Diffusion Approximations for a Class of Sequential Testing Problems

Abstract

We consider a decision maker who must choose an action in order to maximize a reward function that depends on the action that she selects as well as on an unknown parameter . The decision maker can delay taking the action in order to experiment and gather additional information on . We model the decision maker’s problem using a Bayesian sequential experimentation framework and use dynamic programming and diffusion-asymptotic analysis to solve it. For that, we scale our problem in a way that both the average number of experiments that is conducted per unit of time is large and the informativeness of each individual experiment is low. Under such regime, we derive a diffusion approximation for the sequential experimentation problem, which provides a number of important insights about the nature of the problem and its solution. First, it reveals that the problems of (i) selecting the optimal sequence of experiments to use and (ii) deciding the optimal time when to stop experimenting decouple and can be solved independently. Second, it shows that an optimal experimentation policy is one that chooses the experiment that maximizes the instantaneous volatility of the belief process. Third, the diffusion approximation provides a more mathematically malleable formulation that we can solve in closed form and suggests efficient heuristics for the non-asympototic regime. Our solution method also shows that the complexity of the problem grows only quadratically with the cardinality of the set of actions from which the decision maker can choose.

We illustrate our methodology and results using a concrete application in the context of assortment selection and new product introduction. Specifically, we study the problem of a seller who wants to select an optimal assortment of products to launch into the marketplace and is uncertain about consumers’ preferences. Motivated by emerging practices in e-commerce, we assume that the seller is able to use a crowdvoting system to learn these preferences before a final assortment decision is made. In this context, we undertake an extensive numerical analysis to assess the value of learning and demonstrate the effectiveness and robustness of the heuristics derived from the diffusion approximation.

Keywords: Sequential experimentation, sequential testing, Bayesian demand learning, experiment design, optimal stopping, dynamic programming, crowdvoting

1 Introduction

This paper is concerned with the problem faced by a decision maker (or DM for short) who must choose an action from a finite set of available actions in order to maximize a reward function that depends on the action taken, as well as on a parameter . The DM does not know the true value of but has only incomplete information about it and hence about the reward function. Instead of selecting an action immediately, the DM has the option of postponing this decision in order to experiment and gather additional information about the true value of . In this context, the decision maker needs to select the most effective sequence of experiments to implement through time as well as the time when to stop these experiments and select a final action .

A wide range of applications can be modeled using the above general framework. For example, the DM can be a factory manager who needs to decide if a batch of production meets specific quality standards. For that she can sample items sequentially to measure their individual condition and accordingly, extrapolate the quality assessment on the entire batch (Qiu, 2014). Alternatively, the DM can be a pharmaceutical company conducting a sequence of clinical trials to evaluate the efficacy of some new drug or vaccine (Armitage et al., 2002). In yet another example, the decision maker can be an educational institution designing computerized adaptive testing systems to assess the level of proficiency of a cohort of examinees in a particular subject area (Bartroff et al., 2008, Finkelman, 2008).

One particular application, which has served as our initial motivation for this paper, relates to the problem of assortment selection in the context of new product introduction. Launching new products into the marketplace offers great opportunities for companies to generate new revenue streams and increase sales. However, such endeavors represent risky bets as consumers’ preferences are typically unknown and unsuccessful products are a major liability generating possibly great capital expenditure, early markdowns, serious goodwill cost, and loss of market share. It is not infrequent to witness major brands preferring to discontinue a product, shortly after its introduction, rather than taking more risks and incurring higher draining costs†††Making the wrong selection has even driven many major brands to discontinue some of their products, shortly after introduction (see, Sell Big or Die Fast, New York Times, J. Wortham and V.G. Kopytoff, August 23, 2011).. To mitigate these risks, companies seek to test the market’s reaction (e.g., value for the price) to new products before launching decisions are made.

In general experimentation can be expensive and difficult to conduct effectively and probably worth doing only seldomly. However, in many situations, this reality is now changing as companies are beginning to recognize the potential to crowdsource such market testing activities. Online experimentation has been indeed growing exponentially in the last decade or so. Companies such as Uber, Netflix, Amazon, Microsoft and many more‡‡‡We refer the reader to the spot light articles of the March-April 2020 issue of the Harvard Business Review. have been aggressively implementing market experimentation, through dedicated platforms, with the objective of continuously improving the online experiences of their customers and infer customers preferences. In the context of new product introduction, some companies have created crowdvoting platforms (e.g., Threadless.com§§§A site where anyone can design a T-shirt and submit it to a weekly contest. Viewers vote for their favorite T-shirts and the winning designs are selected for production and their designers get rewarded.) where customers can vote for their favorite products among a menu of available options. By doing so, companies generate continuous feedbacks from the “crowd” at almost no cost, except often for the lack of accuracy and veracity of the data gathered. In view of these challenges, an effective execution of a crowdvoting system is required which involves deciding what is the best assortment of products to display to each individual voter in order to maximize the speed of learning as well as when to stop the experimentation process and decide which new products should be commercialized (Kohavi and Thomke (2017)). Section 6 is devoted to this particular crowdvoting example, which we use to illustrate the methodology and results that we develop first in Section 4 for the general case.

Motivated by the operating conditions of many online experimentation platforms, our general formulation of the decision maker’s problem and its analysis are based on two important and distinctive features:(i) We assume that the time epochs at which experimentation is possible are driven by an exogenous point process that the DM does not control. (ii) We consider environments in which the average number of experiments that can be conducted per unit of time is large but the amount of information generated by each individual experiment is low. In the context of the crowdvoting example, the first assumption accounts for a stochastic arrival of viewers/voters to the platform website. As for the second feature, it depicts, as mentioned above, the high velocity at which data can be collected online but also captures the fact that such data is inherently more noisy and less reliable than when experiments are more targeted and carefully designed (e.g., focus groups or surveying experts). Under these conditions, we are able to use asymptotic analysis to derive a diffusion approximation for both the sequential experimentation problem and the underlying optimal stopping problem that the decision maker must solve. As we will see, the diffusion model provides a number of important insights about the nature of the problem and its solution. First, it reveals that the problems of (i) selecting the optimal sequence of experiments and (ii) deciding the optimal time to stop experimenting decouple and can be solved independently. Second, it shows that an optimal experimentation policy is one that chooses the experiment that maximizes the instantaneous volatility of the belief process, a proxy of the learning process. This maximum volatility principle reduces dramatically the complexity of the dynamic experimentation selection problem and its solution. Third, the diffusion approximation also provides a more mathematically malleable formulation of the optimal stopping problem that we can solve in closed form. Interestingly, the computational complexity of the latter grows only quadratically with the cardinality of the set of actions ; in fact we show that solving a problem with actions is equivalent to solving a collection of problems each with only two actions. Fourth, by reinterpreting the maximum volatility principle, we can reformulate the problem of selecting an optimal experimentation policy as a Tchebycheff moment problem that sheds some light on how one could tackle the problem of experiment design, i.e., which experiments to make available in the first place to the decision maker. In addition, we obtain from our diffusion approximations, heuristics-policies for the moderate, non-asymptotic regime. These heuristics turn out to be extremely effective and robust as shown in our numerical analysis. Finally, as a by-product of our analysis of the crowdvoting example in Section 6, we derive diffusion approximations for a setting in which experimentation and learning are driven by the choices that voters make under a multinomial choice model (MNL). Given the popularity of the MNL model to represent consumer preferences, we believe that our approach to obtaining diffusion approximations can possibly be applied to a number of other applications beyond those discussed in this paper.

2 Related Literature

Our paper is related to two streams of literature. Methodologically, we contribute to the literature on hypothesis testing and sequential design of experiments initiated by Wald47 in the early 40’s. In terms of applications, we contribute to the operations literature on assortment planning and demand learning (e.g., CaroGallien07 and Kok2009).

Sequential analysis is concerned with the problem of effectively detecting the validity of a hypothesis through sequential sampling or tests. After each (possibly costly) test and on the basis of the observed history of outcomes, the decision maker needs to either accept one of the hypotheses being tested or continue the experimentation. The sequential probability ratio test (SPRT) developed by Wald45 (see also WaldWolfowitz48) establishes that under certain conditions an optimal policy is determined by the first exit time of an appropriately defined likelihood ratio process from a bounded interval; the end points of this interval are determined by pre-specified type I and II error targets. The initial formulation and ideas of Wald’s SPRT test have been applied to a wide range of applications and extended in many different directions (e.g., Siegmund85 and Lai01). One important extension relevant to our work relates to the problem of sequential design of experiments, where the DM chooses dynamically the experiments to undertake from a set of available options (e.g., Robbins52, Chernoff59; Chernoff72), and do that until she decides to stop and selects what she believes is the true hypothesis. For brevity we denote thereafter this type of problem, sequential hypothesis testing.

In terms of solution techniques large sample analysis has been commonly used to study sequential hypothesis testing problems and evaluate the asymptotic optimality of concrete (often simple) policies. The asymptotic regime in many of these studies is obtained by assuming that the cost of experimentation goes to zero (e.g., Chernoff59, and Keener84). Chernoff mentions that “it may pay to continue sampling even though we are almost convinced about which is the true state of nature.” The alluded “inefficiency” in Chernoff’s regime is required to guarantee a probability of error that is proportional to the cost of experimentation that is becoming increasingly small. Our work also relies on a type of asymptotic analysis in which the number of experiments grow large, however, our approach differs significantly from large sample methods as we not only scale the number of experiments but simultaneously decrease the informativeness of each experiment. As a result, in such asymptotic regime the ‘rate’ of information that the DM collects remains comparable to those in small sample problems, and therefore when the DM is experimenting it does so only because she is still unsure of the true hypothesis. This interplay between larger sample sizes and less informative experiments was also recently explored by Naghshvar13. They also rely on large sample analysis, but introduce a multiple hypothesis setting, and represent the limited informativeness by scaling the number of hypotheses. Their results are a generalization of Chernoff59 where they suggest adjusted policies and find tight bounds to prove their asymptotic optimality. In the context of multi-armed bandit problems, WagerXu21 and FanGlynn21 are two recent arXiv preprints that study a similar type of asymptotic regime and diffusion limits as the ones considered in this paper. In particular, they consider a regime in which the mean rewards of the arms scale as , where is the number of arm pulls. WagerXu21 suggest a framework governed by a well behaved sampling function to implement such approach in the context of sequential experimentation. FanGlynn21 develop the theory from first principles in the specific context of Thompson sampling. In our two hypothesis setting, we introduce a general framework to model lack of informativeness. This framework includes for instance the case of asymptotically indistinguishable hypothesis as well as settings where the experiments generate increasingly noisy outcomes. We show that under our asymptotic regime, the sequential experimentation problem reduces to a diffusion free boundary problem which we are able to solve and develop approximations for the non-asymptotic regime. Other papers have studied diffusion models in the context of sequential testing (e.g., Chernoff61, Breakwell64, Peskirbook or HarrisonSunar15), although in our case we make no Gaussian assumption regarding the initial process that is being observed. Other examples of sequential analysis papers that have relied on diffusion approximations include the work on Bayesian multi-armed bandits by ChangLai87 and BrezziLai02, on ranking and selection problems by ChickGans09 and ChickFrazier12, and also in the context of strategic experimentation, with Bolton who consider a many-agent two-armed Bernoulli bandit problem in which agents can learn from the experimentation of other agents (i.e., information as a public good).

Our work also contributes to a growing stream of sequential hypothesis testing problems in the context of best arm identification (BAI) (see, russo2016simple, garivier2016optimal, and kaufmann2016complexity). In our sequential hypothesis testing setup, we interpret each available experiment as an ‘arm’ that when pulled generates information on the true hypothesis. A key difference between our model and this literature is that we allow for the possibility that the set of arms available for learning to be different from the sets of arms from which the DM chooses a final action. One feature of our model is that the DM learns about the true hypothesis from any pulled arm. This behavior is similar to some BAI settings where the unknown parameters can affect the reward of multiple correlated arms, (see, Soare14). Moreover, in the illustrative example of Section 6, we assume that an experiment is an assortment of products offered to a customer and the outcome is the product selected by that customer. We assume in this example that this selection happens following an MNL model making this setup similar to an MNL-bandit like exploration (see the recent work of, Agrawal2017 and OhIyengar19). Despite some structural difference with BAI and more generally, MAB literature, we compare in the numerical section the performance of some MNL-bandit algorithms - introduced in the literature - with the ones we suggest here.

Finally, we recall that this work naturally belongs to the broad area of reinforcement learning. Our suggested heuristics can be viewed as approximate DP techniques for solving a dynamic learning problem. Such techniques have been shown to be effective in managing the curse of dimensionality (see, Powell12). In this recent review, Powell divides ADP policies in four categories: myopic cost function approximations, lookahead policies, policy function approximations and policies based on value function approximations. The latter two are often based on the specific structure of the problem. Indeed, most of the heuristics we suggest (see, Section 5) belong to these two categories and are obtained either by reducing carefully the set of policies we are optimizing on, or by approximating the value function itself. These approximations are primarily inspired and obtained based on our asymptotic analysis. In our numerical analysis (see Section 7) we also include a lookahead type policy. Some recent works have highlighted the effectiveness of simple policies in the context of dynamic learning such as greedy algorithms (e.g., Bastani20) and Certainty-Equivalence (e.g., Keskin18). The greedy algorithm behaves well when exploration is expensive while in our case it is free. As for the certainty equivalence (CE), it is not appropriate in our setting. Indeed, in a Bayesian setting, CE would assume that the current belief is constant moving forward and hence would always recommend to stop and never to explore. Having said that, we do show that in our case a simple (static) experimentation policy behaves well and is asymptotically optimal.

Our paper also contributes to the operations literature on sequential testing and demand learning. There is a growing stream of papers in revenue management that have focused on the problem of characterizing optimal dynamic pricing strategies when there is incomplete information about consumers’ price sensitivity (see, AramanCaldentey11 and denBoer2015). In this context, pricing strategies play a dual role. On one hand, they have a direct impact on sales and revenues. On the other, they act as tools for experimentation used by sellers to learn demand characteristics. Optimal pricing strategies are those that balance the so-called exploration-exploitation tradeoff between these two roles, e.g., AramanCaldentey09, BesbesZeevi09, Bora2012, BoerZwart14, BroderRusme12, GallegoTaleb12 and KeskinZeevi14. Another stream of papers, which is closer to the crowdvoting example that we consider in Section 6, focuses on optimal assortment planning under unknown demand characteristics. In this literature, the decision maker wants to identify a revenue maximizing assortment of products from a (possibly very large) set of available options. Consumers’ preferences over assortments are typically described in the form of a Luce-type choice model –with the MNL being by far the most popular choice–with unknown parameters. In this setting, the DM experiments by displaying different assortments to different consumers over time. Some representative papers in this area include CaroGallien07, Uluetal2012, SaureZeevi13, Agrawal2017 and Yifan18. A variant of this line of research is the recent paper of Keskin19, where the seller faces unknown cost functions that increase with the quality of the products. At each period, the firm selects vertically differentiated products and self-selection pricing mechanisms to learn and maximize its profit over a finite horizon.

Finally, our research also contributes to the recent and growing literature on crowdsourcing and specifically crowdvoting. We mention the work of Krager14 that looks at adaptively allocating small tasks to workers through crowdsourcing while meeting some reliability target. The recent work of Papanastasiouetal18 tackles the provision of information dissemination in an online setting where customers’ selection of products/services is affected by historical outcomes. On the crowdfunding end, Alaei16 suggest a dynamic model of crowdfunding and assess the probability of success of a campaign by introducing the notion of anticipating random walks. On crowdvoting, the paper by MarinesiGirotra13 focuses on measuring the information that is acquired from a customer voting system. Using a two-period game-theoretical model, they prove among other results that by offering a sufficiently high discount during the voting phase, crowdvoting systems - used to decide whether to develop the product or not - represent an effective way to elicit information on customers willingness-to-pay. Finally, motivated by recent applications in blockchain-based platforms, Tsoulkalas19 consider the problem of information aggregation from a collection of partially informed agents having private information about some unknown state of the world (e.g., the quality of product). Agents submit a vote –in the form of an estimate of the true value of state of the world– and the platform aggregates these votes to produce a final estimate. The value of the platform and the payoffs collected by the agents depend on the accuracy of this final estimate. The paper studies the impact of using different weighting mechanisms to aggregate votes on agents voting strategies and the informativeness of the resulting equilibrium outcomes. Our focus however through our crowdvoting example, is on how to operationally manage a voting platform that faces a stream of myopic (non-strategic) consumers. In that regard our work is close to Yifan18.

The rest of the paper is organized as follows. In the next section, we introduce the different components of the general model together with the main assumptions and formulate the problem as a two-stage dynamic programming problem where the first stage is concerned with the experiment design while the second stage tackles the duration of the experimentation. We also prove the convexity of the value function and discuss how one can leverage this property to simplify the optimization and generate a simple heuristic for the experimentation. Section 4 is fully devoted to the asymptotic analysis. We start by describing the scaling and the corresponding regime and obtain a diffusion formulation of the original problem. We move next to solving for the corresponding optimal experimentation policy as well as the optimal stopping of the experimentation phase. These two decisions are shown to decouple. We first show that a static experimentation policy is optimal at the limit and the optimal experiment is the one that maximizes the volatility of the belief process. As for the optimal duration of experimentation, it is formulated as an optimal stopping problem very much in the spirit of Wald’s SPRT test. The solution is fully characterized by a partition of the belief space into a collection of intervals that determine those regions where experimentation is needed or not. Both the value function and the expected value of the stopping time are obtained in closed form. Motivated by the simple optimality principle that characterizes the diffusion problem, we suggest in Section 5 heuristics for the experimentation policy under a non-asymptotic regime, and discuss ways to identify the various components of the heuristics while relying only on the initial primitives of the problem. In Section 6, we discuss in detail an illustrative example of the assortment selection in the context of new product introduction. The results of the previous sections are adapted to this setting followed, in Section 7, by an extensive numerical analysis. For that, various heuristics of the display set policy are introduced and compared numerically to the diffusion-derived heuristics, confirming the high performance and robustness of the latter. Finally, given the connection of our setting in Section 6 with MNL-bandit and best arm identification literature, we also show numerically that our suggested heuristics outperforms off-the shelf algorithms from this literature. We conclude in Section 8 and offer some possible directions for future work. Most proofs have been relegated to the appendix.

3 Model Description

We consider a decision maker (DM) who must choose an action in order to maximize a reward function that depends on both the action as well as a parameter . The DM selects the action from a finite set of available actions and does not know the value of that can take one of two possible values . Specifically, the DM has incomplete information on , and hence on the reward function, having a prior that with probability .

We assume that the decision maker is risk neutral. If she were to make a decision at time , she would then select an action that maximizes her expected reward conditional on her prior belief . That is, she would select an action that maximizes , where is the expectation operator conditional on the prior belief that with probability †††To be precise, the probabilistic framework that we consider is defined by a probability space equipped with two probability measures and . For each , we associate a probability measure and let denote its expectation operator. Finally, is a Bernoulli random variable that satisfies .. We define the optimal expected reward function

| (1) |

and let be the set of actions at which the maximum reward is achieved. Without loss of optimality, we assume that for every , there exists a such that (otherwise, some actions are uniformly dominated and can be removed from the set of available actions). It is worth noticing that, since is a finite set, the function is piece-wise linear in .

3.1 The Experimentation Process

Instead of selecting immediately an action from the set , the DM has the option of postponing this decision in order to experiment and gather additional information about the true value of . The type of experimentation process that we consider is characterized by two key features:

-

1.

The decision maker has at her disposal a finite set of experiments. Each experiment has associated a finite set of possible outcomes and a likelihood function

where is the conditional probability of observing outcome when the experiment is used and . We assume that every experiment is informative in the sense that there exists such that .

-

2.

There exists an exogenous Poisson process , with rate , that determines the time epochs at which experiments are conducted, where . As a result, while the decision maker selects the experiment at each experimentation epoch, she does not have control over the exact times when these experiments are conducted‡‡‡ This description assumes that the outcomes of the experiments are instantly observed. Alternatively, we can think that each experiment takes an exponential random time (with rate ) to generate an outcome and only at this point in time the next experiment can be set. As a result, the outcomes of the experiments will follow again a Poisson process with rate .

For instance, in the crowdvoting example mentioned in the introduction, experimentation occurs when a customer arrives to the online platform and votes, which we model as a Poisson process. See Section 6 for more details..

In this setting, a policy is a triplet , where is an experimentation policy that adaptively determines the sequence of experiments to conduct at the experimentation epochs , is a stopping time that defines the duration of the experimentation process, and is the action taken at time . Since at optimality we have , we will simply denote by a generic policy. We also denote by the sequence of outcomes of the experiments and by the history (filtration) generated by the experimentation process up to time . We denote by the set of stopping times with respect to . Also, and using a slight abuse of notation, we denote by the experiment that is used at time and by the corresponding outcome. Naturally, we must have .

By judiciously selecting an experimentation policy and observing the outcomes of each experiment, the decision maker can gradually learn the true value of over time. In particular, we define the belief process whose evolution is governed by Bayes rule.

Lemma 1 (Belief Process).

Let be a sequence of experiments and be the corresponding sequence of observed outcomes. If the decision maker has a prior belief , then the belief process evolves as an -martingale given by:

| (2) |

Proof: This and other proofs are relegated to the Appendix.

3.2 The Optimization Problem

Under some mild assumptions on the likelihood ratios the belief process converges to 0 or 1 depending on whether or , respectively. Hence, an infinitely patient decision maker will eventually learn the true value of . However, by running a long experimentation process the decision maker is also delaying the time when the final decision is made. If we assume that, ceteris paribus, the decision maker prefers to collect these rewards as early as possible then she faces a trade-off between learning the true value of (exploration) and collecting the reward (exploitation). To model this trade-off we assume that the decision maker’s objective is to maximize the expected discounted reward that she will collect at the time a final decision is made. That is, she is interested in solving the following optimal stopping time problem:

| (3) |

where is the decision maker’s discount factor. We will tackle the solution of (3) using dynamic programming. To this end, we find it convenient to express the dynamic evolution of the belief process in equation (2) using the following SDE representation.

Lemma 2.

The belief process in (2) admits the SDE representation:

In the statement of the previous lemma, the left-limit notation () stands for the experiment (belief) that is chosen (observed) right before a jump of at time . The factor is the size of the jump of the belief process (i.e., the “amount” of learning) if an experiment is chosen that produces an outcome when the belief process (just before the experiment) is equal to .

Equipped with Lemma 2, we formulate the decision maker’s problem as a Markov Decision Problem (MDP) and without loss of optimality, restrict our attention to the class of deterministic Markovian policies (e.g., Blackwell65 and Section 4.4 in Puterman05). In particular, the experimentation policy maps each value of the belief to an experiment and the stopping time is a hitting time of the belief process on some intervention set . We will interchangeably use and depending on the context. In the following definition, is the set of measurable functions from to and is the set of Borel sets in .

Definition 1.

(Deterministic Markovian Policy) A deterministic Markovian policy corresponds to a pair . For all , the DM displays experiment . On the other hand, for the decision maker chooses to stop the experimentation process and implements an optimal action .

Putting all the pieces together, the decision maker’s optimization in (3) can be rewritten as the following optimal control problem:

| (4) | ||||

Finally, we can express the optimality conditions of the control problem in (4) in the form of the following Hamilton Jacobi Bellman (HJB) equation:

| (5) |

with border conditions and since both and are absorbing belief states (see Lemma 1). By solving the inner maximization, we can compute an optimal experimentation policy , that is,

| (6) |

The HJB equation in (5) leads to a tractable computational approach to solve the decision maker’s problem. For instance, we can implement the value iteration algorithm

| (7) |

which defines a sequence of continuous functions that are monotonically increasing in and converge uniformly to a limit that satisfies the HJB equation in (5), (see the proof of Proposition 1 for details).

Despite its computational simplicity, the HJB equation (5) is not particularly malleable for the purpose of analysis and to derive structural results about an optimal solution and its properties. For this reason, in the next sections, we tackle the decision maker’s optimization problem using a diffusion approximation that preserves the same trade-offs as in the original formulation but provides a more transparent representation of the problem and its optimal solution.

We end this section with a numerical example that illustrates the value iteration method used above and highlights some feature of an optimal solution.

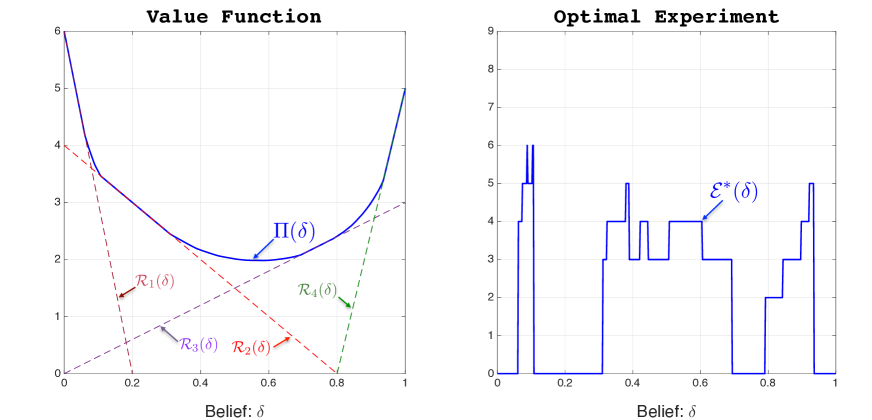

Example 1.

Suppose the decision maker has four alternative actions to choose from (i.e., ) with corresponding payoffs , , and . There are nine possible experiments that the DM can use (i.e., ) and each experiment produces a binary outcome, that is, for all . The table below specifies the probability for each of the nine experiments for and . Finally, we let and .

| Experiment | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|---|

| 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | |

| 0.03 | 0.04 | 0.09 | 0.16 | 0.25 | 0.36 | 0.49 | 0.68 | 0.86 |

Figure 1 depicts the numerically computed solution using the value iteration in (7) after 200 iterations. The left panel shows the value function while the right panel shows the optimal experiment . We use the convention for those values of at which and no experimentation is used.

As we can see, in an optimal solution, the belief space is partitioned into a collection of intervals that define the regions where experimentation is used or not used. For example, in the interval the decision maker does not use any experimentation and selects immediately (at time ) an action in that maximizes her expected reward (in this case ). On the other hand, in the interval the DM wants to experiment. In this case the interval is further partitioned into a collection of subintervals in which a specific experiment is selected. For instance, for the decision maker uses experiment 3 while for she uses experiment 4.

We note that experimentation occurs around those values of where the payoff function has a kink, i.e., where two payoff functions intersect. Intuitively, in these regions a small change in the value of can lead to a discrete change in the optimal action to select and so the DM has locally more incentive to experiment and learn in these regions.

3.3 On the Convexity of the Value Function

The following proposition will prove useful in various places in the analysis that follows.

Proposition 1.

The functions and are both convex in .

One way in which we can take advantage of this property is to simplify the optimization problem. In some applications, the cardinality of the set of possible experiments can be rather large adding an extra layer of complexity to the problem of solving the HJB equation in (5)§§§For example, in the context of an optimal assortment selection problem with products, there are possible display sets that could be offered. We will discuss this example in detail Section 6.. One possible step to mitigate this issue is to reduce the number of potential experiments to consider. Specifically, we can use the fact that the value function is convex to eliminate those experiments that are dominated in a convex order dominance sense¶¶¶The notion that an experiment dominates another one is similar to the notion that an experiment is more informative than another one as discussed in Blackwell51 (see also Lindley56 and Cam96)..

Indeed, for every and , let be the random variable that defines the value of the posterior belief when the prior belief is and experiment is selected. Note that for all . Suppose that for two experiments we have that , that is, the random variable dominates in the convex order sense (see ShakedShanthikumar94). Then, by convexity of in Proposition 1, we get that . As a result, experiment can be excluded from the set of possible experiments to be considered when the belief process equals . It is worth highlighting that this elimination procedure does not rely on any specific knowledge of the value function beyond the fact that it is convex.

One class of problems for which this elimination scheme is particularly simple is the class of problems in which each experiment can only generate two possible outcomes, that is, for all . This is an important special case given the popularity of pairwise comparison methods (see szorenyi2015online, Heckel2016 and references therein). In this case, if and only if the range of is contained in the range of . But this is the same as requiring that the range of the likelihood ratio is contained in the range of , which is a condition that is independent of and one can check efficiently. For example, if we apply this elimination scheme to the special instance in Example 1, we get that Experiments 1, 8 and 9 can be eliminated. To see this, note that the likelihood ratio of Experiment 1 takes values while the likelihood ratio for Experiment 2 takes values . It follows that Experiment 2 dominates Experiment 1. (Similar calculations reveal that Experiments 7 dominates Experiments 8 and 9.)

We can use stochastic dominance one step further to derive a simple experimentation policy. Since implies that , we can implement a heuristic policy which for each value of selects the experiment that maximizes . But and so this heuristic policy reduces to

In the following sections we will show that this simple experimentation policy is indeed optimal in an appropriate asymptotic regime in which the magnitude of the jumps converges uniformly to zero, i.e., in a regime in which each experiment becomes less and less informative.

We can also use the convexity of the value function to gain some intuition about this asymptotic result. Indeed, if we assume that the value function is twice-continuously differentiable, then a second order expansion of leads to the following equality:

The optimal experiment is characterized in equation , which we write here as follows,

By Lemma 2, is a martingale and so we have that . Also, by convexity of the value function, . Combining these two observations together with the assumption that the magnitude of is uniformly small, we conclude that

4 Asymptotic Approximation

In this section we specialize the problem described in the previous section to a particular class of instances in which (i) experiments are conducted at “high frequency” while (ii) the “informativeness” of each experiment is low. There are many natural and practical situations in which the decision maker has access to a large number of experiments, but where the informativeness of each individual one is low. For instance, online experiments are becoming quite common in the business world where each experiment is often linked to one visitor who is offered a set of choices to select from. Such common setup generates a large volume of experiments in a relatively short time period. However, one of the major issues faced by the experimenter is the relevance and veracity of the data generated (we refer the reader to the section “Beware of Low-Quality data” in Kohavi17). In some cases, the heterogeneity of the experementees in online experimentation can generate very noisy data. Moreover, the hypotheses being tested can be marginally different making the task of distinguishing them harder. Both settings are typical and are examples of how little informative online experiments can be. Our illustrative example in Section 6 build on these ideas. The notion of limited informativeness of experiments is also present in other settings. In their recent work, LewisRao15 show how difficult it is to prove the return on investment of advertising campaigns. The paper notes specifically that informative advertising experiments can require more than 10-million person-weeks, which reflects exactly the tension of our regime between large sample size and little informativeness. Clinical trials is another major area that suffers from serious data error and lack of accuracy, see, Nahm12 and as a result would require large sample sizes.

4.1 Diffusion Formulation

To formalize the notion of a “high frequency vs. low informativeness” regime of experimentation, we consider a sequence of instances of the problem indexed by a non-negative integer in such a way that as grows large both the number of experiments conducted per unit of time becomes high and the ‘amount’ of information generated from each individual experiment goes to zero. Under our proposed scaling the magnitude of the jumps of as well as the time between two experiments converge to zero resulting in a belief process that converges weakly to a diffusion process.

We let be the conditional probability of observing outcome when experiment is conducted conditional on for the instance of the problem. To capture the notion of low informativeness of an experiment, we impose the following requirement on the sequence .

Assumption 1.

(Low Informativeness Regime) For each , there exists a probability distribution such that for

| (8) |

where satisfies

Intuitively, the asymptotic scaling in Assumption 1 has the following property: as , the likelihood function converges to one for every and as a result the jumps of (see, Lemma 2) converge to zero. In other words, in this asymptotic regime, the outcomes of an experiment become less and less informative as grows large.

On its own, the scaling in equation (8) would lead to a trivial limit in which remains constant over time. To counterbalance the fact that individual experiments become less informative under (8), we also scale up the arrival rate of in a way that the ‘amount’ of information collected by the experimentation process per unit of time remains comparable to the one in the original unscaled system. Specifically, let denote the Poisson process that determines the experimentation epochs for the instance.

Assumption 2.

(High Frequency Regime) Let be the intensity of . Then, satisfies:

| (9) |

for some fixed constant .

Our objective at this point is to suggest a diffusion approximation of the general formulation problem (4). For that, we combine the parameter scalings in (8) and (9) to obtain a well-defined diffusion limit for the belief process, †††In Sections 5 and 6.2 we show how to interpret and operationalize our asymptotic scaling in practical settings.. We derive this limit over the class of continuous randomized Markovian policies defined below and show that this class contains an -optimal policy for any (see, Proposition 3).

In the following definition, is the set of probability distributions on the collection of possible experiments in and is the set of continuous measurable functions from to . For a randomized experimentation policy , we let denote the probability of selecting experiment , which is continuous in for all .

Definition 2.

(Continuous Randomized Markovian Policy) A continuous randomized Markovian policy is a pair . For all , the DM displays experiment with probability . On the other hand, for the decision maker chooses to stop the experimentation process and implements an optimal action .

Next, we move to state our limiting result for the belief process under the scalings given in (8) and (9).

Proposition 2.

Remark 1.

Throughout the paper, we use tildes (‘’) to denote quantities that are related to the asymptotic approximation.

The next result shows that restricting our attention to continuous randomized policies is without a significance loss of optimality in the sense of the norm.

Proposition 3.

Let be an optimal Markovian policy with a corresponding value function . For any , there exists a continuous randomized policy in with expected payoff function such that,

where is the norm in .

In sum, and in light of Proposition 2 and 3, we suggest the following diffusion-asymptotic approximation of the decision maker’s problem given in (4):

| (11) |

We can view problem (11) as having two decision variables, namely, the experimentation policy and the intervention region . Interestingly, it turns out that we can decouple the optimization of these two decisions, in particular we can solve for the optimal experimentation without computing explicitly . Surprisingly, this implies that the choice of an optimal experiment is independent of the intervention region, and thus of how long the decision maker decides to run the experimentation process. We formalize this observation in the following section.

4.2 Asymptotically Optimal Experimentation Policy

From the diffusion approximation in equation (11), one can easily see that the impact of an experimentation policy has on the decision maker’s optimization problem is channelled only through the volatility of the belief process . We use this fact to derive a rather simple solution to the problem of selecting an asymptotically optimal policy . (The superscript ‘A’ is mnemonic of Asymptotic). To this end, let us define the mapping

which acts as a random time change in the following proposition.

Proposition 4.

The optimization problem in (11) is equivalent to

The previous result provides an alternative interpretation of the effect an experimentation policy has on the decision maker’s performance. According to Proposition 4, a policy impacts only the discount factor, that the decision maker uses to penalize the time value of money. The following corollary follows directly from this observation.

Corollary 1.

(Maximum Volatility) For any stopping set , an optimal asymptotic experimentation policy minimizes the modified discount factor pathwise, or equivalently, maximizes pointwise the belief process’s volatility . Thus, from (10), we conclude that we can select to be a static experimentation policy, namely, for all where is given by

(If there are multiple experiments that maximize the expression inside the brackets then we can select any static experimentation policy that uses an experiment from the argmax set.)

A few remarks about this result are in order. First, Corollary 1 confirms our previous claim that an optimal experimentation policy is independent of the choice of the stopping set and so we can effectively decouple the problem of determining an optimal experimentation strategy and that of when to stop experimenting. We also note that an optimal static experimentation strategy is continuous in and so we can invoke the weak convergence in Proposition 2 directly to .

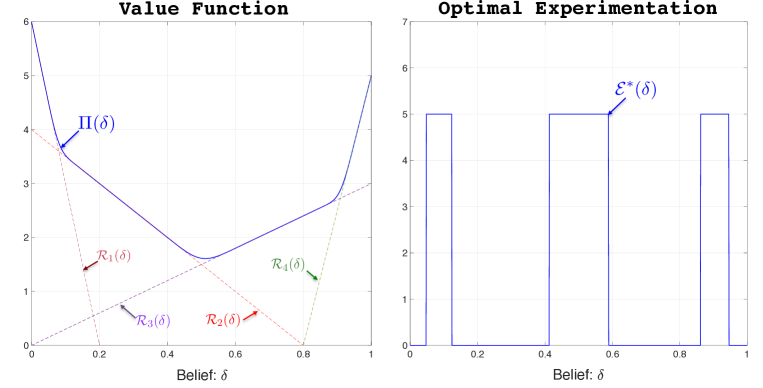

Example 2.

(Example 1 Revisited) To illustrate the result in Corollary 1, let us revisit the instance in Example 1 in the context of the asymptotic regime. To this end, suppose the probabilities for the instance of the problem are equal to

Experiment 2 3 4 5 6 7 0.2 0.3 0.4 0.5 0.6 0.7 0.0 0.0 0.0 0.0 0.0 0.0 -0.8 -0.7 -0.6 -0.5 -0.4 -0.3 .

Note that we are not including Experiments 1, 8 and 9 since they are dominated (see Section 3.3). Also, the original probabilities in Table 1 correspond to the case . Figure 2 mimics Figure 1 but for .

Consistent with the result in Corollary 1, for sufficiently large, the optimal experimentation strategy consists of a single experiment independent of , which in this case corresponds to Experiment 5. One can check that Experiment 5 maximizes the instantaneous volatility of the belief process.

4.3 Optimal Stopping of Experimentation

Let us now turn to the problem of determining the optimal intervention region in the asymptotic regime under consideration. In what follows, we assume that an optimal experimentation policy has been selected based on Corollary 1. That is, we focus on solving problem (11) given the optimal experimentation policy . We find convenient to rewrite this problem using the following optimal stopping time formulation:

| (12) |

For notational convenience, throughout this section we suppress the dependence of and on the display set since it remains fixed.

We approach the problem in two steps. First, we derive optimality conditions in the form of a set of partial differential inequalities that characterize the optimal stopping time. Then, we use these inequalities to characterize an optimal solution and the corresponding payoff.

4.3.1 Quasi-Variational Inequalities

Let denote the set of real-valued continuous functions on having derivatives of order . We define also the set

| (13) |

(Note that the set depends on the specific function .) We also define the operator on as follows

| (14) |

Definition 3.

(QVI) The function satisfies the quasi-variational inequalities for the optimization problem (12), if for all

| (15) | |||

As one might expect, a solution to these QVI conditions partition the interval into two regions: a continuation region in which the firm’s optimal strategy is to keep experimenting and an intervention region in which stopping the experimentation process is optimal.

| Continuation: | ||||

| Intervention: |

For every solution of the QVI conditions we can associate a control .

Definition 4.

Let be a solution of the QVI conditions in (15). We define the control as follows

and refer to it as the QVI-control associated to .

We are now ready to formalize the verification theorem that provides the connection between the QVI conditions and the original optimization problem in (12).

Theorem 1.

(Verification) Let be a solution of the QVI in (15). Then,

In addition, if there exists a QVI-control associated with such that , then is optimal and .

This verification theorem reduces the problem of determining the value function to that of solving the QVI equations defined above. In order to find a solution, we take full advantage of the fact that the payoff function is a piecewise linear continuous function of (see equation (1)). Moreover, an important building block in our methodology is the solution to a special case in which has only two linear pieces, that is, the set includes only two actions. We will focus on this simpler case first and then show how to leverage this solution and extend it to the general case in which includes an arbitrary number of actions.

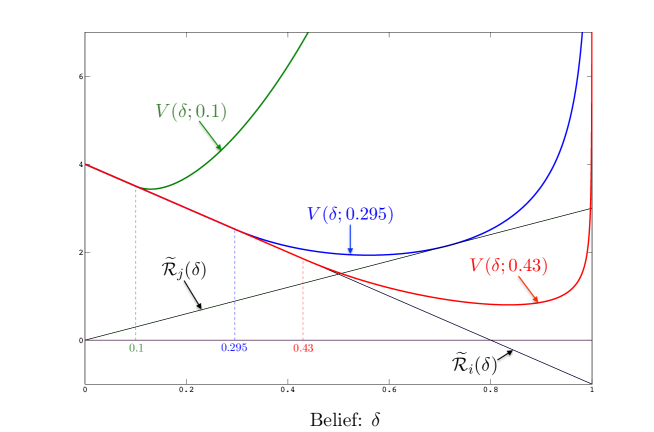

4.3.2 Special Case:

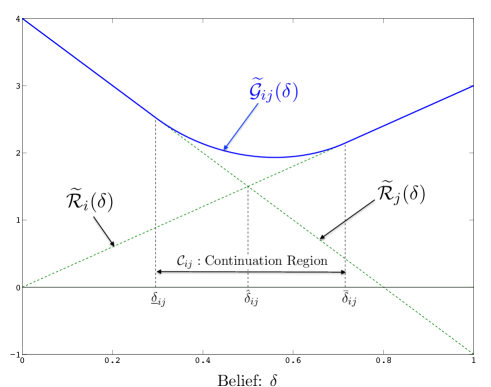

Suppose the set of actions is given by for two distinctive actions and . Let us denote by , where for (see equation (1)). Without loss of generality, we will assume that for all . Let us denote by the value of the belief at which . (Recall that we have assumed that there is no action in the set that is uniformly dominated and this assumption guarantees the existence of .)

To solve the QVI conditions in this special case we take “an educated guess” approach and assume that the continuation region is given by an interval , for two thresholds . Furthermore, we assume the intuitive fact that . To illustrate, consider the example in Figure 3 that depicts the value function as well as the payoff functions and for products and .

Data: , , and .

By definition, in the interior of the continuation region we have that . Hence, according to the third QVI condition, in this region the value function must satisfy . This is a second-order differential equation

whose general solution is given by

| (16) |

and and are two constants of integration.

To complete our proposed characterization of the value function, we need to determine the constants of integration as well as the two thresholds and that define the continuation region. To do that we impose the so-called value-matching and smooth-pasting conditions that regulate the behavior of the value function at the boundaries between the intervention and continuation regions. Specifically, we impose the conditions

| (17) |

We formalize our previous discussion in the next proposition.

Proposition 5.

Let . If then the QVI conditions admit a solution that we denote by given as follows

| (18) |

where and and are positive constants all determined by imposing the value matching and smooth pasting conditions in (17). The function is convex and in .

The verification theorem guarantees that the solution expressed in Proposition 5 is such that when . In terms of implementation, this solution corresponds to the following policy.

Asymptotically Optimal Intervention Policy: Suppose the initial belief lies in the interior of the continuation region that is, . In this case, the decision maker runs an experimentation process and keeps it running as long as . As soon as the belief process hits one of the two thresholds or then the experimentation process stops and the decision maker selects the action that maximizes at that time. On the other hand, if the initial belief is not in the interior of the continuation region then no experimentation is needed and the decision maker selects the action that maximizes at time 0.

The simple representation of the value function in Proposition 5 is due to the diffusion approximation obtained in this asymptotic regime. Moreover, this same diffusion approximation allows one to use some standard results for one-dimensional diffusion processes (e.g., Section 5.5 in KaratzasSchreve) to analyze its optimal solution. For instance, in those cases where experimentation should be conducted, and its duration would correspond to the first exit time of from the interval . The following corollary characterizes the expected duration of this experimentation phase as well as the likelihood that action or will be eventually selected.

Corollary 2.

Suppose and let and . Then,

where is the function

We conclude our discussion of this special case with by exploiting the result in Proposition 4 to derive upper and lower bounds for the value function.

Proposition 6.

The value function satisfies

Furthermore,

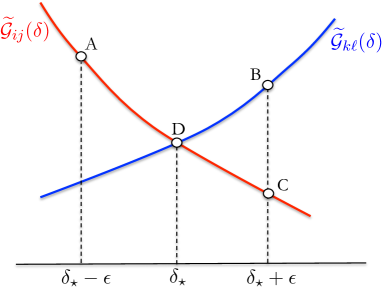

4.3.3 General Case:

Let us now turn to the general case in which the set includes an arbitrary but finite number of actions. Our derivation of the value function in (12) will be obtained based on the solution derived in the previous section. For each pair of actions , the function in Proposition 5 is the value function of a problem in which only actions and are available. It follows that for all and so

where is the point-wise maximum of the functions . Our main result in this section establishes that the inequality is in fact an equality, that is, . To prove this, we will show that the function satisfies the QVI conditions so that we can invoke the verification Theorem 1. To this end, we first show that satisfies all three QVI conditions in (15).

Proposition 7.

For all , we have that . Also, there exists a finite set such that and for all .

The attentive reader might have noticed that the result in Proposition 7 is not enough to invoke the verification Theorem 1. The reason is that, besides verifying the QVI conditions, we also need to show that the function is sufficiently smooth and belongs to the set (see equation (13)). We formalize this condition in the following result.

Theorem 2.

The function is in . As a result, .

It is worth noticing that the previous theorem shows that the complexity of the diffusion optimal stopping problem grows only quadratically with the cardinality of the action set . In fact, Theorem 2 reveals that solving a problem with actions is equivalent to solving a collection of problems each with only two actions.

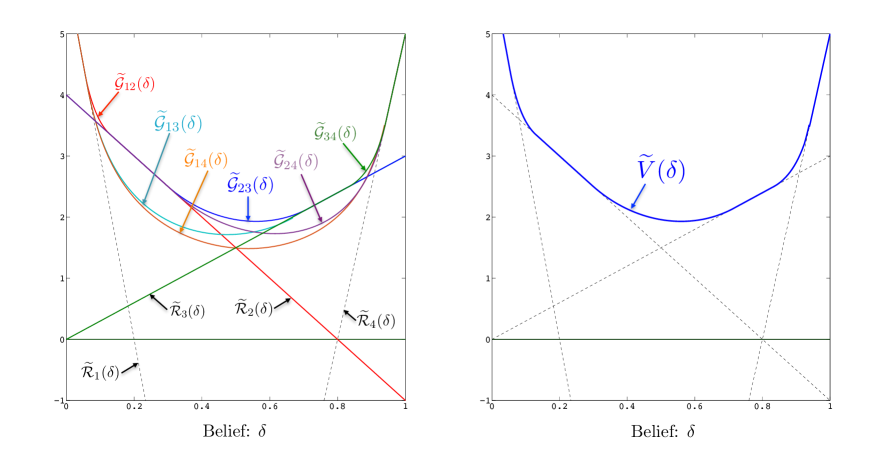

To illustrate the result in Theorem 2 and resulting optimal policy, let us consider the example in Figure 4 in which the set has four actions. The left panel depicts all six functions while the right panel depicts the function .

After a quick inspection, we can check that in this example there exist two (non-unique) thresholds and such that

Furthermore, at the functions and meet smoothly since . A similar smooth pasting occurs at since . As a result, since each of the functions is in by Proposition 5, it follows that is also in . Note also that an optimal policy is given by a sequence of thresholds that define the continuation and intervention regions. In this example, we have that

| Continuation: | ||||

| Intervention: |

where the thresholds and are defined in Proposition 5.

5 Non-Asymptotic Experimentation Policies

In this section we discuss how to interpret the asymptotic analysis developed in the previous section to construct experimentation policies that can be used in an arbitrary instance. Recall from Definition 1 that a policy consists of two components: (a) an intervention region that defines the set of beliefs at which the decision maker stops the experimentation process and selects an optimal action , and (b) an experimentation policy that identifies the experiment that the DM should conduct at each in the continuation region .

The asymptotic analysis of the previous section produces an experimentation strategy and an intervention region defined in Corollary 1 and Proposition 5, respectively. However, we cannot implement these policies directly since they are computed in terms of the non-primitive quantities , and appearing in Assumption 1. Therefore, in order to recover a solution to an arbitrary instance of the problem from the asymptotic analysis of the previous section, we need to derive the values of , and from the primitives of the model, namely, from the values of , and .

In some settings this derivation can be done directly by imposing a specific parametric structure in the definitions of and . The idea in these settings is that the parametric structure is used to capture a distinctive feature of the problem at hand which in turn would determine the asymptotic regime of interest. Let us illustrate this point with a concrete example.

Example 3.

Consider a setting where the primitives are known and assumed to be continuously differentiable in for in some open neighborhood that contains the two hypothesis and . Suppose that we are interested in a setup where a distinctive characteristic of the problem is that the two hypotheses are hard to distinguish. We can model this feature by setting for some fixed scalar . Using a first order Taylor expansion, it follows that , where is the partial derivative of with respect to . Under this specific parametrization of the problem, we can now apply the asymptotic analysis of the previous section (by letting go to infinity) to derive the corresponding values of , and . In this case, it is not hard to see that

In Section 6 we consider at length a concrete application related to crowdvoting where are viewed as choice probabilities governed by an MNL model. In this context, similarly to Example 3 we also derive the quantities and not only for the case of indistinguishable hypotheses but also for the case where the experiments outcomes are very noisy.

The previous example provides some insights on how one can leverage some concrete knowledge about the structure of the problem to identify the proper asymptotic regime to use. However, this approach does not generalize in an obvious way to an arbitrary setting for which such knowledge is not available. In what follows we propose a methodology that does not rely on any additional information beyond the values of , and .

Combining the asymptotic scalings in equations (8) and (9), we have that the input parameters , and satisfy the following relationship for large

| (19) |

Furthermore, going back to the conditions that define the asymptotic regime in Corollary 1, we see that the value of is such that the quantity

converges to zero at a rate of uniformly in , and . Thus, in a non-asymptotic regime, we can reinterpret this condition as one that requires to be as close as as possible for all , and . In other words, we can represent this problem as an optimization problem that minimizes the ‘distance’ between and . We propose the following min-max formulation to compute

| (20) |

After computing the value of , we can obtain the values of and using (19), that is,

| (21) |

The following proposition establishes the consistency between the value of the probability kernel computed in (20) and the corresponding asymptotic limit.

Proposition 8.

Let us now turn to the issue of how to adapt the asymptotic solutions to derive implementable policies. Equations (20) and (21) allow us to compute the values of , and that are needed to derive the asymptotic strategy and . From Corollary 1, we have that

On the other hand, the value of is obtained from our diffusion analysis of the optimal stopping problem combining the results in Proposition 5 and Theorem 2. The volatility of the underlying diffusion process is the one identified in Proposition 2, that is,

We use this asymptotic solution ) to propose two concrete approximation policies.

-

•

Asymptotic Policy (A): This policy implements directly the strategy ).

-

•

Maximum Volatility Policy (MV): This policy uses the same intervention region as the Asymptotic policy. On the other hand, in terms of experimentation, the MV policy reinterprets the solution in Corollary 1 and for each in the continuation region selects the experiment that maximizes the instantaneous volatility, that is, , where

(22) (The subscript ‘MV’ is mnemonic for ‘Maximum Volatility’.)

Note that the Asymptotic policy suggests a static experimentation while the Maximum volatility offers a dynamic experimentation, function of the current belief. However, it should be clear from our previous discussion that both of these policies are asymptotically equal and optimal in the limiting regime defined by equations (8) and (9). It is also worth noticing that in contrast to the derivation of an optimal experimentation policy in equation (6) that requires full knowledge of the value function, the MV policy can be computed directly using only the knowledge of the likelihood function . This, of course, simplifies significantly its computational complexity.

In Section 7, we conduct a set of numerical experiments to test the performance of our proposed policies using a concrete application in the context of new product introduction that we present in the next section. We conclude this section with a remark on how to extend some of the insights that have developed to the problem of designing the type of experiments that the DM can use.

5.1 A Remark on the Optimal Design of Experiments

In some applications (such as the assortment selection problem that will be discussed in the next section), the decision maker has some degree of control over the design of the set of available experiments. In such cases, observe that the optimization in (22) that defines can be reformulated over a more abstract set of likelihood ratios, where each corresponds to an experiment . As a result, the optimization problem that defines the Maximum Volatility policy is given by,

where, denotes the expectation under the probability measure .

Depending on the nature of the set , the optimization problem above can be casted as a Tchebycheff moment problem. Consider the following setting where the DM can design experiments that correspond to any possible likelihood ratio , as long as is bounded by two given quantities and . In this case the following result holds:

Proposition 9.

Suppose that for two non-negative scalars and , and let

Then, is a random variable with a two-point distribution with mass at and .

Proof: The result follows from noticing that the function is convex and so an optimal solution is a two-point distribution with mass at and .

The solution in Proposition 9 suggests that the decision maker should select an experimentation policy that maximizes the range of the likelihood function. In Section 7, we explore this idea and propose a variation of the Maximum Volatility policy that incorporates this ‘maximum range’ condition and show very good numerical performance.

6 Illustrative Example: New Product Introduction

We discuss in this section a concrete application of the methodology and results presented in the previous sections in the context of a new product introduction problem. The literature on the topic is quite broad (see, the recent work of Sunaretal19 and references their). In particular, we consider an environment in which the experimentation outcomes are the result of a consumers’ voting process driven by a Multinomial choice model (MNL). Our objective in developing this example is twofold. First, we use it to provide some specific details on how to formulate and derive our proposed asymptotic approximation policies discussed in the previous section. As a by-product of this discussion, we also show how to obtain diffusion approximations for a belief process that is governed by an MNL model using two different types of asymptotic regimes. Given the popularity of the MNL model to represent consumer preferences, we believe that our diffusion approximation has applications beyond the one discussed in this section. Our second objective is to use this concrete example in Section 7 to conduct a set of numerical experiments to test the quality of our proposed methodology. For instance, we are interested in testing the accuracy of the maximum volatility principle derived in Corollary 1 and the two heuristic policies introduced in Section 5, which provide remarkably simple rules for conducting dynamic experimentation.

6.1 Model Setup

The specific setting that we consider is as follows. Consider a seller (or firm) who is contemplating the possibility of introducing a new product (or products) into the marketplace. In the process of developing these new products, the seller has prototyped different versions and would like to decide which is the right subset to commercialize, if any. These prototypes differ in terms of some specific set of attributes which might include their price and quality as well as launching and manufacturing costs, to name a few. We assume that the intrinsic utility that a consumer assigns to version is equal to , where is some unknown real parameter.

Example 4.

(Linear Utilities) A popular modeling approach is to assume that the utilities are linear in the unknown parameter . For instance, we can have , where and are product ’s quality and price, respectively. In this case measures consumers’ price sensitivity.

The seller is uncertain about market conditions and does not know the value of the parameter . In an attempt to reduce the risk of launching the wrong version(s), the seller sets up an online voting system in which potential customers (those visiting the seller’s website) can vote for the different prototypes. For simplicity, we assume that each voter votes for at most one version and the seller only tracks the cumulative number of votes for each one. (In practice, we could imagine a more sophisticated interface using a more detailed scoring system, e.g., a 0 to 10 scale, or even allowing for consumer reviews.) This voting phase occurs before the seller decides to launch a product and has the potential of offering a win-win situation whereby a consumer who votes hopes to influence the seller to commercialize the right version; and on the other hand, these votes and their pace provide valuable information that the seller can use to better forecast the value of . As we show later, it is not necessarily optimal for the seller to display the entire set during the voting phase. Hence, we assume that the seller selects a subset of prototypes to show during the voting phase. We call the display set and let be its cardinality. To keep some consistency between the notation in this and the previous sections, we note that, in the most general case, both the set of experiments and available actions coincide with the power set of , that is, . In some cases, however, one might need to restrict the set of experiments and actions. For instance, if the number of prototypes is large then it might be impractical to display the entire menu and experimentation should be restricted to display sets of a given cardinality. Similarly, it is also possible that the seller is constrained in the number of versions that she can launch.

Voters arrive according to a Poisson process with rate and vote for one alternative from the display set according to a multinomial choice model. Specifically, a voter who observes a display set assigns to each version a utility , where are idiosyncratic utility shocks that are independent and identically distributed according to a Gumbel distribution with mean zero and variance , for some fixed constant . It follows that a utility-maximizing voter votes for version with probability

| (23) |

Note that our formulation allows for the possibility that a voter might end-up not selecting any of the available options. To model this no-vote option we simply include version ‘0’ with quality, price and intrinsic utility equal to zero, . In what follows we assume that every display set includes the non-purchase option.

We assume that the seller has a prior belief about the value of that can take one of two possible values , and her prior is that with probability . We let and denote voters’ intrinsic utilities under these two hypotheses for and define the likelihood ratio function by

| (24) |

We complete the description of the model by specifying the seller’s objective function. As in the general case, we assume that there exists a piecewise linear function (see equation (1)) that represents the seller’s expected payoff as function of her belief . The seller’s optimization problem is given by

| (25) |

Recall that a policy is defined by an experimentation policy that determines the collection of display sets to use throughout the voting process and an intervention region that defines the duration of the voting campaign.

Remark 2.

(Payoffs from Sales) To illustrate a concrete example of a piecewise linear payoff function in the context of new product introduction, consider the case in which the seller is interested in maximizing the expected discounted value of the cash-flows generated by the sales that occur after time . Specifically, at time , the seller stops the voting process and selects a subset of products to launch based on the available information at this time. Suppose consumers arrive according to a Poisson process of rate and make buying decision according to the same MNL model that governs the voting process. Under this assumption, the seller expected discounted payoff is given by

where , and are the per-unit price, manufacturing cost and fixed launching cost of product , respectively, and

In the case that all products are discarded, one can assume the seller receives a fixed payoff (possibly zero) which captures the opportunity cost of her business. Finally, the seller’s payoff function in this case is given by .

6.2 Asymptotic Approximation

We move now to apply the results in Section 4 to approximate the optimization in (25) by a diffusion control problem. In order to invoke the weak convergence result in Proposition 2, we need to specify an asymptotic regime under which the MNL choice probabilities satisfy the condition in equation (8). In what follows we propose two concrete alternatives, each capturing a different type of uninformativeness associated with the voting process.

6.2.1 Noisy Preferences

Motivated by the issue of low-quality data that has been reported in the context of online learning applications and advertising (Kohavi17, LewisRao15), we consider a regime in which the variance of the MNL idiosyncratic shocks in the instance of the problem grows proportionally with , namely, . In other words, this asymptotic regime is one in which votes –and the information they contain– become more and more noisy as grows large.

Under this scaling, one can show that the choice probability in (23) can be written as

| (26) |

which satisfies the requirements in Assumption 1 with

Recall that under our asymptotic scaling, voters arrive according to a Poisson process with intensity in the instance of the problem. Given this scaling of and , we can use the result in Proposition 2 to obtain the following corollary.

Corollary 3.

Let and . Suppose the seller uses a static display policy during the voting process. Then, the belief process converges weakly to the solution of the SDE

and is a Wiener process.

Combining this result together with the maximum volatility principle in Corollary 1 we can now identify an optimal display set in this asymptotic regime under consideration, namely

| (27) |

(The subscript ‘NP’ stands for Noisy Preferences regime.)

Without loss of generality, let us index the prototypes in ascending order of so that . Also, for , let us define the display set

| (28) |

which includes the non-purchase option together with the first prototypes with the lowest values of and the prototypes with the highest values of .

Proposition 10.

Let be a solution to (27), then there exist integers and with such that . Furthermore, in the special case that all the have the same sign (i.e., or ) then consists of a single prototype together with the non-purchase option ‘0’, that is, .

An important corollary of Proposition 10 is that instead of solving (27) over the power set of we can restrict ourselves to the much simpler problem of maximizing the volatility of the belief process over the significantly smaller class of display sets which has a cardinality of .

Example 5.

(Example 4 Revisited) Suppose the intrinsic utility of product is equal to , then . If all the are of the same sign, for example, if they correspond to the prices of the products, then the are also of the same sign and the optimal display set includes a single prototype, namely, the one with the highest price.

6.2.2 Asymptotically Indistinguishable Hypotheses

An alternative regime in which we can apply the asymptotic analysis of Section 4 corresponds to the case in which the values of and become indistinguishable as grows large. To be precise, let us consider the case in which for , where are fixed constants independent of . Under this scaling, the choice probability in (23) admit the following representation:

| (29) |

where . It follows that these choice probabilities satisfy the conditions in Assumption 1 with

From Corollary 1 the optimal display set in this asymptotic regime is given by

| (30) |

(The subscript ‘IH’ stands for Indistinguishable Hypotheses regime.)

To get some intuition about , consider an arbitrary display set and let be a random variables taking values in with probability distribution . (In this definition we assume that if .) Then, (30) can be rewritten as

Remark 3.

It is worth noticing that the asymptotic regime in which the two alternative hypotheses and are asymptotically indistinguishable does not imply that the DM optimization problem becomes trivial in the limit. To see this, let us consider the payoff structure discussed in Remark 2, where is the discounted payoff that the DM expects to collect if she launches assortment when her belief is . Under the scaling in (29) it is not hard to show that for the instance

where is the selling rate after launching. Thus, depending on the rate of grow of with there is a non-negligible difference in payoffs between the two hypotheses and so it is in the DM best interest to try to learn which one holds true.†††During the voting phase we have assumed that the arrival rate of voters is but during the selling phase the arrival rate does not need to be of the same order and could drop to . In this case, the different payoffs between the two hypotheses would still be significant.

7 Numerical Experiments

In this section, we conduct a set of numerical experiments to assess the quality of our methodology using the application discussed in the previous section. In particular, we are interested in investigating the performance of our proposed Asymptotic and Maximum Volatility policies introduced in Section 5.

Optimality Gap: In our first set of computational experiments, we numerically evaluate the optimality gap of the Asymptotic and Maximum Volatility policies with respect to an optimal policy using the Noisy Preferences model in Section 6.2.1. We let , and denote the value functions generated by the A, MV and optimal policy, respectively, and define the optimality gap of these policies by

We measure and using a set of 500 random instances of the problem. Specifically, we consider a problem with products, whose intrinsic utilities and are randomly generated uniformly in for all . For each random instance we run five different scenarios in which and , with for . The rest of the parameters are kept fixed with , and the terminal payoff function . This is the same terminal payoff function that we used in the examples in Figures 2 and 4. Finally, in these and the rest of our numerical computations we evaluate the value function of a given policy using Gauss-Seidel value iteration (see section 6.3 in Puterman05) with an error tolerance of over a mesh of size for the interval that defines the domain of .

Table 2 presents the mean optimality gap –as well as the maximum value and standard deviation– computed over a run of 500 randomly generated instances.

Optimality Gap:

| Mean | 2.39% | 1.77% | 0.87% | 0.27% | 0.13% |

|---|---|---|---|---|---|

| Max | 26.19% | 22.95% | 13.67% | 1.99% | 0.87% |

| St. Dev. | 4.88% | 4.18% | 1.55% | 0.39% | 0.13% |

Optimality Gap: Mean 0.56% 0.12% 0.26% 0.15% 0.09% Max 4.09% 1.47% 3.56% 1.87% 0.43% St. Dev. 0.86% 0.22% 0.41% 0.22% 0.06% Data: , , and , .

As we can see from the table, the two policies performs very well on average, although, the MV policy is substantially better than the A policy, especially for small value of . As grow large both policies approach the optimal policy, which is consistent with our asymptotic analysis in Section 4. By comparing the ‘Max’ rows that report the maximum optimality gap, we can also see that the MV policy is significantly more robust than the A policy for small values of .