mainReferences

Coordinated Capacity Reductions and Public Communication in the Airline Industry††thanks: This paper was previously circulated under the title “Public Communication and Collusion in the Airline Industry.” We thank Yu Awaya, David Byrne, Karim Chalak, Marco Cosconati, Kenneth G. Elzinga, Leslie Marx, Robert Porter, Mar Reguant, D. Daniel Sokol, and the seminar/conference participants at the DOJ, University of Florida, UVa, the 16th IIOC, 2018 BFI Media and Communication Conference, 2018 DC IO Day, NBER IO SI 2018, EARIE 2018, 2018 FTC Microeconomics Conference, 2018 PSU-Cornell Conference, 8th EIEF-UNIBO-IGIER Bocconi IO Workshop, and 2020 Next Generation of Antitrust Scholars Conference for their constructive feedback. We also thank the Buckner W. Clay Dean of A&S and the VP for Research at UVa for financial support, and Divya Menon for outstanding research assistance. Aryal and Ciliberto acknowledge the Bankard Fund for Political Economy at the University of Virginia for support. Finally, we thank Aureo de Paula and three anonymous reviewers for their helpful feedback.

Abstract

We investigate the allegation that legacy U.S. airlines communicated via earnings calls to coordinate with other legacy airlines in offering fewer seats on competitive routes. To this end, we first use text analytics to build a novel dataset on communication among airlines about their capacity choices. Estimates from our preferred specification show that the number of offered seats is 2% lower when all legacy airlines in a market discuss the concept of “capacity discipline.” We verify that this reduction materializes only when legacy airlines communicate concurrently, and that it cannot be explained by other possibilities, including that airlines are simply announcing to investors their unilateral plans to reduce capacity, and then following through on those announcements.

(JEL: D22, L13, L41, L93)

1 Introduction

There are two legal paradigms in most OECD countries meant to promote market efficiency, but that are potentially at odds with one another. On the one hand, antitrust laws forbid firms from communicating their strategic choices with each other to deter collusion. On the other hand, financial regulations promote open and transparent communication between publicly traded firms and their investors. While these latter regulations are intended to level the playing field among investors, policymakers have raised concerns that they may also facilitate anticompetitive behaviors. For example, the OECD Competition Committee notes that there are pro-competitive benefits from increased transparency, but “information exchanges can … offer firms points of coordination or focal points,” while also “allow[ing] firms to monitor adherence to the collusive arrangement” \citepmainOCED2011. Thus, firms can be transparent about their future strategies in their public communications to investors—e.g., by announcing their intention to rein capacity—which can foster coordination among firms in offering fewer seats.111 Similar situations, where one set of laws is at odds with another, generating unanticipated consequences, often as antitrust violations, occur in many industries. For example, in the U.S. pharmaceutical industry, the tension between the FDA laws and patent law led to the Drug Price Competition and Patent Term Restoration Act (colloquially known as the Hatch-Waxman Act). This Act aims to reduce entry barriers for generic drugs, but it incentivized incumbent firms to “Pay-for-Delay” of generic drugs and stifle competition. For more, see \citemainFedlmanFrondorf2017. Other cases include \citemainByrneRoos2017 who document that gasoline retailers in Australia used a price transparency program called Fuelwatch to initiate and sustain collusion. Furthermore, \citemainBourveauSheZaldokas2019 document that with the increase in cartel enforcement, firms in the U.S. start sharing more detailed information in their financial disclosure about their customers, contracts, and products, which may allow tacit coordination in product markets.

In this paper, we contribute to this overarching research and policy issue by investigating whether the data are consistent with the hypothesis that top managers of legacy U.S. airlines used their quarterly earnings calls to communicate with other legacy airlines to coordinate in reducing the number of seats offered.222An earnings call is a teleconference in which a publicly-traded company discusses its performance and future expectations with financial analysts and news reporters. Legacy carriers are Alaska Airlines (AS), American Airlines (AA), Continental Airlines (CO), Delta Airlines (DL), Northwest Airlines (NW), United Airlines (UA) and US Airways (US), and the low-cost carriers (LCC) are AirTran Airways (FL), JetBlue (B6), Southwest (WN) and Spirit Airlines (NK). Specifically, we investigate whether legacy airlines used keywords associated with the notion of “capacity discipline” in their earnings calls to communicate to their counterparts their willingness to reduce offered seats in markets where they compete head-to-head.333 This idea that “capacity discipline” is used by airlines to signal their alleged intention to restrict supply has been applied in class-action lawsuits filed against a few airlines. \citemainNYT2 and \citemainNYT1 provide coverage of this concept in the popular press. See \citemainRosenfieldCarltonGertner1997 and \citemainKaplow2013 for antitrust issues related to communication among competing firms.

The airline industry is an appropriate industry to investigate the relationship between communication and coordinated reduction in capacities because it is characterized by stochastic demand, and private and noisy monitoring, both of which make coordination difficult without communication.444There is a precedence of accusation against the airlines for using communication technologies to coordinate. For example, in 1992, the U.S. DOJ alleged that airlines used the Airline Tariff Publishing Company’s electronic fare system to communicate and collude, see, for example, \citemainBorenstein2004 and \citemainMiller2010. Demand is stochastic, not least because of exogenous local events, such as the weather, unforeseen events at the airport, and spillovers from other airports. Monitoring is private and noisy because, first, airlines do not instantaneously observe others’ actions; second, they use connecting passengers to manage their load factors; and third, they observe only each other’s list prices, not transaction prices.

Recently, \citemainAwayaKrishna2016, \citemainAwayaKrishna2017 and \citemainSpector2015 have shown that firms may be able to use cheap talk–unverifiable and non-binding communication–to sustain collusion in environments with private and noisy monitoring, where collusion is otherwise unsustainable.555 There is a vast literature on market conduct and the behavior of cartels; see \citemainHarrington2006,MailathSamuelson2006, HarringtonSkrzypacz2011, and \citemainMarshallMarx2014. Among others, \citemainPorter1983, GreenPorter1984 study collusion under imperfect monitoring where all firms observe the same (noisy signal) price. In their setting, access to communication technology does not have any effect because the profits from public perfect equilibrium with or without communication are the same. Some examples where communication helped collusion are \citemainGenesoveMullin2001, \citemainWang2008,Wang2009, \citemainClarkHoude2014, and \citemainByrneRoos2017, among others. In our context, airlines have access to public communication technology, their quarterly earnings calls, through which they can simultaneously communicate with other airlines.666 Airlines may have other avenues for coordination, e.g., via industry conferences and trade organization events \citepmainAwayaKrishna2020 and common-ownership \citepmainAzarSchmalzTecu2018. However, quarterly earnings call are ideal for our purpose because they occur at regular intervals, every publicly listed airline uses them, and we observe the conversation. Our decision to consider only communication through earnings calls can be viewed as conservative because we cannot account for any amount of relevant communication outside this medium and underestimate the negative relationship between communication and capacity. And lastly, we focus only on simultaneous messaging among (legacy) airlines and do not distinguish intra-quarter timing of airlines because determining if there is a “leader” among the airlines by following, say, \citemainByrneRoos2017, would require higher-frequency (e.g., daily) data on communication.

We build an original and novel dataset on the content of public communication from earnings calls to measure communication and assess its relationship with capacity. The Securities and Exchange Commission (SEC) requires all publicly traded companies in the U.S. to file a quarterly report, which is accompanied by an earnings call—a public conference call where top executives discuss the report’s content with analysts and financial journalists. We collected transcripts of all such calls for 11 airlines from 2002:Q4 to 2016:Q4. We then classified each earnings call as either pertinent or not pertinent, depending on whether the executives on the call declared their intention of engaging in capacity-discipline or not.777 Other papers that use “text as data” \citepmainGentzkowKellyTaddy2017, include \citemainLeyden2017, who uses text descriptions of smartphone and tablet apps to define relevant markets, \citemainGentzkowShapiro2010, who use phrases from the Congressional Record to measure the slant of news media, and \citemainHobergPhilips2016, who use the text descriptions of businesses included in financial filings to define markets.

We estimate the relationship between communication and carriers’ monthly, market-level capacity decisions using the Bureau of Transportation Statistics’s T-100 Domestic Segment dataset, which contains domestic non-stop segment data reported by both U.S. and foreign air carriers. To that end, we regress the log of seats offered by an airline in a market in a month on an indicator of whether all legacy carriers operating in that market discuss capacity discipline. Given that airlines’ capacity decisions depend on a wide variety of market-specific and overall economic conditions, we include covariates to control for such variation across markets and carriers over time.

We find that when all legacy carriers operating in an airport-pair market communicate about capacity discipline, the average number of seats offered in that market is 2.02% lower. To put this number in perspective, we note that the average change in capacity among legacy carriers in comparable markets where communication does not occur is 3.67%. So a 2.02% reduction in capacity associated with the phrase “capacity discipline” accounts for more than 50% of this average change, which is economically significant.

Capacity reductions have the potential to benefit consumers if they lead to a more optimal scheduling of flight departure times at the airports without affecting ticket fares. However, we (i) do not find evidence to support the hypothesis that carriers adjust the crowding of departures, and, furthermore, we (ii) find that communication is positively associated with fares. So, even though we do not estimate the social value of communication \citepmainMyattWallace2015, our estimates suggest that the carriers’ capacity reductions are economically significant and they most likely harm consumers.

Nonetheless, we face two primary identification challenges in investigating the accusation that legacy U.S. carriers are using their earnings calls to coordinate capacity reduction. First, there may be a more straightforward, alternative explanation for our findings. In particular, it might be that airline executives are communicating to investors their intention to reduce capacity, not because they want to coordinate, but because reducing capacity is the best response to negative demand forecasts. In other words, our results may be evidence that earnings calls are serving their ostensible purpose.

We address this concern in three ways. First, we find that legacy carriers unilaterally discussing capacity discipline is not associated with them reducing capacities. Second, we find that the capacity is not lower in monopoly markets when legacy carriers discuss capacity discipline. Finally, we find that legacy carriers do not decrease their capacity when all but one of the legacy carriers serving a market have discussed capacity discipline. Suppose discussions of capacity discipline were meant to inform investors about the carrier’s future actions. In that case, we should see a reduction in all three of these cases.

Second, an airline could be using earnings calls to truthfully share its payoff relevant private information with other airlines, which, when others do the same, could induce correlation in their capacity plans. Importantly, this alternative explanation does not require airlines to actively coordinate their capacity choices, as long as they communicate truthfully.

We do not believe that this explains our findings. First, we note that \citemainClarke1983, \citemainGalor1985, and \citemainLi1985 have shown that firms do not have an incentive to share their payoff relevant private information about demand with others unless they intend to coordinate on an action, e.g., capacity choice. Second, if this hypothesis is correct, then it implies that the likelihood of us observing a reduction in capacity by an airline would increase with the number of legacy airlines communicating, irrespective of the said airline’s private information. If airlines were only sharing their information, then an airline should be responsive to others’ announcements. We show that, contrary to this information-sharing hypothesis, even when all of a legacy carrier’s legacy competitors in a market communicate, if the carrier itself does not communicate, then it does not reduce its capacity. However, this result is consistent with airlines using earnings calls to coordinate on their capacities.

2 Institutional Analysis and Data

In this section we introduce the legal cases that motivate our analysis, explain how we use Natural Language Processing (NLP) techniques to quantify communication among airlines, present our data on the airline industry, and show that airlines have flexible capacity at the market level.

2.1 Legal Case

On July 1, 2015, the Washington Post reported that the U.S. Department of Justice (DOJ) was investigating possible collusion to limit available seats and maintain higher fares in U.S. domestic airline markets by American, Delta, Southwest, and United (Continental) \citepmainWapo2015. It was also reported that the major carriers had received Civil Investigative Demands (CID) from the DOJ requesting copies, dating back to January 2010, of all communications the airlines had had with each other, Wall Street analysts, and major shareholders concerning their plans for seat capacity and any statements to restrict it. The CID requests were subsequently confirmed by the airlines in their quarterly reports.888 In Appendix F we consider whether our results vary before and after the January, 2010 threshold, and the July, 2015 reporting of the DOJ investigation.

Concurrently, several consumers filed lawsuits accusing American, Delta, Southwest, and United of fixing prices, which were later consolidated in a multi-district litigation. The case is currently being tried in the U.S. District Court for the District of Columbia.999 This is the “Domestic Airline Travel Antitrust Litigation” case, numbered 1:15-mc-01404 in the US District Court, DC. Another case, filed on August 24, 2015, in the U.S. District Court of Minnesota against American, Delta, Southwest Airlines, and United/Continental, alleges that the companies conspired to fix, raise, and maintain the price of domestic air travel services in violation of Section 1 of the Sherman Antitrust Act.101010 Case 0:15-cv-03358-PJS-TNL, filed 8/24/2015 in the US District Court, District of Minnesota. In November 2015, this case was transferred to the District Court in DC. At the time of this writing, American Airlines and Southwest have settled the class action lawsuits.

The lawsuits allege that the airline carriers collusively impose “capacity discipline” in the form of limiting flights and seats despite increased demand and lower costs, and that the four airlines implement and police the agreement through public signaling of future capacity decisions.111111 The consumers’ lawsuits also stress the role of financial analysts who participate at the quarterly earnings call. See \citemainAzarSchmalzTecu2018 for a recent work on the role of institutional investors on market conduct. We instructed our research assistant (RA) to find all instances where institutional investors were the first to bring up capacity discipline. The RA found only three such instances. Therefore, we decided not to consider the role of institutional investors in our analysis. In particular, one of the consumers’ lawsuits reported several statements made by the top managers of American, Delta, Southwest, United, and other airlines. The statements were made during quarterly earnings calls and various conferences.121212 For example, during the US Airways 2012:Q1 earnings call, the CFO of US Airways Derrick Kerr said “.. mainline passenger revenue were $2.1 billion, up 11.4% as a result of the strong pricing environment and continued industry capacity discipline.” – US Airways. and in the Delta’s earnings calls for the same quarter Delta’s CEO Richard Anderson said “You’ve heard us consistently state that we must be disciplined with capacity.” – Delta

These lawsuits provide the foundation to build a vocabulary from the earnings calls that can capture legacy airlines’ (alleged) intention to restrict their offered capacity. To that end, we have to consider both the semantics (airlines’ intention to rein in capacity) and the syntax (which keywords are used) of the earnings call reports. Next, we explain the steps we take to measure communication.

2.2 Earnings Call Text as Data

All publicly traded companies in the U.S. are required to file a quarterly report with the SEC. These reports are typically accompanied by an earnings call, which is a publicly available conference call between the firm’s top management and the analysts and reporters covering the firm. Earnings calls begin with statements from some or all of the corporate participants, followed by a question-and-answer session with the analysts on the call. Transcripts of calls are readily available, and we assume that carriers observe their competitors’ calls.

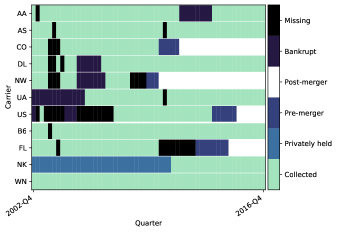

We collected earnings call transcripts for 11 airlines, for all quarters from 2002:Q4 to 2016:Q4 from LexisNexis (an online database service) and Seeking Alpha (an investment news website). Figure 1 indicates the availability of transcripts in our sample for each of the 11 airlines. As the figure shows, transcripts are available for most of the quarters except under (i) Bankruptcy—five carriers entered bankruptcy at least once during the sample period; (ii) Mergers and acquisitions—airlines did not hold earnings calls in the interim period between the announcement of a merger and the full operation of the merger; (iii) Private airlines—Spirit Airlines, which was privately held until May 2011, neither submitted reports nor conducted earnings calls prior to its initial public offering; and (iv) Other reasons—in a few instances the transcripts were unavailable for an unknown reason. In all cases where a call is unavailable, we assume the carrier cannot communicate to its competitors.131313 Of course, the airlines may have other means to communicate, that we do not observe (e.g., see Footnote 6). To the extent to which airlines use other, unobserved, means of communications when earnings calls are unavailable our estimate will be biased toward zero (or positive).

The key step of our empirical analysis is to codify the informational content in these quarterly earnings calls into a dataset that can be used to see how capacity choices change over time in response to communication among legacy carriers. Before delving into the conceptual challenges, we note two preliminary steps. Every statement made by the operator of the call and the analysts is removed from the transcripts, as are common English “stop words” such as “and” and “the.” Then we tokenize (convert a body of text into a set of words or phrases) and lemmatize (reduce words to their dictionary form) the text from the earnings calls. For example, the sentence “The disciplined airline executive was discussing capacity discipline” would be reduced to {discipline, airline, executive, discuss, capacity, discipline}. This process allows us to abstract from the inflectional and derivationally related forms of words to better focus on the substance/meaning of the transcripts.

To do so, we use a combination of NLP techniques and manual review to identify a list of words or phrases that are potentially indicative of managers communicating their intention to cooperate with others in restricting their capacity. Although in most cases managers specifically use the term “capacity discipline,” managers sometimes use other word combinations when discussing capacity discipline. This identification is a time-consuming process, and it is the focus of the remainder of this section.141414 In Section 4.3, we also use NLP to identify words that can be used to evaluate conditional exogeneity in our setting.

To codify the use of the phrase “capacity discipline” and other combinations of words that carry an analogous meaning, we begin by coding “capacity discipline” with a categorical variable , which takes the value if that phrase appears in the earnings call transcript of carrier in the year-quarter preceding the month and otherwise.

In many instances airline executives do not use the exact phrase “capacity discipline,” but the content of their statements is closely related to the notion of capacity discipline, as illustrated in the following text (emphasis added):

“We intend to at least maintain our competitive position. And so, what’s needed here, given fuel prices, is a proportionate reduction in capacity across all carriers in any given market. And as we said in the prepared remarks, we’re going to initiate some reductions and we’re going to see what happens competitively. And if we find ourselves going backwards then we will be very capable of reversing those actions. So, this is a real fluid situation but clearly what has to happen across the industry is more reductions from where we are given where fuel is running.” – Alaska Airlines, 2008:Q2.

Our view is that this instance and other similar ones should be interpreted as conceptually analogous to uses of the phrase “capacity discipline.” Yet in other cases it is arguable whether the content is conceptually analogous to the one of “capacity discipline,” even though the wording would suggest so. For example, consider the following cases:

“We are taking a disciplined approach to matching our plan capacity levels with anticipated levels of demand” – American Airlines, 2017:Q3

“We will remain disciplined in allocating our capacity in the markets that will generate the highest profitability.” – United Airlines, 2015:Q4

These statements, and others like these, cannot be easily categorized as a clear intention of the airlines to reduce capacity.151515 Airlines can change the capacity across markets in multiple ways. They can remove an aircraft from a domestic market and keep it in a hangar, or they can move it to serve an international route, or they can reassign that plane to another domestic market. The airlines can also change the “gauge” of an aircraft, i.e., increase or decrease the number of seats or change the ratio of business to coach seats. Additionally, in markets where carriers outsource some flights and/or routes to regional carriers, moving capacity should be even easier. All of these options are discussed in conference calls. On one hand, the “anticipated levels of demand” depend on the competitors’ decisions, and thus one could interpret this statement as a signal to competitors to maintain capacity discipline. On the other hand, an airline should not put more capacity than what is demanded because that implies higher costs and lower profits.

We take a conservative approach and code all these instances as ones where the categorical variable is equal to 1. This approach is conservative because it assumes that the airlines are coordinating their strategic choices more often than their words would imply, and would work against finding a negative relation. In other words, we design our coding to err on the side of finding false negatives (failing to reject the null hypothesis that communication is not correlated with a decrease in capacity), rather than erring on the side of finding false positives. We take this approach because our analysis includes variables that control for year, market, and year-quarter-carrier specific effects that control for many sources of unobserved heterogeneity that might explain a reduction of capacity driven by a softening of demand. Therefore, our coding approach makes us less likely to find evidence of coordination even when airlines are coordinating.

In practice, to identify all the instances where the notion of capacity discipline was present but the phrase “capacity discipline” was not used, we used NLP to process all transcripts and flag those transcripts where the word “capacity” was used in conjunction with either the word “demand” or “GDP.” This filter identified 248 transcripts, which we read manually to classify as either pertinent or not pertinent for capacity discipline. If the transcript was identified by all three of us as pertinent, then we set the variable , and zero otherwise. Out of the 248 transcripts, 105 contained statements that we deemed pertinent.161616 Besides the coding approach described above, we had a research assistant independently code all transcripts, and coded all transcripts only using the automated, NLP approach. We discuss these approaches, and the results of estimating our primary model with these datasets, in Appendix D.

Table 2.2 presents the summary statistics of . We have 320 earnings calls transcripts for the legacy carriers, and 40.9% include content associated with the notion of capacity discipline. We have fewer transcripts for LCCs, JetBlue and Southwest, and content associated with capacity discipline is much less frequent. Overall, we have 520 transcripts and in of them. Table 2.2 suggests that the LCCs, including Southwest (WN), are much less likely to talk publicly about capacity discipline. In view of this data feature, in our empirical exercise, we focus only on communication by legacy carriers.

| Mean | SD | N | |

| Carrier Type | |||

| Legacy | 0.409 | 0.492 | 320 |

| LCC | 0.124 | 0.331 | 89 |

| Jet Blue | 0.109 | 0.315 | 55 |

| Southwest | 0.071 | 0.260 | 56 |

| Total | 0.292 | 0.455 | 520 |

2.3 Airline Data

We use three datasets for the airline industry: the Bureau of Transportation Statistics’s (BTS) T-100 Domestic Segment for U.S. carriers, the BTS’s Airline On-Time Performance database, and a selected sample from the OAG Market Intelligence-Schedules dataset. We consider the months between 2003:Q1 and 2016:Q3 (inclusive). The BTS’s T-100 Domestic Segment for U.S. carriers contains domestic non-stop segment (i.e., route) data reported by U.S. carriers, including the operating carrier, origin, destination, available capacity, and load factor. The BTS’s Airline On-Time Performance database reports flight times.

In many instances, regional carriers, such as SkyWest or PSA, also operate on behalf of the ticketing carriers. The regional carriers might be subsidiaries fully owned by the national airlines, e.g., Piedmont, which is owned by American (and prior to that by U.S. Airways), or they might operate independently but contract with one or more national carrier(s), e.g., SkyWest. To allocate capacity to the appropriate ticketing carriers, we merge our data with the data from the OAG Market Intelligence, which contains information about the operating and the ticketing carrier for each segment at the quarterly level. Using this merged dataset, we allocate the available capacity in each route in the U.S. to the ticketing carriers, which are the carriers of interest.171717A ticketing carrier is considered to have served a given market in a given month if it performed at least four flights in that month. We aggregate a set of particularly small ticketing carriers into a single “Fringe” carrier in our data. We consider only routes between airports located in the proximity of a Metropolitan Statistical Area in the U.S.181818 We use the U.S. DOC’s 2012 data to identify Metropolitan Statistical Areas in the U.S. We also perform the empirical analysis where markets are defined by the origin and destination cities, rather than airports in Appendix C.

2.4 Alignment of Earnings Calls and Airline Capacity

We investigate the relationship between communication via earnings calls and capacity decisions in the quarter following an earnings call — i.e., in the intervening time between earnings calls. Earnings calls typically take place in the middle of the first month following a quarter. We use the content from a call, e.g., for Q1, occurring in mid-April, to define for the months of May, June, and July.191919 An alternative approach would be to associate the Q1 call taking place in mid-April with the capacity data for April, May, and June. In Appendix Appendix E we present our primary results under this alternative approach. The results are similar to what we find under our preferred approach.

We maintain that airlines can change route capacity (scheduled seats) by adding, removing, or changing flights, or the number of seats on a flight (up- or down-gauging), within few weeks of the scheduled departure day. We do not require that airlines regularly change their capacity in the days or weeks before takeoff across all market, but simply that they are able to make changes on relatively short notice in selected markets. We have several pieces of evidence that support our timing assumption. First, Delta’s “Schedule Change and Ticket Revalidation Policy” notes that “airlines routinely change their flight schedules for a variety of reasons,” such as “seasonal demands, …, new routes, changes to … operating times, [and] flights that no longer operate.” Indeed, Delta further notes that, “most schedule changes occur outside of 7 days before travel,” which suggests a non-negligible number of changes occur within as little as a month before takeoff \citepmainDelta2021. Second, there are court documents that provide additional evidence of airlines’ abilities to make short-run changes. For example, the Memorandum and Order issued in the antitrust case United States of American v. AMR Corporation, American Airlines, Inc., and AMR Eagle Holding Corporation documents several instances where airlines make the strategic decision to add or remove flights within days, and then enact those decisions within as little as two to three weeks \citepmainMO2001.

2.5 Variable Definitions

We say that legacy airlines are communicating with each other when all of the legacy airlines serving a market with at least two legacy carriers discuss capacity discipline. Letting be the set of legacy carriers in market at time , we define a new variable,

Thus, indicates whether all of the legacy carriers in discussed capacity discipline, conditional on two or more legacy carriers serving that market for that month.202020 In \citemainAwayaKrishna2016, AwayaKrishna2017 firms communicate simultaneously, and it is crucial for the construction of their equilibrium. For example, Awaya and Krishna write, “The basic idea is that players can monitor each other not only by what they ‘see’—the signals—but also by what they ‘hear’—the messages that are exchanged” \citemain[page 515]AwayaKrishna2017. In equilibrium, firms cross-check the messages against each other, and under the asymmetric-correlation information structure, concurrent communication ensures that the signal is the most informative. In cases where fewer than two legacy carriers serve a market, is set equal to 0. While varies by carrier and year-month, our treatment varies by market and year-month. This is an important distinction for the empirical analysis, where the observations are at the market-carrier-year-month level.

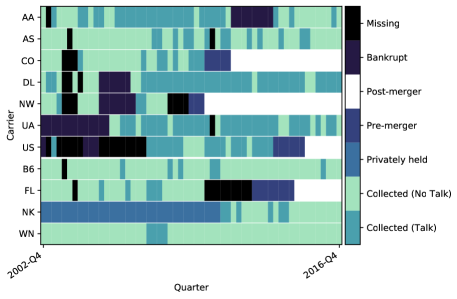

Figure 2 shows the occurrence of in our data. Each row corresponds to one airline and shows the periods for which the carrier discussed capacity discipline. There is variation in communication across both airlines and time, which is necessary for the identification. Even though the reports do not vary within a quarter, the composition of airlines operating in markets—market structure—varies both within a quarter and across quarters, causing the dummy variable to vary by month.

Section 2.5 provides a summary of this airline data. Legacy carriers offer, on average, 11,757.9 seats in a month, while LCCs offer 11,255.1.212121 We use the seats variable in the T-100 dataset, which corresponds to the scheduled seats transported in a month between two airports. If we use seats weighted by the share of performed departures over scheduled departures, the main empirical findings do not change. Consistent with our focus on the communication among only the legacy carriers, we find that legacy carriers are far more likely to be in a market where Capacity-Discipline is equal to 1.222222 Despite the lawsuit, we do not include Southwest (WN) when assessing communication because it is known to have a different cost structure and business model than the legacy carriers, and, more importantly, the notion of capacity discipline appears only four times in the entire Southwest’s transcripts; see row WN in Fig. 2.

We define the categorical variable to be equal to 1 if there are at least two legacy carriers in market in period and 0 otherwise. This variable controls for the possibility that markets where legacy carriers could engage in coordinating communication may be fundamentally different from markets where such communications are not possible. Not including this control variable would confound the correlation between talking and seats. Section 2.5 shows that, on average, 24% of the observations in our sample have the potential for coordinating communications. In a similar vein, markets served by a single carrier could differ from non-monopoly markets. We account for this possibility by introducing a categorical variable , which is equal to 1 if in , market is served by only one firm and equal to 0 otherwise. We also see that, on average, 52% of observations are monopoly markets, and that legacy carriers are more likely to serve monopoly markets than LCCs.

As discussed above, we take special note of markets where we were unable to collect an earnings call transcript.232323 See Section 2.2 for a discussion of when and why we were unable to collect a transcript. Transcripts are missing, mostly for legacy carriers, largely due to their increased prevalence of bankruptcies and mergers. To account for that, we introduce a categorical variable is equal to 1 if at least one of the legacy carriers serving market in period did not hold an earnings call for the quarter prior to month . Section 2.5 shows that legacy carriers are more likely to operate in a market that is missing a report—a result of the bankruptcy by many of the legacies. Following \citemainJones1996, in our regression, we use MissingReport and its interactions with other covariates to account for missing reports.

3 Empirical Analysis

In this section, we specify and estimate a model to investigate whether the data are consistent with the allegation that U.S. legacy carriers used their quarterly earnings calls to coordinate capacity reductions. We begin with the premise that airlines have access to communication technology (the quarterly earnings call) and posit that such technology allows them to signal to others their intention to coordinate future capacities. In particular, we hypothesize that when all legacy airlines serving a market communicate concurrently (by announcing they will adhere to capacity discipline), it signals to everyone else their intention to reduce capacity, maintaining coordination. For our hypothesis to work, it is essential that every legacy airline in a market simultaneously communicates.

3.1 Primary Model and Results

We examine the relationship between communication among legacy airlines and the seats they offer between 2003:Q1 and 2016:Q3 (inclusive). We use panel data model to estimate these relationships by estimating the following model using the within-group estimator:

| (1) | ||||

where the dependent variable is the log of total seats made available by airline in (airport-pair) market in month . Our variable of interest is , which is the dummy variable introduced in Section 2.2 is equal to 1 if there are at least two legacy carriers in market and month , and they all communicated about capacity discipline in their previous quarter’s earnings calls, and 0 otherwise.

The idea behind capacity discipline is that airlines restricted seats even when there was adequate demand, which can vary across both markets and time. To control for these unseen factors, we include carrier-market fixed effects, , and carrier-year-quarter fixed effects, . These fixed effects allow airlines to provide different levels of capacity across different markets and time. During our sample period, we observe several mergers (see Fig. 2). Since it is possible that a carrier’s relationship to a specific market could change in a meaningful way after a merger, we redefine the carrier as the merged entity in order to allow greater flexibility in these fixed effects. For example, the fixed effect for American Airlines serving the ITH-PHL market is allowed to differ before and after American merges with US Airways. Lastly, to control for time-dependent changes in demand we use origin- and destination-airport specific time trends, and .242424 Implicitly, we are assuming that our panel data model satisfies the strict-exogeneity assumption. We performed a diagnostic test proposed by \citepmain[page 285]Wooldridge2001 by including the lead as an additional regressor. This regressor’s estimated coefficient was +0.007 and statistically significant at the 5 percent level, which suggests that the assumption of strict exogeneity is reasonable in our context.

Next, we explain the identification strategy for Eq. 1. To highlight the key sources of variation in the data, we fix an airline—say, Delta (i.e., )—and consider different potential market structures and communication scenarios in Table 3. In markets , only DL operates, so the concept of communication is moot and . Then we can use variation in whether a report is available (for ) or not (for ) to identify and , as shown in the last column. Market is served by both DL and UA and both discuss “capacity discipline” in the previous quarter, so , which identifies . The same identification argument applies to identifying in markets where every airline in the market talks and a report for DL is available, even when an LCC is present (). In contrast, for market , even when both US and UA discuss capacity discipline, we identify because DL did not have a transcript.

| market | market structure | DL reports | communicating | Cap-Dis | Report | Monopoly | Talk-Eligible | parameters |

|---|---|---|---|---|---|---|---|---|

| 1 | {DL} | no | n/a | 0 | 1 | 1 | 0 | |

| 2 | {DL} | yes | n/a | 0 | 0 | 1 | 0 | |

| 3 | {DL, UA} | yes | {DL, UA} | 1 | 0 | 0 | 1 | |

| 4 | {DL, UA, US} | no | {US} or {UA} or {US, UA} | 0 | 1 | 0 | 1 | |

| 5 | {DL, UA, US} | yes | {US, UA} | 0 | 0 | 0 | 1 | |

| 6 | {DL, UA, US} | yes | {DL, UA, US} | 1 | 0 | 0 | 1 | |

| 7 | {DL, UA, US, F9} | yes | {DL, UA, US} | 1 | 0 | 0 | 1 | |

| 8 | {DL, F9} | yes | n/a | 0 | 0 | 0 | 0 | - |

Lastly, we identify the fixed effects using the deviation from the mean. Therefore, the key source of identification is the variation in Capacity-Discipline across markets and over time (see Figure 2), which in turn depends on the variation in market structure and communication. We also assume that conditional on all control variables, Capacity-Discipline is uncorrelated with the error, and this conditional exogeneity of treatment is sufficient to identify the relationship between Capacity-Discipline and log-seats \citepmainRosenbaum1984.

We present the estimation of the semi-elasticity from Eq. 1 in column (1) of Table 4.252525 Throughout the paper, for a binary regressor, we present its estimated semi-elasticity. If the estimated coefficient of a dummy variable in a semilogarithmic regression is , then the effect of the dummy variable on the outcome variable is \citepmainHalvorsenPalmquist1980. Using our model, we find that when all of the legacy carriers in a talk-eligible market communicate with each other about capacity discipline, there is a subsequent reduction in the number of seats offered by an average of 2.02%.262626This estimate is a weighted average of the parameter estimates across markets, time, and types of carriers and should be interpreted as a percentage decrease in capacities. Following \citemainChaisemartinDHaultfuille2020, we estimated the weights for each group, and only 0.07% of those weights were negative, suggesting that negative weights do not drive our estimate. The standard errors are clustered at the bi-directional market level.

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Log Seats | Log Seats | Log Seats | Log Seats | Log Seats | Log Seats | |

| Capacity Discipline | -0.0202 | -0.0150 | ||||

| (0.0060) | (0.0049) | |||||

| Capacity Discipline 2 | -0.0193 | -0.0160 | ||||

| (0.0064) | (0.0052) | |||||

| Capacity Discipline 3 | -0.0285 | -0.0109 | ||||

| (0.0112) | (0.0103) | |||||

| Capacity Discipline 4 | -0.0332 | -0.0018 | ||||

| (0.0541) | (0.0342) | |||||

| Legacy Market x Capacity Discipline | -0.0169 | -0.0197 | ||||

| (0.0074) | (0.0063) | |||||

| Mixed Market x Capacity Discipline (Legacy) | -0.0195 | 0.0010 | ||||

| (0.0115) | (0.0085) | |||||

| Mixed Market x Capacity Discipline (LCC) | -0.0341 | -0.0221 | ||||

| (0.0155) | (0.0107) | |||||

| Carrier-Market FE’s | ||||||

| Carrier-Market-Structure FE’s | ||||||

| R-squared | 0.088 | 0.083 | 0.088 | 0.083 | 0.088 | 0.084 |

| N | 841,991 | 841,991 | 841,991 | 841,991 | 841,991 | 841,991 |

To determine the estimate’s economic significance, we can compare it to the average change in capacities in a set of relevant comparison markets. To do so, we identify all talk-eligible markets where communication did not occur. In other words, we define our set of comparison markets as those where communication could have occurred, but did not. In such markets, we find that the average percentage change in capacities is 3.67%. So, whenever legacy airlines communicate, their capacities drop by more than 50% of the average change in capacities in our comparison markets, a significant reduction.

While we attempt to capture some of the differences in market structures that permit communication (via the Talk-Eligible variable), this may not adequately capture the manner in which competitive behavior may respond to market structure, either in terms of the number or type of carriers, or the specific set of carriers serving a market.272727In our primary specification, identification of relies on variation in communication and/or market structure, as Capacity-Discipline can turn on or off as a result of carriers beginning or ending communication, or when a legacy carrier enters or leaves a market. In our data, we find that 85.4% of changes in Capacity-Discipline derive exclusively from changes in communication, while 14.6% of changes occur concurrently with changes in market structure. To address this concern, we re-estimate our primary specification Eq. 1, but control for specific market structures. In particular, we change the carrier-market fixed effects in Eq. 1 to carrier-market-structure fixed effects.

To best understand the carrier-market-structure fixed effects, consider an example of the Ithaca (ITH) to Philadelphia (PHL) market. Suppose we observe this market for four periods, and during this time the market structures are {AA, DL}, {AA}, {AA, UA}, and {AA, DL}. The carrier-market fixed effects for a given carrier would be constant across all periods in which they compete in the ITH-PHL market, but carrier-market-structure fixed effects allow American (AA) to behave differently when in a duopoly with Delta (DL) compared to when it is competing in a duopoly with United (UA). In Table 4-column (2) we present the estimation results from this alternative specification. We find that communication is associated with a 1.50% reduction in offered capacity.282828 Under the carrier-market-structure fixed effects, Talk-Eligible and Monopoly are redundant and are therefore excluded from the regressions.

Next, we consider whether the relationship between communication and capacity varies with the number of communicating airlines. Let be 1 if market in period is talk eligible, is served by exactly legacy carriers, and all of them use capacity discipline. Then we estimate Eq. 1 after replacing with three (additively separable) indicators . The estimation results using the carrier-market fixed effects and the carrier-market-structure fixed effects are in columns (3) and (4) of Table 4, respectively.292929 While we do observe some markets with five legacy carriers, is always zero in these markets, and so we do not include an additional variable for this case.

In column (3) of Table 4, we find that with the carrier-market fixed effects, the association between communication and capacity reductions are increasing in the number of legacy carriers serving the market. In particular, we find that communication is associated with a reduction in capacity of , and in markets with two, three and four legacy carriers, respectively. Although, because there are few markets with four legacy carriers, this coefficient is imprecisely estimated. With the carrier-market-structure fixed effects, however, we find that communication is associated with a reduction in capacity by in markets with two legacy carriers. For the markets with three or four legacy carriers, the coefficients are imprecisely estimated with no effect.

Lastly, we explore how the estimate change between markets with only legacy carriers and mixed markets with both legacy and LCCs. We present summary statistics for these two types of markets in Section 2.5. We present the results from this exercise using the carrier-market fixed effects and the carrier-market-structure fixed effects in columns (5) and (6) of Table 4, respectively. With the carrier-market fixed effects, we find that communication about capacity discipline is associated with a 1.69% decrease in the number of seats offered. In mixed-markets, we find that communication is associated with a 1.95% decrease in legacy seats and a 3.41% decrease in LCCs seats.

In summary, we find that capacity is lower when all legacy carriers serving a talk-eligible market discuss capacity discipline, a finding which is consistent with the allegation that U.S. legacy carriers used their quarterly earnings calls to coordinate capacity reductions. On average, we find that capacity is between 1.50% and 2.02% lower when this communication occurs, though we find this varies with the number of legacy carriers in a market, and the presence of LCCs.303030 In Appendix B we explore how the relationship between capacity and communication varies with the size of a market and the amount of business travel in a market.

In the analysis that follows, we use the specification outlined in Eq. 1, which employs carrier-market fixed-effects, as our primary specification because it takes advantage of both important sources of variation in Capacity-Discipline, namely, that Capacity-Discipline can turn on or off as a result of a legacy carrier beginning or ending communication, or when a legacy carrier enters or leaves a market.313131 An additional concern with including carrier-market-structure fixed effects is that market structure may correlate with the unobservable in Eq. 1. As noted in Section 4.4, and with more details in Appendix A, using a control function approach we find that our primary results are robust to this concern. For completeness, we provide corresponding estimates in Appendix H for everything that follows using carrier-market-structure fixed effects.

3.2 Market-Level Changes in Capacity and Number of Flights

To complement our previous analysis, we examine the relationship between capacity and communication among legacy airlines at the market level. In particular, we ask whether the firm-level reductions in seats that we have estimated above involve a reduction in total market capacity, a reduction in the number of scheduled flights, or both.

To shed light on the first question, we aggregate capacity to the market level, and estimate the same panel data model as Eq. 1. In this case, the dependent variable is the sum of all seats offered by all the carriers in market in period . We present the estimation of the semi-elasticity from this model in column (1) of Table 5. We find that overall capacity is lower by 1.7% when communication about capacity discipline occurs, suggesting that reductions in individual-level capacities translates into a market-wide reduction in offered seats.

Next, we estimate the relationship between communication and the number of flights in a market. To this end, we assume that the number of flights in a market is a Poisson random variable, where the mean depends on all the explanatory regressors in Eq. 1, including the fixed effects. Let and , respectively denote the number of flights and observed characteristics (i.e., the right-hand side terms in Eq. 1) in market in period ; and let and be the market- fixed effects and time- fixed effects, respectively. We assume that the probability , given and , is given by

| (2) |

with the mean function . We can then use the method of conditional maximum likelihood to estimate ; see, for example, \citemainWooldridge1999 and \citemainWooldridge2001, Chapter 18.2.

The estimate of the coefficient for capacity discipline from Eq. (2) is in column (2) of Table 5. Here too, we find evidence that discussion of capacity discipline is associated 0.02 fewer flights, on average. Thus, we find evidence that, on average, there are fewer total seats offered and fewer flights flown in markets when carriers discuss capacity discipline.

| (1) | (2) | (3) | (4) | (5) | |

| Mkt. Capacity | Flights | Depart. Crowding | Price | Price | |

| Capacity Discipline | -0.0170 | -0.0221 | 0.0501 | 0.0061 | |

| (0.0087) | (0.0053) | (0.0290) | (0.0033) | ||

| Capacity Discipline x Log Market Seats | -0.0043 | ||||

| (0.0026) | |||||

| Capacity Discipline (Legacy) | 0.0049 | ||||

| (0.0035) | |||||

| Capacity Discipline (LCC) | 0.0186 | ||||

| (0.0057) | |||||

| Log Market Seats | 0.0743 | ||||

| (0.0031) | |||||

| R-squared | 0.172 | . | 0.077 | 0.133 | 0.138 |

| Prob chi2 | . | 0.000 | . | . | . |

| N | 614,311 | 614,256 | 463,951 | 649,204 | 649,204 |

3.3 Crowding of Flight Departure Times and Prices

We now turn our attention to other, consumer-welfare relevant outcomes, associated with (i) the preferences of consumers for the time of departure; and, (ii) with the possibility of higher prices.

First, reductions in capacity (relative to demand) could allow airlines to better coordinate the timing of flights. The consumer welfare impact of such coordination is ex-ante ambiguous. On one hand, this could benefit consumers who value greater product differentiation by providing flights at times closer to their preferred time of departure. Additionally, it could reduce the level of congestion (and of associated delays) at capacity constrained airports. On the other hand, such coordination might negatively impact consumers if the distribution of consumers’ preferences for travel times is concentrated around a small number of times in the day (e.g., 7am and 6pm for daily business travelers), or if consumers have preferences for short layovers when making a connecting flight.

Second, the capacity reductions might not ultimately affect prices, thus limiting the impact on consumer welfare.323232 For instance, \citemainArmantierRichard2003 consider the effect of information exchanges between UA and AA out of O’Hare airport and find that while airlines benefit, it only moderately hurts consumers. They conclude, “Hence, a marketing alliance between AA and UA, with the sole objective of exchanging cost information, would be advantageous to airlines without significantly hurting consumers.”

Estimating the welfare effect of communication is well beyond the scope of this paper, but we can determine (i) if conditional on reducing capacity, airlines change their departure times and, thereby reduce the crowding of flight departure times; and (ii) if communication is associated with higher average fares.

As we show next, we find no evidence to support the hypothesis that departure crowding has changed, and we find evidence that fares may have risen, both of which show that capacity discipline likely hurt consumers. We show our results next.

3.3.1 Crowding of Flights Departure Times

First, we examine if, conditional on reducing capacity, legacy airlines change their departure times and reduce the extent to which flights are scheduled at the same time at the airport. To measure the crowding of flight departures times at an airport, we use the following measure proposed by \citemainBorensteinNetz1999.

On a route with daily departures departing minutes after the midnight, the average time difference between two flights is given by

To make this measure comparable across markets with different , we normalize it by the maximum time difference if the flights were equally spaced throughout a day, such that values close to 1 corresponds to the least crowded flights. Although we use the normalized measure, for notational ease, we continue to refer it as Average-Time-Difference. To calculate Average-Time-Difference we use the Bureau of Transportation Statistics’s Airline On-Time Performance database, which records flight times.

We estimate a fixed effects model, where the dependent variable is Average-Time-Difference and the regressors are the same as in Eq. 1, plus two additional variables: the total log-seats offered in the market and an interaction term between the total log-seats and Capacity-Discipline. Departure crowding is at the market-level, so we replace the carrier-market fixed effect with market fixed effects. Our primary variable of interest is the interaction term because it estimates the relationship between log-seats and the changes in the average time difference with communication. If, conditional on reducing offered seats, airlines were increasing the average time between their flights and reducing crowding, then this interaction term’s coefficient would be positive.

We present the estimation results in column (3) of Table 5, under the heading “Depart. Crowding.” As we can see, the coefficient for the interaction term is , but is imprecisely estimated, suggesting that there is no evidence to support the claim that conditional on reducing offered seats, communication is associated with less crowded departures.

3.3.2 Ticket Prices

Next, we consider estimating the relationship between communication and prices. If, whenever airlines communicate, they lower their offered capacities, then, unless capacities never bind, it is reasonable to expect that prices would rise due to communication.

Even though it might seem straightforward to estimate this relationship, for example, by estimating Eq. 1 after replacing the log of offered seats as the dependent variable with the log of the prices as the dependent variable, this empirical strategy is infeasible. Airlines sell tickets for origin to final-destination pairs, but the offered capacities and communication are at the direct-segment level. Thus, to understand the relationship between communication and prices, we must first construct a new dataset of prices and communication.

Connecting tickets involve flights that go through different nonstop segments, possibly with different market structures in each segment. Thus, while the prices are at the origin-destination level, capacity plans and our communication measure are at the nonstop segments level. So, we have to aggregate capacity and communication from the segment level to the origin-destination level. For example, consider flights traveling from A to C via a connecting airport, B. In particular, assume that in segment A–B, two airlines are talking, but in segment B–C, there are three airlines but the third airline is not talking. Our aggregation must account for how to define Capacity-Discipline in these and similar situations. Furthermore, airlines may use multiple routes for the same market (i.e., use multiple airports to connect a given origin and destination), adding additional complexity to our problem.

Next, we define how we aggregate communication in segments A–B and B–C to determine communication in the origin-destination pair A to C. First, we follow \citemainBorenstein1989 and construct a dataset of prices, but instead of aggregating at the market level (e.g., market A to C), we aggregate them at the market-route level. For example, consider a ticketing carrier, say UA, serving A to C via two routes, AB-BC and AB-BD-DC. In this case, we treat these two routes separately, even though they are have the same origin and destination. At the end of this aggregation, we have average prices and the total number of passengers transported by each airline for each market-route. We then use the number of passengers transported to determine weighted average prices and Capacity-Discipline, weighted by the number of passengers in those combinations defined at the carrier-market level.

In particular, to determine at the route level, we calculate Capacity-Discipline for every nonstop segment. Then we merge the price data with these new communication data and restrict the sample in the price data to those markets we observe in our primary analysis.333333 For instance, as ITH-CHO is not served nonstop by any airline, it does not appear in our primary analysis. We drop this market from this analysis, even though there are connecting flights between them. Note that the number of carriers serving a market in our price dataset weakly exceeds the number of carriers serving that market in our primary analysis because they include carriers that serve the origin and destination pair via a connection.

We can then aggregate the dummy variable Capacity-Discipline that we defined previously from the segment level to the origin-destination level. In particular, if the variable in all nonstop segments of a route, then we define for that route. For the market missing report variable, we take the opposite approach: if it is 1 for at least one segment, then it is 1 for the route. Finally, we construct a Capacity-Discipline variable for each market by taking the passenger weighted average of Capacity-Discipline for each route through which a carrier serves that market.

To better understand this approach, consider the following stylized example. Suppose a carrier serves a market-quarter via three different routes, and Capacity-Discipline variable is and for these three routes. Furthermore, if the carrier sends 25% of its passengers along route 1, 25% along route 2, and 50% along route 3, then Capacity-Discipline variable for the carrier in is equal to . We use the same approach to calculate the Talk-Eligible, Monopoly, and Missing-Report variables.

Using these variables in a panel data model like Eq. 1 we estimate the relationship between Capacity-Discipline and the log of (average) route-level prices. The results are in columns (4) and (5) in Table 5. The estimates suggest that the average price increased by 0.59%, and that this increment is mostly due to LCCs, whose average prices increased by 1.80%.

In summary, we find no evidence that the crowding of flight departure times changed, and we find evidence that prices may have risen.343434 Our analysis treats capacity choices as strategic substitutes. It is reasonable to consider the possibility that if consumers care about departures, and if this preference is strong enough, that may soften competition to the effect that the capacity choices become strategic complements and not strategic substitutes. However, we do not believe this to be the case because airlines’ departures and capacity choices are interlinked. Thus, even after setting aside airlines’ communication decisions, we would have to consider three choices (departure times, capacity choices, and airfares) together in our model. There are several ways to model departures. One of them is the Salop/Vickrey circular city model, as in \citemainGuptaLaiPalSarkarYu2004, which is also consistent with \citemainBorensteinNetz1999. We can then embed this model within a \citemainKrepsScheinkman1983 framework, which results in a game played by airlines in three stages. First, they choose departure times, then the capacities and the prices. However, conditional on the circle locations (i.e., the departure times), capacities are still strategic substitutes.

4 Robustness Exercises

In Section 3, we found that whenever all of the legacy carriers in a market discuss capacity discipline, capacity is on average 2% lower in the next quarter, a finding which is consistent with the accusation that legacy carriers used their earnings calls to coordinate with other carriers to reduce capacity. In this section, we perform a series of robustness exercises to address other possible explanations for this finding.

4.1 Financial Transparency or Coordination

We have shown that we observe lower capacity when all legacy carriers in a market discuss capacity discipline. Of course, it could be that airlines are not coordinating but are simply announcing their unilateral intentions to reduce capacity in response to demand forecasts or for other reasons specific to themselves. That is, the airlines may be using the quarterly earnings call for its ostensible purpose: to inform investors about the state of their businesses.

If this is the case, then the number of seats offered by an airline would also fall when the airline is communicating, but its competitors are not. That is not what we find. We do not find evidence that a carrier reduces capacity when it discusses capacity discipline, but its legacy competitors do not. Additionally, carriers do not reduce capacity in monopoly markets, where we would also expect to find capacity reductions following communication. Finally, we find no evidence of capacity reductions when all but one of the legacy carriers serving a market discuss capacity discipline.

To investigate whether airlines decrease capacity when they are the only one discussing capacity discipline, we estimate the following variation of Eq. 1:

| (3) | ||||

where our variable of interest is defined as

| Only-j- | |||

That is, indicates whether carrier is the only legacy carrier in market that discussed capacity discipline, conditional on there being at least two legacy carriers. The parameter shows the extent to which a legacy carrier that discusses capacity discipline when none of its market-level competitors discussed capacity discipline changes capacity. If discussion of capacity discipline is meant to inform investors about future strategic behavior, should be negative and, likely, close to -2.02%. We present the estimation results from Eq. 3 in column (1) of Table 6. As we can see from the estimates in the first row of column (1), there is no evidence of a decline in the capacity associated with the unilateral discussion of capacity discipline. We find the opposite: the number of offered seats is 1.72% higher when airlines communicate unilaterally.

| (1) | (2) | (3) | (4) | (5) | |

| Log Seats | Log Seats | Log Seats | Log Seats | Log Seats | |

| Only Talks | 0.0172 | ||||

| (0.0066) | |||||

| Monopoly Capacity Discipline | 0.0260 | 0.0027 | |||

| (0.0074) | (0.0050) | ||||

| Capacity Discipline | -0.0022 | ||||

| (0.0045) | |||||

| Capacity Discipline “Not ” | -0.0010 | ||||

| (0.0074) | |||||

| R-squared | 0.088 | 0.088 | 0.061 | 0.087 | 0.087 |

| N | 841,991 | 841,991 | 438,980 | 841,991 | 841,991 |

A second approach to addressing the concern mentioned above is to look at capacity decisions in monopoly markets. If carriers discuss capacity discipline to inform investors about their plans to reduce capacity, presumably independent of what other airlines are doing, we should expect to see reductions in monopoly markets following those discussions. To estimate the role of “monopoly capacity discipline” we estimate our primary model Eq. 1, but using the treatment , which is equal to 1 when a carrier in a monopoly market discussed capacity discipline and otherwise. We estimate this model using both our full sample and a sample that consists of only monopoly markets, and present the results in columns (2) and (3) of Table 6, respectively. In the full sample we find the opposite—capacities are higher after a monopoly airline discusses capacity discipline—but for the monopoly markets sample we find no evidence of an effect.

Finally, we consider whether carriers reduce capacity in cases where all but one of the legacy carriers serving the market discuss capacity discipline. To do so, we estimate Eq. 1 with the treatment variable defined as

| Ca | (4) | |||

which is equal to 1 when all but one of the legacy carriers in a Talk-Eligible market discuss capacity discipline, and 0 otherwise. We present this estimation results in column (4) of Table 6. We find no evidence of a relationship between communication and capacity when all but one of the legacy carriers serving a market discuss capacity discipline. In light of these exercises—looking at markets where one carrier speaks but its competitors do not, looking at capacity decisions in monopoly markets, and looking at markets where all but one legacy carrier speak—we conclude that discussion of capacity discipline is not simply a bona fide announcement of future, unilateral intentions.

4.2 Information Sharing

So far, we have shown that when all legacy carriers in a market discuss capacity discipline, capacity is subsequently lower, and, if any one of the legacy carriers is not discussing capacity discipline while the others are, their number of offered seats does not change (Table 6, column (4)). While these two results are consistent with coordination, they could also be consistent with the idea that (for some historical reason) airlines use correlated strategies. That is, when they announce their intention to engage in capacity reduction during the earnings call, they share their private information about the aggregate airline demand.

In fact, our previous finding that the level of capacity reduction is increasing in the number of legacy carriers serving the market (Table 4, columns (3) and (4)) provides suggestive support for such an alternative hypothesis: when more airlines are communicating, the precision of the aggregate signal gets better, which in turn induces stronger correlation in capacity choices. Thus, this alternative “information sharing” model interprets the communication as being payoff relevant, unlike in \citemainAwayaKrishna2016 wherein capacity discipline is cheap talk, but it does not require firms to coordinate on any action.

To better understand this alternative theory, consider the following. Suppose that with probability there is a negative demand shock. Each airline receives a private signal of the actual and publicly announces its during its earnings call, and airlines then base their decisions on all the announced ’s. So, airlines reduce capacity when all signals are unfavorable compared to when only one firm received a negative signal because of the correlation in their strategies induced by information sharing.353535 This alternative model makes a stronger assumption—airlines cannot misrepresent their information. Under our cheap-talk interpretation, however, it is moot whether or not a message is truthful.

This alternative model assumes that airlines always have an incentive to share their information about aggregate demand. \citemainClarke1983, \citemainGalor1985, and \citemainLi1985, however, show that firms do not have an incentive to share their private information about market demand with others unless, as \citemainClarke1983 shows, they can use that information to collude.363636 For more on the role of information-sharing on collusion see \citepmainVives2008, SugayaWolitzky2018.

To verify the validity of the alternative model, we test its implication that absent its signal about low demand airline would still reduce capacity in the presence of a strong, aggregate signal from others. To that end, we estimate the effect of “everyone except airline talking” on ’s capacity choice next quarter. Let be a dummy variable equal to 1 if the market in period is talk eligible and if every legacy carrier serving except airline discusses capacity discipline, and otherwise. Then we estimate Eq. 1 after replacing with and present the results in column (5) of Table 6. We find that even when everyone else except is communicating, it does not affect ’s capacity. Although this “no-effect” result is inconsistent with the information-sharing model, it is consistent with the allegation that legacy carriers communicate to coordinate capacity reductions.

4.3 Conditional Exogeneity

Although we employ a rich set of fixed effects and other covariates as control variables, it is still desirable to explore the possibility that our finding is driven by a missing communication-related variable positively correlated with capacity discipline and negatively correlated with offered seats. To this end, we propose to run a diagnostic test à la \citemainWhiteChalak2010.

We can explain this approach using an example. Suppose we define an additional communication variable equal to 1 whenever all legacy airlines use the word “stable”, and zero otherwise. Furthermore, suppose that the occurrence of “stable” is positively correlated with, and occurs as frequently as, the discussion of “capacity discipline.” Then, under this diagnosis, we verify that adding this new dummy variable that captures the discussion of “stable” as an additional regressor in Eq. 1 neither affects the estimated relationship between capacity discipline and offered seats nor is it negatively correlated with offered seats.

Although intuitive, to implement this diagnostic test, we have first to find all relevant tokens (e.g., “stable”). Given the large amount of text data we have, it is a nontrivial task to find such tokens objectively. To do so, we use methods from computational linguistics to search our entire text and identify tokens or keywords that (i) are “close” in terms of context to the discussion of capacity discipline, and (ii) occur approximately as frequently as “capacity discipline.” Then, for each token, we define a dummy variable that is equal to 1 only if all legacy carriers in talk-eligible market use it in period and include it as an additional regressor in Eq. 1. Then, we test if the estimated coefficient for each is statistically negative or not, and verify whether the coefficient of capacity discipline changes with the introduction of .

To construct such a set of tokens, we identify three tokens that are essential to the concept of capacity discipline: “capacity discipline,” “demand,” and “gdp.” Then, we use the word2vec model from computational linguistics \citepmainMikolovChenCorradoDean2013 to determine other tokens that are close to these three tokens, using a distance metric that we define shortly below.373737 The word2vec model was developed at Google in 2013 \citepmainMikolovChenCorradoDean2013 to analyze text data. For an intuitive and accessible explanation, see \citemainGoldbergLevy2014. We use the gensim implementation of the word2vec model \citepmainRehurekSijka2010. word2vec allows us to be objective in determining the tokens.

Broadly, the word2vec model is a neural network that maps each unique token we observe in the earnings call transcripts to an -dimensional vector space (in our analysis, ) in such a way as to preserve the contextual relationships between the tokens. The vector representation of each token is such that contextually similar tokens are located “close” to each other, and tokens that are dissimilar are located “far” from each other. This sense of “closeness” reflects the likelihood that the given tokens appear near each other in the earnings call transcripts. Thus, if “discipline” and “stable” are close, then the discussion of one term in an earnings call is likely given a discussion of the other. We directly train the word2vec model using our transcript data, so the derived relationships between words are specific to the context of airlines’ earnings calls, as opposed to a more general context. For example, if airline executives use the word “discipline” in a contextually different manner than used in more general conversation or writing, our model will account for that.

To measure the similarity of two tokens in the word2vec vector space, we use a commonly used metric called the cosine similarity metric. This metric is equal to the cosine of the angle between the vector representation of the two tokens \citemainSinghal2001, such that for any two normalized vectors associated with two tokens, , and , this measure of similarity is

where is the norm. When two vectors are the same, cosine similarity is 1, and when they are independent (i.e., perpendicular to each other), it is 0.383838 Note that the cosine metric is a measure of orientation and not magnitude. This metric is appropriate in our cases, as we are interested in comparing the contextual meaning of the words, not in comparing the frequency of the words.

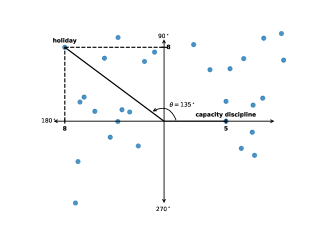

To understand our use of cosine similarity, consider Fig. 3(a), which displays a hypothetical example of training the word2vec model in a 2-dimensional space. The word2vec model maps all of the tokens in our vocabulary to this space. For example, the token “capacity discipline” is represented by the vector , and the token “holiday” is represented by the vector . Our measure of similarity between these two tokens is the cosine of the angle between these two vectors, , so , and thus “holiday” is very dissimilar to “capacity discipline.”

For each of these tokens , we define the set:

where is the set of all tokens. To satisfy the second criterion, we restrict the token to be such that at least 50% of the time it appears in the same report as these three keywords.

In Table 7, we present all the tokens that satisfy the above two criteria. For each token, we define as we did for and use it as an additional regressor in Eq. 1. The estimated coefficients for the tokens are in the first row, with the estimated coefficient for in the second row. As we can see, five out of six a tokens have no relationship with log seats, and even then the coefficient of “domestically” is positive which shows that, if anything, our results understate the true relationship between the discussion of capacity discipline and capacity. What is also reassuring is that for all the tokens, the estimates for Capacity-Discipline are stable, with estimates close to our primary result of .

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| slow | weakness | domestically | internationally | stable | pace | |

| Z Token | -0.0025 | 0.0016 | 0.0187 | 0.0030 | 0.0027 | 0.0052 |

| (0.0063) | (0.0061) | (0.0068) | (0.0054) | (0.0099) | (0.0076) | |

| Capacity Discipline | -0.0200 | -0.0202 | -0.0187 | -0.0202 | -0.0204 | -0.0207 |

| (0.0059) | (0.0060) | (0.0059) | (0.0059) | (0.0060) | (0.0059) | |

| N | 841,991 | 841,991 | 841,991 | 841,991 | 841,991 | 841,991 |

4.4 Additional Robustness Exercises

In addition to the work described above, we conduct two additional robustness exercises. For brevity, we present these results in Appendices A and C.

First, in Appendix A, we consider the possibility that market structure can be endogenous because a factor that affects capacity decisions can also affect airlines’ decisions to serve a market. If a market structure is endogenous, then Capacity-Discipline will be endogenous as well. To address this, we use a control function approach, where the excluded variables are functions of the geographical distances between a market’s endpoints and each carrier’s closest hub, which we define as an airport with “sufficiently” many connections.

The identification assumption is that an airport’s distance to the airline’s nearest hub is a proxy for entry cost and is therefore correlated with the market structure, but is less likely to be directly correlated with capacity decisions \citepmainCilibertoTamer2009. In other words, this approach leverages a timing assumption, namely, that unobservables that affect an airline’s network are not contemporaneously correlated with the unobservables that affect the carrier’s capacity decisions. Additionally, the results in Appendix A help to validate our specifications that use carrier-market-structure fixed effects, as the carrier-market-structure fixed effects would violate the strict conditional exogeneity assumption if the market structure is endogenous, which results in biased estimates.