Achieving Efficiency in Black-box Simulation of

Distribution Tails with Self-structuring Importance

Samplers

Anand

Deo and Karthyek MurthyIndian Institute of Management, Bannerghatta Road, Bangalore 560076

anand.deo@iimb.ac.inSingapore University of Technology and Design, Singapore

487372

karthyek_murthy@sutd.edu.sg

Abstract.

This paper presents a novel Importance Sampling (IS) scheme for estimating distribution tails of performance measures modeled with a rich set of tools such as linear programs, integer linear programs, piecewise linear/quadratic objectives, feature maps specified with deep neural networks, etc. The conventional approach of explicitly identifying efficient changes of measure suffers from feasibility and scalability concerns beyond highly stylized models, due to their need to be tailored intricately to the objective and the underlying probability distribution. This bottleneck is overcome in the proposed scheme with an elementary transformation which is capable of implicitly inducing an effective IS distribution in a variety of models by replicating the concentration properties observed in less rare samples. This novel approach is guided by developing a large deviations principle that brings out the phenomenon of

self-similarity of optimal IS distributions.

The proposed sampler is the first to attain asymptotically optimal

variance reduction across a spectrum of multivariate distributions

despite being oblivious to the specifics of the underlying model. Its applicability is illustrated with contextual shortest path and portfolio credit risk models informed by neural networks.

In addition to being an integral part of quantitative risk management,

the need to estimate and control tail risks is inherent in managing

operations requiring high levels of service or reliability

guarantees. The variety of contexts for which chance-constrained and

risk-averse optimization formulations are employed serve as a

testimony to the importance of tail risk management in operations

research. Naturally, this significance is retained in the numerous

operations and quantitative risk management models which are being enriched with

the use of algorithmic feature-mapping tools (such as neural networks,

kernels, etc.,) employed to facilitate a greater degree of automation

and expressivity in mapping data to

decisions. Recent literature on modeling mortgage risk with deep neural networks

(eg., Sadhwani et al., 2020) and models incorporating contextual side information

into decision making (eg., Ban & Rudin, 2019, Elmachtoub & Grigas, 2022) serve as

illustrative examples.

With the increasing adoption of these expressive models, it is imperative that the risk management practice seeks to measure

and manage the tail risks associated with their use. In a similar vein, considerations of certifying safety, fairness, and

robustness have led to a number of

applications seeking to measure tail risks in avenues extending beyond

operations and risk management as well. Assessing the

safety of automation in cyber-physical systems

get naturally cast in terms of evaluating expectations restricted to

distribution tails

(eg., Zhao et al., 2017, O’ Kelly et al., 2018, Uesato et al., 2019),

as is the case with evaluating severity of algorithmic biases on

minority sub-populations

(Williamson & Menon, 2019, Jeong & Namkoong, n.d.).

Motivated by the importance and the challenges in measuring tail risks in a broad variety of such applications,

we consider the estimation of distribution tails of a rich class of performance functionals specified with enabling tools, such as linear programs, mixed integer linear programs, piecewise linear and quadratic objectives, feature maps/decision rules specified in terms of deep neural networks, etc., which serve as key modeling ingredients in these applications.

To describe the challenges in the tail estimation tasks we consider, suppose that denotes the loss (or cost) incurred when the uncertain variables affecting the system, modeled by a random vector realize the value For example, may denote the losses associated with a portfolio exposed to risk factors

or may capture the optimal value of the cumulative generation and transmission costs which could be incurred in meeting demand in the consumer nodes of a power distribution network.

In general, we take to be

modeling a suitable performance measure of interest.

The distribution of is not analytically tractable even in

elementary models, and related measures such as its mean, or tail risk

measures such as Value-at-Risk, Conditional Value-at-Risk, etc., are

typically estimated from samples. Estimation and

subsequent optimization of tail risks via simulation becomes

computationally expensive however, as mere sample averaging requires

about samples to achieve a

relative precision of in tasks requiring estimation

of with confidence. This

prohibitively large requirement points to the need for samplers whose complexity do not grow as severely with

decreasing to zero.

Application contexts where tail risk measurement is of central

importance, such as those arising in financial engineering, actuarial

risk, system availability, etc., have facilitated the development of

variance reduction techniques which aim to tackle this

difficulty. Prominent examples include the use of importance sampling

and splitting, potentially in combination with other variance

reduction tools such as control variates, stratification, conditional

Monte Carlo, etc; see Glasserman, (2004), Asmussen & Glynn, (2007), Rubino & Tuffin, (2009) for an overview. In particular, Importance

Sampling (IS) is seen as the primary method for combating rarity of

relevant samples in diverse scientific disciplines and is shown to

offer remarkable variance reduction in financial engineering models (see Glasserman et al., 2000, Bassamboo et al., 2008, Glasserman et al., 2008, Liu, 2015), actuarial risk models (see eg., Asmussen & Glynn, 2007, Collamore, 2002), and various queueing and reliability models (see Heidelberger, 1995, Juneja & Shahabuddin, 2006, Blanchet & Mandjes, 2009, and references therein).

The idea behind IS is to accelerate the occurrences of the

target risk event in simulation by sampling from an alternate

distribution which places a much greater emphasis on the risk

scenarios of interest. Observed samples are then suitably reweighed to

eliminate the bias introduced. We shall refer to this alternate

sampling distribution as IS distribution hereafter.

1.1. Conventional approach towards efficient IS and key challenges

Effective use of IS in all the above instances rely, however, on carefully leveraging the specific model structure to explicitly identify a suitable IS distribution.

Typically this involves an initial Step (i) seeking to select a parametric distribution family with the following desirable properties: the family should include distributions which place significantly more probability on the target rare event, while also being rich enough to mirror the large deviations behaviour of the theoretically optimal IS distribution. This variance minimizing optimal IS distribution is merely the conditional law of given the tail event of interest, and is also referred to as the zero-variance distribution (see eg., Asmussen & Glynn, 2007, Chapter 5). Identifying the best IS distribution within is then accomplished in a subsequent Step (ii) devoted to solving an optimization problem (OPT)

formulated suitably in terms of the proposed family the distribution of and level sets of

Such reliance on large deviations characterizations to

explicitly identify an effective IS distribution, while a source of strength, also helps showcase the challenges one may face in our estimation tasks

which seek to go significantly beyond the piecewise linear assumption on and independence/normality assumptions on featuring largely in the literature. Even under these narrow assumptions, execution of Step (i) above requires a case-by-case large deviations analysis leading to distinctly different choices for based on the model-at-hand. These include obtained via exponentially twisting the probability density (eg., Siegmund, 1976, Glasserman et al., 2000), twisting the hazard rate (Juneja & Shahabuddin, 2002), mixture families based on the so-called dominating points (Sadowsky & Bucklew, 1990, Honnappa et al., 2018, Bai et al., 2022), or mixtures featuring one/many big jumps (Asmussen & Kroese, 2006, Dupuis et al., 2007, Chen et al., 2018). Heuristic application of well-known techniques not accompanied by appropriate large deviations have been shown to be ineffective or counterproductive even in instances involving relatively simpler choices of (see eg., Glasserman & Wang, 1997, Juneja et al., 2007).

We next highlight that it is often impractical to invoke the specific form of the functional or that of the distribution of in their entirety, as is typically required

for formulating and solving the optimization problem (OPT) in Step (ii) above. In special cases where is multivariate normal and is additive and explicitly known, (OPT) can be written as a quadratic program (see eg., Glasserman et al., 2000, Glasserman & Li, 2005); it may additionally possess a combinatorial structure as in Glasserman et al., (2008), or may be written as a mixed integer quadratic program as in Bai et al., (2022). For some non-Gaussian (OPT) could get formulated as a dynamic control problem even in instances as elementary as independent sums (eg., Dupuis et al., 2007). Such variedly nuanced formulation of the Step (ii) optimization problem (OPT) could be impractical for more involved objectives or non-Gaussian . Besides this formidable challenge, there is no reason to expect the resulting (OPT) to be convex or solvable in general, and the identified IS distribution to be easy to sample from.

1.2. Novelty of the proposed approach and main contributions

In order to overcome the above challenges,

we recast the search for effective IS distributions instead as follows: “Can we find a transformation whose respective push-forward measure (i.e., the law of ) readily induces an effective IS distribution when deployed across a large class of models?”. This reframed pursuit seeking to induce an effective IS distribution implicitly via a map is a radical departure from the existing prominent approaches (which, as described in Section 1.1, seek to explicitly identify an efficient IS distribution). While this reframed enquiry is spurred by the bottlenecks highlighted in Section 1.1, it is not clear apriori if such widely applicable transformations should exist.

In turn, a primary contribution in this paper is to exhibit a fixed family of transformations which, despite being oblivious to the loss and the underlying distribution, is proved to offer asymptotically optimal variance reduction for a wide variety of models requiring only a mild nonparametric structure.

For a high-level view of why such transformations capable of inducing effective IS distributions could exist, we point to the following ubiquitous yet unexploited phenomenon of the self-similarity of the optimal IS distributions. This notion serves as a key ingredient in our approach and is explained as follows: For any suppose that denotes

the theoretically optimal IS distribution for estimating

in other words, is just the law of

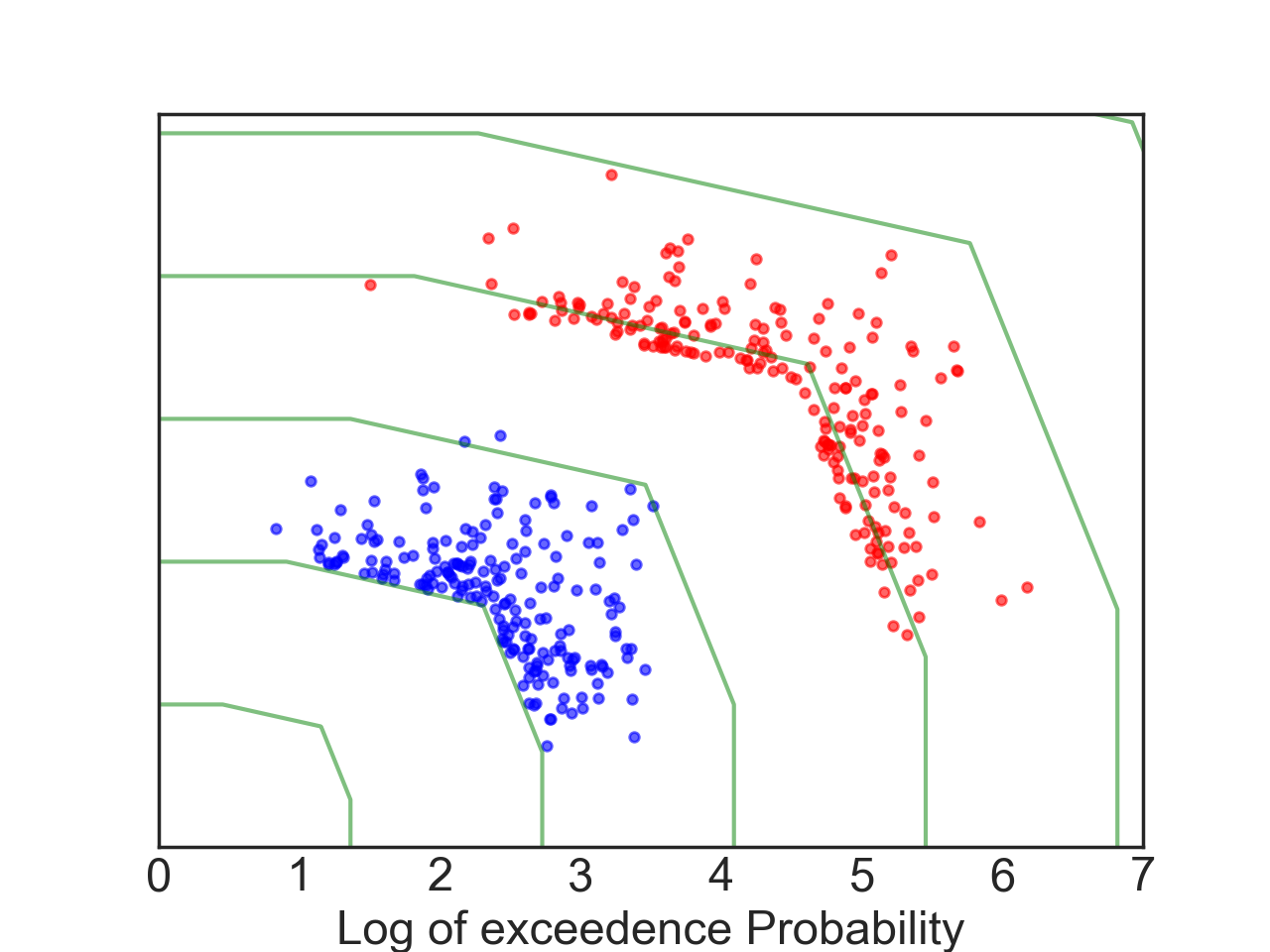

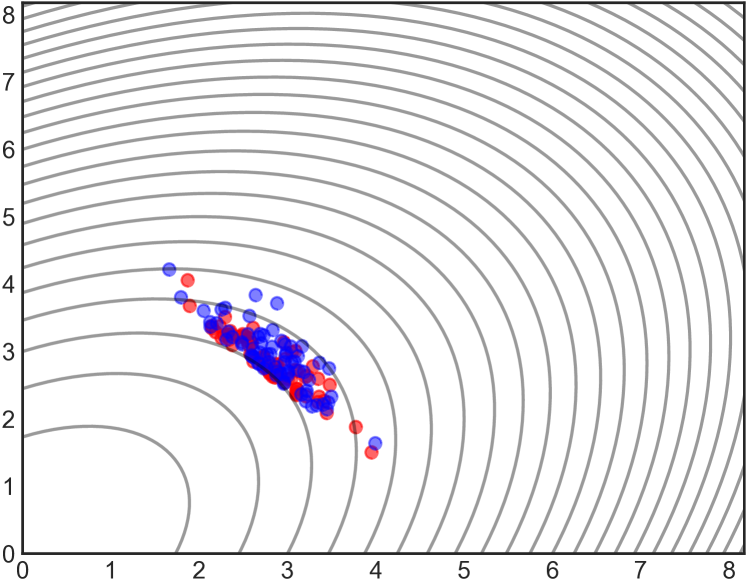

conditioned on (see Asmussen & Glynn, 2007, Chapter 5). As we show that suitably scaled versions of distributions and share similar large deviations behaviour and concentrate their mass on identical sets even if the level is only a fraction of the level Figure 1 below offers a graphical illustration of this self-similarity holding across three different distributions for

Figure 1. Illustration of the notion of self-similarity of

optimal IS distributions: Samples from the distributions

(displayed in blue and red respectively) reveal

that they share similar concentration properties for three

distribution choices of informed by a Gaussian copula

with correlation The levels are such that the

probabilities of exceeding these levels are

approximately and The contours (drawn in green) represent level sets of

derived from a ReLU

neural network with weights given by the matrix with

rows and vector

(a)Normal marginals,

(b)Weibull marginals,

(c)Exponential marginals,

To leverage this remarkable similarity in how the samples of and concentrate, we seek transformations which automatically replicate the large deviations concentration properties of from how the much more frequently occurring samples of manifest. As a product of this entirely novel approach, we are able to make the following main contributions in this paper.

1) Tail modeling framework characterizing self-similarity in optimal IS distributions: Building on the tail modeling approach introduced in de Valk, (2016), we identify a general class of models for which the above self-similarity in optimal IS distributions can be made precise in terms of large deviations principles (Proposition 4.1). This self-similarity phenomenon, being nonparametric in nature, is not limited to objectives/distributions fitting within specific parametric assumptions. As a result, our framework becomes the first to feature a rich set of models with

a)

objectives including, but not limited to, those specified in terms of tools such as linear programs, mixed-integer linear programs, piecewise linear and quadratic objectives, feature-maps/decision-rules informed by neural networks, etc., (see Assumption 2.1); and

b)

a wide variety of light and heavy-tailed multivariate distributions for (see Assumptions 3.1, 3.2, 5.2 and the examples in Tables 2 - 4).

2) Novel approach to IS: We exhibit a fixed family of transformations (see (22)) which, despite being oblivious to the loss and the underlying distribution, is able to induce IS distributions with desirable properties in the considered generality: In particular, the target event is shown to occur exponentially more frequently under the induced IS distributions, while also ensuring that the resulting conditional excess loss samples mirror the large deviations properties of the theoretically optimal The need to explicitly formulate a good IS density family and the optimization problem (OPT) (as described in Section 1.1)

gets obviated with the radical discovery of these transformations, thereby rendering the selection of IS distributions entirely algorithmic.

3) An efficient IS algorithm with wider applicability: The use of the IS transformation in (22) results in a novel IS algorithm whose execution requires only oracle access to the evaluations of loss and the probability density of (see Algorithm 1).

We derive large deviations asymptotic for the distribution tails of and show that the proposed sampler offers asymptotically optimal variance reduction in the considered generality (Theorems 4.1 - 5.3).

This is to be contrasted with the efficient IS changes of measures available, largely on a case-by-case basis, for specific highly stylized objectives and typically under normal distribution assumptions, i.i.d assumptions, or specific copula assumptions in the literature. The proposed sampler joins the recent line of enquiry initiated in the last couple of years (see Bai et al., 2022, Arief et al., 2021) striving to make IS amenable for more sophisticated objectives. The earlier works in this pursuit have restricted the focus to normal distributions and objectives which can be modeled or approximated by piecewise linear functions, with the complexity of the approach scaling less graciously in terms of the number of pieces involved. A distinguishing feature of the proposed sampler is that it is the first in the literature to consider a spectrum of multivariate light and heavy-tailed distributions simultaneously and achieve log-efficiency across this spectrum despite tackling several challenging and important objectives (such as value of linear programs, contextual optimization objectives, etc.) for which efficient IS algorithms are unavailable even under Gaussian distributional assumptions.

We demonstrate the utility of the IS scheme in the evaluation of probabilities of (a) large losses in a portfolio credit risk setting, and (b) large delays in contextual routing.

The proposed sampler for portfolio credit risk also serves as an entirely novel addition that extends the scope of applicability of the line of research pursued in

Glasserman et al., (2000), Glasserman & Li, (2005), Bassamboo et al., (2008), Glasserman et al., (2008), Liu, (2015) to credit risk models which employ diverse copula or algorithmic approaches such as neural

networks.

Following Glynn, (1996) and Hong et al., (2014), a follow-up to this work (Deo & Murthy, 2021) demonstrates how the IS scheme proposed in this paper for estimation of distribution tails can be employed to gain efficient variance reduction in Value-at-Risk and conditional Value-at-Risk estimation. Its use in further optimization tasks, such as minimizing conditional Value-at-Risk, is explored in Section G.

The rest of the paper is organized as follows. Following a description of the problem, our novel IS procedure is introduced in Section 2. The tail modeling framework introduced in Section 3 is used to establish the large deviations asymptotics and the self-similarity property of optimal IS distributions in Section 4. Section 5 identifies transformations capable of inducing efficient IS distributions and presents the main results verifying the asymptotic optimal variance reduction properties. An application to the portfolio credit risk setting and results of numerical experiments are presented in Sections 6 and 7. Proofs and additional useful examples are given in the accompanying supplementary material.

2. The problem considered and the proposed IS procedure

Vectors are written in boldface to enable differentiation from

scalars. For any

and we have

denoting the respective component-wise operations. Let

denote the positive

orthant and

denote its interior.

2.1. A description of the problem considered

Suppose that

denotes the cost incurred when the uncertain variables

affecting the problem, modeled by a random vector

realize the value

While the loss

may be expressed as a linear combination of uncertain

variables in some simple settings, the inherent nature of managing operations under resource constraints often results in expressed suitably as the value of an optimization formulation. We consider the task

of estimating the probabilities or expectations associated with tail

risk events of the form for a threshold

suitably large. The need for having a control over likelihoods of

these risk scenarios is inherently present in many operational

settings affected by uncertainty, due to the need to keep the costs

below a target risk level (or) to meet a service-level agreement which

ensures that a target quality of service is

met. In many applications, high losses are experienced when the random

vector takes undesirably high values in the positive orthant; for

example, large travel durations in vehicle routing instances leading

to large delays. Thus, without loss of generality, we take the set

specifying risk scenarios, to be a subset of the positive orthant

here

denotes the support of the distribution of Considering a rich class of loss functions satisfying Assumption 2.1 below, we aim to design efficient IS schemes for estimating the distribution tails of

Assumption 2.1.

The function satisfies

the following conditions:

a)

the set is

contained in for all sufficiently large and

b)

for any sequence of

satisfying we have

where is a positive constant and the limiting function

is such that the

cone is non-empty.

Assumption 2.1b merely specifies asymptotic homogeneity,

which implies that larger the value of farther is the target rare

set from the origin. The set is

necessarily a cone because

for any Examples 2.1 - 2.3 below provide a non-exhaustive yet indicative list of objectives for which Assumption 2.1 is readily satisfied.

A discussion on verifying Assumption 2.1b when only oracle access to loss evaluations are available is presented in Section F. As Assumption 2.1 does not require convexity,

the treatment in this paper is applicable even if is neither convex nor concave.

Example 2.1(Piecewise affine functions, value of mixed integer

linear programs).

Suppose that can be written as

(1)

where is a bounded subset of and

is a bounded function which

serves to capture terms, if any, which do not involve the random

vector In the case where is a finite set,

could represent a piecewise affine function as in,

where is a positive integer,

and for If the set is described by linear and/or integer

constraints and if the function is affine, we have that

(1) is a linear (or) a mixed integer linear

program. With the notation used in Assumption 2.1, we

have and

for the example in

(1); see (Rockafellar & Wets, 1998, Proposition

7.29). The requirements in

Assumption 2.1 are met, for example, if

at least one vector

in the collection lies outside the negative orthant

or, in other words, if

. Objectives in many planning problems, such as

project evaluation and review networks, linear assignment or

matching, traveling salesman problem, vehicle routing problem,

max-flow, minimum cost flow, etc., satisfy this requirement either

in the native formulation or in the respective dual formulation.

Example 2.2(Piecewise quadratic functions).

As an extension to Example 2.1, one may also consider

piecewise quadratic functions of the form

where is a positive integer, are

-symmetric matrices, and for

As long as the matrices are not all

identically zero, we have and

in this

example. When the support of is bounded from below, the

requirements in Assumption 2.1 are automatically met

if, for example, at least one of the eigen values of the matrices

in the collection is positive. If is instead a piecewise-minimum as in the requirements are readily checked to be

satisfied with if the collection is positive

semidefinite.

Example 2.3(Models using contextual information via feature maps/decision rules).

Suppose that is written as a composition of

functions as in

where is an objective

measuring the cost incurred by plugging in a specific decision

rule or a function approximation based on the feature map

(see

Ban & Rudin, (2019) for an example use of feature-based decision

rules in newsvendor models). In simple settings, one may take the

feature map to be merely or, may include

cross-terms in the feature vector as in

Motivated by the proliferation of deep neural networks in learning

expressive feature maps, one may

consider the feature map to be specified in terms of

several function compositions defined recursively as in,

(2)

In the above, the operation

is a positive integer and for each

are weight parameters in a neural network with

rectified linear activation units (ReLU) in the -th layer. We

have as the dimension of the resulting feature

map. Refer Sadhwani et al., (2020) for a treatment of

their utility in identifying relevant features in the context of

modeling mortgage default risk. For the map

considered in (2), we have

In general, suppose the feature map is such that

for some

and every sequence of

satisfying Then for the desired

convergence in Assumption 2.1b, we have,

and , if, for example, is such that

as

as

with constants satisfying

One may include an additional

composition to consider models of the form,

(3)

where is seen as contextual side information,

is a feature map that models the dependence of

cost vector in terms of the side information and

additional uncertainty and

describes the constraints; see, for example,

Elmachtoub & Grigas, (2022) for details and Section 7.1

for a contextual shortest-path example. Here suppose that the

feature map is as above and the cost mapping

is positive and satisfies

for

and some If

we let we have

Assumption 2.1(b) satisfied with

One can identify more functionals which

satisfy Assumption 2.1b) by taking linear combinations (that is, if and satisfy Assumption 2.1b), so does ) or

compositions suitably (as in Example 2.3) based on modeling needs. Further, the requirements in Assumption 2.1b) can be recast

naturally if a particular application requires the set quantifying

risky scenarios, to be a subset in a different orthant.

2.2. The proposed importance sampling method

The proposed importance sampling (IS) procedure for fast evaluation of

where is taken to satisfy Assumption 2.1, is

presented in Algorithm 1 below. A key ingredient of Algorithm 1 is a multiplicative transformation of the form,

(4)

where is a hyper-parameter choice and is a suitably defined vector-valued map. One may view the components of as a multiplicative stretching of the components of as in with the extent of stretch of each component determined by the respective exponent

Input:Threshold independent samples

of hyperparameter

specify if the exponent is chosen from (7) to be either (or)

Procedure:

1. Transform the samples: For each sample

compute the transformation,

(5)

2. Compute the associated likelihood: For each transformed

sample compute the respective likelihood ratio as,

(6)

where is the probability density of and is the Jacobian of the transformation (see Table 1 for expressions of along with prescribed choices of ).

3. Return the output estimator: Return the IS average

computed as in,

Algorithm 1Self-structuring IS procedure for estimating

We provide efficient variance reduction guarantees for Algorithm 1 when the transformation is used in (5) with the exponent fixed to any one of the following two choices:

(7)

While the former relies on knowledge of the growth parameter in Assumption 2.1, the latter is model-agnostic in the sense that it is free of any dependence on or the distribution of As a result, is applicable more broadly in distribution tail estimation tasks including those in which evaluations of is available only via oracle queries. A discussion on how the choice can be advantageous in preserving convexity of the objective if one is engaged in further optimization tasks (such as minimizing Conditional Value-at-Risk) is presented in Section G.

In

Algorithm 1, the samples for the proposed IS procedure are taken

as

where are independent and identically distributed as

The bias resulting from counting the fraction of samples lying

in the target rare set, instead of that of is adjusted by

multiplying with the respective likelihood ratio term

as in,

(8)

to obtain the estimator returned by Algorithm 1.

As with any IS procedure, the

likelihood ratio term is taken to be the ratio between the

probability densities of and evaluated at (see eg., Asmussen & Glynn, 2007, Chapter 5). With a standard change of variables formula involving the Jacobian of the transformation, can be written conveniently as in Table 1 below. This involves plugging in the choice of in the Jacobian determinant

(9)

almost everywhere, to obtain the associated

likelihood ratio Consequently, as verified in Proposition 2.1 below, the resulting estimator has no bias.

Table 1. Choice of the exponent in (4) and the respective Jacobian determinant

Suppose that the transformation in (5) is employed with either (or) and the likelihood ratio in (6) is computed with the respective Jacobian determinant in Table 1. Then for any the estimator

is unbiased. In other words,

Moreover there exists a map

such that

for almost every

The choice of the transformation in Algorithm 1, which implicitly specifies the IS density, is guided by the

self-similarity properties of the distribution of to be

made concrete with the large deviations framework in following

Sections 3 - 4.

Building on this framework, an account on the rationale behind the

choice of the IS transformation and its variance

reduction properties is offered in Section 5. Roughly

speaking, the transformation seeks to suitably replicate the

concentration properties of the theoretically optimal IS distribution

from observations which are not as rare. This is

facilitated by taking the parameter such that and the

event though also a tail risk event, is much more

frequently observed in the initial samples when compared to the target

event Even if the parameter is relatively negligible when compared to

the level we show the variance of the resulting IS estimator is

small as in,

(10)

as the estimation task is made more challenging by taking

The relationship (10) holds for any

arbitrary and any choice of

which is taken to be slowly varying in and satisfying

see Theorem

5.1 in Section 5 for a precise statement

of the variance reduction result and Section 3.1

for the definition and examples of slowly varying functions.

Recall from Section 1.1 that traditional IS approaches typically require solving a non-trivial optimization problem (OPT) to identify the best distribution within a chosen family IS distribution Unlike these procedures, the selection of IS density in our approach is simplified to that of selecting the single parameter minimizing the sample variance. The robust variance reduction

guarantee for Algorithm 1, obtained for any which is slowly varying in enables to confine the search for a good choice of the hyper-parameter to be within a relatively narrow collection. One may execute the selection of by means of cross-validation

over candidate choices of (or) with a retrospective approximation based search procedure we provide in Section 7 together with numerical examples.

Contrast the reduced variance of the IS estimator in

(10) with that of the naive sample average which merely

counts the fraction of samples in the

target rare set. In the case of naive sample average, the variance is

and the coefficient of variation grows as in

as Thanks to

(10), the coefficient of variation of the proposed IS

estimator grows only as where

can be arbitrarily small, thus requiring only a

negligible fraction of samples compared to that required by the naive

sample average. Any estimator which meets the relative error guarantee in

(10) is said to offer asymptotically optimal variance

reduction and is referred to as logarithmically

efficient. Please refer Asmussen & Glynn, (2007, Chapter 6) for a discussion

on the significance on logarithmic efficiency and why it is a natural

and pragmatic efficiency criterion for estimation tasks pertaining to

rare events.

3. A nonparametric tail modeling description and associated

LDP

A function is

said to be regularly varying with index

if for every

(11)

When referring to (11), we write or,

if there is a need to explicitly specify the

exponent . The function is a canonical example

of the class If then is specifically

referred as slowly varying. Some examples of slowly varying

functions include

where where or

any function satisfying

A function

can be written as for some

slowly varying and Evidently,

(11) is a characteristic of all homogeneous functions and

univariate polynomials. By allowing to be an arbitrary real

number and to be any slowly varying function, the class

possesses substantially improved modeling power.

See, for example, Borovkov, (2008) for a detailed

treatment of the properties of the class

3.2. Assumptions on the probability distribution of

Let and

respectively denote the

complementary c.d.f (also known as survival function) and the

cumulative hazard function of the component in

The marginal components are required to satisfy Assumption

3.1 below.

Assumption 3.1.

For the marginal components

are such that is continuous, strictly increasing

in an interval of the form and

for some

Common examples of distributions which satisfy Assumption

3.1 are as follows: standard exponential

distribution where satisfies

standard normal distribution where

as

satisfies Weibull distribution with shape

parameter where satisfies

Other examples of parametric families, along

with respective tail parameters are given in Table

2 in Appendix

B. This large class includes distributions which are light-tailed and as

well as heavy-tailed distributions of the Weibull type. The case where

the marginal distributions possess even heavier tails, such as

log-normal, pareto, regularly varying distributions, etc., are treated

later in Section 5.3.

To describe the joint distribution of , we first consider the standardizing transformation,

which “standardize” the marginal distributions to that of standard

exponential.

Lemma 3.1.

The marginal distributions of the components for

are identical and is given by,

for

As with the wide-spread practice of modeling joint distributions in

terms of copulas (eg., Embrechts et al., 2001), this

standardization restricts the focus to the dependence structure

without getting distracted by the potential non-identical nature of

marginal distributions of

Assumption 3.2.

The probability density of admits the form

(12)

where satisfy the following: There

exists a limiting function

such that,

(13)

for any sequence of

satisfying and

A sufficient condition for to satisfy Assumption 3.2 is that its pdf is of the form where is multivariate regularly varying (see Section B for a definition of multivariate regularly varying functions and a precise statement of the sufficient condition). The nonparametric nature of the assumption

suggests that a wide variety of dependence models satisfy Assumption

3.2. Indeed, most commonly used distribution families

such as multivariate normal, multivariate , elliptical densities,

archimedean copula models, exponential family with any regularly

varying sufficient statistic, extreme value distributions, suitable

members of generalized linear models, log-concave densities, etc. can

be verified to satisfy Assumption 3.2. Table

4 in Appendix B is intended

to offer a sample of distribution families which satisfy the marginal

and joint distribution conditions in Assumption 3.1

- 3.2 and to serve as a quick reference for the

limiting function in Assumption

3.2.

Example 3.1(Gaussian copula).

Suppose that has a joint distribution given by

a Gaussian copula with correlation matrix Given a copula with

density the respective probability

density can be expressly computed as,

.

Therefore

where

and

is the complementary

c.d.f. of the standard normal variable. Thus, in this example, we

have from the notation in (12) that

and

Since

as we have

and subsequently,

compactly, as We therefore have the

limiting in Assumption 3.2 as

Properties of the limiting function and a continued account of the distributions satisfying Assumption 3.2 are presented after introducing the tail large deviations principle in Section 3.3.

3.3. Tail large deviations principle with as the

rate function

A sequence of random vectors is said to satisfy a

Large Deviations Principle (LDP) with rate function and speed

if,

for every closed subset and open subset

Theorem 3.1 below establishes the LDP which is useful in the

context considered.

Theorem 3.1(Tail LDP).

Suppose that is a random vector whose probability density

admits the form (12), where the functions

satisfy the convergences in

(13) for any sequence of

satisfying and

Then the sequence

satisfies the large deviations principle with rate function

and speed .

The following useful properties of the limiting function

in (13) are deduced

from the conditions in Assumption 3.2 and the

conclusion in Theorem 3.1.

Conversely, any function which satisfies

the above conditions can be used to readily specify a joint

distribution for which has standard exponential marginals and

satisfies the tail LDP. This is verified, for instance, by considering for which

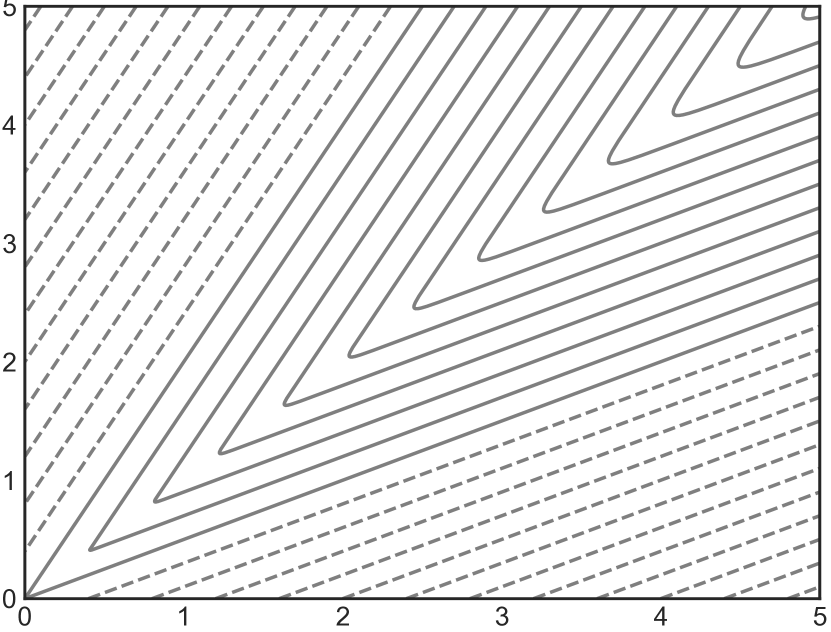

Figure 2. Illustration of the level sets of

capturing different strengths of the positive

(indicated (+)) or negative (indicated (-)) tail correlations

between the components of Range of axes

=[0,5]

(a)Gaussian copula(+)

(b)Gaussian copula (-)

(c)Clayton copula (+)

(d)Clayton copula (-)

While the rate

function is unique for a given distribution for which the

tail LDP holds, it is instructive to note that there may be multiple

distributions which give rise to the same limit Indeed,

the relation “has the same rate function in the tail LDP”

is an equivalence relation, and every function satisfying

properties (a) - (c) in Lemma 3.2 specifies a

equivalence class of distributions for the random vector

Thus, the nonparametric nature of the limiting function

offers a great amount of expressive power in capturing the joint

dependence features observed in the the tail regions. The hazard

functions in Assumption

3.1, on the other hand, offer flexibility in terms

of specifying marginal distributions with various tail strengths.

4. Large deviations characterizations and zero-variance IS distributions

We begin by characterizing the exponential rate at which

decays as in,

where the function which grows to infinity as

is identified in terms of the marginal hazard

functions described in Assumption

3.1, and the constant is identified in

terms of the marginal tail parameters

and the limiting functions

and in Assumptions 2.1 and

3.2. In order to state the result,

let us define

and

as,

(14)

where denotes the

component-wise inverse

with specifying the

left-continuous inverse of the hazard function

Theorem 4.1(Tail asymptotic).

Suppose that the marginal distributions of the components

of the random vector

satisfy Assumption 3.1 and the standardized

vector is such that the tail LDP in

Theorem 3.1 holds. Further suppose that the limit

exists.

Then, for any satisfying Assumption 2.1,

(15)

as here the non-negative constant

is given by,

(16)

As a consequence of Theorem 3.1, the tail asymptotic in

(15) holds automatically for any joint distribution

specified via Assumptions 3.1 -

3.2. While there is a rich literature on tail risk

probabilities of the form where

are independent, the treatment for more general

objectives which arise in modeling operations exist only for specific

instances. As examples, we have Glasserman et al., (2000) deriving asymptotics of

the form (15) for a specific quadratic objective

motivated from the delta-gamma approximation of portfolio

losses. Likewise,

Juneja et al., (2007), Blanchet et al., (2019), Ahn & Kim, (2018), Bai et al., (2022)

derive asymptotics of the form (15) considering

piecewise linear motivated from settings requiring

evaluation of the likelihood of excessive project delays, cascading

failures in product distribution and banking networks, safety in

intelligent physical systems, etc. These results rely, however, on

exploiting the specific structure of and the distributional

assumptions such as being multivariate normal, or elliptical, or

possessing independent components. On the other hand, Theorem

4.1 is applicable for as general as the

instances considered in Examples 1-2.3 and across a broad spectrum of distributions.

Remark 4.1(Sufficient conditions on existence of

).

Let

and

With

the limit when exists,

satisfies,

(17)

for in see the discussion at the end of

Appendix D for additional explanation. Then

for any such that the limit in

(17) expressly evaluates to For

all such that we have that the

limit in (17) exists if

for some positive

constant or more generally if

for

some As the latter condition merely restricts

the magnitude of oscillations of the ratio

we have that the limit

exists for commonly used parametric distribution

families.

To interpret the tail asymptotic (15), first note that

the occurrence of

in the

denominator in (15) is aligned with the phenomenon that

the “heaviest tail wins”. This observation is well-known within the

specialized context of sums of random variables

(see, for eg., Hult et al., 2012, Example 8.17). Thus, as is expected, the presence of an heavier tail results in

larger probability for

With characterized as in (17) in terms

of the ratio the appearance

of in (15) captures the differences in tail

heaviness of the marginal distributions of In the

simpler case where all the components are identically distributed, we

have If, for example, is the component with

the heaviest tail in and if

as then

for some constant if on the other

hand, then

The same description is applicable in higher

dimensions where

Recall from Section 1.1 that the theoretically optimal IS distribution, which possesses zero variance in the estimation of is merely the conditional distribution

(18)

For brevity, let be such that the

for

Proposition 4.1 below gives an LDP for the collection For the LDP reveals how a suitably scaled version of can be seen to concentrate in regions similar to that of In what follows, let be as defined in (16) and functions be defined as below:

Proposition 4.1(Self-similarity in zero variance distributions).

Under the assumptions in Theorem 4.1, the collection satisfies LDP with rate function and speed as Further, if is such that and as then

where is any closed subset of and the respective .

Building on the large deviations characterizations in Sections 3 - 4, this section aims to (i) bring out the rationale behind the choice of employed in Algorithm 1; and (ii) establish the optimal variance reduction properties of the IS estimator returned by Algorithm 1.

5.1. Deducing effective IS transformations from large deviations

The zero variance distribution in (18) is not practical as a choice of IS distribution as its specification relies on the unknown quantity Despite this limitation, the zero-variance distribution is often utilized as a guide for identifying a good choice of IS distribution. Indeed, most verifiably effective IS schemes seek to identify a proposal IS distribution which possess relevant aspects of

the respective zero-variance IS distribution and approximate it in a suitable manner (see, for eg., Juneja & Shahabuddin, 2002, Asmussen & Glynn, 2007, Chapter 6).

In Definition 5.1 below, we instead seek transformations such that (i) the distribution of and the zero-variance distribution in (18) share similar large deviation properties; and (ii) the risky scenarios in the target rare set occur exponentially more frequently under the distribution of

Throughout this section, let denote a mapping with domain and co-domain to be and denote the conditional realization satisfying

(19)

Definition 5.1.

For a given loss density and a family of bijective maps is said to be rate-function preserving for with speed-up if the following hold as

(i)

the collection satisfies LDP with the rate function thereby coinciding with the rate function of LDP satisfied by the zero-variance based counterpart and

(ii)

Observe that the dependence on in requirement (i) of Definition 5.1 is via (19). The requirement (ii) in Definition 5.1 stipulates that, under the change of measure, the target event occurs roughly as frequently as the less rare event In particular, due to Thm. 4.1 and ,

thus rendering to be exponentially larger than when Here, recall that Proposition 5.1 below gives a sufficient condition for to be rate-function preserving.

Proposition 5.1.

Given a loss and density satisfying the conditions in Theorem 4.1, a family of maps is rate-function preserving for with speed-up if as

(20)

Since the characterization in (20) can be viewed as uniformly over for any compact Thus, to obtain a speed-up Proposition 5.1 suggests that it is sufficient if the realizations of in relevant regions are stretched multiplicatively by a suitable factor. The multiplicative factor may need to be different component-wise based on the indices determining the heaviness of distribution tail of the components . Corollaries 5.1 - 5.2 below assert that the transformations

(21)

and

(22)

introduced in Section 2.1, in turn, seek to accomplish this component-wise multiplicative stretching and are rate-function preserving with speed-up for suitable classes of loss and density

Corollary 5.1.

Consider any and as Suppose that the loss satisfies Assumption 2.1 with the given and the density satisfies the requirements in Theorem 4.1. Then

uniformly over in compact subsets of The sufficient condition in (20) is satisfied as a consequence and therefore, the collection of transformations in (21) is rate-function preserving for with speed-up

Corollary 5.2.

Consider any as Suppose that the loss satisfies Assumption 2.1 for any and the density satisfies the requirements in Theorem 4.1. Then we have

uniformly over in compact subsets of The sufficient condition in (20) is satisfied as a consequence and therefore, the collection of transformations in (22) is rate-function preserving for with speed-up

A numerical illustration. Figure 3 below

provides a pictorial illustration of the rate-function preserving property by plotting samples from the conditional

distributions observed for the loss A fixed

number of samples from the zero-variance IS distribution are plotted

in red colour in Figures 3(a) - 3(c) below

considering different distribution choices for In

particular, are taken to have identical normal marginal

distributions in Figure 3(a), exponential marginal

distributions in Figure 3(b), and heavier-tailed Weibull

marginal distributions for which in Figure

3(c). To illustrate cases where the concentration of

conditional distributions happen in different regions, the joint

distributions are taken to be given by i) Gaussian copula with correlation coefficient = 0.5 in Figure 3(A) ii) a -copula with degrees of freedom = 1 in Figure 3(B), and iii) independent copula in Figure

3(c). In order to facilitate an easy comparison across these different choices of joint distributions, the numbers and are taken to be such that and in each of these cases. An identical number of samples of the IS random vector computed from the chosen values of for each of the above

distributions, are plotted in blue colour in the respective sub-figures in Figure 3. In this setup, the following observations are readily inferred from Figure 3.

(a)Gaussian marginals,

correlation

(b)Exponential marginals,

with copula

(c)Weibull marginals with

uncorrelated

(d)

(e)

(f)

Figure 3. Figures (a) - (c) plot independent samples from the zero-variance distribution (in red) and that of the IS vector (in blue) to illustrate their identical concentration behaviour. Contours indicate the level sets of the respective joint distributions. Figures (d) - (f) show the respective histograms for involved in the transformation .

The zero variance and the IS samples tend to concentrate in the same

neighbourhoods in all the three cases considered in Figures

3(a) - 3(c) as asserted by Proposition

5.1. Regardless of the distinctions in the

regions where the zero variance distribution

concentrates, the blue conditional IS samples replicate the concentration in the same

neighbourhood.

To gain intuition behind this phenomenon, we first see that the

multiplicative factor in the

transformation ensures

that the IS vector is more likely to take more extreme

values than Here the exponent ensures that

the components are relatively magnified only to the extent

necessary. Indeed, a quick examination by applying the definition of

in (7)

to the red points in the respective cases in Figure 3

reveals the following observation: The distribution of

concentrates in the neighbourhood of

the points in Figure 3(f), unlike

those in Figures 3(d) - 3(e) where its

concentration is in the vicinity of While a naive

multiplication by the factor will result in both components

being magnified, the introduction of

lets the conditional distribution of concentrate appropriately

near the axes in the heavier-tailed case in Figure

3(c). Thus the transformation is crucial here in

adjusting the magnification of different components of such that

the transformed vector concentrates measure in

the regions deemed suitable by the zero-variance IS

distribution.

Recall the IS estimator

returned by Algorithm 1 is the sample mean computed from independent replications of the random variable,

where and

with as the Jacobian of the map . Here the map employed in Algorithm 1 can be seen to coincide with the rate-function preserving transformations (21) - (22) deduced in Section 5.1. Let denote the second moment of With being the average of independent samples of the variance of is given by If one were to take the naive estimator then as explained in Section 2.2, the resulting second moment is and the relative error scales as Theorem 5.1 below

establishes that the second moment for any , thereby offering nearly optimal variance reduction when considering the lower bound

In order to state Theorem 5.1, let us introduce a regularity

condition on the marginal distributions of

Assumption 5.1.

There exists such that for every the

cumulative hazard function, is

either a convex or concave function over the interval

The condition in Assumption 5.1 is readily satisfied for

the examples in Tables 2 -

3 in Appendix B and for

other commonly used probability distributions.

Theorem 5.1(Logarithmic efficiency).

Suppose satisfies Assumptions 3.1 -

5.1 and the limit exists. For the loss

suppose that satisfies Assumption

2.1 and the limiting function is such

that is not identically zero for

Then for any choice of parameter in the IS

transformation (4) which is taken to be slowly varying

in the family of estimators is

logarithmically efficient in estimating

that is,

(23)

5.3. Log-efficiency in the presence of

heavier-tailed distributions

Here we present the counterpart for Theorems 4.1 and

5.1 when one or more of the components of

are heavier-tailed than considered in Assumption

3.1. Interestingly, the same Algorithm

1 is shown to offer asymptotically optimal variance

reduction in the presence of heavier-tailed distributions. As in

Section 3, we write

for In

addition, let

Assumption 5.2.

For any for which

does not satisfy Assumption 3.1,

is continuous and strictly increasing in the interval , and

for some

Assumption 5.2 enriches Assumption

3.1 by including the possibility that, if the

hazard function for is not regularly varying, then the hazard

function for is instead regularly varying. This immediately

brings commonly used heavier-tailed distributions such as log-normal,

pareto and regularly varying distributions under the framework

considered. Indeed, if is log-normally distributed, we have

satisfying

Instead, if is a pareto or

regularly varying random variable, we have

for some

and a slowly varying function in this case,

(see Table 3).

Since the case where all the components satisfy

Assumption 3.1 is treated in the sections before,

we proceed without any loss of generality by assuming here that there

exists at least one component for which Assumption

3.1 is not satisfied. Let us assign

(24)

if the limit exists. Here,

denotes the component-wise

inverse with

specifying the

left-continuous inverse of the hazard function.

We proceed assuming that the loss

satisfies the following variation of Assumption

2.1.

Assumption 5.3.

Suppose that the function

satisfies Assumption

2.1 and the limiting function is such

that

for all and some limiting function

For instance, in the examples considered earlier in Section

2, we have the resulting

and

for the linear and quadratic losses in Examples 1-2.3 respectively. We have the following counterparts to

Theorems 4.1 & 5.3 in the presence

of heavier tailed distributions.

Theorem 5.2(Tail asymptotic).

Suppose that the marginal distributions of the components

of the random vector

satisfy Assumption 5.2 and the standardized

vector is such that the tail LDP in

Theorem 3.1 holds. Further suppose that the limit

in (24) exists. Then for any

satisfying Assumption 5.3,

(25)

where the non-negative constant

Theorem 5.3(Logarithmic efficiency of Algorithm 1 in

the presence of heavier tails).

Suppose that the random vector satisfies Assumptions

3.2 - 5.1, 5.2

and the limit in (24) exists. For the

loss suppose that satisfies Assumption

5.3 and the resulting limiting function

is such that is

not identically zero for Taking and the choice in the IS

transformation (4) to be slowly varying in the

second moment satisfies (23) and therefore

the family of estimators is logarithmically

efficient.

While Theorems 5.1 & 5.3 prove asymptotically optimal variance reduction at the entire generality considered, we also point out that the proposed IS procedure is not suitable in its current form for example in certain tasks where Assumptions 1-4 are not satisfied: these include for example where is a bounded random variable, or in tail estimation for steady-state simulation.

6. Application to Portfolio Credit Risk

Efficient IS schemes for estimating excess loss probabilities of a

portfolio of loans have been considered in

Glasserman & Li, (2005), Bassamboo et al., (2008), Glasserman et al., (2008). A salient feature of these approaches

is the flexibility to have correlated loan defaults informed suitably

via Gaussian or extremal copula models. The repertoire of loan default

probability models considered in the literature since then have

expanded to include machine learning based approaches aiming to

capture more intricate interactions between the underlying covariates;

see, for example, Sirignano & Giesecke, (2019), Sadhwani et al., (2020) and references

therein. The treatment in this section capitalizes on the generic

applicability of the proposed IS scheme to demonstrate how efficient

samplers can be similarly devised in this

setting.

To introduce the default model studied here, consider a portfolio of

loans indexed by belonging to

types. For any , let denote

the type of loan , denote the indicator random variable that

loan defaults over a fixed horizon of interest, denote the

exposure upon its default, and denote

loan-specific factors (such as original interest rate, original

loan-to-value, original debt-to-income ratios, FICO score, pre-payment

penalty, etc.) which are fixed for a given loan. The average loss

incurred by the portfolio is If we let denote the average of the

exposures, then it is clear that For a given our objective is to estimate the probability of

the excess loss event,

(26)

which is the event that the incurred loss exceeds a given fraction of

the maximum loss. To restrict the focus to main ideas, we take the exposure to be

fixed for every and satisfy

where is the maximum exposure level.

The joint distribution of the default variables is

taken to be determined by the loan-specific variables

and some common stochastic factors

which affect all loans. The common factors

may capture region-level economic effects, such as those given by

unemployment level, median income, etc., whose evolution is uncertain

over the time horizon of interest.

Conditioned on the default indicators

are taken to be independent and the respective

conditional default probabilities are specified by the family of

functions as in,

(27)

almost surely; in the above expression,

and

is a parameter modeling the rarity of loan defaults. While

the functions are typically modeled as members of

parametric families (see eg., Sirignano & Giesecke, 2019), we only require Assumption 6.1 below which is merely a

restatement of Assumption 2.1b suitably adapted to this

portfolio credit risk setting.

Assumption 6.1.

For the function

is such that for any

sequence of

satisfying we have

where is a positive constant and

is the limiting

function such that the cone

is not empty.

The task of estimating is particularly

challenging in portfolios composed of high quality loans with small

default probabilities. This rarity is specified, for example, in the

default probabilities by letting the parameter be large in

(27). In order to study how an IS scheme fares when

the target event becomes increasingly rare, we embed the given problem

in the sequence of estimation problems indexed by with

and the respective in

(27) and the exposures satisfying

(28)

for some positive constants

Similar asymptotic frameworks form the basis of

analysis in Glasserman & Li, (2005), Bassamboo et al., (2008), Glasserman et al., (2008); see Deo & Juneja, (2020) for a

detailed exposition on the appropriateness of this regime in the

context of logit default models. We impose a mild technical requirement that the parameter in

(26) does not lie in the set

. This unrestritive condition is common in the literature for

ease of analysis; see Glasserman et al., (2007).

We first present a tail asymptotic for the excess loss probability

in Theorem 6.1 below as

an application of Theorem 4.1. In order to state the

result, let denote the collection of subsets of the

set whose collective exposure exceeds the specified

threshold; in other words,

Let

(29)

where is a sequence decreasing to zero

as

With the event amenable to be treated via Theorem

4.1, Theorem 6.1 below

establishes that the events and

coincide as and uses this observation to

establish the asymptotic for and

Theorem 6.1(Tail asymptotic for ).

Suppose that the conditional default probabilities are specified as

in (27), with the functions

satisfying Assumption

6.1. In addition, suppose that the convergences in

(28) hold and satisfies the conditions in

Theorem 4.1 with

satisfying

Then as

(30)

for any sequence and

where

Here the constant

and are identified as,

Since the IS procedure introduced in Section 2.2 is readily applicable for estimating

thanks to (30), one may

suitably modify it to arrive at Algorithm 2 below which is efficient in estimating the desired excess loss probability

The conditional sampling of default variables in Step 2a of Algorithm 2 involving exponential twisting is conventional (see, for eg., Glasserman, 2004, Chapter 9).

The selection of a suitable IS distribution for the common factors on the other hand, is often non-trivial (see eg., Glasserman et al., 2008) and is unknown if the functions modeling the default probabilities are specified generally, say, for example, in terms of a ReLU neural network as in Sirignano & Giesecke, (2019). This non-trivial task of arriving at a suitable IS distribution for is however readily handled by the IS transformation in Algorithm 2.

Input: Loss threshold independent

samples of , loan-specific values

hyper-parameter

Procedure:

1. Transform the samples and compute associated likelihood:

Compute IS samples and their likelihoods

as

described in Steps 1 - 2 of Algorithm 1.

2. Obtain samples of portfolio loss: For

do the following steps:

a)

Generate the loan default variables

where for

are independent Bernoulli random variable with success probability

where

(32)

is as in (27), and in (32) is the unique solution of with denoting the conditional cumulant

b)

Set to be the

portfolio loss.

c)

Compute the conditional likelihood associated with the

collection by letting

3. Return the output estimator. Return the IS average

computed as in,

Algorithm 2IS algorithm for estimating the excess loss probability

Suppose that satisfies the conditions in Theorem

5.1 and the density of is bounded away from

on compact subsets of . For the conditional default

probabilities specified in (27), let the functions

satisfy Assumption 6.1

and the resulting constant in (31) is finite. Then

under the asymptotic regime in (28) we have

for any choice of the parameter which is slowly varying in

In other words, the family of unbiased estimators returned by

Algorithm 2 is logarithmically efficient in

estimating

7. Numerical Experiments

We begin with a discussion on the selection of hyperparameter in Algorithm 1 before presenting the results of numerical experiments. Recall that the IS estimator returned by Algorithm 1 is unbiased for any choice of and the number of replications needed to attain a target relative precision is directly determined by the estimator variance. Therefore we seek to select which minimizes the sample average second moment estimate of the resulting IS estimator. Algorithm 3 below utilizes Retrospective Approximation (RA) for accomplishing this, as RA is effective in reducing the overall computational effort by balancing the errors due to sample based approximation of the objective and optimization (see Pasupathy, 2010). The RA procedure in Step 2 seeks to progressively increase the sample size employed, if required, while capitalizing on the current iterate to obtain an improved choice An intermediate quantile of the distribution of computed from a small pilot simulation run is used to obtain the initial choice as a rule of thumb, this may be chosen to be in the last two deciles of the distribution of . An advantage of our transformation based IS approach is that it requires obtaining samples only from the distribution of and therefore the collection of samples in earlier steps get fully reused in successive steps of RA and in the computation of final IS estimate. In all the estimation tasks in Sections 7.1 - 7.2 below, we report results obtained for target relative precision requiring in Algorithm 3 and with the initialisation set to , and .

Step 0: Initialize sample size for pilot run, tolerance tol for terminating optimization, intermediate quantile level

Step 1 (Pilot simulation run): Draw i.i.d. samples of Assign where is the -th largest value in the collection

Step 2 (Retrospective Approximation): Set . Do while ,

a)

Set and draw i.i.d. samples of

b)

Minimise second moment estimate numerically over with the initial iterate set to Assign and respectively, to be the optimal value and the solution obtained by solving until the absolute error between successive iterates becomes smaller than

. The procedure for estimating second moment of the IS estimator given and a collection for any is as follows:

If relative improvement terminate while loop by setting choice of with for ; else increment

end while

Step 3 (Compute IS estimate with desired precision): Set . Do while ,

a)

Draw an independent sample from the distribution of Set , where and . Evaluate as the sample mean and as the sample standard deviation of the collection .

b)

If , terminate loop by setting ; else increment .

end while

Return as the estimate for

Algorithm 3Combining IS with Retrospective Approximation based hyperparameter search for estimating within relative error with -confidence

7.1. Illustration with the contextual shortest path problem

Here we employ the IS scheme for the contextual shortest path problem considered in Elmachtoub & Grigas, (2022). The goal is to travel from the north-west corner to the south-east corner of a grid. From any given vertex, only edges which travel south or east are available. Associated with each edge (enumerated as

) is a traversing cost determined by contextual side information and an additional random vector The context is

taken to have independent Weibull marginals, with

for . The cost is given by,

(33)

where is a fixed matrix, allows nonlinear dependence on and the independent noise has i.i.d. components uniformly distributed on . The loss is given as in (3), where is the shortest path polytope on the considered grid.

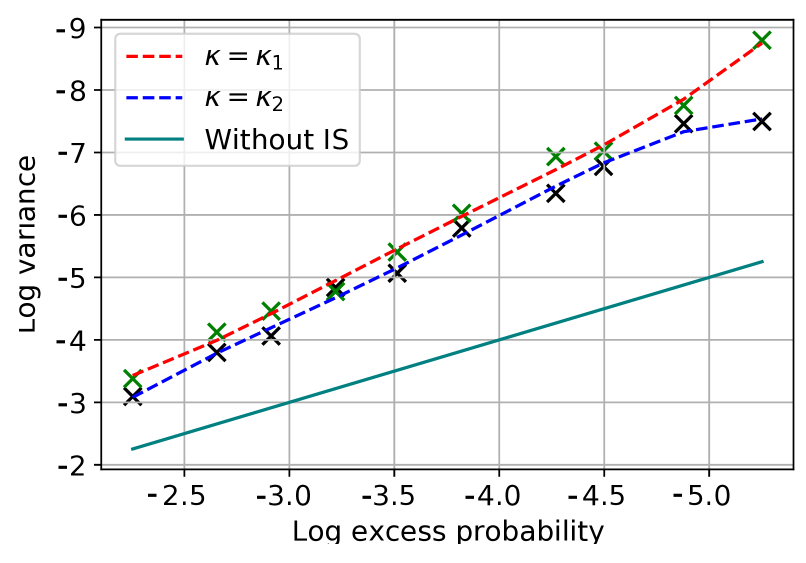

Experiment 1: We consider the estimation of

for values of resulting in The probability of large travel cost is estimated as in Algorithm 3 by averaging i.i.d. samples of where is the IS cost vector and is

the respective likelihood ratio. Letting denote the sample variance of the collection , we plot against in Figure 4(a) obtained for/ both the choices of in (7) and parameter choices

Note that the plot for IS variance is approximately a straight line with a slope of 2, supporting the conclusion from Theorem 5.1. Naive sample averaging, on the other hand, can be seen to have orders of magnitude larger variance in Figure 4(a).

Experiment 2: Here we consider the predictive setting where a

routing decision

is obtained by

plugging in the cost predicted from the realized

contextual side information Note that while the realized

cost depends on both and the

realization of is not available at the time of

decision-making.

Suppose that similar to (Elmachtoub & Grigas, 2022, Section 6.1), the

cost is predicted from a linear model

we take ,

estimated from historical data,

The

total cost realized by deploying the decision

is then given by

where the

edge-traversal costs satisfy (33). A risk manager is then naturally interested in evaluating tail risk

probabilities such as in

that have to be

borne from deploying the routing decision

Drawing

samples

for this purpose (drawn

independently of those used to estimate ), we first

generate the transformed tuple

here is the IS vector,

and

serve as the realized and predicted

costs, and denotes the respective

shortest paths. Our IS estimator for the probability

is then computed by averaging over

as in Step 3 of Algorithm 3. We plot (denoting the sample log variance) against in

Figure 4(b) for the same parameter choices in Experiment 1. As before, we observe that the plot is approximately a straight line with a slope of .

Figure 4(c) presents additional details on cross-validation by plotting the logarithm of estimator variance,

observed (in red) for different choices of

hyper-parameter considered. In Figure 4(c), the

level is such that . The high degree of

variance reduction (exceeding 99.99%) in the interval

demonstrates that the estimator variance is not

unduly sensitive to the choice of parameter Further, we observe that Step 2 concludes after samples and the estimated sample variance closely approximate the true variance. Thus can be seen to constitute only a fraction of the total sample requirement: for eg., a total of samples were required (on an average), in the estimation of with the stated precision.

(a)Estimation of

(b)Estimation of

(c) vs second-moment

Figure 4. Variance of the proposed IS estimator, illustrated via

a log-log plot, for the contextual shortest path problem.

Lines (solid and dashed) represent a polynomial fit to the

variance values marked via crosses.

7.2. Illustration with the portfolio credit risk model

For the portfolio credit risk model considered in Section

6, we take a pool of loans of a single type,

each with an exposure As in Section 7.1, the

common factors are taken to possess standard

Weibull marginal distributions with shape parameter . The dependence is informed by a

Gaussian copula whose non-zero off-diagonal entries of the correlation

matrix are taken to be for

We consider cases where the conditional

default probabilities are given by (a) the logit model in

(27) and (b) the discrete default intensity of the

form, The

function is

informed by a ReLU neural network with hidden layer with weights

for all and

Taking the loss threshold in (26), we aim to

estimate the probability of excess default loss

the parameter in the

conditional default probabilities dictate the rarity of loan defaults

and is varied in the experiments so that the respective

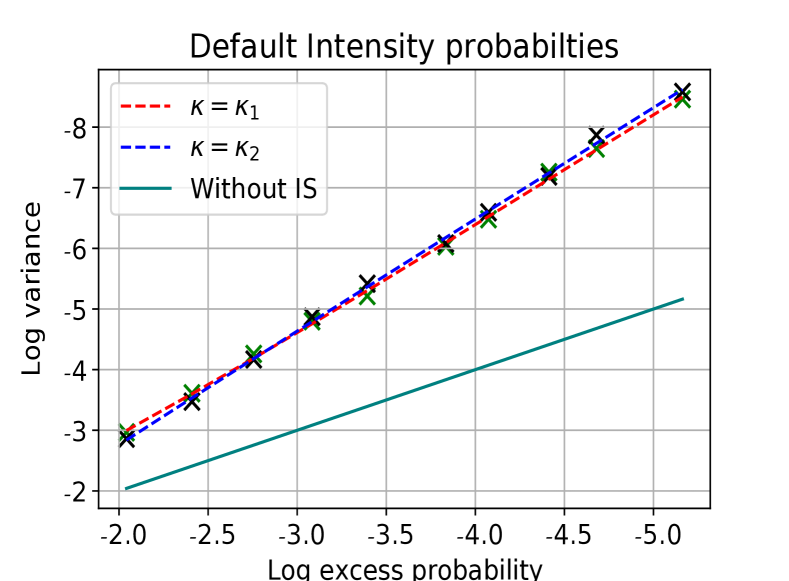

varies from to In Figure 5 below,

we report against where

is the sample variance of the IS estimator.

As in Section 7.1, the

ratio between the logarithm of variance of IS estimator and that of

the naive estimator (without IS) ranges over the interval ,

which points to the IS estimator possessing negligible variance

compared to that of sample averaging without IS.

(a)Logit loan default probabilities

(b)Intensity based default probabilities

Figure 5. Plots displaying the logarithm of sample

variance, of the IS estimator

versus where is

excess default loss probability estimated.

7.3. Comparison with Cross-Entropy

In order to benchmark the number of samples and loss evaluations required by Algorithm 3 against a state-of-the-art adaptive IS algorithm, we compare its performance with that of cross-entropy. To this end, we consider evaluation of exceedence probabilities of (i) the PERT network loss from Rubinstein & Kroese, (2013) and (ii) neural network loss defined in Section 7.2. We assume that has independent and exponential marginals. For cross-entropy, in line with the approach in Rubinstein & Kroese, (2013), we search for an IS distribution from among distributions with independent exponential marginals. For evaluation of probabilities using the proposed method, we use Algorithm 3. To facilitate a comparison of the two methods, we plot in Figure 6 the total number of samples required (across 30 independent experiments) to carry out the estimation to within a relative precision of with confidence using the respective method. Observe that in either setting, at a probability of , the sample requirement for the proposed IS is smaller by a factor exceeding

Further, cross-entropy method takes just under loss evaluations to cross-validate and compute the probabilities, while for the same task IS requires only about .

(a)PERT Network

(b)Neural Network

Figure 6. Box-plots comparing sample requirements of cross-entropy method (in red) with those of the proposed sampler (in blue): Cross-entropy expends about times more effort than the proposed sampler.

Acknowledgements. Support from Singapore Ministry of

Education’s AcRF Tier 2 grant MOE2019-T2-2-163 is gratefully

acknowledged.We thank the anonymous reviewers and the Associate Editor for the insightful suggestions which have helped improve the paper in various respects.

References

Ahn & Kim, (2018)

Ahn, Dohyun, & Kim, Kyoung-Kuk. 2018.

Efficient Simulation for Expectations over the Union of Half-Spaces.

ACM Trans. Model. Comput. Simul., 28(3).

Arief et al., (2021)

Arief, Mansur, Huang, Zhiyuan, Kumar, Guru Koushik Senthil, Bai, Yuanlu, He,

Shengyi, Ding, Wenhao, Lam, Henry, & Zhao, Ding. 2021.

Deep probabilistic accelerated evaluation: A robust certifiable

rare-event simulation methodology for black-box safety-critical systems.

Pages 595–603 of:International Conference on Artificial

Intelligence and Statistics.

PMLR.

Asmussen & Glynn, (2007)

Asmussen, S., & Glynn, P.W. 2007.

Stochastic Simulation: Algorithms and Analysis.

Springer New York.

Asmussen & Kroese, (2006)

Asmussen, Søren, & Kroese, Dirk P. 2006.

Improved algorithms for rare event simulation with heavy tails.

Advances in Applied Probability, 38(2), 545–558.

Bai et al., (2022)

Bai, Yuanlu, Huang, Zhiyuan, Lam, Henry, & Zhao, Ding. 2022.

Rare-Event Simulation for Neural Network and Random Forest

Predictors.

ACM Trans. Model. Comput. Simul., 32(3).

Ban & Rudin, (2019)

Ban, Gah-Yi, & Rudin, Cynthia. 2019.

The Big Data Newsvendor: Practical Insights from Machine Learning.

Operations Research, 67(1), 90–108.

Bassamboo et al., (2008)

Bassamboo, Achal, Juneja, Sandeep, & Zeevi, Assaf. 2008.

Portfolio Credit Risk with Extremal Dependence: Asymptotic Analysis

and Efficient Simulation.

Operations Research, 56(3), 593–606.

Beer et al., (1992)

Beer, Gerald, Rockafellar, RT, & Wets, Roger J-B. 1992.

A characterization of epi-convergence in terms of convergence of

level sets.

Proceedings of the American Mathematical Society, 11(3),

753–761.

Blanchet & Mandjes, (2009)

Blanchet, J, & Mandjes, M. 2009.

Chapter 5. Rare Event Simulation for Queues.

In: Rubino, Gerardo, & Tuffin, Bruno (eds), Rare event

simulation using Monte Carlo methods.

John Wiley & Sons.

Blanchet et al., (2019)

Blanchet, Jose, Li, Juan, & Nakayama, Marvin K. 2019.

Rare-Event Simulation for Distribution Networks.

Operations Research, 67(5), 1383–1396.

Borovkov, (2008)

Borovkov, A.A. 2008.

Asymptotic analysis of random walks.

Vol. 118.

Cambridge University Press.

Chen et al., (2018)

Chen, Bohan, Rhee, Chang-Han, & Zwart, Bert. 2018.

Importance sampling of heavy-tailed iterated random functions.

Advances in Applied Probability, 50(3), 805–832.

Collamore, (2002)

Collamore, J.F. 2002.

Importance Sampling Techniques for the Multidimensional Ruin Problem

for General Markov Additive Sequences of Random Vectors.

Ann. Appl. Probab., 12(1), 382–421.

de Haan & Ferreira, (2010)

de Haan, Laurens, & Ferreira, Ana. 2010.

Extreme Value Theory: An Introduction (Springer Series in

Operations Research and Financial Engineering). 1st edition. edn.

Springer.

de Valk, (2016)

de Valk, Cees. 2016.

Approximation and estimation of very small probabilities of

multivariate extreme events.

Extremes, 19(4), 687–717.

Dembo & Zeitouni, (1998)

Dembo, Amir, & Zeitouni, Ofer. 1998.

Large Deviations Techniques and Applications.

Springer.

Deo et al., (2022)

Deo, A., Murthy, K., & Sarker, T. 2022.

Combining Retrospective Approximation with Importance Sampling for

Optimising Conditional Value at Risk.

P.1-12 of: 2022 Winter Simulation Conference (WSC).

Deo & Juneja, (2020)

Deo, Anand, & Juneja, Sandeep. 2020.

Credit Risk: Simple Closed-Form Approximate Maximum Likelihood

Estimator.

Operations Research.

Deo & Murthy, (2021)

Deo, Anand, & Murthy, Karthyek. 2021.

Efficient black-box importance sampling for VaR and CVaR estimation.

Pages 1–12 of:2021 Winter Simulation Conference (WSC).

IEEE.

Dupuis et al., (2007)

Dupuis, Paul, Leder, Kevin, & Wang, Hui. 2007.

Importance Sampling for Sums of Random Variables with Regularly

Varying Tails.

ACM Trans. Model. Comput. Simul., 17(3).

Einmahl et al., (2021)

Einmahl, John HJ, Yang, Fan, & Zhou, Chen. 2021.

Testing the multivariate regular variation model.

Journal of Business & Economic Statistics, 39(4),

907–919.

Elmachtoub & Grigas, (2022)

Elmachtoub, A., & Grigas, P. 2022.

Smart “Predict, then Optimize”.

Management Science, 68(1), 9–26.

Embrechts et al., (2001)