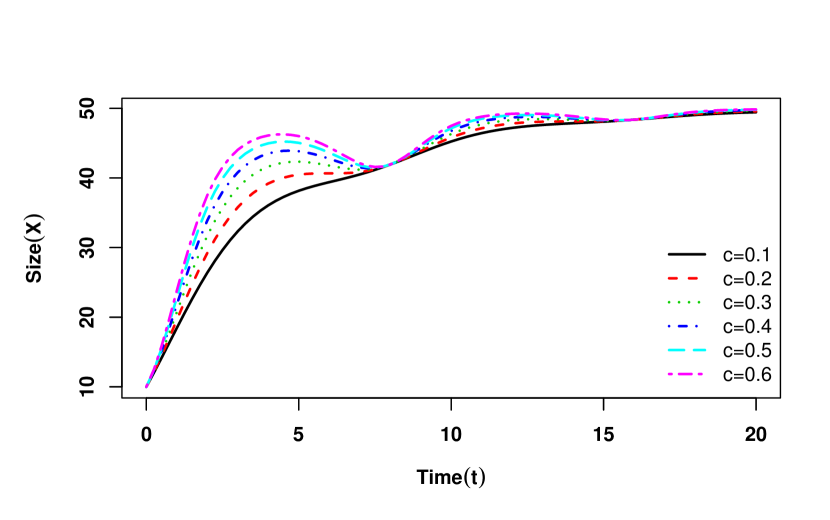

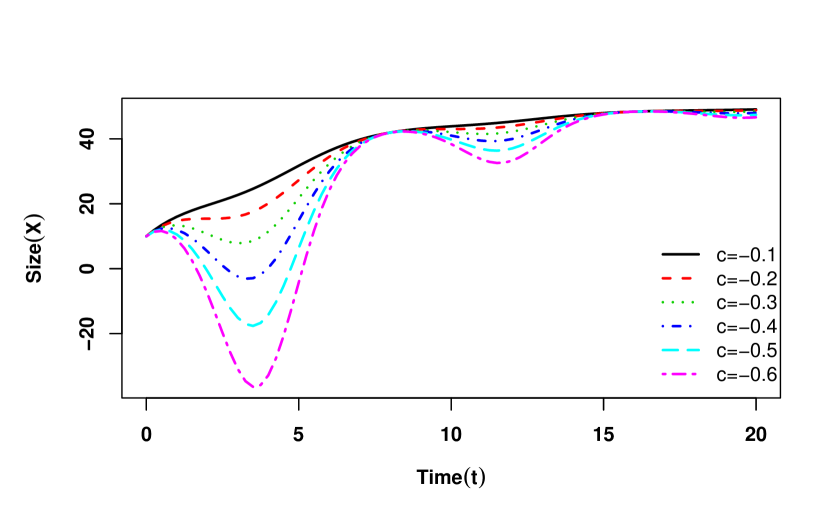

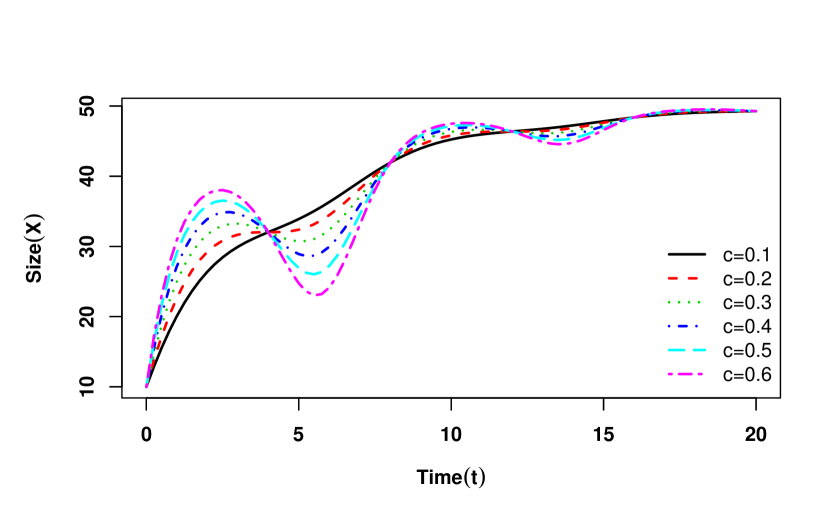

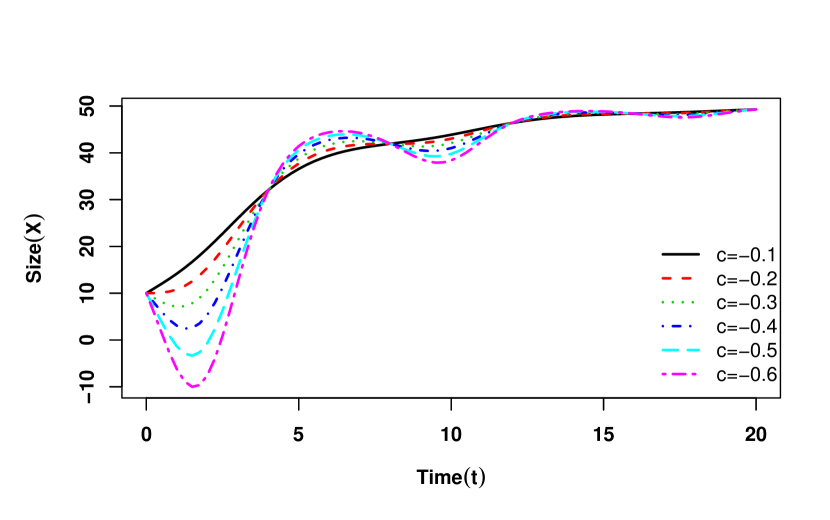

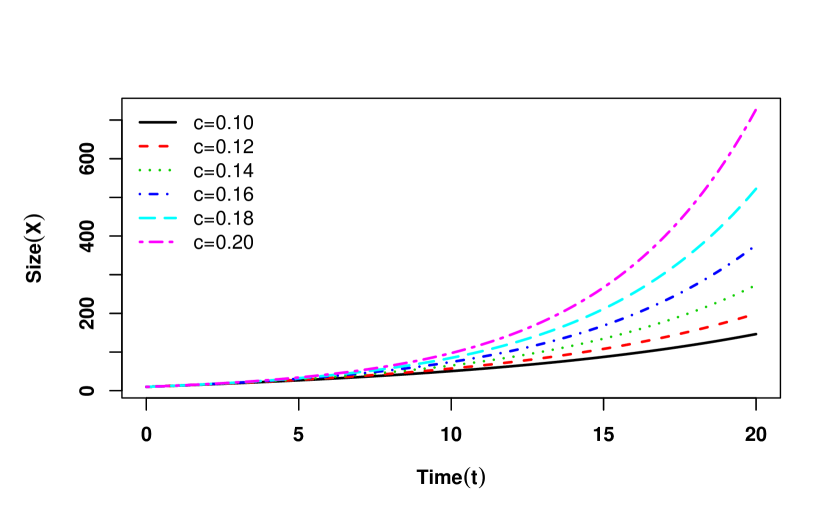

Under this transformation, a new growth equation (Table 3; srl.) is obtained. In this case growth is not monotonic. For small , first increases and then decreases to zero. As (or ) increases at a faster rate (Fig. 2(b)).

(a) , ()

(b) , ()

(c) , ()

(d) , ()

(e) , ()

(f) , ()

(g) , ()

(h) , ()

(i) , ()

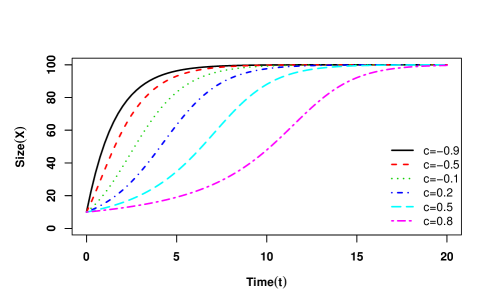

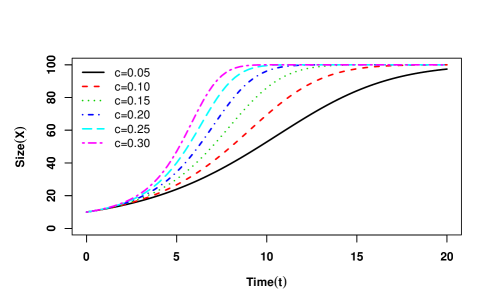

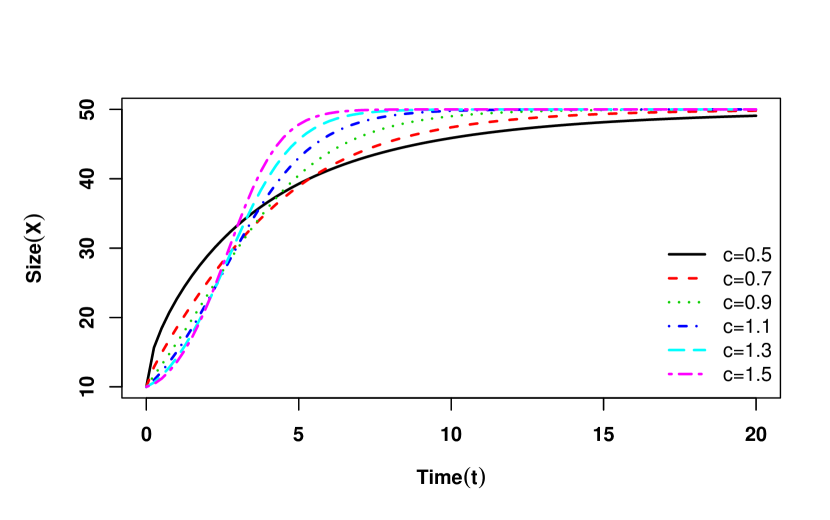

(j) , () Figure S2: Time () vs size () plot for continuously varying parameter in Logistic Model. In the first panel (Fig. (a), (b) and (c)), we consider as a linearly increasing, decreasing and polynomial function of time, respectively. In the second panel, in Fig. (d) and (e), we consider as a exponentially decreasing and increasing function of time, respectively and in Fig. (f), we consider as inverse function of time. In the third panel, in Fig. (g) and (h) varies periodically (sine function) with time and in Fig. (i) and In the forth panel (in Fig. (j)), varies periodically (cosine function) with time. In all the cases, be the initial values of the parameter . and are kept fixed. - 3.

- 4.

- 5.

- 6.

-

7.

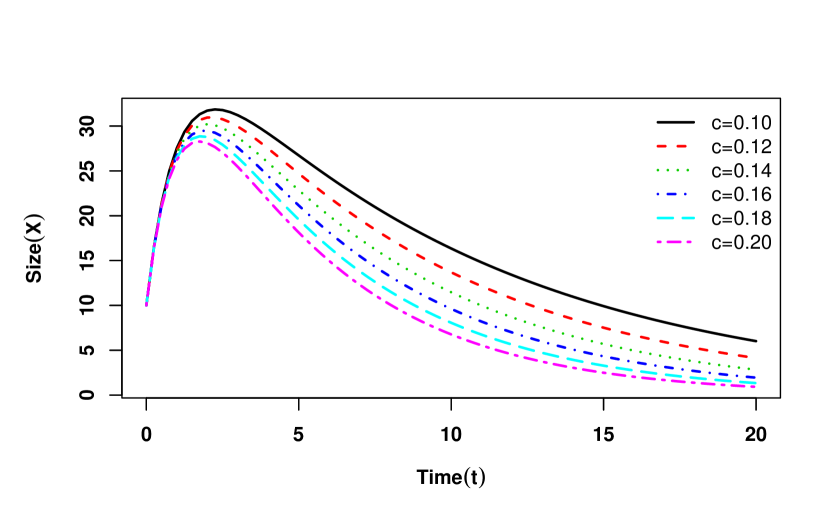

, ( ):

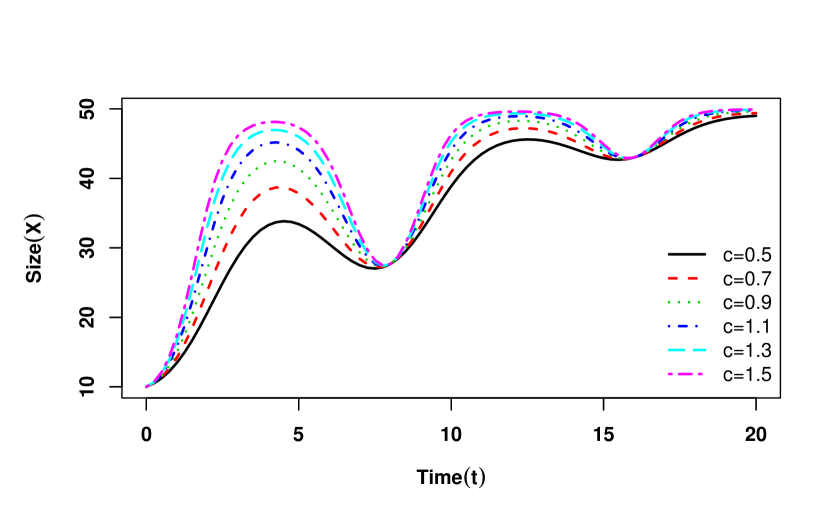

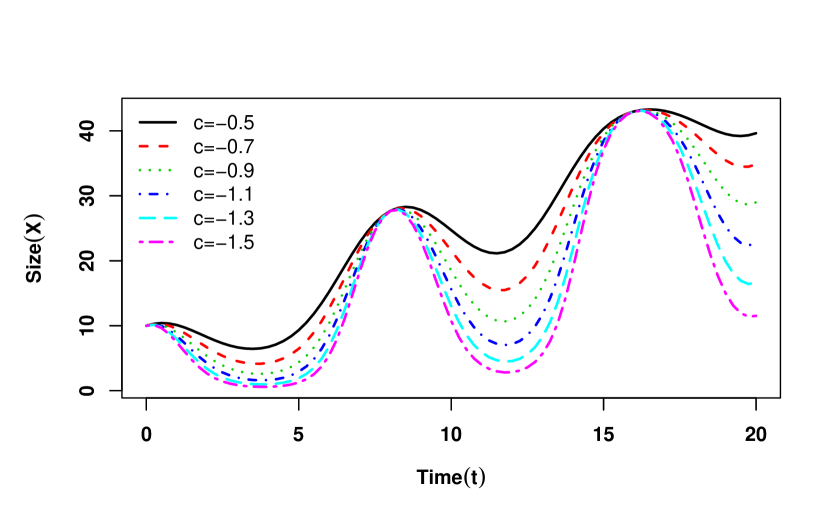

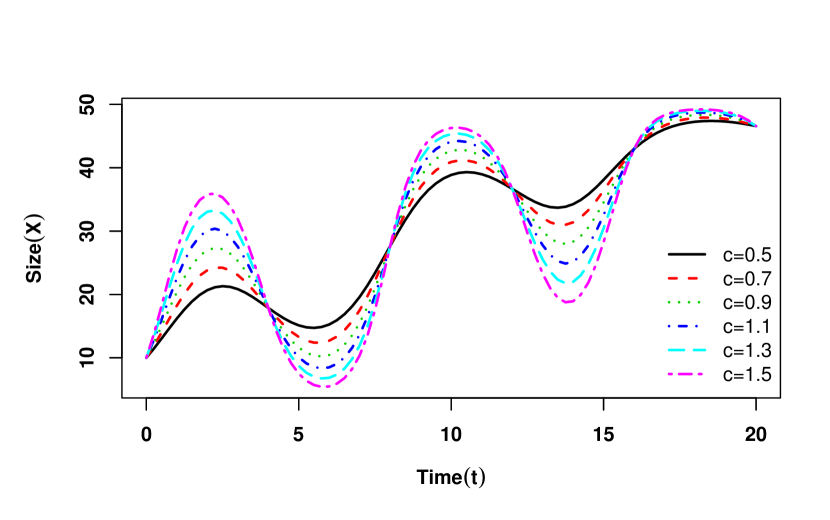

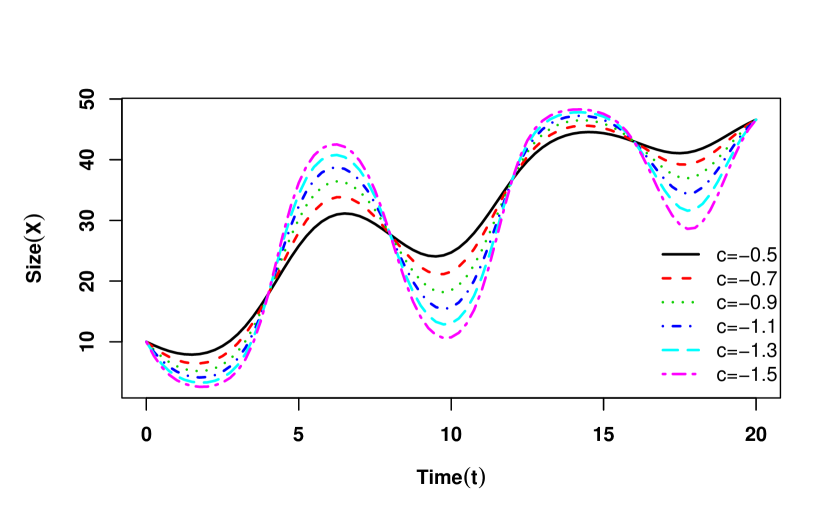

In this case, eqn.(10) turns into a new model (Table 3; srl.). For , in a damped oscillation manner (Fig. 2(g)) and also for , a similar behaviour is observed (Fig. 2(h)). If we take cosine function instead of sine function in eqn.(10), then also we get a new model (Table 3; srl.) with similar kind of behaviour (Fig. 2(i), 2(j))).

B.1.3 Variation in theta-logistic growth model

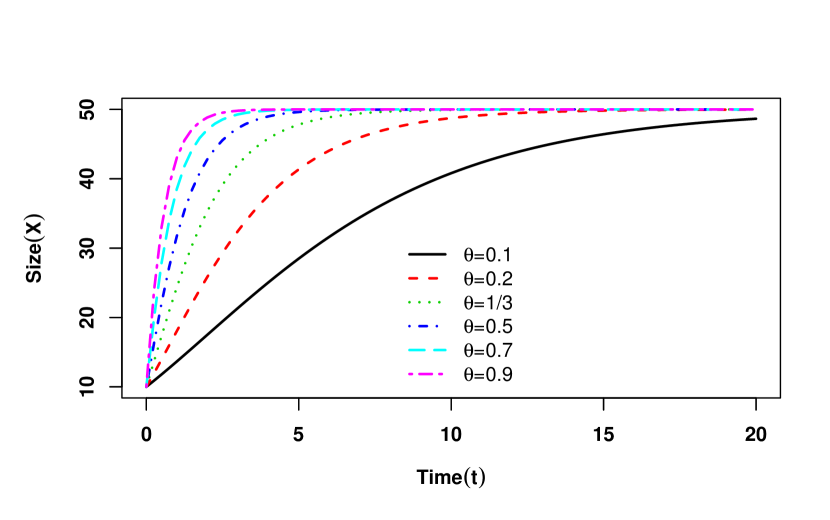

The theta-logistic model (eqn. 8) (also referred as generalized logistic) is one of the most widely used growth equations in ecological literature. The model was first proposed by Gilpin and Ayala (1973) in the concept of competitive interactive systems. Several studies are available in the literature based on this model (Sibly et al. (2005); Barker and Sibly (2008); Clark et al. (2010); Zhao and Tang (2011); Bhowmick et al. (2016) and other references there in). We consider both time and density dependent variation in and is kept as constant since almost for all the cases, the resulting growth equations do not have analytical solution. They must be solved numerically. We investigate the equations for different range of values of . In the following we categorically discuss each cases.

- 1.

- 2.

-

3.

:

If we consider this limitation in in eqn.(8), then it turns into Richard’s growth law (Richards, 1959). For negative value of , but for positive value of , (Fig. 3(b)) (Table 4; srl.). If we take equal to zero then is constant. However in application one should evaluate limiting case as demonstrated in Sæther et al. (1998). -

4.

(), :

For such variation, the eqn. (8) turns into Koya-Goshu Model (Koya and Goshu, 2013). In the revised equation the asymptotic size remains . For , there is no point of inflection i.e. no lag phase or log phase, but for , point of inflection is present in Koya-Goshu model (Fig. 3(c)) (Table 4; srl.). - 5.

- 6.

-

7.

, (), :

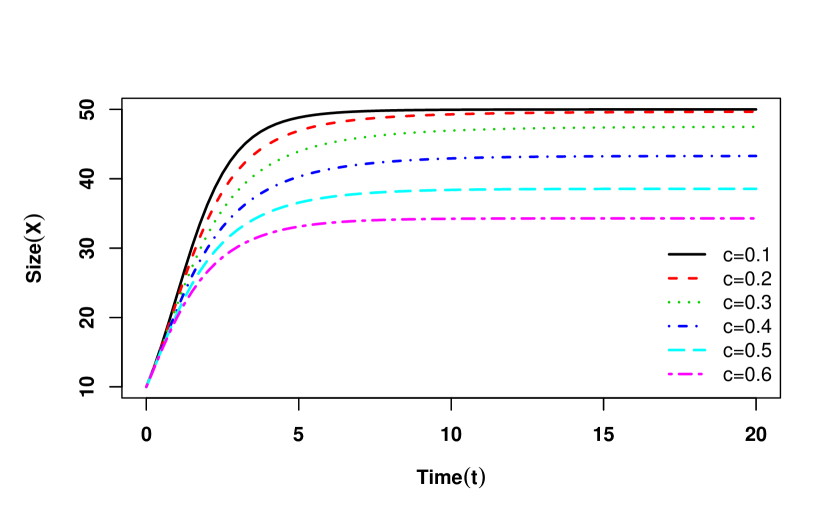

If we take this type of variation of and limitation of in eqn. (8), then it turns into extended gompertz model (Bhowmick et al., 2014) for which remains the asymptotic size and for large , goes towards the asymptotic size at a much faster rate (Fig. 3(f)) (Table 4; srl.).

(a) ,

(b) ,

(c) , (, )

(d) , (, )

(e) , (, )

(f) , (, )

(g) , ()

(h) , (, )

(i) , (, ) Figure S3: Size profile of the theta-logistic model for different choices of and . In the upper panel, in Fig. (a), we consider and , in Fig. (b), we consider and and in Fig. (c), we consider as a polynomial function of time. In the middle panel, in Fig. (d) and (e), we consider as a linearly increasing and decreasing function of time, respectively and in Fig. (f), we consider as a polynomial function of time in the presence of . In the lower panel (Fig. (g), (h) and (i)), we consider as a density dependent function to get Generalized Von-Bertalanffy Model, Crescenzo-Spina Model and Second-order Exponential Polynomial from theta-logistic Model, respectively. In all cases, be the initial values of the parameter . and are kept fixed. -

8.

, () :

For this type of density dependent variation in and limitation in eqn. (8) transforms into Generalized Von-Bertalanffy Model (Von Bertalanffy, 1960) for which and the rate of convergence depends on . For large value of , goes at faster rate towards (Fig. 3(g)) (Table 4; srl.). If we take , then eqn. (8) turns out into Von-Bertalanffy Model (Von Bertalanffy, 1949) (Table 4; srl.). -

9.

(), :

For this type of density dependent variation in and limitation in , eqn. (8) turns out into generalized gompertz model (Chakraborty et al., 2017) (Table 4; srl.). If we take , then generalized gompertz model turns into gompertz model (Gompertz, 1825). If we take , then this model turns out into second-order exponential polynomial (Chakraborty et al., 2017) for which the asymptotic size is zero (Fig. 3(h)) (Table 4; srl.). If we take , then generalized gompertz model turns out into Cresenzo-Spina model (Crescenzo and Spina, 2016) for which is the asymptotic size (Fig. 3(i)) (Table 4; srl.). Basically for , always. Thus in generalized gompertz model, for , asymptotic size is zero and for , asymptotic size is .

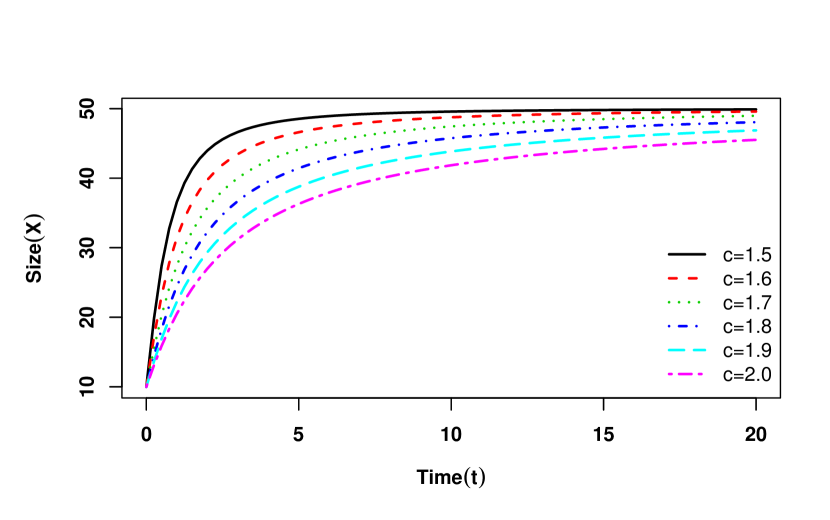

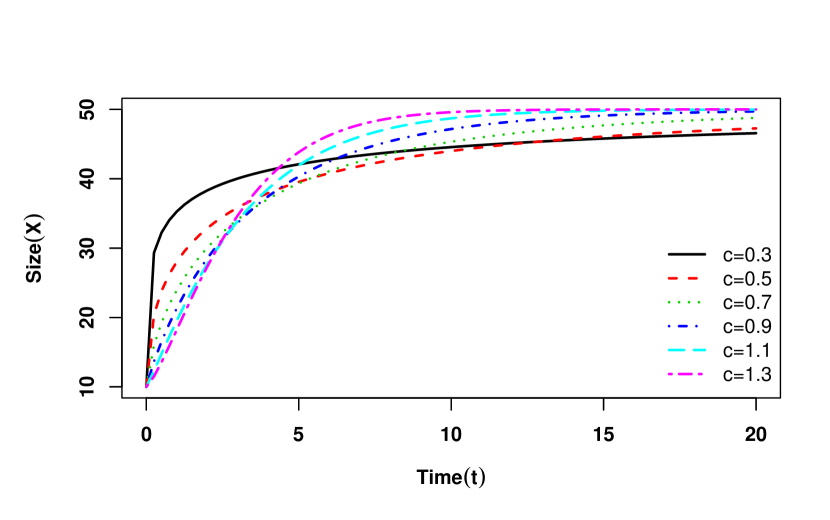

B.1.4 Variation in confined exponential growth model

In this section, we discuss various changes in the shapes of confined exponential model (eqn. 9) (also known as Monomolecular growth law) by varying the parameters in the the model. Banks (1994) had already discussed about some variation of in the confined exponential model set up and found relationship with extreme minimal value distribution. Here, we explore other possible variations. In some cases, we have also obtained new growth equations as well. In the following we categorically discuss different cases.

- 1.

-

2.

:

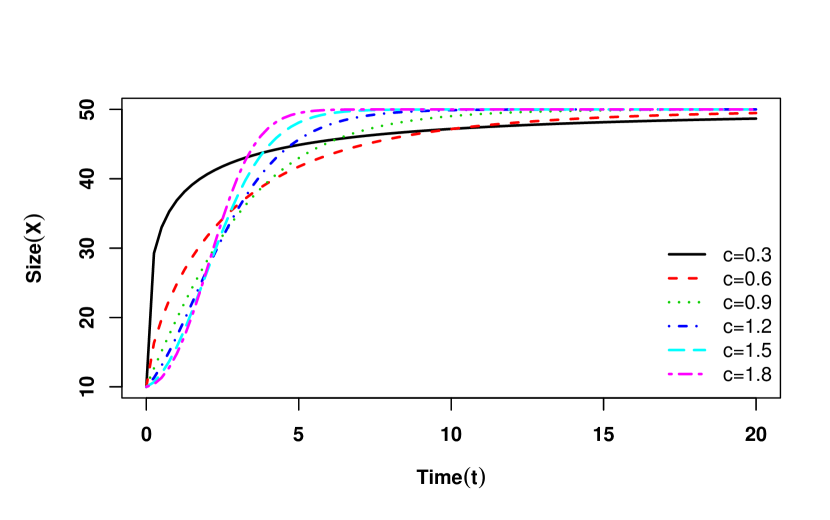

If we take this density dependent variation in , then eqn. (9) transforms into logistic model with asymptotic size (Verhulst, 1838) (Table 5; srl.).

(a) , ()

(b) , ()

(c) , ()

(d) , ()

(e) , ()

(f) , ()

(g) , ()

(h) , ()

(i) , ()

(j) , ()

(k) , ()

(l) , () Figure S4: Size profile of the confined exponential model for different choices of and . In the first panel, in Fig. (a) (b) and (c), we consider as a polynomial function, linearly decreasing and increasing function of time, respectively. In the second panel, in Fig. (d) we consider as an exponentially decreasing function of time, in Fig. (e) and (f), varies inversely and periodically with time, respectively. In the third panel,in Fig. (g), (h) and (i), varies periodically with time. In the forth panel (Fig. (j), (k) and (l)), we consider as a linearly increasing, exponentially increasing and decreasing function of time, respectively. In all cases, and are initial values of the parameters and , respectively. is kept fixed at 10. - 3.

- 4.

- 5.

- 6.

-

7.

, () :

For this periodic variation in , eqn. (9) turns into a new model in which the asymptotic size goes towards periodically with reduced amplitude (Fig. 4(f), 4(g)) (Table 5; srl.). If we take cosine function instead of sine function, then a new model (Table 5; srl.) is obtained having similar behaviour (Fig. 4(h), 4(i)). - 8.

- 9.

- 10.

B.2 Nonavailability of explicit expression of ISRP

In the previous section, we have discussed the growth models in which a parameter varies continuously with time following some specific functional form. It is to be noted that for each of the case, the final differential equation (after replacing by ) can be solved analytically or solutions are available using some special functions. In general this may not be the case and the differential equations must be solved numerically to obtain the size profile. In this section, we deal with few cases in which the analytical expression for the size variable is not available.

- 1.

- 2.

- 3.

- 4.